2016 technology industry report

TRANSCRIPT

Risk. Reinsurance. Human Resources.

U.S. Technology & Communications Industry ReportPowered by Aon GRIPSM, February 2016

Aon Risk Solutions

2 Technology and Communications Industry Report

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

Top 10 Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Risk Preparedness for the Top 10 Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Losses Associated with Top 10 Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Projected 2018 Top Five Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Identifying, Assessing, Measuring and Managing Risks . . . . . . . .10

Identifying & Assessing Major Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Risk Maturity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Risk Management Department and Function . . . . . . . . . . . . . . .15

Chief Risk Officer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Risk Management Department . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

External Drivers Strengthening Risk Management . . . . . . . . . . . . . . . . . . 18

Risk Management Budget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Risk Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

Retentions/Deductibles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Limits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Cyber Risk Coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Multinational Programs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Captives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

Market Insights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Priorities in Choice of Insurer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Desired Market Changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Carrier/Marketplace Participation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Common Carrier Win Reasons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Common Reasons for Carriers Not Quoting . . . . . . . . . . . . . . . . . . . . . . . 34

Common Reasons for Rejecting a Carrier’s Quote . . . . . . . . . . . . . . . . . . 35

Key Carriers Financials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Financial Insights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36

Key Contacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

Table of Contents

Introduction

In today’s global environment, technology and communications companies are facing increasingly complex challenges: weak and uneven global economic recovery, evolving regulatory and industry standards, frequent new product introductions, and large-scale network security breaches, all of which could potentially affect corporate profitability and, for some, survival . The stakes for the sector are high . With increased scrutiny on operating efficiencies and a need to constantly innovate to meet mercurial consumer tastes and demands, it is critical to access accurate and timely information, and proactively address risk at every level of the organization .

At Aon, our 72,000 colleagues in over 120 countries handle more risk and people issues on a daily basis than any company in the world . As the leading provider of risk and human capital solutions, we have an appreciation for the challenges these issues create and the opportunities that can be unlocked if they are identified and addressed .

We believe in the power of data and analytics to provide insight in this era of greater complexity and are committed to leveraging our unmatched global network to provide leading organizations with business intelligence .

Aon’s 2015 Technology and Communications Industry Report provides comprehensive, industry specific data on key issues and concerns . These findings allow organizations to benchmark their risk management and risk financing practices against those of their peers and help identify practices or approaches that may improve the effectiveness of their own risk management strategies .

If you have any comments or questions about the survey, or wish to discuss the findings further, please contact your Aon account executive .

Best regards,

Eric BoyumNational Practice Leader – Technology PracticeAon Risk Solutionseric .boyum@aon .com 1 .303 .639 .4120

2 Technology and Communications Industry Report

In the age of information overload, the technology and

communications industry is facing a barrage of data about

their customers, but many are struggling to make sense of the

information, and figure out how to capitalize on it . Aon aims to

bridge this gap . It is Aon’s belief that information and analytics

will be the way to complement and supplement the knowledge

base of our clients, enabling them to understand the risks and

succeed .

As part of our efforts to help companies stay abreast of emerging

issues and learn what their peers are doing to manage risks and

capture opportunities, we have compiled this report, which

is based on Aon’s 2015 Global Risk Management Survey and

contains some detailed facts and analyses on the technology and

communications sectors . Topics in the report include:

• Current and projected top risks

• Risk readiness and losses

• Techniques utilized to identifying and assessing major risks

• Organizational risk maturity

• Risk management department and function

• Risk financing

• Cyber risk coverage

• Multinational programs

• Captives

• Market insights

• Financial insights

Executive Summary

Key Findings

Topic Key Finding

Top 10 risks

Increasing competition is ranked as the most challenging risk for the technology and communications sectors . Second on the list is damage to reputation/brand, followed by failure to innovate and meet customer needs . Given the recent high-profile cyber attacks, it is not surprising that computer crime/ hacking /viruses /malicious codes has jumped in ranking, from number eight in Aon’s 2013 survey to number five this year .

Risk preparedness for the top 10 risks

In comparison with that of 2013, overall readiness for the top 10 risks has decreased slightly by two percent to 65 percent . Preparedness for two closely inter-related risks - business interruption, and computer crime/hacking/viruses/malicious codes and technology /system failure have experienced the greatest percentage changes, jumping from 73 percent in 2013 to 92 percent in 2015, and from 72 percent to 92 percent respectively . Economic slowdown has seen the largest decrease in readiness, from 63 percent to 26 percent .

Losses associated with top 10 risks

On average, reported loss of income from the top 10 risks has decreased from 49 percent in 2013 to 24 percent in 2015 . Increasing competition and technology/system failure top the list of income losses related to the most cited risks in the past 12 months, at 56 percent and 42 percent respectively . The reduction in losses can also be attributed to the fact that corporate leadership is taking a more proactive role in managing risks .

Projected 2018 top five risksThe ranking for the top five risk concerns in the next three years remains the same as this year’s - increasing competition, damage to reputation/brand, failure to innovate/meet customer needs, failure to attract and retain top talents, and computer crime/hacking/viruses/malicious codes .

Identifying and assessing major risks

Board and/or management discussion of risk during annual planning, risk assessment or other processes is cited as the method most often used by surveyed organizations to identify major risks facing their organizations (67 percent), and senior management judgment and experience the most cited for assessing major risks at 57 percent .

Risk maturity

The Aon Risk Maturity Index (RMI) includes a variety of questions concerning risk management practices, corporate governance and management decision processes . Overall, an organization can rate at a maturity level ranging from initial (“1”) to advanced (“5”) . The technology industry sample set includes over 50 organizations to date, with an average risk maturity of a “2 .5” or “basic to defined .” This is in line with the current global average that represents all industries .

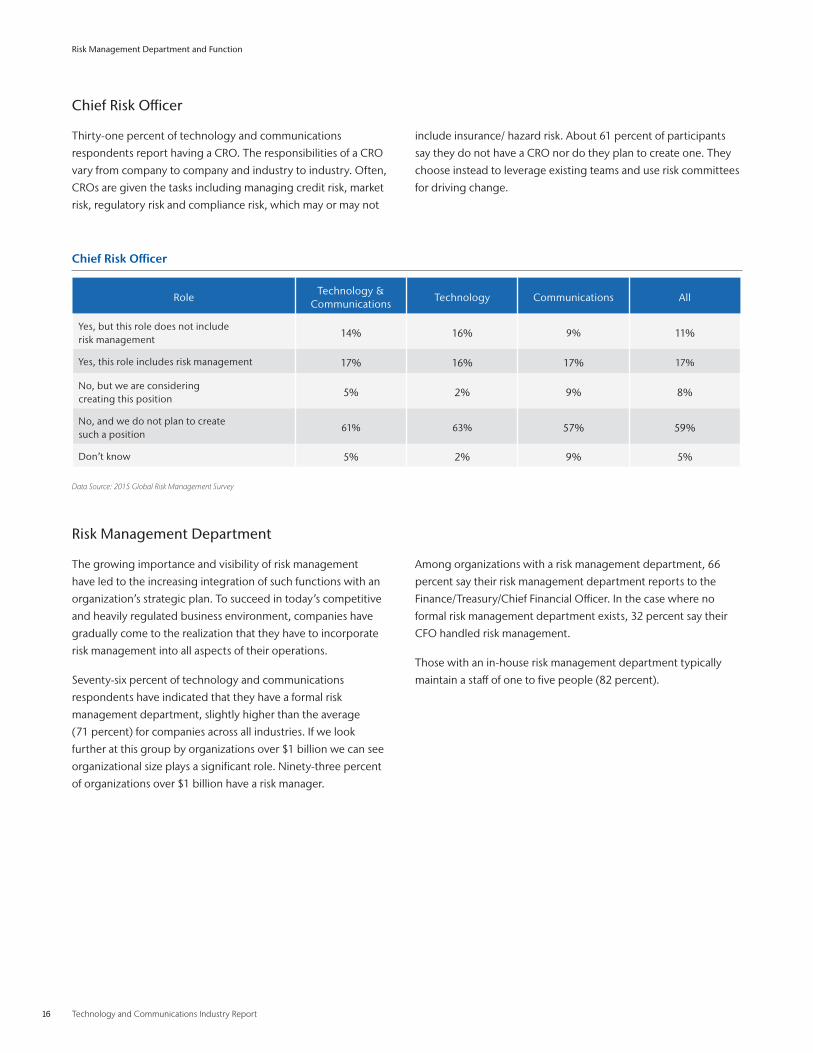

Chief Risk OfficerAbout 17 percent of technology and communications respondents report having a CRO whose duties include risk management .

Risk management departmentSeventy-six percent of technology and communications respondents have indicated that they have a formal risk management department . Ninety-three percent of organizations over $1 billion have a risk manager . Those with an in-house risk management department typically maintain a staff of one to five people .

Aon Risk Solutions 3

Key Findings

Topic Key Finding

External drivers strengthening risk management

Cyber threat environment (51 percent), pressure from customers (39 percent) and increased focus from regulators (31 percent) are the most important external drivers strengthening risk management for the technology and communications industry .

Risk management budgetForty-one percent of respondents say their risk management spend/resources over the next 12 months remains the same while 29 percent have indicated a marginal or significant planned increase .

Retentions/deductiblesThe majority of organizations have not changed their retentions from the prior policy period . Three lines have registered the most changes in retention levels: general liability (14 percent), director and officers liabilities (13 percent), and properties (12 percent) .

Limits

Technology and communications respondents say the most commonly purchased umbrella/excess liability limit stands at USD100 million and the average limit purchased for all surveyed companies totals USD113 million . Similar to umbrella/excess liability, directors’ and officers’ liability limits purchased by publicly traded technology and communications companies are in direct proportion to a company’s revenue size . The highest limit purchased stands at USD655 million, while the lowest limit purchased was USD1 million .

Cyber risk coverage

About 40 percent of respondents say their companies have purchased cyber insurance coverage, and 17 percent plan to purchase this coverage . Among companies that have purchased cyber insurance coverage, the majority feel that the terms and conditions, and the liability limits are sufficient and effective to manage their exposures (at 83 and 67 percent respectively) .

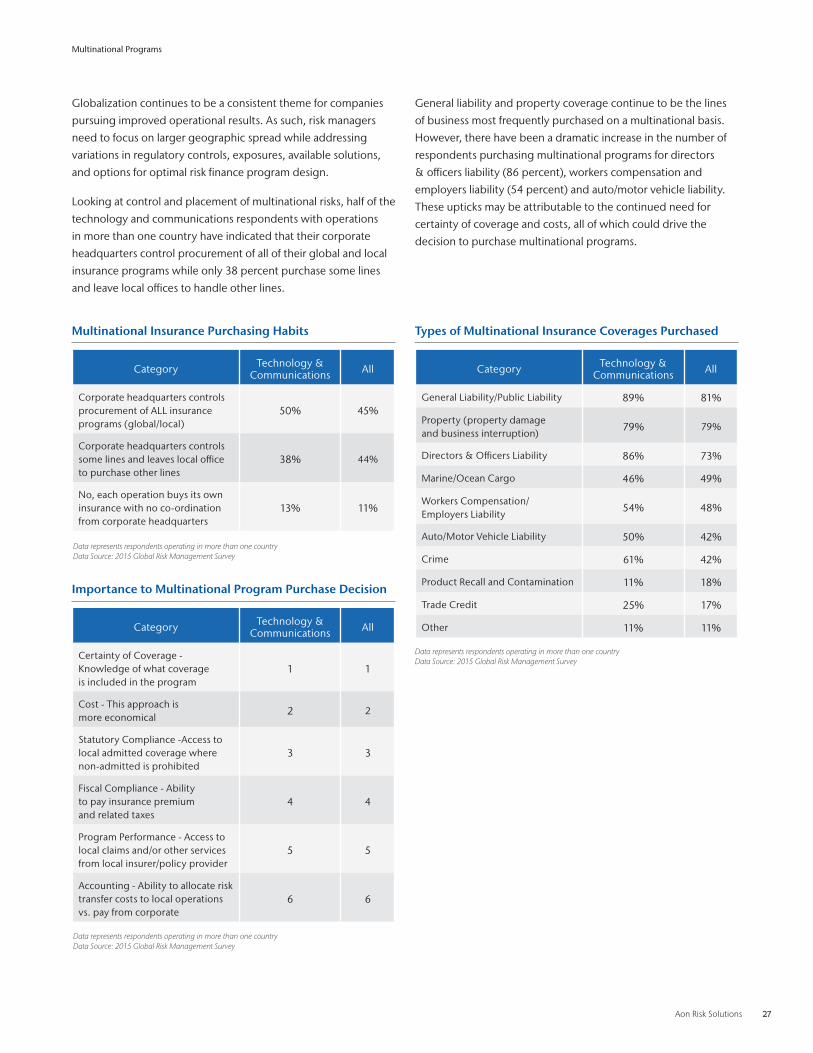

Multinational programs

In the survey, half of technology and communications respondents with operations in more than one country have indicated that their corporate headquarters control procurement of all of their global and local insurance programs while 38 percent say their corporate headquarters purchase some lines and leave local offices to handle . General liability, property, and directors and officers liability coverage continue to be the lines of business most frequently purchased on a multinational basis .

Captives

About 13 percent of technology and communications respondents have reported having an active captive or Protected Cell Company (PCC), with nine percent also indicating a plan to create a new or additional captive or PCC in the next three years . Product liability and completed operations, professional indemnity/Errors and Omissions and Property are the most frequently underwritten lines of coverage within a captive, all at 71 percent .

Priorities in choice of insurerAbility to execute and deliver risk finance support proximate to global locations is cited by technology and communications respondents as the top criterion in an organization’s choice of insurers, followed by coverage terms and conditions .

Desired market changesRespondents are looking for broader coverage/better terms and conditions, along with more flexibility in underwriting, coverage, pricing; and recognition of investments in internal risk management efforts through lower premiums .

Common carrier win reasons When it comes down to selecting a carrier, the most common win reason is incumbent relationship .

Common reasons forcarriers not quoting

The most common reasons for a carrier not providing a quote for casualty/liability, automobile liability, workers compensation, financial lines and property are: terms and conditions, underwriting concerns and pricing .

Common reasons forrejecting a carrier’s quote

The reason most often given by clients for rejecting a carrier’s quote is inferior pricing .

Financial insights

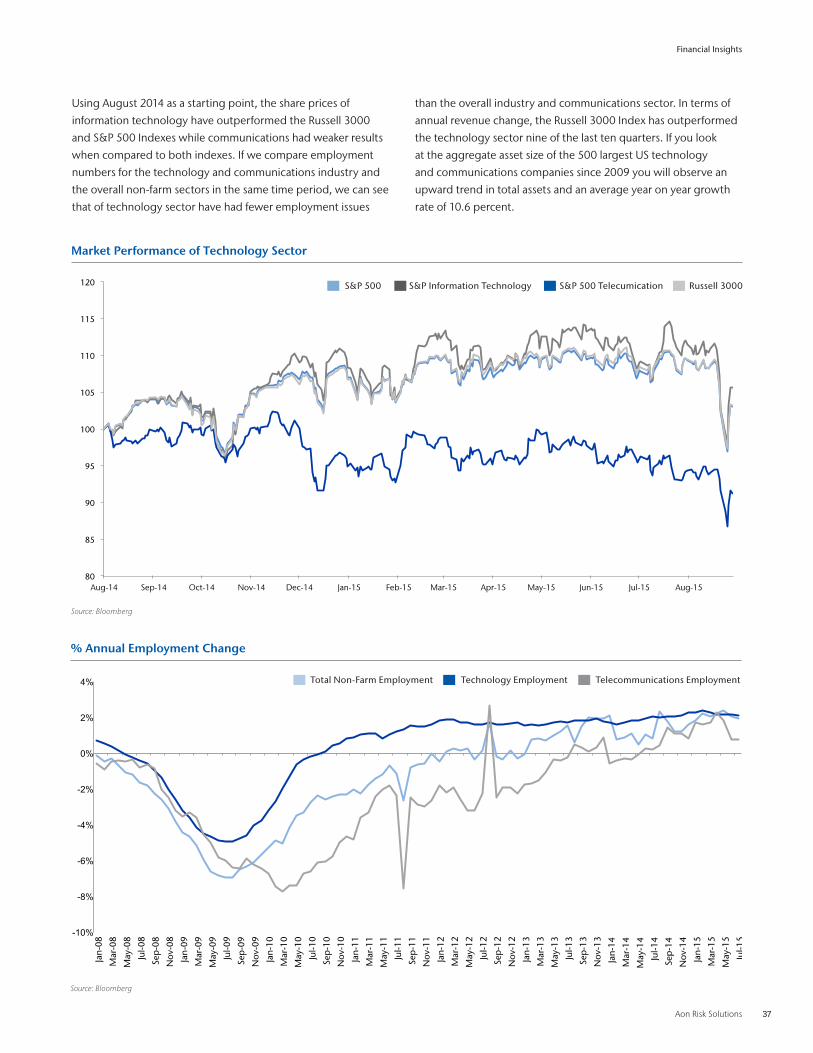

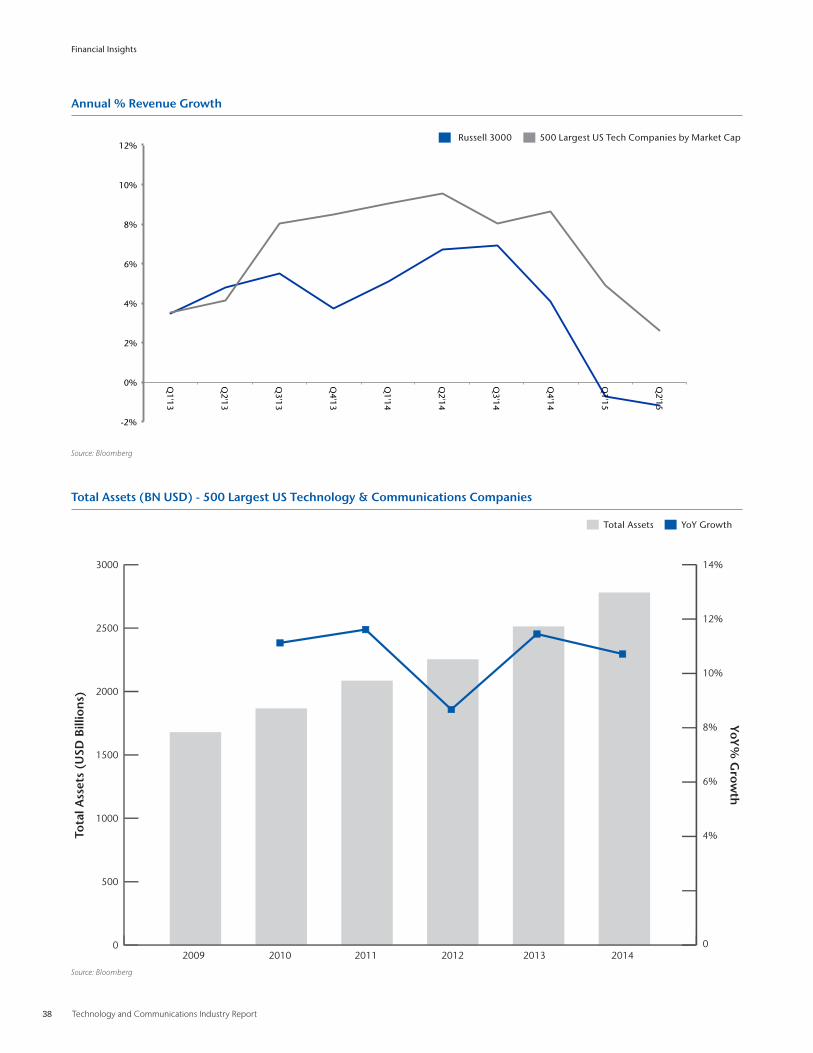

The share prices of information technology have outperformed the Russell 3000 and S&P 500 Indexes since August 2014 while telecommunication had weaker results when compared to both indexes . The technology sector has less employment issues than the overall industry and communications sector . In terms of annual revenue change, the Russell 3000 Index has outperformed the technology sector nine of the last ten quarters . If you look at the aggregate asset size of the 500 largest US technology and communications companies since 2009 you will observe an upward trend in total assets and an average year on year growth rate of 10 .6 percent .

4 Technology and Communications Industry Report

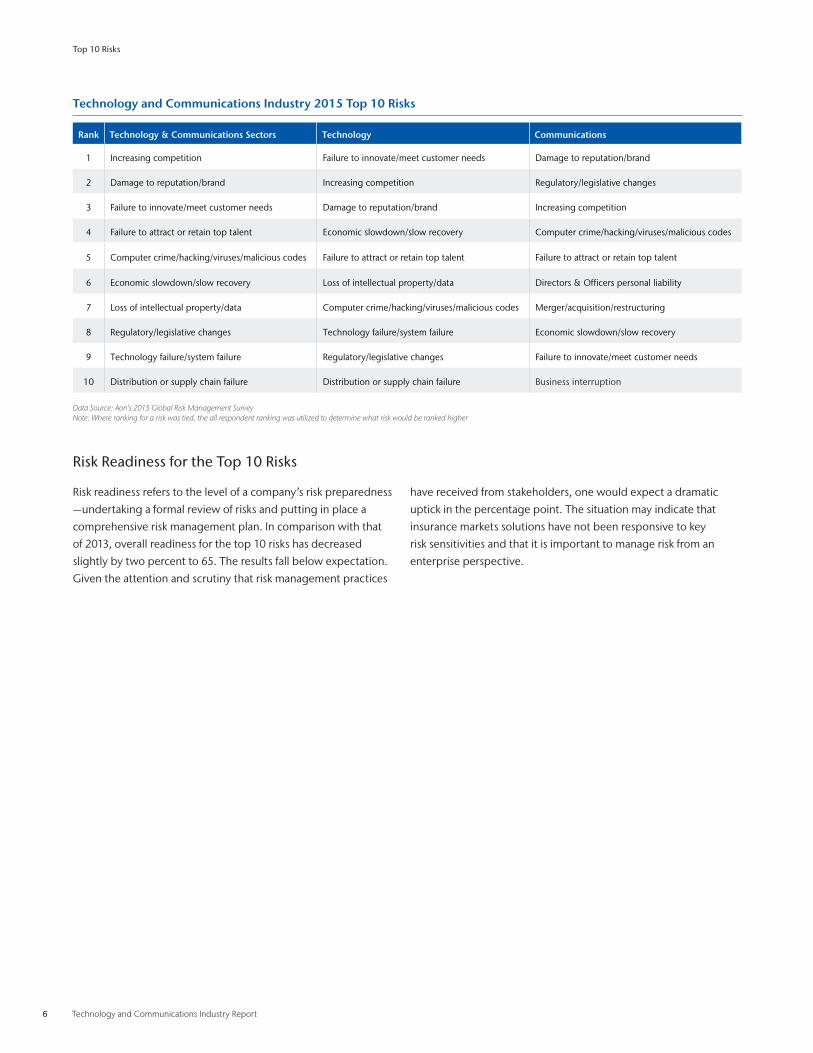

Top 10 Risks

Aon Risk Solutions 5

In Aon’s 2015 Global Risk Management Survey, respondents are

provided a list of 53 risks and asked to select 10 that they believe

to be the top risks facing their own industries and organizations .

Increasing competition is ranked by the technology and

communications sectors as the most challenging risk . Second

on the list is damage to reputation/brand, followed by failure to

innovate and meet customer needs .

Competition, central to the operation of markets, fosters

innovation, productivity and growth . At the same time,

increasing competition can also eat away a company’s market

share and end a business . Increasing competition presents an

acute risk for the technology and communications companies,

which face tougher anti-monopoly rules, competition from

foreign suppliers of basic communications services, rapidly

changing technology, fast-evolving regulatory and industry

standards, frequent new product introductions, and price and

cost reductions . While larger business organizations may be able

to fend off higher amounts of competition than smaller ones

with limited resources, all organizations, regardless of size, see

competition as a priority risk .

If we break down the technology and communications group

further to sub-categories, we’ll see that the communications

sector sees damage to reputation/brand as a number one risk .

This could be attributed to a long list of well-known companies,

which saw their reputation affected by unexpected incidents

–customer services snafus, privacy concerns, inappropriate

remarks or behavior by company executives and large-scale data

breaches . In an age of 24-hour news cycles and instant social

media, crisis could spread globally within hours or minutes .

As a result, reputation, which was categorized by experts as

“priceless” or “an intangible asset,” is becoming increasingly

“pricey,” exerting a direct impact on the company’s bottom line .

For the technology sector, where the lifetime of products

continues to shrink, the race to market has intensified and

consumer needs are fickle, failure to innovation/meet customer

needs pose as the number one risk .

When comparing with the ranking of various risks in the 2013

survey, we have noted that computer crime/ hacking/viruses /

malicious codes has jumped from number eight to number

five . New technologies such as cloud computing, social media,

mobile devices and big data analytics have helped companies

achieve profits and reach operational goals . However, these same

businesses face an increasingly diverse and sophisticated array of

threats to the security of their information management systems .

Each time the industry develops or adds a new feature to a

system, the chance of cyber risks rises .

Each year, the security industry strives to protect companies

with new potent tools, but a new crop of hackers emerges with

more damaging cyber attack techniques . At the same time,

users’ careless online behavior will continue to create exploitable

opportunities for hackers or directly result in security breaches .

As hackers and anti-hackers remain locked into a fierce arms race,

survey participants expect the risk to be a top risk concern three

years from now .

The Center for Strategic and International Studies, a well-known

Washington think tank, has estimated that the annual cost of

cyber crime and economic espionage to the world economy

runs as high as USD 445 billion—or almost one percent of global

income . The average time to resolve a cyber attack is also rising,

climbing to 45 days, up from 32 days in 2013 . As cyber crimes are

becoming more rampant, more costly, and more time consuming

to resolve, businesses are faced with an increased possibility of

legal exposure, reputation damage, and operational interruption

that can wreak havoc on their bottom line .

Similar to the prior survey, our study findings highlight the

interdependency among many of the top risks . For example, a

cyber attack causes disruption to business and IT operations and

a business disruption leads to damage to reputation/brand, which

will dent a business’s competitiveness, making it harder to attract

and maintain top talents . Lack of talents stunts a company’s

ability to stay competitive in a tough business environment . The

list goes on . This interdependency between risks illustrates that

organizations can no longer evaluate risk in isolation but must

consider their interconnectedness .

Top 10 Risks

6 Technology and Communications Industry Report

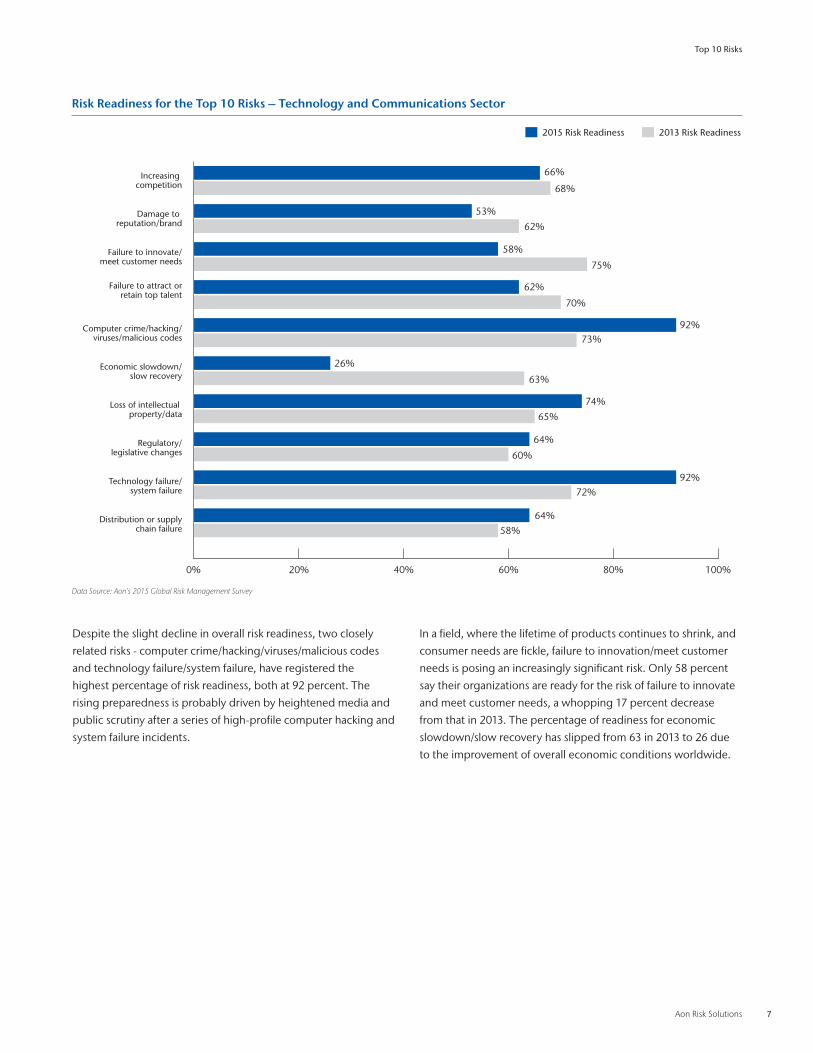

Risk Readiness for the Top 10 Risks

Risk readiness refers to the level of a company’s risk preparedness

—undertaking a formal review of risks and putting in place a

comprehensive risk management plan . In comparison with that

of 2013, overall readiness for the top 10 risks has decreased

slightly by two percent to 65 . The results fall below expectation .

Given the attention and scrutiny that risk management practices

have received from stakeholders, one would expect a dramatic

uptick in the percentage point . The situation may indicate that

insurance markets solutions have not been responsive to key

risk sensitivities and that it is important to manage risk from an

enterprise perspective .

Technology and Communications Industry 2015 Top 10 Risks

Rank Technology & Communications Sectors Technology Communications

1 Increasing competition Failure to innovate/meet customer needs Damage to reputation/brand

2 Damage to reputation/brand Increasing competition Regulatory/legislative changes

3 Failure to innovate/meet customer needs Damage to reputation/brand Increasing competition

4 Failure to attract or retain top talent Economic slowdown/slow recovery Computer crime/hacking/viruses/malicious codes

5 Computer crime/hacking/viruses/malicious codes Failure to attract or retain top talent Failure to attract or retain top talent

6 Economic slowdown/slow recovery Loss of intellectual property/data Directors & Officers personal liability

7 Loss of intellectual property/data Computer crime/hacking/viruses/malicious codes Merger/acquisition/restructuring

8 Regulatory/legislative changes Technology failure/system failure Economic slowdown/slow recovery

9 Technology failure/system failure Regulatory/legislative changes Failure to innovate/meet customer needs

10 Distribution or supply chain failure Distribution or supply chain failure Business interruption

Data Source: Aon’s 2015 Global Risk Management SurveyNote: Where ranking for a risk was tied, the all respondent ranking was utilized to determine what risk would be ranked higher

Top 10 Risks

Aon Risk Solutions 7

Risk Readiness for the Top 10 Risks – Technology and Communications Sector

2015 Risk Readiness 2013 Risk Readiness

68%

66%

62%

53%

63%

26%

70%

62%

60%

64%

72%92%

75%

58%

92%73%

65%

74%

58%64%

0% 20% 40% 60% 80% 100%

Distribution or supply chain failure

Technology failure/system failure

Regulatory/legislative changes

Loss of intellectual property/data

Economic slowdown/slow recovery

Computer crime/hacking/viruses/malicious codes

Failure to attract orretain top talent

Failure to innovate/meet customer needs

Damage to reputation/brand

Increasing competition

Despite the slight decline in overall risk readiness, two closely

related risks - computer crime/hacking/viruses/malicious codes

and technology failure/system failure, have registered the

highest percentage of risk readiness, both at 92 percent . The

rising preparedness is probably driven by heightened media and

public scrutiny after a series of high-profile computer hacking and

system failure incidents .

In a field, where the lifetime of products continues to shrink, and

consumer needs are fickle, failure to innovation/meet customer

needs is posing an increasingly significant risk . Only 58 percent

say their organizations are ready for the risk of failure to innovate

and meet customer needs, a whopping 17 percent decrease

from that in 2013 . The percentage of readiness for economic

slowdown/slow recovery has slipped from 63 in 2013 to 26 due

to the improvement of overall economic conditions worldwide .

Top 10 Risks

Data Source: Aon’s 2015 Global Risk Management Survey

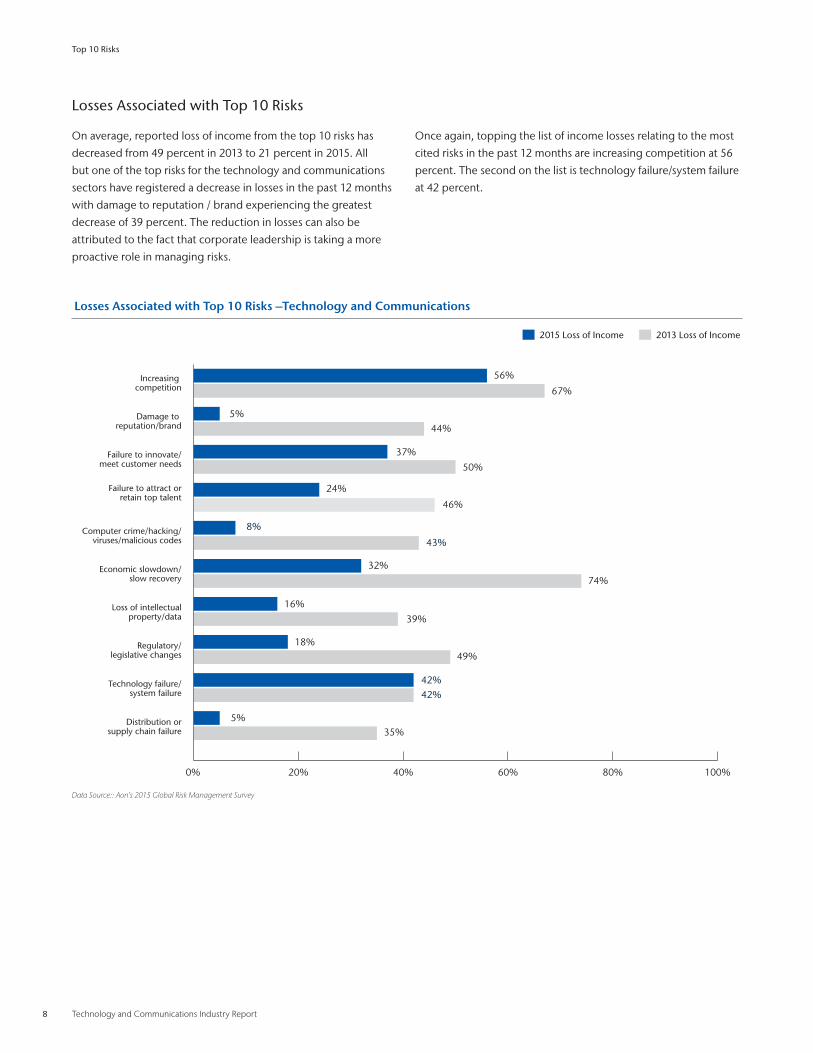

8 Technology and Communications Industry Report

Losses Associated with Top 10 Risks –Technology and Communications

Distribution orsupply chain failure

Technology failure/system failure

Regulatory/legislative changes

Loss of intellectualproperty/data

Economic slowdown/slow recovery

Computer crime/hacking/viruses/malicious codes

Failure to attract orretain top talent

Failure to innovate/meet customer needs

Damage to reputation/brand

Increasing competition

2015 Loss of Income 2013 Loss of Income

67%

56%

5%44%

32%

74%

46%

24%

49%18%

42%42%

50%37%

43%

8%

39%16%

35%5%

0% 20% 40% 60% 80% 100%

Losses Associated with Top 10 Risks

On average, reported loss of income from the top 10 risks has

decreased from 49 percent in 2013 to 21 percent in 2015 . All

but one of the top risks for the technology and communications

sectors have registered a decrease in losses in the past 12 months

with damage to reputation / brand experiencing the greatest

decrease of 39 percent . The reduction in losses can also be

attributed to the fact that corporate leadership is taking a more

proactive role in managing risks .

Once again, topping the list of income losses relating to the most

cited risks in the past 12 months are increasing competition at 56

percent . The second on the list is technology failure/system failure

at 42 percent .

Top 10 Risks

Data Source:: Aon’s 2015 Global Risk Management Survey

Aon Risk Solutions 9

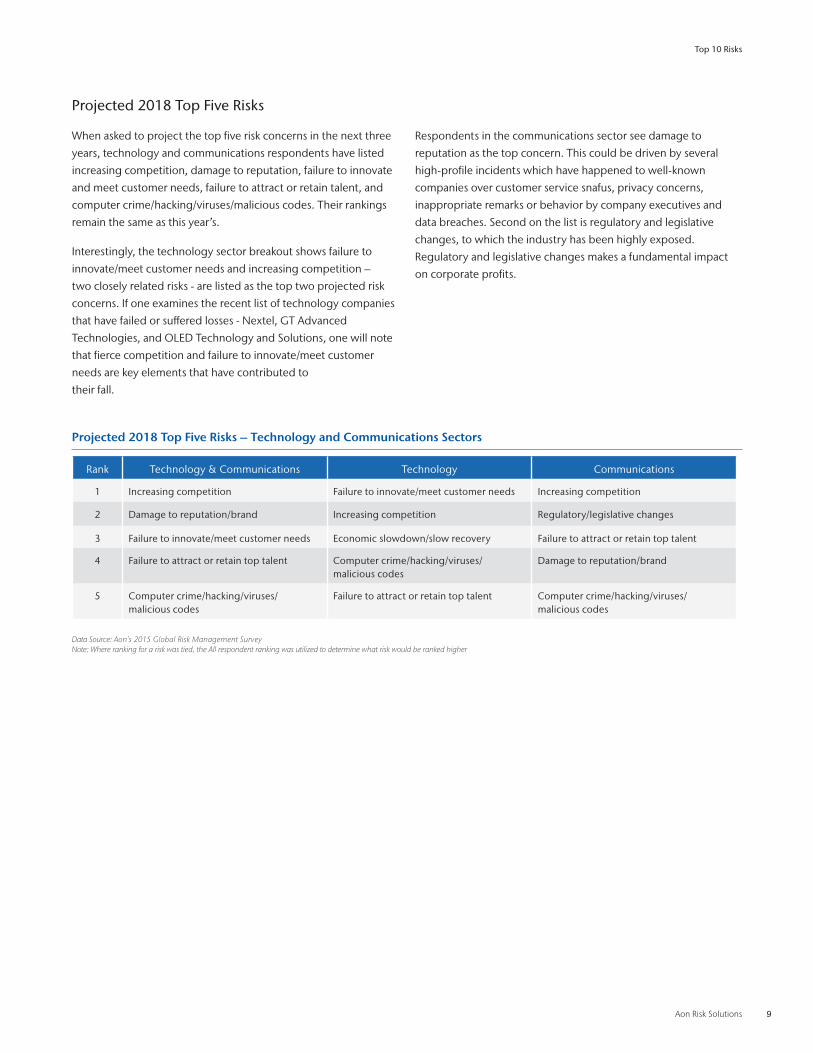

Projected 2018 Top Five Risks

When asked to project the top five risk concerns in the next three

years, technology and communications respondents have listed

increasing competition, damage to reputation, failure to innovate

and meet customer needs, failure to attract or retain talent, and

computer crime/hacking/viruses/malicious codes . Their rankings

remain the same as this year’s .

Interestingly, the technology sector breakout shows failure to

innovate/meet customer needs and increasing competition –

two closely related risks - are listed as the top two projected risk

concerns . If one examines the recent list of technology companies

that have failed or suffered losses - Nextel, GT Advanced

Technologies, and OLED Technology and Solutions, one will note

that fierce competition and failure to innovate/meet customer

needs are key elements that have contributed to

their fall .

Respondents in the communications sector see damage to

reputation as the top concern . This could be driven by several

high-profile incidents which have happened to well-known

companies over customer service snafus, privacy concerns,

inappropriate remarks or behavior by company executives and

data breaches . Second on the list is regulatory and legislative

changes, to which the industry has been highly exposed .

Regulatory and legislative changes makes a fundamental impact

on corporate profits .

Projected 2018 Top Five Risks – Technology and Communications Sectors

Rank Technology & Communications Technology Communications

1 Increasing competition Failure to innovate/meet customer needs Increasing competition

2 Damage to reputation/brand Increasing competition Regulatory/legislative changes

3 Failure to innovate/meet customer needs Economic slowdown/slow recovery Failure to attract or retain top talent

4 Failure to attract or retain top talent Computer crime/hacking/viruses/ malicious codes

Damage to reputation/brand

5 Computer crime/hacking/viruses/ malicious codes

Failure to attract or retain top talent Computer crime/hacking/viruses/ malicious codes

Data Source: Aon’s 2015 Global Risk Management SurveyNote: Where ranking for a risk was tied, the All respondent ranking was utilized to determine what risk would be ranked higher

Top 10 Risks

10 Technology and Communications Industry Report

Identifying, Assessing, Measuring and Managing Risk

Aon Risk Solutions 11

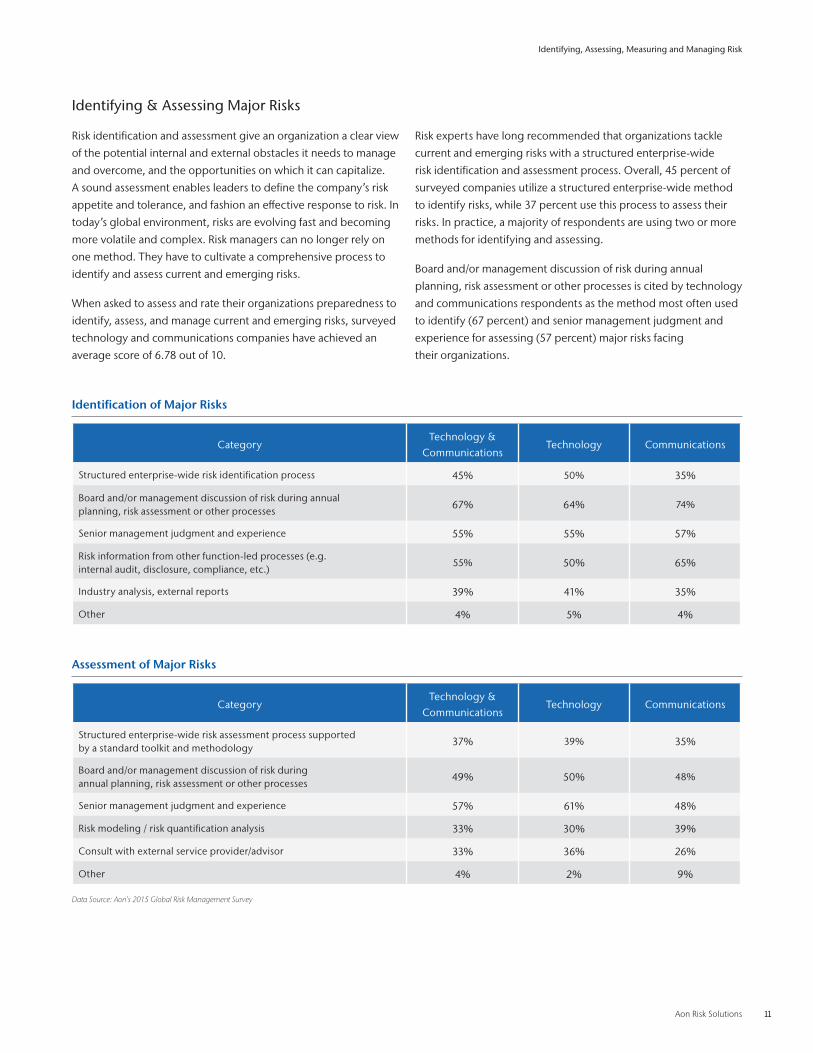

Identifying & Assessing Major Risks

Risk identification and assessment give an organization a clear view

of the potential internal and external obstacles it needs to manage

and overcome, and the opportunities on which it can capitalize .

A sound assessment enables leaders to define the company’s risk

appetite and tolerance, and fashion an effective response to risk . In

today’s global environment, risks are evolving fast and becoming

more volatile and complex . Risk managers can no longer rely on

one method . They have to cultivate a comprehensive process to

identify and assess current and emerging risks .

When asked to assess and rate their organizations preparedness to

identify, assess, and manage current and emerging risks, surveyed

technology and communications companies have achieved an

average score of 6 .78 out of 10 .

Risk experts have long recommended that organizations tackle

current and emerging risks with a structured enterprise-wide

risk identification and assessment process . Overall, 45 percent of

surveyed companies utilize a structured enterprise-wide method

to identify risks, while 37 percent use this process to assess their

risks . In practice, a majority of respondents are using two or more

methods for identifying and assessing .

Board and/or management discussion of risk during annual

planning, risk assessment or other processes is cited by technology

and communications respondents as the method most often used

to identify (67 percent) and senior management judgment and

experience for assessing (57 percent) major risks facing

their organizations .

Identification of Major Risks

CategoryTechnology &

CommunicationsTechnology Communications

Structured enterprise-wide risk identification process 45% 50% 35%

Board and/or management discussion of risk during annualplanning, risk assessment or other processes

67% 64% 74%

Senior management judgment and experience 55% 55% 57%

Risk information from other function-led processes (e .g .internal audit, disclosure, compliance, etc .)

55% 50% 65%

Industry analysis, external reports 39% 41% 35%

Other 4% 5% 4%

Identifying, Assessing, Measuring and Managing Risk

Assessment of Major Risks

CategoryTechnology &

CommunicationsTechnology Communications

Structured enterprise-wide risk assessment process supportedby a standard toolkit and methodology

37% 39% 35%

Board and/or management discussion of risk during annual planning, risk assessment or other processes

49% 50% 48%

Senior management judgment and experience 57% 61% 48%

Risk modeling / risk quantification analysis 33% 30% 39%

Consult with external service provider/advisor 33% 36% 26%

Other 4% 2% 9%

Data Source: Aon’s 2015 Global Risk Management Survey

12 Technology and Communications Industry Report

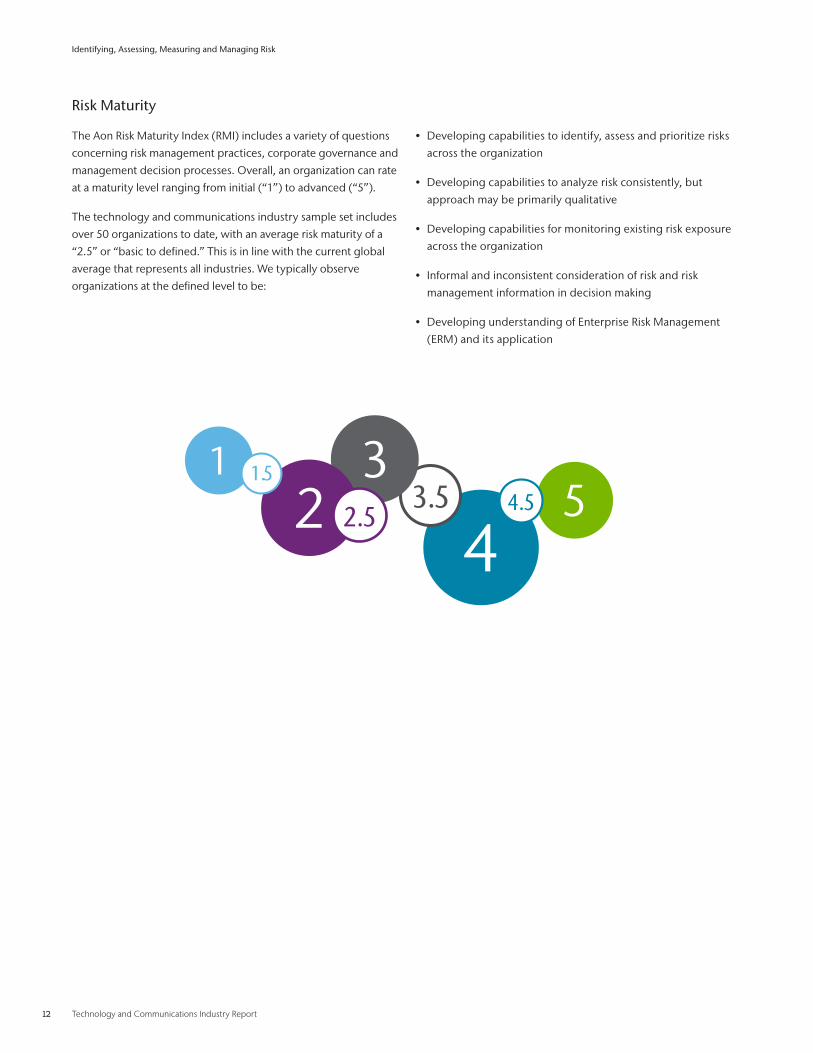

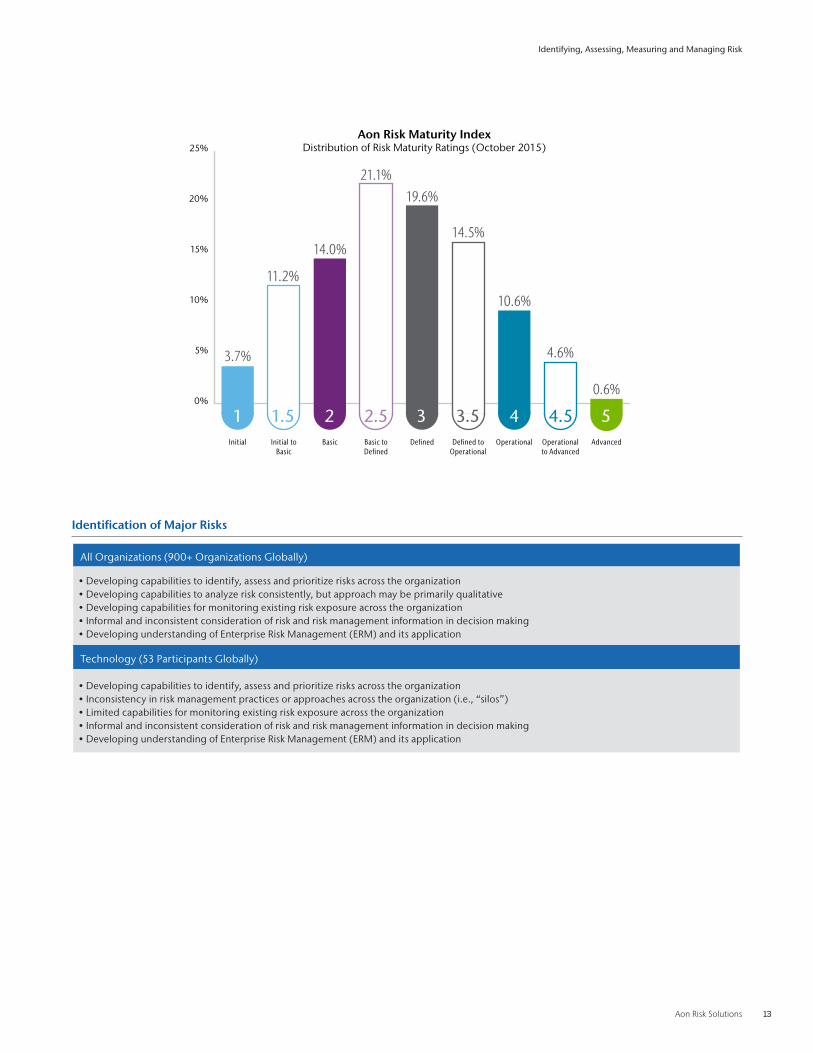

Risk Maturity

The Aon Risk Maturity Index (RMI) includes a variety of questions

concerning risk management practices, corporate governance and

management decision processes . Overall, an organization can rate

at a maturity level ranging from initial (“1”) to advanced (“5”) .

The technology and communications industry sample set includes

over 50 organizations to date, with an average risk maturity of a

“2 .5” or “basic to defined .” This is in line with the current global

average that represents all industries . We typically observe

organizations at the defined level to be:

• Developing capabilities to identify, assess and prioritize risks

across the organization

• Developing capabilities to analyze risk consistently, but

approach may be primarily qualitative

• Developing capabilities for monitoring existing risk exposure

across the organization

• Informal and inconsistent consideration of risk and risk

management information in decision making

• Developing understanding of Enterprise Risk Management

(ERM) and its application

Identifying, Assessing, Measuring and Managing Risk

54

3.531

2 2.5 4.51.5

Aon Risk Solutions 13

Identification of Major Risks

All Organizations (900+ Organizations Globally)

•Developingcapabilitiestoidentify,assessandprioritizerisksacrosstheorganization•Developingcapabilitiestoanalyzeriskconsistently,butapproachmaybeprimarilyqualitative•Developingcapabilitiesformonitoringexistingriskexposureacrosstheorganization•Informalandinconsistentconsiderationofriskandriskmanagementinformationindecisionmaking•DevelopingunderstandingofEnterpriseRiskManagement(ERM)anditsapplication

Technology (53 Participants Globally)

•Developingcapabilitiestoidentify,assessandprioritizerisksacrosstheorganization•Inconsistencyinriskmanagementpracticesorapproachesacrosstheorganization(i.e.,“silos”)•Limitedcapabilitiesformonitoringexistingriskexposureacrosstheorganization•Informalandinconsistentconsiderationofriskandriskmanagementinformationindecisionmaking•DevelopingunderstandingofEnterpriseRiskManagement(ERM)anditsapplication

Identifying, Assessing, Measuring and Managing Risk

AdvancedOperationalto Advanced

OperationalDefined toOperational

DefinedBasic toDefined

BasicInitial toBasic

Initial

Aon Risk Maturity IndexDistribution of Risk Maturity Ratings (October 2015)

0%

5%

10%

15%

20%

25%

1 1.5 2 2.5 3 3.5 4 4.5 5

0.6%

4.6%

10.6%

14.5%

19.6%21.1%

14.0%

11.2%

3.7%

14 Technology and Communications Industry Report

Technology and communications organizations as a group appear

to have especially strong practices related to risk management

stewardship, and are more mature in their ability to integrate risk

insights into human capital processes . In particular, they are likely

to have the most transparency around their risk communications .

The technology and communications industry tends to score

lower in areas related to the use of quantification methods to

understand risk . In addition, technology and communications

companies seem to have the lowest level of involvement of key

stakeholders in risk management strategy setting . In particular,

they seem less mature with formally collecting and incorporating

risk information into the decision making process .

One section of the RMI is dedicated to best practices regarding

identification of existing and emerging risks . When it comes to

these practices, there are a few interesting differences between

those organizations at lower levels of risk maturity (2 .5-) and

higher levels of risk maturity (3 .5+) .

Specifically, over 60 percent of less mature organizations rarely

or never collaborate with their strategic partners to identify

potential emerging risks, while over 86 percent of more mature

organizations collaborate on an ad-hoc basis, if not more

consistently through a defined process . In an increasingly

interconnected world, this difference illustrates the importance

of collaboration outside of just an internally-focused risk

identification process .

There also appears to be a notable difference between how

organizations measure and track risks once identified . Based

on our research, not only do more mature organizations have

processes in place to identify risks at an enterprise level, but

they are also more than twice as likely to follow through with

implementing, measuring, and tracking risk management

activities to completion .

Identifying, Assessing, Measuring and Managing Risk

Aon Risk Solutions 15

Risk Management Department and Function

16 Technology and Communications Industry Report

Chief Risk Officer

Thirty-one percent of technology and communications

respondents report having a CRO . The responsibilities of a CRO

vary from company to company and industry to industry . Often,

CROs are given the tasks including managing credit risk, market

risk, regulatory risk and compliance risk, which may or may not

include insurance/ hazard risk . About 61 percent of participants

say they do not have a CRO nor do they plan to create one . They

choose instead to leverage existing teams and use risk committees

for driving change .

Risk Management Department

The growing importance and visibility of risk management

have led to the increasing integration of such functions with an

organization’s strategic plan . To succeed in today’s competitive

and heavily regulated business environment, companies have

gradually come to the realization that they have to incorporate

risk management into all aspects of their operations .

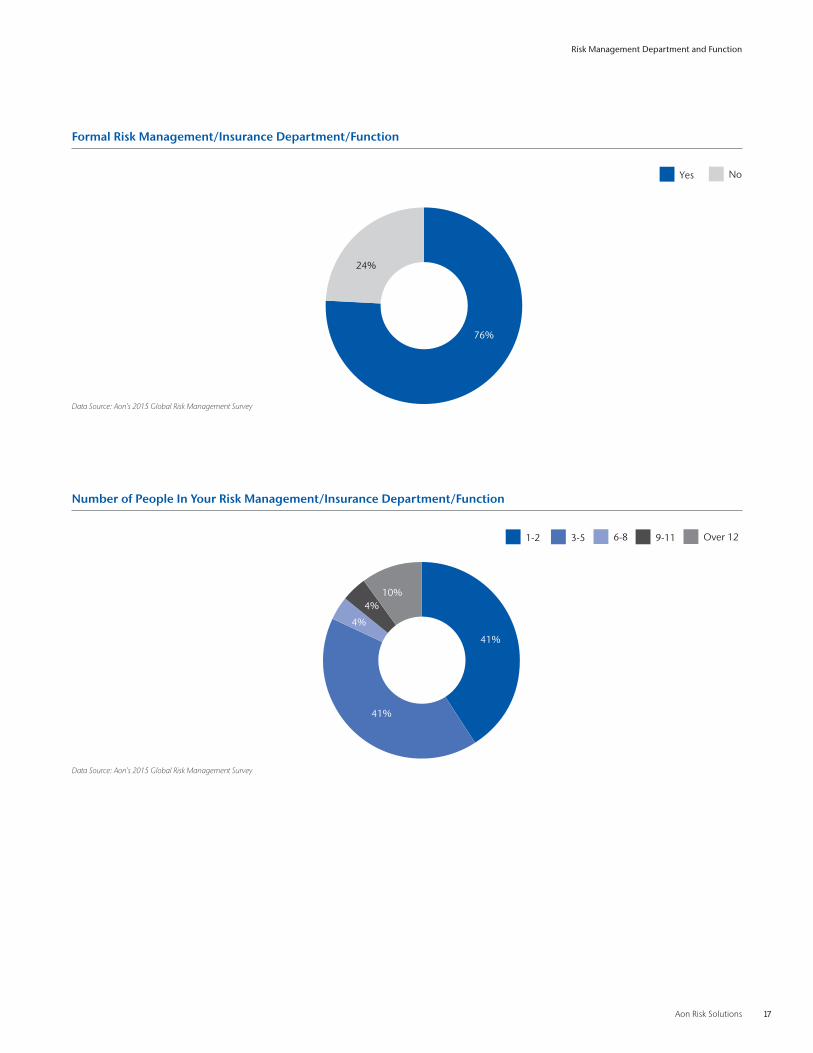

Seventy-six percent of technology and communications

respondents have indicated that they have a formal risk

management department, slightly higher than the average

(71 percent) for companies across all industries . If we look

further at this group by organizations over $1 billion we can see

organizational size plays a significant role . Ninety-three percent

of organizations over $1 billion have a risk manager .

Among organizations with a risk management department, 66

percent say their risk management department reports to the

Finance/Treasury/Chief Financial Officer . In the case where no

formal risk management department exists, 32 percent say their

CFO handled risk management .

Those with an in-house risk management department typically

maintain a staff of one to five people (82 percent) .

Chief Risk Officer

RoleTechnology &

CommunicationsTechnology Communications All

Yes, but this role does not includerisk management

14% 16% 9% 11%

Yes, this role includes risk management 17% 16% 17% 17%

No, but we are consideringcreating this position

5% 2% 9% 8%

No, and we do not plan to createsuch a position

61% 63% 57% 59%

Don’t know 5% 2% 9% 5%

Data Source: 2015 Global Risk Management Survey

Risk Management Department and Function

Aon Risk Solutions 17

Formal Risk Management/Insurance Department/Function

Number of People In Your Risk Management/Insurance Department/Function

Data Source: Aon’s 2015 Global Risk Management Survey

Data Source: Aon’s 2015 Global Risk Management Survey

24%

76%

NoYes

24%

76%

NoYes

10%

41%

4%

4%

41%

Over 129-116-83-51-2

10%

41%

4%

4%

41%

Over 129-116-83-51-2

Risk Management Department and Function

18 Technology and Communications Industry Report

External Drivers Strengthening Risk Management – Technology and Communications (past two years)

0% 15% 30% 45% 60%

Political uncertainty

Pressure fromcompetitors

Pressure fromcustomers

Random actsof violence

Risk events/blackswan events

Workforce issues

Other

Natural weather events

Large third partyliability losses/litigation

Increased focusfrom regulators

Globalization

Exposure from suppliers/vendors

Economic volatility

Demand from investorsfor greater disclosure

and accountability

Cyber threatenvironment

20%28%

11%18%

13%18%

12%8%

15%9%

18%18%

38%31%

22%51%

15%16%

37%27%

15%12%

21%

2%0%

27%

26%39%

17%16%

Technology & Communications All

External Drivers Strengthening Risk Management (past two years)

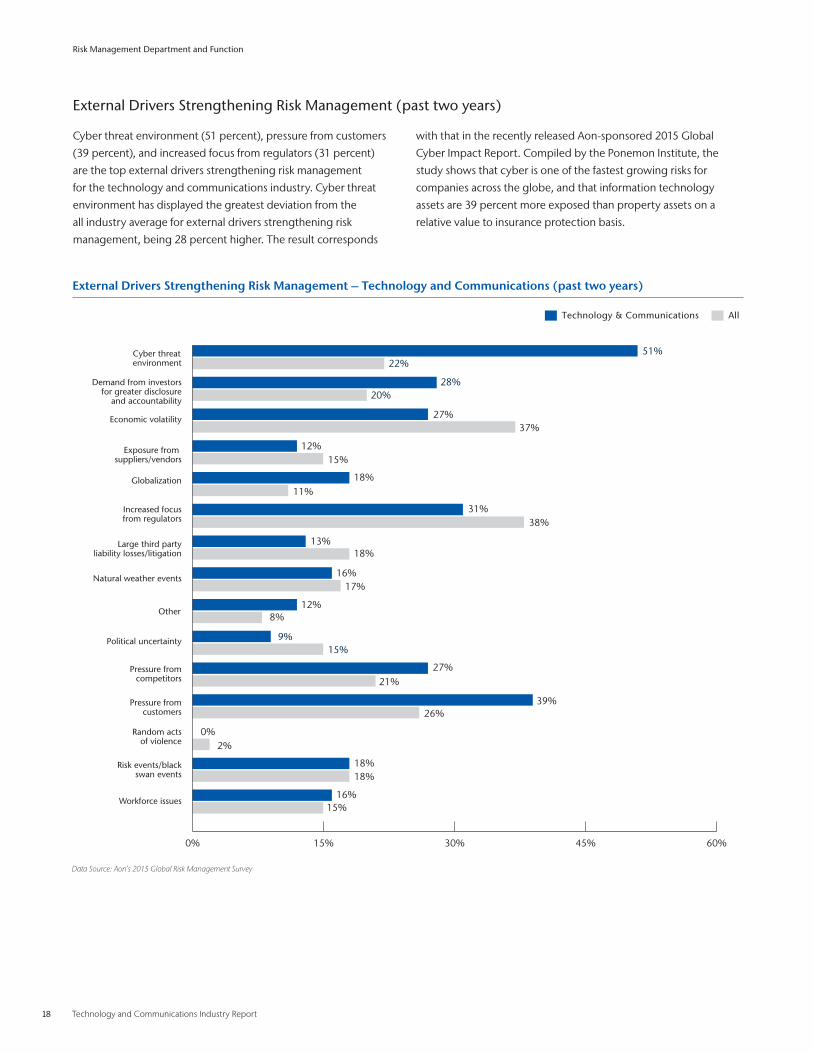

Cyber threat environment (51 percent), pressure from customers

(39 percent), and increased focus from regulators (31 percent)

are the top external drivers strengthening risk management

for the technology and communications industry . Cyber threat

environment has displayed the greatest deviation from the

all industry average for external drivers strengthening risk

management, being 28 percent higher . The result corresponds

with that in the recently released Aon-sponsored 2015 Global

Cyber Impact Report . Compiled by the Ponemon Institute, the

study shows that cyber is one of the fastest growing risks for

companies across the globe, and that information technology

assets are 39 percent more exposed than property assets on a

relative value to insurance protection basis .

Risk Management Department and Function

Data Source: Aon’s 2015 Global Risk Management Survey

Aon Risk Solutions 19

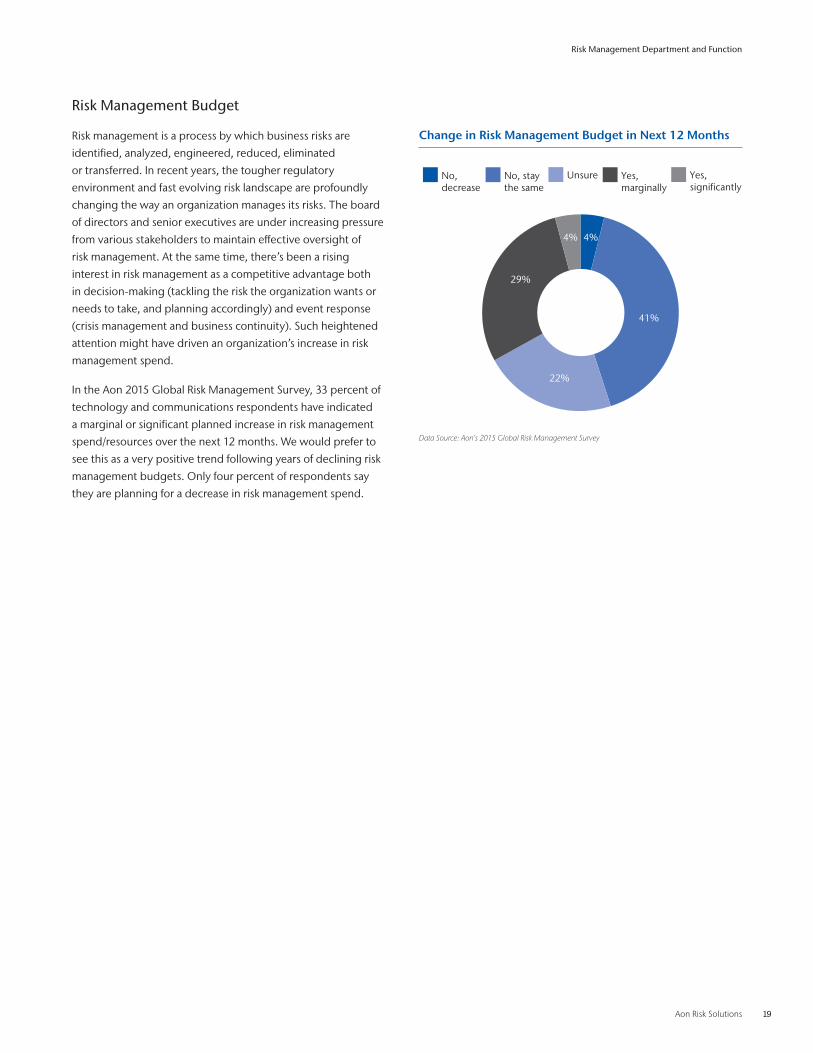

Risk Management Budget

Risk management is a process by which business risks are

identified, analyzed, engineered, reduced, eliminated

or transferred . In recent years, the tougher regulatory

environment and fast evolving risk landscape are profoundly

changing the way an organization manages its risks . The board

of directors and senior executives are under increasing pressure

from various stakeholders to maintain effective oversight of

risk management . At the same time, there’s been a rising

interest in risk management as a competitive advantage both

in decision-making (tackling the risk the organization wants or

needs to take, and planning accordingly) and event response

(crisis management and business continuity) . Such heightened

attention might have driven an organization’s increase in risk

management spend .

In the Aon 2015 Global Risk Management Survey, 33 percent of

technology and communications respondents have indicated

a marginal or significant planned increase in risk management

spend/resources over the next 12 months . We would prefer to

see this as a very positive trend following years of declining risk

management budgets . Only four percent of respondents say

they are planning for a decrease in risk management spend .

Change in Risk Management Budget in Next 12 Months

Data Source: Aon’s 2015 Global Risk Management Survey

4%

22%

29%

4%

41%

Yes, significantly

Yes, marginally

UnsureNo, stay the same

No, decrease

Risk Management Department and Function

20 Technology and Communications Industry Report

Risk Financing

Aon Risk Solutions 21

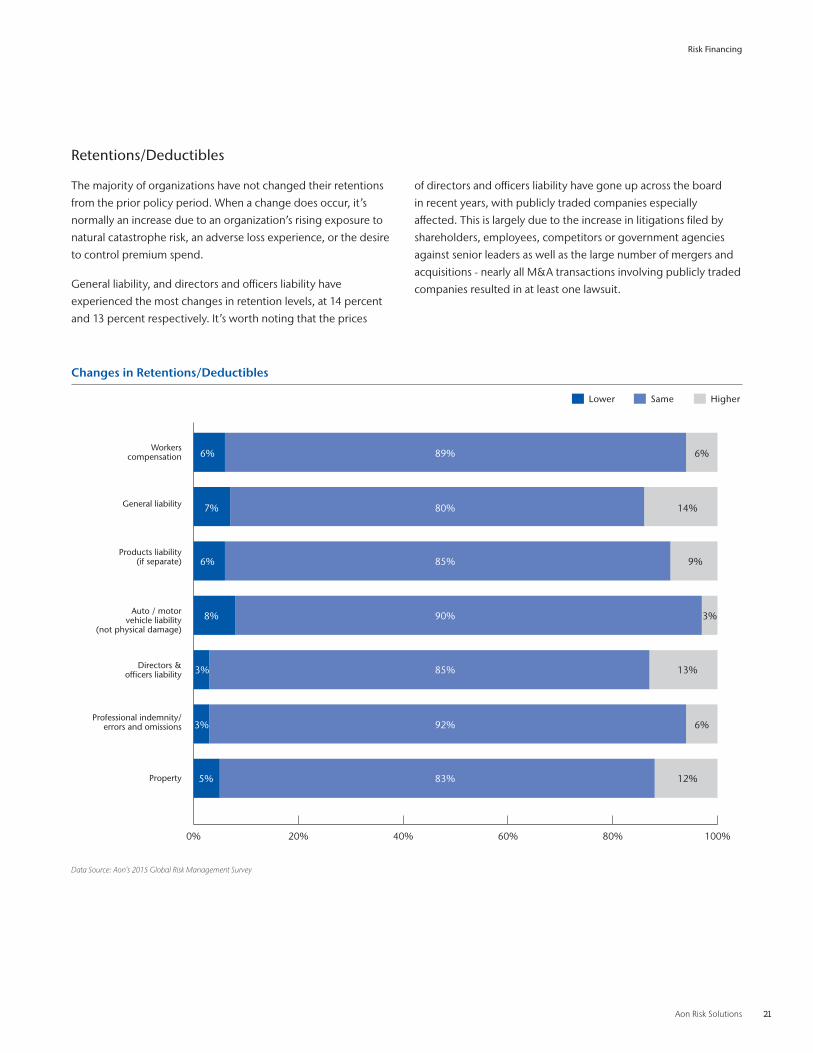

Retentions/Deductibles

The majority of organizations have not changed their retentions

from the prior policy period . When a change does occur, it’s

normally an increase due to an organization’s rising exposure to

natural catastrophe risk, an adverse loss experience, or the desire

to control premium spend .

General liability, and directors and officers liability have

experienced the most changes in retention levels, at 14 percent

and 13 percent respectively . It’s worth noting that the prices

of directors and officers liability have gone up across the board

in recent years, with publicly traded companies especially

affected . This is largely due to the increase in litigations filed by

shareholders, employees, competitors or government agencies

against senior leaders as well as the large number of mergers and

acquisitions - nearly all M&A transactions involving publicly traded

companies resulted in at least one lawsuit .

Changes in Retentions/Deductibles

0% 20% 40% 60% 80% 100%

Property

Professional indemnity/errors and omissions

Directors &officers liability

Auto / motorvehicle liability

(not physical damage)

Products liability(if separate)

General liability

Workerscompensation

Lower Same Higher

89%

80%

85%

90%

85%

92%3%

83%5% 12%

6%

3% 13%

8% 3%

6% 9%

7% 14%

6% 6%

Data Source: Aon’s 2015 Global Risk Management Survey

Risk Financing

22 Technology and Communications Industry Report

Directors and Officers Liability Similar to the umbrella/excess liability, directors’ and officers’

liability limits purchased by publicly traded technology and

communications companies are in direct proportion to a

company’s revenue size . The highest limit purchased stands at

USD 655 million, while the lowest limit purchased USD 1 million .

Umbrella/Excess Liability Limits

Revenue Minimum 1st Quartile Average Median Mode 3rd Quartile Maximum

All $4,000,000 $50,000,000 $113,350,877 $100,000,000 $100,000,000 $125,000,000 $700,000,000

$1M-$500M $4,000,000 $10,500,000 $32,272,727 $25,000,000 $50,000,000 $50,000,000 $100,000,000

$500M-$1B $10,000,000 $24,000,000 $44,000,000 $25,000,000 $24,000,000 $62,500,000 $100,000,000

$1B-$5B $25,000,000 $50,000,000 $90,500,000 $100,000,000 $100,000,000 $100,000,000 $200,000,000

$5B-$15B $75,000,000 $100,000,000 $171,875,000 $125,000,000 $100,000,000 $225,000,000 $350,000,000

Over $15B $5,000,000 $125,000,000 $237,545,455 $175,000,000 $150,000,000 $262,500,000 $700,000,000

S&P Technology and Communications Sector

Market Cap Minimum 1st Quartile Average Median 3rd Quartile Maximum

All $1,000,000 $35,000,000 $102,582,645 $65,000,000 $130,000,000 $655,000,000

$1M-$100M $1,000,000 $5,000,000 $11,718,750 $12,750,000 $15,500,000 $30,000,000

$100M-$500M $20,000,000 $25,000,000 $45,714,286 $35,000,000 $60,000,000 $120,000,000

$500M-$1B $5,000,000 $50,000,000 $90,153,846 $70,000,000 $130,000,000 $230,000,000

$1B-$5B $10,000,000 $60,000,000 $86,470,588 $75,000,000 $121,250,000 $200,000,000

Over $5B $20,000,000 $125,000,000 $212,857,143 $200,000,000 $270,000,000 $655,000,000

Data Source: Aon’s 2015 Global Risk Management Survey and other Aon proprietary databases

Data Source: The Aon Financial Services Group

Limits

Umbrella/Excess LiabilityWhen an organization considers what level of risk to transfer via

insurance policies, it has to take into account multiple factors .

These include: risk severity, risk mitigation measures already

in place or under consideration, the regulatory landscape, an

organization’s historical trend of loss activities, the insurance

marketplace and its appetite for risk . The choice made by one

individual organization may not work for another . Consideration

must always be given to the impact of that loss retention on an

organization’s ability to achieve its objectives .

In the 2015 survey, technology and communications respondents

say the most commonly purchased limit amounts to USD 100

million and the average limit purchased for all surveyed companies

totals USD 113 million . The level of limits purchased stands in

direct proportion to a company’s revenue size - a larger company

with a higher profile could represent a bigger target for legal

actions . As the Chinese saying goes: a tall tree catches most of

the wind .

Risk Financing

Aon Risk Solutions 23

Cyber Risk Coverage

In the Aon-sponsored 2015 Global Cyber Impact Report (the

research was conducted by the Ponemon Institute), we have found

that cyber is one of the fastest growing risks for companies across

the globe as mobile technologies, cloud computing, corporate

bring-your-own-device policies, and big data analytics are

becoming increasingly popular . About 37 percent of companies

surveyed experienced a “material or significantly disruptive

security exploit or data breach one or more times during the past

two years and the average economic impact of the event was

USD 2 .1 million .”

Given the proliferation of internet-connected devices, which

are expected to grow from 10 to 50 billion within five years,

cyber risk is expected to skyrocket . On average, probable

maximum loss of tangible assets amounts to USD 648 million and

probable maximum loss on intangible assets USD 612 million .

But, organizations buy insurance to cover just over half of the

maximum probable loss of property, plant and equipment, and

only 12 percent of the probable maximum loss of information

assets .

Organizations need to consider cyber assets and exposures in

the context of financial statement impact compared to historical

tangible assets and exposures . According to a sobering new

report from FireEye, on average 96 percent of computer systems

across all industry segments have been breached . Yet, the

Verizon 2015 Data Breach Investigations Report only shows

confirmed data loss in less than three percent of the almost

80,000 incidents reported . As far as financial impact

is concerned, 80 percent of incidents result in less than

USD 1 million in total cost and indemnity, 15 percent in losses

between USD 1 million and USD 20 million, and five percent

in losses over USD 20 million . Identification, quantification,

mitigation, incident response plans and risk transfer are some

of the key issues in macro-level enterprise risk management .

While a cyber attack often causes disruption to business and IT

operations, catastrophic cyber losses can also result in potential

director’s and officer’s liability allegations . In the wake of

numerous publicly reported material incidents in 2015, cyber

insurance gross written premium is forecast to grow at the

same time insurance carriers are limiting capacity, coverage and

raising premiums for certain industry classes, such as large retail,

healthcare and financial institutions .

In the face of more frequent contractual insurance requirements

for cyber liability and potential shareholder derivative actions,

forward-thinking companies are taking proactive steps to

explore and transfer cyber risks . Underwriting and purchasing

of cyber insurance process can assist to:

• Satisfy customer and partner cyber insurance

contract requirements

• Stabilize balance sheet

• Address regulatory (including SEC) guidelines

• Reduce Total Cost of Risk

• Enable organization-wide cyber risk management culture

• Align cyber insurance solution with Enterprise

Risk Management

Finally, despite the growth of cyber insurance sales,

initial insurance carrier denials of 2015 cyber insurance

claims re-emphasize the critical importance of negotiated

customized coverage – the devil is in the details .

Risk Financing

24 Technology and Communications Industry Report

Cyber Risk

PropertyGeneral Liability

Crime/Bond K&RProfessional Indemnity

Cyber

1st Party Privacy/Network Risks

Physical damage to data only

Virus/hacker damage to data only

Denial of service attach

B .I . loss from security event

Extortion or threat

Employee sabotage of data only

3rd Party Privacy/Network Risks

Theft/disclosure of private info .

Confidential corporate info . breach

Technology E&O

Media liability (electronic content)

Privacy breach expense/notification

Damage to third-party’s data only

Regulatory privacy defense/fines

Virus/malicious code transmission

Limited coverage CoverageNo coverage

* For reference and discussion only.

Risk Financing

Aon Risk Solutions 25

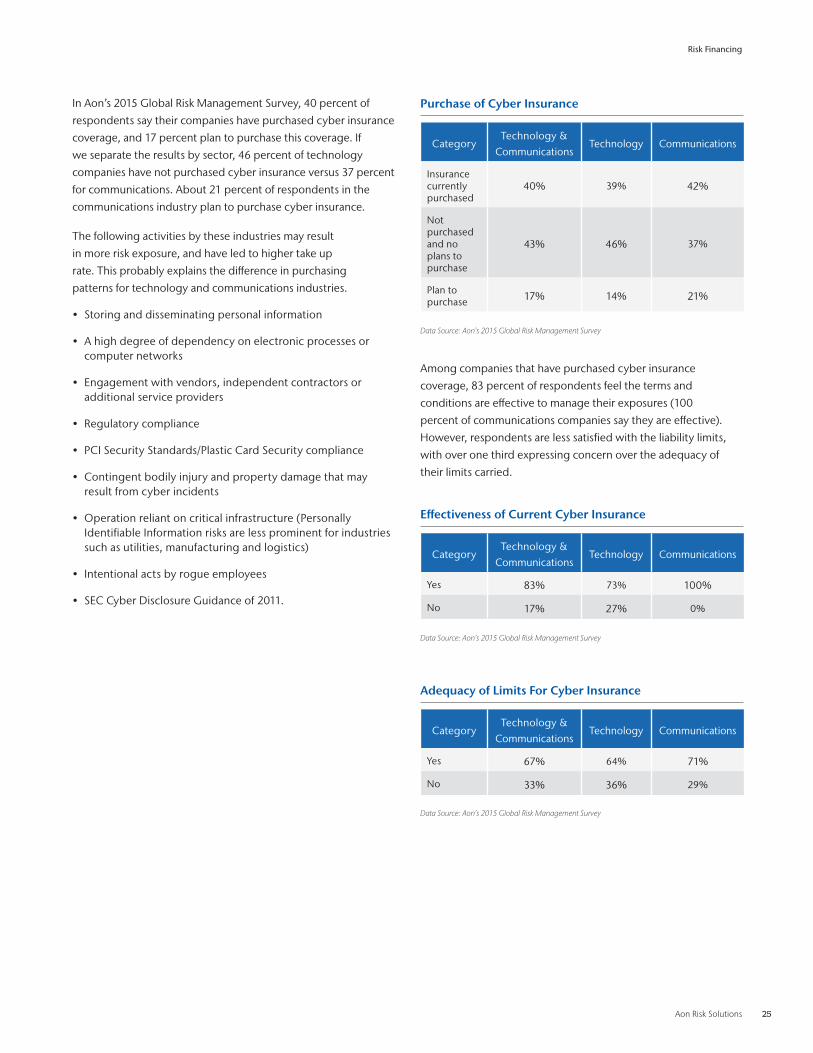

In Aon’s 2015 Global Risk Management Survey, 40 percent of

respondents say their companies have purchased cyber insurance

coverage, and 17 percent plan to purchase this coverage . If

we separate the results by sector, 46 percent of technology

companies have not purchased cyber insurance versus 37 percent

for communications . About 21 percent of respondents in the

communications industry plan to purchase cyber insurance .

The following activities by these industries may result

in more risk exposure, and have led to higher take up

rate . This probably explains the difference in purchasing

patterns for technology and communications industries .

• Storing and disseminating personal information

• A high degree of dependency on electronic processes or computer networks

• Engagement with vendors, independent contractors or additional service providers

• Regulatory compliance

• PCI Security Standards/Plastic Card Security compliance

• Contingent bodily injury and property damage that may result from cyber incidents

• Operation reliant on critical infrastructure (Personally Identifiable Information risks are less prominent for industries such as utilities, manufacturing and logistics)

• Intentional acts by rogue employees

• SEC Cyber Disclosure Guidance of 2011 .

Among companies that have purchased cyber insurance

coverage, 83 percent of respondents feel the terms and

conditions are effective to manage their exposures (100

percent of communications companies say they are effective) .

However, respondents are less satisfied with the liability limits,

with over one third expressing concern over the adequacy of

their limits carried .

Purchase of Cyber Insurance

CategoryTechnology &

CommunicationsTechnology Communications

Insurance currently purchased

40% 39% 42%

Not purchased and no plans to purchase

43% 46% 37%

Plan to purchase 17% 14% 21%

Data Source: Aon’s 2015 Global Risk Management Survey

Effectiveness of Current Cyber Insurance

CategoryTechnology &

CommunicationsTechnology Communications

Yes 83% 73% 100%

No 17% 27% 0%

Data Source: Aon’s 2015 Global Risk Management Survey

Adequacy of Limits For Cyber Insurance

CategoryTechnology &

CommunicationsTechnology Communications

Yes 67% 64% 71%

No 33% 36% 29%

Data Source: Aon’s 2015 Global Risk Management Survey

Risk Financing

26 Technology and Communications Industry Report

Multinational Programs

Aon Risk Solutions 27

Globalization continues to be a consistent theme for companies

pursuing improved operational results . As such, risk managers

need to focus on larger geographic spread while addressing

variations in regulatory controls, exposures, available solutions,

and options for optimal risk finance program design .

Looking at control and placement of multinational risks, half of the

technology and communications respondents with operations

in more than one country have indicated that their corporate

headquarters control procurement of all of their global and local

insurance programs while only 38 percent purchase some lines

and leave local offices to handle other lines .

General liability and property coverage continue to be the lines

of business most frequently purchased on a multinational basis .

However, there have been a dramatic increase in the number of

respondents purchasing multinational programs for directors

& officers liability (86 percent), workers compensation and

employers liability (54 percent) and auto/motor vehicle liability .

These upticks may be attributable to the continued need for

certainty of coverage and costs, all of which could drive the

decision to purchase multinational programs .

Multinational Insurance Purchasing Habits

Category Technology & Communications All

Corporate headquarters controls procurement of ALL insurance programs (global/local)

50% 45%

Corporate headquarters controls some lines and leaves local office to purchase other lines

38% 44%

No, each operation buys its own insurance with no co-ordination from corporate headquarters

13% 11%

Importance to Multinational Program Purchase Decision

Category Technology & Communications All

Certainty of Coverage - Knowledge of what coverage is included in the program

1 1

Cost - This approach is more economical

2 2

Statutory Compliance -Access to local admitted coverage where non-admitted is prohibited

3 3

Fiscal Compliance - Ability to pay insurance premium and related taxes

4 4

Program Performance - Access to local claims and/or other services from local insurer/policy provider

5 5

Accounting - Ability to allocate risk transfer costs to local operations vs . pay from corporate

6 6

Types of Multinational Insurance Coverages Purchased

Category Technology & Communications All

General Liability/Public Liability 89% 81%

Property (property damage and business interruption)

79% 79%

Directors & Officers Liability 86% 73%

Marine/Ocean Cargo 46% 49%

Workers Compensation/ Employers Liability

54% 48%

Auto/Motor Vehicle Liability 50% 42%

Crime 61% 42%

Product Recall and Contamination 11% 18%

Trade Credit 25% 17%

Other 11% 11%

Data represents respondents operating in more than one countryData Source: 2015 Global Risk Management Survey

Data represents respondents operating in more than one countryData Source: 2015 Global Risk Management Survey

Data represents respondents operating in more than one countryData Source: 2015 Global Risk Management Survey

Multinational Programs

28 Technology and Communications Industry Report

Captives

Aon Risk Solutions 29

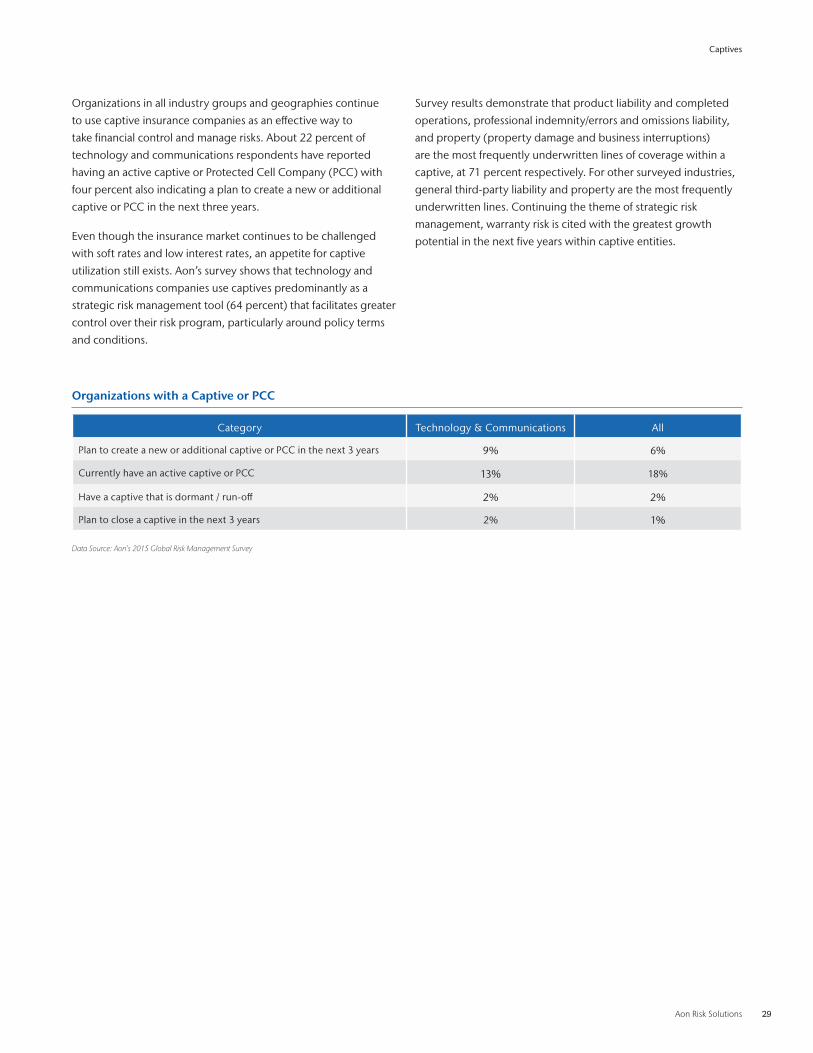

Organizations in all industry groups and geographies continue

to use captive insurance companies as an effective way to

take financial control and manage risks . About 22 percent of

technology and communications respondents have reported

having an active captive or Protected Cell Company (PCC) with

four percent also indicating a plan to create a new or additional

captive or PCC in the next three years .

Even though the insurance market continues to be challenged

with soft rates and low interest rates, an appetite for captive

utilization still exists . Aon’s survey shows that technology and

communications companies use captives predominantly as a

strategic risk management tool (64 percent) that facilitates greater

control over their risk program, particularly around policy terms

and conditions .

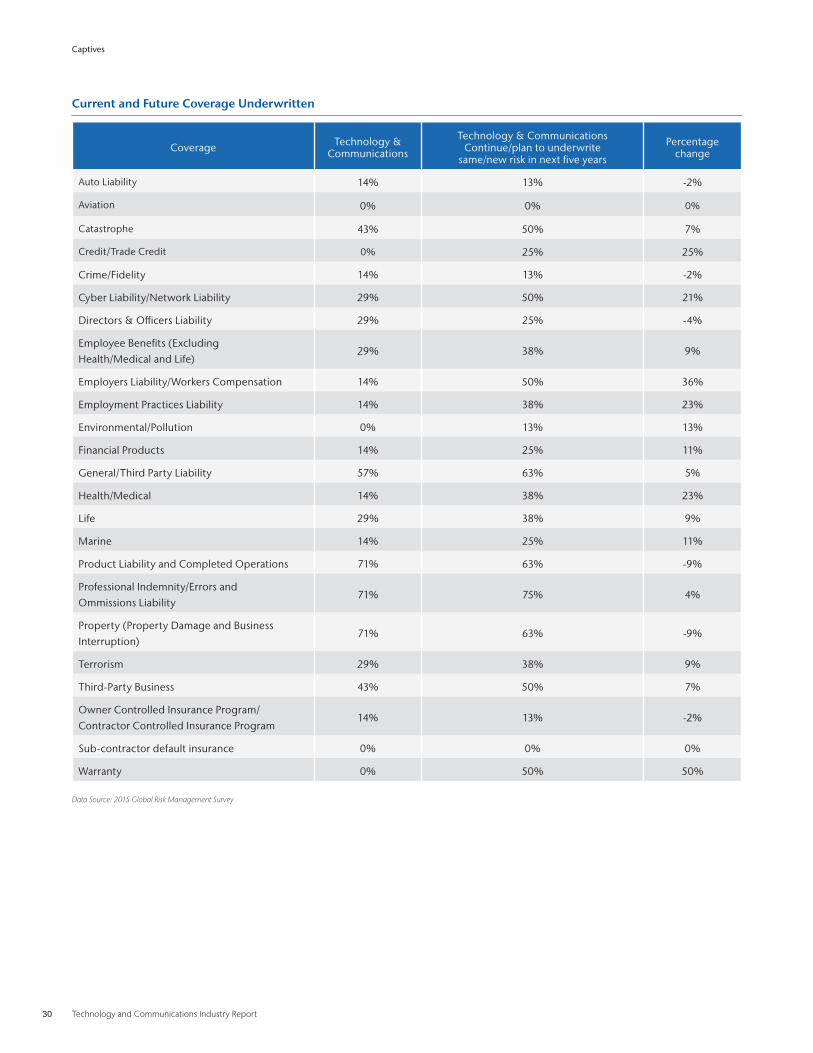

Survey results demonstrate that product liability and completed

operations, professional indemnity/errors and omissions liability,

and property (property damage and business interruptions)

are the most frequently underwritten lines of coverage within a

captive, at 71 percent respectively . For other surveyed industries,

general third-party liability and property are the most frequently

underwritten lines . Continuing the theme of strategic risk

management, warranty risk is cited with the greatest growth

potential in the next five years within captive entities .

Organizations with a Captive or PCC

Category Technology & Communications All

Plan to create a new or additional captive or PCC in the next 3 years 9% 6%

Currently have an active captive or PCC 13% 18%

Have a captive that is dormant / run-off 2% 2%

Plan to close a captive in the next 3 years 2% 1%

Data Source: Aon’s 2015 Global Risk Management Survey

Captives

30 Technology and Communications Industry Report

Current and Future Coverage Underwritten

Coverage Technology & Communications

Technology & Communications Continue/plan to underwrite

same/new risk in next five years

Percentage change

Auto Liability 14% 13% -2%

Aviation 0% 0% 0%

Catastrophe 43% 50% 7%

Credit/Trade Credit 0% 25% 25%

Crime/Fidelity 14% 13% -2%

Cyber Liability/Network Liability 29% 50% 21%

Directors & Officers Liability 29% 25% -4%

Employee Benefits (Excluding Health/Medical and Life)

29% 38% 9%

Employers Liability/Workers Compensation 14% 50% 36%

Employment Practices Liability 14% 38% 23%

Environmental/Pollution 0% 13% 13%

Financial Products 14% 25% 11%

General/Third Party Liability 57% 63% 5%

Health/Medical 14% 38% 23%

Life 29% 38% 9%

Marine 14% 25% 11%

Product Liability and Completed Operations 71% 63% -9%

Professional Indemnity/Errors and Ommissions Liability

71% 75% 4%

Property (Property Damage and Business Interruption)

71% 63% -9%

Terrorism 29% 38% 9%

Third-Party Business 43% 50% 7%

Owner Controlled Insurance Program/Contractor Controlled Insurance Program

14% 13% -2%

Sub-contractor default insurance 0% 0% 0%

Warranty 0% 50% 50%

Data Source: 2015 Global Risk Management Survey

Captives

Aon Risk Solutions 31

Market Insights

32 Technology and Communications Industry Report

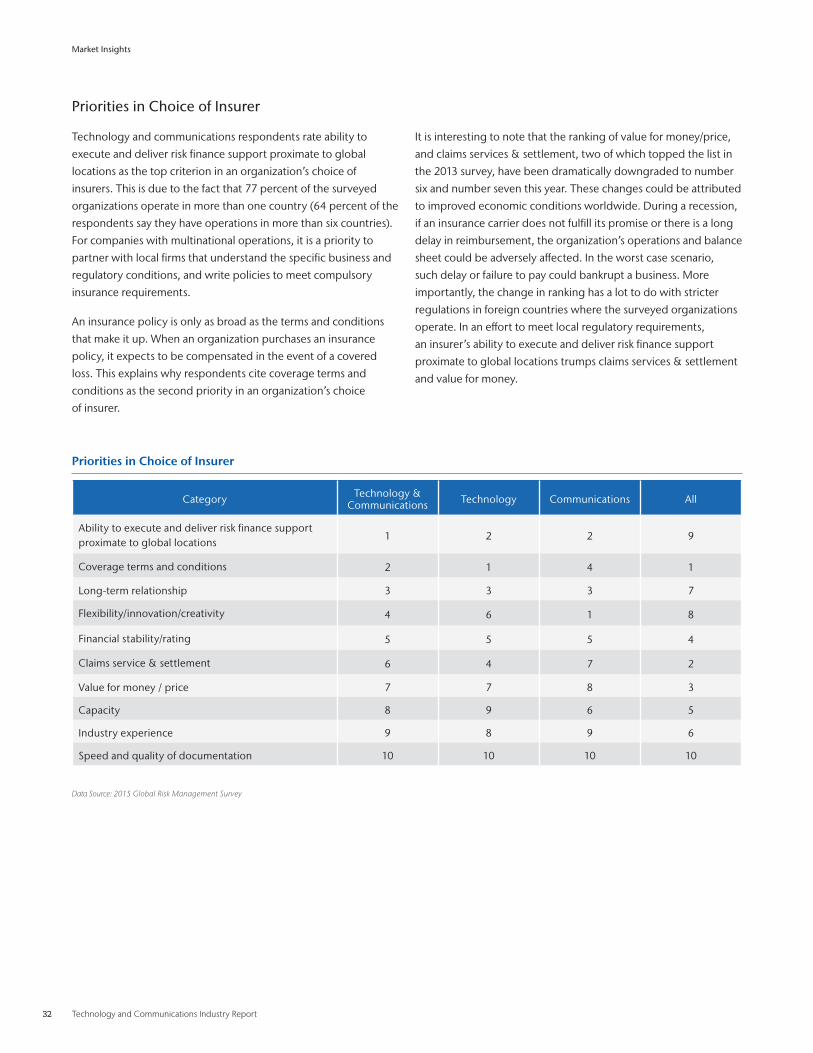

Priorities in Choice of Insurer

Technology and communications respondents rate ability to

execute and deliver risk finance support proximate to global

locations as the top criterion in an organization’s choice of

insurers . This is due to the fact that 77 percent of the surveyed

organizations operate in more than one country (64 percent of the

respondents say they have operations in more than six countries) .

For companies with multinational operations, it is a priority to

partner with local firms that understand the specific business and

regulatory conditions, and write policies to meet compulsory

insurance requirements .

An insurance policy is only as broad as the terms and conditions

that make it up . When an organization purchases an insurance

policy, it expects to be compensated in the event of a covered

loss . This explains why respondents cite coverage terms and

conditions as the second priority in an organization’s choice

of insurer .

It is interesting to note that the ranking of value for money/price,

and claims services & settlement, two of which topped the list in

the 2013 survey, have been dramatically downgraded to number

six and number seven this year . These changes could be attributed

to improved economic conditions worldwide . During a recession,

if an insurance carrier does not fulfill its promise or there is a long

delay in reimbursement, the organization’s operations and balance

sheet could be adversely affected . In the worst case scenario,

such delay or failure to pay could bankrupt a business . More

importantly, the change in ranking has a lot to do with stricter

regulations in foreign countries where the surveyed organizations

operate . In an effort to meet local regulatory requirements,

an insurer’s ability to execute and deliver risk finance support

proximate to global locations trumps claims services & settlement

and value for money .

Priorities in Choice of Insurer

Category Technology & Communications Technology Communications All

Ability to execute and deliver risk finance support proximate to global locations

1 2 2 9

Coverage terms and conditions 2 1 4 1

Long-term relationship 3 3 3 7

Flexibility/innovation/creativity 4 6 1 8

Financial stability/rating 5 5 5 4

Claims service & settlement 6 4 7 2

Value for money / price 7 7 8 3

Capacity 8 9 6 5

Industry experience 9 8 9 6

Speed and quality of documentation 10 10 10 10

Data Source: 2015 Global Risk Management Survey

Market Insights

Aon Risk Solutions 33

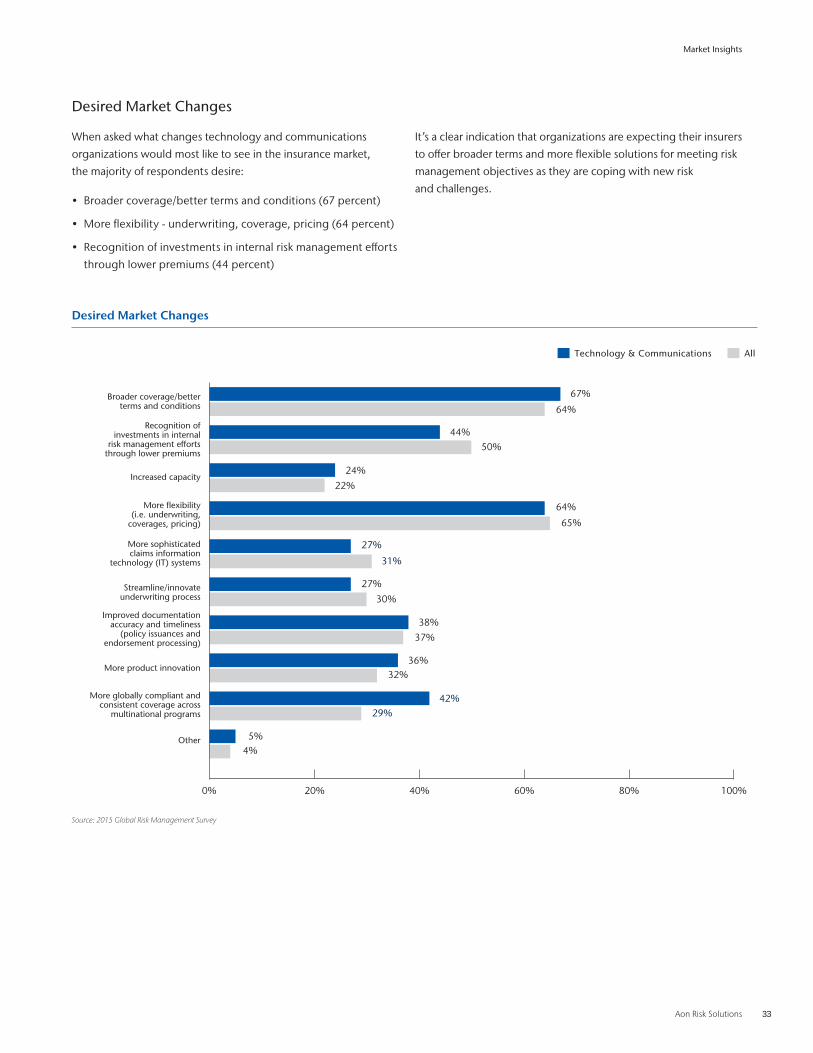

Desired Market Changes

When asked what changes technology and communications

organizations would most like to see in the insurance market,

the majority of respondents desire:

• Broader coverage/better terms and conditions (67 percent)

• More flexibility - underwriting, coverage, pricing (64 percent)

• Recognition of investments in internal risk management efforts

through lower premiums (44 percent)

It’s a clear indication that organizations are expecting their insurers

to offer broader terms and more flexible solutions for meeting risk

management objectives as they are coping with new risk

and challenges .

Desired Market Changes

Other

More globally compliant andconsistent coverage across

multinational programs

More product innovation

Improved documentationaccuracy and timeliness

(policy issuances andendorsement processing)

Streamline/innovateunderwriting process

More sophisticatedclaims information

technology (IT) systems

More flexibility(i.e. underwriting,

coverages, pricing)

Increased capacity

Recognition ofinvestments in internal

risk management effortsthrough lower premiums

Broader coverage/betterterms and conditions

Technology & Communications All

64%

67%

44%50%

27%

30%

65%

64%

32%36%

42%29%

22%24%

31%

27%

37%38%

4%5%

0% 20% 40% 60% 80% 100%

Market Insights

Source: 2015 Global Risk Management Survey

34 Technology and Communications Industry Report

Casualty/Liability Automobile Workers Compensation Financial Lines Property

Ace Ace Ace AIG Ace

AIG AIG AIG Beazley AIG

Alleghany Liberty Mutual CV Starr Chubb Berkshire Hathaway

Swiss Re MS & AD Travelers XL FM Global

Travelers Travelers Zurich Zurich Zurich

* For a Property/Casualty Package AIG, Ace, Chubb and Zurich are the top marketData Source: Global Risk Insight Platform

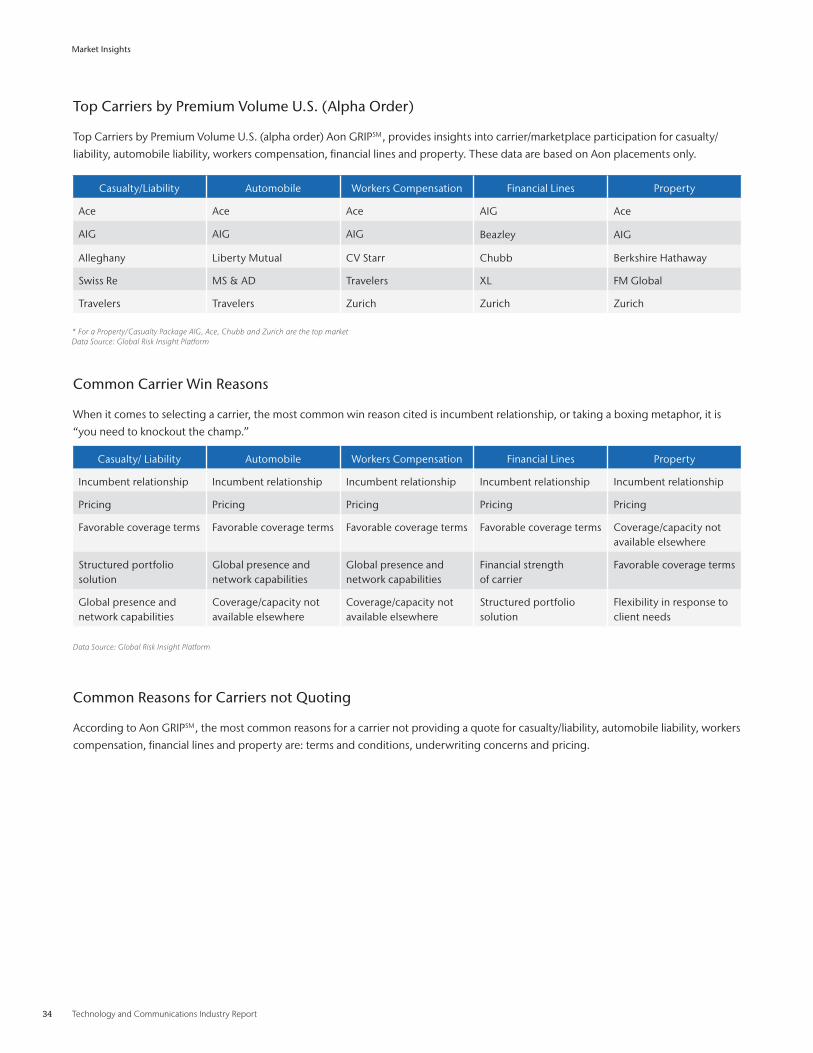

Top Carriers by Premium Volume U .S . (Alpha Order)

Top Carriers by Premium Volume U .S . (alpha order) Aon GRIPSM , provides insights into carrier/marketplace participation for casualty/

liability, automobile liability, workers compensation, financial lines and property . These data are based on Aon placements only .

Casualty/ Liability Automobile Workers Compensation Financial Lines Property

Incumbent relationship Incumbent relationship Incumbent relationship Incumbent relationship Incumbent relationship

Pricing Pricing Pricing Pricing Pricing

Favorable coverage terms Favorable coverage terms Favorable coverage terms Favorable coverage terms Coverage/capacity not available elsewhere

Structured portfolio solution

Global presence and network capabilities

Global presence and network capabilities

Financial strength of carrier

Favorable coverage terms

Global presence and network capabilities

Coverage/capacity not available elsewhere

Coverage/capacity not available elsewhere

Structured portfolio solution

Flexibility in response to client needs

Data Source: Global Risk Insight Platform

Common Carrier Win Reasons

When it comes to selecting a carrier, the most common win reason cited is incumbent relationship, or taking a boxing metaphor, it is

“you need to knockout the champ .”

Common Reasons for Carriers not Quoting

According to Aon GRIPSM , the most common reasons for a carrier not providing a quote for casualty/liability, automobile liability, workers

compensation, financial lines and property are: terms and conditions, underwriting concerns and pricing .

Market Insights

Aon Risk Solutions 35

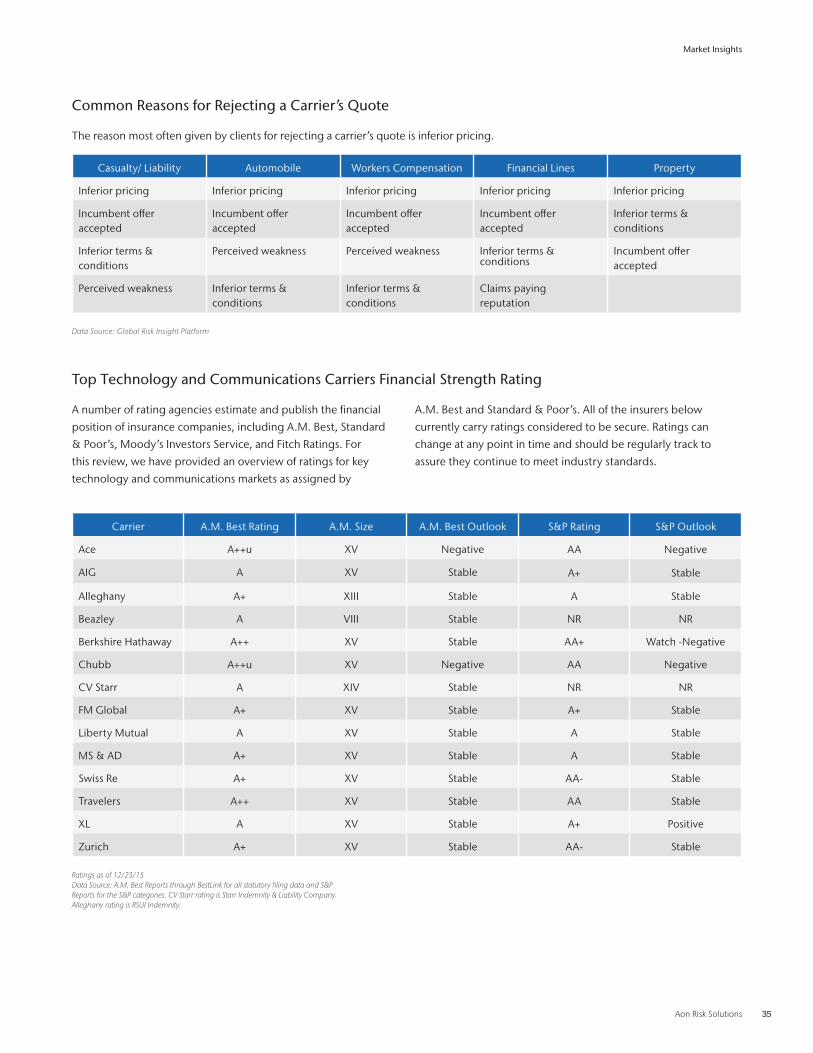

Casualty/ Liability Automobile Workers Compensation Financial Lines Property

Inferior pricing Inferior pricing Inferior pricing Inferior pricing Inferior pricing

Incumbent offer accepted

Incumbent offer accepted

Incumbent offer accepted

Incumbent offer accepted

Inferior terms & conditions

Inferior terms & conditions

Perceived weakness Perceived weakness Inferior terms & conditions

Incumbent offer accepted

Perceived weakness Inferior terms & conditions

Inferior terms & conditions

Claims paying reputation

Data Source: Global Risk Insight Platform

Common Reasons for Rejecting a Carrier’s Quote

The reason most often given by clients for rejecting a carrier’s quote is inferior pricing .

Top Technology and Communications Carriers Financial Strength Rating

A number of rating agencies estimate and publish the financial

position of insurance companies, including A .M . Best, Standard

& Poor’s, Moody’s Investors Service, and Fitch Ratings . For

this review, we have provided an overview of ratings for key

technology and communications markets as assigned by

A .M . Best and Standard & Poor’s . All of the insurers below

currently carry ratings considered to be secure . Ratings can

change at any point in time and should be regularly track to

assure they continue to meet industry standards .

Carrier A .M . Best Rating A .M . Size A .M . Best Outlook S&P Rating S&P Outlook

Ace A++u XV Negative AA Negative

AIG A XV Stable A+ Stable

Alleghany A+ XIII Stable A Stable

Beazley A VIII Stable NR NR

Berkshire Hathaway A++ XV Stable AA+ Watch -Negative

Chubb A++u XV Negative AA Negative

CV Starr A XIV Stable NR NR

FM Global A+ XV Stable A+ Stable

Liberty Mutual A XV Stable A Stable

MS & AD A+ XV Stable A Stable

Swiss Re A+ XV Stable AA- Stable

Travelers A++ XV Stable AA Stable

XL A XV Stable A+ Positive

Zurich A+ XV Stable AA- Stable

Ratings as of 12/23/15Data Source: A.M. Best Reports through BestLink for all statutory filing data and S&P Reports for the S&P categories. CV Starr rating is Starr Indemnity & Liability Company. Alleghany rating is RSUI Indemnity.

Market Insights

36 Technology and Communications Industry Report

Financial Insights

Aon Risk Solutions 37

Using August 2014 as a starting point, the share prices of

information technology have outperformed the Russell 3000

and S&P 500 Indexes while communications had weaker results

when compared to both indexes . If we compare employment

numbers for the technology and communications industry and

the overall non-farm sectors in the same time period, we can see

that of technology sector have had fewer employment issues

than the overall industry and communications sector . In terms of

annual revenue change, the Russell 3000 Index has outperformed

the technology sector nine of the last ten quarters . If you look

at the aggregate asset size of the 500 largest US technology

and communications companies since 2009 you will observe an

upward trend in total assets and an average year on year growth

rate of 10 .6 percent .

Market Performance of Technology Sector

Source: Bloomberg

80

85

90

95

100

105

110

115

120

Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15

Market Performance of Technology Sector

S&P 500 S&P 500 Informa.on Technology S&P 500 Telecommunica.on Services Russell 3000

Source: Bloomberg

S&P 500 S&P Information Technology S&P 500 Telecumication Russell 3000

Financial Insights

% Annual Employment Change

Source: Bloomberg

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep

-10

Nov

-10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

% Annual Employment Change

Total Non-Farm Employment Technology Employment Telecommunications Employment

Source: Bloomberg

Total Non-Farm Employment Technology Employment Telecommunications Employment

38 Technology and Communications Industry Report

Annual % Revenue Growth

-2%

0%

2%

4%

6%

8%

10%

12%

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Annual % Revenue Growth

Russell 3000 500 Largest US Tech Companies by Market Cap

Source: Bloomberg Total Assets (BN USD) - 500 Largest US Technology & Communications Companies

Total Assets YoY Growth

Tota

l Ass

ets

(USD

Bill

ion

s)YoY

% G

row

th

0

500

1000

1500

2000

2500

3000

0

4%

2009 2010 2011 2012 2013 2014

6%

8%

10%

12%

14%

Financial Insights

Russell 3000 500 Largest US Tech Companies by Market Cap

Source: Bloomberg

Source: Bloomberg

Aon Risk Solutions 39

ContactsTechnology and CommunicationsEric BoyumNational Practice Leader – Technology PracticeAon Risk Solutionseric .boyum@aon .com 1 .303 .639 .4120

Aon InpointGeorge M. Zsolnay IVAnalytics ManagerAon Client and Business Analyticsgeorge .zsolnay@aon .com1 .312 .381 .3955

For Media and Press InquiresCybil RoseKemper Lesnickcybil .rose@kemperlesnick .com1 .312 .755 .3537

About Aon Aon plc (NYSE:AON) is a leading global provider of risk management, insurance brokerage and reinsurance brokerage, and human resources solutions and outsourcing services. Through its more than 72,000 colleagues worldwide, Aon unites to empower results for clients in over 120 countries via innovative risk and people solutions. For further information on our capabilities and to learn how we empower results for clients, please visit: http://aon.mediaroom.com.

© Aon plc 2016. All rights reserved.The information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate profes-sional advice after a thorough examination of the particular situation.

www.aon.com

Risk. Reinsurance. Human Resources.