2017 pre-budget tour: the state of the middle class

TRANSCRIPT

PRE-BUDGET

TOUR: THE STATE OF

THE MIDDLE CLASS

Growing and helping the middle class

• Our government is committed to grow the economy

and the middle class.

• Canada’s middle class is facing real challenges and

feeling the effects of a technological and global

economic change.

• Our government’s measures will spur growth and

deliver tangible results to meet the needs and

expectations of middle class Canadians.

2

Why is the middle class important?

Middle Class

Growth Trust Investments/ Human and Physical Capital

Expectations / Mobility

3

Drivers of growth

y = f(A,K,L)

Innovation (A) Private and Public Capital (K) Labour/Human Capital (L)

4

5

Inflation-adjusted wages have stagnated

since the 1970s, particularly for men…

Annual Median Gross Wage Income of Canadians,

1976-2016 (2016 constant dollars)

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

1976 1981 1986 1991 1996 2001 2006 2011 2016

$ 2016

Median wage income of men

Median wage income

Median wage income of women

6

Note: Figure are for full-year, full-time workers (persons who usually worked 30 hours per week at their main job). For the years 1976 to 2011, data was

sourced from the Survey of Consumer Finances and Survey of Labour and Income Dynamics. For the years 2012 to 2014, data was sourced from the

Canadian Income Survey. Figures for 2015-2016 were imputed by applying growth experienced over the 2015-2016 period in weekly wage income of full-time

workers, sourced from the labour force survey and converted to real dollars using the Consumer Price Index.

Source: Statistics Canada; Department of Finance Calculations.

1.0

1.7

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Bottom 90 per cent Top 1 per cent Top 0.1 per cent Top 0.01 per cent

…and income growth has been

concentrated at top income levels…

Notes: Based year for growth rates is 1982. Growth for top 1, 0.1, and 0.01 per cent is based on individual real after tax after transfer income of Canadians tax files from

the Longitudinal Administrative Databank. Growth for the bottom 90 per cent is based on real after-tax, after-transfer household income (adjusted for family size) from a

combination of the Survey of Consumer Finance, the Survey of Labour and Income Dynamics and the Canadian Income Survey data. After-tax, after-transfer income is

the sum of all income from market and government sources, minus income tax. Source: Statistics Canada; Department of Finance calculations.

Average Annual Growth in Inflation-Adjusted Family Income, 1982-2014

Per cent

7

3,5

3,0

2,5

2,0

1,5

1,0

0,5

0,0

… not only in Canada but in many

other countries.

Top 1% before tax and transfer income shares, Canada and selected countries

*2014 or most recent year available.

Sources: The Top Incomes Database for U.S., U.K., Sweden. The Canadian series uses taxation data from Statistics Canada's Longitudinal Administrative Databank.

8

U.S. U.K. Canada Sweden

1982 10.3 6.9 7.6 4.1

2014* 22.0 12.7 11.6 8.7

Many Canadians feel the next generation's

standard of living will be lower

Perception on Future Standard of Living

Source: Nanos Research, February 12, 2016

9

Certain groups remain particularly vulnerable

to poverty, and are remaining in poverty longer

30.2

23.7 22.5

20.7 20.3

8.8

0

5

10

15

20

25

30

35

Unattachedpeople 45-

64

Singleparents

People withdisabilities*

Indigenouspeople off-

reserve

Recentimmigrants

All people

Low Income Rate for Selected Sub-Groups (2014 or most recent year available)

Per cent

Persistence of Low Income for

Vulnerable Groups, 2005-2010 (in low income for at least 3 out of 6 years)

5.9

9.9

15.8 16.2 17.3

24.2

0

5

10

15

20

25

30

35

All peopleIndigenouspeople off-

reserve

Singleparents

People withdisabilities

Recentimmigrants

Unattachedpeople 45-

64

*From 2012 Canadian Survey on Disability

**Sources: From the backgrounder on the Poverty Reduction Strategy; Statistics Canada, Canadian Income Survey, Survey of Labour and Income Dynamics.

Based on available indicators (employment,

income, education) the situation is worse for

Indigenous peoples on-reserve.**

Per cent

10

Costs for essentials are increasing

faster than inflation

0

10

20

30

40

50

60

70

80

All Items Shelter costs Child Care Services Tuition Fees

Nominal Price Growth for all products and Key Household Costs, 2000-2015

Per cent

Notes: Shelter costs are a weighted average of rent, mortgage, insurance, property taxes, water, fuel and electricity costs.

Source: Statistics Canada, Consumer Price Index.

32.7

39.9

50.1

75.6

11

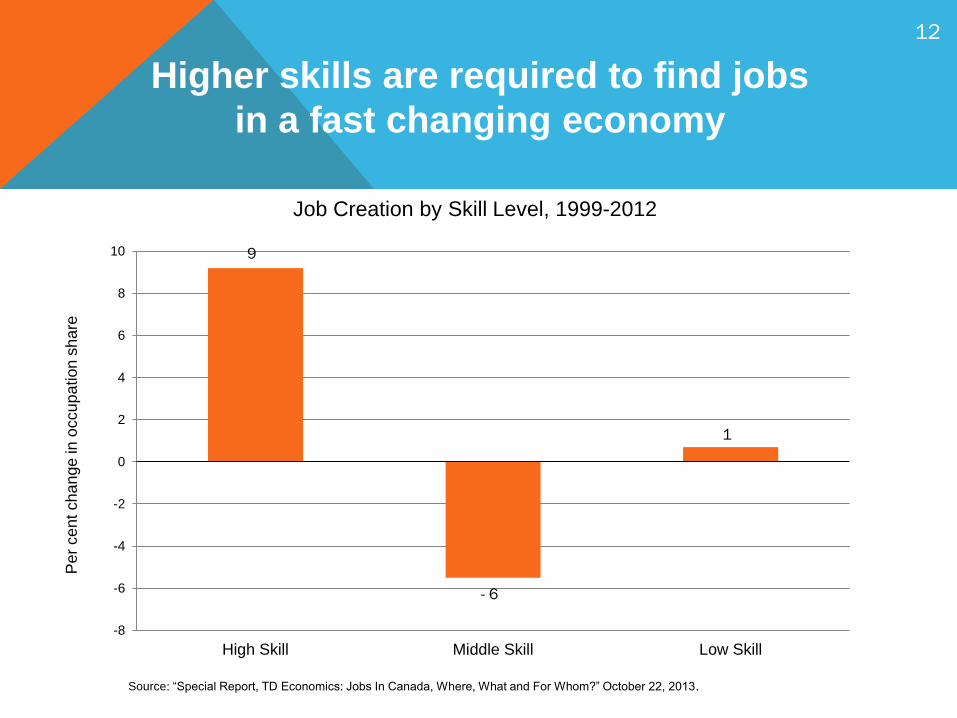

Higher skills are required to find jobs

in a fast changing economy

-8

-6

-4

-2

0

2

4

6

8

10

High Skill Middle Skill Low Skill

Pe

r ce

nt ch

an

ge

in o

ccu

pa

tion

sh

are

Job Creation by Skill Level, 1999-2012

Source: “Special Report, TD Economics: Jobs In Canada, Where, What and For Whom?” October 22, 2013.

9

1

- 6

12

Canadians are increasingly feeling

left out of the middle class

0

10

20

30

40

50

60

70

2009 2016

Working class or poor Middle-Class

Source: EKOS Research Associates, June 2016 and April 2009

Share of Canadians that self identify as middle class, working class or poor.

Per cent

Middle class

28.9

63.3

44.3

48

13

What do these challenges

mean for Canadians?

Growth: “Just not getting ahead.”

• It is harder to benefit from opportunities that growth is creating

(i.e., growth has not been inclusive).

• Persistent barriers for some disadvantaged groups mean they may be falling

further behind.

Affordability: “Harder to make ends meet.”

• Cost of necessary goods has outstripped inflation.

• Housing costs/costs of raising a family are increasing.

• Saving for retirement is harder/fewer employers offering defined benefit pensions.

• Greater indebtedness.

Changing nature of work: “Harder to qualify for a job and keep it.”

• Job insecurity is increasing, making it harder to enter and stay in the middle class.

• More education needed to get a good job & tuition costs are rising.

• Innovation in training and upskilling in order to create more jobs.

• Greater risk in investing in human capital.

14

15

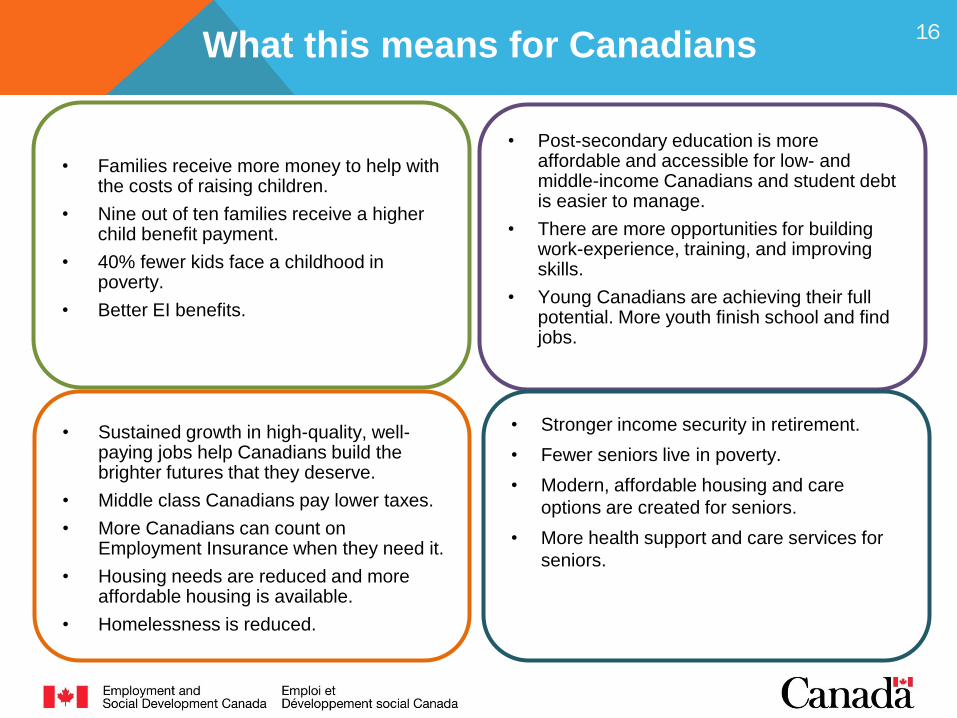

What this means for Canadians

• Families receive more money to help with the costs of raising children.

• Nine out of ten families receive a higher child benefit payment.

• 40% fewer kids face a childhood in poverty.

• Better EI benefits.

• Post-secondary education is more affordable and accessible for low- and middle-income Canadians and student debt is easier to manage.

• There are more opportunities for building work-experience, training, and improving skills.

• Young Canadians are achieving their full potential. More youth finish school and find jobs.

• Sustained growth in high-quality, well-paying jobs help Canadians build the brighter futures that they deserve.

• Middle class Canadians pay lower taxes.

• More Canadians can count on Employment Insurance when they need it.

• Housing needs are reduced and more affordable housing is available.

• Homelessness is reduced.

• Stronger income security in retirement.

• Fewer seniors live in poverty.

• Modern, affordable housing and care

options are created for seniors.

• More health support and care services for

seniors.

16

A vision for helping and

growing the middle class

All Canadians benefit from strong, sustained, and

inclusive economic growth

and everyone has a real and fair chance at economic

opportunity and success.

17