2011 self funding magazine issue 26

DESCRIPTION

he Self Funding Magazine was created by healthcare executives who have run and administers self funded plans for employers for years. The creators of self funding magazine is Free Health LLC, www.freehealth.com a leading multi-media and publishing company and the creator of the Employer Healthcare Congress, www.employerhealthcarecongress.com, the leading national healthcare conference for employers. Thousands of companies provide either insurance products or vendor services and solutions in the self funded industry, and yet there is not a single dedicated online magazine with a large readership base. Employers and agents even to this day do not know where to look for quality TPA’s, administrators, networks, reinsurers, MGU’s and where to look for vendors who provide unique solutions and where to find the best self funded solutions.TRANSCRIPT

Self Funding Magazine

Self Funding Magazine

Self Funding Magazine

TABLE OF CONTENTS

Copyright © 2011 Self Funding Magazine. All rights reserved. Self Funding Magazine is published monthly by Global Health Insurance Publications. Material in this publication may not be reproduced in any way without express permission from Self Funding Magazine. Requests for permission may be directed to [email protected]. Self Funding Magazine is in no way responsible for the content of our advertisers or authors.

16 JULY 2011 EMPLOYER HEALTHCAREBENEFITS SURVEY RELEASED

START UP EXPENSES AND ORGANIZATIONAL EXPENSESby Sandy Botkin

29EDITORIALEditor-in-ChiefAssistant Editor

ADVERTISING SALES

PRODUCTIONGraphic Designer Tercy U. Toussaint

For any questions regarding advertising, permissions,reprints, or other general inquiries, please contact:

Jonathan EdelheitJenny Dodson

04 LETTER FROM THE EDITORTINY STEPS, THE RIPPLE EFFECT

by Jonathan Edelheit

06 HEALTHCARE CHEAPER, BETTER & FASTER IS THE “NEW” GAME

by Rajeev Mudumba

13 HEALTHCARE REFORM:THE GOOD, THE BAD AND THE UGLYby Christy Yaccarino

26 WHO IS RESPONSIBLE?by Theresa Healy

36 USING REMOTE HEALTH MANAGEMENT SYSTEMS TO MANAGE CRITICAL ILLNESSESby Jason Goldberg

TABLE OF CONTENTS

18 MANAGEMENT OF ORGANIZATIONALBEHAVIOR: THE HEALTHIEST COMPANY TO WORK FORby Toni Sorenson

GOOD NEWS IN ALTERNATIVE SUPPLEMENTALPLANSby Scott Krienke

40

PROTECTING THE HEALTH OF EMPLOYEES TRAVELING OVERSEASby William W. Spangler

44

THE AMERICAN OSTEOPATHIC ASSOCIATION URGES AMERICANS TO BREAK THROUGH THEIR PAIN

by Dr. Giaimo

52

Self Funding Magazine

think one of the problems we are facing with the declining health of Americans is that we are trying to tackle the problem on too large of a basis; a macro level, when we should be focusing on a micro level. I think some insurance companies or employers think we can significantly change the way employees think, act and behave, and so

we try to implement large programs to encourage these monumental changes. The truth of the reality is that we need to think small, at first. We need to get individuals to want to change, and it doesn’t need to be a big step. Even a little step, can be like a ripple in a pond that has much larger implications, because once an individual takes that small step and wants to become healthy, a true transformation will happen. As an industry, we need to focus on where motivation lies at the core of the employees.

Our challenge is truly the fact of that matter that we are all busy in our daily work lives and caught up with family at home. In today’s culture, it can be overwhelming to fully engage in a healthy lifestyle. Between the constant distractions on TV, unhealthy food everywhere, and the fact walking has become an art form and we simply drive from place to place, it can be a true challenge to eat right and find time to exercise.

Here’s a thought- Let’s stop focusing on saying that we want employees to “engage” in healthy behavior, and instead, focus on motivating employees to want to engage in one simple, healthy behavior. If employees set an attainable goal, one that makes them feel better about themselves when they take action, they will strive to achieve even more. Once we can accomplish this, only then can we get employees to engage in an overall healthier lifestyle.

I

Jonathan Edelheit

EDITOR’S LETTER

Tiny Steps, The Ripple Effect

Self Funding Magazine

15w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

evisiting an old management truism, a business must execute cheaper, better and faster to do well. But alas, the magic formula has its own limitations. If you want high quality at a low cost, then it will take a long time. If it’s high quality at

a fast pace, then cost will take a hit and if it’s low cost at a high speed, quality will go down.

Now, this does not hold true for healthcare. Speed in terms of healthcare translates into the urgency to respond as well as the reach of that response. In other words, it translates into how many more people have access to service and how quickly in case of need. Healthcare is a high accuracy science and hence, efficiency and effectiveness go hand in hand. The solution is not viable just with reach; it has to produce the promised results. That’s where quality comes in. As for costs, the lower they are kept, the simpler healthcare is to manage

R

6 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Rajeev Mudumba

Self Funding Magazine

and the further its reach. Healthcare can be efficient while effective, accessible and still reasonably priced.

In today’s environment of healthcare reform and changing health dynamics, the success of future healthcare is hinged on doing better for less. And,

enterprises are awakening to this. In fact, some are already

headed in that direction.

According to a study conducted by Thompson Reuters, out of the $2 trillion spent

on healthcare, $700 billion is spent correcting preventable mistakes and errors [1]. There is

an estimated $250 billion spent on unnecessary procedures. In other words, about a trillion

dollars in savings are waiting to be discovered. With that much

money, we could more easily afford universal healthcare. And when I say universal, I am talking

about healthcare that is accessible to all.

The Centers for Medicare & Medicaid Services data shows that the agency spent $4.4 billion in 2009 on care for patients harmed in hospitals and another $26 billion on patients who were readmitted within 30 days [2].

According to the Kaiser Family Foundation, U.S. spends twice or more while leaving millions uninsured than other comparable countries such as France, Australia, Germany, Japan, etc., which spend less while covering everyone in their countries. Not only that, WHO studies have shown that we get less bang for our buck when compared to these countries.

Countries that are ahead of the U.S. in such studies have reflected valuable lessons we need to take note of.

Countries offering universal healthcare have shown that the care offered is the same to all citizens irrespective of their economic status. Canada, France and Israel have shown that investments in primary care are important [3]. Availability and accessibility of primary care to all ensures, that in the long run, there is a lower incidence of the need for urgent care which is both expensive and puts pressure on the available resources. Primary care advocates the wellness philosophy of prevention, thus helping control and minimize cases where a cure is needed.

Britain and France have advocated the optimization of non health personnel that are not doctors [4]. Nurses, midwives, physician assistants, etc.,

have their roles to play but can be optimized to service patients where a doctor’s expertise

is not necessarily required. These personnel can play an effective role is spreading the

reach of healthcare to remote areas and to non urgent clinical situations.

These countries have championed the cause of guaranteed treatment taking

7 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

out the debate around what is insurable and what is not, who can get treatment and who cannot. As a result, doctors can do what they are trained for, which is, manage people’s health instead of managing the business of health.

Prescription drugs are also relatively cheaper in the East than in the West. Reason; governments ensure that there is fair trade practice associated with drugs. In France and Japan, any injuries as a result of medical errors are promptly covered removing the need for medical malpractice law suits [5].

This does not mean that healthcare is totally on the right track in these countries. They are wrestling with their own issues. They face the same healthcare inflation that we do in the U.S. This results in higher taxes to sustain the system they have in place. These countries are also seeking avenues to fight

8 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

the rising costs of healthcare. But, they have a better percentage of satisfied citizens than we do.

Governmental intervention in healthcare is a double edges sword. On the one end, it is a major cause of today’s high and rising healthcare costs. Medicare, Medicaid, and tax deductibility of employer provided health insurance created a system in which patients at the point of service pay only a fraction of their medical bills out of pocket. This subsidized system puts pressure on the available resources and those guaranteeing services. On the other hand, the expectation is that the Government intervenes further in guaranteeing healthcare access to all while also bringing costs down. Healthcare is a service business and should be treated as such. Today, healthcare is big business generating multimillion dollars in profits for the service providers, hospitals, insurance companies and drug companies among others. It would be a culture change to move from this model to one where it’s treated as primarily a service business administered at reasonable costs and profits.

U.S. investors say they are focused even more intently than before on companies with products that aim to lower the cost of healthcare. Entrepreneurs are now thinking in terms of making healthcare more efficient. Just based on what we already know, let us review some immediate steps that can be taken to see results in the right direction.

1. Focus on Primary Care - As we have discussed before, countries that are doing better than the U.S in healthcare have shown that they have focused on primary care. Primary care ensures that preventive steps are taken proactively to reduce the risk of chronic conditions later. We should focus more on extending quality primary care to all and ensure that citizens are educated about primary and preventive care. Another point to note is that in countries like France, medical education is either free or highly subsidized. As a result, doctors are not burdened with loans once they finish their education. They have similar opportunities whether they specialize or go into primary care. In the U.S., doctors end up with

huge loans by the time they complete their education. They look for more lucrative careers and hence, pursue specialties since a specialist earns far more than a primary care physician. Steps need to be taken to bring primary care on par with other specialties so that primary care attracts quality health practitioners as well. Medical education can be subsidized to alleviate the loan burden on those who pursue it. Also, instead of relying solely on doctors, nurse practitioners can be leveraged to provide primary care across the country. Any or all of these measures will reduce costs, increase the reach and quality of healthcare.

2. Streamline and Digitize Medicine - Universal application of information technology to digitize patient records, physician practices and the interactions between healthcare providers, insurance carriers, third party administrators and Federal/State bodies will ensure lower costs and increased efficiency. Electronic Healthcare Records (EHR) and Computer Physician Order Entry (CPOE) are a step in the right direction. eHealth, Teleradiology and other advancements in eMedicine help improve accuracy while simplifying procedures. These investments today are poised for great savings in the future.

3.Standardize Prevention & Maintenance - Chronic illnesses are on the rise in the U.S. and the world. Chronic diseases are the number one

9 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

cause of death and disability in the United States. According to Centers for Disease Control and Prevention, more than 133 million Americans, 45% of the total population, have at least one chronic disease. Chronic diseases kill more than a million Americans each year, and are responsible for 7 of 10 deaths in the United States. Chronic diseases account for 75 percent% of the nation’s health care spending. Advocacy of health based prevention and regular health checkups are a precursor to tackling them. As a standard, if people have regular preventative health maintenance similar to the vaccine schedules and well baby checkups for children, most of the chronic illnesses can be prevented or caught at onset. When caught early, they are easier and cheaper to manage.

4.Manage Healthcare Accessibility - Healthcare costs vary within our own borders in the U.S. Based on the doctor-patient ratios in various locations, the number of patients seen by a practice also varies. As a result, there are rural locations where costs are less relative to urban locations and further, due to the lower doctor-patient ratio in such areas, the quality of care is also better. Such models should be propagated across the country. When the doctor-patient ratio is balanced in any area, it ensures better quality outcomes and can ensure balanced costs. To take healthcare to the most remote corners in the country, India is adopting telemedicine among its rural populace in a huge way. A foundation had been laid for a health superhighway to make the promise of universal healthcare a reality. The health superhighway will connect a chain of hospitals; both government and private through applications like telemedicine, mobile software and wireless networks so that doctors can connect with villages in India. Embracing technology and relying on resources other than just doctors to raise awareness levels helps lay the path to better health.

5. Tighten Control on Costs – In India, there is a growth in investments in a niche market for smaller

companies that want to make healthcare affordable, accessible, and ubiquitous. They offer high quality services similar to their larger counterparts, but costs are kept under a tight leash. The aim is to have hospitals that are accessible and efficient, run with a tight control on cost, and a firm grip on pricing. These companies are geared towards catering to the middle class and lower economic status clientele but without compromising on quality and service. Some of the innovative steps taken by them to cut costs include shared resources, mobile clinical units and scheduled procedures in various locations where healthcare is not accessible. Innovation is key to control costs. There is a lesson to be taken from this example that shows that a uniform quality of service at reasonable costs can

10 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

be provided to the farthest reaches of our society by leveraging innovative practices.

6. Advocate Checklists - Critical procedures can be monitored using simple checklists. These simple steps hugely contribute in minimizing medical errors as well as trauma and costs associated with such errors. ICUs in Michigan use a simple checklist famously chronicled in “The Checklist Manifesto” written by a cancer surgeon at Johns Hopkins, Atul Gawande. As we have seen before, a major chunk of healthcare costs are attributed to medical errors that are preventable. Adopting a checklist includes ensuring that simple things like hand washing and donning sterile gloves are done and it

proved very effective.In the first year, the Michigan hospitals reduced infections by two-thirds, saving 1,500 lives.Seton Family of Hospitals has shown successes in patient safety. They have adopted a nurse-led initiative that virtually eliminated bed sores, ranking Seton first internationally. Major reductions in infections were achieved. Seton has also dropped its birth injury rate to zero by putting best practices for obstericians around birthing processes. In 2003, when the safety initiative began, Seton billed Medicaid $500,000. In 2009, Medicaid was not billed at all [6].

This is just the beginning of a list. Further thought and discussion on this matter can provide several avenues for continuing the task of improving our healthcare infrastructure and services. Even without reinvention, restructuring our current healthcare system to make it cheaper, better and faster is a definite reality.

About the Author

Rajeev Mudumba works with a leading HRO/Healthcare organization. Rajeev has over 16 years of leadership experience in the HRO, Healthcare and

Technology consulting industries. His distinguished record of accomplishment and innovation includes high level strategy and ideation, precise execution and enhanced focus on efficiencies through the use of technology in business across various verticals. He can be contacted at [email protected].

References:1 Joe Flower, 15 Ways to Make Healthcare Cheaper by Making it Better3,4,5. Arthur Caplan, Ph.D, Spinning the globe offers lessons in health care. What does the rest of the world know that we don’t? - By Arthur Caplan, Ph.D – msnbc.com, Sept., 18th, 20092,6. Tony Inglis, Efficiency can make health care better and cheaper, May 10th, 2011

11 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

Self Funding Magazine

ow that the Patient Care and Affordability Act, otherwise known as healthcare reform, has been circulating for a while, we are seeing different aspects come to

light – as the good, the bad and the ugly of health care reform begin to take shape. Some aspects of the bill are good, and do put a focus on prevention and protecting the regular employee/consumer. But other provisions of the bill are bad, and some are downright ugly.

The Good

The good parts of the health care reform law are the following:

Preventative Care Covered at 100 Percent: Though this part of reform will initially add costs to plans, I do think it is a good provision. The only way to truly lower costs over the long term is to keep people healthy. And the way to keep people

By Christy Yaccarino

N

13 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

healthy is to ensure they get their screenings so problems can be detected early – while they can be treated with less cost.

Removal of Lifetime Maximums: Again, even though it will add costs to plans, I do think this is a good provision. If someone is going to hit a $1 million or $5 million maximum on a plan then they are seriously ill and should a plan then be allowed to just cut them off at that point when they truly need the coverage? The point to having insurance is for it to be there when you need it – and this provision allows just that.

Removal of Preexisting Conditions – First for Children, Then in 2014 for Everyone: Another one that may add costs to plans, but is a good provision. We should not deny coverage to a child for a pre-existing condition they have, and if we deny adults coverage for pre-existing conditions we will never get rid of the uninsured problem. However those with pre-existing conditions should be rated accordingly by the insurance carrier.

Nondiscrimination Requirements: Though this affects only non-grandfathered plans to start with, eventually it will affect all plans, and I do think it is a good provision. I don’t think it’s a bad thing to no longer allow key employees to have better benefits or costs than other employees.

The Bad

As for the bad parts of the health care reform law, they include:

Dependent Coverage Until Age 26: Extending coverage to age 26 with virtually no requirements is ridiculous. Under this law, a dependent can be married and still remain on their parent’s plan – and if the plan is not grandfathered they can even be employed with their own coverage and still remain

on their parent’s plan. There should have been more restrictions under this provision – such that you could not be married, could not have your own coverage available and had to be a full time student. It shouldn’t have been made the free-for all that it was.

Adding Cost of Medical Insurance on Employee’s W2 Beginning in 2012, for W2’s Issued in 2013: This is just an administrative nightmare for employers. There could have been a requirement made that once a year you have to notify employees of the cost of the medical insurance – but not on the w2. Employers are scrambling to ensure their systems are updated to allow this, and this is adding more cost to the employer.

Removal of over the counter drugs from Flexible Spending Accounts (FSA) reimbursement without a prescription: Removing over the counter drugs from allowable FSA reimbursements will drive employees to use higher cost medications that they can reimburse from their FSA. If they have to go to their doctor to get a prescription for an over the counter drug, they are most likely walking out instead with a prescription for a higher cost drug. This provision also increases medical plan costs by now forcing an office visit when not necessary in order to obtain the prescription.

The Ugly

And now for the ugly. These are parts of the bill that make you say what were they thinking?, and include:

Flexible Spending Account (FSA) cap of $2,500 in 2013: At a time when we are asking employees to pay more out of their paychecks for medical coverage, and more out of their pocket for deductibles, coinsurance and copays, limiting the FSA is not helping them. You’re now taking away

14 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

the one pretax benefit so employees are not only being asked to pay more for their medical coverage but they are also being asked to pay more in taxes.

“Cadillac tax” in 2018: This provision levies a 40 percent nondeductible tax on the annual value of health care plan costs for employees that exceed 410,200 for single coverage and $27,500 for family coverage beginning in 2018. Given the cost of medical inflation, by the time 2018 comes around, most plans will hit this threshold – even if they are not truly “Cadillac” plans. The threshold needs to be raised significantly if this is truly a “Cadillac” plan tax. Otherwise it just looks like another way to hit employees with a new tax, or significantly higher out of pocket expenses as plans will be forced to slash benefits to be under the annual value requirement.

Health care exchanges: This is a BIG ugly provision. Since every state is being left on their own to develop these it will be interesting to see how they play out. Carriers are not being forced to join the exchanges – so I wonder how many will choose to? If they do make it up and running, the exchanges will add tons of notification requirements onto employers and give many an incentive to no longer offer employee’s coverage – they can just send them to the exchanges. And let’s be serious, has the government ever implemented any program well?

There is still hope that these bad and downright ugly provisions will get modified as the fight against this bill continues in Washington….but I don’t think we should count on it. It seems that most – if not all – of the health care reform bill’s provisions are here to stay – for now anyway.

About the Author

Christy Yaccarino has been in the Benefits industry for over 8 years. She currently serves as Benefit Manager for Ambrose Employer Group in New York City and is a Contributing Editor

to Employee Benefit News. Previously, Christy was employed on the Corporate Health and Welfare team of Campbell Soup Company, and as a Benefit Consultant for Gallagher Benefit Services, one of the nation’s largest insurance brokers. Christy holds the employee benefit designations of GBA (Group Benefit Associate), EHBA (Employee Healthcare Benefits Associate) and HIPAAA (HIPAA Associate) and is a licensed insurance producer. She also holds a Bachelor’s Degree from Marist College in Poughkeepsie, NY.

15 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

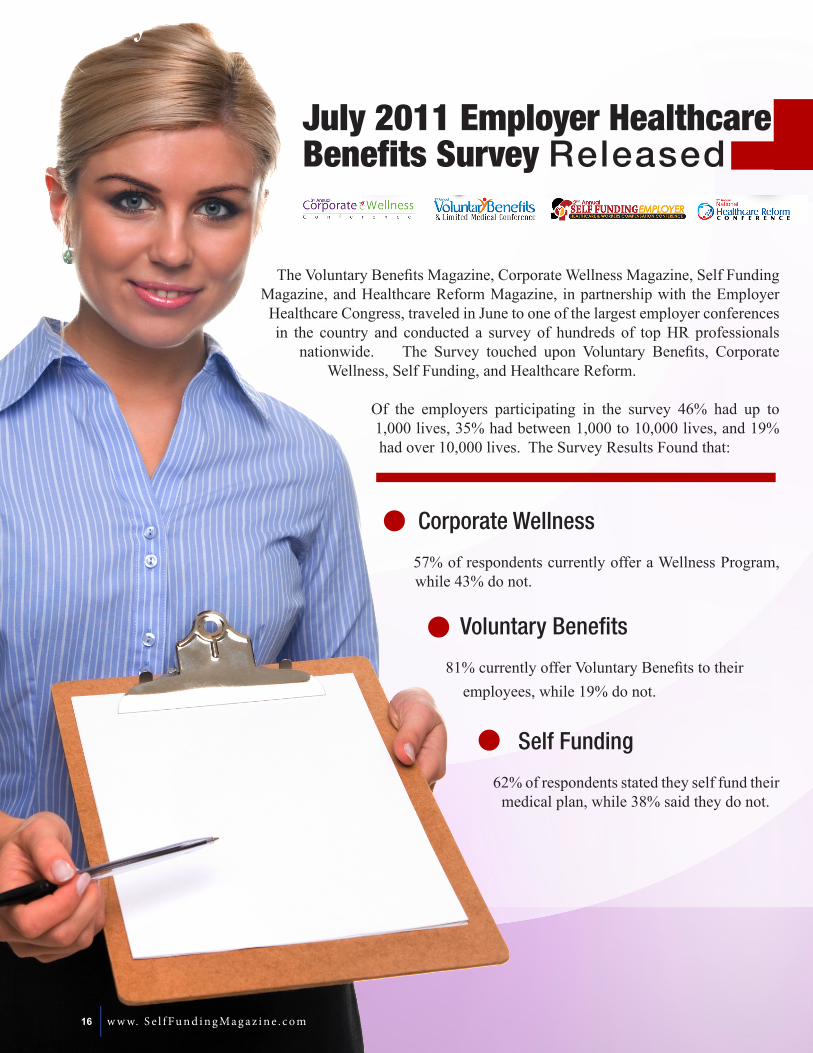

The Voluntary Benefits Magazine, Corporate Wellness Magazine, Self Funding Magazine, and Healthcare Reform Magazine, in partnership with the Employer Healthcare Congress, traveled in June to one of the largest employer conferences in the country and conducted a survey of hundreds of top HR professionals

nationwide. The Survey touched upon Voluntary Benefits, Corporate Wellness, Self Funding, and Healthcare Reform.

Of the employers participating in the survey 46% had up to 1,000 lives, 35% had between 1,000 to 10,000 lives, and 19% had over 10,000 lives. The Survey Results Found that:

Corporate Wellness

57% of respondents currently offer a Wellness Program, while 43% do not.

Voluntary Benefits

81% currently offer Voluntary Benefits to their employees, while 19% do not.

Self Funding

62% of respondents stated they self fund their medical plan, while 38% said they do not.

July 2011 Employer Healthcare Benefits Survey Released

Survey

16 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

July 2011 Employer Healthcare Benefits Survey Released

Healthcare Reform – Will it Increase Costs?

• An overall 76% felt healthcare costs would increase under healthcare reform; 57% of respondents felt that Healthcare Reform will significantly increase health insurance costs, while 11% felt it would lower healthcare costs. 19% felt it would just “increase” healthcare costs, but not significantly and 13% felt healthcare costs would remain the same.

Healthcare Reform – Will it be Positive or Negative for Business?

• 57% of respondents felt Healthcare Reform negatively affects their business while 43% believe it positively affects their business.

Healthcare Reform – Fine/Penalty for not buying insurance in 2014

65% of respondents felt that the $95 a year penalty for individuals who don’t buy health insurance in 2014 (increasing to $695 in 2016), is a large enough incentive to force people to buy health insurance. 35% of respondents felt it was not a large enough incentive to force people to buy health insurance.

Healthcare Reform – Destroying the Underwriting Process by Allowing Guarantee Issue and No Pre-ex in 2014

76% of respondents felt that starting in 2014, allowing any person to wait until they are sick to purchase health insurance and have immediate guaranteed coverage at the same price as a healthy person, would destroy the underwriting process, while 24% felt it would not.

Online Healthcare Information

78% of respondents felt that internet news, resource websites and social media are one of the most important sources for gathering information on healthcare issues, while 22% disagreed.

17 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

fter completing much research for the best long standing vehicle, you decided to buy that car and hoped it would last you for several years to come. You made all your payments

and carefully make sure the required scheduled maintenance was completed. Your oil changes have been done every 3000 miles and your tires replaced after 40,000 miles. You detail your car regularly and keep it in the garage when not in use. You even use

premium gasoline. You want to keep this car until it has over 200,000 miles.

Now, none of this maintenance above was paid for with your insurance premiums. Your car

insurance is available for that unfortunate accident or event that may cause damage to your car, yourself and others that may be involved.

We maintain our vehicles so they last, but we are not maintaining our bodies so they last. The health care industry has not put an emphasis on the importance of prevention. The U.S. Surgeon General Regina Benjamin said Monday that health care in the United States must shift its primary focus to disease prevention rather than the treatment of illness (Institure of Food Technologies, 2011). Consumer driven health plans have been on a rise, and our company has

one of those in a high deductible health plan as well as the traditional

By Toni Sorenson

A

18 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding MagazinePPO. Being self-funded, the organization pay for all claims and premiums and claims experience is based not on a large population as it is in fully insured health plans. But, the claims experience is calculated solely on the claims of the company’s employee population. We as a company need to pay higher attention to the health of the employee and change the focus to prevention.

We do not exercise regularly and it shows. Over the past several decades, obesity has grown into a major global epidemic. In the United States , more than two-thirds of adults are now overweight and one-third is obese. Research to date has identified at least four major categories of economic impact linked with the obesity epidemic: direct medical costs, productivity costs, transportation costs and human capital costs (Levine, 2010). Three out of the four categories financially impact our organization.

With the following statistics reported in the Denver Post late last year, wellness programs are becoming an essential element of the business plan.

• The projected 14.4 percent increase in insurance costs is up sharply from last year’s 11.8 percent rise and the highest since 2004, when Colorado premiums rose 15 percent.

• According to the Colorado Health Institute, the average total annual Colorado premium for an individual went from $1,910 in 1996 to $4,570 in 2009.

• Of the total, the employee portion rose from an average $350 to $971 a year, an increase of 177 percent since 1996. (Post, 2010)

Implementing an effective wellness program for company is not a short term goal and it is not an annual goal. To design, establish and refine a wellness program with a rate of return of five to one, it will take several years. Worksite health promotion can have a the following financial impact;

• Average 27 reduction in sick leave absenteeism

• Average 26 percent reduction is healthcare costs

• Average 32 percent reduction in workers’ compensation and disability management claims cost• Average $5.81-to-$1 savings-to-cost-ratio (Mercer, 2011)

With these economics forces laid out in front of us it make sense to establish wellness as an objective and goal for our organizational, and an organizational change should be implemented to benefit from the above reductions as well as intangible rewards such as more satisfied employees with higher energy levels and higher productivity.

How do you define wellness? We continually hear this word during the news, in conversations, at work or read it in newspapers, magazines and the like. Surprisingly, there’s no definition of wellness that seems to be universally accepted. Nonetheless there is a set of general characteristics found in most good attempts at define wellness. We routinely see a references made to wellness being a “state of well-being,” which is very vague. We also routinely see wellness defined as a “state of acceptance or satisfaction with our present condition.”

Truth be told, wellness is a very tough difficult word to define. Personally I like what Charles B. Corbin from Arizona State University has to say. He defines wellness as a “multidimensional state of being describing the existence of positive health in an individual as exemplified by quality of life and a sense of well-being.”

Wellness is considered to be an active process of becoming aware and learning to make choices (healthy choices) that lead toward a longer and more successful existence.

• We use the word “process” to note that further improvement is always possible

• We use the word “aware” to note that we are continuously seeking more knowledge about how we can improve.

19 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

• We use the word “choices” to note that we consider many options and choose those in our best interest. (Wellness Proposals, 2009)

In prior years the Wellness Committee consisted of a small group of volunteers that was given a slight budget and was activity based. Although the committee met once a month, it did not have any long term goals or no metrics. The intentions were good, but there was no way of measuring the rate of return or if their efforts actually changed the behavior of the employees toward healthier lifestyles.

Our current health and dental plans are self-funded. It is in our best interest as a company to assist the employees with their journey towards a healthier lifestyle and created better healthcare consumers. To accomplish this goal a strong three year plan is being proposed. The first year would be considered the year of employee engagement. The second year would be the year of health sustainment and the third year the year of health accountability. The first year will be establishing the program and engaging the employees to participate through programs, educations and rewards. The second year would be the year of maintaining the health and rewarding behavior change and acceptable health assessment numbers. The second year would incorporate the spouse as well in the program. The third year is the year you will be accountable for your health behavior and health assessment numbers. A two tiered rewards program will be introduced with a gold level and a silver level. Employees who have unhealthy habits such as smoking will have a higher insurance rate.

The organizational change must be carefully planned and should also align with the corporate goals and three year plan. The long term goal is to be the healthiest company allowing the company to pay 100% of employee premium. This wellness program will also allow the company to attract and retain talent.The attached addendum one is broken into: corporate

culture, employee engagement, communication, education, staffing/responsibility and budget, and then is further broken into years: one, two and three.

Corporate culture is the key for success, and will help form new values and expectations for the employee. It needs to start at the top with the legitimate power of the company, the executive leadership team (ELT) (James L. Gibson, 2009). Their support of this initiative is imperative, so the mission can be communicated throughout the organization. A strong model will need to be presented to gain their approval and support.

To start that cultural change, the company will need to ensure food brought into the company for meetings and functions is healthy. A class by a dietician for all the employees responsible arranging food for meetings and functions should would be beneficial. This philosophy should also include the foods that are offered in the company vending machines. Since the company has three shifts that range from 10 hours to 12 hours a day with employees on their feet during that time, we must also consider the types of food brought into the break rooms. It is recommended that healthy, high energy food should be brought in a couple times a week. The guidelines should be reviewed and incorporated into a Company policy. The Wellness Committee should also rebrand itself and align their mission with the corporate mission. Honoring the gift of donation, AlloSource responsibly develops processes and distributes lifesaving and life-enhancing human tissue for our communities. (AlloSource)

Communication is instrumental in exposure and engagement of the employees. There are several locations beside the headquarters. Posters will not be enough and there is the need to also provide communication electronically.

20 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

This can be accomplished through company e-mail blasts as well as through the company intranet. It is recommended wellness has its own SharePoint page on the intranet. That space will be used to house announcements, links to healthy site, a calendar of upcoming wellness activities, etc. It is further recommended that a section of the quarterly company meeting dedicated to the wellness program. Also, once the new logo is finalized, merchandise, such as water bottles, given to all employees can be used in everyday life as a reminder of the program.

Next, to assist in the employee engagement, rewards will need to be built into the three year program. Every employee will have different motivation for changing their behavior. A survey should be given to all the employees prior to creating the points/reward program. This survey is to evaluate the most effective

methods of rewards and the employees’ expectation of a wellness program. As we found discovered in the past, it is difficult to get more than thirty-five to forty-five percent of the workforce to complete a survey sent by e-mail. As a means of gathering information from most of the workforce the format should be at an event where most attend. The quarterly town hall meeting would be a great opportunity to have that done. A new device can instantly record their responses with a click of a button. This information is then gathered almost instantly and results calculated in charts. This technology could be used for other functions outside the wellness surveys. It is recommended that Marketing and Communication try this technology and evaluate its uses for the corporation. (Turning Technologies, 2002-2011)

The rewards or incentives could be premium deduction,

21 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

PTO days, drawing for big ticket items, awards

and public recognition. The rewards built into

the system should be both intrinsic as well extrinsic. The

rewards should also increase in value with each year of the

plan. But as with any reward, they should be earned thus making the

employee have a stake in their behavior

change towards a healthier lifestyle. The second piece of employee communication is actually education. Fear of not knowing or understanding certain aspects of their health can create resistance. To be better health consumers they need to be able to understand how to navigate through the health care system and our current health plans. We

22 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

must be able to give them the tools to accomplish that successfully. This can be done with additions to our health plans of disease management and medical claims case specialists. When a catastrophic incident occurs, the employees may need professional help to guide them through their illness or diagnosis, and they may need assistance to with compilation of claims and understanding of benefit payments. Lunch and learns can also assist the employee of the plan design and benefits.

As part of prevention the employee needs to be educated on how to have a healthy lifestyle. Lunch and learns on how to read a food label, healthy eating and portion control are just a few of the subjects. These can lead to reducing cholesterol and current BMI as well as other possible health problems.

Establishing healthy exercise is also a key factor in the prevention of many health conditions. Negotiating a corporate wellness program with a local gym would be a beneficial benefit to the employee. This will offer an avenue to foster employee exercise that will not only assist in exercise but could also improve their mental state of mind.

A third element is offering actually sponsored programs and activities to foster these behaviors. If the screenings reveal that a significant population of employees has a noteworthy problem, the company can address this by adding a program designed around

changing that behavior. This could be version of the biggest loser that would create competition

as well as offering the group dynamic of support in the same effort. Or giving credit or rewarding points for community events such as the “Donor Dash” and “Race for the Cure,” aids the employee their goal for physical activity. This also aligns with the company mission of giving back to the community. Other activities of team play where points can be given are a

bowling or softball league. Other

programs can planned for lunch or breaks such as walking programs. Pedometers can be given with the new logo to assist the employee with recording the calories or distance walked.

Centers for Disease Control and Prevention that smokers cost the country $96 billion a year in direct health care costs, and an additional $97 billion a year in lost productivity. (Werner, 2009). This is a staggering figure that affects almost every business. Substance abuse can also be costly to a company in health care claims, job related injuries, absenteeism, and lost production. We need to offer a tool of intervention for those who are willing to try to make that change. It would be wise to include that as tool in a confidential website, and after successfully completing that intervention, an individual would receive reward points toward the incentive.

The campus could also decide to become tobacco free. There will be much resistance from those employees that smoke or use tobacco. They need to be given plenty of notice before implementing this new policy. The policy needs to be in writing and distributed to be then employees. The argument that will need to be addressed is it is not the business of the corporate. There is some education of how smoking indirectly affects health care claims, absenteeism and lost productivity.

Addendum two is the first year proposed rewards system. The above points of communication are outlined as categories in the point system. A wide range of activities of activities should cover the demographics of most of the organization. The minimum requirement of points, 600 out of 1118 points is extremely achievable. To show that the company is dedicated to the employee in this effort, the company should extend the definition of “volunteer” in the benefit that is offered to pay four hours a month for volunteer hours. The hours should actually be extended to include wellness hours. The employees who volunteer on the committee or assist

23 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

the wellness committee should be paid for that time and not use their lunch or break time. The wellness hours should be used only for AlloSource sponsored programs or events. This will need to be written into the current policy and redistributed to the employees. Managers will need to be educated on this policy and how it will affect their employees.

The current committee members are volunteers and a member of human resources. There are times when their workload would not allow them time to attend the meetings in the past. As the new three year plan is established management should communicate the importance of the committee involvement. The short term and the long term goals should also be part of the committee members’ SMART goals. By adding accountability to the committee the company hopes to minimize social loafing (James L. Gibson, 2009). The structure of the committee needs to include areas or departments that will add value to the committee. Human Resources, Marketing, IT and Safety are examples of departments that are important in the contributions they could bring to the committee.

Initial output and budget need to be assessed, metrics established and possible calculation on the return of investment. As with organizational change the results must ultimately have a positive outcome to the bottom line. Some of the factors are easier to measure than others.

Let’s start with the obvious: the cost of health premium and claims. The baseline needs to be established and probably the best way to measure would be based on the annual cost of healthcare per employee. There also need to be a baseline for participation in the program. Reasonable goals need to be established for each year to successfully achieve the long term goal.

Using prior year claims numbers and premium, the cost per enrolled employee is easily calculated. As it takes a few years to realize the rate of return, the first year reduction in claims might be minimal if any. A reasonable percentage in the decrease of claims per employee should be a little a two and half percent. An analysis the of current year claims will assist in designing the education and program that need to be targeted in the following year, but hopefully by year three the company will see a downward trend in the average healthcare cost per employee.

The second key metric is participation. To have an effective wellness program, participation need to be at least 70% of the employee population. This can be measured by annual health screening and personal wellness profile, which will be the only two required wellness activities. If the employee participation in the first year was forty-five percentages, it would be reasonable to try and increase the participation by ten percent a year. The wellness survey should also be done annually and adjustments can be made to the program to increase participation based on motivational factors and employee requirements.

Another measurable item is the number of recordable workman compensation accidents. As stated earlier in the paper there are three shifts with employees having to suit up to enter the core and work several hours at a time. It is important that those employees to be properly hydrated

24 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

and have eaten properly. Harvesting bone and tissue involves using sharp instruments and band saws. This could be a dangerous combination if an employee is not at 100% when starting their shift. Injuries can be tracked to see if there is a trend in the type of accident or injury. An example would be if there is a trend of repetitive motion injuries, a class on ergonomics can be conducted and mandatory stretching exercise performed before each shift.

And finally an item that is harder to measure is the reduction in absenteeism. Currently the organization has a personal time off (PTO) policy. But there is not distinction between scheduled PTO and unscheduled PTO. To obtain a baseline and then track usage the current policy must be revised and the procedure for recording PTO must be updated to handle.

A confidential database is required to house employee health records and data with HIPPA requirements. An evaluation of current wellness vendors will need to be done. Based on our employee demographics, the requirements of the database will become part of the scorecard in the review and comparison of the vendors. The younger population may want the look and feel of a social network while the others that are not as computer savvy want easy icons and navigation. The vendor must be able to handle the each tier of the current drafted wellness program. In addendum three is scorecard comparison of the industry top vendors. (Brent Atkinson, IMA, 2011) It is recommended that a focus group be formed that would contain employees from different areas of the company and with varied ranges of computer skills. Ask them to evaluate each of the vendor database sites and provide feedback. Each of the wellness committee also needs to evaluate the based on the current projected design and provide additional feedback.

The project implementation timeline for this organizational change should be not less than three months and not longer than six months. This timeframe will allow the company time to put out

a request for proposal for the health database and website. The design and implementation of the SharePoint page will also need to be incorporated into the timeline, and then be able to implement before the beginning of the next calendar year. This timeline all allows for a campaign of communicate of the new goals and mission of the Wellness Committee and to educate the employees on the upcoming wellness program.

The initial for the implementation of this program will the cost of the wellness vendor, the proposed activities and the time of the wellness committee. All of which are outlined in addendum three. Total estimated cost per employee will be $265 per employee. If we can achieve the five to one rate of return that would mean we could end up saving $1353 per employee or $397,800 of savings in the next few years. Each year will be evaluated and adjusted. I believe the total possible savings in dollars health far outweigh the initial costs.

Bibliography

AlloSource. (n.d.). Corporate Mission. 1994. Centennial, CO, United States.Brent Atkinson, IMA. (2011, June 18). Wellness Consultant. Wellness Vendor Scorecard. Denver, CO, United States.Institure of Food Technologies. (2011, June 17). Healthcare in the U.S. Must Focus Primarily on Disease Prevention: Surgeon General. Retrieved June 22, 2011, from Mews Medical: http://www.news-medical.net/news/20110617/Health-care-in-the-US-must-focus-primarily-on-disease-prevention-Surgeon-General.aspxJames L. Gibson, J. M. (2009). Organizations: Behavior, Structure and Processess. New York: McGraw-Hill Companies Inc.Levine, R. A. (2010). The economic impact of obesity in the United States. Washinton DC: DovePress.Mercer. (2011). Wellness at Work, Building the business case & program best practices. Mercer (p. 12). Denver: Mercer.Post, D. (2010, October 29). Colorado health insurance costs projected to rise 14.4 percent next year. Retrieved June 21, 2011, from denverpost.com: http://www.denverpost.com/business/ci_16463537Turning Technologies. (2002-2011). Audience Response Products. Retrieved June 24, 2011, from TurningTechnologies.com: http://www.turningtechnologies.com/audienceresponseproducts/Wellness Proposals. (2009). Defination of Wellness. Retrieved June 24, 2011, from WellnessProposals.com: http://www.wellnessproposals.com/definition-of-wellness.htmlWerner, E. (2009, April 7). HuffPost Living. Retrieved June 24, 2011, from TheHuffingPost.com: http://www.huffingtonpost.com/2009/04/08/how-much-does-smoking-cos_n_184554.html

25 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

hen it comes to your health, who do you claim is responsible for your well being? Are you of the thought that physicians and nurses are responsible?

Is it the insurance companies? Maybe you believe it is a government responsibility to see to it that everyone has health care.

What does wellness mean to you? Have you ever stopped to think about it? There are many interpretations for the word. One of the best ways I can explain it: Wellness is more than the absence of disease. It is a sense of balance and peace within oneself. It is the ability to know what you need to function optimally, both physically and emotionally. It is up to you, to supply the body and your life with the proper fuel.

Our healthcare system has turned into a disease maintenance system that treats a symptom and hopes the odds will be in your favor, and the problem will be gone with their treatment. But, fixing the symptom will not cure the problem that caused the symptom. In fact, many of the treatments, e.g. pills, will only cause more problems. In the book Selling Sickness, you can find, in great detail, the overwhelming data on how the pharmaceutical companies have become so “big” that it wasn’t enough for them to come up with authentic medications that truly eliminate the problem - antibiotics, for one.But with expanding parameters and “guidelines” for placing consumers on meds, even healthy people can be told they are sick and started on medications. The marketing strategies, using celebrities and rebranding conditions or ‘creating’ new conditions to convince

WHO IS RESPONSIBLE?By Theresa Healy

26 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

W

Self Funding Magazinethe population of this new ‘disorder,’are popular strategies on convincing the population not to worry, Big Pharma to the rescue! We can help with our newest medication! “You don’t have to suffer with…”, “Live your life free of pain with…”, and then there is the fine print or the quickly stated, very quiet disclaimers; call your doctor immediately if you experience this side effect or that side effect, and it could even cause death. Really?

The thought that drug companies would create new illnesses may seem outrageous to some, but according to industry insiders, it is all too familiar. In Reuters Business insight, designed for pharmaceutical company executives, they report that the ability to create new disease markets is bringing untold millions in drug sales. (1)

Anyone working in the healthcare system for any time can testify to the fact that parameters for dangerous numbers have changed quite a bit over the years. It used to be that blood sugars were normal from 60-110. Now, if you have numbers from 110-120, you are considered a diabetic. Blood pressures of 120-140 used to be considered ok, but now if you have 130 or above, you are considered in dangerous territory. These examples go on and on. And, the worst part is all it takes is one high number and you are prescribed a pill. It’s not considered someone might be under some stress, or passing flu, that would cause these numbers. And once the stress or illness has passed, the numbers will return to normal ON THEIR OWN! Or, you could prescribe some lifestyle changes that would actually correct the problem, instead of covering it up with a pill.

Let’s discuss cholesterol. Nations everywhere have spent more on cholesterol lowering drugs

in recent years than any other category of prescribed medicine. (2) AS A GROUP THESE DRUGS GENERATE 25 BILION A YEAR IN REVENUE FOR THE MANUFACTURERS. Cholesterol is another parameter that keeps being expanded, to include healthier people, and eight of nine experts who wrote the latest cholesterol guidelines are paid speakers, consultants, and researchers to the world’s big pharmaceutical companies. (3)

So what are we to do? The first step is to challenge and question the status quo. It is

very difficult finding any information on

drugs and disease that is free from the influence of drug companies. The boundaries on what are real illnesses and a stretching to

include healthier people are growing

larger and continue to be blurred. It is important

to talk to family and friends to help determine for yourself

if your

27 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

present pain, soreness, etc., are

reasons to see a physician, or something you can care for, and it will resolve on its own. The body does have an amazing ability to heal itself, without interference from chemicals. I am not dismissing there are real diseases and problems that need intervention from our healthcare system. All I am saying is to depend on the healthcare system 100 percent is not a recommendation I would give. My point in sharing this information is to ask the questions that will have you look at how you perceive your health, your role in your health, to evaluate for yourself and what is happening in healthcare. If you do not like what you see, evaluate if it is time for you to take your health back by changing your choices in food, adjusting your thoughts and increasing your physical activity. Your health is ultimately your own responsibility. It is up to us to make better choices, and listen to our body,because it will tell you what you need. If you treat your body well, it will give back great health to you.

About the Author

Theresa Healy, RN, CCH, HHC. has a 30 year history of nursing in various settings, with experience in intensive care, emergency and trauma. She presently is the Wellness

Center Manager for Vi, an Independent Living Retirement community in Scottsdale, Arizona. She is happy to be in a position to promote wellness and healthy aging among the residents. Theresa also stays connected and up to date on the trends and changes with the ongoing research in how healthy choices influence how well we age and extend the quality of life.

1. J. Coe,” Healthcare: The Lifestyle drugs outlook to 2008, unlocking new value in well-being,” Reuters Business Insight, Data monitor, PLC,2002.2. Ray Moynihan, Alan Cassels: “Selling Sickness,”, 2005; Chap.1. Pg 1.3. http://www.nhlbi.nih.gov/guidelines/cholesterol/atp3upd04_disclose. htm (accessed Nov. 16, 2004).Submitted by: Theresa Healy, RN, CCH, [email protected]: Rx Food: Let Food be your Medicine623.696.5709

28 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

W hat if I told you that most of you could be potentially missing $5,000, $10,000, $20,000 or even $40,000 or more of deductions?

Would you be a bit ticked? Even worse, this omission would result in not only a substantial overpayment of income taxes but an overpayment of state taxes, employment taxes and Medicare. Most of these problems are frankly due to ignorance of the tax laws. However, for those of you who are reading this, you won’t have this problem.

One of the most overlooked deductions constitutes start up expenses for individual

businesses and organizational expenses for corporations. The problem is that there are four ways people treat these expenses of which three result in bad results.

First, some people just ignore them, in which case, they get no deduction for these costs.

The second approach is to write all of them off without knowing the rules and under the hope that IRS won’t catch you. This can result in serious penalties and interest. Remember, the IRS doesn’t take kindly to pulling the wool over its eyes.

29 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

START UP EXPENSES AND ORGANIZATIONAL EXPENSESBy Sandy Botkin

Self Funding Magazine

The third approach, which some accountants have taken, is to capitalize these expenses. This results in cheating yourself of potentially tens of thousands of dollars in deductions that can only be taken when you sell or close your business.

The final, and best approach, is to take the deductions correctly.

What are startup expenses?

Startup expenses are amounts paid or incurred for:

1. Investigating the creation or acquisition of a business, or

2. Creating an active trade or business, or

3.Activities engaged in for profit and for the production of income before the day on which the active trade or business begins, in anticipation of the activities becoming an active trade or business and which would have been deductible if paid by an existing trade or business.

Common types of startup expenses include:• Advertising costs

• Salaries and wages paid to employees and their instructors for training before the business actually begins,

• Travel and related expenses incurred in the

course of finding potential distributors, supplies and customers before the business begins;• Salaries and fees paid to executives and consultants, as well as for professional services, if incurred before the business actually begins, and

• Expenses of investigating the creation or acquisition of a trade or business (investigatory expenses). These are the costs incurred in seeking and reviewing prospective businesses before reaching a final decision to acquire or enter any business. Investigatory expenses include expenses for the analysis and survey of potential markets, products, labor supply and transportation facilities as well as advertising and travel to search for new business as well as the cost of audits designed to help decide whether to attempt the acquisition

Sandy’s hot tip: The cost of a franchise, licenses for the business and initial purchase costs for distributorships might be deductible if the useful life of these items can be ascertained with reasonable accuracy. Thus, if it has an indefinite life, the cost would not be a startup expense and must be capitalized. Thus, these non-startup costs would only be deductible upon sale or closure of the business.Sandy’s elaboration: The major idea you need to know about startup costs is that it involves “new businesses” and “new careers” and “new professions.”

Thus, if you were to start up a new medical, legal, CPA or dental practice, you have start up

30 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

costs. If you were to start up as a realtor or real estate broker, you have start up costs. Any costs incurred to investigate starting up a new business are generally startup costs.

What aren’t startup costs? Now that you know what startup expenses are, you need to know what they are not. They do not include monies that you spend on interest, which are deductible anyway, taxes or research and development. They also don’t include any depreciable assets such as furniture, vehicles, machinery and cost of depreciable real estate. These are treated separately as depreciable assets and can be written off over a number of years or can be written off using bonus depreciation or the expense election.

Also, funds that you spend to qualify to get into the business or profession does not qualify as start up costs. Thus, costs incurred to get a real estate license, which has an unlimited duration as long as you pay fees and get continuing education, aren’t qualified start up costs. The same can be said for CPA exam preparation and licenses, bar review courses and licenses and getting an undergraduate bachelors degree. However, other than getting yourself qualified for the new profession or trade or business, any monies spent on investigating these business would be a qualified startup expenses.What are organizational expenses? Now that you know what startup costs are, we should differentiate them from organizational costs. Qualified organizational costs related to the creation of a corporation normally would be capitalized costs. These expenses include:

• Legal expenses incurred for the organization of the corporation, such as drafting the corporate charter, by-laws, minutes of organizational meetings, terms of original stock certificates.

• Necessary accounting services

• Expenses of temporary directors and of organizational meetings of directors or stockholders, and

• Fees paid the state of incorporation,

• Other legal costs incurred in connection with state corporate charter renewals of limited duration.

So, what aren’t organizational expenses? The following expenses would be capitalizable (nondeductible) and not qualified organizational expenses:

• Commissions and other expenses incurred with the issuance or sale of stock or other securities,

• Expenses incurred with the transfer of assets to a corporation,

Tax Treatment of Startup and Organizational Expenses:

The key here is that start up expenses and organizational expenses are not deductible unless you elect to deduct them in according with IRS rules noted below. What is interesting, is that tax law presumes you have made the appropriate election, unless you choose to forgo it. In other words, if you do nothing, you are assumed to make the appropriate election by simply take the correct deduction and/or amortization on your tax return.

Sandy’s elaboration: I would recommend that you don’t rely on the deemed election but make a formal election on your tax return. To do this, you or your accountant would claim the start up expenses on IRS Form 4562. In addition, you

31 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

would add a statement to your tax return saying

that you want to deduct your start up expenses up to $5,000 and amortize the rest.

Example: Assuming you have $20,000 of start up expenses in 2011 before September when you started your business, your statement would say, “Taxpayer elects to deduct, under section 195 of the Internal Revenue Code, $5,000 of startup costs and amortize the remaining $15,000 of startup costs over 180 months beginning in September 2011. This is the month in which taxpayer’s business started.” The following costs comprised the $20,000 of startup costs:

• Investigatory and travel expenses incurred and

paid in January of $8,000

• Rent paid in January for 10 months of $6,000

• Advertising costs incurred in March of $3,000

• Wages paid employees from June to September 2011 of $3,000. Thus, your statement that you should attach to your tax return should show:

• The name of the business or some identification of the business that incurred the start up costs, and

• The dates that the costs were paid or incurred

32 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

• The amount of the each cost

• The month that the business began operations

• The total amount that was deducted this year, and finally

• The number of months that you have amortized expenses over $5,000. It must be a minimum of 180 months or more.

What you can deduct?

Starting in 2010 and thereafter, or both startup expenses and organization expenses, you can deduct up to $5,000 of startup expenses in the year in which the business begins. Any startup costs that exceed this $5,000 amount must be amortized over a period of at least 180 months as long as the total startup costs are less than $50,000. However, Congress can’t do anything with any degree of simplicity. If the startup costs exceed $50,000, for every dollar that these costs exceed $60,000, you lose part of your $5,000 immediate write off.

Thus, if you incur $55,000 of start up costs, you can deduct only $5,000 of these costs. The remainder must be amortized over at least the next 180 months. If your startup costs are $60,000 or more, all of it must be amortized over 180 months or more.

These expenses can be taken in the tax year in which your trade or business begins. This means that when you are ready to start taking customers or clients, you can start taking the deduction for startup/organization expensesExample: You incur $4000 of start up expenses in April of 2011. However, your business doesn’t formally begin until February 2012. You can elect to deduct the $4000 in 2012.

Sandy’s Observation Regarding Startup Expenses and Organizational Expenses:

• In 2011 and thereafter, unless Congress changes the law, you can claim both the $5,000 of startup or organization expenses and amortize any additional startup or organizational expenses incurred over the $5,000 deduction.

•These rules benefit smaller businesses. Larger businesses with larger start up expenses over $55,000 have to deduct their startup or organizational expenses over 180 months.

What happens if you sell your business or don’t start the business in which the startup expenditures were incurred?

If you have an unsuccessful startup or close your business, the tax effects of startup expenses vary depending on whether they were incurred by you or by a corporation and whether you started amortizing startup costs.

If the startup costs were partially amortized, the deferred part of the costs (unamortized portion) can be immediately deducted if you either close the business or sell the business.

Moreover, if a corporation pays or incurs expenses in searching for, investigating a new venture, it may deduct the unsuccessful search as a business loss as long as the corporation abandons the search of investigation.

However, with respect to individuals, these expenditures are treated more harshly as nondeductible expenses. There is one exception for individuals where they can deduct investigatory and other startup costs. This exception is where you went beyond a

33 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

general, investigatory search for a new business with a focus on acquiring a specific business or investment. Here you are deemed to enter a for profit transaction, and any unsuccessful startup investigatory expenses would be deductible. Thus, there would be no need to actually enter the business or buy the for-profit investment to get the loss deduction.

Here are some illustrations of where the courts held that there was a specific enough focus:

• A broker investigated a particular business and spent $5,000 for air and taxi fares, hotels, legal and accounting expenses, etc. He orally agreed to acquire the business and had some preliminary contracts drafted up. He familiarized himself with the operation of the business. However, a last minute problem arose and the deal as dropped.

• Taxpayer agreed with others to buy a franchise in order to own and operate a motel. The agreement called for the parties to contribute cash in a corporation for stock. Taxpayer advanced money for feasibility reports, architect fees, and travel expenses. For reasons beyond his control, the proposed site couldn’t be acquired consequently the deal fell through.

Bottom line for Noncorporate Taxpayers: The key is to target a specific business and take preliminary steps to enter into the transaction of buying or starting up that business. Documents that help prove this specific focus would be any agreements, advice from professionals about the specific business, and review and/or preparation of any financial statements.

In conclusion, most businesses have some sort of startup expenses. Knowing the rules can greatly enhance your deductions and thereby put a lot of potential cash in your pocket and

make your life less taxing.

About the Author

Sandy Botkin CPA, Esq. is the principal lecturer for the Tax Reduction Institute of Germantown, Maryland.

Sandy is a best selling author of “Lower Your Taxes:Big Time” and “Real Estate Tax Secrets of the Rich.” He lectures throughout the U.S. on tax reduction techniques for small business professionals. You can access his web site for more information, including lots of free financial tools, by going to www.sandybotkin.com. You can also access his free blog at www.facebook.com/loweryourtaxes and his free videos at http://www.2012taxdeductions.com/

References1.IRC Section 195 ©(1)(A)2.Section 1.195-1T(b) of the Income tax regulations.3.IRS section 195©(1)4.Section 248(b) of the IRC5.Section 1.248-1(b)(3) of the income tax regulations.6.Section 195(b)(1)(A)ii of the IRC7.Section 195(b)(2) of the IRC8.Rev. Rul. 56-520, 1956-2 CB 170; Roy Harding, TC Memo 1970-179 (1970)9.Rev. Rul 55-237, 1955-1 CB 31710.Rev. Rul. 77-254, 1977-2 CB 63 and Rev. Rul. 57-418, 1957-2 CB 143. See also Harris Seed, 52 TC 880 (1969) acq. 1970-2 CB xxi. 11.Johan Domenie, TC Memo 1975-9412.Merrill Finch, vs. U.S., 18 AFTR 2d 5259 ( 1966)

34 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

Self Funding Magazine

n estimated 133 million Americans are currently living with one or more chronic conditions – a figure that is only expected to grow as the baby boomer generation ages. Many experience frustration with monitoring and managing their own or their loved ones’ complex medical needs.

In addition, hospitals are especially challenged to find ways to improve management of all critical illnesses in the face of proposals to slash Medicare payments to facilities that readmit patients within a specific time period. According to the American Hospital Association, these new regulations would raise costs to hospitals an estimated $19 billion over 10 years.

The good news is that today health management providers are offering solutions that make it possible for these individuals to manage their health from anywhere, at any time, while also providing important informational updates to their caregivers or doctors. Remote health monitoring has the potential to not only drastically reduce health care costs, but also to improve patients’ quality of life by allowing them to continue living independently at home rather than being hospitalized or moved into an assisted living facility.

High blood pressure alone affects 73 million Americans. As of 2008, the estimated direct and indirect cost of high blood pressure was $69.4 billion, according to the American Heart Association. In an attempt to combat these high costs, the use of home blood pressure monitoring is recommended by several national and international guidelines for the management of hypertension, including The American Heart Association and The American Society of Hypertension. In one study’s analysis of 904 patients using real-time readings from a remote hypertension

ABy Jason Goldberg

36 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazinemanagement program for a period of six months, the average reduction of systolic blood pressure was 9 mmHg. These decreases in blood pressure are significant because controlled blood pressure has been associated with a 35-40 percent mean reduction in stroke incidence, 20-25 percent mean reduction in myocardial infarctions and more than 50 percent reduction in heart failure. A 12mmHg drop in average systolic blood pressure will save one life in every 11 treated patients over ten years. This means that in the 904 patient population, almost 40 lives would be saved.

Regarding congestive heart failure (CHF), there are approximately 5.3 million people suffering from CHF in the United States. The lifetime risk of developing heart failure at the age of 40 is 20 percent, and approximately 380,000 people above the age of 65 will be diagnosed with CHF annually. The estimated total of direct and indirect cost of heart failure in the United States for 2008 is $34.8 billion, with the greatest share being hospitalizations. The increasing number of patients being hospitalized with CHF has been great cause for concern. The number of patients with CHF discharged from the hospital rose from 400,000 in 1979 to over 1 million in 2005. Furthermore, within 4-6 months after discharge, 47 percent of the patients are likely to be readmitted. A recent study of 417 CHF patients using a remote health monitoring system proved that this was an effective method to reduce congestive heart failure hospital admissions by 57 percent, demonstrating that these systems can significantly reduce healthcare costs.

Our company has created a revolutionary remote health management platform that addresses many of today’s most challenging and costly healthcare issues. For people managing critical conditions such as congestive heart failure, hypertension, diabetes, asthma or obesity, our system provides relevant, real-time, reliable and actionable data. This can deliver interactive, personalized communication, allowing individuals to become more engaged and active participants in their own health. This

approach also makes proactive prevention more realistic than ever, as it is instrumental in gauging health issues before critical conditions manifest themselves into acute events. For example, daily blood pressure readings are more indicative of someone developing hypertension than having one reading taken every six months at the doctor’s office. Remote health monitoring devices and programs

37 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

are designed to empower patients to take an active role in the management of their personal health. Patients with a critical illness need to be able to easily follow their care plans and make necessary lifestyle or medication modifications. This can minimize the chance that they will develop additional complications that could further jeopardize their health, thus requiring expensive treatment. Consistent and regular monitoring of blood glucose levels or body weight, for example, can help reinforce adherence to good health practices as well. As a bonus, because some remote health monitoring devices, like ours, are wireless, they can also make it possible to manage health while traveling or on the go.

Many remote health management systems not only offer solutions for patients, but for their caregivers as well. Often times caregivers look to technology for assistance in tracking a person’s status or progress, and now computers, smart phones and even tablets can enable health care providers to monitor patients in their homes and let adult children and other

family members keep an eye on aging parents. When a patient steps on the scale in the morning or checks their blood glucose level before a meal, for example, a designated caretaking team can be notified, even if they are hundreds or thousands of miles away.

The compact, affordable and easy-to-use devices monitor data and can automatically and wirelessly transmit this information to the individual’s healthcare team without the need for cumbersome wires or manual data entry.

One person who has experienced first-hand the benefits of remote health monitoring is 70-year-old Ira Roberts, who is living with diabetes. A church minister for 35 years, he also teaches at William Patterson University and travels over 300 miles a week as a gospel musician. With such a busy schedule, Ira can’t afford to let his diabetes slow him down. At home or on the road, he stays on a healthy track by providing his doctors with 24/7 access to all his latest health information.

38 w w w. S e l f Fu n d i n g Ma g a z i n e . c o m

Self Funding Magazine

Ira does this by using a remote glucose meter, which makes it easy to capture and transmit important blood sugar data, no matter where he happens to be. For Ira, being able to send his glucose readings wirelessly and automatically via our system is what has allowed him to remain active and fully independent.

The device “helps me manage my health by getting all my doctors on the same page,” said Ira. “The system acts as a watchdog of my diabetes.”