20121004swaps slides

TRANSCRIPT

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 1/27

Swaps

Financial Derivatives

Finance 206/717

Philipp ILLEDITSCH

Fall 2012

Financial Derivatives Fall 2012 1/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 2/27

Introduction

What are Swaps?

Commodity Swaps

Interest Rate Swaps

Financial Derivatives Fall 2012 2/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 3/27

Definition

A swap is an agreement between two parties to exchange cash flowsat future dates according to certain rules

Financial Derivatives Fall 2012 3/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 4/27

Swaps

Forward or futures are used to lock in price at one future date

e.g. price of oil one year from today

What if you want to lock in prices at different dates?

Option 1:

buy “strip” of futures contracts

Option 2:

enter into swap agreement

Swap is just sequence of forward/futures contracts, combined withborrowing and lending

Financial Derivatives Fall 2012 4/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 5/27

Commodity Swaps Example

Utility Inc is going to buy

100,000 barrels of oil 1 year from today

100,000 barrels of oil 2 years from today

Current forward/futures prices:

F 0,1 = $100/barrel

F 0,2 = $105/barrel

We will need interest rates: 1-year cont. comp. risk-free rate is 6%

2-year cont. comp. risk-free rate is 6.5%

Financial Derivatives Fall 2012 5/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 6/27

Commodity Swaps Example cont.

Swap agreement:

sign agreement with counter-party to buy 100,000 barrels in

both year 1 and year 2,

for price $X /barrel

What is swap price X ?

Financial Derivatives Fall 2012 6/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 7/27

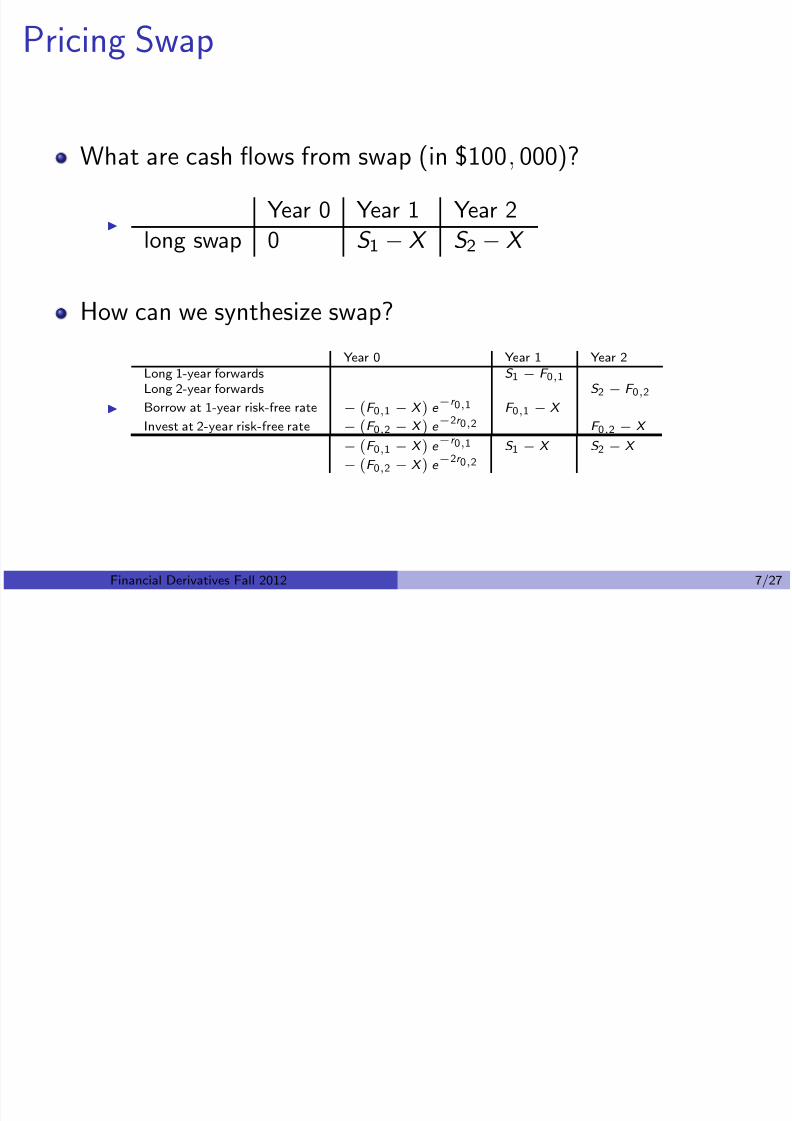

Pricing Swap

What are cash flows from swap (in $100, 000)?

Year 0 Year 1 Year 2

long swap 0 S 1 − X S 2 − X

How can we synthesize swap?

Year 0 Year 1 Year 2Long 1-year forwards S 1 − F 0,1Long 2-year forwards S 2 − F 0,2

Borrow at 1-year risk-free rate − F

0,

1− X e

−r 0,1 F

0,

1− X

Invest at 2-year risk-free rate −

F 0,2 − X

e −

2r 0,2 F 0,2 − X

−

F 0,1 − X

e −r 0,1 S 1 − X S 2 − X

−

F 0,2 − X

e −2r 0,2

Financial Derivatives Fall 2012 7/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 8/27

Swap Price

No-arbitrage implies

− (F 0,1 − X ) e −r 0,1

− (F 0,2 − X ) e −2r 0,2 = 0

i.e.,X

e −r 0,1 + e

−2r 0,2

= F 0,1e −r 0,1 + F 0,2e

−2r 0,2

Substituting in for forward prices and interest rates

X = 100e −.06 + 105e −2×.065

e −.06 + e −2×.065 = $102.4125

Financial Derivatives Fall 2012 8/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 9/27

In General

Suppose forward prices of oil are F 0,t

Then price per barrel of swap covering periods t 1, t 2, . . . , t n is

X =

n

i =1 e −r 0,t i

·t i F 0,t i n

i =1 e −r 0,t i

·t i

i.e. it is price at which PV of swap paymentsn

i =1

Xe −r 0,t i

·t i

is equal to PV of payments under strip of forward agreementsn

i =1

e −r 0,t i

·t i F 0,t i

Financial Derivatives Fall 2012 9/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 10/27

Swap Embeds Loan

To extent to which forward prices predict spot prices, Utility Incexpects to pay above spot price at date 1, and below spot priceat date 2

That is, there is loan hidden in swap price

Of course, spot prices might turn out to be different

But Utility Inc can use swap to construct pure loan

How?

Financial Derivatives Fall 2012 10/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 11/27

Value of Swap

Value of swap is zero initially

Value may change because

futures prices may change

interest rates may change

swap payments are made

What is value of swap at any time t ?

Financial Derivatives Fall 2012 11/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 12/27

Interest Rate Swaps

We will look at “plain vanilla” interest rates swaps

These swaps are an agreement for the exchange of floating rate

interest payments and fixed rate interest rate payments

As of Dec 2011, the Bank of International Settlements estimatesa worldwide notional amount outstanding of 403 trillion USD,and a market value of 18 trillion USD

Financial Derivatives Fall 2012 12/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 13/27

Example

Suppose BlueChip borrows $1M in a floating rate loan in October

2010, which they expect to repay in 3 years e.g. they take 1-year loan for $1M , which they plan to roll-over

or they take 3-year floating rate loan

In either case, we assume that BlueChip pays interest of r LIBOR + 0.25%

(note: not continuously compounded)

To hedge interest rate exposure, BlueChip can use swap

agrees to pay amount equal to $1M × (r fix − r LIBOR ) tocounter-party

say LB (large bank)

Financial Derivatives Fall 2012 13/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 14/27

Example cont.

BlueChip’s resulting net payment is

$1M × (r LIBOR + 0.25%) + $1M × (r fix − r LIBOR )

= $1M × (r fix + 0.25%)

They have converted 3-year floating-rate loan into a 3-year fixedrate loan

Financial Derivatives Fall 2012 14/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 15/27

Example cont.

12-month LIBOR rates turn out to be:

Oct 2010 6%Oct 2011 5%Oct 2012 8%

i.e. if you take 12-month $1,000 loan in Oct 2010 at LIBOR,you must repay (1 + 6%) × $1, 000 in Oct 2011.

If BlueChip’s swap agreement specifies annual payments,

and uses fixed rate of 7.2%,

then loan interest payments and swap payments made byBlueChip to LB are:

Financial Derivatives Fall 2012 15/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 16/27

Net Payments

Oct Interest payments Swap payments/receipts Total2010

2011

2012

2013

Financial Derivatives Fall 2012 16/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 17/27

Net Payments

Oct Interest payments Swap payments/receipts Total2010 0 0 0

2011 $1M × (6% + 0.25%) $1M × (7.2% − 6%)

= $62,

500 = $12,

000 $74,

5002012 $1M × (5% + 0.25%) $1M × (7.2% − 5%)= $52, 500 = $22, 000 $74, 500

2013 $1M × (8% + 0.25%) $1M × (7.2% − 8%)= $82, 500 = −$8, 000 $74, 500

Floating rate used here is the one 12-months prior to paymentdate

Financial Derivatives Fall 2012 17/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 18/27

Fixed-Rate and Floating Rate Payers

BlueChip is fixed rate payer

LB is floating rate payer

Why would somebody prefer fixed over floating payments?

Why would somebody prefer floating over fixed payments?

Financial Derivatives Fall 2012 18/27

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 19/27

Swap Pricing—Back to Example

BlueChip entered into swap agreement with LB in October 2010

Swap agreement required BlueChip to pay $1M × (r fix − r LIBOR ) forthree years

Let r LIBOR t ,t +1 denote LIBOR rate from date t to date t + 1

What is cash flow of Blue Chips’s swap position?

2010 2011 2012 2013

swap 0 $1M ×

r LIBOR10,11

− r fix

$1M ×

r LIBOR11,12

− r fix

$1M ×

r LIBOR12,13

− r fix

Financial Derivatives Fall 2012 19/27

P S

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 20/27

Pricing Swap

We could do this just as before with commodities

e.g. LB’s cash flow in Oct 2012 is $1M ×r fix − r LIBOR 11,12

where r LIBOR 11,12 is 12-month LIBOR rate from Oct 2011 to Oct

2012

LB could hedge floating rate, r LIBOR

by locking in forward rate; e.g. using FRA or Eurodollar futures

We could then take the present value of certain cash flows andfind the value of r fix such that the net present value is zero ...

Financial Derivatives Fall 2012 20/27

E i W D i P i

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 21/27

Easier Way to Determine Price

Financial Derivatives Fall 2012 21/27

E i W D i P i

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 22/27

Easier Way to Determine Price

Cash flows of LB’s swap position are

2010 2011 2012 2013

LB’s swap 0 $1M ×

r fix − r LIBOR10,11

$1M ×

r fix − r LIBOR11,12

$1M ×

r fix − r LIBOR12,13

buy a fixed 0 $1M × r fix $1M × r fix $1M × r fix

rate bond −B fix2010 +$1M

sell a floating 0 −$1M × r LIBOR10,11 −$1M × r LIBOR11,12

−$1M × r LIBOR12,13

rate bond +B float2010 −$1M

Let B fix2010 denote price of fixed rate coupon bond in Oct 2010 that matures in

Oct 2013

Let B float2010 denote price of floating rate coupon bond in Oct 2010 that

matures in Oct 2013

No arbitrage implies that B float2010 = B

fix2010

Financial Derivatives Fall 2012 22/27

E i W t D t i P i

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 23/27

Easier Way to Determine Price

Net cash flows would be same if:

BlueChip pays LB $1M × r fix in Oct 2011, 2012, 2013

and in Oct 2013 pays LB principal $1M

LB pays BlueChip $1M × r LIBOR in Oct 2011, 2012, 2013

and in Oct 2013 pays BlueChip principal $1M

That is:

BlueChip sells LB bond that has face value of $1M , and pays

coupon rate of r fix

LB sells BlueChip bond that has face value of $1M , and payscoupon rate equal to LIBOR rate

Choose r fix such that B fix2010 = B

float2010

Financial Derivatives Fall 2012 23/27

Wh t i Bfloat?

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 24/27

What is B float2010?

What is price of bond that pays floating rate (LIBOR) as coupon?

Bond that is paying floating rate is just worth par value

Back to example

Price at maturity is equal to face value; i.e. B float2013 = $1M

What is B float2012 ?

B float2012 = $1M × r LIBOR12,13 + $1M

1 + r LIBOR12,13

= $1M

What is B float2011 ?

B float2011 =

$1M × r LIBOR11,12 + B float2012

1 +r

LIBOR11,12

= $1M

What is B float2010 ?

B float2010 =

$1M × r LIBOR10,11 + B float2011

1 + r LIBOR10,11

= $1M

Financial Derivatives Fall 2012 24/27

Wh t i ?

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 25/27

What is r fix?

r fix is coupon rate such that B fix2010 = B

float2010 = $1M

Suppose yield curve in 2010 is: r 0,1 = 6%

r 0,2 = 6.5%

r 0,3 = 7%

We have

$1Mr fixe −0.06 + $1Mr fixe

−0.065×2 + ($1Mr fix + $1M ) e −0.07×3 = $1M

Solving for r fix:

r fix = 1 − e −0.07×3

e −0.06 + e −0.065×2 + e −0.07×3 = 7.2%

Financial Derivatives Fall 2012 25/27

In General

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 26/27

In General

r fix is par value coupon rate

i.e. rate such that

T

t =1

e −t ×r 0,t $1M × r fix + e

−T ×r 0,T $1M = $1M

Financial Derivatives Fall 2012 26/27

Market Value of Swap

8/13/2019 20121004Swaps Slides

http://slidepdf.com/reader/full/20121004swaps-slides 27/27

Market Value of Swap

Swap has value of zero when it is issued

But not at subsequent dates

What is value of swap at any time t?

Financial Derivatives Fall 2012 27/27