2013 annual report - panalpina€¦ · 2013 annual report. ... in productivity and secure our...

TRANSCRIPT

2013 Annual Report

the yeaR in bRief

Letter to the Shareholders 3

Facts and Figures 4

Information for Investors 6

GRoup RepoRt

Strategy and Results 9

Performance by Product 17

Performance by Region 19

Global Network 22

Industry Know-How 23

Compliance 26

Employees 27

Information Technology 29

Procurement 31

Security 32

Quality, Health, Safety and Environment 33

Social Commitments 37

CoRpoRate GoveRnanCe ⁄ CoMpensation RepoRt

Corporate Governance 39

Compensation Report 51

finanCial RepoRt

Consolidated Financial Statements 63

Annual Financial Statements 142

Contents

the yeAR

inbRief

contents

Letter to the Shareholders 3

Facts and Figures 4

Information for Investors 6

3Letter to the Shareholders

Panalpina Annual Report 2013

LetteR to the shARehoLdeRs

Dear shareholders,

In 2013, we were able to improve our result by CHF 80 million. Whilst this is a positive improvement over last year, we still have much to do to reach the targets we have set ourselves. We are therefore focusing our organization into converting more of our considerable gross profit into net profit, in which our shareholders participate.

At the 2013 Annual General Meeting, we bid farewell to our former corporate leader Monika Ribar, who had served our company for 22 years. Once again, we would like to give a special thanks to Ms. Ribar for her great service in developing Panalpina, and especially for succeeding in transforming the corporate culture into a professionally managed company. On the same day, Peter Ulber was welcomed to the company as our new CEO.

We have recently undertaken a review of our strategy and as a result consider it appropriate, fit for purpose, and concluded that we have no fundamental changes to make. However, we want to concentrate on sharpening our focus on the core elements of our business, specifically through Ebit conversion rate improvement, productivity gains and in the turnaround of lossmaking units. Our expertise in customized project business and in supporting global oil and gas companies will continue to contribute to our success.

The very direct implementation of these objectives has led us to make some consequential structural and staff changes. For example, hav ing created a new, fourth region, Middle East/Africa/CIS, we plan to capitalize far more in this attractive growth market. We are continuing to invest heavily in our IT and supporting systems to put us in a leading position in the industrialization of processes within the freight forwarding business which in turn leads to productivity gain and better ability to meet our customer needs. As a result, we have elevated the position of Chief Information Officer, held by Rod Angwin, to full membership of the Executive Board which reflects the strategic significance of information technology for our company.

Based on the results from the 2013 fiscal year and in view of our healthy balance sheet, the Board of Directors is proposing to the Annual General Meeting to pay out a dividend of CHF 2.20.

We aim to consistently pursue the course of actions initiated over the last year. In doing so, we intend to achieve sustainable profit through further increases in productivity and secure our position as one of the world’s top five companies in our markets.

We would like to thank all of our more than 16,000 staff around the world for their great dedication, our customers and suppliers for the excellent, trustbased cooperation, and our shareholders for their loyalty.

Peter Ulber Rudolf W. hugChief Executive Officer Chairman of the Board of Directors

4Facts and Figures

fActs And figURes

Key FiguresNet forwarding revenue of CHF 6,758 million Gross profit of CHF 1,561 million Adjusted EBIT of CHF 108 millionForwarding volumes: 825,000 tons in Air Freight (+3% year on year) 1,495,000 TEU in Ocean Freight (+ 7.7% year on year)

gross profit by product2013

40 %Air Freight

28 %Logistics

32 %Ocean Freight

gross profit by region2013

20 %APAC

30 %Americas

9 %MEAC

41 %Europe

energy balance by energy categoryGigajoule

280,000

240,000

200,000

160,000

120,000

80,000

40,000

0

Electricity

221,000

18,000

Heating

15,000

104,000

Owned vehicles

175,000

Indirect renewable energy Indirect energy Direct energy

co2 emission by scope and activityTons of CO2 equivalent

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

Indirect CO2 emission Direct CO2 emission

30,939

Electricity

5,998

2,338

Heating

12,675

Owned vehicles

5Facts and Figures

Panalpina Annual Report 2013

five-yeAR deveLoPment

gross profit Million CHF

1,900

1,750

1,600

1,450

1,300

1,150

1,000

10

1,480

11

1,477

12

1,465

13

1,561

09

1,377

net forwarding revenue Million CHF

7,500

6,250

5,000

3,750

2,500

1,250

0

10

7,164

11

6,500

12

6,617

13

6,758

09

5,958

ebit Million CHF

200

160

120

80

40

0

–40

–80

13

48

12

–40*

11

174

10

15

09

30

consolidated profit Million CHF

160

120

80

40

0

–40

–80

–120

13

11.7

12

–72*

11

127

10

–26

09

10

total equityMillion CHF

900

750

600

450

300

150

0

13

709

12

743*

11

928*

10

812

09

864

* Prior year’s figures have been restated due to the application of IAS 19 (as revised in 2011) retrospective)

five-yeAR deveLoPment

6

Panalpina Annual Report 2013

infoRmAtion foRinvestoRs

Good development – Panalpina shares performed well over the reporting period. The price quoted increased by 61.0%, from CHF 92.85 at the beginning of the year to CHF 149.50 on the last day of trading in the business year. The Swiss Performance Index (SPI) rose by 24.6% in the same period, so Panalpina performed significantly better than the Index as a whole, which includes more than 200 companies. The market capitalization at the end of the year amounted to CHF 3,551 million.

Share Symbol PWTN

Reuters PWTN.S

Bloomberg PWTN SW

Trading exchange SIX

Fiscal year ends December 31

ValorenNr. 000216808

ISIN CH0002168083

Share register SIS Aktienregister AG, Olten, Switzerland

Number of registered shares 23,750,000

share information

January 1 to December 31 Financial year

April 29 Firstquarter results

May 9 Annual General Meeting

July 22 Secondquarter results

October 21 Thirdquarter results

financial calender

share price development in comparison to sPi

Information for Investors

Panalpina World Transport Swiss Performance Index (SPI)

180%

170%

160%

150%

140%

130%

120%

110%

100%

90%

80%

dec 31 2012

mAR 1 mAy 1 JUL 1 seP 1 nov 1 dec 31 2013

7

Panalpina Annual Report 2013

IN MIO CHF 2013 2012 chAnge in %

Net forwarding revenue 6,758 6,617 +2.1

Gross profit 1,561 1,465 – 6.6

EBITDA 120 34 +249.6

EBIT 48 –40 u/a

Consolidated profit 12 –72 u/a

Earnings per share 0.5 –3.05 u/a

Key figures

2013 2012

Last day of trading previous year CHF 95.75 96.20

High CHF 151.80 109.50

Low CHF 82.40 78.90

Last day of trading current year CHF 149.50 92.85

Average trading volume CHF 33,306 40,917

Total shareholder return % 56.1 0.6

Market capitalization as per Dec 31 MIO CHF 3,551 2, 205

share price development

2013 2012

Amount MIO CHF 52.2 47,3

Per share CHF 2.20* 2.00

* Proposal to the Annual General Meeting.

ordinary gross dividend payments

Information for Investors

gRoUP RePoRt

contents

Strategy and Results 9

Performance by Product 17

Performance by Region 19

Global Network 22

Industry KnowHow 23

Compliance 26

Employees 27

Information Technology 29

Procurement 31

Security 32

Quality, Health, Safety and Environment 33

Social Commitments 37

9Strategy and Results

Panalpina Annual Report 2013

stRAtegy And ResULts

market developmentThe growth of the global eco nomy and world trade remained in low gear in the latest reporting year. The International Monetary Fund (IMF) estimates that both world output and global trade volumes rose around 3% in 2013 – approximately the same growth rate as in the previous year. However, growth dynamics are changing, with advanced economies gradually strengthening, supported by strong private demand in the United States and the Euro Area starting to crawl out of recession. At the same time, growth in emerging market economies has slowed, with particularly the once much hailed BRIC (Brazil, Russia, India, China) economies losing steam. The Chinese economy is estimated to have grown around 7.7% in 2013 and thus at the lowest rate since 1999, while the other three economies are estimated to have grown only between 1.5% (Russia) and 4.4% (India).Against this economic backdrop, freight markets continued to be plagued by overcapacities and significant rate volatility, which in turn can lead to increased volatility of forwarders’ unit yields. On the demand side, growth remained lackluster. The ocean freight market grew just about 3% and the air freight market – while still declining in the first quarter – was in stagnation during most of the year and only gained some traction towards year end, leading to a growth rate for the full year of just about 1%.

business strategyDuring the year under review, with the arrival of both a new CEO and CFO, Panalpina further sharpened its strategy and set out a range of strategic priorities with respect to the company’s product mix, geographic co ver age, cus tomers and growth model. The core competence in Air and Ocean Freight remains the foundation of Panalpina’s business and at the same time Logistics will be further developed as an important differentiator by focusing on the delivery of valueadded services to complement the endtoend solutions offering for international customers. Furthermore, the service offering includes the specialties Projects and Oil and Gas where the Group is widely recognized by its customers to have deep and unrivalled knowl edge and expertise. The focus on these specialties will enable Panalpi na to further differentiate its product offering from competition.Geographically, apart from strengthening its position in key European markets such as the UK, the Netherlands, France and Italy, the company also aims to expand its global footprint by increasing its market share on the IntraAsia and Asiaoutbound trade lanes as well as in the United States where management feels the market potential is currently not fully tapped. Moreover, the Group complemented its organizational structure by setting up a fourth region covering the Middle East, Africa and the CIS (MEAC), which will allow to better focus on the potential within these growing economies. In the period under review, the reporting structure has been adjusted accordingly: MEAC as well as Europe are reported as two separate operating segments (previously one operating segment). Panalpina will continue to leverage its expertise to serve customers in the Technology and Automotive sectors, and will increase its investment focus to attract additional business in the Oil and Gas, Healthcare, Consumer and Retail, Fashion and Manufacturing industry verticals.In the near future, the Group’s business growth is likely to remain organic. However, for the medium term, it is Panalpina’s objective to become fit for acquisitions as suitable opportunities arise and as a means to reach or retain its position among the global top 5 players in air and ocean freight forwarding. Along with the goal to further expand its business while gaining market share, the Group’s major focus is to improve its operating margin, measured as the conversion ratio of EBIT over gross profit.

To this end, the Group has launched a number of profitability improvement initiatives and has embarked on a comprehensive Operations Transformation Program (OTP) to significantly increase productivity in the years to come. The key cornerstones of OTP are the rollout of SAP Transportation Management (TM), which began in 2013 in the Ocean Freight segment with the replacement of the old system and the centralization of noncustomerfacing processes in four business service centers located in Asia, Central America and Eastern Europe.

Initiating the business transformation – In a continuously slow market environment, Panalpina gained market share and posted a considerable rise in profitability thanks to focusing on selective business growth and cost containment. The corporate strategy was sharpened and clear priorities have been set to secure sustainable growth above market while further improving operating margins. First milestones have been achieved in the journey to transform the Panalpina Group into the most customerfocused global provider of freight forwarding and logistics solutions.

10Strategy and Results

Panalpina Annual Report 2013

Furthermore, the Group’s financial transparency has been enhanced during the period under review by allocating all operating expenses down to the smallest organizational unit as well as to the product level (Air Freight, Ocean Freight, Logistics). As a result, a number of underperforming operations and business activities has been identified, and concrete plans have been put in place to eliminate these inefficiencies. At the same time, clear financial ownership has been assigned and directly linked to compensation such that the vast majority of managers within the Group is financially incentivized to focus on EBIT.To further facilitate the execution of the corporate strategy, the Group also simplified and aligned its organizational structure, with the following changes becoming effective on January 1, 2014: appointment of a regional CEO for the newly created region MEAC who is part of the Group’s Executive Committee; appointment of a Chief Commercial Officer on Executive Board level in order to further increase Panalpina’s customer focus and to drive the Group’s sales performance management; elevation of the Chief Information Officer function from Executive Committee to Executive Board level to underline the importance of IT for the company and the industry as a whole. Moreover, most country organizations within the Panalpina network will in the future report directly to one of the Group’s four regions, with the consequence that the previous area structure will be dissolved.

outlookThe IMF expects output in 2014 to slowly gain traction in most countries and growth of world trade to accelerate to 5% from 3% in the previous year. At the same time, management does not expect a significant pickup in growth in Panalpina’s core markets. However, regardless of the economic environment and in line with its strategy of sustainable, profitable growth above market across all regions and products, the Group remains committed to further increase its customer orientation and to improve productivity and operating margins in the years to come. To strengthen Panalpina’s global competitive position, selective investments in the business platform and industrial expertise will continue and will be balanced with strict cost control.

Management generally expects world trade and the outsourcing of logistics services to expand further in the years to come, although the dynamics of growth may vary by geography. With its global and assetlight network, coupled with the ability to react swiftly to changing customer needs and to offer its clients firstclass, tailormade, endtoend supply chain solutions, Panalpina is well prepared to take advantage of the growth opportunities ahead and to further enlarge its footprint in the global logistics market.

11Strategy and Results

Panalpina Annual Report 2013

net foRWARding RevenUe (nfR)

Net forwarding revenue in 2013 amounted to CHF 6,758 million, an increase of 2.1% compared to the CHF 6,617 million the year before. The translation of foreign currencies into the reporting currency (CHF) had a negative impact on the Group’s NFR in the amount of CHF 127 million or 2.0%, hence organic growth amounted to 4.1%. The Group did not undertake any acquisitions during the reporting year.

At regional level, net forwarding revenue in Europe – the Group’s largest region in terms of turnover – declined 1.9% from CHF 2,658 million in 2012 to CHF 2,608 million in 2013. In North, Central and South America (Americas), NFR increased by 1.0% from CHF 2,288 million to CHF 2,310 million. Compared to 2012, Panalpina’s NFR in 2013 in Asia Pacific (APAC) increased 2.3% from CHF 1,238 million to CHF 1,266 million. The region Middle East, Africa and CIS (MEAC) saw an increase in NFR of 32.6% from CHF 433 million to CHF 574 million.

In 2013, the Panalpina Group generated 39% of its net forwarding revenue in Europe, 34% in the Americas, 19% in APAC and 8% in MEAC.On a product level, net forwarding revenue in Air Freight declined 1.6% from CHF 3,106 million in 2012 to CHF 3,056 million in 2013. In contrast, in Ocean Freight, the Company increased its NFR by 6.3% from CHF 2,615 million to CHF 2,781 million. In Logistics, NFR saw an increase of 2.8% from CHF 896 million to CHF 921 million.

In 2013, the Panalpina Group generated 45% of its net forwarding revenue with Air Freight, 41% with Ocean Freight and 14% with Logistics.

net forwarding revenue by region 2013

19 %APAC

34%Americas

8 %MEAC

39 %Europe

net forwarding revenue by product 2013

45 %Air Freight

14 %Logistics

41 %Ocean Freight

net forwarding revenue by product Million CHF

3,500

3,000

2,500

2,000

1,500

1,000

500

0

2013 2012

Logistics

921 896

Ocean Freight

2,7812,615

Air Freight

3,056 3,106

net forwarding revenue by regionMillion CHF

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Americas

2,310 2,288

APAC

1,266 1,238

MEAC

574433

Europe

2,608 2,658

2013 2012

12Strategy and Results

Panalpina Annual Report 2013

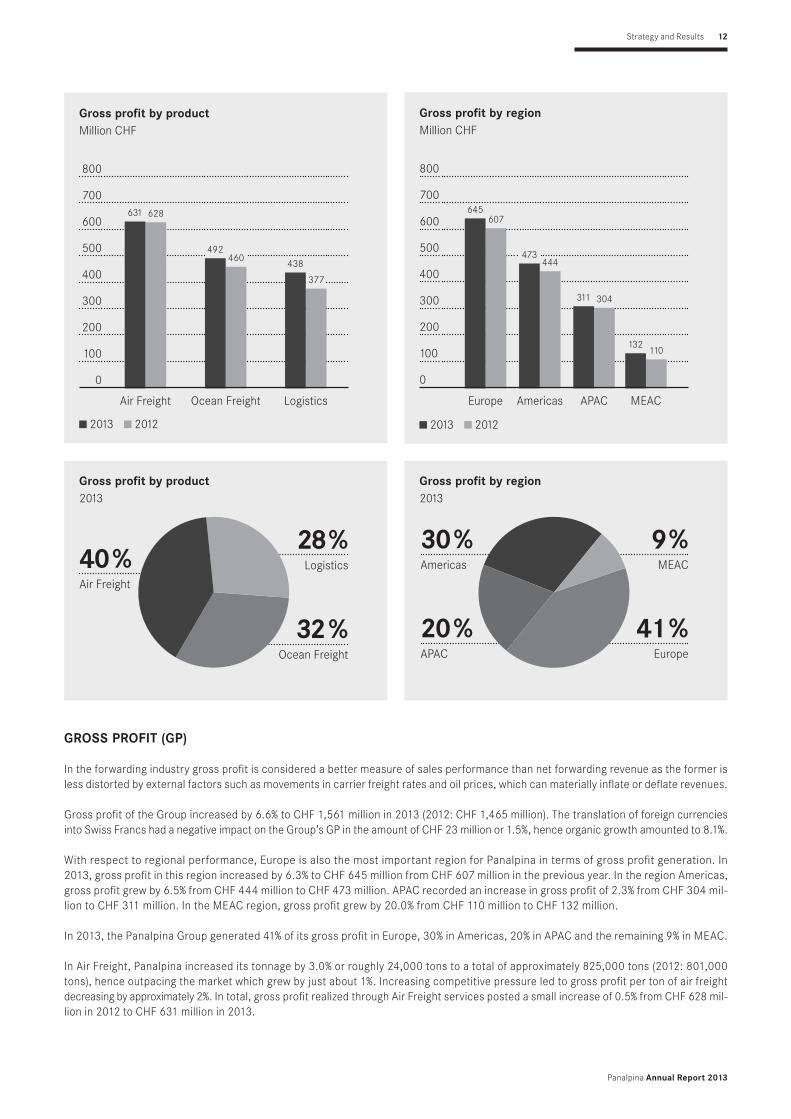

gRoss PRofit (gP)

In the forwarding industry gross profit is considered a better measure of sales performance than net forwarding revenue as the former is less distorted by external factors such as movements in carrier freight rates and oil prices, which can materially inflate or deflate revenues.

Gross profit of the Group increased by 6.6% to CHF 1,561 million in 2013 (2012: CHF 1,465 million). The translation of foreign currencies into Swiss Francs had a negative impact on the Group’s GP in the amount of CHF 23 million or 1.5%, hence organic growth amounted to 8.1%.

With respect to regional performance, Europe is also the most important region for Panalpina in terms of gross profit generation. In 2013, gross profit in this region increased by 6.3% to CHF 645 million from CHF 607 million in the previous year. In the region Americas, gross profit grew by 6.5% from CHF 444 million to CHF 473 million. APAC recorded an increase in gross profit of 2.3% from CHF 304 million to CHF 311 million. In the MEAC region, gross profit grew by 20.0% from CHF 110 million to CHF 132 million.

In 2013, the Panalpina Group generated 41% of its gross profit in Europe, 30% in Americas, 20% in APAC and the remaining 9% in MEAC.

In Air Freight, Panalpina increased its tonnage by 3.0% or roughly 24,000 tons to a total of approximately 825,000 tons (2012: 801,000 tons), hence outpacing the market which grew by just about 1%. Increasing competitive pressure led to gross profit per ton of air freight decreasing by approximately 2%. In total, gross profit realized through Air Freight services posted a small increase of 0.5% from CHF 628 million in 2012 to CHF 631 million in 2013.

gross profit by product2013

40 %Air Freight

28 %Logistics

32 %Ocean Freight

gross profit by region2013

20 %APAC

30 %Americas

9 %MEAC

41 %Europe

gross profit by product Million CHF

800

700

600

500

400

300

200

100

0

Air Freight

631 628

492460

Ocean Freight

438

377

Logistics

2013 2012

gross profit by region Million CHF

800

700

600

500

400

300

200

100

0

2013 2012

MEAC

132110

APAC

311 304

Americas

473444

Europe

645607

13Strategy and Results

Panalpina Annual Report 2013

In Ocean Freight, Panalpina’s volumes grew by 7.7% – well ahead of the market which grew by about 3% – to reach a new alltime high of approximately 1,495,000 twentyfoot equiv alent units or TEU (2012: 1,388,000 TEU). Gross profit per TEU came in just slightly below previous year’s level despite a very volatile freight rate environment during the year. In combination with the strong volume performance, gross profit generated through Ocean Freight services expanded by 7.0% from CHF 460 million in 2012 to CHF 492 million in 2013.

Gross profit in Logistics saw strong growth of 16.2% from CHF 377 million in 2012 to reach a total of CHF 438 million in 2013. The improved GP result was driven by a strong expansion across all subactivities such as Warehousing & Distribution, ValueAdded Logistics Services and Overland.

In 2013, the Panalpina Group generated 40% of its gross profit with Air Freight, 32% with Ocean Freight and 28% with Logistics.

eARnings befoRe inteRest And tAxes (ebit)

Management considers earnings before interest and taxes (EBIT) a key performance indicator for assessing the Group’s operating performance. The Group’s EBIT in 2013 was substantially hit by a provision of CHF 40.9 million (2012: CHF 59.2 million) which the Company recognized to cover fines and charges by various parties and government authorities for alleged antitrust violations related to isolated air freight surcharges on certain trade lanes during limited periods of time prior to 2008. Moreover, the Group incurred an impairment charge in the amount of CHF 19.1 million (2012: CHF 29.6 million) for writing off the remaining goodwill of an acquisition done in 2011.

The Group’s EBIT in 2013 amounted to CHF 48 million (2012: loss of CHF 40 million). The translation of foreign currencies into Swiss Francs had a negative impact on the Group’s EBIT in the amount of CHF 1.4 million.Excluding the extraordinary charges described above, Pan alpina achieved an adjusted EBIT of CHF 108 million in the reporting year (2012: CHF 49 million) and an adjusted EBIT/GP margin of 6.9% (2012: 3.4%).

The two main items included in operating expenses – personnel expenses and other operating expenses – developed as follows: Personnel expenses amounted to CHF 960 million in 2013 and thus were largely unchanged from previous year (2012: CHF 957 million). The small increase was mainly a result of more personnel being hired to support the continued growth of Logistics.

Other operating expenses amounted to CHF 440 million in 2013 and thus came in approximately 6% higher compared to the previous year (2012: CHF 414 million). Other operating expenses increased as the Group continued to invest particularly in a number of new Logistics facilities and the rollout of new IT solutions in both Logistics (Red Prairie) and Ocean Freight (SAP TM).

Depreciation and amortization charges changed from CHF 44 million in 2012 to CHF 53 million in 2013. The increase of CHF 9 million was mainly related to the beginning of the amortization of previously capitalized costs in connection with the SAP TM project.

overall developmentMillion CHF

120

100

80

60

40

20

0

–20

–40

–60

EBIT EBIT excl. nonrecurring items

2013

48

108

–40

49

2012

9.0%

7.5%

6.0%

4.5%

3.0%

1.5%

0.0%

–1.5%

–3.0%

–4.5%

EBIT/GP margin EBIT/GP margin excl. nonrecurring items

2013

3.1

6.9

–2.7

3.4

2012

14

With respect to regional EBIT performance, adjusted for the nonrecurring items mentioned above, EBIT in Europe improved from a loss of CHF 12 million in 2012 to a positive result of CHF 13 million in 2013. EBIT in the Americas turned from a loss of CHF 1 million in 2012 to a positive result of CHF 23 million in 2013. The largest contribution to Group EBIT was contributed by APAC which improved its EBIT from CHF 65 million in 2012 to CHF 71 million in 2013. In MEAC, EBIT improved from a loss of CHF 3 million in 2012 to a positive result of CHF 1 million in 2013.

In the products adjusted for the nonrecurring items mentioned above, Air Freight delivered the highest EBIT with CHF 119 million, a sharp increase compared to the CHF 79 million achieved in the previous year. In Ocean Freight, EBIT increased from CHF 9 million in 2012 to CHF 28 million in 2013. In Logistics, the EBIT result stayed unchanged at a loss of CHF 39 million in 2013 (2012: loss of CHF 39 million).

bALAnce sheet

current assetsPanalpina’s cash and cash equivalents amounted to CHF 337 million on December 31, 2013 and thus decreased by CHF 56 million from the year before (December 31, 2012: CHF 393 million). The cash reduction can mainly be attributed to dividends paid to shareholders (CHF 47 million) as well as an increase in net working capital.

Trade receivables and unbilled forwarding services increased by CHF 33 million, from CHF 1,118 million at the end of 2012 to CHF 1,151 million at the end of 2013. The increase can be mainly attributed to the increase of turnover. The net working capital intensity (defined as net working capital as a percentage of gross forwarding revenue) at the end of 2013 increased to 2.0%, compared to 1.7% a year earlier. The increase can mainly be attributed to pressure from customers for longer payment terms.

non-current assetsPanalpina’s noncurrent assets decreased by CHF 11 million and amounted to CHF 351 million on December 31, 2013 (December 31, 2012: CHF 362 million). The decrease can mainly be attributed to the decrease in intangible assets as a result of the aforementioned impairment charges recognized during the reporting year.

Strategy and Results

Panalpina Annual Report 2013

Adjusted ebit by product Million CHF

140

120

100

80

60

40

20

0

–20

–40

–60

Air Freight

119

79

28

9

Ocean Freight

–39 –39

Logistics

2013 2012

Adjusted ebit by region Million CHF

80

70

60

50

40

30

20

10

0

–10

–20

2013 2012

1

–3

MEAC

71

65

APAC

23

–1

AmericasEurope

13

–12

15Strategy and Results

Panalpina Annual Report 2013

trade payables and accrued cost of servicesPanalpina’s trade payables and accrued cost of services at yearend 2013 amounted to CHF 762 million compared to CHF 773 million at yearend 2012 and hence saw a slight reduction of CHF 11 million.

other liabilitiesPanalpina’s other liabilities increased by CHF 37 million from CHF 441 million at yearend 2012 to CHF 478 million at yearend 2013 and can be mainly attributed to an increase in provisions in connection with the extraordinary charges mentioned above.

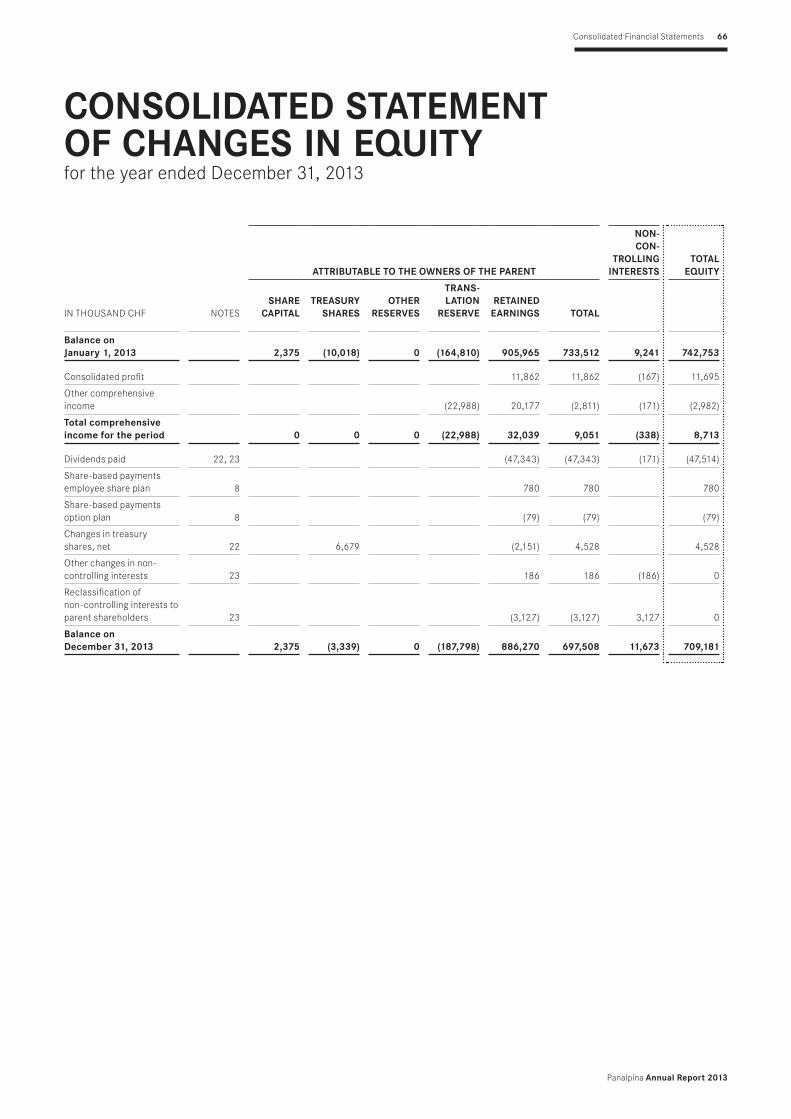

total equityTotal equity decreased by CHF 34 million during the reporting period, from CHF 743 million on December 31, 2012, to CHF 709 million on December 31, 2013. The decrease in shareholders’ equity mainly reflects the payment of the dividend.

cAsh fLoW net cash from operating activitiesPanalpina’s net cash from operating activities in the reporting period amounted to CHF 42 million (2012: CHF 72 million). Major contributors to this development were the improvement of the net result for the period and the simultaneous increase in provisions and net working capital.

cash flow from investing activitiesExpenditures on property, plant and equipment decreased by CHF 22 million during the reporting year to CHF 29 million (2012: CHF 51 million) as the company postponed certain investments not deemed as business critical in an effort to preserve cash. Capital expenditures in 2013 amounted to 0.8% of net forwarding revenue (2012: 1.3%), a figure which is in line with the company’s longterm average.Also, in 2012 the cash flow from investing activities was inflated by two extraordinary cash inflows: the Group had received inflows of CHF 57 million due to the repayment of money market and time deposits and a further CHF 28 million mainly due to the sale of its investment of 12% of Luxair SA’s shares. In 2013 no such extraordinary transactions were recorded. Overall, the net cash outflow from investing activities increased from CHF 10 million in 2012 to CHF 48 million in 2013.

total assetsMillion CHF

2,000

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

Cash and cash equivalents Trade receivables and unbilled forwarding services Other current assets Noncurrent assets

2013 2012

337 393

1,151 1,118

110 84

351 362

total liabilities and equityMillion CHF

2,000

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

Trade payables and accrued cost of services Other liabilities Equity

762

478

709

773

441

743

2013 2012

16Strategy and Results

Panalpina Annual Report 2013

cash flow from financing activitiesWhereas the company paid an ordinary dividend amounting to CHF 47 million in both 2012 and 2013, in 2012 an additional payment to shareholders totalling CHF 45 million (2013: nil) took place via a reduction of the nominal value of the registered shares.The net cash used in financing activities thus decreased from CHF 96 million in 2012 to CHF 41 million in 2013.

net cash

IN MIO CHFdec 31

2013dec 31

2012 diffeRence %

Cash and cash equivalents 336.9 393.1 –56.2

Other current financial assets 5.5 0.0 5.5

Shortterm debt –3.1 –1.6 –1.5

Longterm debt – 0.2 – 0.2 – 0.0

Net cash 339.1 391.3 –52.2

Net cash decreased by CHF 52 million during the year under review to CHF 339 million on December 31, 2013 (December 31, 2012: 391 million).

17Performance by Product

Panalpina Annual Report 2013

PeRfoRmAnce by PRodUct

AiR fReight

market situationIn 2013, the macroeconomic environment has improved and slightly increased demand for international traffic. The air freight market has therefore returned to growth. Freight rates remained under pressure due to steadily increasing overcapacity. However, fuel prices only slightly increased in 2013. Further shift of production and increased demand from middleclass households led to volume growth on Asia (both in and outbound) and IntraAsia trade lanes. Emerging markets in the Middle East, Africa, CIS and Latin America also contributed to air freight growth.

Looking at industry verticals, technology, fashion and manufacturing companies were the key growth drivers whereas perishables absorbed evergrowing capacities. Increasing requirements from regulatory authorities raised the demand for qualified temperaturecontrolled services.

highlights Investment in own controlled network. Increased load factors in own controlled network. Official opening of Luxembourg Pharma & Healthcare Hub, an important milestone in Panalpina’s GDPcompliant service offering as a prerequisite to retain healthcare customers and grow market share.

First totally paperless flight in the air freight industry. Industry leading Global Sourcing Program. Business wins enabled Panalpina to grow at abovemarket rate.

outlookPanalpina is cautiously optimistic for the 2014 air freight market. Rates are expected to follow a sideways trend as new aircraft deliveries increase supply above demand, and passenger service demand grows nearly twice as much as cargo demand. The fuel risk will remain a major threat. Panalpina strives to catch up in perishables, consumer and retail, and fashion, while increasing activities in healthcare. Growth in emerging markets, such as the Middle East, Africa, CIS and Latin America, will be leveraged. Digitalization of air freight documentation will continue and improve productivity.

oceAn fReight

market situationMajor trade lane uncertainty continued unabated. The market showed extreme rate volatility due to a supplyanddemand imbalance from carriers. This was driven by a significant buildup of new tonnage in the Far East Westbound trade as well as the impact of the cascading effects in other Asiaoutboundrelated trade lanes. Nevertheless, the global demand for ocean freight grew by approximately 34 % against a net capacity increase of 6%.

highlights Further enhancement of global LCL network, Panalpina now operates more than 450 services globally. Ocean freight TEU growth was well above average market growth. The intraAsia trade lane developed extremely positively. Managed Solutions team was established and new order management based on the software MyPanalpina+ was rolled out. Panalpina made inroads into niche markets such as the transport of recycled materials.

Fully integrated door-to-door solutions – Panalpina combines the intercontinental transport of air and ocean freight with comprehensive valuegenerating logistics. Its three products end 2013 with strong results and further developments.

18Performance by Product

Panalpina Annual Report 2013

outlookGlobal market growth of 3–4 % is anticipated for ocean freight in 2014. Traditional trade lanes, like Far East Westbound and Transpacific Eastbound, will start to recover. The overcapacity and cascading effect will continue to cause rate volatility. Panalpina will focus on nontraditional trade lanes, such as intraAsia, AsiaLatam or AsiaMiddle East.

Logistics

market situationThe outsourced logistics market continues to grow. The nature of some customer’s supply chains is changing as they consider nearshoring and onshoring. This is not only driven by transport costs, but by the rise in manufacturing costs in previous lowcost labor markets and by government investments and incentives to stimulate local economic growth.

highlights ValueAdded Services in targeted industry verticals grew to 13% of Logistics business. Introduction of Logistics Manufacturing Services (LMS) as a distinct product; Panalpina undertakes the inventory planning, shop scheduling, final assembly, configuration and testing (FACT), and quality assurance of Technology Infrastructure Products.

20,000 sqm highfashion hub opened in New Jersey with semiactive RFID item tagging, coupled with origin consolidation, air freight forwarding and destination services in an endtoend solution.

New facilities opened in New Zealand, Austria, Australia, Singapore, Colombia, United States, Poland and Brazil. Accreditation from The Lean Enterprise Research Centre allowing PA Logistics to certify Lean practitioners. Research partnership established with Cardiff Business School for demanddriven inventory modelling. Continuation of Red Prairie rollout as Panalpina’s global platform for logistics operations.

outlookIn 2014, eliminating the legacy loss making businesses and further establishing VAS within Logistics will continue. For VAS, the focus is in the industry verticals Panalpina has gained most traction in, such as technology and fashion. As the manufacturing cycle decouples within certain sectors, positioning Panalpina as a logistics service provider in the location the customer requires, such as logistics manufacturing services close to enduser or fashion hubs offering endtoend VAS closer to the market, will be crucial.

19Performance by Region

Panalpina Annual Report 2013

PeRfoRmAnce by Region

AmeRicAs

market situationNorth America saw huge growth in industries such as oil and gas and automotive manufacturing. Crude oil production grew at a historic pace in the US, to over one million barrels per day. Automobile manufacturing increased in the US with the implementation of NAFTA (North American Free Trade Agreement) between neighboring countries, such as Mexico and Canada. As a result, US automotive factories exported over three times the amount of automobiles and light trucks from previous years. The air freight market was negatively impacted by increased volatility. The ocean freight market continued to outpace last year’s growth rate.The Canadian economy proved to be flat with high competition for Canadian business. The oil and gas industry in Canada has stayed strong with the production of tools and other machinery holding steady, much like in 2012. Substantial new business wins for Panalpina Canada resonated across 2013 for both the FCL and LCL Ocean product.

highlights Panalpina US capitalized its position in the North American oil and gas sector by strengthening core relationships and partnering with major players in the industry.

Panalpina celebrated the opening of a new coolchain facility in San Juan, Puerto Rico, to further leverage its strong position in the healthcare sector.

In September 2013, Panalpina Miami became the first USshared service center to officially become paperless.Upon implementing the early stages of the EFile program, Panalpina OSC Miami has centralized FCL import communications from ocean carriers to the business units electronically. This change in processing dramatically reduces the amount of time spent on each file with the added environmental benefit of eliminating paper consumption.

Panalpina implemented new LCL services, covering the main worldwide ports. Panalpina is supporting customers to prepare for mega events: the FIFA World Cup in a dozen different cities in 2014 and the 2016 Summer Olympics in Rio de Janeiro – both of which demand new infrastructure for telecommunication, transport and general market.

Panalpina Brazil consolidated its position in the aerospace sector, extended its Supply Chain Management Solutions and was honored as “Best Operational Service Supplier” and “Best Supplier of the Year”.

New temperature controlled services were implemented, anticipating the healthcare industry’s growing demands, which have seen an enormous surge in imported and internally manufactured pharmaceutical products.

Growth in Logistics, pushed by automobile spare parts and telecommunications operations in Brazil. A stateoftheart warehouse management system was implemented in all warehouses in Brazil, allowing us to deliver highquality and efficient services to our customers.

outlookGrowth of crude oil production outpacing the entire world market is expected to continue in 20142015. Automobile manufacturing should also keep its high growth rate leading to a substantial influx of reshoring or nearshoring activity. A further increase of volatility in the air freight market might impact mature markets such as the US. The United States continues with various port expansion projects to accommodate the introduction of super vessels. In turn this will most likely drive more demand towards the ocean freight forwarders.In Canada the proposed pipelines to the west and to the US could have a significant impact on shortterm infrastructure growth. Panalpina will take advantage from freight that originates from or is destined to the industry surrounding the oil sand exports. South America and its developing economies, which were the driving force in the past five years, are slowing down. Latin America's combined economies are expected to grow by 3.0 % in 2014, one of the lowest growth rates in recent years.

Moving ever closer to customers – The Panalpina Group has realigned its regional setup and introduced a fourth region consisting of the Middle East, Africa and the CIS (MEAC). Here is a look at the performance of this new region along with all the others in the world of Panalpina.

20Performance by Region

Panalpina Annual Report 2013

AsiA PAcific

market situationThere was slow market demand in Air Freight for the first eight months of the year, but much stronger demand towards the traditional yearend peak season. In terms of capacity, many carriers have adjusted to better reflect current market conditions. China continues to be the biggest market in Asia Pacific. Panalpina’s Logistics footprint is still relatively small. Panalpina will establish its business in niche markets to avoid competition with lowcost competitors. The global ocean trade forecast for 2013 was lowered from 4.5 to 3.8% in May 2013, primarily due to weaker Chinese trade growth, which in turn reduced figures across Asia.

highlights After two years of reduced volume, total air freight volumes (both imports and exports) grew by almost 8%, with strong growth from IntraAsia and AsiaLATAM trades.

Volumes and market share grew in traditionally weaker markets such as Thailand, Japan or Korea. Red Prairie was successfully implemented in Malaysia, marking its first use in Asia. Expansion of a logistics facility in Singapore, from 4000 sqm to 26,000 sqm. Solid ocean freight growth on IntraAsia trade lanes. Implementation of 26 new direct LessthanContainer Load (LCL) services in Asia.

outlook2014 is expected to remain highly volatile and uncertain in view of airlines undertaking massive capacity rationalization. Buy rates will remain unstable and unpredictable, characterized by multiple short term spikes. Carriers will also continue to rationalize and remove capacity in view of the losses they have sustained over the last few years. In terms of market outlook, IntraAsia is expected to remain stable, though Transpacific and FEWB are expected to remain volatile in view of the uncertain economic outlook in both markets. The need for innovation remains high, especially regarding valueadded services that enhance supply chains.

eURoPe

market situationIn the European Union, GDP stagnated in 2013 after a decline in 2012. Across the euro area, the economic situation has not improved and unemployment rate remains very high with the exception of Germany. Pressure on margins and rate volatility remained high in ocean freight and air freight. The generally poor economic situation, and a drop in consumption in SouthEuropean countries, led to negative development in freight volumes on European routes. Inbound trades from Asia saw high volatility and pressure on ocean and air freight rates. Volume has grown and Panalpina succeeded to counter the market trend. Export volumes have grown from Europe to Asia based on Panalpina’s strategy to invest in new market segments, e.g., secondary raw materials. Especially in the fields of oil and gas, healthcare and automotive where Panalpina could win market share.

highlights Luxemburg/Frankfurt gateway optimized transit times and pricing as well as the utilization of Panalpina’s own controlled air freight capacities.

Restructuring of overland business helped to counter the negative market trend in Europe. Very successful implementation of new business in Azerbaijan, Turkey and Middle East in oil and gas and other major industry verticals.

Restructuring of geographies and reduction of overhead cost led to steady improvement of bottom line. Strong growth in the ocean Far East westbound trade through focused sales approach. New logistics opportunities and end–toend business was acquired and implemented.

outlookMuch like in 2013, the Baltic States will yield the strongest growth in 2014. The main impact on the euro area’s recovery will be a combination of growth in Germany together with a modest return to growth in Italy and Spain. Outside the euro area, Sweden and Britain are expected to show promising GDP growth in 2014. A clear product organization, and focused marketing and sales teams, will facilitate the uplift in demand and help to market all products more effectively. The margin pressure and volatility will not change in the near future. The new regional organization is able to react faster to challenges in all markets and trade lanes.

21Performance by Region

Panalpina Annual Report 2013

middLe eAst, AfRicA And cis

market situationGeneral market conditions in the Middle East were mixed in 2013. A number of countries were severely impacted by the Syrian conflict, which also disrupted the overland services from Europe to the southern part of the Middle East. Other countries were impacted by domestic conflicts, including Egypt and Bahrain, or global trade embargos, as in the case of Iran and Syria. Some countries, including Saudi Arabia and Iraq, developed positively due to large investments in infrastructure to support the oil and gas and petrochemical industry. However, conditions remained very challenging even within these countries due to severe congestion at ports and airports. Overall the UAE developed positively due to growth in the domestic market as well as growth in the need for logistics hub services in Africa.

highlights Large growth in volumes, GP and EBIT. Turnaround in Turkey from loss in 2012 to positive EBIT in 2013. Established fully owned Panalpina operating entities in Iraq (Basra and Erbil). Obtained Saudi Arabian General Investment Authority (Sagia) approval to open two additional entities in Saudi Arabia (Jeddah and Riyadh).

Significant new business in Saudi Arabia and Iraq. Double digit growth in oil and gas business across the Middle East. Strong growth in ocean and air freight volumes out of Dubai to Europe and Africa.

outlookPanalpina will concentrate on growing its business in the Middle East and Turkey, where the company has a solid foundation and enjoys positive market conditions. The region will streamline its service and customer portfolio in West Africa, and invest in improving its service levels. Organic growth will be the subject in CIS, covering all industrial verticals, while Panalpina will concentrate on oil and gas, projects and telecom in Africa. From a product perspective Panalpina will focus on the development of Dubai as a gateway for air and ocean freight, serving Europe, CIS and Africa. The profitability of the Logistics facilities in Russia and Dubai will be improved by seeking the right customer mix. In Sub Saharan Africa market conditions are good for the oil and gas industry in almost all countries where Panalpina operates.

22Global Network

Panalpina Annual Report 2013

gLobAL netWoRK

Globally local – Panalpina operates a worldspanning network embracing some 500 branches. The comprehensive service is backed by the expertise of local teams who apply their uptotheminute insights on local conditions to deliver any time doortodoor solutions tailored to Panalpina’s customers.

Europe

5760

3974Net forwarding revenue in Million CHF

Fulltime equivalents

Middle EastAfrica

CIS 1631

770Net forwarding revenue in Million CHF

Fulltime equivalents

Americas

Fulltime equivalents4556Net forwarding revenue in Million CHF3114

Head Office

412Fulltime equivalents

AsiaPacific

3651

2789Net forwarding revenue in Million CHF

Fulltime equivalents

23Industry KnowHow

Panalpina Annual Report 2013

indUstRy KnoW-hoW

PAnPRoJects

Panprojects meets the project forwarding requirements of the energy and resources sector, which often involves the transportation of very heavy and oversized loads. It is an important part of Panalpina’s unique product range, together with the oil and gas industry vertical. Panprojects entered 2013 with a strong order book carried forward from 2012, which it added to throughout 2013, with noticeable successes in the liquid natural gas (LNG) and offshore project sectors. Mining stayed strong in Latin America but was less sustainable in other regions with some projects delayed. The Asia Pacific region remains the key growth area with major awards in South East Asia and Australia noted. Ongoing projects in the Middle East and contracts in the North Sea are other key areas of growth. Panalpina’s new Middle East, Africa and CIS region saw expansion in the Caspian sea area that will continue in 2014 and beyond. Africa is a key target for 2014 with some key awards in the pipeline at the end of 2013. Shale and crackingrelated projects in the US also drive business with domestic LNG plant construction awards in hand. Overall 2013 was a strong year for Panprojects.

oiL And gAs

For more than five decades, Panalpina has proven its commitment to the oil and gas industry with a focus on servicing the highly demanding upstream part of the business (exploration and production). Due to a stable oil price, investments in oilfield expansions, exploration and productions continue to be steady. Because of high capital expenditure requirements for tools and equipment, transport and logistics costs remained under pressure. Panalpina strengthened its position in the oilfield service sector, and continued to penetrate the drilling and deep water sector in 2013. The Panalpina’s oil and gas operations are setting the standard for compliance in the respective industry and are regularly consulted by major oil companies.

teLecom

The growing importance of highbandwidth mobile services, anytime and anywhere connections, video communication and mediadriven entertainment have caused significant investments in wireless telecommunications infrastructure – and this will only continue. There are increased market activities in telecom: emerging markets are expanding their networks while established economies upgrade to 4G technology. By 2107 there will be over one billion fast LTE (Long Term Evolution) connections in the world, representing approximately 12% of all mobile phone connections (around 8.3 billion connections). In the next two years, this segment will grow by 20% per annum, with overproportional growth in Asia and Latin America. Panalpina is well positioned to support that growth. In Latin America, for example, Panalpina has established light assembly (Semi Knock Down) infrastructure for an Asian network account for speedy reaction to market demands. This setup is a benchmark model that can easily be replicated elsewhere.

hi-tech

The PC market continues to decrease while tablet and smartphone use grows. For forwarders, this means smaller and lighter cargo, hence less profit. Clients are more and more interested in endtoend solutions with valueadded logistics. With IT spending for business solutions remaining flat and a growing trend to the bringyourown devices strategy, it is expected that IT spend in 2014 will grow by 4%, twice the amount in 2013. The hitech industry is still a very competitive environment where differentiation and reliable performance is king. To save money, air freight volumes are reduced and shifted to ocean freight. Panalpina continues to build relationships with small and mediumsized enterprise accounts, and it focuses its internal mindset on profitable business.

Comprehensive expertise and tailor-made solutions – Panalpina provides this knowhow to nine industry verticals, plus its special Panprojects product. In 2013 these ten verticals further strengthened their knowhow and gained new business. As of 2014, Oil and Gas and Panprojects will be managed as distinct products and no longer as industry verticals because of Panalpina’s marketleading knowhow in both fields.

24Industry KnowHow

Panalpina Annual Report 2013

heALthcARe

Healthcare remains one of the company’s fastest growing industry verticals. There is continual cost pressure on the pharmaceutical and medical device industry, due to governmental attempts to cut healthcare cost across the globe. The empty pipelines in pharma and higher generic competition increase the pressure on businesses. Pharmaceutical market growth has slowed in mature markets to 23% only, while “pharmerging” markets continue to show doubledigit growth, especially in China. Regulations are expanding everywhere and getting stronger, while GDP compliance must be guaranteed. Panalpina will continue to pursue GDP certification at its logistic hubs. As with hitech, healthcare companies are reducing their logistics spend by shifting from air to ocean freight. Meanwhile, the efficiency of logistics solutions are more and more in focus (visibility, control, innovations, quality, planning, cost). Network optimization is required now more than ever.

mAnUfActURing

Panalpina provides transportation and logistics services that make manufacturing companies’ supply chains leaner and more agile. In return, Panalpina’s customers achieve the necessary flexibility to effectively manage their clients’ complex supply and demand. Panalpina’s competition is very comfortable in this vertical because the big players are very open to new ideas and concepts. All the traditional manufacturing markets are strong and manufacturing has rampedup globally, with the focus on Asia Pacific and the Americas. Market conditions do not change very quickly in this segment, therefore the outlook will not change for years to come. Panalpina has noticed a strong tendency to source domestically, but that is a slow process. Manufacturing customers are attempting to mimic best practices from the automotive industry, which opens up attractive opportunities for Panalpina to use its expertise in the Automotive vertical. A global restructuring of resources in manufacturing as well as in automotive is ongoing. Indications for the agriculture segment show very positive development over the next few years, especially in emerging markets, such as Africa.

AUtomotive

Panalpina’s operations in the automobile industry include the shipment of production materials and finished products across the globe. The vast majority of such cargo is transported by sea, but the industry continues to rely on regular air freight services to handle special loads, spikes in demand or urgent shipments. In 2013, the conditions in the automotive industry improved on 2012 and growth is expected to continue through 2014. Certain regions developed quite differently; a weak economy in Europe, accompanied by high petrol prices and an ageing population, puts a heavy burden on all massmarket carmakers, while the automotive industry in America is booming. Growth in China remained strong and progress is expected to continue. Panalpina’s automotive business picked up globally but at a slow pace. The new management team focused on solution selling rather than transactional business.

chemicALs

In the chemicals business environment, customers require dependable, ontime delivery from their suppliers. The chemicalgoods supply chain is very complex, leading to increased logistics and transport spend due to tighter security controls, environmental aspects, and increasing regulatory requirements. Customers are generally price sensitive and only switch their focus onto solutions once low prices are secured. In general, chemicals are highly reactive to changes in the world’s regional GDP. Therefore, worldwide chemical production grew in 2013 but was weighed down by Europe with strongly declining freight volumes. Nevertheless, the chemicals market bears huge potential for Panalpina across all regions, especially in Asia. Flows of chemical products touch all major trade lanes. Panalpina’s managed solutions in ocean freight are well received by the chemical industry. As for air freight, the chemical industry depends on cargoaircraftonly (CAO) products because most of the cargo is not allowed on passenger flights, for security reasons. With its own controlled network, Panalpina is well positioned to meet these growing demands.

consUmeR And RetAiL

This industry vertical is in an exciting phase right now; in line with technical developments and tablet launches, ecommerce is booming and consumers are quickly finding new channels to meet their buying needs. This has a massive impact on supply chains in terms of visibility, reliability, operational excellence and consolidation to ensure commodity is properly spread between the different retailing

25Industry KnowHow

Panalpina Annual Report 2013

channels. To counter changing buying behaviors while supporting fastmoving consumer goods (FMCG) and helping retail companies to navigate the multichannel environment, Panalpina has developed better endtoend visibility and optimization tools to ensure efficient consolidation of cargo flows. Its investment in a new order management tool secured new business, predominantly with mediumsized retailers. Despite the slow market, Panalpina’s consumer and retail vertical performed well, with 10 % growth, outperforming the market. The achievement is the result of a focused sales approach towards global FMCG giants, plus some major furniture and big box retailers.

fAshion

Fashion brands are fighting for perception more than ever in a world with an everincreasing number of buying channels. In a multichannel retail environment, a new brand experience is just a click away. Additionally, the world’s buying power is rapidly increasing and by 2020 one billion additional middleclass people will populate these channels. In line with increasing global buying power, the fashion industry is growing rapidly – not least are luxury brands. Historically, fashion is a strong industry vertical for Panalpina. The company will develop fashion competence centers to leverage on its experience and meet future demands. The ambition is to build endtoend solutions for fashion customers that give a high degree of visibility, out and inbound logistics solutions, plus finalmile delivery. The current business environment is marked by a recession in many European countries, which has led to slow development in Asia. Even though the US is experiencing stronger growth, Panalpina had a weak year in the industry, mainly because of its high dependency on European fashion retailers. Eroding margins in air freight was another clear reason for slow growth.

26Compliance

Panalpina Annual Report 2013

comPLiAnce

Panalpina’s corporate culture evokes shared values, crosscultural understanding and ethical behavior based on fairness, respect and responsibility in all its dealings – both inside and outside the company. Its Code of Conduct is central to Panalpina’s business success and enhances its reputation as a company that takes ethics and compliance seriously.

Recognizing the importance of employees understanding how their actions contribute to the success of the company and the condition of their workplace, Panalpina expanded its Code of Conduct in 2012. The intention was to further emphasize the need for employees to show the highest standards of ethical conduct and acceptable behavior. This new Code of Conduct has been instrumental in supporting Panalpina’s goal to fully integrate its values across the company and influence the actions of its employees.

With an emphasis on committing to performance, integrity and professionalism, the Code focuses not only on laws and regulations but on expectations of personal conduct. The Code covers detailed information on fostering a positive work environment by valuing diversity, rejecting discrimination and harassment, ensuring fair employment practices, and upholding health and safety measures. Additional chapters of the Code provide guidance on avoiding conflicts of interest, conducting business with integrity (including information on anticorruption practices), ensuring financial integrity, managing the company assets and information and protecting the environment.

Available in 27 languages, the Code is accessible to all employees through the intranet and on Panalpina’s corporate website. Additionally, every employee is trained on the Code of Conduct through a facetoface session with their supervisor. Upon completion of this training, it is requested that each employee provide a signature to affirm their understanding of and commitment to adhere to the standards therein.

This structured training program started in 2012 and ran through 2013 to ensure all Panalpina employees were given adequate training on how to handle difficult situations. When such circumstances arise, employees are encouraged to report breaches of the Code of Conduct to their Human Resources managers or to the Corporate Ethics and Compliance Department. Alternatively, employees are free to report concerns to the Ethics and Compliance Hotline, which is a secure and confidential option for submitting reports at any time anywhere in the world, either by phone or online.

Adhering to strict corporate ethics is a cornerstone of Panalpina’s organizational structure. The Ethics and Compliance Officer reports right to the top, to the CEO and to the Ethics and Compliance Committee of the Board of Directors. Since 2008, Panalpina also conducts training on anticorruption, trade regulation and antitrust matters at various locations. And elearning modules are available as supplements for quick and easy referencing.

To ensure that training and materials make an impact, the Ethics and Compliance Department assessed Panalpina sites in 27 countries in 2013, resulting in visits to 53 offices and interviews with 282 staff. Approximately 13,000 people took comprehensive anticorruption training through elearning sessions, while onsite sessions for management also had 1,146 participants attending 93 sessions.

In addition, Panalpina strives to engage key suppliers in these matters. This effort to ensure honest practices throughout all aspects of its business is complemented by Panalpina’s involvement in the World Economic Forum Partnering Against Corruption Initiative (PACI) as a signatory member for the third consecutive year in 2013.

Performance, integrity and professionalism – Panalpina’s values reflect its strong and unique culture. Panalpina’s employees are proud to be a part of its mission and continually demonstrate their willingness to go above and beyond the call of duty for both the good of the company and its customers.

27Employees

Panalpina Annual Report 2013

emPLoyees

Panalpina’s four strategic human resource (HR) priorities remain at the core of the HR transformation strategy that was established in 2007. These are (1) to identify, attract and retain talented people, (2) to propagate a highperformance organization, (3) to develop leadership and other capability requirements and (4) to design, implement and optimize HR processes, policies, service delivery and resources to be “fit for the purpose”. These four priorities remain the organizing principles behind the ongoing efforts to make Panalpina’s HR team as efficient, effective and integral to its broader business success. A the end of 2013, Panalpina had 16,010 employees in over 70 countries. Its global human resources function is responsible for enabling organizational development so as to secure the high engagement and organizational effectiveness of Panalpina’s employees.

committed to hR transformationHR is committed to aligning its strategy and initiatives to assist the business effectively and efficiently, now and in the future. The transformation continued to focus on the “Business–HR partnership” in Panalpina through workshops and a HR effectiveness survey. In order to best deliver highquality HR services, we have ensured alignment between the HR strategy and business strategy. The HR structures have been adjusted to mirror the new matrix organizational structure of the business to facilitate efficient and effective partnership. HR processes are being continuously improved to effectively support the business and its line managers with the ultimate aim of HR to support attraction, development, engagement and retention of the right people, in the right parts of the company.

efficient human-resource managementIn 2012, the implementation of PanLink as the integrated humanresources information system solution continued extensive rollout in Panalpina. Other countries such as Switzerland, Italy, Austria, France, Turkey, China, Korea, Japan and Taiwan were added to the portfolio with over 6000 employees at the end of 2013 now using PanLink.The Panlink system supports all standard humanresource processes in the area of performance and talent management, and helps to align people to the Group’s strategy and goals. There are several other key elements to the PanLink system, such as the recruiting module that helps to quickly identify the best candidates for an open position, and the succession planning tool, which helps support the development and retention of Panalpina’s employees. In 2013 the recruiting and marketing platform and the learning management system was successfully piloted in USA and Canada. It is expected that by end of 2014 approximately 16,000 employees will be using the complete PanLink suite of tools with all employees having access to some modules.

creating new business leadersTalent management and succession planning to ensure that we have a robust pipeline of business leaders is crucial to our success. Over the past year, Panalpina has successfully attracted some really highprofile people from the competition. From being a company with a very basic HR department seven years ago and no core values, the organization now has a clear sense of its own identity and a concrete strategy for nurturing its employees and future leaders. As a result it has become an exciting and rewarding place to work that attracts some of the best in the business.The company continues to invest a great deal of time and resources in the development of its managers and leadership teams. In 2013, 36 more participants graduated from the “Navigating Our Future” program, Panalpina’s global talent program. This program is offered to highpotential employees in midsenior positions who are willing to pursue an international career. An additional 35 candidates were selected to participate in 2014. Over 225 department heads, team leaders and supervisors participated in three modules of the Steering Success global leadership and managerial skills program. This program is offered in Mandarin, German, French, Portuguese, Spanish, Italian, and English. The program has been strengthened with fresh content and a more refined focus to hone performance management skills.

Creating partnership with the business – Panalpina is committed to achieving its vision and engaging our employees to make this a reality is pivotal. By fostering a culture of transparent communications, customerfocused attitudes to collaborate across the boundaries, and a mindset of continuous improvement, the company will continue to recruit, retain and develop the best and most capable team of employees in the logistics industry.

28

Panalpina Annual Report 2013

In 2013, the four new learning and development programs covering communications, empowerment, performance management and skills were attended by over 500 employees. These programs have been designed globally for local distribution and have been very well received. In 2014, they will be offered in over 10 languages. These programs have created new opportunities to support the development of management and leadership capability within middle management. The sales academy is an important enabler to improve the sales performance across all layers with a focus on fastest and biggest impact. The academy will help identify and develop the right skills for the key sales positions. In 2013, the sales academy rolled out a robust set of programs – over 320 employees attended sessions led on consultative selling, value selling and recruitment of highperformance sales and pipeline management.

harnessing learning technologies to move forwardPanalpina is committed to using technology to ensure the ongoing and long term development of all of its employees. Eventually it is envisioned that we will implement a learning management module once PanLink is fully rolled out. Meanwhile, there are a variety of training opportunities in place for the staff, and all employees are encouraged to take advantage of these programs. In 2013, Pan Academy, Panalpina’s elearning platform, expanded to include 55 learning units offered in over 15 languages. These learning units cover subjects such as the company’s strategic environmental PanGreen initiative as well as operations, product competence, compliance, and refresher courses on code of conduct and anticorruption. Additionally 2013 saw the establishment of PanFilms, the company’s inhouse portal to disseminate key strategic messages and product information across the globe.

transforming the way we reward 2013 has been the year to educate and professionalize our HR people within the countries in the totalreward context, starting with grading all positions to the shop floor, positioning all positions by country, standardizing more and more the benchmarks we use, cascading further down bonus principles and finally looking at total reward including benefits. This process of education and professionalization of compensation and benefits in all countries is half way and will continue throughout 2014. We also prepared some standardization to ensure jobs are evaluated consistently across all countries at all levels and we prepared the rollout of the new country business organization.We also assessed in depth our mobility practices with some amendments to our policy towards operational efficiency of our mobility service, better assessing the need and the business case for our assignments and adapting the policy by assignment type and business needs. The amended policy will become effective early 2014.Further we assessed our reward principles for our top management (Executive Board and Executive Committee) looking at all reward compounds and principles and debated this in the Board of Director’s Compensation and Nomination Committee with an action plan as a consequence which will be rolled out in 2014 and 2015.

Employees

29Information Technology

Panalpina Annual Report 2013

infoRmAtion technoLogy

Panalpina’s IT team focuses on three core concepts: firstly, IT resources must be deployed strategically to support the customer value proposition, which ultimately drives customer loyalty. Secondly, IT must provide integrated tools that improve productivity and efficiency throughout the business. Finally, the IT organization and infrastructure setup must ensure efficient operation while enabling product and service innovation to drive future revenue growth and efficiency.

transforming the it organizationAs Panalpina continues to focus on delivering abovemarket growth and improved profitability, it is important that IT is organized to support that strategy. Furthermore, with the plan to increase the standardization of processes across the company, IT needs to adapt accordingly. As a result, Panalpina’s IT organization was restructured in 2013.

For each Panalpina region, a Head of Business Solutions was appointed to focus on understanding customer needs and defining appropriate solutions, as well as supporting the deployment of standard solutions across the region. To support this improvement in customerfacing capabilities, the position of Head of Customer Systems was created. This role delivers a scalable portfolio of solutions, ranging from locally configured standard products to highly customized solutions, which support everything from general industry verticals through to bespoke customer projects, while continuing to deliver global support for strategic customers.

To drive the increase in productivity required to improve profitability, the Head of TM IT Program supports the implementation of the new transportation management system, while the Head of Productivity Systems manages other critical productivityfocused initiatives.

To ensure the alignment of IT with overall business goals, the Head of IT Governance drives improved governance of IT investments through better financial management, formal IT procurement and enhanced IT processes.

The new position of Head of IT Service Delivery combines IT Operations and Applications Support under one management structure, focusing on improving the integrity of our infrastructure and driving up service levels, while delivering synergies that reduce likeforlike IT operating costs.

improving performance through radical simplificationThe IT team is implementing a backbone of core information systems that is both stateoftheart and robust. This will enable the highspeed flow of information through the organization, facilitating decisionmaking, innovation and revenue generation.

A key component is the ongoing implementation of the transportation management system, which is expected to be completed in 2016. By the end of 2013, the new system and business processes for ocean freight were rolled out to five countries, namely Switzerland, Germany, Italy, Mexico and Singapore, covering 20% of the total ocean freight business. Altogether, roll out activities have started in more than 50 countries and will continue throughout 2014.

In addition, Panalpina is investing to support the growth in its Logistics business through the deployment of advanced warehouse management systems. This project has made significant progress and continued global rollout is expected over the next few years.

hit the road with information securityInformation security is taken very seriously. In recent years, the IT infrastructure has been strengthened by replacing and upgrading security technology, and by updating the Panalpina Information Security Policy. A critical element is Panalpina employees who must adhere to security policy. Awareness campaigns and mandatory elearning modules support these efforts.Also, Panalpina has invested in the strategic upgrading of professional datacenter facilities to significantly improve resilience and disaster recovery capabilities.

IT is key – The ability to collect, process, analyze and present information quickly and accurately enables Panalpina to maximize revenue, reduce costs and, more importantly, provide a worldclass service to its customers.

30Information Technology

Panalpina Annual Report 2013

meeting customer expectationsAnother key element of Panalpina’s IT strategy is to meet information and datarelated customer needs by improving customerfacing systems. This effort will initially focus on specific segments but ultimately will extend throughout the business. With myPanalpina+, a new order management product is introduced that is designed to address the increasing complexity of supply chains, while providing reliability and consistency. Customers benefit from enhanced orderprocessing capabilities, improved visibility, automated exception management and alerts. myPanalpina+ complements the internally developed myPanalpina application, which has proved successful for more than a decade.

outlookIn 2014, Panalpina will continue to improve its IT systems to increase efficiency, support customer needs and drive innovation. The deployment of the transportation management system is key to this effort. Managing costs will remain a focus in the coming year to ensure that limited resources are deployed effectively and IT systems operate at maximum efficiency.

31Procurement

Panalpina Annual Report 2013

PRocURement

Panalpina’s strong relationships with its partners directly impact its ability to maintain the competitive advantages it enjoys and to provide the highest value to its customers. Therefore the selection and management of subcontractors is a carefully managed process, to ensure that these relationships reflect Panalpina’s own values, and will ultimately support the strategic objectives and growth of the company.

As subcontractors play a crucial role in Panalpina’s business, it is imperative that they represent Panalpina well and meet the company’s high expectations regarding quality and ethical business practices. Therefore finding trustworthy partners who are technically qualified to meet the needs of Panalpina’s customers in a costeffective manner is a high priority. Subcontractors must have a proven track record in their business and have exceptional reputations for service and quality. Panalpina assesses potential suppliers based on strict criteria that reflect the company’s expectations in the areas of ethics and compliance, credibility, pricing, quality of service, consistency and performance. Coupled with these distinct selection criteria, Panalpina also recognizes the right of subcontractors to be treated with complete fairness. To this end, the company conducts its selection practices such that all subcontractors are provided an equal opportunity to be awarded contracts, regardless of nationality. Panalpina also does not have a policy to preferentially hire suppliers that are local to its operations. Regardless of a supplier’s location, it’s expected that all the company’s rules and policies are adhered to so that they may remain compliant with all applicable laws and regulations.

Panalpina considers compliance with all applicable laws and regulations as nonnegotiable for itself and for those with whom it does business. This is especially relevant in terms of national and international laws and regulations related to anticorruption, environmental protection, and other legal conditions. Panalpina takes all necessary precautions to ensure full compliance with all laws, including conducting internal audits and compliance audits of subcontractors to ensure that there are no unknown legal risks or liabilities and that there are no actual or perceived violations of any laws or regulations where Panalpina does business.