2010 earnings results - newspress-kia.s3.amazonaws.com · 13 2011 business plan * based on shipment...

TRANSCRIPT

1

2010 Earnings Results

January 28, 2011

2

Notes for InvestorsThis presentation has been prepared with unaudited 4th quarter results of year 2010 for investors’ convenience.

Therefore, some numbers may change upon the review of Kia’s independent auditors.

33

Contents

Sales Overview

Income Statement

Balance Sheet

Cashflow Statement

Revenue Analysis

COGS and SG&A

Non-Operating Income/Expense

2011 Business Plan

New Model Launch Schedule

2011 Management Policy

I. 2010 Earnings ResultsI. 2010 Earnings Results II. 2011 Business PlanII. 2011 Business Plan

I. 2010 Earnings ResultsI. 2010 Earnings Results

Sales Overview

Income Statement

Balance Sheet

Cashflow Statement

Revenue Analysis

COGS and SG&A

Non-Operating

Income/Expense

5

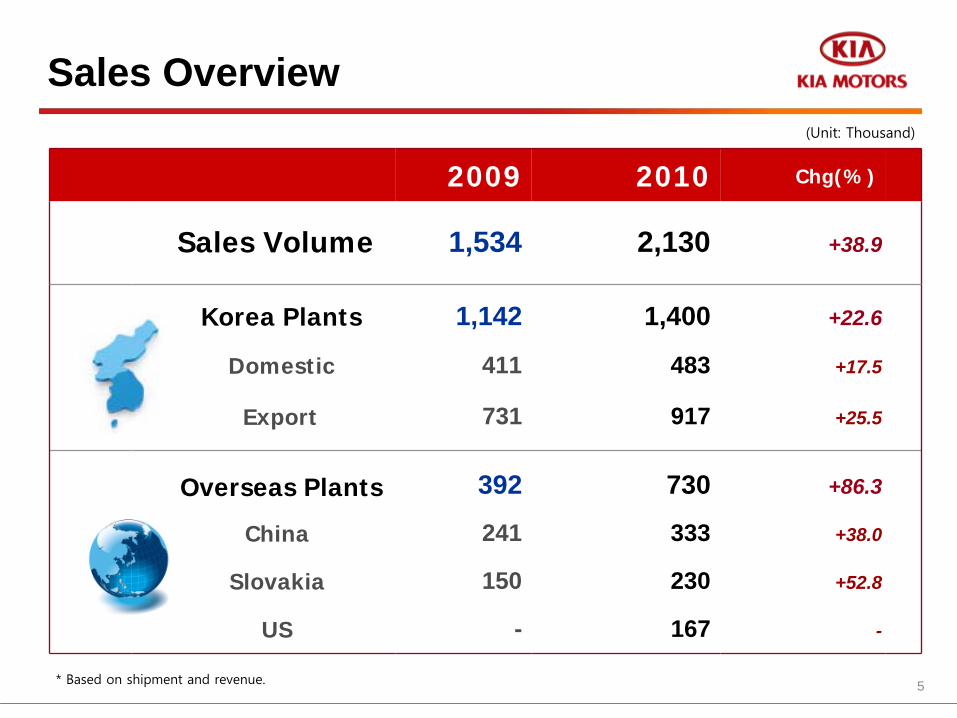

Sales Overview

2009 2010 Chg(%)

Sales Volume 1,534 2,130 +38.9

Korea Plants 1,142 1,400 +22.6

Domestic 411 483 +17.5

Export 731 917 +25.5

Overseas Plants 392 730 +86.3

China 241 333 +38.0

Slovakia 150 230 +52.8

US - 167 -

* Based on shipment and revenue.

(Unit: Thousand)

6

Income Statement

2009 (%) 2010 (%) Chg(%)

Sales Volume 1,142 100 1,400 100 +22.6

Domestic 411 36 483 35 +17.5

Export 731 64 917 65 +25.5

Revenue 18,416 100 23,261 100 +26.3Domestic 6,953 38 9,182 39 +32.1

Export 11,463 62 14,079 61 +22.8

Gross Profit 4,591 24.9 5,330 22.9 +16.1

Operating Profit 1,144 6.2 1,680 7.2 +46.8

Recurring Profit 1,700 9.2 2,776 11.9 +63.3

Net Profit 1,450 7.9 2,254 9.7 +55.4

EBITDA 1,828 9.9 2,310 9.9 +26.4

(Unit: Billion Won, Thousand)

*EBITDA = Operating Profit + Depreciation + Amortization

7

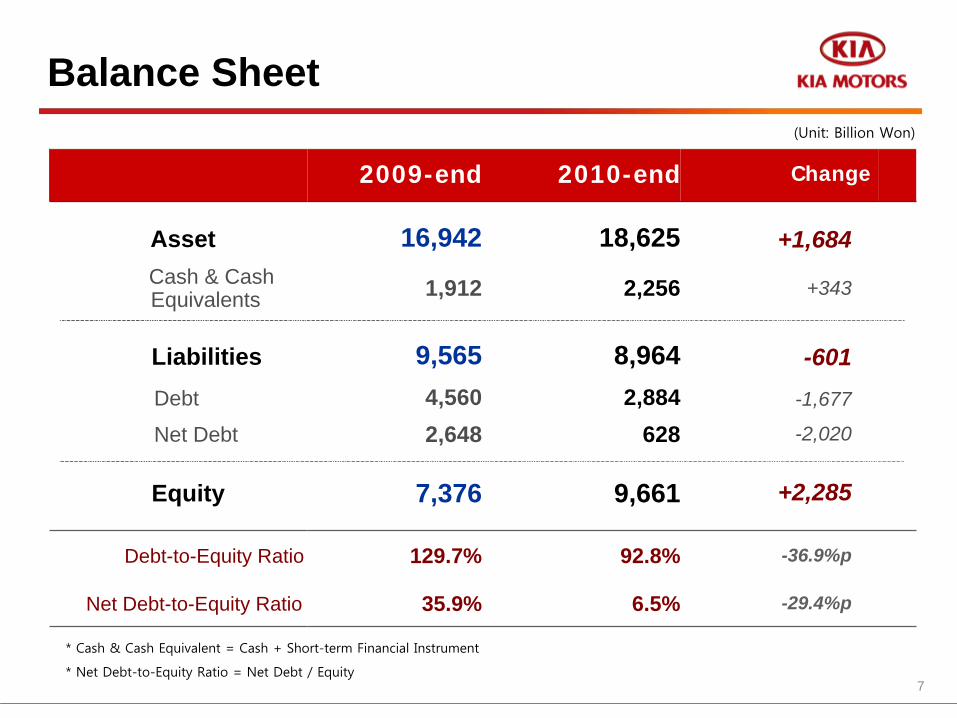

Balance Sheet

2009-end 2010-end Change

Asset 16,942 18,625 +1,684Cash & Cash Equivalents 1,912 2,256 +343

Liabilities 9,565 8,964 -601Debt 4,560 2,884 -1,677

Net Debt 2,648 628 -2,020

Equity 7,376 9,661 +2,285

Debt-to-Equity Ratio 129.7% 92.8% -36.9%p

Net Debt-to-Equity Ratio 35.9% 6.5% -29.4%p

(Unit: Billion Won)

* Cash & Cash Equivalent = Cash + Short-term Financial Instrument

* Net Debt-to-Equity Ratio = Net Debt / Equity

8

Cashflow Statement

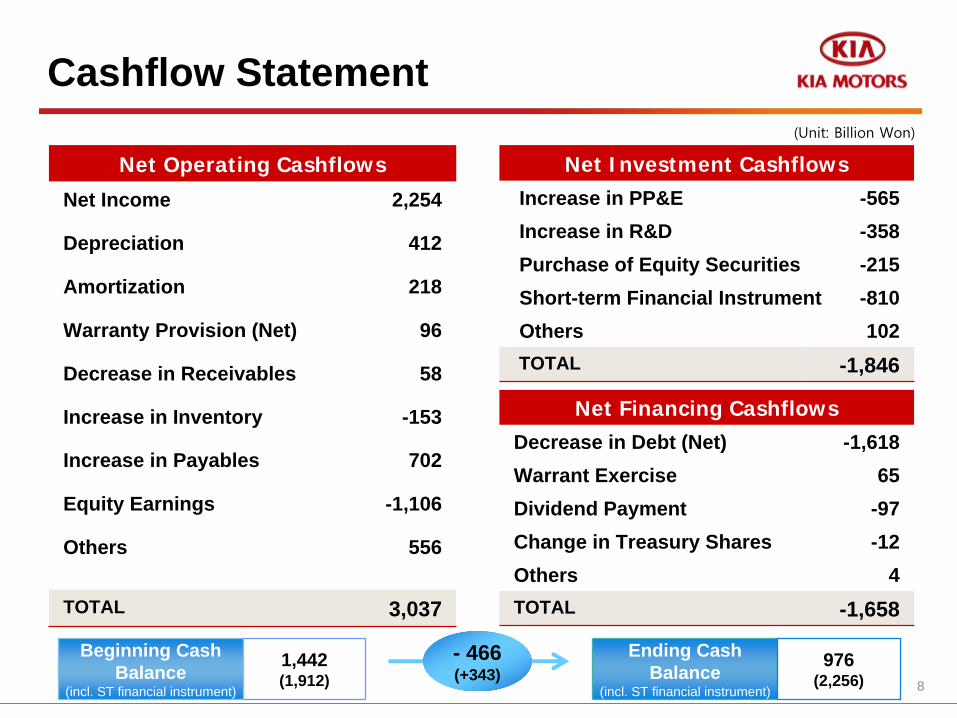

Net Operating Cashflows

Net Income 2,254

Depreciation 412

Amortization 218

Warranty Provision (Net) 96

Decrease in Receivables 58

Increase in Inventory -153

Increase in Payables 702

Equity Earnings -1,106

Others 556

TOTAL 3,037

Net Investment CashflowsIncrease in PP&E -565Increase in R&D -358Purchase of Equity Securities -215Short-term Financial Instrument -810Others 102TOTAL -1,846

Net Financing CashflowsDecrease in Debt (Net) -1,618Warrant Exercise 65Dividend Payment -97Change in Treasury Shares -12Others 4TOTAL -1,658

Beginning Cash Balance

(incl. ST financial instrument)

1,442(1,912)

- 466(+343)

Ending Cash Balance

(incl. ST financial instrument)

976 (2,256)

(Unit: Billion Won)

9

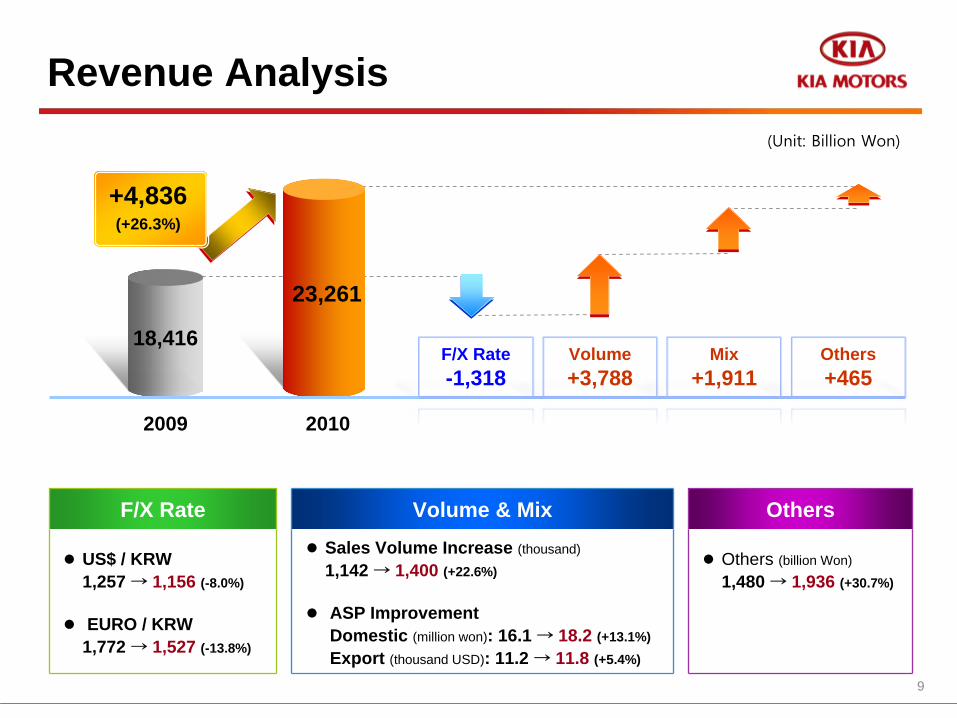

Revenue Analysis

F/X Rate-1,318

Volume+3,788

Mix+1,911

Others+465

F/X Rate

US$ / KRW 1,257 → 1,156 (-8.0%)

EURO / KRW 1,772 → 1,527 (-13.8%)

Volume & Mix

Sales Volume Increase (thousand)

1,142 → 1,400 (+22.6%)

ASP Improvement Domestic (million won): 16.1 → 18.2 (+13.1%) Export (thousand USD): 11.2 → 11.8 (+5.4%)

Others

Others (billion Won)

1,480 → 1,936 (+30.7%)

18,416

23,261

2009 2010

+4,836(+26.3%)

(Unit: Billion Won)

10

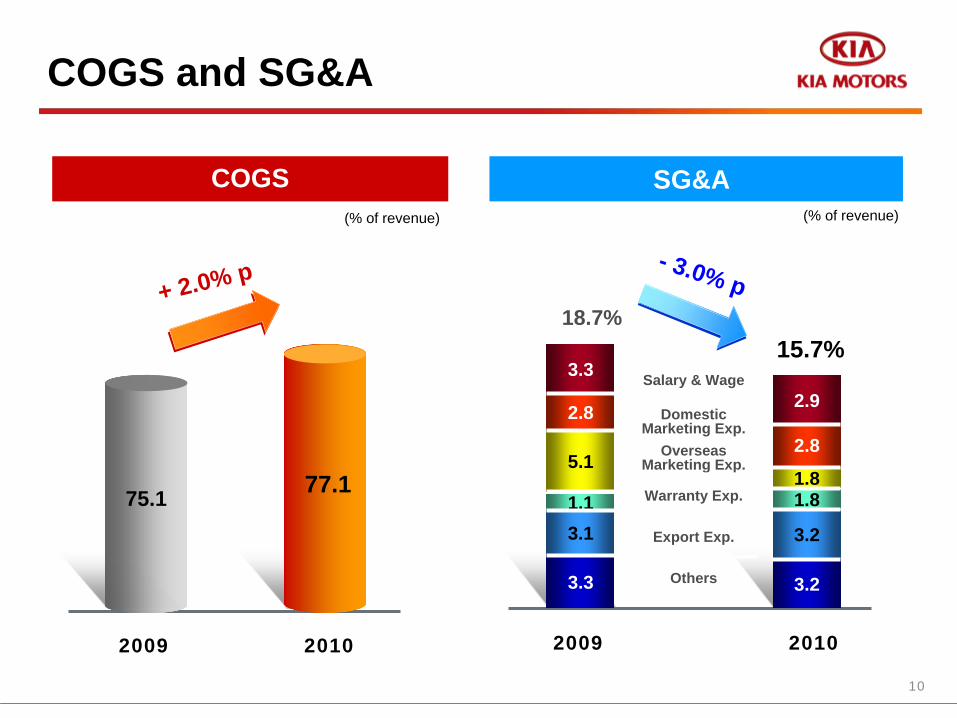

2009 2010

18.7%

(% of revenue)

COGS(% of revenue)

15.7%

2009 2010

3.3

2.8

5.1

1.13.1

3.3

Salary & Wage

Domestic Marketing Exp.

Overseas Marketing Exp.

Warranty Exp.

Export Exp.

Others

2.9

2.8

1.81.8

3.2

3.2

COGS and SG&A

SG&A

+ 2.0% p - 3.0% p

77.175.1

11

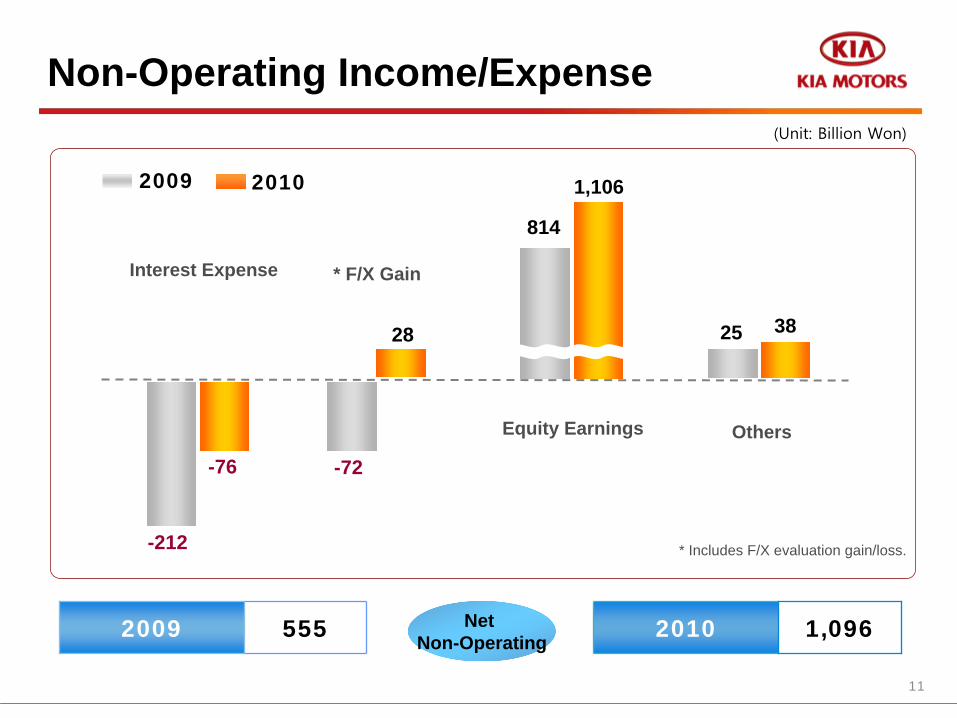

2009 2010

Non-Operating Income/Expense

OthersEquity Earnings

1,106

814

25 3828

-72

Interest Expense * F/X Gain

-76

-212 * Includes F/X evaluation gain/loss.

Net Non-Operating2009 555 2010 1,096

(Unit: Billion Won)

12

II. 2011 Business PlanII. 2011 Business Plan

2011 Business Plan

New Model Launch Schedule

2011 Management Policy

13

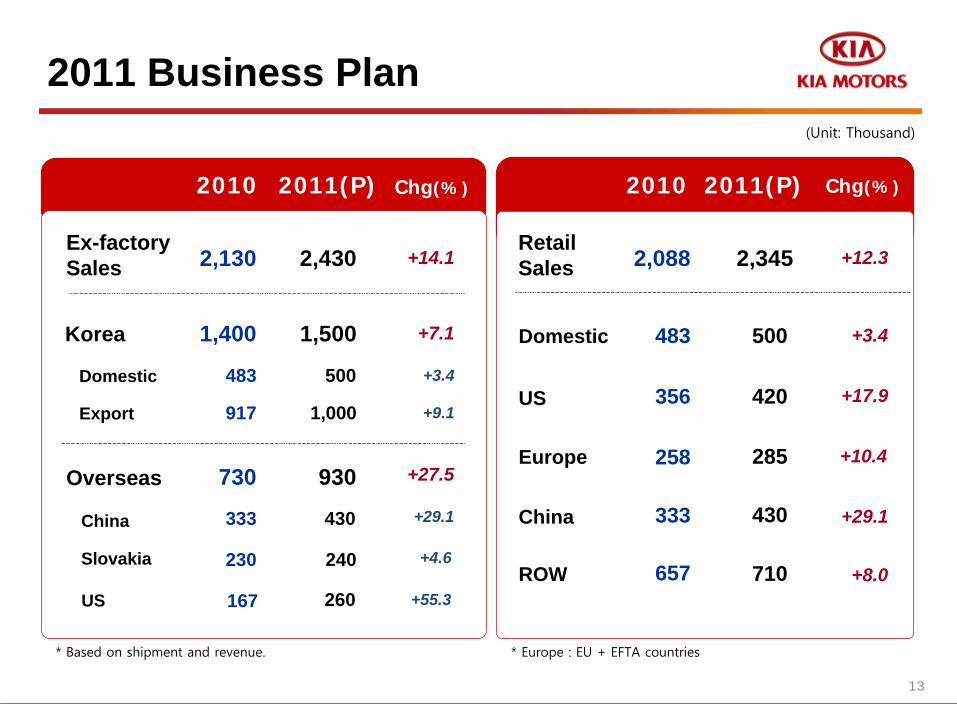

2011 Business Plan

* Based on shipment and revenue. * Europe : EU + EFTA countries

2,130 +14.1Ex-factory Sales

1,400 +7.1

483 +3.4Domestic

917 +9.1Export

2,430

1,500

500

1,000

2010 2011(P) Chg(%)

Korea

730 +27.5

333 +29.1China

230 +4.6Slovakia

930

430

240

Overseas

167 +55.3US 260

2,088 +12.3Retail Sales

+3.4

2,345

+17.9

+10.4

+29.1

+8.0

500

420

285

430

710

483

356

258

333

657

Domestic

US

Europe

China

ROW

2010 2011(P)

(Unit: Thousand)

Chg(%)

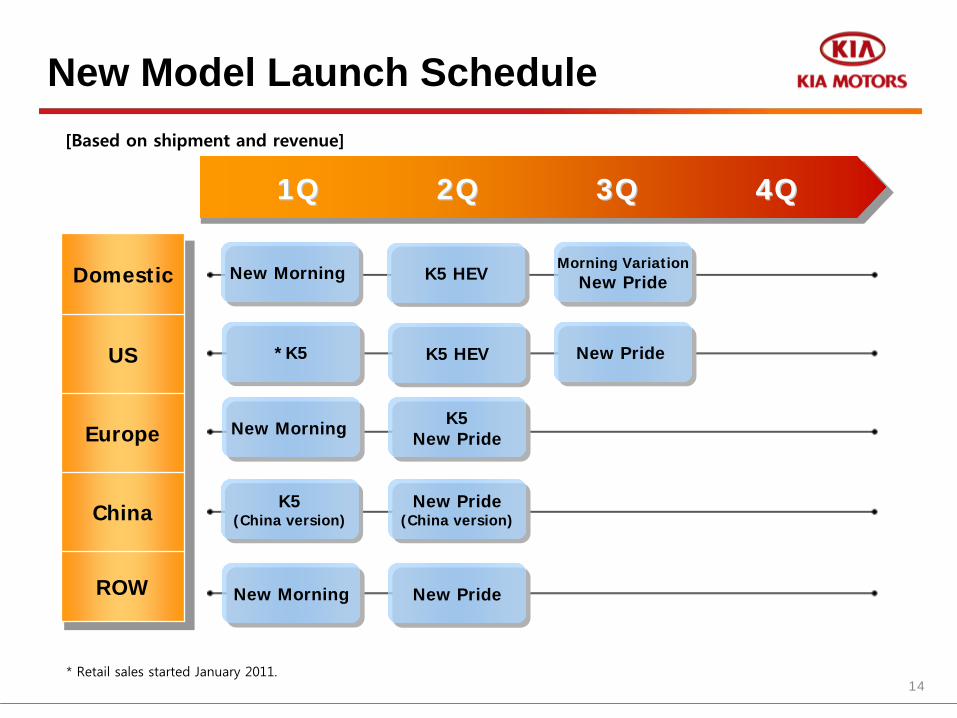

14* Retail sales started January 2011.

New Morning New Morning

1Q1Q 2Q2Q 3Q3Q 4Q4Q

Domestic

US

Europe

China

ROW

K5(China version)

K5(China version)

New Pride(China version)New Pride

(China version)

Morning VariationNew Pride

Morning VariationNew Pride

New Pride New Pride

New Morning New Morning K5New Pride

K5New Pride

New PrideNew Pride

*K5*K5

New Model Launch Schedule

New MorningNew Morning

K5 HEVK5 HEV

K5 HEVK5 HEV

[Based on shipment and revenue]

15

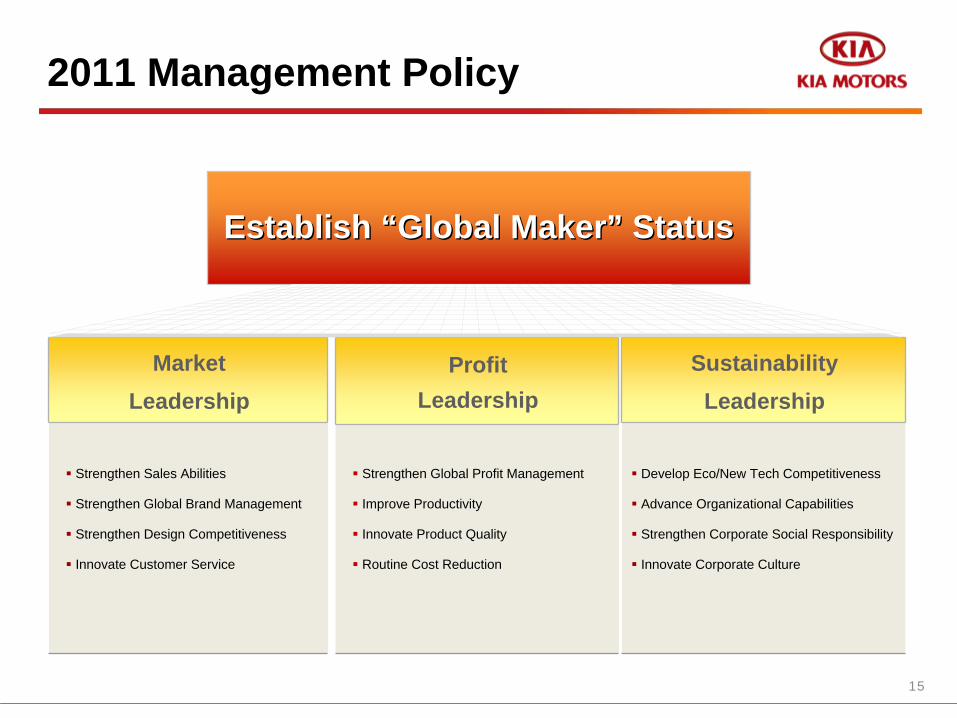

2011 Management Policy

Profit Leadership

Market Leadership

Establish Establish ““Global MakerGlobal Maker”” StatusStatus

SustainabilityLeadership

Strengthen Sales Abilities

Strengthen Global Brand Management

Strengthen Design Competitiveness

Innovate Customer Service

Strengthen Global Profit Management

Improve Productivity

Innovate Product Quality

Routine Cost Reduction

Develop Eco/New Tech Competitiveness

Advance Organizational Capabilities

Strengthen Corporate Social Responsibility

Innovate Corporate Culture

http://www.kmcir.comhttp://www.kmcir.com

Thank you.

17

III. AppendixIII. Appendix

Quarterly Income Statement

2010 Sales Overview

2011 Strategy by Market

- Korea

- US

- Europe

- China

- ROW

18

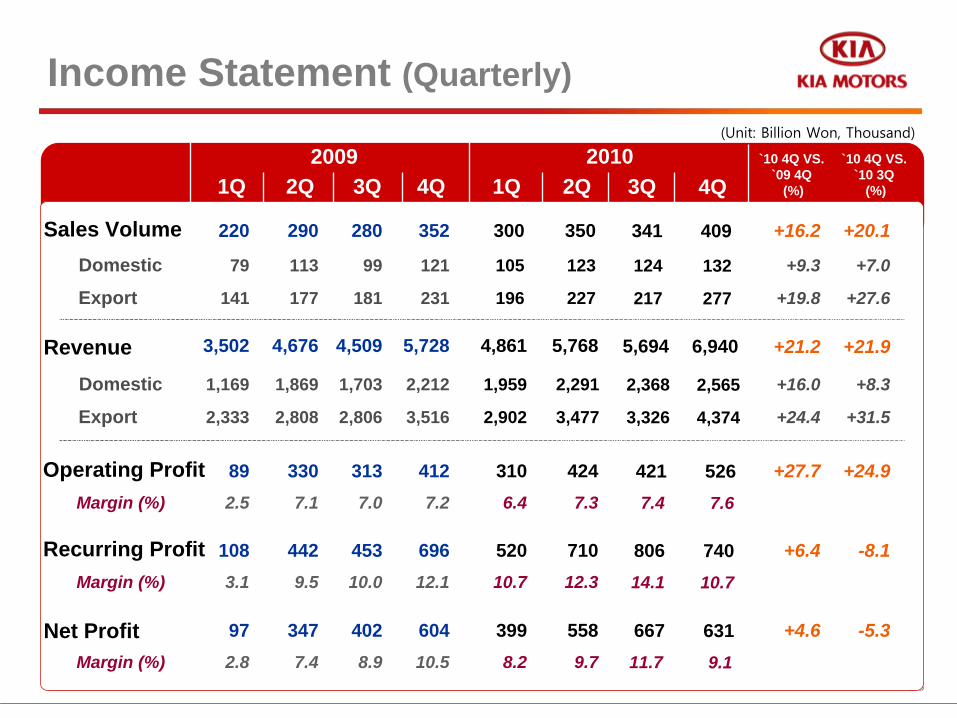

Sales VolumeDomestic

Export

220

79

141

290

113

177

280

99

181

352

121

231

1Q 2Q 3Q 4Q2009 2010

1Q 2Q`10 4Q VS.

`09 4Q (%)

`10 4Q VS. `10 3Q

(%)

300

105

196

350

123

227

+16.2

+9.3

+19.8

+20.1

+7.0

+27.6

RevenueDomestic

Export

3,502

1,169

2,333

4,676

1,869

2,808

4,509

1,703

2,806

5,728

2,212

3,516

4,861

1,959

2,902

5,768

2,291

3,477

+21.2

+16.0

+24.4

+21.9

+8.3

+31.5

Operating ProfitMargin (%)

892.5

3307.1

3137.0

4127.2

3106.4

4247.3

+27.7 +24.9

Recurring ProfitMargin (%)

1083.1

4429.5

45310.0

69612.1

52010.7

71012.3

+6.4 -8.1

Margin (%)

972.8

3477.4

4028.9

60410.5

3998.2

5589.7

+4.6 -5.3

3Q

341

124

217

2,368

3,326

4217.4

80614.1

66711.7

5,694

Net Profit

409

132

277

2,565

4,374

5267.6

74010.7

6319.1

6,940

4Q

Income Statement (Quarterly)(Unit: Billion Won, Thousand)

19

Sales Overview by Region

1,534 +38.9

1,142 +22.6

411 +17.5

731 +25.5

2,130

1,400

483

917

392 +86.3

241 +38.0

150 +52.8

730333

230

- -167

1,651 +26.5

+17.5

2,088

+18.7

+6.6

+38.0

+44.3

483

356

258

333

657

411

300

242

241

455

2009 2010 chg(%) 2009 2010 chg(%)

(Unit: Thousand)

Ex-factorySales

Domestic

Export

Korea

China

Slovakia

Overseas

US

Retail Sales

Domestic

US

Europe

China

ROW

* Based on shipment and revenue. * Europe : EU + EFTA countries

20

Market & Strategy

411

Sales & Market Share

29.5%

11%

26%

63%

33.0%

PC

RV

CV

11%

25%

64%

11%

25%

64%

483500

Korea Market

+3.4%

Market Outlook- Limited growth of +1.2% in ‘11E vs. +7% in ‘10.

- Better consumer sentiment with new model launches.

- Influence of Korea-EU FTA in 2H on imported car market.

2009 2010 2011(P)

(Thousand units)

Strategy - Reinforce New Model Sales Momentum

New Morning (Jan), K5 HEV (Jun),

Morning Variation (Aug), New Pride (Sept)

- Increase Market Presence with Full Line-up Equipment

- Build-up Sales Growth in Volume Models (K / R Series)

- Improve Brand Image via PR Activities

Promote “Design Kia,” Social Responsibility Marketing

21

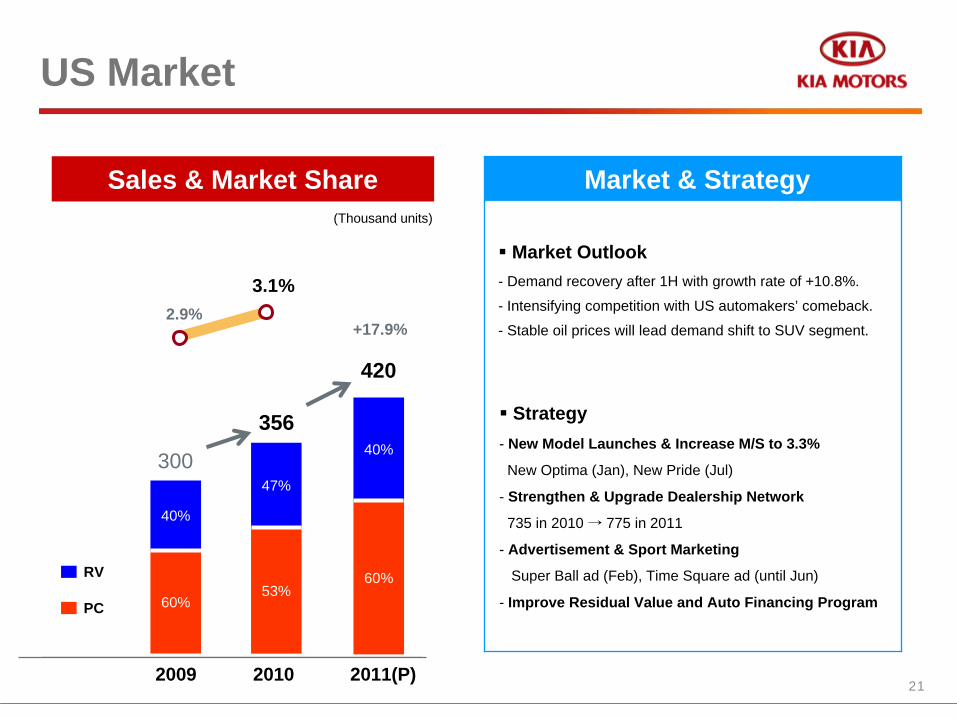

300

Sales & Market Share

2.9%

40%

60%

3.1%

PC

RV

47%

53%

40%

60%

356

420

US Market

+17.9%

Market & Strategy

‘09 ‘10 ‘11[P2009 2010 2011(P)

Market Outlook - Demand recovery after 1H with growth rate of +10.8%.

- Intensifying competition with US automakers’ comeback.

- Stable oil prices will lead demand shift to SUV segment.

Strategy- New Model Launches & Increase M/S to 3.3%

New Optima (Jan), New Pride (Jul)

- Strengthen & Upgrade Dealership Network

735 in 2010 → 775 in 2011

- Advertisement & Sport Marketing

Super Ball ad (Feb), Time Square ad (until Jun)

- Improve Residual Value and Auto Financing Program

(Thousand units)

22

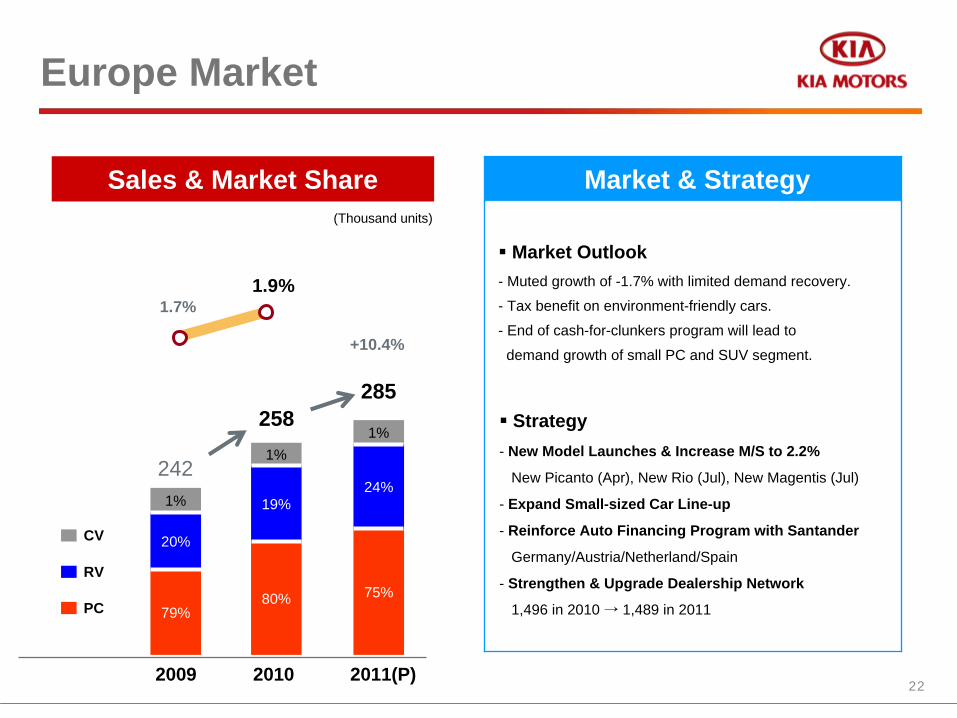

242

Sales & Market Share

1.7%

1%

20%

79%

1.9%

PC

RV

CV

1%

19%

80%

1%

24%

75%

258285

Europe Market

+10.4%

Market & Strategy

2009 2010 2011(P)

(Thousand units)

Market Outlook - Muted growth of -1.7% with limited demand recovery.

- Tax benefit on environment-friendly cars.

- End of cash-for-clunkers program will lead to

demand growth of small PC and SUV segment.

Strategy- New Model Launches & Increase M/S to 2.2%

New Picanto (Apr), New Rio (Jul), New Magentis (Jul)

- Expand Small-sized Car Line-up

- Reinforce Auto Financing Program with Santander

Germany/Austria/Netherland/Spain

- Strengthen & Upgrade Dealership Network

1,496 in 2010 → 1,489 in 2011

23

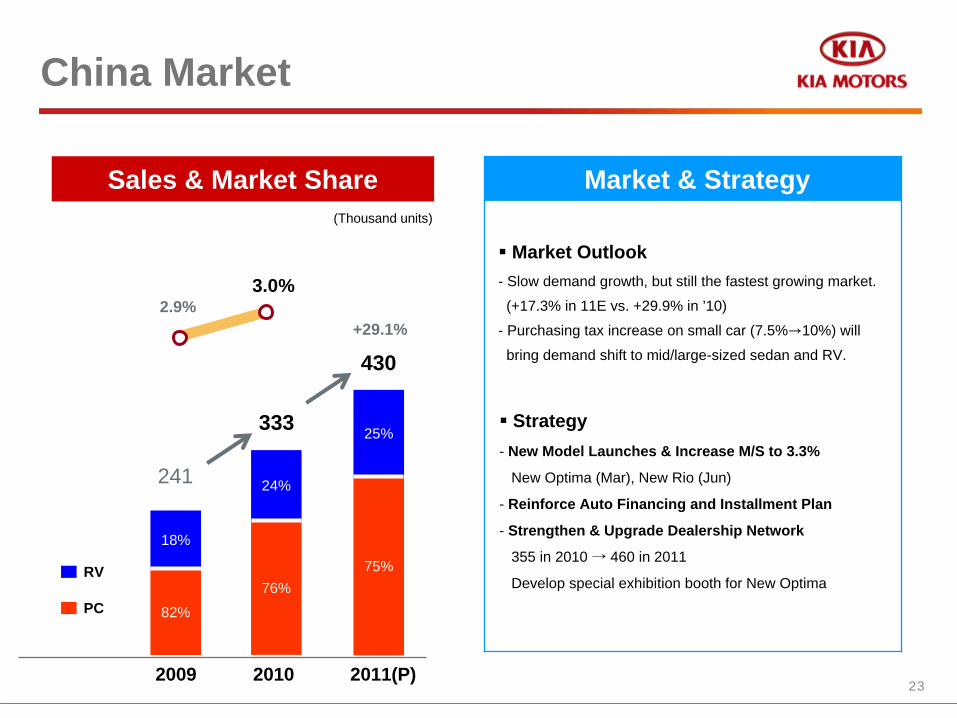

241

Sales & Market Share

2.9%

18%

82%

3.0%

PC

RV

24%

76%

25%

75%

333

430

China Market

+29.1%

Market & Strategy

2009 2010 2011(P)

(Thousand units)

Market Outlook - Slow demand growth, but still the fastest growing market.

(+17.3% in 11E vs. +29.9% in ’10)

- Purchasing tax increase on small car (7.5%→10%) will

bring demand shift to mid/large-sized sedan and RV.

Strategy- New Model Launches & Increase M/S to 3.3%

New Optima (Mar), New Rio (Jun)

- Reinforce Auto Financing and Installment Plan

- Strengthen & Upgrade Dealership Network

355 in 2010 → 460 in 2011

Develop special exhibition booth for New Optima

24

Sales & Market Share

Rest of World

Strategy

Sales by Region2010 2011[P] Growth

Rest of World 100% 100% +8.0%

Middle East/Africa 39% 38% +5.6%

East Europe 20% 21% +13.9%(Russia) (16%) (17%) (+16.9%)

South America 21% 20% +5.5%

Asia & Pacific 12% 12% +6.8%

Canada 8% 9% +13.2%455

7%

31%

62%PC

RV

CV

8%

28%

64%

7%

30%

63%

657710

+8.0%

‘09 ‘10 ‘11[]2009 2010 2011(P)

(Thousand units)

- Ride on new model sales momentum : New Picanto, New Rio, New Optima (Dec ’10)

- Increase market leadership in focused countries : Middle East (Africa), East Europe (Russia), South America

- Strengthen and upgrade dealership network