2017 annual report - bca.cv4f61db7d-e068-490e-aa1e-ab8612e425a6}.pdf · francisco pinto machado...

TRANSCRIPT

2017 Annual Report

4

Contents

1. GOVERNING BODIES ....................................................................................................................... 5

2. DEPARTMENTS AND BRANCH OFFICE NETWORK .......................................................................... 6

3. SHARE CAPITAL ............................................................................................................................... 9

6. INTERNATIONAL AND NATIONAL ENVIRONMENT ....................................................................... 12

6.1. INTERNATIONAL .................................................................................................................... 12

6.2. NATIONAL .............................................................................................................................. 15

6.2.1. General Information ................................................................................................... 15

6.2.2. Financial System ......................................................................................................... 17

6.2.3. BCA in the System ....................................................................................................... 19

7. STRATEGIC VISION ........................................................................................................................ 21

8. COMMERCIAL ACTIVITY ................................................................................................................ 23

8.1. FUNDS ................................................................................................................................... 23

8.2. LOAN ...................................................................................................................................... 25

8.2.1. Constraints on lending activity ................................................................................... 25

8.2.2. Analysis of Granted Loans .......................................................................................... 25

9. OTHER ACTIVITIES ........................................................................................................................ 28

9.1. HUMAN RESOURCES ............................................................................................................. 28

9.2. RISK MANAGEMENT, INTERNAL AUDIT AND CONTROL ........................................................ 32

9.3. MARKETING AND PUBLIC RELATIONS ................................................................................... 36

9.4. OTHER SUPPORTING ACTIVITIES ........................................................................................... 40

10. ANALYSIS OF ECONOMIC-FINANCIAL SITUATION ...................................................................... 42

10.1. BALANCE SHEET ................................................................................................................... 42

10.2. INCOME STATEMENT .......................................................................................................... 46

10.3. ANALYSIS OF THE RATIOS .................................................................................................... 48

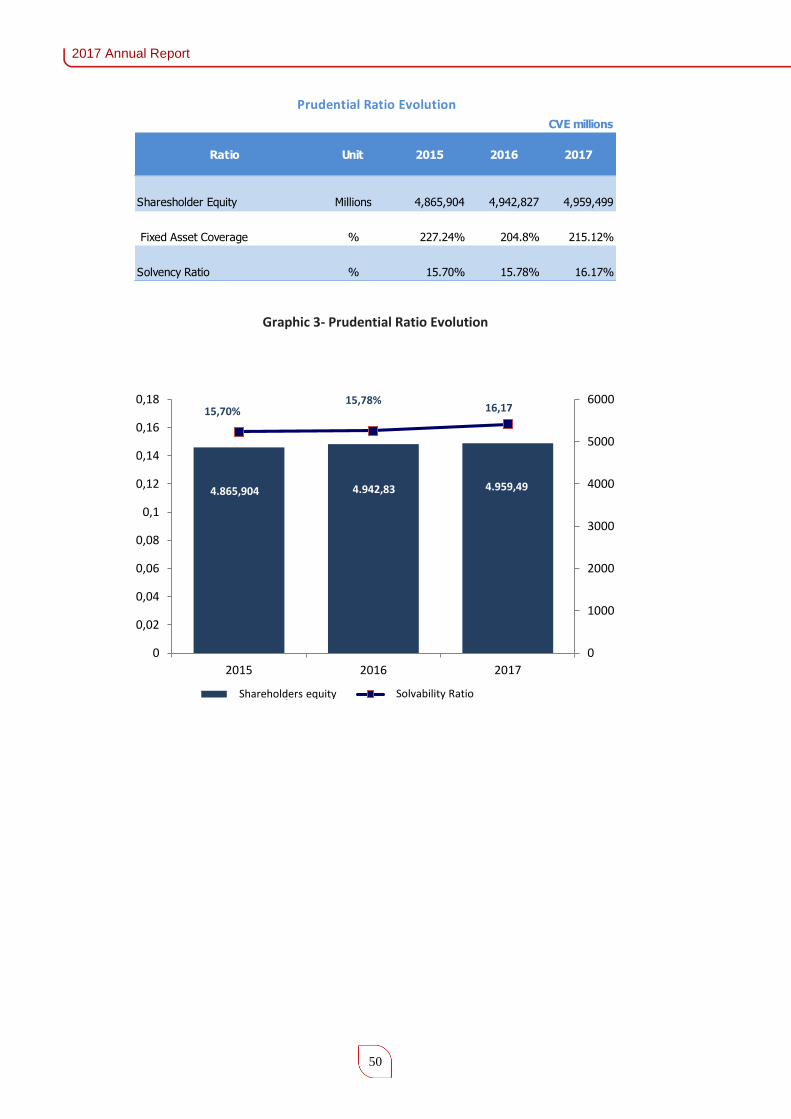

10.4. PRUDENTIAL RATIOS ........................................................................................................... 49

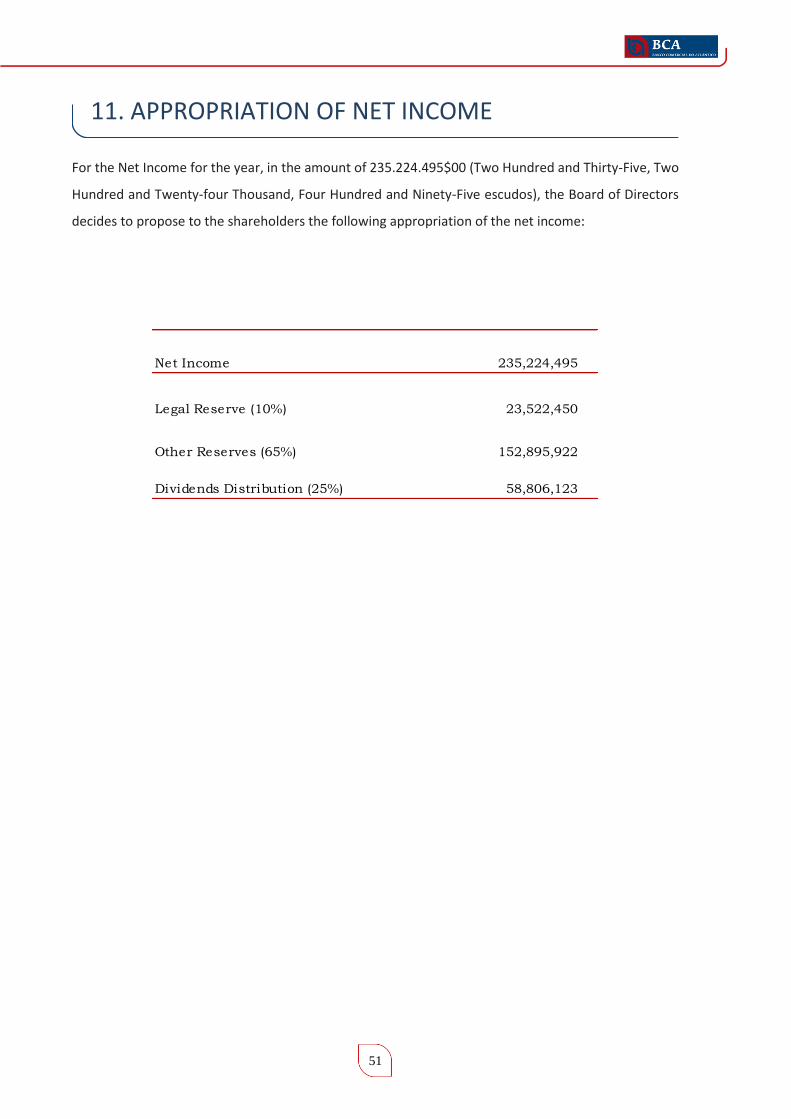

11. APPROPRIATION OF NET INCOME .............................................................................................. 51

12. CORRESPONDENT BANKS ........................................................................................................... 52

13. NOTES ......................................................................................................................................... 54

5

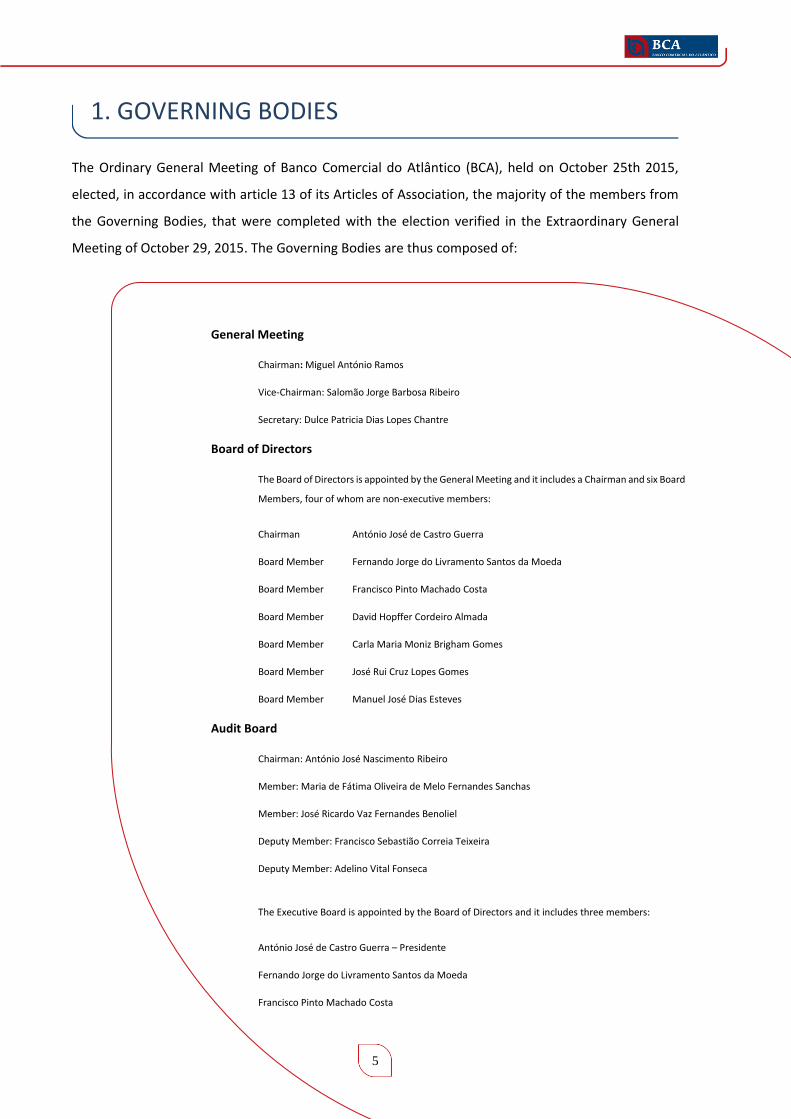

1. GOVERNING BODIES

The Ordinary General Meeting of Banco Comercial do Atlântico (BCA), held on October 25th 2015,

elected, in accordance with article 13 of its Articles of Association, the majority of the members from

the Governing Bodies, that were completed with the election verified in the Extraordinary General

Meeting of October 29, 2015. The Governing Bodies are thus composed of:

General Meeting

Chairman: Miguel António Ramos

Vice-Chairman: Salomão Jorge Barbosa Ribeiro

Secretary: Dulce Patricia Dias Lopes Chantre

Board of Directors

The Board of Directors is appointed by the General Meeting and it includes a Chairman and six Board

Members, four of whom are non-executive members:

Chairman António José de Castro Guerra

Board Member Fernando Jorge do Livramento Santos da Moeda

Board Member Francisco Pinto Machado Costa

Board Member David Hopffer Cordeiro Almada

Board Member Carla Maria Moniz Brigham Gomes

Board Member José Rui Cruz Lopes Gomes

Board Member Manuel José Dias Esteves

Audit Board

Chairman: António José Nascimento Ribeiro

Member: Maria de Fátima Oliveira de Melo Fernandes Sanchas

Member: José Ricardo Vaz Fernandes Benoliel

Deputy Member: Francisco Sebastião Correia Teixeira

Deputy Member: Adelino Vital Fonseca

The Executive Board is appointed by the Board of Directors and it includes three members:

António José de Castro Guerra – Presidente

Fernando Jorge do Livramento Santos da Moeda

Francisco Pinto Machado Costa

2017 Annual Report

6

2. DEPARTMENTS AND BRANCH OFFICE NETWORK

Northern Commercial Department – DCN Gilda Monteiro Director

Southern Commercial Department - DCS Herminalda Rodrigues Director

Financial and International Department – DFI Amélia Figueiredo Director

Risk Management Department -DGR Filomena Figueiredo Director

Means and Channels Department – DMC Américo Andrade Director

Organization and Innovation Department - DOI Águeda Monteiro Director

IT Systems Department – DSI Luís Barbosa Director

Security and Logistics Department – DSL Adalberto Melo Director

Operational Support Department - DSO Anibal Moreira Director

Credit Recovery Office - GRE Nuno Cabral Coordinator

Human Resources Department – GRH Niva Barbosa – Head of Division Jacqueline Cruz – Head of Division

Internal Audit Department – DAI

Emanuel Miranda Diretor

Legal and Pre-Legal Office - GJC Dulce Lopes Coordinator

Compliance Supporting Office – GFC

Monica Sanches Coordinator

Marketing and Public Relations Office – GMR Paula Martins

Coordinator

Research and Studies Office Evaldo Lima Coordinator

7

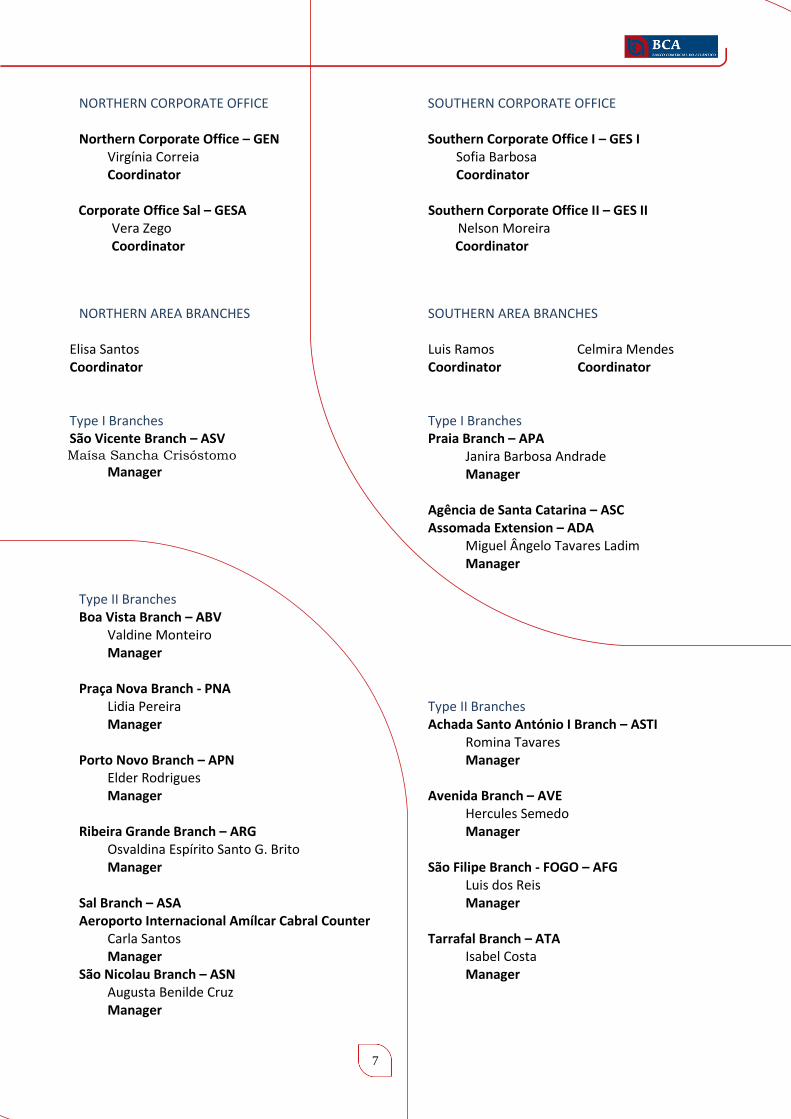

NORTHERN CORPORATE OFFICE Northern Corporate Office – GEN

Virgínia Correia Coordinator

SOUTHERN CORPORATE OFFICE Southern Corporate Office I – GES I

Sofia Barbosa Coordinator

Corporate Office Sal – GESA Southern Corporate Office II – GES II

Vera Zego Nelson Moreira Coordinator Coordinator

NORTHERN AREA BRANCHES

Elisa Santos Coordinator

SOUTHERN AREA BRANCHES

Luis Ramos Celmira Mendes Coordinator Coordinator

Type I Branches São Vicente Branch – ASV Maísa Sancha Crisóstomo

Manager

Type I Branches Praia Branch – APA

Janira Barbosa Andrade Manager

Agência de Santa Catarina – ASC Assomada Extension – ADA

Miguel Ângelo Tavares Ladim Manager

Type II Branches Boa Vista Branch – ABV

Valdine Monteiro Manager

Praça Nova Branch - PNA

Lidia Pereira Manager

Porto Novo Branch – APN

Elder Rodrigues Manager

Ribeira Grande Branch – ARG

Osvaldina Espírito Santo G. Brito Manager

Sal Branch – ASA Aeroporto Internacional Amílcar Cabral Counter

Carla Santos Manager

São Nicolau Branch – ASN Augusta Benilde Cruz Manager

Type II Branches Achada Santo António I Branch – ASTI

Romina Tavares Manager

Avenida Branch – AVE

Hercules Semedo Manager

São Filipe Branch - FOGO – AFG

Luis dos Reis Manager

Tarrafal Branch – ATA

Isabel Costa Manager

2017 Annual Report

8

Type III Branches Fonte Filipe Branch – AFF

António Evora Manager

Ponta do Sol Branch – APS Paúl Counter – APL (Ext. ARG)

Osvaldina Espirito Santo G. Brito Manager

Santa Maria Branch – ASM

Elizabeth Alexandre Manager

Tarrafal de São Nicolau Branch – ATS Manuel Freitas Manager

Type III Branches Achada Santo António II Branch – ASTII

Dulce Santos Manager

Achada S. Filipe Branch - ASF São Domingos Branch - PSD

Maria Borges Manager

Assomada Branch – ADA Cláudio Filipe Barros Mendonça

Manager Brava Branch – ABR

Ângela Rosa Manager

Chã de Areia Branch – ACA

Neusa Melo Manager

Maio Branch – AMA

Alexandrino Anes Manager

Mosteiros Branch – AMO

Luis dos Reis Manager

Palmarejo Grande Branch – APG

Joaquina Lopes Tavares Manager

Santa Cruz Branch – STC

José Moniz Manager

9

3. SHARE CAPITAL

BCA has a Share Capital of 1,324,765,000 CVE (one billion, three hundred and twenty-four million,

seven hundred and sixty-five thousand Cabo Verdean escudos) held, as of December 31st 2017, by the

shareholders set out in the following table, which shows that the equity stakes of Caixa Geral de

Depósitos, SA/ Banco InterAtlântico, SA, INPS – Instituto Nacional de Previdência Social, Garantia –

Companhia de Seguros de Cabo-Verde, SA and Caixa Geral de Depósitos were qualified:

CVE

Shareholders Amount Percentage

CGD/INTERATLÂNTICO 697,446,000 52.65%

INPS 166,078,000 12.54%

CAIXA GERAL DE DEPOSITOS 89,504,000 6.76%

GARANTIA 76,322,000 5.76%

ASA - AEROPORTO E SEGURANÇA AÉREA, SA 28,780,000 2.17%

Employees 27,418,000 2.07%

Others Shareholders 239,217,000 18.05%

TOTAL 1,324,765,000 100.00%

Table 1-Share Capital 31/12/2017

2017 Annual Report

10

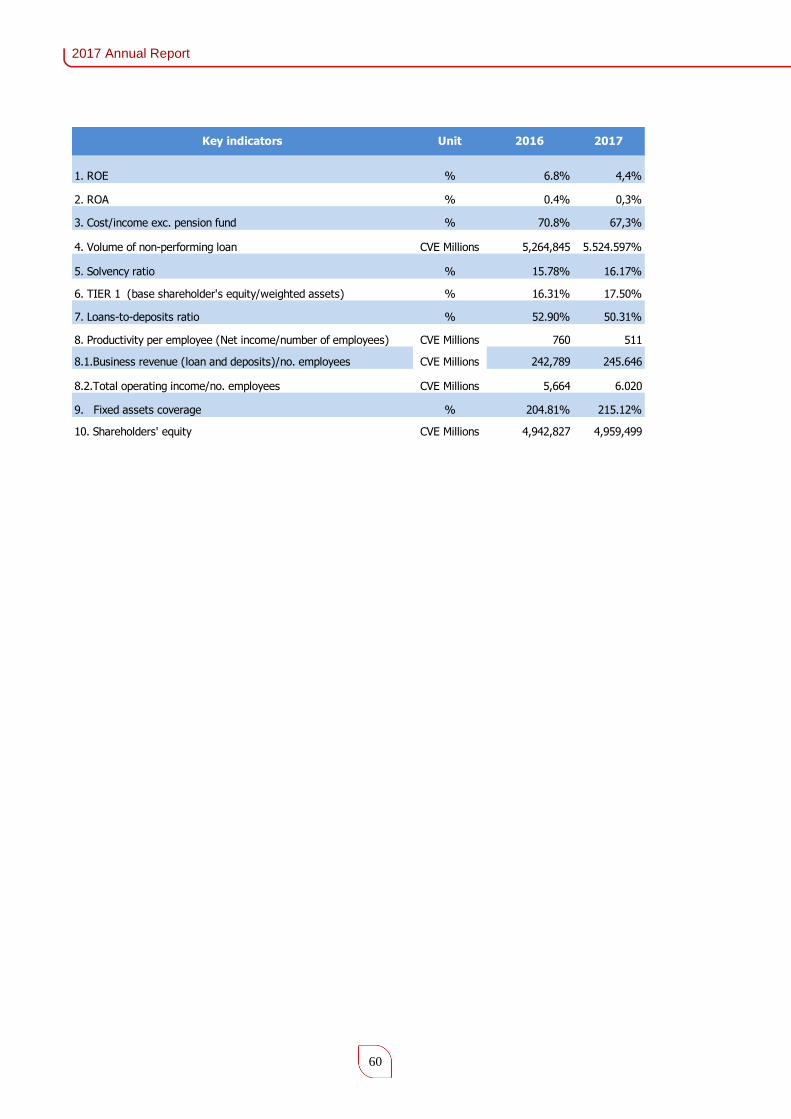

4. KEY INDICATORS

Variables Unit 2016 2017 Change

BALANCE

Total asset CVE Millions 84,520 89,106 5,4%

Total net asset CVE Millions 45,687 46,181 1.1%

Total liabilities CVE Millions 79,241 83,663 5,6%

Customers' loan CVE Millions 72,703 75,703 4,3%

Net worth CVE Millions 5,278 5.442 3,1%

Operating Account

Net Interest Income CVE Millions 1,978 2,027 2.5%

+ Non-Interest Income CVE Millions 588 742 26.2%

=Operating Income CVE Millions 2,566 2,769 7.9%

-Administratives Costs CVE Millions 1,887 1,926 2.1%

=Cash-Flow Exposure CVE Millions 679 843 24.2%

+ Income from subsidiaries exc. from cons. Assoc. CVE Millions 45 47 3.5%

-Depreciation for period CVE Millions 208 208 0.0%

-Impairment/ Net Provisions for period CVE Millions 98 390 298.0%

-Tax exc./Profits CVE Millions 74 57 -23.0%

= Net Income for period CVE Millions 344 235 -31.7%

RATIO

Overdue Credit/Customers loan % 13.8% 14.6%

Overdue Credit up to + 90 days/Customers loan % 13.2% 13.4%

Credit Impairment /Overdue Credit % 71.5% 75.2%

Credit Impairment and liabilities/Overdue Credit % 72.5% 74.5%

Customers loan/Customers Deposits % 52.9% 50.3%

Net Income/Own Capital (ROE) % 6.8% 4.4%

Net Income/Asset (ROA) % 0.4% 0.3%

Solvency Ratio % 15.78% 16.17%

Operating

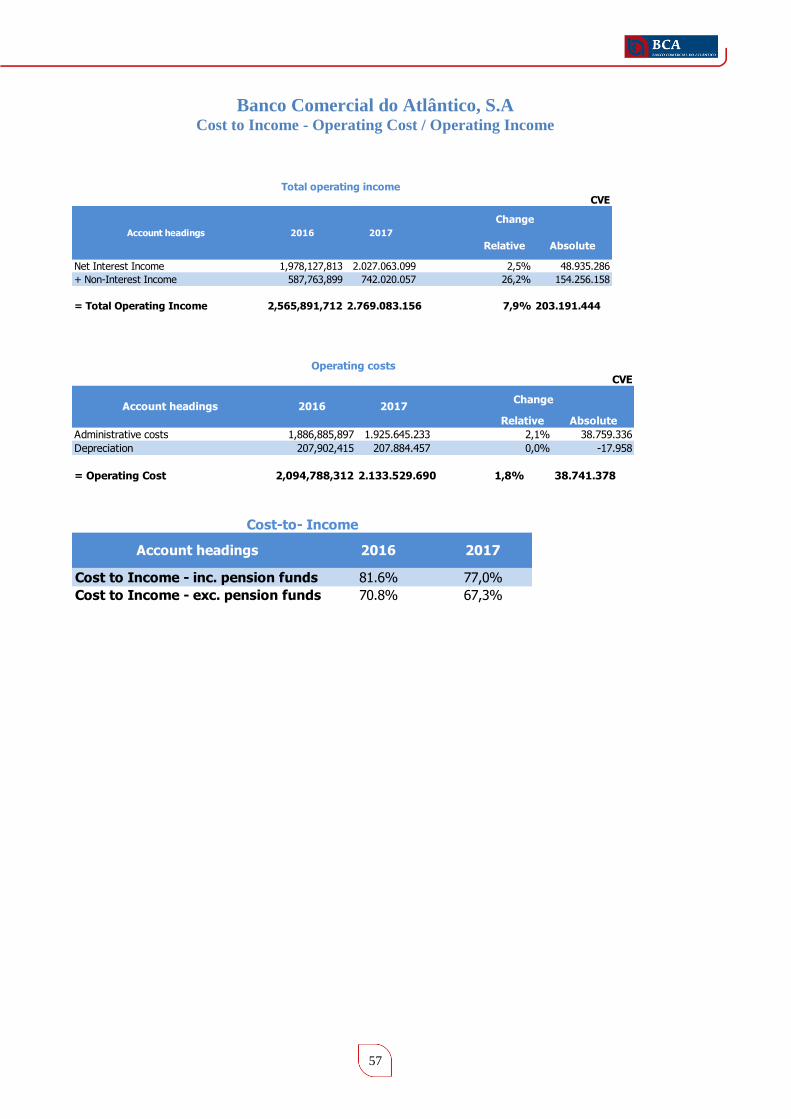

(Cost-to-Income) inc. Pensions Funds % 81.6% 77.1%

(Cost-to-Income) exc. Pensions Funds % 70.8% 67.3%

Total Asset/ Total Asset Invested CVE Millions 187 194 3.7%

Total Credit and Deposit/Nº of Asset Employees CVE Millions 243 246 1.3%

Total Credit and Deposit/ Nº of branches CVE Millions 3,235 3,323 2.7%

Number of total Active employees Unit 453 460 1.5%

Number of Fixed Active employees Unit 396 379 -4.3%

Number of branches Unit 34 34 0.0%

Table 2 - Key Values and Indicators from Activity and Income

11

5. MESSAGE FROM THE BOARD OF DIRECTORS

This Annual Report reflects clearly and objectively the most relevant activity of Banco Comercial do

Atlântico during the year 2017 and it is intended to be a document of analysis and support for all the

Bank's stakeholders.

In this sense, the Board of Directors reiterates its sincere gratitude to all BCA employees who, through

their mobilization, their professionalism and dedication, have made possible the results presented

here. We are sure that we will continue to count on the same dedication and professionalism of our

staff, in overcoming the challenges that lie ahead.

The Board of Directors also expresses its appreciation to all Shareholders, the General Assembly, the

Audit Board, the External Auditor, to Banco de Cabo Verde, to Auditoria Geral do Mercado de valores

Mobiliários, to Bolsa de Valores, for the competent cooperation in monitoring the day-to-day

management of the Bank.

To our customers, who are our reason for being, we thank you for the privilege of their trust and we

reiterate all our commitment to the satisfaction of their expectations in the relationship with the BCA,

by strengthening and making products compatible with their interests and needs, reinforcing ties of

loyalty, on the basis of trust, respect and common interests.

2017 Annual Report

12

6. INTERNATIONAL AND NATIONAL ENVIRONMENT

6.1. INTERNATIONAL

The IMF on 22 January 2018, during the World Economic Forum in Davos, Switzerland, upgraded the

estimates of the World Economic Forum (WEF) of October 2017. About 120 countries, which contribute

to more than ¾ of world GDP, registered positive product variations in 2017, evidencing the highest

synchronized world growth since 2010.

A better-than-expected performance of the economy in 2017 was reflected in the projection of an

average growth of the global economy of 3.7% in that year (+0.1 pp above the projections of Oct17)

and of 3.9% in 2018 and 2019 (+0.2 pp above previous projections).

The advanced economies are projected to have GDP

growth rates of 2.3% in 2017 and 2018 and 2.2% in 2019,

with revised initial estimates of 0.3 pp in 2018 and 0.4 pp

in 2019, reflecting a growth above that projected for the

United States of America, Germany, Japan and South

Korea, as a result of an increase in global demand and

investment.

For the US, GDP growth is expected to accelerate from 1.5% in 2016 to 2.3% in 2017. For 2018 the IMF

projects a growth of 2.7% (0.4 pp above the previous estimates), followed by a reduction of the growth

rate to 2.5% in 2019 (0.6 pp above previous estimates), reflecting the positive effects of the Senate-

approved fiscal package with short-term impact on investment.

The Eurozone should show a GDP growth rate in 2017 of 2.4% (+0.6 pp vs. 2016), 2.2% in 2018 and 2%

in 2019, with a revision of the initial estimates in a range of 0.3 pp, to be sustained by a more positive

performance from Germany, Italy and The Netherlands.

Banco de Portugal (BdP) in its Economic Bulletin of December 2017 upgraded the GDP estimates,

forecasting a growth of 2.6% in 2017, 2.3% in 2018 and 1.9% in 2019, with the Portuguese economy

benefiting from a favorable external environment.

13

Emerging and developing economies are the biggest contributors to the growth of the Global Economy,

with GDP growth rates of 4.7% in 2017 (+ 0.3 pp vs. 2016), 4.9% in 2018 and 5% in 2019, maintaining

the October WEO projections unchanged, reflecting different dynamics in each country.

The Asian emergent economy presents the greatest contribution to this projection, with estimated growth

of 6.5% in 2017 and 2018 and 6.6% in 2019, with China standing out (6.6% in 2018 and 6.4% in 2019)

and India (7.4% in 2018 and 7.8% in 2019).

Growth recovery in sub-Saharan Africa from 2.7% in 2017 to 3.3% in 2018 and 3.5% in 2019 is close to

the initial estimates (-0.1pp in 2018 and + 0.1pp in 2019) with upward revisions to Nigeria and downward

to South Africa, where rising political uncertainty weighs on confidence and investment.

Data published in the Oct17 WEO point to the reduction of the unemployment rate in the Euro Zone to

9.2% in 2017 (-0.8 pp compared to 2016) and 8.7% in 2018. In the UK, the rate should be around 4.4%

in 2017 and 2018 (-0.5 pp vs. 2016), and in the US it could also reach 4.4% in 2017 (-0.5 pp vs. 2016)

and 4.1% in 2018.

Concerning the behavior of consumer prices in the Eurozone, it is expected to accelerate from 0.2% in

2016 to 1.5% in 2017 and 1.4% in 2018. In the United Kingdom the forecasts point to 0.7% in 2016 and

2.6% in 2017 and 2018. In the US, it is projected to be 1.3% for 2016 and an increase to 2.1% in 2017

and 2018.

Table 1 presents a summary of the key international macroeconomic indicators:

2017 Annual Report

14

Table 3- Evolution of Key International Macroeconomic Indicators

Despite the optimism reflected in the upward revision of world economic growth forecasts, the IMF

warns of downside risks, especially in the medium term.

The restriction of financing conditions, as inflation increases and monetary stimuli are withdrawn,

poses some risk of adverse reaction on the financial markets due to the impact of a faster than expected

increase in interest rates on asset prices and capital flows.

In addition, a more modest-than-expected reaction to the US tax cut could have repercussions on the

strength of external demand directed at the main trading partners of this country, putting some

pressure on forecasts of growth of the world economy.

The outcome of trade agreements under review, in particular NAFTA and the EU-UK negotiations, will

also have an impact on growth, as a potential increase in trade barriers could weaken investment and

reduce potential growth.

2016 2017p 2016 2017p 2016 2017p

Global Economy 3.2% 3.7% n.d n.d n.d. n.d.

Advanced Economies 1.7% 2.3% 0.8% 1.7% n.d. n.d.

USA 1.5% 2.3% 1.3% 2.1% 4.9% 4.4%

Euro Zone 1.8% 2.4% 0.2% 1.5% 10.0% 9.2%

Germany 1.9% 2.5% 0.4% 1.6% 4.2% 3.8%

Italy 0.9% 1.6% -0.1% 1.4% 11.7% 11.4%

Holanda 2.2% 3.1% 0.1% 1.3% 5.9% 5.1%

Japan 0.9% 1.8% -0.1% 1.4% 3.1% 2.9%

United Kingdom 1.9% 1.7% 0.7% 2.6% 4.9% 4.4%

Emerging Economies 4.4% 4.7% 4.3% 4.2% n.d. n.d.

Brazil -3.5% 1.1% 8.7% 3.7% 11.3% 13.1%

Russia -0.2% 1.8% 7.0% 4.2% 5.5% 5.5%

Emerging Asia 6.4% 6.5% 2.8% 2.6% n.d. n.d.

China 6.7% 6.8% 2.0% 1.8% 4.0% 4.0%

India 7.1% 6.7% 4.5% 3.8% n.d. n.d.

Sub-saharan Africa 1.4% 2.7% 11.3% 11.0% n.d. n.d.Sources: WEO - Word Economic Outlook - October 2017

WEO - Word Economic Outlook Update - January 2018

GDP InflaTtion Unemployment

15

Other non-economic factors such as geopolitical tensions in Asia and the Middle East, elections in Brazil,

Colombia, Italy and Mexico as well as extreme weather conditions in Australia and sub-Saharan Africa

may have adverse economic effects and lead to lower-than-expected growth.

6.2. NATIONAL

6.2.1. General Information

In the General Government Budget for 2018, the Government of Cabo Verde forecasts GDP growth in

2017 in the range of 4% to 5% and an acceleration to the 5% to 5.5% interval in 2018, based on the

dynamics of the national tourism sector and consequently a good performance of the tertiary sector,

with emphasis on commerce, hotels and restaurants. There is also expected to be a contagion effect in

the secondary sector, namely in manufacturing and construction.

From the perspective of demand, economic growth is expected to be positively influenced by Gross

Fixed Capital Formation, as a result of the increase in Foreign Direct Investment (FDI), as well as of

national investments, taking into account the mechanisms created by the Government for the

improvement of the business environment and access to credit, and also by the increase in Private

Consumption, justified by the empowerment of families.

The economic evolution of the country also benefits from a context of recovery of world economic

activity, particularly in the Euro Zone, the country's main economic partner. The more favorable

external environment, in line with the IMF's most optimistic reviews, will have a positive impact on

tourist demand, and may also improve the execution of planned projects and favor the Emigrants

remittances.

In 2018, it is expected that the transmission of external to domestic inflation will be less than in 2017,

with values ranging from 0% to 1% expected. However, the lack of rain in 2017, which resulted in a bad

agricultural year, represents an upward risk to the general level of food prices.

BCV's monetary forecasts point to an increase in both the Monetary Mass and the Credit to the

Economy, with the Government considering that there is a positive risk for the credit in 2018, resulting

from several financial instruments foreseen in the State Budget for 2018 and that will facilitate access

to the credit market by micro, small, medium and large enterprises and also promote the

internationalization of Cabo Verdean companies. In 2017, the increase in the money supply, expressed

by the M2 aggregate, decelerated, from 8.4% in December 2016 to 4.9% in November 2017, as a result

2017 Annual Report

16

of the decrease in the Net International Reserves (-1.3% in November 2017 compared to + 20.8% in the

same period last year), despite the growth of credit to the Economy of 5.25% (5.2% in November 2016).

Regarding the external sector, in 2017, projections point to an increase in the current account deficit,

driven by a significant increase in imports. In 2018 a more moderate acceleration is expected. As a

result, the net reserves / imports ratio will reach 6 and 5.8 months in 2017 and 2018 respectively. It

should be noted that in order to finance the deficit in the Balance of Payments, it was necessary to

reduce the level of Reserve Assets by about -2 billion CVE by the 3rd Quarter of 2017, confirming the

less optimistic forecasts regarding the evolution of the external position.

For 2018, a budget deficit of 3.1% of GDP is expected, financed essentially from concessional external

resources. The Debt Stock Ratio is expected to reach 132.2% of GDP, with Budgetary consolidation and

debt sustainability continuing to be a major concern and challenge. In this line, the successive speeches

of the Government have emphasized the private initiative as a source of economic growth, and the

State has a role of regulator and creator of opportunities, since the margin to stimulate the economy

through more indebtedness is very small.

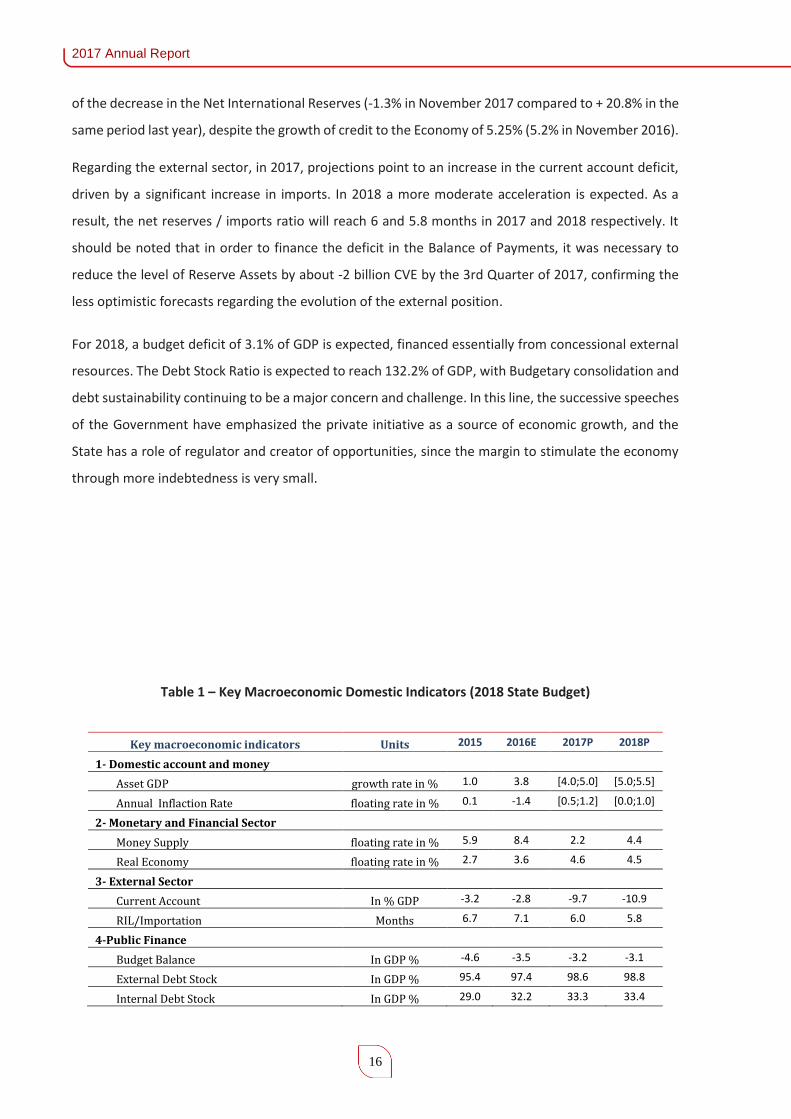

Table 1 – Key Macroeconomic Domestic Indicators (2018 State Budget)

Key macroeconomic indicators Units 2015 2016E 2017P 2018P

1- Domestic account and money

Asset GDP growth rate in % 1.0 3.8 [4.0;5.0] [5.0;5.5]

Annual Inflaction Rate floating rate in % 0.1 -1.4 [0.5;1.2] [0.0;1.0]

2- Monetary and Financial Sector

Money Supply floating rate in % 5.9 8.4 2.2 4.4

Real Economy floating rate in % 2.7 3.6 4.6 4.5

3- External Sector

Current Account In % GDP -3.2 -2.8 -9.7 -10.9

RIL/Importation Months 6.7 7.1 6.0 5.8

4-Public Finance

Budget Balance In GDP % -4.6 -3.5 -3.2 -3.1

External Debt Stock In GDP % 95.4 97.4 98.6 98.8

Internal Debt Stock In GDP % 29.0 32.2 33.3 33.4

17

Global Debt Stock In GDP % 124.4 129.6 131.9 132.2

Source: MF, BCV, INE.

In January 2018 a team from the International Monetary Fund - IMF, after completing a visit to the

country, presented some conclusions about the Cabo Verdean economy, subject to approval by the

institution's Executive Board.

Contrary to the Government's most optimistic expectations, the IMF team estimates growth

acceleration from 4% in 2017 to 4.3% in 2018, stabilizing at 4% in the medium term.

The leader of the team says that the improvement in the pace of growth of the national economy

reflects a favorable international environment and the result of ongoing economic reforms. Growth in

2017 was underpinned by double-digit growth in tourist arrivals, credit growth in the private sector,

and increased consumer and business confidence, with the same factors expected to contribute to the

expected economic performance in 2018.

The team warns of the need to deepen the great fiscal consolidation effort underway, complete the

restructuring of state-owned enterprises and contain the growth of public debt.

The level of Non-Performing Loans (NPLs) and the low profitability of the Banking Sector is seen as a

threat to the stability of the financial sector, despite some improvement in the indicators of financial

stability. In addition, the resolution of high levels of NPL is indicated as a priority and it is recommended

to avoid further loosening of the write-off rules of irrecoverable loans.

6.2.2. Financial System

Banco de Cabo Verde - BCV continued its policy of monetary easing implemented since 2015, which

aimed at making monetary policy more effective and, at the same time, boosting the market and

fostering economic growth. In this sense, it reduced its reference interest rate in June, of absorption

and lending interest rate and discount window. It also implemented interventions in the Monetary

Regularization Securities (MRS) through fixed rate tenders, with placement at the Banco de Cabo

Verde's reference rate, in order to improve the effectiveness of monetary policy; Elimination of the

exemption to the Banking Financial Institutions of 1,000 million CVE on the Basis of Incidence of the

Minimum Reserves regime.

In 2017, among the legal and regulatory diplomas that were published, the following stand out:

Law 7/IX/2017 establishing the Guarantee and Deposits Fund.

2017 Annual Report

18

Notice 1/2017, which amends point 4 of Notice 4/2007 of 25 February 2008, providing that

for own funds matters, institutions shall ensure a total capital adequacy ratio of not less

than 12%.

Notice 3/2017 which establishes the general conditions for opening bank deposit accounts

at credit institutions, thereby amending BCV Notice 2/2011.

Notice No. 4/2017 which establishes the minimum requirements that the internal control

system of a financial institution must respect, and the responsibilities of the governing

body in this area.

Notice no. 5/2017, which defines the conditions, mechanisms and procedures required to

effectively fulfill the preventive duties of money laundering and terrorist financing with

respect to the provision of financial services subject to the supervision of Banco de Cabo

Verde.

Notice nº 6/2017 approving the Corporate Governance Code of financial institutions,

which establishes the criteria of good governance that are most relevant to the activity

carried out by financial institutions.

Notice No. 7/2017, which establishes the minimum content of the annual corporate

governance report of financial institutions.

Notice no. 8/2017 that regulates the management of the Deposit Guarantee Fund and

aims to regulate the operation of the management of the Deposit Guarantee Fund.

Notice no. 9/2017 about the value of the annual contribution to be delivered to the

Deposit Guarantee Fund by the participating institutions.

Notice no. 10/2017 amending Notice 4/2015, of July 10, which establishes the recovery

plan for Credit Institutions. It was considered necessary that the Credit Institutions include

in their respective recovery plans the framework of qualitative and quantitative indicators

that allow them to point out more easily the moment when the recovery measures

presented in the plan can be activated. It is then added that the institutions subject to this

are obligated to incorporate qualitative and quantitative indicators into their recovery

plans.

Notice no. 11/2017 amending Notice no. 5/2015 of 10 July on the resolution plan for credit

institutions. This notice shortens for a year the deadline at which the subject Credit

19

Institutions, exempted from the obligation to present resolution plans, will have to request

a new waiver request.

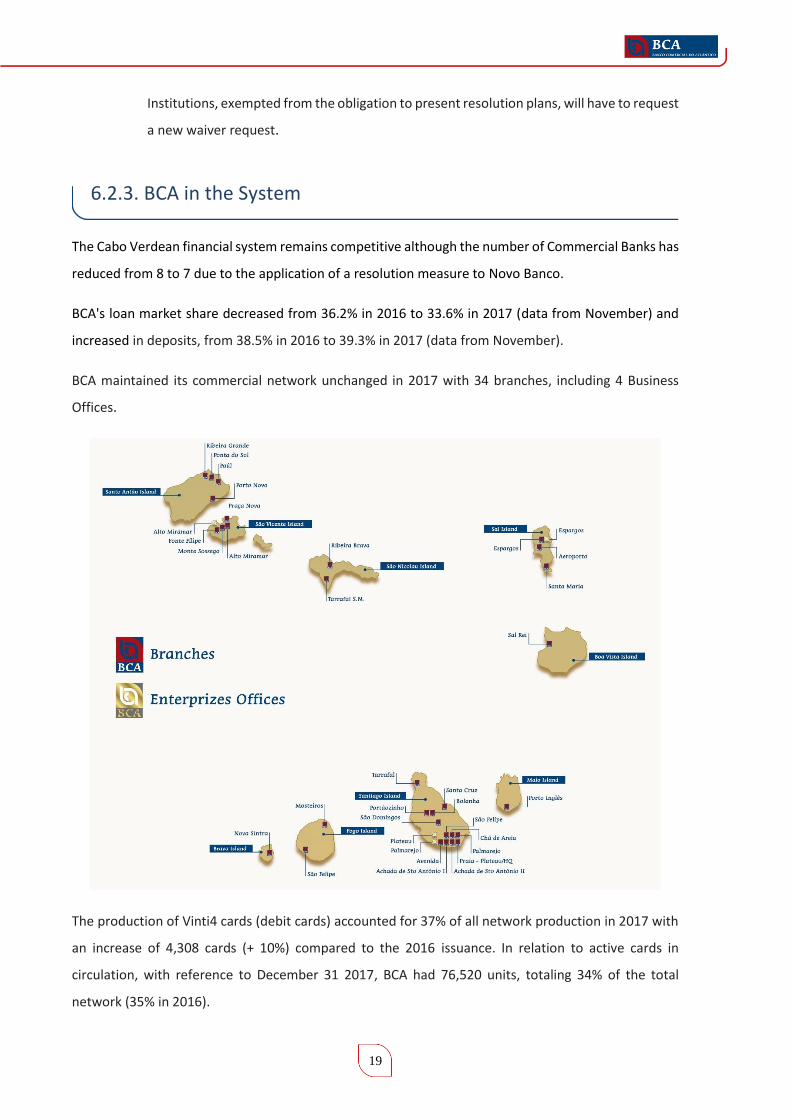

6.2.3. BCA in the System

The Cabo Verdean financial system remains competitive although the number of Commercial Banks has

reduced from 8 to 7 due to the application of a resolution measure to Novo Banco.

BCA's loan market share decreased from 36.2% in 2016 to 33.6% in 2017 (data from November) and

increased in deposits, from 38.5% in 2016 to 39.3% in 2017 (data from November).

BCA maintained its commercial network unchanged in 2017 with 34 branches, including 4 Business

Offices.

The production of Vinti4 cards (debit cards) accounted for 37% of all network production in 2017 with

an increase of 4,308 cards (+ 10%) compared to the 2016 issuance. In relation to active cards in

circulation, with reference to December 31 2017, BCA had 76,520 units, totaling 34% of the total

network (35% in 2016).

2017 Annual Report

20

The year 2017 was the consolidation of the services BCADirecto Telephone (Contact Center) and

BCADirecto Mobile, which allow customers to obtain information, check and make transactions on their

accounts through the landline and also the mobile devices with Internet access.

BCA registered around 7 thousand new users / members of BCA Directo Multi-channel service (Internet,

Mobile and Telephone). BCA Directo service ended the year with 48 thousand active users (44 thousand

in 2016).

In 2017 BCA's ATM machine grew at a rate of 11% compared to the previous year, ending the year with

61 machines installed and active in the vinti4 network. In terms of market shares, there was a growth

of 2pp in the equipment installed in the vinti4 network, totaling 34%.

The Point of Sale (POS) supported by BCA

maintained the growing trend, reaching 2,059

installed and active equipment, which

represented a growth of 4% over the previous

year. In the meantime, the market share

remained at 31%, both with respect to the

equipment installed in the Vinti4 network, as

well as with regard to the number of transactions

carried out in the POS channel, with an improved

share in terms of amounts transacted in 1 pp.

The deposit machines remained unchanged, totaling 6 machines located in branches located in the

islands of Santiago, São Vicente and Sal.

This channel continued to have a very positive acceptance among customers, as evidenced by the

growth in number of deposits (+ 35%) and the amount of deposits (+ 34%), with approximately 85

thousand deposits totaling 1,7 million escudos.

BCA continued to be the only Bank in the country to offer its customers this complementary channel

to make their deposits with speed, security and convenience.

21

7. STRATEGIC VISION

The perspectives of relative stability of the international environment and improvement of the

domestic environment, along with the acceleration of the rhythm of approach of the national

supervision of BCV to the international standards, configure the framework in which BCA will adjust

its strategy.

In this context, the strategic performance of BCA continues through the following vectors:

1. Final Strategic Goals:

a. Increase of Business Profitability through:

The improvement of Net Interest Income of loan operations

I. The increase of Loan-to Deposit Ration

II. A greater contribution of Non-Interest Income

b. Reduction of Cost-to-Income, through:

I. The Increase of the Operating Income

II. The improvement of Technical and Operational Efficiency

c. Strengthening of Solvency based on

I. A Commercial Policy sensitive to the capital risk and consumption of the operations

II. A prudent Dividend Policy

2. Specific Strategic Goals

a. Growth of the Regular Portfolio, through:

I. A greater Commercial Proactivity without prejudice to risk weighting and capital

consumption of operations

II. The improvement of the Quality of Service at branches

2017 Annual Report

22

III. A better Communication between the commercial network (branches) and

operational services

IV. Reducing the Response Time for internal and external customers

b. Reduction of the Non-Performing Loans Portfolio, through:

I. A particular attention to the First Signs of Default

II. More Sustainable Restructuring

III. Better Functional Articulation between GRE and GJC

c. More Proactivity (internal and external) in the management and alienation of the assets

in the portfolio (court proceedings and enforcement)

d. Improvement of Technical and Operational Efficiency.

I. Organizational Improvements

II. Control and reduction of Operational Costs.

III. Reduction of Operational Risk

IV. Improvement of Internal Control

V. New Investments, on a business-case basis

VI. Qualification of Human Resources

23

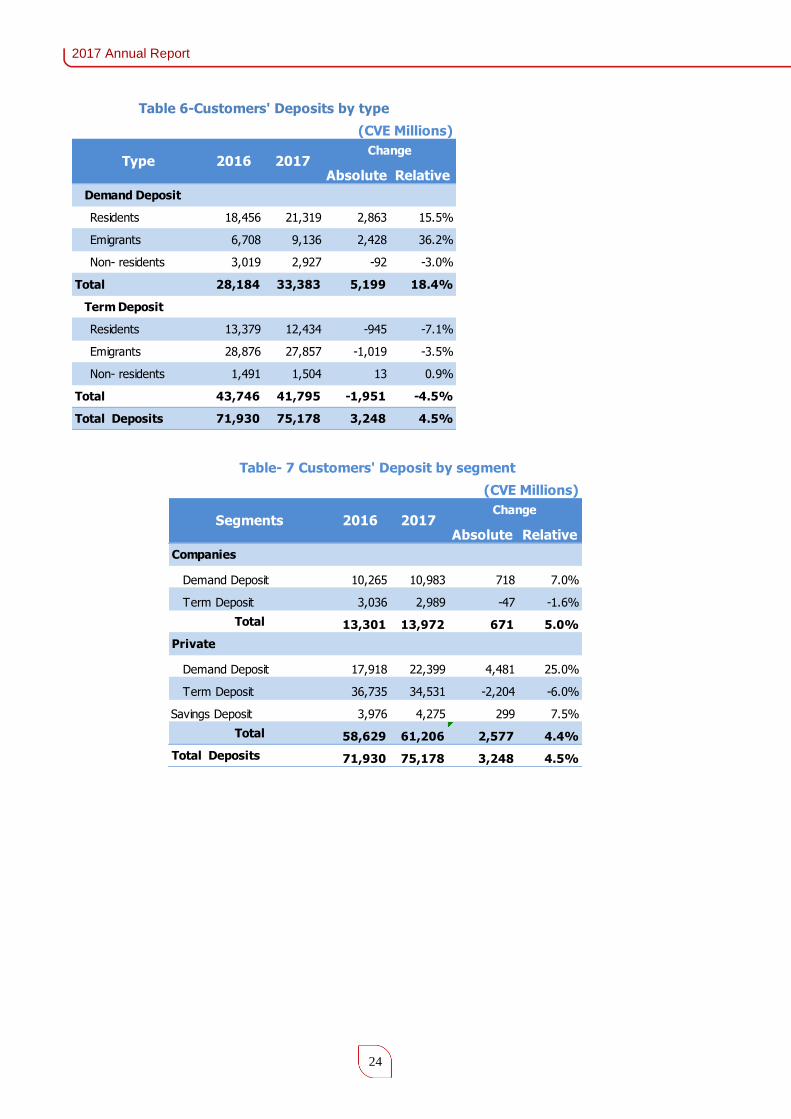

8. COMMERCIAL ACTIVITY

8.1. FUNDS

The focus on the quality of service provided to customers, product innovation, recognition by Cabo

Verdeans in the country and in the Diaspora, and the election of BCA as a Marca de Confiança (trusted

brand) make the Bank a reference in the national banking market.

The balance of Customer Deposits reached 75.2 billion CVE, an increase of 4.5% compared to 2016, and

continues to demonstrate the trusted in the BCA brand. This evolution was evidenced by the increase

in Demand Deposits by 18.4% and the Savings Deposits by 7.5%. The Time Deposits decreased at the

rate of 5.7%.

The table below illustrates the evolution of Customer Funds:

In terms of customer segment, the BCA Deposits belong mostly to Individual Customers with a weight

of 81.4% (81.5% in December 2016), an increase of 4.4%. Business Deposits also increased compared

to 2016. Total Emigrant Deposits represent 49.2% of the total BCA Deposits Portfolio and grew 4%

compared to December 2016.

Table 5- Customers' Funds

(CVE Millions)

Absolute Relative

Deposits 71,930 75,178 3,248 4.5%

Demand Deposits 28,184 33,383 5,199 18.4%

Term Deposits 39,770 37,520 -2,250 -5.7%

Savings Deposits 3,976 4,275 300 7.5%

Type 2016 2017Change

2017 Annual Report

24

Absolute Relative

Demand Deposit

Residents 18,456 21,319 2,863 15.5%

Emigrants 6,708 9,136 2,428 36.2%

Non- residents 3,019 2,927 -92 -3.0%

Total 28,184 33,383 5,199 18.4%

Term Deposit

Residents 13,379 12,434 -945 -7.1%

Emigrants 28,876 27,857 -1,019 -3.5%

Non- residents 1,491 1,504 13 0.9%

Total 43,746 41,795 -1,951 -4.5%

Total Deposits 71,930 75,178 3,248 4.5%

Table 6-Customers' Deposits by type

Change2016 2017

(CVE Millions)

Type

Absolute Relative

Companies

Demand Deposit 10,265 10,983 718 7.0%

Term Deposit 3,036 2,989 -47 -1.6%

Total 13,301 13,972 671 5.0%

Private

Demand Deposit 17,918 22,399 4,481 25.0%

Term Deposit 36,735 34,531 -2,204 -6.0%

Savings Deposit 3,976 4,275 299 7.5%

Total 58,629 61,206 2,577 4.4%

Total Deposits 71,930 75,178 3,248 4.5%

Segments 2016 2017

Table- 7 Customers' Deposit by segment

Change

(CVE Millions)

25

8.2. LOAN

8.2.1. Constraints on lending activity

The activity of BCA in 2017 has been influenced by the resumption of economic dynamics, with some

business opportunities sustained by good market prospects, with an impact on credit demand and

competition among banks for good operations that are emerging.

The Central Bank, in June 2017, aimed at stimulating credit to the economy, adopted a set of monetary

easing measures, namely the reduction of the reference interest rate by 200 basis points, from 3.5% to

1.5%; the reduction of the deposit facility rate from 0.25% to 0.1%; the decrease in rates of lending

facility and discount window in the same amount as the reference interest rate, since they are indexed

to these, going from 6.5% to 4.5% and 7.5% to 5.5% respectively; the implementation of Monetary

Regularization Securities interventions through fixed rate tenders, with placement at Banco de Cabo

Verde's reference rate, in order to improve the effectiveness of monetary policy; the elimination of the

exemption to the Banking Financial Institutions of 1,000 million CVE on the Base of Incidence of the

regime of Required Reserves.

In response to the policies of the Central Bank, BCA decided in September to reduce the asset´s interest

rates, which had an impact in the last quarter of the year, with the increase in demand for loans from

customers. For 2018, in light of favorable economic growth prospects and investor optimism, loan is

expected to grow at a faster rate.

8.2.2. Analysis of Granted Loans

Total new loans granted in 2017, including restructured loans, totaled approximately 8.4 billion CVE,

slightly more than 2016 at 0.8% (64 million CVE), with loans granted to households during the year to

increase by 16.9%, compared to the year 2016. It shall be noted the increase of 14.5% and 18.1% in the

new production of home loans for Permanent Private Residence and Income and in loans for Other

Purposes.

Of note is the decrease in the business segment, despite the strong commitment on loans granted to

SMEs under the credit line launched in 2014.

The following table shows the evolution of new loan granted by customer segments.

2017 Annual Report

26

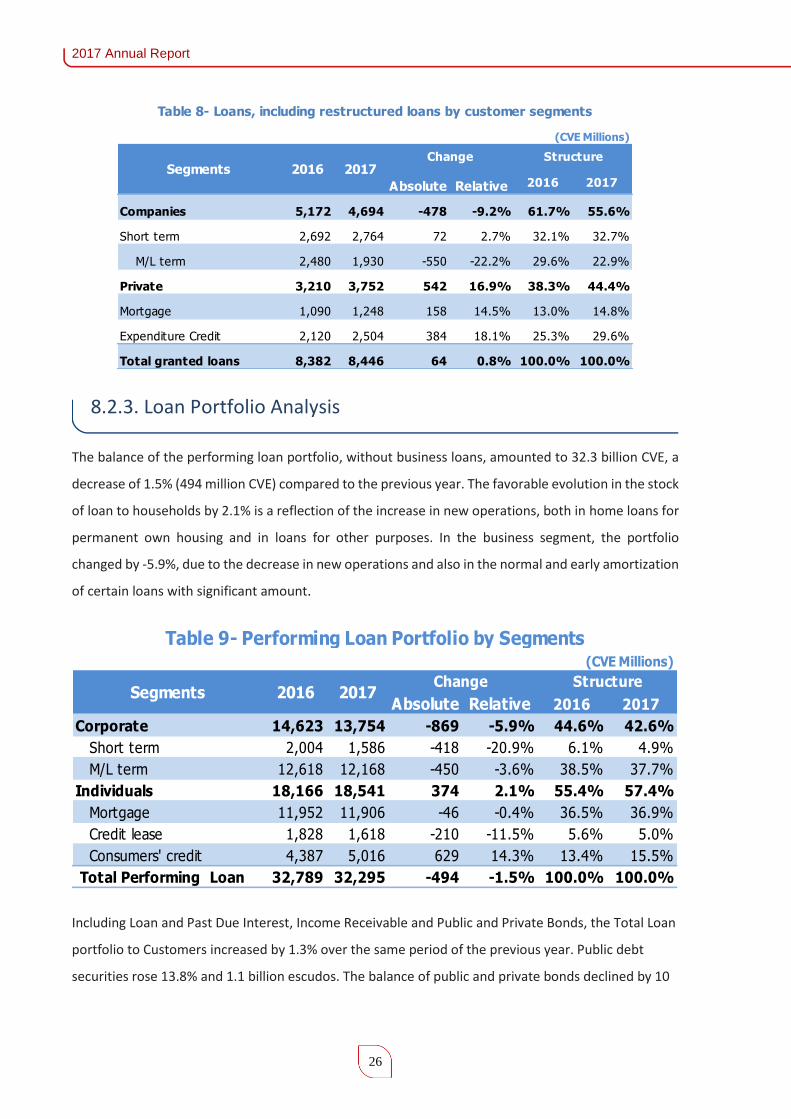

8.2.3. Loan Portfolio Analysis

The balance of the performing loan portfolio, without business loans, amounted to 32.3 billion CVE, a

decrease of 1.5% (494 million CVE) compared to the previous year. The favorable evolution in the stock

of loan to households by 2.1% is a reflection of the increase in new operations, both in home loans for

permanent own housing and in loans for other purposes. In the business segment, the portfolio

changed by -5.9%, due to the decrease in new operations and also in the normal and early amortization

of certain loans with significant amount.

Including Loan and Past Due Interest, Income Receivable and Public and Private Bonds, the Total Loan

portfolio to Customers increased by 1.3% over the same period of the previous year. Public debt

securities rose 13.8% and 1.1 billion escudos. The balance of public and private bonds declined by 10

Absolute Relative 2016 2017

Companies 5,172 4,694 -478 -9.2% 61.7% 55.6%

Short term 2,692 2,764 72 2.7% 32.1% 32.7%

M/L term 2,480 1,930 -550 -22.2% 29.6% 22.9%

Private 3,210 3,752 542 16.9% 38.3% 44.4%

Mortgage 1,090 1,248 158 14.5% 13.0% 14.8%

Expenditure Credit 2,120 2,504 384 18.1% 25.3% 29.6%

Total granted loans 8,382 8,446 64 0.8% 100.0% 100.0%

Table 8- Loans, including restructured loans by customer segments

(CVE Millions)

Segments 2016 2017Change Structure

(CVE Millions)

Absolute Relative 2016 2017

Corporate 14,623 13,754 -869 -5.9% 44.6% 42.6%

Short term 2,004 1,586 -418 -20.9% 6.1% 4.9%

M/L term 12,618 12,168 -450 -3.6% 38.5% 37.7%

Individuals 18,166 18,541 374 2.1% 55.4% 57.4%

Mortgage 11,952 11,906 -46 -0.4% 36.5% 36.9%

Credit lease 1,828 1,618 -210 -11.5% 5.6% 5.0%

Consumers' credit 4,387 5,016 629 14.3% 13.4% 15.5%

Total Performing Loan 32,789 32,295 -494 -1.5% 100.0% 100.0%

Table 9- Performing Loan Portfolio by Segments

Segments 2016 2017Change Structure

27

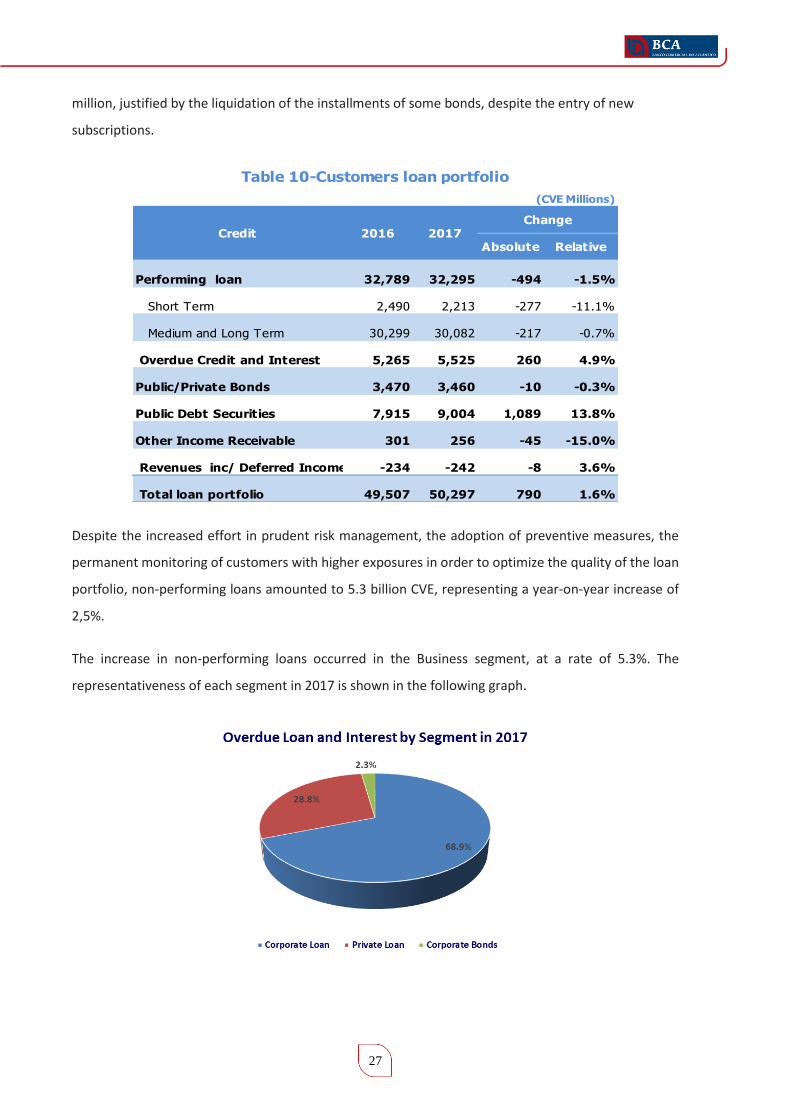

million, justified by the liquidation of the installments of some bonds, despite the entry of new

subscriptions.

Despite the increased effort in prudent risk management, the adoption of preventive measures, the

permanent monitoring of customers with higher exposures in order to optimize the quality of the loan

portfolio, non-performing loans amounted to 5.3 billion CVE, representing a year-on-year increase of

2,5%.

The increase in non-performing loans occurred in the Business segment, at a rate of 5.3%. The

representativeness of each segment in 2017 is shown in the following graph.

(CVE Millions)

Absolute Relative

Performing loan 32,789 32,295 -494 -1.5%

Short Term 2,490 2,213 -277 -11.1%

Medium and Long Term 30,299 30,082 -217 -0.7%

Overdue Credit and Interest 5,265 5,525 260 4.9%

Public/Private Bonds 3,470 3,460 -10 -0.3%

Public Debt Securities 7,915 9,004 1,089 13.8%

Other Income Receivable 301 256 -45 -15.0%

Revenues inc/ Deferred Income -234 -242 -8 3.6%

Total loan portfolio 49,507 50,297 790 1.6%

Table 10-Customers loan portfolio

Credit 2016 2017Change

2017 Annual Report

28

The accumulated balance of the Loan Impairment, which includes the impairment of the obligations of

private companies, totaled PTE 4,1 billion, representing a variation of 7.8% and PTE 297,000, and

coverage of Loan Loss Due to Impairment of 74, 5%.

9. OTHER ACTIVITIES

9.1. HUMAN RESOURCES

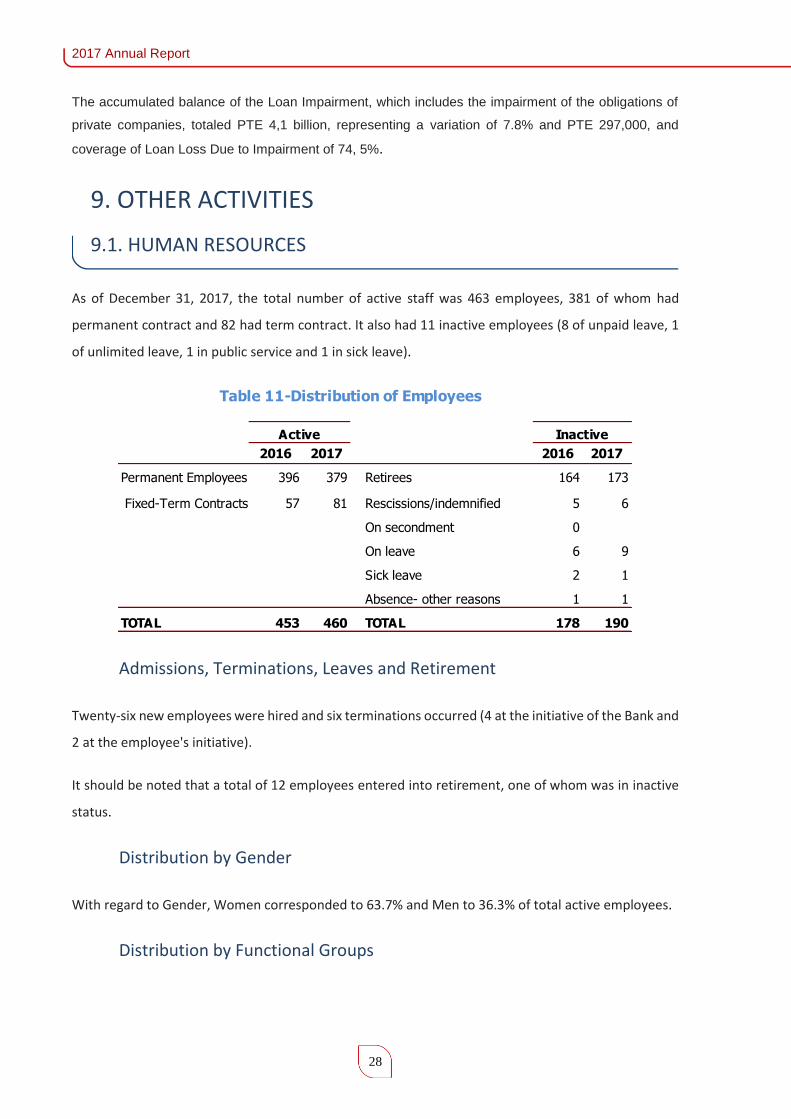

As of December 31, 2017, the total number of active staff was 463 employees, 381 of whom had

permanent contract and 82 had term contract. It also had 11 inactive employees (8 of unpaid leave, 1

of unlimited leave, 1 in public service and 1 in sick leave).

Admissions, Terminations, Leaves and Retirement

Twenty-six new employees were hired and six terminations occurred (4 at the initiative of the Bank and

2 at the employee's initiative).

It should be noted that a total of 12 employees entered into retirement, one of whom was in inactive

status.

Distribution by Gender

With regard to Gender, Women corresponded to 63.7% and Men to 36.3% of total active employees.

Distribution by Functional Groups

2016 2017 2016 2017

Permanent Employees 396 379 Retirees 164 173

Fixed-Term Contracts 57 81 Rescissions/indemnified 5 6

On secondment 0

On leave 6 9

Sick leave 2 1

Absence- other reasons 1 1

TOTAL 453 460 TOTAL 178 190

Table 11-Distribution of Employees

Active Inactive

29

Regarding the distribution by Functional Groups, 47.2% of the employees performed Technical

functions, 22.6% held Management positions, 14.1% Auxiliary and Support functions, 10.4% were

Multi-functions, and 5.7 % performed administrative functions.

Distribution by Level of Education

At the level of literacy, there is an increase in the number of employees holding a bachelor degree, to

49.9% of the total. It is also observed that the percentage of employees with Polytechnic Higher

Education maintained at 2.2%, and those who hold Technical-Vocational Education increased to 5.8%,

27.4% with Secondary Education and 14.7% with Basic Education. It is observed the maintenance and

reinforcement of the decreasing tendency of the number of employees with academic qualifications of

Basic and Secondary level versus the increase of the same with higher education levels.

Training and Professional Qualification

In 2017 BCA invested in 58 training sessions reaching a total of 768 participants, with a total workload

of 7,076 hours.

Training was carried out in several areas and with great impact on the Bank's activity, of which the

following stand out: Course on protection of personal data; Workshop on - Legislation on financial

instrument markets; Seminar "Internal Audit and Control"; Motivation and teamwork; General and

operational FACTA; Governance model for operational risk; Results-oriented management; Money

laundering and terrorist financing; International foundation level for compliance officer function;

No. % No. %

Primary 75 16.6% 68 14.8%

Secondary 131 28.9% 127 27.6%

Vocational 30 6.6% 27 5.9%

Polytechnic 10 2.2% 10 2.2%

University 207 45.7% 228 49.6%

TOTAL 453 100% 460 100%

Table 12-Educational Qualifications

2016 2017

2017 Annual Report

30

Techniques for decision-making in the management of financial institutions; Workshop on risk

management and internal control; Workshop on

ICAAP & ILAAP; AML - Program Breakdown. The

Western Union case dissected; International

accounting standards; Contract management;

Complaints management; Internships at Caixa

Geral de Depósitos.

It should be noted the great investment made in

training in the areas of Risk Management and Internal Control and Compliance.

Of the training sessions carried out, 25 were in the country (out of company) covering 101 employees,

with a workload of 3,420 hours, while in the country (in the company) 25 sessions were carried out

covering 648 participants, with a workload of 3,003 hours.

In terms of training abroad, 19 employees

participated in 8 training courses in Caixa Geral

de Depósitos and in the Bank Training Institute

in areas such as Impairment, International

Accounting Standards, Document

Management, Risk Management, Money

Laundering and Terrorism Financing, with

workload of 653 hours. Compared to 2016, there was an increase in the number of training sessions

and the number of workload.

During the year 2017 a total of 12 professional internships were provided. Of the six placements offered

in 2016, three were converted into fixed-term contracts in 2017, one was terminated and two

continued the internship for the same year, with BCA's role as a partner in the country's development

in job creation, especially among the young.

With regard to the participation in the academic qualification, throughout the year, the bank supported

three employees in Bachelor's and Master's program.

BCA Participation in the GMC – Global Management Challenge

31

The year 2017 was highlighted by the results achieved by BCA in the Global Management Challenge

Competition - giving shape to an axis of the Strategic Plan of BCA related to the improvement of the

quality of Human Resources and the promotion of talents.

Global Management Challenge is a negotiation competition, created 37 years ago, that operates in a

competitive environment between virtual companies and is, above all, a training tool that enables

participants to develop management skills but also behavioral skills.

In March 2017 a team made up of BCA Employees won the first place in the 1st Edition of the Global

Management Challenge in Cabo Verde, qualifying for the final of the World Competition that was held

in Qatar and counted with the participation of countries of four continents (Africa, Europe, Asia and

America). This achievement also earned the recognition of the Government of Cabo Verde to the BCA’s

Team, for having managed to lead the country to participate, for the first time, in the international

elimination of this important competition of management strategy.

In October 2017, BCA participated in the "2nd Edition of the Global Management Challenge CGD

Internacional 2017/2018". In this intra-group initiative, aimed only at Caixa Geral de Depósitos Group

employees, BCA was represented by three teams from the Sal, São Vicente and Santiago Islands. For

BCA, the result of the competition could not be better: the teams of Praia and S. Vicente were cleared

for the final and the team of the island of São Vicente was the winner of this edition, which was

attended by twenty three teams, representing thirteen CGD Group Units.

Social Benefit for Employees

The employees of the Bank's Private Social Security System, retired employees, and their families have

benefited, in the country, from clinical diagnosis, general and specialist clinic visits, ocular and stomatal

prostheses, infirmary treatments, surgeries and hospitalizations.

Also, under the protocol between BCA and SAMS - Serviços de Apoio Médico e Social dos Sindicatos

dos Bancários do Sul e Ilhas, de Portugal - 105 Terms of Responsibility and 8 Prior Authorizations were

issued, totaling 636 treatments for the benefit of these collaborators, namely.

There were eight evacuations abroad for the benefit of employees of the Private System, including an

accompanying person, and the Bank continued to bear the costs of an evacuee and an escort who

remain in Portugal.

2017 Annual Report

32

In the Country, 20 beneficiaries of the Social Security System and three companions were evacuated to

Praia and S. Vicente. Medical expenses in the country amounted to approximately 32 million CVE and

abroad totaled approximately 7 million CVE.

The Bank continued to support its employees and pensioners through the lending policy, namely for

the acquisition or construction of permanent own housing.

In addition to the HRD routine tasks, it is worth emphasizing the strong commitment of this OE in

fulfilling its responsibilities related to the Compliance function. In this regard, in close collaboration

with the GFC, DSI and ISD, and STIF a diagnosis was made of the legal, regulatory and procedural

compliance of the Video Surveillance Systems and the Access and Attendance Control System installed

in the different installations and BCA’s buildings, and the aspects considered risk enhancers of non-

compliance with BCA Code of Conduct, internal regulations and other applicable legislation with the

Comissão Nacional de Proteção de Dados (CNPD) were identified and remedied.

9.2. RISK MANAGEMENT, INTERNAL AUDIT AND CONTROL

Risk Management

In 2017, two structural projects for the Bank were implemented: the implementation of the Risk

Management Function and the adoption of IFRS 9. The main objectives of these projects are to ensure

that the BCA's risk management system is adequate and effective, ensuring that all material risks of the

activity carried out are duly identified, evaluated, monitored and controlled and also advise and present

complete and pertinent information to the Board of Directors and the Fiscal Board on the relevant risks

associated with BCA activity.

As part of the process of reviewing the risk management framework, and in particular with regard to

the implementation of the Risk Management Function, the Internal Regulations of the Risk

Management Function were adopted, in order to comply with article 16 of BCV Notice No. 4/2017 of

Sep0717 - Internal Control System.

Likewise, it was necessary to determine the BCA Risk Adjustment Factor (RAF), in accordance with the

Risk Adjustment Governance Model approved by the BCA's Board.

33

In 2017, the Risk Management Department continued to coordinate the fulfillment of the Internal

Capital Adequacy Assessment Process (ICAAP), in a process that is transversal to BCA's various

Organizational Units and allows an in-depth self-assessment of the institution's main risks.

Credit Risk

As of July 31, 2017, in compliance with the international standards requirements, we marked on the

core system the concept of Non-Performing Exposure (NPE), that is, defaulted loans, whose definition

and scope was also revised, and with individual impairment attributed, and the Non-Performing Loan

(NPL) corresponds to the subset of the loan and advance agreements, thus excluding securitized loans

and off-balance sheet exposures.

As a recurring activity, the Risk Factors underlying

the impairment loss model ((PI – Probability of

Impairment, PD – Probability of Default and LGD -

Loss Given Default) were updated, and an

improvement of the PIs and PDs was recorded,

translating a presumed improvement in the

portfolio, but diluted, due to the negative impact

of late recovery, which implied a strengthening of

LGD's.

Loan Recovery

Monitoring and recovery of non-performing loan operations is one of the key areas for the bank's good

performance and sustainability. In this sense, the organic structure includes a Loan Recovery Office,

with the responsibility of monitoring and promoting the recovery of all loan operations in default for

more than 60 days. In cases where it is not possible to recover by negotiation, the Loan Recovery Office

proposes to activate the legal mechanisms available to BCA for coercive collection, namely judicial

enforcement.

The year was also marked by the reinforcement of Loan Recovery Office's collaboration with the Legal

and Litigation Office, resulting in the recovery of loans that were already in judicial execution phase, by

promoting the end of the executive process, through the adjudication of assets. Other situations and

procedures have been identified that will have a positive impact on BCA's defaults portfolio in 2018.

2017 Annual Report

34

Liquidity Risk

In the fiscal year 2017 there were no significant changes in the liquidity conditions. The Bank continued

to evolve in a favorable way in reference to liquidity and unfavorable manner to the profitability of the

business. While on the liabilities side the growth of the Balance was supported by Demand Deposits,

on the assets side the increase was mainly due to the amount invested in Investments in Financial

Institutions and Public Debt Securities, with a reduction of the Loan portfolio in normal situation, better

paid asset. Thus, despite the strategies adopted, it was not possible to return to the stagnation of the

loan portfolio, translating into very low loan to deposit ratio.

Interest Rate Risk

The Interest Rate Risk was monitored thru the

quarterly analysis of the evolution of the Loan

Portfolio with indexed interest rate and the

evolution of the internal and external Indexes, as

well as the Repricing Gap.

Prudential maps also produced for BCV, namely

the monthly Map for the preparation of the Stress-

Tests and the semi-annual Map of calculation of the impact of interest rate risk on the Net Position and

the Net Interest Income.

Exchange Rate Risk

Exchange Rate Risk was monitored by monthly analysis of the exchange position, exchange rates and

revaluation results of the USD, the main international currency subject to exchange rate risk. The

exposure of the Foreign Currency Portfolio was also monitored through the Value-at-Risk analysis

Report. A quarterly report was also produced which briefly summarizes the main aspects of the

abovementioned reports for submission to the Executive Board.

Exchange positions rarely exceeded the limits set for the various currencies that make up the portfolio,

with most of the excesses resulting from sporadic increases in the volume of orders made at the

branches. All the excesses were promptly justified and corrected, ensuring a seamless process of

exchange risk management.

35

Compliance Risk

BCA has formally instituted a Compliance Function which is characterized by being an independent,

permanent and effective function of compliance control of the obligations arising from laws,

regulations, rules of conduct, ethical principles and other duties to which BCA is subject. It promotes

the mitigation of Compliance risks and the implementation of adequate measures to solve deficiencies

or detected failures, in close collaboration with other BCA and CGD structures.

Management of the Compliance Function is the responsibility of all the Structure Bodies, under the

coordination of the Compliance Function Support Office, which is also responsible for safeguarding the

proper execution of procedures for the prevention of money laundering and financing of terrorism, as

well as the prevention of market abuse crimes.

As in the previous year, 2017 was also characterized by a strong intervention in information

technologies to support compliance and money laundering activities, requiring a series of adaptations

to the system, implementation of new modules and acquisitions of own support platforms (FACTA,

Profiling, Live).

Operational Risk

In the Fiscal year that just ended, the process of consolidating operational risk management continued,

namely in the implementation of the different tools associated with the corporate management model,

which includes a set of structural and instrumental challenges.

At the structural level, the operational risk area was separated from the internal control area, and the

latter became part of the Internal Audit Department, and in the instrumental field, emphasis was placed

on training sessions for the institution's employees, in addition to the improvement of the corporate

tools used in the management of operational risk, with a direct impact on the monitoring and mitigation

of the same ones.

Internal Audit and Control

The Internal Audit Department was created in February 2017, resulting from the transformation of the

Audit and Inspection Office, due to the need for the Bank to strengthen and align this function with the

best international practices.

2017 Annual Report

36

With the approval of the new statute, the Department now has two offices, namely, the Office of Audit

and Inspection and the Office of Internal Control. What was intended with the new department is the

implementation of a true internal audit function on the one hand, and, on the other hand, the

integration of the internal control function in the Department of Internal Audit.

During the first months after its creation, in addition to the routine tasks, the Department was

committed to creating and approving the following instruments: Internal Regulation of the Audit

Function; Internal Audit Manual and the Multi-Year Plan of activities and Budget for the triennium

2017-2019.

The branches activities were monitored during the year by the auditors, in accordance with the

established routines, in which each auditor is responsible for monitoring a group of branches. Another

very important task was the investigation of customer complaints, taking into account the importance

of providing a quality service to customers and the timely detection of any nonconformities. However,

the main focus, especially in the last 4 months of the year, was the audit actions carried out, a total of

51, of which 12 were branches and 39 were cases. In this sense, we highlight the auditing of the Bank's

information systems started in the last quarter of the year, using specialized external auditing. Some

process audit actions only end in the first two months of 2018.

The Internal Control Office monitored and supported the different areas in the resolution of the

deficiencies identified in the scope of the review of the Internal Control System carried out in 2016 and

2017 and also in the resolution of the deficiencies identified by the internal auditors and Fiscal Board.

9.3. MARKETING AND PUBLIC RELATIONS

In 2017, the focus was strengthened on the transversal and integrated offer of products, services and

channels, along with social responsibility and the management of customer complaints, with a positive

impact on the brand and contributing to the consolidation of BCA's market positioning.

Communication

Institutional Campaign

At the beginning of the year an institutional campaign was launched in response to the strategic

guidelines for strengthening BCA’s brand positioning, focusing on distribution channels. This campaign

focused on the valuation of the Bank's differentials presented several situations of real life experience

37

and its interconnection with the Bank as a channel available in several dimensions, and it was casted

by employees.

The signature of the “Kel Ke di Nôs Nu ta da Valor” campaign,

which was also the motto for the jingle, sought to express the

values that BCA gives to the people who have made and will be

part of this Bank. A Bank that has always in mind to think about

what people need, seeking to align their needs to the new times.

Throughout the year 2017 BCA organized and participated (when

promoted by the City Councils) in meetings with the Emigrants on

vacation in Cabo Verde. In these meetings, BCA focused on the

various channels available for interaction with the customer

residing abroad, as well as the advantages of having their data

updated in the Bank's Database and the delivery of proof of

emigrant status to obtain the tax benefits that the State of Cabo Verde grants this segment.

Products Campaign

Still in the scope of the reinforcement of the communication and

with the purpose of assisting the commercial network to meet the

commercial goals, actions were developed associated with

strategic products, namely:

Home Loan, with the objective of making the product more

competitive and adequate to the current situation, the offer was

reformulated for the residents in the country, creating special

price differential conditions aimed at different customer needs,

namely for the acquisition of houses, associated with a

communication and ad campaign, called "BCA Nos Kasa", present

in different social media and in the Bank's internal channels.

In addition to maintaining the Loans linked to protocols with several Commercial Stores, from the

islands of Santiago, São Vicente and Sal, BCA deepened the relational strategy by promoting flexible

access to Consumer Loan, adapting it according to the employment relationship and professional

profile of the customer.

2017 Annual Report

38

The Credit Line for Small and Medium Enterprises was reinforced by

more than 2 Billion CVE, totaling 5 billion escudos, made available on

preferential terms since 2014, and the "5 Billion CVE for SMEs"

Campaign was launched, with a view to publicizing not only the

strengthening of the Line of credit, but also the lowering of the

interest rate of the product.

Financing to support economic and social development was

available, within the scope of microcredit, based on agreements

established directly with several Associations. In addition, BCA

strengthened its participation in the initiatives of public entities

aimed at boosting microcredit financing through the signing of a Protocol with the Ministério das

Finanças and the Associação Profissional das Instituições de micro-finanças de Cabo Verde (APIMF) -

CV).

Claims Management

BCA continually strives to provide its customers with quality services based on high ethical standards,

facing all complaints presented as an opportunity to continuously improve the quality of service and

deepen customer relations.

In 2017, there was a decrease in the total number of complaints processes, 21% compared to the

number received in 2016, which contributed to improvements in some of the complaints filed in 2016.

Regarding the deadline for reply, it should be noted that 78% of the new complaints were answered

within 10 working days or less.

Given the quality, transparency and rigor that BCA prints in the commercialization of its products and

services, throughout the year, awareness raising actions and proposals to improve processes, aimed at

eliminating, from the root, the causes of the complaints presented.

Social Responsibility

Campaign "Less Alcohol More Life"

BCA signed a protocol with the Coordination Commission of the Campaign "Less Alcohol More Life",

assuming, for three years (2017-2019), the sponsorship of said campaign. The Campaign "Less Alcohol

More Life" - promoted by a Commission formed by the Presidency of the Republic, Ministry of Health

39

and Social Security, Ministry of Education, Family and Social Inclusion and the World Health

Organization - aims to prevent and reduce abusive use of alcoholic beverages through actions that

provide behavioral changes.

Fundação Cabo-verdiana de Ação Social Escolar - FICASE

The "School Kit Distribution Campaign 2017", which has been endorsed by BCA for 8 years, and which

extends throughout the country, made it possible to provide 15,250 Kits to students in need from the

1st to the 6th grades, benefiting, thus, thousands of Cabo Verdean families.

4th World Forum of Local Economic Development

This event which was supported by BCA and brought together, in Cabo Verde, national and foreign

experts. It counted with the participation of about two thousand participants, from high entities to

students, national and foreign. This Forum is part of an ongoing process to facilitate dialogue and

promote exchanges on Local Economic Development with a view to combating rising inequalities and

achieving more equitable and sustainable development for all.

Festa das Bandeiras, São João Feast, Carnival and Tabanca

Festa das Bandeiras of São Filipe on the island of Fogo, the Festivities of São João in Porto Novo, the

Carnival and Tabanca which are cultural manifestations present in several islands of Cabo Verde and

are part of the cultural heritage of the country, had the support of BCA. These festivities count on the

participation of thousands of citizens who include the Cabo Verdean emigrants residing in the diaspora,

many of them BCA Customers.

Sponsorship

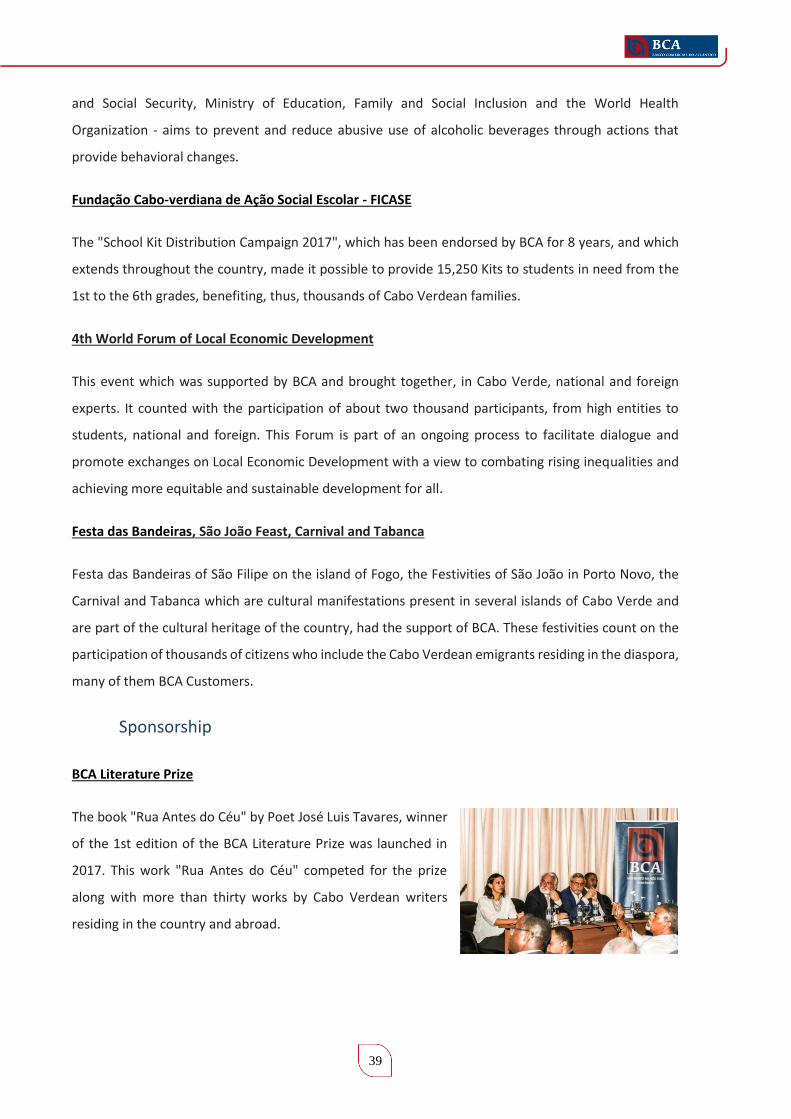

BCA Literature Prize

The book "Rua Antes do Céu" by Poet José Luis Tavares, winner

of the 1st edition of the BCA Literature Prize was launched in

2017. This work "Rua Antes do Céu" competed for the prize

along with more than thirty works by Cabo Verdean writers

residing in the country and abroad.

2017 Annual Report

40

The BCA Literature Prize - which as of 2017 changed the name to Corsino Fortes Prize - was created

under a partnership between the BCA and the Academia Cabo-verdiana de Letras (ACL), and aims to

award an unpublished work of a Cabo Verdean author in the field of literature.

Also, within the scope of this partnership, was launched in 2017, the project " Reedição de Livros de

Autores Cabo-Verdianos Consagrados " sponsored by BCA, with the reprint of the work "Antologia de

Ficção Cabo-verdiana Vol. I Pré-Claridosos" by Arnaldo França.

Atlantic Music Expo – AME

The 5th edition of the Atlantic Music Expo, an initiative of the

Ministry of Culture and Creative Industries, which has BCA as

Bronze Sponsor - had dozens of concerts with free access to

the population, conferences, showcases and a hundred music

professionals who gathered during the three days of the event

with the objective of exposing their products and reflecting on their area of activity.

With this partnership, which has lasted for four years, the BCA brand has increased its reputation

among its target audience and has strengthened the promotion of the economic and cultural dynamics

of Cabo Verde and its music in the world.

9.4. OTHER SUPPORTING ACTIVITIES

In 2017, BCA continued to focus on improving the quality of customer service, reinforcing alternative

means to the branch to obtain information and make payments and other banking operations.

With regard to strengthening the external image of the Bank and improving the working conditions of

employees, some works have been completed to improve branches. In addition, the conditions were

established in terms of installation and furniture, to start the important projects of Centralization and

Digitalization of the Archive. BCA is now able to scan and sort about 12,000 documents per day, with

scanning aligned with processes. The great challenge is not only to recover the history, but to reduce

the very production of the documents at their origin.

Aligned with one of the strategic vectors of BCA, cost containment, the information systems area

simplified the technology used through MPLS (Multiprotocol Label Switching), with unmistakable

operational gains and financial savings in the order of 25 %, without neglecting security.

41

During 2017, some correspondents requested the termination of relations with the Bank, based mainly

on their policy of discontinuing their presence in Africa and also the high cost of maintaining the

accounts.

In order to respond to this situation, operations were diverted to other correspondents, in particular

CGD (Caixa Geral de Depósitos) and BofA (Bank of America), seeking to avoid compromising the quality

of service provided to customers.

The year ended with a network of 21 correspondents covering 17 countries and multiple operations in

different currencies (USD, EUR, EUR, CHF, CAD, DKK, SEK, NOK, JPY, ZAR and CNY).

In January 2017 a new Organic Unit was implemented: the Research and Analysis Office. The main

objective of this new structure is to deepen the knowledge of BCA and its relationship with the external

environment, producing information to assist in the definition of strategies and decision making. It also

has as an attribution to increase the culture of knowledge sharing in BCA and to stimulate the

organizational communication, to promote the commitment of the employees in the pursuit of the

goals defined for each period.

In this sense, in addition to completing the bureaucratic aspects of the installation process, the new

unit produced a set of new reports to follow the contextual and transactional environment of BCA and

introduced improvements in the quality of information from other existing analyzes.

In terms of communication, among the presentations made to diversified audience, it is worth

mentioning the dissemination and analysis of BCA's accounts, which sought to cover employees from

all the islands and had an enthusiastic adherence of more than half of the total number of active

employees of the Bank.

2017 Annual Report

42

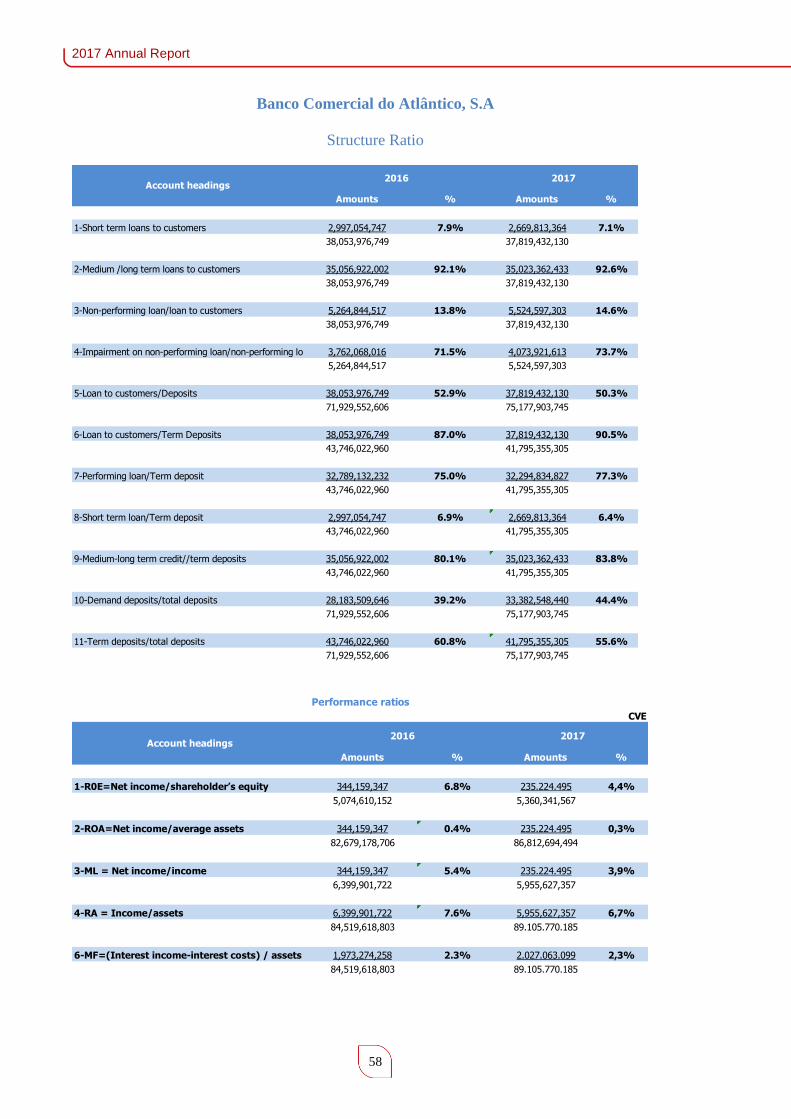

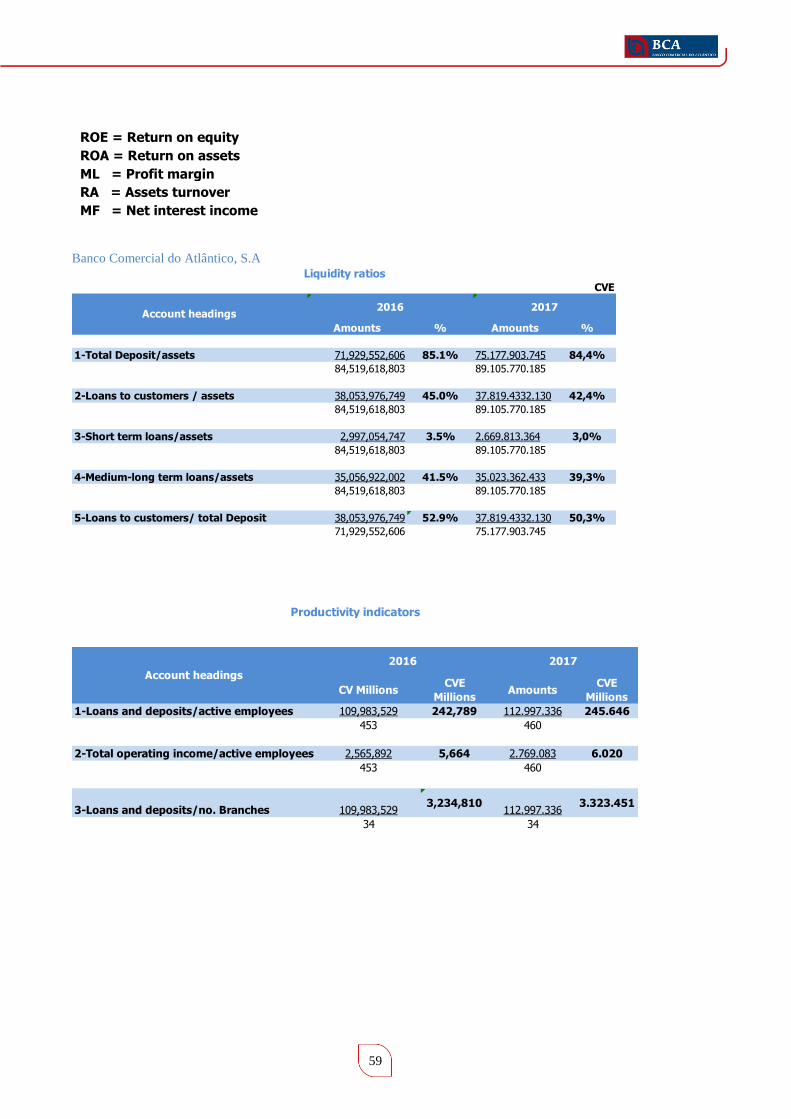

10. ANALYSIS OF ECONOMIC-FINANCIAL SITUATION

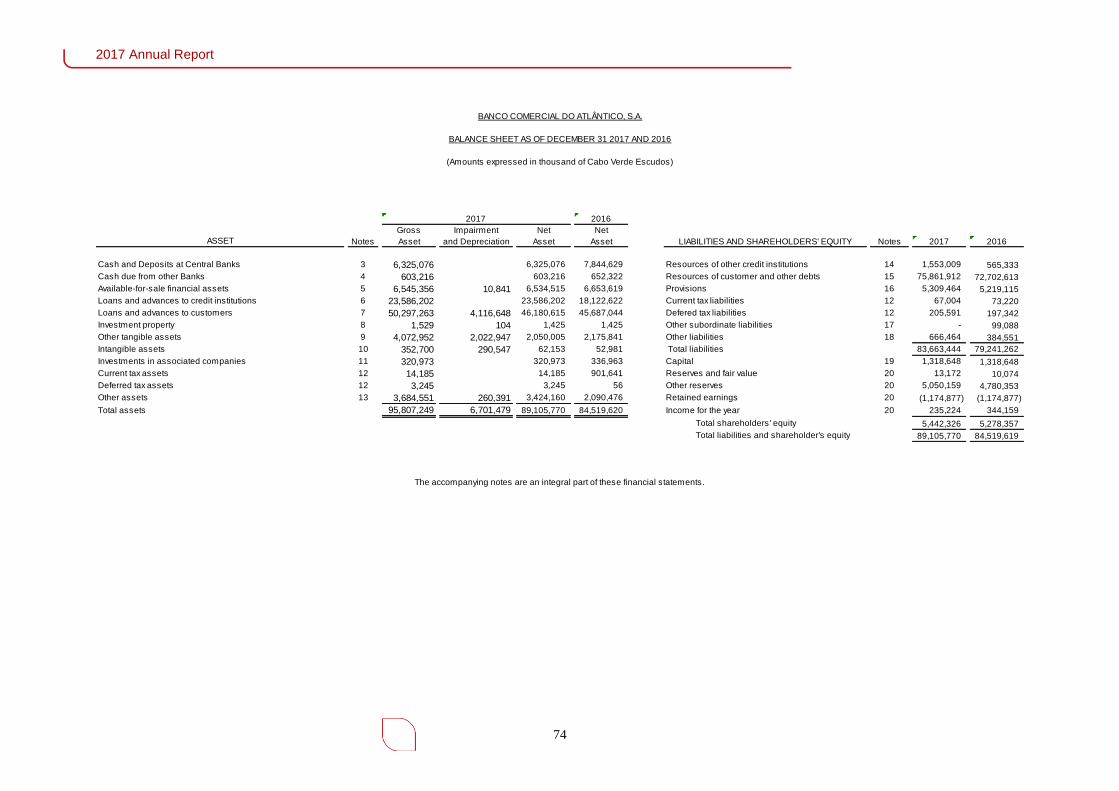

10.1. BALANCE SHEET

In December 2017, BCA's net assets reached 89 billion CVE, an increase of 5.4% (+4.6 billion CVE) in

relation to the value recorded in December 2016. This evolution was contributed by an increase of

30.1% (+5.5 billion CVE) under the caption Investments in Credit Institutions and Other Assets by 63.7%

(+1.3 billion CVE), this latter due to the credit recognized by the State related to the tax impact and

previously recorded under the caption Current Assets.

43

Loans and Advances to Customers

The Global Loans Portfolio, net of impairments, amounted to 46.1 billion CVE, higher than the balance

registered in December 2016 at 1% and about 494 million CVE, reflecting some recovery, especially in

the last quarter of 2017. This growth was contributed by the Cabo Verdean Public Debt Securities

Portfolio, which grew 13.8% in 2017 and recorded a cumulative balance of 9 billion CVE, corresponding

to 10.1% of BCA's net assets.

Absolute Relative

Asset

Cash and Deposits at Central Banks 7,845 6,325 -1,520 -19.4%

Balances due from other Banks 652 603 -49 -7.5%

Available-for-sale Financial Assets 6,654 6,535 -119 -1.8%

Loans and advances to Credit Institutions 18,123 23,586 5,463 30.1%

Loans and advances to Customers 45,687 46,181 494 1.1%

Other Tangible net Assets 2,176 2,050 -126 -5.8%

Intangible Assets 53 62 9 17.0%

Investment Proprieties 1 1 0 0.0%

Investments in associated companies 337 321 -16 -4.7%

Current tax Assets 902 14 -888 -98.4%

Deferred tax Assets 3 3 100.0%

Other Assets 2,090 3,425 1,335 63.9%

Total Assets 84,520 89,106 4,586 5.4%

Liabilities

Resources of Other Credit Institutions 565 1,553 988 174.9%

Resources of customers and other debts 72,703 75,862 3,159 4.3%

Provisions 5,219 5,309 90 1.7%

Current tax liabilities 73 67 -6 -8.2%

Deferred tax liabilit ies 197 206 9 4.6%

Subordinated liabilities 99 -99 -100.0%

Other Liabilities 385 666 281 73.0%

Total liability 79,241 83,663 4,422 5.6%

SHAREHOLDERS' EQUITY 5,278 5,442 164 3.1%

of which : Net Income 344 235 -109 -31.7%

TOTAL 84,520 89,106 4,586 5.4%

Consolidated Balance Sheet

(CVE Millions)

2016 2017Change

2017 Annual Report

44

The accumulated balance of the Loan Impairment, which includes impairment on the bonds of private

companies, reached 4.1 billion CVE and represented a coverage rate of 74.51%.

Securities Portfolio

The balance of the Securities Investments portfolio, which includes the Available-for-Sale Securities,

namely the Consolidated Financial Mobilization Securities, and the share in Promotora and in the

companies not supervised by BCV - Sociedade Cabo-verdiana de Tabacos, Sita, Fundo Gari and Visa,

totaled 6.5 billion CVE. The investments in consolidated financial mobilization securities, in the amount

of 6.4 billion CVE, represented 98.4% of this caption.

Customer’s Funds

The Customer Funds portfolio, including deposits from financial institutions, showed a year-on-year

growth of 5.7% and 4.2 billion, reflecting the preference of its broad and stable customer base, reaching

a cumulative balance of 77.4 billion CVE. The weight of Customer Funds in the bank's net assets in

December 2017 was 88.4%, compared to 86% in 2016.

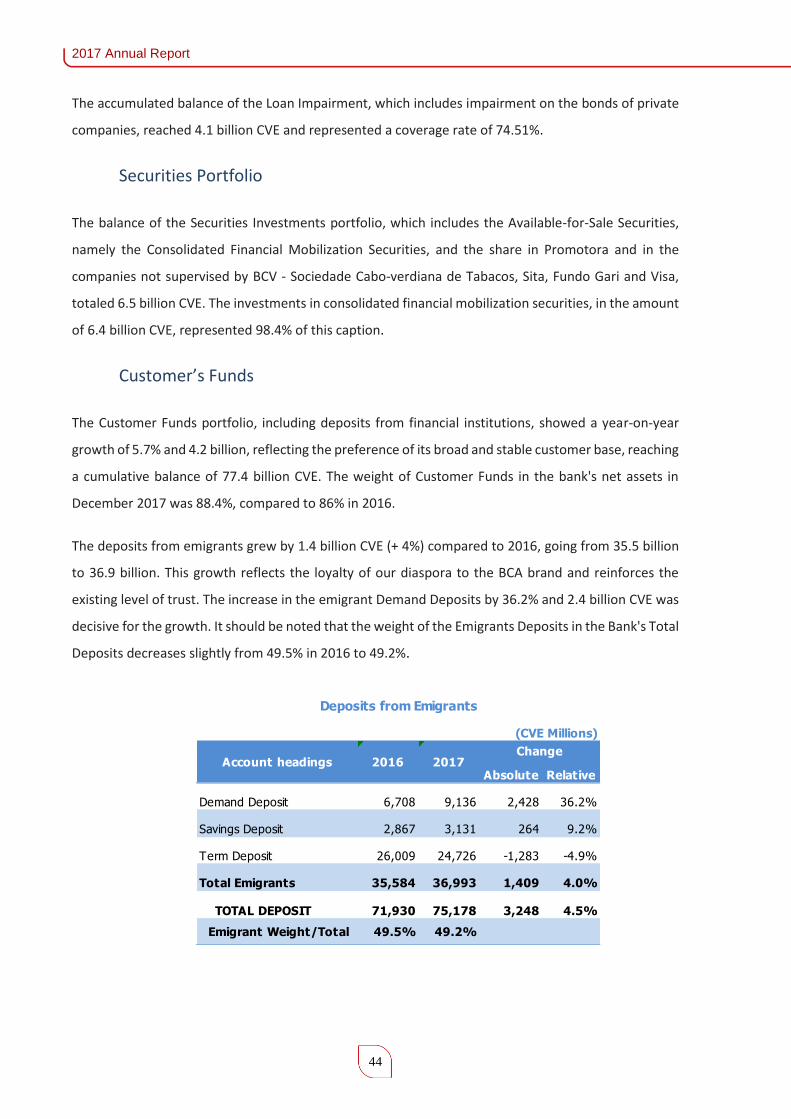

The deposits from emigrants grew by 1.4 billion CVE (+ 4%) compared to 2016, going from 35.5 billion

to 36.9 billion. This growth reflects the loyalty of our diaspora to the BCA brand and reinforces the

existing level of trust. The increase in the emigrant Demand Deposits by 36.2% and 2.4 billion CVE was

decisive for the growth. It should be noted that the weight of the Emigrants Deposits in the Bank's Total

Deposits decreases slightly from 49.5% in 2016 to 49.2%.

Absolute Relative

Demand Deposit 6,708 9,136 2,428 36.2%

Savings Deposit 2,867 3,131 264 9.2%

Term Deposit 26,009 24,726 -1,283 -4.9%

Total Emigrants 35,584 36,993 1,409 4.0%

TOTAL DEPOSIT 71,930 75,178 3,248 4.5%

Emigrant Weight/Total 49.5% 49.2%

Account headings 2016 2017Change

Deposits from Emigrants

(CVE Millions)

45

Provision for Risks and Costs

The Provision for Costs with the Retirement and Survival Pension Fund reached a total of 5 billion CVE

(4.9 billion CVE in 2016), + 108 million CVE.

The normal contribution of the workers and BCA to the Costs for Retirement and Survival Pensions

amounts to 46.6 million, of which 17.2 million of the employees 29.3 million of the bank. The uses for

payment to the retired and pre-retired totaled 220.1 million. It should be noted that the costs borne

by the bank, which include the normal costs and those related to interest costs and current service

costs, for the Pension and Survival Fund reached 290 million, with a direct impact on personnel costs.

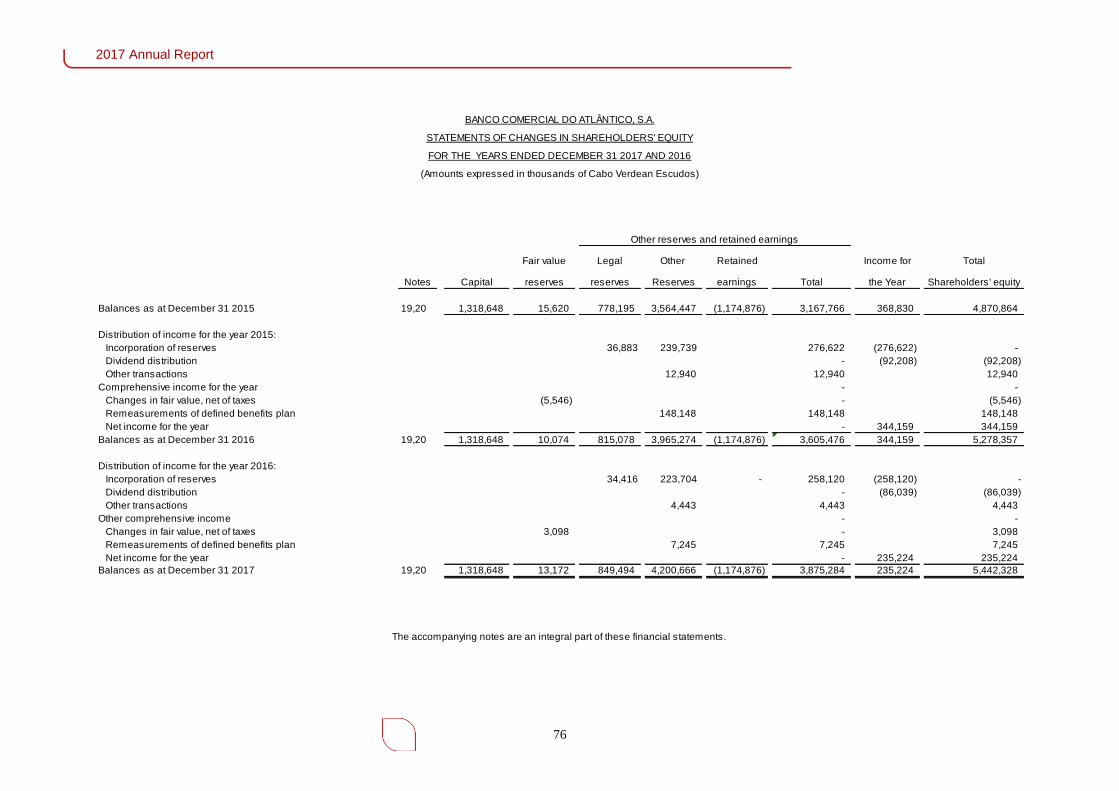

Shareholders’ Equity

The Bank's shareholders’ equity increased by 3.1% and 164 million in 2017, as a result of the combined

effect of the incorporation in reserves of 75% of the Net Profit of 2016.

2017 Annual Report

46

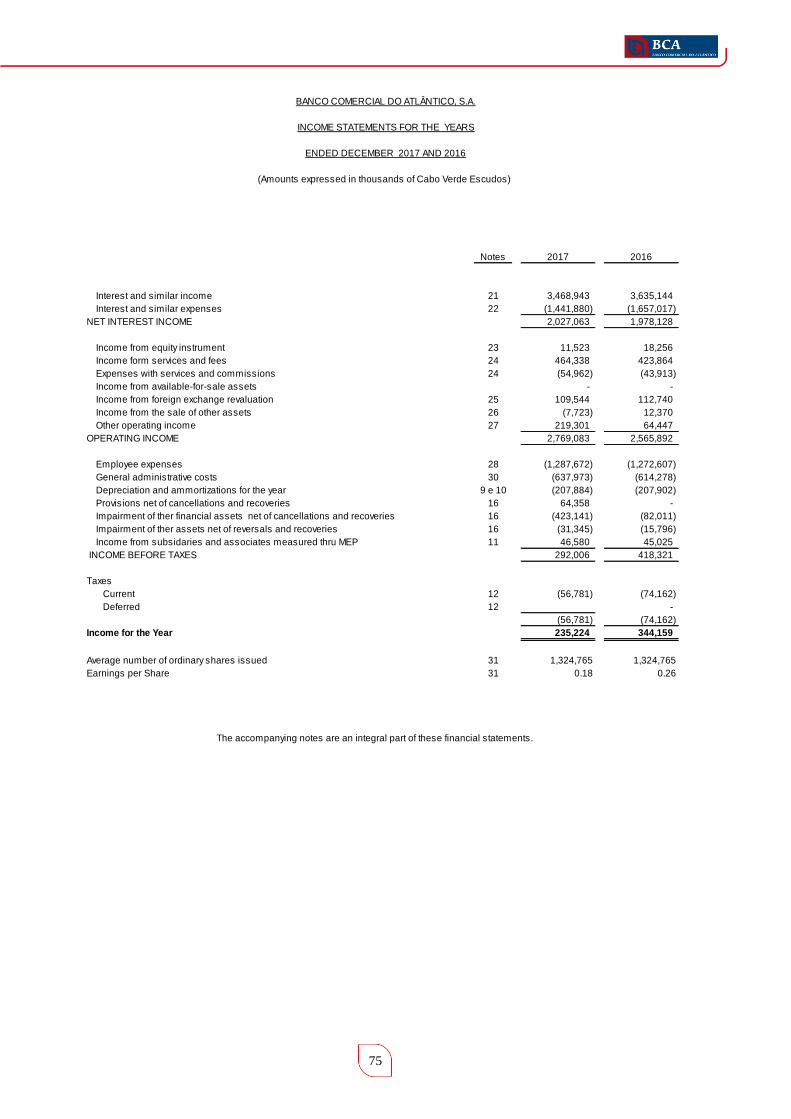

10.2. INCOME STATEMENT

Net Income

BCA recorded a negative variation of 31.7%, about 109 million CVE, reaching 235 million CVE, negatively

justified by the increase in impairment/provisions of 298.9% and about 292.3 million CVE and by

operating costs 1.8% and 39 million CVE. On the positive side, the variation in total operating income

was 7.9% and 203 million CVE, despite the continuous decrease in the rate of return on investments in

Consolidated Financial Mobilization Securities of only 0.17%. The evolution of the net income for the

last four years is shown below.

(CVE Millions)

Absolute Relative

Interest and similar income 3,635 3,469 (166) -4.6%

Interest and similar expenses 1,657 1,442 (215) -13.0%

Net interest income 1,978 2,027 49 2.5%

Income from equity instruments 18 12 (6) -33.3%

Income from services and commissions 424 464 40 9.4%

Costs of services and commissions 44 55 11 25.0%

Income from foreign exchange revaluations 113 110 (3) -2.7%

Income from disposals of other assets 12 (8) (20) -166.7%

Other operating income 64 219 155 242.2%

Net Interest Income 588 742 154 26.2%

Operating Income 2,566 2,769 203 7.9%

Employees Costs 1,273 1,288 15 1.2%

General Administractive Costs 614 638 24 3.9%

Depreciation for period 208 208 - 0.0%

Operating Costs 2,095 2,134 39 1.9%

Impairment of other assets net of reversals and recoveries - (64) (64) 100.0%

Net Impairment form Other Financial Assets 98 454 356 363.3%

Income from subsidiaries exc. from consolidation 45 47 2 3.5%