2015 nacha presentation - ach network roadmap for iso 20022

TRANSCRIPT

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

ACH Network Roadmap for ISO 20022

Robert Unger, Senior Director, NACHA

Nasreen Quibria, Managing Director, Q insights

Tom Durkin, Managing Director, Bank of America

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

2

Today’s Discussion

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

3

ISO 20022 Overview

What is ISO?• The International Standards Organization

• The U.S. is a member and contributor through the Accredited Standards

Committee (ASC) X9

What is ISO 20022?• A harmonized set of XML messaging standards across major financial services

domains – Payments, Securities, Trade, Card and FX

• Based on a shared data dictionary and business process model

• Freely available to all members of the financial services community

• Foundation of SWIFT’s future standards development (SWIFT MX)

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

4

What is ISO 20022 for Payments?

SWIFT’s ISO 20022 adoption mApp for iPad - download from the App Store

on https://itunes.apple.com/app/iso-20022-adoption-88197590?ls=1&mt=8

Live ISO 20022 standards or on the future roadmap…

› Robust standard with room

for additional payment-

related information –

addresses end-to-end

communications – from the

remitter through beneficiary

› Standard being adopted by

an increasing number of the

world’s payments, clearing &

settlement systems

› Growing interest from

financial institutions,

corporations and financial

applications providers

› SWIFT Standards and the

Payments Market Practice

Group have developed

global implementation

guidelines for high-value

payments with a cross-border

leg

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

5

Who are the players?

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

6

“One Foot in the Present and the Other in the Future”

› Meeting the current needs

of early adopter and

innovative end-users

› Leading the U.S. payments

industry in the future

adoption of ISO 20022

NACHA’s implementation and support strategy for the ISO 20022 Payment Messaging Standard and the ACH Network includes two focal points:

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

7

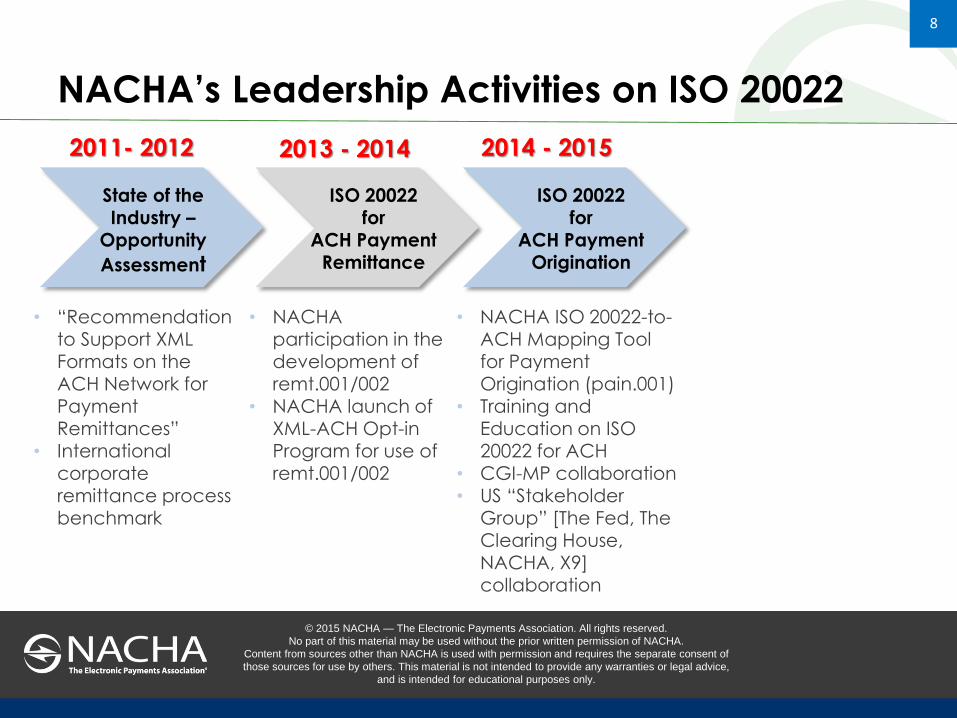

NACHA’s Leadership Activities on ISO 20022

2011- 2012 2013 - 2014

• “Recommendation to Support XML Formats on the ACH Network for Payment Remittances”

• International corporate remittance process benchmark

State of the Industry –

Opportunity

Assessment

ISO 20022 for

ACH Payment Remittance

• NACHA participation in the development of remt.001/002

• NACHA launch of XML-ACH Opt-in Program for use of remt.001/002

› In 2013, NACHA launched an XML-ACH Opt-in

Program that allows participants to exchanged

XML formatted payments information for CTX

transactions

‾ Participating FI’s must sign up to send and

receive

‾ NACHA developed XML schema, data

dictionary, and rules

‾ Formatting was harmonized with FED’s ERI

specification

› In 2014, NACHA completed its work with industry

partner IFX-Interactive Financial Exchange for

the ISO submission and approval of two ISO

20022 messages for payments information

(remt.001) (remt.002)

‾ ISO 20022 remt messages maybe sent with

payment instructions or stand-alone

‾ https://www.nacha.org/programs/xml-

ach-remittance-xml-ach

› In 2014, NACHA completed work to adopt ISO

20022 remit messaging for its XML Remittance

Opt-in Program

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

8

NACHA’s Leadership Activities on ISO 20022

2011- 2012 2013 - 2014 2014 - 2015

• “Recommendation to Support XML Formats on the ACH Network for Payment Remittances”

• International corporate remittance process benchmark

State of the Industry –

Opportunity

Assessment

ISO 20022 for

ACH Payment Remittance

ISO 20022 for

ACH Payment Origination

• NACHA participation in the development of remt.001/002

• NACHA launch of XML-ACH Opt-in Program for use of remt.001/002

• NACHA ISO 20022-to-ACH Mapping Tool for Payment Origination (pain.001)

• Training and Education on ISO 20022 for ACH

• CGI-MP collaboration• US “Stakeholder

Group” [The Fed, The Clearing House, NACHA, X9] collaboration

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

9

ISO 20022 Business Case Assessment Strategic Reasons to Consider ISO 20022 Adoption in the U.S. Market

Strategic Reason Description

Global Momentum Large U.S. corporates and banks are actively adopting ISO 20022 and that is

expected to continue.

Global Competition Compatibility with the ISO 20022 format enables the United States to maintain

parity with other global markets and U.S. dollar clearing systems in other

jurisdictions that are adopting ISO 20022 messaging, which may help preserve the

attractiveness of the U.S. dollar as a global currency.

Cost Savings &

Processing Efficiency

Standardizing message formats allows for consolidation of payments platforms at

banks and corporations, which could promote straight-through processing and

drive down costs.

Consistent & Rich Data The ISO 20022 format enables all parties to leverage a common set of data

dictionary elements and expands capacity to carry rich data in the payment

message.

Interoperability A common format promotes ease of transacting domestically and globally by

using a single, open standard rather than multiple proprietary standards.

Agility to meet evolving

regulatory needs

The ISO 20022 format provides for full originator and receiver information (third

party or ultimate beneficiary) allowing for improved regulatory reporting and

monitoring.

New, innovative

products

A common format across systems reduces the amount of change required to

bring innovative new products and services to market.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

10

NACHA’s Leadership Activities on ISO 20022

2011- 2012 2013 - 2014 2014 - 2015

• “Recommendation to Support XML Formats on the ACH Network for Payment Remittances”

• International corporate remittance process benchmark

State of the Industry –

Opportunity

Assessment

ISO 20022 for

ACH Payment Remittance

ISO 20022 for

ACH Payment Origination

• NACHA participation in the development of remt.001/002

• NACHA launch of XML-ACH Opt-in Program for use of remt.001/002

• NACHA ISO 20022-to-ACH Mapping Tool for Payment Origination (pain.001)

• Training and Education on ISO 20022 for ACH

• CGI-MP collaboration• US “Stakeholder

Group” [The Fed, The Clearing House, NACHA, X9] collaboration

7

› 1st QTR 2015 NACHA

releases the ISO 20022

Mapping Guide to

standardize ODFI

conversion of ISO 20022

(pain) messaging to ACH

formats:

– CTX, CCD, and IAT

credit transactions will

be initially supported

– Payments Remittance

information mapping is

included

– Guidelines for returns

and exceptions is

included

The NACHA ISO 20022 Mapping Guide will allow financial institutions to better serve the needs of originators that are planning too or have adopted ISO20022

for accounts payable functions

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

11

NACHA’s Leadership Activities on ISO 20022

2011- 2012 2013 - 2014 2014 - 2015 Future

• “Recommendation to Support XML Formats on the ACH Network for Payment Remittances”

• International corporate remittance process benchmark

State of the Industry –

Opportunity

Assessment

ISO 20022 for

ACH Payment Remittance

ISO 20022 for

ACH Payment Origination

Full Compatibility

with ISO 20022

• NACHA participation in the development of remt.001/002

• NACHA launch of XML-ACH Opt-in Program for use of remt.001/002

• Assess NACHA Rules update to require RDFI receipt of ISO 20022 XML

• Evaluate ACH Network infrastructure migration to ISO 20022 XML

• NACHA ISO 20022-to-ACH Mapping Tool for Payment Origination (pain.001)

• Training and Education on ISO 20022 for ACH

• CGI-MP collaboration• US “Stakeholder

Group” [The Fed, The Clearing House, NACHA, X9] collaboration

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

12

Today’s Discussion

NACHA ISO 20022 Tools

13

The NACHA ISO 20022 Tool and Guide were developed

with the helpful information provided by the following financial institutions and large global corporations:

Bank of America Bayer Bank of New York Mellon Citi

Deutsche Bank JPMorgan Chase Microsoft PNC

Wells Fargo US Bank

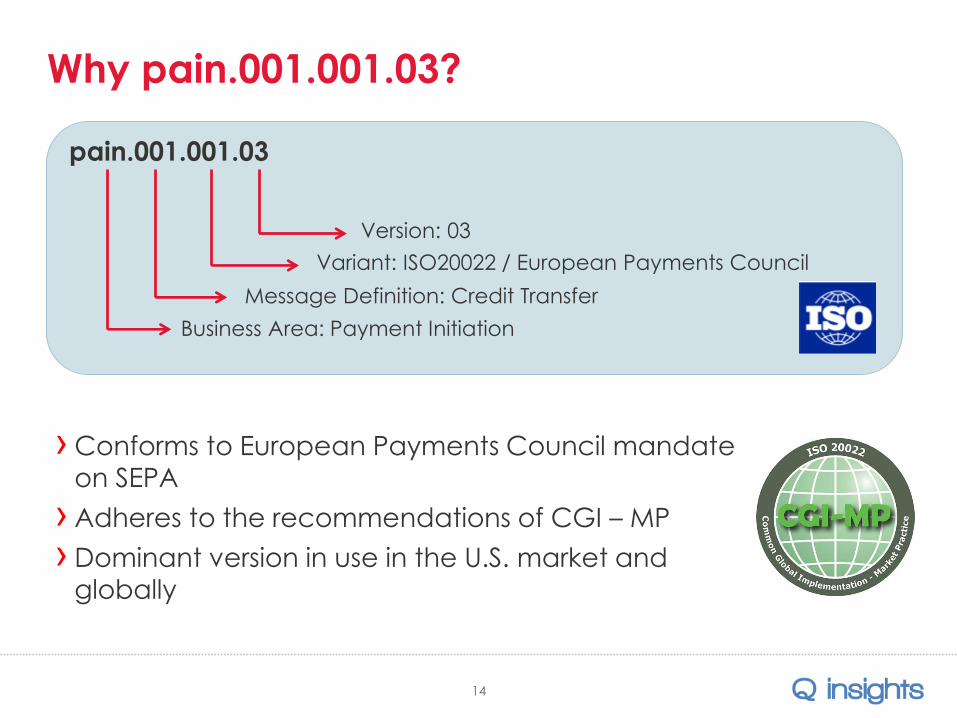

Why pain.001.001.03?

pain.001.001.03

Business Area: Payment Initiation

Message Definition: Credit Transfer

Variant: ISO20022 / European Payments Council

Version: 03

›Conforms to European Payments Council mandate

on SEPA

›Adheres to the recommendations of CGI – MP

›Dominant version in use in the U.S. market and

globally

14

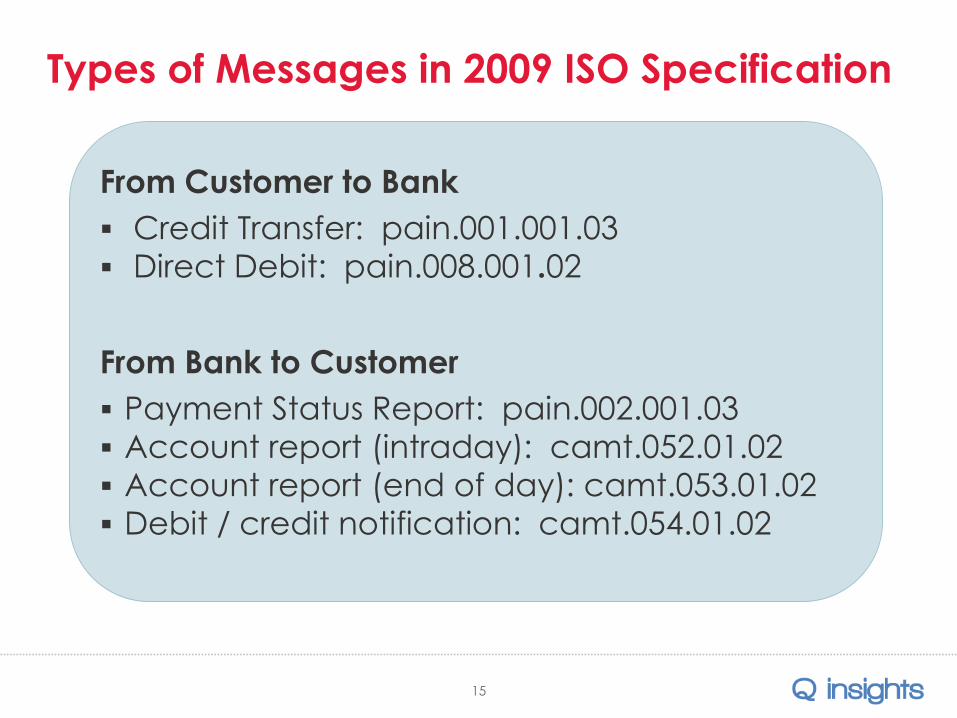

Types of Messages in 2009 ISO Specification

15

From Customer to Bank

Credit Transfer: pain.001.001.03

Direct Debit: pain.008.001.02

From Bank to Customer

Payment Status Report: pain.002.001.03

Account report (intraday): camt.052.01.02

Account report (end of day): camt.053.01.02

Debit / credit notification: camt.054.01.02

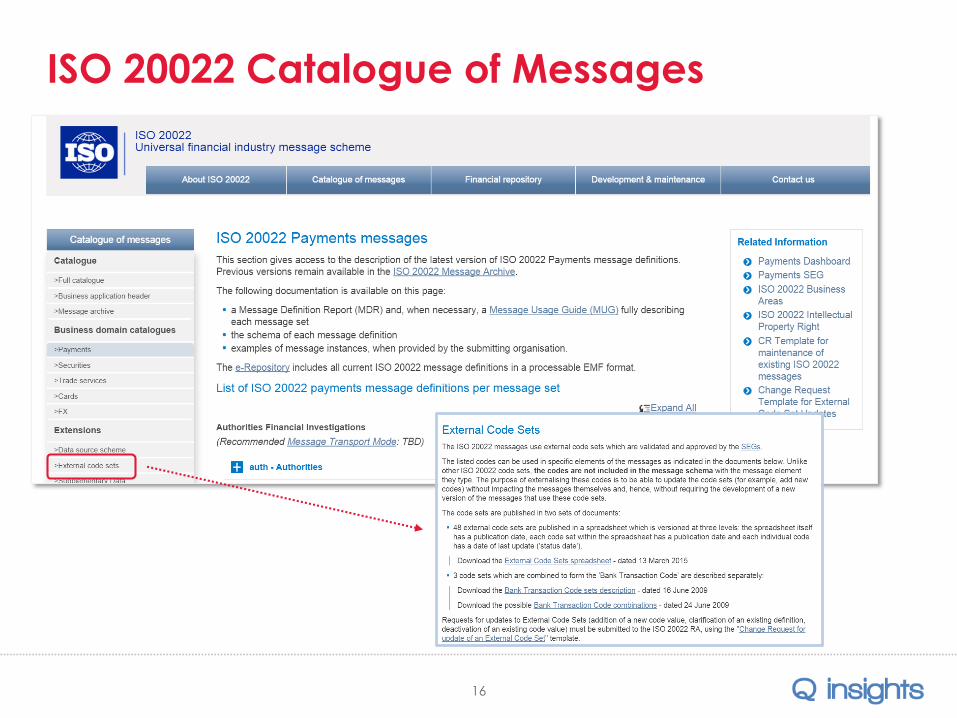

ISO 20022 Catalogue of Messages

16

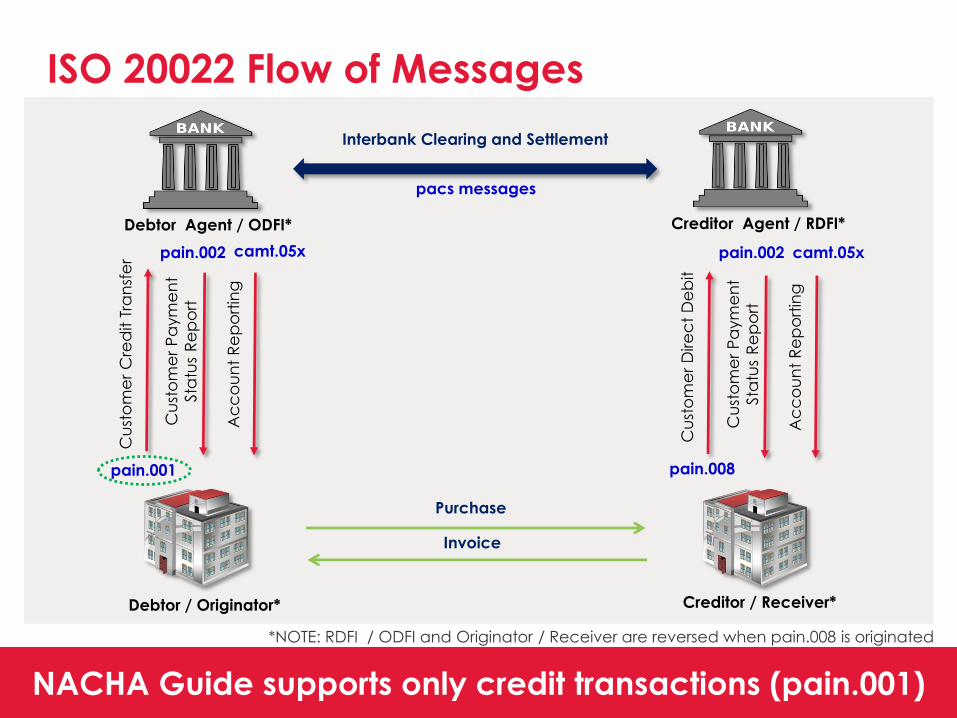

ISO 20022 Flow of Messages

17NACHA Guide supports only credit transactions (pain.001)

Debtor / Originator* Creditor / Receiver*

Debtor Agent / ODFI* Creditor Agent / RDFI*

Interbank Clearing and Settlement C

ust

om

er

Cre

dit T

ran

sfe

r

Cu

sto

me

r P

aym

en

t

Sta

tus

Re

po

rt

Ac

co

un

t R

ep

ort

ing

pain.001

pain.002 camt.05x

Cu

sto

me

r D

ire

ct

De

bit

Cu

sto

me

r P

aym

en

t

Sta

tus

Re

po

rt

Ac

co

un

t R

ep

ort

ing

pain.008

pain.002 camt.05x

pacs messages

Purchase

Invoice

*NOTE: RDFI / ODFI and Originator / Receiver are reversed when pain.008 is originated

ISO 20022 Flow of Messages

1818U.S. ACH Operators only transmit NACHA file formats today

Debtor / Originator Creditor / Receiver

Debtor Agent / ODFI Creditor Agent / RDFI

Interbank Clearing and Settlement

Cu

sto

me

r C

red

it T

ran

sfe

r

pain.001

Purchase

Invoice

CCD

CTX

IAT

NACHA File Formats

Translate

from ISO

20022 to

NACHA file

formats

Flow of information Flow of funds

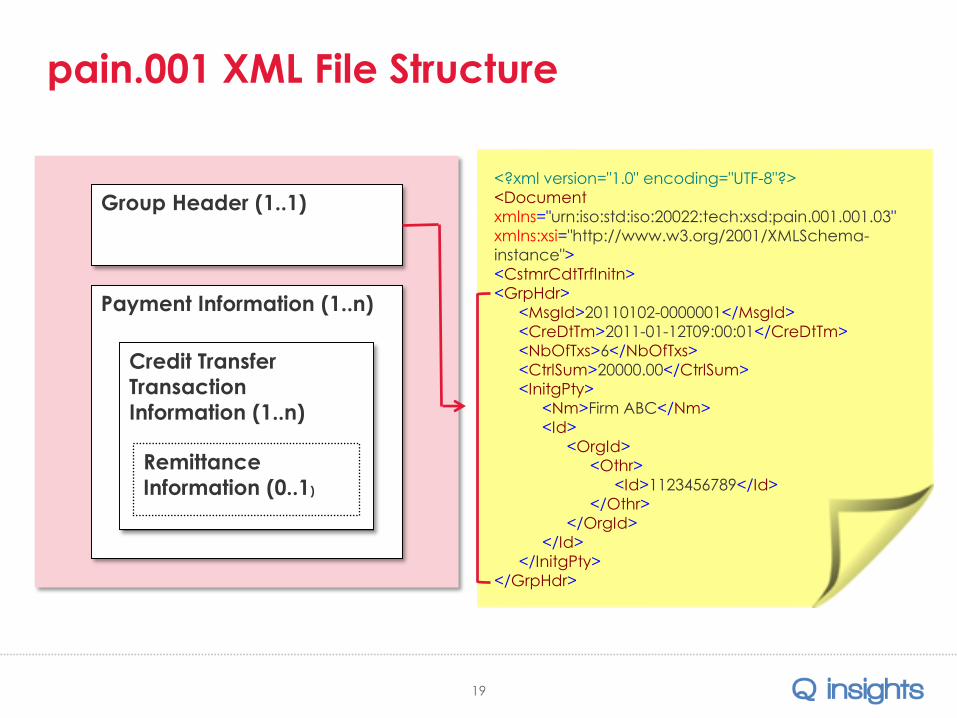

Group Header (1..1)

Payment Information (1..n)

Credit Transfer

Transaction

Information (1..n)

Remittance

Information (0..1)

pain.001 XML File Structure

19

<?xml version="1.0" encoding="UTF-8"?>

<Document

xmlns="urn:iso:std:iso:20022:tech:xsd:pain.001.001.03"

xmlns:xsi="http://www.w3.org/2001/XMLSchema-

instance">

<CstmrCdtTrfInitn>

<GrpHdr>

<MsgId>20110102-0000001</MsgId>

<CreDtTm>2011-01-12T09:00:01</CreDtTm>

<NbOfTxs>6</NbOfTxs>

<CtrlSum>20000.00</CtrlSum>

<InitgPty>

<Nm>Firm ABC</Nm>

<Id>

<OrgId>

<Othr>

<Id>1123456789</Id>

</Othr>

</OrgId>

</Id>

</InitgPty>

</GrpHdr>

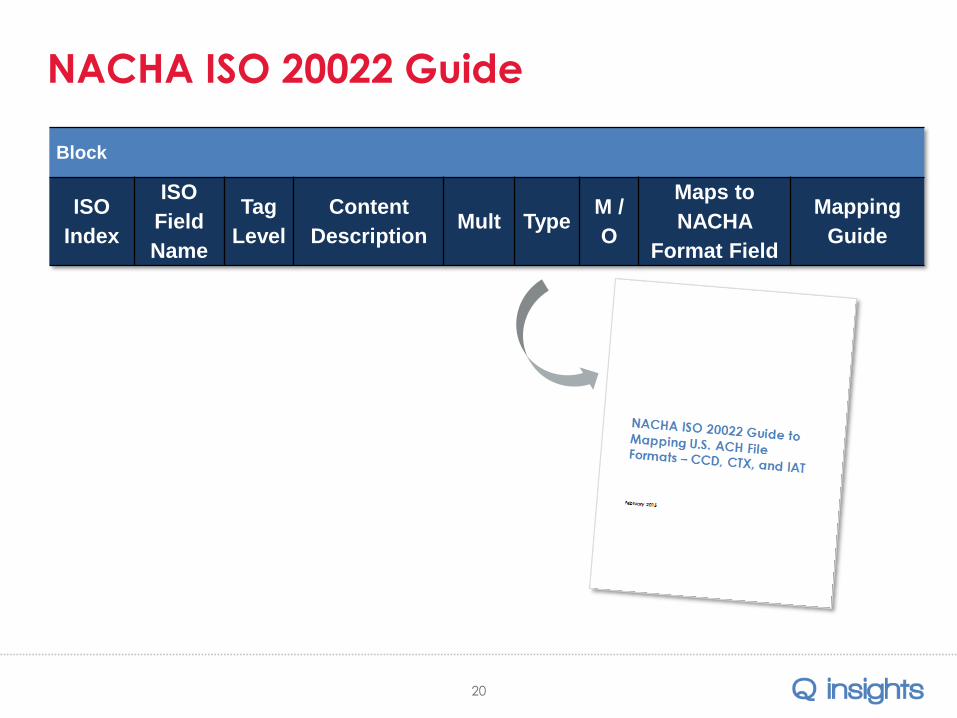

NACHA ISO 20022 Guide

20

Block

ISO

Index

ISO

Field

Name

Tag

Level

Content

DescriptionMult Type

M /

O

Maps to

NACHA

Format Field

Mapping

Guide

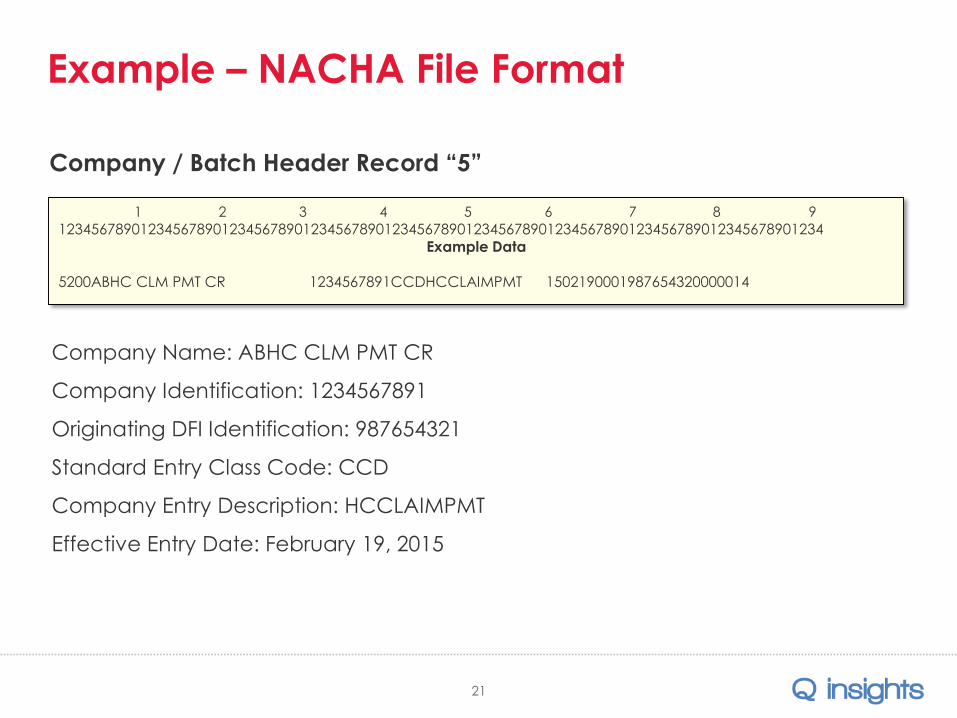

Example – NACHA File Format

21

Company Name: ABHC CLM PMT CR

Company Identification: 1234567891

Originating DFI Identification: 987654321

Standard Entry Class Code: CCD

Company Entry Description: HCCLAIMPMT

Effective Entry Date: February 19, 2015

1 2 3 4 5 6 7 8 9

1234567890123456789012345678901234567890123456789012345678901234567890123456789012345678901234Example Data

5200ABHC CLM PMT CR 1234567891CCDHCCLAIMPMT 1502190001987654320000014

Company / Batch Header Record “5”

Example – ISO 20022 XML Format

22

<PmtInf>

<PmtInfId>011011</PmtInfId>

<PmtMtd>TRF</PmtMtd>

<PmtTpInf>

<SvcLvl>

<Cd>NURG</Cd>

</SvcLvl>

<LclInstrm>

<Cd>CCD</Cd>

</LclInstrm>

<CtgyPurp>

<Prtry>HCCLAIMPMT</Prtry>

</CtgyPurp>

</PmtTpInf>

<ReqdExctnDt>2015-02-19</ReqdExctnDt>

Non-Urgent / ACH payment

NACHA SEC Code

Company entry description

Effective entry date

Example – ISO 20022 XML Format

23

<Dbtr>

<Nm>ABHC CLM PMT CR</Nm>

<Id>

<OrgId>

<Othr>

<Id>1234567891</Id>

</Othr>

</OrgId>

</Id>

</Dbtr>

<DbtrAgt>

<FinInstnId>

<ClrSysMmbId>

<ClrSysId>

<Cd>USABA</Cd>

</ClrSysId>

<MmbId>987654321</MmbId>

</ClrSysMmbId>

<Nm>USA BANK</Nm>

</FinInstnId>

</DbtrAgt>

</PmtInf>

Company Name

Company Identification

Originating DFI Identification

7/18/201524

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

24

Today’s Discussion

21

NACHA Payments Conference

Tom Durkin

Managing Director, Digital Channels

Bank of America Merrill Lynch

April 20, 2015

26

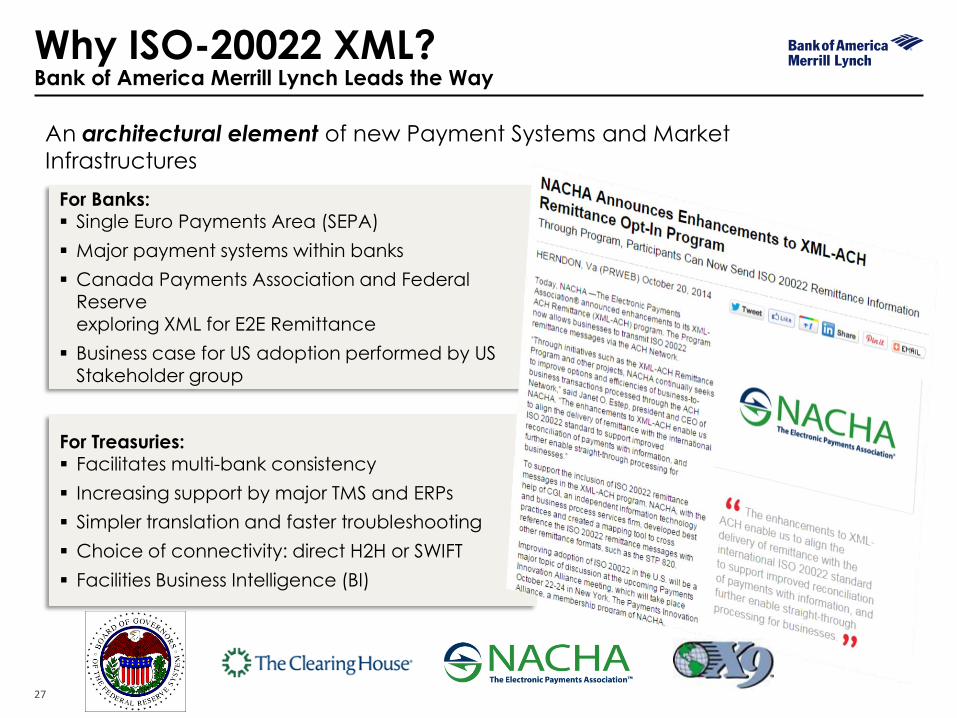

ISO-20022 XMLAdoption Landscape

A global, unified standard for messaging has the potential to enable efficient end-to-end processing across domains and geographies, promote STP and operational efficiencies in cash management, and overcome difficulties in multiple domestic and international standards.

The commitment to ISO 20022 implementation initiatives with major global clearing systems in Europe and other countries such as Singapore, India and Australia continues to drive the international momentum for adoption.

United States•Adoption driven by clients with global reach

Europe•SEPA Regulation migration deadline was in 2014 •Target 2 and Euro 1 testing is scheduled to begin with industry migrations target of November 2017

India•NG-RTGS is operational as the first ISO 20022 compliant RTGS system in the world

Singapore•ISO 20022 will serve as the messaging standard for G3, the low-value real-time payments solution

Australia•Intention to adopt ISO 20022 for the NPP (ACH) initiativeSource: KPMG LLP

27

An architectural element of new Payment Systems and Market Infrastructures

For Treasuries: Facilitates multi-bank consistency

Increasing support by major TMS and ERPs

Simpler translation and faster troubleshooting

Choice of connectivity: direct H2H or SWIFT

Facilities Business Intelligence (BI)

For Banks: Single Euro Payments Area (SEPA)

Major payment systems within banks

Canada Payments Association and Federal Reserveexploring XML for E2E Remittance

Business case for US adoption performed by US Stakeholder group

Why ISO-20022 XML?Bank of America Merrill Lynch Leads the Way

Questions?

Robert Unger | Senior Director, Product Management &

Strategic Corporate Alliances

(o) 703.561.3913

Nasreen Quibria| Managing Director & Founder

(m) 617.388.6207

Tom Durkin| Managing Director, Digital Channels

(o) 312.904.7370

© 2015 NACHA — The Electronic Payments Association. All rights reserved.

No part of this material may be used without the prior written permission of NACHA.

Content from sources other than NACHA is used with permission and requires the separate consent of

those sources for use by others. This material is not intended to provide any warranties or legal advice,

and is intended for educational purposes only.

31

22

29

Notice to Recipient

“Bank of America Merrill Lynch” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., member FDIC. Securities, strategic advisory, and other investment banking activities are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp., both of which are registered as broker-dealers and members of SIPC, and, in other jurisdictions, by locally registered entities. Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp. are registered as futures commission merchants with the CFTC and are members of NFA.

Investment products offered by Investment Banking Affiliates: Are Not FDIC Insured * May Lose Value * Are Not Bank Guaranteed.

These materials have been prepared by one or more subsidiaries of Bank of America Corporation for the client or potential client to whom such materials are directly addressed and delivered (the “Company”) in connection with an actual or potential mandate or engagement and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with us. These materials are based on information provided by or on behalf of the Company and/or other potential transaction participants, from public sources or otherwise reviewed by us. We assume no responsibility for independent investigation or verification of such information (including, without limitation, data from third party suppliers) and have relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the managements of the Company and/or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to estimates and forecasts obtained from public sources,represent reasonable estimates). No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Company and are being furnished and should be considered only in connection with other information, oral or written, being provided by us in connection herewith. These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Bank of America Corporation or any of its affiliates to provide or arrange any financing for any transaction or to purchase any security in connection therewith. These materials are for discussion purposes only and are subject to our review and assessment from a legal, compliance, accounting policy and risk perspective, as appropriate, following our discussion with the Company. We assume no obligation to update or otherwise revise these materials. These materials have not been prepared with a view toward public disclosure under applicable securities laws or otherwise, are intended for the benefit and use of the Company, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without our prior written consent. These materials may not reflect information known to other professionals in other business areas of Bank of America Corporation and its affiliates.

Bank of America Corporation and its affiliates (collectively, the “BAC Group”) comprise a full service securities firm and commercial bank engaged in securities, commodities and derivatives trading, foreign exchange and other brokerage activities, and principal investing as well as providing investment, corporate and private banking, asset and investment management, financing and strategic advisory services and other commercial services and products to a wide range of corporations, governments and individuals, domestically and offshore, from which conflicting interests or duties, or a perception thereof, may arise. In the ordinary course of these activities, parts of the BAC Group at any time may invest on a principal basis or manage funds that invest, make or hold long or short positions, finance positions or trade or otherwise effect transactions, for their own accounts or the accounts of customers, in debt, equity or other securities or financial instruments (including derivatives, bank loans or other obligations) of the Company, potential counterparties or any other company that may be involved in a transaction. Products and services that may be referenced in the accompanying materials may be provided through one or more affiliates of Bank of America Corporation. We have adopted policies and guidelines designed to preserve the independence of our research analysts. These policies prohibit employees from offering research coverage, a favorable research rating or a specific price target or offering to change a research rating or price target as consideration for or an inducement to obtain business or other compensation. We are required to obtain, verify and record certain information that identifies the Company, which information includes the name and address of the Company and other information that will allow us to identify the Company in accordance, as applicable, with the USA Patriot Act (Title III of Pub. L. 107-56 (signed into law October 26, 2001)) and such other laws, rules and regulations as applicable within and outside the United States.

We do not provide legal, compliance, tax or accounting advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by us to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. If any person uses or refers to any such tax statement in promoting, marketing or recommending a partnership or other entity, investment plan or arrangement to any taxpayer, then the statement expressed herein is being delivered to support the promotion or marketing of the transaction or matter addressed and the recipient should seek advice based on its particular circumstances from an independent tax advisor. Notwithstanding anything that may appear herein or in other materials to the contrary, the Company shall be permitted to disclose the tax treatment and tax structure of a transaction (including any materials, opinions or analyses relating to such tax treatment or tax structure, but without disclosure of identifying information or, except to the extent relating to such tax structure or tax treatment, any nonpublic commercial or financial information) on and after the earliest to occur of the date of (i) public announcement of discussions relating to such transaction, (ii) public announcement of such transaction or (iii) execution of a definitive agreement (with or without conditions) to enter into such transaction; provided, however, that if such transaction is not consummated for any reason, the provisions of this sentence shall cease to apply. ©2015 Bank of America Corporation.