2017 outlook for the intercity bus industry in the united states

TRANSCRIPT

RUNNING EXPRESS2017 Outlook for the Intercity

Bus Industry in the United States

CHADDICK INSTITUTE FOR METROPOLITAN DEVELOPMENT AT DEPAUL UNIVERSITY | POLICY SERIES

BY BRIAN ANTOLIN & JOSEPH P. SCHWIETERMAN* | JANUARY 13, 2017

2017

CHADDICK INSTITUTE FOR METROPOLITAN DEVELOPMENT AT DEPAUL UNIVERSITY CONTACT: JOSEPH SCHWIETERMAN, PH.D. | PHONE: 312.362.5732 | EMAIL: [email protected]

BRIAN ANTOLIN AND JOSEPH P. SCHWIETERMAN*

RILEY O’NEIL AND DANA YANOCHA DATACOLLECTION

AUTHORS

THE STUDY TEAM

RACHAEL SMITHGRAPHICS

FROM TOP RIGHT, COUNTER CLOCKWISE: PHOTO BY ROB YOUNG, HUSSEIN ABDALLAH, EDDIE (USERNAME), AND M.O. STEVENS. ALL PHOTOS LICENSED UNDER CREATIVE COMMONS.

PHOTOGRAPHY

*CORRESPONDING AUTHOR

VERSION 2

1

Intercitybuslinesrolledintothenewyearwithanimprovedshort-termoutlookduetoseveralfactors:aslowlyrecoveringeconomy,upwardmovementinthecostofgasoline,andgrowingcustomerawareness

ofnewtech-orientedserviceenhancements.Severalpotentiallydisruptiveforces,however,loomonthehorizon.Thisreportsummarizesthe intercitybus industry’sperformanceandcompetitivestatus.Part Iprovidesinsightsintowhatcanbeexpectedtoaffectthesectoroverthenextseveralyearsbasedona

reviewofnotabletrends.PartIIexplorestheevolvingcompetitivelandscapeoftheintercitybusindustry,includingtheprevalenceofexpressbusserviceinthecountry’smostheavily-traveledmarkets.

I. SHORT-TERM OUTLOOK FOR THE INTERCITY BUS INDUSTRY

Thefollowingtrendsaresourcesofbothoptimismanduncertaintyforscheduledintercitybustravel.

TREND 1:Years of relatively flat traffic and passenger revenues culminated in targeted cuts by prominent

carriers in 2016, but revenues from passenger operations appear on an upward trajectory and arelikelytogrowaroundthreepercentthisyear.Severalfactors,includinganuptickinthepriceoffuel,suggestthatmarketforcesthathavemarginalizedthegrowthinbustrafficaresubsiding.

Thepast twocalendaryearshaveshowntryingtimes forscheduled intercityoperators.Relatively lowfuel prices nullified some of the advantages of being a fuel-efficientmajormode of intercity ground

travel.Automobilecompetitionintensifiedasaresult,withthenationalaveragepriceofgasolinestayingbelow$2.50throughoutallof2016.1Airlinepricesremainedattheirlowestlevelsinyears,withaverageroundtripticketpricesfallingto$361.20 in2016,downalmost$20from2015,apparentlyhurtingbus

travelonroutesinwhichflyingisanoption.2Worst-casescenariosaboutlongTSAsecuritylinesfailedtomaterialize. Finally, a downturn in rail-freight traffic significantly improved Amtrak’s on-time

performance,luringsomeshort-hoppassengersawayfrombuses.

Nevertheless,recentsignalshavebeenencouraging.Mostnotably,thepriceofoilhasgraduallymoved

upward,risingfromaround$31.68inJanuary2016,to$48.76inJune,tomorethan$52inearly2017.The economy is also improving, resulting in a reduced unemployment rate, which fell from 6.1% inFebruaryto4.5%inNovember.WhileGDPgrewbyonlyabout1.6%lastyear,theFederalOpenMarket

Committeeprojectsgrowthataround2.1%in2017.3

The lackluster rate of economic growth in recent years surely affected the financial performance of

majorbuslines.ResultspublishedbyFirstGroup,convertedfrompoundsterlingtoU.S.dollars,indicatethatitssubsidiary,GreyhoundLines,hadabouta4%dropinrevenuesduringits2016fiscalyear(whichended June30).Ouranalysis suggests thatpassenger revenuesweredowncloser to5% (anestimate

subject to rounding error).4 Meanwhile, conversions to U.S. dollars indicates that megabus.com(“Megabus”),aunitofScotland-basedStagecoachGroup,hadabouta9%dropinrevenuefromNorthAmericanoperations, although theholding company’s total revenues in this regionweredownmuch

less.Theseestimatesmaybeaffectedbyswingsintheexchangerateoverthecourseoftheyear,whicharenottakenintoaccount5.

2

Despite falling revenues from these twonationalproviders, thenumberofpassengers andpassengermilesoftravelontheseandothercarriersappearstohavefallenbyamuchsmallermargin,andinsome

casesevenroseslightly.Someoftherevenuedropappearstobeattributabletopricediscountinginahotlycompetitiveenvironment rather thandecliningdemand.Asnoted inpreviousChaddick Instituteannual intercity bus reviews, accurate estimates of bus traffic remain elusive due to the absence of

comprehensive reporting requirements. We estimate that total intercity bus travel stayed relativelyconstant, at about 62millionpassengers annually,making the sector about twice the sizeofAmtrak.Pleaserefertolastyear’sreportforasummaryofmethodsusedtomakethisearlierestimate.

Only a small number of routes were cut in 2016 despite these difficult conditions. Citing risingautomobile competition,Megabus discontinued its Cleveland, OH to Atlanta, GA service in February.

Launched by Coach USA subsidiary, Lakefront Lines, before being rebranded, this twice-daily serviceconsisted of single level coaches operating via Columbus, Cincinnati, OH, and Knoxville, TN. Moresignificantly, Megabus downsized its Chicago hub, eliminating its route to Omaha—in turn ending

servicetoIowaCityandDesMoines—aswellasservicetoEastLansing,MI,inearly2017.Thesecuts,aswellasselectedroutesinFlorida,markMegabus’mostsignificantdownsizinginrecentyears.

Citing similar concerns, Bieber Tourways discontinued service to Pottsville and Schuylkill Haven, PA,alongitsReadingtoPhiladelphiaroute,whilealsoreducingweekdayfrequencyfromfivetofourtrips.PeterPanBusLinespointedtosoftdemandbeforediscontinuingitsSturbridge,MA-areastopsalongits

SpringfieldtoBostonroute.Frequencyonmostotherroutesacrossthecountrymaintainedfirm,whilesomecorridorsexperiencedmodestexpansion,asnotedbelow.Greyhoundappearstohaveadjustedtodemandconditionslargelybyreducingthenumberofextrasectionsoperatedonmajorroutes.

Severalfactorssuggestthatrevenueshavebegunreboundingandthatthistrendwillcontinuethrough

2017and2018:

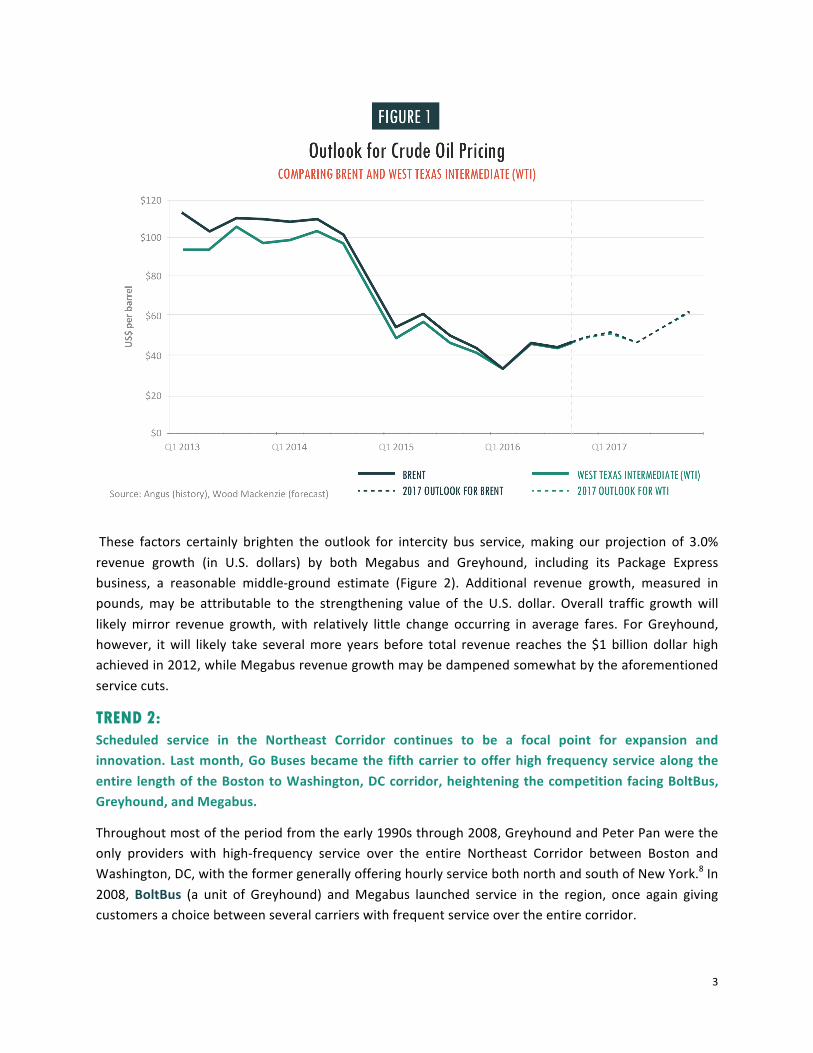

• A consensus exists among commodity analysts that fuel priceswillmove closer to the $55

rangebylate2017.Pricesinthisrangehavespurredmanytravelerstoturntobustravelduetothehighercostsofdrivingandairtravel.AforecastbyWoodMackenzieisshowninFigure1.6

• London-based investment firm Liberum expects that Greyhound revenues will be on theupswingand isupgrading itsoverall recommendation tomakeFirstGroupa “buy”. The firmprojects that Greyhound revenues will rise sharply in 2017, although some of the increase

appears to be due to the more favorable exchange rate when converting dollars to poundssterlingfollowingBrexit.

• TheFederalOpenMarketCommitteerecentlyincreaseditsforecastfornationalGNPto2.1%this year and expects similar growth in 2018. Kipplinger projects similar GDP growth, butsuggeststhatitwillriseto2.5-3%in2018.7

3

These factors certainly brighten the outlook for intercity bus service,making our projection of 3.0%

revenue growth (in U.S. dollars) by both Megabus and Greyhound, including its Package Expressbusiness, a reasonable middle-ground estimate (Figure 2). Additional revenue growth, measured inpounds,may be attributable to the strengthening value of the U.S. dollar. Overall traffic growthwill

likelymirror revenue growth,with relatively little change occurring in average fares. For Greyhound,however, itwill likely take severalmore years before total revenue reaches the$1billion dollar highachievedin2012,whileMegabusrevenuegrowthmaybedampenedsomewhatbytheaforementioned

servicecuts.

TREND 2:Scheduled service in the Northeast Corridor continues to be a focal point for expansion andinnovation.Lastmonth,GoBusesbecamethe fifthcarrier toofferhigh frequencyservicealong the

entire lengthoftheBostontoWashington,DCcorridor,heighteningthecompetitionfacingBoltBus,Greyhound,andMegabus.

Throughoutmostoftheperiodfromtheearly1990sthrough2008,GreyhoundandPeterPanweretheonly providers with high-frequency service over the entire Northeast Corridor between Boston andWashington,DC,withtheformergenerallyofferinghourlyservicebothnorthandsouthofNewYork.8In

2008,BoltBus (a unit of Greyhound) andMegabus launched service in the region, once again givingcustomersachoicebetweenseveralcarrierswithfrequentserviceovertheentirecorridor.

4

Go Buses is the intercity bus division ofAcademyBus, one of the country’s largest bus

operators. Its new service between New York,Washington,DCandNorthernVirginialaunchedin December, complementing existing service

between New York and Boston/Providence.Academy appears prepared to elbow its wayinto the crowded Northeast market and

perhaps even intends to eventually spread itswingselsewhere.

OthermovesbyGoBusesfurthersuggestthatitispositioned forgrowth. InMarch, itextendedits New York to Providence, RI route to the

BrownUniversitycampus,nowservedbytwotothree coaches in each direction fromThursdaythrough Sunday. In September, it entered the

Providence toCambridge/Newton,MAmarket,a distinct operation from its heavily-usedBoston toNew York route. This route features

two to four daily roundtrips, with pricesgenerallyundercutting commuter rail faresoutofBoston’sSouthStation.

Megabus defended its turf by going head-to-head againstGo Buses betweenNewton andNew York,

launching twice-daily express trips that are similarly separate from its Boston toNew York trips. ThecarrieralsoaddedaBrattleboro,VTstopto itsBurlingtontoNewYorkroute,givingthatcommunityanewdirectservicetoManhattan.Furthermore,MegabusaddedstopsinUncasville,CT,onitsNewYork

toFallRiver,MAroute,targetingleisuretravelersvisitingthemassiveMoheganSunCasinoandmakingtwice-dailystopsineachdirectiononFridaysandSundays.BoththisandtheaforementionedVermontserviceareoperatedbyMegabus’operatingpartnerDattco.

Competitionon the routebetweenBostonandHyannis intensifiedwhenPeterPan launchedsixdailyroundtrips, competing with buses of the Plymouth & Brockton Street Railway Company, a fixture in

Massachusetts transportation. Following Route 6, these buses also serve park & ride locations inBarnstableandSagamore.

Greyhoundretainsadominantposition in theNortheastCorridorandhasaparticularly largestake intheunfoldingplansforthePortAuthorityBusTerminalinMidtownManhattan,atwhichGreyhoundisamajortenant.ThePortAuthorityofNewYorkandNewJerseybeganthearduoustaskofplanningfor

thereplacementofthisagingfacilityin2015,andtheplanningcontinuestoday.Regardedastheworld’sbusiest bus terminal by traffic volume, the facility operates at or near its designed capacity, oftencausing significant delays for commuters during rush hour. According to a 2016 study by the Port

Authority,theterminalserves232,000passengers,7,800dailybusesandapproximately615peakhour

5

departures during the afternoon/evening rushas of 2011. Restricted capacity andmovement

has significantly impeded the ability to expandrushhourfrequenciesoraddnewservices.

Although state governors and the agency’sboard agree that a new terminal is needed,severalproblemsstandintheway.Chiefamong

themarewhereexactlyitwillbelocated,howitwill be built and who will pay for whatpercentage of the construction project. The

latest agency budget, which includes a $3.5billion fund allocation for design andenvironmentalstudies,wasapprovedinJanuary

2017.Pressuretoexpandtheterminalwilllikelygrow in intensity due to the projectedexpansion of economic activity in the region

and the particular strength of New York City’seconomy.

TREND 3:Public agencies that had provided subsidized bus services primarily to link rural communities with

nearby population centers are gradually expanding their focus to give these places interlinedconnectionstothenationalnetwork.Thefederal“Section5311”programisenhancingthestrengthofGreyhound’shub-and-spokesystem,restoringsomeoftheconnectivitylostdecadesago.

Alargelyunpublicizedtrendinintercitybustravelhasbeenthegradualexpansionofsubsidizedservice

and the integration of this service into the Greyhound national network. The Federal TransitAdministration’s“Section5311”programloomslargeinthisarena,providingfundingfortransportationservicestocommunitiesoutsideofurbanareaswithpopulationsof50,000orless.Fundsareawardedto

stategovernments,whicharefreetousethefundswithconsiderablediscretion.Therequirementthat15%ofallfundsawardedbeallocatedforintercitybusserviceshasbeenaboonforsmall-townservice.

Stateandlocalgovernmentsarerequiredtomatchasignificantportionofthefederalfundsprovided.Insomeinstances,thisisaccomplishedthroughin-kindservice,suchasadditionalfrequencies,providedbybus companies. State and local governments are also making other funds available for new “feeder

services”thatarenotself-supporting.Itisnotuncommonforbuscompaniestoreceivefundsequivalenttoabout$2.00perbusmiletoprovidethisservice.Forexample,publicagenciesmaygivetheequivalentof$400insubsidesforeach200mileone-waybustripoperated.

PreviousannualintercitybusreportsbytheChaddickInstitutehaveshowcasedthegradualexpansionofthe subsidizednetwork.Over thepast year,Greyhoundhas forged arrangements to allowother new

carrierstosellbothlocalserviceandconnectionstomoredistantpoints.Thisallowssmallcarrierstosellawiderarrayofdestinationstotheircustomerswhilealsostrengtheningtheroleofgreyhound.comas

6

an all-purpose mobility tool, which at present has few rivals in the travel arena. This strategy alsogeneratesadditionalrevenueforthisprominentlegacycarrier.

Greyhoundhasalsobeenactiveinexpandingitsruralnetworkwiththehelpofgovernmentalfinancialsupport.InFloridain2016,thecarrierlaunchedthreenewintra-stateservices,withstatecooperation,

that serve smaller communities along corridors that already have Greyhound Express service. A newMiamitoOrlandoserviceoperatesviaFortLauderdale,WestPalmBeach,andMelbourne,whileanewMiami to Jacksonvilleserviceruns throughthesesamepointsaswellasNewSmyrnaBeachandPalm

Coast,bothservingmanysmallerpoints.AnewMiamitoTampaservicefollowstheAtlanticCoastroutetoMelbournebeforedivergingtothewestthroughWinterHaven,Sebring,andAuburndale.

InNorthCarolina,Greyhoundlaunchedaonce-dailyWilmingtontoCharlotteroutewithstatesupporttomakesstopsatRayetteville,Rockingham,Monroeandseveralruraltowns.InLouisiana,Greyhoundbuilton the recentBatonRouge toNewOrleansexpansionwithanew twice-daily servicemaking stops in

Lafayette,Thibodaux,Raceland,andotherpoints.ThisservicealsofeaturesanewstopatNewOrleans’LouisArmstrongInternationalAirport.

Reallocationsinfundingdidleadtothecancellationofafewroutes.PeterPandroppedoneofitstwice-dailyAlbanytoSpringfield(viaRoute2)routes in2016duetoa lossofcertainMassachusettsBusPlusprogram funds, leaving only onemidday roundtrip. True North Transportation Group, also known as

MAXBus, had operated a pair of daily roundtrips in the north and eastern parts of the state withgovernmentalsupport,butitsnewBusPlusgrantprovidesitfundingforonlyoneBrattleborotoBostontrip, operating via Worcester and Framingham. This resulted in a loss of service to Clinton, Salem,

Pelham, Amherst and other points. These exceptions aside, the outlook for new subsidized routesappearsbright.

TREND 4: Businessclassandluxuryserviceremainonagrowthtrajectory,withexpansioncenteredonspecialty

lines rather than national carriers. The largest scheduled bus lines are not expected to make anymajormovesintheupcomingyear.

As noted in our previous annual intercity bus reports, major bus lines have gradually enhanced thequality of their customers’ onboard experience through mobile-apps, free onboard WiFi, and “bus

tracker”programs(ofwhichGreyhound’sBustracker,launchedin2015,isamongthenewest).Megabusbeganoffering reserved seatsacross itsentireU.S. system that sameyear,with reportedly successfulresults, while Greyhound has been investing in a bring-your-own device entertainment system. Both

carriers,aswellasBoltBus,AdirondackTrailways,andPeterPan,nowsellticketsthroughBusbud.comand Wanderu.com, helping make these “ticketing aggregator” sites for bus travel the equivalent ofExpedia and Travelocity for air travel. Wanderu, in fact, has won a major award from Conde Nast

Traveler.

Evenso,noneof thesebus lineshavemadepublicanyplans toofferbusinessor first class service in

NorthAmerica,despitethegrowingpopularityofpremiumservicesbynichecarrierssuchasEurope’sMegabusGoldservice,whichboastslow-configurationseating.Regionalcarriers,however,continueto

7

leadthewayintheluxurycategory.Vonlane,afirstclassoperatorinTexasthataimstoattracttravelerswhopreviouslyhaveusedcommercialflights,launchedanAustintoHoustonroutelastJanuarywithone

ortworoundtripsdaily.VonlanenowoperatesonallsidesoftheTexasTriangle,havinglaunchedDallastoAustinandDallastoHoustonservices,withcustom-designedbusesrepletewithanonboardmeetingroomandmealsservedbyanattendant.

In April,Concord expanded its “Plus” service fromNew York to Portland,ME from one to two dailyroundtrips, givingpassengers amorning andearly afternoonoption in eachdirection. First class-style

seatingandotheramenities,aswelltheconvenienceofavoidingtheneedtotransferinBoston(ararityfor bus travelers and entirely unavailable for train travelers between Manhattan and Maine) arebolsteringdemand.

InSeptember,Florida’sRedCoach launchedapremium-levelroutefromtheFortLauderdaleairporttoUniversity of South Florida campus in Tampa, a once-a-day with a stop in Naples that significantly

expands the carrier’s footprint in the Sunshine State. The carrier also added a second Miami stop,located at Florida International University, to better serve students aswell as those traveling to andfromMiamiBeachanddowntown.Previously,RedCoachonlyservedMiami InternationalAirport.One

firstclassbusandonebusinessclassbusmakethenewcampusstopineachdirectiondaily.

TREND 5: ThedramaticexpansionofFlixbusinEurope—anditsacquisitionofMegabus’retailoperationonthecontinent’smainland—couldforeshadownewapproachestobrandingandcontractingbusservicesin

theUnited States. Interest inmore sophisticated pricing strategies is also growing,mirroring thoseemployedbycommercialairlines.

TheexpansionofFlixbus inEuropehasbeenoneofthebiggeststories in intercitybustraveloverthepast year. This technology-based startuphas abusinessmodel that is quitedifferent than thatwhichprevailsinmostoftheU.S.Ratherthanoperatingbuses,thecompanycontractswithexistingcarriersto

rebrandas“Flixbuses”inexchangefortakingonallresponsibilityformarketing,pricing,schedulingandpromotion.TobepartofFlixbus,carriersneedtoadheretoarigidsetofqualitycontrolguidelinesthat

assureconsistencyofservice.

FlixBus touts itselfnot justasabus servicebut“acombinationof tech-startup,e-commerceplatform

and transportation company”. Beginning as two separate bus carriers, FlixBus and MeinFernbuscombinedforcesin2015inresponsetoGermany’sderegulationofthetransportationindustry.Flixbusquicklymorphed intoa juggernaut ingroundtravelthroughoutContinentalEurope,anexpansionthat

hassincebeenenhancedbyaEuropeanUnionlawthatderegulatescross-borderbustravel.

Severalnetworkdevelopments in2016havekeptFlixBusonarapidgrowthtrajectory. InJanuary, the

company launched a new network of routes in Central and Eastern Europe, with headquarters inBudapest and Zagreb. From there, new daily connections to 50 destinations in the Czech Republic,Slovakia,Hungary,PolandandCroatiawereadded.InMarch,SpainandtheUKwereaddedasnewcross

border service regions, connecting two of Europe’s largest cities (London and Paris) aswell as Spain,FranceandItaly.

8

Themonth of June brought online new locations to the Flixbus networkwith connections in Croatia,SloveniaandBucharestinRomania,aswellastheacquisitionofMegabus’retailbusinessinContinental

Europe. With the latter, Stagecoach (parent company of Megabus) became a contractor for selectFlixBusservicesinBelgium,France,Italy,Germany,SpainandtheNetherlands—solidifyingitsstatusasEurope’slargestintercitybusnetwork.ThismovewassoonfollowedbytheacquisitionofPostbus,the

longdistancecoachserviceofDeutschePost(morecommonlyknownasDHLintheUS),inAugustandtheannouncementthatahubinDenmarkwouldbeestablishedin2017.Byoneestimate,Flixbusnowholds81%oftheinternalGermanintercitybusmarket.9

Flixbus is eying expansion elsewhere, possibly the United States, supported by an infusion of freshventurecapitalinlate2016.Perhapsthemostsalientlessonfromthiscarrieristhatitispossiblefora

startup to quickly develop enormous brand awareness for operators that once had only a regionalpresence, and to give smaller operators the opportunity to gain access to sophisticated pricing andschedulingtechnologiesthroughnewtypesofcontractualarrangements.

A philosophy similar to Flixbus is evident in the Atlanta-based Shofur, an innovative transportationmanagement company serving corporate, event and charter groups, which made its first foray into

scheduled intercity service in September. Starting with one daily round trip linking Austin, Houston,Dallas and Waco, the company attempted to differentiate itself through tech- and data-focusedcustomerservice,withticketssoldbothonlineandthroughamobileapp.Coacheswereoperatedbyits

charterbuspartners andbrandedas Shofurbefore servicewas suspended forundisclosed reasons inNovember.

Sophisticated data analysis and technology are also hallmarks ofBusBot, aManhattan-based startupthatusesartificial intelligencetohelp intercitybusoperationsreachrevenuegoals.Drawinguponthe

statisticalmethodsusedforairlineschedulingandpricing,BusBothelpsbuscompanies“leverage[their]ownhistorical data aswell as external data tomakebetter demandpredictions”—something smallerbuslineshavenotbeenabletodo.10SeveralcarriersarenowusingBusBot’sschedulingandpricingtools

withreportedlysuccessfulresults.

TREND 6:New technological platforms could transform the way intercity ground transport services aremarketedandsold. Innovativeapp-basedservicessuchasFlitwaysandSkedaddlehaveemergedas

leadersandcouldbecomedisruptiveforcesintheyearsahead.

The following three technology innovations gained significantmomentum in 2016 and could become

disruptiveforcesinintercitybustravel.

Crowd-SourcedBusService:

New technological platforms are emerging that allow bus services to set schedules throughcrowdsourcing.Ifenoughtravelersexpressawillingnesstopay,abuscanoperatebetweentwopointsatasettimeonaparticularday.RallyBusandSkedaddleemergedasmarketleadersinthiscategory—

bothallowtheindividualwholaunchesthebustriptotravelfreeifenoughotherriderssignuptojoin

9

theride.Thefaresriseasthenumberofreservationsincrease.Ifthetripfailstoattractenoughriders,however,itdoesnotoperateandnofaresarecollected.

OuranalysisrevealedthatSkedaddleadvertised242routesonJune15,2016,56routesonSeptember,16, 2016 and 238 routes on January 9, 2017. This suggests wide month-by-month variation in trip

availability, and greater demand for tripswhen a large event is set to occur.11 Althoughmost routesinvolve travel to festivals, music and sporting events, and other cultural activities, some resembleintercityservices,withroutesleavingfromlocationsadvertisedasnearthePortAuthorityBusTerminal

inNewYork.

Atpresent,thissectorshouldberegardedasaninfant industry.Ascrowd-sourcedbustravelgrows, it

will likely need to confront regulatory challenges associated with curbside pickup and drop-off. InBoston, forexample, such regulation requiresall intercitybusoperators touse theSouthStationBusTerminal, which requires paying a usage fee.12 In New York, curbside operators using advertised

schedules must obtain permits to serve a specific location.13 If crowdsourced bus service spills intoconventionalcity-to-cityroutes,however,itcoulddiverttrafficfromestablishedbuslines.

Pre-arrangedRideServices:Whereas Lyft and Uber generally do not allow customers to “pre-book” rides, several new apps aremaking this possible, with flitways.com (Flitways) emerging as a clear leader. Working with taxicab

companies,vanoperators,andothers,Flitwaysquotestravelersapriceinadvance.Thisserviceis,atthemoment,acclimatedtowardsmallgroupsandcorporatetravelers.Arecentsearchshowedthatone-waypricesforacarwithdrivercouldbeattractiveforgroupsofthreeorfouronnumerousroutes,suchas

CincinnatitoDayton($96),BostontoProvidence($131),andSanFranciscotoSanJose($116).Althoughmore costly than bus travel, these services give travelers unable or unwilling to drive a new option.

Interestingly,FlitwaysaddedMegabustoitssearchenginein2016.

There is speculation thatpre-arranged rideappscouldgrow in sophistication toallow formuchmore

affordableoptions.Forexample, ifamethod isdeveloped tomatch travelers indifferentpartieswiththe same driver, or enlist driverswho are already traveling to a desired destination, prices could falldramatically and possibly competewith bus travel. Similarly, one can envision a timewhen Lyft and

Uber begin offering similarly pre-arranged rides. At present, none of these services appear to bedramatically shifting traffic from scheduled intercity bus lines, but the pace of technological changemake the future difficult to predict. Throughout this year, the potential diversion of traffic from

ridesplitting and pre-booked ride services seems more acute for airport shuttle operators thandowntown-orientedbusoperators.

There is also concern that ridesourcing companies suchas Lyft andUbermightoffernewoptions fortravelers willing to share rides on intercity routes. Although trips over 60 miles are rare on thesetransportationnetworkcompanies today, it seems likely that such“TNCs”willonedayoffernew low

costlongdistanceoptionstoconsumers.

10

II. HOW ARE CITY-TO-CITY EXPRESS BUS LINES CHANGING TRAVEL?

Thissectionevaluateshowtheexpansionofscheduledintercitybusserviceisaffectingthemobilityof

U.S. travelers. The analysis focuses particularly on the nature of competition between city-to-cityexpress(C2C)carriers,whicharedefinedhereascarriersthat:

• Specializeinexpressservicebetweenlargecities• Emphasizeonlineticketing• Provideguaranteedseatingtoallticketbuyers

• Utilizecurbsidedropoffandpickupinmostcitiesratherthanconventionalterminals

Thesecarriersgenerallydonotoffer interlineticketingwithotherbus linesorprovide localserviceto

smallercommunities.Theyalsoavoidhavingtripswithnumerousintermediatestops,whichaddtraveltimetojourneys.

Bestbus,GoBuses,BoltBus,Vamoose,TripperBus,andMegabusareamongthecarriersinthiscategory.SomebuslineshaveseveralbutnotallofthequalitiesofC2Ccarriers,andarethusexcludedfromourconsideration.

TheresultsarebasedonadatasetcreatedbytheChaddickInstitutewithinformationonroutesservedby leading C2C carriers. For each segment, the mileage and schedule frequency was recorded, and

informationwas collected to determine the status of competingGreyhound, Amtrak, and air service.Longermulti-segmentsjourneyswereusedtoevaluatetheairlinecompetition,andAmtrakrouteswereevaluatedtoassessthebus-railcompetitiveoverlap.

Threefindingsstandoutfromthisdata:

FINDING 1: Despitebeing relativelynewto theU.S.marketplace,BoltBusandMegabushavegrown tooperate

247 intercitypairs.LessthanaquarterofMegabus’dailybusmileagecompeteswithBoltBus,whilemostofBoltBus’servicecompeteshead-to-headagainstitslargerrival.

Thefindingsshowtheenormous impactthatBoltBusandMegabushavehadsincetheybeganserviceon theU.S.mainland in 2006 and 2008, respectively. Analysis of the schedule information described

abovesuggeststhatMegabusoperatesabout41millionbusmilesyear,makingitapproximatelythreetimeslargerthanBoltbus(14millionbusmiles)andaboutone-thirdthesizeofGreyhound(114millionbusmiles).MegabusoperatesslightlymorebusmilesthanAmtrakdoestrainmiles(about38million),

butfarfewerseatmiles.

Megabus tends to overlap less with other prominent C2C carriers than BoltBus does. Just 24% of

MegabusdeparturescompetedirectlywithBoltBusandotherprominentC2Ccarriers.ItsentireAtlanta,Chicago, and Texas hubs, for example, lack prominent C2C competition. Conversely, BoltBus,with itsfocus on high-density corridors, faces competition from Megabus on 65% of its routes. Among the

routesservedbyBoltbusnotservedbyotherC2CcarriersareLosAngelestoLasVegasandPortland,ORtoVancouver,BC,viaSeattle.

11

Although it is not considered a C2C carrier, Greyhound has an almost ubiquitous presence for routecompetition. BoltBus andMegabus face competition from it onmore than 90% of their routemiles,

althoughonlyarelativelysmallshareofthesecarrier'sbusmilesoverlapwiththepremiumGreyhoundExpressservice.

FINDING 2: Amtrak faces competition from BoltBus or Megabus on nearly three quarters of its short- and

medium-distancecorridormileage.MorethanathirdofMegabusbusmiles,however,areonroutesnotservedbyAmtrak.

CompetitionbetweenexpressbusandAmtrakservice is intenseandgrowing,althoughrelatively littleanalysis of the nature of this competition has been undertaken. Our analysis shows that 97.6% ofBoltbus’busmilesareonroutesthatarecompetitivewithAmtrak(allbuttheBarstow,CAtoLasVegas

segment,partofitsroutefromLosAngelestotheNevadagamingcenter),whilejust68.6%ofMegabus’busmilescompetewithAmtrak.AmongthemostnotableroutesnotservedbyAmtrakareBoltBus’LosAngelestoLasVegasrouteandMegabus’DallastoHoustonandChicagotoColumbus,OHandLouisville

services,aswellasitsextensiveoperationsto/fromAtlanta,easternTennessee,andStateCollege,PA.

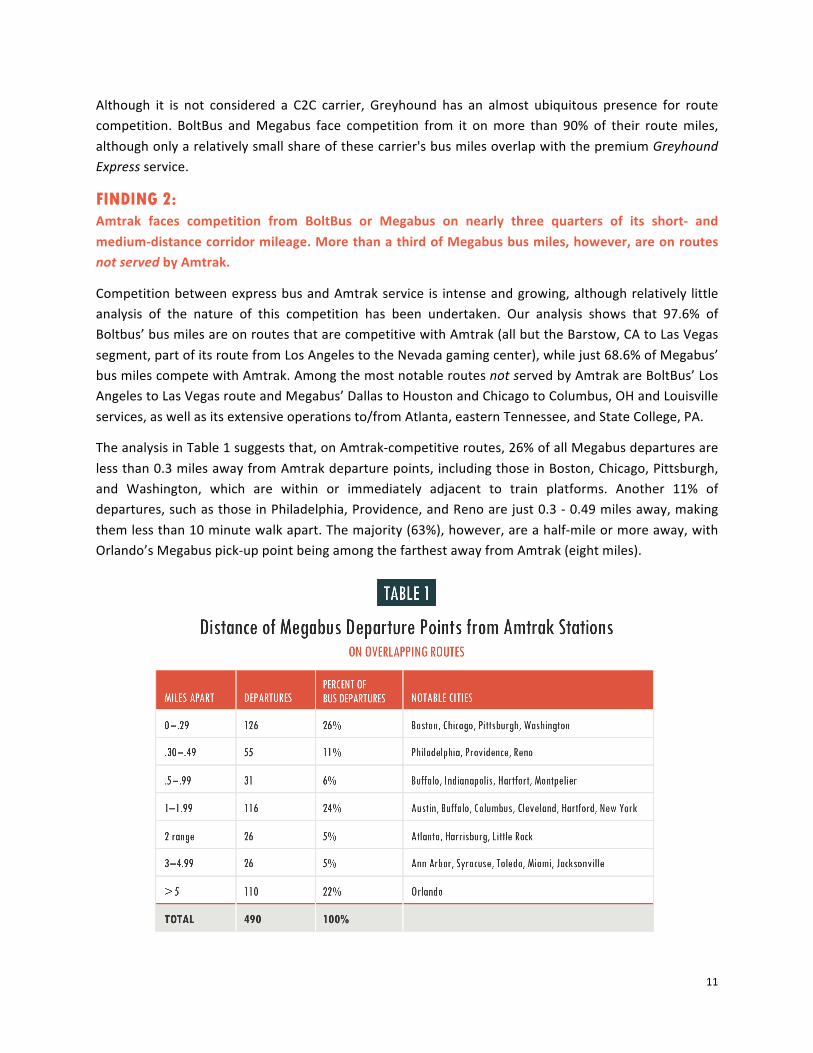

TheanalysisinTable1suggeststhat,onAmtrak-competitiveroutes,26%ofallMegabusdeparturesare

lessthan0.3milesawayfromAmtrakdeparturepoints,includingthoseinBoston,Chicago,Pittsburgh,and Washington, which are within or immediately adjacent to train platforms. Another 11% ofdepartures,suchasthoseinPhiladelphia,Providence,andRenoarejust0.3-0.49milesaway,making

themlessthan10minutewalkapart.Themajority(63%),however,areahalf-mileormoreaway,withOrlando’sMegabuspick-uppointbeingamongthefarthestawayfromAmtrak(eightmiles).

12

Many cities havepushedbus companies tomoveout of central business districts or away from trainstations because of congestion and crowd control. Thus, it is amischaracterization to claim that C2C

busesinvariablychoosedeparturelocationsimmediatelyadjacenttomajortrainstations.

AcrossAmtrak’sentire21,822 route-milenetwork,9,935miles (46%)are subject tocompetition from

BoltBusandMegabus.Amongthe4,854milesthatcompriseitsshort-andmedium-distancecorridors,3,598miles (74%)are subject to competition.Trainson theNortheastCorridor (NEC),easilyAmtrak’sbusiest route, facecompetition frombothBoltBusandMegabus,while69%ofAmtrak routesoutside

theNECfacecompetitionfromonebusprovider.14

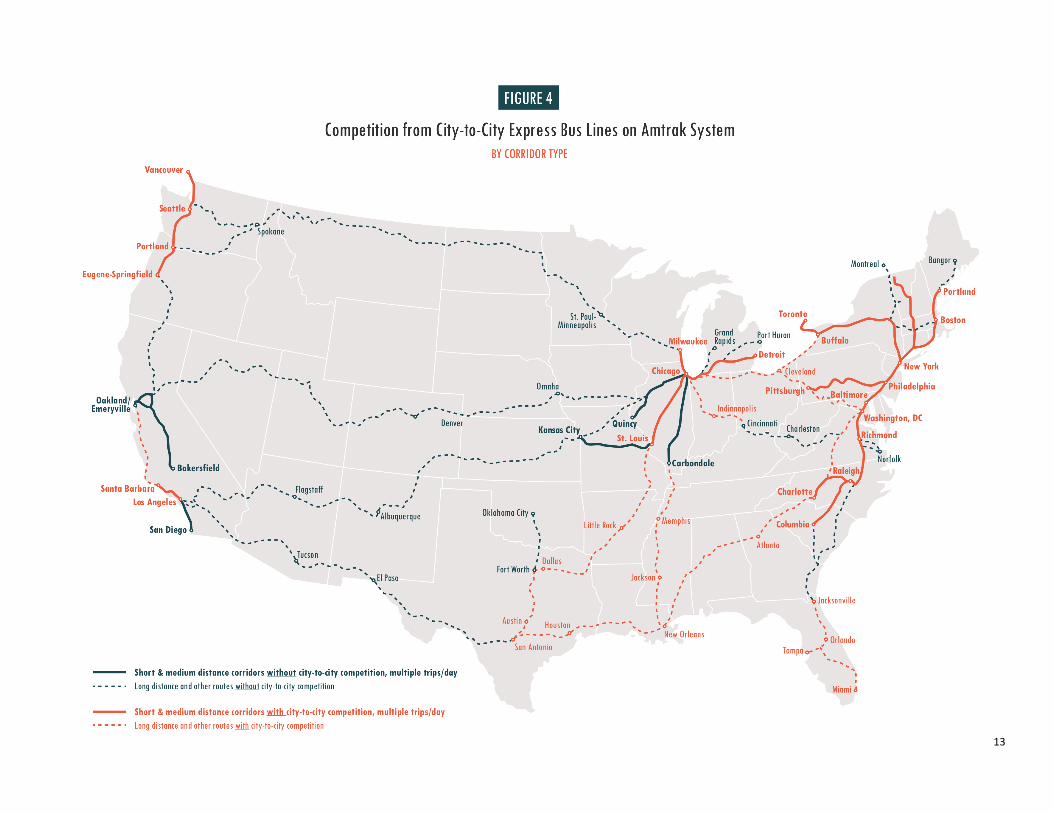

The special pattern of bus-rail competition is depicted in Figure 4, which shows short- andmedium-

distanceAmtrakcorridorswithmultipledailytrainfrequenciesinbold.Themostnotablerouteswithoutbus competition (shown in light blue) are Los Angeles to San Diego; Oakland to Sacramento andBakersfield;andChicagotoCarbondaleandWestQuincy.Therelativelyshortdistanceassociatedwith

some routes appears to offset some of the advantages of bus service. The two California routesmentionedabove, forexample,are lessthan125miles long.Competitionfrombuses isalsorelativelymodestonthe90-mileChicagotoMilwaukeecorridor,overwhichMegabusgenerallyoperatesonlya

pairofdailyroundtripscomparedtoAmtrak’sseven.Onmostotherroutes,however,thefrequencyofbusserviceiscomparableto,orabove,thatofferedbytherailoperators.

TheseverityofthecompetitiononsomeroutesisalsolessenedbytheabsenceofBoltBusorMegabusservice to intermediate stops. Buses often run express from one end of the corridor to the other,bypassing along-the-way cities that are the source of many Amtrak passengers. This is evident on

Amtrak’sChicagotoSt.Louisroute,whichservesJoliet,Bloomington,SpringfieldandothercitiesinthePrairieStatethatarenotservedbyC2Ccarriers.TheNortheastCorridor isoneofthefewcorridors in

which there is competitiveC2Cbus serviceatmany intermediate stops, andeven then these carriersoftenonlyoperatefromtheintermediarycitytothemajorcities,withoutlinkingsmallerstops.

A largenumberofMegabusroutesconnectcities inwhichnoAmtrakservice isavailable (Figure5).AparticularlylargenumberemanatefromAtlanta,Columbus(OH),Houston,Louisville,StateCollege(PA)and various Tennessee points, including Chattanooga,Memphis andNashville. These cities are either

alongonlyoneAmtrak route, or, likeChattanooga,Columbus, Louisville,Nashville, and StateCollege,havenointercitytrainserviceatall.ThissuggeststhatC2CcarriersaremakingnotablecontributionstomobilityinareaspoorlyservedbyAmtrak.

13

14

15

FINDING 3: Despitetherapidexpansionofcity-to-cityexpressservice,manymarketsremainunservedbythesepopularcarriers.Moreover,manycorridorscanberegardedas“GroundTransportationGaps”,astheyalso lack rail-passenger service, making options for ground travel other than private automobiles

extremelylimited.

City-to-cityexpressbusservice isquitepervasiveamongthecountry’smostheavily-traveledcitypairs

(i.e.,origin-destinationcombinations).Considerfirstthesector’sprevalenceinthe200heavily-traveledcity pairs in the United States. The list of thesemarkets was obtained from the federally sponsoredMultimodal Interregional Passenger Travel Origin Destination Data project15. C2C carriers are quite

prevalent among the subset of city pairs that are between 100 and 375 miles and link cities withpopulationsofat least100,000people—qualitiesthatmakethemfavorableforbustravel.Amongthe50largestcitiesthatmeetthesecriteria,C2Ccarriersserve30,or60%ofthetotal.Amongall128city

pairsthatmeetthesedistanceandpopulationcriteria,thesectorserves63,orslightlylessthanhalf.

Themostheavily-traveledroutesthatmeetthepopulationcriteriamentionedabovethatarenotserved

byC2C linesare shown inTable2.The largest citypairnot served is LosAngeles toSanDiego,whichrankssecondinvolumeamongroutesmeetingthesecriteria.

As can be seen on Table 2, many underservedroutes involve an endpoint with a metropolitanpopulationoflessthanhalf-million.Asnotedinthe

right-hand column,Megabushaspreviously servedasignificantnumberoftheseroutes.

Other notable city pairs that are not on the list(someofwhichinvolveddistancesofmorethan375miles) includeColumbus,OHtoDetroit,MI;Fresno

to Los Angeles; Los Angeles to Sacramento;Brownsville, TX to San Antonio; and El Paso to

Albuquerque. C2C service is even less common inmarketsthataremorethan400milesapart,asthatdistancemakes bus travel too time-consuming for

mosttravelers.

Some city pairs could be regarded as “Ground

TransportationGaps”astheylacknotonlyC2CbusservicebutAmtrakserviceaswell.Conventionbusserviceisgenerallyavailableontheseroutes.Some

travelers, however, are (rightly or wrongly)unwilling to travel on conventional bus lines,making their options for ground transportation,

otherthandrivingquitelimited.

Largest City Pairs Not Served byCity-to-City Express Bus Lines

TABLE 2

110-375 MILES

RANK

2

14

20

22

CITY PAIR MILES NOTES

Los Angeles – San Diego

Bakersfield – Los Angeles

Phoenix – Tucson

Norfolk/Virg.Beach – Washington DC

124

113 Amtrak Thruway Bus Service

116

209

29

30

33

Los Angeles – Phoenix

New York – Scranton

Laredo – San Antonio

Former Megabus route

372 Former Megabus route

120

156

57

58

59

64

Asheville – Atlanta

Detroit – Grand Rapids Former Megabus route

Phoenix – San Diego

Chicago – Peoria

199

158

355

166

69

72

73

Dallas – Oklahoma City

Harrisburg – Washington

Cincinnati – Columbus Former Megabus route

206

120

111

16

17

On some of these routes, bus travelers must also accept the uncertainties of traveling without aguaranteedseat.Thisoften leads to travelersarrivingat thebus stationveryearly toassure theyare

abletoboardthebus,eventhoughtheriskofnotgettingaseatonapreferredbusisgenerallyminimaldue to advances in computer reservations systems. Heavily-traveled Ground Transportation GapsincludeChicagotoPeoria,ILandFt.Wayne,IN;DetroittoColumbus,OHandCincinnati;Atlanta,GAto

Asheville,NCandnumerousroutesinsouthTexascenteredaroundSanAntonio(Figure6).

These results illustrate that, while C2C bus service has had transformative effects, many markets

remainedunserved.WhileAmtrak’scorridorshavebeenaffectedbythiscompetition,itslongdistancerouteshavebeen largelyunaffected. In the short term, expansionbyC2C carriers is arguably amoreviable way to bring improved service to the aforementioned Ground Transportation Gaps than the

expansionof rail service.New rail service generally takes years to launch,while the economics of airservicemakeitdifficultforairlinestoprofitwithlowfaresonrouteslessthan250miles.

FutureChaddick Institute reportswill seek to conduct additional analysisof the competitive statusofbusserviceandtheoutlookforexpansionintopreviouslyunservedmarkets.

To reach the study team, please email [email protected] or call 312.362.5731. AdditionalChaddickInstitutepublications,includingpastannualreviewsofintercitybustravel,canbefoundatlas.depaul.edu/Chaddick.

1EstimatesforaveragefuelpricesobtainedfromtheU.S.EnergyInformationAdministration.http://www.eia.gov/outlooks/steo/

2TheseestimatedarefromtheBureauofTransportationStatisticsforscheduledomesticairfares.Foraneasilyaccessedsummaryofthisinformation,pleaserefertohttps://ycharts.com/indicators/us_average_airfares/BTS

3GDPestimatefromKiplinger.comareobtainedfromhttp://www.kiplinger.com/article/business/T019-C000-S010-gdp-growth-rate-and-forecast.html

4FirstGroupreportstheshareofitsrevenuefromfarerevenue,PackageExpress,foodsales,andothercategoryinpercentagesroundtothenearestinteger,whichpreventpreciseestimatesoftrends.Theseestimatesarebasedonthoseintegrals.However,theshareofrevenueattributabletopassengeroperationsin2015forpassengerrevenueisassumedtobe79.4%(ratherthan70%)duetothefactthatthisnumberappearstohovernear80%.

5ExchangesrateswerederivedbytakingthearithmeticaverageoftheU.S.FederalGovernment’srecommendexchangerateconversationsforthetwoyearsinwhicheachfiscalyearstraddles.Forexample,theexchangerateforthe2010fiscalyearistheaveragefor2009and2010.ThefollowingGBPtoUSDratesareused:2010:.6730,2011:.6610,2012:.6525,2013:.6605,2014:.6585,2016:.6755 6Projectionsforfuelpricesobtainedfromhttp://www.eia.gov/outlooks/steo/report/prices.cfm

7TheannouncementbytheFederalOpenCommitteecanbefoundat:http://www.jec.senate.gov/public/index.cfm/republicans/analysis?ID=DE809839-03D8-4102-9AE1-AF4982C79762Pleaserefertofootnote3fortheKipplingerlink.

8VamoosebrieflyoperatedbusesfromNewYorktoboththeBostonandWashingtonmetropolitanareasin2007

18

9ForasummaryFlixbus’Germanmarketshare,pleaserefertohttps://global.handelsblatt.com/companies-markets/flixbus-grows-up-603094

10Forinformationaboutthisstartup,pleaserefertowww.busbot.us

11TheLastBusStartupStanding,TechCrunch,November29,2016.AccessedonSeptember5,2016athttps://techcrunch.com/2015/11/29/the-last-bus-startup-standing-chariot/

12“BostonAreaTerminalActivityandCapacity,”2013MassachusettsRegionBusStudy,BostonRegionalMetropolitanPlanningOrganization,2013.AccessedonSeptember2,2016athttp://www.ctps.org/data/html/studies/transit/2013_Mass_Regional_Bus_Study/CH4_Regional_Bus_Study.html

13IntercityBusPermits,NewYorkDepartmentofTransportation.n.d.AccessedonSeptember2,2016athttp://www.nyc.gov/html/dot/html/ferrybus/intercity-bus.shtml

14Amtrak’sCoastStarlightcompeteswithBoltBusandMegabusontheLosAngeles–SanFranciscoroute,butthisroutehasonlyonetrainineachdirectiondailyandthusisnotclassifiedasacorridor.

15Forasummaryofthisresearchinitiative,pleasereferto:https://www.fhwa.dot.gov/policyinformation/analysisframework/03.cfm