2015 new york survey of genx boomer voters€¦ · quarter of gen x voters interviewed say they are...

TRANSCRIPT

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 1

About AARP

AARP is a nonprofit, nonpartisan organization, with a membership of nearly 38 million, that helps people turn their goals and dreams into real possibilities, strengthens communities and fights for the issues that matter most to families such as healthcare, employment and income security, retirement planning, affordable utilities and protection from financial abuse. We advocate for individuals in the marketplace by selecting products and services of high quality and value to carry the AARP name as well as help our members obtain discounts on a wide range of products, travel, and services. A trusted source for lifestyle tips, news and educational information, AARP produces AARP The Magazine, the world's largest circulation magazine; AARP Bulletin; www.aarp.org; AARP TV & Radio; AARP Books; and AARP en Español, a Spanish-language website addressing the interests and needs of Hispanics. AARP does not endorse candidates for public office or make contributions to political campaigns or candidates. The AARP Foundation is an affiliated charity that provides security, protection, and empowerment to older persons in need with support from thousands of volunteers, donors, and sponsors. AARP has staffed offices in all 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands. Learn more at www.aarp.org.

Acknowledgements

AARP staff from the New York State Office; Community, State and National Affairs (CSN); and AARP Research

contributed to the design, implementation and reporting of this study.

Contributors include:

Beth Finkel, Bill Ferris, David McNally, Erik Kriss, Erin Mitchell, Donna Liquori and Kimberly Spell from the New

York State office; Sarah Mysiewicz and Reshma Mehta from CSN; Angela Houghton, Eowna Young Harrison,

Brittne Nelson, Kate Bridges, Rachelle Cummins, Darlene Matthews and Cheryl Barnes from AARP Research;

and Doris Gilliam, Office of General Counsel.

Special thanks to Precision Opinion for the collection and tabulation of these data.

Copyright © 2015 AARP

AARP Research

601 E Street NW Washington, DC 20049

www.aarp.org/research

For more information contact:

Angela Houghton, Senior Research Advisor

State Research

AARP Research

Tel. (202) 434-2261

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 2

TABLE OF CONTENTS

Introduction ................................................................................................................................................. 3

Executive Summary ...................................................................................................................................... 4

About the Survey & Report Terms ................................................................................................................ 7

Detailed Survey Findings .............................................................................................................................. 8

Current Financial Situation ......................................................................................................................... 8

Confidence In Retiring .............................................................................................................................. 10

Access to retirement plans (Among employed) ................................................................................... 12

Retirement Savings Behavior ............................................................................................................... 13

Retirement Income Expectations......................................................................................................... 14

Debt and Other Barriers to Saving ............................................................................................................ 16

New York Affordability.............................................................................................................................. 18

Support for A State Facilitated Retirement Savings Option........................................................................ 20

Demographic Profile of Respondents ......................................................................................................... 23

Methodology ............................................................................................................................................. 25

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 3

INTRODUCTION

This year Generation X turned 50. With 2.5 million members across the state, AARP New York is

the state’s leading advocate for the 50+, and we believe now is the time for us to take stock of the

financial plans of Gen Xers and how prepared they are for their financial future. To that end,

AARP New York presents, “High Anxiety: New York’s Gen X and Boomers Struggle with Stress,

Savings and Security,” a report detailing the findings behind a groundbreaking statewide voter

survey of New York voters aged 35-69, Generation X and Baby Boomers together.

As Generation X emerges from the long shadow cast by the Baby Boomers, they find themselves

sandwiched between raising their children and caring for their aging parents while working longer

hours to pay the bills. We found that Gen Xers lack the time and knowledge needed to manage and

plan for their future. Not building a secure retirement is adding more worry to this most important

and stressed population. It is vital that these worries are addressed by our elected leaders because

an uncertain financial future for New Yorkers is an uncertain financial future for the state.

Last year, we presented a voter survey that showed a majority of working New York Baby

Boomers plan to leave the state for their retirement. This year, we found even more members of

Gen X intend to flee New York – 66 percent, compared to the Boomers’ 55 percent. In fact, one

quarter of Gen X voters interviewed say they are “extremely likely to leave New York” when it’s

time to retire because they don’t believe they can afford to stay in the state. Our state’s cost of

living, including the highest utility bills in the country, may lead to a “Gen-Xodus” for New York.

But it doesn’t have to be that way. At AARP New York we believe the critical insights into the

economic position of the voters of both generations contained in this “High Anxiety” report can

help serve as a roadmap for fostering better financial and retirement security and independence

including access to a new kind of retirement blueprint.

One solution that other states such as Illinois and Washington recently created is a state-

facilitated retirement plan for those with no workplace pension or 401k, which AARP believes

would ease Gen Xers’ and future generations’ worries. New York’s elected officials and state

policymakers are in a position to lend working New Yorkers a helping hand by ensuring that all

who want to save for their retirement have a simple option for doing so.

AARP is committed to ensuring New Yorkers are able to live their best lives as they age, and we

believe financial and retirement security are key to that goal. In the long run, helping our citizens

plan for their future and help themselves helps us all.

Sincerely,

Beth Finkel

State Director, AARP New York

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 4

EXECUTIVE SUMMARY Much attention has been paid to America’s retirement crisis.1 With disappearing pensions,

increasing longevity, a culture of spending versus saving and most recently the impact of the Great

Recession on wealth and security – the very

way that Americans “retire” is changing.

While Boomers are at the forefront of this

evolution, Gen X is the first generation that

will fully come into retirement age with a

new playbook, having lived the entirety of

their working years during the rise of 401k

plans and a shift away from traditional

pension plans.

As the first Gen Xers turn 50 this year,

survey results reveal that New York’s Gen X

voters are even more anxious about

retirement than their pre-retiree Boomer

counterparts. With lower confidence in Social

Security, fewer guaranteed benefits from

retirement plans and more widespread debt,

Gen X has reason to be worried.

One-fourth of New York’s Gen X and Boomer

aged labor force is not confident they will

ever be able to retire. One very big difference

between Gen X and Boomer generations

regarding retirement relates to their Social

Security expectations. Thirty-eight percent

(38%) of Gen Xers do not expect to receive

any Social Security in retirement, which is

nearly three times the share of equally

pessimistic Boomers (13%). Moreover, the

majority of Gen Xers who do expect to receive

any Social Security think it will be only a

minor share of their retirement income.

In spite of weaker expectations about Social

Security, Gen Xers are only marginally more

likely than Boomers to participate in

retirement savings. Thirty-seven percent of

1 For more discussion, see http://www.forbes.com/sites/edwardsiedle/2013/03/20/the-greatest-retirement-crisis-in-american-history/; and for more economic analysis: Are U.S. Workers Ready for Retirement? Schwartz Center for Economic Policy Analysis. 2014. http://www.economicpolicyresearch.org/images/docs/research/retirement_security/Are_US_Workers_Ready_for_Retirement.pdf

KEY SURVEY FINDINGS

The top personal finance concerns for

both Gen X and Boomer voters are: 1)

not saving enough; and 2) not

preparing enough for retirement.

In both cohorts, a majority feels

anxious about being able to have a

comfortable retirement and one-fourth

does not expect to retire at all.

30 percent of New York Gen Xers and

38 percent of Boomers have no

retirement savings.

Gen X workers have significantly

lower expectations of Social Security

than Boomers.

Paying for education and student loan

debt are barriers to retirement saving.

Seven in ten Gen Xers are either

current or expected future holders of

student debt.

Gen Xers indicate even stronger

likelihood than Boomers to leave New

York during retirement – 66 percent of

Gen X compared to 55 percent of

Boomers.

There is widespread voter support to

improve access to workplace

retirement plans with a state-

facilitated savings option.

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 5

Gen X workers and 48 percent of Boomer workers in New York either do not have access to

employer-sponsored retirement plans or do not participate in currently available employer plans.

Among all voters in each cohort and taking into consideration personal savings in retirement

accounts, 30 percent of Gen X and 38 percent of Boomers do not have any retirement savings

account at all.

For both Gen Xers and Boomers, a common obstacle to saving for retirement is not having enough

money after paying bills, which likely contributes to the lower likelihood of self-funding an

individual retirement account outside of work. AARP research shows that workers are 15 times

more likely to save for retirement if their employer offers a plan.2 In New York State, 54% of

private sector workers, or 3,621,611 people, are not offered a workplace retirement plan through

their employer.3

Paying for children’s education is also an obstacle to saving for retirement, particularly for Gen X.

Twenty-six percent of Gen X voters currently have student loan debt and nearly half (45%) expect

to acquire student loan debt in the future to pay for a college education for themselves or their

children. With two-thirds of student loan borrowers saying these loans make it even harder to save

for retirement, a significant number of Gen Xers are at risk of further jeopardizing their

retirement security due to student loans.

The Schwartz Center for Economic Policy Analysis estimates that 32 percent of New York state’s

present day near retirees are at risk of retiring with incomes below poverty level. The next

generation of retirees has arguably less favorable retirement circumstances, and yet, the majority of

Gen X expects to retire by age 65. This disconnect suggests a retirement reality gap and

demonstrates the need for more public financial literacy as well as new solutions.

Without a drastic change in their current retirement preparedness, Gen X will be forced to make

choices different than their parents’ generation for their retirement years. Retirement options for

many may include resorting to working longer, relying on family and public assistance or by

significantly reducing their standard of living.4 When faced with the reality of having to significantly

reduce consumption, concern about the affordability of living in New York may contribute to a pre-

meditated intention to leave the state post-retirement. Gen Xers indicate even stronger likelihood

than Boomers to leave New York during retirement – 66 percent of Gen X compared to 55 percent of

Boomers, with nearly one-fourth of Gen X saying they are extremely likely to leave.

Whether for themselves or others, a large majority of voters worry about New Yorkers having to

rely on public assistance in retirement because they have not prepared or lack access to plans.

Taxpayers and state government will certainly feel the impact of having to provide aid and

services to increasing numbers of potentially poor retirees.5

2 Data compiled by AARP’s Public Policy Institute from unpublished estimates from the Employee Benefit Research Institute of the 2004 Survey of income and Program Participation Wave 7 Topical Module (2006 data). 3 http://www.aarp.org/politics-society/advocacy/financial-security/info-2014/americans-without-retirement-plan.html 4 The Reality of the Retirement Crisis, January 2015. Center for American Progress. https://www.americanprogress.org/issues/economy/report/2015/01/26/105394/the-reality-of-the-retirement-crisis/ 5 The Cost of Retiring Poor. Retiring Poor Impact Study, January 2015. Notalyss. http://states.aarp.org/aarp-utah-commissions-study-on-cost-of-retiring-poor-in-the-state/

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 6

A legislative proposal for a state-facilitated retirement savings option that would be available to all

workers in New York garners strong support from a majority of all voters in both generational

cohorts, regardless of employment status or current access to workplace retirement plans. Gen X

and Boomer voters clearly want New York elected officials to support the creation of a state-

facilitated retirement savings option so that more New York workers have an opportunity to save

for retirement.

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 7

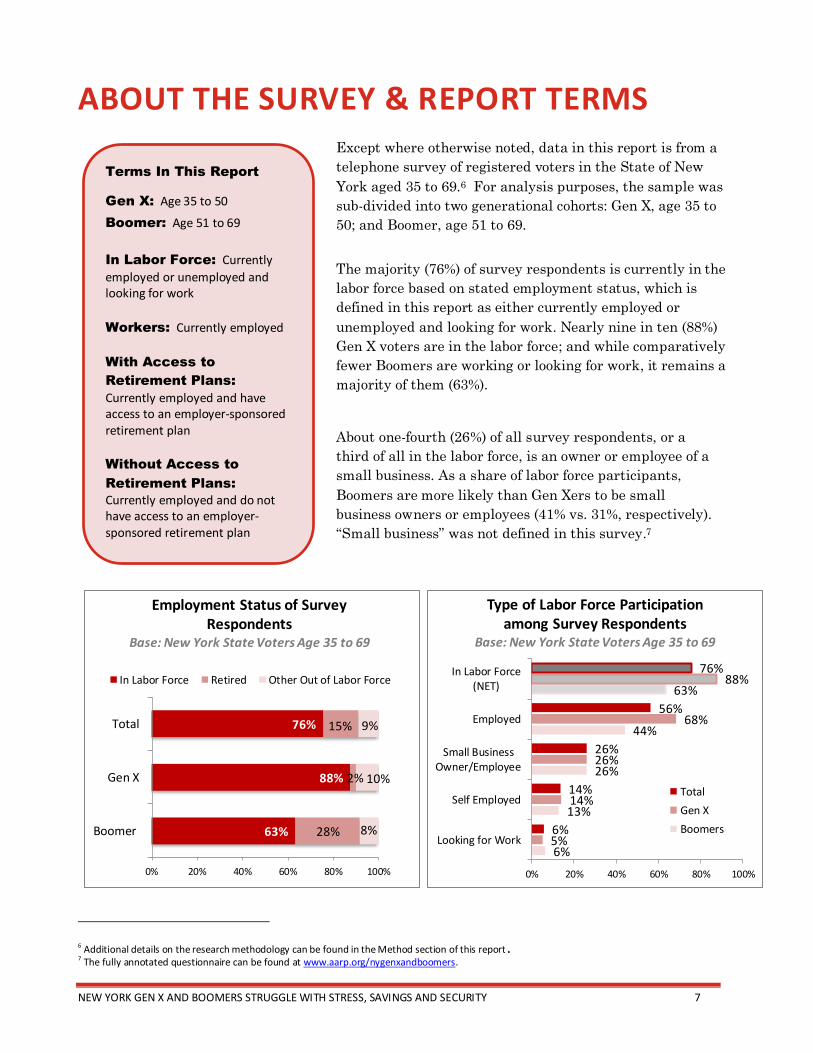

ABOUT THE SURVEY & REPORT TERMS Except where otherwise noted, data in this report is from a

telephone survey of registered voters in the State of New

York aged 35 to 69.6 For analysis purposes, the sample was

sub-divided into two generational cohorts: Gen X, age 35 to

50; and Boomer, age 51 to 69.

The majority (76%) of survey respondents is currently in the

labor force based on stated employment status, which is

defined in this report as either currently employed or

unemployed and looking for work. Nearly nine in ten (88%)

Gen X voters are in the labor force; and while comparatively

fewer Boomers are working or looking for work, it remains a

majority of them (63%).

About one-fourth (26%) of all survey respondents, or a

third of all in the labor force, is an owner or employee of a

small business. As a share of labor force participants,

Boomers are more likely than Gen Xers to be small

business owners or employees (41% vs. 31%, respectively).

“Small business” was not defined in this survey.7

6 Additional details on the research methodology can be found in the Method section of this report. 7 The fully annotated questionnaire can be found at www.aarp.org/nygenxandboomers.

63%

88%

76%

28%

2%

15%

8%

10%

9%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

Total

Employment Status of Survey Respondents

Base: New York State Voters Age 35 to 69

In Labor Force Retired Other Out of Labor Force

6%

13%

26%

44%

63%

5%

14%

26%

68%

88%

6%

14%

26%

56%

76%

0% 20% 40% 60% 80% 100%

Looking for Work

Self Employed

Small BusinessOwner/Employee

Employed

In Labor Force(NET)

Type of Labor Force Participation among Survey Respondents

Base: New York State Voters Age 35 to 69

Total

Gen X

Boomers

Terms In This Report

Gen X: Age 35 to 50

Boomer: Age 51 to 69

In Labor Force: Currently

employed or unemployed and looking for work

Workers: Currently employed

With Access to

Retirement Plans:

Currently employed and have access to an employer-sponsored retirement plan

Without Access to

Retirement Plans: Currently employed and do not have access to an employer-sponsored retirement plan

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 8

DETAILED SURVEY FINDINGS

CURRENT FINANCIAL SITUATION

According to the Bureau of Labor Statistics, the Great Recession ended in June 2009 after a 19-

month economic decline8. Since its end, the unemployment rate has decreased, the stock market

has returned to pre-recession levels and home values are increasing. Despite these economic

improvements, many still feel financially insecure. Nationally, as many as 35 percent of Gen X

workers and 40 percent of Boomer workers believe the Great Recession has not yet ended and only

one-fourth of either cohort say the economy is recovering or has fully recovered.9

Among surveyed New York voters age 35 to 69, nearly four in ten are dissatisfied with their

personal financial situation – 24 percent are somewhat dissatisfied and 13 percent are very

dissatisfied. Of note, a larger share of Gen Xers than Boomers report dissatisfaction with their

personal financial situation (40% vs. 33%, respectively).

In a list of personal financial concerns that include saving, debt, expenses and employment

opportunity into older age, the two things both Gen X and Boomers worry about most are saving

and planning for retirement. Nearly three-fourths (73%) of Gen Xers worry about not saving

enough and two-thirds (67%) worry about not planning enough for retirement. Among Boomers, six

in ten worry about not saving enough (62%) and more than half (55%) worry about not planning

enough for retirement.

8 http://www.bls.gov/opub/mlr/2014/article/consumer-spending-and-us-employment-from-the-recession-through-2022.htm

9 The Retirement Readiness of Three Unique Generations:Baby Boomers, Generation X, and Millennials. 15th Annual Transamerica Retirement Survey of Workers, April 2014, Transamerica Center for Retirement Studies (TCRS) https://www.transamericacenter.org/docs/default-source/resources/center-research/tcrs2014_sr_three_unique_generations.pdf

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 9

With the single exception of older worker security, Gen X is more likely than their Boomer

counterparts to worry about personal finances across the board, in particular about not saving

enough, not planning for retirement, having too much debt and not being able to pay bills. Despite

their theoretic longer time to plan for retirement compared to Boomers, this particular worry holds

a top of mind presence as often for Gen X as it does for Boomers.

14%

19%

18%

22%

30%

32%

16%

18%

24%

30%

25%

30%

0% 20% 40% 60% 80% 100%

Not being able to keep or find a jobbecause of age

Not being able to pay your bills

Having or taking on too much debt

Having an unexpected emergency that you won’t be able to pay for

Not planning enough for retirement

Not saving enough

How frequently do you worry about ... when it comes to your personal financial situation?

Base: New York State Boomer Voters

Often Sometimes

62%

55%

53%

42%

37%

29%

9%

21%

24%

23%

30%

41%

14%

26%

31%

35%

37%

33%

0% 20% 40% 60% 80% 100%

Not being able to keep or find ajob because of age

Not being able to pay your bills

Having or taking on too much debt

Having an unexpected emergency that you won’t be able to pay for

Not planning enough forretirement

Not saving enough

How frequently do you worry about ... when it comes to your personal financial situation?

Base: New York State Gen X Voters

Often Sometimes

73%

67%

58%

55%

47%

24%

Gen X:

Boomer:

74%

67%

58%

55%

47%

23%

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 10

CONFIDENCE IN RETIRI NG

As further confirmation that retirement, or rather lack of sufficient retirement planning and

saving, is a source of stress and anxiety, there is also lagging confidence in being able to ever retire

or to do so comfortably.

Among both Gen X and Boomer voter cohorts in New York, one-fourth of those in the labor force is

not confident they will ever be able to retire and another one-third is only somewhat confident. A

similar proportion of each age group feels anxious about not having enough money to live

comfortably through their retirement years, with Gen X slightly more likely to be anxious than

Boomers. It is clear that a substantial share of each generation is facing a tough reality of working

indefinitely and/or having to reduce their standard of living to below what is currently considered

comfortable.

The fact that confidence

levels in this regard

among Gen X are equal

to or worse than

Boomers suggests that

retirement

circumstances are not

going to improve for

younger generations.

Although Gen X has

more time to accelerate

savings and planning

before a hoped-for

retirement age, they are

not any more optimistic

than Boomers.

In brief, decreasing

retirement confidence

implies a future shift

toward the importance

of earning potential, job

opportunity and work

security during one’s

later years.

14% 19%

23% 25%

43% 35%

19% 20%

0%

20%

40%

60%

80%

Gen X Boomer

How anxious do you feel about having enough money to live comfortably through your retirement years?

Base: New York State Voters Age 35 to 69

Not anxious at all Not very anxious Somewhat anxious Very anxious

62% Anxious 55% Anxious

14%

17%

24%

22%

33%

32%

12%

14%

13%

11%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

How confident are you that you will be able to retire at some point and no longer work for money?

Base: New York State Voters in the Labor Force Age 35 to 69

Extremely Very Somewhat Not too Not at all

25% Not Confident

25% Not Confident

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 11

40%

26%

7%

18%

7%

30%

17% 16% 15% 16%

0%

20%

40%

60%

Under 65 65 66 to 69 70 and over Don't know

Expected Retirement Age Base: New York State Voters in the Labor Force Age 35 to 69, At Least Somewhat Confident They Will Retire

Gen X Boomer

43%

24%

11% 12% 9%

17% 22%

9%

31%

18%

0%

20%

40%

60%

Under 65 65 66 to 69 70 and over Don't know

Expected Retirement Age by Access to Workplace Retirement Plan

Base: New York State Voters in the Labor Force Age 35 to 69, At Least Somewhat Confident They Will Retire

With Access Without Access

For the three-fourths of voters age 35 to 69 currently in the New York labor force who expect to

retire, the average age of expected retirement is 65 for both Gen X and Boomers. However, two-

thirds of Gen X expects to retire at age 65 or before, whereas a larger percentage of older working

Boomers are unsure at what age they will retire.10 Although Gen X has more time to build up

savings, their expectations seem unrealistic considering nearly one-third of New York State’s

present day near retirees are at risk of retiring with incomes below poverty level.11

Having access to an employer-sponsored retirement savings plan makes a significant difference in

worker expectations about working into later life. Forty-three percent of those with access to

workplace retirement plans expect to retire under age 65 compared to only 17 percent of those

without access. On the other end of the spectrum, 31 percent of those without access to a plan

expect to work until age 70 and beyond before retiring, versus 12 percent of those with access to a

plan saying the same.

10 Similar results reported nationally: Gen X workers are significantly more likely than Boomer workers to expect to retire at age 65 (36% vs 18%). https://www.transamericacenter.org/docs/default-source/resources/center-research/tcrs2014_sr_three_unique_generations.pdf 11 Are U.S. Workers Ready for Retirement? Schwartz Center for Economic Policy Analysis. 2014. http://www.economicpolicyresearch.org/images/docs/research/retirement_security/Are_US_Workers_Ready_for_Retirement.pdf

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 12

24%

40%

42%

42%

13%

16%

25%

21%

5%

11%

10%

10%

52%

29%

20%

24%

0% 20% 40% 60% 80% 100%

Small BusinessOwner orEmployee

Boomer

Gen X

Total

Which of the following ways to save for retirement does your current employer provide?

Base: Currently Employed New York State Voters Age 35 to 69

Both Defined Benefit and Defined Contribution DC Only DB Only None

ACCESS TO RETIREMENT PLANS (AMONG EMPLOYED12)

In New York, 20 percent of Gen X workers and 29 percent of Boomer workers have no access to a

workplace retirement savings plan. While many in both generations have access to both Defined

Contribution and Defined Benefit plans, Defined Contribution plans are much more common for

Gen X workers.

For small business owners and employees in the state, half of them (52%) have no access at all to a

workplace retirement savings plan - a level comparable to that of all private sector workers in the

state.13

Retirement confidence is correlated

with access to retirement plans.

Among Gen X and Boomer workers

in New York without access to plans,

nearly one in three (31%) is not

confident they will ever be able to

retire compared to one in five (20%)

among those with access.

12 Survey data includes both public and private sector workers. 13 Fifty-four percent of private sector employees or 3,621,611 New York workers had no access to retirement plans through their employer (average 2010-2012). http://www.aarp.org/politics-society/advocacy/financial-security/info-2014/americans-without-retirement-plan.html

56%

29%

46%

31%

20%

0% 20% 40% 60% 80% 100%

Without Access toWorkplace

Retirement Plan

With Access toWorkplace

Retirement Plan

Extremely/Very confident Not too/Not at all confident

How confident are you that you will be able to retire at some point and no longer work for money?

Base: Currently Employed New York State Voters Age 35 to 69

NET PLAN

ACCESS

Defined Contribution

Total = 63% Gen X = 67% Boomer = 56% Small Business = 37%

Defined Benefit

Total = 52% Gen X = 52% Boomer = 51% Small Business = 29%

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 13

RETIREMENT SAVINGS B EHAVIOR

Taking into account plan participation,

overall workplace retirement saving is

even less common. Thirty-seven percent of

Gen X workers and 48 percent of Boomer

workers are not saving through a

workplace retirement plan. Among small

business owners and employees, the rate

of non-participation is comparatively

lower. Yet, due to limited availability of

plans, nearly two-thirds of small business

owners and employees are not saving for

retirement through a workplace plan.

Without workplace retirement plans, it is

even more important to build up personal

savings through an IRA or other

retirement savings plan. However, just

under half of surveyed New York voters

age 35 to 69 have done so.

When taken together and on net, 30

percent of Gen X voters in New York and

38 percent of Boomers have neither a work

sponsored nor a personal retirement

savings plan. A similar share of small

business owners and employees is not

saving at all (35%) and just over half are

saving in personal retirement savings

accounts outside of work.

24% 20% 29%

52% 41% 37%

48%

65%

0%

20%

40%

60%

80%

Total Gen X Boomer Small BusinessOwner/

Employee

Workplace Retirement Plans (Among Workers)*

Base: Currently Employed New York State Voters Age 35 to 69

No Access to Workplace Retirement Plan

Do Not Participate in Workplace Retirement Plan

35%

28%

51%

39%

54%

50%

46%

48%

35%

38%

30%

34%

0% 20% 40% 60% 80%

Small BusinessOwner orEmployee

Boomer

Gen X

Total

Total Retirement Savings (All Voters) Base: New York State Voters Age 35 to 69

None

Personal

Employersponsored

*Note: Survey data includes both public and private workers.

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 14

RETIREMENT INCOME EXPECTATIONS

In spite of lagging participation in retirement plans or savings accounts, both Gen Xers and

Boomers are most likely to expect their largest share of retirement income to come from a

retirement savings plan. But, when it comes to expectations of Social Security, there are

significant differences between the generations.

Nearly eight in ten (79%) Gen Xers say their savings will provide the largest share of their income

in retirement – either from a retirement plan or their own personal savings outside of a retirement

plan or account. Just 14 percent of

Gen X say that Social Security will

be their largest share of income.

Furthermore, 38 percent of Gen X

voters in New York do not expect to

receive any Social Security income

at all.

Among Boomers, twice as many

(30%) say Social Security will be

their largest share of income in

retirement and just 13 percent do

not expect to receive any social

security income at all in retirement.

Among workers without access to

workplace retirement plans, about

half have personal retirement plan

accounts such as an IRA (54%) -

only slightly more than all workers

in the 35 to 69 age cohort (48%).

However, just one-third of workers

without access to workplace

retirement plans expect their

retirement savings to be their major

source of income. Somewhat larger

shares expect personal savings

outside of retirement accounts or

Social Security to provide their

largest share of income, but a fairly

sizeable portion (22 percent) do not

expect to receive any Social

Security income at all.

9%

12%

5%

18%

18%

9%

50%

56%

48%

22%

13%

38%

0% 20% 40% 60% 80% 100%

No Access toWorkplace

Retirement Plan

Boomer

Gen X

Role or Expected Role of Social Security in Retirement Income

Base: New York State Voters Age 35 to 69

Only Source Major Source Minor Source None

62% Any SS Income

87% Any SS Income

78% Any SS Income

12%

24%

28%

35%

9%

11%

30%

49%

7%

18%

14%

61%

0% 20% 40% 60% 80%

Other/Don't Know

Personal savings orinvestments not in a

retirement plan

Social Security

A retirement savingsplan, like a pension,

401k or IRA

Percent Expecting Each Source to Provide the Largest Share of Retirement Income Base: New York State Voters Age 35 to 69

Gen X

Boomer

No Access toWorkplaceRetirement Plan

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 15

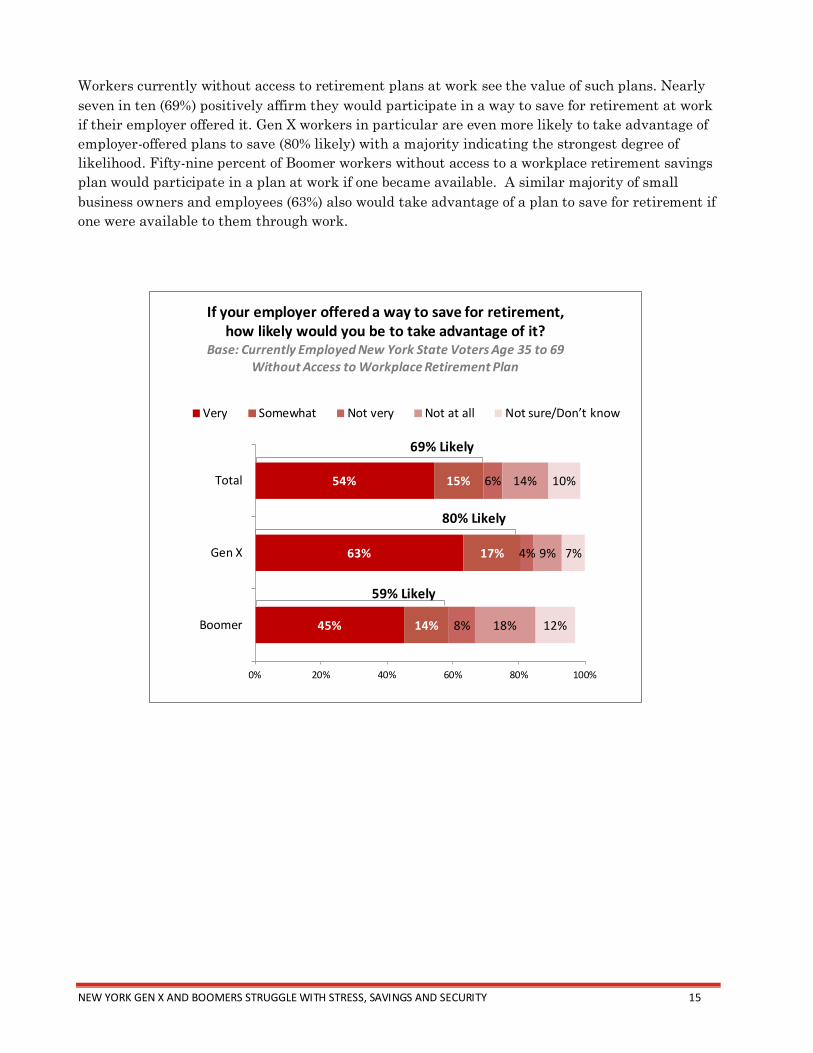

Workers currently without access to retirement plans at work see the value of such plans. Nearly

seven in ten (69%) positively affirm they would participate in a way to save for retirement at work

if their employer offered it. Gen X workers in particular are even more likely to take advantage of

employer-offered plans to save (80% likely) with a majority indicating the strongest degree of

likelihood. Fifty-nine percent of Boomer workers without access to a workplace retirement savings

plan would participate in a plan at work if one became available. A similar majority of small

business owners and employees (63%) also would take advantage of a plan to save for retirement if

one were available to them through work.

45%

63%

54%

14%

17%

15%

8%

4%

6%

18%

9%

14%

12%

7%

10%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

Total

If your employer offered a way to save for retirement, how likely would you be to take advantage of it?

Base: Currently Employed New York State Voters Age 35 to 69 Without Access to Workplace Retirement Plan

Very Somewhat Not very Not at all Not sure/Don’t know

69% Likely

80% Likely

59% Likely

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 16

DEBT AND OTHER BARRI ERS TO SAVING

Despite high levels of anxiety about not saving or preparing enough for retirement, current

expenses are considered financial barriers for many New York voters age 35 to 69. The most

reported obstacle is not having enough money left after paying bills –more than half (56%) report

this as an obstacle; and nearly half (49%) are hindered by paying for their children’s education.

Two in five say losing a job or taking a pay cut (41%), facing a major health need (41%), or having

to pay off debt (40%) are

obstacles to saving for

retirement years. Other

major obstacles to saving for

retirement are moving or

purchasing a new home (34%),

caring for an elderly loved one

(33%), and decreased property

value (32%). On all items,

Gen X is more likely than

Boomers to cite them as

obstacles to saving for

retirement, save one: facing a

major health need or problem.

In its ongoing Retirement

Confidence Survey, the

Employee Benefit Research

Institute (EBRI) has

consistently found a

relationship between the

level of debt among workers

and their retirement

confidence.14 In New York,

the majority of Gen X and

Boomer aged voters (80%)

have some form of debt.

When asked about types of

loans or debt currently held,

credit cards (55%) and home

loans (53%) were the most

reported. For nearly all types

of debt included in the survey,

Gen Xers are more likely to

have it than Boomers.

14 2015 Retirement Confidence Survey, Employee Benefit Research Institute. http://www.ebri.org/surveys/rcs/2015/

32%

32%

32%

36%

43%

39%

42%

54%

32%

34%

37%

44%

38%

44%

56%

59%

0% 20% 40% 60% 80%

Decreased home value

Caring for an elderly parent or relative

New home purchase or move

Having a lot of debt to pay off

Facing a major health need

Losing a job or taking a big pay cut

Paying for children’s education

No money left after paying for bills

Major Obstacles to Saving For Retirement Years Base: New York State Voters Age 35 to 69

Gen X

Boomer

11%

15%

33%

46%

51%

74%

10%

26%

44%

59%

59%

85%

11%

21%

39%

53%

55%

80%

0% 20% 40% 60% 80% 100%

Any other type of loan ordebt

Student loan

Auto loan

Home loan

Credit card

Any Loan/Debt (NET)

Types of Loans or Debt Currently Held Base: New York State Voters Age 35 to 69

Total

Gen X

Boomer

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 17

With regard to student loans

specifically, about one in five (21%) of

Gen X and Boomer voters currently

have student loan debt. Notably, even

more (33%) expect to have student

loans in the future – this is true for

both Gen X (45%) as well as Boomers

(20%). One-fourth of Gen X voters

currently have student loans and an

incredible 45 percent expect to

become student loan holders in the

future. Among Boomers, levels are

relatively lower but still one-third

overall are either current or future

student loan borrowers.

Two-thirds of current and future

student loan holders say paying off

such debt has made or will make it

harder to save for retirement.

Significant proportions also say it has

a negative impact on paying bills or

affording a home.

As might be expected, the presence of

debt is correlated with a much higher

likelihood to worry about personal

finances and at a more frequent rate.

While all Gen X and Boomer New

Yorkers worry about saving enough

and planning for retirement, student

loan holders are 33 percent more

likely to worry about these concerns.

Furthermore, holders of student loan

debt are less likely to be satisfied

with their personal financial

situation (47% versus 63% satisfied

among all 35 to 69 year olds); and are

significantly more likely to cite

barriers to saving for retirement, in

particular having no money after

paying for bills (73% vs. 56%); paying

for children’s education (69% vs.

49%); and having too much debt (67%

vs. 40%).

54%

71%

35%

21% 26%

15%

33%

45%

20%

0%

20%

40%

60%

80%

100%

Total Gen X Boomer

Current and Expected Future Student Loan Holders

Base: New York State Voters Age 35 to 69

Current or Future (Net) Current Future

40%

55%

65%

0% 20% 40% 60% 80% 100%

Make it harder for you toafford a home

Make it harder for you topay other bills or make ends

meet

Make it harder for you tosave for retirement

In What Ways Do You Worry that Paying Off Student Loan Debt Will Affect You?

Base: Expected Future Student Loan Holders Among New York State Voters Age 35 to 69

38%

60%

68%

0% 20% 40% 60% 80% 100%

Made it harder to afford ahome

Made it harder to pay otherbills or make ends meet

Made it harder to save forretirement

In What Ways Has Paying Off Student Loan Debt Affected You?

Base: Current Student Loan Holders Among New York State Voters Age 35 to 69

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 18

NEW YORK AFFORDABILITY

For both generational cohorts, the most

commonly cited obstacle to saving for

retirement is not having enough money left

after paying for bills. For New Yorkers, the

affordability of month-to-month housing

expenses is concerning to both Gen X and

Boomer voters. Half or more of each group is

at least somewhat concerned about their

ability to pay rent/mortgage, property taxes

or utility bills in the coming years. In general,

the level of concern is comparable between

the two age groups with little variation or

differentiation.

12%

12%

14%

14%

20%

28%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

How concerned are you about your ability to pay RENT/MORTGAGE in the

future? Base: New York State Voters Age 35 to 69

Extremely concerned Very concerned Somewhat concerned

54%

15%

14%

22%

17%

25%

27%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

How concerned are you about your ability to pay PROPERTY TAXES in the

future? Base: New York State Voters Age 35 to 69

Extremely concerned Very concerned Somewhat concerned

13%

9%

14%

13%

26%

30%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

How concerned are you about your ability to pay UTILITY BILLS in the

future? Base: New York State Voters Age 35 to 69

Extremely concerned Very concerned Somewhat concerned

46%

58%

62%

52%

53%

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 19

Three out of five (60%) New York State voters age 35 to 69 say they are at least somewhat likely to

leave New York once they retire. A 2014 AARP survey of New York voters found that 60% of future

Baby Boomer retirees were likely to leave New York State after retiring, thus creating economic

implications for the state economy when retirees take their consumer expenditures elsewhere. 15

Here again in this survey, a near similar proportion of Boomers age 51 to 69 are at least somewhat

likely to leave the state in the future (55%). Moreover, Gen X presents even stronger intent to

leave the state post-retirement. Nearly one-fourth (23%) of Gen X voters in New York can scarcely

see themselves retiring in the state, reporting extreme likelihood of leaving once they retire. A

total of 66 percent of Gen Xers consider themselves at least somewhat likely to leave.

15 2014 State of the 50+ in New York State, AARP Research. www.aarp.org/nystate50plus

13%

23%

18%

16%

18%

17%

25%

26%

26%

19%

18%

19%

26%

15%

20%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

Total

How likely are you to leave New York State and live somewhere else once you retire/in the future?

Base: New York State Voters Age 35 to 69

Extremely likely Very likely Somewhat likely Not very likely Not at all likely

60% Likely

66% Likely

55% Likely

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 20

SUPPORT FOR A STATE FACILITATED RETIREMENT SAVINGS OPTION

In order to help close the gap in access to

retirement savings plans, New York voters

age 35 to 69 support a state facilitated

retirement savings option for New York.

Specifically, about seven in ten strongly

(44%) or somewhat (27%) support such a

proposal.

A state facilitated retirement savings option

would most directly benefit those without

access to a plan in their workplace, including

small business owners and employees who

tend to have lower levels of access currently.

These two sub-groups of New York workers

present similarly strong levels of support for

such a solution. More than three-fourths of

workers without access to a workplace

retirement plan support a proposal for a state-facilitated plan; and 70 percent of small business

owners and employees support it.

45%

47%

45%

42%

44%

25%

29%

22%

31%

27%

11%

10%

13%

11%

12%

4%

4%

6%

5%

5%

10%

7%

8%

8%

8%

0% 20% 40% 60% 80% 100%

Small Business Owner orEmployee

Without Access toWorkplace Retirement

Plan

Boomer

Gen X

Total

How Strongly do you support or oppose the proposal for a state retirement savings plan?

Base: New York State Voters in the Labor Force Age 35 to 69

Strongly support Somewhat support Neither/nor Somewhat oppose Strongly oppose

70% Support

73% Support

67% Support

76% Support

70% Support

PROPOSED STATE FACILITATED

RETIREMENT SAVINGS OPTION FOR

WORKERS

One way to help more New Yorkers save would be for

the state to set up a retirement savings plan, similar to

a 529 college savings plan, where workers can

contribute to a private retirement account that is

professionally managed. Workers can choose whether

or not to participate, and the account would be

portable from job to job. The plan would have low fees

and not cost taxpayer dollars.

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 21

When asked about potential features in a state facilitated savings option for retirement, all

features are considered important. The top-ranked important feature is portability. Almost all

(92%) believe account funds should be portable so that the money travels with the owner. About

nine in ten also say it should be easy to use (90%), have a low cost to taxpayers and participants

(89%), provide tax advantages to enrollees (88%), be voluntary (88%) and be available to everyone

(87%). Many (81%) also believe it is important for the money to be professionally managed.

51%

68%

68%

66%

72%

76%

74%

82%

30%

19%

20%

22%

17%

13%

16%

10%

0% 20% 40% 60% 80% 100%

Professional money management

Available to everyone in the state

Voluntary enrollment

Tax advantages for enrollees

Low cost to participants

Low cost to taxpayers

Easy to use

Portability (account can move from job to job)

If New York Were to Implement a Retirement Savings Plan, How Important Would Each Feature Be?

Base: New York State Voters Age 35 to 69

Very Important Somewhat Important

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 22

Most (75%) New York voters age 35 to 69 agree that New York elected officials should support

creating a state managed retirement savings plan so more New York workers have an opportunity

to save for retirement. Forty-three percent strongly agree that this should be a concern of elected

officials.

Taxpayers themselves are

concerned that New Yorkers are

not saving enough for retirement.

A majority (82%) are concerned

that many could end up relying on

public assistance. Almost half of

New York voters are very

concerned while another third

(34%) are somewhat concerned.

Although Gen X and Boomers are

comparably worried, Boomers are

slightly more likely to be very

concerned that retirees are ill

prepared and will become reliant

on public aid.

50%

46%

48%

33%

35%

34%

9%

12%

10%

7%

6%

7%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

Total

How concerned are you as a taxpayer that some New Yorkers have not saved enough for

retirement and could end up reliant on public assistance?

Base: New York State Voters Age 35 to 69

Very Somewhat Not very Not at all

82% Concerned

81% Concerned

83% Concerned

45%

43%

43%

29%

33%

33%

12%

12%

12%

3%

3%

3%

8%

7%

7%

0% 20% 40% 60% 80% 100%

Boomer

Gen X

Total

Should New York elected officials support the creation of a state managed retirement savings plan?

Base: New York State Voters Age 35 to 69

Strongly agree Somewhat agree Neither/nor Somewhat disagree Strongly disagree

75% Agree

76% Agree

74% Agree

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 23

DEMOGRAPHIC PROFILE OF RESPONDENTS

72%

3%

9%

15%

24%

74%

22%

26%

25%

26%

36%

24%

23%

13%

28%

30%

21%

17%

9%

13%

16%

15%

16%

14%

18%

29%

21%

26%

23%

1%

12%

11%

69%

4%

Married or living with a partner

Widowed

Divorced or separated

Never married

AARP Member

AARP Non-Member

High school graduate or less

Post high school or 2 year degree

4 year degree

Post graduate study or graduate degree

Democrat

Republican

Independent

Something else

Conservative

Moderate

Liberal

None of these

<$30K

$30K-<$50K

$50K-<$75K

$75K-<$100K

$100,000-<$150,000

$150,000+

Don't know/Refused

35-44

45-50

51-60

61-69

Asian

Black or African American

Hispanic or Latino

White or Caucasian

Mixed/ some other race

CIV

IL S

TATU

SA

AR

PED

UC

ATI

ON

PA

RT

YA

FFIL

IAT

ION

PO

LITI

CA

LV

IEW

SIN

CO

ME

AG

ER

AC

E

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 24

Gen X Boomers

Civil Status

Married or living with a partner 72% 64%

Widowed 1% 5%

Divorced or separated 3% 14%

Never married 19% 12%

Membership

AARP 7% 42%

AARP Non-Member 92% 56%

Education

High school graduate or less 18% 27%

Post high school or 2 year degree 26% 25%

4 year degree 27% 23%

Post graduate or graduate degree 28% 24%

Party Affiliation

Democrat 34% 38%

Republican 22% 25%

Independent 25% 21%

Something else 16% 11%

Political Views

Conservative 26% 30%

Moderate 30% 29%

Liberal 20% 22%

None of these 20% 14%

Income

<$30K 8% 11%

$30K-<$50K 8% 18%

$50K-<$75K 15% 18%

$75K-<$100K 17% 12%

$100,000-<$150,000 18% 13%

$150,000+ 17% 11%

Don't know/Refused 16% 18%

Race/Ethnicity

Asian 2% 1%

Black or African American 15% 10%

Hispanic or Latino 13% 8%

White or Caucasian 65% 72%

Mixed/ some other race 3% 5%

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 25

METHODOLOGY

AARP 2015 NY State Gen X-Boomer Survey

Prepared by Precision Opinion for AARP

May 2015

SUMMARY:

The AARP 2015 New York State Gen X-Boomer Survey was conducted as a telephone survey among

registered voters age 35 to 69 in the state of New York. The survey collected the opinions of New York

registered voters on issues related to financial worries and retirement security. The survey was

approximately 15 minutes in length. The interviews were conducted in English by Precision Opinion from

February 26th to March 12th, 2015. Respondents were sampled from a voter list with a total of 801

interviews completed: 400 among 35 to 50 year old voters (“Gen X”) and 401 among 51 to 69 year old voters

(“Boomer”). The sample was split into two strata by age (Gen X and Boomer) and quotas were set in order to

achieve a 50/50 split among these two cohorts. In addition, quotas were set by gender within age group in

order to maintain the proper representation of males and females. The margin of sampling error for the New

York statewide sample of 801 is +/-3.5%. The margin of sampling error for the Gen X and Boomer samples

of 400 each is +/-5.0%.

DESIGN AND DATA COLLECTION PROCEDURES:

Sample

The survey respondents were sampled from a registered voter list provided by L2 (Labels & Lists). The voter

list was age targeted to 35-69 based on L2’s database of registered voters in the state of New York. The

sample list was a blended landline and cell phone. A total of 36,178 records were dialed. From this total,

12,329 cell phone records were dialed, from which 98 surveys were completed.

Questionnaire Development and Testing

The questionnaire was developed by AARP staff. Prior to this project’s launch, testing was completed

internally at Precision Opinion and additionally by AARP staff. Further, Precision Opinion ran a simulated

data set and conducted a full review of said data prior to commencing field work.

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 26

Contact Procedures

Precision Opinion asked to speak with the registered voter listed on file. If that person was unavailable,

Precision Opinion asked to speak with another registered voter in the household aged 35-69.

WEIGHTING

The sample was weighted by gender and region within the Generation X and Baby Boomer strata. The

combined sample was weighted by gender and region to reflect the total population of registered voters in

the state of New York age 35-69.

Total 35 to 69 Unweighted

Total 35 to 69 Weighted Factor

N= % N= %

Total 801

801

Male 366 45.69% 368 45.99% 1.00650

Female 435 54.31% 433 54.01% 0.99453

NYC 208 25.97% 306 38.16% 1.46953

Long Island 101 12.61% 137 17.13% 1.35853

Erie 56 6.99% 42 5.20% 0.74379

Onondaga 27 3.37% 20 2.51% 0.74463

Dutchess 7 0.87% 13 1.58% 1.80797

Monroe 42 5.24% 32 4.04% 0.77049

Capital Region 31 3.87% 38 4.73% 1.22217

Rest of state 329 41.07% 213 26.65% 0.64883

Gen X Unweighted

Gen X Weighted Factor

N= % N= %

Total 400

400

Male 180 45.00% 182 45.50% 1.01111

Female 220 55.00% 218 54.50% 0.99091

NYC 110 27.50% 171 42.68% 1.55200

Long Island 54 13.50% 66 16.56% 1.22667

Erie 28 7.00% 19 4.86% 0.69429

Onondaga 14 3.50% 9 2.32% 0.66286

Dutchess 2 0.50% 6 1.42% 2.83999

Monroe 21 5.25% 15 3.80% 0.72381

Capital Region 13 3.25% 18 4.42% 1.36000

Rest of state 158 39.50% 96 23.94% 0.60608

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 27

Boomer Unweighted

Boomer Weighted Factor

N= %= N= %=

Total 401

401

Male 186 46.38% 185 46.25% 0.99711

Female 215 53.62% 216 53.75% 1.00250

NYC 98 24.44% 140 34.82% 1.42478

Long Island 47 11.72% 73 18.23% 1.55537

Erie 28 6.98% 22 5.42% 0.77622

Onondaga 13 3.24% 11 2.65% 0.81742

Dutchess 5 1.25% 7 1.77% 1.41954

Monroe 21 5.24% 17 4.18% 0.79818

Capital Region 18 4.49% 20 4.87% 1.08493

Rest of state 171 42.64% 113 28.06% 0.65802

Note: Universe proportions according to L2 database for all registered voters, state of New York age 35-69.

RESPONSE RATE / COOPERATION RATE / REFUSAL RATE

The response rate for this study was measured using AAPOR’s response rate 3 method. The cooperation

rate was measured using AAPOR’s cooperation rate 3 method. The refusal rate was measured using

AAPOR’s refusal rate 3 method. The table below contains these rates.

Response Rate Cooperation Rate Refusal Rate

Total 11% 92% 4%

Gen X 10% 93% 3%

Boomer 12% 92% 5%

*Source: AAPOR Outcome Rate Calculator Version 2.1 May 2003

ANNOTATED QUESTIONNAIRE

A fully annotated questionnaire and more information about this survey can be found at:

www.aarp.org/nygenxandboomers.

NEW YORK GEN X AND BOOMERS STRUGGLE WITH STRESS, SAVINGS AND SECURITY 28

AARP New York

780 Third Ave 33rd Floor

New York, NY 10017

Phone: (866) 227-7442

Email: [email protected]

Website: http://www.aarp.org/ny

AARP Research

601 E Street NW

Washington, DC 20049

www.aarp.org/research