2015 licensing and joint ventures

DESCRIPTION

Price listTRANSCRIPT

Life Sciences Dealmaking 2015 Laura Vitez and Vinay Singh 11 January 2016

Thomson Reuters life sciences content DISCOVERY

TRANSLATIONAL

BUSINESS DEVELOPMENT

PRE-CLINICAL

REGULATORY

COMMERCIALIZATION

Chemistry – 2.5 million+ compounds structure searchable

Genetic Sequences – Over 65 million nucleic and amino-acid sequences from patent claims, 1981-present

Biological Pathways – 1.4M+ interactions, 684 disease-specific pathway maps

Biological Effects – 1.5M Preclinical Pharmacology Records, 180K+ experimental models with 15K+ drugs tested

Biomarkers – 26,000+ Biomarkers with over 1.1M uses

Gene Variants – 372,000 variant-disease associations, 10,000 drug response records

Intellectual Property – More than 6M patents from 92 countries grouped in 2.3M+ families

Pipeline Drugs Intelligence – 53,000+ drugs in R&D status, indications, and licensing

Clinical Intelligence – 200,000+ Clinical Trial records. Key time, cost and quality performance metrics are derived from data collected directly from biopharmaceutical companies including metrics such as success rates, cycle times, enrollment rates and protocol deviations

Deals – 45,000+ Alliance summaries, 2,800+ Contract analyses, 1,700+ Deal snapshots

Corporate Intelligence – Coverage of 100,000 companies involved in Drug Development

Event Transcripts – 37,000+ transcripts of investor calls and meetings where pharmas/biotechs reveal information and plans, often before they are disclosed elsewhere, and field questions from analysts and reporters

Regulatory Intelligence – Enhanced regulatory data covering 70 countries & regions

Generic Drug Intelligence – 12,000 launched drugs, 360,000 trade names, 73 world markets, 56,000 manufacturing sites, 400 US patent challenges

News: 20+ years of biopharmaceutical news archives and market intelligence

Scientific Journals: 17,000+ peer-reviewed journals

Conferences: 300 events attended annually

Disease briefings: Comprehensive overviews of 27 therapeutic areas

Epidemiology: Incidence and prevalence for over 4,500 diseases and procedures

CLINICAL

2

Make a better deal, faster with Thomson Reuters Our asset valuation services:

• Leverage insight into leading practices to enable structuring the highest value deal possible

• Benchmark deal size, upfronts, milestones, royalty and equity payments

• Identify potential deal partners by therapeutic area, indication, mechanism, drug class, technology, and stage of development

• Understand individual potential partners

We can help you develop and implement strategic partnering plans, supplement resources for specific engagements, and align perspectives from a neutral position.

Vinay Singh: Prior to joining the Thomson Reuters team, Mr. Singh worked as an investment banker at Burrill & Company helping to close over $250M in public equity financings and M&As for life sciences companies

Laura Vitez: Ms. Vitez has over 25 years of experience in the life sciences industry. She has held lead or advisory roles at multiple small biotechs, a mid-sized pharma company, and two consulting firms, bringing in over $2 billion in deal dollars.

THOMSON REUTERS This report contains general information only and is based on the experiences and research of Thomson Reuters practitioners. Thomson Reuters is not, by means of this report, rendering business, financial, investment, or other professional advice or services. This report is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Thomson Reuters, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this report.

Contents • Mergers and acquisitions (M&A)

– Volumes – Valuations – Hostile attempts – Friendly options

• Licenses and joint ventures (JV) – Initial Public Offerings (IPOs) – Licensing trends – License/IPO case study

• Contact information

5

Mergers and Acquisitions

10 Years of M&A: Volume

468

0

50

100

150

200

250

300

350

400

450

500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Anno

unce

d M

&A

tran

sact

ions

Volume of announced life sciences industry-wide M&A events by year

Average 320 events / year

NOTE: $$ throughout presentation are USD. All dollars are nominal values (not adjusted for inflation). 7

3%

3% 3%

3% Diversified Cancer Infectious Disease Neurology Endocrine/Metabolic Autoimmune/Inflammatory Cardiovascular Dermatologic Ophthalmology Genitourinary/Sexual Function Hematologic Gastrointestinal Pulmonary/Respiratory Other/Miscellaneous

M&A 2015: Volume by therapeutic arena

NOTE: Excludes deals for non-therapeutic assets, and therapeutic asset deals for unknown therapeutic arenas.

2% each

Diversified 38%

Infect 9%

Cancer 15%

AI/Inflam 6%

Neuro 7%

Endo/Met 7%

1% each

8

M&A 2015: Therapeutic arenas cf. 2014

Other

Gastrointestinal

Pulmonary/Respiratory

Genitourinary

Hematologic

Cardiovascular

Dermatology

Ophthalmology

Autoimmune/Inflam

Endo/Metabolic

Neurology

Infectious disease

Cancer

0 5 10 15 20 Number of announced M&A events for companies with therapeutic assets

2015

2014

9

NOTE: Excludes deals for non-therapeutic assets, and therapeutic asset deals for unknown or diverse therapeutic arenas.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

5 year average 2009-13 (n = 425)

2014 (n = 71)

2015 (n = 89)

Percent distribution of lead product stages for therapeutic product company M&As

Discovery / Preclinical Phase I Phase II Phase III Registratoin Approved

Early Stage Late Stage Products Clinical Stage Products

Phase II n = 18

Disc/Preclinical n = 20

Approved n = 28

Phase II n = 16

Disc/Preclinical n = 16

Approved n = 21

54% Approved

23% Phase II

9% Disc/PC

2015 (n=89)

2014 (n=71)

M&A 2015: Breakdown by stage cf. history

5 year average 2009 -13 (n=425)

NOTE: Stage of deal is the most advanced development stage entered by the lead asset on the sellside of the transaction. For example, a deal for a company whose lead compound has completed Phase I but not yet begun Phase II is classified as a Phase I event. 10

10 Years of M&A: Aggregate announced dollars

$515

$0

$100

$200

$300

$400

$500

$600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Anno

unce

d M

&A

dolla

rs (U

S bi

llion

)

Volume of announced life sciences industry-wide M&A events by year

Average $182B / year

NOTE: All dollars are USD and are nominal values (i.e. are not adjusted for inflation). 11

10 years of M&A: Aggregate dollars by tier

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Aggr

egat

e an

noun

ced

M&

A do

llars

($bi

llion

)

Annual aggregate M&A dollars by tier

> $100B $10-$100B $5-10B $1-5B < $1B

Total deal size:

$114

$175 $166

$105

$140 $135

$71

$113

$288

$515

12 NOTE: All dollars are USD and are nominal values (i.e. are not adjusted for inflation).

Bayer/Schering AG J&J/PFE consumer

MerMedImmuneerono

S Plough/Organon

AZ/MedImmune

Novartis/Alcon

Roche/Genentech

PFE/Wyeth

Merck/S Plough

Sanofi/Genzyme

J&J/Synthes

Takeda/Nycomed

Gilead/Pharmasset

Actavis/Forest

Novartis/GSK Onc

Bayer/Merck Merck KGaA/S Aldrich

Actavis/Allergan

Valeant/Salix

PFE/Hospira

Abbvie/Pharmacyclics

Teva/Allergan generics

Shire/Baxalta

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 20

Tota

l dea

l siz

e ($

B)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

10 years of M&A: $10+ billion pharma deals Pfizer/Allergan,

$160 billion

13

Year

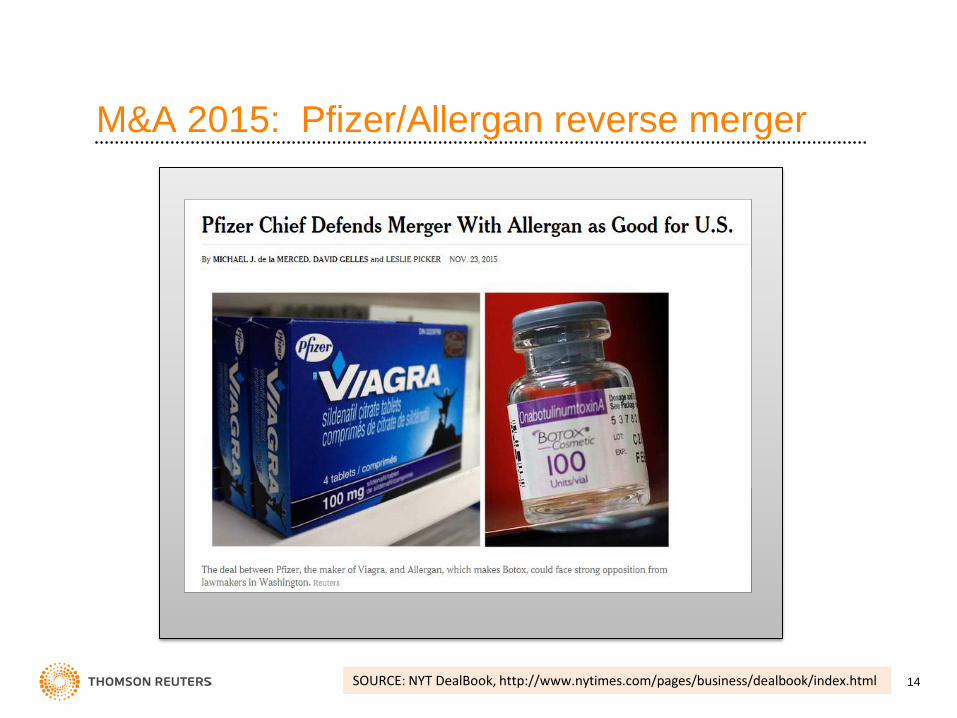

M&A 2015: Pfizer/Allergan reverse merger

SOURCE: NYT DealBook, http://www.nytimes.com/pages/business/dealbook/index.html 14

The Pfizer family tree

Warner-Lambert

2000 ($90B)

Merger 1950s

Parke-Davis 1970s

AHP merger 1999

Agouron 1999 ($2.1B)

Pharmacia 2002 ($60B)

Kabi merger early 90s

Procardia 1990 ($2.4B)

Upjohn 1995 ($7B)

Monsanto/ Searle, 1999

($27.3B)

Esperion 2003 ($1.3B)

Vicuron 2005 ($1.9B)

Wyeth 2009 ($68B)

AH Robins 1989 ($3.2B)

American Cyanamid

1994 ($9.6B)

Genetics Institute 1996 ($1.3B)

King 2010 ($3.6B)

Jones Phar 2000 ($2.4B)

Alpharma 2008 ($1.6B)

Hospira 2015 ($17B)

Pfizer

Pfizer acquisitions with < $1B or undisclosed total deal size: Active · Adria · Alacer · Alanex · Angiomedics · Angiosyn · Apollon · Bioren · BioRexis · Coley · Corvita · CovX · Embrex · Encysive · Erbamont · Excaliard · Ferrosa · FoldRx · Gene/Networks · Genetics Institute · Geoffrey Manner · Haptogen · Icagen · Idun · ImmunoPharmaceutics · InnoPharma · Lab Teuto · Leibinger · Medco · Meridian · Meridica · NextWave · PowderMed · Praxis · Redvax · Rinat · Sensus · Serene · Sugen · Synbiotics · Talaria · Thiakis · Vesta · Vetnex 15

Pfizer value history

Est.

$0

$50

$100

$150

$200

$250

$300

$350

$ U

S bi

llion

(not

adj

uste

d fo

r inf

latio

n)

Accumulated total spent on acquisitions* ($B)

Market capitalization at year end ($B)

Annual net sales ($B)

NOTES: All dollars are nominal values (i.e. are not adjusted for inflation) *Acquisition totals exclude milestone payments and stock-for-stock mergers **2015 data exclude pending acquisition of Allergan

16

M&A 2015: Top three tiers in 2015, $5B and up

$5,168

$5,200

$6,500

$6,800

$7,000

$7,200

$8,050

$8,400

$11,100

$17,000

$21,000

$32,000

$37,000

$40,500

$54,000

$160,000

$0 $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 $140,000 $160,000 $180,000

BI/Merial

Shire/NPS

Shire/Dyax

Centene/HealthNet

AstraZeneca/Acerta

Celgene/Receptos

Endo/Par

Alexion/Synageva

Valeant/Salix

Pfizer/Hospira

AbbVie/Pharmacyclics

Shire/Baxalta

Aetna/Humana

Teva/Allergan generics

Anthem/CIGNA

Pfizer/Allergan

Health benefits

Rx: rare diseases / BLA filed

Rx: GI disorders / approved

Rx: injectables, biosimilars / approved

Rx: generics / approved

Total deal value ($M)

Health benefits

Rx: generics / approved

Rx: cancer / approved

Rx: rare diseases (hematology) / approved

Rx: diversified/ approved

Rx: cancer / Phase III

Rx: rare diseases (HAE) / approved

Rx: ulcerative colitis and multiple sclerosis / Phase III

Swap of Sanofi’s animal health biz Merial for BI’s consumer health biz + $5.2B cash

Health benefits

Rx: rare diseases (HPT) / approved

NOTE: Gray denotes pending transactions. Orange deals have closed.

......

$10B

and

up

$5 to

$10

B

16 deals over multiple market segments: • 4 rare disease (3 by Shire) • 3 generics/specialty pharma • 3 health benefits (insurance) • 2 Pfizer • 2 cancer • 1 ulcerative colitis/multiple sclerosis • 1 consumer/animal health swap

The 13 therapeutics are all late: • 10 approved • 1 BLA filed • 2 Phase III

17

M&A 2015: Not all deals are friendly and successful ...

18

M&A 2015: Unsolicited bids and alternative outcomes

Bidder Target Date Bid ($B) Instead ...

Horizon Depomed July 2015 $3.0 Horizon bought Hyperion ($1.1B) and Crealta ($510M)

Depomed bought 3 pain drugs from Janssen ($1.05B)

Teva Mylan April 2015 $40.1 Teva bought Allergan’s generics business

($40.5B); also Auspex, ($3.5B), Rimsa ($2.3B), Immuneering, and Gecko

Mylan bid on Perrigo ...

Mylan Perrigo April 2015 $28.9 Mylan bought Famy Care's female health biz ($800M)

Perrigo bought Patheon, Naturwohl, OTCs from GSK,

and a Crohn’s Rx from AZ

Endo Salix March 2015 $11.2 Endo bought Par ($8.05B) Valeant bought Salix ($11.1B)

AbbVie Shire June 2014 $46.0 AbbVie bought Pharmacyclics ($21B) Shire bought Dyax ($6.5B), NPS ($5.2B),

Foresight ($300M), with a pending acquisition of Baxalta ($32B)

Valeant Allergan April 2014 $45.5

Valeant bought Salix ($11.1B), Sprout ($1B), Amoun ($800M), Dendreon

($495M), Synergetics ($192),Unilens, Marathon, Commonwealth BioTech

(US/Can), Mycorrhizal

Actavis bought Allergan in 2014 ($66B) and this year bought Kythera ($2.1B), Naurex ($560M), Oculeve ($125M), Auden Mckenzie ($458M), AqueSys

($300M), with a pending reverse merger with Pfizer ($160B)

Pfizer AstraZeneca May 2014 $119.0 Pfizer has a reverse merger pending with Allergan ($160B), plus bought

Hospira ($17B) and Redvax

AZ bought ZS Pharma ($2.7B), Acerta ($700M), and the branded

respiratory biz from Allergan ($700M)

19

M&A 2015: Successfully triggered options Meritage Quanticel Annovation

Acquired by: Shire (post-ViroPharma acquisition) Celgene The Medicines Company

Time from option to exercise: 3 yrs 3 mo 3 yrs 5 mo 2 yrs 5 mo

Option upfront: $7.5M CON participation in Series A with

Versant + $45M over 3.5 years Medicines Co participated in $8.75M Series A with Atlas

Option term collaboration:

ViroPharma provided $12.5M in milestones for Phase II work

Celgene got “early access” to technology, team, molecules

Medicines Co had "significant influence, but not control"

Technology: Novel form of budesonide for

eosinophilic esophagitis, from UCSD

Single-cell genomic analysis and drug discovery platform,

from Stanford

Next-generation anesthetic, from Mass Gen

Stage when optioned: Phase II Discovery Preclinical

Acquisition trigger:

Receipt of data from a final Phase II study and agreement with FDA on

acceptable Phase III endpoint (Update: Phase III began Mar 2015)

3.5 years (extendable) (Update: multiple INDs

expected in 2016)

Completion of Phase II POC (Update: Phase III began

In Nov 2015)

Acquisition upfront: $70M $100M $28.4M

Acquisition contingencies: $175M $385M $26.3M milestones +

low single digit royalties

20

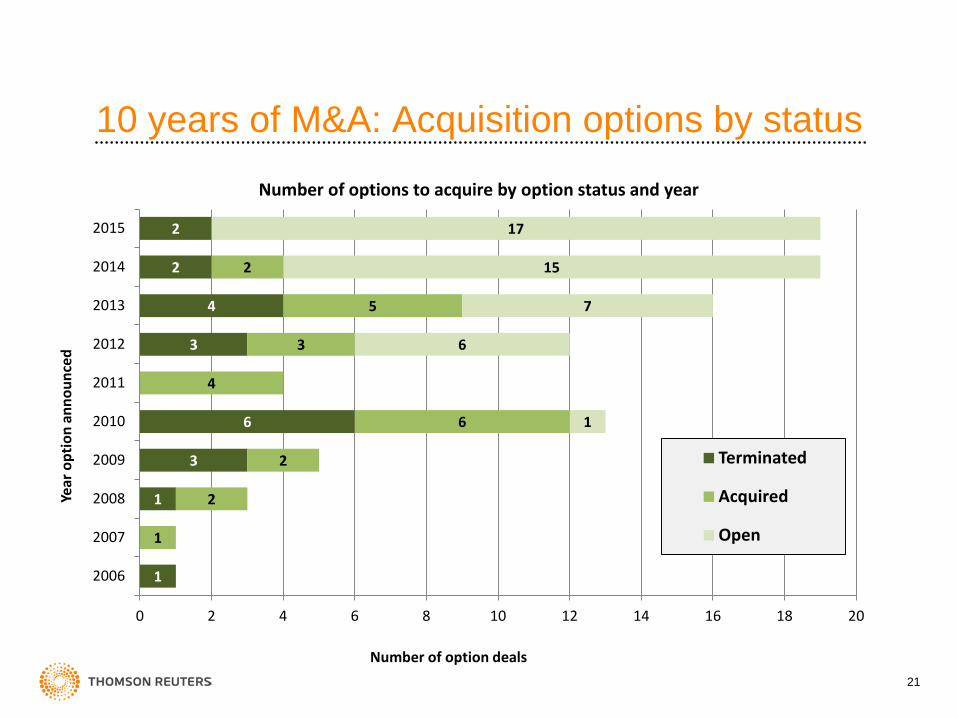

1

1

3

6

3

4

2

2

1

2

2

6

4

3

5

2

1

6

7

15

17

0 2 4 6 8 10 12 14 16 18 20

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Number of option deals

Year

opt

ion

anno

unce

d

Number of options to acquire by option status and year

Terminated

Acquired

Open

10 years of M&A: Acquisition options by status

21

Licensing and Joint Ventures

Biotech markets take a turn

23

4

2 2 4

6

15 14

6

28

15

21

12 10

21

14

10 $0.3

$0.2 $0.1 $0.2

$2.5

$1.1 $1.1

$0.7

$1.8

$1.0

$2.0

$1.3

$0.8

$2.0

$1.4

$0.6

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

0

5

10

15

20

25

30

Tota

l Am

ount

Rai

sed

(USD

B)

Tota

l The

rape

utic

IPO

s on

US

Exch

ange

s

Volume Amount Raised (USD B)

Initial Public Offering (IPO) market shows signs of teetering

NOTE: $2B of the $2.5B funding in Q1 2013 was from one IPO – Zoetis

2012

Number of Therapeutic IPOs and Aggregate Total Raised By Quarter

2013 2014 2015

57.4%

73.7%

56.7%

80.0%

23%

12%

7%

19%

77%

26% 26%

43%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2012 2013 2014 2015

Insi

der P

artic

ipat

ion

Median % of IPO's w/ 25% or more Insider Participation

Insider Participation in IPOs

24

But IPO market is not closed

(100%)

(50%)

0%

50%

100%

150%

Dec 2014 Feb 2015 Apr 2015 May 2015 Jul 2015 Sep 2015 Oct 2015 Dec 2015

Post

IPO

Per

form

ance

(Iss

ue P

rice

vs. P

rice

12/3

1/15

)

Post IPO performance wasn’t great in 2015

Overall 61% of 2015’s

Biotech IPOs finished at or below their issue price

And nearly 20% of 2015’s

IPO class lost 50% or more of its value

BUT…Despite the

downturn in the markets in mid-September, 12

Biotech IPOs still got out with favorable valuations and more than half have

performed very well, including Aclaris

Therapeutics which finished the year up 134%

25

Date of IPO

Licenses and joint ventures (JVs) by quarter

137 128

119

181

198 182

159 151

191

171 170

207

217

246

218

274

$5.7

$3.2

$6.2

$8.1

$4.7 $5.2 $3.8

$8.2

$6.4

$10.7

$8.0

$11.0

$14.8

$12.9 $13.1

$24.4

$0

$5

$10

$15

$20

$25

$30

0

50

100

150

200

250

300

1Q 2012

2Q 2012

3Q 2012

4Q 2012

1Q 2013

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

1Q 2015

2Q 2015

3Q 2015

4Q 2015

Aggr

egat

e Di

sclo

sed

Deal

Val

ue ($

B)

# Li

cens

es a

nd JV

s

# Licenses/JVs Aggregate Disclosed Value ($B)

2013 2014 2015

Number of Disclosed Licenses/JVs and Aggregate Total Disclosed Deal Value By Quarter

NOTES: This analysis includes all announced licenses and JVs for products or technologies. Licenses for intellectual property and/or data only are excluded. All dollars are USD.

2012

26

Top ten 2015 licensing transactions by announced total size Licensee Licensor Total Size

(US $ M) Upfront (US $M) Subject Stage* Primary

Rx Area

1 Sanofi Hanmi $4,266 $445 Sanofi to develop Hanmi's Portfolio (specifically 3 assets) of long-acting diabetes treatment Reformulation Endo/Meta

2 AstraZeneca Ionis (fka Isis) $4,090 $65 Discovery and development of antisense therapies for

cardiovascular, metabolic and renal diseases Discovery Diversified

3 Vertex CRISPR $2,625 $75 Vertex and CRISPR to use CRISPR-Cas9 gene editing

technology to discover and develop new treatment for genetic diseases

Discovery Diversified

4 Gilead Galapagos $2,075 $300 Gilead Sciences to develop and commercialize Galapagos' filgotinib against rheumatoid arthritis Phase II AI/Inflam

5 Pfizer Heptares $1,890 undisclosed Heptares and Pfizer to develop novel drugs targeting GPCR against multiple therapeutic indications Discovery Diversified

6 BMS Five Prime $1,740 $350 BMS to develop and commercialize Five Prime's CSF1R

antibody program, including FPA-008 for immunology and oncology

Phase I Diversified

7 Sanofi Lexicon $1,730 $300 Sanofi to develop and commercialize Lexicon's sotagliflozin against diabetes, with an option to license Phase III Endo/Meta

8 Amgen Xencor $1,702 $45 Amgen to develop and commercialize Xencor's bispecific cancer immunotherapy and inflammation programs Preclinical Diversified

9 Sanofi Regeneron $1,665 $640 PD-1 inhibitor and other new immuno-oncology antibodies, with an option Phase I Cancer

10 Ultragenyx Arcturus $1,570 $10 Arcturus and Ultragenyx to discover and develop mRNA therapeutics using UNA Oligomer chemistry and LUNAR

nanoparticle delivery platform Discovery Diversified

*Stage: Recap classifies clinical development program deals by the highest stage entered by the lead asset at the time of deal signature. E.g., an asset that has completed Phase II but not yet begun Phase III is classified as a Phase II transaction.

27

Top 20 2015 licenses with upfronts > $50M Licensee Licensor Upfront

($M) Equity ($M) Stage Rx Area

Sanofi Regeneron $640 Phase I Cancer

Celgene MedImmune / AZ $450 Phase III Cancer

Sanofi Hanmi $445 Reformulation Endo/Meta

Bristol-Myers Squibb Five Prime $350 Phase I Diversified

Astellas Immunomic $300 Discovery AI/Inflam

Gilead Galapagos $300 $425 Phase II AI/Inflam

Sanofi Lexicon $300 Phase III Endo/Meta

MedImmune / AZ Innate $250 Phase II Cancer

Allergan Merck $250 Phase II Neurology

Novartis Aduro $200 $25 Preclinical Cancer

Celgene Juno $150 $850 Phase II Diversified

Celgene Nurix $150 Discovery Diversified

Merck KGaA Intrexon $115 Discovery Cancer

Celgene Lycera $105 Phase I Cancer

Janssen Hanmi $105 Phase I Endo/Meta

Bayer Ionis (fka ISIS) $100 Phase II Cardiovascular

DiaVax City of Hope $100 Phase I Viral Infect

Bayer Ionis (fka ISIS) $100 Phase II Hematologic

Merck NGM $94 $106 Preclinical Endo/Meta

Vertex Parion $80 Phase II Pulm/Resp 28

Trend in upfront license payments

$0

$10

$20

$30

$40

$50

$60

2010 (n = 106)

2011 (n = 104)

2012 (n = 94)

2013 (n = 83)

2014 (n = 121)

2015 (n=131)

Upf

ront

pay

men

t ($M

)

Year license announced

AVERAGE upfront payments

MEDIAN upfront payments

(n = 106) (n = 104) (n = 94) (n = 83) (n = 121) (n=136)

2010-2015 in aggregate

Number reporting upfront 508

Average upfront $33 M

Median upfront $10 M

NOTE: Analysis includes upfront cash payments only. Equity investments and near-term milestones are excluded.

Upfront payments in licensing transactions by year, 2010-2015

29

Trend in license deal upfront payments by stage

$0 $10 $20 $30 $40 $50 $60 $70 $80 $90

$100 $110 $120

2010

20

11

2012

20

13

2014

20

15

2010

20

11

2012

20

13

2014

20

15

2010

20

11

2012

20

13

2014

20

15

2010

20

11

2012

20

13

2014

20

15

Ave

rage

repo

rted

upf

ront

pay

men

t ($M

)

Year

Average reported upfront ($M) Median reported upfront ($M)

Disc/Preclin n = 242

Phase I n = 63

Phase II n = 134

Phase III/Reg n= 93

Average and median announced upfront payments by year and stage of lead asset, 2010-2015

30

Share of number of pharmaceutical licenses by therapeutic area, 2015

Cancer 35%

Neurology 11% Infection

10%

Diversified 10%

Endo/Meta 8%

AI/Inflam 7%

CV/Hema 3%

Other 16%

Percent change in number of pharmaceutical licenses by therapeutic area, 2010 to 2015

19%

38%

56%

63%

91%

250%

393%

0% 100% 200% 300% 400% 500%

CV/Hema

Neurology

Infection

AI/Inflam

Endo/Meta

Cancer

Diversified

NOTES: Charts includes licenses and JVs for which a therapeutic area is applicable and disclosed. “Other” includes dermatology, chromosomal abnormalities, gastrointestinal disease, genitourinary/sexual function, pulmonary/respiratory, ophthalmic, nutritional supplements, cosmetics, animal health.

2015 n = 777

Baseline: 2010 Comparator: 2015

Trend in number of licensing/JV transactions by therapeutic area

78 in 2010 vs. 273 in 2015

34 in 2010 vs. 65 in 2015

15 in 2010 vs. 74 in 2015

35 in 2010 vs. 57 in 2015

48 in 2010 to 75 in 2015

60 in 2010 vs. 83 in 2015

21 in 2010 vs. 25 in 2015

31

Most active dealmakers of 2015 by number of announced in-licenses

0

5

10

15

20

25

30

Num

ber o

f in-

licen

ses a

nnou

nced

in 2

015

Undisclosed or non-pharmaceutical asset

Approved

Clinical

Discovery/Lead/Preclinical

NOTE: Chart includes in-licensing activity of majority and wholly-owned subsidiaries.

748 companies announced in-

licenses/JVs in 2015

52 companies announced 3 or more

26

16 14

13

11

9 8

6 6 6 6

54% of the in-licenses announced by these top dealmakers were for discovery/preclinical stage assets.

Number of announced in-licenses by company

26

10 10

6

32

October 2013: Spark is spun out of CHOP with $50M investment

May 2014:

Spark raises $72.8M Series B led by Sofinnova Ventures, with leading institutional investors T. Rowe Price and Brookside

December 2014:

Spark announces pre-clinical licensing deal with Pfizer for SPK-FIX for hemophilia B, valued at up to $280M

January 30, 2015:

Spark files IPO (NASDAQ: ONCE) and shares nearly double amid excitement for gene therapy

December 2015: Investor group that participated in Spark’s mezzanine Series B leads a successful

$141M follow-on

Riding the wave: High-value strategic deal amid a series of large financing events

33

More sophisticated landscape enables Spark to ride through volatility

Spark Therapeutics

(100%)

(50%)

0%

50%

100%

150%

Dec 2014 Feb 2015 Apr 2015 May 2015 Jul 2015 Sep 2015 Oct 2015 Dec 2015

Post

IPO

Per

form

ance

(Iss

ue P

rice

vs. P

rice

12/3

1/15

) Drivers of Success

Founded on astounding science

Leveraging strong capital markets

Leveraging seller’s market

Validation from strategic partners

Post-IPO performance

fantastic

34

Date of IPO

Contact Information

2014 Dealmaker’s Report Available from sales, the report includes: Life Sciences Dealmaking 2015

presentation slides Twenty deal snapshots

2015’s top licensing deals 2015’s top M&A events

BioWorld Today reprints on top 2015 licensing and M&A transactions

Spreadsheet with complete set of all life science transactions announced in 2015. Details include buyer/seller, therapeutic arena, stage at selling, total deal size, upfront payment, territory, etc.

Contact your Thomson Reuters account representative for details.

The Thomson Reuters Recap of 2015 Dealmaking Landscape Report

36

Laura J. Vitez Principal Business Analyst Thomson Reuters Recap [email protected] Vinay Singh Senior Deals Analyst Thomson Reuters Recap [email protected] www.thomsonreuters.com

37

37