2016 sourcing trends & predictions

TRANSCRIPT

4Q15 Global Sourcing Advisory

Pulse Survey Results—February 10, 2016

2©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

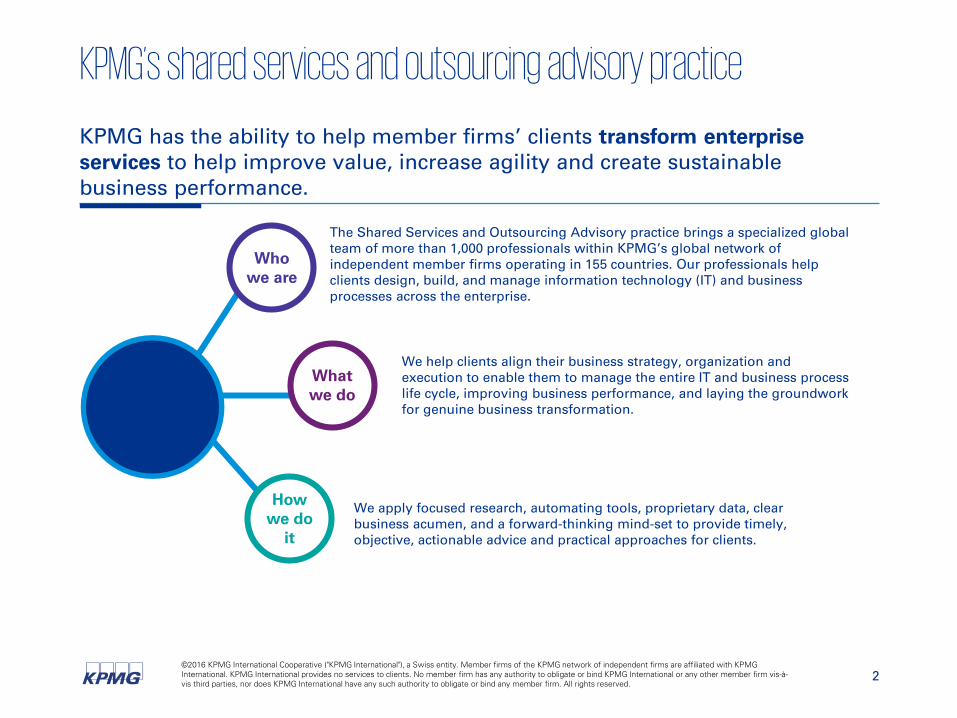

KPMG’s shared services and outsourcing advisory practice

KPMG has the ability to help member firms’ clients transform enterprise services to help improve value, increase agility and create sustainable business performance.

How we do

it

What we do

Who we are

The Shared Services and Outsourcing Advisory practice brings a specialized global team of more than 1,000 professionals within KPMG’s global network of independent member firms operating in 155 countries. Our professionals help clients design, build, and manage information technology (IT) and business processes across the enterprise.

We help clients align their business strategy, organization and execution to enable them to manage the entire IT and business process life cycle, improving business performance, and laying the groundwork for genuine business transformation.

We apply focused research, automating tools, proprietary data, clear business acumen, and a forward-thinking mind-set to provide timely, objective, actionable advice and practical approaches for clients.

3©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

4Q15 Global Sourcing Advisory Pulse Survey results

4©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

KPMG Pulse Surveys

The Global Sourcing Advisory Pulse SurveysThe surveys are a quarterly review of global business services (GBS) market trends and individual observations from the ‘front lines’.

Input sources: Topics evaluated: Primary functional focus:

— 1000+ KPMG sourcing advisors

— 12 leading global business, IT, and cloud service providers

— KPMG market research

— HfS Research

— The annual Top Trends and Predictions Pulse also polls 400+ additional KPMG executives globally across Audit, Tax and Advisory

— Drivers for GBS usage

— Demand and buying patterns

— Deal attributes

— Thematic topics for each Pulse survey

- Top trends and predictions for 2016 and beyond

— Call center/customer care

— Finance and Accounting

— Human Resources

— Information Technology

— Procurement

— Real Estate and Facilities Management

— Vertical Industry BPO

— Emerging BPO/KPO functions

* KPMG LLP (US) KPMG Holdings Limited (UK) and KPMG International acquired the business and subsidiaries of advisory firm EquaTerra, Inc. in February 2011.

Focus on performance, trends, and futures

— Launched in 2004 by EquaTerra*

— Part of a growing family of KPMG Pulse market research studies

5©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

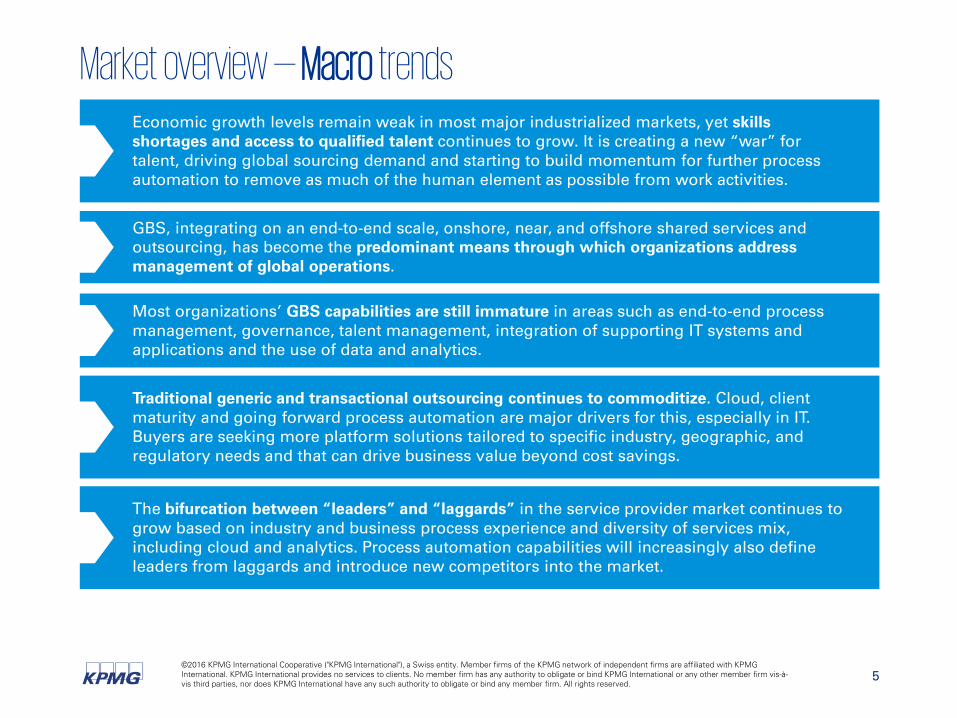

Market overview — Macro trendsEconomic growth levels remain weak in most major industrialized markets, yet skills shortages and access to qualified talent continues to grow. It is creating a new “war” for talent, driving global sourcing demand and starting to build momentum for further process automation to remove as much of the human element as possible from work activities.

GBS, integrating on an end-to-end scale, onshore, near, and offshore shared services and outsourcing, has become the predominant means through which organizations address management of global operations.

Traditional generic and transactional outsourcing continues to commoditize. Cloud, client maturity and going forward process automation are major drivers for this, especially in IT. Buyers are seeking more platform solutions tailored to specific industry, geographic, and regulatory needs and that can drive business value beyond cost savings.

The bifurcation between “leaders” and “laggards” in the service provider market continues to grow based on industry and business process experience and diversity of services mix, including cloud and analytics. Process automation capabilities will increasingly also define leaders from laggards and introduce new competitors into the market.

Most organizations’ GBS capabilities are still immature in areas such as end-to-end process management, governance, talent management, integration of supporting IT systems and applications and the use of data and analytics.

6©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Market overview — Current market trendsTalent shortages and talent management challenges - the “war” for talent - remain the top challenges facing organizations and is a driving factor for ongoing increased adoption of global business service delivery models (optimize leverage of scarce talent globally) and emerging process automation efforts (eliminate the need for talent). Concern over government gridlock remains high and worries about negative geopolitical events (i.e., terrorism) continues to grow.

As usual, top initiative cited for organizations in 2016-17 remains driving down operating costs though most firms face diminishing returns from these efforts. Seeking greater cost savings is a given for all organizations with innovative technologies such as process automation the key to taking these savings to the next level while simultaneously improving process performance.

There is a general sense of pessimism about general economic and geopolitical market conditions, but with some pockets of optimism on improving consumer demand, though this varies by sector and region and in some cases speaks to wishful thinking. Weak Eurozone growth, a renewed concern of a potential Eurozone break-up or at least fragmentation, and weak or weakening BRIC economies also drives negative market sentiment.

While process automation is a hot topic among service providers, buyers view it as a longer term opportunity, at least in terms of higher level cognitive computing. The major near term buyer technology focus is on big data, both from a technology perspective but increasingly from a talent perspective as firms recognize enabling the technology is easier than figuring out how to exploit it successfully.

Cautious buyers and increased focus on process automation, often delivered via cloud services, will create growing challenges for third-party services providers that have relied on high-skilled yet lower-cost labor as a differentiator. This is reflected in relatively weak expected pipeline growth among legacy service providers. Weak economies, tanking stock markets, and tax inversions out of the US, drive demand for alternative service delivery models to reduce costs, but shared services and global business services gain a proportionally greater focus than just pursuing outsourcing as has been the case in the past.

7©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Summary — key findings

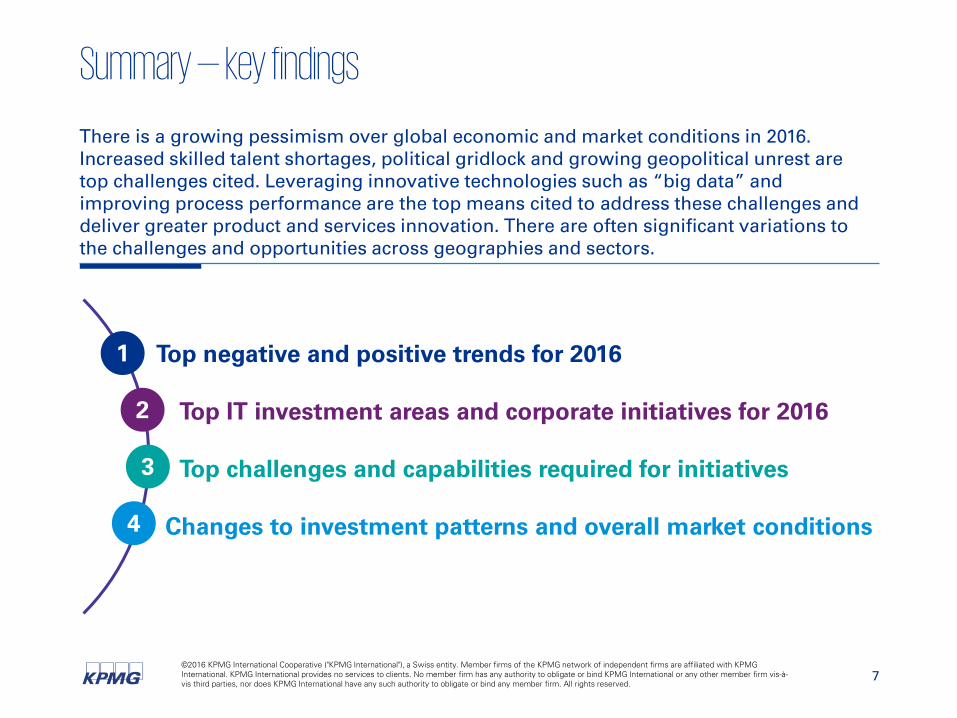

There is a growing pessimism over global economic and market conditions in 2016. Increased skilled talent shortages, political gridlock and growing geopolitical unrest are top challenges cited. Leveraging innovative technologies such as “big data” and improving process performance are the top means cited to address these challenges and deliver greater product and services innovation. There are often significant variations to the challenges and opportunities across geographies and sectors.

1

2

3

4

Top IT investment areas and corporate initiatives for 2016

Changes to investment patterns and overall market conditions

Top negative and positive trends for 2016

Top challenges and capabilities required for initiatives

8©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

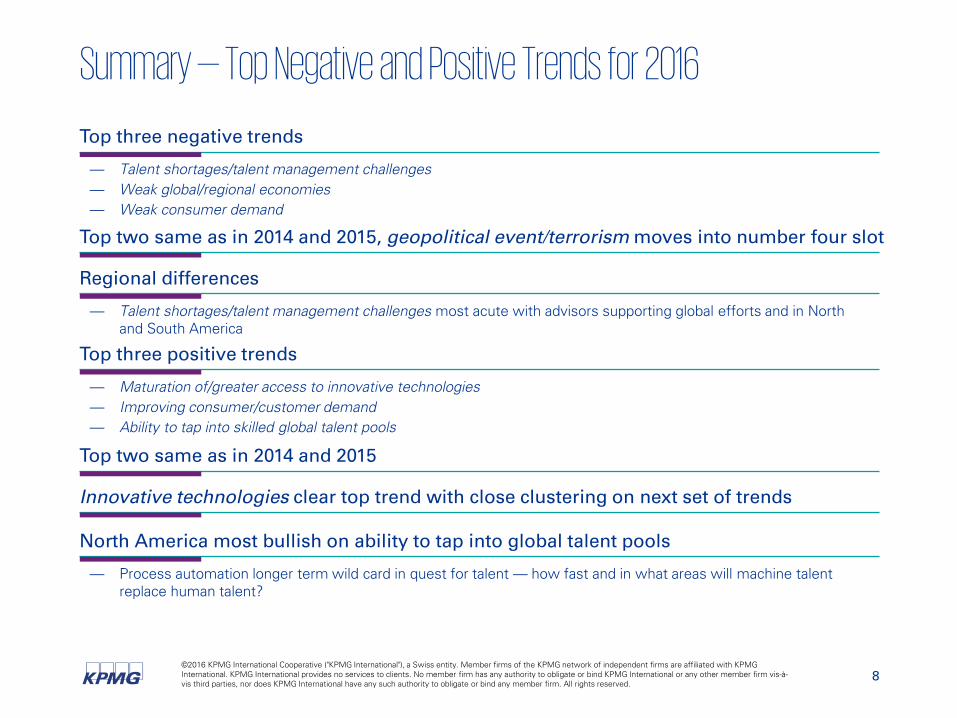

Summary — Top Negative and Positive Trends for 2016

Top three negative trends

— Talent shortages/talent management challenges— Weak global/regional economies— Weak consumer demand

Top two same as in 2014 and 2015, geopolitical event/terrorism moves into number four slot

Regional differences

— Talent shortages/talent management challenges most acute with advisors supporting global efforts and in North and South America

Top three positive trends

— Maturation of/greater access to innovative technologies— Improving consumer/customer demand— Ability to tap into skilled global talent pools

Top two same as in 2014 and 2015

Innovative technologies clear top trend with close clustering on next set of trends

North America most bullish on ability to tap into global talent pools

— Process automation longer term wild card in quest for talent — how fast and in what areas will machine talent replace human talent?

9©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

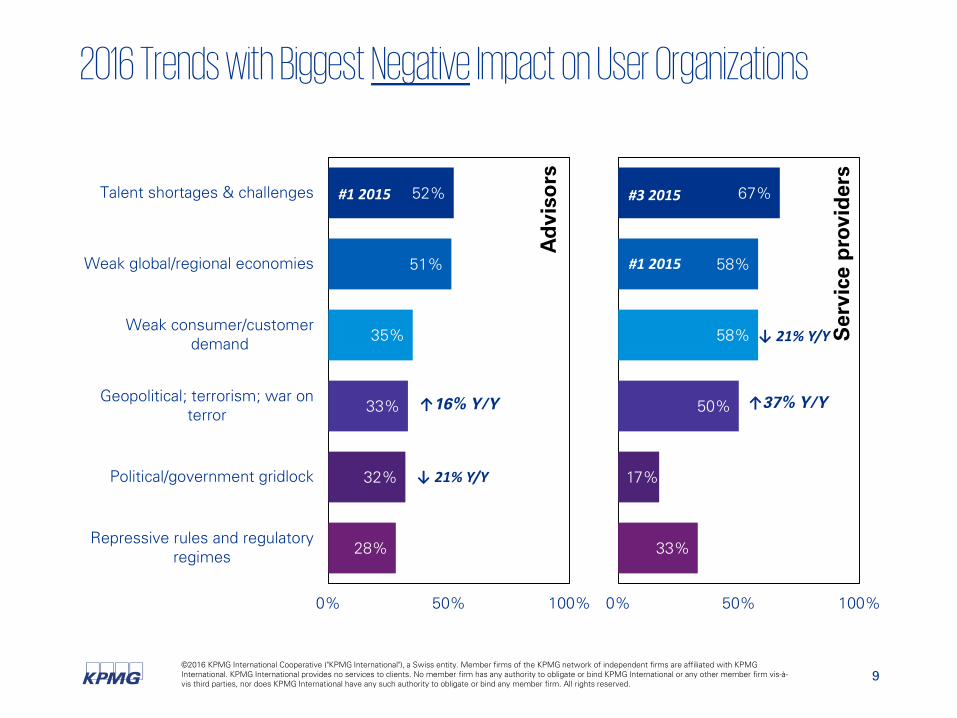

33%

17%

50%

58%

58%

67%

0% 50% 100%

2016 Trends with Biggest Negative Impact on User Organizations

28%

32%

33%

35%

51%

52%

0% 50% 100%

Repressive rules and regulatoryregimes

Political/government gridlock

Geopolitical; terrorism; war onterror

Weak consumer/customerdemand

Weak global/regional economies

Talent shortages & challenges

Ad

viso

rs

Ser

vice

pro

vid

ers

↑16% Y/Y

↓ 21% Y/Y

↑37% Y/Y

↓ 21% Y/Y

#1 2015 #3 2015

#1 2015

10©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

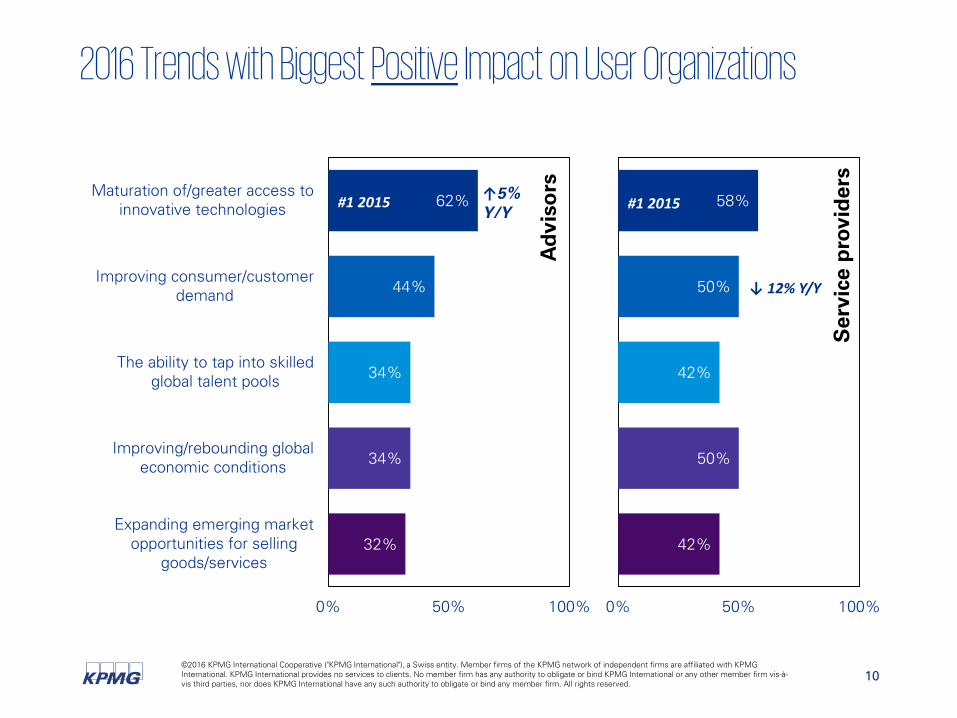

42%

50%

42%

50%

58%

0% 50% 100%

2016 Trends with Biggest Positive Impact on User Organizations

32%

34%

34%

44%

62%

0% 50% 100%

Expanding emerging marketopportunities for selling

goods/services

Improving/rebounding globaleconomic conditions

The ability to tap into skilledglobal talent pools

Improving consumer/customerdemand

Maturation of/greater access toinnovative technologies

Ad

viso

rs

Ser

vice

pro

vid

ers

↓ 12% Y/Y

#1 2015#1 2015 ↑5% Y/Y

11©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

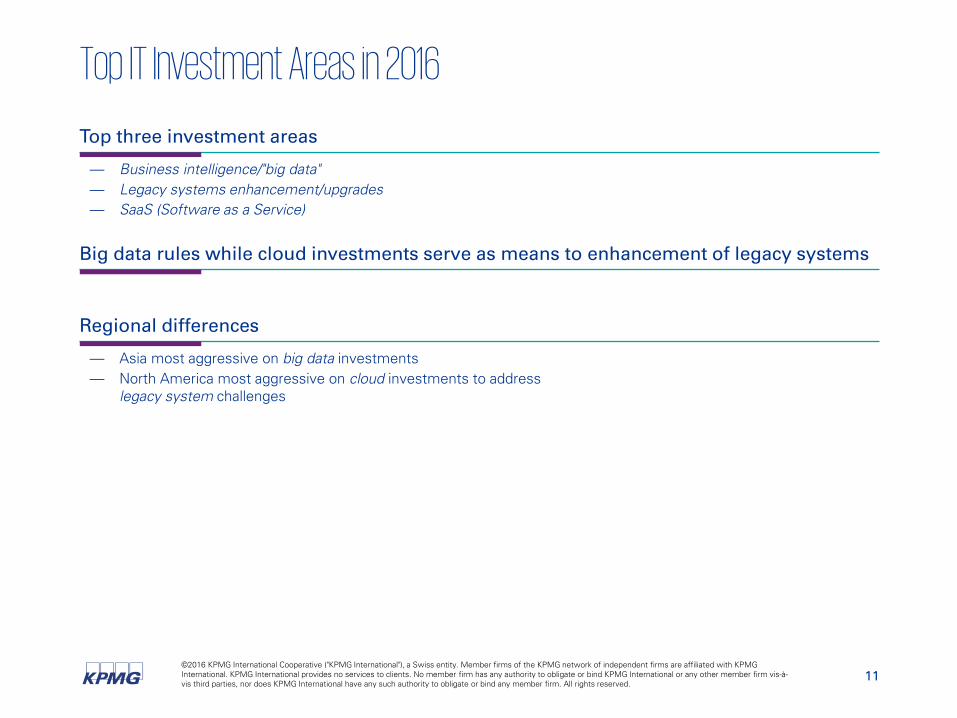

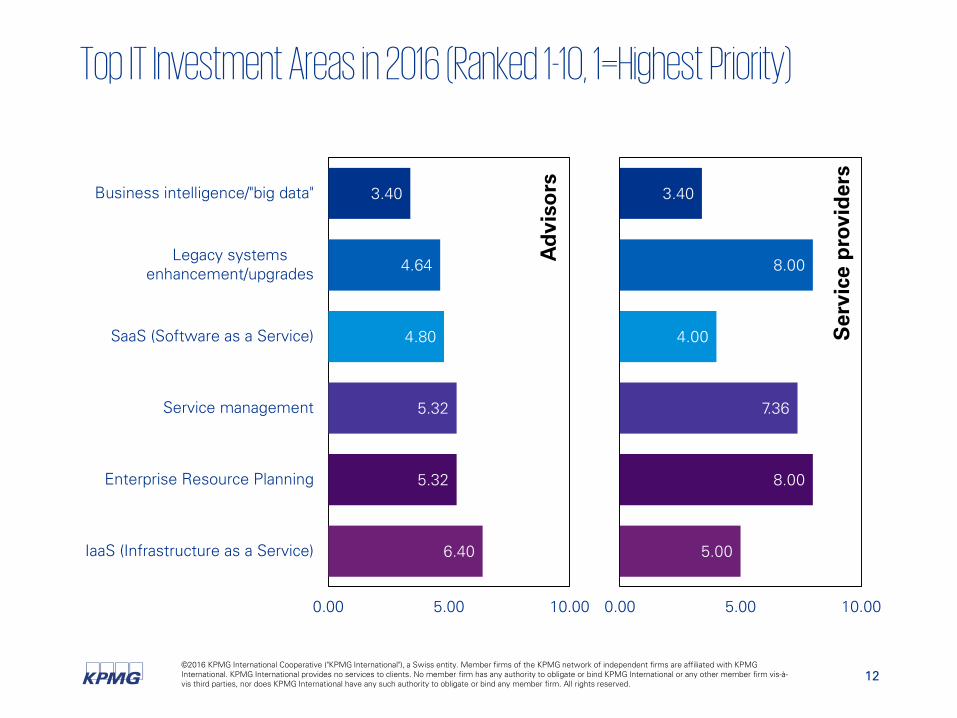

Top IT Investment Areas in 2016

Top three investment areas

— Business intelligence/"big data"— Legacy systems enhancement/upgrades— SaaS (Software as a Service)

Big data rules while cloud investments serve as means to enhancement of legacy systems

Regional differences

— Asia most aggressive on big data investments— North America most aggressive on cloud investments to address

legacy system challenges

12©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

5.00

8.00

7.36

4.00

8.00

3.40

0.00 5.00 10.00

Top IT Investment Areas in 2016 (Ranked 1-10, 1=Highest Priority)

6.40

5.32

5.32

4.80

4.64

3.40

0.00 5.00 10.00

IaaS (Infrastructure as a Service)

Enterprise Resource Planning

Service management

SaaS (Software as a Service)

Legacy systemsenhancement/upgrades

Business intelligence/"big data"

Ad

viso

rs

Ser

vice

pro

vid

ers

13©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

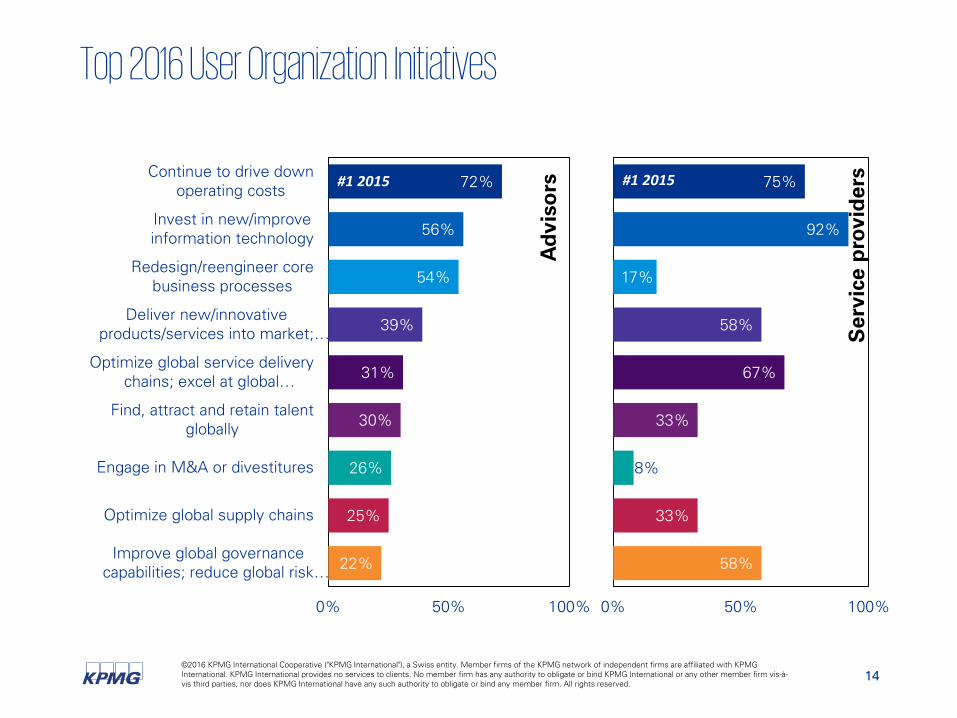

Top 2016 User Organization Initiatives

Top three initiatives

— Continue to drive down operating costs— Invest in new/improve information technology— Redesign/reengineer core business processes

Top three same as in 2014 and 2015

Regional differences

— North America most aggressive on process redesign and reengineering

— Drive down operating costs a common priority globally

14©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Top 2016 User Organization Initiatives

22%

25%

26%

30%

31%

39%

54%

56%

72%

0% 50% 100%

Improve global governancecapabilities; reduce global risk…

Optimize global supply chains

Engage in M&A or divestitures

Find, attract and retain talentglobally

Optimize global service deliverychains; excel at global…

Deliver new/innovativeproducts/services into market;…

Redesign/reengineer corebusiness processes

Invest in new/improveinformation technology

Continue to drive downoperating costs

Ad

viso

rs

Ser

vice

pro

vid

ers

58%

33%

8%

33%

67%

58%

17%

92%

75%

0% 50% 100%

#1 2015#1 2015

15©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

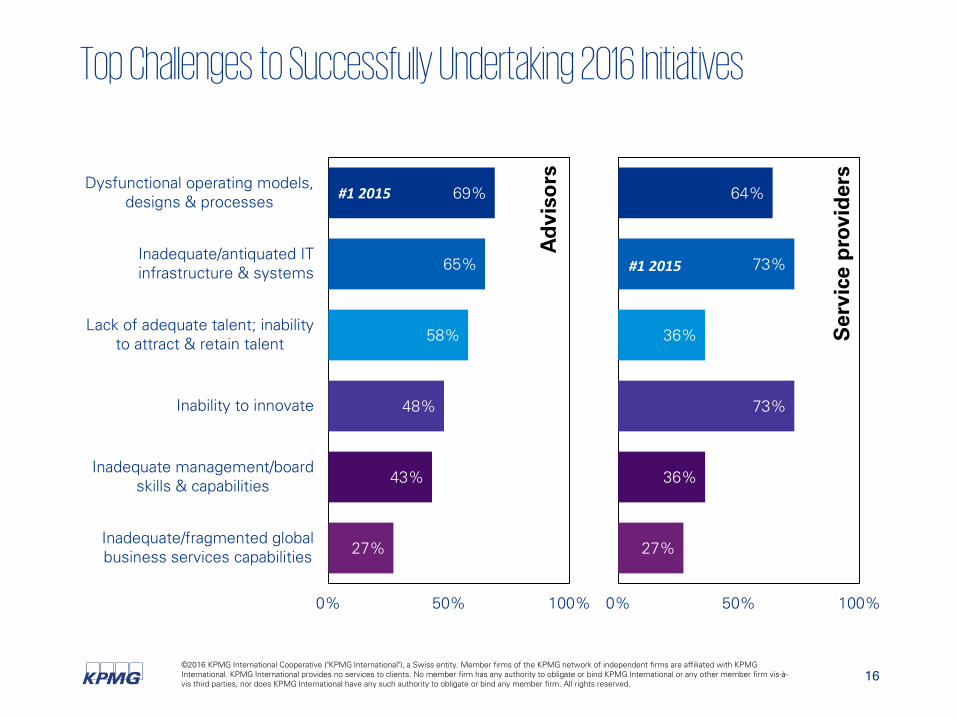

Top Challenges to Successfully Undertaking 2016 Initiatives

Top three challenges

— Dysfunctional/fragmented organizational/operating models, designs and processes— Inadequate/antiquated IT infrastructure and systems— Lack of adequate and skilled talent; inability to attract and retain talent

Top three same as in 2014 and 2015

— Lack of adequate and skilled talent; inability to attract and retain talent continues to grow as a problem, up five percent year over year

Regional differences

— North America most concerned about lack of adequate and skilled talent; inability to attract and retain talent

— Inadequate/antiquated IT infrastructure and systems a common problem globally

16©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Top Challenges to Successfully Undertaking 2016 Initiatives

27%

36%

73%

36%

73%

64%

0% 50% 100%

27%

43%

48%

58%

65%

69%

0% 50% 100%

Inadequate/fragmented globalbusiness services capabilities

Inadequate management/boardskills & capabilities

Inability to innovate

Lack of adequate talent; inabilityto attract & retain talent

Inadequate/antiquated ITinfrastructure & systems

Dysfunctional operating models,designs & processes

Ad

viso

rs

Ser

vice

pro

vid

ers

#1 2015

#1 2015

17©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

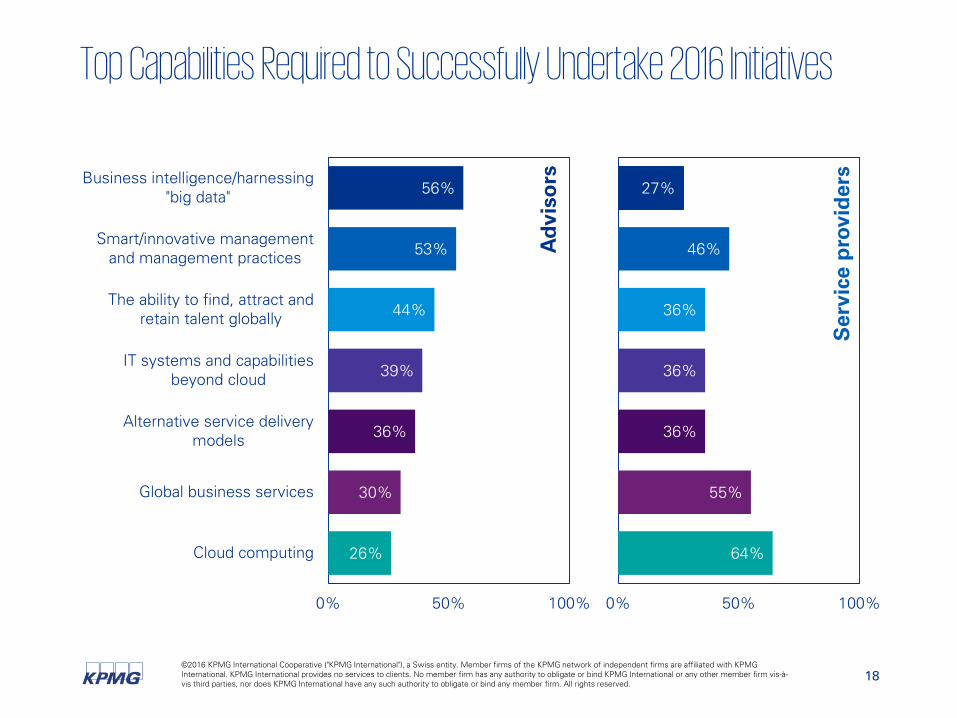

Top Capabilities Required to Successfully Undertake 2016 Initiatives

Top three required factors and capabilities

— Business intelligence/harnessing "big data"— Smart/innovative management and management practices— The ability to find and attract talent globally

Shifting of top perceived required capabilities

— Big data moves past smart/innovative management to take top spot— Global talent moves up into top three

Regional differences

— Business intelligence/harnessing "big data” especially important in Europe, Middle East and Africa, and Asia Pac, much more so than in 2015

— The ability to find, attract and retain talent globally most relevant in North America and Middle East and Africa

Major differences of opinion between advisors and service providers

18©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Top Capabilities Required to Successfully Undertake 2016 Initiatives

26%

30%

36%

39%

44%

53%

56%

0% 50% 100%

Cloud computing

Global business services

Alternative service deliverymodels

IT systems and capabilitiesbeyond cloud

The ability to find, attract andretain talent globally

Smart/innovative managementand management practices

Business intelligence/harnessing"big data"

Ad

viso

rs

Ser

vice

pro

vid

ers

64%

55%

36%

36%

36%

46%

27%

0% 50% 100%

19©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Additional Results

Top IT investment areas for 2016

— D&A software and services— D&A staff and resources— Cloud infrastructure

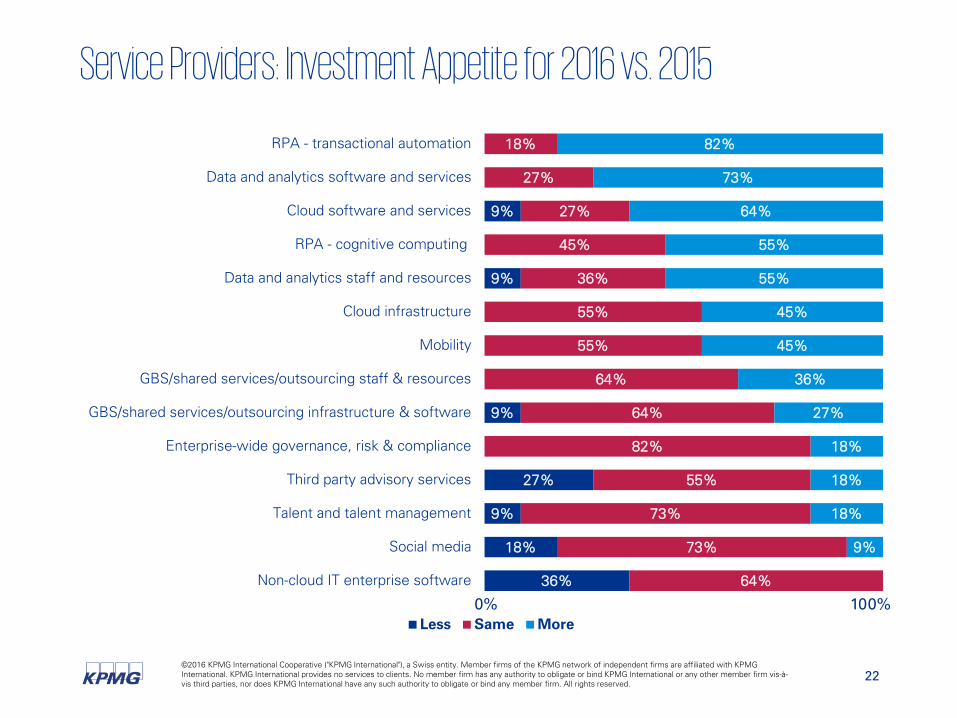

Service providers very bullish on robotics process automation (RPA)

Most positive market trends areas (though in general there is much pessimism on general market trends over the coming two years)

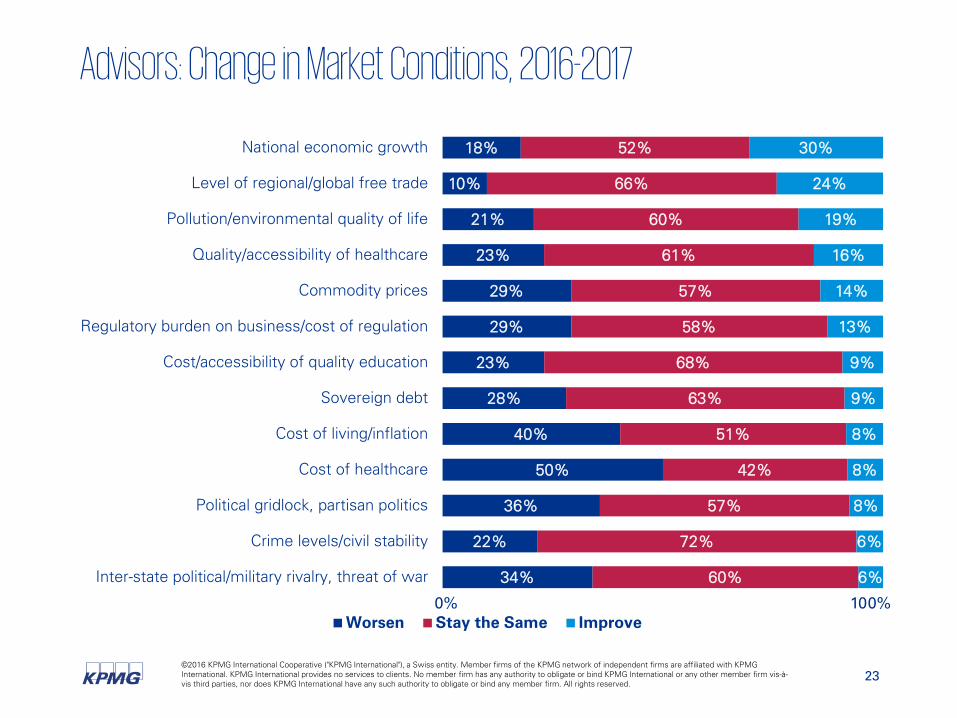

— National economic growth— Level of regional/global free trade— Pollution/environmental quality of life

Some differences in investments by geography and major differences on market trends by geography

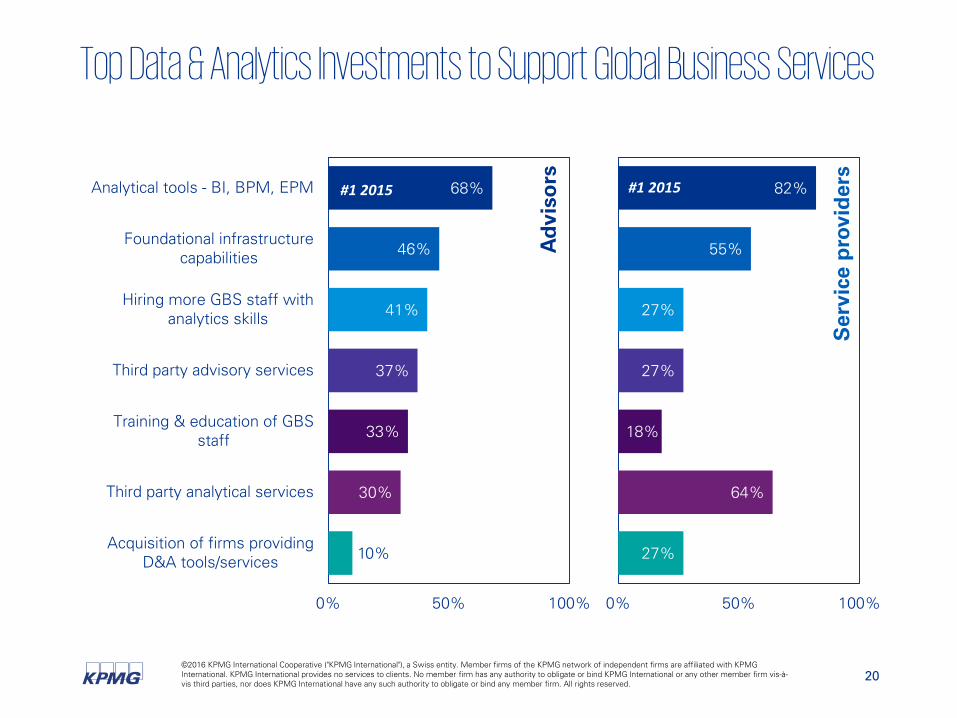

Top D&A investment are to support GBS is analytical tools, same as in 2015

20©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Top Data & Analytics Investments to Support Global Business Services

10%

30%

33%

37%

41%

46%

68%

0% 50% 100%

Acquisition of firms providingD&A tools/services

Third party analytical services

Training & education of GBSstaff

Third party advisory services

Hiring more GBS staff withanalytics skills

Foundational infrastructurecapabilities

Analytical tools - BI, BPM, EPM

Ad

viso

rs

Ser

vice

pro

vid

ers

27%

64%

18%

27%

27%

55%

82%

0% 50% 100%

#1 2015#1 2015

21©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

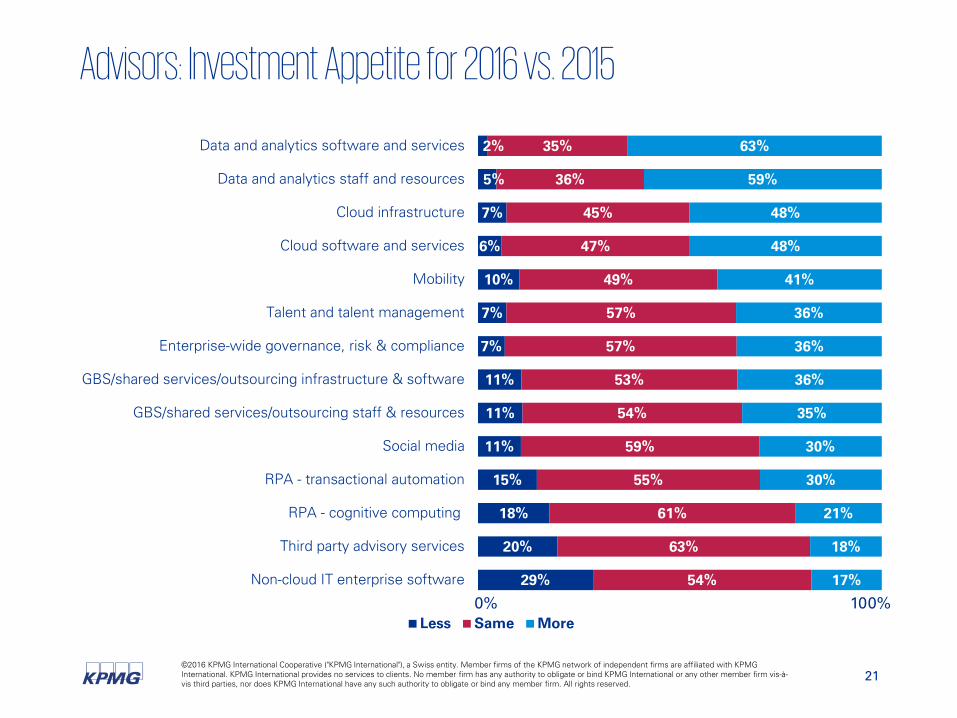

Advisors: Investment Appetite for 2016 vs. 2015

29%

20%

18%

15%

11%

11%

11%

7%

7%

10%

6%

7%

5%

2%

54%

63%

61%

55%

59%

54%

53%

57%

57%

49%

47%

45%

36%

35%

17%

18%

21%

30%

30%

35%

36%

36%

36%

41%

48%

48%

59%

63%

Non-cloud IT enterprise software

Third party advisory services

RPA - cognitive computing

RPA - transactional automation

Social media

GBS/shared services/outsourcing staff & resources

GBS/shared services/outsourcing infrastructure & software

Enterprise-wide governance, risk & compliance

Talent and talent management

Mobility

Cloud software and services

Cloud infrastructure

Data and analytics staff and resources

Data and analytics software and services

Less Same More0% 100%

22©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Service Providers: Investment Appetite for 2016 vs. 2015

36%

18%

9%

27%

9%

9%

9%

64%

73%

73%

55%

82%

64%

64%

55%

55%

36%

45%

27%

27%

18%

9%

18%

18%

18%

27%

36%

45%

45%

55%

55%

64%

73%

82%

Non-cloud IT enterprise software

Social media

Talent and talent management

Third party advisory services

Enterprise-wide governance, risk & compliance

GBS/shared services/outsourcing infrastructure & software

GBS/shared services/outsourcing staff & resources

Mobility

Cloud infrastructure

Data and analytics staff and resources

RPA - cognitive computing

Cloud software and services

Data and analytics software and services

RPA - transactional automation

Less Same More0% 100%

23©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Advisors: Change in Market Conditions, 2016-2017

34%

22%

36%

50%

40%

28%

23%

29%

29%

23%

21%

10%

18%

60%

72%

57%

42%

51%

63%

68%

58%

57%

61%

60%

66%

52%

6%

6%

8%

8%

8%

9%

9%

13%

14%

16%

19%

24%

30%

Inter-state political/military rivalry, threat of war

Crime levels/civil stability

Political gridlock, partisan politics

Cost of healthcare

Cost of living/inflation

Sovereign debt

Cost/accessibility of quality education

Regulatory burden on business/cost of regulation

Commodity prices

Quality/accessibility of healthcare

Pollution/environmental quality of life

Level of regional/global free trade

National economic growth

Worsen Stay the Same Improve0% 100%

24©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

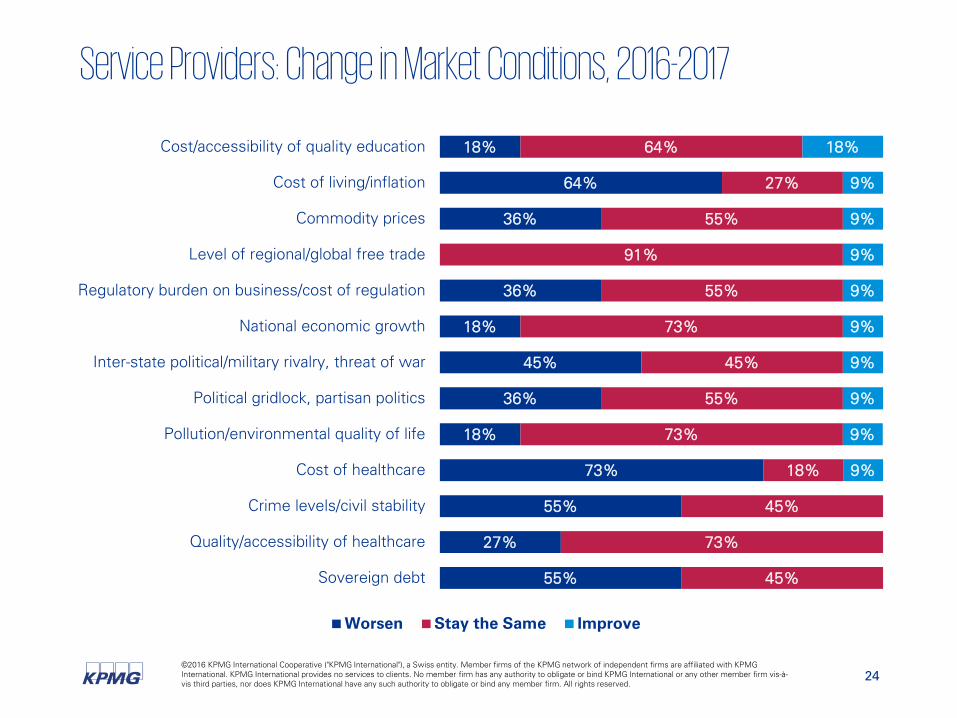

Service Providers: Change in Market Conditions, 2016-2017

55%

27%

55%

73%

18%

36%

45%

18%

36%

36%

64%

18%

45%

73%

45%

18%

73%

55%

45%

73%

55%

91%

55%

27%

64%

9%

9%

9%

9%

9%

9%

9%

9%

9%

18%

Sovereign debt

Quality/accessibility of healthcare

Crime levels/civil stability

Cost of healthcare

Pollution/environmental quality of life

Political gridlock, partisan politics

Inter-state political/military rivalry, threat of war

National economic growth

Regulatory burden on business/cost of regulation

Level of regional/global free trade

Commodity prices

Cost of living/inflation

Cost/accessibility of quality education

Worsen Stay the Same Improve

25©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

David J. BrownGlobal Lead, Shared Services and Outsourcing AdvisoryKPMG LLP (US)E: [email protected]

Thank youFor more information visit: www.kpmg.com/2016SourcingTrends

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

kpmg.com/socialmedia kpmg.com/app