2010 comprehensive economic development -

TRANSCRIPT

LEHIGH VALLEY COMPREHENSIVE ECONOMIC DEVELOPMENT

STRATEGY COMMITTEE

2010 & 2011 Appointees

Lehigh County Appointees

Nancy Dischinat, Executive Director, Lehigh Valley Workforce Development Board

Cindy Feinberg, Lehigh County Director of Community and Economic Development

Jerome Frank, Attorney, King, Spry, Herman, Freund & Faul, LLC

Sara Hailstone, City of Allentown, Director of Community and Economic Development

Donald Snyder, President, Lehigh Carbon Community College

Tamara Weller, Executive Director, Allentown Parking Authority

Northampton County Appointees

Peter Albanese, Green Knight Economic Development Corporation

J. Lee Boucher, President, Bardot Plastics, Inc.

Alicia Karner, Northampton County Economic Development Administrator

Esther Lee, President, Bethlehem NAACP

Dr. Arthur Scott, President, Northampton Community College

Marc Troutman, Area Manager, FirstEnergy

Also part of this process were the following 2010 appointees whose terms have expired:

Donald Bernhard Cynthia Lambert

Richard Daughterty John Mehler

William Erdman William D. Michalerya

David Fink Mayor Ed Pawlowski

Tony Hanna Thomas Stine

ACKNOWLEDGMENTS

The following people headed subcommittees, prepared subcommittee reports, and provided staff

assistance for this project.

CEDS Subcommittees

Cynthia Lambert, Past Chair

Marc Troutman, Chair

Don Bernhard & Bob Wendt, Targeted Industry Clusters

Nancy Dischinat, Workforce Development

Staff for this Report

Lehigh Valley Planning Commission

Michael Kaiser, Executive Director

David Berryman, Senior Planner

Lehigh Valley Economic Development Corporation

Pete Reinke, Vice President of Regional Development

Laurie Demko, Executive Assistant

Special Initiatives Section

Holly Edinger, Lehigh Valley Economic Development Corporation, Alternative Energy

Steve Melnick, Lehigh Valley Economic Development Corporation, Wall Street West

and South Bethlehem Keystone Innovation Zone

Jarrett Witt, Lehigh Valley Economic Development Corporation, Foreign Trade Zone

John Taylor, Lehigh University, Lehigh Valley Life Science Network

Comprehensive Economic Development Strategy Page i

TABLE OF CONTENTS

Section Page

INTRODUCTION .............................................................................................................................. 1

I. PRIORITY PROJECTS FOR THE LEHIGH VALLEY .................................................................... 2

City of Allentown ...................................................................................................................... 3

City of Bethlehem, Northampton and Lehigh Counties ............................................................ 5

City of Easton ... ........................................................................................................................ 9

County of Lehigh .................................................................................................................... 12

Northampton County ............................................................................................................... 16

II. REGIONAL BACKGROUND ......................................................................................................... 20

Economic History of the Lehigh Valley.................................................................................. 20

Geography ............................................................................................................................... 25

Environment ............................................................................................................................ 28

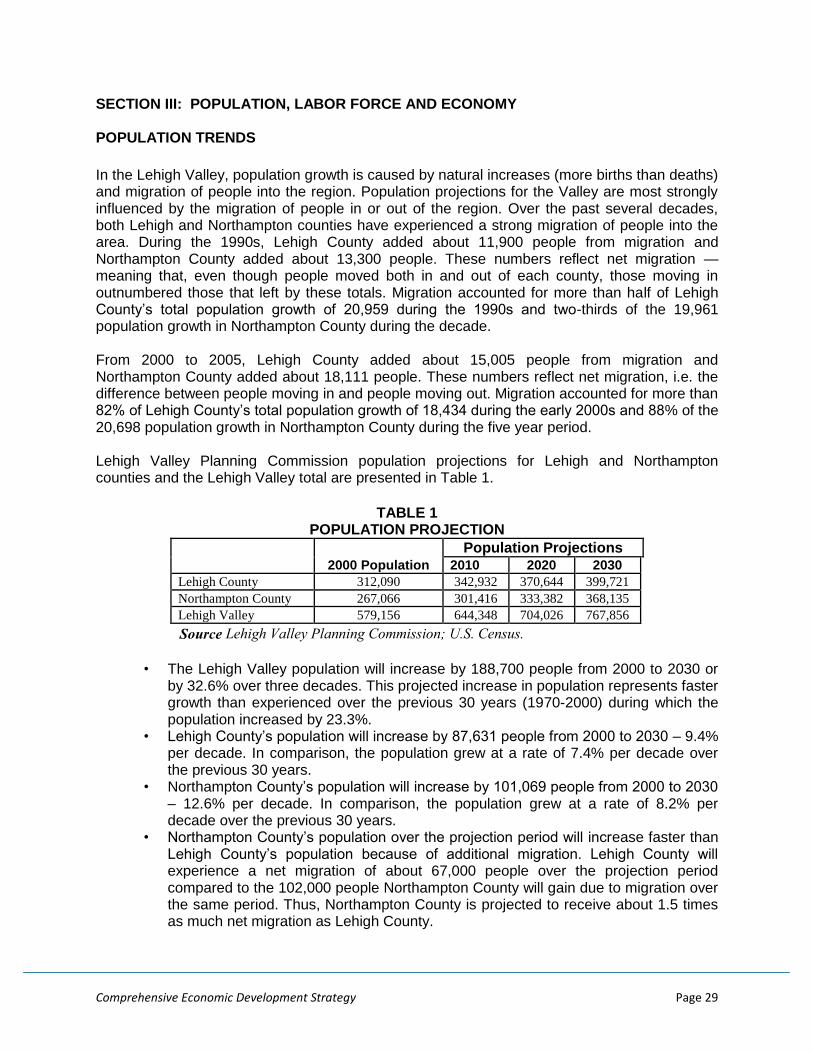

III. POPULATION, LABOR FORCE AND ECONOMY ..................................................................... 29

Population Trends ................................................................................................................... 29

Labor Force ............................................................................................................................. 30

Planning and Development Activities ..................................................................................... 37

IV. ASSESSMENT OF POTENTIALS AND ISSUES TO BE RESOLVED ........................................ 40

Potentials ................................................................................................................................. 40

Issues to be Resolved .............................................................................................................. 49

V. GOALS AND OBJECTIVES ........................................................................................................... 57

VI. PLAN FOR IMPLEMENTATION ................................................................................................... 62

LIST OF TABLES

Table Page

1 Population Projection ........................................................................................................................ 29

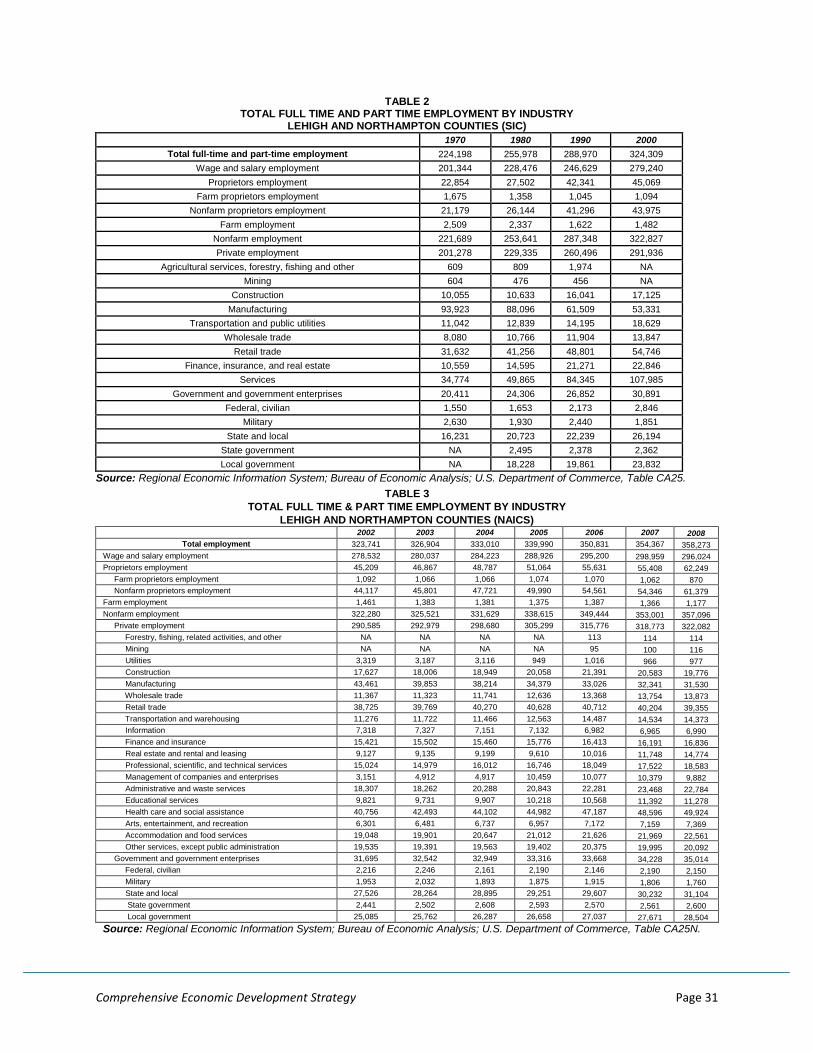

2 Total Full Time and Part Time Employment by Industry

Lehigh and Northampton Counties (SIC) ............................................................................... 31

3 Total Full Time & Part Time Employment by Industry

Lehigh and Northampton Counties (NAICS) .......................................................................... 31

4 Largest Employers ............................................................................................................................ 33

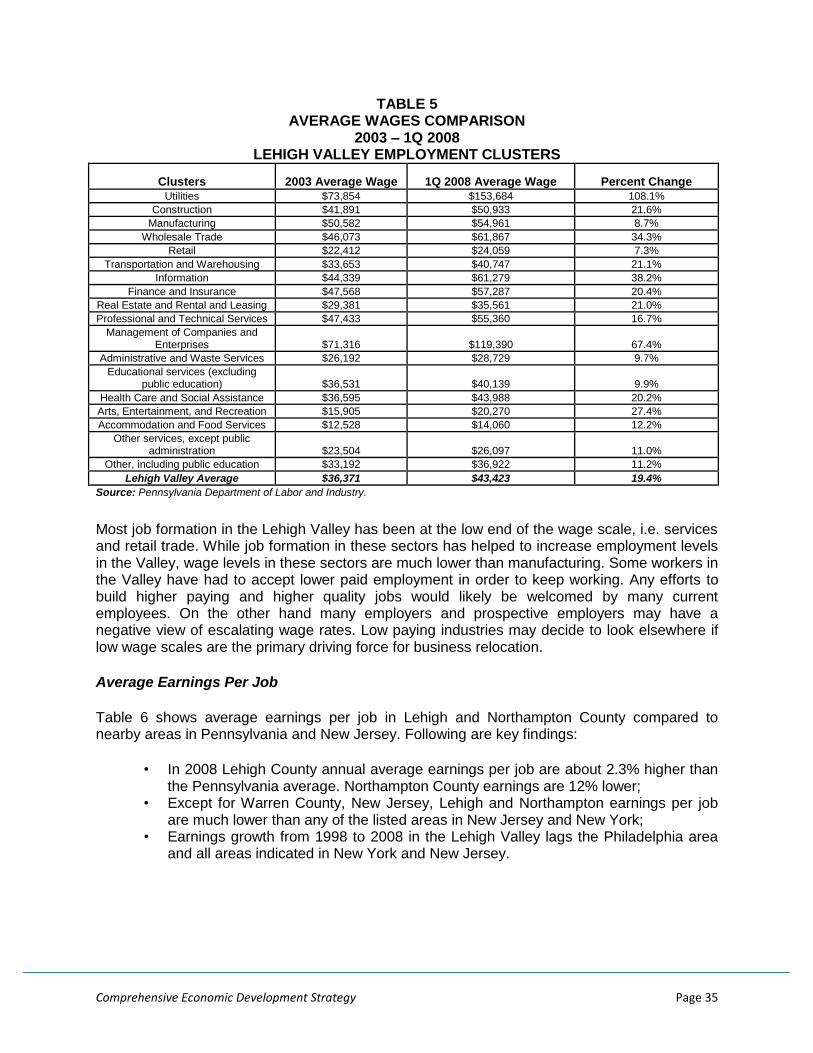

5 Average Wages Comparison 2003 - 1Q 2008 Lehigh Valley Employment Clusters ....................... 35

6 Annual Average Earnings per Job for Lehigh County, Northampton County,

Northampton County and Nearby Areas: 1997-2007 .............................................................. 36

7 Labor Force, Employment and Unemployment Statistics for the Lehigh Valley, July 2009 ........... 36

Comprehensive Economic Development Strategy Page ii

8 Economic Development Resources Lehigh and Northampton Counties .......................................... 38

9 Keystone Opportunity Zones in the Lehigh Valley .......................................................................... 42

10 Utilization of the Lehigh Valley International Airport: 2002-2008 .................................................. 47

TABLE OF MAPS

Map Page

1 Regional Setting ................................................................................................................................ 26

2 Surface Terrain .................................................................................................................................. 27

3 Keystone Opportunity Zones, Lehigh Valley, PA ............................................................................ 43

Appendix A: CEDS Committee Data

Appendix B: Committee Summary Reports

Appendix C: Committee Minutes — 2010

Appendix D: Cluster Analysis

Comprehensive Economic Development Strategy Page 1

INTRODUCTION

The Comprehensive Economic Development Strategy (CEDS) refers to the planning process and document generated from it which sets forth the Lehigh Valley’s economic development vision, goals, strategies, and priorities for the future. CEDS work in the Lehigh Valley is accomplished by the Lehigh Valley Economic Development Corporation (LVEDC) and other organizations who participate in various ways on project implementation. The 2010 CEDS represents the eighth major update, with a previous document (formerly referred to as the Overall Economic Development Program) completed in 1999. The CEDS is viewed as the economic development plan for the Valley, with desired outcomes and action steps aimed at:

• Creating better jobs and incomes. • Business and job retention. • Diversifying the economy and strengthening economic sectors. • Exposing new market potentials and business opportunities. • Protecting resources and environment. • Developing and improving infrastructure. • Enhancing the quality of life.

Considerable effort was made in this process to choose the strategies and priorities most likely to produce these outcomes and offering the best returns on investment of time, money, and staff resources. The CEDS and Planning Committee met six times in 2009 and once in 2010. Priorities reflect the input provided by the counties and municipalities in our region concerning their goals and concerns, and are also based on in-depth analysis of the regional economy.

Comprehensive Economic Development Strategy Page 2

SECTION I: PRIORITY PROJECTS FOR THE LEHIGH VALLEY

This section of the CEDS Report provides a list of projects as presented by both Lehigh and Northampton counties and the cities of Allentown, Bethlehem and Easton that are important to the Lehigh Valley, regardless of EDA eligibility. The list of EDA-eligible projects appears in Section VI. The projects listed here change from year to year and were the projects presented in 2010. The Lehigh Valley Economic Development Corporation (LVEDC) was founded to promote and foster economic prosperity in the Lehigh Valley, while creating a culture of collaboration and regionalism in order to retain, create and grow jobs in the region. Our efforts have made Lehigh Valley a national model for collaboration and have greatly aided economic development efforts. One example of this regional effort is the development of the priority project list for the Lehigh Valley's economic and community development projects. In 2003, LVEDC began working cooperatively with the economic development professionals in the cities of Allentown, Bethlehem and Easton, and Lehigh and Northampton Counties to develop a regional economic development priority project list. During the last seven years, LVEDC’s regional approach to economic development has helped the organization become identified as a leader in building a regional response to local and urban economic development needs. This united effort has identified more than 100 potential economic development projects as priorities for Redevelopment Assistance Capital Program Funding (RACP) and other funding. The Commonwealth has provided funding for over 35 of those projects, putting more than $92 million of public investment to work in Lehigh Valley. These projects have resulted in hundreds of jobs and leveraged hundreds of millions of dollars in direct and indirect private investment. We are grateful for Commonwealth’s confidence in these Lehigh Valley projects. Some of the projects identified as priorities by this process that secured funding in 2009 are: Ben Franklin Technology Incubator, St. Luke’s Riverfront Campus, redevelopment of Martin Towers, SteelStacks Performing Arts Center, Gambet Center at DeSales University and the new Lehigh University Science Center. These projects are added to a distinguished list of Lehigh Valley community development projects that have received state help over the last seven years. LVEDC continues to successfully collaborate and bring together Lehigh Valley’s economic and community development leaders to present to the Commonwealth and other funding sources a unified list of Lehigh Valley priority projects. This section contains a list of the 2010 state priority projects. And this year, LVEDC is publishing a separate list of priority projects for funding under the Federal Department of Commerce’s Economic Development Administration grants.

Comprehensive Economic Development Strategy Page 3

CITY OF ALLENTOWN, LEHIGH COUNTY

WASTE TO ENERGY FACILITY PROJECT DESCRIPTION

Delta Thermo Energy, Inc. will construct an alternative energy facility which will generate electricity, create green jobs. It will recycle the energy content of biomass and industrial waste in order to generate large amounts of clean, thermal energy. It does not require fossil fuels. The fundamental idea is to locate this plant between the Allentown waste water treatment facility and a PPL power substation. They will take the sludge from the waste water treatment facility plus municipal solid waste collected in the municipality and will process the waste to produce clean energy (electricity, steam and hot water) to eventually power the waste water treatment facility and sell the excess power to the substation. This plant will be the first in the nation to bring this new process/technology into operation. This plant will become the demo facility/plant for other communities to visit as a working example of what could be installed. Approximately 20 jobs will be created in the first 2 phases and over 200 jobs once plant is operating and manufacturing begins for new plant components. STATUS OF PROJECT/TIMELINE

Project to be completed in three phases. It is ready to begin in mid 2010. First phase to be complete in early 2011. Second phase immediately following phase 1 and will be completed by end of 2011. Third Phase will be completed in 2012. Over 1 million dollars is committed from the Department of Energy and another commitment from DOE of at least 20 million dollars is expected shortly.

FUNDING

$2 million dollars is requested. TOTAL PROJECT INVESTMENT/COST: $44 million dollars ALLENTOWN INDUSTRIAL DISTRICT EXPANSION THROUGH FREIGHT RAIL EXPANSION PROJECT DESCRIPTION

The 1.5 mile Barber’s Quarry Branch freight rail extension will directly support the creation and retention of a significant number of manufacturing jobs in Allentown in three specific ways. First, it will greatly improve the capacity of two existing businesses and support their needs to grown and expand while reducing their transportation needs. These two existing businesses are immediately adjacent to the proposed freight rail expansion currently employ 95 people. Their expansions would create an additional 50 jobs. Second, there are two underutilized industrial sites along the BQB that could be redeveloped as modern rail served industrial space that would retain 12 existing jobs and create industrial space that would support approximately 190 new jobs. Finally, the extension of freight rail service is also adjacent to the City’s former incinerator which is industrially zoned and contains 9 acres of developable land which could support the development of a 50,000 square food manufacturing facility, creating another 40-50 jobs. The rail service will support the investment of at least $19,000,000 to redevelop the two existing underutilized sites and an additional $9,000,000 to develop the former incinerator site. In total the requested EDA funding will retain 107 existing jobs, potentially create 290 new

Comprehensive Economic Development Strategy Page 4

manufacturing jobs and induce the investment of $31,000,000 of additional private and public funding. STATUS OF PROJECT/TIMELINE

Bidding Documents and Permitting: Fall of 2010 Bidding for Rail Construction: Winter 2010 Construction: Spring 2011 to Spring 2012 Completion: Spring 2012

FUNDING

$2 million dollars requested. TOTAL PROJECT INVESTMENT/COST: $2.8 million dollars

BRIDGEWORKS ENTERPRISE CENTER CLERESTORY REPLACEMENT PROJECT DESCRIPTION

AEDC proposes to create a green business incubator in an energy efficient industrial building. The green business incubator will invest resources in facilitating entrepreneurship in green industries with a manufacturing focus. AEDC will focus on home-grown small businesses servicing the energy conservation industry and the renewable energy industry. The goal is to leverage existing local capacity in the production of machined parts, plastics manufacture, and construction materials to grow new businesses for the green economy. These efforts cannot be undertaken without the addressing energy conservation problems with the existing roof. AEDC will use EDA funds to replace the existing acrylic window panels with higher R-Value panes. This would result in the replacement of 2,400 linear feet of acrylic panes at a cost of $1.3 million. It is expected that the renovated center will employ approximately 120 staff.

STATUS OF PROJECT/TIMELINE

Construction will be ready to begin in Fall of 2010. 2011 will be used to complete renovations of existing facility, marketing for green business incubator, and support of continued expansion.

FUNDING

$1 million dollars is requested. TOTAL PROJECT INVESTMENT/COST: $1,300,000

LEHIGH RIVERFRONT PROJECT DESCRIPTION The Lehigh Riverfront Project involves the creation of a mix of uses including retail, entertainment, residential and an anchor building project such as an arena or hotel. Currently the Riverfront includes approximately 26 acres which is underutilized by Valley residents and tourists because of the industrial uses. The beauty of the Lehigh River is completely obstructed by older, industrial uses. The project would feature a riverwalk with the intent of re-connecting the community with the River. The section of the Lehigh River which would border this development is the only navigable section of the Lehigh River. The Riverfront will become a destination for the entire Lehigh Valley and has the potential of the creation 150 to 200 jobs.

Comprehensive Economic Development Strategy Page 5

Additionally, the construction of the American Parkway bridge will create additional access to the site linking the east side of Allentown to the downtown. STATUS OF PROJECT/TIMELINE Phase I includes acquisition, clean up and infrastructure. Total cost of Phase I is approximately $25 million. Identified land parcels are under site agreement. $5 million in RACP funds have been awarded to the project. Neighborhood Improvement Zone has been approved by the State of Pennsylvania. Phase I is expected to be underway in near future. Phase II includes construction of the buildings. FUNDING TOTAL PROJECT INVESTMENT/COST: Phase I and II Project Total: $175 million RACP award: $5 million to date. Additional funds are necessary for Phase II.

WEST END STREETSCAPE IMPROVEMENTS PROJECT DESCRIPTION This project will result with the following list of key projects that are programmed into a Multi-Year Revitalization Strategy.

Improve crosswalks/sidewalks.

Develop and enhance the organization’s website.

Work with the City to ensure zoning and land use ordinances are consistent with the vision statement.

Place new trash and recycling bins.

Improve street lighting.

Create sustainable merchants’ and residents’ associations.

Create unified advertising and marketing for the business district.

Install benches, planters, banners, trees and other streetscape improvements.

STATUS OF PROJECT/TIMELINE $1.5 million has been secured in RACP funding from the State of Pennsylvania. Additional requests are pending at this time. Conceptual designs are complete. Construction is expected to begin in fall of 2010. FUNDING $1.5 million is under request. TOTAL PROJECT INVESTMENT/COST: $ 3,000,000

CITY OF BETHLEHEM, NORTHAMPTON COUNTY

SOUTH MAIN STREET PARKING

PROJECT DESCRIPTION

Project involves implementation of parking solutions including the construction of a new parking garage adjacent to the existing parking garage at the south end of Main Street in Downtown Bethlehem behind the Main Street Commons. The existing structure will be rehabilitated, and

Comprehensive Economic Development Strategy Page 6

connected to the new garage once built. The garage will contain approximately 400 parking spaces and will support additional development contemplated by Moravian College at its Priscilla Payne Hurd campus along with existing needs to the Central Moravian Church, Moravian book Shop, Hotel Bethlehem and other businesses along the southern end of Main Street. The total project cost is estimated to be $10 million. STATUS OF PROJECT/TIMELINE

A feasibility study has been completed. Existing parking structure was acquired in Fall 2009, with rehab work commenced in January 2010. The City of Bethlehem has received an earmark for $3.5 million in RACP funding for the garage.

FUNDING

The City of Bethlehem is requesting $1.5 million in RACP funding. The remaining funds will be generated through City and Parking Authority borrowing. TOTAL PROJECT INVESTMENT/COST: $10,000,000

MAJESTIC BETHLEHEM CENTER

PROJECT DESCRIPTION Majestic Bethlehem Center is a 441 acre piece of property located on the former Bethlehem Steel Plant in Bethlehem. The parcel is owned by a Roski/Majestic affiliated entity, Bethlehem Commerce Center, LLC. It is located adjacent to the LVIP VII and it is a major part of the old Bethlehem Steel, Bethlehem Plant. Majestic Realty is one of the largest private developer of commercial real estate in the United States. They have developments in Southern California, Las Vegas, Dallas, Denver, Atlanta and now Bethlehem. Even in this difficult real estate market place, Majestic Realty is planning to begin construction, within the year, on the development’s first building. They have a number of potential end users looking at the site and they are committed to developing in Bethlehem. The initial building will generate $60 Million in construction investment. The site will require $60 Million for environmental remediation, basic site work and infrastructure improvements in order to transform the Majestic Bethlehem Center from a brownfield into a strong real estate site. When the site is fully developed, Majestic Bethlehem Center will have 7.5 Million square feet of LEED certified space, $500 million in construction investment and create between 3,000 and 5,000 jobs.

STATUS OF PROJECT/TIMELINE Northampton County has provided over $13 Million in funding to build Commerce Center Blvd, a road and rail grade separation project that makes the property fully accessible from Route 412 and I-78. Majestic has secured $1.75 Million in RACP funding and is using those funds to begin site work and environmental remediation work on the site. Additionally, Majestic is awaiting word on Growing Greener funding. The application for the initial $1 Million RACP has been completed and the Budget Office has approved the initial use of those funds. Phase I is estimated at $120 million, including $60 million towards remediation, site work, and infrastructure improvements. Majestic received $250,000 in RACP funding.

FUNDING

The City of Bethlehem and Majestic are requesting $5 million in RACP funding and $2 million in EDA funding. TOTAL PROJECT INVESTMENT/COST: $500 million

Comprehensive Economic Development Strategy Page 7

SOUTHSIDE PARKING STRUCTURE PROJECT DESCRIPTION

This is an integral project to the revitalization efforts for the Southside commercial business district. Aside from the planned First Fridays events which brings thousands of people to this area, everyday business opportunities become limited due to lack of parking. A number of key economic development projects remain reliant on this project to ensure that parking capacity will be available upon build out of these projects. Three sites in the South Side’s commercial business district under consideration and assessed for feasibility. Feasibility Study completed in winter of 2010. Sites under consideration are accessible to transit users, shoppers, businesses and downtown residents.

STATUS OF PROJECT/TIMELINE

A feasibility study has been completed for this project, and construction can begin in 2011 pending receipt of grant assistance. FUNDING

A total of $2.75 Million in RACP support is being requested. The remaining funds will be generated through City and Parking Authority borrowing. TOTAL PROJECT INVESTMENT/COST: $5.5 million

4TH AND BROADWAY PARKING GARAGE PROJECT DESCRIPTION

Build a parking garage connected adjacent to the historic Flatiron Building at 4th and Broadway. The garage will have three levels and contain approximately, 450 spaces. It will support both the commercial revitalization of West Broadway, Wyandotte Street, and the adaptive re-use of the Flatiron Building. Major activity representing millions of dollars of investment along both the Broadway and Wyandotte Street corridors will require the addition of more off street parking. This area was targeted for revitalization in the South Side Master Plan completed by Sasaki Associates for the City of Bethlehem. The total project cost is estimated to be $7.5 million. STATUS OF PROJECT/TIMELINE

Acquisition is under agreement. Preliminary design and feasibility are currently underway. Project could be under construction pending receipt of grant assistance in 2011.

FUNDING

The City of Bethlehem is requesting $3 million in RACP funding. TOTAL PROJECT INVESTMENT/COST: $7.5 million

MARTIN TOWER

PROJECT DESCRIPTION The Martin Tower Complex was acquired in May 2006 by local developers with deep roots in the Lehigh Valley with the intent to redevelop the property. The Complex, including a 650,000 square foot 21-story high-rise completed in 1972, was developed by the Bethlehem Steel Corporation as its sole-occupant corporate world headquarters. Today, the building, due to its

Comprehensive Economic Development Strategy Page 8

age, design, code compliance deficiencies and extensive environmental issues remains obsolete and no longer viable for its originally intended purpose. The ―project‖ consists of the preservation and adaptive reuse of the 21-story Martin Tower into a mixed use facility containing office, retail and residential uses, in conjunction with various amenities including a complete fitness center, public spaces, interior and exterior recreation areas, and convenience store and meeting rooms. STATUS OF PROJECT/TIMELINE The City of Bethlehem and Martin Tower has received commitments for $2.825 million in RACP funding. The project is in final design. FUNDING The City of Bethlehem and Martin Tower are requesting and additional $8.3 million in RACP funding. Martin Tower anticipates an additional $8 to $10 million in TIF funding. TOTAL PROJECT INVESTMENT/COST: $200 million+

LEHIGH UNIVERSITY SCIENCE AND TECHNOLOGY INFRASTRUCTURE

PROJECT DESCRIPTION

A newly constructed state-of-the-art Science, Technology, Environment, Policy & Society (STEPS) building designed specifically for collaborative research, undergraduate teaching of life sciences and other environmental and energy fields, and the renovation of an existing former steel research building, Jordan Hall, for Cellular and Bimolecular Science & Engineering (CBSE) purposes. The newly constructed building will include modern classrooms equipped with the latest technologies to extend the learning experience beyond the classroom, instructional laboratories integrating both experimental and computational facilities, and research laboratories for faculty and students. Renovation of the current Jordan hall space will include undergraduate teaching laboratories, shared research facilities, lecture and meeting rooms, individual PI laboratory space, student and support staff offices for about 20,000 sq. ft. of usable space. This project will allow the University to seek and foster partnerships with medical schools, hospitals, medical device companies, and local entrepreneurs, and is located adjacent to the newly expanded en Franklin Incubator in Building G. Total investment for this project is $103M. This includes new building construction ($55M), renovations of an existing facility ($10M), and other programmatic investments ($38M) by the University such as endowed chairs and graduate fellowships, undergraduate research funds, seed grants for collaboration, new faculty hires, new graduate programs and industry, hospital and other partnerships. Construction of these facilities and the expanded partnership with the City of Bethlehem and the other partners of the Southside Bethlehem Keystone Innovation Zone are essential for the University to contribute to redevelopment of the community and to compete on a statewide, national and international level.

STATUS OF PROJECT/TIMELINE

Lehigh’s President and the Board of Trustees have approved the project. The project broke ground in the fall of 2008 with completion expected in 2010. Lehigh University has committed $65 million in capital investments for the project. The City of Bethlehem and Lehigh University received $1 million in RACP funding.

Comprehensive Economic Development Strategy Page 9

FUNDING

The City of Bethlehem and Lehigh University is requesting $10 million in RACP funding. TOTAL PROJECT INVESTMENT/COST: $103 million

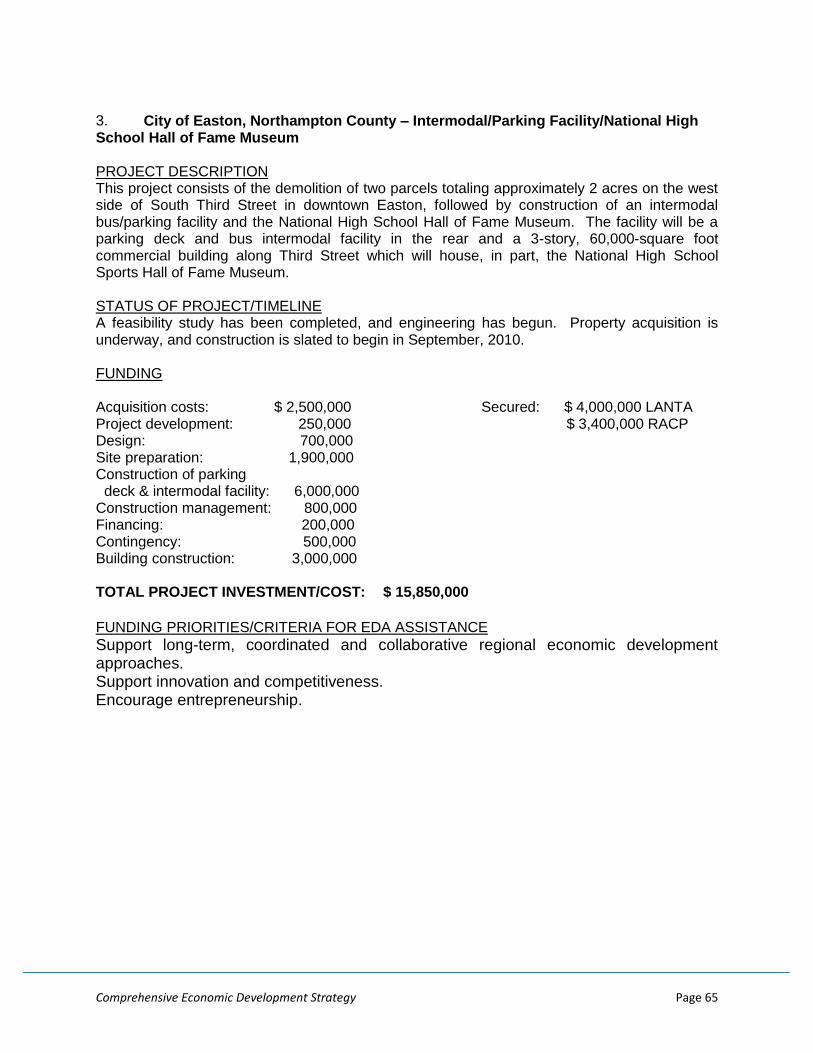

CITY OF EASTON, NORTHAMPTON COUNTY

13TH STREET SILK MILL PROJECT

PROJECT DESCRIPTION The 13th St. Silk Mill project includes the acquisition and redevelopment of several underutilized commercial and industrial properties along N. 13th Street (former Simon Silk Mill and Moon Properties). Proposed redevelopment is a mix of commercial, residential, and open space/community uses with a focus on the creative industries, the arts, and energy efficient technologies. Great progress has been made in 2009. A full site, structural, geotechnical, and building analysis have been completed as well as the development of a master plan. Also, the asbestos and containerized waste remediation has been completed. Additionally, feasibility of a geothermal system has been studied as well as the use of solar technology. The next step in this project is to install the necessary infrastructure to facilitate the rehabilitation of the individual buildings in the complex. Proposals have been received for the engineering and design of this infrastructure. Additionally, cost estimates for the construction of the infrastructure have been generated. The Redevelopment Authority of Easton is in the process of identifying funding sources to complete this important phase of the project. Upon completion of the infrastructure, solidifying and leveraging the private funds needed to complete the building restorations will be viable. Total permanent job creation upon project completion is estimated at 200+. STATUS OF PROJECT/TIMELINE Site and facilities analysis, program development, and asbestos and containerized waste abatement have been completed. A grant with DCED is pending in the amount of $500,000 for the acquisition of a small parcel and the design of the initial infrastructure at the site that is required to facilitate the rehabilitation of the buildings. This work includes the installation of water, sewer, and gas lines as well as the construction of a central boulevard and the parking lot for phase 1. The construction cost for this phase is estimated at $2,000,000. Engineering and construction of these improvements can begin as soon as the funding source is identified and permits are obtained. Funding sources received to date: EPA $ 200,000 (brownfield cleanup grant) EPA/County 477,000 (sub-grant and sub-loan for environ. cleanup) RACP 3,500,000 (acq.) EPA 40,000 (environmental assessment grant) DCED ISRP 1,000,000 (environmental assessment grant) DCED 115,000 (site planning & analysis, bldg. analysis & master

design) Preserve America 150,000 Total $ 5,557,000

Comprehensive Economic Development Strategy Page 10

FUNDING Financial Request: $1 million for infrastructure construction including water, sewer and gas lines, the main boulevard, and the parking lot for Phase 1.

Acquisition $ 3,500,000 expended Site/Facilities Design 75,000 expended Master Plan Design 75,000 expended Environmental 2,000,000 expended or secured for future lead

abatement work Engineering (phase 1 infr.) 500,000 Grant Pending Engineering (later phases) 500,000 unsecured Phase 1 infr. Construction 2,000,000 unsecured Construction/hard costs 70,000,000 unsecured private investment Total $ 78,650,000

$2,000,000 needed to complete phase 1 infrastructure.

TOTAL PROJECT INVESTMENT/COST: In excess of $70 Million

INTERMODAL/PARKING FACILITY/ NATIONAL HIGH SCHOOL SPORTS HALL OF FAME MUSEUM PROJECT DESCRIPTION

This project consists of the demolition of two parcels totaling approximately 2 acres on the west side of South Third Street in downtown Easton, followed by construction of an intermodal bus/parking facility and the National High School Hall of Fame Museum. The facility will be a parking deck and bus intermodal facility in the rear and a 3-story, 60,000-square foot commercial building along Third Street which will house, in part, the National High School Sports Hall of Fame Museum. STATUS OF PROJECT/TIMELINE

A feasibility study has been completed, and engineering has begun. Property acquisition is underway, and construction is slated to begin in September, 2010.

FUNDING

Acquisition costs: $ 2,500,000 Secured: $ 4,000,000 LANTA Project development: 250,000 $ 3,400,000 RACP Design: 700,000 Site preparation: 1,900,000 Construction of parking deck & intermodal facility: 6,000,000 Construction management: 800,000 Financing: 200,000 Contingency: 500,000 Building construction: 3,000,000

TOTAL PROJECT INVESTMENT/COST: $ 15,850,000

Comprehensive Economic Development Strategy Page 11

BLACK DIAMOND SOUTH SIDE MILL COMPLEX PROJECT DESCRIPTION

This project consists of the redevelopment of a blighted and structurally unsound mill complex on the city’s South Side at Lincoln and Coal streets. This 4 AC parcel is in an excellent middle class neighborhood adjacent to an elementary school. The complex encompasses a full square block that is prime real estate for a mixed use development of single family, townhouses and neighborhood services.

STATUS OF PROJECT/TIMELINE

Funds will be used for acquisition and demolition of the property to provide a developable 4-acre site.

FUNDING

Acquisition costs: $ 1,200,000 Environmental costs: 1,000,000 Demolition costs: 800,000+ Soft costs: 400,000 Construction costs: 8,000,000+ Total: $ 11,400,000+

TOTAL PROJECT INVESTMENT/COST: +/- $ 12 Million

13TH STREET AND INTERSECTION IMPROVEMENTS PROJECT DESCRIPTION

Improvements to 13th Street and the intersections at 13th Street and Wood Ave., one of the Route 22 exchanges in Easton, and 13th St. and Bushkill Drive need to be done in preparation for extensive redevelopment activities at the Silk Mill on North 13th Street and east along the Bushkill Creek as part of the larger Bushkill Creek Corridor RACP Project. These activities have the potential to generate a great deal of additional traffic to an area that is already congested. Additionally, these intersections need to be pedestrian and bike friendly to accommodate this type of traffic to the Silk Mill site and interconnection to the regional trail system.

STATUS OF PROJECT/TIMELINE

Design: Summer, 2010 Construction: Spring, 2011 FUNDING

Design: $ 150,000 Construction: $ 1,000,000 TOTAL PROJECT INVESTMENT/COST: $(+/-) $ 1,200,000

Comprehensive Economic Development Strategy Page 12

LEHIGH COUNTY, CATASAUQUA BOROUGH REDEVELOPMENT OF F.L. SMIDTH PROPERTY

PROJECT DESCRIPTION

F.L. Smidth currently owns a 12.52 acre parcel in Catasauqua along the Delaware and Lehigh Heritage Trail Corridor adjacent to the Lehigh River. The property, along Front Street, makes up 3% of the Borough of Catasauqua. F.L. Smidth is actively marketing the property for sale. Several developers have been interested in the property but the complexities of redeveloping the property, including soil contamination and flood plain issues, are making it difficult to sell. The Borough is interested in having the property redeveloped to help generate needed tax revenue and to help with the revitalization of the community. Catasauqua has been part of the Lehigh Valley Borough Business Revitalization Program for the past four years and has been very proactive about revitalization of their business district. The property is a brownfield as soil investigations have been done on the site and identified raised levels of lead, arsenic, and Benzo(a)pyrene.A Special Industrial Area cleanup plan was approved for the site that outlined a need for capping and deed restrictions to the site. Ground water was not tested on the site, but is a concern for prospective developers. Ground water testing will need to be done before redevelopment of the site can begin. This is a significant project for the Borough, Lehigh County and the Lehigh Valley Land Recycling Initiative (LVLRI). The best reuse for the site has been determined to be multi-use with townhomes, apartments, retails and mixed use units along Front Street. Redevelop efforts could result in $453,000 in new taxes for the Borough. STATUS OF PROJECT/TIMELINE

F.L. Smidth is actively marketing the property. Several developers and the Borough of Catasauqua are considering redevelopment opportunities. LVLRI, DEP, EPA and FEMA have been involved in redevelopment discussions with the Borough. Once a purchaser is confirmed for the property timelines and detailed project plans will be developed.

FUNDING

Amount of funds still needed/being requested for project completion. Please include details on leveraged and/or matching funds. Property acquisition is under discussion. RACP Request: $5M TOTAL PROJECT INVESTMENT/COST: TBD

Comprehensive Economic Development Strategy Page 13

LEHIGH COUNTY, CITY OF BETHLEHEM REGIONAL DEVELOPMENT – CITY CENTRAL LAND DEVELOPMENT (FORMER MARTIN TOWER COMPLEX) PROJECT DESCRIPTION

The City Central land development (formerly the Martin Tower complex), located in the City of Bethlehem, consists of 53 acres of land and encompasses the 21-story Martin Tower constructed in 1970 with a gross floor area of 664,450 square feet. In addition to the Tower, the property includes three peripheral buildings: 1) the U-shaped Annex, a 253,452 square foot building adjacent to the Tower (connected by a common corridor) was constructed in 1958; 2) the Printery Building, a one story industrial building containing 95,000 square feet with an office area, loading dock and printing reproduction area; and 3) the Central Heating and Refrigeration Building (known as the CH&R Building) is a one-story plus mezzanine level industrial plant building used to generate hot and cold water which heated and cooled the Tower. In total, the former Martin Tower complex contains over one million square feet of building area – all of which has been completely vacant since the last tenants moved out in February 2007. The conditions of the property apply to the respective characteristics of blight as defined in the Urban Redevelopment Act, which resulted in the City of Bethlehem declaring the entire property a Redevelopment Area in 2008. The City Central land development plan is centered around the adaptive re-use and redevelopment of the Tower and surrounding 53-acres as a mixed-use residential, retail and commercial property. A committee made up of members from Lehigh County, the City of Bethlehem and the Bethlehem School District have been involved (with future meetings planned) in the evaluation of financial opportunities for the project, including the development of Tax Increment Financing (TIF) District. STATUS OF PROJECT/TIMELINE

The current owners purchased the property in 2006. Master Development Plans are being finalized for review with the City of Bethlehem (see attached concept plan). RACP funding of $2,825,000.00 has been authorized by the Office of the Budget, with additional RACP funding pending. A meeting with the TIF Committee (consisting of Lehigh County, the City of Bethlehem and the Bethlehem School District) will be scheduled once the Master Development Plan has been reviewed by the City of Bethlehem. The project will be developed in various stages to support the mixed-use elements planned for the property.

FUNDING

Estimated Project Value: The investment for the proposed redevelopment of Martin Tower is approximately $90 million. The planned redevelopment of the peripheral land will exceed $200 million in total value. RACP Funds: $10,000,000 TIF Funds: $10,000,000 Conventional Financing: To be determined Owner Equity: To be determined TOTAL PROJECT INVESTMENT/COST: $200,000,000.00

Comprehensive Economic Development Strategy Page 14

LEHIGH COUNTY, CITY OF ALLENTOWN REGIONAL DEVELOPMENT – J.G. PETRUCCI AND AZTAR/TROPICANNA LAND AND LSI OFFICE/MANUFACTURING FACILITY PROJECT DESCRIPTION

Coca-Cola Park opened to Lehigh Valley baseball fans in April of 2008. The return of professional baseball to the Lehigh Valley for the first time since 1960 was met with remarkable community support, unprecedented excitement and unrivaled fanfare in 2008. By becoming one of just six Minor League franchises to surpass the 600,000 mark for total attendance, the IronPigs emerged as one of the top draws and premier franchises in Minor League Baseball. Coca-Cola Park, the foremost baseball and entertainment venue in the Minors, drew rave reviews for its intimacy, fan-friendly atmosphere and architectural design. The success and excitement continued through the second session and in year-three Coca-Cola Park will host the Triple-A 2010 All Star Game. Retail, entertainment and sports venues are an economic generator for the community and are often clustered in one area. There are two vacant parcels and one office/manufacturing facility, adjacent to Coca-Cola Park, which are available for development. The first vacant parcel, bordering Dalphin Street is 26 acres and is owned by J.G. Petrucci. The second vacant parcel, consisting of 18 acres, was planned to be used by Aztar/Tropicanna for the development of a slots-based casino if they received the license. The development of these two parcels and the redevelopment or the reuse of the office/manufacturing facility would complete the redevelopment of east Allentown and allow for continued economic revitalization of the community.

STATUS OF PROJECT/TIMELINE

The two vacant parcels are available for development. The office/manufacturing facility, currently owned by LSI, is mostly vacant and has been on the market for several years. FUNDING

RACP funding may be appropriate for the project based on final plans. TOTAL PROJECT INVESTMENT/COST: $ To be determined based upon the scope of the project.

LEHIGH COUNTY, MULTIPLE MUNICIPALITIES

TRANSPORTATION – ROADS, BRIDGES, MASS TRANSIT AND AIRPORTS

PROJECT DESCRIPTION

Safe roads, structurally sound bridges, modern airports and efficient mass transit projects are important to the economic stability of Lehigh County and the entire Lehigh Valley. With the number of projects planned, it’s imperative for the region to have an understanding of the process, funding timelines and project contingencies for all projects. Lehigh County continues to collaborate with legislators and funding agencies to ensure the successful funding and timely completion of projects in the region.

Comprehensive Economic Development Strategy Page 15

Plans for Route 22 have been re-designed and PennDOT is reviewing the changed plans with the region and the MPO. Lehigh County, Northampton County and LVEDC are completing a regional transportation/rail study with New Jersey Transit and Systra to help understand the transportation needs of the region. LANTA has completed a comprehensive strategic plan which looks at the system needs for the next 12 years. Lehigh Northampton Airport Authority (LNAA) has planned and designed upgrades to the Main Terminal at Leigh Valley International Airport. The project is under construction with funding assistance from Federal and Commonwealth agencies. Additional hanger and infrastructure projects are needed to generate additional revenue, particularly in the area of general aviation. STATUS OF PROJECT/TIMELINE

The Transportation Improvement Plan (TIP) has been authorized by the region through 2012. A new TIP is under discussion and will be finalized this year. Route 22 plans need to be finalized and funding needs to be authorized for the project. The federal stimulus funds have been used for updating bridges and a few enhancements to major roads in the Lehigh Valley. The regional transportation/rail study will be completed in late March 2010 and will prompt discussions on how to fund the recommended projects. LANTA’s plan requires increased funding and regional collaboration with the Lehigh Valley Planning Commission and the municipalities. Regional collaboration will be instrumental to the development and adoption of the effective land use plans recommended in the LANTA strategic plan. FUNDING

To be determined once a compete review of all the transportation, mass transit, roads, bridges and airports needs are reviewed and a comprehensive picture of all the needs of the Lehigh Valley are understood. A priority needs to be established and state and federal elected offices need to understand the overall needs for funding in the Lehigh Valley.

LEHIGH COUNTY, WESTERN LEHIGH COUNTY

INFRASTRUCTURE – WATER/WASTE WATER PROJECT DESCRIPTION Effective water and wastewater plans are important to the successful growth of Lehigh County. This is especially important in Western Lehigh County where several of the municipalities have experienced heavy growth in commercial and residential projects. Lehigh County Authority (LCA), Lehigh County and the City of Allentown signed a regional collaboration agreement to help provide for the long term water needs for Lehigh County municipalities. For now, the water needs of the community are being met. The Lehigh County Authority provides the majority of the water and wastewater services. The Lehigh County Authority has developed a 10-year capital plan consisting of $150 million in projects. Additional water supply and wastewater capacity accounts for approximately 50% of the plan. The Lehigh County Authority has $12 million in reserves and other loan funds in hand

Comprehensive Economic Development Strategy Page 16

and has applied for $28 million in infrastructure development funds from the Commonwealth Financing Authority (CFA) to move forward with the initial projects. The total amount of funding was not authorized by the CFA so additional funds are being requested. Wastewater capacity is depleted in Western Lehigh County. LCA and its signatory communities are preparing to embark on numerous projects associated with its wastewater treatment and conveyance infrastructure to obtain the additional capacity required to meet its short and long-term capacity needs. The projects are interrelated, very large in scope and will require support from LCA staff, consultants, surrounding communities and regulatory staff. STATUS OF PROJECT/TIMELINE The Lehigh County Authority has developed a 10-year Capital Plan which includes $150 million in projects. $28 million in projects are ready for development The Lehigh County Authority has $12 million in funds available and has requested $28 million in Commonwealth Financing Authority (CFA) funds which were not approved. Additional funds are needed to allow the Lehigh County Authority to provide additional capacity, particularly with wastewater to allow expansion of current businesses and development of new businesses to occur. FUNDING Lehigh County Authority: $12 million Pennvest: $7 million Current CFA Requests: $28 million – Not Approved TOTAL PROJECT INVESTMENT/COST: $150,000,000.00 over 10-years

NORTHAMPTON COUNTY

ST. LUKE’S RIVERSIDE HEALTH CAMPUS – BETHLEHEM TOWNSHIP PROJECT DESCRIPTION St. Luke’s Hospital & Health Network plans to develop 500 acres of land into the Riverside Health Campus at the intersection of Rt. 33 & Freemansburg Avenue. When fully developed, it is expected to integrate patient care with teaching, research, housing, recreation and retail activities. This will be one of the largest health care campuses in the country, enhancing the profile of Northampton County and the region as a destination for comprehensive and state-of-the-art health care. Initially 685 direct new jobs with an estimated $28 million annual payroll will be created along with 715 indirect new jobs with an estimated $24 million payroll impact. The Health Complex portion, which encompasses 40 acres of the project, represents 251,000 square feet of new space consisting of a 77,000 square foot medical office building, a 126,000 square foot acute care inpatient hospital, and a 48,000 square foot free standing Cancer Center has an estimated expense of $96 million. This portion of the project is scheduled to begin in late Spring of 2010 and finish in late 2011. Planned future phases could include a medical school, pharmaceutical research center, hotel and conference center, school of nursing, life care and a retirement community and represents about 4,000,000 square feet of new construction. STATUS OF PROJECT/TIMELINE Property acquisition totaling $40 million is completed. Preliminary site work is completed.

Comprehensive Economic Development Strategy Page 17

Building Pad Construction is scheduled to be completed in 2010 Health Complex construction scheduled to begin late Spring 2010 and finish in late 2011. FUNDING $4,950,000 in RACP funding has been committed to date. TOTAL PHASE 1 ( ROADS, LAND, INFRASTRUCTURE, CONSTRUCTION COSTS) PROJECT INVESTMENT/COST: $147,599,976

RTE. 33/TATAMY INTERCHANGE – PALMER TOWNSHIP

PROJECT DESCRIPTION A Point-of Access Study (POA) was completed at the expense of Chrin Companies and submitted to PennDOT in September 2009. Approval of the POA is expected by June 2010, which could provide for the completion of the interchange in 2013. In 2008, then State Senator Wonderling put forth a $14 million request in the PA Capital Budget, which represents approximately one-half the estimated cost to complete the interchange Construction of the interchange may be financed using both public and private monies. The interchange will open up the entire 800 acres to development, potentially resulting in the creation of over 6,700 jobs once full build-out of the entire Centre is achieved. STATUS OF PROJECT/TIMELINE Interchange plans are moving forward. Senator Mensch attended a meeting March 12, 2010 with Chrin Companies, Northampton County, LVEDC and other interested parties in order to move the project forward. POA approval expected June 2010 and construction is expected to be completed in 2013. FUNDING Amount of funds still needed/being requested for project completion. Please include details on leveraged and/or matching funds. Interchange Funding. 2008 RCAP request for $14 million to cover infrastructure and construction. Possible $6.9 million in Northampton County RZEDBs. TOTAL PROJECT INVESTMENT/COST: $25,000,000

LEHIGH VALLEY ENTERTAINMENT COMPLEX – PALMER TOWNSHIP PROJECT DESCRIPTION

The Lehigh Valley Entertainment Complex will seat 8,000 - 10,000 for sporting events, including AHL ice hockey, indoor soccer, lacrosse and basketball, national concert tours, family entertainment and related shows, with surface parking for approx 3,500 cars. The complex is proposed as part of the 800-acre Chrin Commerce Centre, located in Palmer Township. The entertainment complex staff and the team will create 200 jobs. The estimated economic value to the community for both the arena and the interchange will be in the millions of dollars within two years of completion. The annual positive economic impact will be $25 -$35 million. The entertainment complex staff and the team will create 200 jobs.

Comprehensive Economic Development Strategy Page 18

STATUS OF PROJECT/TIMELINE Entertainment Complex. Northampton County is proposing this site to the AHL Philadelphia Phantoms owners. Site selection is expected on or before July 30, 2010. The complex is expected to open no later than the end of September 2013. Estimated costs are $60 million with approximately 50% public funds leveraging 50% private investment in the project. Possible sources of public funding are the state RCAP and/or county TIF and the hotel tax. Interchange is in the planning phase. PennDOT is expected to approve the Point of Access Study by the end of June 2010. FUNDING Entertainment Complex Funding. Developer is seeking significant public investment in support of the project. Various economic and infrastructure development resources will need to be accessed to make this project feasible. There is a $30 million line item in the 2006 PA Capital Budget available for potential funding. Project will have private investment component of approximately 50% of the project cost. ENTERTAINMENT COMPLEX TOTAL PROJECT INVESTMENT/COST: $60,000,000

CHRIN COMMERCE CENTRE – PALMER TOWNSHIP AND TATAMY BOROUGH PROJECT DESCRIPTION The Chrin Commerce Centre is a unique multi-phased development to be constructed on an 800-acre site along Route 33. Phase I, the Business Park, consists of 11 lots primarily designed for light industrial and offices. This 77-acre tract received subdivision approval in 2008 and is home to Porsche’s 130,000 square-foot Northeast Retail Support Center, which received LEED Gold certification for environmental sensitivity. Chrin is exploring alternative development scenarios for Phases II and III ranging from town center and mixed-use development to office and light industrial. Current projections estimate that over 5,000 jobs can be created with the build-out of these phases. PennDOT required on-site and off-site traffic improvements with a cost $2,195,354. In May 2009, An Infrastructure Development Program Grant (IDP) was approved for the development, in the amount of $1.25 million. Approximately $4 million, excluding land costs, has been privately invested by Chrin Companies for on-site infrastructure development to-date. A key component in the ability to continue to attract top tier companies and employment is the construction of an interchange at Route 33 and Main Street. STATUS OF PROJECT/TIMELINE Detailed Phase I engineer’s construction costs estimates are completed and all on-site and off-site traffic improvements are scheduled for completion in 2010. $600,000 of the Pennsylvania IDP grant proceeds have been applied to improvements completed in 2009. The remaining improvements are expected to be completed in 2010. The Porsche facility was completed and occupied in July 2009. FUNDING Phase I Funding Leveraged Investment: $39,330,000 Equity in flex building and on-site improvements: $3,445,354 PA Industrial Development Program Grant for off-site traffic improvements: $1,250,000 TOTAL PROJECT INVESTMENT/COST: $44,025,354 for Phase I

Comprehensive Economic Development Strategy Page 19

SLATE BELT INDUSTRIAL DRIVE – PALMER TOWNSHIP AND SLATE BELT INDUSTRIAL DRIVE PROJECT DESCRIPTION PA Routes 512 and 115 run through the Borough of Wind Gap. Route 512 is classified as a minor arterial roadway with current Average Daily Traffic (ADT) of approximately 17,000 vehicles per day, including 700 trucks per day. In the borough, PA Route 512 is characterized by one thru lane in each direction with on-street parking on both sides of the road. The SR512 and SR1007 corridor receives significant through business traffic from the north going south along SR1007 and east along SR 512 through Plainfield Township, Washington Township and Bangor Borough. The construction of Industrial Drive will provide valuable local access which is required for the beneficial development of a 10-Lot Industrial Park. This Industrial Park will redevelop an existing Brownfield Site, and will provide over one mile of new industrial frontage. The development will also include infrastructure improvements including sanitary sewer mains, pump station, water mains, and additional storm water drainage improvements. A future Phase 2 bypass road is envisioned to further alleviate traffic congestion within the Borough. Phase 2 will connect Industrial Drive with PA Route 33 via a new south interchange. The benefit projected by these improvements is a reduction of 6,200 vehicles per day (21%) due to the Phase 1 and 2 connector roads when fully developed. STATUS OF PROJECT/TIMELINE Detailed engineer’s construction costs estimates are complete, as well as on-site storm water improvements. To date, $600,000 has been spent on Engineering, Environmental and Legal costs and approximately $350,000 has been spent on the storm water improvements. FUNDING Construction $8,262,991 NEPA and Permit Renewal $300,000 Contingencies $743,669 Engineering, Legal, Administrative $743,669

TOTAL PROJECT INVESTMENT/COST: $10,050,329

Comprehensive Economic Development Strategy Page 20

SECTION II: REGIONAL BACKGROUND The Lehigh Valley region (Lehigh and Northampton counties) is located in the central-eastern portion of Pennsylvania; within 300 miles of the major metropolitan areas of the eastern United States. In 1978, both counties adopted Home Rule charters, which provide for government by nine-member elected legislative bodies and an elected County Executive. Within the two-county region, there are 62 municipal governments, 17 school districts, and various special purpose authorities.

ECONOMIC HISTORY OF THE LEHIGH VALLEY

The Lehigh Valley was settled in the early 1700’s by German and Scotch-Irish farmers who established farmsteads and small villages in the southern part of Lehigh and Northampton counties. The Walking Purchase was negotiated between the Delaware Indians and the Proprietary British Government in 1737. The Walking Purchase transferred to the proprietary government ownership of all land that now comprises Lehigh and Northampton counties. It made the area available for future settlement. Bethlehem and Nazareth were settled by the Moravian religious sect in the 1740’s. They were the first towns in the region. Bethlehem was planned and located to serve as the economic and trade center for the Moravian Community in the region. Easton was planned and located by the British Proprietary Government at the Forks of the Delaware in the 1750’s to serve as a trade center for the newly settled region. In 1752, Northampton County was created out of Bucks County to promote Easton as the county seat and trading center. Indian uprisings between 1755 and 1763 slowed growth, particularly north of the Bethlehem-Easton area. In 1762, Allentown was founded on land owned by William Allen in the fort of the Jordan Creek and Little Lehigh Creek. The site was chosen for its potential trade and milling advantages. Influence of the Pennsylvania German settlement The years 1763 to 1790 were characterized by the settlement of the region by Pennsylvania German farmers in the region. Farmers were principally self-sufficient, depending upon their own crops and using a barter economy to obtain necessities they could not produce. Poor transportation and the scarcity of money inhibited commercial trade. Industry and commerce was initiated on a small scale during this period in the form of small shops such as weavers, tanners, shoemakers, gunsmiths and other artisans. Flour and gristmills were also located along swift flowing streams. The immigration of the Pennsylvania Germans continued through the years 1790 to 1830. During this 40-year period, the region benefited from an increasingly prosperous agricultural economy. Farmers prospered while villages increased in number. Taverns, gristmills and tanneries were common in villages. A few villages had distilleries, saw mills, limekilns and iron furnaces. Road and bridge improvements around the turn of the century facilitated trade and travel over stagecoach routes.

Comprehensive Economic Development Strategy Page 21

Easton was the fastest growing and most prosperous of the region’s towns from 1790 to 1830, benefiting from its location and county seat status. Bethlehem, under Moravian ownership and control, grew at a more moderate rate. Allentown was a smaller town at this time, but grew due to its importance as a county seat and farm trade from the area. Allentown became the county seat of Lehigh County in 1812, the year Lehigh County was created from Northampton. Mining and the Industrial Revolution The industrial revolution in the Lehigh Valley was characterized by the mining of anthracite coal, slate, iron and zinc ore, and the building of canals and railroads. The mining of anthracite began in the counties to the north of the Lehigh Valley. By 1830, coal was being transported down the Lehigh River Canal to Easton and from there to Philadelphia and, later, to New York. In addition to coal, the transportation potential of the canals created a greatly expanded trade area for the products of the agricultural economy of the Lehigh Valley. The Lehigh Canal was a major force in land use changes and the creation of new commercial settlements. The mining of iron and zinc, slate and limestone began in the Lehigh Valley during this same period. A technological breakthrough in the 1830’s perfected the anthracite smelting process and resulted in a major increase in the production of iron in the region. By 1855, large iron furnaces using steam power instead of waterwheels could be found in the region. Over this same period, the mining of iron ore also increased greatly. Substantial zinc mining and smelting occurred in the Saucon Valley between 1845 and 1855. The Lehigh Canal was vital to the slate industry due to the transportation difficulties inherent in moving slate. Slate was first quarried commercially near Slatington in 1844. By 1850, five major quarries were operating along the Slate Belt from Slatington to Bangor. Cement kilns were established in Allen Township in the 1850’s. The cement industry, however, did not reach its peak until much later. The growth of mining, particularly anthracite, led to the growth of railroads in the region. The railroads were an improvement in transportation over the canals in that they were less affected by weather and terrain and less restricted in routing. The Lehigh Valley Railroad Line from Mauch Chunk to Phillipsburg, NJ was completed in 1855 primarily to carry anthracite coal to major eastern markets. The Lehigh Coal and Navigation Company, builders of the Lehigh Canal, completed construction of a railroad line from Wilkes-Barre to Phillipsburg in 1868. The line, called the Lehigh and Susquehanna, was also principally a coal carrying line and was sold to the Central Railroad of New Jersey in 1871. The Philadelphia and Reading Railroad was also an influence on the region through its purchasing and leasing of smaller railroads in the valley. The most important was the purchase of the North Pennsylvania Railroad, which had a line from the coalfields to Philadelphia through the Lehigh Valley. By 1890, the last of the major railroad routes had been laid out in the Lehigh Valley. With the growth of the railroads, the industries of the region increased the value of their products from $4.7 million in 1850 to $41.9 million in 1890. Employment increased from 3,419 in 1850 to 19,539 in 1890. Iron and Steel The iron and steel industry continued to expand rapidly in the 1870’s. By 1873, railroads, anthracite, limestone and iron ore made iron production the leading industry in the region in terms of product value. Many iron furnaces existed along the Lehigh River at Coplay,

Comprehensive Economic Development Strategy Page 22

Catasauqua, Allentown, South Bethlehem, Glendon and South Easton. Furnaces were also located in Alburtis, Emmaus, Lower Saucon Township and Allentown. After 1873, local mining began to decline and ore was transported into the valley. Competition reduced the number of companies through consolidation and shutdowns. Bethlehem Iron Company began in 1865 and expanded to become the region’s largest by 1890. By 1890, many manufacturers in the region were dependent upon the iron and steel industry for raw materials and machinery. During the same period, other important product manufacturers in the region were flour and gristmills, tanning and shoemaking, cigar making, zinc oxide making and smelting. During the 1890’s, the production of cotton, wool cloth and raw silk became important. The slate and cement industries north of the cities were also beginning to employ substantial numbers of people. Industrialization No company has affected physical growth in the region as profoundly as Bethlehem Steel Corporation. By 1890, success in the iron and steel industry required tremendous capital, worldwide markets, research, sophisticated marketing, and control of production from mining to consumer. Bethlehem Steel was the only company in the region to meet these requirements and survive past the 1930’s. In the early 1900’s, Charles M. Schwab organized the Bethlehem Steel Corporation, headquartered in South Bethlehem, with subsidiaries throughout North America. Acquisitions and expansion continued at a fast pace through the 1920’s. By 1930, Bethlehem Steel was the second largest producer of steel in the United States. Bethlehem Steel’s primary impact on physical growth has been in the Bethlehem area. The presence of Bethlehem Steel, however, has also encouraged companies fabricating iron and steel products to locate in the region. By 1920, metal and metal products were well established as the principal industry in the region. In 1875, David O. Saylor manufactured the first Portland Cement at the Coplay Cement Company. Portland Cement was more durable, uniform and harder than natural cement. This discovery, together with improved kilns and a growing demand for superior building products, resulted in the rapid expansion of the cement industry in the region. In 1900, about 70 percent of the Portland Cement in the United States was produced in the Lehigh Valley region. Relatively large numbers of independent companies were initially involved and continued to be involved in cement production. Plants existed at or near Martin’s Creek, Nazareth, Bath, Stockertown, Sandts Eddy and Northampton in Northampton County, and Egypt, Ormrod and Fogelsville in Lehigh County. Cement production continued to increase in the region until 1930 when it hit 27 million barrels annually. Not until the 1960’s did the cement industry of the region begin to face serious economic problems due to competition from other cement producing areas. The textile and clothing industry began to grow in the region during the 1880’s due to the arrival of skilled workers and the advent of the silk production industry. The immigration of Eastern Europeans for the steel and cement industries created a pool of skilled labor in the spinning, weaving and sewing trades. The region also benefited from being close to major eastern markets. The spinning and weaving of silk cloth was important in the region from 1880 to 1930. With the declining demand for silk, the textile industries switched to other fabrics and man-made fibers.

Comprehensive Economic Development Strategy Page 23

The garment industry began in the region about 1910 with decentralization from New York City and the increasing demand for ready-to-wear clothing. The industry was then and is now characterized by many small companies in a highly competitive market. There have always been many individual failures and many new company starts. The primary influence of the textile and garment industry in the region was in the employment of thousands of workers. The importance of agriculture has declined in the region since 1890 although it has continued to play a significant role in the economy of the valley. Technological improvements and scientific methods aided the farmer in increasing crop yields despite the fact that the percentage of the population employed in agriculture declined drastically. During the twentieth century, the growth of industry and changes in lifestyle in the region created greatly increased demand for retail and wholesale trade and services. New products and marketing techniques created demand for electrical appliances, automobiles, gasoline and home heating furnaces. Around the turn of the century, department stores began to appear in downtown areas. The Hess Brothers opened the first department store in the region in Allentown in 1897. Other department stores located in the three cities of the region during the early 1900’s. Chain stores appeared in the 1920’s with branch stores of national organizations replacing the neighborhood variety and grocery stores. Post World War II years saw the rise of the shopping center and suburban discount store following residential growth in suburban areas. Modern Times The building of U.S. Route 22 between 1952 to 1957, created great opportunity for development of the suburban perimeter north of the valley’s urban core. In 1959, the first section of the Lehigh Valley Industrial Park (LVIP) was opened to developers at the Airport Road interchange of U.S. 22. Additional LVIP sections opened in 1964 and 1974. In 1966, the Whitehall Mall opened at the MacArthur Road interchange, joined in 1976 by the Lehigh Valley Mall in that same vicinity. The highway improved travel between the cities of the region and brought a wider labor pool accessible to local employers. U.S. 22 was a direct link to New Jersey and New York City. With the completion of Pa. 309 in 1958 and Pa. 33 in 1973 (both connecting to U.S. 22), inter-regional transportation was improved to the markets of suburban Philadelphia and New England ports. With immediate access to U.S. 22, the ABE Airport (opened in 1929) grew to a regional-scale facility. A modern terminal was built in 1975, and International Full-Service Port of Entry status was conferred in 1985 by the U.S. Customs Service. Passenger traffic continues to grow. The continuing dispersal of the regional population to suburban and rural areas and the reliance upon automobiles has resulted in the decline in use of mass transit (the public bus system) and the discontinuation of passenger rail service connecting the region to New York and Philadelphia. In 1976, Conrail took over the rail freight service in the area. While a major east-west switching yard is located in Allentown and some local industries are still served by rail, numerous lines have been abandoned. The completion of I-78 in 1989 facilitated motor freight service to the region. The late 1960’s and the 1970’s were periods of rapid suburban industrial construction. In 1966, the Lehigh County Authority was established to plan the provision of sewer and water service in western parts of the Lehigh Valley; by 1971 the first interceptor sewer had been built to serve industrial plants such as Kraft Foods and Schaefer (now Guinness) Brewing Company and the Iron Run Industrial Park. The establishment of suburban industrial parks drew some companies

Comprehensive Economic Development Strategy Page 24

away from their urban locations, such as Binney & Smith, Inc., Victaulic Co. of America and James River Dixie-Northern Inc., which have relocated from close-in sites to Easton to the Forks Township industrial area. Before 1970, office space construction was slow in the suburbs. During the 1975-1990 period, most office space was built in the suburbs. Suburban industrial parks attracted offices of a number of major insurance companies. General purpose, luxury office space was built to meet the needs of expanding industries such as health services, utilities and business services. Expansion of office space during this period was in response to the shift from a manufacturing-based economy to a service-based economy. In addition, in the 1975-1990 period, government programs began to encourage the redevelopment of older areas (the cities and boroughs): Allentown, Bethlehem and Easton experienced some commercial and residential renovation and construction projects. Reuse of former factory buildings (e.g. for apartment buildings) in the boroughs has occurred and the older housing stock is becoming attractive to renovators or young persons unable to afford suburban housing costs. The national recession of 1980-1981 lingered in its effects in the Lehigh Valley through mid-decade. People began to realize that a new diverse regional economy must be built to shelter citizens from the high unemployment caused by cycles in demand for durable products such as steel and transportation equipment. In the early 1980’s, numerous economic development organizations were created, including the Northampton County Development Corporation, the three cities’ economic development corporations, the Ben Franklin Partnership, the Lehigh Valley Partnership, and the Lehigh Valley Convention and Visitor’s Bureau. Their roles differ, but they share the goal of a healthy future Lehigh Valley economy. Immigration of new residents and businesses from New Jersey started in the early 1980’s and continues to be the primary population growth force in the early 2000’s. The 1980’s real estate boom quickly escalated both land and housing values in the Lehigh Valley. During the 1980’s and 1990’s, Lehigh and Northampton Counties concentrated their development efforts on highway improvements such as the widening of Route 512 and the completion of the three-mile link in Route 33 between Route 22 and I-78, relocation of Route 222 in Lehigh County and improved road access to the airport. In Northampton County the major business and industrial growth corridor of the future is expected to be along Route 33. The Route 33 link was completed in 2002. In Lehigh County, it is expected that development will continue at a rapid rate in the Route 222 and Route 100 corridors coupled with the Route 222 bypass, scheduled for completion in 2004. In the mid to late 1990’s there was a resurgence of interest in renewal of the downtown areas of Allentown, Bethlehem and Easton. All three cities are making progress. Easton’s Two Rivers Landing/Crayola Factory has sparked new business activity in downtown Easton. Business and investment is also expanding in downtown Bethlehem as a result of tourism, successful historic preservation activities and renewal of numerous properties in and around the Downtown. Allentown is also making progress in the downtown renewal activity. The Hamilton Mall environment is being transformed with removal of the canopies, opening of the Lehigh County Government Center in the refurbished Leh’s building, development of Portland Place, refurbishment of Symphony Hall and redevelopment of the 9th and Hamilton site by PPL. In the late 1990’s, the Lehigh Valley Economic Development Corporation (LVEDC) was created to promote economic growth activities regionally. LVEDC has a vigorous marketing program that promotes Lehigh Valley interests nationally and internationally, LVEDC has also become the prime point of contact for the retention and attraction of business in the Lehigh Valley.

Comprehensive Economic Development Strategy Page 25

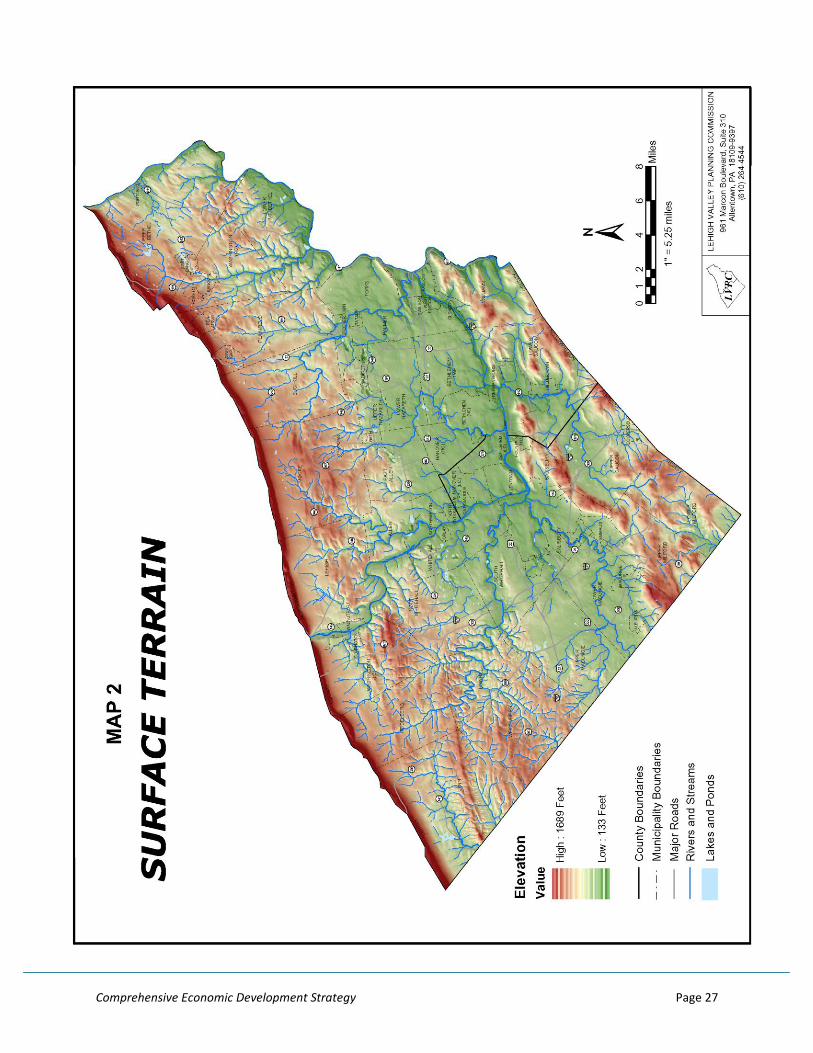

GEOGRAPHY Although there are numerous ways to describe the geography of the Lehigh Valley, from a local political, historic and cultural perspective the Lehigh Valley is mainly identified as the area bounded by Lehigh and Northampton Counties, Pennsylvania. The counties are situated in the east-central portion of Pennsylvania approximately 90 miles west of New York City and 60 miles north of Philadelphia. The two counties form the core of a metropolitan area defined by the Bureau of the Census as the Allentown-Bethlehem-Easton Metropolitan Statistical Area. The Lehigh-Northampton county area contains three cities, twenty-seven boroughs and thirty-two townships. The cities of Allentown, Bethlehem and Easton and the suburban fringe on their boundaries comprise a large share of the regional population. In 2000 seventy-seven percent of the population of the Lehigh Valley lived in the cities, boroughs and townships in the urban core. Most of the urban infrastructure (public sewer, water and major roads) in the region is located in these municipalities. Predominant geographic features include the Blue Mountain at an elevation of 1,700 feet separating the counties from Monroe and Carbon counties to the north, the South Mountain at an elevation of 1,000 feet which forms a scenic mountainous backdrop for Allentown, Bethlehem and Easton and separates the cities from the suburban areas to the south. The Lehigh River runs south from the Blue Mountain to Allentown and then east to the Delaware River at Easton. The Delaware River forms the eastern boundary of the region, and is the longest free-flowing river east of the Mississippi. It forms a natural border between Pennsylvania and New Jersey. The southern half of the valley is limestone area with gentle slopes. It contains most of the prime agricultural land of the region. The northern portion of the Lehigh Valley is underlain by shale, and is higher in elevation and rougher in terrain. It contains less productive agricultural land. South of the South Mountain, there is a complex pattern of valleys and hills with some prime agricultural lands interspersed with steeply sloping wooded areas.

Comprehensive Economic Development Strategy Page 26

Comprehensive Economic Development Strategy Page 27

Comprehensive Economic Development Strategy Page 28

ENVIRONMENT Two major rivers flow through the region, the Lehigh and the Delaware. The Coplay, Jordan and Little Lehigh creeks in the west, the Saucon Creek in the south, and the Monocacy, Bushkill and Martins creeks in the north, all drain into the Lehigh or Delaware rivers. The topography ranges from elevated regions along the northern edge of the area and along a line just south of the three cities to the relative flat, undulating terrain of the central portion of the Lehigh Valley. Elevations vary from 200 feet above mean sea level (MSL) along some parts of the Lehigh and Delaware rivers to greater than 1,695 feet MSL on the Blue Mountain and 1,042 feet MSL on South Mountain. There are over 1,000 wetland sites in the Lehigh Valley, with more than 300 in Upper Mount Bethel Township, Northampton County. Forty-six of the 62 municipalities in the Lehigh Valley are underlain entirely or in part by carbonate rock. The area enjoys a moderate climate, with an annual average temperature of 51 degrees Fahrenheit. Temperatures are rarely above 100 degrees or below 0 degrees Fahrenheit. Precipitation is generally ample and reliable, with destructive storms seldom occurring. The growing season is 170 to 185 days.

Comprehensive Economic Development Strategy Page 29

SECTION III: POPULATION, LABOR FORCE AND ECONOMY POPULATION TRENDS