©2015, college for financial planning, all rights reserved. session 8 zero, constant, and non-...

TRANSCRIPT

©2015, College for Financial Planning, all rights reserved.

Session 8Zero, Constant, and Non-Constant Dividend Discount Model (DDM), Valuation Scenario

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMInvestment Planning

Session Details

Module 4

Chapter(s)

2

LOs 4-2 Explain terminology related to equity investment valuation models.

4-3 Calculate the intrinsic value of a stock using various stock valuation techniques or calculate the expected return of a stock.

4-4 Evaluate the appropriateness of investment decisions based on stock valuation models.

8-2

Required Return (r)

)βr(rrr fmf

8-3

Expected Return

gP

DE(r)

1

8-4

Constant Growth DDM

gr

DV

1

8-5

Dividend Growth Rate (g)

g ROE RR

8-6

Valuation Approaches

• Dividend Discount Model

• Price/Earnings Ratio

• Price/Book Ratio• Price/Sales Ratio• PE/Growth (PEG)

Ratio

8-7

Valuation

• The determination of what a stock is worth; the stock's intrinsic value

• If the valuation exceeds the price, buy the stock.

• If the valuation is less than the price, do not buy or short the stock.

8-8

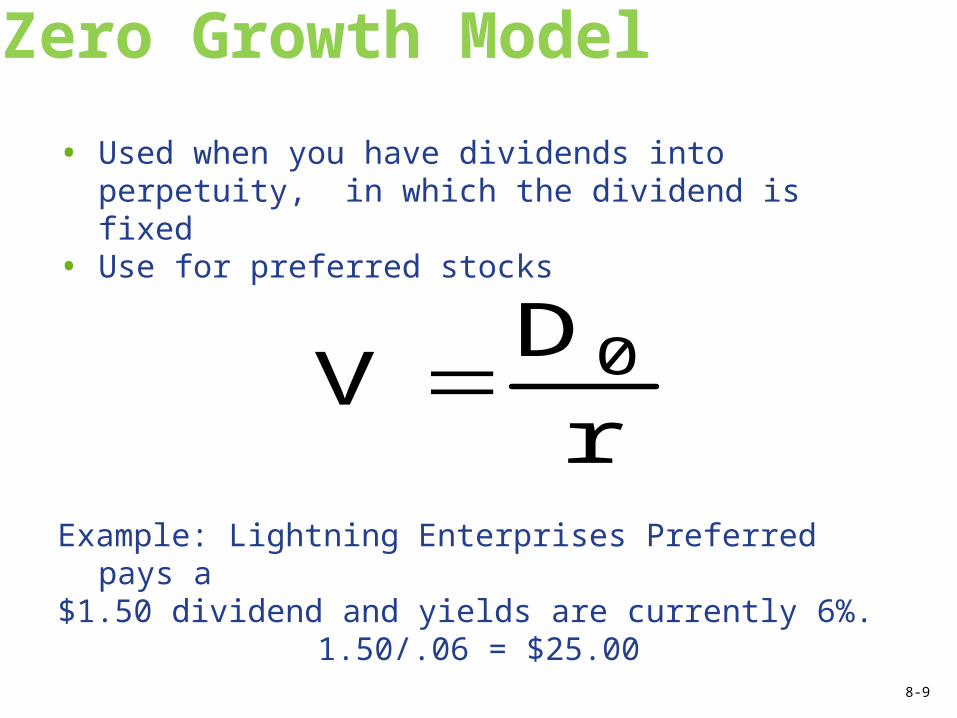

Zero Growth Model

• Used when you have dividends into perpetuity, in which the dividend is fixed

• Use for preferred stocks

Example: Lightning Enterprises Preferred pays a

$1.50 dividend and yields are currently 6%.1.50/.06 = $25.00

r

DV 0

8-9

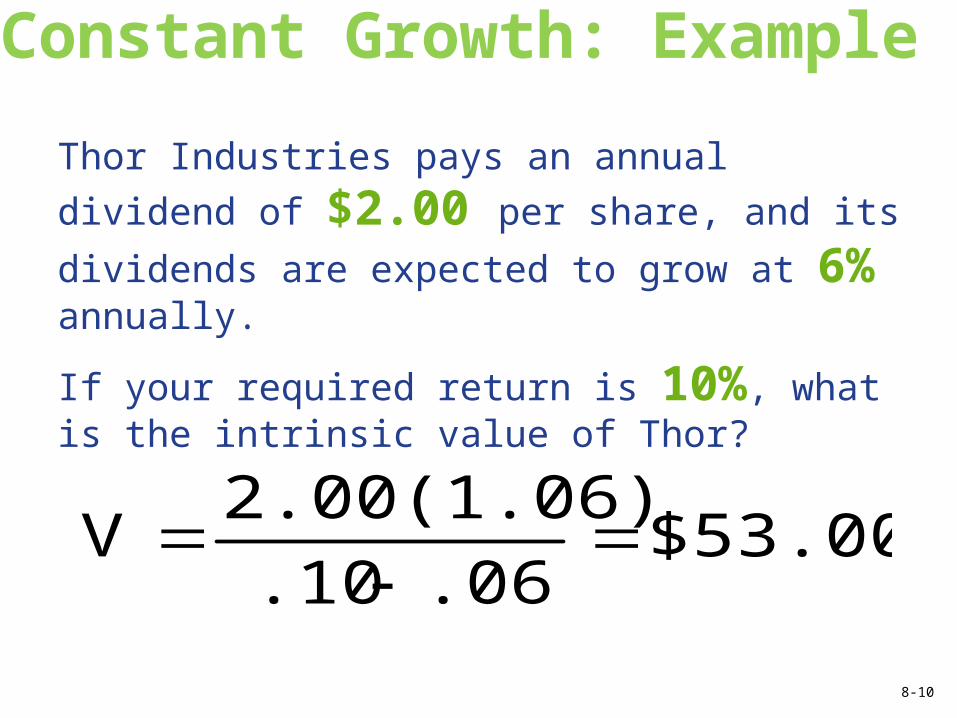

Constant Growth: Example

Thor Industries pays an annual dividend of

$2.00 per share, and its dividends are

expected to grow at 6% annually.

If your required return is 10%, what is the intrinsic value of Thor?

$53.00.06.10

2.00(1.06)V

8-10

Constant Growth: Example

Fair Market Value

Relative Value Action

Less than $53 Undervalued Buy

$53 Fairly valued Buy

Greater than $53 Overvalued Do not buy or sell short

8-11

Expected Return

10.24%.1024.0650

2.00(1.06)E(r)

10%.10.0653

2.00(1.06)E(r)

9.79%.0979.0656

2.00(1.06)E(r)

8-12

Valuation Scenario

Stock VIP sells for $50 and pays an annual dividend of $3.00; its dividends are expected to increase by 3% annually. The stock has a beta of .85. The required rate of return on the market is 10%, and the risk-free rate is 5.5%.a. What is the investor’s required rate of return?

= 5.5 + (10 – 5.5) .85 = 5.5 + 3.83 = 9.33%

)βr(rrr fmf

8-13

Valuation Scenario

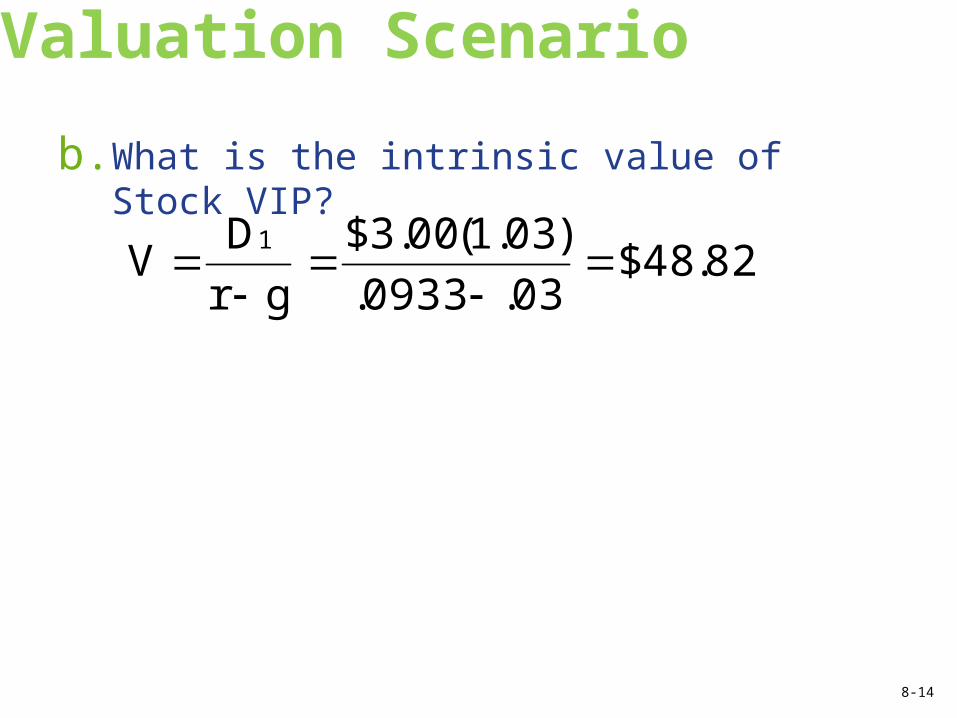

b. What is the intrinsic value of Stock VIP?

82.48$03.0933.

)03.1(00.3$

gr

DV

1

8-14

Valuation Scenario

c. What is the expected rate of return on Stock VIP?

= $3.09 + .03 $50

= 9.18%

1DE(r) g

P

8-15

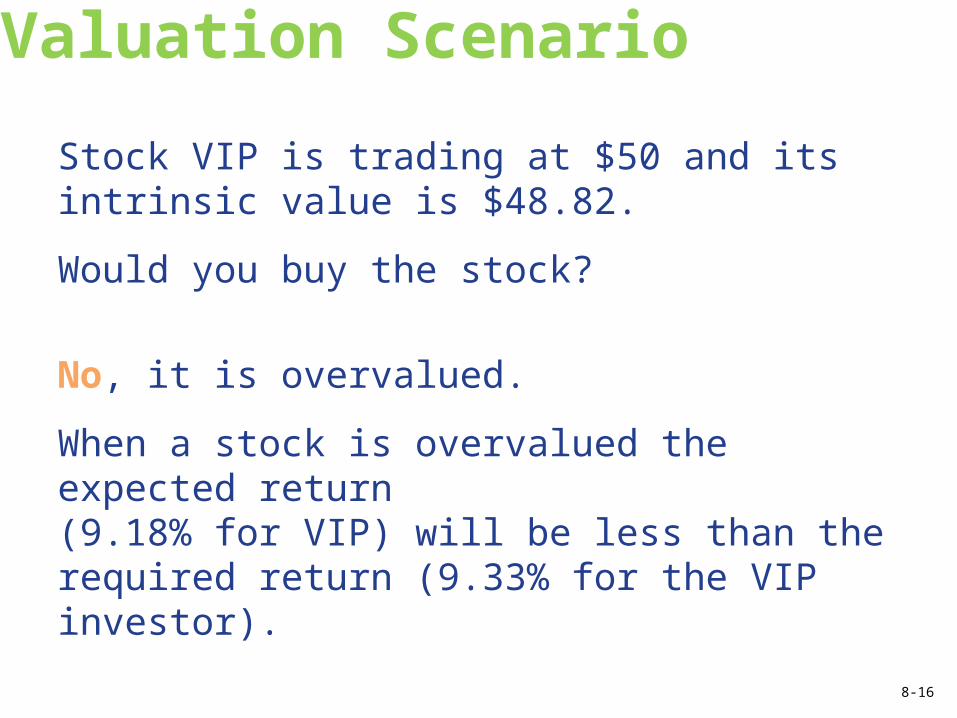

Valuation Scenario

Stock VIP is trading at $50 and its intrinsic value is $48.82.

Would you buy the stock?

No, it is overvalued.

When a stock is overvalued the expected return (9.18% for VIP) will be less than the required return (9.33% for the VIP investor).

8-16

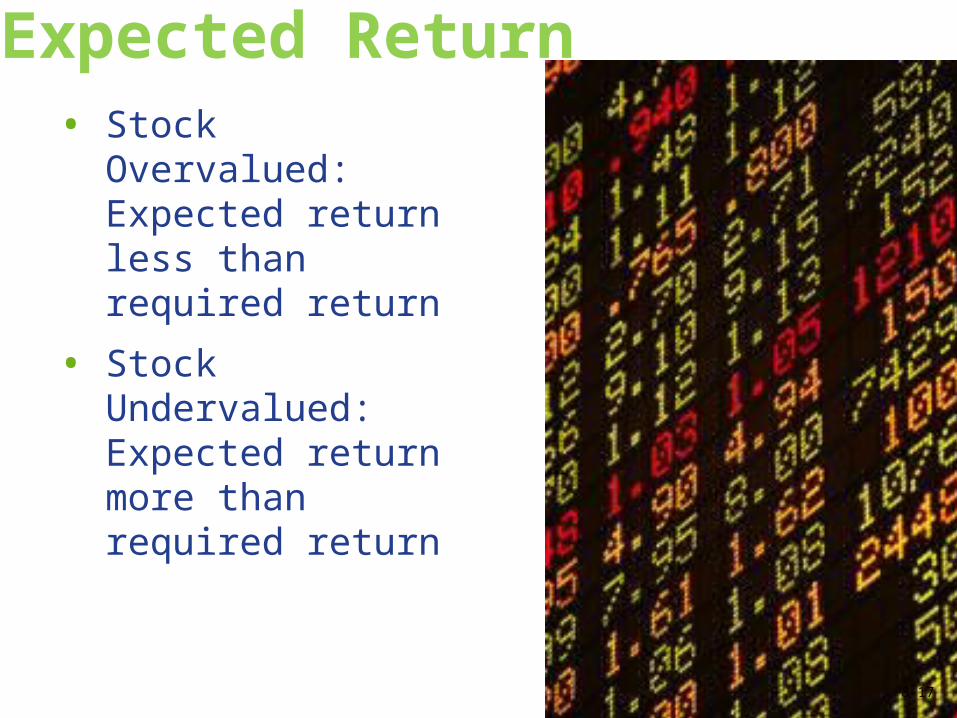

Expected Return• Stock Overvalued:

Expected return less than required return

• Stock Undervalued:Expected return more than required return

8-17

Non-Constant Growth DDM• Uses more than one growth rate, with a higher

growth rate initially, and then a lower rate as the company matures

• Calculation requires the use of the cash flow key (CFj) on the financial calculator

Note: With HP12c, always use the CFo key first, then the CFj key.

8-18

Non-Constant Growth DDM Calculation

Travis is interested in buying a stock that currently pays a dividend of $0.60 cents per share annually. His required return on investments is 9%. The dividend is expected to grow 15% annually for the next two years,

followed by an expected growth rate of 6% thereafter.

What is the most that Travis should pay for the stock?

Step 1: Find the amount of the dividend at the end of each of the two years of the non-constant growth:

0.60 x 1.15 = 0.690.69 x 1.15 = 0.7935

8-19

Non-Constant Growth DDM Calculation

Step 2: Find the value of the stock at the end of Year 2 based on the dividend to be paid at the end of Year 3 (constant growth):

0.7935 (1.06) = $28.04 0.09 - 0.06

Step 3: Using the calculator, solve for the PV of unequal cash flows using the timeline.

8-20

Non-Constant Growth Timeline

8-21

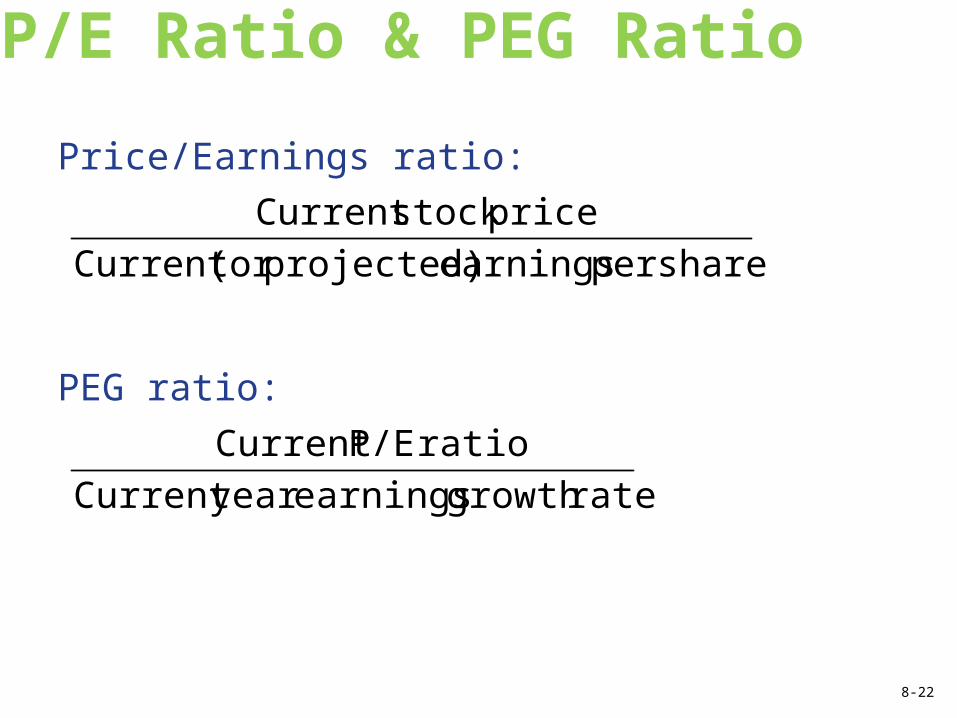

P/E Ratio & PEG Ratio

Price/Earnings ratio:

PEG ratio:

shareperearningsprojected)(orCurrent

pricestockCurrent

rategrowthearningsyearCurrent

ratioP/ECurrent

8-22

PSR & P/B Ratio

Price to Sales ratio:

Price to Book ratio:

shareperSales

pricestockCurrent

sharepervalueBook

pricestockCurrent

8-23

Question 1

If the risk premium in the CAPM equation for a stock decreases, what is the likely consequence of the valuation of the stock when the dividend growth model is used to compute its value?a. The stock’s value will increase.b. The stock’s value will not change.c. The stock’s value will decrease.d. The risk premium is not relevant to the

CAPM.

8-24

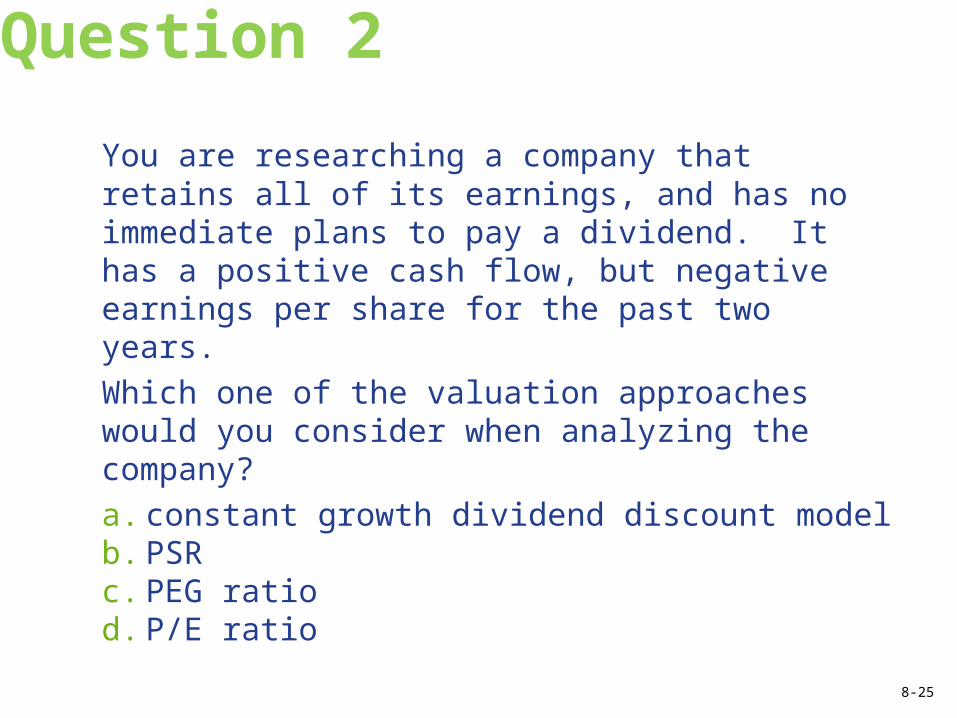

Question 2

You are researching a company that retains all of its earnings, and has no immediate plans to pay a dividend. It has a positive cash flow, but negative earnings per share for the past two years. Which one of the valuation approaches would you consider when analyzing the company?a. constant growth dividend discount modelb. PSRc. PEG ratiod. P/E ratio

8-25

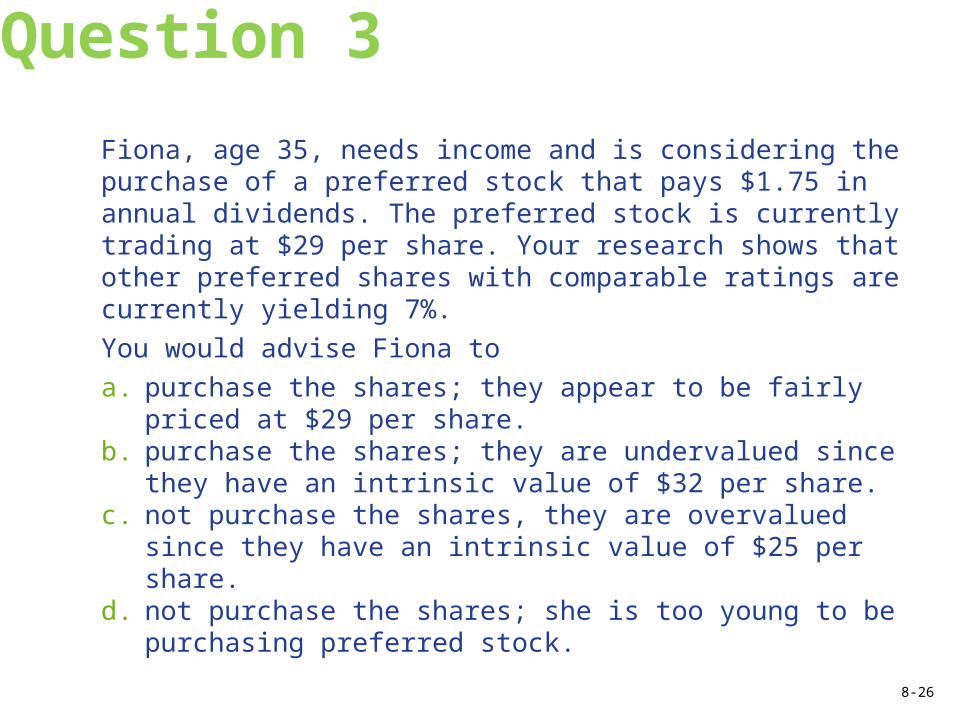

Question 3

Fiona, age 35, needs income and is considering the purchase of a preferred stock that pays $1.75 in annual dividends. The preferred stock is currently trading at $29 per share. Your research shows that other preferred shares with comparable ratings are currently yielding 7%.

You would advise Fiona to

a. purchase the shares; they appear to be fairly priced at $29 per share.

b. purchase the shares; they are undervalued since they have an intrinsic value of $32 per share.

c. not purchase the shares, they are overvalued since they have an intrinsic value of $25 per share.

d. not purchase the shares; she is too young to be purchasing preferred stock.

8-26

Question 4

Your client is considering a purchase of Titan Industries, and you are helping the client evaluate the stock. This past year the company earned $3.00 a share, and paid out 25% of its earnings as dividends. Titan expects both dividends and earnings to grow at 5% for the foreseeable future, and it expects the payout ratio to remain at 25%. Your required rate of return is the current 10-year Treasury note rate of 6%, plus a risk premium of 6%.What is the intrinsic value of Titan Industries?a. $11.25b. $28.55c. $45.00d. $78.75

8-27

Question 5

You are evaluating Retro Holdings, Inc., for a possible purchase. Last year it paid $1.00 in dividends, and you expect the dividend to grow at a rate of 12% for the next three years, and then grow at 6% thereafter. Your required return is 9%. What is the maximum amount you should pay for the stock?a. $35.33b. $41.50c. $45.22d. $47.86

8-28

Question 6Echo Echo Inc. sells for $79 per share and pays an annual dividend of $2.48. The price and dividend is expected to increase by 5% annually.

Using the constant growth dividend discount model for valuation, and assuming an investor has a required rate of return of 8%, which of the following are true statements?

I. The expected rate of return is greater than the required rate of return.

II. The expected rate of return is less than the required rate of return.

III. The stock is undervalued.IV. The stock is overvalued.

a. I and II onlyb. I and III onlyc. I and IV onlyd. II and III only

8-29

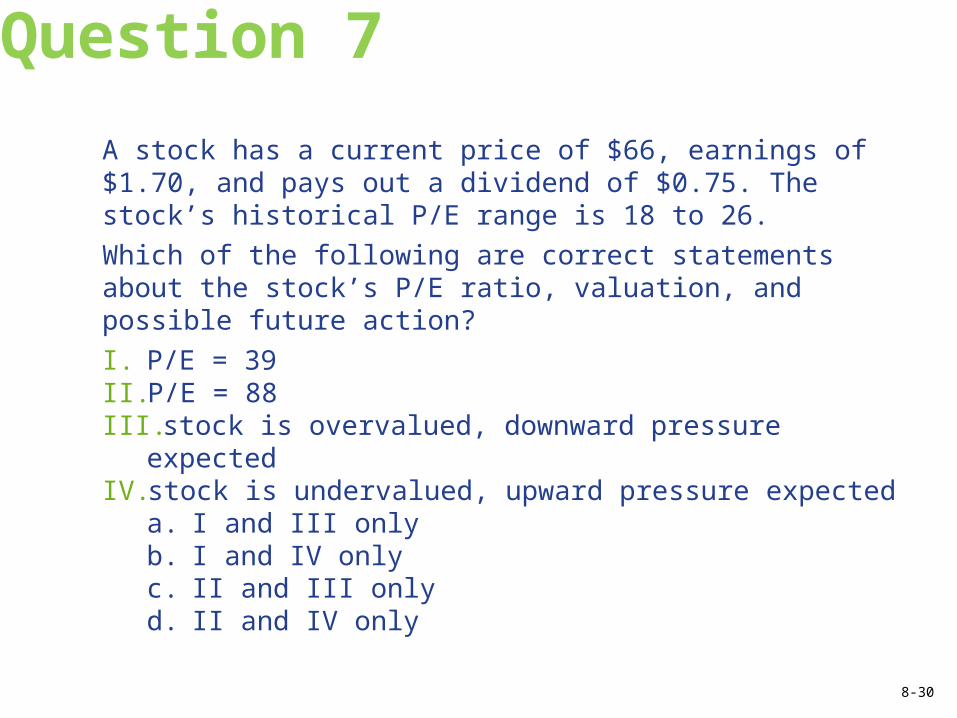

Question 7

A stock has a current price of $66, earnings of $1.70, and pays out a dividend of $0.75. The stock’s historical P/E range is 18 to 26.

Which of the following are correct statements about the stock’s P/E ratio, valuation, and possible future action?

I. P/E = 39II. P/E = 88III. stock is overvalued, downward pressure expectedIV. stock is undervalued, upward pressure expected

a. I and III onlyb. I and IV onlyc. II and III onlyd. II and IV only

8-30

©2015, College for Financial Planning, all rights reserved.

Session 8End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMInvestment Planning