2009 representation update

TRANSCRIPT

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 1/75

I.

2009 REPRESENTATION UPDATE

by

ROBERT E. McKENZIE, EA, ATTORNEY ©2009

ARNSTEIN & LEHR SUITE 1200

120 SOUTH RIVERSIDE PLAZAChicago, Illinois 60606

(312) 876-7100 [email protected]

http://www.mckenzielaw.com/

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 2/75

2009 IRS REPRESENTATION UPDATE© By: Robert E. McKenzie

1. A CHANGING IRS ........................................................................................................1More Compliance Centers to Cease Processing Returns:............................................1Shrinking IRS Workforce ................................................................................................1New IRS Commissioner ................................................................................................2

2. TAXPAYER ADVOCATE ..............................................................................................2National Taxpayer Advocate Releases Report To Congress ........................................ 2The Most Litigated Tax Issues ..................................................................................... 11

3. ENFORCEMENT ........................................................................................................ 13Highlights of 2008 Enforcement................................................................................... 13Individual Enforcement................................................................................................. 13Millionaires ................................................................................................................... 13

Businesses ................................................................................................................... 14Collection Enforcement................................................................................................ 14Electronic Filing IRS Webpage .................................................................................... 14State Information Sharing ............................................................................................ 19Federal Tax Returns and Return Information.............................................................. 19Return Information ........................................................................................................19IRS Study Provides Tax Gap Estimate ........................................................................ 20Sources of Misreporting ............................................................................................... 20Understanding the Tax Gap ......................................................................................... 20Components of the Tax Gap ........................................................................................ 20Underreporting ............................................................................................................. 20

Underreporting Is Largest Component......................................................................... 21Noncompliance Rising ................................................................................................. 21Areas Where Compliance Has Decreased .................................................................. 21Areas With Improved Compliance ............................................................................... 22Businesses More Likely to Not Comply....................................................................... 22NRP Subchapter S Corporation Study Overview ........................................................ 222009 Budget................................................................................................................. 262009 Budget ................................................................................................................ 26Overview - Abusive Return Preparer ........................................................................... 27Audits of 30 Clients ...................................................................................................... 28

4. EXAMINATION ........................................................................................................... 29

Examination Reengineering ......................................................................................... 29The Dirty Dozen ........................................................................................................... 295. APPEALS .................................................................................................................... 32

Strategic Priorities:....................................................................................................... 32Campus Appeals Program ........................................................................................... 32OIC and TFRP Mediation and Arbitration .................................................................... 32Application Process ..................................................................................................... 33TFRP ............................................................................................................................ 33

i

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 3/75

6. USEFUL INFORMATION FOR PRACTITIONERS .................................................... 34Whistleblower Reforms ................................................................................................ 34Mortgage Relief Act...................................................................................................... 34Basis Reduction ........................................................................................................... 35Qualified Principal Residence Indebtedness ............................................................... 35

Misclassified Workers .................................................................................................. 35Misclassification ........................................................................................................... 35Recommendations ....................................................................................................... 36UBS Criminal Charges ................................................................................................. 36Agreement.................................................................................................................... 36Allegations .................................................................................................................... 36Prior Charges ............................................................................................................... 37Comments of Government Officials ............................................................................. 37Settlement Offer Unreported Offshore Income ........................................................... 37Highlights of the Offer. ................................................................................................ 37Penalties ....................................................................................................................... 38

Fully Cooperate ............................................................................................................ 38VITA Grant Program .................................................................................................... 38Identity Theft................................................................................................................. 39

7. COLLECTION ............................................................................................................. 42Taxpayer Advocate’s Report On Enforced Collection ................................................ 42Flawed Private Collection Ends ................................................................................... 42Help for People Who Owe Taxes ................................................................................. 43Flexibility ....................................................................................................................... 43Online Payment Agreement (OPA) ............................................................................. 44Guaranteed Availability of Installment Agreements .................................................... 45

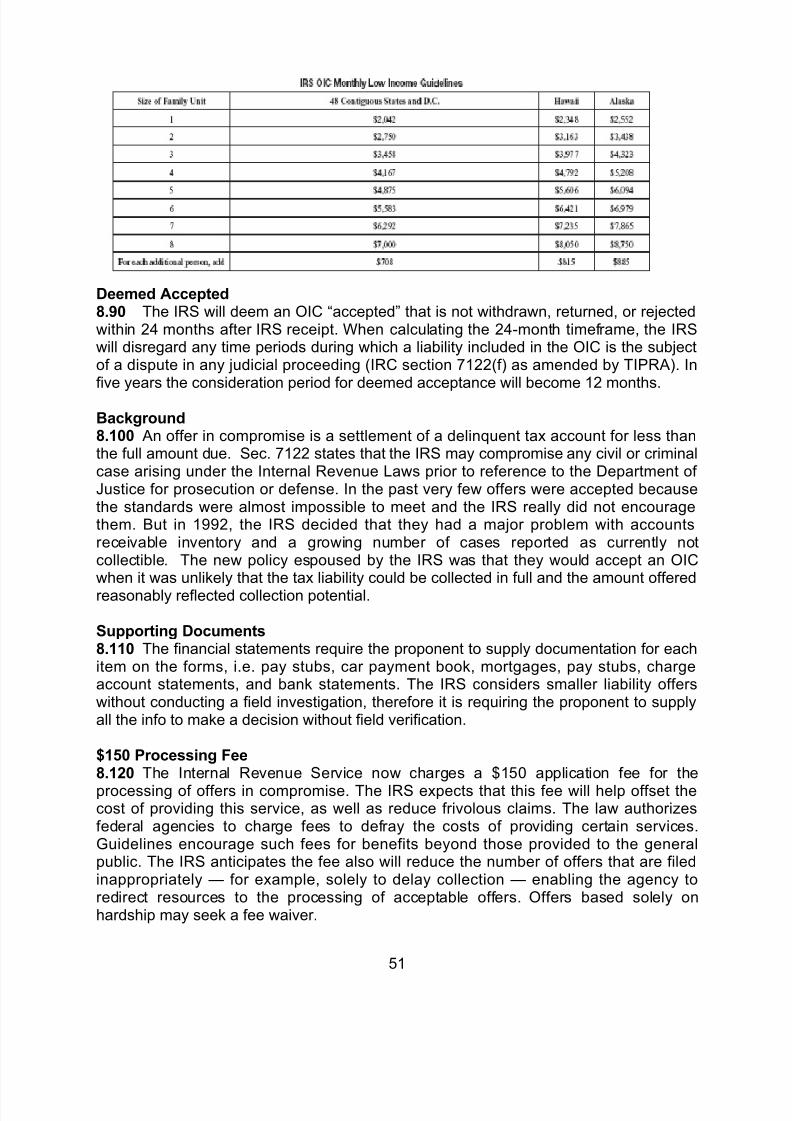

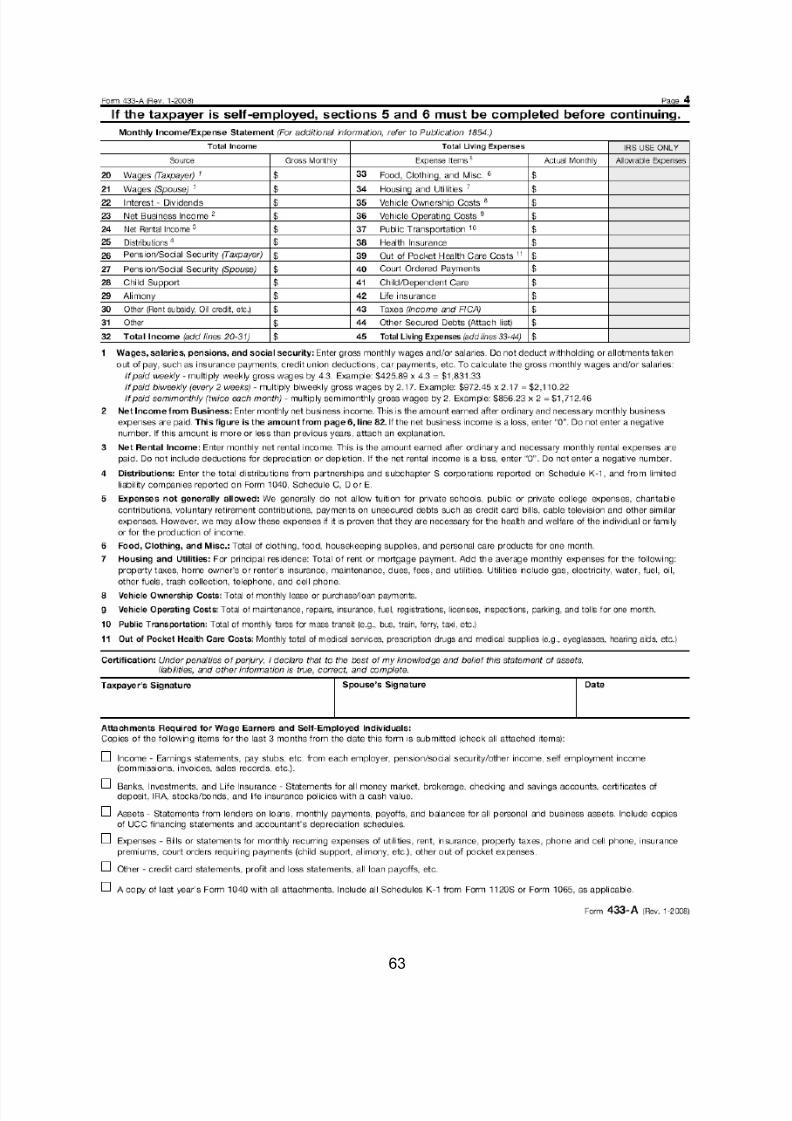

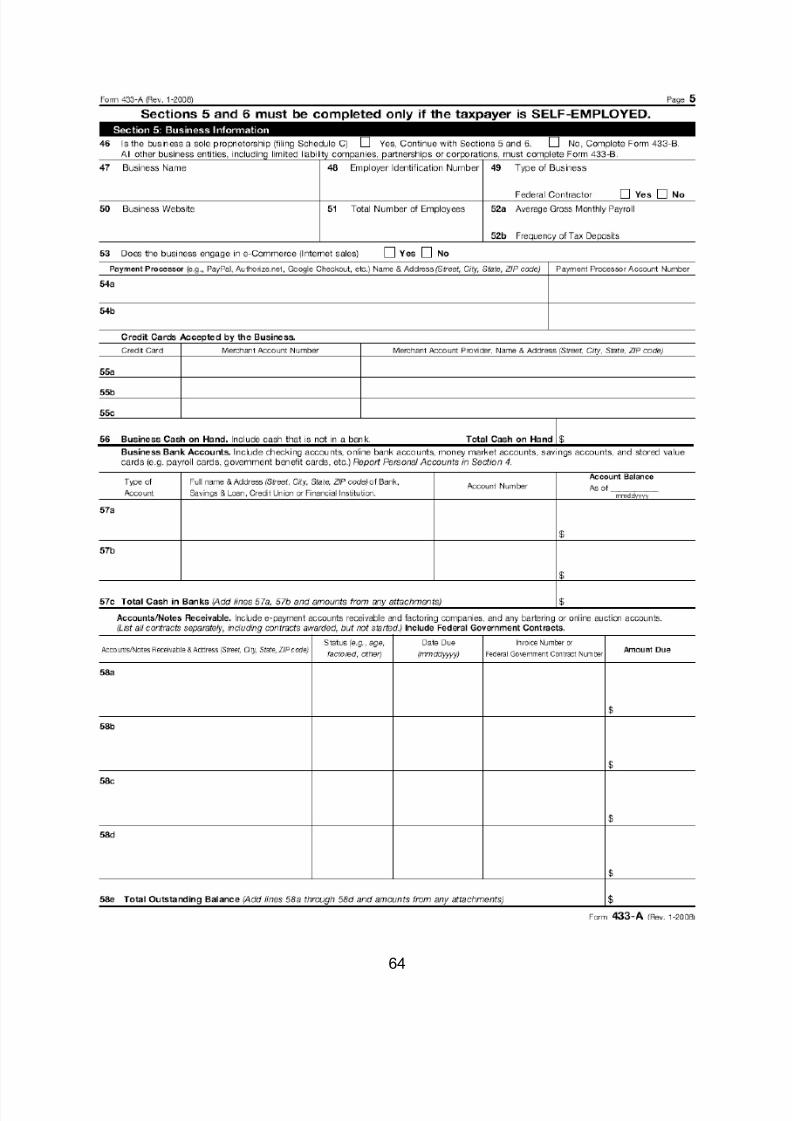

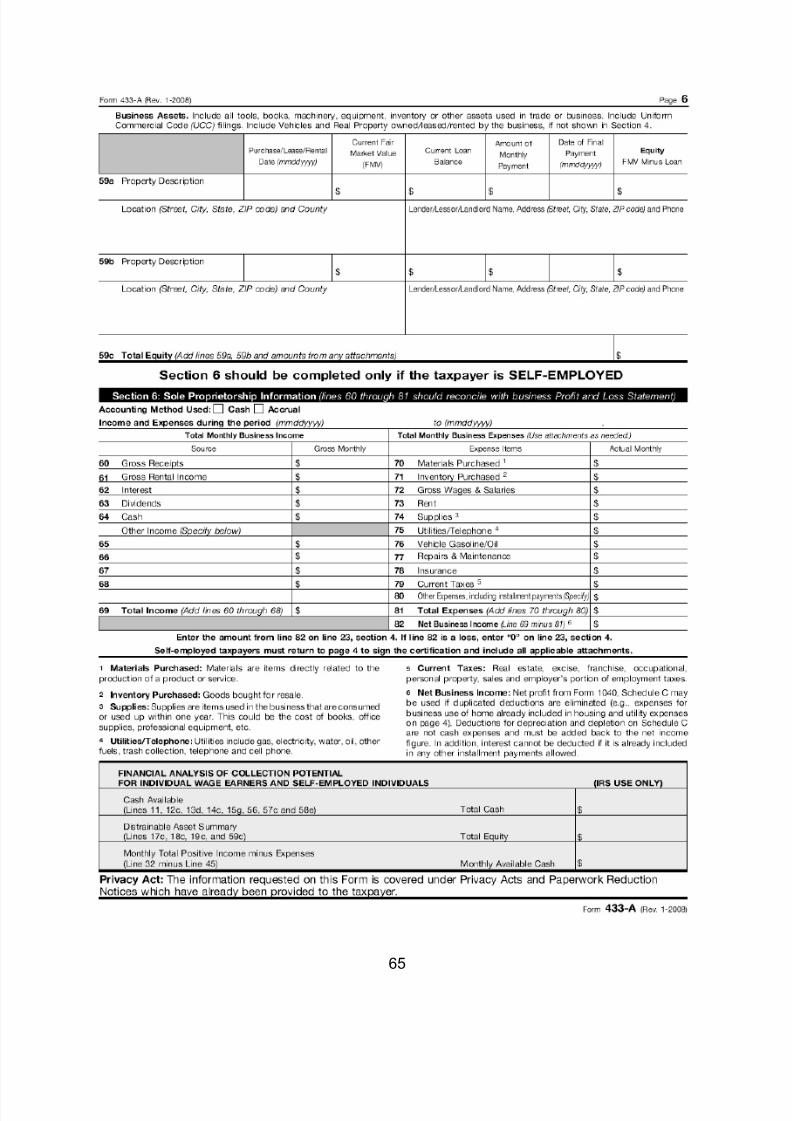

<$25,000 Liabilities ...................................................................................................... 45Form 433A .................................................................................................................... 45New more Onerous Allowable Expense Standards ..................................................... 45Five Year Test.............................................................................................................. 48

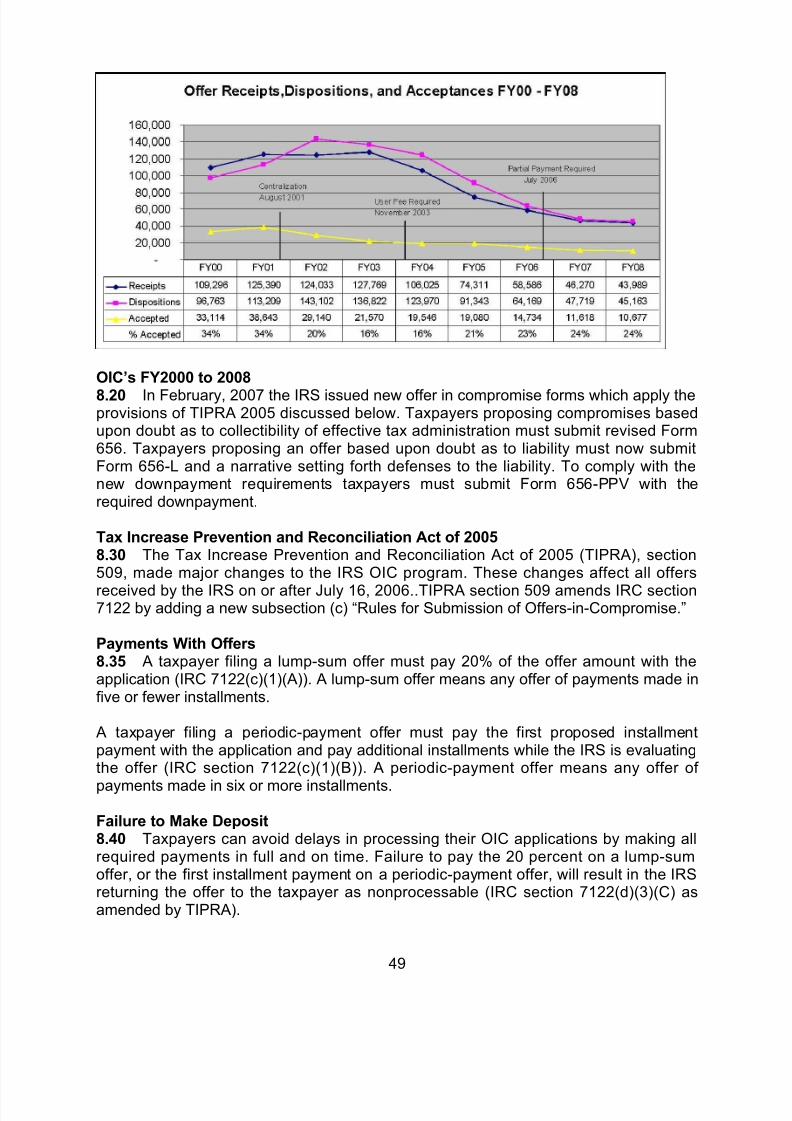

8. OFFER IN COMPROMISE ......................................................................................... 48Number of Offers .......................................................................................................... 48OIC’s FY2000 to 2008 .................................................................................................. 49Tax Increase Prevention and Reconciliation Act of 2005 ............................................ 49Payments With Offers .................................................................................................. 49Failure to Make Deposit............................................................................................... 49Not Refundable ............................................................................................................ 50Taxpayer Advocate Research ...................................................................................... 50Failure to Make Installment Payments ......................................................................... 50Low Income Taxpayers ................................................................................................ 50Deemed Accepted ........................................................................................................ 51Background .................................................................................................................. 51Supporting Documents ................................................................................................. 51$150 Processing Fee ................................................................................................... 51Determining Processability ........................................................................................... 52Full Pay Processing ......................................................................................................53

ii

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 4/75

Initial Review ................................................................................................................ 53Computation of Offer Amount...................................................................................... 53Cash Offer .................................................................................................................... 54Short-Term Deferred Payment Offer ............................................................................ 54Deferred Payment Offers ............................................................................................. 54

Corporate Trust Fund Liabilities ................................................................................... 55Pursuit of Officers After Compromise.......................................................................... 55Promote Effective Tax Administration .......................................................................... 55Encourage Compliance ................................................................................................ 55Only Available If There Is No Doubt As to Liability Or Collectibility ............................. 56Rules for Evaluating Offers to Promote Effective Tax Administration ......................... 56Factors ..........................................................................................................................56Undermine Compliance ................................................................................................ 56Exceptional Circumstances .......................................................................................... 56California ...................................................................................................................... 68..................................................................................................................................... 68

EXHIBITS 59-70

iii

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 5/75

2009 IRS REPRESENTATION UPDATE© By: Robert E. McKenzie

1. A CHANGING IRS

More Compliance Centers to Cease Processing Returns:1.10 Because of electronic filing the IRS is gradually eliminating its return processingcenters. The closure schedule is as follows.

• Philadelphia, Memphis & Holtsville no longer process

• Andover 10-09

• Atlanta 10-11

As of October, 2011 there will be 2 returns processing centers for business returns and3 returns processing centers for individual returns. Each of the remaining compliancecenters will continue performing correspondence audits and collection activities.

Shrinking IRS Workforce1.15 As a result of Congressional cuts in IRS budgets its workforce continued toshrink in 2008. It’s workforce has shrunk from about 100,000 in 2002 to about 90,000 in2008.

Table 30. Internal Revenue Service Personnel Summary and Type of Personnel, Fiscal Years2007 and 2008

Employment status, budget activity,

and selected personnel type

Average positions realized

[1]

Number of employees

at close of fiscal year

2007 2008 2007 2008

(1) (2) (3) (4)

Internal Revenue Service, total [r] 92,017 90,647 86,638 90,210

Selected personnel type:

Customer Service Representatives [r] 18,681 17,736 19,307 18,316

Revenue Agents [r] 12,816 12,587 13,026 12,951Seasonal employees [r] 9,861 10,025 4,525 8,422Revenue Officers [r] 5,663 5,493 5,468 5,481Tax Technicians [r] 3,110 1,496 1,506 1,538Special Agents [r] 2,677 2,590 2,683 2,617Attorneys [r] 1,415 1,397 1,455 1,429Appeals Officers [r] 775 768 798 781

1

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 6/75

New IRS Commissioner 1.20 In March, 2008 the Senate unanimously confirmed IRS Commissioner DouglasH. Shulman. He promised would work to ensure that the tax agency is fair, and hewould concentrate both on enforcement and service. "For the majority of Americanswho pay their taxes willingly and on time, there must be clear guidance, accessible

education and outstanding service," he said in a statement. "For taxpayers whointentionally evade paying taxes, there must be rigorous enforcement programs."Shulman has been vice chairman of the Financial Industry Regulatory Authority,previously known as the National Association of Securities Dealers. He also has servedon the bipartisan National Commission on Restructuring the Internal Revenue Service.

2. TAXPAYER ADVOCATE

National Taxpayer Advocate Releases Report To Congress2.10 In January 2009 National Taxpayer Advocate Nina E. Olson released a report toCongress. Internal Revenue Code (IRC) § 7803(c)(2)(B)(ii)(III) requires the National

Taxpayer Advocate to describe at least 20 of the most serious problems encountered bytaxpayers. Each of the most serious problems includes the National Taxpayer Advocate’s description of the problem, the IRS’s response, and the National Taxpayer Advocate’s final comments and recommendations. This format provides a clear pictureof which steps have been taken to address the most serious problems and whichadditional steps the National Taxpayer Advocate believes are required. The problemsdescribed in the report are as follows:

1. Complexity of the Tax Code. The largest source of compliance burdens for taxpayers is the complexity of the tax code. IRS data show that taxpayers andbusinesses spend 7.6 billion hours a year complying with tax-filing requirements.To place this in context, it would require 3.8 million full-time employees to work7.6 billion hours. In dollar terms, we estimate that taxpayers spend $193 billion ayear complying with income tax requirements, which amounts to 14 percent of aggregate income tax receipts. One count shows the number of words in the taxcode has reached 3.7 million, and over the past eight years, changes to the taxcode have been made at a rate of more than one a day – including more than500 changes in 2008 alone. All of this complexity imposes additional monetarycosts on taxpayers – about 60 percent of individual taxpayers pay practitioners toprepare their returns and an additional 22 percent purchase tax software to assistthem. Perhaps most troubling, tax law complexity leads to perverse results. Onthe one hand, taxpayers who honestly seek to comply with the law often makeinadvertent errors, causing them either to overpay their tax or to become subject

to IRS enforcement action for mistaken underpayments of tax. On the other hand, sophisticated taxpayers often find loopholes that enable them to reduce or eliminate their tax liabilities. The NTA recommends that Congress substantiallysimplify the tax code. To assist Congress in pursuing tax simplification, this reportincludes a series of recommendations, including recommendations to repeal theAlternative Minimum Tax, streamline education and retirement savings taxincentives, simplify the family status provisions of the Code, allow taxpayers toexclude modest amounts of canceled debts from income without having to make

2

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 7/75

an affirmative claim, reduce tax sunset and phaseout provisions, and revise theoverall penalty structure..

2. The IRS Needs to More Fully Consider the Impact of CollectionEnforcement Actions on Taxpayers Experiencing Economic Difficulties.When the IRS contemplates taking enforced collection action against a taxpayer,

both the tax code and IRS procedures require that IRS personnel consider whether the collection action will impose an economic hardship on the taxpayer.When the economy struggles and more taxpayers become unable to pay their tax liabilities, the importance of considering the impact of collection actions ontaxpayers and their families becomes critical. In addition, while levy and seizureauthority are important collection tools that allow the IRS to address seriousincidents of noncompliance, a review of IRS historical enforcement data suggeststhat expanded use – as opposed to judicious use – of these tools does notnecessarily translate into more tax dollars collected. For example, while thenumber of levies issued by the IRS increased by an astonishing 1,608 percentfrom fiscal year (FY) 2000 to FY 2007 – from 220,000 levies to about 3.76 million

– the increase in total collection yield during this period was slightly less than 45percent. To the contrary, historical enforcement data indicate that collectionalternatives may be more effective at collecting liabilities from taxpayers havingtrouble paying their tax debts. To more effectively deal with taxpayers in thesedifficult economic times, the NTA recommends that the IRS provide specificguidance requiring pre-decisional consideration of economic hardship in allInternal Revenue Manual sections related to collection enforcement andencourage greater use of collection payment alternatives such as offers incompromise and partial payment installment agreements where economichardship is present.

3. Understanding and Reporting the Tax Consequences of Cancellation of Debt Income. When a creditor writes off a debt, the tax code generally treats theamount of the canceled debt as taxable income to the debtor, but Congress hascarved out a number of exceptions. The rules that determine whether cancellation of debt income is includible in gross income are complex, andtaxpayers often do not receive reliable information about their tax reporting andpayment obligations. For example, the Mortgage Forgiveness Debt Relief Act of 2007 carved out an exception for debts canceled in the course of a homeforeclosure, but the exception only applies to the extent that the loan proceedswere used to acquire or improve a principal residence. It appears that mostsubprime borrowers use a portion of their loans for other purposes (e.g., to payoff car loans, credit card balances, student loans, or medical bills), and theexception does not apply to the extent loan proceeds were used for these “non-qualified” purposes. Moreover, taxpayers do not automatically receive the benefitof any exception. If they do not file Form 982, Reduction of Tax Attributes Due toDischarge of Indebtedness (and Section 1082 Basis Adjustment), with their taxreturns to claim an exclusion and adjust their tax attributes, the IRS will assumethe cancellation of debt is taxable (based on its receipt of a Form 1099-C,Cancellation of Debt, filed by the creditor). Even where Form 982 is properlyfiled, taxpayers who exclude canceled debt from income under the “insolvency”exception may receive IRS notices requesting additional documentation if they

3

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 8/75

do not also provide a statement of insolvency, a requirement that does notappear in any IRS forms or publications. The NTA recommends that the IRS takeseveral steps to address this problem, including developing an insolvencyworksheet that taxpayers can file with their returns and creating a centralized unitdedicated to handling cancellation of debt issues.

4. Employment Taxes. The NTA is concerned that IRS employment tax policiesmay overreach and undermine some of the important protections enacted in theTaxpayer Bill of Rights and the IRS Restructuring and Reform Act of 1998. Withan estimated $58 billion in unpaid employment taxes, it is clear that the IRS facesa significant noncompliance problem. At the same time, the overall employmenttax compliance rate is high – approximately 88 percent of all employment taxreturns are filed and fully paid. While the need to collect unpaid payroll taxes isobvious, the IRS should follow a tailored approach to address the problem,including applying different treatments to taxpayers based on their levels of andreasons for noncompliance, encouraging prospective voluntary compliance byhelping taxpayers who are attempting to follow complex rules and procedures,

concentrating sufficient resources on early intervention techniques to prevent theaccumulation of substantial employment tax liabilities, and building a localcompliance presence that balances enforcement with outreach and education.

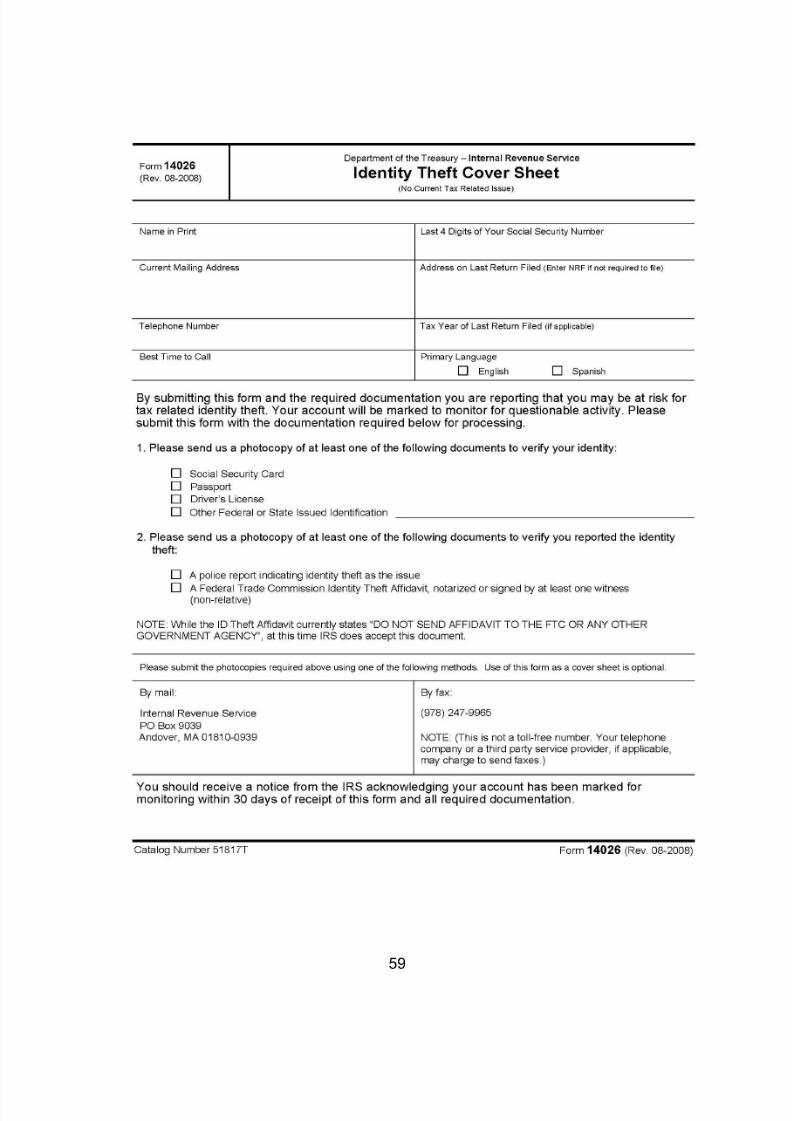

5. IRS Process Improvements to Assist Victims of Identity Theft. Identitytheft occurs when one person unlawfully uses another person’s personal data tocommit fraud or other crimes. In the past year, the IRS has improved its identitytheft process in a number of ways, including establishing an Identity ProtectionSpecialized Unit and a toll-free hotline for identity theft victims. These changes, if properly managed, should provide more assistance to victims of identity theft.The IRS recognizes identity theft as a serious problem and has agreed toaddress the concerns and recommendations that the NTA has previously raised.In light of the IRS’s agreement with our suggestions, the NTA makes no specificadditional recommendations at this time. However, she will continue to urge theIRS to implement the following actions: provide global account review andaccount monitoring (if necessary) for all identity theft victims; allow employeesthe discretion to deviate from established guidelines in accepting evidence of identity theft; and allow employees more latitude in determining the rightful owner of a disputed Social Security number.

Taxpayer Service Issues

6. Taxpayer Service: Bringing Service to the Taxpayer. Since announcing itsoriginal plan in 2001 to establish 676 Taxpayer Assistance Center (TAC) sites,the IRS has established only 401 TACs and just 55 percent of them are open 36to 40 hours per week. Further, 40 percent of taxpayers live more than a 30-minute drive from a TAC, and TACs are unable to handle many issues andquestions. Similarly, the Small Business/Self-Employed Division since 2001 hassharply reduced its planned education and outreach program for small businesstaxpayers. In both instances, the IRS has sought to meet taxpayer needs byincreasing Internet service. While that trend is generally positive, there remainsignificant numbers of taxpayers who do not have access to the Internet and

4

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 9/75

there are certain categories of service that are more effectively handled throughface-to-face interaction. The NTA recommends that the IRS collaborate with TASon all ongoing and new studies pertaining to taxpayer service, including theTaxpayer Assistance Blueprint for small business and self-employed taxpayerscurrently underway, and take steps to identify innovative approaches todelivering in-person assistance.

7. Navigating the IRS. The IRS employs more than 100,000 workers in 12 major business units in over 800 offices within and outside the United States.Taxpayers, practitioners, and even IRS employees have difficulty finding theappropriate office or employee to help them resolve tax problems. The IRS doesnot publish a topical or personnel directory that would assist taxpayers innavigating the agency. By comparison, this information is provided clearly on thewebsites of taxing authorities in other countries and U.S. states. The NTArecommends that the IRS take steps to address this problem, including revisingthe Internal Revenue Manual to direct IRS employees to accommodate taxpayer requests to speak to a particular employee, adding departmental phone numbers

to the topical index on IRS.gov, and considering the creation of a phone number staffed by operators who would obtain details about the taxpayer’s question or problem and direct the taxpayer to the function that can help.

8. IRS Handling of ITIN Applications Significantly Delays Taxpayer Returnsand Refunds. Any individual who must file a tax return but is not eligible toobtain a Social Security number must apply to the IRS for an Individual Taxpayer Identification Number (ITIN). With limited exceptions, ITIN applications must besubmitted with a tax return filed on paper. In 2005, the inability to receive an ITINbefore preparing and filing a paper tax return caused processing delays thataffected 280,000 refunds totaling over $500 million. In addition, the IRSrequirement for ITIN applicants to file paper returns is inconsistent with thecongressional mandate for the IRS to achieve an 80 percent e-file rate. The IRShas provided inadequate assistance and information to applicants, as evidencedby the high number of Incomplete and rejected applications, restricted telephoneaccess to ITIN personnel, and failure to expand the Certified Acceptance Agentprogram. The NTA recommends several actions for streamlining the ITINprocess, which include permitting individuals to submit an ITIN application prior to the filing season where the individuals can demonstrate an imminent need tofile a return, allowing new ITIN applicants to file returns electronically, andpromptly acknowledging all applicant requests for the return of originaldocuments.

9. Access to the IRS by Individual Taxpayers Located Outside the UnitedStates. Approximately five million American citizens living outside the countryand over a half million troops deployed overseas need a way to contact the IRSwhen they have inquiries about their accounts or the tax laws. These taxpayershave limited options for obtaining information, filing returns, and replying to IRSnotices and letters. There are only four IRS overseas customer service postsavailable to taxpayers with U.S. filing obligations, who are spread over 194countries and more than 60 territories. Those outside the United States generallyincur greater expenses, such as international telephone charges, transportation,

5

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 10/75

and carrier mailing costs, when trying to communicate with the IRS. Although theIRS has developed customer service initiatives as a part of its strategy for international tax administration, it does not provide enough resources to meet theneeds and preferences of taxpayers based outside the country. The NTA’srecommendations for improving customer service for overseas taxpayers includeopening toll-free international telephone lines and providing overseas taxpayers

with secure online access to their tax accounts.

Compliance Issues

10. Customer Service Within Compliance. Simply stated, the IRS gets what itmeasures. The IRS largely rates operational performance by using efficiencymeasures (e.g., cycle time, case closures, and average call time) instead of effectiveness measures (e.g., did the IRS’s actions achieve the desired voluntarycompliance results?). The 2008-2009 IRS Strategic Initiative includes the goal to“Improve service to make voluntary compliance easier.” Yet current measures donot promote customer service and may ultimately lead to noncompliant behavior

by taxpayers, because IRS business strategies and measures do not adequatelyemphasize a balanced approach between taxpayer service and enforcementwithin the IRS’s compliance organizations. The IRS has the opportunity toestablish taxpayer-centric measures that encompass effectiveness as well asefficiency components to accomplish this strategic goal. The NTA recommendsfour actions to address this problem, including creating an IRS CognitiveLearning Lab and making it possible for taxpayers to work with one employeefrom start to finish on a case.

11. Local Compliance Initiatives Have Great Potential But Face SignificantChallenges. Research suggests that concentrated examinations targeted at alocal business segment or industry have a greater “ripple effect” on voluntarycompliance by other taxpayers than seemingly random examinations.Compliance initiative projects (CIPs) allow local IRS employees to generate thisimpact by focusing on specific local compliance problems using examinations or “alternative treatments,” which may include outreach, education, form changes,regulatory changes, or even agreements with the states. The CIP process alsoenables employees from different IRS functions to work together, utilize localsources of information, and reach out to local organizations to addressnoncompliance at the local level. In addition, CIPs allow the IRS to learn aboutwhat works and what does not. The NTA is concerned that the IRS hasneglected this important program. She recommends that the IRS take steps torevitalize it, such as developing better measures for local CIPs, allocating moreresources to local CIPs, and making CIP reports more widely available topreserve the benefits of any lessons learned.

12. Customer Service Issues in the IRS’s Automated Collection System(ACS). ACS is a main component of the IRS’s collection process, sendingautomated collection notices to millions of taxpayers and employing numeroustelephone assistors to receive calls from these taxpayers. Although ACSgenerally receives relatively high customer satisfaction survey ratings andinternal quality assessments, TAS has received numerous complaints from tax

6

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 11/75

professionals and taxpayers that suggest the need for improvements. ACScustomers have raised concerns about extensive wait times, the inability to faxdocuments to employees, overly burdensome procedures, and generaldissatisfaction with the ACS process. Neither ACS’s customer satisfactionsurveys nor its internal quality reviews measure these important aspects of taxpayer service. The NTA has identified several steps the IRS can take to

improve processes that drive customer satisfaction, most importantly the need for the IRS to evaluate the entire customer experience with ACS instead of assessing only a “snapshot” in time.

13. The IRS Should Proactively Address Emerging Issues Such as ThoseArising From “Virtual Worlds.” By one estimate, about $1 billion in real dollarschanged hands in computer-based environments called “virtual worlds” in 2005.Over 16 million people are estimated to have active subscriptions to theseenvironments, many of which have their own virtual economies and currencies.However, IRS employees have been unable to respond to taxpayer inquiriesabout how to report transactions associated with them. Economic activities in

virtual worlds may present an emerging area of tax noncompliance, in partbecause the IRS has not provided guidance about whether and how taxpayersshould report such activities. To improve voluntary tax compliance, the NTArecommends that the IRS issue guidance addressing how taxpayers shouldreport economic activities in virtual worlds.

Examination Issues

14. Suitability of the Examination Process. Since 2000, the IRS hascontinuously increased the number of individual income tax return examinationsit conducts. The number more than doubled from 617,765 in FY 2000 to1,384,563 in FY 2007, with examinations completed by correspondenceaccounting for 83 percent of all individual taxpayer audits. Although taxpayersunderstandably do not like to be audited, the IRS should initially assume goodfaith on the part of taxpayers and avoid taking an unnecessarily adversarialapproach. The Internal Revenue Manual and IRS publications provideopportunities for the IRS to meet taxpayer needs and preferences throughout theexamination process, including allowing taxpayers to choose a method for conducting an examination (face-to-face versus correspondence), request atelephone discussion with the examiner, and even set up a payment agreementfor any taxes owed. Because the IRS often fails to meet taxpayer needs andpreferences due to limited resources or policy reasons, the resulting unsuitabilityof the examination process can lead to disparities in audit and customer satisfaction results, including tax assessments that sometimes reflect thetaxpayer’s inability to navigate the audit process rather than the amount trulyowed. The NTA recommends five actions to help the IRS address problems withthe suitability of the examination process, including directing its focussubstantially toward meeting taxpayer needs and preferences and immediatelyeliminating the so-called “combination letter” from the process.

15. The IRS Correspondence Examination Program Promotes PrematureNotices, Case Closures, and Assessments. In FY 2007, the IRS conducted 83

7

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 12/75

percent of all individual income tax examinations exclusively by mail in an effortto expand its audit coverage. The program as currently designed, however, isplagued by problems that increase taxpayer burden. These problems include apreoccupation with closing cases rather than working with taxpayers to resolveaudit issues and an automated process that causes perpetual delays inresponding to taxpayer correspondence. These issues lead to premature notices,

premature case closures, and premature assessments, all of which drivetaxpayers to TAS for help and generate needless re-work for IRS employees.The NTA urges the IRS to protect taxpayers by requiring managers andemployees to adhere to the agency’s longstanding audit quality standards inconducting correspondence examinations.

Tax Administration Issues

16. The Impact of IRS Centralization on Tax Administration. Over the years,the IRS has centralized many of its major operations and programs. Thiscentralization has significantly changed the organizational structure,

management, work processes, and the quality of interaction between the IRSand taxpayers. When carried out correctly, centralization can significantly reduceredundancies and increase effectiveness. However, if the IRS fails to consider the impact of centralization on taxpayer service and compliance, it may harmtaxpayers. The IRS needs to do a better job of measuring the downstreamconsequences to taxpayers, including the impact on taxpayer service andcompliance, when evaluating the costs and benefits of centralization. The NTArecommends that the IRS establish a standard matrix that defines the project,provides background information, sets forth objectives, establishes tangibleproducts, quantifies expected benefits, and identifies necessary resources. TheIRS should then use this standard project matrix to evaluate programs anddetermine whether the anticipated benefits of centralization have been realized.

17. Incorrect Examination Referrals and Prioritization Decisions CauseSubstantial Delays in Amended Return Processing for Individuals. Everyyear, more than three million taxpayers file amended returns for various reasons,including the complexity of the tax code, changes in their circumstances, late-year tax legislation, and incomplete or inaccurate tax preparation software. Manyof these taxpayers experience unnecessary burden and delays. A cooperativeIRS-TAS study of TAS amended return cases found the average taxpayer waited26 weeks for the amended return to be processed before contacting TAS for assistance. These delays stem from the IRS not meeting its own processingguidelines, unnecessary referrals for audits, and management decisions to de-emphasize processing so-called “duplicate filings,” which occur when more thanone Form 1040 is filed with the same name and Social Security number. TheNTA recommends that the IRS allow individual taxpayers to file amended returnselectronically to reduce errors and shorten processing times, eliminateunnecessary audit referrals, and create a special unit to resolve duplicate filingcases as a top priority.

18. Inadequate Files Management Burdens Taxpayers. From FY 2005through FY 2008, the IRS refunded over 40 percent (more than $3.7 million) of

8

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 13/75

the fees it collected for photocopies of taxpayers’ documents because it could notlocate the files the taxpayers needed. The IRS is required by law to efficientlymaintain and manage agency records, including electronic and paper files, asevidence of IRS policies, decisions, and operations. Both taxpayers and IRSemployees need prompt access to paper documents to resolve tax return issuesor verify taxpayer information, yet the IRS has failed to follow procedures and

implement safeguards for maintaining and managing paper files and records.This failure has contributed to complaints from taxpayers, practitioners, IRSemployees, and other stakeholders who experienced substantial delays or received the wrong taxpayer’s documents. Although control of the Files operationreverted back to the IRS in 2008 after being contracted out for the past twoyears, the transition has not resolved most of the associated problems. To further improve the Files operation, the NTA recommends the IRS take proactive stepsto develop a service-wide recordkeeping and paper-file management strategyand database, take steps to convert paper returns to an electronic format, andrevise relevant Internal Revenue Manual provisions to employ adequate qualitycontrol and specific timeliness measurements for expedited taxpayer files

requests.

19. The IRS Miscalculates Interest and Penalties But Fails to Correct TheseErrors Due to Restrictive Abatement Policies. A TAS study has found that theIRS is miscalculating the failure to pay penalty and could be negatively impactingabout two million taxpayer accounts annually. Moreover, the IRS’s manualcalculations of interest yields an accuracy rate of only 67.7 percent, which meansnearly one out of three restricted interest accounts are incorrectly computed. TheIRS is aware of, but has failed to correct, certain systemic problems that causepenalty and interest miscalculations. These incorrect calculations lead numeroustaxpayers to believe they have fully paid what the IRS says they owe, only toreceive subsequent bills for accruals of interest, penalties, or both. The IRSbears the cost of these inaccurate calculations, not only through rework byemployees but also by taxpayers’ reduced confidence in the IRS. The NTArecommends that the IRS consider allocating adequate resources towardplanning and programming to resolve common penalty and interest computationissues, revising pertinent Internal Revenue Manual sections so all taxpayers areentitled to accuracy reviews of interest and penalty calculations, and re-evaluating the overly complex restricted interest procedures to make certain thatall taxpayers receive accurate interest charges.

20. Inefficiencies in the Administration of the Combined Annual WageReporting Program Impose Substantial Burden on Employers and WasteIRS Resources. The Combined Annual Wage Reporting (CAWR) program isdesigned to ensure that employers accurately report annual wage data to the IRSand the Social Security Administration. If the IRS discovers a discrepancy in thewage and tax data reported by an employer, it issues a notice and requests thatthe employer provide information to resolve the discrepancy. However, theCAWR notices are not clearly written. As a result, employers are often unable toidentify the cause of the discrepancy and respond timely, which in turn may leadthe IRS to improperly impose penalties on the employers. From FY 2003 to FY2008, the IRS eventually abated 81 percent of the penalty dollars it previously

9

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 14/75

assessed, causing substantial rework for the IRS and needlessly burdeningemployers. The NTA recommends that the IRS provide specific information aboutthe wage reporting discrepancy on notices, include the phone number for a liveassistor in the CAWR unit on notices, and continuously train its employees aboutwhen it is appropriate to assess CAWR penalties.

Status Update

The IRS’s Private Debt Collection (PDC) Initiative I 21. s Failing In MostRespects. IRS data now shows that the IRS’s Collection function outperformsprivate collection agencies (PCAs) in almost every way, collecting three times asmuch as the PCAs and resolving more cases earlier in the process. Overall, thePCAs have only collected about four percent of the outstanding tax balancesassigned to them, bringing in less than $56 million in commissionable paymentson $1.46 billion of tax debt. The NTA has addressed a number of the PDCinitiative’s deficiencies in prior Annual Reports to Congress and testimony. Manyof these concerns remain while new ones have arisen. In addition, despite initial

expectations that the IRS could learn about state-of-the-art collection practices inprivate industry through its work with PCAs, the IRS has now acknowledged thatit has not been able to identify any “best practices” from the private debtcollection industry. The NTA remains concerned that there is an inherentlygreater risk to taxpayer compliance, taxpayer rights, and taxpayer privacy whentax collection is outsourced to private, for-profit businesses. Given this risk andthe PCAs’ unambiguous underperformance as compared with the IRS’s ownCollection function, the NTA continues to believe that the PDC program shouldbe terminated.

10

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 15/75

The Most Litigated Tax Issues2.20 IRC§7803(c)(2)(B)(ii)(X) requires the National Taxpayer Advocate to identify theten tax issues most often litigated in the federal courts and to classify those issues bythe category of taxpayer affected. The following is a table the most litigated asdetermined by TAS:

Gross Income 68 8 12% 13710

7%

Collection Due Process 104 8 8% 7510

13%

Summons Enforcement 108 1 1% 38 8 21%

Trade or Business Expense 7821

27% 3810

26%

Accuracy-Related Penalty 47 8 17% 40

1

7 43%

Civil Damages for Certain Unauthorized Collection 60 8 13% 18 1 6%

Failure to File and Estimated Tax Penalties 47 5 11% 19 3 16%

Joint and Several Liability 27 5 19% 23 7 30%Frivolous Issues Penalty (and analo-gous appellate-level sanctions)

45 8 18% 4 1 25%

Family Status Issues 33 2 6% 1 0 0%

Totals 61774

12% 39367

17%

11

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 16/75

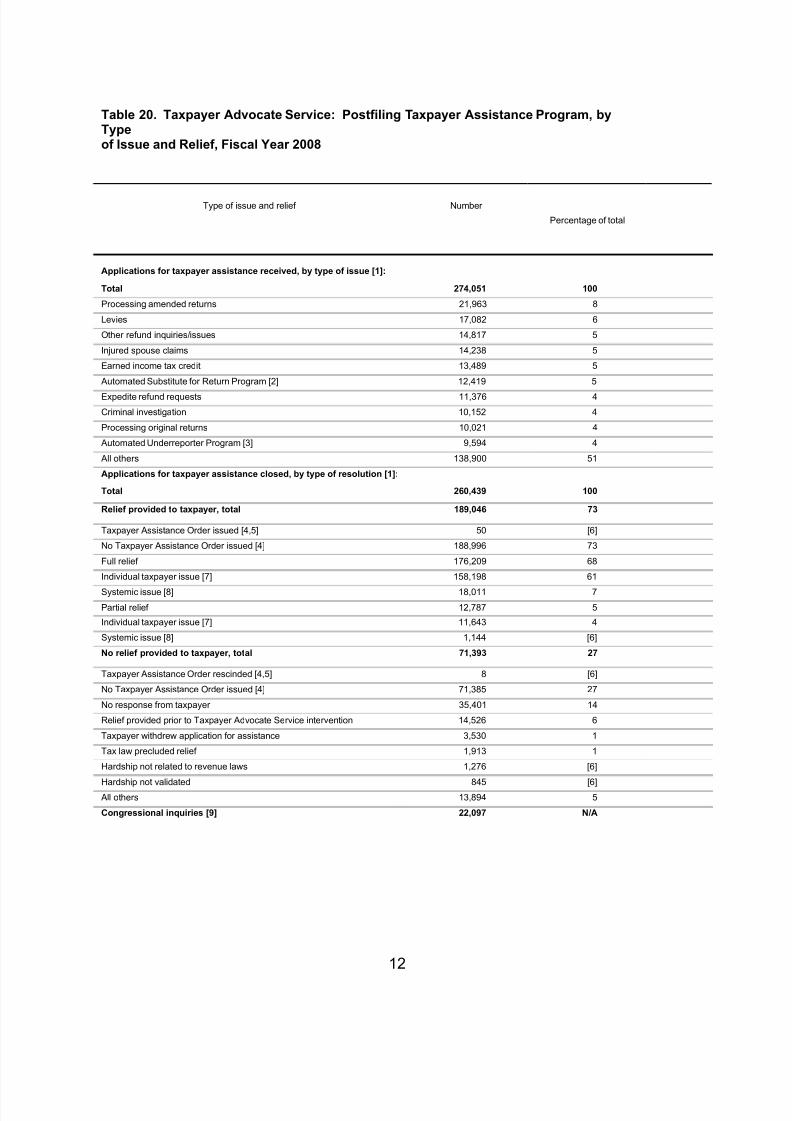

Table 20. Taxpayer Advocate Service: Postfiling Taxpayer Assistance Program, byTypeof Issue and Relief, Fiscal Year 2008

Type of issue and relief Number

Percentage of total

Applications for taxpayer assistance received, by type of issue [1]:

Total 274,051 100

Processing amended returns 21,963 8

Levies 17,082 6

Other refund inquiries/issues 14,817 5

Injured spouse claims 14,238 5

Earned income tax credit 13,489 5

Automated Substitute for Return Program [2] 12,419 5

Expedite refund requests 11,376 4

Criminal investigation 10,152 4

Processing original returns 10,021 4

Automated Underreporter Program [3] 9,594 4

All others 138,900 51

Applications for taxpayer assistance closed, by type of resolution [1]:

Total 260,439 100

Relief provided to taxpayer, total 189,046 73

Taxpayer Assistance Order issued [4,5] 50 [6]

No Taxpayer Assistance Order issued [4] 188,996 73

Full relief 176,209 68

Individual taxpayer issue [7] 158,198 61

Systemic issue [8] 18,011 7

Partial relief 12,787 5

Individual taxpayer issue [7] 11,643 4

Systemic issue [8] 1,144 [6]

No relief provided to taxpayer, total 71,393 27

Taxpayer Assistance Order rescinded [4,5] 8 [6]

No Taxpayer Assistance Order issued [4] 71,385 27

No response from taxpayer 35,401 14

Relief provided prior to Taxpayer Advocate Service intervention 14,526 6

Taxpayer withdrew application for assistance 3,530 1

Tax law precluded relief 1,913 1

Hardship not related to revenue laws 1,276 [6]

Hardship not validated 845 [6]All others 13,894 5

Congressional inquiries [9] 22,097 N/A

12

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 17/75

3. ENFORCEMENT

Highlights of 2008 Enforcement3.10 The IRS continues increase its enforcement activities. he IRS enforcementefforts increased again in fiscal year 2007. For instance, during 2007 the IRS audited 84percent more returns of individuals with incomes of $1 million or more than during 2006.Overall, enforcement revenue reached $59.2 billion, up from $48.7 billion in 2006 andnearly $34.1 billion in 2002. IRS collected $56.4 billion in enforcement revenue in 2008,down $2.8 million from 2007, Stiff said. She said 2007 was a record-breaking year for enforcement and saw some anomalies that did not repeat themselves in 2008, such as

a few large corporate closures and cases closed out during tax shelter inventories. Auditenforcement revenue decreased from $23.8 billion to $20.6 billion; and Collectionenforcement revenue decreased slightly from $31.8 billion to $31.1 billion

Individual Enforcement3.20 The number of audits of individual returns increased slightly in 2008. Those whoearned less than $200,000 had about a 1 percent chance of being audited. Those withincomes of $200,000 and more had about a 3 percent chance of being audited.

Millionaires3.30 Meanwhile, taxpayers with incomes of more than $1 million had a 5.6 percent

chance of being audited, a drop from 6.8 percent the year before. The number of auditsfor millionaires dropped even though their ranks increased by nearly 54,000.

“We essentially audited as many millionaires as in the previous year, but there weremore returns,” said Terry Lemons, an I.R.S. spokesman. The I.R.S. said it audited justover 23,000 returns of the nearly 340,000 filed by millionaires in 2007. That compareswith just over 21,800 returns filed by 398,000 millionaires in 2008.

13

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 18/75

The income of the 400 wealthiest Americans swelled in 2006, to an average of $263million, according to I.R.S. data. Since 1996, this group’s share of the nation’s totalwealth has nearly doubled to more than 22 percent.

Businesses3.40 On the business front, the overall number of audits rose slightly, but dropped as

a percentage of businesses that submitted a tax return. More emphasis was placed onmedium and large corporations, as audit rates increased slightly for those companieswith more than $50 million in assets and dropped slightly for those with less than $50million in assets. According to 2008 IRS enforcement data released by the IRS audited15.3% of returns of corporations with assets of $10 million or more. That is the lowestaudit coverage level since 2003 and down from a 20% coverage rate in 2005.

The tax audit rates of the largest companies are less than half what they were 20 yearsago while more small and mid-size businesses are coming under scrutiny, according toan organization that monitors the Internal Revenue Service. The Syracuse University-based Transactional Records Access Clearinghouse has described a "historic collapse"

in audits for corporations holding assets of $250 million or more. About 26 percent of them were audited in the 2007 budget year compared with 34 percent in 2006 and 43percent in 2005.

Collection Enforcement3.50 Overall, some of our most common enforcement tools at the IRS also showedincreases:

The IRS filed 2.6 million levies in 2008 and 3.8 million in 2007. It filed 683,659liens in 2007 and 768,168 liens during 2008, a substantial increase from fiveyears earlier.

Electronic Filing IRS Webpage3.60 More taxpayers chose to file electronically in 2008 than during the prior year, with58 percent of individual tax filers choosing to e-file in 2008, up from 57 percent in 2007.More people visited the IRS internet site, IRS.gov. The IRS site was accessed morethan 217 million times in 2007 and 347 million times in 2008.

14

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 19/75

15

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 20/75

16

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 21/75

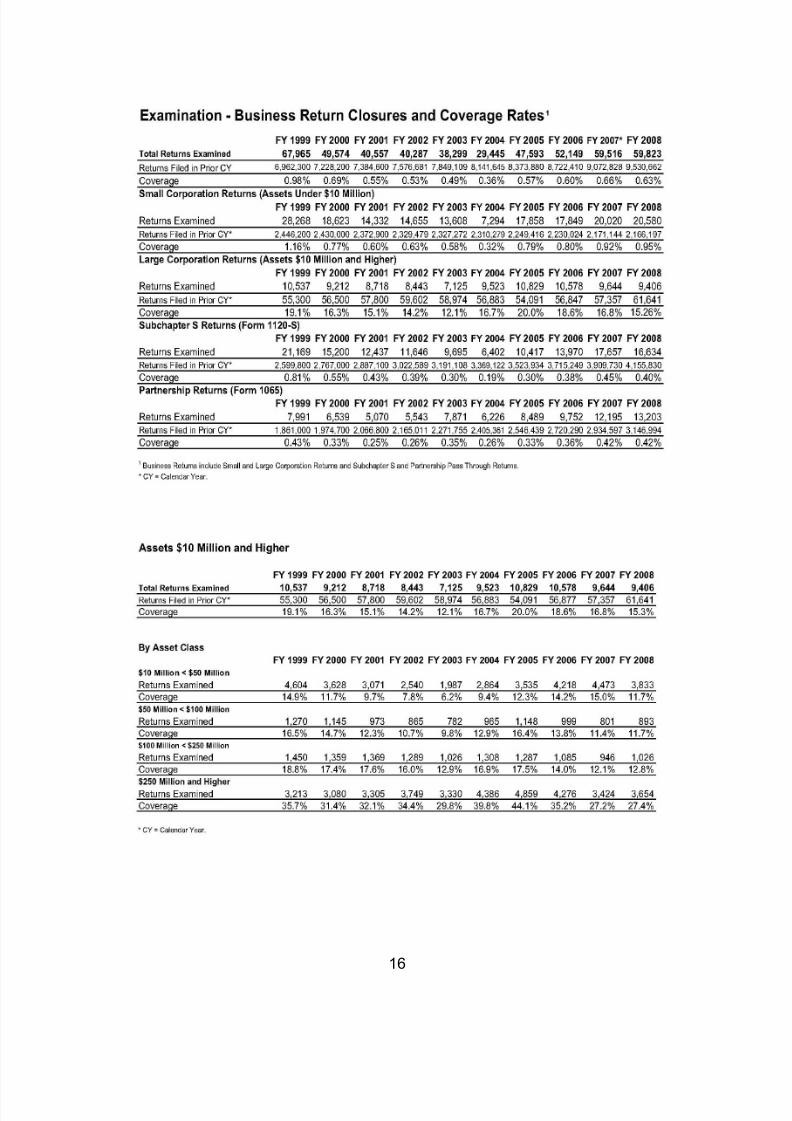

United States, totalTaxable returns: u Individual income tax

w Returns with total

Table 9a. Exami

Examination, by

17

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 22/75

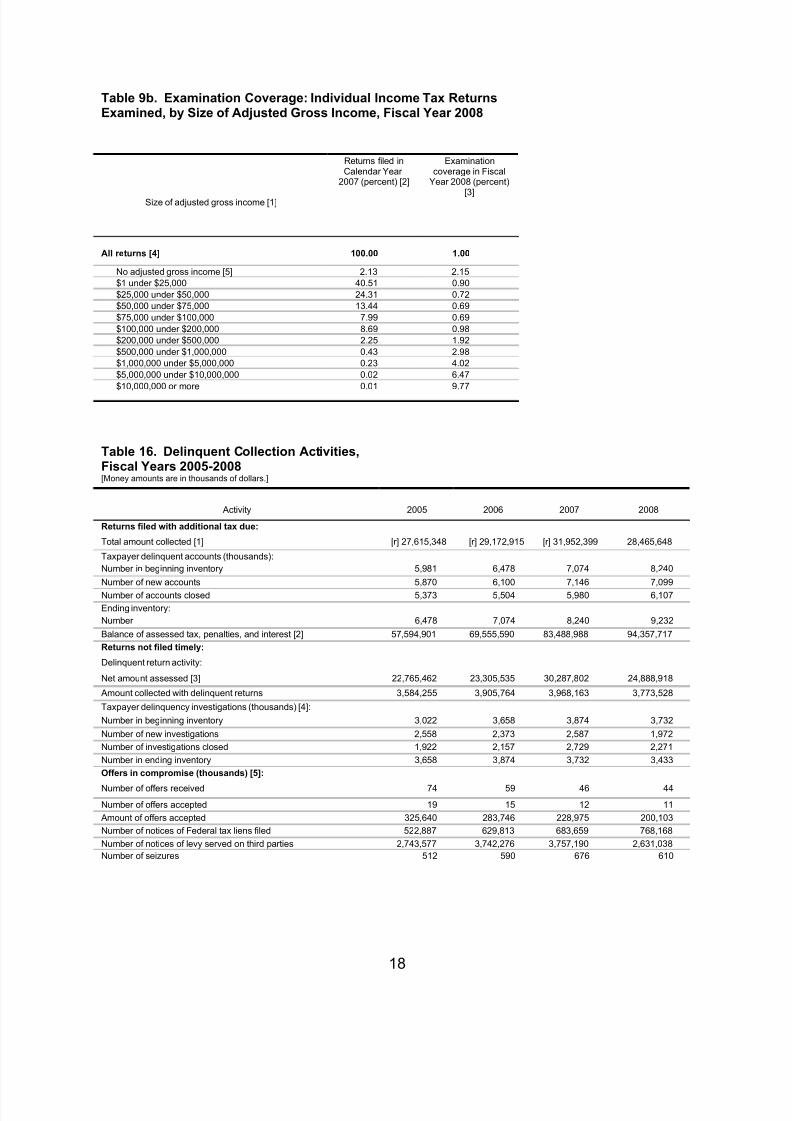

Table 9b. Examination Coverage: Individual Income Tax ReturnsExamined, by Size of Adjusted Gross Income, Fiscal Year 2008

Returns filed inCalendar Year

2007 (percent) [2]

Examinationcoverage in Fiscal

Year 2008 (percent)

[3]Size of adjusted gross income [1]

All returns [4] 100.00 1.00

No adjusted gross income [5] 2.13 2.15

$1 under $25,000 40.51 0.90

$25,000 under $50,000 24.31 0.72

$50,000 under $75,000 13.44 0.69

$75,000 under $100,000 7.99 0.69

$100,000 under $200,000 8.69 0.98

$200,000 under $500,000 2.25 1.92

$500,000 under $1,000,000 0.43 2.98

$1,000,000 under $5,000,000 0.23 4.02

$5,000,000 under $10,000,000 0.02 6.47

$10,000,000 or more 0.01 9.77

Table 16. Delinquent Collection Activities,Fiscal Years 2005-2008[Money amounts are in thousands of dollars.]

Activity 2005 2006 2007 2008

Returns filed with additional tax due:

Total amount collected [1] [r] 27,615,348 [r] 29,172,915 [r] 31,952,399 28,465,648

Taxpayer delinquent accounts (thousands):

Number in beginning inventory 5,981 6,478 7,074 8,240

Number of new accounts 5,870 6,100 7,146 7,099

Number of accounts closed 5,373 5,504 5,980 6,107

Ending inventory:

Number 6,478 7,074 8,240 9,232

Balance of assessed tax, penalties, and interest [2] 57,594,901 69,555,590 83,488,988 94,357,717

Returns not filed timely:

Delinquent return activity:

Net amount assessed [3] 22,765,462 23,305,535 30,287,802 24,888,918

Amount collected with delinquent returns 3,584,255 3,905,764 3,968,163 3,773,528

Taxpayer delinquency investigations (thousands) [4]:

Number in beginning inventory 3,022 3,658 3,874 3,732

Number of new investigations 2,558 2,373 2,587 1,972

Number of investigations closed 1,922 2,157 2,729 2,271

Number in ending inventory 3,658 3,874 3,732 3,433

Offers in compromise (thousands) [5]:

Number of offers received 74 59 46 44

Number of offers accepted 19 15 12 11

Amount of offers accepted 325,640 283,746 228,975 200,103

Number of notices of Federal tax liens filed 522,887 629,813 683,659 768,168

Number of notices of levy served on third parties 2,743,577 3,742,276 3,757,190 2,631,038

Number of seizures 512 590 676 610

18

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 23/75

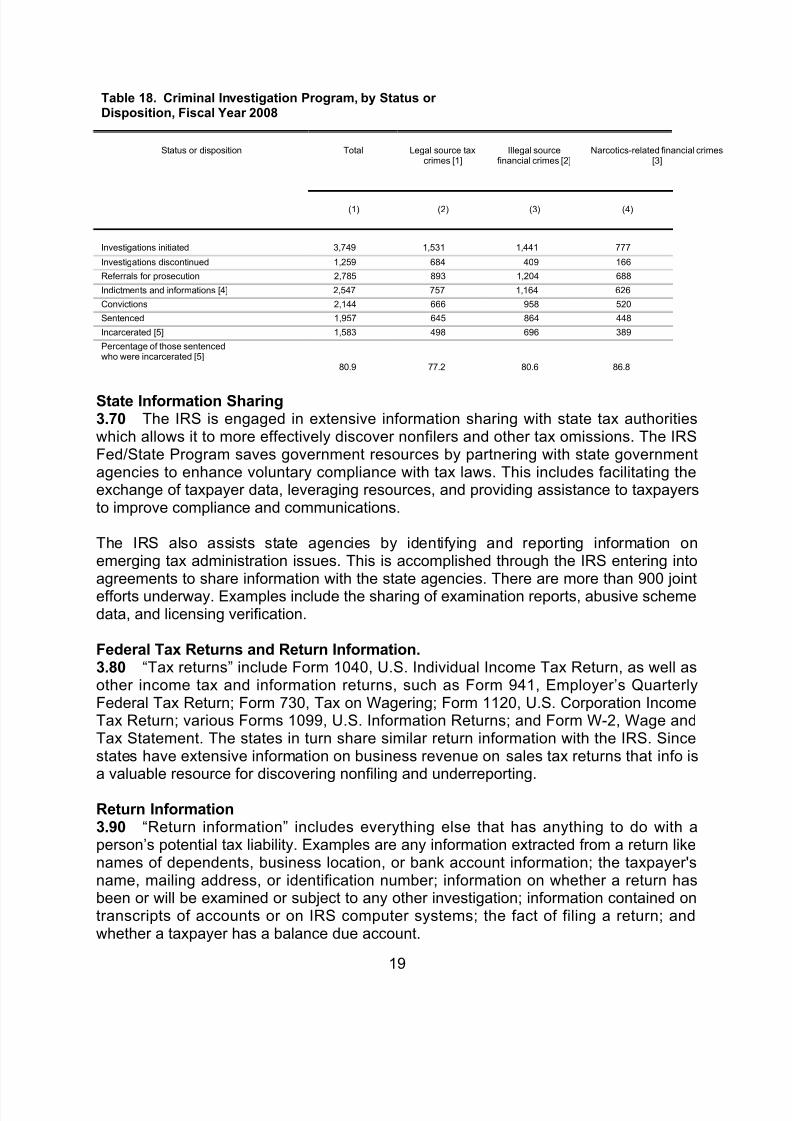

Table 18. Criminal Investigation Program, by Status or Disposition, Fiscal Year 2008

Status or disposition Total Legal source taxcrimes [1]

Illegal sourcefinancial crimes [2]

Narcotics-related financial crimes[3]

(1) (2) (3) (4)

Investigations initiated 3,749 1,531 1,441 777

Investigations discontinued 1,259 684 409 166

Referrals for prosecution 2,785 893 1,204 688

Indictments and informations [4] 2,547 757 1,164 626

Convictions 2,144 666 958 520

Sentenced 1,957 645 864 448

Incarcerated [5] 1,583 498 696 389

Percentage of those sentencedwho were incarcerated [5]

80.9 77.2 80.6 86.8

State Information Sharing3.70 The IRS is engaged in extensive information sharing with state tax authoritieswhich allows it to more effectively discover nonfilers and other tax omissions. The IRSFed/State Program saves government resources by partnering with state governmentagencies to enhance voluntary compliance with tax laws. This includes facilitating theexchange of taxpayer data, leveraging resources, and providing assistance to taxpayersto improve compliance and communications.

The IRS also assists state agencies by identifying and reporting information onemerging tax administration issues. This is accomplished through the IRS entering intoagreements to share information with the state agencies. There are more than 900 jointefforts underway. Examples include the sharing of examination reports, abusive schemedata, and licensing verification.

Federal Tax Returns and Return Information.3.80 “Tax returns” include Form 1040, U.S. Individual Income Tax Return, as well asother income tax and information returns, such as Form 941, Employer’s QuarterlyFederal Tax Return; Form 730, Tax on Wagering; Form 1120, U.S. Corporation IncomeTax Return; various Forms 1099, U.S. Information Returns; and Form W-2, Wage andTax Statement. The states in turn share similar return information with the IRS. Sincestates have extensive information on business revenue on sales tax returns that info isa valuable resource for discovering nonfiling and underreporting.

Return Information3.90 “Return information” includes everything else that has anything to do with aperson’s potential tax liability. Examples are any information extracted from a return likenames of dependents, business location, or bank account information; the taxpayer'sname, mailing address, or identification number; information on whether a return hasbeen or will be examined or subject to any other investigation; information contained ontranscripts of accounts or on IRS computer systems; the fact of filing a return; andwhether a taxpayer has a balance due account.

19

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 24/75

IRS Study Provides Tax Gap Estimate3.100 Internal Revenue Service officials have announced that they have updated their estimates of the Tax Year 2001 tax gap based on the National Research Program(NRP). The updated estimate of the overall gross tax gap for Tax Year 2001 – thedifference between what taxpayers should have paid and what they actually paid on a

timely basis – comes to $345 billion. This figure falls at the high end of the range of $312 billion to $353 billion per year, an estimate released in March, 2005.

Sources of Misreporting3.110 Though the net misreporting percentage varies by category of income, therates reflect that compliance is highest where there is third-party reporting or withholding. Simply stated, compliance is highest where there is third-partyreporting.

For example, one percent of all wage, salary, and tip income ismisreported, contributing an estimated $10 billion to the tax gap. Incontrast, nonfarm sole proprietor income, which is reported on a ScheduleC and is subject to little third-party reporting or withholding, has a netmisreporting percentage of 57 percent, contributing about $68 billion to thetax gap.

Understanding the Tax Gap3.120 The Internal Revenue Service developed the concept of the tax gap as a way togauge taxpayers’ compliance with their federal tax obligations. The tax gap measuresthe extent to which taxpayers do not file their tax returns and pay the correct tax ontime.

Components of the Tax Gap3.130 The tax gap can be divided into three components:

• nonfiling,

• underreporting and

• underpayment.

Underreporting3.140 Of these three components, underreporting of income tax, employment taxes andother taxes represents about 80 percent of the tax gap. The single largest sub-component of underreporting involves individuals understating their incomes, taking

improper deductions, overstating business expenses

20

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 25/75

and erroneously claiming credits. Individual underreporting represents about half of thetotal tax gap. Individual income tax also accounts for about half of all tax liabilities.

Underreporting Is Largest Component3.150 Underreporting noncompliance is the largest component of the tax gap.Preliminary estimates show underreporting accounts for more than 80 percent of thetotal tax gap, with non-filing and underpayment at about 10 percent each. Individualincome tax is the single largest source of the annual tax gap, accounting for about two-thirds of the total. For individual underreporting, more than 80 percent comes fromunderstated income, not overstated deductions.

Noncompliance Rising3.160 Overall, the noncompliance rate is from 15 percent to 16.6 percent of the true taxliability. The old estimate, derived from compliance data for Tax Year 1988 and earlier,was 14.9 percent.

Areas Where Compliance Has Decreased3.170 Among the areas where taxpayer compliance appears to have worsened are:

• Reporting of net income from flow-through entities, such as partnerships and Scorporations

• Reporting of proprietor income and expenses, such as gross receipts, bad debtsand vehicle expenses

• Reporting of various types of deductions

21

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 26/75

Areas With Improved Compliance3.180 Among the areas where compliance seems to have improved is the reporting of farm income. Overall, compliance is highest where there is third-party reporting and/or withholding.

For example, most wages, salaries and tip compensation are reported byemployers to the IRS through Form W-2. Preliminary findings from theNRP indicate that less than 1.5 percent of this type of income ismisreported on individual returns. IRS researchers anticipate identifyingother specific areas of deterioration and improvement in the comingmonths as they complete the detailed analysis of the study’s data.

Tax Year 2001 Gross Tax Gap by Type of Tax and Type of Noncompliance (in $ billions

Type of Tax

Type of Noncompliance TOTAL

NonfilingGap

Underreporting Gap

Underpayment Gap*

Amount

PercentDistributio

n

Individual Income Tax

25 197 23.4 245 71.1%

Corporation Income Tax

# 30 2.3 32 9.3%

Employment Tax # 54 5.0 59 17.0%

Estate & Gift Tax 2 4 2.1 8 2.4%

Excise Tax # # 0.5 1 0.1%

TOTAL Percent

Distribution

27 7.8% 285 82.5% 33.3 9.7% 345

100.0%

Businesses More Likely to Not Comply.3.190 Most of the understated income comes from business activities, not wages or investment income. Compliance rates are highest where there is third-party reporting or withholding. Preliminary findings show less than 1.5 percent of wages and salaries aremisreported.

NRP Subchapter S Corporation Study Overview3.200 During 2007 & 2008 the IRS continued its NRP of S corporations. The study hasthe following elements:

• Random Sample consists of approximately 5,000 returns from SmallBusiness/Self-Employed (SB/SE) and Large & Mid-Size Business (LMSB)taxpayers covering two tax years, TY2003 and TY2004.

• The study follows the standard NRP methodology:

• Each tax year will have an examination cycle of approximately 24 months.

• The TY 2003 portion of the sample (1,200 returns) is complete, and these casesare now in the hands of Revenue Agents.

22

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 27/75

• NRP is selecting the TY 2004 (3,800 returns) portion of the sample. Expectresults by December 2008

Tax Year 2001 Gross Tax Gap by Type of Tax and IRS Operating Division (in $ billions)

Type of Tax

IRS Operating Division TOTAL

Wage &Invest-ment

Small Business / Self-Employed Large &

Mid-SizeBusines

Tax-Exempt& Gov’tEntities

TaxGap

Non-Compliance

RateIndi-

vidualsCorpor-ation

T o t a l

IndividualIncome Tax

50 195 N/A 195 N/A N/A 245 20.9%

CorporationIncome Tax *

N/A N/A 6 6 25 1 32 18.5%

Employment Tax 0 40 7 47 8 4 59 8.1%

S e l f -Employment

N/A 39 N/A 39 N/A N/A 39 51.9%

FICA andFUTA

0 1 7 8 8 4 20 3.0%

Estate & Gift Tax # 8 N/A 8 N/A N/A 8 22.9%

ExciseTax †

0 0 0 0 0 0 1

TOTAL GapPercent of Total

5 014.5%

24370.5%

144.0%

25774.5%

3 49.8%

41.2%

345100.0%

NoncomplianceRate

12.1% 27.1% 5.3% 22.3% 8.0% 3.4% 16.3%

* Unrelated Business Income Tax is shown as corporation income tax. † Includes

underpayment gap only.

# No estimate is available for this component.

Amounts may not add to totals due to rounding. Zeros indicate amounts less than $0.5 billion. See Figure 1 regardingreliability of estimates.

23

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 28/75

Tax Year 2001 Individual Income Tax Underreporting Gap and Net MisreportingPercentage (NMP) Associated with Income and Offset Line Items

Type of Income or OffsetUnderreporting

Gap ($B)

NetMisreporting

Percentage †Total Underreporting Gap 197 18%

Underreported Income 166 11%

Non-Business Income 56 4%

Wages, salaries, tips 10 1%

Interest income 2 4%

Dividend income 1 4%

State income tax refunds 1 12%

Alimony income * 7%

Pensions & annuities 4 4%

Unemployment compensation * 1 1 %

Social Security benefits 1 6%

Capital gains 11 12%

Form 4797 income 3 64%

Other income 23 64%

Business Income 109 43%

Non-farm proprietor income 68 57%

Farm income 6 72%

Rents & royalties 13 51%

Partnership, S-Corp,Estate & Trust, etc.

22 18%

Overreported Offsets to Income 15 4%

Adjustments -3 -21 %

SE Tax deduction§ -4 -51%

All other adjustments 1 6%

Deductions 14 5%

Exemptions 4 5%

Credits 17 26%

Net Math Errors (non-EITC) *

† The amount of income or offset misreported divided by the amount that should have been reported. The NRP contains an adjustmentfor income amounts that were underreported, but does not have a corresponding adjustment for offset amounts that were notclaimed.

* Less than $0.5 billion.

§ Taxpayers understate this adjustment because they understate their self-employment income and, thereby, their self-

employment tax. Therefore, the gap associated with this item is negative.

24

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 29/75

25

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 30/75

2009 Budget3.210 The Internal Revenue Service will hire more than 3,500 frontline enforcementemployees as it embarks on its largest hiring initiative in recent history, DeputyCommissioner for Services and Enforcement Linda E. Stiff said March 30. This number includes more than 2,000 new revenue agents and revenue officers, Stiff said during aluncheon at the Tax Executives Institute's 59th Midyear Conference. Several hundred of these new hires will be directed at large corporate compliance, and as many as 700 willbe hired to deal with international issues, she said.

The hiring push comes on the heels of the fiscal year 2009 omnibus bill, which contains$630 million above IRS's current funding level for it to address noncompliance throughimproved technology, collection efforts, and audits, Stiff said. The Obama administrationand the Treasury Department are strongly supporting IRS in its efforts to combatabuses in the international arena, Stiff said. IRS's strategy in this area includes anintegrated approach composed of separate yet complementary programs, such asinternational collaboration and information sharing, as well as information reporting andwithholding, she said.1

2009 Budget3.220 The FY 2009 President’s Budget for the IRS increased funding as part of astrategy to improve compliance by focusing on the following priorities:

• Improving voluntary compliance and reducing the tax gap by:

• Increasing front-line enforcement resources,

•

Improving taxpayer service options,

• Enhancing research, and

• Implementing legislative and regulatory changes.

• Maintaining balance between taxpayer service and enforcement.

• Investing in technology to improve infrastructure, modernize, and increase theproductivity of existing resources.

1 Mar. 31 -- BNA, Inc. Daily Tax Report

26

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 31/75

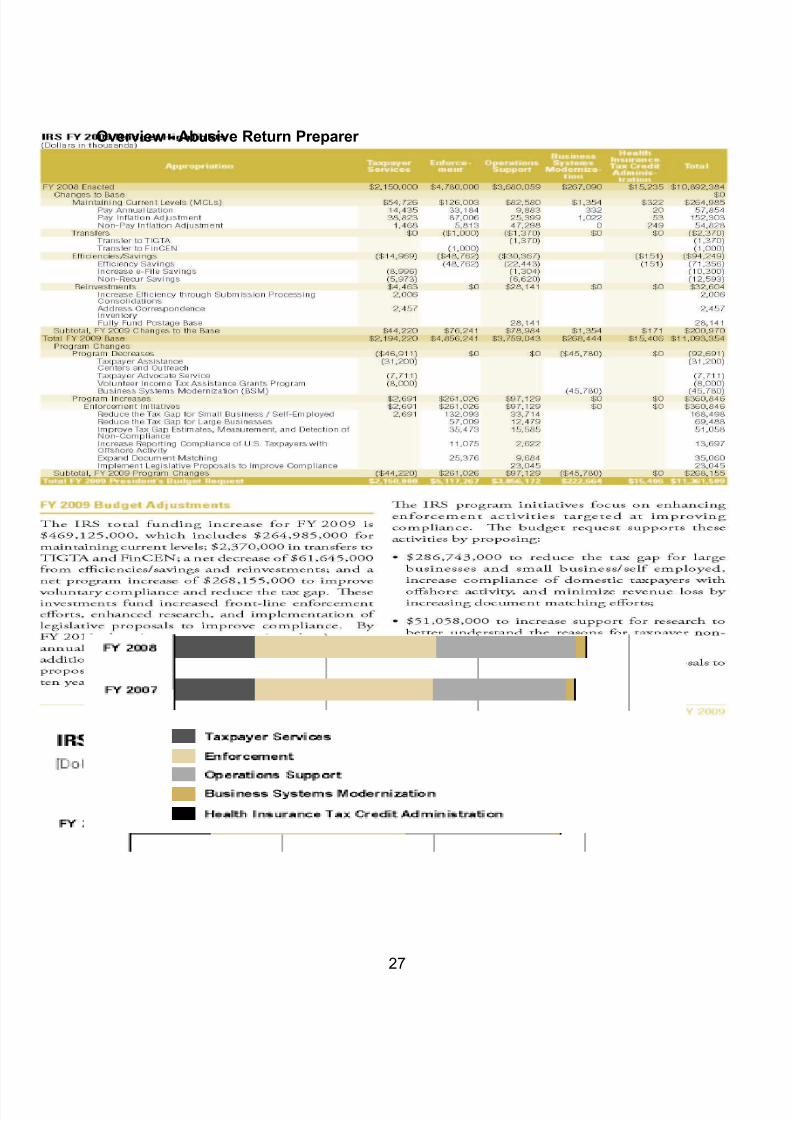

Overview - Abusive Return Preparer

27

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 32/75

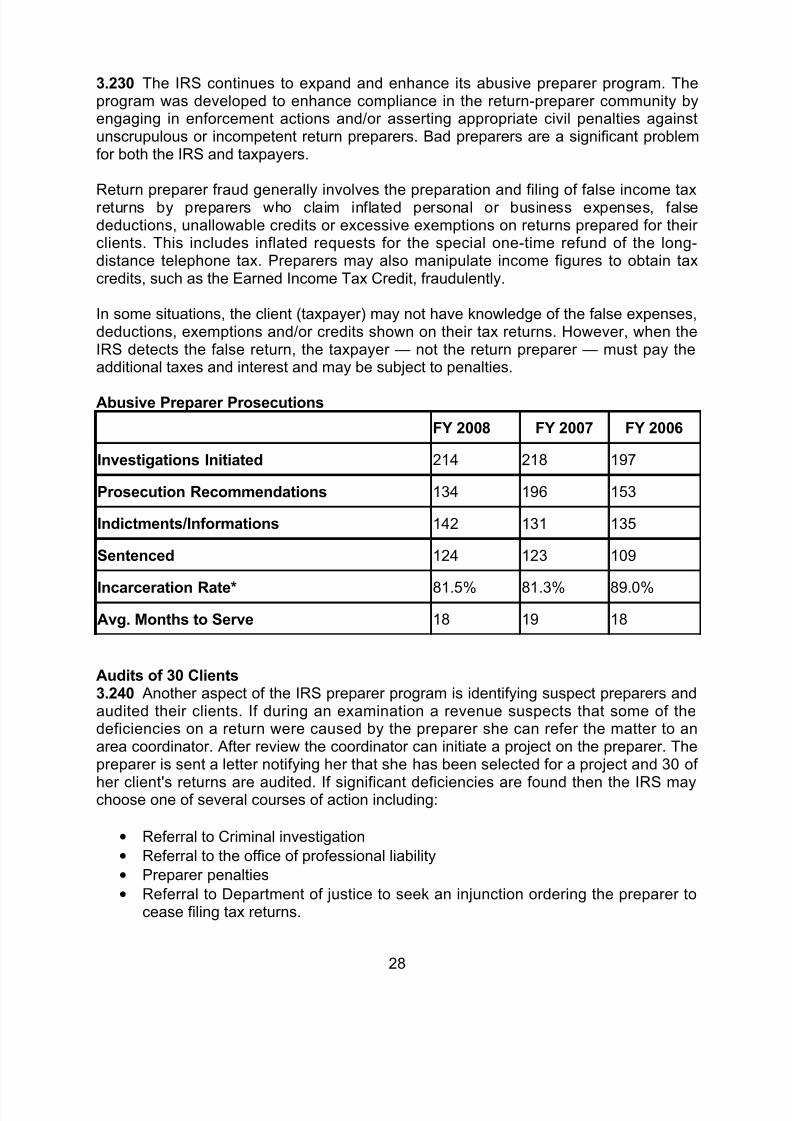

3.230 The IRS continues to expand and enhance its abusive preparer program. Theprogram was developed to enhance compliance in the return-preparer community byengaging in enforcement actions and/or asserting appropriate civil penalties againstunscrupulous or incompetent return preparers. Bad preparers are a significant problemfor both the IRS and taxpayers.

Return preparer fraud generally involves the preparation and filing of false income taxreturns by preparers who claim inflated personal or business expenses, falsedeductions, unallowable credits or excessive exemptions on returns prepared for their clients. This includes inflated requests for the special one-time refund of the long-distance telephone tax. Preparers may also manipulate income figures to obtain taxcredits, such as the Earned Income Tax Credit, fraudulently.

In some situations, the client (taxpayer) may not have knowledge of the false expenses,deductions, exemptions and/or credits shown on their tax returns. However, when theIRS detects the false return, the taxpayer — not the return preparer — must pay theadditional taxes and interest and may be subject to penalties.

Abusive Preparer Prosecutions

FY 2008 FY 2007 FY 2006

Investigations Initiated 214 218 197

Prosecution Recommendations 134 196 153

Indictments/Informations 142 131 135

Sentenced 124 123 109

Incarceration Rate* 81.5% 81.3% 89.0%

Avg. Months to Serve 18 19 18

Audits of 30 Clients3.240 Another aspect of the IRS preparer program is identifying suspect preparers andaudited their clients. If during an examination a revenue suspects that some of thedeficiencies on a return were caused by the preparer she can refer the matter to anarea coordinator. After review the coordinator can initiate a project on the preparer. Thepreparer is sent a letter notifying her that she has been selected for a project and 30 of

her client's returns are audited. If significant deficiencies are found then the IRS maychoose one of several courses of action including:

• Referral to Criminal investigation

• Referral to the office of professional liability

• Preparer penalties

• Referral to Department of justice to seek an injunction ordering the preparer tocease filing tax returns.

28

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 33/75

4. EXAMINATION

Examination Reengineering4.10 Changes to the tax law, technology, and the business environment necessitatedthe IRS to make changes to its examination process. SB/SE initiated ExaminationReengineering in order to improve the quality and consistency of its examinations

across the country. SB/SE gathered feedback from multiple sources to design the newfield and office examination processes. Since 2003 the IRS has been implementing thisprocess.

Some of the features of the reengineered field examination process are:

• Clearly communicated expectations of both the taxpayer and field agent throughmandatory discussions between the revenue agent and taxpayer regarding thespecific examination issues, required documentation, and a mutually agreedupon date to complete the examination.

•

At the beginning of each examination, field agents and their managers will meetto discuss the agent’s approach to the examination, the plan to close theexamination, and the mutual commitment date arrived at with the taxpayer.

• Field agents will use standardized templates for every examination issue togather the information necessary to resolve issues. Agents will use astandardized guide when deciding if additional issues need to be added to theexamination. The agent will explain to the taxpayer if any additional issues areincluded in the examination.

The Dirty Dozen

4.20 Each year the IRS announces its Dirty Dozen and urges people to avoid thesecommon schemes: The 2009 list was as follows:

1. Phishing is a tactic used by Internet-based scam artists to trickunsuspecting victims into revealing personal or financial information. Thecriminals use the information to steal the victim’s identity, access bank accounts,run up credit card charges or apply for loans in the victim’s name.

Phishing scams often take the form of an e-mail that appears to come from alegitimate source, including the IRS. The IRS never initiates unsolicited e-mailcontact with taxpayers about their tax issues. Taxpayers who receive unsolicited

e-mails that claim to be from the IRS can forward the message [email protected]. Further instructions are available at IRS.gov. To date,taxpayers have forwarded scam e-mails reflecting thousands of confirmed IRSphishing sites. If you believe you have been the target of an identity thief,information is available at IRS.gov.

2. Hiding Income Offshore The IRS aggressively pursues taxpayers andpromoters involved in abusive offshore transactions. Taxpayers have tried toavoid or evade U.S. income tax by hiding income in offshore banks, brokerage

29

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 34/75

accounts or through other entities. Recently, the IRS provided guidance toauditors on how to deal with those hiding income offshore in undisclosedaccounts. The IRS draws a clear line between taxpayers with offshore accountswho voluntarily come forward and those who fail to come forward.

Taxpayers also evade taxes by using offshore debit cards, credit cards, wire

transfers, foreign trusts, employee-leasing schemes, private annuities or lifeinsurance plans. The IRS has also identified abusive offshore schemes includingthose that involve use of electronic funds transfer and payment systems, offshorebusiness merchant accounts and private banking relationships.

3. Filing False or Misleading Forms The IRS is seeing scam artists filefalse or misleading returns to claim refunds that they are not entitled to. Frivolousinformation returns, such as Form 1099-Original Issue Discount (OID), claimingfalse withholding credits are used to legitimize erroneous refund claims. The newscam has evolved from an earlier phony argument that a “strawman” bankaccount has been created for each citizen. Under this scheme, taxpayers

fabricate an information return, arguing they used their “strawman” account topay for goods and services and falsely claim the corresponding amount aswithholding as a way to seek a tax refund.

4. Abuse of Charitable Organizations and Deductions The IRS continuesto observe the misuse of tax-exempt organizations. Abuse includesarrangements to improperly shield income or assets from taxation and attemptsby donors to maintain control over donated assets or income from donatedproperty. The IRS also continues to investigate various schemes involving thedonation of non-cash assets, including easements on property, closely-heldcorporate stock and real property. Often, the donations are highly overvalued or the organization receiving the donation promises that the donor can purchase theitems back at a later date at a price the donor sets. The Pension Protection Act of 2006 imposed increased penalties for inaccurate appraisals and new definitionsof qualified appraisals and qualified appraisers for taxpayers claiming charitablecontributions.

5. Return Preparer Fraud Dishonest return preparers can cause manyheadaches for taxpayers who fall victim to their ploys. Such preparers derivefinancial gain by skimming a portion of their clients’ refunds and charging inflatedfees for return preparation services. They attract new clients by promising largerefunds. Taxpayers should choose carefully when hiring a tax preparer. As thesaying goes, if it sounds too good to be true, it probably is. No matter whoprepares the return, the taxpayer is ultimately responsible for its accuracy. Since2002, the courts have issued injunctions ordering dozens of individuals to ceasepreparing returns, and the Department of Justice has filed complaints againstdozens of others, which are pending in court.

6. Frivolous Arguments Promoters of frivolous schemes encourage peopleto make unreasonable and unfounded claims to avoid paying the taxes they owe.The IRS has a list of frivolous legal positions that taxpayers should stay awayfrom. Taxpayers who file a tax return or make a submission based on one of the

30

8/14/2019 2009 Representation Update

http://slidepdf.com/reader/full/2009-representation-update 35/75

positions on the list are subject to a $5,000 penalty. More information is availableon IRS.gov.

7. False Claims for Refund and Requests for Abatement This scaminvolves a request for abatement of previously assessed tax using Form 843,Claim for Refund and Request for Abatement. Many individuals who try this have

not previously filed tax returns. The tax they are trying to have abated has beenassessed by the IRS through the Substitute for Return Program. The filer usesForm 843 to list reasons for the request. Often, one of the reasons given is"Failed to properly compute and/or calculate Section 83-Property Transferred inConnection with Performance of Service."

8. Abusive Retirement Plans The IRS continues to uncover abuses inretirement plan arrangements, including Roth Individual RetirementArrangements (IRAs). The IRS is looking for transactions that taxpayers areusing to avoid the limitations on contributions to IRAs as well as transactions thatare not properly reported as early distributions. Taxpayers should be wary of

advisers who encourage them to shift appreciated assets into IRAs or companiesowned by their IRAs at less than fair market value to circumvent annualcontribution limits. Other variations have included the use of limited liabilitycompanies to engage in activity which is considered prohibited.

9. Disguised Corporate Ownership Some taxpayers form corporations andother entities in certain states for the primary purpose of disguising the ownershipof a business or financial activity. Such entities can be used to facilitateunderreporting of income, fictitious deductions, non-filing of tax returns,participating in listed transactions, money laundering, financial crimes, and eventerrorist financing. The IRS is working with state authorities to identify theseentities and to bring the owners of these entities into compliance.