2015 hsrif annual report draft v3 - haas school of...

TRANSCRIPT

HaasSociallyResponsibleInvestment

Fund

AnnualReport

May2015

1

TABLE OF CONTENTS

Introduction...............................................................................................................................................................................................2

InvestmentApproach............................................................................................................................................................................3

PortfolioSummary..................................................................................................................................................................................4

FinancialPerformanceAnalysis........................................................................................................................................................7

ESGPerformanceanalysis.................................................................................................................................................................10

PortfolioCompanies.............................................................................................................................................................................13

Divestitures..............................................................................................................................................................................................20

NewPositions.........................................................................................................................................................................................28

Accomplishments..................................................................................................................................................................................34

FundPrincipals–Classof2015.......................................................................................................................................................39

FundPrincipals–Classof2016.......................................................................................................................................................41

AdvisoryCommittee.............................................................................................................................................................................43

2

INTRODUCTIONForthe2014–2015academicyear,theHaasSociallyResponsibleInvestmentFund(“HSRIF”)continuedanevolutionarycyclewherethePrincipalssoughtmultipleavenuesofheightenedengagement.Newareasofachievementincludevisitingafirminthefieldofresponsibleinvesting,meetingwithaportfoliocompany,andattendinganumberoftopicalconferences.ThePrincipalsaregratefulforthecontinuedsupportfromtheCenterforResponsibleBusiness(“CRB”)andthegenerousdonationsreceivedthroughtheirefforts.ThePrincipalshavealsobeenfortunatetohaveNadjaGuenster’sleadershipandSumnerField’scontributions,bothofwhichhavebeencriticaltotheHSRIF’ssuccess.Aftermonthsofworkingtogether,theClassof2015PrincipalshavepreparedthenextclasstocontinuetotacklethechallengesofHSRIF’sdualmissiontoinvestforbothfinancialperformanceandenvironmental,social,andgovernanceperformance.

3

INVESTMENT APPROACH The HSRIF investment approach has evolved with each new class of Principals. Although the corefundamental investmentphilosophyis largelyunchanged,eachclasshasbeenableto leverageitsuniqueskills and experiences tohelp enhance the investmentprocess. ThePrincipals evaluate each investmentopportunityfrombothafundamentalvalueperspectiveandanESGperspective.Consistentwithprioryears,thePrincipals’goalistooutperformthebenchmark.ThePrincipalsusetheRussell3000asagaugeofrelativeperformanceandriskexposure.BelowareoutlinedsomeoftheFund’skeyinvestmentprocessinitiatives:PortfolioDiversificationandPositionSizingTheFund re‐evaluatedportfoliodiversificationandposition sizing to ensureadequate riskmanagementthroughproperdiversification.TheFundultimatelydecidedtotargetaportfolioofapproximately15‐20positionstobalancethetradeoffofhavingtoomanypositionsspreadacrosstoofewPrincipalsagainstthediversificationbenefitsofhavingalargerportfolio.Basedonareviewofacademicresearchanddiscussionswith practitioners, the Principals believe the vastmajority of diversification benefit is realized at 15‐20positions.PitchFeedbackandVotingforInvestmentDecisionsThePrincipalshavecontinuedwithablindvotingprocesswherevotes are submittedonline tomitigatepotentialgroup‐basedbiases.EachstockpitchisvotedonESGcriteriaandfinancialperformance,andmusthaveasimplymajorityvoteineachcategorytobeaddedtotheportfolio.EngagementwithAdvisoryBoardThe Principals have continued to encourage involvement of the Advisory Board to better leverage theknowledgeandexperienceofeachboardmember.Boardmembersareinvitedtoattendeithertelephonicallyor in‐personeach full investmentpitchmeeting.Thesesessionsprovedtobehighlyproductiveasboardmembersprovidedvalue‐addedinsightsthathelpedguidethediscussion.ThePrincipalsplantocontinuetofurtherintegrateboardmembersintheinvestmentpitchprocess.Theyalsoheldanin‐personboardmeetingonFebruary6th,2015.Thein‐depthdiscussioncoveredtheFund’sperformanceandinvestmentprocessaswellasthebroaderstrategy fortheFundandcurrent fundraisingefforts.ThePrincipals lookforwardtodeepeningtheirengagementwiththeboardonmultiplefronts.IdeaGenerationandInvestmentPitchesThePrincipalsfurtherrefinedtheideagenerationprocesstobetteridentifythemostcompellinginvestmentopportunitiestofurtherresearch.Theideagenerationprocesstypicallystartswithahighleveldiscussionofpotentialnewideasgeneratedfromadiversesetofsourcesfromwhichasubsetareselectedfora“quickpitch”consistingofashortinvestmentmemothatispresentedtothegroup.Ideasthatsuccessfullymakeitthrough the “quick pitch” process become full investment pitches. The Principals introduced greaterdiscussiononthefront‐endoftheideagenerationprocesstomoreefficientlyscreenthenumerouspotentialinvestmentopportunitiesforfurtherdiligence.OntheESGfront,thePrincipalshavemadeaconcertedeffortto incorporateadditionalproprietaryresearch to theprocess inaddition to leveraging theavailableESGresearchplatforms.

4

PORTFOLIO SUMMARY AsofApril24,2015,theFund’sportfoliowasmadeupofadiversesetofeighteen(18)companiesandcash:

PortfolioIncluding Cash

Holding Weight

AmericanWaterWorks(AWK) 5.35%

AMNHealthcare(AHS) 5.37%

CompassMinerals(CMP) 5.35%

EatonCorp(ETN) 5.34%

GoogleClassA(GOOGL) 5.33%

Keycorp(KEY) 5.36%

MastercardClassA(MA) 5.37%

Microsoft(MSFT) 5.34%

Nucor(NUE) 5.38%

Qualcomm(QCOM) 5.38%

SolarCity(SCTY) 5.34%

Starbucks(SBUX) 5.39%

Stericycle(SRCL) 5.35%

TEConnectivity(TEL) 5.33%

Toronto‐DominionBank(TD) 5.33%

UnitedNaturalFood(UNFI) 5.33%

Vodafone(VOD) 5.35%

WaltDisney(DIS) 5.35%

Cash 3.67%

ComparedtotheApril30,2014annualreport,thiscompositionreflectsthefollowingchangesintermsofholdings:Divestitures: ThePrincipals voted todivest fromDaVitaHealthCarePartners (DVA),Google‐C (GOOG),PepsiCo(PEP),Salesforce.com(CRM),Mylan(MYL),DollarTree(DLTR),WhiteWaveFoods(WWAV),Deere&Co(DE)andEcolab(ECL).ThesedivesturesresultedfromconversationsregardingESGfactorsaswellasthefinancialconditionofeachcompany.Additions: The Principals initiated positions in AmericanWaterWorks (AWS), AMNHealthcare (AHS),Disney (DIS), Keycorp (KEY), Nucor (NUE), Qualcomm (QCOM), SolarCity (SCTY), Strericycle (SRCL),Toronto‐DominionBank(TD),TEConnectivity(TEL),UnitedNaturalFoods(UNFI)andVodafone(VOD).TheFundisaimingtokeepacashpositionof3.67%asneededforthedistributiontotheCRBinJuneof2015of$102,567.06.Detailsregardingthesedivestituresandadditionsareprovidedlaterintheannualreport.

5

CompositionofthePortfolio:Ingeneral,thePrincipalsstrivetomaintainaportfoliooftwelvetotwentyfourpositions.ThePrincipals feel thataminimumoftwelve isnecessarytoachievediversificationwhiletwenty four is themaximum thatwill allow each principal to remain sufficiently in tunewith the dailychangesofthestock.Afterdiscussingrebalancingprocedureswithprofessionalportfoliosmanagerswehaveadopteda(1/n)strategyforweightingindividualsecurities.Aftertherecommendationfrompractitionersandsupportforouracademicadvisor,thePrincipalsfeltthattheyaddmorevaluebyallocatingtheirtimetoconductingindepthresearchonindividualsecuritiestoidentifymis‐valuedopportunities.

Comparisonvs.Benchmark:Thecurrentbenchmark for theFund’sperformance is the iSharesRussell3000Index(IWV).TheiSharesRussell3000ETFseekstotracktheinvestmentresultsofabroad‐basedindexcomposedofU.S.equities.However,itisimportanttonotethatthePrincipalsdonotconstrainthemselvestotheiSharesRussell3000toidentifynewholdings.ThebenchmarkwaschangedtotheiSharesRussell3000Index(IWV)asthePrincipalsbelieveitaccuratelycapturestheperformanceofthewiderUSmarket.Furthermore,byusingMSCIUSAESGSelectETF(KLD)asabenchmarkweloseouradvantageinpickingcompanieswithsolidESGfactors;comparisontotheKLDdoesnottestthethesisthatcompanieswithpositiveESGwilloutperformthegeneralmarketovertime.Wealsoinclude theperformanceof theprevious benchmark, theMSCIUSAESG Select ETF (KLD) for continuitypurposes.ThefollowingtableshowsacomparisonbetweentheFund,itsbenchmarkandtheiSharesESGSelectETFintermsofweightedaveragemarketcapitalization,averageprice‐to‐earningsratio(P/E)andaveragedividendyield:

Holding MarketCap(BN) P/E DividendYieldRussell3000(IWV) $111.29 19.00 1.65%iSharesESGETF(KLD) $7.76 19.57 1.24%

AmericanWaterWorks(AWK) $9.83 23.22 2.30%AMNHealthcare(AHS) $1.14 35.06 n/aCompassMinerals(CMP) $3.00 13.85 2.80%

EatonCorp(ETN) $32.33 18.38 2.90%GoogleClassA(GOOGL) $379.42 26.55 n/a

Keycorp(KEY) $12.27 14.40 1.80%MastercardClassA(MA) $104.37 29.32 0.60%

Microsoft(MSFT) $355.55 17.48 2.89%Nucor(NUE) $15.45 21.81 3.20%

Qualcomm(QCOM) $112.73 14.44 2.40%SolarCity(SCTY) $5.81 n/a n/aStarbucks(SBUX) $74.13 29.98 0.58%Stericycle(SRCL) $11.93 37.07 n/a

TEConnectivity(TEL) $27.93 15.06 1.20%Toronto‐DominionBank(TD) $85.17 13.96 3.70UnitedNaturalFood(UNFI) $3.54 21.10 n/a

Vodafone(VOD) $91.80 1.34 5.30%WaltDisney(DIS) $185.25 24.23 1.15%

6

SectorExposures:TheabovechartillustratestheFund’ssectorexposures.

SectorWeighting:4/24/2015

Sector Exposures: The above chart illustrates each position’s correlation with other positions andbenchmarksoverthepast365daysasof04/24/2015

Cash, 4% Consumer Discretionar

y, 11%

Consumer Staples, 5%

Financials, 11%

Health Care, 5%Industrials,

16%

Information Technology,

27%

Materials, 11%

Telecommunication

Services, 5%

Utilities, 5%

SectorDistribution

Tickers AHS AWK CMP DIS ETN GOOGL KEY MA MSFT NUE QCOM SBUX SCTY SRCL TEL TD UNFI VOD IWV KLD

AHS 1.00 0.10 0.08 0.22 0.26 0.29 0.27 0.29 0.20 0.14 0.20 0.21 0.26 0.19 0.28 0.16 0.31 0.16 0.38 0.37

AWK 0.10 1.00 0.05 0.25 0.25 0.18 0.18 0.25 0.22 0.17 0.18 0.28 0.15 0.34 0.20 0.13 0.18 0.24 0.40 0.40

CMP 0.08 0.05 1.00 0.21 0.33 0.25 0.32 0.22 0.20 0.34 0.25 0.15 0.22 0.27 0.29 0.26 0.22 0.21 0.44 0.42

DIS 0.22 0.25 0.21 1.00 0.40 0.37 0.47 0.50 0.33 0.34 0.26 0.40 0.29 0.41 0.40 0.33 0.33 0.38 0.64 0.60

ETN 0.26 0.25 0.33 0.40 1.00 0.36 0.50 0.46 0.39 0.45 0.35 0.23 0.34 0.41 0.51 0.49 0.32 0.39 0.71 0.74

GOOGL 0.29 0.18 0.25 0.37 0.36 1.00 0.43 0.49 0.40 0.35 0.27 0.41 0.30 0.29 0.34 0.23 0.34 0.25 0.59 0.54

KEY 0.27 0.18 0.32 0.47 0.50 0.43 1.00 0.40 0.32 0.43 0.23 0.39 0.30 0.39 0.40 0.42 0.31 0.33 0.68 0.63

MA 0.29 0.25 0.22 0.50 0.46 0.49 0.40 1.00 0.31 0.38 0.33 0.37 0.30 0.44 0.52 0.35 0.43 0.37 0.67 0.62

MSFT 0.20 0.22 0.20 0.33 0.39 0.40 0.32 0.31 1.00 0.27 0.22 0.35 0.19 0.27 0.24 0.28 0.26 0.31 0.54 0.56

NUE 0.14 0.17 0.34 0.34 0.45 0.35 0.43 0.38 0.27 1.00 0.28 0.22 0.31 0.29 0.42 0.43 0.30 0.31 0.59 0.57

QCOM 0.20 0.18 0.25 0.26 0.35 0.27 0.23 0.33 0.22 0.28 1.00 0.15 0.25 0.32 0.37 0.32 0.18 0.23 0.45 0.42

SBUX 0.21 0.28 0.15 0.40 0.23 0.41 0.39 0.37 0.35 0.22 0.15 1.00 0.25 0.29 0.27 0.20 0.36 0.26 0.51 0.48

SCTY 0.26 0.15 0.22 0.29 0.34 0.30 0.30 0.30 0.19 0.31 0.25 0.25 1.00 0.22 0.33 0.32 0.23 0.25 0.43 0.37

SRCL 0.19 0.34 0.27 0.41 0.41 0.29 0.39 0.44 0.27 0.29 0.32 0.29 0.22 1.00 0.39 0.27 0.29 0.29 0.60 0.60

TEL 0.28 0.20 0.29 0.40 0.51 0.34 0.40 0.52 0.24 0.42 0.37 0.27 0.33 0.39 1.00 0.35 0.32 0.38 0.64 0.63

TD 0.16 0.13 0.26 0.33 0.49 0.23 0.42 0.35 0.28 0.43 0.32 0.20 0.32 0.27 0.35 1.00 0.17 0.36 0.52 0.52

UNFI 0.31 0.18 0.22 0.33 0.32 0.34 0.31 0.43 0.26 0.30 0.18 0.36 0.23 0.29 0.32 0.17 1.00 0.30 0.52 0.47

VOD 0.16 0.24 0.21 0.38 0.39 0.25 0.33 0.37 0.31 0.31 0.23 0.26 0.25 0.29 0.38 0.36 0.30 1.00 0.53 0.50

IWV 0.38 0.40 0.44 0.64 0.71 0.59 0.68 0.67 0.54 0.59 0.45 0.51 0.43 0.60 0.64 0.52 0.52 0.53 1.00 0.96

KLD 0.37 0.40 0.42 0.60 0.74 0.54 0.63 0.62 0.56 0.57 0.42 0.48 0.37 0.60 0.63 0.52 0.47 0.50 0.96 1.00

7

FINANCIAL PERFORMANCE ANALYSIS1 YearEndedApril21,2015TheFundrealizedatotalreturnof16.36%betweenApril21,2014andApril21,2015,outperformingtheiSharesRussell3000ETF’stotalreturnof13.80%by256basispoints.TheFundbalanceasofApril21,2014was$2,274,667.22.TheFundreceivedthefollowingcashdeposits:$40,000onJanuary23,2014,$68,583.54on04/23/14,$131,209on5/14/14,$20,264.02on08/20/14and$1,945.13on9/18/14.Thefund’sonlywithdrawalfortheyearfortheannualwithdrawaltofundtheCRB.Thisamountwas$71,285andoccurredon11/26/14.BecausetheFund’sreturniscalculatedonaholdings‐basis,cashwithdrawalsanddepositshavenoimpactonreturnscalculations.

HSRIFperformancerelativetoIWV(includingcash),04/21/2014‐04/21/2015

TheFund’sperformanceoverthepast12monthsmaybeexplainedby:

WehavereducedcashdragbyattemptingtoremainedfullyinvestedinindividualequitiesorwhennecessaryinvestedinKLDtoreapthereturnsoftheoverallESGmarket

Ourwinnersoutperformedour losersbyasolidmargin;DLTR(51.43),WWAV(42.10)andSBUX(39.31)vs.NUE(‐11.99),DE(‐7.52)andETN(‐3.44)

Finally,theworkcompletedlastsemesterhadon‐boardingofthenextclassrunmuchmoresmoothlywhichcontributedtoourconcentrationbeingfocusedoninvestingratherthanprocess

1 Bloomberg computes performance on a holding basis. Performance reflects total returns for thebenchmark,i.e.dividendsarereinvested.However,dividendsgeneratedbyHSRIFholdingsflowtocash.

8

Top10andBottom10ContributorstoReturn,04/21/2014‐04/21/2015

CumulativePerformanceChartsThefollowingchartshowstheFund’shistoricalperformanceversusthebenchmark,IWV.Forthelast3years,theFundoutperformedIWVby14basispoints.

HSRIFperformancerelativetoIWV,04/21/2012‐04/21/2015

9

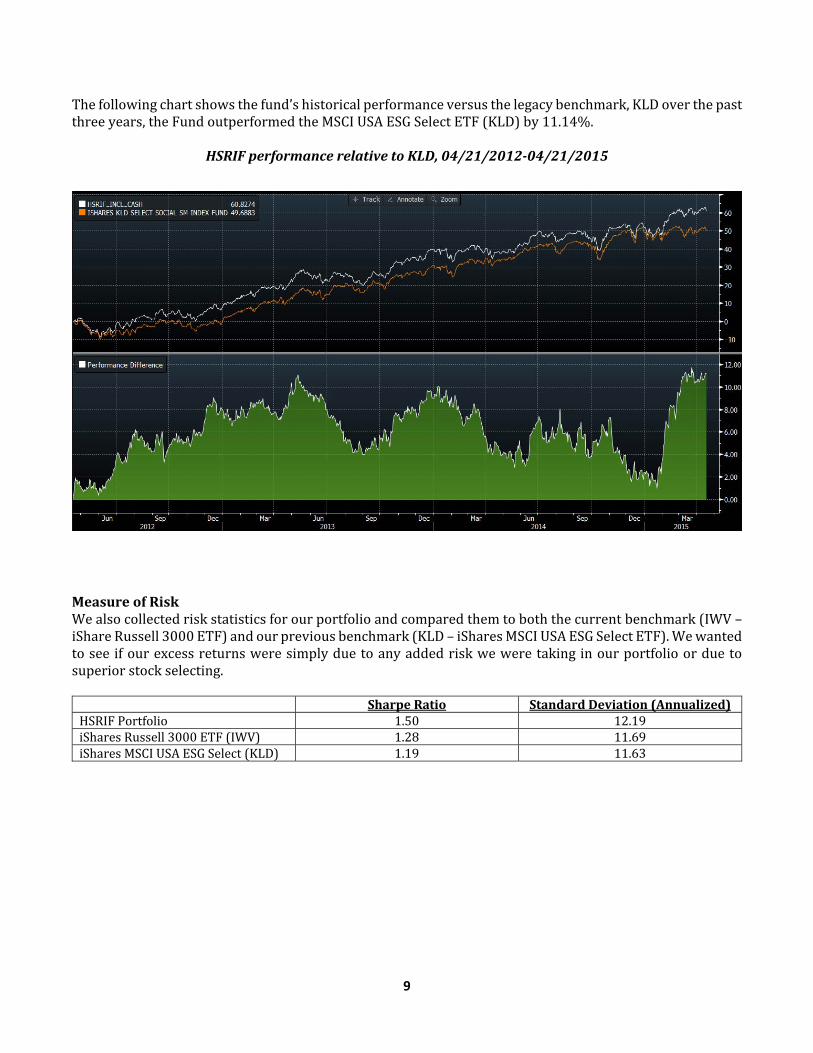

Thefollowingchartshowsthefund’shistoricalperformanceversusthelegacybenchmark,KLDoverthepastthreeyears,theFundoutperformedtheMSCIUSAESGSelectETF(KLD)by11.14%.

HSRIFperformancerelativetoKLD,04/21/2012‐04/21/2015

MeasureofRiskWealsocollectedriskstatisticsforourportfolioandcomparedthemtoboththecurrentbenchmark(IWV–iShareRussell3000ETF)andourpreviousbenchmark(KLD–iSharesMSCIUSAESGSelectETF).Wewantedtoseeifourexcessreturnsweresimplyduetoanyaddedriskweweretakinginourportfolioorduetosuperiorstockselecting. SharpeRatio StandardDeviation(Annualized)HSRIFPortfolio 1.50 12.19iSharesRussell3000ETF(IWV) 1.28 11.69iSharesMSCIUSAESGSelect(KLD) 1.19 11.63

10

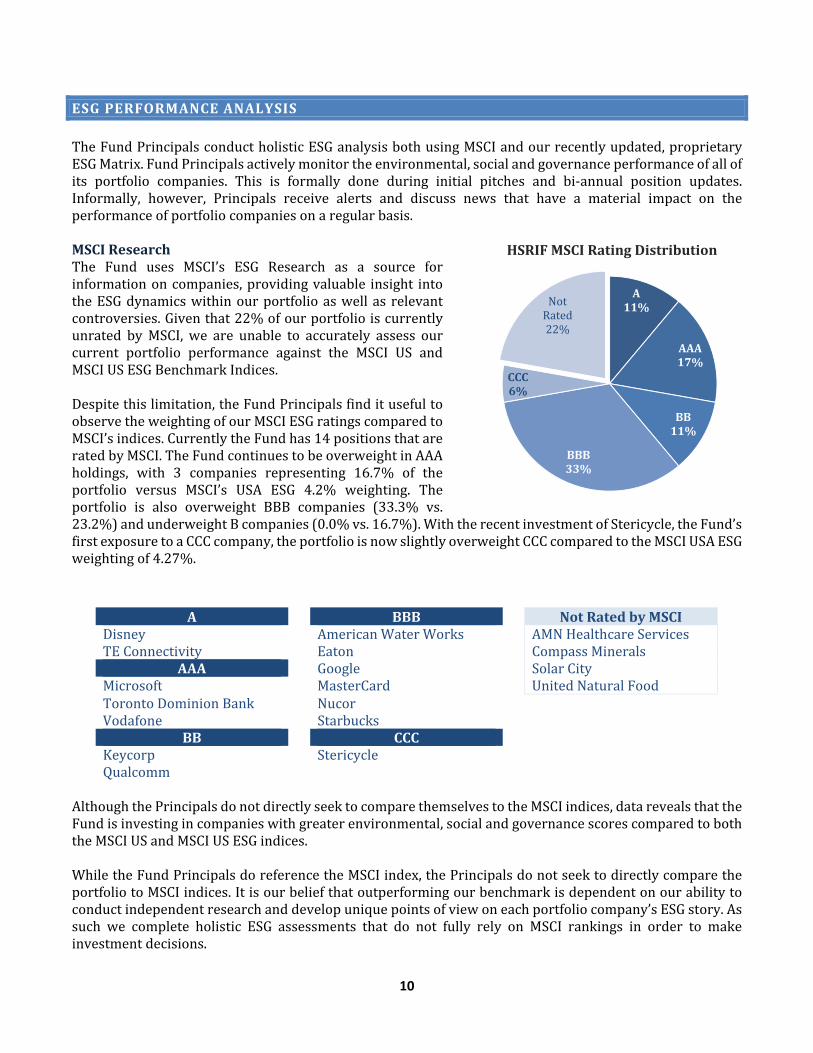

ESG PERFORMANCE ANALYSIS TheFundPrincipalsconductholisticESGanalysisbothusingMSCIandourrecentlyupdated,proprietaryESGMatrix.FundPrincipalsactivelymonitortheenvironmental,socialandgovernanceperformanceofallofits portfolio companies. This is formally done during initial pitches and bi‐annual position updates.Informally, however, Principals receive alerts and discuss news that have a material impact on theperformanceofportfoliocompaniesonaregularbasis.MSCIResearchThe Fund uses MSCI’s ESG Research as a source forinformationoncompanies,providingvaluable insight intotheESGdynamicswithinourportfolioaswellas relevantcontroversies.Giventhat22%ofourportfolioiscurrentlyunrated byMSCI, we are unable to accurately assess ourcurrent portfolio performance against the MSCI US andMSCIUSESGBenchmarkIndices.Despitethislimitation,theFundPrincipalsfinditusefultoobservetheweightingofourMSCIESGratingscomparedtoMSCI’sindices.CurrentlytheFundhas14positionsthatareratedbyMSCI.TheFundcontinuestobeoverweightinAAAholdings, with 3 companies representing 16.7% of theportfolio versus MSCI’s USA ESG 4.2% weighting. Theportfolio is also overweight BBB companies (33.3% vs.23.2%)andunderweightBcompanies(0.0%vs.16.7%).WiththerecentinvestmentofStericycle,theFund’sfirstexposuretoaCCCcompany,theportfolioisnowslightlyoverweightCCCcomparedtotheMSCIUSAESGweightingof4.27%.

AlthoughthePrincipalsdonotdirectlyseektocomparethemselvestotheMSCIindices,datarevealsthattheFundisinvestingincompanieswithgreaterenvironmental,socialandgovernancescorescomparedtoboththeMSCIUSandMSCIUSESGindices.WhiletheFundPrincipalsdoreferencetheMSCIindex,thePrincipalsdonotseektodirectlycomparetheportfoliotoMSCIindices.Itisourbeliefthatoutperformingourbenchmarkisdependentonourabilitytoconductindependentresearchanddevelopuniquepointsofviewoneachportfoliocompany’sESGstory.Assuch we complete holistic ESG assessments that do not fully rely on MSCI rankings in order to makeinvestmentdecisions.

A BBB NotRatedbyMSCIDisney AmericanWaterWorks AMNHealthcareServicesTEConnectivity Eaton CompassMinerals

AAA Google SolarCityMicrosoft MasterCard UnitedNaturalFoodTorontoDominionBank NucorVodafone Starbucks

BB CCC Keycorp StericycleQualcomm

A11%

AAA17%

BB11%

BBB33%

CCC6%

NotRated22%

HSRIFMSCIRatingDistribution

11

HSRIFProprietaryESGMatrixWhile MSCI allows Principals to monitor and track the ESG factors of most of its portfolio companies,PrincipalshaveupdatedtheFund’sproprietaryframeworktoallowforamoreholisticanalysis.Theupdatedframeworkseekstoaccomplishfourprimarygoals:

1. AligndifferentPrincipals’ESGprioritiestoguideourinvestmentdecisions.2. ClarifyapreviouslyambiguousprocessforESGanalysis.3. Facilitateresearchandanalysisofpotentialalpha‐generatingESGcriteriabeyondwhat’sincludedin

MSCI.4. QuantifymetricsinordertomakelesssubjectiveESGinvestmentdecisions.

The resulting framework has seven ESG criteria that the Principals deemedmost important: Diversity,CommunityEngagement,EnergyandEnvironment,BoardGovernance,SupplyChain,WorkingConditions,andSocialImpact.Eachcriteriahasarangeofconsiderationsthatdrivesascorefrom1‐5,asoutlinedbelow:

HSRIFESGCriteria Considers:

1) Diversity• Positivelytarget/hire/supplyfromunder‐servedgroups• Women/diversityinleadership(board,c‐suite)

2) CommunityEngagement

• Politicalactivismonkeyissues(climatechange,LGTBrights,etc)• Politicaldonations:dotheydisclose,towhom?• Clear efforts to positively impact communities (local + overseas

supplychain)

3) EnergyandEnvironment

• Efforts to reduce energy consumption, emissions, toxic waste,general environmental impact (within operations and/orcommunity)

• Strong/clearsustainabilitygoals/policies

4) BoardGovernance• Balanced(skillset,experience)• Directorsindependent/elected• Executivepaydisclosed

5) SupplyChain• Sourcingpoliciespositivelyconsiderlabor,impactonenvironment,

sharedvalueinitiatives• Transparentmonitoringandissuesmanagement

6) WorkingConditions • Promotespositiveworkingenvironment• Treatsemployeeswell,goodbenefits

7) SocialImpact• Core mission: enhances quality of life/access, promotes healthy

lifestyles,revolvesaroundsolvingasocialproblem• Philanthropy

12

Wemeasureeverycompany’ssuccesswithineachcriterionwithafive‐stageassessment,whichisassociatedwithascorefrom1‐5:Stage1:NoreportingonkeyissuesStage2:TransparentreportingofkeyofissuesbutneedforactionStage3:DevelopmentofaneffectivestrategyandmetricstoaddresskeyissuesStage4:SignificantprogresstowardgoalsandtransparentreportingonallmetricsStage5:Successfultrackrecord;industryleaderonkeyissuesThescoresforeachofthesevencriteriaarethensummed,creatinganaggregate“ESGScore”foreachcompany.Whilecompaniesarenotchosensimplyonhowhightheyscore,thePrincipalsusethisscore(alongwiththeMSCIscore,ifavailable)tocomparecompaniesandguidediscussions.ThenewframeworkhaspushedPrincipalstoperformmorethoroughESGresearchandanalysis,withthebeliefthatdatathatisnotalreadycapturedwithinMSCIcouldpotentiallygeneratelargeralphafortheFund.

13

PORTFOLIO COMPANIES

CompassMineralsInternational(NYSE:CMP)Sector:MaterialsIndustry:Metals&MiningCompanyDescription:CompassMineralsInternational(CMP)isamajorproducerofsalt,magnesiumchloride,andsulfateofpotash(SOP)specialtyfertilizerinNorthAmerica.ItisalsoalargeproducerofsaltintheU.K.CMPprovidessaltforuseinhighway,consumerandindustrialdeicing,watercare,andanimalnutritioninNorthAmericaandtheU.K. (~81% of revenues) and specialty fertilizer for use with high value crops worldwide (~19% ofrevenues).Thecompanyalsohasasmallrecordsmanagementbusiness(DeepStore)intheU.K.thatutilizesexcavatedportionsofasaltmineforsecureundergrounddocumentstorage.InvestmentPitch:Thesalt industryenjoysstabledemand througheconomiccyclesandhasexperienced long‐termvolumegrowthof1‐2%annuallyandpricinggrowthof3‐4%.AsoneofthreemajorsaltproducersinNorthAmerica,Compassisamarketleaderinanoligopoly.Compassenjoysaccesstotheworld’slargestrocksaltmineandtheonlynaturallyoccurringsourceofSOPinNorthAmerica,bothofwhichgiveCompassasustainablecostadvantage.Further,itsminesanddepotsarelocatednearstrategicwaterwaysthatminimizetransportationcostsandallowittobethelow‐costproducerinitsserviceareas,animportantadvantagesincesaltconsistslargely of localized markets. These advantages allow Compass to enjoy 20%+ operating margins for acommodityproduct.From an ESG perspective, Compass provides the necessary, life‐saving service of deicing the nation’shighways.Thecompany’ssolarevaporationfacilitiesareagreatexampleofacorebusinessstrategythatisalsogoodfortheenvironmentasitisbothgreenandlow‐cost.Compassalsohasanexcellentsafetyrecordandevenincludessafetymetricsindeterminingmanagementcompensation.Outcome:CMPhasbeenaportfolioholdingsinceMay2012.Shareshaverisen6%overthepastyear,aswinterweatherhasbeenslightlymoreseverethanexpectations,causingrelativelymodestincreasesinsaltprices.Initsmostrecentearningsrelease,CMPreported2014salesup14%year‐over‐yearto$1.28billion.Earningspersharein2014increased67%to$6.44.AdjustedEBITDAwasup20%YOY,showingstrongoperatingresultsacrosstheboard.Goinginto2015,CompassMineralsannounceda10%increaseinquarterlydividend.

14

EatonCorporation(NYSE:ETN) Sector:IndustrialsIndustry:ElectricalEquipmentCompanyDescription:EatonCorporationisadiversifiedpowermanagementcompanyandaglobaltechnologyleaderinelectricalcomponentsandsystemsforpowerquality,distributionandcontrol;hydraulicscomponents,systemsandservices for industrial and mobile equipment; aerospace fuel, hydraulic and pneumatic systems forcommercialandmilitaryuse;andtruckandautomotivedrivetrainandpowertrainsystemsforperformance,fueleconomy,andsafety.Putsimply,Eatonprovidestheinfrastructuretodeliverandcontrolenergy.Thecompanyhasover100,000employeesandsellsproductsin175countries.Eatonsellsintoawiderangeofmarkets, including agriculture, aviation, communications, IT, electronics, government and military,healthcare,manufacturing,residential,andvehicles.InvestmentPitch:Eaton’scoremissionis“thinkingpowerfully”todeliverinnovativepowermanagementsolutionsthatnotonly improvecustomerbusinesses,butalsohelp improvetheworld. Withthecostofenergyextraction,distribution,andutilizationincreasing,alongwithmorestringentgovernmentregulationtocontrolenergyconsumption,companiesincreasinglyneedpowermanagementtechnologiestoensureenergyisusedsafelyand economically. Eaton has been gaining market share and outperforming its end markets, and thePrincipalsexpectthistoaccelerateinthecomingyears.Eatonhasbeenactivelyexpandingitsbusinessbymakingacquisitions.MostnotablewastheNov.30,2012acquisitionofCooperIndustries,amanufacturerofelectricalcomponentsandtoolswithsalesof$5.4Bin2011. ThestrategicrationalebehindthedealistoexpandEaton’saddressablemarketthroughCooper’sportfolio of complementary products, specifically targeting the utility power distribution network(upstream) and lighting/lighting controls (downstream). Previously, Eaton’s electrical product portfolioprimarilytargetedfacility‐levelpowerdistribution.CostcuttingdivestmentsandstrategicacquisitionsarehelpingEatoncreatedifferentiatedproductsandtechnologythatpositionitwellforfuturegrowth.Synergiesandrevenuegrowthfromacquisitionsarealreadybeingrealizedataratehigherthananticipated.From an ESG perspective, Eaton’s diverse portfolio of energy‐efficient products, strong supply chainmanagement policies, and internal commitment to sustainability add value by driving revenue growth,controllingcostsatthecompany‐levelandacrossthesupplychain,andmitigatingsupply‐chainrisk.MSCIratedEatonAAAon1/3/13,primarilyforitsenvironmentalstewardship.EatonisfocusedonreducingGHGemissions, water consumption, and waste generation, and their strong ESG has been recognized bynumerous parties: listed on the Carbon Disclosure Project’s Index of S&P 500 companies that practiceexemplary environmental reporting; named as one of the “100 Best Corporate Citizens” in CorporateResponsibilitymagazineforthe fifthstraightyear;and listedontheEthisphere Institute’s listof“World’sMostEthicalCompanies”fortheseventhstraightyear.Outcome:ETNhasbeenaportfolioholdingsinceNovember2010,withsharesupnearly50%inthattimeframeandmorethan25%inthepastyear.TheFundvotedtocontinuetoholdthestockinApril2014.

15

GoogleInc.(NASDAQ:GOOG,GOOGL) Sector:InformationTechnologyIndustry:InternetSoftware&ServicesCompanyDescription:GoogleInc.isoneoftheleadinginternettechnologyandadvertisingcompaniesintheworldandisthelargestinternetsearchengine.TheCompanymaintainsanindexofwebsitesandothercontentandmakesthemfreelyavailableontheInternetthroughitsautomatedsearchtechnology.Advertisingrevenuesmakeup90%ofitsrevenues.Thecompany’sadditionalrevenuesarederivedfromtheAndroidoperatingsystemplatform,itsenterpriseproducts(GoogleApps),aswellasdisplayadvertisingmanagementservicestoadvertisers,adagencies,andpublishers.InvestmentPitch:Whenthestockwasfirstpitched,thethesiscenteredonrisingcost‐per‐click,increasingmarketshareandimprovingoperatingmargins.Noneofthesestillholdtrue.EvenasmarketshareisthreatenedbyFacebookandothercompetitors,onanabsolutebasis,Googlewilllikelymaintainitsdominantshareandadvertisingrevenueshouldcontinuetogrowasonlineadvertisingspendbecomesanincreasinglylargerportionoftotaladvertisingdollars.Thecompanydoesnottypicallydisclosedifferencesincost‐per‐clickandaggregatepaidclicks betweenmobile and desktop search, but the increased use ofmobile searchwill put pressure onmargins.However,Google recentlyannounced the introductionof app installads to thePlaystore. AppinstalladshavebeencriticaltoFacebook’smobilerevenuegrowth,andwillbeanimportantrevenuesourceforGoogleinthefuture.GooglehasincreaseditsR&Dspendinrecentyears.Thisislikelytobebeneficialinsomeareas,particularlywithcontentgenerationatYouTube. However,wecontinuetobemindfuloftherevenuepotentialof“10”projectsininthe70/20/10model.Googlehasonlyrecentlyappearedasahighperformerinvarioussustainabilitymetrics,suggestingthatthemarkethasnotyet fullyrealizedthescopeorpotential impactof itssustainabilityprogram. In turn, thissuggeststhatthevaluetobegained fromthese initiatives isnotyet incorporated into itsstockprice.Oncertain issues (sustainability, social impact/philanthropy) Google is a clear market leader. On others,particularlyprivacyandcorporategovernance,Googleraisesseriousconcerns.Outcome:Google’ssharepriceonApril24,2015was$573.66,comparedtotheFund’sinitialpurchasepriceof$277.12inOctoberof 2009 (increaseof 107%,or an annualized returnof 14%). Googlemadeanumberof keyannouncementsinthespringof2015.Googlerecentlyannouncedthatitwouldlaunchawirelessservice–Project Fi. The servicewill be small‐scale, intending to demonstrate technological innovations and notcompetewithexistingcarriers.TheservicewouldidentifythebestsignalamongcellularnetworksandWi‐Fi.InFebruary,GoogleannouncedthatitwillallowappdeveloperstopurchaseadsthatwillbedisplayedintheGooglePlaystoreonAndroiddevices.GooglealsorecentlyannouncedthatAT&T,VerizonandT‐Mobilewillpre‐installGoogleWalletonAndroidphonessoldintheU.S.beginninglaterthisyear.Googlestatedthatitwouldacquiretechnologyandintellectualpropertyfromapaymentsservicestartedbythecarriers.TheWalletappwillinclude“tapandpay”technology.InApril,theEuropeanCommissionfiledantitrustchargesagainst Google related to shopping search results and launched an investigation into whether GoogleengagedinanticompetitivebehaviortoblockrivalstotheAndroidmobileoperatingsystem.InMarch2015,FundPrincipalsvotedtoholdandmonitorGoogle,mindfulofthemixofESGpositivesandnegatives.

16

MasterCardIncorporated(NYSE:MA) Sector:ServicesIndustry:BusinessServicesCompanyDescription:MasterCard (“MA”) is a technology company in the global payments industry. It connects consumers,financialinstitutions,merchants,governments,andbusinessesworldwidetouseelectronicpaymentsratherthancashandchecks. Itofferspaymentsolutionsthatallowforthedevelopmentandimplementationofcredit, debit, prepaid, commercial, and related payment programs and solutions for consumers andmerchants.MasterCard’sbrandsincludeMasterCard,Maestro,andCirrus.MasterCardprocessespaymentsovertheMasterCardworldwidenetworkandprovidesrelatedsupportservicestoitscustomers.InvestmentPitch:MasterCard is an attractive investment given the secular trend toward non‐cashpayments in the globalpaymentsspace.MasterCardalsohasahighlyscalablebusinessmodel.Personalconsumptionexpendituregrowth will support MasterCard’s top‐line growth via its vast network and robust market share.MasterCard’s wide geographic exposure provides great global diversification and growth upside.MasterCardalsohasseveralupsidecatalysts. Itbenefitsfromanincreasedcrossbordervolumemultiplewithhighertransactionpaymentfees.ItspartnershipwithChinaUnionPayalsopositionsMasterCardwellforfuturelong‐termopportunityforgrowingcreditcardpaymentsinChina.MasterCardalsohasexcellent,shareholder‐friendlyfinancialperformanceandhassustaineddouble‐digitrevenuegrowth.Netrevenueforthefourthquarterof2014was$2.4billion,a14%increaseversusthesameperiodin2013as‐reportedand17%increaseadjustedforcurrency.FromanESGperspective,MasterCard’seffortstopromotefinancialinclusionaroundtheworldaredirectlytiedtoitsstrategicgoalsanditsbottomline.Thecompanyhaslaunchedmanywin‐wincorporatecitizenshipprograms,whichtrulyembodythegoalof“doingwellbydoinggood.” InMarch2015alone,MasterCardlaunched remittance services inNigeria and Zimbabwe and announced a partnershipwith the Egyptiangovernment thatwill enable54millionEgyptian citizens to link theirnational ID to thenationalmobileecosystem,thusfacilitatingtheirparticipationintheformalelectroniceconomy.Outcome:TheFundPrincipalsvotedtoenterwithapproximately5%ofourtotalportfolioallocationinMay2013atanaveragepriceof$538.89/share.Subsequently,MasterCardexceededitsthree‐yeartargetsinlessthanayear.A10xstocksplitinMarch2014resultedinastockpriceofabout$78/shareatthattime.Nowoneyearlater,MasterCard’sstockpricehasrisentoroughly$90/share.InMarch2015,FundPrincipalsvotedtoholdandmonitorMasterCardgivenitsstrongfinancialperformancedrivenbyinternationalgrowthcoupledwithapowerfulandunchangedESGstoryaroundfinancialinclusion.

17

Microsoft(NYSE:MSFT)

Sector:TechnologyIndustry:Software&Services

CompanyDescription:Microsoft is theworld’s largest software company.Over 80%of its revenue and nearly all of its profitscontinuetobederivedfromtheWindowsOS,WindowsService,andOffice.Thecompany'sproductsincludeoperatingsystemsforcomputingdevices,servers,phones,andotherintelligentdevices;serverapplicationsfordistributedcomputingenvironments;productivityapplications;businesssolutionapplications;desktopand servermanagement tools; software development tools; video games; and online advertising. It alsodesigns and sells hardware devices including surface rt and surface pro, the xbox 360 gaming andentertainmentconsole,kinectforxbox360,xbox360accessories,andmicrosoftpcaccessories.Thecompanyoperatesitsbusinessthroughfollowingsegments:DevicesandConsumer(D&C)Licensing,ComputingandGamingHardware,D&COther,CommercialLicensing,andCommercialOther.InvestmentPitch:Theoriginalpitchcenteredonthesethreecatalystsforimprovingupside:

StableRevenueGeneration:Microsoftisbecomingaleanerbusinessfocusedonitsprimarydifferentiatorsandcustomervaluepropositions.Over80%ofitsrevenueandnearlyallofitsprofitscontinuetobederivedfromtheWindowsOS,WindowsService,andOffice.Thesearetheconsumerstaplesofbigbusiness.TheEnterpriseLicensingDivisionremainsthejewelinthecrownandcontinuestodriveMicrosoft’srevenuegrowth.

EvolvedGrowthStrategy:CEONadellacontinuestodeliveronhisstrategytoembracethewindsofchangeintheworldofbigtechandwebelievethefirm’swellestablishedproductsuiteispositionedtothriveinthenewworld.LaunchesofOffice365fortheAppleiPadandEnterpriseMobilitySuitedisplayanincreasedwillingnesstoinvestinnon‐Windowsplatformsinpursuitofopportunitiesinmobileandcloudservices.

ESGLeader:Microsoft’sESGqualitieswereupgradedfromAAtoAAAbyMSCI–arewardforthefirm’sexemplaryperformanceinallareasofESGanditssignificantimprovementsinhumancapitalmanagement.

Fortheportfolioupdate,itwasfoundthatthesemaincriteriastillholddespiterecentdownwardmovementsinthecompany’sshareprice.MicrosofthavebeenconfrontedwithheadwindsininternationalsaleswhichhavebeendampenedbythestrongUSDrelativetoothercurrencies.ThePrincipalsagreedthatthelong‐termstrategyandcorecapabilitiesofthecompanyisstrongandthattherecentnegativemovesinstockpriceareareflectionoftheunimpressedshort‐termtraders.Outcome:InMarch2015,theFundPrincipalsvotedtoholdMicrosoftwithapproximately5%ofourtotalportfolioallocation.Since theoriginalpitch inApril2014, thestockvaluehasappreciated6%witha further22%increasetargetedoverthenextthreeyears.

18

SolarCity(NYSE:SCTY) Sector:EnergyIndustry:RenewablesCompanyDescription:In late April 2014, the Fund Principals voted to invest in SolarCity, a company offering installation,monitoringandrepairservicesofsolarenergysystemsintheU.S.Throughinnovativefinancingstructures,SolarCitymakescleanenergyavailabletohomeowners,businesses,schools,non‐profits,andgovernmentorganizationsatalowercostthantheypayforenergygeneratedbyburningfossil fuelslikecoal,oil,andnaturalgas.Wefoundthiscompanycompellingduetoitstransformativeimpactonsolarenergythroughfinancialinnovationcoupledwithitsstronggrowthpotentialinaburgeoning$63billionelectricitymarket.Atitscore,SolarCityishelpingpeopleandorganizationsreducetheircarbonfootprintandtheirutilitybills.InvestmentPitch:Our 2014 valuationmodel assumed explosive growth in the retail segment (75%+) and continued costdeclines,whichatthattimepointedtoafinancialvaluationof40%overtheprevalentmarketprice.During2015, we maintained a HOLD recommendation on the stock, as Solar City performed extremely welloperationally.ThecompanywasabletogrowitsmarketshareofUSresidentialinstallationsfrom27%in4Q13to39%in4Q14‐thisisequivalenttothenext70installerscombined.Itmanagedtodrivedownitsunitcosts(‐20%lastyear)andoutperformedthenearestcompetition,whichisexpectedtoreachSCTY’s$2.87/W cost level only in 2017. On the customer side, SCTY doubled its customer base to 190,000customers.Outcome:SolarCityhashadavolatileyear,withasignificantrisetoover$70/shareandthensubsequentdroptoourentrylevelinthelow50s,inpartdrivenbyadropinoilpricesandthemarketsbearishviewonthesolarindustryoverall.Thestockiscurrentlytestingthe$60levelagain,onthepositivetailwindsofaproposedcollaborationwithTesla’sbatterytechnologiestostorethepowerthatitspanelscollect,aswellasa$1bnfundraisedwithCreditSuisse to fund furtherexpansion in commercial solarprojects, includingschools,businessesandgovernment.WallStreetremainsbullishonthestockwithMerrillLynchrecentlygivingita75%upsidetargetpriceof$95.ThecontinuedstrongESGangleinsolar,aswellasthepotentiallystrongupsidethatwebelievewillberealizedbythestockhaveledustocontinueholdingSolarCityaspartofourportfolioasofApril2015.

19

StarbucksCorporation(NASDAQ:SBUX)Sector:ConsumerDiscretionaryIndustry:RestaurantsCompanyDescription:Starbucks Corporation operates as a roaster, marketer, and retailer ofspecialty coffee worldwide. Its stores offer coffee and tea beverages,packagedroastedwholebeanandgroundcoffees,singleserveproducts,andjuicesandbottledwater.Thecompany’sstoresalsoprovidefreshfoodofferings;ready‐to‐drinkbeverages;andvariousfoodproducts,includingpastries,andbreakfastsandwichesandlunchitems,aswellasbeverage‐makingequipmentandaccessories.Inaddition,itlicensestherightstoproduceanddistributeStarbucksbrandedproductstoTheNorthAmericanCoffeePartnershipwiththePepsi‐ColaCompany,aswellaslicensesitstrademarksthroughlicensed stores, grocery, and national foodservice accounts. The company offers its products under theStarbucks,Teavana,Tazo, Seattle’sBestCoffee, StarbucksVIA, StarbucksRefreshers, EvolutionFresh, LaBoulange,andVerismobrandnames.AsofSeptember29,2013,itoperatedapproximately10,194company‐operatedstoresandapproximately9,573licensedstores.StarbucksCorporationwasfoundedin1985andisbasedinSeattle,Washington.InvestmentPitch:Starbucks is a best in class example of a company who has consistently and strategically integratedsustainabilitywithinitscorebusinessmodel.ThePrincipalsfeelthatthesustainabilityinitiativestheyhaveundertakenoverthepast8yearswillproducenotonlyrealizablecostsavingsbutalsoriskmanagementinthetougheconomicclimate;particularlyintheirethicalsourcinginitiatives.Similarly,discretionarygoodshavetakensignificanthitoverthepastyear,Starbuckincluded,butthePrincipalsfeelthattheCompany’sfocusonsustainabilityaswellascontinuedexpansionintonewgeographicareaswillofferacompetitiveadvantageovercompetitorsasthemarketcontinuestorebound.Outcome:TheFundPrincipalsinitiallyvotedtoinvestinSBUXattheendof2013.Despitestrongperformancein2013(12%increaseto$14.9billion)andrecordfiscalsecondquarter2014salesof$3.9billion,SBUXhasbeenone of the lowest performing positions in the Fund’s portfolio. YTD return as ofMay 1, 2014 is ‐9.6%.However,giventhecompany’sbestinclasssustainabilitystrategyandWallStreetanalysts’beliefinsharevalueupsidetheFundPrincipalsareconfidentinthevalueoftheSBUXpositionintheFund’sportfoliooverthe3‐Yearinvestmenthorizon.

20

DIVESTITURES

DaVitaHealthCarePartners,Inc.(DVA)Sector:HealthcareIndustry:SpecializedHealth

CompanyDescription:DaVitaHealthCarePartners Inc.operates in twomajorbusinesssegments.Thecompany’s largest lineofbusinessisprovidingkidneydialysisservicestopatientssufferingfromchronickidneyfailureandendstagerenal disease. As of December 31, 2013, DaVita operated or provided administrative services at 2,074outpatientdialysiscentersintheUnitedStatesservingapproximately163,000patients.DaVitaalsooperates73outpatientdialysiscentersin10countries.HealthCarePartnersmanagesandoperatesmedicalgroupsandaffiliatedphysiciannetworksinCalifornia,Nevada,Florida,Arizona,andNewMexicoinitspursuittodeliverexcellent‐qualityhealthcareinadignifiedand compassionate manner. As of December 31, 2013, HealthCare Partners provided integrated caremanagementforapproximately765,000managedcarepatients.InitialInvestmentPitch:DaVitaisamarketleaderwitha33%shareofthedialysismarketintheU.S.Themarketalsoremainsstrongwith patient demand growing at 4‐5% per year. DVA’s kidney dialysis business remains stable and theacquisition of HealthCare Partners last year provides great growth opportunity given trends in the U.S.healthcare market. Integrated healthcare service providers should experience greater demand givenconcernsoverrisinghealthcarecosts;HCPiswell‐positionedtotakeadvantageofthisconsumershiftintheindustry.DaVita’s core business shows a commitment to social responsibility as they continuously promote earlychronickidneydiseasedetection,sustainablepractices,supportlocalcommunities,anddeliverqualitycare.DaVita’scompany‐widegreenpoliciesareparticularlystrong.Additionally,thelevelofcorporategivingtolocal communities, partnerships with non‐profits to provide dialysis care to underserved areas, anddonationsandvolunteereffortsatthecorporateandindividuallevelremainshigh.DivestmentRationale:DaVita’sfinancialscontinuetobestableanditcontinuestobeoneofthetopandlargestdialysisprovidersin the US. DaVita also presents a stable ESG story. However, a number of factors on the policy siderepresented strong headwinds for DVA. First, Medicare reimbursement rates are continuing to facedownwardpressure;DaVitahasbeenconcerned that lower reimbursement rateswouldhaveanegativeimpactonitsoperatingincome.Inaddition,uncertaintyaroundMedicareandMedicaidunderhealthcarereform signaled further ambiguity around DaVita’s service lines. Lastly, the performance of HealthCarePartners has yet to realize its potential. Following our analysis of the model, we determined growthopportunitiesatDaVitatobeappropriatelypricedintothestockprice.

21

Deere&Company(NYSE:DE) Sector:IndustrialGoodsIndustry:FarmandConstructionMachineryCompanyDescription:Deereoperatesinthreesegments:AgricultureandTurf,ConstructionandForestryandFinancialServices.TheJohnDeereAgricultureandTurfsegmentmanufacturesanddistributesalineofagriculturalandturfequipmentandrelatedserviceparts.JohnDeereconstruction,earthmoving,materialhandlingandforestryequipmentincludesabroadrangeofbackhoeloaders,crawlerdozersandloaders,four‐wheel‐driveloaders,excavators,motorgraders,articulateddumptrucks,landscapeloaders,skid‐steerloaders,logskidders,logloaders, log forwarders, log harvesters and a range of attachments. The John Deere Financial Servicessegmentprimarily finances salesand leasesby JohnDeeredealersofnewandusedagricultureand turfequipmentandconstructionandforestryequipment.InitialInvestmentPitch:Deerewassettocapitalizeuponthelong‐term,globalmegatrendsofpopulationgrowth,incomegrowthandrural‐to‐urban migration. By 2050, the world’s population is expected to reach 9 billion, which is anadditional2billionmouthstofeed.Globalconsumersinemergingmarketswillalsodemandmoremeatsastheirincomesriseovertime,whichinturnrequireshighergrainproduction.Tomeetthisgreaterexpecteddemandforfood,agriculturalproductionneedstoincreaseby70%,thevastmajorityofwhichwillcomefromyieldandproductivitygainsasopposedtoexpansionofnewfarmland.Theworldisalsoexpectedtowitnesscontinuedrural‐to‐urbanmigration.In2010,morethan50%oftheplanet’spopulationlivedincitiesforthefirsttimeinhumanhistory,andthatnumberisexpectedtohit70%by2050.AreducedruralworkforcewillleadtoanincreaseinmechanizedfarmingandtheuseofDeere’sproducts. Deere’s construction business is also poised to benefit from a boom in urban infrastructurespendingascitiesbuildnewbuildings,roadsandbridges.Becauseofthesemegatrends,Deerewasprojectingrevenueof$50billionin2018,upfrom$36billionin2012 (+38%). The greatest opportunity for Deere exists outside of the United States. Deere earnedapproximately1/3ofitsrevenuefromoutsideofNorthAmericain2010,andthecompanyisestimatingthatnumbertoincreaseto1/2ofitsrevenueby2018.DeereisfocusedonexpandinginBrazil,Russia,ChinaandIndiainparticular.FromanESGperspective,notonlydoesDeereprovideequipmentandservicesthathelpfeedtheworld,butitisalsocommittedtosafety,environmentandphilanthropy.ThecompanyisratedAAbyMSCI.DivestitureRationale:Thesectorhasdroppedasawholeinresponsetodeclininggrowthinkeyinternationalmarkets(primarilyChina), poor crop production and high production costs, and unfavorable effects of foreign currencyexchange.Whilepeerswerealsodownfrompreviousquarters,Deere’ssalesin4WDTractorandCombineshavedeclinedgreaterthantheindustryaverage. Tomanagethedownturnindemand,Deereunderwentsignificantlayoffsglobally.WhileanalystconsensusestimatesstillforecastedyearendresultsupfromQ3,ouranalysisofthemacroconditionsoutweighedthisrecommendationandwetookmotiontosellintermsofvaluationandESG.

22

DollarTree,Inc.(NASDAQ:DLTR)Sector:ServicesIndustry:Discount,VarietyStoresCompanyDescription:DollarTreeistheleadingoperatorofdiscountvarietystoresofferingproductsatthe$1.00pricepoint($1.25inCanada).ThecompanyoperatesstoresunderanumberofbrandsincludingDollarTree,Deal$,DollarTreeDeal$,DollarTreeCanada,DollarGiantandDollarBills.NotetheDeal$brandedstoresalsosellitemsforabovethe$1.00pricepoint.AsofNovember1,2014,DollarTreeoperated5,282storesin48statesandtheDistrictofColumbiaandfiveCanadianprovincesrepresentingatotalof45.8millionsquarefeet.Thecompany’sstoresarelocatedinabroadrangeofdiversegeographiesincludingmetropolitanareas,mid‐sizedcitiesandsmalltowns.InitialInvestmentPitch:DollarTreehasasignificantorganicgrowthopportunitywithpotentialforupto7,000storesintheU.S.and1,000storesinCanada.Uniteconomicsarehighlycompellingat>30%cash‐on‐cash.Thecompanyalsohasastronghistoryofpositivesame‐store‐salesbothduringandafterthedownturnasthecompany’suniquepositioningallowsittocaptureconsumerstradingdownaswellasincreasingsizeofbasket.Furthermore,DollarTree’shighlyflexibleorder‐by‐ordermerchandisingmodelallowsittobuytoitstargetmarginsandfacilitatea“treasurehunt”shoppingexperience.TherearealsomeaningfulgrowthopportunitiesthroughtheDeal$format,onlinechannel,add‐onacquisitionsandexistingstoreremodels/expansions.AlthoughDollarTree’sCSReffortsarenotmeaningfullydifferentiatedfromitsmasschannelcompetitors,thecompanyhasauniquepositioningasavalue‐orientedretailerandhashelpedgrowandsustainanewsegmentofretailfocusedoncreatingvalueforthelowerendofthemarket.DivestmentRationale:InFebruaryof2015thePrincipalsreviewedourinvestmentinDollarTree.Thefinancialscontinuetolookstrong,particularlyaftertheacquisitionofFamilyDollar.Synergiesresultingfromdistributionefficiency,improvedbuyingpower,andimprovedSG&Aindicatedstrongfinancialgrowthopportunities.However,thePrincipalsraisedconcernsoverthebleakESGpicture,especiallywhencombinedwithB‐ratedFamilyDollar.WhiletheoriginalESGthesisofprovidingaffordablegoodstolowerincomesegmentsstillholds,DollarTreewasfoundtolagcomparablesinenvironmental,social,andgovernanceaspects,withonlyminimaleffortsand very little transparency. The company has no reportable efforts to reduce its carbon emissions, isvulnerabletosupplychain labormanagement issues,andhasbeen foundtobe inviolationofworkplacesafetyregulationsin3states.InlightoftheweakESGstory,thePrincipalsdecidedtodivestfromDollarTreeinFebruary2015atapriceof$76.78.

23

Ecolab(NYSE:ECL)Sector:ProducerDurablesIndustry:ChemicalsCompanyDescription:Ecolab Inc.provideswater,hygiene,andenergy technologiesandservices forcustomersworldwide.Thecompanyoperates in foursegments:GlobalIndustrial,GlobalInstitutional,GlobalEnergy,andOther.TheGlobalIndustrialsegmentprovideswatertreatmentandprocessapplications,andcleaningandsanitizingsolutionsprimarilytolargeindustrialcustomerswithinthemanufacturing,foodandbeverageprocessing,chemical,miningandprimarymetals,powergeneration,pulpandpaper,andcommerciallaundryindustries.The Global Institutional segment offers specialized cleaning and sanitizing products to the foodservice,hospitality,lodging,healthcare,governmentandeducation,andretailindustries.TheGlobalEnergysegmentprovidestheprocesschemicalsandwatertreatmentneedsofthepetroleumandpetrochemicalindustriesinbothupstreamanddownstreamapplications.TheOthersegmentofferspestelimination,andkitchenrepairandmaintenanceservices.Thecompanysellsitsproductsthroughcompany‐employedfieldsalespersonnel,healthcare distributors, and dealers. Ecolab Inc. was founded in 1923 and is headquartered in St. Paul,Minnesota.EcolabInc.operatesasasubsidiaryofAthlonSolutions,LLC.InitialInvestmentPitch:

GlobalMarketLeaderinwater,hygiene,energytechnologiesandservicesthatprovideandprotectcleanwater,safefood,abundantenergyandhealthyenvironments;

FavorableSecularTrends:Globalpopulationgrowth,resourcescarcityandindustrializationacrosstheworld;

Growth Strategy: Organic (innovation and customer base expansion) and acquisition (Nalco,Champion);

Diversification:Business lines includecleaningandsanitizing;pestelimination;equipmentcare;watertreatment;paper;andenergy;

ReasonableValuation:ForwardP/Eof22.3x(attimeofinitialpitch;currently–24.0x)isslightlyabovehistoricalaveragebutupsideisstillattractive;

ESGLeader:Asagloballeaderincleaning,foodsafety,healthprotection,andtheindustrialwaterand energy sectors, ECL has incredibly strong ESG activities that are core to its business andoperations. ECL’s corporate responsibility work focuses on economic progress, environmentalstewardship,socialresponsibility,andsafetyacrossanumberofbusinesssegments.

DivestureRationale:While ECL continues to lead its industry – both financially and in terms of ESG – it faces severemacroeconomicheadwinds,includingloweroilandgas(O&G)pricesandexplorationactivityandrevenueweightedindepreciatingcurrencies,thatarecoretoECL’sgrowthstrategies(O&Gexplorationandemergingmarkets).Further,ECLisalreadypricedgenerously.TheupdatedHSRIFvaluationofECL–whichrelieson(somewhatoptimistic)assumptionsatthemidpointofmanagementguidance–hasdeclinedtolessthana5%premiumonECL’scurrentshareprice–inlinewiththepricetargetsofmostindustryanalysts.HSRIFcertainlyenjoyeditsECLride,butthisspringwasanopportunetimetoexit.

24

Mylan(NYSE:MYL)Sector:HealthcareIndustry:Drugs–GenericCompanyDescription:Mylan Inc., a Pennsylvania‐based global pharmaceutical company, develops,manufactures,markets, anddistributesgenerics,brandedgenerics,andspecialtypharmaceuticals.Thecompanycurrentlyhas42first‐to‐fileAbbreviatedNewDrugApplicationspending,which,accordingtoIMSHealth,representsanestimated$25.4 billion in annual brand sales.While the company has a large and diverse portfolio of over 1,200pharmaceuticals some of its target disease areas includeHIV/AIDS, diabetes, cancer, hepatitis, allergies,chronicobstructivepulmonarydisorder,andotherinfectiousdisease.Mylan’smissioncentersonprovidingaffordableaccesstopharmaceuticalsandtargetsthosediseaseareasthathavelargepatientpopulationsinhigh‐andlow‐incomecountries,helpingtocontaincostsandimprovehealthworldwide.InitialInvestmentPitch:MylaniscurrentlyataninflectionpointasithasacquiredAgila,theinjectablesunitofStridesAcrolab,FamyCare, and the generics unit of Abott, and has forged strong partnerships with Biocon, India’s topbiotechnologyfirm.Thesemovespositionthecompanytodevelopbiosimilars,anemergingareaofgenericstargeting chronic disease and requiring capabilities in biotechnology. Biosimilars promise significantdemand frompatients strugglingwith thehigh costof insulin,heart treatments, andother largeproteintherapies.As a stableplayer in genericswith aproven record innavigating regulatoryhurdles,winningpatentlitigations,andsupportinglarge‐scaleglobalhealthinitiatives,MylanisastrongfinancialandsocialinvestmentfortheFund.DivestureRationale:The principals voted to divest fromMylan based on an ESG risk that its productsmay be used in drugcocktailsforlethalinjectionsanditssharepricerisingtofairvalue.Mylancontinuestoofferarobustportfolioofgenericpharmaceuticalproductswhilepursuingnewfilingsandbiosimilaropportunities,butitspricemetourtargetandourupdatedmodelsuggeststhatthestockistradingatfairvalue.InadditionMylanhasmetsignificantnegativepressaftertheStateofAlabamaannouncedthatitmightusethecompany’srocuroniumbromidecompoundinitslethalinjectioncocktails.Recuroniumbromideisamusclerelaxantthatisnormallyusedasapartofanesthesiaduringsurgicalprocedures,butitcanbeusedduringexecutions.WhilethereisnoevidencethattheStateofAlabamahasprocuredthedrugforthispurpose,Mylanhasrefusedtoexplicitlyadopt measures to prevent procurement of its products for execution. This is a step that many otherpharmaceuticalcompanieshavealreadytaken.

25

PepsiCo,Inc.(NYSE:PEP)Sector:ConsumerStaplesIndustry:Food,Beverage,andTobaccoCompanyDescription:PepsiCo,Inc.isaglobalfood,snack,andbeveragecompanywithadiverseproductportfolioincluding22brandsthatgeneratesmorethan$1billioninannualretailsales.Thecompany’sproductscanbefoundinmorethan200countriesaroundtheglobeandincludeleadingbrandssuchasPepsi‐Cola,MountainDew,Lays,Gatorade,andTropicana.ThecompanyoperatesfourbusinessunitsincludingPepsiCoAmericasFoods,PepsiCo Americas Beverages, PepsiCo Europe, and PepsiCo Asia, Middle East, and Africa. The companyoriginallyincorporatedin1919.PepsiCocompetesprimarilyonthebasisofprice,quality,productvariety,anddistribution.Thecompanyfocusesitseffortsonmanufacturing,marketing,anddistributingitsproductsinthreeseparatecategories:“fun‐for‐you,”“better‐for‐you,”and“good‐for‐you.”InitialInvestmentPitch:Pepsicoisastronginvestmentopportunitywithgrowthpotential.Astheglobalmiddleclassgrows,demandfor the company’s products will significantly increase, along with global appetite for its newer line of“healthy”offerings.Thecompanyhasanattractivevaluation,returnssignificantcashtoinvestors,andfacesrelativelyinelasticdemand.FromonESGperspectiveseniorleadershiphaspursuedanumberof“sharedvalue”initiatives,andthecompanyhasasizablecharitablegivingprogram.DivestitureRationale:InSeptemberof2014thePrincipalsreviewedourinvestmentinPepsiCo.Thecompanyhasbeenpursuinggrowthinemergingmarketsandhaspostedstablerevenuegrowthoverthelastfewyears.However,thestockhadfarexceededitsoriginalpricetargetof$78.Alsoatthereview,Principalsraisedconcernsaboutthe company’s ESG strategy in terms of a businessmodel primarily focused on unhealthy foods, watermanagement,andrecentcontroversiessurroundingitspalmoilandsugarsourcingpolicies.Therearealsosomereportsthatthecompany’ssharedvalueinitiativeshaveprovenunprofitableandmaybescaledback.InlightofthecontroversialESGstoryandreachingfairvaluation,thePrincipalsdecidedthatPepsihasrunits course for the fund anddivested from the stock inNovember2014 at aprice of 96.63/share. Itwaspurchasedin2011at$63.10/share.

26

Salesforce.com,Inc.(NYSE:CRM) Sector:InformationTechnologyIndustry:InternetSoftwareandServicesCompanyDescription:Salesforce.com,Inc.isaproviderofenterprisecloudcomputingservices.TheCompanyisdedicatedtohelpingcustomersofallsizesandindustriesworldwidetransformthemselves into “customer companies” by empowering them to connectwith their customers, partners,employeesandproducts inentirelynewways.TheCompanyprovidescustomerswiththesolutionstheyneedtobuildanextgenerationsocialfrontofficewithsocialandmobilecloudtechnologies. InitialInvestmentPitch:Salesforce,whichsellsCustomerRelationshipManagement(CRM)software,operateswithinafast‐growingsegmentofthesoftwareindustry.ExpectedannualgrowthoftheCRMsoftwaremarketis15%through2017whenitreaches$36billioninannualsales.Salesforcehasexhibitedstronggrowthwithrevenuesgrowingthe previous three years greater than 30% year‐over‐year YoY. Salesforce’s acquisition of ExactTargetprovidesstrongsynergiesandsolidpartnerindigitalmarketingandanalytics.FromanESGperspectiveSalesforcerunstheSalesforceFoundationthattoutsthe1/1/1Pledge.Thegoalofthisprogramistodonate1%ofSalesforce’sequity,1%ofemployees’timeand1%ofSalesforce’sproductsto improving communitiesaround theworld. Since inception theprogramhasgivenover$53million ingrants,580,000hoursofcommunityservice,andprovidedproductdonationsforover20,000nonprofits.Salesforcealsoencouragesothercompaniestotakethe1/1/1pledge.MSCIhasmaintainedtheirratingofAforSalesforcewithnocontroversieswithinanycategories.DivestitureRationale:ThestockhasbeenbeatingexpectationsthelasttwoquartersbutstillremainsinEPSnegativeterritory.OurinitialinvestmentthesisprojectedstrongrevenuegrowthandthatCRMwouldbecomethemarketleader;CRMhasbeenabletoreachthesetargetsbutnowfacesanextremelysaturatedmarketwheretheonlywaytogrowistodevelopnewproductswhichwillputastrainonmarginsgoingforward.CRMhashadagreatrunbutafterreachingallthemilestoneswehadsetinourinvestmentpitchin2013webelievethisisanexcellentmomenttoexitthepositionsincethereisonlylimitedpotentialappreciationforHSRIF.

27

WhiteWaveFoods(NYSE:WWAV)Sector:ConsumerStaplesIndustry:Food‐DairyProductsCompanyDescription:TheWhiteWaveFoodsisaleadingconsumerpackagedfoodandbeveragecompanyfocusedonhigh‐growthproductcategoriesthatarealignedwithemergingconsumertrends.Theymanufacture,market,distribute,and sell branded plant‐based foods and beverages, coffee creamers and beverages, premium dairy andorganicgreensandproduceproductsthroughoutNorthAmericaandEurope.TheirproductsincludeSilk,InternationalDelight,HorizonOrganic,EarthboundFarm,andLand‐O‐LakesinNorthAmericaandAlproinEurope.InitialInvestmentPitch:WhiteWavewasoriginallypitchedasastockwithexcellentgrowthopportunitiesarisingfromhighdomesticpenetration inarapidlygrowingmarket.Plant‐basedbeveragesandmorebroadly,organicproducts,areseeingdemandrise innearlyallmarkets.WhiteWavealreadyrunsahouseofbrands thatcater to thesemarketsandsaleswillincreasewithdemand.InadditiontoorganicgrowthinNorthAmericaandEurope,WhiteWaverecentlymadeinroadsintoChinawithajointventurewithamilkproducer.ThisfootholdinoneofthefastestgrowingeconomieswillprovideWhiteWavewithexcellentsalesopportunitiesnowandwellintothefuture.WhiteWave’smission is to “change theway theworld eats for the better by providing consumerswithinnovative, great‐tasting food and beverage choices that meet their increasing desires for nutritious,flavorful,convenientandresponsiblyproducedproducts.”FromanenvironmentalperspectiveWhiteWavetracks and attempts to reduce greenhouse‐gasses,waste andwater usage. Socially they encourage theiremployeestoparticipateintheirvolunteeringprogramwith98%ofemployeesparticipating.DivestmentRationale:OurinvestmentinWhiteWavewentextremelywellforthefund.WeenteredthepositiononMay9th,2014atanaveragepriceof$29.13.ThestockperformedextremelywellovertheholdingperiodandweexitedonMarch16th,2015atapriceof$41.85.Thisrepresentsaholdingperiodreturnof43.6%andanannualizedreturnof51.1%.Thiswasatoughpositiontoexit;WhiteWavehadperformedextremelywellforthefundandwe thoroughly agreedwith their ESG story.Whenwe ran themodel though,we found the growthopportunities tobeappropriatelypriced into thepriceof thestockandweexitedbecausethemarginofsafetywenormallylookfornolongerexisted.

28

NEW POSITIONS

AmericanWaterWorksCompany,Inc.(NYSE:AWK) Sector:UtilitiesIndustry:WaterUtilitiesAmericanWaterWorksisthelargestpubliclytradedwaterandwastewaterutilitycompany,asmeasuredbyoperatingrevenueandpopulationserved.Itprovides14millionpeoplewithdrinkingwater,wastewater,andotherwater‐relatedservicesinover40statesandtwoCanadianprovinces.Thisinvestmentprovidesportfoliodiversification,bothbyaddinganewindustrytotheportfolioandbyaddingastockwithaverylowBeta (0.33 as ofMarch 2015), providing stability for some of themore volatile portfolio positions. Thecompanyoffersattractiverisk‐adjustedreturnwithlimiteddownside.AWK’sregulatedbusinesssegment(whichmakesup89%ofAWK’soperatingrevenue)hashighbarrierstoentry,alargeandgeographicallydiversecustomerbase,andapredictablemarketduetoeconomicregulation.Thecompanyseemsfocusedonthoughtfullyconsideringandpreparingforriskstothesustainabilityoftheirbusiness,includingeffortstoreducegreenhousegasemissionsanddevelopinfrastructuretoimproveconservationofwaterintransittohomesandbusinesses.AWKalsohasamorediverseleadershipteamthanmanyothercompaniesofitssize,withseparateCEOandChairmanroles,afemaleCEOandCFO,anda44%femaleBoardofDirectors.The company’smission toprovideaccess to cleandrinkingwater forboth low‐ andhigh‐incomepeoplealignswellwiththeFund’ssocialimpactgoals.AMNHealthcareServices(NYSE:AHS) Sector:HealthcareIndustry:SpecializedHealthServicesAMNHealthcareprovidesworkforcesolutionsandstaffingservicestopublicandprivatehospitals,clinics,communityhealthcenters, andotherhealthcareworkplacesaround the country.AMNprimarily recruitsnursesandphysicians,althoughitalsoprovidesplacementservicesforotheralliedhealthprofessionalssuchasphysicaltherapists,homehealthaides,etc.Beyondbasicrecruitingandplacement,AMNoffershealthcarefacilities holistic workforce management support through its consulting practices. It helps healthcarenetworks identify their optimal staffing mix that allows for the least complexity and highest level ofefficiency, coordinates all workforce vendor management, implements professional development andupskillingprograms,anddevelops/implementselectronichealthrecordssystems.ByofferingasuiteofservicesAMNHealthcareattractsanumberofclientstoitsManagedServiceProgram(MSP)inwhichitmanagesandpurchases100%ofstaffingservicesforitsclients.Thismodelisparticularlylucrativeforthecompanyasitreceivesfeesforcontractingandmanagingvendorsandforprovidingdirecthiresfromitsownnetwork.Thecompanyalreadyhas100ofthesecomprehensiveMSPrelationships,whichismorethananyotherfirmintheindustry.AccordingtoStaffingIndustryAnalysts,AMNHealthcarehasover10%ofthemarketshareforhealthcarestaffing,whichisgreaterthananyofitscompetitors.TheFundboughtintoAMNbasedonseculargrowthtrends,thecompany’sdifferentiatedmodelanditsESGstrengths.Demandforhealthcarestaffingservicesisexpectedtoincreasegreatlywithincreasedspendingonhealthcareand theprojectedshortfallofnursesandphysicians. AMNprides itselfasan innovator inhealthcare workforce solutions and differentiates itself from competitors through its MSP, vendor

29

management systems, and recruitmentprocessoutsourcingofferings. AMNalsohasa strongESGstory,playingapivotalroleinhelpingtomanageandreducecostsatpublicandprivatehealthcarefacilities.Inaddition, it has a female CEO, female representation on the board, strongworkplace policies, and solidreportingproceduresinplace.

Disney(NYSE:DIS) Sector:CommunicationsIndustry:MediaTheWaltDisneyCompany,togetherwithitssubsidiariesandaffiliates,isaleadingdiversifiedinternationalfamilyentertainmentandmediaenterprisewithfivebusinesssegments:medianetworks,parksandresorts,studioentertainment,consumerproductsandinteractivemedia:

‐ Disney’smedianetworksportfoliocomprisesavarietyofhighmarginhouseholdnamescoveringfamily,children’s,andsportsentertainment.ABC,ESPN,andtheDisneyChannelarethestandoutnames.

‐ Theparksandresorts business isperhaps themost famous, including fiveworld‐classvacationdestinationswith11themeparksand44resorts inNorthAmerica,EuropeandAsia,withasixthdestinationcurrentlyunderconstructioninShanghai.WDP&RalsoincludestheDisneyCruiseLinewithits fourships‐theDisneyMagic,DisneyWonder,DisneyDreamandDisneyFantasy;DisneyVacation Club, with 12 properties and approaching a total of 200,000 member families; andAdventuresbyDisney,whichprovidesguidedfamilyvacationexperiencestodestinationsaroundtheglobe.

‐ Studio entertainment refers predominantly to Disney’s behemoth film business. The division’ssignificantscaleallowsittobringthecreative,distribution,andfinancefunctionsin‐house.Majorstudios owned by Disney includeWalt Disney Animation Studios, Pixar, Marvel, Lucasfilm (StarWars),andTouchstonePictures(Dreamworks).

‐ Theconsumerproductsportfoliocomprisesavastrangeofretailproducts,fromtoystofineart.Thedivisionissplitintothreeparts–licensing,publishing,andDisneyStore.

‐ ProductsandcontentreleasedandoperatedbyDisneyInteractiveincludeblockbustermobileandconsolegames,onlinevirtualworlds,andNo.1‐rankedwebdestinationsDisney.comandtheMomsandFamilynetworkofwebsites.

DIS isapowerfulgrowthstockwithconsiderablemarketshare inagrowing industry.Thecompanyhasconsistentrevenueandmargingrowthalongwithaprovenabilitytogeneratefreecashflow.Managementhas stated clearly its intent to return at least 20%of this cash flow to investors throughdividends andbuybacks.MajorcatalyststosharepriceappreciationforDISincludethescheduledopeningofShanghaiDisneylandinDecember2015,ablockbusterfilmpipelinefeaturingtwonewStarWarsepisodes,andkeycontractwinsforitsESPNbusiness.DISisamarketleaderindiversity,notonlythroughworkplacepoliciesbutinadedicationtodiversitywithinitscreativecontent.Further,thecompanyisveryactiveinthecommunitythroughwhatitcalls ‘strategicphilanthropy’.DIShashadsomecontroversiesinthepastregardingthesupplychainofitslicensedproducts.Thefirm’sprogressinthisareahasbeenrewardedwithinclusionintheCalvertSocialIndex.

30

KeyCorp(NYSE:KEY) Sector:FinancialIndustry:Regional–MidwestBanksKeyCorp, headquartered in Cleveland, Ohio, is the nation’s 15th largest bank‐based financial servicescompany,withconsolidatedtotalassetsofapproximately$92.9billionatDecember31,2013.KeyCorpistheparentholdingcompanyforKeyBankNationalAssociation(“KeyBank”),employingover14,000acrossitstwomajorbusinesssegments:KeyCommunityBankservingover2millionindividualsandSMEsthroughits12statebranchnetwork;andKeyCorporateBank,a full‐servicecorporateand investmentbankservingprimarilymiddlemarketclients.TheFundfoundthiscompanycompellingdueto its forecasted financialgrowthanddiversificationtoourportfolio. Undertheleadershipofoneofthemostpowerful females infinance, BethMooney, the firm has successfully achieved results in reducing costs, improving customerservicesthroughtheintroductionofmobilebankingsolutions,diversifyingrevenuethroughitsexpansionofnoninterest revenueorganically and through the acquisition of Pacific Crest Securities. With aportfoliosensitivetointerestrates,themacroconditionsareripeningforrevenuetospike,counteredbyESGresultsingoodstridealthoughunder‐ratedbyMSCIasaresultofseverallawsuitsthefirmissettling.

Nucor(NYSE:NUE)Sector:BasicMaterialsIndustry:Steel&IronNucorCorporationisthelargeststeelproducerintheUnitedStatesandthelargestrecyclerofscrapsteelinthecountry.Itisthe14thlargeststeelcompanyintheworldbyproductionvolume(4thbymarketcap).Itrecyclesaboutonetonofsteeleverytwosecondsandhasrecycledover12milliontonssofarthisyear.Nucorusesadistinctiveelectricarcfurnace(EAF)processtousescrapsteelasaprimaryinputforitsproductionprocess. Nucor was the first company to use EAF in small decentralized “mini‐mills” and proved thatdecentralization steel production couldwork at scale.WhenNucor firstmade a transition to using EAFproductioninmini‐millsinthe1960s,itwasabletoquicklyrespondtochanginglocaldemandindozensofdifferentlocalmarkets.AsNucorhasgrown,ithasleveragedthissameflexibilityforlargeandinternationalmarkets.Nucor currently operates about 23 scrap‐basedproductionmills, andhas traditionally had thehighestmarginsintheindustry.In addition Nucor has displayed an ESG turnaround. In 2002 Nucor ranked Nucor as the 14th largestcorporate contributor to U.S. air pollution in 2002. Since then it has embraced a strong environmentalprogram,trainingforstaff,andfurtherenhanceditsscraprecyclingcapabilities.By2010thecompanyhadmovedtothe69thpositionafterhavingreduceditsreleaseofairtoxinsbyover65%whilestillmaintainingand/orincreasingproductionvolumes.Nucorpresentsastronglong‐termopportunityforthefundbasedonitsupwardESGtrajectory,diversifiedproductmix,flexibleproductionandlabormanagementpractices,andverticalintegration.

31

Qualcomm(NYSE:QCOM) Sector:TechnologyIndustry:CommunicationEquipmentQualcommis the innovatorofCDMAtechnology, thebackboneofall3Gwirelessnetwork.Thecompanydesigns, manufactures and markets digital communications products and services including integratedcircuitsandsystemsoftwareused inmobiledevicesand inwirelessnetworks.TheCompanyoperates inthreesegments,includingQualcommCDMATechnologies(QCT),QualcommTechnologyLicensing(QTL)andQualcomm Strategic Initiatives (QSI). QTL provides rights to use portions of its property portfolio. QCTdevelops and supplies integrated circuits and system software wireless technologies. Finally, the QSIsegmentisfocusedonopeningnewopportunitiesforitstechnologies.ThefundbelievesthatQualcommwillbe a strong addition to the HSRIF portfolio, as the company is not only an eminent force in thecommunicationstechnologyspace,buthasastrongESGcorporateculturewithacompany‐widefocusonsustainability.Itsstrategydriveslong‐termgrowthandprofitabilitythroughtheinclusionofenvironmental,socialandcorporategovernanceissuesinitsbusinessmodel;specificallyastheyrelatetokeyspheresofinfluence: its workplace (with focus on inclusion, and diversity), supply chain and local communities(includingaccessibilitytotechnologyandeducationalimpactonminoritiesandwomeninSTEMfields),aswellasthemarketplaceandpublicpolicyrealm.

Stericycle(NASDAQ:SRCL) Sector:IndustrialGoodsIndustry:WasteManagementStericycle, Inc., together with its subsidiaries, provides compliance solutions to the healthcare andcommercial businesses. The company’s main business activity comprises the collection and disposal ofmedicalwaste.Stericycleservesadiversecustomerbaseofnearly599,000customersthroughouttheUS,Argentina,Brazil,Canada,Chile,Ireland,Japan,Mexico,Portugal,Romania,SouthKorea,Spain,andtheUK.Thecompanysplitsitscustomerbaseintotwocategories:SmallQuantity(SQ)andLargeQuantity(LQ)accounts.LQsaredefinedasproducing200+pounds/monthofmedicalwaste.LQstendtobehospitals,nursinghomes,largeclinicsandlabsamongothers.SQstendtobedentists,privatedoctorspractices,andveterinariansamongothers.Inadditiontothecoreregulatedmedicalwastemanagementservices,Stericycleoffersahostofservicesthatcomplementitsmainbusiness.Suchservicesincluderecallsupport,liveandautomatedcustomerservice,sharpsmanagement,andspecialistcompliancetraining.TheFundboughtintoStericyclegivenitsmarketleadershipintheUnitedStates,diversifiedandstickyclientbase,wellfoundedplansforinternationalexpansion,underappreciatedcross‐sellingopportunities,andthepowerful secular tailwinds that it faces. Stericycle also provides the Fund with fresh exposure to thehealthcare industrywithout the risks associatedwith patent battles anddrugdiscovery. The company’sbusinessactivitiesofferimmediate,inherentbenefittotheenvironmentviaminimizationanddiversionofwaste as well as energy efficiency, and furthermore, Stericycle is an industry leader in supply chainmanagement.

32

TEConnectivityLtd.(NYSE:TEL) Sector:TechnologyIndustry:DiversifiedElectronicsTEConnectivity,headquarteredinSwitzerland,isthelargestplayerintheconnectorindustry,andalargeplayerinthesensorindustry.Atahighlevel,theirproductsconsistofconnectors,sensors,fiberoptics,circuitprotection,sealingandprotection,antennas,relays,precisionwireandcables,andwireless.Wechosethisinvestmentduetomacrotrendsofferingupsidetothecompanyinthefuture,thecompany’sleadingpositioninahighlyfragmentedmarket,strategicmovestoimprovemargins,expectedfuturestrategicacquisitionsthatwill increasemarket shareandbringsynergies, anda strongESGstory.Thecompany is focusedonproductlineswhoseaddressablemarketweexpectwillgrowdramaticallyinthenextfewyears.Thoughatechnologycompanyatfirstglance,TELalsoprovidesportfoliodiversification,asitsmainmarketsegmentistransportation.TEL’sproductsenableitscustomerstomeetthedemandsforsafer,greener,smarter,andmore connected products. This has allowed for more fuel‐efficient automobiles, energy‐efficient datacommunications,andsaferindustrialvehicles.Thecompanyhasreduceditsowngreenhousegasemissions,waterusage,andhazardouswasteproductionsignificantlysince2010,andreceivedCisco’sExcellenceinSustainabilityawardin2014.TheEthisphereInstitutenamedTELoneofthemostethicalcompaniesin2015.TorontoDominionBankGroup(NYSE:TD) Sector:FinancialServicesIndustry:MoneyCenterBankTorontoDominionBank(TDBank)isCanada’ssecondlargestbankbymarketcapitalizationandlargestbankbyassets.TDBankhasthreekeybusinesslines:Canadianretailbanking,U.S.retailbanking,andwholesalebankingwiththebulkof itsrevenuesgenerated inCanadianretailbanking.TDBankanditssubsidiariesserve approximately 22million customers in Canada and theUnited States. TDBank provides personalbanking, credit card, auto financing, small business and commercial banking, corporate and specialtybanking,insurance,research,investmentbanking,andcapitalmarketservices.Overthepastseveralyears,TDBankhasdevelopedandexecutedaretail‐focusedstrategy.TDBankexiteditsstructuredproductsbusiness,non‐franchisecreditproductsbusiness,anditsnon‐franchiseproprietarytradingbusinessbetween2005and2010.Theretail‐focusedstrategyhasresultedinalowerriskbusinessmodel,andhasincreasedthecompany’sfocusoncustomerservice.Inadditiontocustomerservice,TDhasmadeprovidingfinancialliteracy,access,andeducationtotheunderservedpopulations,suchasindigenouspopulations,oneofitssocialmissions.

33

UnitedNaturalFoods(NYSE:UNFI) Sector:ServicesIndustry:FoodWholesaleUnitedNaturalFoods,Inc.isadistributorofnatural,organic,andspecialtyfoods and relatedproducts includingnutritional supplements, personal care items andorganicproduce.UNFIhasover40,000customersacrossbuyingclubs,conventionalsupermarkets,massmarketchains,andother foodservice companies, primarily in the U.S. and Canada. The company operates 33 distributioncenters,representingabout7.2millionsquarefeetofwarehousespace,whichrepresentsthelargestcapacityof anyNorthAmerican‐baseddistributor in thenatural, organic, and specialty products industry.HSRIFbelievesthatUNFIisastrongadditionfrombothafinancialandESGperspective.Thecompanyhasastrongtrackrecordasthemarketleaderinarapidlygrowingindustry,withsalesgrowthaveraging15%overthepast10years.Withstrongcustomerrelationships,arobustdistributionnetwork,andahistoryofsuccessfulacquisitionstheyarepoisedtocontinuegrowingwiththeirmarket.UNFIplaysinanindustrywithrapidgrowthandthinmargins;asthebiggestplayer,morethantwicethesizeoftheirnearestcompetitor, thecompany stands to benefit significantly from increasing economies of scale with growth. From an ESGperspective,UNFI’scorebusinesssuccessisalignedwithpromotionofhealthylifestyles,creatingsocialgoodfortheircustomers.Beyondthecorebusiness,UNFIishighlyconsciousofcorporatesocialresponsibility,withaparticularfocusonenvironmentalsustainability.

VodafoneGroupPlc(NASDAQ:VOD) Sector:TelecomIndustry:WirelessTelecomVodafoneGroup(VOD)isawirelesstelecommunicationscompanyheadquarteredintheUKwithoperationsin30countriesandpartnershipswithnetworksinanadditional48countries.ItistheUK’smostvaluablebrand,currentlyworthUSD$30billionaccordingtoBrandFinanceGlobal500.Theworld’ssecondlargesttelecom,VODserves434millionmobile customersaround theworldand is typically the firstor secondlargestoperator(outof3‐4)withineachofthemarketsinwhichitoperates.90%ofmobilecustomersareindividuals,withtherestbeingenterprisecustomersrangingfromsmallbusinessestolargemultinationals.Themajorityof–andagrowingshareof–Vodafone’smobilecustomersareinemergingmarkets.Thecompanyrecentlyexpandedintofixedbroadbandandnowprovidesservicesto9.3millioncustomersin17differentmarkets.ItsprimarymarketforfixedservicesisEuropewhereitisthefourthlargestproviderinWesternEuropeandwillbecomethethirdpendingitsacquisitionofOnoinSpain.Vodafonereachescustomersthrough14,500exclusivebrandedstores,whichincludefranchises,anetworkofdistributionpartnersaswellasthirdpartyretailers.Onlineisbecominganincreasinglyimportantchannelforsalesandaftersalesservicesforthecompany.

34

ACCOMPLISHMENTS Every yearpresentsnewopportunities to grow theFund in adiversenumberofways. The2014‐2015academicyearhascontinuedthispractice.TheFund’skeyaccomplishmentsduringtheperiodincludethefollowing:I. FormalizedCRBFundingFormula.Theprincipals,NadjaGuensterandrepresentativesfromthe

CenterforResponsibleBusiness(CRB)agreedthataformalizedprocedurefortheannualwithdrawalfromthefundwouldinboththefund’sandCRB’sbestinterest.WeconsideredtheneedsoftheCRBaswell as the bestway tominimize a negative impact on the fund. The agreementwas that thewithdrawalwouldtakeplaceeachyearonJune30thorthenextclosestbusinessday.Theamountofthewithdrawalwouldbe fourpercent (4%)of the fund’s20‐quarteraverage total accountvaluecalculatedasofMarch30thofeachyear.ThiswouldgivebothpartiesampletimetoplanaroundtheamountofmoneyleavingthefundandenteringtheCRB’sbudget.Itistheresponsibilityofthefundprincipalstoensurethatmoneyisearmarkedforthiswithdrawaleachyear.

II. Recruiting. The principals redesigned and formalized the Fund’s recruiting process this year to

ensure that thatFund continues to attract and accepthigh caliber studentswith adiverse set ofexperiences.PrincipalsagreedthatprincipalsoftheFundshouldexemplifythefollowingtraits:

Anexpressedpassionforfinanceandsocially‐responsibleinvesting Anabilitytobeprovenwrongandacceptcriticism Anabilitytooperatewellinalargedecision‐makinggroup Entrepreneurialattitude—anagentofchange Self‐motivation InterestinadvancingtheFund

Based on these traits and a select set of critical skills, the principals created an application andinterview process to assess interested candidates. The principals reviewed over 30 writtenapplications,interviewed20+candidatesinpersonbasedonaninitialscreen,andwelcomed8newprincipalsintotheFund.Everycandidatewhoreceivedaninvitationtojointhegroupacceptedtheoffer,whichtheFundviewsasamarkerofsuccessandsignalofitsstandingintheHaascommunity.ThePrincipalsareveryexcitedaboutthesuccessofourlatestrecruitingeffortsandlookforwardtocontinuingtobuildontheFund’ssuccessintheupcomingyears.

III. Onboarding.TheClassof2015Principalsimplementedamorestructuredonboardingprocessfor

theincomingPrincipalsthisyear.Inthepast,2ndyearPrincipalstaught1styearPrincipalshowtousetheeValmodelinpreparationforpositionupdatesandlongpitches.However,thisyearweaskedProfessorRichardSloan,instructorofFinancialInformationAnalysis,toteachhisproprietarymodelto us. Additionally, we implemented weekly Macro Updates and weekly ESG Updates to allowPrincipals tohaveabetterunderstandingof themarket, its impactonourportfolio,andtoallowPrincipals to explore ESG topics of interest. We also outlined the entire semester’s worth ofmeetings/classtimesinadvanceof thesemestertoprovideampletimeinplanningforpreparingpositionupdatesandlongpitches.

IV. Visits to Parnassus andMSCI. On Friday November 21st, the fund principals travelled to San

Francisco to visit Parnassus Investments andMSCI. Thiswas an opportunity not only to discussinvestmentstrategieswithindustryprofessionals,butalsoto introducethenewly‐appointedfirstyearprincipalstothefundandtheworldofSRI.

35

Our first appointmentwaswithBenAllen of Parnassus.BenisthePortfolioManageroftheParnassusCoreEquityFund and a Haas alum. The discussion was centeredpredominantlyonBen’sinvestmentstyleandhowhefindsvalueusingfinancialandESGanalysis.Wediscussedanumberofspecificholdings,someofwhicharecommontoBen’sfundandourownSRIfund.Wealsodiscussedwiderportfoliomanagementtheoryandcareersintheindustry.WethenmovedontomeetwithSebastianBrinkmannatMSCI.Sebandhisteam took us through an in‐depth ESG analysis of our portfolio and thesensitivitiesourholdingshavetokeylevers.Thisallowedtheprincipalstonotonlygetabetterappreciationofourportfolio’sESGperformance,butalsotobetterunderstandMSCI’sratingmethodology.

V. VisittoSolarCity.InApril2015,theHSRIFPrincipalsvisitedSolarCity’sheadquartersinSanMateo,CA.WearrangedforameetingwithChiefFinancialOfficer,BradBuss.Only7monthsintohistenureasSolarCity’sCFO,BussgaveaspiriteddescriptionofhisreasonsforjoiningCFO,despiteturningdownanoffertobecomeCFOofGooglein2005).Duringthisonehourmeeting,thePrincipalsaskedcandid questions about the future of SolarCity, macro trendsimpacting thecompany,andBuss’vision for the future.BussalsosharedhisbullishviewonSolarCity’s stock,his relationshipwithElonMusk, andadescriptionofdemanding,but rewarding,workenvironmentatSolarCity.

VI. RebalancingProcedures.FollowingalengthydiscussionbetweenBenAllenofParnassusandthe

principals,weelectedtoemploya1/nrebalancingmethodologytothefund.Theprimaryreasonisthat,as long‐terminvestors,wedonotconsiderourselves tradersormarket timers.Further,ourrenewedfocusonsectordiversificationmeansthatwearenowwell‐diversifiedwithoutneedingtoadjustourindividualholdingstobalancesectorexposure.Rebalancingtakesplaceattheendofeachsemesterandattheendofeachstockupdateornewpitchperiod.CRBwithdrawalsaresubtractedpriortorebalancingandheldincash.

VII. ConferencesAttended.