2016 outlook in dire straits - nigeria’s no1 economy · pdf file2 research in dire...

TRANSCRIPT

2016 OUTLOOK – IN DIRE STRAITS

JANUARY 14, 2016

2

RESEARCH

In Dire Straits

2016 Outlook

Global Economy – Weak EM Outlook threatens Global Growth Very strong headwinds threaten the overall global economic outlook for 2016. China’s

economic growth has slowed to its lowest in 25 years and low commodity prices

continue to have far reaching implications for growth in other emerging and developing

nations. On the flipside, advanced economies, following reasonable signs of recovery,

are forecast to be at the forefront of global growth in 2016. The International Monetary

Fund (IMF) forecasts global growth at 3.6% noting downside concerns including China’s

new growth model, increased volatility across global financial markets and geopolitical

tensions in the Middle East and parts of Africa. The IMF however sees a potential boost

to global consumption especially in advanced economies, given the muted consumption

response to lower commodity prices in 2015.

Nigeria – High Expectations in Tough Times With oil price at a 12 year low ($31 per barrel), a weakening balance of payment

position (down 38% YoY as at Q3’15), and projections of even lower oil price – Nigeria

faces very tough choices in 2016, key amongst which is currency adjustment and

controlled deregulation of the downstream sector. The interplay of fiscal, monetary and

exchange rate policies will determine growth trajectory in 2016 even as the government

pursues an expansionary budget of N6.07 trillion – $30 billion (with over N2 trillion –

$10 billion deficit) and the central bank pushes easing measures to drive output growth.

Inflationary concerns are paramount, given the uptick in prices throughout 2015. We

project an average inflation rate of 11% in 2016 and a real GDP growth rate in the range

of 2% - 4% with the higher end of the range highly dependent on flexibility to the

current exchange rate regime and improved FX supply. In hindsight, government will

need to pay particular attention to ongoing socio-political tensions including the Boko

Haram insurgency in the Northeast the recent clash between the country’s troops and

the ‘Shiite’ Muslims across the North and other sectional agitations.

Oil Price Correction: the One Vital Catalyst for Market Rebound Despite attractive valuations, the reversal of fortunes for the equities market in 2016

will depend on currency adjustment and a sustained rebound in crude oil price. Given

current depressed prices, dividend yield looks attractive; hence the equity market may

see some respite in Q1 end/early Q2 as local participants position ahead of FY 2015

dividends. Notwithstanding the easing measures of the central bank which resulted in

the correction of the yield curve in Q4’15, the outlook for bond yields is dependent on

the interplay between demand and supply.

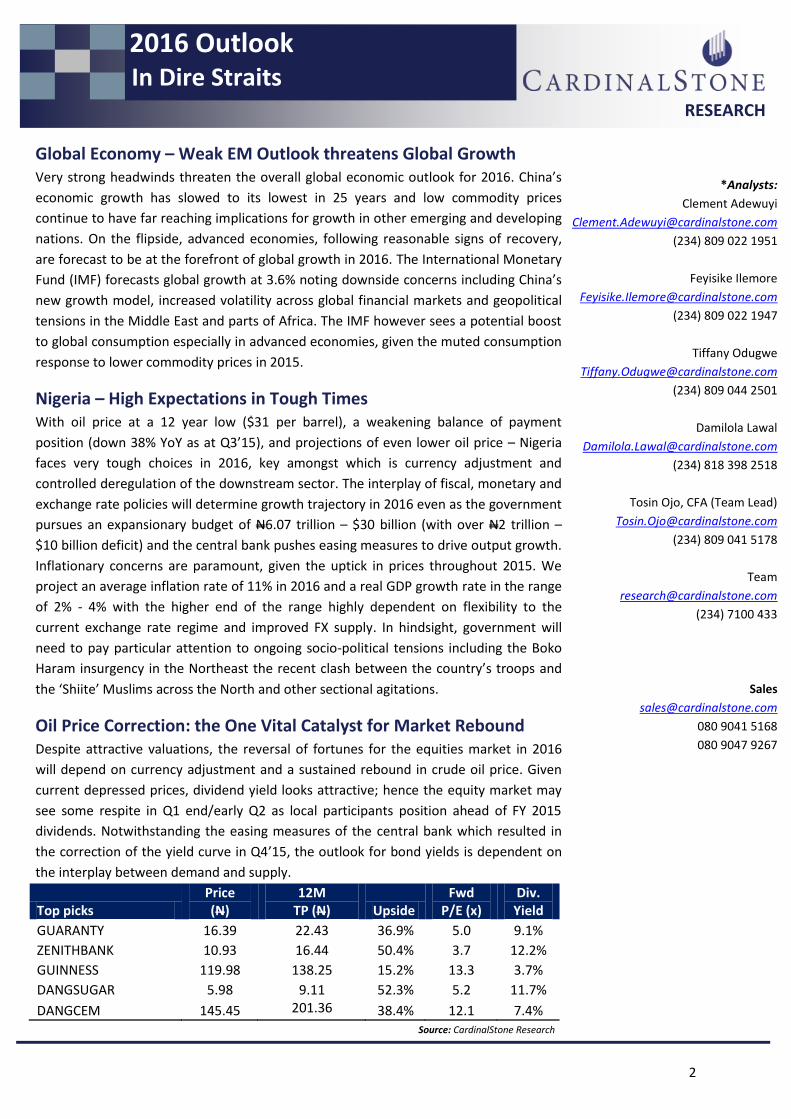

Top picks Price (N)

12M TP (N) Upside

Fwd P/E (x)

Div. Yield

GUARANTY 16.39 22.43 36.9% 5.0 9.1%

ZENITHBANK 10.93 16.44 50.4% 3.7 12.2%

GUINNESS 119.98 138.25 15.2% 13.3 3.7%

DANGSUGAR 5.98 9.11 52.3% 5.2 11.7%

DANGCEM 145.45 201.36 38.4% 12.1 7.4%

*Analysts:

Clement Adewuyi

(234) 809 022 1951

Feyisike Ilemore

(234) 809 022 1947

Tiffany Odugwe

(234) 809 044 2501

Damilola Lawal

(234) 818 398 2518

Tosin Ojo, CFA (Team Lead)

(234) 809 041 5178

Team

(234) 7100 433

Sales

080 9041 5168

080 9047 9267

Source: CardinalStone Research

3

RESEARCH

In Dire Straits

2016 Outlook

Table of Contents

Summary ..................................................................................................................................... 2

Recommendation snapshot ................................................................................................................ 3

Global Economy: Increased economic integration threatens global recovery ...................................... 3

Advanced Economies – On the path to recovery ............................................................................... 3

Emerging and Developing Economies ................................................................................................. 3

Commodities – Lower for long ........................................................................................................... 5

Agriculture .......................................................................................................................................... 6

Nigerian Economy: High Expectations in Tough Times ................................................................... 6

Social Democracy Model ..................................................................................................................... 6

Monetary Policy and the Economy ..................................................................................................... 9

Fiscal Policy and the Masses ............................................................................................................. 11

Equities - Market Return heavily Dependent on Macro Events ..................................................... 13

Fixed Income – Yields, What Direction in 2016? ........................................................................... 24

Banking Sector – Murky Waters – Time to be Cautious ...................................................................... 32

Insurance Sector – Premium Growth Threatened in 2016................................................................... 46

Consumer Goods Sector – Many Moving Parts – Mixed Outlook ................................................... 48

Industrial Goods Sector – Budget Allocation to CAPEX supports Construction Outlook ................... 52

Energy Sector – Power and Oil & Gas ........................................................................................... 55

Agriculture Sector – Still a Priority Sector for the Buhari Government ........................................... 58

Companies ................................................................................................................................ 60

Appendix .................................................................................................................................. 76

Financial Statements and Key Ratios ................................................................................................ 77

Disclosure and Disclaimer .............................................................................................................. 107

4

RESEARCH

In Dire Straits

2016 Outlook

*NW – Negative Watch List

Company Ticker Rating TP (N) Current

Price1 (N)

Up/ Mkt Cap (N'Bn)

2016F P/E

2016F D/ Y Down Side

Financial Services

AIICO Buy 1.58 0.90 76% 6.24 2.3x 13.2%

UBA Buy 5.46 2.79 96% 101.22 1.8x 17.8%

ZENITHBANK Buy 16.44 10.93 50% 343.16 3.7x 12.2%

ACCESS Buy 6.00 4.37 37% 126.42 3.0x 11.8%

GUARANTY Buy 22.43 16.39 37% 482.38 5.0x 9.1%

DIAMONDBNK Buy 2.68 2.00 34% 46.32 3.0x 10.2%

CUSTODYINS Buy 5.59 4.20 33% 24.70 5.6x 5.0%

FBNH Buy 5.07 3.99 27% 143.22 2.3x 6.6%

STANBIC Buy 17.72 14.25 24% 142.50 8.4x 5.3%

STERLNBANK Buy 2.10 1.79 17% 51.53 5.4x 7.5%

FIDELITYBK Hold 1.48 1.30 14% 37.67 2.9x 8.5%

ETI Hold 16.79 16.15 4% 296.35 4.7x 6.3%

FCMB *NW N/A 1.36 N/A 26.93 1.4x 27.5%

Consumer Goods

FLOURMILL Buy 66.08 19.76 234% 51.85 22.5x 2.4%

UACN Buy 31.62 18.59 70% 35.71 7.6x 6.5%

DANGSUGAR Buy 9.11 5.98 52% 71.76 5.2x 11.7%

NB Buy 140.12 97.18 44% 770.55 16.7x 3.9%

GUINNESS Buy 138.25 119.98 15% 180.68 13.3x 3.7%

PZ Hold 24.14 21.13 14% 83.90 18.8x 3.2%

NESTLE Sell 763.92 779.00 -2% 617.48 23.8x 2.5%

UNILEVER Sell 15.41 43.25 -64% 163.63 104.0x 0.9%

Industrial Goods

DANGCEM Buy 201.36 145.45 38% 2,478.54 12.1x 7.4%

WAPCO Hold 99.05 91.31 8% 415.91 10.5x 2.9%

Oil & Gas

SEPLAT Buy 312.79 196.07 60% 110.47 5.4x 10.7%

TRANSCORP Sell 1.02 1.14 -11% 44.14 21.8x 1.9%

MOBIL Sell 133.19 151.20 -12% 54.52 9.6x 4.0%

TOTAL Sell 130.47 155.92 -16% 52.94 13.7x 3.2%

OANDO *NW N/A 4.64 N/A 55.84 18.8x 0.0%

Agriculture

PRESCO Hold 32.88 33.00 0% 33.00 5.8x 3.2%

OKOMUOIL Sell 32.02 32.64 -2% 31.14 14.0x 3.3%

Stock Recommendations Overview

Source: CardinalStone Research

5

RESEARCH

In Dire Straits

2016 Outlook

Macro & Markets

6

RESEARCH

In Dire Straits

2016 Outlook

Global Economic Outlook

Weak EM outlook threatens global growth

If there was any doubt before, the year 2015 has shown that the world is more

integrated than ever. The drop in crude oil prices and slowdown in China’s growth have

had far reaching implications for emerging and developing nations in particular, and also

the more advanced nations. Brazil and Russia, two of the BRIC1 nations expected to be

at the forefront of economic growth, slipped into recessions in 2015 due to weak oil

exports, while Chinese GDP growth slowed to an average of 7.0% in 9M’15 - it’s lowest

pace of growth in 25 years. Sub Saharan African economies continue to be hindered by

low commodity prices and will be focused on steering their economies through a weak

global outlook in 2016 while dealing with depreciating currencies. The more advanced

economies especially the United States, previously viewed as ill-equipped to drive

growth in 2015/2016, are now, following reasonable signs of recovery this year since

the 2013 financial crisis, expected to significantly contribute to global growth in 2016.

Broadly reflecting these growth expectations, the IMF recently cut its global growth

forecast for 2016 to 3.6% from 3.8%. The IMF cited increasing downside concerns such

as the increasing difficulty for China in its transition to a new model of growth;

increasing financial market volatility across the globe; and likely economic spill-overs

from increasing geopolitical tensions in the Middle East, and parts of Africa. On the

positive side, the IMF however noted the muted consumption response to lower oil

prices so far, forecasting a greater boost to global consumption in 2016 especially in

more advanced economies.

Advanced Economies – On the path to recovery: While the US (average YoY

GDP growth of 2.2% in 9M’15) has raised rates for the first time in a decade, Japan and

the Eurozone (average GDP growth of 0.2% and 0.4% in 9M’15 respectively) continue

with their asset purchase programs designed to stimulate their respective economies.

The US is clearly on a path of sustained recovery with six consecutive quarters of strong

GDP growth since Q1’14. Weak inflation however remains a concern in the US (inflation

has averaged 0.03% in the first 9mths of 2015), a theme that has played out across most

other developed nations and is being attributed to the sharp decline in crude oil prices.

The United Kingdom also remains on track for modest growth with consumer sentiment

and housing prices in 2015 increasing the likelihood of further growth in 2016. The euro

area’s expansionary program ($65.2 billion monthly asset purchase until September

2016) however seems to be having a delayed effect with mixed growth in Germany and

France evident in the first half of 2015. The IMF has therefore revised its 2016 growth

projection slightly downwards for the euro area to 1.6% from 1.7% previously.

1 1The BRIC nations- Brazil, Russia, India and China- are emerging market economies considered to be at

very advanced stages of economic development, expected to drive global growth in the medium to long

term

For Advanced economies,

2016 is forecast to be a year

of recovery

Global growth for 2016

remains threatened by a

number of downside risks

7

RESEARCH

In Dire Straits

2016 Outlook

The continued influx of refugees from war torn Syria and the Middle East could however

be a blessing in disguise, helping to stimulate rather than hinder economic growth,

forcing euro area countries to spend money on refugees which will eventually filter

through the economy. Overall, despite the sluggish pace of recovery in more advanced

nations, especially in Japan where GDP growth remains muted amidst weak consumer

demand, the IMF forecasts GDP growth of 2.2% for advanced economies in 2016, higher

than the growth rate of 2.0% expected for 2015.

Emerging and Developing Economies – Slowdown complicated by

increased global integration: Perhaps underestimated at first, China’s slowing

growth, a fallout of its deliberate move from an investment-driven, export-driven

economic model to a consumption-driven one, has led to serious repercussions for

emerging markets. China, the largest world exporter and second largest importer, has

seen both its imports and exports dwindle in line with this new economic era. The IMF

forecasts growth of 6.3% for China in 2016 which will even be slower than expected

growth in 2015. The peculiarities of the Chinese economy - centrally planned, with

significant government influence especially in the banking sector - make it unlikely that

growth will accelerate in 2016 especially if the government continues to moderate its

previous reckless spending. As a result, Emerging and Developing economies who

typically conduct a lot of trade with China will see their economic growth and foreign

exchange earnings shrink.

The drop in crude oil price has put an even bigger strain on growth of oil exporting

countries. Large oil producing nations like Russia and Brazil slipped into recessions in

2015 and will have to focus on deep structural reforms to foster a recovery in 2016; the

IMF forecasts weak GDP growth in these economies in 2016. Elsewhere, India is

expected to continue on its current growth trajectory, driven by increasing exports and

a pickup in investments following recent policy reforms. Growth in Sub-Saharan Africa is

expected to average 4.3% in 2016 (compared to an earlier forecast of 5.1%) according to

the IMF. The pace of policy adjustments to current economic realities – falling

commodity prices and a soon-to-be less favourable external environment shapes the

economic outlook for the region in 2016. Fiscal policies will need to be guided by

medium term expenditure frameworks that strike a balance between debt sustainability

and addressing development needs while monetary policies will need to be

accommodative, paying attention to the effect of global shocks on the economy and

allowing for exchange rate depreciations that can absorb the shocks.

Overall, capital inflows to emerging and developing economies have slowed,

exacerbating growth concerns, with investors seeking home comfort and a continuous

lift-off in the US’ fed rate. The IMF however remains relatively bullish on developing

nations’ growth in 2016, forecasting growth of 4.5% in 2016 which represents an

increase in 2015 expected growth of 4.0%.

A combination of weak

commodity prices and

China’s transition to a

consumption-led economy is

likely to place a cap on

growth in emerging

economies

8

RESEARCH

In Dire Straits

2016 Outlook

Commodities – Lower for longer

Commodity prices are expected to remain depressed in 2016 due to a combination of

oversupply and weak demand. While oil prices have mostly been affected by increased

supply from North America and the decision by OPEC not to restrict output, the prices of

base metals have predominantly been affected by weak demand from China. China is

the largest importer of base metals (copper, iron, aluminium nickel) controlling c.50% of

the entire world market for metal imports and thus, the slowdown in China has

significantly affected metal prices. The IMF expects metal prices to decline by c.22% in

2015 (the World Bank expects a 20% decline).

Energy – Strong negative outlook for crude oil price: The IMF and World Bank

are aligned on expectations of weak crude oil prices in 2016 (IMF-$50.4/bbl; World

Bank- $51/bbl on average) mostly informed by expectations of slowed global growth

(particularly in China and emerging markets) and Iran scaling up production in 2016

after an agreement with the P5 + 1 (US, Britain, Russia, China, France and Germany) to

limit Iranian nuclear activity in return for the lifting of imposed sanctions. The

international agreement on Iran’s nuclear program is to be implemented in the first half

of 2016 when Iran is likely to ramp up crude oil production by up to 0.5-0.7mbpd, taking

the country’s oil production to 2011 pre-sanction levels of 3.6mbpd. Iran is also

expected to immediately start selling 40million bbl of oil currently available in its

floating storage. According to the World Bank, although U.S production is expected to

decline moderately in 2016, helping to reduce current surplus and rebalance the

market, the pace of demand and supply will determine how quickly a rebalancing will

occur.

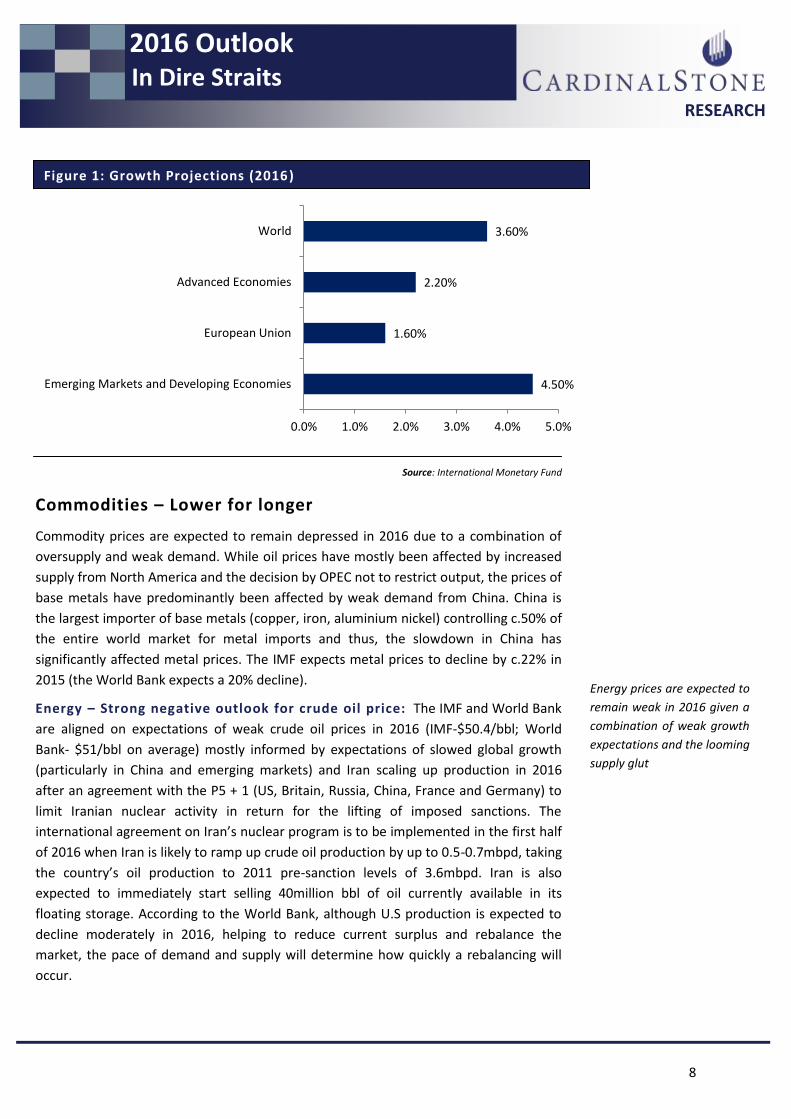

4.50%

1.60%

2.20%

3.60%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

Emerging Markets and Developing Economies

European Union

Advanced Economies

World

Figure 1: Growth Projections (2016)

Source: International Monetary Fund

Energy prices are expected to

remain weak in 2016 given a

combination of weak growth

expectations and the looming

supply glut

9

RESEARCH

In Dire Straits

2016 Outlook

With OPEC, in its December 2015 meeting, stating that there will be no supply cuts in

2016 unless non-OPEC oil producing nations agree to cooperate, the outlook for oil

prices remains firmly negative.

Agriculture – Oversupply to weigh down food prices: In the agricultural

commodities market, modest growth in the euro area and the US especially (large

exporters of agricultural produce) has led supply of agricultural commodities to outstrip

demand. Consequently, prices continue to decline with the World Bank’s Food

Commodity Price Index expected to average about 15 percent lower for 2015 compared

to 2014 and growing only marginally by 2 percent in 2016. The World Bank forecasts

rising global stocks of edible oils, meals, and grains next year which are likely to keep

agricultural commodity prices depressed in 2016. Overall, with China determined to

stay on its new growth path, and prospects for economic growth in the US and Euro

area modest at best, metals, oil, and agricultural commodity prices will likely fluctuate

around current lows in 2016 – reinforcing an overall weak outlook for global growth.

Commodity Unit 2014 2015 2016

Crude oil avg. spot $/bbl 96.2 52.5 51.4

Grains – Wheat $/mt 285 205.0 201.0

Oils & meals Soybeans $/mt 492 390.0 401.0

Other food – Sugar $/kg 0.37 0.29 0.29

Figure 2: Average price forecast of select commodities, nominal USD

Source: World Bank

Expectations of a slight

rebound in food prices in

2016

10

RESEARCH

In Dire Straits

2016 Outlook

Nigeria – High Expectations in Tough Times

President Muhammadu Buhari (PMB), a man with whom the people associate with

change, mounted the reins and has opted to run the country in a manner which in our

view is akin to a ‘social democracy’. The Introduction of social welfare spending into

Nigeria’s budget despite expectations of significantly lower government revenue

following the decline in crude oil prices highlights the President's focus on the masses.

Rather than focus on successfully implementing its social and capital ideas, the new

government has to contend with terrorism in the North, nascent socio-political tensions

in the South and corruption in the polity. While we expect the All Progressives Congress

(APC) led government to continue to grapple with these challenges in 2016, on its way

to achieving its manifesto, we examine below the 'social democratic' model and the

potential challenges that the new government could face in its implementation.

Buhari, the social democracy model and parallels with Brazil

PMB, a one-time military head of state of Nigeria and widely regarded as a man of the

people, has openly declared himself a converted democrat. It is however not far-fetched

to expect that he still holds some ideals of a pure socialist and thus may try to pursue

methods in line with a social democratic model. Social democracy is an ideology that a

democratically elected government can, within the boundaries of capitalism, gradually

re-order the society, through social policies and reforms, into a more equitable and

beneficial economy that promotes social justice for the general population. Social

democracy aims to foster an environment for a more egalitarian society within which

capitalism can thrive. It is a system native to Europe and widely practiced in the

Scandinavia and sometimes called the Nordic system of government. In modern-day,

social democracy is characterised by policies aimed at putting a check on poverty,

inequality and the oppression of the underrepresented, key features that resonate with

the propositions and disposition of the current government.

Although Scandinavia is often referred to as "probably the best governed" region in the

world, we align our expectations of the merits of social democracy with that of a

country with similar demographics as Nigeria. One such country is Brazil. Bolsa Familia is

the social welfare program of the Brazilian government which has had positive

implications for its economy and is winning converts worldwide. Although at a much

advanced stage, parallels can be drawn between the ideals of this program and what

the new Nigerian government may be trying to achieve. The Bolsa Familia program has

its roots in an initial program which was initiated in 1998/9 to cater directly to pregnant

women and the low income population through the distribution of foodstuff. This

however impacted negatively on local market output and was redesigned into a

conditional cash transfer scheme such that money was directly transferred to

beneficiaries. This conditional cash transfer scheme is closely related to the monthly

stipend program recently proposed by the Nigerian government.

New government seems to

be pushing a new economic

ideology – ‘social democracy’

with the record introduction

of a social welfare spend in

the 2016 budget

Social democracy aims to

foster a more egalitarian

society. The Brazilian ‘Bolsa

Familia’ is a case in point and

has won many converts

worldwide including Nigeria

11

RESEARCH

In Dire Straits

2016 Outlook

Bolsa Famila has had resounding implications on the economy of Brazil and has been

lauded as contributing to reduced poverty levels as well as to improvements in

employment. Key factors responsible for the success of Bolsa Familia so far are

continuity in implementation by different governments and the presence of a robust

database operated and maintained by Caixa – a Federal Savings Bank in Brazil. Given

that the Brazilian government delivers these monies through bank issued debit cards,

we believe it is no coincidence that the new Nigerian government successfully pushed

forward the implementation of the Bank Verification Number (BVN) scheme. We see

this as a spring board to the successful implementation of its social investment scheme.

While the idea seems laudable, it is no secret that there are other factors - security

concerns and economic instability that threaten to undermine any plans for social

reform. This is because a significant portion of likely beneficiaries live in the towns

encumbered with unrest.

“Boko Haram” in the Northeast, the threat of secession in the

Southeast and the recent clash

Dealing with the Boko Haram insurgency which has plagued Nigeria over the last four (4)

years is a major hurdle for the government. Although commendable steps have been

taken, such as the movement of the military command centre into the heart of the crisis

and the retake of most of the towns earlier captured by the terrorists, the crisis remains

unabating with more deaths reported regularly.

Boko Haram has been termed the most dangerous terrorist group in the world having

reportedly killed more people in the last year compared to the Islamic State of Iraq and

the Levant (ISIS). This does not bode well for the government especially given the

December 2015 deadline which the President had given the military to quell the

insurgency. A lot more would need to be achieved in this year if the stipend program

being launched as well as any other social interventions is to have any far reaching

impact.

There is also the rising threat of loyalists clamouring for a breakout from the country to

form their own nation called ‘Biafra’. These loyalists are known as ‘Movement for the

Actualization of Sovereign State of Biafra’ (MASSOB) and the ‘Indigenous People of

Biafra’ (IPOB). While the presidency has dismissed these protests as non-issues, such

dismissals are reminiscent of the previous government's attitude towards the initial

tensions from the Boko Haram terrorist group; clearly the government would be wise to

look at this nascent issue critically.

The recent clash between Nigeria’s Army troops and Shiite Muslims in the Zaria area of

Northern Kaduna is also a case for concern. Although government will need to check the

activities of the group especially given the complaints by residents of Zaria and

neighbouring environs, we do not see it escalating into a major crisis for the country

given that the group has been in existence since the 1980s and have only operated

within the boundaries of Zaria. Also, with no major uprising after a similar clash with

Nigeria’s troops in 2014, the potential for a crisis is minimal.

The insurgency in the north

and the recent ‘MASSOB’

protests in the Southeast

threaten to undermine

government plans for social

reform

12

RESEARCH

In Dire Straits

2016 Outlook

Still a growing economy: short term pain, long term gain

The interplay of monetary and fiscal policies shapes the economic outlook for 2016.

While Federal Government initiatives are likely to be targeted at huge capital and

infrastructure investments as well as social investments, easing monetary policy will

ensure that cheap funds are availed to the real sector, specifically agriculture,

manufacturing and solid minerals, in order to drive output and employment growth. To

this end, the Federal Government plans to set up a $25 billion (N4.9 trillion)

infrastructure fund to directly invest in the transport and energy sectors. Investors in the

fund will comprise of both local and international investors. The government has also

provided N500 billion ($2.5 billion) in its 2016 budget framework for a pilot social

intervention scheme that will entail cash payments to unemployed individuals and free

meals for primary school children.

The direction of monetary policy points towards easing with Central Bank of Nigeria’s

monetary policy committee recently reducing the benchmark interest rate to 11% (from

13% since November 2014) and also reducing the Cash Reserve Requirement (CRR) to

20% from 25% (mandating that the realized 5% CRR will only be obtained by individual

banks that grant loans to the real sector). The current currency/capital controls in the

economy are, in our view, another by-product of the government's intended focus on

social welfare. Rather than allowing the Naira to continue to weaken as a result of

"speculative activities", the government has decided to keep the Naira strong by

controlling the supply of forex. We opine that the rationale behind this is to keep

domestic prices low (Nigeria depends on imported foods and other inputs) thereby

controlling inflation (inflation remained at an average of 9.3% in 2015 despite

expectations that it would be much higher) and keeping the masses' purchasing power

intact. While we acknowledge that many of the economic policies are somewhat

complimentary, we believe that the potential economic benefits of these policies are

realizable only in the long term at the expense of short term pain. We also feel that the

success of the ongoing policies depend, quite critically, on the effective implementation

by key stakeholders including current members of the government, business owners,

and aggrieved political opponents.

Monetary Policy and the Economy

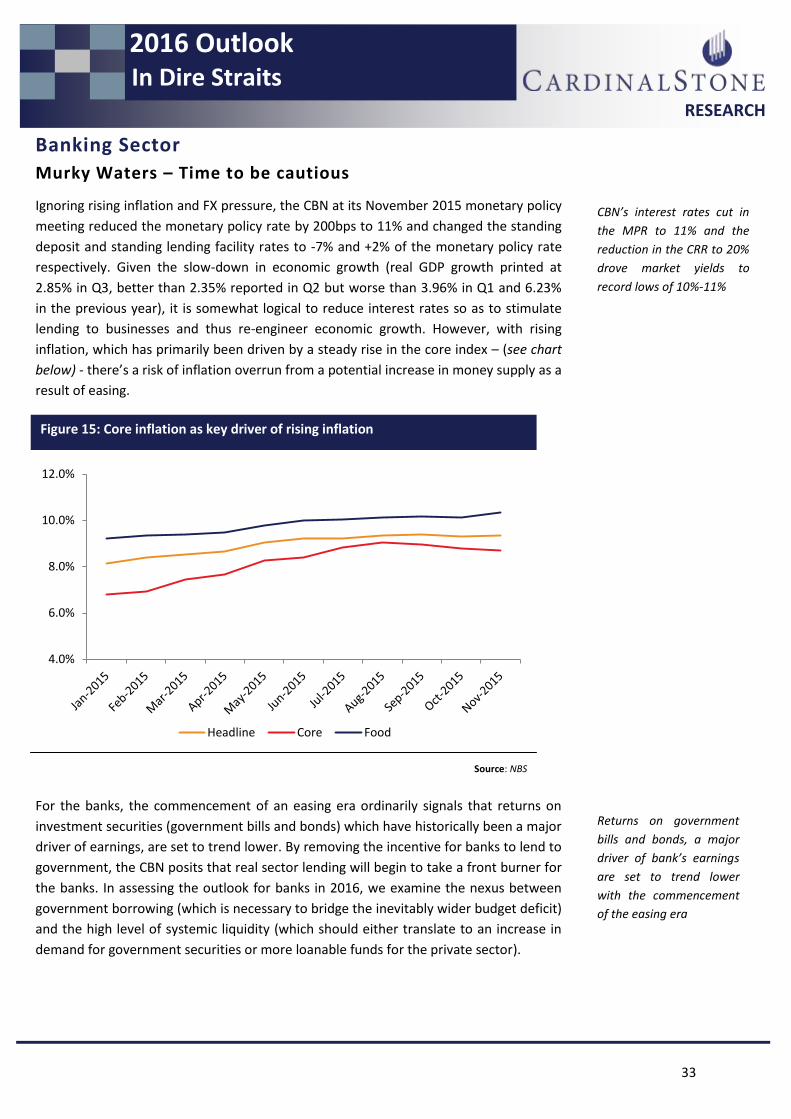

Inflationary concerns linger – In 2016, given the policy decision of the Central Bank of

Nigeria (CBN) to reduce the monetary policy rate (MPR) to 11% with a corridor of

+200bps/-700bps around the MPR and to reduce the CRR from 25% to 20%, the question

of how the apex bank intends to control consequent inflationary pressures arises. Also,

the heightened possibility of devaluation in the first to second quarter of 2016 and the

resulting pass-through effect, present the likelihood of double-digit inflation in 2016. The

pressure point for headline inflation will stem majorly from the core index (All items less

food) because of higher prices of imported food/items. We therefore expect an uptick in

headline inflation in 2016 and see the average for the year at around 11%.

The interplay of monetary

and fiscal policy will shape

the economic direction for

this year – a combination of

expansionary fiscal policy

and monetary easing

13

RESEARCH

In Dire Straits

2016 Outlook

New monetary stance possible mid-2016 – We opine that devaluation is in the fore

come 2016, as the CBN struggles to meet legitimate dollar obligations from its already

dwindling reserves. So far the government has kept the exchange rate around N198/$ but

with the continued downward spiral in crude oil prices (our major source of foreign

exchange receipts) and very limited foreign participation in the country’s financial

markets, the need for a devaluation cannot be overemphasized. In our view, the federal

government is almost out of policy arsenals (after resorting to foreign exchange controls)

to defend the Naira. With import cover at four (4) months, we believe that government

may not be able to continue its staunch foreign exchange control policy and will allow the

Naira weaken in H1 2016. Using guessestimate, we project an equilibrium value for the

Naira within the range of N240/$1 to N275/$1. However, given the various qualitative

factors affecting the demand/supply dynamics of the NGN/USD exchange rate, we realize

that projecting the true value of the NGN/USD rate will be an inaccurate task.

We anticipate a slowdown in real GDP growth – With continued capital controls

amidst dwindling foreign exchange reserves, we anticipate that real sector output will

continue to slow as manufacturing companies face the difficulty of timely access to raw

materials for production. The expected positive impact on GDP of reduced interest rates

may thus be muted. However, should there be timely devaluation; we forecast real GDP

growth at 4% for 2016. Barring devaluation and a recovery in crude oil prices, we foresee

real GDP slowing to 2%. Although any devaluation is incapable of solving the long term

problem of foreign exchange supply, we think it is a necessary short term tool to eliminate

forex controls and possibly boost necessary economic activity. In the medium to long

term, the need to push for structural economic reforms to diversify the country’s export

base cannot be overemphasized.

Bleak outlook for the Nigerian capital market – Maintaining the exchange rate at

N198/$ will only serve to delay the re-entry of foreign portfolio investments given that

underlying economic realities present a case for a Naira devaluation at least in the short

term. Barring devaluation, a reversal in the current direction of oil prices is the only other

catalyst that could lead to increased foreign participation in Nigeria’s financial market.

This may however not be immediately possible as OPEC will continue in its strategy to

preserve market share rather than prop up prices.

Barring devaluation by Q1

2015 and a reversal in crude

oil prices, we foresee GDP

growth at 2% YoY. On the

flipside we anticipate a YoY

average growth of 4%

Inflationary pressures are

anticipated throughout 2016

given a mix of monetary

easing measures (and thus

buoyant system liquidity) and

a heightened likelihood of

devaluation by Q1 2015

Increased foreign

participation in country’s

financial market highly

dependent on a number of

factors – naira liquidity, oil

prices and US interest rate

hike

14

RESEARCH

In Dire Straits

2016 Outlook

Fiscal Policy and the Masses – Highlights of the 2016 Budget and

analysis of its underlying assumptions

The Medium Term Expenditure Framework (MTEF) and the Fiscal Policy Strategy (FPS)

which outlined the expenditure plans and proposed revenue sources for the period

2016-2018, was submitted to the National Assembly for approval. The 2016, N6.07

trillion ($30.65 billion) spending plan is based on the following macroeconomic

assumptions: (i) real GDP growth of 4.82%; (ii) exchange rate of N198/$1; (iii) $38 per

barrel and (iv) 2.2 million barrels per day (mbpd) of oil production.

Total revenue is forecast at N3.82 trillion ($19.29 billion) approximately 10.6% above

2014 budget levels. Although oil remains the main source of revenue for the federal

government implying a significant decline in revenue considering the massive decline in

oil prices, we opine that this revenue target is still conservative. This is because the

Federal Inland Revenue Service (FIRS) has stated that it will target a 200% increase in tax

revenues above 2015 levels, approximately N4.01 trillion ($20.36 billion). This, in

addition to revenues from Oil and Gas sales, should result in total government revenue

well above N3.82 trillion ($19.39 billion).

The proposed aggregate expenditure of N6.07 trillion ($30.65 billion) reinforces

government’s drive towards stimulating growth and employment especially through

infrastructure investments. Aggregate expenditure comprises a huge N1.82 trillion

($9.19 billion) (30% of total budget) earmarked as Capital Expenditure, N2.9 trillion

($14.68 billion) for Recurrent Expenditure (Non-debt) and N1.36 trillion ($6.90 billion)

for debt service.

The budget deficit is thus N2.22 trillion ($11.21 billion) equal to c.2.16% of GDP, with

total borrowings estimated at N1.82 trillion ($9.19 billion) split into N984 billion ($4.67

billion) of domestic loans and N900 billion ($4.55 billion) of foreign loans.

Rationale

Oil price assumption implies prudence but not in line with reality: The

benchmark oil price of $38 per barrel is about 28.3% below the 2015 budget assumption

of $53 per barrel but still higher than current market price level which is at historic lows

of $31 per barrel. The oil benchmark price may need to be revised to reflect current

market realities.

Exchange rate assumption – still in denial: At an official exchange rate of

N198/$1, the government has refused to acknowledge the reality that the economy

cannot be sustained on a seemingly ‘false’ currency value. Theoretically, by not allowing

the free adjustment of prices (i.e. exchange rate) in the event of any external shock, the

burden of adjustment is automatically laid on real variables such as output and

employment. The parallel market exchange rate, a somewhat realistic market value for

In 2016, the FGN is set to run

an expansionary budget at

N6.07 trillion ($30.65 billion)

with a budget deficit of N2.2

trillion. Non-oil revenue to

form the bulk of revenue

receipts

Basic budget assumptions

may need to be revised to

reflect market realities

including the oil price

benchmark and the

NGN/USD exchange rate. Oil

production volume is

achievable.

15

RESEARCH

In Dire Straits

2016 Outlook

the Naira, hit historic highs at N290/$. Foreign currency reserves have also depleted,

currently at $29.1 billion.

Oil production close to 2015’s target: Oil production volume of 2.20mbpd aligns

with 2015’s budgeted target of 2.27mbpd which is prudent given that Nigeria’s daily

average oil production level for 2015 (Third Quarter) was 2.17mbpd. We believe the

lower target may be to account for issues of pipeline vandalism and consider the target

realizable although conservative when compared with the total spending plan of the

government. According to OPEC2 data, Nigeria is currently producing below its quota

which stands at 3.5mbpd.

Growth Outlook – Sector Winners and Losers

Considering budget provisions, current fiscal & monetary policy, low crude oil prices,

and the overall state of the economy we attempt to identify the sectors that could

significantly benefit from the current policy direction. We think the capex budget (N1.8

trillion – $9 billion) is positive for companies in infrastructure related sectors (cement

producers and power companies). Also, easy monetary policy will favour funding of long

term infrastructure projects at very low costs. With a substantial part of government’s

budget focusing on social spending, we envisage increased consumption (as most of the

social benefits for the poorest Nigerians will filter into staple foods if properly

implemented) which is positive for consumer goods companies especially the food

producers. We however expect the existing capital controls to negatively impact

manufacturers generally, but especially consumer goods companies that import a

significant portion of their inputs. The drop in crude oil prices has already began to

negatively affect the upstream oil & gas sector, while the downstream sector is

embroiled in a subsidy battle but is expected to maintain its steady performance despite

current realities. Overall, we summarize our expectations for the different sectors in the

table below:

Figure 3: Sector Winners and Losers

Sector Contribution to

real GDP (%)3

Winner(W)

/Loser (L)

Rationale

Agriculture 26.79 W Government’s drive towards diversification to influence growth in agriculture

Consumer Goods/Manufacturing

9.67 W Food producers to benefit from federal government’s expenditure on social interventions

Banking & Financial Services

2.76 L Heightened risk of loan default presents weak outlook for Banks

Oil and Gas – Upstream

10.61 L Low international crude oil price to weigh on output growth

Industrial Goods /Construction

3.22 W Huge government spending on infrastructure projects to spur growth in sector

2 OPEC – Organisation of Petroleum Exporting Countries

3 As at Third Quarter 2015

Source: CardinalStone Research

We see the Agricultural,

Industrial and Consumer

Goods sectors as key sector

winners in 2016

16

RESEARCH

In Dire Straits

2016 Outlook

Equities

Market return heavily dependent on macro events

The macroeconomic conditions that ushered in 2015 – the oil glut that saw oil prices

crash to new lows and the consequent adjustment of the Naira - have weighed

negatively on investor sentiment throughout the year. Oil prices averaged $54/barrel in

2015, down 50% from 2014 average of $100/barrel, leading the CBN to change the

foreign exchange allocation policy by scrapping the Retail Dutch Auction System

(following the devaluation in November 2014), which saw NGN/USD exchange rate

move to 198/$1. Expectations of an interest rate hike in the US by the Federal Reserve

also led to significant foreign investment outflows from the Nigerian stock market.

Overall, market participation dipped with the Nigeria Stock Exchange (NGSE) losing

17.36% in 2015. Our outlook on equities considers key factors that could weigh in on

investor sentiments in 2016. We anticipate that the following key events and factors will

influence the performance of the NGSE considering that the 2015 selloff has improved

the risk-reward outlook for equities to outperform fixed income. ;

― The intervention of local investors

― Perceptions of exchange rate stability given global outlook on crude oil prices,

and its attendant implications for the Naira

― Market initiatives by the Nigerian Stock Exchange (“NGSE” or the “Exchange”)

Intervention of locals, the return of FPI’s or death of the equity

market

Local participation to determine market resurgence : The recovery of the

equities market in 2016 will depend on increased local participation by both retail and

institutional investors (pension fund managers etc). Foreign transactions have

dominated market activity, accounting for over 50% of total value traded in the last 3

years and dictating direction and market fortunes over the same period. Negative stock

market returns and overall market volatility have historically been associated with huge

foreign capital outflows and thus to ensure market stability there is the need for policies

and strategies that will attract and sustain local interest in the market. Local

participation forms the bedrock of any market and thus a huge local market presence

serves to check any economic eventualities that could have a run on the market. The

NGSE recently implementing the X-BOSS (“Broker Oversight & Supervision System”)

initiative, the first in West Africa, holds the optimism that stricter oversight function is

necessary to boost investor confidence and enhance capabilities for market integrity.

The initiative is geared towards the automation of the regulatory and oversight function

of the Exchange over dealing members with a focus on the automation of regulatory

filings, the analysis of various ratios of financial renditions, capital and liquidity

monitoring as well as compliance monitoring.

Increased local retail and

institutional participation

will be a key determinant of

market recovery in 2016

Asides macro factors, local

intervention, exchange rate

stability and NGSE market

initiatives will primarily

influence equity market

performance in 2016

17

RESEARCH

In Dire Straits

2016 Outlook

According to the NGSE, the system is poised to offer investors access, on a near real

time basis, to dealing members information including corporate profile, compliance

history, regulatory reports submitted to the Securities and Exchange Commission (SEC)

as well as complaints management and tracking solutions.

The equities market is dominated by foreign investors seeking higher returns than

obtainable in their domestic, usually more developed markets. We see less interest in

frontier emerging markets if the Federal Reserve commences its mooted rate hike cycle

due to the narrowing of interest rate differentials. The benchmark rate has been at a

low of 0.25% since 2009, which in addition to surplus liquidity from quantitative easing

programs, spurred inflows to emerging and frontier markets. If the US benchmark rate

is hiked (median estimates by Federal Reserve officials indicate a hike to 1.125% in

H2’15), we expect a much slower pace of capital flows into Nigerian equities.

Furthermore, quickening growth in the US (with the Federal Reserve forecasting an

increase in real GDP growth of 3.1% in 2015 from an average of 2.4% in 2014), which

may be better-than-projected as a result of falling gasoline prices, makes a case for

better performance of US equities especially on the back of the strong performance

seen in 2015 (-0.73% S&P return vs. NGSE return of -17.36%). The UK, another Country

with considerable interest in our market, is also expected to hike its 0.5% interest rate

to 0.75% in Q3’16 according to the British Chambers of Commerce. We expect this rate

hike to also spur reversal of funds flow from the UK.

51% 58%

52%

73%

56% 50%

55%

34%

63% 56% 53% 51%

57%

49% 42%

48%

27%

44% 50%

45%

66%

37% 44% 47% 49%

43%

Total Foreign Transaction Total Domestic Transaction

Figure 4: Foreign vs. Domestic Transactions

Source: Nigerian Stock Exchange

The Nigerian equities

market is dominated by

foreign players

18

RESEARCH

In Dire Straits

2016 Outlook

Pension funds and the multi-fund structure: Pension funds play a huge role in

the development of an economy and with favourable regulatory climate; have the

potential to positively impact the capital market. The Nigerian Pensions Industry, with

pension Assets under Management (AUM) totalling N5.149 trillion ($26 billion) as at

October 2015, is rife with the potential to revive the local equities market. Total AUM is

split between four asset classes which include Approved Existing Scheme (AES) –

N659.49 billion - $3.3 billion (12.8% of AUM), Closed Pension Fund Account (CPFA) –

N719.24 billion - $3.6 billion (14.0% of AUM), RSA4 ‘Active’ Fund – N3,363 billion - $17

billion (65.3% of AUM) and RSA ‘Retiree’ Fund – N407.51 billion - $2 billion (7.9% of

AUM). The regulation on the investments of pension fund assets is such that Pension

Fund Administrators (PFAs) are permitted to allocate not more than 25% of total RSA

‘Active’ Fund (equal to N840.8 billion - $4.3 billion) to equities and up to 80% in Fixed

Income Securities while RSA ‘Retiree’ Funds are to be heavily weighted in fixed income

assets. The total value of RSA ‘Active’ Funds invested in both public equities as at

October 2015 however is N341.45 billion - $1.7 billion or 10.0% compared to the

industry limit of 25%. PFAs have a strong capacity to influence market stability but have

not been able to because of regulatory constraints including the focus on short-term

performance reporting and the lack of a multi-fund structure. The constraint of the lack

of a multi-fund structure is being addressed as the RSA ‘Active’ and ‘Retiree’ Funds will

be replaced with a multi-fund structure as follows:

Fund I: 10% – 70% of total fund to be invested in variable income instruments

(explained below) and open to contributors under the age of 35 years.

Fund II: 5% – 50% of total fund to be invested in variable income instruments and

open to contributors between the ages of 36 – 45 years

Fund III: 0% – 30% of total fund to be invested in variable income instruments and

open to contributors above 46 years

Fund IV: The current RSA ‘Retiree’ fund open only to Retirees

Fund V: A non-interest/ethical fund with strict compliance to Islamic Shariah

Principles

The lower end of the range represents the compulsory minimum exposure to variable

income instruments. The implementation of the multi-fund structure is scheduled to

commence in 2016 and could help kick-start increased interest from PFAs in the equities

market.

Modalities and potential impact of the multi -fund structure: According to the

National Pension Commission (PenCom), a PFA’s exposure to variable income

instruments is defined as the sum of investments in ordinary shares, open and closed-

end funds, infrastructure funds and private equity funds including the PFAs current

holdings and any future acquisition of additional investment units. The focus is on the

first three (3) funds where PFAs are expected to invest in such a way that actual variable

income exposure in Fund I is higher than exposures in Fund II and exposures in Fund II

higher than that of Fund III.

4 RSA – Retirement Savings Account

The proposed multi-fund

structure will help boost local

equity play by PFAs and

hopefully contribute to

market recovery

19

RESEARCH

In Dire Straits

2016 Outlook

We believe this multi-fund structure will drive increased local participation and thus

boost activity and ensure stability in the equities market. Other considerations capable

of boosting local participation include the deliberate inclusion of the informal sector of

the economy which will increase pension fund assets available for investments.

Attractive dividend yields to spur local interest in 2016 : At current depressed

stock prices, dividend yields are very attractive. Dividend yields calculated using closing

stock prices as at December 2015 and 2014 full year company results, stand between

7%-15% especially for banks. Savvy local investors are likely to ride on this earlier in the

year, paying particular attention to companies with very good dividend paying history

and strong earnings potential. We therefore expect a dividend yield play this year with

the potential to boost market activity and maybe reverse market fortunes.

The return of Foreign Portfolio Investors (FPIs) – Clearly, over the last few

years, the direction of activities in the equities market has been influenced mostly by

the activities of foreign portfolio investors. With the drop in crude oil prices, FPI’s began

to pull out of the market as fears of an economic slowdown, increased exchange

controls, and unmet foreign exchange demand became rife. With the official exchange

rate maintained at N198/$1, the re-entry of foreign investments into the equities

market in 2016 is unlikely given that underlying economic realities present a case for

exchange rate adjustment. This will be further aggravated if the current direction of oil

prices is not reversed. With forecasts by the US Energy Information Agency (EIA) that

crude oil prices will only pick up in 2018, the only other catalyst capable of attracting

foreign portfolio investments is an adjustment of the Naira to a fair equilibrium level.

Low-level crude oil prices seem to have come to stay as the Organization for Petroleum

Exporting Countries (OPEC) continues its strategy to preserve market share by pumping

oil rather than its default approach of propping up prices by modifying production

limits.

What we expect in 2016

The overall direction of the Nigerian equities market in 2016 will be determined

primarily by market catalysts and their influence on overall investor sentiments. We

discuss our 2016 equity market projection under the following scenarios:

SCENARIO CATALYST MARKET DIRECTION

I Rebound in oil prices, positive outlook for the Naira

II No rebound in oil prices but a short to medium term solution to the foreign exchange situation – an adjustment of the currency

III No rebound in oil prices and status quo on foreign exchange continues

The return of FPI’s largely

dependent on sentiments

about naira stability and

crude oil prices

We foresee a dividend yield

play in 2016 given very

attractive dividend yields at

current prices

Three possible scenarios for

the direction of the equity

capital market in 2016

20

RESEARCH

In Dire Straits

2016 Outlook

Scenario I – Oil price outlook and the possibility of a reversal in 2016 :

Historical numbers lay credence to the fact that a rebound in crude oil price in 2016 is

the single most crucial catalyst for the redirection of equity market fortunes. Figure 3

shows the direct correlation between the price of crude oil and the direction of the ASI

which measures overall equity market performance in Nigeria. According to the U.S

Energy Information Administration (EIA) however, the crude oil market faces a number

of uncertainties heading into 2016 given that the pace and volume of Iran’s re-entry, the

response of non-OPEC production to low oil prices and the strength of consumption

growth will all jostle to determine market’s new equilibrium. An oil price rebound is

highly uncertain therefore in the short to medium term.

It will take an output concession by OPEC to prop up oil prices and that seems unlikely

as data has led the cartel to believe that the strategy to achieve market share by

increasing production (and influencing prices) and driving out higher-cost producers

seems to be paying off. OPEC’s revised forecast (December 2015) for non-OPEC oil

supply growth in 2015 stands at 1.00mbpd from an earlier forecast of 1.31mbpd citing

the impact of low oil prices and declining investments in the oil industry, with

expectations of a further contraction in 2016 by 0.38mbpd. The 2016 outlook is a

further dip in oil prices.

Scenario II – Possible Uhuru for the Naira?: Nigeria’s foreign exchange earnings

are primarily from crude oil exports (86.8% of Q3 2015 exports) and, with oil prices at

currently low levels, the Naira has come under immense pressure. Foreign exchange

reserves stood at $29.1 billion as at December 2015, an equivalent of approximately

four (4) months worth of imports.

0

20

40

60

80

100

120

140

160

Jan

-85

Ap

r-8

6

Jul-

87

Oct

-88

Jan

-90

Ap

r-9

1

Jul-

92

Oct

-93

Jan

-95

Ap

r-9

6

Jul-

97

Oct

-98

Jan

-00

Ap

r-0

1

Jul-

02

Oct

-03

Jan

-05

Ap

r-0

6

Jul-

07

Oct

-08

Jan

-10

Ap

r-1

1

Jul-

12

Oct

-13

Jan

-15

Crude Oil Price All Share Index Figure 5: Crude oil price ($/bbl) and the ASI (‘000)

Source: CardinalStone Research

An oil price rebound will

redirect equity market

fortunes however the 2016

outlook for oil prices is

negative

21

RESEARCH

In Dire Straits

2016 Outlook

In the absence of devaluation, the CBN will continue to grapple with maintaining the

exchange rate at N198/$1 in the coming year, meanwhile rates at parallel markets

reached an all time high at N290/$1. In theory, when currency demand far outweighs

supply, the currency (in this case the Dollar) appreciates in search of a new equilibrium.

Nigeria operates a fixed exchange rate regime and thus a new equilibrium can only be

reached through currency devaluation, a path the CBN is wary of threading. The only

other catalyst for a reversal of equity market fortunes, asides a rebound in crude oil

price and increased local participation, is improved liquidity in the foreign exchange

market. This begs the question of the possible existence of a short term fix to the

unavailability of foreign exchange to meet demand. Policies capable of encouraging the

inflow of forex directly through increased earnings receipts and/or indirectly through

reduced savings on imports, are needed to ease liquidity pressures which in turn will

boost investor sentiment and reverse market direction in 2016. There are two options –

reducing the country’s import base to increase forex savings and possibly reducing

leakages in reserves and/or shoring up the export base in order to generate inflows and

boost supply. The latter is however long term, as a complete diversification from oil can

only come on the heels of improved critical infrastructure needed for local production

to compete favourably with international brands. Reducing the import base through

strategic import substitution policies is therefore the most practical immediate solution.

Although substantial savings on imports may not be realisable within one year, the

removal of the import subsidy on petroleum products can generate sufficient forex

savings for the country. Total dollar value of petroleum subsidy claims (excluding the

Nigerian National Petroleum Corporation- NNPC’s subsidy bill) between 2013 and 2015

was approximately $8.5 billion (N1.7 trillion) and with a major bulk of that amount

funding spurious and speculative demands and encouraging round tripping. Given that

substantial amounts can be generated in foreign exchange savings, and thus a boost in

forex supply, there is the hope of equity capital market resurgence in 2016.

Scenario III – A looming doomsday?: If crude oil prices continue to decline

coupled with no respite in the foreign exchange market, the capital market will continue

on its southward trajectory in 2016.

A short to medium term

solution for the naira can

positively influence market

direction

Barring a rebound in crude

oil price and no respite for

the naira, a southward

direction is expected

22

RESEARCH

In Dire Straits

2016 Outlook

2015 Review – Bears Held Sway

Macro dynamics hamper stock market returns for Nigeria - The NGSE

recorded a 17.36% decline in 2015 following the continued decline in crude oil prices

and the overall impact on government finances and the currency. Foreign participation

declined, triggered majorly by heightened uncertainties about the general elections in

March 2015. The stock market attempted a recovery in April 2015 (see Figure 6) gaining

9.3% MoM and 0.15% YTD (as at April 30 2015), after the peaceful outcome of the

general elections. The gains were however short-lived with market returns reversing

and then remaining mostly negative throughout the year. The Banking and Consumer

Goods sectors recorded the biggest losses at -23.59% and -17.41% respectively.

Figure 6: NGSE Sector Indices Performance in 2015

Macro factors primarily

influenced NGSE

performance in 2015

Source: CardinalStone Research

-23.59%

-17.41%

-6.20%

-4.70%

1.27%

-25.00% -20.00% -15.00% -10.00% -5.00% 0.00% 5.00%

Banking

Consumer Goods

Oil & Gas

Insurance

Industrial Goods

23

RESEARCH

In Dire Straits

2016 Outlook

Negative YTD equity return across African markets – African stock

markets performance was largely lacklustre in 2015. Measured by the year-to-date

return in local currency of each country’s equity benchmark index, the best performer

was the South African Johannesburg Stock Exchange (+1.85. The Nairobi Stock Exchange

was second with a return of (-10.55%) and Ghana was next with a return of (-11.76%).

20,000

25,000

30,000

35,000

40,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

Dec

14

Jan

15

Feb

15

Mar

15

Ap

r 1

5

May

15

Jun

15

Jul 1

5

Au

g 1

5

Sep

15

Oct

15

No

v 1

5

Dec

15

Market Cap. (N'Bn) ASI

-

5

10

15

20

25

30

35

01

-Dec

-14

01

-Jan

-15

01

-Feb

-15

01

-Mar

-15

01

-Ap

r-1

5

01

-May

-15

01

-Ju

n-1

5

01

-Ju

l-1

5

01

-Au

g-1

5

01

-Sep

-15

01

-Oct

-15

01

-No

v-1

5

01

-Dec

-15

Trade Value (N'Bn)

Figure 7: NGSE Market Performance (2015)

Overall bleak macro

outlook lead ASI to

negative YTD return

Foreign investors

stay on the sidelines

awaiting policy

clarity

Source: CardinalStone Research, NGSE

Eve

nt Concerns about 2015

general elections lead

to negative ASI return

Re

turn

(%

)

QTD: -10.3

YTD: -10.3

Rally following

successful elections

lead to +ve return

QTD: +5.4

YTD: -3.5

QTD: -6.7

YTD: -9.9%

QTD: -14.3

YTD: -22.9

-

1,000

2,000

3,000

4,000

01

-Dec

-14

01

-Jan

-15

01

-Feb

-15

01

-Mar

-15

01

-Ap

r-1

5

01

-May

-15

01

-Ju

n-1

5

01

-Ju

l-1

5

01

-Au

g-1

5

01

-Sep

-15

01

-Oct

-15

01

-No

v-1

5

01

-Dec

-15

Trade Volume ('Mn)

Figure 8: Trading Activity (2015)

Source: NGSE

Lacklustre returns across

major African markets

throughout 2015

24

RESEARCH

In Dire Straits

2016 Outlook

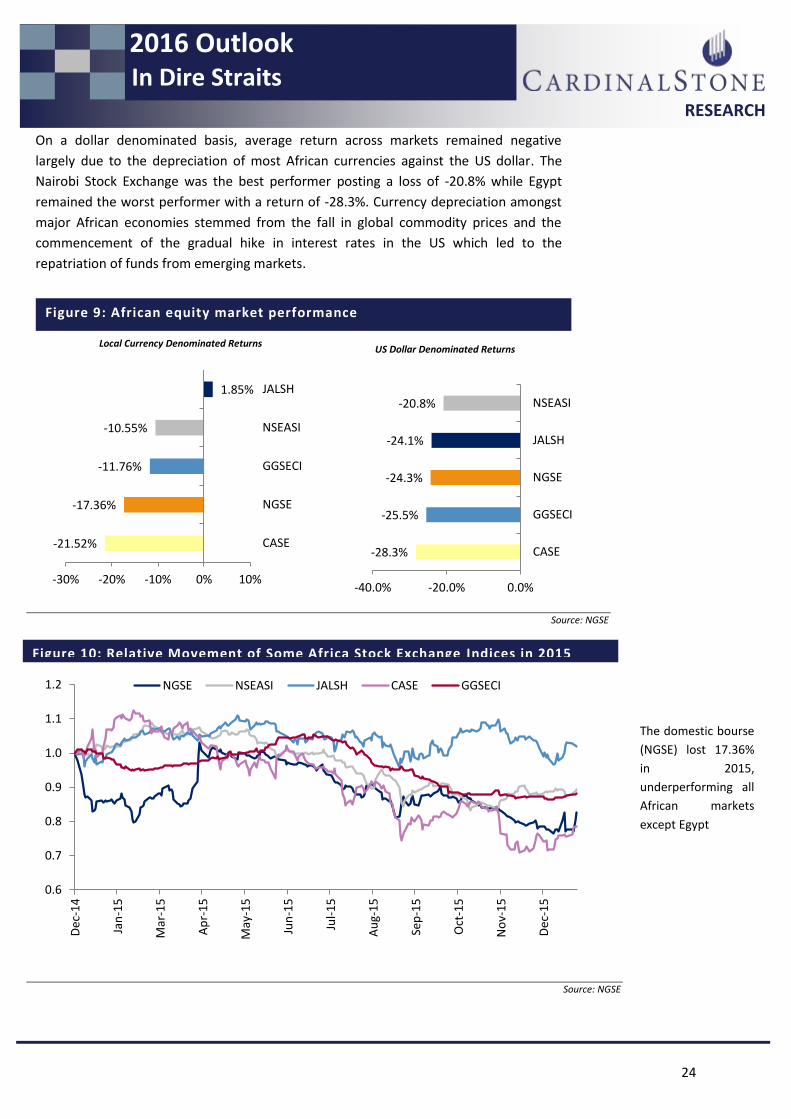

On a dollar denominated basis, average return across markets remained negative

largely due to the depreciation of most African currencies against the US dollar. The

Nairobi Stock Exchange was the best performer posting a loss of -20.8% while Egypt

remained the worst performer with a return of -28.3%. Currency depreciation amongst

major African economies stemmed from the fall in global commodity prices and the

commencement of the gradual hike in interest rates in the US which led to the

repatriation of funds from emerging markets.

Figure 10: Relative Movement of Some Africa Stock Exchange Indices in 2015

Sources: Bloomberg, CardinalStone Research

The domestic bourse

(NGSE) lost 17.36%

in 2015,

underperforming all

African markets

except Egypt

Figure 9: African equity market performance

Local Currency Denominated Returns US Dollar Denominated Returns

-28.3%

-25.5%

-24.3%

-24.1%

-20.8%

-40.0% -20.0% 0.0%

CASE

GGSECI

NGSE

JALSH

NSEASI

-21.52%

-17.36%

-11.76%

-10.55%

1.85%

-30% -20% -10% 0% 10%

CASE

NGSE

GGSECI

NSEASI

JALSH

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Dec

-14

Jan

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

NGSE NSEASI JALSH CASE GGSECI

Source: NGSE

Source: NGSE

25

RESEARCH

In Dire Straits

2016 Outlook

0.5

0.7

0.9

1.1

1.3

1.5

1.7

Dec-2010 Dec-2011 Dec-2012 Dec-2013 Dec-2014 Dec-2015

NGSEASI MSCI Frontier

Figure 11: NGSE and MSCI Frontier Index – 5 year relative movement

Source: Bloomberg

26

RESEARCH

In Dire Straits

2016 Outlook

Fixed Income

Yields, what direction in 2016?

The 2016 budget deficit financing to influence bond yields : On the

backdrop of major fiscal pressures expected in 2016 – the continued downward spiral in

oil prices and the debt-ridden financial position of state governments - the Federal

Government has put forward a total budget of N6.07 trillion ($30.71 billion) with a

projected N2.2 trillion ($11.21 billion) deficit to be financed through domestic and

foreign borrowings estimated at N984 billion ($4.97 billion) and N900 billion ($4.55

billion) respectively. Following from this, Nigeria is positioned to issue more bonds in

2016 relative to 2015 (total bonds issued in 2015 was N788.72 billion - $4 billion) which

will ordinarily imply that bond yields should rise. With a bleak outlook for crude oil

prices and the Naira – crude oil accounting for about 70% of consolidated government

revenues and over 90% of foreign exchange earnings, Nigeria’s perceived credit

worthiness may have been weakened and as such investors are likely to demand for

higher returns.

Heightened liquidity to boost demand in bond market : A second key

determinant of the direction of yields is the signalled path of monetary policy – an era of

low interest rates targeted primarily at boosting output growth. The CBN reviewed its

policy rate from 13% to 11%, the CRR from 25% to 20% and halted its Open Market

Operation (OMO) for a two-month period, aiming primarily to boost system liquidity

and redirect cheap funds to the real sector. The impact has however been a downward

spiral in yields as it is customary that such liquidity first finds its way to the fixed income

market. Furthermore, considering the current pressures which have led to slowing

economic growth in the country, we think Deposit Money Banks (DMBs) will remain

reluctant to lend to the real sector especially in Q1 2016 despite increasing liquidity.

Therefore, the sustained high level of liquidity in the banking sector (average of about

N1 trillion - $5 billion) and the additional liquidity from debt servicing by the federal

government (estimated at N1.36 trillion - $6.9 billion) in 2016 budget proposal implies

that demand may outweigh supply thus keeping yields relatively low. We expect this to

continue at least till Q1 2016 as DMBs, primary players in the fixed income market, take

some time to make adequate preparations against credit risks and default associated

with increased/aggressive lending.

Inflationary expectations and Interest rates : Critical fallout of increased

liquidity in the system is the possible impact on inflation and the consequent impact of

inflation expectations on market yields. High inflation expectations generally drive rates

north as investors seek to be compensated for rising prices. For Nigeria, this may not

pose major concerns as there’s usually a lag effect from the impact of rising inflation on

real returns.

Budget deficit financing and

negatively perceived credit

worthiness will see yields

rise in 2016

Buoyant system liquidity

given monetary easing will

boost demand and influence

direction of fixed income

yields downwards

High inflationary

expectations to drive yields

northwards

27

RESEARCH

In Dire Straits

2016 Outlook

US Interest rate lift-off and the Naira’s many woes : The commencement

of a gradual hike in US interest rates may likely slow the comeback of foreign investors

into the fixed income market in 2016. This is particularly the case as Nigeria continues to

manage currency pressures with dwindling oil prices impacting on the foreign exchange

earnings. We analyzed the possibility of a comeback by looking at the interest rate

differential between similar tenured instruments trading in both the US and the

Nigerian market. Using current yields on US treasury bonds and assuming that the Fed

will gradually increase rates on average by 25 bps every two-months, the interest rate

differential is approximately 8.93%5 - calculated as the 12.54% yield on 10 year FGN

bonds minus a 3.61% yield on 10 year US treasury assuming that current yields (at

2.11%) increase by a total of 1.50% in 2016 were the Fed raises rates by 0.25% every

two-months. Although attractive, the average foreign investor will pay particular

attention to the ease of repatriating potential investment profits. This is the game

changer for the market as foreign investors would only return if they can be certain of

improved foreign exchange supply over their investment horizon.

Likelihood of increased corporate issuances : With average FGN bond yields

going as low as 9%, there is an opportunity for large and medium corporates to consider

issuing bonds in the market at lower rates than were historically possible. While many

banks are comfortable issuing bonds, only a few large companies have been willing to

raise money from the capital market. One of the reasons for this reluctance was the

typically high yields on FGN bonds which are deemed as nearly risk free; however the

increased system liquidity which has forced yields down is a positive trend that could

lead to the rebirth of corporate bond issues.

The 2016 Q1 treasury bills calendar : The government plans to raise N1.22

trillion ($6.13 billion) from treasury bills in the first quarter of 2016 split between

N245.77 billion ($1.24 billion) worth of 91-day bills, N238.51 billion ($1.20 billion) worth

of 182-day bills and N735.54 billion ($3.71 billion) worth of 364-day bills. The amount to

be raised however is the exact amount maturing into the system during the period, an

indication that government intends to keep yields low on the short end of the curve by

not increasing borrowing.

Demand and supply to determine overall direction of yields : We

anticipate that the fixed income market will primarily be a local play with the weightier

of the two of demand – buoyed by system liquidity and supply – fueled by the need for

the government to bridge financing gaps, determining the overall direction of market

yields in 2016.

5 Calculated as at January 12, 2016

The gradual lift off in US

interest rate will stall

comeback of foreign

investors even with a high

interest rate differential

A high likelihood of

corporate bond issues in

2016 given current low

yields

FG not increasing short term

borrowing, a strategy to

keep yields on short tenured

instruments low

2016 will primary be a local

play with the weightier of

the two of demand and

supply determining overall

direction for yields

28

RESEARCH

In Dire Straits

2016 Outlook

2015 Review – A volatile year for yields

Nigeria’s 2015 presidential election : 2015 stood out as a very volatile year for

the fixed income market. Yields were driven to both high and low extremes as varying

macroeconomic and political events influenced investor confidence. The socio-political

uncertainties that surrounded the 2015 general elections saw market yields at 15%

levels (compared to 12-13% levels as at December 2014) as investors sold off, worried

primarily about the outcome of the March 2015 presidential elections and JP Morgan

placing Nigeria on a negative index watch. 2015 Q1 average bond return stood at 0.6%,

staying negative throughout the month of March. For the first time and in a tightly

contested election, Nigeria witnessed the ‘peaceful’ defeat of an incumbent with a calm

post-election period triggering a bullish momentum for the market – the Financial

Market Dealers Quotation (FMDQ) overall bond market index grew by 6.5% mid April

(see chart below).

Cautious trading at mid-year as investors sought policy clarity:

Following the election however, it took the new government a long time to take a stand

on its intended policies especially with regards to exchange rate as a result of dwindling

crude oil prices. Market yields remained relatively flat around 13-14% levels during the

period, with investors trading cautiously and waiting for clarity on fiscal and monetary

policies.

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

1,000.0

1,050.0

1,100.0

1,150.0

1,200.0

1,250.0

1,300.0

1,350.0

1,400.0

Overall Market Index Implied Yields

Figure 12: FMDQ Bond Index and Implied Market Yields, 2015

Source: FMDQ

Overall bond index grew by

6.5% mid April following the

successful presidential election

which took place in March

Market yields remained flat

around 13-14% as the new

government took a long time

to give clarity on policies

29

RESEARCH

In Dire Straits

2016 Outlook

JP Morgan’s announcement and heightened expectations of a US

interest rate hike sends yields back up again : The announcement of a likely

phase out of Nigeria’s FGN bonds from the JP Morgan Emerging Markets Bond Index

saw major funds which tracked the index exiting huge positions. Market yields inched

up during the period (August-September), with the benchmark FGN bonds reaching

record levels of 17% in September. Meanwhile, there was a heightened likelihood

during the same period, of a lift-off in US interest rates as strong positive economic data

showed healthy signs of economic recovery. This further served to drive yields upward

as investors priced in a possible rate hike.

CBN’s interest rate cut reverses yield directions : In a sudden twist, the

CBN, working to manage continuing pressures on the economy, cut interest rates to

record lows of 11% at its November MPC meeting. Also, given that the TSA policy served

to tighten system liquidity, the apex bank reduced the Cash Reserve Requirement (CRR)

from 25% to 20%. This shored up system liquidity consequently driving market yields to

record lows of 10-11%. Q4 2015 thus witnessed the return to normality of the yield

curve.

Following JP Morgan’s

announcement to phase out

Nigeria from its Emerging

Markets Bond Index and the

anticipation of a US interest

rate hike, yields went higher

to record levels of 17%

CBN’s interest rates cut in

the MPR to 11% and the

reduction in the CRR to 20%

drove market yields to

record lows of 10%-11%

30

RESEARCH

In Dire Straits

2016 Outlook

15.30

15.40

15.50

15.60

15.70

15.80

15.10 APR 2017

15.54 FEB 2020

14.2 MAR 2024

12.14 JUL 2034

Mar-15

13.60

13.80

14.00

14.20

14.40

15.10 APR 2017

15.54 FEB 2020

14.2 MAR 2024

12.14 JUL 2034

Apr-15

15.15

15.20

15.25

15.30

15.35

15.40

15.45

15.10 APR 2017

15.54 FEB 2020

14.2 MAR 2024

12.14 JUL 2034

Aug-15

7.00

8.00

9.00

10.00

11.00

12.00

13.00

15.10 APR 2017

15.54 FEB 2020

14.2 MAR 2024

12.14 JUL 2034

Nov - Dec 15

The period of the 2015 general election marked

with fears of a probable post election crisis sets

off abnormal direction of the yield curve

Post election calm saw a bit of correction in the

yield curve

Foreign investors priced in the likelihood of a

phase out of the FGN bond from the JP Morgan

Bond Index amidst currency demand pressures

and the lack of policy clarity

The CBN interest rate cut and the consequent

liquidity driven demand that saw yields crash to

record lows and the yield curve return to

normality

Figure 13: The many shapes of the yield curve through 2015

Source: FMDQ, CardinalStone Research

31

RESEARCH

In Dire Straits

2016 Outlook

0

100

200

300

400

500

600

20

15

Jan

-27

Feb

-19

Mar

-16

Ap

r-1

0

May

-22

Jun

-17

Jul-

10

Au

g-0

5

Sep

-04

Oct

-02

Oct

-27

No

v-1

9

Dec

-14

0

0.1

0.2

0.3

0.4

0.5

0.6

20

15

Jan

-29

Feb

-25

Mar

-24

May

-11

Jun

-08

Jul-

03