2017 full year - glanbia/media/files/g/glanbia-plc/documents/2018...investing in plant-based...

TRANSCRIPT

2017 Full Year

Results Presentation 21 February 2018

CAUTIONARY STATEMENT

2017 Full Year Results | Slide 2

Full Year

Highlights

2017 Full Year Results Presentation

8TH YEAR OF DOUBLE-DIGIT GROWTH

2017 Full Year Results | Slide 4

Total Group Pro-forma¹ EBITA

+8.6% constant currency²

Wholly-owned volume growth

+5.3%

Dividend payout

raised to 25%

2017 FINANCIAL Highlights 2017 STRATEGIC Highlights

Acquisition of Amazing Grass and Body & Fit

Disposal of 60% of Dairy Ireland

Refreshed Group strategy

Group structure focused on two growth platforms and strategic JVs

1. Pro-forma Adjusted Earnings Per Share for the continuing Group calculation

assumes the Dairy Ireland segment and related assets were disposed of at the

beginning of the 2016 financial year. A reconciliation of the pro-forma and

reported adjusted earnings per share can be found in the appendix of this

presentation

2. To arrive at the Constant Currency Change, the average FX rate for the current

period is applied to the relevant reported result from the same period in the

prior year. The average Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY

2016: €1 = $1.107)

Pro-forma¹ adjusted EPS

+10.2% constant currency²

2017 TOTAL GROUP PRO-FORMA EBITA¹ PROGRESSION

2017 Full Year Results | Slide 5

JVs €56m

JVs €68m

GN €111m

GN €114m

GPN €162m

GPN €170m

€0m

€50m

€100m

€150m

€200m

€250m

€300m

€350m

€400m

2016 2017

Glanbia Performance Nutrition

Like-for-like branded revenue growth and acquisitions

Glanbia Nutritionals

Continued growth in Nutritional Solutions

Joint Ventures

Strong dairy markets and volume growth

Drivers

€330m

Total Group

pro-forma EBITA GPN EBITA

GN EBITA JV pro-forma EBITA

€351m

+ 21.9%

+ 4.1%

+ 7.0%

Constant currency growth

1. Pro-forma Adjusted Earnings Per Share for the continuing Group calculation assumes the Dairy Ireland segment and related assets were disposed of at the beginning of the 2016 financial year. A reconciliation of the pro-forma and

reported adjusted earnings per share can be found in the appendix of this presentation

2. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the same period in the prior year. The average Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY

2016: €1 = $1.107)

STRONG YEAR OF STRATEGIC EXECUTION

Amazing Grass and

Body & Fit acquired

for €168m

Investing in plant-based nutrition and DTC¹ capability

On-going investment planned to drive growth

Disposal of 60% of

Dairy Ireland for

€209m

Glanbia Ireland joint venture created with ambitious growth plans

SwC – 25% expansion

in production capacity

$140m

Commissioning to be completed by Q3 2018

Initiatives

2017 Full Year Results | Slide 6

Update

1. Direct-to-consumer

IMPACT OF DAIRY IRELAND TRANSACTION

2017 Full Year Results | Slide 7

Creation of

Glanbia Ireland JV

The majority of the

Group’s primary dairy

processing now

in JVs

Two wholly-owned

growth platforms

Improved margin

profile in wholly-

owned Group

+120 bps

plc 40%

CO-OP 60%

Glanbia

Ireland

Ownership

GPN 47% GN

53%

2017

Revenues

10.7%

11.9%

0%

2%

4%

6%

8%

10%

12%

14%

2016¹ 2017²1. 2016 margin is the Glanbia wholly-owned reported margin, which includes the Dairy Ireland segment

2. 2017 margin is the Glanbia wholly-owned margin, excluding the Dairy Ireland segment. The Dairy Ireland segment was disposed of on 02 July 2017

Operational

Review

2017 Full Year Results Presentation

ACQUISITIONS

REVENUE

€1,121.1m

+13.7% (cc²)

EBITA

€169.7m

+7.0% (cc²)

LFL BRANDED

REVENUE

+6.3%

Vol. +8.0%

EBITA margin

15.1%

-100 bps (cc²)

INNOVATION

GLANBIA PERFORMANCE NUTRITION

2017 Full Year Results | Slide 9

Performance Good performance with total

branded revenue growth of 15%

Growth Growth driven by LAPAC,

EMEA and acquisitions

Innovation Strong performance in

ready-to-eat format

1. Percentage movements are on a constant currency basis

2. To arrive at the Constant Currency Change, the average FX rate for

the current period is applied to the relevant reported result from the

same period in the prior year. The average Euro US Dollar FX rate

for 2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

3. Reported & constant currency reconciliations can be found in the

Appendix of this presentation

GPN MARKET OVERVIEW

• A global market leader

• GPN brands are

available across a

broad mix of

geographies and

channels

• GPN positioned to

deliver mid-to-high

single-digit volume

growth in 2018

2017 Full Year Results | Slide 10

Online 26%

Distributors 30%

Specialty 28%

FDMC¹ 16%

Total €1,121m

GPN Global Revenue 2017

by Channel

North America

62%

Rest of World 38% Total

€1,121m

GPN Global Revenue 2017

by Region

1. Food, Drug, Mass and Club

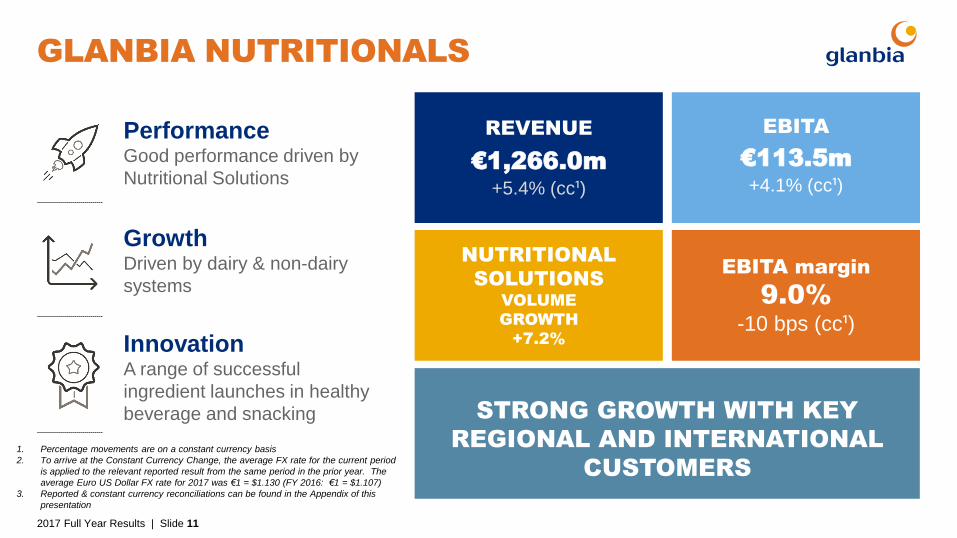

GLANBIA NUTRITIONALS

2017 Full Year Results | Slide 11

Performance Good performance driven by

Nutritional Solutions

Growth Driven by dairy & non-dairy

systems

Innovation A range of successful

ingredient launches in healthy

beverage and snacking

REVENUE

€1,266.0m

+5.4% (cc¹)

EBITA

€113.5m

+4.1% (cc¹)

NUTRITIONAL

SOLUTIONS

VOLUME

GROWTH

+7.2%

EBITA margin

9.0%

-10 bps (cc¹)

STRONG GROWTH WITH KEY

REGIONAL AND INTERNATIONAL

CUSTOMERS

1. Percentage movements are on a constant currency basis

2. To arrive at the Constant Currency Change, the average FX rate for the current period

is applied to the relevant reported result from the same period in the prior year. The

average Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

3. Reported & constant currency reconciliations can be found in the Appendix of this

presentation

NUTRITIONAL SOLUTIONS OVERVIEW

2017 Full Year Results | Slide 12

Dairy 39% Non-

dairy 61%

Total

€532m

• Nutritional Solutions

is a key growth

engine

• Growth is being

driven by consumers

seeking ‘Better-For-

You’ and convenient

products

• Nutritional Solutions

supplies a range of

customers in a variety

of consumer

categories

Nutritional Solutions

42% US Cheese 58%

SPORTS &

PERFORMANCE

NUTRITION

LIFESTYLE

NUTRITION &

SUPPLEMENTS

EARLY

LIFE

FUNCTIONAL

BEVERAGE

CLINICAL

& MEDICAL

NUTRITION

DRESSINGS,

SAUCES &

SPREADS

BAKERY COSMETICS &

PERSONAL CARE

ANIMAL

NUTRITION

BARS, CEREALS

& SNACKS

Glanbia Nutritionals

Total Revenue 2017 €1,266m

Nutritional Solutions

Dairy/Non-dairy Revenue

Nutritional Solutions consumer categories

US CHEESE – INNOVATIVE PARTNER MODEL

2017 Full Year Results | Slide 13

• #1 position in the American-style

cheddar cheese category

• Commercial, technical and

operational partner for US JVs on

route-to-market and innovation

• Partnership approach with customers

on innovation

• On track for commissioning of new

plant in Michigan in 2020

52%

48%

2017 Total cheese production

Glanbia Nutritionals SwC JV

420,000

tonnes

STRONG PERFORMANCE FROM

JOINT VENTURES

2017 Full Year Results | Slide 14

Performance Strong performance in Revenue,

EBITA & margin

Growth Driven by mainly by volume

growth and relatively strong dairy

markets

Strategic Partnerships Innovative & robust business

model

REVENUE

€1,093.4m

+35.7% (cc¹)

EBITA

€63.4m

+50.2% (cc¹)

EBITA margin

5.8%

+60 bps (cc¹)

Joint Ventures Revenue

JV

Glanbia

Ireland SwC

Glanbia

Cheese Total

100% Revenue (€’m) 1,407 738 317 2,462

Glanbia share (€’m) 563 369 162 1,093

1. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the

same period in the prior year. The average Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY 2016: €1 = $1.107).

Financial

Review

2017 Full Year Results Presentation

INCOME STATEMENT

2017 Full Year Results | Slide 16

2017 results summary

Pre-exceptional

€’m Reported currency

2017 2016 Change

Revenue (Wholly-owned) 2,387.1 2,231.7 +7.0%

EBITA (Wholly-owned) 283.2 273.3 +3.6%

EBITA margin 11.9% 12.2% -30 bps

Amortisation (43.1) (37.4)

Net Finance Costs (23.0) (22.8)

Share of Joint Ventures 42.8 26.0

Income Tax (38.3) (39.3)

Profit from continuing operations 221.6 199.8

Profit from discontinued operations 9.8 27.1

Profit for the period 231.4 226.9

Adjusted EPS - Continuing operations on a pro-forma¹ basis 87.11c 80.40c +8.3%

Adjusted EPS – Reported (continuing & discontinued operations) 89.17c 86.02c +3.7%

Constant

currency²

2017

+9.2%

+5.8%

-30 bps

+10.2%

+5.3%

1. Pro-forma Adjusted Earnings Per Share for the continuing Group calculation assumes the Dairy Ireland segment and related assets were disposed of at the beginning of the 2016 financial year. A reconciliation

of the pro-forma and reported adjusted earnings per share can be found in the appendix of this presentation

2. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the same period in the prior year. The average Euro US Dollar FX rate for

2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

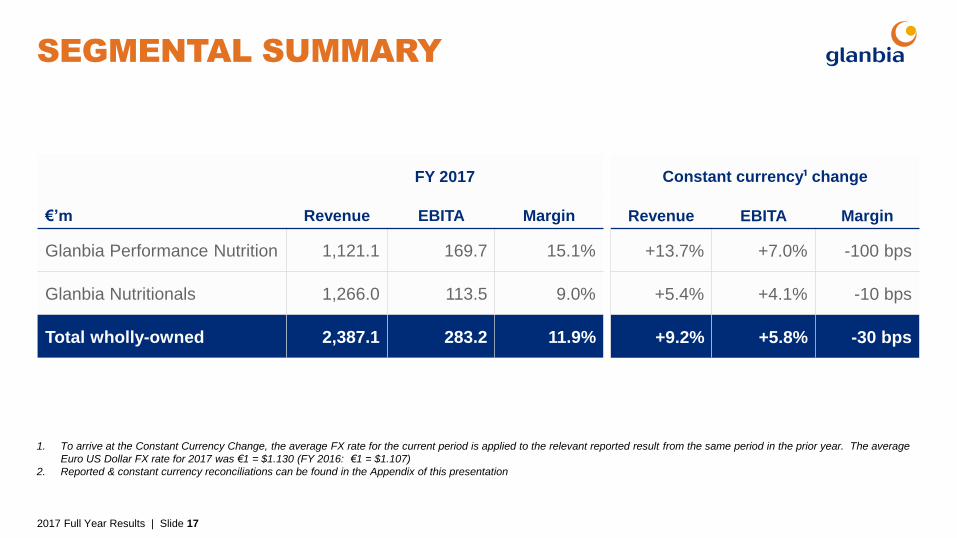

SEGMENTAL SUMMARY

2017 Full Year Results | Slide 17

FY 2017

€’m Revenue EBITA Margin

Glanbia Performance Nutrition 1,121.1 169.7 15.1%

Glanbia Nutritionals 1,266.0 113.5 9.0%

Total wholly-owned 2,387.1 283.2 11.9%

Constant currency¹ change

Revenue EBITA Margin

+13.7% +7.0% -100 bps

+5.4% +4.1% -10 bps

+9.2% +5.8% -30 bps

1. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the same period in the prior year. The average

Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

2. Reported & constant currency reconciliations can be found in the Appendix of this presentation

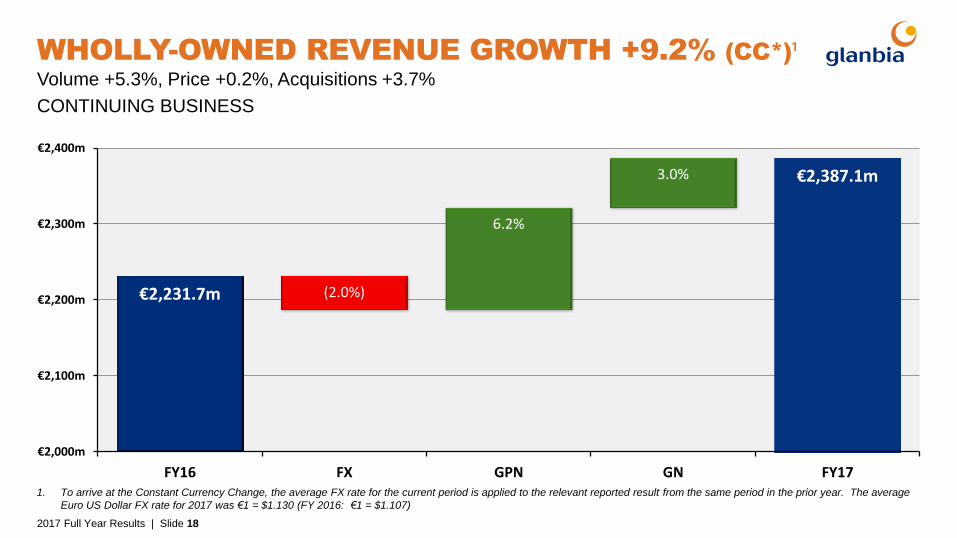

WHOLLY-OWNED REVENUE GROWTH +9.2% (CC*)¹

2017 Full Year Results | Slide 18

Volume +5.3%, Price +0.2%, Acquisitions +3.7%

CONTINUING BUSINESS

€2,231.7m (2.0%)

6.2%

3.0% €2,387.1m

€2,000m

€2,100m

€2,200m

€2,300m

€2,400m

FY16 FX GPN GN FY171. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the same period in the prior year. The average

Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

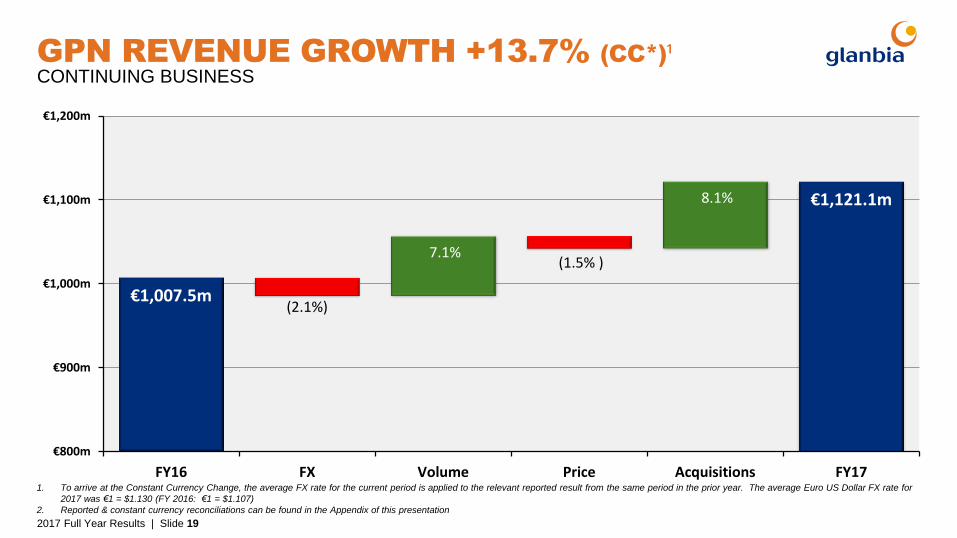

GPN REVENUE GROWTH +13.7% (CC*)¹

2017 Full Year Results | Slide 19

CONTINUING BUSINESS

€1,007.5m

7.1%

8.1%

(2.1%)

(1.5% )

€1,121.1m

€800m

€900m

€1,000m

€1,100m

€1,200m

FY16 FX Volume Price Acquisitions FY171. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the same period in the prior year. The average Euro US Dollar FX rate for

2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

2. Reported & constant currency reconciliations can be found in the Appendix of this presentation

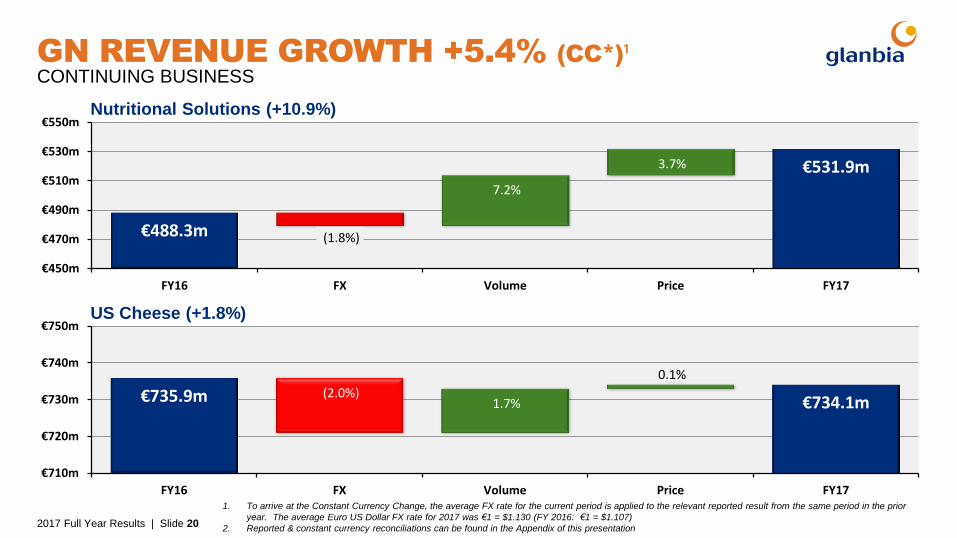

GN REVENUE GROWTH +5.4% (CC*)¹

2017 Full Year Results | Slide 20

CONTINUING BUSINESS

€488.3m

7.2%

3.7%

(1.8%)

€531.9m

€450m

€470m

€490m

€510m

€530m

€550m

FY16 FX Volume Price FY17

€735.9m 1.7%

0.1%

(2.0%) €734.1m

€710m

€720m

€730m

€740m

€750m

FY16 FX Volume Price FY17

Nutritional Solutions (+10.9%)

US Cheese (+1.8%)

1. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the same period in the prior

year. The average Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

2. Reported & constant currency reconciliations can be found in the Appendix of this presentation

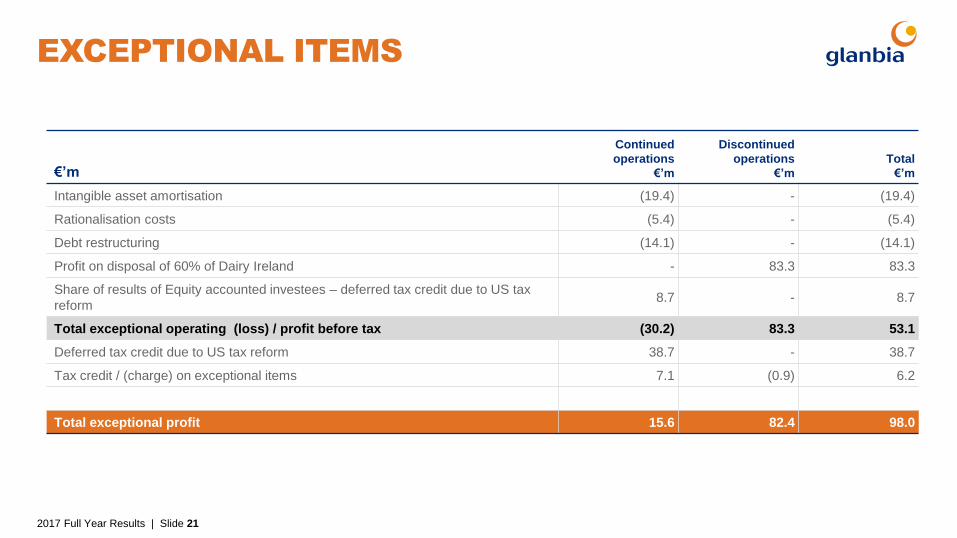

EXCEPTIONAL ITEMS

2017 Full Year Results | Slide 21

€’m

Continued

operations

€’m

Discontinued

operations

€’m

Total

€’m

Intangible asset amortisation (19.4) - (19.4)

Rationalisation costs (5.4) - (5.4)

Debt restructuring (14.1) - (14.1)

Profit on disposal of 60% of Dairy Ireland - 83.3 83.3

Share of results of Equity accounted investees – deferred tax credit due to US tax

reform 8.7 - 8.7

Total exceptional operating (loss) / profit before tax (30.2) 83.3 53.1

Deferred tax credit due to US tax reform 38.7 - 38.7

Tax credit / (charge) on exceptional items 7.1 (0.9) 6.2

Total exceptional profit 15.6 82.4 98.0

CASH FLOW FROM CONTINUING OPERATIONS

2017 Full Year Results | Slide 22

€328m

€16m

€123m

€20m €58m

€6m

€185m

€137m

€0m

€100m

€200m

€300m

€400m

2017 EBITDA Working Capital BusinessSustaining

Capex

2017 OperatingCash Flow

Net Interest &Tax

Dividends fromJV&A's

Other FCF 2017

• The pro-forma movement in working capital was (€123m), primarily due to an increase of receivables of (€76m) due to the

increased sales activity in Q4

• On a pro-forma basis operating cash flow conversion of EBITDA for 2017 was 56.4% compared to 101.5% in 2016

• The target for 2018 is 80% operating cash flow conversion

INVESTMENT & RETURNS

2017 Full Year Results | Slide 23

• Major projects were the new

GPN R&D Innovation Centre,

plant improvements and IT

systems upgrades

• Amazing Grass and Body &

Fit acquired in 2017 and

thinkThin in 2015

• 2018 Capital Expenditure

expected to be €75 to

€85 million

• Return on Capital Employed

– “ROCE” 13.4% (2016: 13.9%*)

ROCE 2017: 13.4% ROCE 2016: 13.9% ROCE 2015: 14.8%

Sustaining Capex Strategic Capex Acquisitions Total Investment

*Restated to include deferred tax

€24m €32m €37m

€49m €57m

€86m

€168m

€15m

€190m

2017 2016 2015

€241m

€104m

€313m

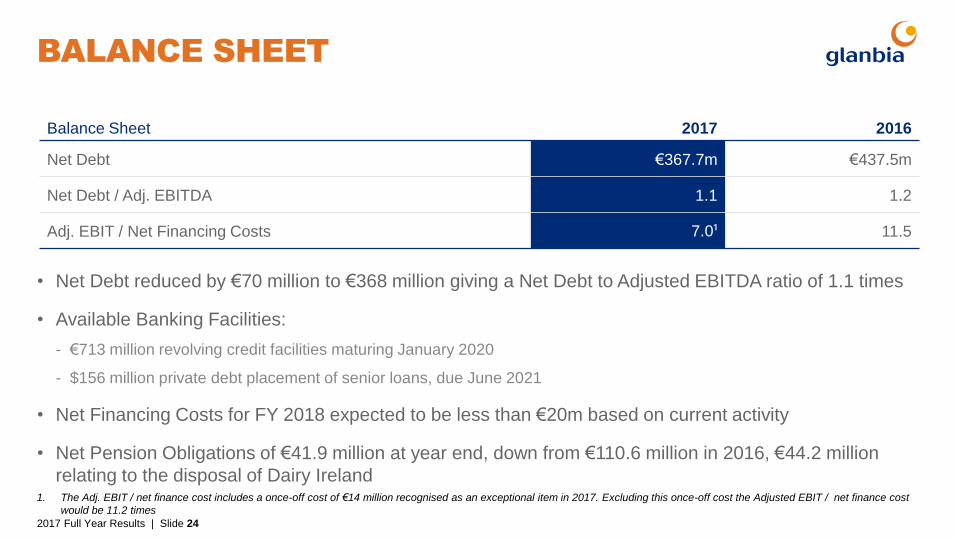

BALANCE SHEET

• Net Debt reduced by €70 million to €368 million giving a Net Debt to Adjusted EBITDA ratio of 1.1 times

• Available Banking Facilities:

- €713 million revolving credit facilities maturing January 2020

- $156 million private debt placement of senior loans, due June 2021

• Net Financing Costs for FY 2018 expected to be less than €20m based on current activity

• Net Pension Obligations of €41.9 million at year end, down from €110.6 million in 2016, €44.2 million

relating to the disposal of Dairy Ireland

2017 Full Year Results | Slide 24

Balance Sheet 2017 2016

Net Debt €367.7m €437.5m

Net Debt / Adj. EBITDA 1.1 1.2

Adj. EBIT / Net Financing Costs 7.0¹ 11.5

1. The Adj. EBIT / net finance cost includes a once-off cost of €14 million recognised as an exceptional item in 2017. Excluding this once-off cost the Adjusted EBIT / net finance cost

would be 11.2 times

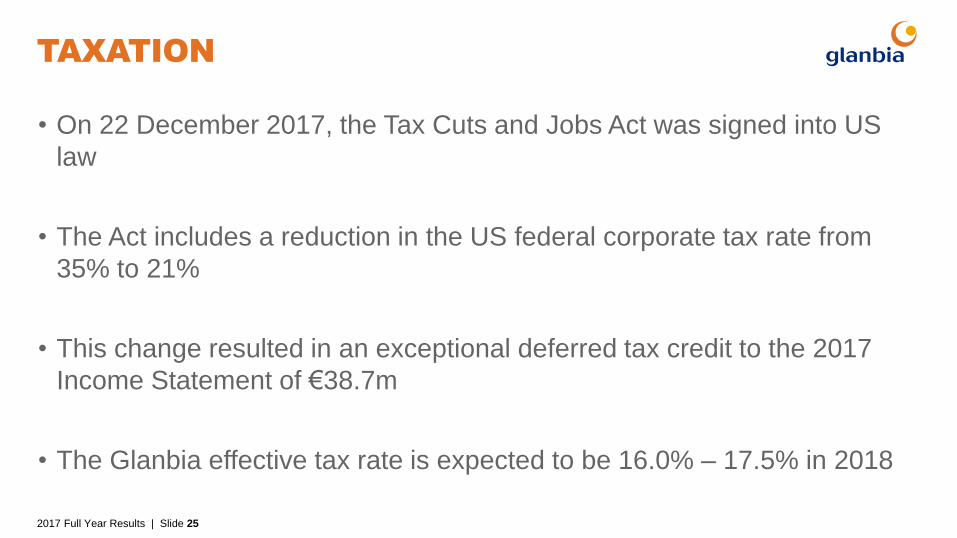

TAXATION

• On 22 December 2017, the Tax Cuts and Jobs Act was signed into US

law

• The Act includes a reduction in the US federal corporate tax rate from

35% to 21%

• This change resulted in an exceptional deferred tax credit to the 2017

Income Statement of €38.7m

• The Glanbia effective tax rate is expected to be 16.0% – 17.5% in 2018

2017 Full Year Results | Slide 25

DIVIDEND UPDATE

2017 Full Year Results | Slide 26

Completed review of dividend policy

Progressive dividend policy with target payout ratio 25% to 35%

2017 dividend payout will be 22c / share, an increase of 65% on 2016,

representing a payout of 25%

Strategy

&

Outlook

2017 Full Year Results Presentation

GLANBIA STRATEGY DRIVERS

2017 Full Year Results | Slide 28

Our Purpose: To deliver better nutrition for every step of life’s journey

Our Vision: To be one of world’s top performing nutrition companies trusted to enrich lives everyday

Trends driving our business

Health and

wellness

On-the-go food

& beverage

Digitally

connected

Clean

labelling

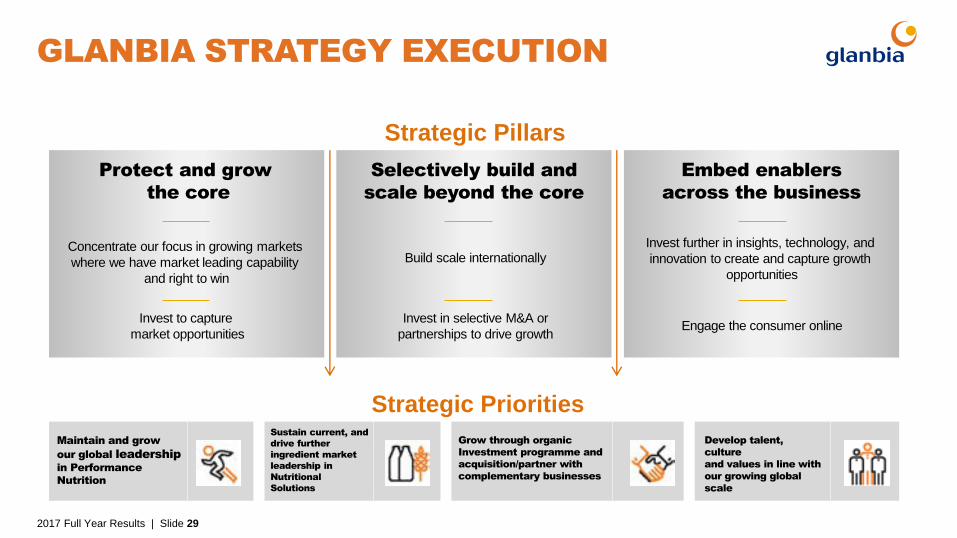

GLANBIA STRATEGY EXECUTION

2017 Full Year Results | Slide 29

Strategic Priorities

Maintain and grow

our global leadership

in Performance

Nutrition

Sustain current, and

drive further

ingredient market

leadership in

Nutritional

Solutions

Grow through organic

Investment programme and

acquisition/partner with

complementary businesses

Develop talent,

culture

and values in line with

our growing global

scale

Protect and grow

the core

Selectively build and

scale beyond the core

Embed enablers

across the business

Concentrate our focus in growing markets

where we have market leading capability

and right to win

Invest to capture

market opportunities

Build scale internationally

Invest in selective M&A or

partnerships to drive growth

Invest further in insights, technology, and

innovation to create and capture growth

opportunities

Engage the consumer online

Strategic Pillars

2018 OUTLOOK

2017 Full Year Results | Slide 30

• Positive outlook for FY 2018

• Growth will be driven by wholly-owned

business offsetting declines in JVs

• Mid-to-high single-digit like-for-like volume

growth expected across both the branded

portfolio of GPN & Nutritional Solutions

• GPN & GN margins expected to be in-line with

2017

• Pro-forma¹ adjusted EPS is expected to grow

by 5% – 8% constant currency²

1. Pro-forma Adjusted Earnings Per Share for the continuing Group calculation assumes the Dairy Ireland segment and related assets were

disposed of at the beginning of the 2016 financial year. A reconciliation of the pro-forma and reported adjusted earnings per share can be found in

the appendix of this presentation

2. To arrive at the Constant Currency Change, the average FX rate for the current period is applied to the relevant reported result from the same

period in the prior year. The average Euro US Dollar FX rate for 2017 was €1 = $1.130 (FY 2016: €1 = $1.107)

3. If the EUR/USD FX rate remains at approximately $1.24, we expect a pro-forma adjusted EPS headwind of c.8%

To register your interest please email: [email protected]

GLANBIA CAPITAL MARKETS DAY 2018

2017 Full Year Results | Slide 31

Date: 23 May 2018

Location: Chicago, USA

Focus: Glanbia Group with Site Tour

2017 Full Year Results | Slide 32

Appendix 2017 Full Year Results Presentation

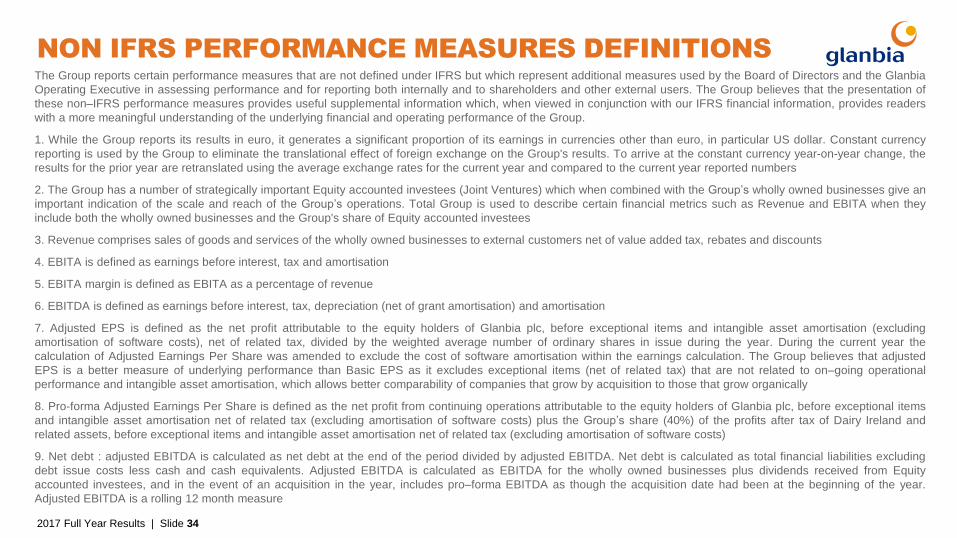

NON IFRS PERFORMANCE MEASURES DEFINITIONS

The Group reports certain performance measures that are not defined under IFRS but which represent additional measures used by the Board of Directors and the Glanbia

Operating Executive in assessing performance and for reporting both internally and to shareholders and other external users. The Group believes that the presentation of

these non–IFRS performance measures provides useful supplemental information which, when viewed in conjunction with our IFRS financial information, provides readers

with a more meaningful understanding of the underlying financial and operating performance of the Group.

1. While the Group reports its results in euro, it generates a significant proportion of its earnings in currencies other than euro, in particular US dollar. Constant currency

reporting is used by the Group to eliminate the translational effect of foreign exchange on the Group's results. To arrive at the constant currency year-on-year change, the

results for the prior year are retranslated using the average exchange rates for the current year and compared to the current year reported numbers

2. The Group has a number of strategically important Equity accounted investees (Joint Ventures) which when combined with the Group’s wholly owned businesses give an

important indication of the scale and reach of the Group’s operations. Total Group is used to describe certain financial metrics such as Revenue and EBITA when they

include both the wholly owned businesses and the Group's share of Equity accounted investees

3. Revenue comprises sales of goods and services of the wholly owned businesses to external customers net of value added tax, rebates and discounts

4. EBITA is defined as earnings before interest, tax and amortisation

5. EBITA margin is defined as EBITA as a percentage of revenue

6. EBITDA is defined as earnings before interest, tax, depreciation (net of grant amortisation) and amortisation

7. Adjusted EPS is defined as the net profit attributable to the equity holders of Glanbia plc, before exceptional items and intangible asset amortisation (excluding

amortisation of software costs), net of related tax, divided by the weighted average number of ordinary shares in issue during the year. During the current year the

calculation of Adjusted Earnings Per Share was amended to exclude the cost of software amortisation within the earnings calculation. The Group believes that adjusted

EPS is a better measure of underlying performance than Basic EPS as it excludes exceptional items (net of related tax) that are not related to on–going operational

performance and intangible asset amortisation, which allows better comparability of companies that grow by acquisition to those that grow organically

8. Pro-forma Adjusted Earnings Per Share is defined as the net profit from continuing operations attributable to the equity holders of Glanbia plc, before exceptional items

and intangible asset amortisation net of related tax (excluding amortisation of software costs) plus the Group’s share (40%) of the profits after tax of Dairy Ireland and

related assets, before exceptional items and intangible asset amortisation net of related tax (excluding amortisation of software costs)

9. Net debt : adjusted EBITDA is calculated as net debt at the end of the period divided by adjusted EBITDA. Net debt is calculated as total financial liabilities excluding

debt issue costs less cash and cash equivalents. Adjusted EBITDA is calculated as EBITDA for the wholly owned businesses plus dividends received from Equity

accounted investees, and in the event of an acquisition in the year, includes pro–forma EBITDA as though the acquisition date had been at the beginning of the year.

Adjusted EBITDA is a rolling 12 month measure

2017 Full Year Results | Slide 34

NON IFRS PERFORMANCE MEASURES DEFINITIONS

10. Adjusted EBIT: net finance cost is calculated as earnings before interest and tax plus dividends received from Equity accounted investees divided by net finance

cost. Net finance cost comprises finance costs less finance income per the Group income statement plus capitalised borrowing costs

11. The Group has adopted an income statement format that seeks to highlight significant items within the Group results for the year. Such items may include

restructuring, impairment of assets, adjustments to contingent consideration, material acquisition integration costs, restructuring costs, profit or loss on disposal or

termination of operations, material acquisition costs, litigation settlements, legislative changes, gains or losses on defined benefit pension plan restructuring and profit

or loss on disposal of investments. Judgement is used by the Group in assessing the particular items which by virtue of their scale and nature should be disclosed in

the income statement and notes as exceptional items

12. Volume increase/(decrease) represents the impact of sales volumes within the revenue movement year on year, excluding volume from acquisitions, on a constant

currency basis. Pricing increase/(decrease) represents the impact of sales pricing within the revenue movement year on year, excluding acquisitions, on a constant

currency basis

13. Like-for-like branded revenue growth represents the sales growth / (decline) year on year on branded sales, excluding acquisitions, on a constant currency basis

14. The effective tax rate is defined as the pre-exceptional income tax charge divided by the profit before tax less share of results of Equity accounted investees

15. The Group defines business sustaining capital expenditure as the expenditure required to maintain/replace existing assets with a high proportion of expired useful

life. This expenditure does not attract new customers or create the capacity for a bigger business. It enables the Group to keep running at current throughput rates but

also keep pace with regulatory and environmental changes as well as complying with new requirements from existing customers

16. The Group defines strategic capital expenditure as the expenditure required to facilitate growth and generate additional returns for the Group. This is generally

expansionary expenditure beyond what is necessary to maintain the Group’s current competitive position

17. Operating cash flow is defined as pre–exceptional EBITDA of the wholly owned businesses net of business sustaining capital expenditure and working capital

movements, excluding exceptional cash flows. ROCE is defined as the Group's earnings before interest, and amortisation (net of related tax) plus the Group's share of

the results of Equity accounted investees after interest and tax divided by capital employed. Capital employed comprises the sum of the Group's total assets plus

cumulative intangible asset amortisation less current liabilities less deferred tax liabilities excluding all financial liabilities, retirement benefit assets and cash. It is

calculated by taking the average of the relevant opening and closing balance sheet amounts. In years where the Group makes significant acquisitions or disposals, the

ROCE calculation is adjusted appropriately, to ensure the acquisition or disposal are equally time apportioned in the numerator and the denominator

18. Dividend pay-out ratio is defined as the annual dividend per ordinary share divided by the pro-forma Adjusted Earnings Per Share. The dividend pay–out ratio

provides an indication of the value returned to shareholders relative to the Group's total earnings

2017 Full Year Results | Slide 35

ADJUSTED EPS - REPORTED

2017 Full Year Results | Slide 36

Adjusted Earnings Per Share

Year

2017

€’m

Constant

currency

2016

€’m

Year

2016

€’m

Profit attributable to the equity holders of the company 329.4 208.6 211.8

Amortisation 31.7 26.7 27.3

Exceptional items (net of tax) (98.0) 14.5 14.8

Adjusted net income 263.1 249.8 253.9

Weighted average number of ordinary shares in issue 295,010.5 295,130.8 295,130.8

Adjusted Earnings Per Share (cent) 89.17 84.66 86.02

Constant currency growth +5.3%

PRO-FORMA ADJUSTED EPS

2017 Full Year Results | Slide 37

Pro-forma Adjusted Earnings Per Share

Pro-forma

2017

€’m

Constant

currency

Pro-forma

2016

€’m

Pro-forma

2016

€’m

Adjusted net income 263.1 249.8 253.9

Discontinued operations adjusted net income (100%) (10.1) (27.6) (27.6)

40% of Discontinued operations adjusted net income 4.0 11.1 11.1

Adjusted net income (pro-forma) 257.0 233.3 237.4

Weighted average number of ordinary shares in issue 295,010.5 295,130.8 295,130.8

Adjusted Earnings Per Share (cent) pro-forma 87.11 79.05 80.40

Constant currency growth +10.2%

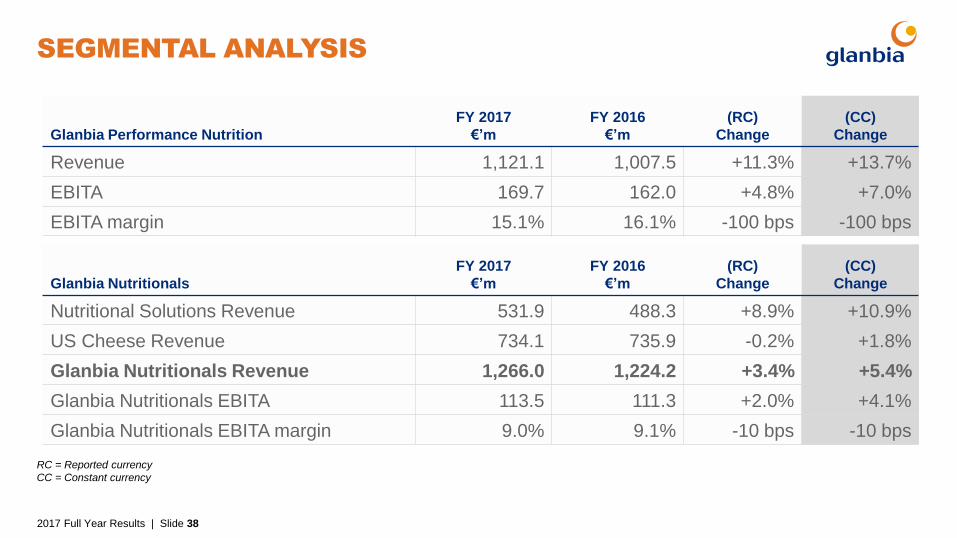

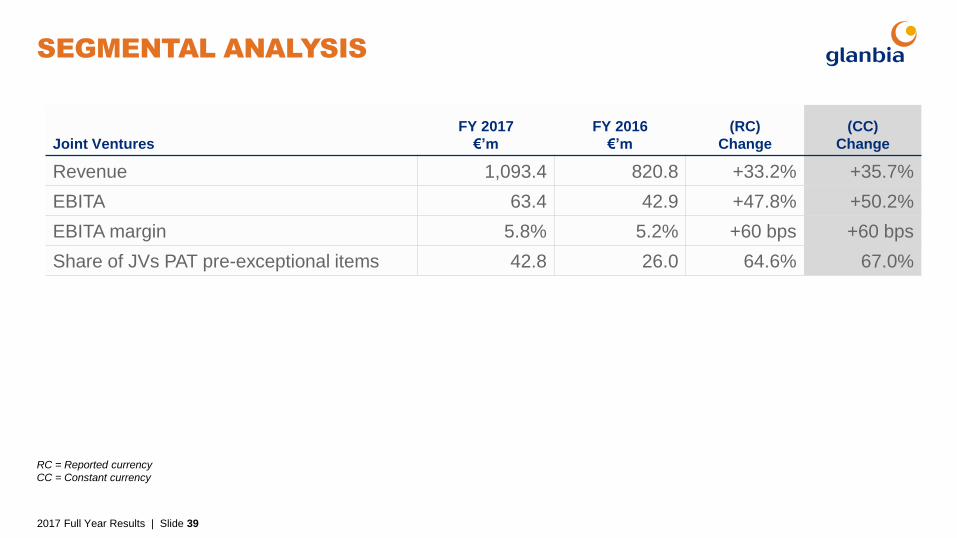

SEGMENTAL ANALYSIS

2017 Full Year Results | Slide 38

Glanbia Performance Nutrition

FY 2017

€’m

FY 2016

€’m

(RC)

Change

(CC)

Change

Revenue 1,121.1 1,007.5 +11.3% +13.7%

EBITA 169.7 162.0 +4.8% +7.0%

EBITA margin 15.1% 16.1% -100 bps -100 bps

Glanbia Nutritionals

FY 2017

€’m

FY 2016

€’m

(RC)

Change

(CC)

Change

Nutritional Solutions Revenue 531.9 488.3 +8.9% +10.9%

US Cheese Revenue 734.1 735.9 -0.2% +1.8%

Glanbia Nutritionals Revenue 1,266.0 1,224.2 +3.4% +5.4%

Glanbia Nutritionals EBITA 113.5 111.3 +2.0% +4.1%

Glanbia Nutritionals EBITA margin 9.0% 9.1% -10 bps -10 bps

RC = Reported currency

CC = Constant currency

SEGMENTAL ANALYSIS

2017 Full Year Results | Slide 39

Joint Ventures

FY 2017

€’m

FY 2016

€’m

(RC)

Change

(CC)

Change

Revenue 1,093.4 820.8 +33.2% +35.7%

EBITA 63.4 42.9 +47.8% +50.2%

EBITA margin 5.8% 5.2% +60 bps +60 bps

Share of JVs PAT pre-exceptional items 42.8 26.0 64.6% 67.0%

RC = Reported currency

CC = Constant currency

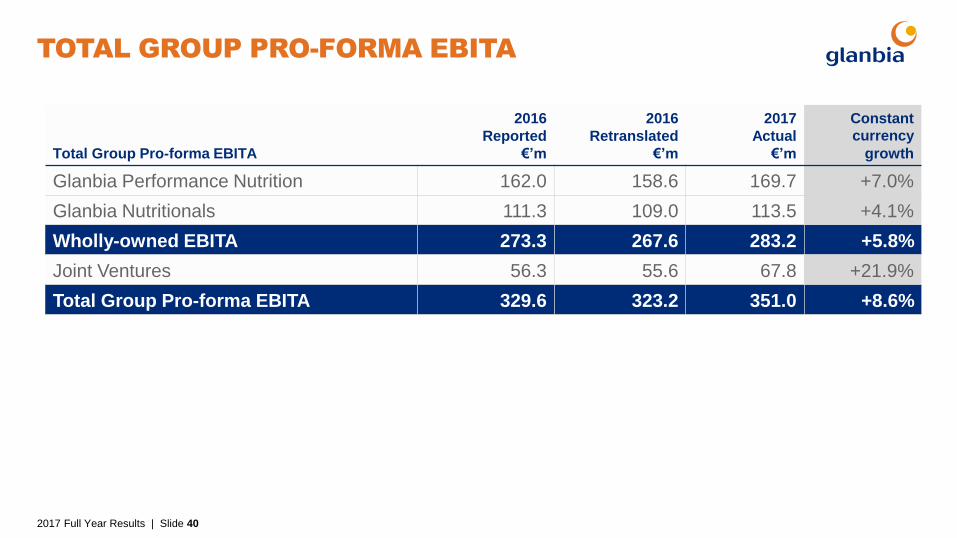

TOTAL GROUP PRO-FORMA EBITA

2017 Full Year Results | Slide 40

Total Group Pro-forma EBITA

2016

Reported

€’m

2016

Retranslated

€’m

2017

Actual

€’m

Constant

currency

growth

Glanbia Performance Nutrition 162.0 158.6 169.7 +7.0%

Glanbia Nutritionals 111.3 109.0 113.5 +4.1%

Wholly-owned EBITA 273.3 267.6 283.2 +5.8%

Joint Ventures 56.3 55.6 67.8 +21.9%

Total Group Pro-forma EBITA 329.6 323.2 351.0 +8.6%