2013 annual report - ministry of health · 2019-09-26 · 6 municipal employees’ pension plan •...

TRANSCRIPT

2013

Municipal Employees’ Pension Plan

Annu

al R

epor

t

1Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Letters of Transmittal 2

Chair’s Comments 3

Financial Highlights 4

Plan Profile 6

Municipal Employees’ Pension Commission 7

Commission Goals & Values

Education

Contracted Services

Plan Expenditures and Statistics 12

Strategic Initiatives 17

Customer-oriented Communications & Service

Maintain the Financial Integrity of the Plan

Plan Governance

Accountability

Risk Management 22

Investments 26

Trustees

Investment Policy

Investment Consultant

Custodia

Investment Objectives

Management’s Report 30

Actuaries’ Opinion 31

Financial Statements 33

Independent Auditor’s Report

Statement of Financial Position

Statement of Changes in Net Assets Available for Benefits

Statement of Changes in Pension Obligations and Provision

for Annuity Obligations

Notes to the Financial Statements

Appendix ‘A’ - Description of Market Indices 61

This annual report is available in electronic format at www.peba.gov.sk.ca

Table of contents

2 Municipal Employees’ Pension Plan • Annual Report • 2013

Her Honour, The Honourable Vaughn Solomon Schofield Lieutenant Governor of the Province of Saskatchewan

May it Please Your Honour:

I respectfully submit the Annual Report of the Municipal Employees’ Pension Plan for the year ending December 31, 2013.

Ken Krawetz Minister of Finance

The Honourable Ken Krawetz Minister of Finance

Sir:

On behalf of the Municipal Employees’ Pension Commission, I have the honour of submitting the Annual Report of the Municipal Employees’ Pension Plan for the year ending December 31, 2013.

Betty Moleski Chair

Ken KrawetzMinister of Finance

3Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Betty MoleskiChair

As the new chair of the Municipal Employees’ Pension Plan, I would like to take this opportunity to thank the dedicated members of the 2013 Commission. I want to specifically recognize the leadership of outgoing chair, Bonnie Ozirny, for her support, leadership and continued insights and contributions.

After another year of thorough plan management, we continue to evaluate MEPP’s current and future challenges and work to find solutions. As a defined benefit plan, financial pressures will exist and flexible and realistic options must be explored to address matters such as Plan sustainability.

A changing pension environment framed our decisions this past fiscal year and ensured we set a sound strategic direction to move the Plan forward. As a result, the Commission continues to be committed to strong governance practices and attentiveness, which will lead into a thorough consultative process with our members in 2014. This process will ensure all members are aware of the long term vision, ongoing management and future sustainability of the Plan.

With an increasing demand for quality and timely services, the Commission has continued to improve MEPP’s capabilities and capacities to deliver pension services to members. We continue to offer an array of valuable retirement planning tools and workshops, which includes the ability to access

one-on-one meetings with our Retirement Information Consultants. In addition, we expanded communication offerings in 2013 and are focused on rebuilding our current website to offer modern and interactive communication channels that will be more beneficial to our members.

In 2014, the MEPP Commission will strive to again achieve our mission and key values through diligent plan monitoring. As we reach out during consultations this year, we will act in a transparent and balanced manner so our members can trust that plan management is conducted with the highest integrity.

On behalf of the MEPP Commission, I am pleased to present the Municipal Employees’ Pension Plan Annual Report for the year ended December 31, 2013.

Betty Moleski Chair

4 Municipal Employees’ Pension Plan • Annual Report • 2013

17.6

11.2

18.9

25.4 26.3

20.5 19.6

04 05 06 07 08 09 10 11 12 13

16.6

25.6

31.1

(as at December 31, 2013)

32.3 33.3 35.8 39.6 42.8 45.956.7

04 05 06 07 08 09 10 11 12 13

70.9 74.7

86.5

31.233.8

36.6 38.6 41.0 43.4 45.7

04 05 06 07 08 09 10 11 12 13

48.5 51.454.8

1,399

1,1481,258

1,3921,415

1,1511,285

04 05 06 07 08 09 10 11 12 13

1,3951,561

1,685

Transfers, Refunds & Termination Payments ($ millions)

1.68 bil l ion$

ToTal asseTs

2013 Financial highlights

$86.5 million NeT CoNTribuTioNs

$54.8 million ToTal PeNsioN Payroll

Total Assets ($ millions) Pension Payroll ($ millions)

Total Contributions & Transfers-In ($ millions)

5Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Total MEPP Fund Investment Performance (%)

2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Total Fund Real Return 9.6 14.5 0.6 10.0 14.5 (16.2) 4.2 13.6 12.1 11.4

Benchmark 8.6 10.8 0.4 10.1 15.5 (17.7) 3.3 12.9 10.6 9.8

Rolling 4-year Average Returns (%)

Total Fund Real Return 7.8 9.8 1.5 2.4 3.2 2.7 10.3 13.0 8.9 6.5

Benchmark 7.6 9.4 0.1 1.9 2.7 1.7 9.3 12.0 6.9 3.4

Comparative Investment and Administration Costs ($ thousands)

2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Administrative Costs 4,997 4,894 4,922 4,048 3,654 3,162 2,822 2,540 2,328 2,051

Custodial fees 786 518 141 155 167 210 207 128 131 128

Investment fees 7,865 5,498 4,655 4,254 4,828 6,112 3,906 3,237 2,708 2,296

Totals 13,648 10,910 9,718 8,457 8,649 9,484 6,935 5,905 5,167 4,475

23.3 thousandPlaN members 4.8 thousand PeNsioNers

average age of aCTive members 47.1

M e m b e r s S e r v e d

6 Municipal Employees’ Pension Plan • Annual Report • 2013

The Municipal Employees’ Pension Plan (MEPP or the Plan) is a ‘defined benefit’ plan. Pensions are based on a formula that provides pension, disability, death and termination benefits for all eligible members. The formula is based on highest average salary, pensionable service and the accrual rate in effect during the years of service. Members contribute a fixed percentage of salary. Employers match these contributions.

The amount of pension a member will receive is not directly related to investment returns. An adequate level of contributions and positive investment returns are necessary to secure the Plan’s ability to pay benefits.

Under normal retirement rules, members may retire and receive a pension with no reduction if they are 65 years of age, or if their age and eligibility service equal at least 80 years. Members may retire and receive a reduced pension if they have reached age 55 and have at least 15 years of eligibility service.

Designated firefighters and police officers may receive an unreduced pension if their age and eligibility service equal at least 75, they are 55 years of age, or they have at least 25 years of eligibility service. These members may retire and receive a reduced pension if they have reached age 45 and their age and eligibility service equal at least 70.

MEPP’s history begins in the 1940s. Initially, the Rural Municipal Secretary Treasurer’s Superannuation Plan was established in 1941. In 1949, the Urban Employees’ Superannuation Plan was established. In 1959, these two plans joined to form the Municipal Employees’ Superannuation Plan, which became the current plan in 1973.

MEPP is registered under the Income Tax Act (Canada) and is governed by The Municipal Employees’ Pension Act and related regulations, and The Pension Benefits Act, 1992 and related regulations.

The Plan holds close to $1.7 billion in total assets. MEPP’s membership consists of more than 23,000 members; of which 4,800 are pensioners.

Your plan

7Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

The Municipal Employees’ Pension Commission (the Commission) administers MEPP. The Commission has the fiduciary responsibility for administering MEPP and managing the investment activities in the best interests of all MEPP members.

Our MissionTo oversee and direct the administration of the Plan and manage the assets in the best interests of members.

Our Goals• Provide customer-oriented communications and service:

The Commission is determined to ensure that all Plan stakeholders have access to pension services and information which meet their needs.

• Maintain the financial integrity of the Plan: The Commission is committed to achieving the needs of Plan members and employers through affordable, sustainable Plan benefits and services.

• Plan Governance: The Commission strives to demonstrate leading practices of pension plan governance.

• Accountability: Performance of the Plan and the Commission’s service providers is managed, measured and reported.

Our Values• Accountability: We are accountable to the members and the

stakeholders of MEPP for our administration of the Plan. We operate in a transparent manner.

• Professionalism: We strive for excellence in the administration of MEPP by being diligent and making informed decisions.

• Integrity: As trustees of the Municipal Employees’ Pension Fund, we hold ourselves to the highest standards of integrity. We strive to act always with honesty and in a manner worthy of the trust our members have placed in us.

• Fairness: We administer MEPP in the best interests of all members of the Plan. We strive to ensure that our decisions are equitable for all Plan members by adhering to decision making that is fair and open-minded. Our actions are courteous, considerate and responsive.

The commission

8 Municipal Employees’ Pension Plan • Annual Report • 2013

AttendanceThe Commission met nine times in 2013. Table 1.1 shows the number of meetings each Commission member attended.

The Commission has 10 members, five appointed on behalf of participating employers and five on behalf of employees. The full term of office for Commission members is four years. A member may be appointed for two full terms. Each year the Commission

members elect a Chair and a Vice-Chair. The Chair and Vice-Chair are elected for a one-year term. At December 31, 2013, the Commission was composed of the members listed below.

Bonnie Ozirny, ChairSaskatchewan School Boards Association

Betty Moleski, MemberTrade Unions representing employees who are members of the Plan

Rory Griffith, Vice-ChairThe Saskatchewan Association of School Business Officials

Ray Orb, MemberThe Saskatchewan Association of Rural Municipalities

Randy Goulden, MemberThe Saskatchewan Urban Municipalities Association

Brad Hvidston, MemberThe Urban Municipal Administrators’ Association of Saskatchewan

Beverly Crossman, MemberRegional Colleges/Regional Libraries

Wayne Steen, MemberSaskatchewan School Boards Association

Don McCallum, MemberThe Rural Municipal Administrators’ Association of Saskatchewan

Randy Hurd, MemberAssociations representing Designated Police Officers and Firefighters

Name Number of Meetings Attended Name Number of Meetings Attended

Bonnie Ozirny 9 Allan Johnson* 6

Rory Griffith 9 Earl Braun* 6

Randy Goulden 8 Orrin Redden* 6

Don McCallum 5 Brad Hvidston** 3

Betty Moleski 9 Beverly Crossman** 3

Ray Orb 4 Randy Hurd** 3

Wayne Steen 8Table 1.1

* These Commission members’ appointments ended August 31, 2013. They attended 100 per cent of meetings they were eligible to attend during their appointment.

** These Commission members’ appointments began September 1, 2013. They attended 100 per cent of meetings they were eligible to attend during their appointment.

9Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

The Commission has an education program for its members. The purpose of this program is to ensure the Commission members possess a sound knowledge and understanding of pension, investment and governance issues. The Commission budgets $5,000 per year for each Commission member for educational registration fees.

Upon appointment to the Commission, new members receive information outlining the documents that come before the Commission, the Municipal Employees’ Pension Plan member booklet, the Annual Report, information on the budget, funding policies, the Statement of Investment Policies and Procedures (SIP&P), the Strategic Business Plan and updates, the Risk Management plan and most recent review, as well as the meeting minutes for the past year.

Within three months of appointment, members will receive an orientation provided by the Public Employees Benefits Agency’s (PEBA) Executive Management.

Commission members have a formal education program that they are required to attend. The program provides a list of courses and seminars that deliver content specific to investment-related, funding-related and governance-related information:

• Within one year, members must attend education sessions on basic investment principles and on basic actuarial principles. Also, members are to attend the Queen’s Governance Program facilitated by Queen’s School of Business, Queen’s University.

• Within two years, members must complete the Board Effectiveness Program presented by the International Centre for Pension Management at the Rotman School of Management, University of Toronto.

Commission members who have completed the formal education program are required to attend one educational event annually that is facilitated by an industry-recognized pension and benefits organization. A Commission member who is actively pursuing the formal education program is exempt from the ongoing developmental requirements for members. However, all members are strongly encouraged to attend an educational event.

Conferences and other events attended by Commission members as part of their ongoing education provide the Commission with information on the current governance, investment and legal environment affecting pension plans. They also provide opportunities for Commission members to meet with pension experts and trustees from other plans to discuss common issues.

Table 1.2 lists the education events attended by Commission members to December 31, 2013.

educaTion

10 Municipal Employees’ Pension Plan • Annual Report • 2013

Education Events Attended by Commission Members in 2013

Commission Member Course

TotalRegistration

FeesTotal

HonorariumTotal Other Expenses Total

Betty Moleski Rotman Board Effectiveness Program $ 6,950.00 $ 1,750.00 $ 1,836.01 $10,536.01

Bonnie Ozirny British Columbia Public Sector Pensions and Benefits Conference

Canadian Pension and Benefits Institute Forum 2013

46th Annual Canadian Employee Benefits Conference

$ 1,925.00 $ 3,921.30 $ 6,070.98 $11,917.28

Brad Hvidston Queen’s Governance Program $ 4,100.00 $ 1,882.00 $ 1,366.50 $ 7,348.50

Don McCallum Investment Basics

Mercer School of Pension Investment Management$ 2,700.00 $ 1,677.50 $ 2,446.21 $ 6,823.71

Randy Goulden Investment Basics Complimentary $ 120.00 $ 195.36 $ 315.36

Ray Orb Rotman Board Effectiveness Program $ 6,950.00 $ 1,549.00 $ 1,862.47 $10,361.47

Rory Griffith Deloitte Transformational Transactions: the Board’s Role

Rotman Board Effectiveness Program$ 6,950.00 $ 1,750.00 $ 1,934.84 $10,634.84

Wayne Steen Investment Basics

Queen’s Governance Program$ 4,100.00 $ 1,805.40 $ 1,148.27 $ 7,053.67

Earl Braun British Columbia Public Sector Pensions and Benefits Conference

$ 500.00 $ 1,000.00 $ 1,361.04 $ 2,861.04

Totals $34,175.00 $15,455.20 $18,221.68 $67,851.88

Table 1.2

11Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Contracted Services The Commission is ultimately responsible for the Plan’s administration, communication and investment activities. To discharge these responsibilities, the Commission uses the services of various organizations.

The Commission contracts with the PEBA to provide executive management and administrative services for the Plan. PEBA is part of the Ministry of Finance, Government of Saskatchewan, and administers a wide range of pension and benefits plans.

Under contract with the Commission, PEBA:

• maintains all member and accounting records;

• collects and deposits contributions to the Municipal Employees’ Pension Fund (the Fund);

• transfers contributions to the custodian of the Fund for investment;

• monitors, administers and assists in the execution of the Plan’s investment program in accordance with the investment policy;

• determines coverage and eligibility for benefits;

• calculates and pays all pension benefits;

• communicates with members and participating employers;

• recommends an actuary as an advisor to PEBA and the Commission, and retains an actuary selected on behalf of the Commission;

• recommends policy regarding calculating rates of interest and implements and calculates the rates of return for the plan; and

• prepares the annual report.

PEBA is responsible for ensuring that all transactions are made in accordance with The Municipal Employees’ Pension Act, The Pension Benefits Act, 1992, and their related regulations.

The Commission retains RBC Investor Services Trust as the Plan custodian, Aon Hewitt as the Plan actuary, and Mercer (Canada) Limited as the investment consultant. The Commission also retains the investment managers listed in Table 1.10 on page 27 of this report.

12 Municipal Employees’ Pension Plan • Annual Report • 2013

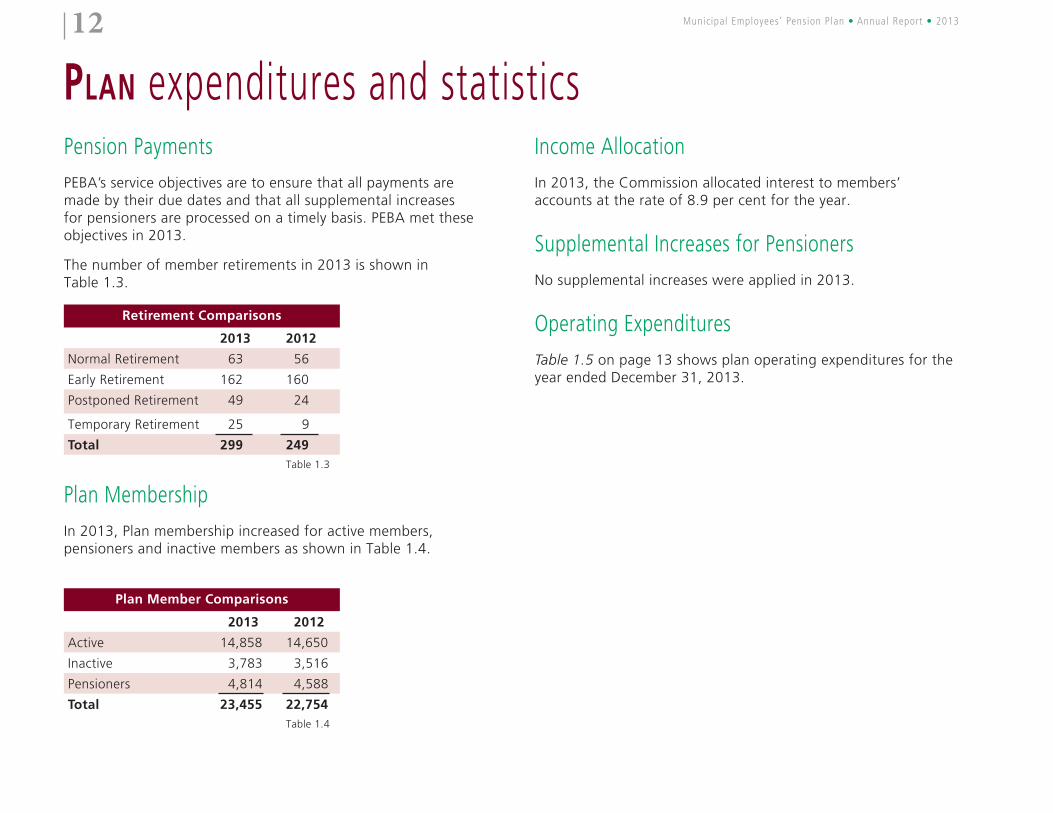

Pension PaymentsPEBA’s service objectives are to ensure that all payments are made by their due dates and that all supplemental increases for pensioners are processed on a timely basis. PEBA met these objectives in 2013.

The number of member retirements in 2013 is shown in Table 1.3.

Retirement Comparisons

2013 2012

Normal Retirement 63 56

Early Retirement 162 160

Postponed Retirement 49 24

Temporary Retirement 25 9

Total 299 249Table 1.3

Plan Membership In 2013, Plan membership increased for active members, pensioners and inactive members as shown in Table 1.4.

Plan Member Comparisons

2013 2012

Active 14,858 14,650

Inactive 3,783 3,516

Pensioners 4,814 4,588

Total 23,455 22,754Table 1.4

Income Allocation In 2013, the Commission allocated interest to members’ accounts at the rate of 8.9 per cent for the year.

Supplemental Increases for Pensioners No supplemental increases were applied in 2013.

Operating ExpendituresTable 1.5 on page 13 shows plan operating expenditures for the year ended December 31, 2013.

Plan expenditures and statistics

13Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Expenses ($ thousands)Total Cost (%)

Administration costs / Investment consultant fees $4,997 36.61

Custodial fees 786 5.76

Investment management fees

Global Infrastructure Partners - C, LP 2,014 14.76

Greystone Managed Investments Inc. 425 3.11

Foyston, Gordon & Payne Inc. 436 3.20

Brandes Investment Partners, LP 510 3.73

BlackRock Asset Management Canada Ltd. 56 0.41

Snyder Capital Management, LP 637 4.67

Pareto Investment Management Ltd. 90 0.66

Steel River Infrastructure Fund North America, LP 1 0.01

TDAM Fixed Income Overlay 501 3.67

Canso Investment Domestic Portfolio 329 2.41

PIMCO Investments Global Shadow A/C 374 2.74

Wellington Management Global Shadow 265 1.94

GIP II 581 4.26

Global Transition Account 6 0.04

CGOV Asset Management 441 3.23

Schroder Investment Management North America Inc. 334 2.45

Vontobel Asset Management, Inc. 528 3.87

Private Equity 337 2.47

$13,648 100.0Table 1.5

14 Municipal Employees’ Pension Plan • Annual Report • 2013

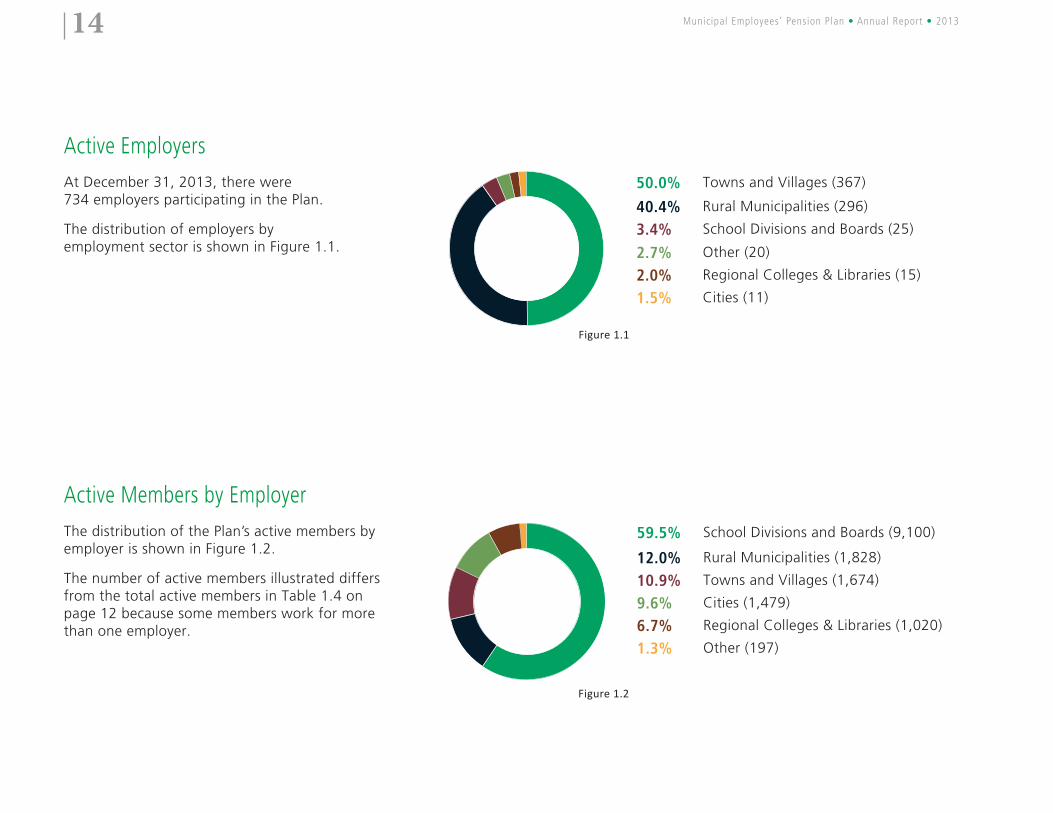

Active EmployersAt December 31, 2013, there were 734 employers participating in the Plan.

The distribution of employers by employment sector is shown in Figure 1.1.

Active Members by EmployerThe distribution of the Plan’s active members by employer is shown in Figure 1.2.

The number of active members illustrated differs from the total active members in Table 1.4 on page 12 because some members work for more than one employer.

Figure 1.1

50.0% Towns and Villages (367)

40.4% Rural Municipalities (296)

3.4% School Divisions and Boards (25)

2.7% Other (20)

2.0% Regional Colleges & Libraries (15)

1.5% Cities (11)

59.5% School Divisions and Boards (9,100)

12.0% Rural Municipalities (1,828)

10.9% Towns and Villages (1,674)

9.6% Cities (1,479)

6.7% Regional Colleges & Libraries (1,020)

1.3% Other (197)

Figure 1.2

15Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

PEBA Service Standards January 1, 2013 to December 31, 2013

CompletedNumber that Meet or Exceeded Standard

% that Meet or Exceeded Standard

*Standard (Business Days and % Target)

Statement on Termination (Option Letter) 1,707 1,611 94.4 20* 75%

Statement on Death (Active/Deferred) (Option Letter)

34 29 85.3 10 80%

Statement on Death (Pensioners) (Option Letter) 166 163 98.2 10 80%

Payments (includes on termination and death) 1,536 1,381 89.9 10 80%

Payment of New Retirements 272 262 96.3 15* 80%

Pension Estimates (Retirement Option Letter) 486 452 93.0 10* 90%

Marriage Breakdown Calculations 52 48 92.3 10* 75%

Purchase of Service 28 25 89.3 20* 80%

Portability Transfer Values 21 20 95.2 30 80%

Total 4,302 3,991 92.8Table 1.6

PEBA Periodic Requirements January 1, 2013 to December 31, 2013

CompletedNumber that Meet or Exceeded Standard

% that Meet or Exceeded Standard

*Standard (Business Days)

Annual Member Statement 1 1 100.0 75

Budget Variance Reporting 4 4 100.0 Quarterly

Proposed Annual Budget 1 1 100.0 Annually

Performance Measurement 4 4 100.0 Quarterly

Decisions Affecting Stakeholders 0 0 n/a 1 Month

Newsletter (MEPP Matters) 2 2 100.0 Semi-annually

Total 12 12 100Table 1.7

* Standard is set within the contract between the Commission and PEBA

PEBA reports measurement against standards to the Commission quarterly. Table 1.6 and Table 1.7 provide measurement results for the 2013 year.

16 Municipal Employees’ Pension Plan • Annual Report • 2013

LEFT TO RIGHT: Rory Griffith, Beverly Crossman, Brad Hvidston, Ray Orb, Jeff McNaughton, Don McCallum, Betty Moleski, Randy Hurd, Randy Goulden

NOT PICTURED: Wayne Steen

17Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

In May 2011, the Commission reviewed and amended its three-year strategic business plan for the period 2011 to 2013.

The strategic business plan sets out goals for the planning period in four major categories:

The strategic business plan was developed as part of the Commission’s comprehensive governance process, which includes regular strategic business planning and risk management planning. It was developed within the context of the Plan’s purpose, mission and goals, and the Commission’s values of accountability, professionalism, integrity and fairness.

The new strategic business plan considers a number of internal and external factors.

This annual report will provide reporting for the strategic initiatives completed in 2013 and other activities accomplished in 2013.

STraTegic initiatives

Maintain the Financial Integrity of the Plan

Plan Governance Accountability

The Commission is determined to identify, assess and, where appropriate, implement opportunities to add value to the services the Plan provides

to its members.

The Commission is committed to achieving the needs of Plan members and employers through a�ordable, sustainable Plan bene�ts and services.

The Commission strives to demonstrate leading practices in pension plan governance.

Performance of the Plan and the Commission’s service providers is measured, managed, and reported.

Customer-orientedCommunications and Service

...flexible and realistic options must be explored to address matters such as Plan sustainability

18 Municipal Employees’ Pension Plan • Annual Report • 2013

The Commission’s objectives:

• Support member understanding of the Plan, including individual member benefits and responsibilities.

• Provide relevant, timely and accurate information which is easy to understand.

• Support participating employers.

• Maintain an up-to-date suite of services that meet evolving member needs.

The Commission has a number of ongoing communication strategies that are designed to inform members and employers about the Plan, including:

• A stakeholder consultation process.

• Plan overview presentations for employers and employees.

• Plan member retirement workshops.

• Print materials that include the MEPP Matters newsletter, the MEPP Member Booklet, the MEPP In-Depth publications for specific Plan issues, and quarterly MEPP Employer Bulletins. These materials are available on the Plan’s website.

• The MORe retirement planner is available on the Plan website.

Activities planned and accomplished in 2013

Communicate the value of the Plan.

The content audit of the website has been completed. Updating the format of the website will continue into 2014 as significant changes are needed to the content management system in order to modernize web viewing compatibility to include contemporary content styles.

Expand uses for the Employer Remittance System.

Online forms for enrolling Plan members and updating Plan member information were implemented in November 2013.

Electronic media.

E-mail communications are now provided to members who prefer to receive their pension information electronically. Member statements are not included at this time but investigation continues into the feasibility of a secure way for members to view their statements online.

Customer-oriented communications and service

19Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Maintain the financial integrity of the plan

The Commission’s objectives:

• Maintain Plan funding that will be able to pay promised benefits in full as they come due while keeping contribution rates stable over the long term.

• Ensure Plan design includes benefits that meet the needs of all stakeholders.

• Identify, assess and manage the Plan’s financial risks.

The Commission has implemented a funding policy that monitors the ability of the Plan to pay benefits on a fully-funded basis. The policy includes established target ranges that the Commission uses to make decisions concerning plan contributions and benefit levels.

Activities planned and accomplished in 2013

The Commission will conclude a plan design study that will form the basis for consultations with the Plan’s stakeholders – this will determine whether or not changes in legislation are required.

The Commission completed its plan design study. Stakeholder consultations are to take place in 2014.

Over 140%

Temporary bene�t increasesIndexation of bene�tsContribution decrease

Funding Level

125% - 140%

Indexation of pensionsContribution decrease

115% - 125%110% - 115%Up to110%

Watch contribution levelsContribution increase to

maintain funding

Keep Contribution and bene�t levels

steady

Indexation of pensions for current year

Considerations

105%Minimum

Funding Target

20 Municipal Employees’ Pension Plan • Annual Report • 2013

The Commission’s objectives:

• The Commission demonstrates that it is a responsible fiduciary.

• Ensure the Plan’s business model, including roles and responsibilities of both the Commission and the contracted service providers, is consistent with the Plan’s strategy and operations.

The Commission employs various tools to achieve its objectives, including:

• The Commission’s member orientation program and its formal and ongoing educational program.

• A comprehensive Governance Manual.

• The development of a Policy Manual.

• The establishment of service standards with the Plan’s administrator.

Activities planned and accomplished in 2013

The Commission will continue to conduct a formal evaluation of the provision of executive management services by its plan administrator.

The Commission received the results of the evaluation of the Public Employees Benefits Agency’s provision of executive management services for the year-ended 2012. These results were discussed at the March meeting.

Plan governance

...the Commission continues to be committed to strong governance practices and attentiveness.

21Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

The Commission’s objectives:

• Understand stakeholder and member information requirements and provide them with information regarding the Plan’s strategy, operations and values.

• Provide relevant and timely reporting on the performance of the Plan, the Commission and service providers.

The Commission demonstrates its accountability to the Plan’s members and employers through:

• Annual self-assessments completed by the Commission.

• The development, implementation and review of the Commission’s Strategic Business Plan.

Activities planned and accomplished in 2013

The Commission will receive proposed measures for the enhanced reporting tool. If the proposed measures are approved, the implementation of enhanced performance reporting for the Plan, the Commission and service providers will commence in late 2013.

Enhanced reporting using the approved measures commenced in 2013.

Accountability

STraTegic initiatives for 2014 - 2016The Commission met in November 2013 for a strategic planning session. This included a review of the values, goals and objectives of the plan as well as identification of the current strategic risks for the Plan. From this planning session, the Strategic Plan for 2014-2016 and the associated initiatives are currently under development.

22 Municipal Employees’ Pension Plan • Annual Report • 2013

Within its mandate, the Commission is responsible for managing risks that could affect the operation of the pension plan, the Plan’s members and other stakeholders. The risk management process provides the Commission and its administrator with the means to identify and evaluate the foreseeable risks in the Plan. Supporting strategies are developed to manage or mitigate these risks.

The Risk Management Plan and its annual review ensure that a regular, documented process is in place that provides rationale for the Commission’s risk management decisions.

In order to assist in the identification and assessment of all foreseeable risks in the Plan, the Commission has identified the following key broad-based risks of the Plan:

riSk management

Broad-based Risks (definition of risk) Key RisksStrategic Risk encompasses the potential risks

as they relate to communication and service delivery, plan design suitability, plan reputation, plan governance and accountability

• Communications and member engagement

• Governance

• Risks to members/Plan stemming from members’ need for advice

Financial Risk relates to the investment, funding, and benefit policies, plan design costs, and demographic considerations

• Market risk

• Funding requirement shortfall

• Changes in cost

• Fraud

Regulatory Risk associates with non-compliance with legislation, fiduciary obligations and the legal requirements of pension plan management

• Non-compliance with legislative requirements

• Failure to meet fiduciary obligations to Plan members and their beneficiaries

Operational Risk includes operational emergencies and non-compliance with governance policies

• Investment manager performance

• Errors or omissions

• Loss of service provider

• Poor performance of service providers

• Capacity to deliver services

Table 1.8

23Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

The Commission believes that these broad-based risks are integrated with each other and with the processes of the Plan. Therefore, the Commission has to retain a balanced approach in the management of all four types of risk.

The Commission has developed and implemented the following strategies and ongoing business practices to manage these risks:

• The Commission recognizes the need to maintain a healthy Plan for all stakeholders. A stakeholder consultation process provides employers and Plan members with the opportunity to consider the affordability of the benefits provided and the contributions needed to fund these benefits.

• The design of the Plan is a key element of the overall financial security of its members and an important component of employers’ human resources strategies. It is this recognition that prompted the Commission to take proactive measures to ensure the health of the Plan through a formal funding policy.

• The funding policy enables the Commission to be proactive in managing the financial status of the Plan and helps to facilitate communication with stakeholders on the status of the Plan.

• The Commission implemented a Statement of Investment Policies and Procedures (SIP&P) that outlines the Commission’s investment beliefs and provides for risk management through diversification of asset classes, capital markets and investment managers. The Commission annually reviews the SIP&P.

• The Commission communicates investment performance. Monitoring of investment performance is carried out by PEBA and Mercer (Canada) Ltd.

• The Commission ensures initiatives and Plan related activities are adequately funded through its budgeting process.

• The Commission reviews the performance standards for the Commission’s administrator quarterly, investment consultant annually, investment managers quarterly, and custodian semi-annually.

• The Commission annually evaluates the performance of the executive management services provided by its administrator.

• The Commission requires that service providers confirm that they maintain business continuity plans and adhere to a code of conduct.

• The Commission’s administrator has internal controls in place. These controls are audited annually.

There are two levels of audit:

• The Commission retains Deloitte LLP to conduct an audit of the Plan.

• The Provincial Auditor of Saskatchewan reports to the Legislative Assembly regarding the audit of the Plan.

• The Commission has an Acquisition and Retention of Services policy that details how the Commission is to retain and evaluate service providers.

• The Commission’s administrator reviews and reports compliance with legislative requirements annually.

• The Periodic Checklist is a list of major items identified by the Commission that are necessary for the prudent administration of a pension plan. The checklist allows verification that an activity has been carried out. The completed Periodic Checklist is provided to the Commission on a semi-annual basis.

• Commission members are required to review and sign the Commission’s Code of Conduct and Conflict of Interest Procedures at least annually.

24 Municipal Employees’ Pension Plan • Annual Report • 2013

• The Commission has outlined the education required to aid Commission members in executing their fiduciary and governance duties.

• The Commission formally reviews its Strategic Business Plan on a periodic basis.

• The Commission regularly consults with legal counsel and other expert advisors regarding issues on which it is deliberating.

• The Commission retains service providers who are experts in the responsibilities to which they are assigned with respect to the Plan.

• PEBA staff provides retirement information seminars and individual information to Plan members.

• Information tools include member and employer seminars, employer bulletins and guides, website information, and written materials.

Activities planned and accomplished in 2013

The Commission will continue to work with its administrator and actuary on the review of the current Plan design for MEPP and the potential options for future plan design to determine if changes in legislation are required.

The Commission completed its plan design study. Stakeholder consultations are to take place in 2014.

The Commission will conduct an evaluation of executive management services for 2012 in the first quarter of 2013.

The Commission received the results of the evaluation of executive management services for 2012 at its March 2013 meeting. An evaluation of 2013 services will be received in March 2014.

The Commission will initiate an enhanced risk management process to monitor risks to the Plan.

A review of the enhanced risk management assessment was conducted in November 2013 that resulted in the identification of a number of key risks to the Plan and the development of incremental strategies to further manage these risks. This process more directly relates the risk management process with strategic business planning and other governance processes.

The Commission will conduct a review to confirm that all of its service providers maintain a Business Continuity Plan.

The Commission conducted a review and received confirmation that all of its service providers maintain a Business Continuity Plan and that their staff abide by a code of conduct/conflict of interest policy.

25Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Risk Management Activities Planned for 2014

The Risk Management review identified ways to incrementally strengthen risk management strategies for the key broad-based risks.

Incremental strategies identified for 2014:

Strategic Risk:

• Examine whether the Plan should provide advice; and

• Implement measures on asset retention.

Financial Risk:

• Continue the sustainability review; and

• Develop a communications plan for the sustainability review.

Operational Risk:

• Continue to monitor and review the process of investment manager oversight.

• Ensure continuous monitoring of the personnel planning process

• Ensure timely implementation of enhanced reporting.

26 Municipal Employees’ Pension Plan • Annual Report • 2013

TrusteesAs trustees of the Fund, the Commission is responsible for prudently investing the Fund’s assets.

Investment PolicyIn fulfilling its responsibility to prudently invest the Fund’s assets, the Commission has adopted an investment policy for the Plan. This policy is set out in the SIP&P, which the Commission reviews annually.

The SIP&P contains guidelines for investment of Plan assets, and includes:

• investment and risk philosophy;

• asset mix and diversification policy, including portfolio return expectations;

• benchmarks for each investment manager and for the Fund;

• permitted investments and quality guidelines;

• monitoring and control responsibilities, including performance targets;

• compliance reporting and monitoring requirements; and

• conflict of interest guidelines.

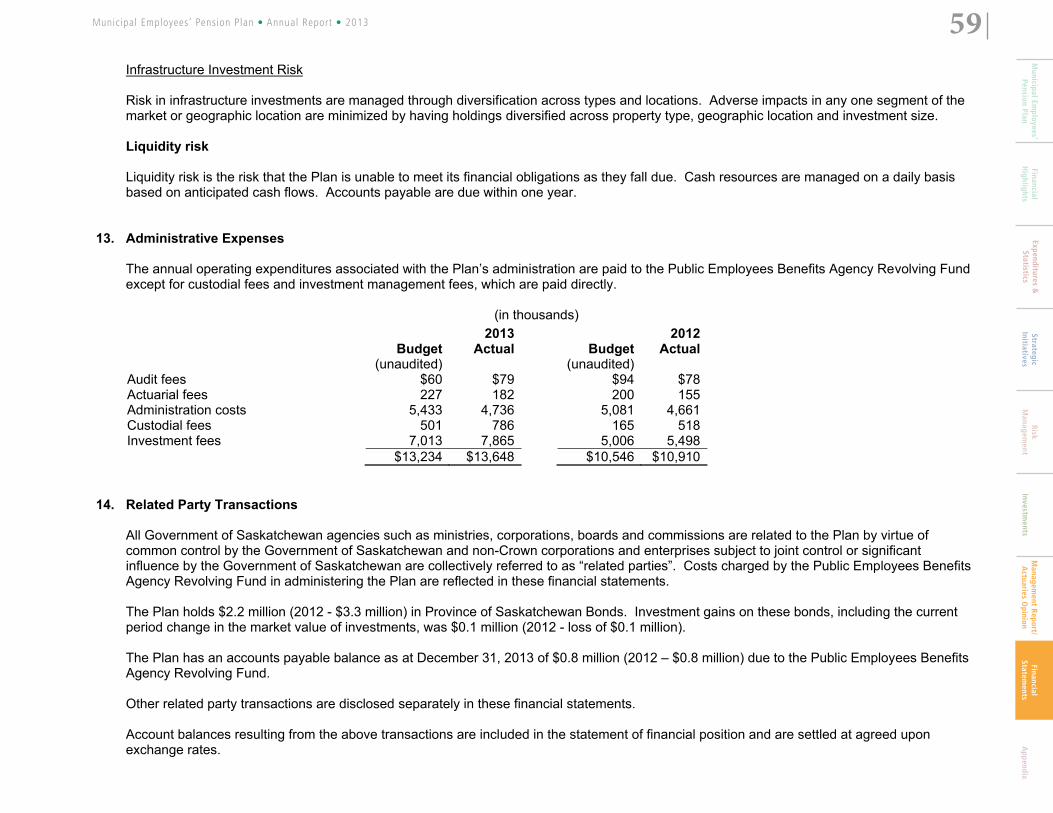

Investment ConsultantThe Plan’s investment consultant is Mercer (Canada) Ltd. In 2013, the investment consultant provided strategic investment guidance, performance monitoring, regular and special project investment consulting, and reports to the Commission. The Commission paid consulting fees of $549,800 in 2013 (Table 1.9).

Fees Paid for Investment Services in 2013

Investment Managers (total) $7,865,000

Investment Consultant 550,000

Custodian 786,000

Total $9,201,000Table 1.9

Investment ManagersThe Commission delegates responsibility for investing the Fund assets to professional investment managers. Each manager invests within a specific mandate, as outlined in Table 1.10. Investment managers were paid a total of $7,865,000 in 2013.

inveSTmenTS

27Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Investments by Investment Manager

Figure 1.3

11.1% Schroder Investment Management North America Inc.

10.9% CGOV Asset Management

10.2% Vontobel Asset Management, Inc.

9.3% Canso Investment Council Ltd.

8.6% PIMCO Canada Corp.

8.2% Wellington Management Company, LLP

8.0% BlackRock Asset Management Canada Ltd.

6.9% TD Asset Management, Inc.

6.8% Foyston, Gordon & Payne Inc.

6.2% Greystone Management Investments Inc.

5.6% Brandes Investment Partners, LP

5.1% Snyder Capital Management, LP

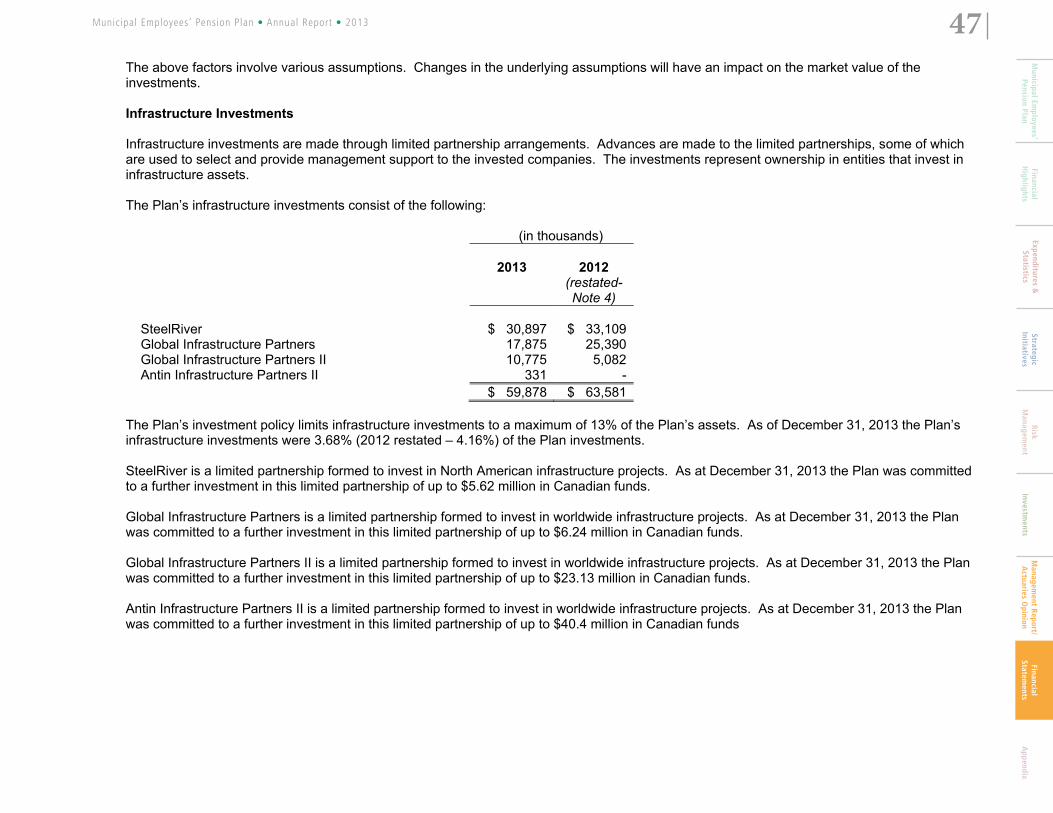

3.3% Infrastructure (Various)

0.1% Private Equity (Various)

-0.3% Pareto Investment Management Ltd.

Investment Manager Mandate Investment Manager Mandate

Canso Investment Council Ltd. Corporate Bonds Pareto Investment Management Ltd. Currency

PIMCO Canada Corp. Core Plus Bonds Greystone Management Investments Inc. Real Estate

TD Asset Management, Inc. Bond Overlay Antin Infrastructure Partners Infrastructure

Wellington Management Company, LLP Long Bonds Plus Global Infrastructure Partners Fund Infrastructure

CGOV Asset Management Canadian Equities SteelRiver Infrastructure Fund North America, LP Infrastructure

Foyston, Gordon & Payne Inc. Canadian Equities Falcon Investment Advisors, LLC Private Equity

BlackRock Asset Management Canada Ltd. U.S. Equities Great Hill Partners Private Equity

Brandes Investment Partners, LP Non-North American Equities

Neuberger Berman Group LLC Private Equity

Schroder Investment Management North America Inc.

Global Equities New Mountain Capital LLC Private Equity

Vontobel Asset Management, Inc. Global Equities Silver Lake Management LLC Private Equity

Snyder Capital Management, LP U.S. Small Cap Equities

Table 1.10

-2

0

2

4

6

8

10

12

28 Municipal Employees’ Pension Plan • Annual Report • 2013

MEPP Asset Mix

Figure 1.4

34.9% Foreign Large Cap Equities

33.0% Fixed Income

17.7% Canadian Equities

6.2% Real Estate

5.1% U.S. Small Cap Equities

3.3% Infrastructure

0.1% Private Equity

-0.3% Cash Currency Forwards

Investment Objectives Total Fund

The Fund’s primary objective is to grow at a rate which exceeds the growth of the Plan’s liabilities. To measure the growth of the Plan’s liabilities, a fixed income portfolio that approximates its going-concern pension liabilities behaviour (the liability benchmark) has been established.

To achieve its goal, the Commission has established:

• a long-term strategic asset mix that is reflected by the Plan’s benchmark (a standard against which performance is measured); and,

• an investment management structure consisting of one or more investment managers in each major asset class.

Custodian The Commission retains RBC Investor Services Trust as the custodian of the Plan. The custodian is responsible for:

• safekeeping of assets;

• collection of income;

• settlement of investment transactions; and

• recording and verifying investment transactions.

RBC Investor Services Trust received $786,000 in fees in 2013.

29Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

Performance by Asset Class

Four-year Return

Four-year Benchmark

FixedIncome

CanadianEquities

Foreign LC Equities

US SC Equities RealEstate

InfrastructureCurrencyOverlay

0.7% 0.7%

12.0%

10.2%

11.7%

18.7% 18.8%

10.7%11.1%

10.2%

6.8%

4.3%3.4%

5.1%

One-year Return

One-year Benchmark

FixedIncome

CanadianEquities

Foreign LC Equities

US SC Equities RealEstate

Infrastructure

CurrencyOverlay

-1.1% -0.5%

4.4%6.1%

11.7%

7.2%

36.4%

48.1%

30.7%28.0%

20.7%

13.0%

-6.0% -6.2%

30 Municipal Employees’ Pension Plan • Annual Report • 2013

To the Members of the Legislative Assembly of Saskatchewan:

Administration of the Municipal Employees’ Pension Plan is presently assigned to the Public Employees Benefits Agency of the Ministry of Finance. Management is responsible for financial administration, administration of funds and managing of assets.

The financial statements which follow have been prepared by management in conformity with Canadian accounting standards for pension plans. Management uses internal controls and exercises its best judgment in order that the financial statements fairly reflect the financial position of the Plan.

The Municipal Employees’ Pension Commission reviews and approves the financial statements. In doing so, the Commission has had the opportunity to discuss the statements with management throughout the year.

The provision for annuity benefits and the accrued pension benefits are determined by an actuarial valuation. Actuarial valuation reports require best estimate assumptions about future events and require approval by management.

The financial statements have been audited by Deloitte LLP whose report follows.

Brian SmithAssistant Deputy MinisterPublic Employees Benefits Agency

Regina, SaskatchewanMarch 21, 2014

managemenT’S report

31Municipal Employees’ Pension Plan • Annual Report • 2013M

unicipal Employees’

Pension PlanExpenditures &

StatisticsStrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsFinancial

Highlights

Appendix

acTuarieS opinion

Actuarial Opinion With respect to the Municipal Employees’ Pension Plan, I have prepared an actuarial valuation as at December 31, 2012 with the results subsequently extrapolated to December 31, 2013, for the purpose of determining the necessary actuarial information for financial statement reporting purposes in accordance with Section 4600 of the CPA Canada Handbook.

In my opinion, for the purpose of this actuarial valuation and extrapolation: The data on which this valuation and subsequent extrapolation are based are sufficient and reliable. Where applicable, the assumptions have been adopted as management’s best estimates for accounting purposes and

consequently I have not rendered a specific opinion on them; however, in my opinion, the assumptions are, in aggregate, not unreasonable when considering the circumstances of the program and the purpose of the valuation and extrapolation.

The actuarial cost methods, extrapolation methods and valuation methods employed are appropriate. The actuarial valuation and extrapolation conform to the requirements of Section 4600 of the CPA Canada Handbook. Nonetheless, emerging experience differing from the assumptions will result in gains or losses which will be revealed in subsequent valuations.

This report has been prepared and this actuarial opinion has been given in accordance with accepted actuarial practice.

David R. Larsen Fellow, Society of Actuaries Fellow, Canadian Institute of Actuaries

February 10, 2014

We administer MEPP in the best interests of all members of the Plan.

33Municipal Employees’ Pension Plan • Annual Report • 2013Financial

Highlights

Expenditures &Statistics

StrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsM

unicipal Employees’

Pension PlanA

ppendix

Municipal Employees’ Pension Plan

Financial Statements

Year ended December 31, 2013

34 Municipal Employees’ Pension Plan • Annual Report • 2013

indePendenT auditor’s reportTo Members of the Legislative Assembly of Saskatchewan:

We have audited the accompanying financial statements of the Municipal Employees’ Pension Plan, which comprise the statement of financial position as at December 31, 2013, and the statement of changes in net assets available for benefits and the statement of changes in pension obligations and provision for annuity obligations for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian accounting standards for pension plans, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of Municipal Employees’ Pension Plan as at December 31, 2013, and the changes in its net assets available for benefits and changes in its pension obligations and annuity obligations for the year then ended in accordance with Canadian accounting standards for pension plans.

Emphasis of Matter

Without modifying our opinion, we draw attention to Note 4 of the financial statements which explains that certain comparative information for the year ended December 31, 2012 has been restated.

Chartered AccountantsMarch 21, 2014Regina, Saskatchewan

35Municipal Employees’ Pension Plan • Annual Report • 2013Financial

Highlights

Expenditures &Statistics

StrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsM

unicipal Employees’

Pension PlanA

ppendix

Municipal Employees’ Pension Plan

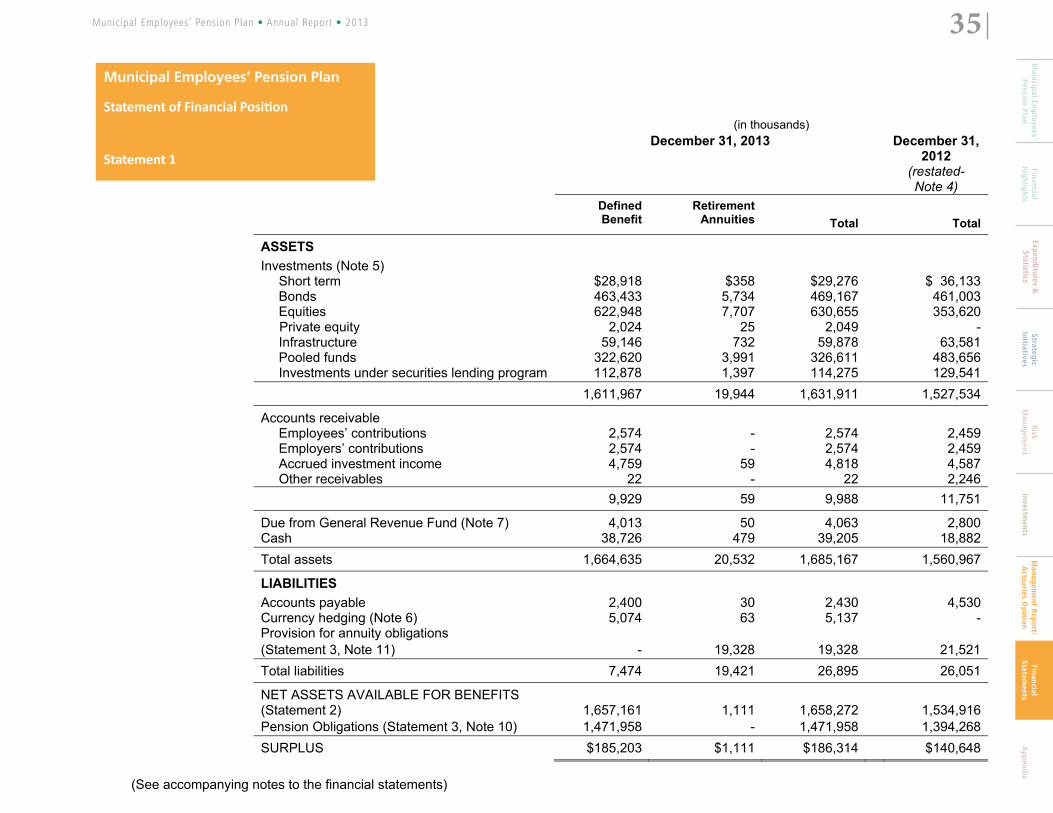

Statement of Financial Position

Statement 1

Municipal Employees’ Pension Plan Statement 1 Statement of Financial Position

(in thousands) December 31, 2013 December 31,

2012 (restated- Note 4)

Defined Benefit

Retirement Annuities

Total

Total

ASSETS Investments (Note 5) Short term $28,918 $358 $29,276 $ 36,133 Bonds 463,433 5,734 469,167 461,003 Equities 622,948 7,707 630,655 353,620 Private equity 2,024 25 2,049 - Infrastructure 59,146 732 59,878 63,581 Pooled funds 322,620 3,991 326,611 483,656 Investments under securities lending program 112,878 1,397 114,275 129,541 1,611,967 19,944 1,631,911 1,527,534

Accounts receivable Employees’ contributions 2,574 - 2,574 2,459 Employers’ contributions 2,574 - 2,574 2,459 Accrued investment income 4,759 59 4,818 4,587 Other receivables 22 - 22 2,246 9,929 59 9,988 11,751

Due from General Revenue Fund (Note 7) 4,013 50 4,063 2,800Cash 38,726 479 39,205 18,882Total assets 1,664,635 20,532 1,685,167 1,560,967

LIABILITIES Accounts payable 2,400 30 2,430 4,530Currency hedging (Note 6) 5,074 63 5,137 -Provision for annuity obligations (Statement 3, Note 11) - 19,328 19,328 21,521Total liabilities 7,474 19,421 26,895 26,051

NET ASSETS AVAILABLE FOR BENEFITS (Statement 2) 1,657,161 1,111 1,658,272 1,534,916Pension Obligations (Statement 3, Note 10) 1,471,958 - 1,471,958 1,394,268SURPLUS $185,203 $1,111 $186,314 $140,648

(See accompanying notes to the financial statements)

36 Municipal Employees’ Pension Plan • Annual Report • 2013

Municipal Employees’ Pension Plan

Statement of Changes in Net Assets Available for Benefits

Statement 2

Municipal Employees' Pension Plan Statement 2 Statement of Changes in Net Assets Available for Benefits

(in thousands) 2013 2012 (restated-

Note 4)

Year Ended December 31 Defined Benefit Retirement Annuities Total Total

INCREASE IN ASSETS Investment income Interest Security lending Pooled funds Dividends Infrastructure

$23,621 173

6,869 14,754

7,615

$3142

91196101

$23,935 175

6,960 14,950

7,716

$18,294 112

10,953 11,782

6,943 53,032 704 53,736 48,084Change in fair value of investments 98,730 1,222 99,952 143,533Contributions Employee contributions Employer contributions Reciprocal transfers in Arrears contributions and interest

42,853 42,673

772 210

- - - -

42,853 42,673

772 210

36,778 36,787

833 322

86,508 - 86,508 74,720

Net decrease in provision for annuity benefits (Statement 3, Note 11) - 2,193 2,193 3,771

Total increase in assets 238,270 4,119 242,389 270,108DECREASE IN ASSETS Transfers and refunds (Note 9) Benefit payments (Note 9) Pension obligation payments Annuities Investment transaction costs Administrative expenses (Note 13)

31,056 9,568

51,722 -

9,835 13,513

---

3,074130135

31,056 9,568

51,722 3,074 9,965

13,648

25,592 7,519

48,081 3,330 6,691

10,910Total decrease in assets 115,694 3,339 119,033 102,123INCREASE IN NET ASSETS 122,576 780 123,356 167,985NET ASSETS AVAILABLE FOR BENEFITS, BEGINNING OF YEAR 1,534,585 331 1,534,916 1,366,931NET ASSETS AVAILABLE FOR

BENEFITS, END OF YEAR $1,657,161 $1,111 $1,658,272 $1,534,916(See accompanying notes to the financial statements)

37Municipal Employees’ Pension Plan • Annual Report • 2013Financial

Highlights

Expenditures &Statistics

StrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsM

unicipal Employees’

Pension PlanA

ppendix

Municipal Employees’ Pension Plan

Statement of Changes in Pension Obligations and Provision For Annuity Obligations

Statement 3

Municipal Employees' Pension Plan Statement 3 Statement of Changes in Pension Obligations and Provision for Annuity Obligations

(in thousands) Year Ended December 31 2013 2012 PENSION OBLIGATIONS, BEGINNING OF YEAR $1,394,268 $1,599,687

Increase in pension obligations Interest on pension obligations Pension obligations accrued Transfers-in Experience loss

90,102 75,397

772 3,765

80,227 90,105

833 -

170,036 171,165Decrease in pension obligations Transfers, refunds and defined pension obligations paid Experience gain Transfer to provision for annuities Change in assumptions

92,346 - - -

81,192 28,201

36 267,155

92,346 376,584PENSION OBLIGATIONS, END OF YEAR (Note 10) $1,471,958 $1,394,268 PROVISION FOR ANNUITY OBLIGATIONS, BEGINNING OF YEAR $21,521 $25,292Increase in provision for annuity obligations Interest on annuity obligations New annuities purchased Experience loss

1,299 - -

1,182 36

270 1,299 1,488

Decrease in provision for annuity obligations Annuities paid Change in assumptions

3,074 418

3,330 1,929

3,492 5,259

PROVISION FOR ANNUITY OBLIGATIONS, END OF YEAR (Note 11) $19,328 $21,521 (See accompanying notes to the financial statements)

38 Municipal Employees’ Pension Plan • Annual Report • 2013

Municipal Employees’ Pension Plan

Notes to the Financial Statements

December 31, 2013

Municipal Employees' Pension Plan Notes to the Financial Statements December 31, 2013 1. Description of the Municipal Employees' Pension Plan General

The Municipal Employees' Pension Plan (the “Plan”) which is domiciled in Regina, Saskatchewan, is comprised of three components: defined benefit, defined contribution benefit and retirement annuities. The following description of the Plan is a summary only. For more complete information, reference should be made to The Municipal Employees' Pension Act. The Municipal Employees' Pension Act (the “Act”) provides authority for the Plan. The Act directs that all allowances, payments and refunds under the Act shall be payable out of the Plan in the manner provided in the Act together with all benefits granted under a former Act. The Municipal Employees' Pension Commission (the “Commission”) is responsible for holding in trust and investing the monies of the Plan. The Commission's composition and authority to administer the Plan are provided in Section 7 of the Act. The Plan is registered under The Pension Benefits Act, 1992 and is required to provide valuations every three years as to whether the Plan has sufficient assets to meet its pension obligations on an on-going basis as well as on a hypothetical wind-up basis. These valuations are filed with the Superintendent of Pensions (the “Superintendent”). If the Plan has insufficient assets, the Act outlines the steps to address the shortfall of assets. The Commission filed its December 31, 2012 valuation with the Superintendent. Due to an accounting adjustment on the 2012 financial statements (Note 4), a revised valuation was prepared on December 13, 2013 and re-filed with the Superintendent on December 18, 2013. The fund is required to obtain the next actuarial valuation as at December 31, 2015. Defined Benefit Component The Defined Benefit Component became effective July 1, 1973. This Defined Benefit Component is mandatory for permanent employees and optional for some non-permanent employees. A. Funding

Effective January 1, 2013, employee contributions are 8.15% of salary for general members and 11.35% for police officers and firefighters (2012- 7.4% and 10.2% respectively). Employee contributions are matched by the employer. There are some employee contributions that are not matched by employers, these contributions consist of transfers from other plans and purchase of prior services.

B. Pensions

Employees receive a pension at age 65 for general members and at age 60 for police officers and firefighters, for each year and fractional year of contributory service in the Plan prior to retirement that is determined as:

39Municipal Employees’ Pension Plan • Annual Report • 2013Financial

Highlights

Expenditures &Statistics

StrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsM

unicipal Employees’

Pension PlanA

ppendix

For service earned before 1990 and service earned after 2000 but before 2006, the number of years of contributory service during these periods times the greater of: a) 1.8% times the average salary for the highest three annualized years of the member's total pensionable service in the Plan (2% for

police officers and firefighters); or b) i) 1.3% of that portion of the member’s average salary not exceeding the average yearly maximum pensionable earnings under

the Canada Pension Plan; and ii) 2% of that portion of the member's average salary exceeding the average yearly maximum pensionable earnings under the

Canada Pension Plan. For all other service, the number of years of contributory service for the period times the greater of: a) 1.5% times the average salary for the highest three annualized years of the member's total pensionable service in the Plan

(1.7% for police officers and firefighters); or b) i) 1.3% of that portion of the member's average salary not exceeding the average yearly maximum pensionable earnings under

the Canada Pension Plan; and ii) 2% of that portion of the member's average salary exceeding the average yearly maximum pensionable earnings under the

Canada Pension Plan. Members who commenced employment on or after January 1, 1993:

For service earned after 2000 but before 2006, the number of years of contributory service during this period times 1.8% times the average salary for the highest three annualized years of the member's total pensionable service in the Plan (2% for police officers and firefighters). For all other service, the number of years of contributory service for the period times 1.5% times the average salary for the highest three annualized years of the member's total pensionable service in the Plan (1.7% for police officers and firefighters).

C. Retirement Normal retirement is at age 65 for general members and age 60 for police officers and firefighters. Members may retire earlier under

certain conditions.

The Plan also provides benefits in the event of termination of employment, death or disability.

D. Surplus Any surpluses arising in the Plan can be utilized at the discretion of the Commission.

40 Municipal Employees’ Pension Plan • Annual Report • 2013

E. Transfers Subject to lock in provisions of the Plan, transfer of a member’s commuted value is payable when a member ceases to be employed. As the December 31, 2012 actuarial valuation for filing purposes stated a solvency ratio of 77.2%, commuted value transfers out of the

Plan are limited to 77.2%. Payment of the remaining transfer deficiency shall occur over the following five-year period.

Defined Contribution Component The Defined Contribution Component consists of members who made contributions to the Defined Contribution Component in effect prior to July 1, 1973. Members may retire and purchase an annuity at age 65. Members may retire earlier under certain conditions. Upon retirement a member can purchase an annuity from either the Plan or a private insurer based on employee and employer contributions together with the interest thereon. In the event of death prior to retirement, the member's spouse may receive a life annuity or elect to receive a lump-sum payment of employee and employer contributions plus interest. If the member's beneficiary is other than the spouse, a lump-sum payment of employee and employer contributions plus interest is made. Retirement Annuities Component If a member elects to purchase an annuity through the Commission, an annuity contract is issued based on the member's balance, current interest rates and annuity tables. The present value of these annuities is reflected as a liability of the Plan. Supplementary Benefits In accordance with the Act, the Commission may grant supplementary benefits to those members receiving pensions and annuities to compensate them for lost purchasing power. The Commission may grant the supplementary benefits as long as the solvency of the entire Plan is not impaired. Income Taxes The Plan is a registered pension plan, as defined by the Income Tax Act (Canada) and, accordingly, is not subject to income taxes.

2. Basis of Preparation

a. Statement of Compliance

The financial statements for the year ended December 31, 2013 have been prepared in accordance with Canadian accounting standards for pension plans as defined in the CPA Canada Handbook section 4600, Pension Plans. For matters not addressed in Section 4600, International Financial Reporting Standards (IFRSs) have been followed.

41Municipal Employees’ Pension Plan • Annual Report • 2013Financial

Highlights

Expenditures &Statistics

StrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsM

unicipal Employees’

Pension PlanA

ppendix

b. Functional and Presentation Currency

These financial statements are presented in Canadian Dollars, which is the Plan’s functional currency, and are rounded to the nearest thousand unless otherwise noted.

3. Significant Accounting Policies

The significant accounting policies are as follows: a. Basis of Presentation

The Plan has disclosed financial results for its Defined Benefit and Retirement Annuities components separately. The Plan maintains a single investment portfolio and assets were allocated to the retirement annuities component at January 1, 2002 based upon the provision for annuity obligations as at that date. Investment income is split so that it matches the rate of return and operating expenses and the change in fair value have been allocated relative to the assets. These financial statements were authorized and issued by the Commission on March 21, 2014.

b. Investments

Investments are stated at their fair value in the Statement of Financial Position. The change in the fair value of investments at the beginning and end of each year is reflected in the Statement of Changes in Net Assets Available for Benefits. Fair value of investments is determined as follows: Short-term investments are valued at cost which, together with accrued investment income, approximates fair value given the short-term nature of these investments. Bonds are valued at year-end quoted bid prices in an active market when available. When quoted market prices are not available, the fair value is based on a valuation technique, being the present value of the principal and interest receivable discounted at the appropriate market interest rates. Equities are valued at year-end quoted bid prices from accredited stock exchanges on which the security is principally traded. Private equity investments are valued at market values supplied by the private equity investment manager. These market values are based on a year-end valuation of the underlying investments performed by the private equity investment manager. Infrastructure investments are valued at market values supplied by the infrastructure investment manager. These market values are based on a year-end valuation of the underlying investments performed by the infrastructure investment manager. Pooled fund investments are valued at the year-end unit value supplied by the pooled-fund administrator, which represent the underlying net assets of the pooled fund at fair values determined using closing bid prices. Real estate pooled-fund underlying assets are valued by third-party appraisals.

42 Municipal Employees’ Pension Plan • Annual Report • 2013

Investments in derivative financial instruments, including futures, repurchase agreements, forwards and option contracts, are valued at year-end quoted market prices where available. Where quoted market prices are not available, values are determined using pricing models, which take into account current market and contractual prices of the underlying instruments, as well as time value and yield curve or volatility factors underlying the position. Investment transactions are recorded on the trade date.

c. Other Assets and Financial Liabilities

Accounts receivable are classified as loans and receivables and accounts payable are classified as other financial liabilities and are measured at amortized cost. Due to their short-term nature, the amortized cost of these instruments approximates their fair value.

d. Investment Income and Transaction Costs

Investment income, which is recorded on the accrual basis, includes interest income, dividends, real estate operating income, pooled-fund income, infrastructure income, and security lending income. Brokers’ commissions and other transaction costs are recognized in the statement of changes in net assets available for benefits in the period incurred.

e. Foreign Currency Translation

The fair values of foreign currency denominated investments included in the statement of Financial Position are translated into Canadian dollars at year-end rates of exchange. Gains and losses from translations are included in the change in fair value of investments.

Foreign currency-denomination transactions are translated into Canadian dollars at the rates of exchange on the trade dates of the related transactions. Realized gains and losses on the sale of investments are included in the change in fair value of investments.

f. Provision for Annuity Obligations

Provision for annuity obligations represents the present value of the retirement annuities underwritten by the Plan and is determined pursuant to an actuarial valuation or extrapolation. Any change in the liability pursuant to the valuation or extrapolation is recognized as an increase or decrease in that year’s statement of changes in pension obligations and provision for annuity obligations.

g. Use of Estimates

The preparation of financial statements in accordance with Canadian accounting standards for pension plans requires management to make estimates and assumptions that affect the recorded amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statement and the recorded amounts of revenue and expenses during the year. Significant items subject to such estimates and assumptions include the valuation of investments, the provision for annuity obligations and pension obligations. Actual results could differ from these estimates.

h. Changes in Accounting Policies

The Plan has adopted the following new standards, along with any consequential amendments, effective January 1, 2013, or on such a date they became applicable. The adoption of these changes did not result in any adjustments and had no significant impact on the financial statements:

43Municipal Employees’ Pension Plan • Annual Report • 2013Financial

Highlights

Expenditures &Statistics

StrategicInitiatives

RiskM

anagement

Investments

Managem

ent Report/A

ctuaries Opinion

FinancialStatem

entsM

unicipal Employees’

Pension PlanA

ppendix

IFRS 13 - Fair Value Measurement IFRS 13, issued in May 2011, redefines fair value to emphasize that it is a market-based measurement, not an entity-specific measurement. It also provides a single framework for measuring fair value and applies, with limited exceptions, when another standard permits or requires fair value measurement. In addition, IFRS 13 requires specific disclosures about fair value measurement. The standard is effective for annual periods beginning on or after January 1, 2013.

i. Future Accounting Policy Changes

A number of new standards, amendments to standards and interpretations, are not yet effective for the year ended December 31, 2013, and have not been applied in preparing these financial statements. In particular, IFRS 9, Financial Instruments, for which the effective date of adoption, has not been determined. The extent of the impact of adoption of this standard is not known at this time, but is not expected to be material.

4. Accounting Adjustment In November 2013, an accounting error was discovered pertaining to the 2012 financial statements. The error was due to an inaccuracy in the

estimate of the year-end market value of the infrastructure assets. The error resulted in a $17.6 million overstatement of the infrastructure assets on the Statement of Financial Position and an overstatement of the change in the fair value of investments on the Statement of Changes in Net Assets Available for Benefits. In addition, the error resulted in an overstatement of the surplus reported in 2012 by $17.6 million. The December 31, 2012 financial statements have been restated to reflect the following adjustments:

Statement of Financial Position (in thousands)Infrastructure reported in 2012 $ 81,150 Adjustment (17,569)

$ 63,581

Surplus reported in 2012 $ 158,217Adjustment (17,569)Restated surplus $ 140,648

Statement of Changes in Net Assets Change in fair value of investments reported in 2012 $ 161,102Adjustment (17,569)Restated change in fair value of investments $ 143,533

Net assets available for benefits reported in 2012 $1,552,485 Adjustment (17,569)Restated net assets available for benefits $1,534,916

44 Municipal Employees’ Pension Plan • Annual Report • 2013

5. Investments Details of significant terms and conditions, exposure to interest rate and credit risks of investments are as follows: Investments The carrying values of the Plan’s investments are as follows: 2013 2012

(restated) Short-term $ 29,276 $ 36,133 Bonds 469,167 461,003 Equities Private equity

630,655 2,049

353,620 -