2014 state of the consumer report -...

TRANSCRIPT

2014 State of the ConsumerReport

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

Mission .......................................................................................................................................................................................1

Acknowledgements ................................................................................................................................................................1

SGCC Member List .................................................................................................................................................................2

Introduction...............................................................................................................................................................................3

Methods and Study Overviews ............................................................................................................................................3Customer Engagement Success Stories ............................................................................................................3Smart Grid Economic and Environmental Benefits ......................................................................................4Consumer Pulse and Market Segmentation Research Program – Wave 4 ..................................................4Segmentation Successes......................................................................................................................................4Voices of Experience............................................................................................................................................4

What We Have Learned: The State of the Consumer .....................................................................................................5

Theme 1: Consumer Awareness and Favorability Are Stable Over Time ...............................................................7Consumer Awareness is Stable—But Low ...........................................................................................................7Consumers Continue to View Smart Grid Favorably ...........................................................................................9The Smart Grid Favorability Index .....................................................................................................................10

Theme 2: Segmentation Drives Performance ..............................................................................................................11 Smart Grid Consumer Segments ........................................................................................................................11How Utilities Have Successfully Applied Segmentation ....................................................................................12Consumers Seek Information, Advice, and Buying Opportunities From Multiple Channels ..........................12

Theme 3: Utilities Can Use Field-Tested Best Practices Frameworks to Successfully Engage Consumers ................................................................................................................13

Customers at the Core.........................................................................................................................................14A Guide to Successful Engagement Efforts .......................................................................................................14

Theme 4: Consumers Want Smart Grid “Made Real” For Them ............................................................................15

Energy Management ............................................................................................................................................15Smart Grid-Enabled Technology .........................................................................................................................16Product and Service Design Best Practices .......................................................................................................17Make it “Real” ......................................................................................................................................................18

Theme 5: Consumers Value Clean Energy ...................................................................................................................19At What Price? .....................................................................................................................................................19Generation at Home ............................................................................................................................................20

Theme 6: The Smart Grid Offers Real Benefits that Consumers Care About .....................................................21

Outage Management ............................................................................................................................................22Renewable Generation Integration .....................................................................................................................22Economic Benefits ...............................................................................................................................................23Growing Support..................................................................................................................................................23

What’s Next .............................................................................................................................................................................24Innovation ............................................................................................................................................................24Security ................................................................................................................................................................25Renewables ..........................................................................................................................................................25

Conclusion ..............................................................................................................................................................................26

Appendix – SGCC Consumer Segments .........................................................................................................................27

table of contents

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

1

Mission

The Smart Grid Consumer Collaborative is a 501(c)(3) nonprofit organization

chartered to be the trusted source representing consumers, advocates, utilities,

and technology providers in order to advance the adoption of a reliable, efficient,

and secure Smart Grid and ensure long-lasting sustainable benefits to consumers.

acknowledgeMents

This fourth release of the Smart Grid Consumer Collaborative (SGCC) State of the Consumer expands upon previous reports by not only reporting on the latest in Smart Grid consumer understanding, but also sharing how utilities and others are utilizing this understanding in increasing consumer engagement. By sharing and disseminating these insights, we continue our drive to increase awareness of a consumer-safe, consumer-friendly Smart Grid and advance widespread understanding and interest from consumers in the benefits of an intelligent and sustainable electricity grid.

Our members were critical to the work that we chose to do and the high quality delivery of the research. SGCC membership demonstrates that collectively we are making great strides in partnering to better understand Smart Grid consumers—who they are, what they know, what they want, and how to engage them successfully.

The SGCC would like to thank the many companies and organizations that formulated insights from the research findings, and provided feedback on layout, content, and theme iterations. Only by continuing to collaborate on consumer issues will we be able to fully realize the promise of Smart Grid. If you are not a member, we invite you to join us as we continue to listen, collaborate, and educate going forward.

— SGCC Research Committee

www.smartgridcc.org

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

2

Accenture

ACEEE

Aclara Technologies

Advanced Energy

Alameda Municipal Power

Alliance to Save Energy

Ameren Corporation

Arizona Public Service Company

Association for Demand Response and Smart Grid

Avista Utilities

Baltimore Gas and Electric Company

Benton PUD

Bonneville Power Administration

Brookhaven National Laboratory

California Center for Sustainable Energy

California Public Utilities Commission

CenterPoint Energy

Citizens’ Utility Board of Oregon

Climate + Energy Project

CNT Energy

Cobb EMC

Colorado Public Utilities Commission

Columbia Water and Light Department

ComEd

Commonwealth of Massachusetts Department of Public Utilities

Comverge

Consumers Energy

CPS Energy

DNV KEMA

Dominion Resources

DTE Energy

Duke Energy

Duquesne Light Company

Earth Networks

Electric Power Board of Chattanooga (EPB)

Environmental Defense Fund (EDF)

EPCE – Energy Providers Coalition for Education

EPRI

Fayetteville Public Works Commission

First Energy Corporation

Florida Power & Light

Future of Privacy Forum

Gainesville Regional Utilities

Galvin Electricity Initiative

GE Energy

Georgia Institute of Technology

Georgia Watch

Great Plains Institute

GREEN DMV

Greenlining Institute

GridWise Alliance

Huntsville Utilities

Hydro One

IBM

Idaho Falls Power

Illinois Citizens Utility Board

Institute for Energy & Environment at Vermont Law

Intelligent Energy Solutions LLC

Itron

Landis+Gyr

Lawrence Berkeley National Laboratory

Market Strategies International

Memphis Light, Gas and Water

Michigan Public Service Commission

Middle Tennessee EMC

Montana State University

National Institute of Standards and Technology

National Renewable Energy Laboratory

Natural Resources Defense Council (NRDC)

NC Department of Commerce – Energy Office

NC Sustainable Energy Association

NETL – SG Implementation Task Force

New Brunswick Power Corporation

Office of People’s Counsel – DC

Office of the Ohio Consumers’ Counsel

Oklahoma Gas & Electric

Opower

Oracle

Pacific Gas and Electric Company

Pacific Northwest National Laboratory

PayGo

Peak Load Management Alliance (PLMA)

Pepco Holdings, Inc.

Portland General Electric

PSC

Public Utility Commission of Texas

Purdue University

Research Triangle Region Cleantech Cluster

Sacramento Municipal Utility District

Sempra Utilities / San Diego Gas & Electric

Silver Spring Networks

Simple Energy

Smart Grid Oregon

Southeast Energy Efficiency Alliance

Southern California Edison

Southern Company

Southface Energy Institute

Southwest Research Institute

Stoel Rives LLP

TechAmerica

Tendril Inc.

Tennessee Valley Authority

Texas Office of Public Utility Counsel

Tri-County Electric Cooperative

TVPPA

Utility Consumers’ Action Network

Vermont Energy Investment Corporation

sgcc MeMber list

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

3

IntroductionThe first step in meaningful collaboration is establishing a shared context among and between stakeholders. This has become especially important as both the pace of change in and growth of expectations of the electric utility sector have accelerated over the past years. The Smart Grid Consumer Collaborative (SGCC) endeavors to create this shared context through its research and to facilitate meaningful collaboration between stakeholders.

The SGCC’s consumer research program is rigorously designed to truly understand consumers and how they relate to the Smart Grid. We have defined the market segments that exist related to Smart Grid technology, and have delved deeply into their interests and desires. At the same time, we have begun to examine how utilities have produced benefits meaningful to consumers through their grid modernization efforts, and how they have successfully engaged consumers in the process.

methods and Study OverviewsThe 2014 State of the Consumer report draws its key themes from SGCC research conducted in 2013. This research includes: Customer Engagement Success Stories, Smart Grid Economic and Environmental Benefits, and Consumer Pulse and Market Segmentation Wave 4, along with an examination of utility segmentation efforts to be released in early 2014. We also reviewed non-SGCC research related to consumer engagement, and include selected findings from the US Department of Energy’s Voices of Experience as part of this report.

Customer Engagement Success Stories

Customer Engagement Success Stories examined the communication and outreach strategies and tactics used by four leading U.S. utilities to successfully increase consumer engagement with a variety of Smart Grid-enabled programs. This examination was the basis for a seven-point engagement framework that is useful for all industry stakehold-ers in guiding their consumer engagement efforts. Additional case studies were released throughout 2013, yielding greater insight into how this engagement framework serves to help effectively educate and motivate consumers to engage with various Smart Grid-enabled programs and technologies.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

4

Smart Grid Economic and Environmental Benefits

Because real-world experience with the Smart Grid is growing, SGCC completed a review of available research quantifying the actual—rather than forecast—benefits and costs to help stakeholders analyze and maximize the value of various Smart Grid capabilities. This report summarizes available research on the benefits of grid modern-ization in terms that stakeholders and consumers can understand. It synthesizes the findings in a “per customer” context whenever possible and documents the assumptions and calculations used in this synthesis so that stakeholders can easily translate this research into information relevant for their particular Smart Grid application.

Consumer Pulse and Market Segmentation Research Program – Wave 4

Starting in August 2011, SGCC began regularly taking the pulse of the consumer market to gauge consumers’ journey in Smart Grid understanding, acceptance, and engagement. This seminal study was designed to measure and track changes in consumer awareness, favorability, and understanding of Smart Grid messages and consumer benefits.

The findings from the SGCC Consumer Pulse and Market Segmentation study are derived from over 4,000 in-depth, nationally-representative consumer telephone surveys. Wave 1 was completed in August 2011 among 1,200 U.S. consumers. Wave 2 was completed November 2011 among a sample of 1,003 U.S. consumers. Wave 3 was completed in August 2012 among 1,089 U.S. consumers. Wave 4 was completed in Septem-ber 2013 among 1,001 U.S. consumers.

Segmentation Successes

From SGCC’s Consumer Pulse and Market Segmentation study, we know that consumers are not monolithic when it comes to Smart Grid. Instead, there are five distinct segments that hold different interests, priorities, and willingness to engage with Smart Grid-enabled programs and technologies. We looked at how a small sample of utilities have applied segmentation to their Smart Grid programs, what the results were, and what capabilities the utilities had to develop to do this work. The resulting white paper will be released in February 2014.

Voices of Experience

As a member of the US Department of Energy’s (DOE) Voices of Experience steering committee, SGCC and a number of its members helped develop this report. In Smart Grid Peer-to-Peer Workshops conducted by DOE, utilities of different sizes and operating structures shared the approaches and methods that worked best for them and their communities, and the valuable lessons they learned along the way. This report captures these approaches in order to share the large base of knowledge that exists about Smart Grid implementation in utilities throughout the United States.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

5

What We have Learned: The State of the ConsumerSince its founding, the Smart Grid Consumer Collaborative has made it a priority to increase industry knowledge about how U.S. consumers are thinking about and engaging with grid modernization efforts. In 2013, we have expanded our work to help industry stakeholders understand how to apply that knowledge to grow consumer awareness, favorability, and engagement with these new technologies.

Based on SGCC’s 2013 research, below are six key themes about the state of the Smart Grid consumer:

Theme 1: Consumer Awareness and Favorability Are Stable Over TimeDespite Smart Meters being installed in nearly 40% of U.S. homes and the emergence of the term “Smart Grid” in mainstream use, consumer awareness and favorability is largely the same today as it was when SGCC began the Consumer Pulse and Market Segmentation program in 2011. This shows that we still have a long way to go in helping consumers understand Smart Grid and why it matters to their future. Fortunately, this also shows that pockets of noisy opposition to grid modernization do not appear to have a negative impact on consumer sentiment.

Theme 2: Segmentation Drives PerformanceBecause consumers care about different things, utilities that approach consumers with benefits that they care about realize better program performance than those that use a blanket message. Additionally, our research indicates that there may be opportunities for utilities to drive revenues by offering added value to consumers. Segmentation can be a win-win, with consumers enjoying more personalized products and messaging about things they care about, and utilities finding new areas for growth in a changing energy landscape.

Theme 3: Utilities Can Use Field-Tested Best Practices Frameworks to Engage Customers

While segmentation is critical to engaging consumers, we have found commonalities that underlie the most effective utility customer engagement efforts. The resulting frameworks provide a core set of activities that any utility can use to successfully engage their customers. Important among these activities are:

• Engaging customers before technology deployment;

• Facilitating employee and community engagement;

• Listening and engaging with customer concerns and questions.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

6

Theme 4: Consumers Want Smart Grid “Made Real” For ThemAlthough they may not be aware of the underlying Smart Grid technology, consumer interest in Smart Grid-enabled technologies and programs is very strong, though program participation and technology adoption rates remain low. We believe that this gap between interest and adoption can be narrowed through consumer-focused product/service development and by communicating with consumers in the language and via the channels that they prefer.

Theme 5: Consumers Value Clean EnergySince the inception of SGCC’s Consumer Pulse research program, consumers have told us that clean energy and grid reliability are extremely important benefits of the Smart Grid—and that they would be willing to pay more to receive them. This year, we tested several price points for these benefits, and the results are surprising. Not only do consumers demonstrate a continued willingness to pay, but their responses also show that support is not inversely correlated with price. This indicates an opportunity for utilities and others to reexamine how they approach providing clean energy.

Theme 6: The Smart Grid Offers Real Benefits that Consumers Care AboutWe know that consumers care about a number of different benefits that the Smart Grid can offer—from the immediate and personal to the long-term and societal. Fortunately, many of these benefits are no longer hypothetical, but proved by real-world experience. Looking at actual Smart Grid deployments, we found that the net present value of Smart Grid investment ranges from $247 to $713 per customer and that there are significant environmental and reliability improvements from these investments.

We invite your feedback and look forward to continuing dialog on these insights as well as the more detailed findings that follow. SGCC is committed to continuing to provide research and thought leadership that support increased understanding of the implications of new grid technologies for American consumers.

Consumers have told us that clean energy and grid reliability

are extremely important benefits of the Smart Grid—

and that they would be willing to pay more to receive them.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

7

In 2013, smart meter penetration reached 40% of all consumers.1 Additionally, the term “Smart Grid” began to receive more mainstream use, with GMC using it to create a favorable impression of their new Sierra truck and IBM promoting it as part of their “Smarter Planet” initiative.

Despite the progress utilities have made in Smart Grid implementation and the popular-ization of the term, consumers remain largely unaware of Smart Grid, its components, and the benefits it offers.

Consumer Awareness is Stable—But LowSince SGCC began its Consumer Pulse and Market Segmentation program in 2011, we have spoken with over 4,000 U.S. residential consumers. Although much has changed in the Smart Grid landscape since the first research wave, consumer awareness does not appear to be tracking the change.

Watch at http://tinyurl.com/GMCSmartGrid

Watch at http://tinyurl.com/SG-IBM

Theme 1: Consumer Awareness and Favorability Are Stable Over TimeConsumers continue to be generally unaware of the grid modernization efforts that are happening around them.

1 Utility Scale Smart Meter Deployments, Plans, & Proposals, Institute for Electric Efficiency, 2013

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

8

Specifically, 53% of respondents in 2013’s Wave 4 survey have never heard the term “Smart Grid” while an additional 22% have heard of “Smart Grid”, but don’t know much about what it means.

Similarly, 48% have not heard the term “Smart Meter”, while 17% have heard the term but don’t know much about it.

These results are statistically identical to the responses from Waves 1-3, indicating the need for continued outreach and education to consumers about these technologies.

Additionally, although 40% of households now have a smart meter, only 17% of Wave 4 respondents say that they have a smart meter on their home. The accompanying graph shows the widening gap between actual smart meter installations and consumer awareness that the installations have occurred.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

9

Consumers Continue to View Smart Grid FavorablyAlthough most consumers have not heard—or don’t know much—about the Smart Grid, those who are aware con-tinue to hold favorable views toward it.

When respondents were asked an open-ended question about why they gave the favorability rating they did for smart meters, 19% of those who indicated favorability indicated that they were simply satisfied/happy with the meter. Other responses echoed typical consum-er value propositions, including remote readings, availability of energy data to control usage, and energy conservation.

Although many open-ended responses aligned with typical Smart Grid value propositions, there is a gap between what consumers say is important when prompted with value propositions and what they say in the absence of a prompt. Comparing the prompted responses in Wave 3 to the open-ended responses in Wave 4 shows this gap.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

10

For consumer-friendly information that addresses frequently heard concerns about the Smart Grid,

download SGCC’s Consumer Information Kit for the Smart Grid at http://smartgridcc.org/

sgcc-consumer-concerns-and-educational-toolkit

The Smart Grid Favorability Index SGCC created the Smart Grid Favorability Index to serve as a single metric over time to track the state of Smart Grid awareness and favorability. It provides a summary measure of consumers’ current level of knowledge about the Smart Grid and their favorability towards it.2 Because the two components—awareness and favorability—have remained essentially unchanged over all four Waves of the Consumer Pulse survey, the Smart Grid Favorability Index currently stands at 24, right where it was at the inception of the Index in 2011.

Nearly 1 in 5 consumers who are aware of smart meters say their overall feelings about smart meters are “unfavorable.” These consumers’ responses to the open-ended question about why they gave the rating they did indicates a need for continued consumer education to dispel misperceptions about the technol-ogy. As an example, 23% of unfavorable respondents said that they held unfavorable views because smart meters allowed their utility to monitor and/or control their energy usage. Other responses include concerns about accuracy, health impacts, privacy, and expense. Correcting these misperceptions and reducing the number of consumers who hold unfavorable views of the technology needs to be a priority for the industry.

Interestingly, 14% of both favorable and unfavorable respondents indicated that they gave the rating they did because they didn’t know enough about it. It seems that as many consumers are willing to give the technology the benefit of the doubt as are not—and that these consumers’ favorability could be swayed as they learn more about it.

2 The Favorability Index is calculated by multiplying percent aware by percent favorable. For instance, if awareness were 50% and favorability were 60%, the Index would be 30 (50 x 60/100).

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

11

Theme 2: Segmentation Drives PerformanceResidential consumers are not a monolithic class, and utilities that approach consumers in a more individualized way see greater program and business performance.

As discussed in the previous theme, consumers value different benefits that the Smart Grid can provide—from saving money to greater reliability to environmental performance. Consequently, there are a wide array of products and services that have strong appeal among consumer segments, though the reason for their appeal may differ for different consumers. Additionally, the marketing message is not the only place where segmentation matters, as we discovered strong consumer preference for certain purchase channels.

Segmentation has long been seen as a valuable tool to drive performance within other business sectors. It is now something that is seeing increasing use in the utility sector, both in regulated and deregulated markets, to drive program and business performance.

3 Nationally, based on findings from Consumer Pulse and Market Segmentation Study Wave 4

Source: IBM Institute for Business Value survey, 2003

Importance of customer segmentation in reaching profitable customers through marketing activities

Smart Grid Consumer SegmentsThe Smart Grid Consumer Collaborative has developed a segmentation framework based on consumer attitudes and behaviors towards the Smart Grid. Utilities and others seeking to engage consumers with Smart Grid-enabled products and services can use this framework to reach them more effectively.

Segment Name % of Population3 Attitudinal disposition

Easy Street 25% “ We can afford to pay for electricity. The cost isn’t that much, on our budget.”

Concerned Greens 24% “ Smart Grid and smart meters will help protect the environment”

Young America 20% “ We wish someone would tell us how Smart Grid can help us save money and help the environment.”

DIY & Save 17% “ Energy efficiency and Smart Grid programs sound appealing, because they would help us save money.”

Traditionals 14% “ Frankly, we’re not at all sure Smart Grid is needed.”

For more detail on each segment’s attitudes and select demographic characteristics, please see the Appendix of this report.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

12

How Utilities Have Successfully Applied SegmentationBy segmenting their customer databases, a number of utilities have seen important real-world improvements in customer satisfaction, program uptake rates, and customer care costs. Examples4 include:

Customer Satisfaction • To help communicate the significant reliability enhancements that were made, Pepco developed targeted reliability

messages based on their customer segmentation that contributed to improved overall customer satisfaction by almost 10 points over the previous year.

Program Uptake Rates • When offering a demand response program, Duke Energy made the same number of offers—but to a different mix

of targets based on predictive analytics—and enjoyed a 50% to 100% improvement in response rates.

• When encouraging customers to enroll in paperless billing, Arizona Public Service tailored the message to address privacy concerns for a “technology averse” segment and increased response rates from 1% to almost 5%.

Customer Care Costs • When explaining an impending cost increase to customers, San Diego Gas & Electric developed specific messages and

targeted energy savings solutions for each customer segment. They were able to address the issues of each segment with the right tone and avoided a significant amount of backlash.

• Using predictive analytics, Duke Energy was able to present customers with relevant solutions when they called their call centers. This resulted in a better customer experience and a reduction in the cost of service.

Consumers Seek Information, Advice, and Buying Opportunities From Multiple ChannelsWe asked consumers who they thought would do the best job at acting as a “one-stop shop” selling products, technology, services, and expertise to help them use energy more wisely. Home improvement stores such as Home Depot or Lowes topped the list, though energy utilities were also seen as highly credible. Although we did not ask respondents why they expressed the channel preferences they did, we hypothesize that it is because most consumers have minimal contact with their utility and fairly regular contact with a home improvement store.

For those seeking to enhance customer engagement by bringing new products and services to market, this indicates that there are at least two key distribution channels to reach consumers, and that consumers encountering a product at a home improvement store may be more likely to make a purchase. It is important to note the differences between segments, such as DIY & Save’s significantly higher propensity to prefer home improvement stores and Young America’s preference for telecom providers, and map those preferences against that segment’s values.

4 Examples in this section come from SGCC’s Segmentation Successes white paper, which will be released in February 2014

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

13

Theme 3: Utilities Can Use Field-Tested Best Practices Frameworks to Successfully engage ConsumersOperating environments differ, but successful consumer engagement is as much science as art.

Looking across the Smart Grid landscape, SGCC identified many different utilities that have successfully engaged consumers in their Smart Grid programs. The lessons from these utilities were discussed in our Smart Grid Customer Engagement Success Stories report, and although they all had different particulars, each utility used a core set of strategies to drive its success.

These strategies include:

1. Educate customers before deployment.

2. Anticipate and answer questions before customers ask them.

3. Facilitate community engagement.

4. Communicate ways to shift usage off-peak.

5. Deploy a user-friendly web portal.

6. Offer user-friendly Smart Grid enabled technology.

7. Create authentic customer testimonials.

The Voices of Experience guide offers similar—and complimentary—advice on the characteristics of successful customer engagement programs:

1. Establish strong guiding principles.

2. View customers as partners.

3. Engage employees from the start and throughout the program.

4. Start customer engagement efforts prior to technology deployment.

5. Manage change within the organization proactively.

6. Meet customers in their preferred forum—traditional mail, in person, or online. The channel is just as important as the message.

7. Recognize the importance of listening and engaging with customers who have concerns about the technology.

These lists are not exclusive, rather, they are mutually reinforcing. For example, Voices of Experience suggests engaging employees, and SGCC’s research suggests that educating and deploying employees into the community helps facilitate community engagement. We also see similar recommendations around proactively engaging with customers who have questions or concerns, and the need to communicate through the channels that customers prefer.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

14

Customers at the CoreThroughout all of these activities, we found that utilities that are successful at engaging consumers put customers first. For example, Gulf Power strove to make participation in their Energy Select program (a time-of-use/critical peak pricing program) as simple as possible. Gulf Power is upfront with customers about its pricing structure and the conditions under which a critical event will be called. They also worked closely with their vendors to ensure that supporting technologies—programmable thermostats and load-control relays—were as consumer-friendly as possible.

The Voices of Experience guide explores how knowing your customers helps create happier, more engaged customers. It cautions that understanding customers does not stop with consumer economics, but rather extends to understanding consumers’ worldviews. Stakeholders who participated in crafting this guide recommended that utilities engage in face-to-face exchanges to complement and enhance research done in pursuit of understanding customers’ worldviews.

CenterPoint Energy and San Diego Gas & Electric accomplished this face-to-face interaction in part through their employee training and engagement programs:

• CenterPoint Energy tapped its Houston-area workforce of 2,175 employees to communicate smart meter essentials with a smart meter training program. Approximately 1,500 of those employees were trained using a separate intelligent grid training module. Those who passed an online course for each became “ambassadors” for the company’s “energyInSight” campaign. The company’s ambassadors fanned out to speak to a variety of civic, religious, and business groups demonstrating along the way how serious they are in making the Smart Grid work for all of the consumers in their service territory.

• To ensure they were plugged into customers’ adoption of smart meters and what it could do for them, SDG&E deployed an “Infield Liaison Team” comprised of three recent retirees to canvass about 50,000 customers in a representative sample of neighborhoods about two weeks after the installation.

t Things Every Utility Should Know5

q Smart Grid impacts the entire organization and must be championed by the top executives.

w Smart Grid technology changes the customer-utility relationship; it is a cultural shift in the utility industry.

e Smart Grid is a community effort not just a utility effort.

r Utility customers do not all have the same needs and preferences. Customer choice is important.

t Media coverage—particularly social media—can change community perceptions quickly, especially if customers have not been informed and educated upfront.

A Guide to Successful Engagement EffortsSomewhat surprisingly, these factors identified through our case studies and the Voices of Experience work were shared among the successful consumer engagement programs we identified despite coming from regulated and deregulated markets, and from utilities large and small. They therefore serve as a foundation upon which utilities seeking to better engage their consumers can build a successful program, taking into account the uniqueness of their markets and regu-latory environment.

5 From Voices of Experiences

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

15

Theme 4: Consumers Want Smart Grid “made Real” For ThemHardware is only the first step in the Smart Grid journey.

Throughout SGCC’s research, we have continually found that consumers have a high degree of interest in products and services that are enabled or enhanced by the Smart Grid. For many of these products and services, penetration is currently very low, offering a significant opportunity for utilities and others to fill the gap.

Energy ManagementEach of the five segments SGCC has identified expresses a strong desire to use advanced metering infrastructure (AMI) data to manage their energy use, though the particulars of how they want to do so differ. In Wave 3 of the Consumer Pulse study, 79% of respondents indicated that they were likely to use AMI data to manage and attempt to reduce their electricity usage and cost. In Wave 4, we asked respondents their likelihood to use various ways of accessing this data and found energy reports and online analysis to be the most compelling offerings, likely to be used by two-thirds of respondents.

With the exception of online energy analysis, Concerned Greens and Young America are significantly more likely than other segments to engage with these energy management offerings. Thus, these two segments in particular are ready to be engaged by utilities or technology providers who can meet their needs with compelling offerings.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

16

Smart Grid-Enabled TechnologyFor the first time in 2013, we tested consumers’ interest in purchasing a number of technologies that are enabled or enhanced by the Smart Grid.

A significant number of respondents —22%—already had a programmable thermostat, but this remains the most desirable technology to consumers across all segments. This validates a program that we have noted among some utilities where they provide a programmable thermostat to consumers who choose a certain rate plan. This kind of program is an easy “win” for utilities that are looking to engage consumers more proactively and/or drive program enrollment.

As with providing energy data, Concerned Greens and Young America tend to be the most interested in these technologies, though DIY & Save edges out Young America for interest in programmable thermostats. While we did not test why respondents indicated purchase interest, we do know that Young America is the most likely segment to rent and may be constrained in their adoption of programmable thermostats as a result.

A significant number of respondents—

22%—already had a programmable thermostat, but this remains the most

desirable technology to consumers across

all segments.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

17

Product and Service Design Best PracticesSGCC worked closely with the US Department of Energy and over 50 utilities and vendors to create the Voices of Experience guide to customer engagement with the Smart Grid. Voices of Experience participants stated that it was critical that customers see an immediate benefit when Smart Grid technology is installed. These stakeholders recommended that utilities do the following when developing their product/service roadmap:

Conduct Research

• Conduct a survey of customers or study emerging consumer research to determine the specific products, services, and features to implement.

• Have personal conversations (on the phone, online, or in person) with customers to determine what they care about, want, and need.

Develop A Plan

• Develop a product road map that includes having a product that provides consumers with energy insights, choices and convenience options available when the meter is installed so consumers can understand and see the benefits on the first day. For some, the roadmap may only include a couple of products (perhaps time of use rate or home energy monitor); for others, it will be much more robust.

• Give customers choices. Develop a range of products and services that demonstrate value to the consumer. Customers have different preferences and needs so they will value different products and services.

• Give customers the choice not to choose; customers want the choice to do nothing.

• Make programs, products, and services voluntary, easy, and pleasant.

• Consider the benefits of making a program opt-in versus opt-out.

• Develop a web portal with easy access to information about the utility’s programs, products, and services such as personalized energy management information, alternative rate and payment plans, and tools for energy management.

Ted Reguly from San Diego Gas & Electric shared how they used these principles in their approach to Smart Grid innovation, and the success they saw in engaging their customers:

“ From day one, SDG&E focused on rolling out a number of valuable services to benefit our customers.

These included things like outage communications, energy charts, incentives and alerts for peak time

reductions, and weekly email alerts. We took a new approach and launched a customer-centric

approach … The feedback has been great, due to the fact that we effectively targeted to ensure we

were providing the right information to the right customers in a channel that they preferred.”

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

18

Make it “Real”Consumers demonstrate a strong interest in value-added products and services made possible by the Smart Grid. As discussed in Theme 2, it’s important to develop messages and use channels that are customized for each consumer segment when marketing these products and services to consumers. As noted in Voices of Experience, marketing should be staged to correspond with the operational deployment of new products and services. Voices of Experience stakeholders provided the following recommendations on messaging:

• Focus on the benefits to customers and what is in it for them, but do not oversell the benefits.

• Do not focus on the “Smart Grid” or “smart meter” when educating consumers. Customers do not always care about the underlying technology; focus on the products, services, and benefits it enables.

• Avoid technical terms such as “kWh” to describe usage. Equivalencies such as “this is enough electricity to power 10 homes for a year” or “that’s about $1,200 worth of electricity” are more helpful.

• Include a simple call to action that is relevant to the specific segment. For example, “Consider signing up for a time of use rate” or “Your usage is 30% higher than the same month last year. Check to see you’re not leaving your computers on at night.”

With proper planning and consumer insight, utilities and others can deliver products and services that drive higher consumer engagement and satisfaction.

It is critical that customers see an immediate benefit when Smart Grid

technology is installed

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

19

Theme 5: Consumers Value Clean energyWhile saving money is important, consumers have consistently said that they would pay more for products and services they value.

In Consumer Pulse Wave 3, two segments—Concerned Greens and Easy Street—said that the Smart Grid benefit that they thought was most important and were willing to pay for was making it easier to connect renewable energy sources to the grid. The other three segments indicated that preventing outages and reducing the length of those that do occur was their top “important and willing to pay for” benefit.

At What Price?In Consumer Pulse Wave 4, we fol-lowed up on this finding by asking consumers about their likelihood to support programs increasing clean energy generation (including solar, wind, geothermal and biomass), exclusively solar generation, and grid reliability at four different price points.

Notably, for each of the programs tested, support at a $15 per month electricity bill increase was greater than support at $10 per month. We believe that this is a result of some consumers placing a high value on these benefits and being willing to pay to enjoy them.

Also remarkable from these results is that the support for clean energy (and even solar PV by itself) surpasses that for grid reliability. Although we do not know definitively why this is, we think that the primary factor driving these results is that many consumers view reliability as “table stakes”—that is, utilities ought to be investing in reliability without additional charges flowing through to consumers.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

20

Generation at HomeAs shown in the graph on page 16, interest in Smart Grid-enabled technology in the previous theme, 56% of consumers have an interest in installing rooftop solar PV to generate electricity for their homes. An even greater number—nearly two-thirds—of Concerned Greens and Young America indicate interest in solar PV. Although we did not test price points for rooftop solar PV, and actual purchase behavior almost certainly varies depending on price, financing structure, and ease of installation, it is clear the consumers have a strong interest in solar PV—and that there is similar interest in a “DIY” solution as there is to a utility-driven solution.

It is clear from these results that some consumers care a lot about clean energy, and are conceptually willing to pay for it. Utilities and other stakeholders should take a second look at whether consumers in their service territory might be willing to fund new Smart Grid-enabled capabilities that deliver the consumer benefits of clean energy.

56% of consumers have an interest in installing rooftop solar PV to generate electricity for their homes

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

21

Theme 6: The Smart Grid Offers Real Benefits that Consumers Care AboutReal-world experience shows that the benefits of the Smart Grid are not just hypothetical—they’re material, and support benefits consumers say they care about.

In Wave 3 of SGCC’s Consumer Pulse study, we asked consumers which Smart Grid benefits were important to them, and which benefits they’d be willing to pay for:

With the increasing number of utilities that have fully implemented their Smart Grid programs, we are no longer constrained to forecasts of these benefits—we now have actual data that can quantify the level of benefits available to consumers from grid modernization. In our Smart Grid Economic and Environmental Benefits study, we looked at nine distinct Smart Grid capabilities:6

• Integrated Volt/VAr control

• Remote meter reading

• Time-varying rates

• Prepayment and remote dis-/reconnect

• Revenue assurance

• Customer energy management

• Service outage management

• Fault location and isolation

• Renewable generation integration

For all capabilities, we examined research that quantified their direct and indirect economic benefits, reliability benefits, and environmental benefits from reduced greenhouse gas emissions. Outage management and renewable generation integration, in particular, align with the Smart Grid benefits that consumers have indicated are important to them. Additionally, we found that all of the capabilities provide economic benefits to consumers.

6 Please see the Smart Grid Economic and Environmental Benefits study at http://smartgridcc.org/sgccs-smart-grid-environmental-and-economic-benefits-report for detailed descriptions of these capabilities.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

22

Outage ManagementThree out of five segments (DIY & Save, Young America, and Traditionals) report that preventing outages and reducing the length of outages that do occur is the most important benefit that Smart Grid can offer. In total, we found that the Smart Grid can improve reliability by approximately 25%, which equates to a reduction in Customer Average Interruption Duration Index (CAIDI) of 27.2 minutes per year. The capabilities that generate these benefits are:

• FaultLocationandIsolation. By permitting remote diagnostics of the distribution grid and a degree of autonomous “self healing” capability, fault location and isolation constitutes the bulk of the benefit with a 20.5% improvement in reliability (22.3 minute/year improvement in CAIDI).

• ServiceOutageManagement.The “last gasp” capability of many smart meters provides utilities with better intelligence on the location and causes of outages and also helps ensure that all customers are restored prior to service crews leaving an area. These capabilities help reduce outage duration by 4.5% (4.9 minute/year improvement in CAIDI).

Although not directly related to outage management, we found that Integrated Volt/VAr Control can help improve power quality, ensuring that appliances and equipment run at their most optimal efficiency and reducing disruptions to sensitive computer equipment.

Renewable Generation IntegrationTwo out of five segments (Concerned Greens and Easy Street) report that the Smart Grid’s ability to more easily accommodate renewable energy integration is the most important benefit that they’d be willing to pay for. By enabling grid operators to more effectively deal with renewables’ intermittency and technical challenges associated with two-way power flows on the grid, the Smart Grid accommodates greater amounts of renewables on the grid.

For example, utilities in California and Hawaii have used Smart Grid technology to allow up to 100% of the minimum load on a distribution line to come from customer-sited renewables. For a typical utility, this is approximately double the 15% of maximum load that IEEE Standard 1547.2 sets.7

7 Although every utility’s—and every distribution line’s—load profile differs, minimum load on a residential feeder is often 30–50% of maximum, so permitting 100% of minimum is at least double the 15% of maximum allowed under IEEE 1547.2.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

23

Though renewable integration is likely the most effective way to decarbonize generation, we also found that Smart Grid can drive a significant amount of energy efficiency and conservation benefits. The capabilities that provide, in aggregate, 55-5928 lbs. CO2e reduction per customer per year include:

• Integrated Volt/VAr control

• Time-varying rates

• Prepayment and remote dis-/reconnect

• Customer energy management

There is consequently an opportunity for industry to educate and engage consumers on how the Smart Grid can contribute to solving climate change apart from its ability to better integrate renewables.

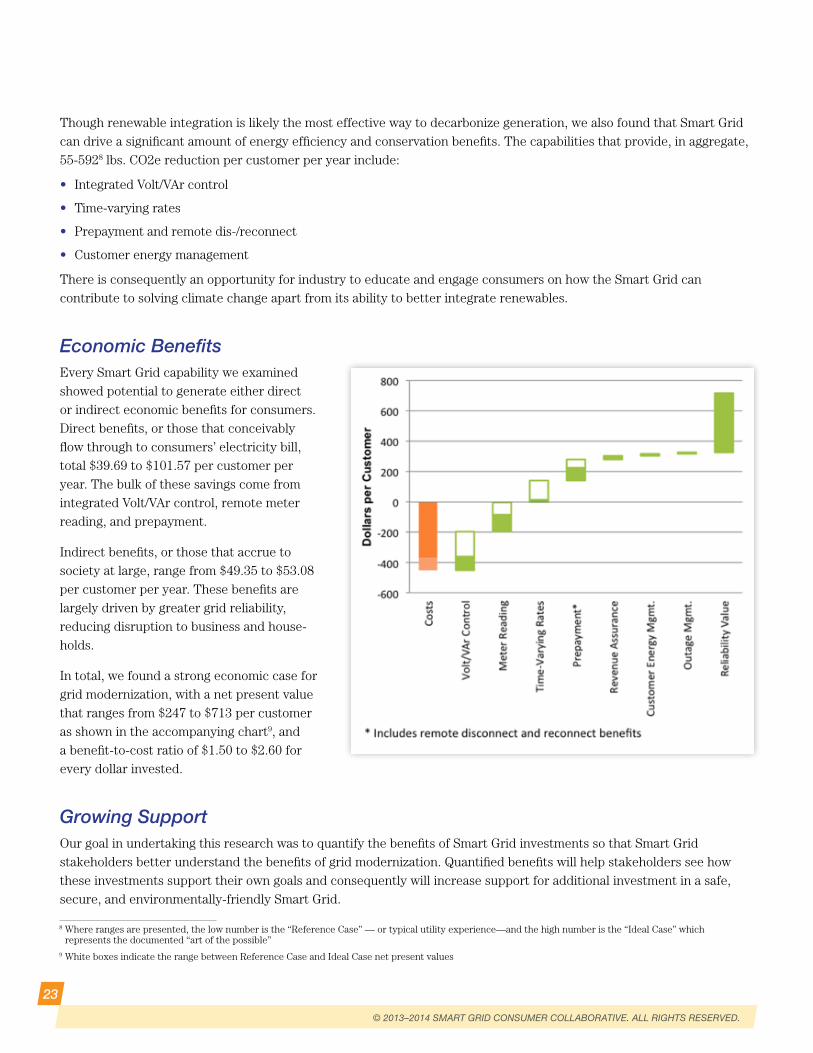

Economic BenefitsEvery Smart Grid capability we examined showed potential to generate either direct or indirect economic benefits for consumers. Direct benefits, or those that conceivably flow through to consumers’ electricity bill, total $39.69 to $101.57 per customer per year. The bulk of these savings come from integrated Volt/VAr control, remote meter reading, and prepayment.

Indirect benefits, or those that accrue to society at large, range from $49.35 to $53.08 per customer per year. These benefits are largely driven by greater grid reliability, reducing disruption to business and house-holds.

In total, we found a strong economic case for grid modernization, with a net present value that ranges from $247 to $713 per customer as shown in the accompanying chart9, and a benefit-to-cost ratio of $1.50 to $2.60 for every dollar invested.

Growing SupportOur goal in undertaking this research was to quantify the benefits of Smart Grid investments so that Smart Grid stakeholders better understand the benefits of grid modernization. Quantified benefits will help stakeholders see how these investments support their own goals and consequently will increase support for additional investment in a safe, secure, and environmentally-friendly Smart Grid.

8 Where ranges are presented, the low number is the “Reference Case” — or typical utility experience—and the high number is the “Ideal Case” which represents the documented “art of the possible”

9 White boxes indicate the range between Reference Case and Ideal Case net present values

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

24

what’s next

Across the country, an increasing number of consumers live in areas with fully deployed AMI and/or significant upgrades in distribution automation. However, our research indicates that the industry has only scratched the surface of consumer awareness and engagement. For many, it is now time to shift into a “post-AMI” mindset and start tackling the next set of Smart Grid challenges, including:

• Enabling and cultivating innovation across the industry;

• Ensuring the security of the Smart Grid;

• Broadening renewable generation.

InnovationJust as the smart phone provided a platform for significant innovation in consumer applications and services, so too does the Smart Grid provide a platform for innovation in generation and energy management. Utilities, established vendors, and startups are all pursuing this to varying degrees, and ultimate success will depend on adopting a “consumer first” mindset and overcoming sometimes significant market barriers.

Nest Labs, manufacturer of the Nest Thermostat, has become an overnight success by developing its thermostat first and foremost as a compelling consumer device. Only after three years on the market have they begun to integrate what many would consider traditional programs (e.g., peak-time pricing) into their service offering. Similarly, new product and service offerings—regardless of where they come from—must focus on solving consumers’ problems with a strong value proposition.

In 2014, SGCC will be conducting research that will offer insight into consumer problems and resonant value propositions. Among other projects, SGCC will be updating its Smart Grid consumer segmentation framework as part of the Consumer Pulse and Market Segmentation Survey Wave V, and will be exploring the motivations and emotions of utility customers who engage with various programs and technologies.

While a “consumer first” approach is necessary to foster innovation in the industry, it is not in itself sufficient. Barriers abound to bringing products and services to market. The regulatory compact varies from state to state, sometimes significantly. Regulators need to develop as deep an understanding about consumer attitudes, behaviors, and needs as utilities and vendors have. We are no longer in a “one size fits all” economy, and although there is not a regulatory silver bullet, the interaction between regulators and utilities needs to acknowledge and accommodate serving individual consumers with products and services tailored to their wants and needs.

Similarly, new business models need to be developed to allow utilities and others to capture the value they create through innovation. The specifics of these business models will vary across the country, but the SGCC believes that innovators need to be able to generate revenue at a level that supports further innovation and investment.

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

25

SecurityThe utility industry takes customer data privacy and the physical security of the grid very seriously. However, it will only take one widely publicized instance of a cyber-attack that shuts off power or compromises consumer information to sour consumers on grid modernization. Consumers are increasingly aware of the vulnerability of information provided to third parties as news of attacks against online service providers such as LinkedIn proliferate. Indeed, nearly one in ten consumers holding an unfavorable view of smart meters cites privacy concerns as reason for their view.

The GridEx II national cyber-security exercise in late 201310 is a great example of how utilities can plan and prepare for security threats. SGCC is pleased that utilities and the federal government organize and participate in these exercises to ensure that grid infrastructure is as safe as possible from potential threats. The more utilities are open and transparent with their customers about the steps they are taking to ensure the security of customer data and the reliability of the grid, the more likely it is that consumers will trust that the utility is managing their data and infrastructure appropriately.

RenewablesIn many parts of the country, renewables are competitive with conventional generation as both centralized and distributed generation. This trend is likely to continue and accelerate as renewable technology manufacturers climb the productivity curve and utilities are forced to increase electricity rates to support the investments they’re being asked to make by customers and policymakers.

In 2014, we anticipate that stakeholders will begin to create clarity around the answers to a number of critical questions such as:

• Who will own the customer relationship?

• How will intermittency challenges be cost-effectively addressed?

• How are grid reliability and grid-provided “backup power” cost-effectively maintained?

In many cases, Smart Grid technology will enable solutions heretofore impossible. The solutions, however, are not merely technical. They will require collaboration between stake-holders to optimize sometimes-competing interests and put consumer experience first.

In many parts of the country, renewables are competitive with conventional generation as both centralized and distributed generation.

10 See http://www.nerc.com/pa/CI/CIPOutreach/Pages/GridEX.aspx for more information on GridEx

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

26

Conclusion

SGCC’s consumer research program is rigorously designed to truly understand consumers and how they relate to the Smart Grid. From these efforts, we have distilled six themes related to how consumers think about and experience grid modernization. The bottom line from all of these themes is that engaging consumers is critical to Smart Grid success.

We have also begun to examine how utilities have produced meaningful benefits to consumers through their grid modernization efforts, and how they have successfully engaged consumers in the process. We know that consumers have a near-universal desire and expectation for utilities to offer energy savings advice, and we know that the energy landscape is changing tremendously. 2014 promises to be a year filled with more home energy management products and services, increased momentum for rooftop solar PV installations, and greater consumer demand for grid resiliency and improved outage communications with each storm event.

By rigorous analyses of reliable data from actual Smart Grid implementations, SGCC research has demonstrated that there’s a strong value proposition for consumers supporting investments in Smart Grid. We’ve also shown how a positive consumer value proposition aligns with the responsibilities and goals of differing stakeholders, from regulators and policymakers to consumer advocates and environmental advocates.

The massive and sustained investments needed to modernize the thousands of individual grids in the U.S. will require a keen understanding by myriad stakeholders of the costs and benefits involved. Utilities with a sound business plan for implementing Smart Grid technologies need an informed, supportive base of customers, as well as support and innovative thinking among other stakeholders, to adapt to changing circumstances and evolving utility business models.

We have only scratched the surface of consumer awareness, education, and empowerment. It is now time for the electric power industry to more fully understand who their customers are and what they want, and it is time for regulators and policy-makers to create new ways for utilities to take risks and help meet consumer demand for energy knowledge and energy savings while maintaining their business integrity.

We hope 2014 is a year that will see more progress in the transformation of the electric power industry into the new world we know is coming: where consumer energy data is widely available to consumers so they are more empowered; where consumers enjoy an array of apps that provide more fun and engagement; and where consumers can sign up for new pricing plans that help them save money while reducing pressure on the grid.

SGCC is committed to doing its part in driving this progress through its consumer research and education programs, and by facilitating collaboration among industry stakeholders. We ask you to join us in this exciting effort.

A p p e n d i x — S G C C C o n S u m e r S e G m e n t S

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

27

• 24% of population

• high levels of education

• highest income of any segment—28% above $100k

• Middle aged, moderate-liberal politics

• fairly diverse: 15% hispanic, 13% african american

• concentrated in the south and Midwest regions

• 17% of population

• Middle-income

• families; 20% have three or more children at home

• diverse range of ages from 25–65+

• largely white, 12% hispanic

• average levels of education

• conservative politics

EASy STREET

COnCERnED GREEnS

yOUnG AMERICA

DIy & SAVE

TRADITIOnALS

• 14% of population

• Predominantly older (25% are age 65+)

• the most politically conservative and religious segment

• higher concentrations in the west and south regions

• relatively low levels of education

• average income

• More men than women

• Mostly white

• 25% of population

• Highest levels of education

• High income—23% above $100K

• Moderate/liberal politics

• Higher concentrations in Northeast and West regions

• Middle-aged (65% are between 25–54 years of age)

• More women than men

• Largely White, 14% Hispanic

SEGMEnT: KEy CHARACTERISTICS:

• 20% of population

• Youngest and most ethnically diverse segment

• Lowest levels of education and income

• Least likely to have kids under 18 at home

• Likely to live in apartments/condos/mobile homes

• Concentrated in the South and Midwest regions

A p p e n d i x — S G C C C o n S u m e r S e G m e n t S

© 2013–2014 SMART GRID CONSUMER COLLABORATIVE. ALL RIGHTS RESERVED.

28

DISTInCTIVE ATTITUDES AnD BEHAVIORS: COnSUMER EnGAGEMEnT OPPORTUnITIES:

• Most concerned and active regarding environmental issues

• High smart grid knowledge, favorability, and support

• Most likely to participate in smart grid programs

• Eager to buy new products and technologies

• Want to save energy for the future of our children and grandchildren and for the environmental benefits; not as concerned about saving money

• Segmentisreceptivetoenvironmentalconcernsandtriestoprotecttheenvironmentthroughtheirownactions.

• Thissegmentisthemostnaturallyinclinedtowardparticipatinginenergyefficiencyandsmartgridprograms.

• Theylikenewtechnology,andhavetheresourcestomakeinvestmentsinbetterenergymanagement.

• Highest level of concern regarding environmental issues

• Think energy efficiency is important, but lack knowledge of how it works and feel they may have already done all they can to save energy

• Say they have low likelihood to participate in smart grid programs, but they are interested in using information from a smart meter for energy management

• They say the most important reasons to save energy are saving money and for the future of our children and grandchildren

• Theprimaryfocusincommunicationwiththissegmentshouldbeeducation.

• Theyareconcernedaboutenvironmentalissuesandfacefinancialconstraints—letthemknowhowSmartGridproductsandprogramscanhelpaddressboth.

• Maybeconsideredalongertermdevelopmentalopportunity,astheymatureandbecomemorelikelytobehomeowners.

• Low levels of interest in smart grid programs or using smart meter information for energy management

• Moderately concerned about the environment at a global level, but not interested in making individual-level environmental efforts

• Believe global warming is real and the government should do more to promote energy efficiency and alternative fuel sources

• Low likelihood to try to minimize impact on the environment through daily actions

• Believe the most important reason to save energy is for the environmental benefits, followed by “for children and grandchildren,” then saving money

• EasyStreetcustomersareunlikelytoexhibitahighlevelofengagementwithenergymanagement.Simplicityandease-of-usearekeystoacceptance.

• Messagingshouldemphasizeenvironmentalbenefitsandstewardshipforfuturegenerations.

• Itwillbeachallengetomotivatethemtochange;theyaresatisfiedwiththeircurrentenergyconsumptionhabitsandexpenditures.

• high levels of interest in smart grid programs, especially toU pricing, primarily for the financial benefits

• believe the most important reason to save energy is to save money

• high percentage of homeowners, and 84% agree they like to “do it themselves” to save money

• low level of environmental interest and involvement

• not motivated to minimize impact on the environment through daily actions

• Most likely segment to say “religion guides the way i live”

• Productandprogramdesignandmessagingshouldemphasizesavingmoneyandde-emphasizeenvironmentalbenefits.

• ThereareopportunitiestomarketproductsandprogramsthatleveragetheirDIYinterestandexperience.

• Consideroutreachthroughreligiousaffiliationsandcommunities.

• least favorable segment toward smart grid programs

• lowest interest in monitoring energy usage

• least engaged in environmental issues

• Prefer comfort and saving time and effort over saving energy

• feel their financial situation compared to a year ago is worse

• Segmentisprobablynotahighpriorityinitialtargetforsmartgridprograms.

• Program/productdesignandpromotionforthissegmentshouldemphasizeimmediatemoneysavingsandde-emphasizeenvironmentalconsiderations.

• Messagingmayalsocommunicatethatenergyefficiencycancontributetohavingacomfortablehome.

SGCC is a consumer focused non-profit organization aiming to promote the understanding and benefits of modernized electrical systems among all stakeholders in the United States. Membership is open to all consumer and environmental advocates, technology vendors, research scientists, and electric utilities for sharing in research, best practices, and collaborative efforts of the group.

Join @ www.smartgridcc.org.

© 2014 Smart Grid Consumer Collaborative. All rights reserved.

Working for a consumer-friendly, consumer-safe smart grid