201409 nedbank group 2014 interim results … aug 14 nedbank gdp growth ... 93 95 96 98 00 02 04 06...

TRANSCRIPT

NEDBANK GROUP LIMITED

INTERIM RESULTSINVESTOR PRESENTATION

for the six months ended 30 June 2014

2

-2

0

2

4

6

00 02 04 06 08 10 12 14

1,8%

3,22,6

1,8

0

2

4

6

Aug13

Feb14

Aug14

Nedbank GDP growth forecast

SA macro environment deteriorated further over the past 6 months

GDP growth slowing (% annual)

Forward rate agreements point to flatter rate cycle

2014 GDP expectations revised downward

Prime increases later than expected

Global & local economy remains volatile, uncertain, complex & ambiguous

Source: Nedbank Group Economic Unit

8

9

10

11

12 13 14 15 16 17

H1 2014 resultsFYE 2013 results

Prime rate forecast (%)

4

8

12

16

00 02 04 06 08 10 12 14

Actual 3-month JIBARImplied market forecast - currentImplied market forecastsImplied market forecast (31 Jan 2014)

2,5%1,2%

- historic

3

Wholesale credit growth improves while consumers remain under pressure Credit growth: corporates vs households

Source: Nedbank Group Economic Unit

Consumers remain under pressure

…but, insolvencies & liquidations still muted

-6

-2

2

6

10

00 02 04 06 08 10 12 14Consumer spending: q-o-q % changeHousehold disposable income: q-o-q% change

100

200

300

400

0

200

400

600

00 02 04 06 08 10 12 14Insolvencies Liquidations

Insolvencies (12-m mov avg) Liquidations (12-m mov avg)

-10

-5

0

5

10

15

20

25

30

35

40

00 02 04 06 08 10 12 14

Households

Corporates

Credit growth (%)

4

0

200

400

600

800

93 95 96 98 00 02 04 06 08 10 12 14

Private sectorPublic sector

Medium-to-long term opportunities from the National Development Plan (SA) & Rest of Africa

Source: Nedbank Group Economic Unit

GDP growth forecasts from IMF, robust for RoA(%)

Trade flows SA to Africa (Rbn), Africa as % of SA exports

Nedbank large SA capital project schedule (R billion - constant 2014 prices)

R3 trillion potential by

2030

The 2014 figure (*) is value of projects announced in the first half of the year – annualisedNote: R3 trillion potential announced projects sourced from 2013 Budget Review document

-2

0

2

4

6

8

10

00 02 04 06 08 10 12 14 16 18

Sub-Saharan AfricaSouth Africa

10

12

14

16

18

20

0

40

80

120

160

00 02 04 06 08 10 12

SA exports to Rest of Africa (LHS - Rbn)Rest of Africa contribution (RHS - %)

Debt ratingsNedbank local & foreign currency & SA Sovereign

Nedbank Moody’s, Fitch, S&P

SA SovereignMoody’s, Fitch, S&P

Ratingsgrade

A1, A+, A+ A1, A+, A+Upper medium

gradeA2, A, A A2, A, AA3, A-, A- A3, A-, A-

Baa1 (↓), BBB+, BBB+ Baa1 (↓), BBB+, BBB+Lower medium

gradeBaa2, BBB (↓), BBB Baa2, BBB (↓), BBBBaa3, BBB-, BBB- Baa3, BBB-, BBB-

Ba1, BB+, BB+ Ba1, BB+, BB+ Non-investment grade

↓ indicates negative ratings agency outlook, all others stable

*

5

9 39

7

10 1

28

11 1

43

12 1

80

13 5

96

2010 2011 2012 2013 2014

Nedbank Group: consistent focus on drivers of value creation

212 26

5 340 39

0 460

2010 2011 2012 2013 2014

12,2

13,7

15,8 16,1 16,5

14,2

13,0 13,1 13,0 13,5

2010 2011 2012 2013 2014

ROE (excl GW) Cost of equity

NAV per share(cents)

ROE & Cost of Equity (%)

Interim dividend per share(cents)

NAV ROE > COE

11,6%

EP

Dividends

17,9%

Underpinned by strong CET1, surplus liquidity & high coverage

H1 H1 H1

6

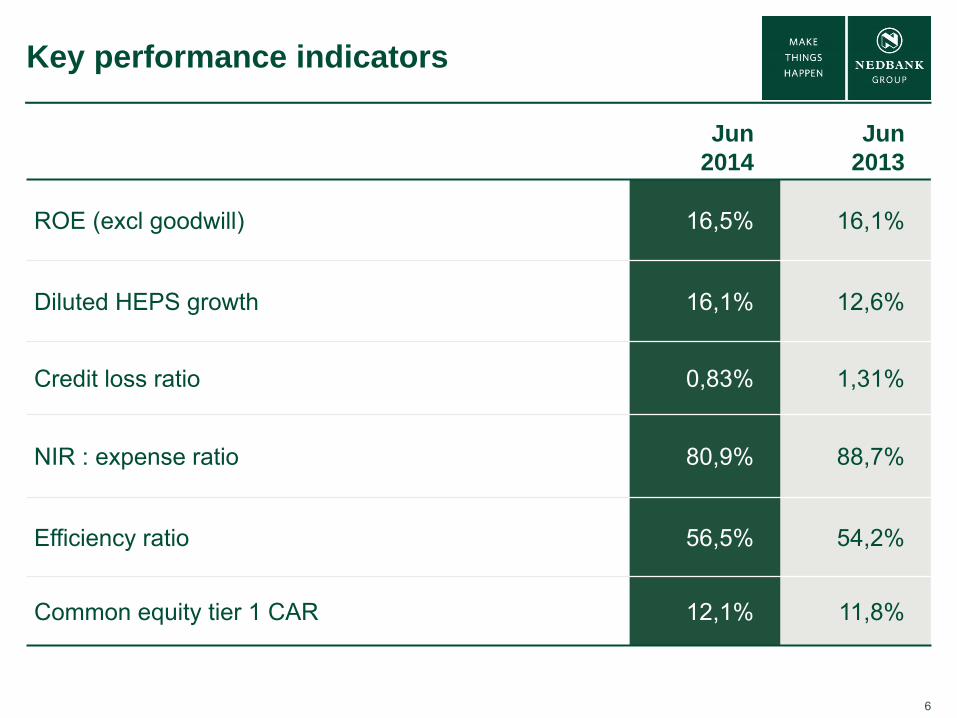

Key performance indicators

Jun2014

Jun2013

ROE (excl goodwill) 16,5% 16,1%

Diluted HEPS growth 16,1% 12,6%

Credit loss ratio 0,83% 1,31%

NIR : expense ratio 80,9% 88,7%

Efficiency ratio 56,5% 54,2%

Common equity tier 1 CAR 12,1% 11,8%

7

3 914 4 599

954

992

55

962 244

H12013

NII Impairments NIR Expenses Direct tax &other

H12014

9,3% 29,8% (0,6%) 8,9%

Headline earnings growth drivers

Headline earnings (Rm)

17,5%

8Graph excludes the impact of H1 2013 base effects & slowdown in client transactional activity in the challenging macro-economic environment

NIR growth reflects impact of strategic choices

9 4419 515

9 843

126

H1 2013excl. FV

H1 2014excl. FV

PLs slowdown& credit life

Maintainfees at

2013 level

H1 2014 excl. FV &adj. for strategic

actions

0,8%

2,1%1,3%

Credit lifepricing & benefits

PL volumedecrease

4,2%

…NIR-to-expense ratio at 80,9% (MLT target >85%)

202

NIR (Rm)

9

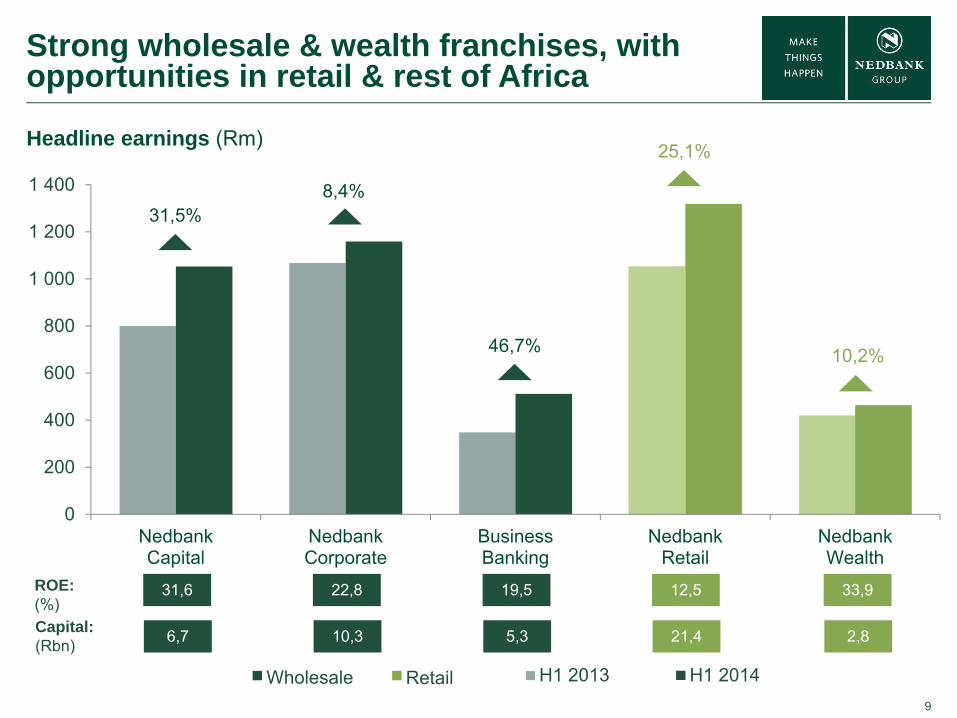

Strong wholesale & wealth franchises, with opportunities in retail & rest of Africa

0

200

400

600

800

1 000

1 200

1 400

NedbankCapital

NedbankCorporate

BusinessBanking

NedbankRetail

NedbankWealth

H1 2013 H1 2014

Headline earnings (Rm)

Wholesale Retail

31,5%8,4%

46,7%

25,1%

10,2%

ROE:(%)

31,6 22,8 19,5 12,5 33,9

Capital:(Rbn) 6,7 10,3 5,3 21,4 2,8

10

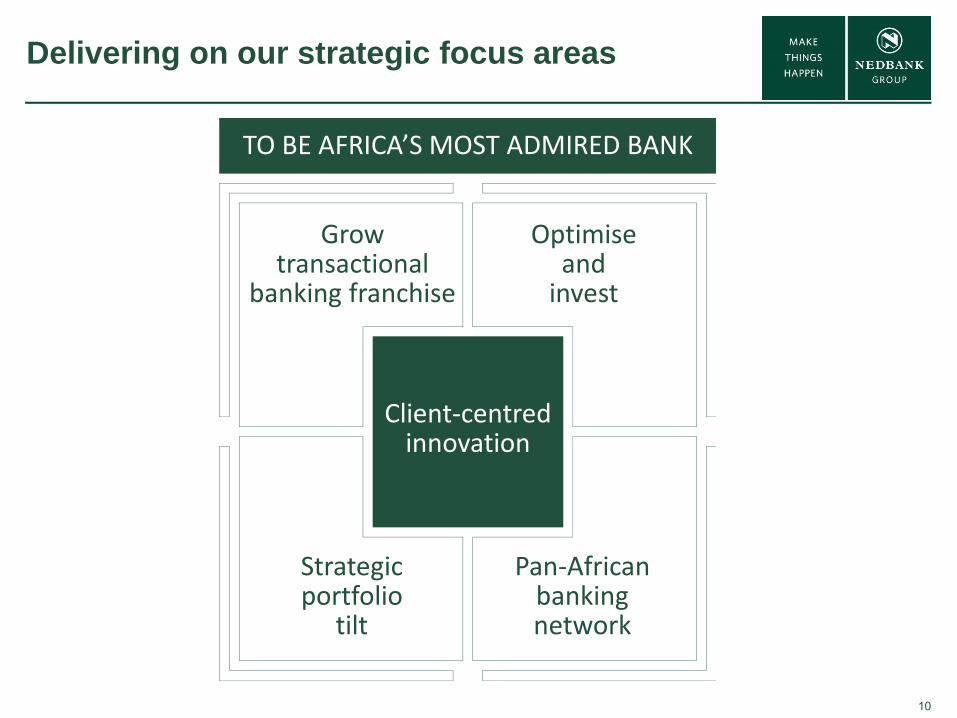

Delivering on our strategic focus areas

TO BE AFRICA’S MOST ADMIRED BANK

Client‐centred innovation

Grow transactional

banking franchise

Optimiseandinvest

Strategic portfolio

tilt

Pan‐African banking network

11

Client-centred innovation

Aug12

Dec12

Apr13

Aug13

Dec13

Apr14

Aug12

Dec12

Apr13

Aug13

Dec13

Apr14

App suite downloads‘000

Secure Approve-it transactions# million

Digitally enabled clients‘000

Award for Innovation in

Banking2014

Corporate payment system revenuesMonthly average

Netbank Business volumesMonthly average

10 11 12 13 H114

10 11 12 13 H114

H110

H111

H112

H113

H114

12

4,45,0

5,86,4

6,9

2010 2011 2012 2013 2014

Total clients(m)

Grow transactional banking franchise

Continued client growth across all clusters

Source: 1. Client groups with GOI greater than R500pm, 2. Brand Finance (calculated in Rand), 3. Millward Brown, Nielsen Adex

H1

Investment in footprint expansion since 2009 ATMs up 83% Staffed outlets up 41% Intelligent Depositor devices up 100%

Investment in integrated channels & mobile

Benefits from ‘Branch of the Future’

Kept transactional fees at 2013 levels

Progress in ELB & youth clients migrating to middle market

Focus on cross-sell & collaboration

Increased marketing spend & effectiveness

Brand value2 R12,5bn up 15% from 2013 & advertising share of voice3 increased to 24% (H1 2013: 20%)

1,92,2 2,3

2010 2013 2014

Retail main banked clients (m)

H1

Business Bankingclient groups1 (‘000)

21,723,8 24,8

2010 2013 2014

Initiatives to unlock future growth

H1

13

Grow transactional banking franchise

(#000) (Rm)

Card

Trans-actional

Secured

PersonalLoans

306 335 380

1 247 1 405 1 519

1 726 1 851

1 907

522 612 456

2012 2013 2014

4 203 4 262

418 402

332

2012 2013 2014

6 6556 164

+8,0%

+10,2%

5 5933 801

PersonalLoans1

Total retail client base NIR

Retail exclPersonalLoans1

H1 H1

+11,3%+10,0%

6 3235 762

5 175

1 single product clients2 total growth excluding personal loans

Total

Total

+1,4%+10,6%

+6,0%2

+9,5%2

Retail client & NIR growth influenced by risk appetite & pricing choices

14

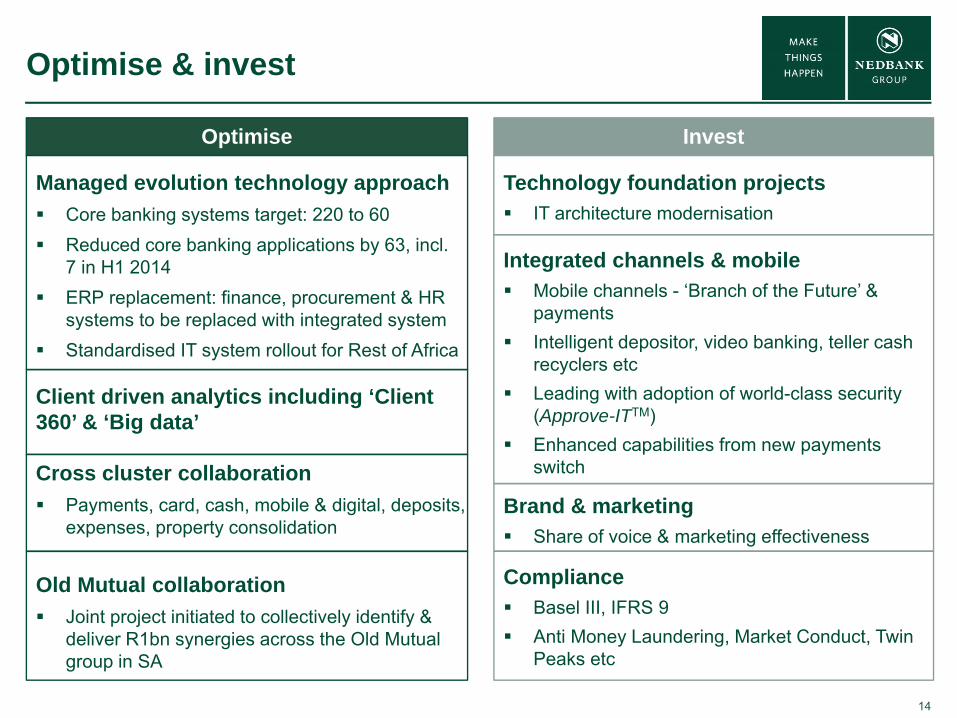

Managed evolution technology approach Core banking systems target: 220 to 60 Reduced core banking applications by 63, incl.

7 in H1 2014 ERP replacement: finance, procurement & HR

systems to be replaced with integrated system Standardised IT system rollout for Rest of Africa

Client driven analytics including ‘Client 360’ & ‘Big data’

Cross cluster collaboration Payments, card, cash, mobile & digital, deposits,

expenses, property consolidation

Old Mutual collaboration Joint project initiated to collectively identify &

deliver R1bn synergies across the Old Mutual group in SA

Optimise & invest

Optimise Invest

Technology foundation projects IT architecture modernisation

Integrated channels & mobile Mobile channels - ‘Branch of the Future’ &

payments Intelligent depositor, video banking, teller cash

recyclers etc Leading with adoption of world-class security

(Approve-ITTM) Enhanced capabilities from new payments

switch

Brand & marketing Share of voice & marketing effectiveness

Compliance Basel III, IFRS 9 Anti Money Laundering, Market Conduct, Twin

Peaks etc

15

Strategic portfolio tilt

Wholesale1 advances growth ahead of retail(% growth2)

Faster advances growth in attractive EP areas(% growth2)

Greater capital deployed to Rest of AfricaEconomic capital (Rbn), % of Group

Slower advances growth to protect against downside risk (% growth2)

-10

-5

0

5

10

10 11 12 13 14

Retail advancesWholesale advances

Notes: 1. Wholesale includes Nedbank Corporate & Nedbank Capital2. Growth reflects 6 monthly growth

-10

0

10

20

30

10 11 12 13 14

Home loans

Personal loans

0

5

10

15

10 11 12 13 14

Commercial propertyCredit cardVehicle finance

0,9 0,91,8 2,1

2,92,2 2,0

3,6 3,74,6

-1

1

3

5

7

10 11 12 13 14

Economic capital

% of Group OSE

H1

16

Strategic portfolio tilt

CLR (%)

0,620,42

0,46

0,56

0,40 0,37

0,060,07

H12013

H22013

H12014

Personal loans methodology changes

First Strut

Personal loans

Rest of the group

1,31

0,82 0,83

Credit loss ratio improved off a high base to the lower end of the CLR range

17

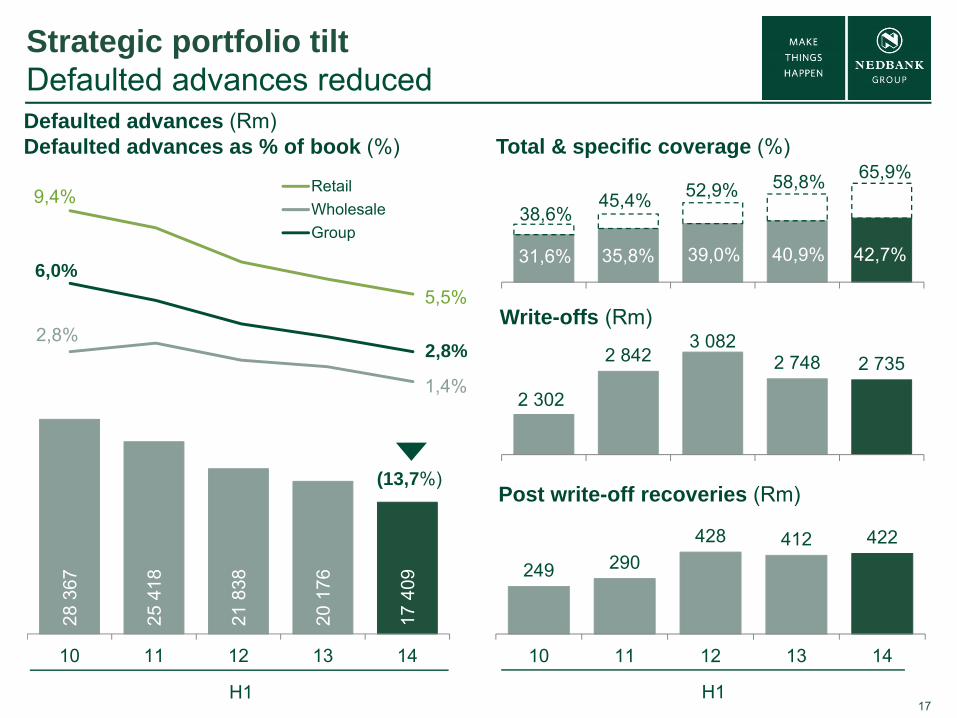

9,4%

5,5%

2,8%

1,4%

6,0%

2,8%

RetailWholesaleGroup

28 3

67

25 4

18

21 8

38

20 1

76

17 4

09

10 11 12 13 14

Strategic portfolio tilt Defaulted advances reducedDefaulted advances (Rm)Defaulted advances as % of book (%)

31,6% 35,8% 39,0% 40,9% 42,7%

2 302

2 8423 082

2 748 2 735

249 290428 412 422

10 11 12 13 14

Total & specific coverage (%)

Write-offs (Rm)

Post write-off recoveries (Rm)

58,8%52,9%45,4%38,6%

65,9%

H1H1

(13,7%)

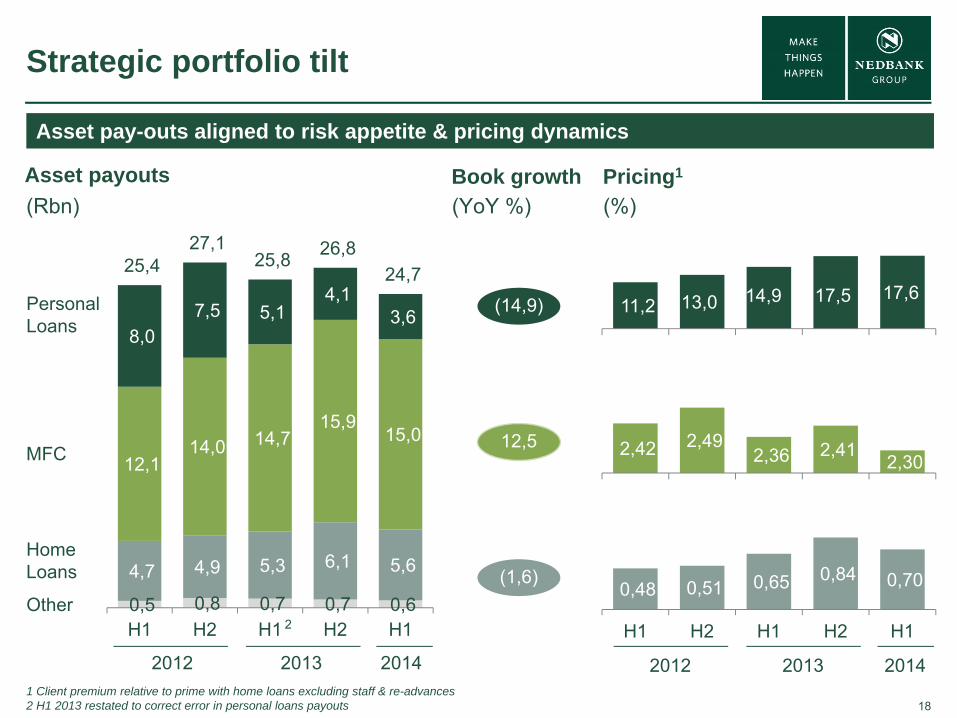

181 Client premium relative to prime with home loans excluding staff & re-advances2 H1 2013 restated to correct error in personal loans payouts

Strategic portfolio tilt

12,5

(1,6)

(14,9)

(YoY %)(Rbn) (%)

2,42 2,49 2,36 2,41 2,30

0,48 0,51 0,65 0,84 0,70

H1 H2 H1 H2 H1

MFC

Home Loans

Personal Loans

Other

2012 2013

0,5 0,8 0,7 0,7 0,6

4,7 4,9 5,3 6,1 5,6

12,1 14,0 14,7

15,9 15,0

8,0 7,5 5,1

4,1 3,6

25,4 27,1

25,8 26,8 24,7

H1 H2 H1 H2 H1

20142012 2013 2014

11,2 13,0 14,9 17,5 17,6

Asset payouts Book growth Pricing1

2

Asset pay-outs aligned to risk appetite & pricing dynamics

19

5

10

15

20

25

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

Strategic portfolio tiltPersonal loans operating within strategic intent & lowered risk profile

1 Asset growth reflects the 6 months on the preceding 6 months growth annualised2 GOI margin is the total gross operating income (Net Interest Income & Non Interest Revenue) divided by average advances, before Wealth related income3 PD is the probability of loan going into default based on early warning risk indicators4 H1 includes actuals for Jan - Jun

Early, comprehensive actions to mitigate risk as industry concerns escalate

Warning signs observed late 2011

Actual risk of vintages worse than expected

Outcome achieved: Book R3,2bn lower than Jun ‘13 Better quality risk, within desired risk

appetite at higher pricing Defaults peaked in May ’13, now

back in line with expectations Methodology changes raised from H1

2012 to address risk of higher write-offs than forecast by models

PL asset growth1

Nedbank growth (%)Rest of market (%)

R1,7bn reduction YTD

-20

0

20

40

Expected PD model calibration 3 (%)Actual / Predicted PD 3 (%)

Avg GOI margin2(%)

GOI margin & risk over time

20142009 2010 2011 2012 2013 4

Headline Earnings

Rm

161239 219

66

280

2010 2011 2012 2013 2014

H1

20

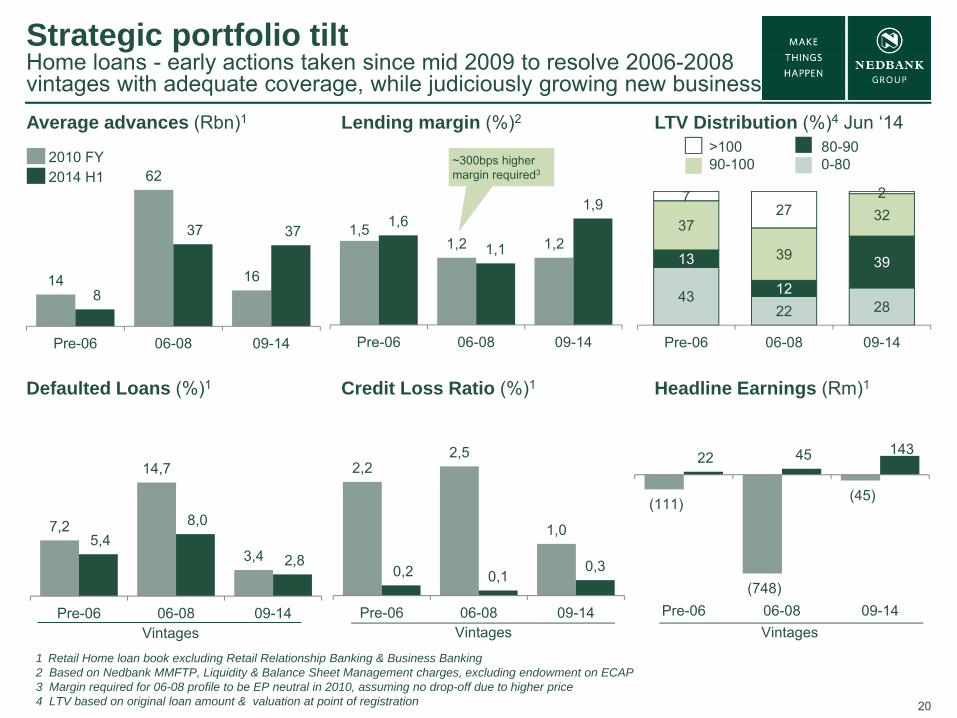

14

62

168

37 37

Pre-06 06-08 09-14

2010 FY2014 H1

Strategic portfolio tiltHome loans - early actions taken since mid 2009 to resolve 2006-2008 vintages with adequate coverage, while judiciously growing new businessAverage advances (Rbn)1

Headline Earnings (Rm)1Defaulted Loans (%)1 Credit Loss Ratio (%)1

Vintages Vintages Vintages

1 Retail Home loan book excluding Retail Relationship Banking & Business Banking2 Based on Nedbank MMFTP, Liquidity & Balance Sheet Management charges, excluding endowment on ECAP3 Margin required for 06-08 profile to be EP neutral in 2010, assuming no drop-off due to higher price4 LTV based on original loan amount & valuation at point of registration

>10090-100

LTV Distribution (%)4 Jun ‘14Lending margin (%)2

~300bps higher margin required3

80-900-80

7,2

14,7

3,45,4

8,0

2,8

Pre-06 06-08 09-14

2,22,5

1,0

0,2 0,10,3

Pre-06 06-08 09-14

1,51,2 1,2

1,6

1,1

1,9

Pre-06 06-08 09-14

(111)

(748)

(45)

22 45 143

Pre-06 06-08 09-14

4322 28

13

12

39

37

39

327

272

Pre-06 06-08 09-14

21

A

B

Pan-African banking networkA client-centred, risk-mitigated, capital-efficient, longer-term strategy

‘One bank’ experience for clients across 38 countries & >2 000 staffed outlets

SADC & East Africa (A) Standardised operating model & IT system

progressing well

Banco Unico (Mozambique): Acquired 36,4% stake for R252m (with pathway to control)

West & Central Africa (B) Rights to acquire up to 20% equity stake in ETI

Ecobank building its franchise

‒ New Board, Chairman & CEO

‒ #1 in 6 countries, top 3 in 14 countries

‒ H1 2014 profit after tax $194m up 15% at ROE of 17,7%

Wholesale, trading & investment activity Senior coverage bankers in East & West Africa

A number of deals concluded in rest of Africa together with Ecobank & Bank of China

22

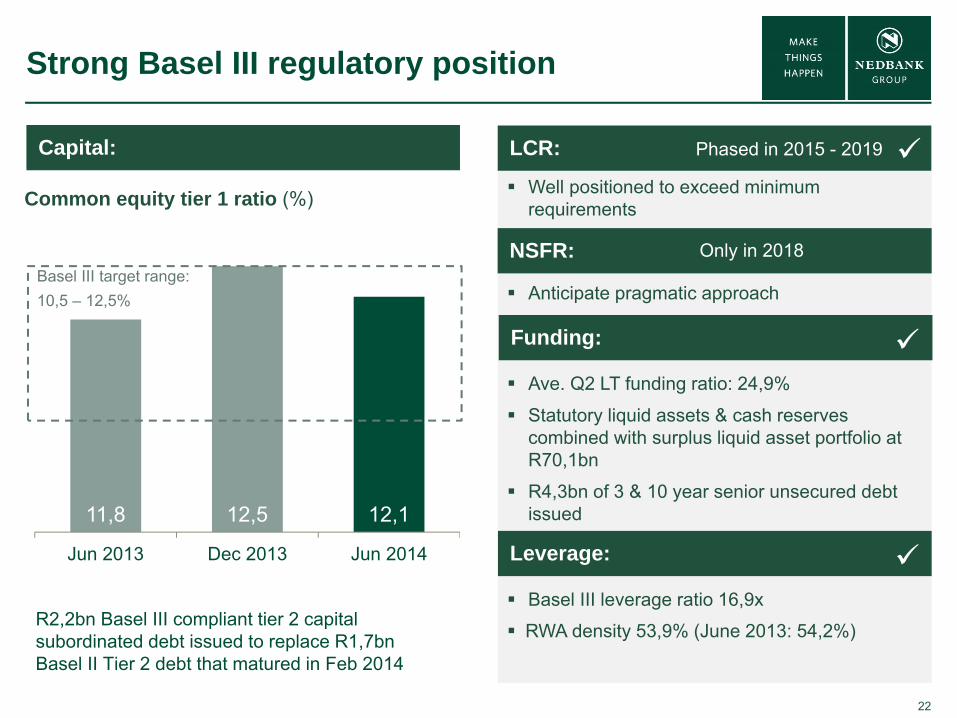

11,8 12,5 12,1

Jun 2013 Dec 2013 Jun 2014

Capital: Only 2015

Well positioned to exceed minimum requirements

Anticipate pragmatic approach

Ave. Q2 LT funding ratio: 24,9%

Statutory liquid assets & cash reserves combined with surplus liquid asset portfolio at R70,1bn

R4,3bn of 3 & 10 year senior unsecured debt issued

Basel III leverage ratio 16,9x

RWA density 53,9% (June 2013: 54,2%)

Strong Basel III regulatory position

Common equity tier 1 ratio (%)

NSFR: Only in 2018

LCR: Phased in 2015 - 2019

Funding:

R2,2bn Basel III compliant tier 2 capital subordinated debt issued to replace R1,7bn Basel II Tier 2 debt that matured in Feb 2014

Leverage:

Basel III target range: 10,5 – 12,5%

23

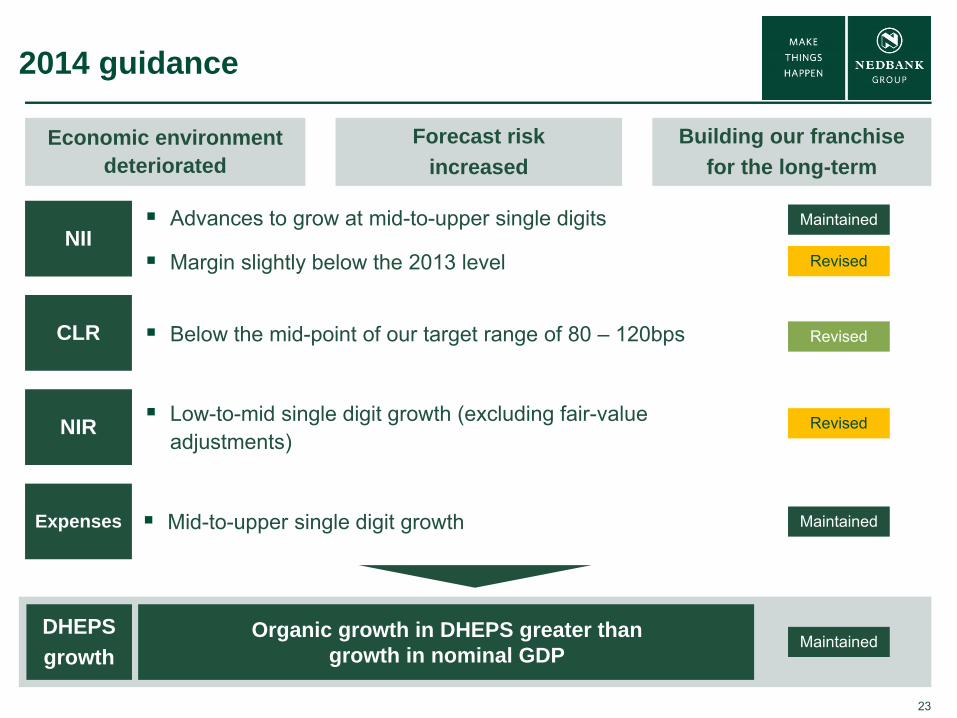

2014 guidance

Advances to grow at mid-to-upper single digits

Margin slightly below the 2013 levelNII

Below the mid-point of our target range of 80 – 120bps

Low-to-mid single digit growth (excluding fair-value adjustments)

Mid-to-upper single digit growth

CLR

NIR

Expenses

Economic environment deteriorated

Forecast risk increased

Building our franchise for the long-term

Revised

Revised

Revised

Maintained

Maintained

Organic growth in DHEPS greater than growth in nominal GDP

DHEPSgrowth

Maintained

24

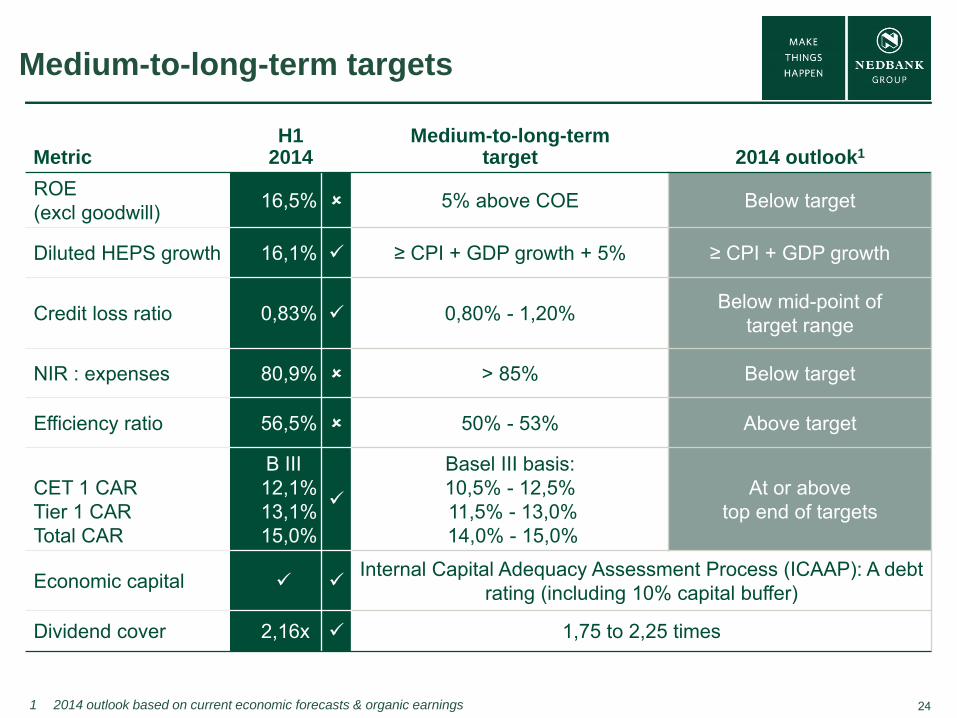

Medium-to-long-term targets

MetricH1

2014Medium-to-long-term

target 2014 outlook1

ROE (excl goodwill) 16,5% 5% above COE Below target

Diluted HEPS growth 16,1% ≥ CPI + GDP growth + 5% ≥ CPI + GDP growth

Credit loss ratio 0,83% 0,80% - 1,20% Below mid-point of target range

NIR : expenses 80,9% > 85% Below target

Efficiency ratio 56,5% 50% - 53% Above target

CET 1 CARTier 1 CARTotal CAR

B III12,1%13,1%15,0%

Basel III basis:10,5% - 12,5%11,5% - 13,0%14,0% - 15,0%

At or above top end of targets

Economic capital Internal Capital Adequacy Assessment Process (ICAAP): A debt

rating (including 10% capital buffer)

Dividend cover 2,16x 1,75 to 2,25 times

1 2014 outlook based on current economic forecasts & organic earnings

25

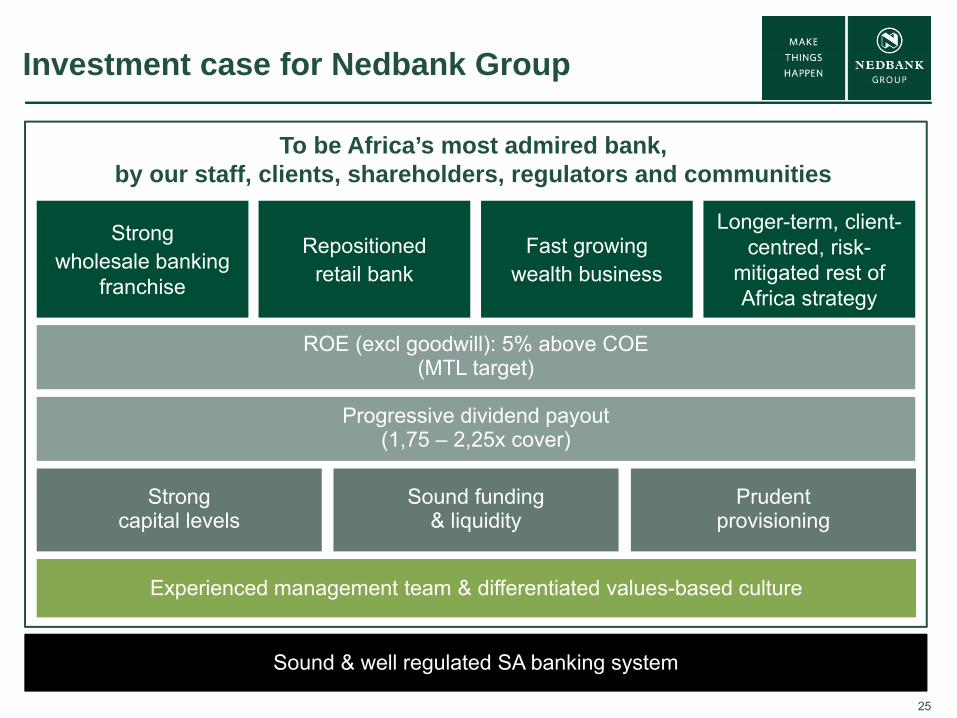

Investment case for Nedbank Group

Strong capital levels

Sound funding & liquidity

Prudent provisioning

Experienced management team & differentiated values-based culture

Sound & well regulated SA banking system

Strong wholesale banking

franchise

Repositioned retail bank

Fast growing wealth business

Longer-term, client-centred, risk-

mitigated rest of Africa strategy

To be Africa’s most admired bank, by our staff, clients, shareholders, regulators and communities

Progressive dividend payout(1,75 – 2,25x cover)

ROE (excl goodwill): 5% above COE(MTL target)

26

0

50

100

150

200

250

Aug‐09 Aug‐10 Aug‐11 Aug‐12 Aug‐13 Aug‐140

40

80

120

160

200

Aug‐11 Feb‐12 Aug‐12 Feb‐13 Aug‐13 Feb‐14 Aug‐14

0

40

80

120

160

Aug‐13 Oct‐13 Dec‐13 Feb‐14 Apr‐14 Jun‐14 Aug‐14

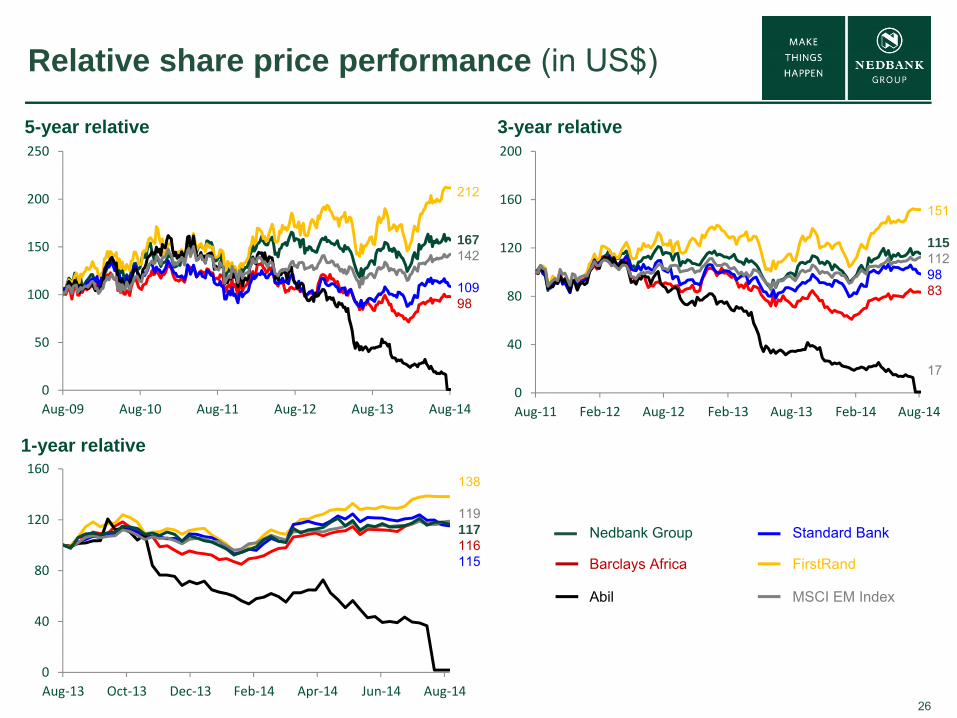

Relative share price performance (in US$)

5-year relative 3-year relative

1-year relative

Nedbank Group

Barclays Africa

Standard Bank

FirstRand

Abil MSCI EM Index

212

167142

10998

138

119117116115

151

1151129883

17

27

Nedbank Group segmental overview

Nedbank Capital

Nedbank Corporate

Nedbank Business Banking

Nedbank Retail

Nedbank Wealth

Investment banking, global markets & treasury solutions to institutional and corporate clients.

Offices: SA & LondonRep offices: Angola, Toronto

Lending, deposit taking, transactional banking for SA corporates with t/over >R700m p.a. & commercial property finance.

Commercial banking solutions to small- to medium-sized businesses with turnover of R10m – R700m p.a.

Holistic offering for the business, business owners / households & employees

A bank for all financial needs of individuals & small businesses <R10m turnover p.a. Transactional, card, lending, deposit taking, risk management and investment products / services, as well as card-acquiring services for business

Insurance, asset management & wealth management solutions

Offices in SA, London, Isle of Man, Jersey, Guernsey & Middle East.

AUM:R210bn

Clients among top 200 SA corporates & parastatals

Top 3 mergers & acquisitions player

Industry expertise in: Infrastructure Mining & resources Oil and gas Telecoms Energy

Top 2 SA corporate bank > 600 large corporate clients Strong market share in public

sector loans Continued market leadership in

commercial property finance

25 000 client groups and strong primary client gains

A leader in Corporate Saver deposits & debtor management

Excellent client-centred risk management & worldclasscustomer management capabilities

Distinctive client value propositions & accountable empowered decentralised business service model

6,7m clients

762 branches and alternate outlets, 279 Personal Loan kiosks and 3 445 ATMs

Strong positioning in household motor finance (25% share), and household deposits (20%)

Compelling, innovative CVPs for all segments

Life embedded value: R2,2bn Assets under management:

R209,5bn >10 000 high-net-worth clients

Nedgroup Investments: Raging Bull awards: Top 3

management company in SA for the 5th consecutive year;

Plexus Survey: 3rd amongst domestic managers;

2nd in international categoryNedbank Private Wealth:

Four of our top funds ranked top in their categories over 10 years.

Strong Investment Banking (IB) pipeline with more cross-sell across businesses.

Strategic growth in Africa and leverage Ecobank & Bank ofChina.

Leverage industry expertise. Leverage trading systems. Participating strongly in SA’s

infrastructure build programme & leverage leadership in renewable energy.

Strong client relationships. Continued product and NIR

growth through enhanced capabilities & primary-client growth.

Increased Pan-African focus. Strong risk management.

A choice of distinctive client-centred banking experiences.

A rigorous approach to capturing virtuous circle & interdependencies between client segments.

Integrated-channels strategy leveraging mobile innovation, digital channels & social media; selected micro markets for growth/optimisation; area collaboration.

Robust risk management supporting strong product niches.

Liabilities innovation sustaining historical strength.

Collaborative, people-centred culture.

Explore broader complimentaryfinancial services opportunities.

Continued enhancements to value propositions & offerings.

Unlocking new value & efficiencies through business transformation.

Leverage advantage of group collaboration.

Des

crip

tion

Ope

ratio

nal

over

view

Fina

ncia

lm

etric

sK

ey s

trate

gic

driv

ers

Assets Headline earnings Assets

Headline earnings Assets

Headline earnings Assets

Headline earnings

Headline earnings

ROE: 29,4% ROE: 26,4% ROE: 19,4% ROE: 11,6% ROE: 36,2%

24% 23% 26% 25% 13% 11% 26% 29% 10%

28

Contact us

Nedbank Groupwww.nedbankgroup.co.zaNedbank Group LimitedTel: +27 (0) 11 294 4444Physical address 135 Rivonia RoadSandown 2196 South Africa

Download the Nedbank Investor Centre App from the Nedbank App Suite:

Nedbank Investor RelationsHead of Investor Relations Alfred Visagie Direct tel: +27 (0) 11 295 6249 Cell: +27 (0) 82 855 4692 Email: [email protected]

Investor Relations Consultant Penny Him Lok Direct tel: +27 (0)11 295 6549 Email: [email protected]

Investor Relations AnalystCaron Askew Direct tel: +27 (0) 11 294 0752Email: [email protected]

DisclaimerNedbank Group has acted in good faith and has made every reasonable effort to ensure the accuracy and completeness of the information contained in this document,including all information that may be defined as 'forward-looking statements' within the meaning of United States securities legislation.Forward-looking statements may be identified by words such as ‘believe’, 'anticipate', 'expect', 'plan', 'estimate', 'intend', 'project', 'target', 'predict' and 'hope'.Forward-looking statements are not statements of fact, but statements by the management of Nedbank Group based on its current estimates, projections, expectations,beliefs and assumptions regarding the group's future performance.No assurance can be given that forward-looking statements will prove to be correct and undue reliance should not be placed on such statements.The risks and uncertainties inherent in the forward-looking statements contained in this document include, but are not limited to: changes to IFRS and the interpretations,applications and practices subject thereto as they apply to past, present and future periods; domestic and international business and market conditions such as exchangerate and interest rate movements; changes in the domestic and international regulatory and legislative environments; changes to domestic and international operational,social, economic and political risks; and the effects of both current and future litigation.Nedbank Group does not undertake to update any forward-looking statements contained in this document and does not assume responsibility for any loss or damagewhatsoever and howsoever arising as a result of the reliance by any party thereon, including, but n limited to, loss of earnings, profits, or consequential loss or damage.†