2005 accounting higher finalised marking instructionssolutions.pdf · £60,000 sales in the trading...

TRANSCRIPT

2005 Accounting

Higher

Finalised Marking Instructions These Marking Instructions have been prepared by Examination Teams for use by SQA Appointed Markers when marking External Course Assessments.

2005 Accounting

Higher – Special

Finalised Marking Instructions These Marking Instructions have been prepared by Examination Teams for use by SQA Appointed Markers when marking External Course Assessments.

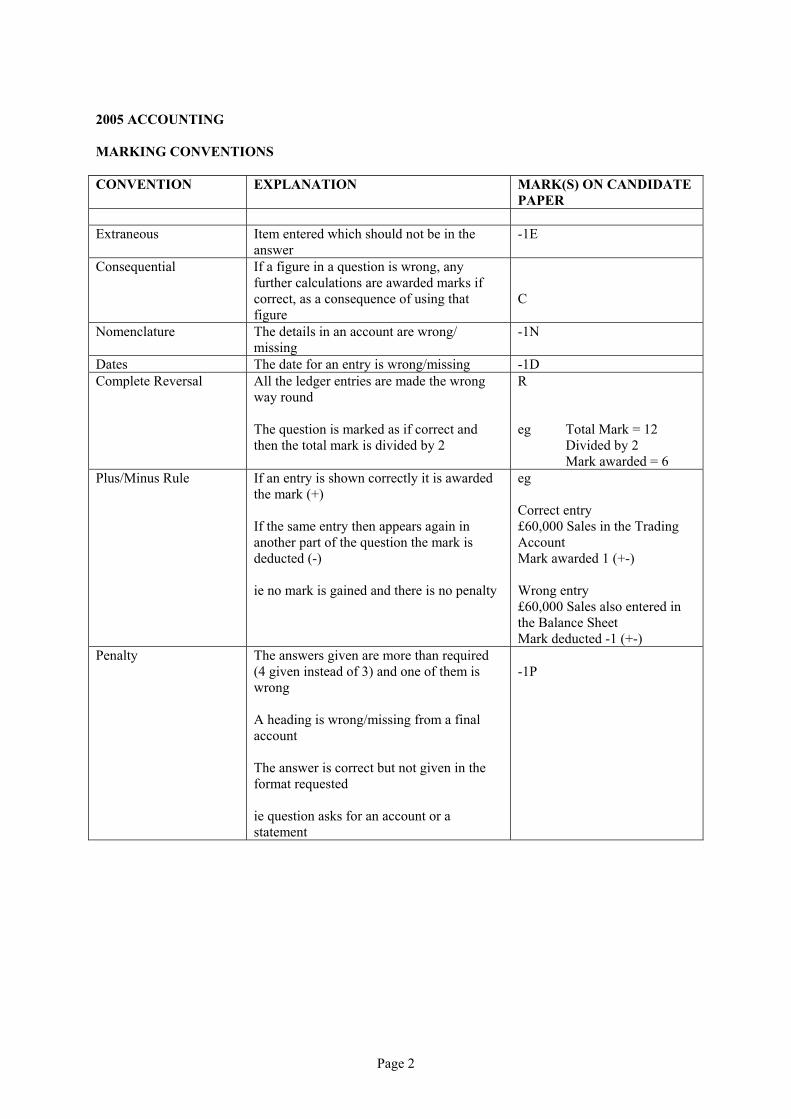

2005 ACCOUNTING MARKING CONVENTIONS CONVENTION EXPLANATION MARK(S) ON CANDIDATE

PAPER Extraneous Item entered which should not be in the

answer -1E

Consequential If a figure in a question is wrong, any further calculations are awarded marks if correct, as a consequence of using that figure

C

Nomenclature The details in an account are wrong/ missing

-1N

Dates The date for an entry is wrong/missing -1D Complete Reversal All the ledger entries are made the wrong

way round The question is marked as if correct and then the total mark is divided by 2

R eg Total Mark = 12 Divided by 2 Mark awarded = 6

Plus/Minus Rule If an entry is shown correctly it is awarded the mark (+) If the same entry then appears again in another part of the question the mark is deducted (-) ie no mark is gained and there is no penalty

eg Correct entry £60,000 Sales in the Trading Account Mark awarded 1 (+-) Wrong entry £60,000 Sales also entered in the Balance Sheet Mark deducted -1 (+-)

Penalty The answers given are more than required (4 given instead of 3) and one of them is wrong A heading is wrong/missing from a final account The answer is correct but not given in the format requested ie question asks for an account or a statement

-1P

Page 2

General 1 Assess pencil figures and working. If the script is predominantly in pencil refer to the Principal

Examiner. 2 A maximum of 10% of marks gained on any individual question may be deducted for untidy

work and poor style. This penalty should only be applied in exceptional circumstances. 3 Work which has been deleted gains no marks even if it is correct. Exceptional cases may be

drawn to the attention of the Principal Examiner. 4 Consequential errors MUST NOT be penalised, subject to the marking instructions for each

question. 5 Mark workings whether or not they are incorporated in the final answer. Deduct a penalty of -1

mark per question for working which is not incorporated in the final answer. 6 Incorrect figures, supported by adequate workings – award marks for any correct operations

performed. 7 Incorrect figures, not supported by adequate workings – lose awards, unless the marking

instructions specify otherwise. If arithmetic error – lose 1 mark. 8 EXTRANEOUS ITEMS: see instructions for specific questions. Penalties should be shown beside the figure and encircled, eg -1P -1E -1 +/- 9 If right and wrong – give value of award where right, deduct value of award where wrong

(cross reference +/- against relevant figures). 10 Indicate awards given for each item, eg £1500 1 In essay type questions indicate marks awarded beside the point made by candidate – NOT IN

THE MARGIN. Sub-totals for sections should be indicated and encircled, eg 4/6 Final total should be clearly indicated and easy to check, eg Q1 = 45/50.

Page 3

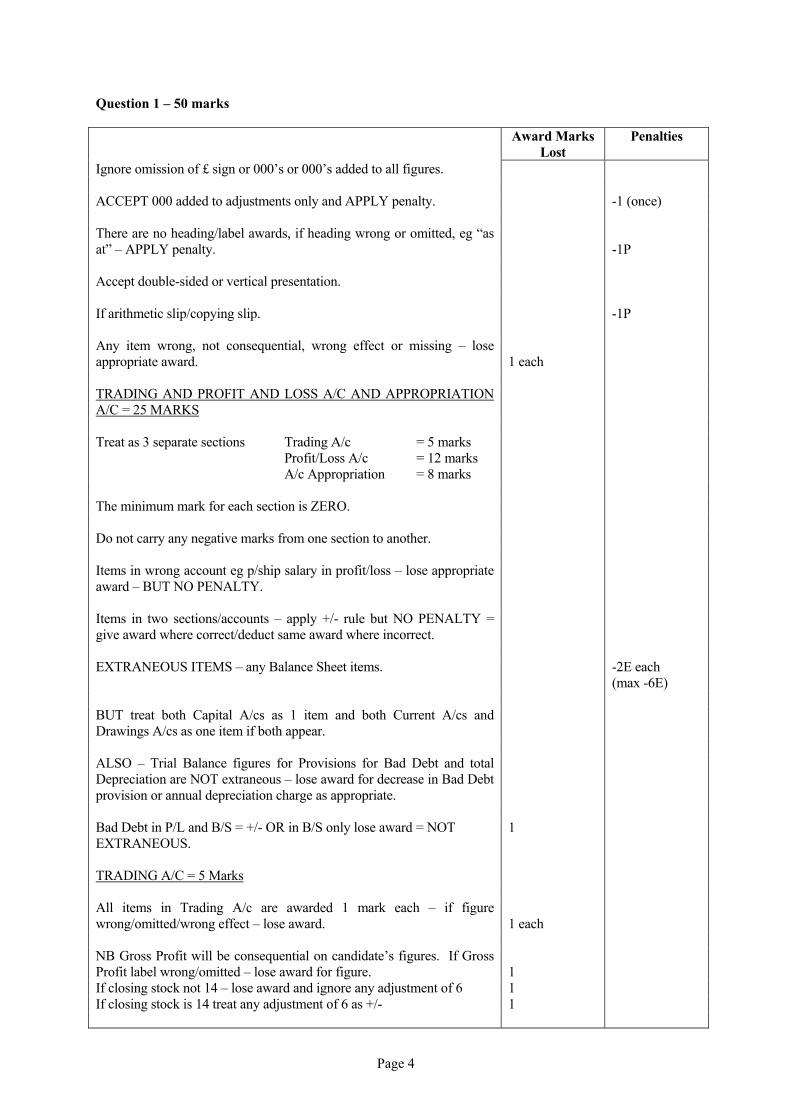

Question 1 – 50 marks Award Marks

Lost Penalties

Ignore omission of £ sign or 000’s or 000’s added to all figures. ACCEPT 000 added to adjustments only and APPLY penalty. -1 (once) There are no heading/label awards, if heading wrong or omitted, eg “as at” – APPLY penalty.

-1P

Accept double-sided or vertical presentation. If arithmetic slip/copying slip. -1P Any item wrong, not consequential, wrong effect or missing – lose appropriate award.

1 each

TRADING AND PROFIT AND LOSS A/C AND APPROPRIATION A/C = 25 MARKS

Treat as 3 separate sections Trading A/c = 5 marks Profit/Loss A/c = 12 marks A/c Appropriation = 8 marks

The minimum mark for each section is ZERO. Do not carry any negative marks from one section to another. Items in wrong account eg p/ship salary in profit/loss – lose appropriate award – BUT NO PENALTY.

Items in two sections/accounts – apply +/- rule but NO PENALTY = give award where correct/deduct same award where incorrect.

EXTRANEOUS ITEMS – any Balance Sheet items. -2E each

(max -6E) BUT treat both Capital A/cs as 1 item and both Current A/cs and Drawings A/cs as one item if both appear.

ALSO – Trial Balance figures for Provisions for Bad Debt and total Depreciation are NOT extraneous – lose award for decrease in Bad Debt provision or annual depreciation charge as appropriate.

Bad Debt in P/L and B/S = +/- OR in B/S only lose award = NOT EXTRANEOUS.

1

TRADING A/C = 5 Marks All items in Trading A/c are awarded 1 mark each – if figure wrong/omitted/wrong effect – lose award.

1 each

NB Gross Profit will be consequential on candidate’s figures. If Gross Profit label wrong/omitted – lose award for figure.

1

If closing stock not 14 – lose award and ignore any adjustment of 6 1 If closing stock is 14 treat any adjustment of 6 as +/- 1

Page 4

Question 1 (continued) Award Marks

Lost Penalties

PROFIT AND LOSS A/C = 12 marks Mark as per solution – figure wrong/omitted/wrong effect – lose award 1 each If Decrease in Prov. for Bad Debt is shown as expense – award 1 for correct calculation of decrease If Decrease in Prov. for Bad Debt is added to actual Bad Debt to give a net figure of (-1) – ACCEPT for 3 marks. If Bad Debt is shown as a total of 5 – ACCEPT for 2 marks. If Provision for Bad Debt is given as 2 – lose award

1 1 2

ADJUSTMENTS – GIVE full award to a TOTAL expense figure which includes the adjustment: eg Off/Expenses = 9 = 2 marks

BUT: If adjustment shown as separate item – it must be directly

attached (ie on next line) to gain adjustment award.

OR: If adjustment is wrongly treated – ie added instead of subtracted

(or vice versa) eg Office = 13 = 1 mark and Selling = 16 = 1 mark

1

If Depreciation of Fixed Assets is shown as 15 ie Fittings 3 + Vehicles 12 – ACCEPT for 2 marks

If Net Profit label wrong or omitted – lose figure award 1 APPROPRIATION A/C = 8 marks Mark as per solution – item wrong/omitted/ wrong effect/not consequential – lose award

1 each

NB. Share of profit will be consequential on candidate’s figures. General reserve in not extraneous – lose transfer award 1

Page 5

Question 1 (continued) Award Marks

Lost Penalties

BALANCE SHEET = 25 marks

ACCEPT any recognised Balance Sheet layout – horizontal or vertical

There is no heading award if missing/wrong, eg ‘for year ended’ apply a penalty

-1P

If item under wrong heading (eg stock in fixed assets section) – lose award BUT NO PENALTIES

1

If item in two sections – apply the +/- rule 1 EXTRANEOUS ITEMS (ie any final A/c items – except actual bad debt) – APPLY PENALTY

-2E each (Max -6E)

There are no awards for headings/sub-totals/working capital/balance sheet totals

FIXED ASSETS = 6 marks MARK as per solution – figure wrong/omitted/wrong effect – lose award

1 each

ACCEPT the following alternatives for Property: NBV £130 = 1 NBV £150 = 2

1 0

If Cost/Agg Dep Fittings/Vehicles wrong/not consequential – lose award If omitted and NBV is correct – ACCEPT NBV for 2 marks If omitted and NBV is wrong – lose award as appropriate

1 each

ACCEPT as consequential any dep. figure for Fittings or Vehicles which is an aggregate of: the candidate’s dep. figure in the profit statement and the Trial Balance provision for depreciation given

If no depreciation charged in P/L, DO NOT give awards to P/L figures (Fittings 3, Vehicles 12) or trial balance figures (Fittings 20, Vehicles 30)

1 each

OTHERWISE, if Agg Dep for Fittings/Vehicles not 23/42 respectively

1 each

NBV will be consequential on Candidate’s figures for both cost value and agg. dep – if wrong, treat as arithmetic slip and apply penalty

-1P

Page 6

Question 1 (continued) CURRENT ASSETS = 4 marks Award Marks

Lost Penalties

All items are 1 mark each, if wrong/omitted/not consequential/wrong effect – lose award

NB ACCEPT consequentially correct provision for bad debt from the figure used by the candidate in the profit statement

1 each

Accept consequential stock from trading and 14 any

adjustment +/-

ACCEPT Net Debtors = 38 = 2 marks, if Prov. For Bad Debt not shown.

ACCEPT any adjusted Debtors figure if 40 implied 1

If Debtors less actual bad debts lose new provision award but DO NOT treat as extraneous

1

If actual bad debt given with new provision – apply +/- rule 1

CURRENT LIABILITIES = 4 marks ALL items are 1 mark each, if wrong/omitted/not consequential/wrong effect – lose award

1 each

Accept loan as current liability If figures combined correctly – ACCEPT for full award eg Creditors = 35 (= 32 + 3 unpaid expense) = 2 marks

Overdraft interest in BS/lose Bank award 1 REPRESENTED BY = 11 marks Mark as per solution, if item wrong/omitted/not consequential/wrong effect – lose award

1 each

New Current A/c Balances will be consequential on candidate’s workings, if wrong/omitted/not consequential

3 each

ACCEPT Loan deducted from Net Assets otherwise Loan must be last item in ‘Represented by’ Section – if not lose award

1

Page 7

Question 1 (continued) CURRENT ACCOUNTS These were not asked for so if new balances are shown only as calculations/workings ACCEPT FOR FULL AWARDS = 3 marks each

If Current A/cs given mark as per solution – if item wrong/omitted/not consequential/wrong effect – lose award (No heading penalty)

1 each

ACCEPT Current A/cs given as list of additions/subtractions ACCEPT complete reversal – give awards. NO PENALTY If no Current A/cs shown and balances in B5 given as 5 (cr) and -6 (dr) ie opening balances = 1 mark

5

EXTRANEOUS ITEMS – NB: Treat Capital in both Current A/cs as one item

-2E ONCE

If Current shown and balances not properly transferred to B5 – apply penalty

GIVE THE FINAL AWARDS FOR CURRENT ACCOUNTS TO THE BALANCES IN THE BALANCE SHEET AS APPROPRIATE

-2p

Page 8

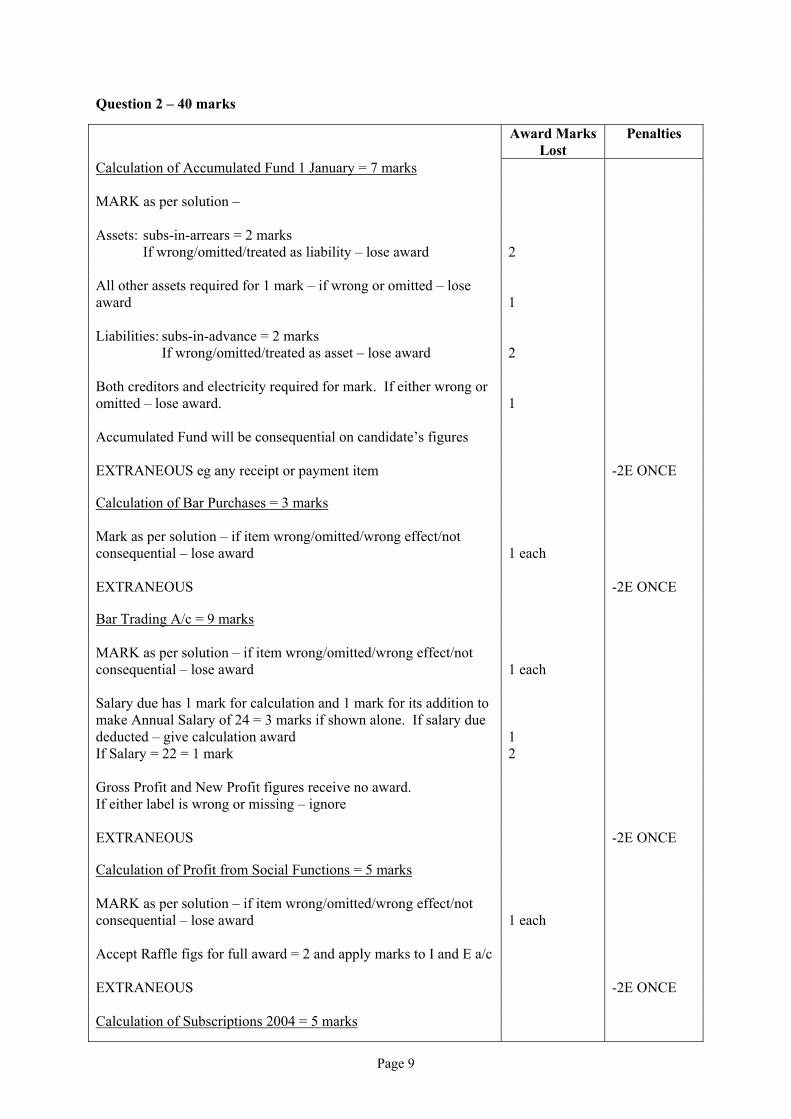

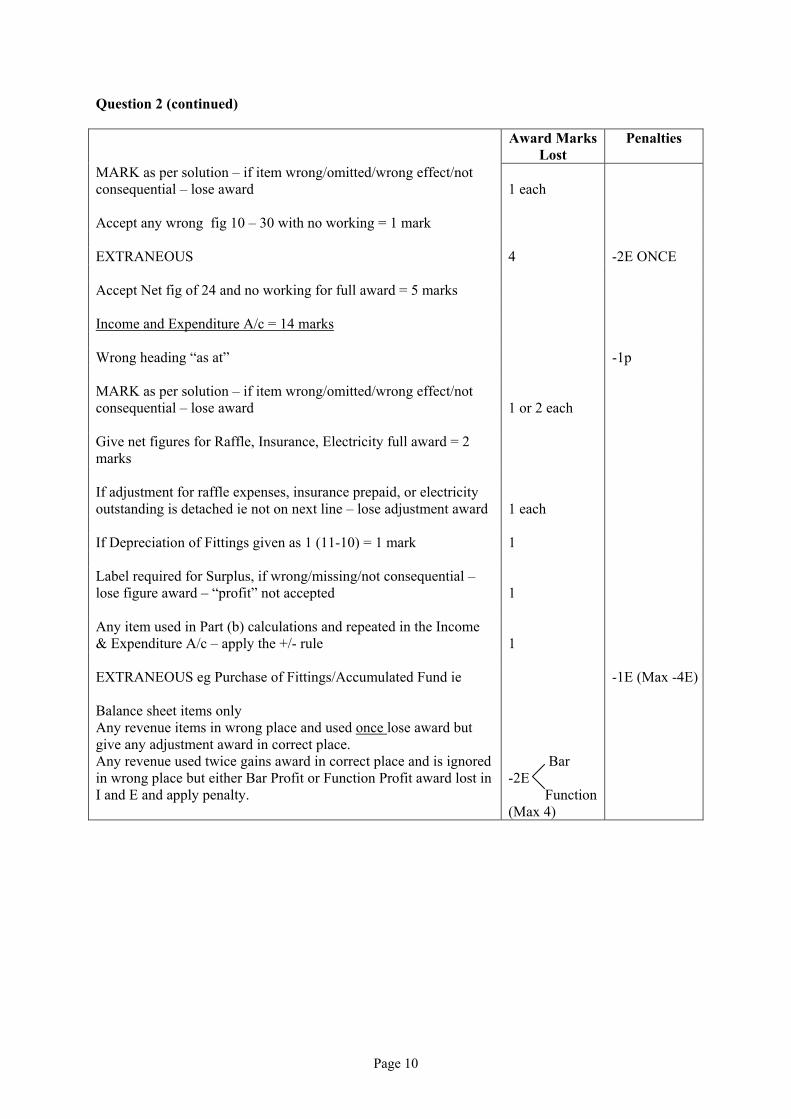

Question 2 – 40 marks Award Marks

Lost Penalties

Calculation of Accumulated Fund 1 January = 7 marks MARK as per solution – Assets: subs-in-arrears = 2 marks If wrong/omitted/treated as liability – lose award 2 All other assets required for 1 mark – if wrong or omitted – lose award

1

Liabilities: subs-in-advance = 2 marks If wrong/omitted/treated as asset – lose award

2

Both creditors and electricity required for mark. If either wrong or omitted – lose award.

1

Accumulated Fund will be consequential on candidate’s figures EXTRANEOUS eg any receipt or payment item -2E ONCE Calculation of Bar Purchases = 3 marks Mark as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

EXTRANEOUS -2E ONCE Bar Trading A/c = 9 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

Salary due has 1 mark for calculation and 1 mark for its addition to make Annual Salary of 24 = 3 marks if shown alone. If salary due deducted – give calculation award If Salary = 22 = 1 mark

1 2

Gross Profit and New Profit figures receive no award. If either label is wrong or missing – ignore

EXTRANEOUS -2E ONCE Calculation of Profit from Social Functions = 5 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

Accept Raffle figs for full award = 2 and apply marks to I and E a/c EXTRANEOUS -2E ONCE Calculation of Subscriptions 2004 = 5 marks

Page 9

Question 2 (continued) Award Marks

Lost Penalties

MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

Accept any wrong fig 10 – 30 with no working = 1 mark EXTRANEOUS 4 -2E ONCE Accept Net fig of 24 and no working for full award = 5 marks Income and Expenditure A/c = 14 marks Wrong heading “as at” -1p MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 or 2 each

Give net figures for Raffle, Insurance, Electricity full award = 2 marks

If adjustment for raffle expenses, insurance prepaid, or electricity outstanding is detached ie not on next line – lose adjustment award

1 each

If Depreciation of Fittings given as 1 (11-10) = 1 mark 1 Label required for Surplus, if wrong/missing/not consequential – lose figure award – “profit” not accepted

1

Any item used in Part (b) calculations and repeated in the Income & Expenditure A/c – apply the +/- rule

1

EXTRANEOUS eg Purchase of Fittings/Accumulated Fund ie Balance sheet items only Any revenue items in wrong place and used once lose award but give any adjustment award in correct place. Any revenue used twice gains award in correct place and is ignored in wrong place but either Bar Profit or Function Profit award lost in I and E and apply penalty.

Bar -2E Function (Max 4)

-1E (Max -4E)

Page 10

Question 3 – 40 marks Award Marks

Lost Penalties

Calculation of Net Profit = 2 marks MARK as per solution – if net profit not = 4 x 9 BUT if 4 x 5 (=2004 tax) = 20

2 1

Trading Account = 9 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 or 2

If Sales not = candidate’s Net Profit/15x100 2 If Gross Profit not – 40% candidate’s Sales 2 EXTRANEOUS -2E ONCE Calculation of Dep/Deb Interest/Expenses = 7 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 or 2

If Depreciation not = 18

If 30 or 12 2

accept for 1 mark 1 If Debenture interest = 4 or 2 or 6 1 Total expenses is consequential on candidate’s gross and net profits

Other expenses is consequential on candidate’s figures for Depreciation and Debenture Interest

Appropriation A/c = 4 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

Unappropriated Profit C/f label is required – if wrong or omitted lose figure award

1

EXTRANEOUS -2E ONCE

Page 11

Question 3 (continued) Award Marks

Lost Penalties

Calculation of figures for 2005 = 9 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 or 2 or 3

Any wrong formula – lose awards 2 or 3 If Credit Sales not = 80% x 240 (or candidate’s sales) 1 If Debtors = 35 or 25 1 If timescale not weeks 1 If Credit Purchases not = 136 or candidate’s purchases 1 If Creditors = 18 or 16 1 If timescale not weeks 1 If decrease in working capital not labelled or change not indicated eg -20 – apply penalty

-1P

Accept decrease in WC ratio 0.56% = 1 1 Calculation of figures for 2006 = 9 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 or 2

If Rate of Stock Turnover not = 18 (or candidate’s answer from (e) x 2)

1

If Other Expenses not = £39000 (or candidate’s answer from (c)) 1 If Debenture Interest = 2 1 Net Profit is consequential on candidate’s Gross Profit and Total Expenses

EXTRANEOUS -2E ONCE

Page 12

Question 4 – 10 marks Award Marks

Lost Penalties

Mark as per solution Award marks for valid points not in solution If more than TWO topics have been attempted in (b) – mark all topics and select only the marks of the best two for the final total

Question 5 – 10 marks Award Marks

Lost Penalties

Mark as per solution Accept Max 7 advantages Or Max 7 disadvantages

Award marks for valid points not in solution

Page 13

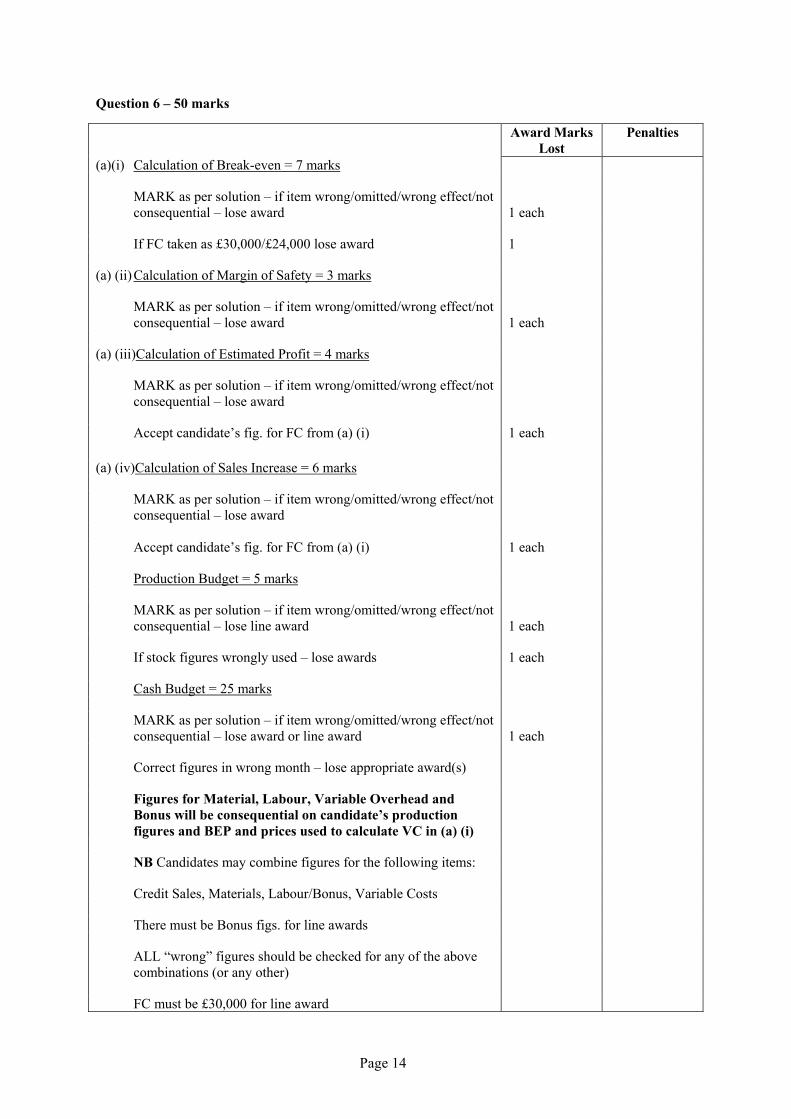

Question 6 – 50 marks Award Marks

Lost Penalties

(a)(i) Calculation of Break-even = 7 marks

MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

If FC taken as £30,000/£24,000 lose award 1

(a) (ii) Calculation of Margin of Safety = 3 marks

MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

(a) (iii)Calculation of Estimated Profit = 4 marks

MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

Accept candidate’s fig. for FC from (a) (i) 1 each

(a) (iv)Calculation of Sales Increase = 6 marks

MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

Accept candidate’s fig. for FC from (a) (i) 1 each

Production Budget = 5 marks

MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose line award

1 each

If stock figures wrongly used – lose awards 1 each

Cash Budget = 25 marks MARK as per solution – if item wrong/omitted/wrong effect/not consequential – lose award or line award

1 each

Correct figures in wrong month – lose appropriate award(s)

Figures for Material, Labour, Variable Overhead and Bonus will be consequential on candidate’s production figures and BEP and prices used to calculate VC in (a) (i)

NB Candidates may combine figures for the following items: Credit Sales, Materials, Labour/Bonus, Variable Costs There must be Bonus figs. for line awards ALL “wrong” figures should be checked for any of the above combinations (or any other)

FC must be £30,000 for line award

Page 14

Question 6 (continued)

If Opening Balances included with Receipts and added – give total receipts and total payments the line awards as per marking scheme.

Question 7 – 40 marks Award Marks

Lost Penalties

CONSEQUENTIALITY IS PARTICULARLY IMPORTANT IN THIS QUESTION. THE CANDIDATE’S FIGURES FOR CONTRIBUTION PER UNIT AND FULL CAPACITY HAVE TO BE ACCEPTED IN SUBSEQUENT CALCULATIONS.

If any profit labels wrong or missing – apply penalty -1P once Profit for current year = 12 marks Mark as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

NB Some figures are combined for a 1 mark award If ANY figure wrong/missing/not consequential – lose award

1 each

BUT if the answer given is correct, the missing figures are implied and the correct answer gets the award

No. of Machine Hours taken = 5 marks Mark as per solution – if wrong/omitted/not consequential – lose award

1 each

Combined figures – as above No. of Units to be Produced = 7 marks Mark as per solution – if wrong/omitted/not consequential – lose award

1 each

Combined figures – as above If X and Y production taken as 23000 and 15500 units ie no limiting

factor for X – see alternative solution 4

Maximum Profit at Full Capacity = 3 marks Mark as per solution – if wrong/omitted/not consequential – lose award

1 each

Combined figures – as above Change in Maximum Profit and Advice = 8 marks Mark as per solution – if wrong/omitted/not consequential – lose

award 1 each

Combined figures – as above Page 15

Question 7 (continued) Award Marks

Lost Penalties

If Contribution per hour from Z not £5 – lose award 1 If Sales of Z and Y not 10,000 and 21,000 respectively – lose award

1 each

If Sales of X taken as 21,000 units

2

If reason for advice not based on increase in profit (or consequential figure) – lose award

1

Maximum Profit from 14,000 units of X = 5 marks Mark as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

Combined figures – as above If loss of Y not 4500 units – lose fig. award and multiply award 3

Page 16

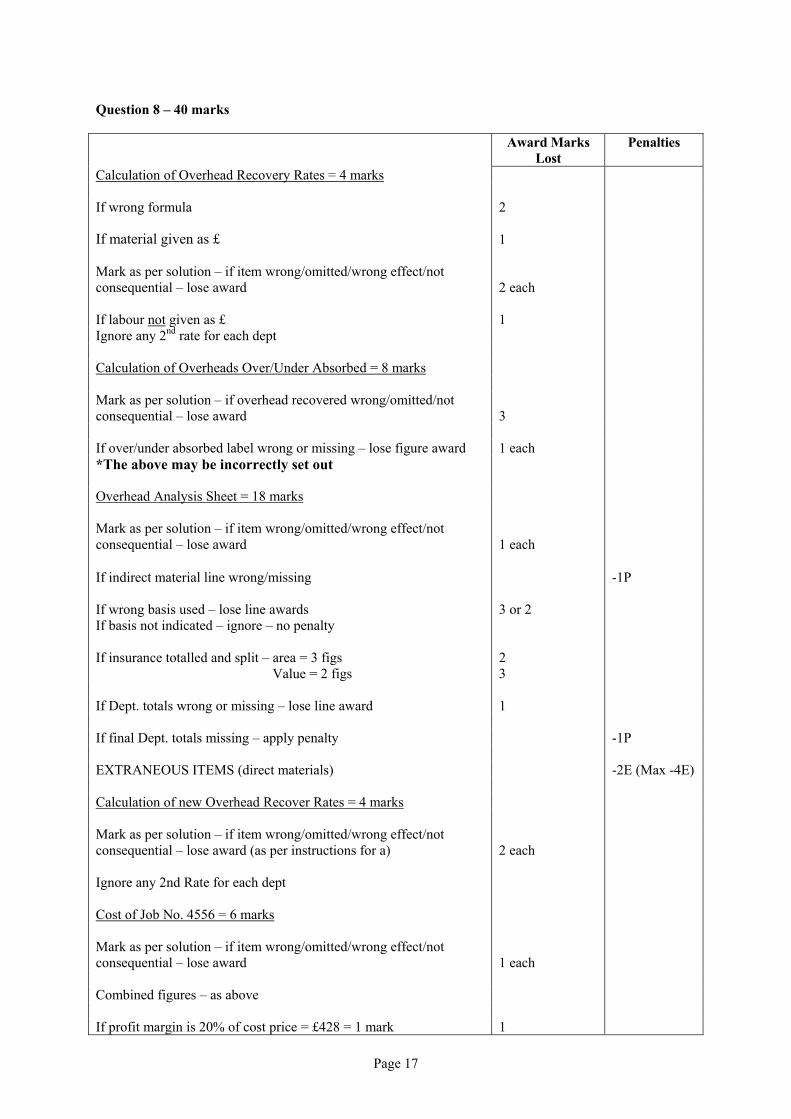

Question 8 – 40 marks Award Marks

Lost Penalties

Calculation of Overhead Recovery Rates = 4 marks If wrong formula If material given as £

2 1

Mark as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

2 each

If labour not given as £ 1 Ignore any 2nd rate for each dept Calculation of Overheads Over/Under Absorbed = 8 marks Mark as per solution – if overhead recovered wrong/omitted/not consequential – lose award

3

If over/under absorbed label wrong or missing – lose figure award 1 each *The above may be incorrectly set out

Overhead Analysis Sheet = 18 marks Mark as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

If indirect material line wrong/missing -1P If wrong basis used – lose line awards 3 or 2 If basis not indicated – ignore – no penalty If insurance totalled and split – area = 3 figs 2 Value = 2 figs 3 If Dept. totals wrong or missing – lose line award 1 If final Dept. totals missing – apply penalty -1P EXTRANEOUS ITEMS (direct materials) -2E (Max -4E) Calculation of new Overhead Recover Rates = 4 marks Mark as per solution – if item wrong/omitted/wrong effect/not consequential – lose award (as per instructions for a)

2 each

Ignore any 2nd Rate for each dept Cost of Job No. 4556 = 6 marks Mark as per solution – if item wrong/omitted/wrong effect/not consequential – lose award

1 each

Combined figures – as above If profit margin is 20% of cost price = £428 = 1 mark 1

Page 17

Page 18

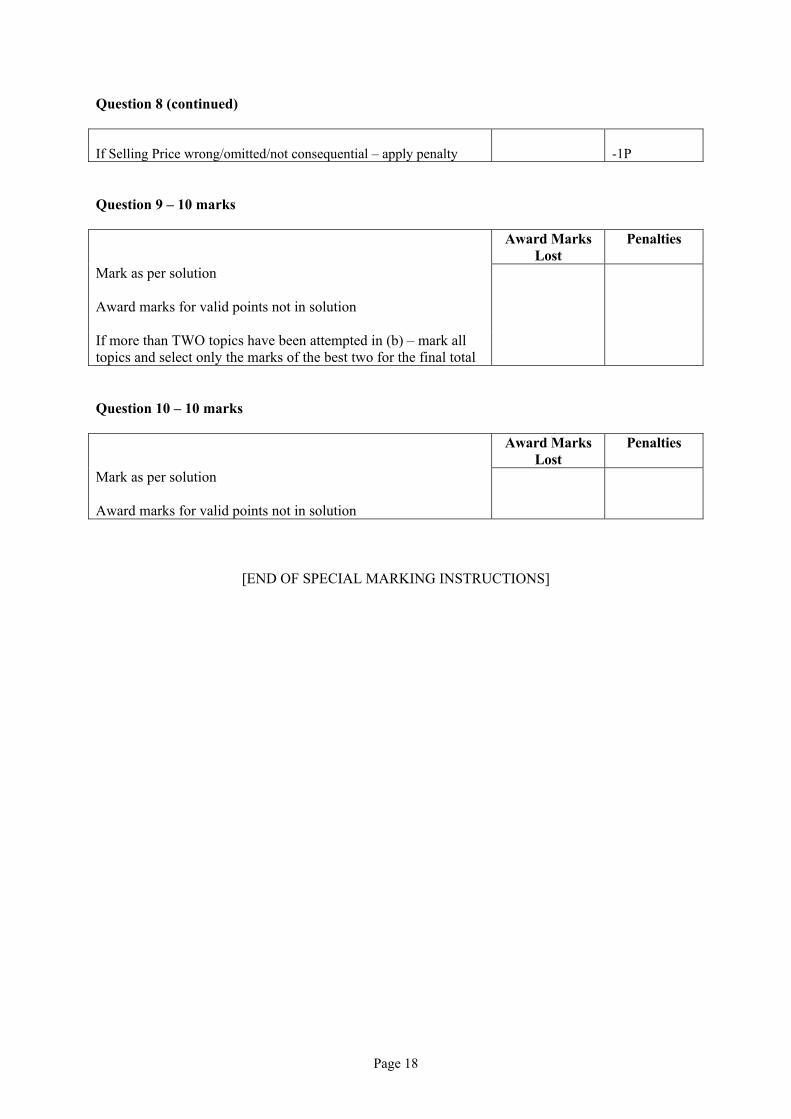

Question 8 (continued) If Selling Price wrong/omitted/not consequential – apply penalty -1P Question 9 – 10 marks Award Marks

Lost Penalties

Mark as per solution Award marks for valid points not in solution If more than TWO topics have been attempted in (b) – mark all topics and select only the marks of the best two for the final total

Question 10 – 10 marks Award Marks

Lost Penalties

Mark as per solution Award marks for valid points not in solution

[END OF SPECIAL MARKING INSTRUCTIONS]

2005 Accounting

Higher – Solutions

Finalised Marking Instructions These Marking Instructions have been prepared by Examination Teams for use by SQA Appointed Markers when marking External Course Assessments.

2005 Accounting Higher Solutions Question 1 Trading Profit and Loss Accounts for year ended 30 April 2005 £000 £000 SALES 273 1 Less: COST OF SALES OPENING STOCK 15 1 Add: PURCHASES 160 1 175 Less: CLOSING STOCK 14 1 161 0 GROSS PROFIT 112 1 5 DECREASE IN PROV FOR BAD DEBT 3 1+1 115 Less: EXPENSES Selling (19 (1) + 3 (1)) 22 Office (11 (1) – 2 (1)) 9 Loan Interest (10% × 40) 4 1 Overdraft Interest (15% × 20) 2 1 Depreciation – Vehicles (20% × 60) 12 1 Depreciation – Fittings (10% × 30) 3 1 Actual Bad Debt 2 1 54 0 NET PROFIT FOR YEAR 61 1 12 PARTNERSHIP APPROPRIATION ACCOUNT NET PROFIT FOR YEAR 61 0 Less: Transfer to General Reserve 5 1 56 Add: Interest on Drawings Armour 2 1 Burns 4 1 6 62 Less: Interest on Capital Armour 5 1 Burns 3 1 8 54 Less: Partnership Salary Armour 6 1 (Residual Profit to be shared) 48 SHARE OF PROFIT Armour 30 1 Burns 18 1 48 8 25

Page 2

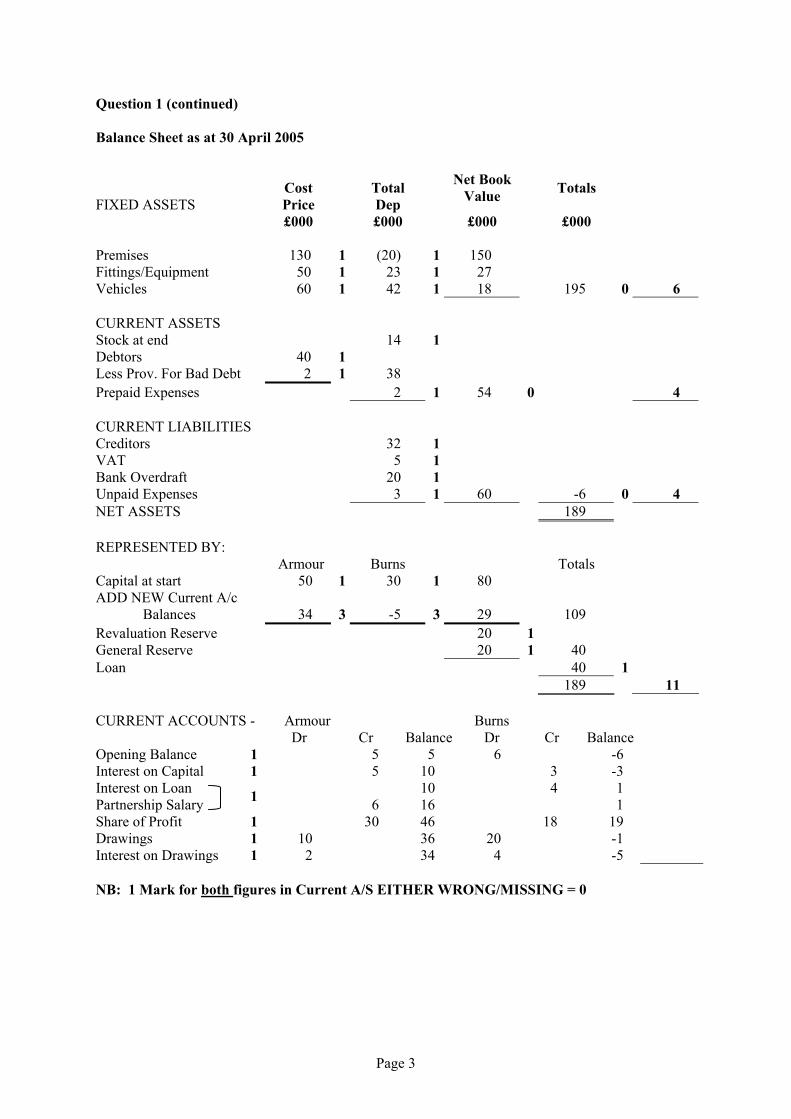

Question 1 (continued) Balance Sheet as at 30 April 2005 FIXED ASSETS

Cost Price

Total Dep

Net Book Value

Totals

£000 £000 £000 £000 Premises 130 1 (20) 1 150 Fittings/Equipment 50 1 23 1 27 Vehicles 60 1 42 1 18 195 0 6 CURRENT ASSETS Stock at end 14 1 Debtors 40 1 Less Prov. For Bad Debt 2 1 38 Prepaid Expenses 2 1 54 0 4 CURRENT LIABILITIES Creditors 32 1 VAT 5 1 Bank Overdraft 20 1 Unpaid Expenses 3 1 60 -6 0 4 NET ASSETS 189 REPRESENTED BY: Armour Burns Totals Capital at start 50 1 30 1 80 ADD NEW Current A/c Balances 34 3 -5 3 29 109 Revaluation Reserve 20 1 General Reserve 20 1 40 Loan 40 1 189 11 CURRENT ACCOUNTS - Armour Burns Dr Cr Balance Dr Cr Balance Opening Balance 1 5 5 6 -6 Interest on Capital 1 5 10 3 -3 Interest on Loan 10 4 1 Partnership Salary 1 6 16 1 Share of Profit 1 30 46 18 19 Drawings 1 10 36 20 -1 Interest on Drawings 1 2 34 4 -5 NB: 1 Mark for both figures in Current A/S EITHER WRONG/MISSING = 0

Page 3

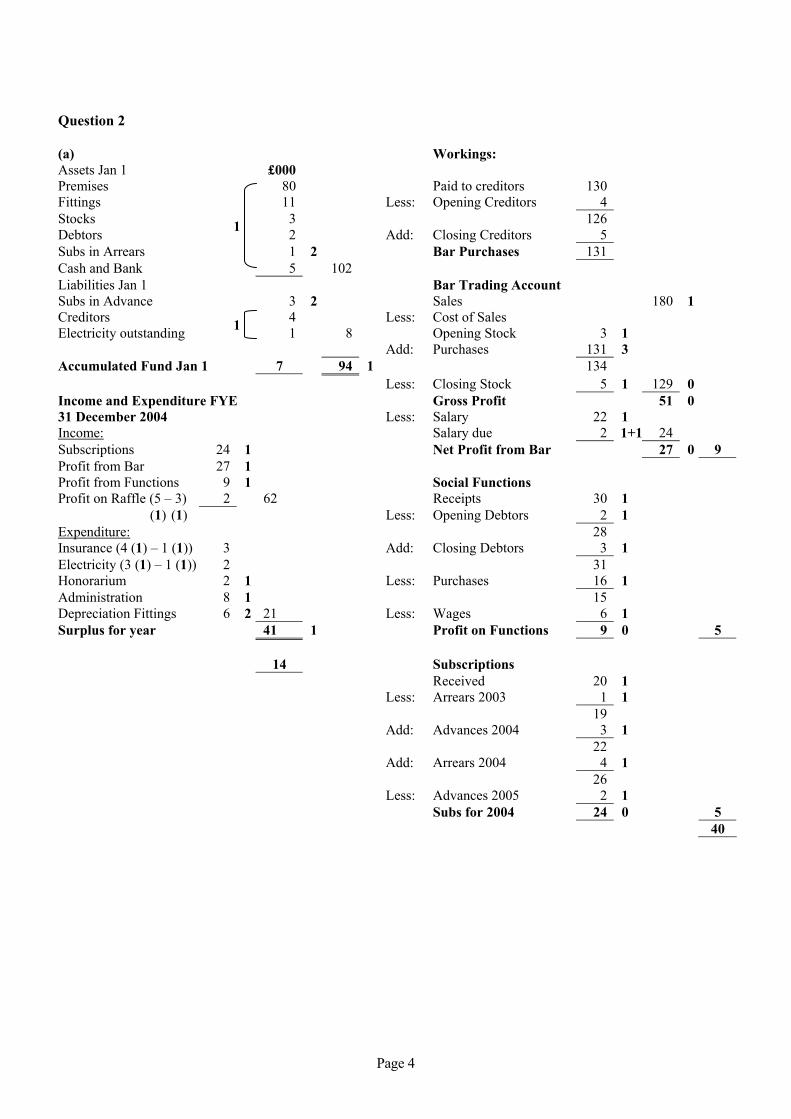

Question 2 (a) Workings: Assets Jan 1 £000 Premises 80 Paid to creditors 130 Fittings 11 Less: Opening Creditors 4 Stocks 3 126 Debtors 1 2 Add: Closing Creditors 5 Subs in Arrears 1 2 Bar Purchases 131 Cash and Bank 5 102 Liabilities Jan 1 Bar Trading Account Subs in Advance 3 2 Sales 180 1 Creditors 4 Less: Cost of Sales Electricity outstanding 1 1 8 Opening Stock 3 1 Add: Purchases 131 3 Accumulated Fund Jan 1 7 94 1 134 Less: Closing Stock 5 1 129 0 Income and Expenditure FYE Gross Profit 51 0 31 December 2004 Less: Salary 22 1 Income: Salary due 2 1+1 24 Subscriptions 24 1 Net Profit from Bar 27 0 9 Profit from Bar 27 1 Profit from Functions 9 1 Social Functions Profit on Raffle (5 – 3) 2 62 Receipts 30 1 (1) (1) Less: Opening Debtors 2 1 Expenditure: 28 Insurance (4 (1) – 1 (1)) 3 Add: Closing Debtors 3 1 Electricity (3 (1) – 1 (1)) 2 31 Honorarium 2 1 Less: Purchases 16 1 Administration 8 1 15 Depreciation Fittings 6 2 21 Less: Wages 6 1 Surplus for year 41 1 Profit on Functions 9 0 5 14 Subscriptions Received 20 1 Less: Arrears 2003 1 1 19 Add: Advances 2004 3 1 22 Add: Arrears 2004 4 1 26 Less: Advances 2005 2 1 Subs for 2004 24 0 5 40

Page 4

Question 3 Calculation of Net Profit Tax = 9 = 25% of Net Profit = 4 (1) × 9 (1) = 36 = Net Profit 2 Trading A/C FYE 30 April 2005 Workings 2005 £000 Sales 240 2 - Cost of Sales Net Profit = 36 = 15% of Sales = 36/15 × 100 = 240 = Sales Opening Stock 20 1 + Purchases 136 1 Gross Profit = 40% of Sales = 240/100 × 40 = 96 156 1 - Closing Stock 12 1 144 1 Cogs = Sales – GP = 240 – 96 = 144 Gross Profit 96 2 Purchases = Cogs + Closing St – Opening St Calculations: = 144 + 12 – 20 = 136 9 1 1 Depreciation = 30 – 12 = 18 Debenture Interest = 50,000 × 8% × 1/2 year = 2 1 + 25,000 × 8% × 1/2 year = 1 1 Total Debenture Interest 3 0 Total Expenses = Gross Profit – Net Profit = 96 – 36 = 60 Other Expenses = Total Expenses 60 (1) – (DEP 18 (1) + DEB Int 3 (1)) = 39 7 Appropriation Account for year ended 30 April 2005 Net Profit before Tax 36 - Corporation Tax 9 1 Net Profit after Tax 27 0 + Unappropriated 2004 6 1 33 0 - Proposed Dividend 20 1 Unappropriated Profit C/f 13 1 4 Rate of Stock Turnover 144 1 Average Debtors 30 (1) × 52 (1) 16 1 Collection (weeks) 192 (1) = 9 times = 8 weeks Average Creditors’ 17 × 52 (1) Working Capital 2004 28 (1) Payment

1 136 2005 8 (1)

Decrease in WC 20 = 6.5 weeks 9

Page 5

Workings 2006 Stock Turnover = 9 × 2 = 18 Cost of Sales = Average Stock 10,000 (1) × 18 (1) = 180,000 Mark up = 60% of COGS = 180 × .6 = 108,000 = Gross Profit Net Profit = 108,000 (1) – 55,000 = 53,000 Other Expenses = 39,000 – 8,000 = 31,000 Debenture Interest = 8% × 50,000 = 4,000

(1)

(1)

(1)

Depreciation = 10% (1) × 200,000 (1) = 20,000 Total Expenses = 55,000 (0) 9 40

Page 6

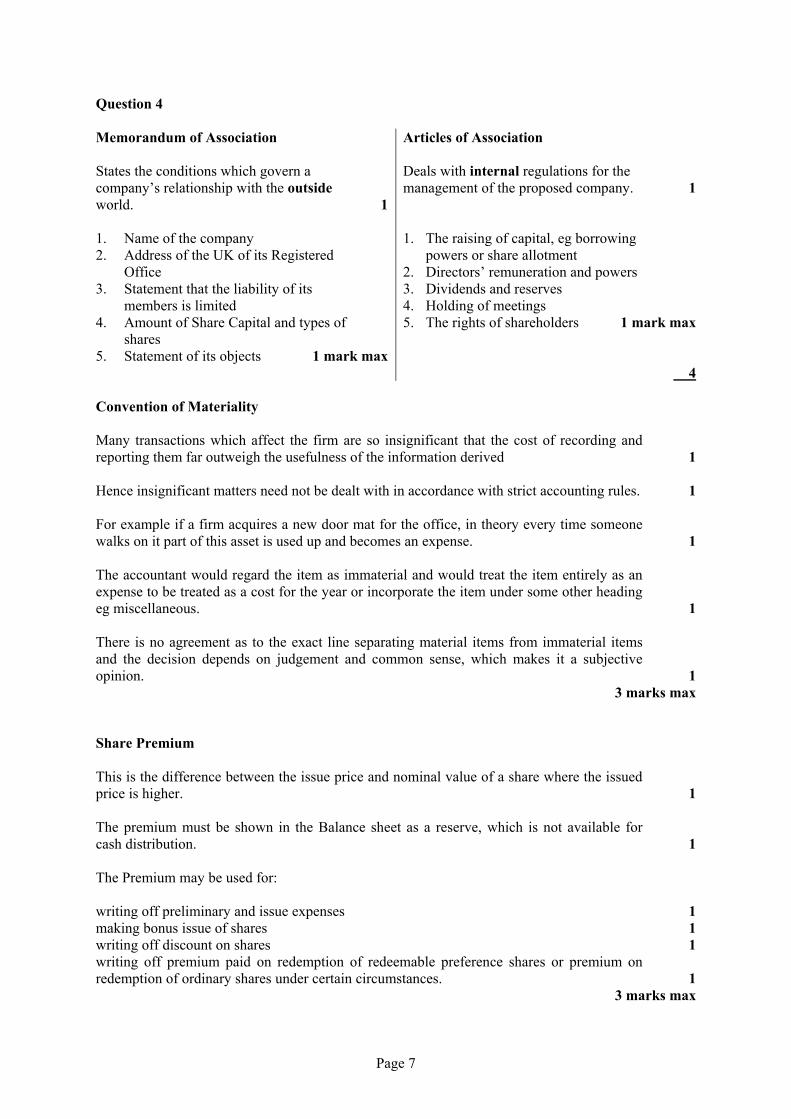

Question 4 Memorandum of Association States the conditions which govern a company’s relationship with the outside world. 1 1. Name of the company 2. Address of the UK of its Registered

Office 3. Statement that the liability of its

members is limited 4. Amount of Share Capital and types of

shares 5. Statement of its objects 1 mark max

Articles of Association Deals with internal regulations for the management of the proposed company. 1 1. The raising of capital, eg borrowing

powers or share allotment 2. Directors’ remuneration and powers 3. Dividends and reserves 4. Holding of meetings 5. The rights of shareholders 1 mark max 4

Convention of Materiality Many transactions which affect the firm are so insignificant that the cost of recording and reporting them far outweigh the usefulness of the information derived 1 Hence insignificant matters need not be dealt with in accordance with strict accounting rules. 1 For example if a firm acquires a new door mat for the office, in theory every time someone walks on it part of this asset is used up and becomes an expense. 1 The accountant would regard the item as immaterial and would treat the item entirely as an expense to be treated as a cost for the year or incorporate the item under some other heading eg miscellaneous. 1 There is no agreement as to the exact line separating material items from immaterial items and the decision depends on judgement and common sense, which makes it a subjective opinion. 1 3 marks max Share Premium This is the difference between the issue price and nominal value of a share where the issued price is higher. 1 The premium must be shown in the Balance sheet as a reserve, which is not available for cash distribution. 1 The Premium may be used for: writing off preliminary and issue expenses 1 making bonus issue of shares 1 writing off discount on shares 1 writing off premium paid on redemption of redeemable preference shares or premium on redemption of ordinary shares under certain circumstances. 1 3 marks max

Page 7

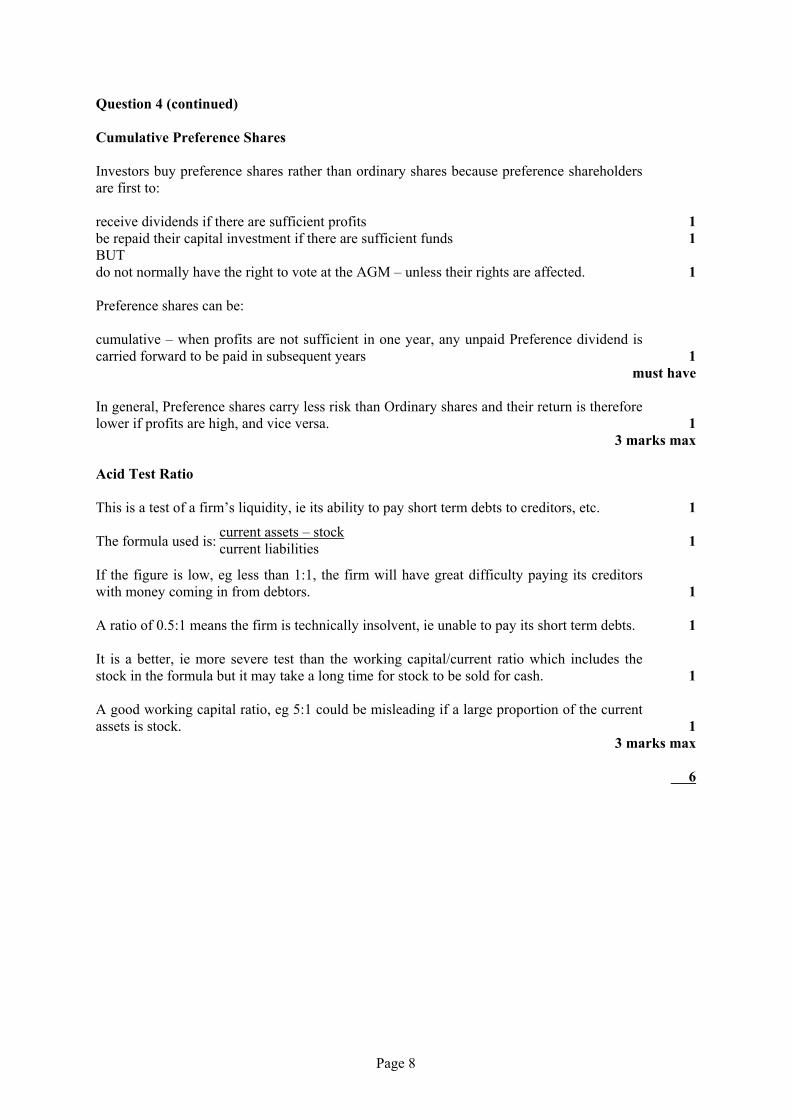

Question 4 (continued) Cumulative Preference Shares Investors buy preference shares rather than ordinary shares because preference shareholders are first to: receive dividends if there are sufficient profits 1 be repaid their capital investment if there are sufficient funds 1 BUT do not normally have the right to vote at the AGM – unless their rights are affected. 1 Preference shares can be: cumulative – when profits are not sufficient in one year, any unpaid Preference dividend is carried forward to be paid in subsequent years 1 must have In general, Preference shares carry less risk than Ordinary shares and their return is therefore lower if profits are high, and vice versa. 1 3 marks max Acid Test Ratio This is a test of a firm’s liquidity, ie its ability to pay short term debts to creditors, etc. 1 The formula used is: 1 current assets – stock

current liabilities If the figure is low, eg less than 1:1, the firm will have great difficulty paying its creditors with money coming in from debtors. 1 A ratio of 0.5:1 means the firm is technically insolvent, ie unable to pay its short term debts. 1 It is a better, ie more severe test than the working capital/current ratio which includes the stock in the formula but it may take a long time for stock to be sold for cash. 1 A good working capital ratio, eg 5:1 could be misleading if a large proportion of the current assets is stock. 1 3 marks max 6

Page 8

Question 5 Advantages of a PLC All shareholders have limited liability and cannot be held responsible for the PLC’s debts – (1) at least one partner must have unlimited liability to pay for the partnership’s debts out of personal funds. (1) The amount of capital can be greatly increased by appealing to the public for funds (1) – the partnership’s capital is limited to the no. of partners and the amount of their capital investment.(1) A PLC is a separate entity from its owners (shareholders) (1) and continues despite a change of shareholders (1) – a partnership is not a separate entity and cannot continue if a partner were to leave or die. (1) A PLC can raise additional capital more easily through the issue of debentures (1) – a partnership can only raise extra capital through loans which may be difficult to obtain. (1) The capital (ie value of shares) invested by shareholders in a PLC may increase as a result of the company’s success (1) – the capital of a partner remains the same as the amount invested. (1) Disadvantages of a PLC There are more legal formalities required to set up a PLC, eg memorandum (1) and articles of association – a partnership can be set up with no legal requirements. (1) There is more legal control over a PLC, eg the Companies Act – a partnership has fewer legal restrictions with which to conform. (1) There are more costs involved in setting up a PLC, eg printing and issuing of share certificates – a partnership can be set up with little or no cost. (1) Although shareholders in a PLC have voting rights, their say in the company’s affairs can be out-voted by a minority who hold the majority of shares or equity (1) – each partner has a say in the affairs of the partnership. (1) Shareholders in a PLC may not always receive a return on their investment, ie a dividend even when the company shows profit (1) – each partner will receive a share of any profit made by the firm. (1) Max 10

Page 9

Question 6

Page 10

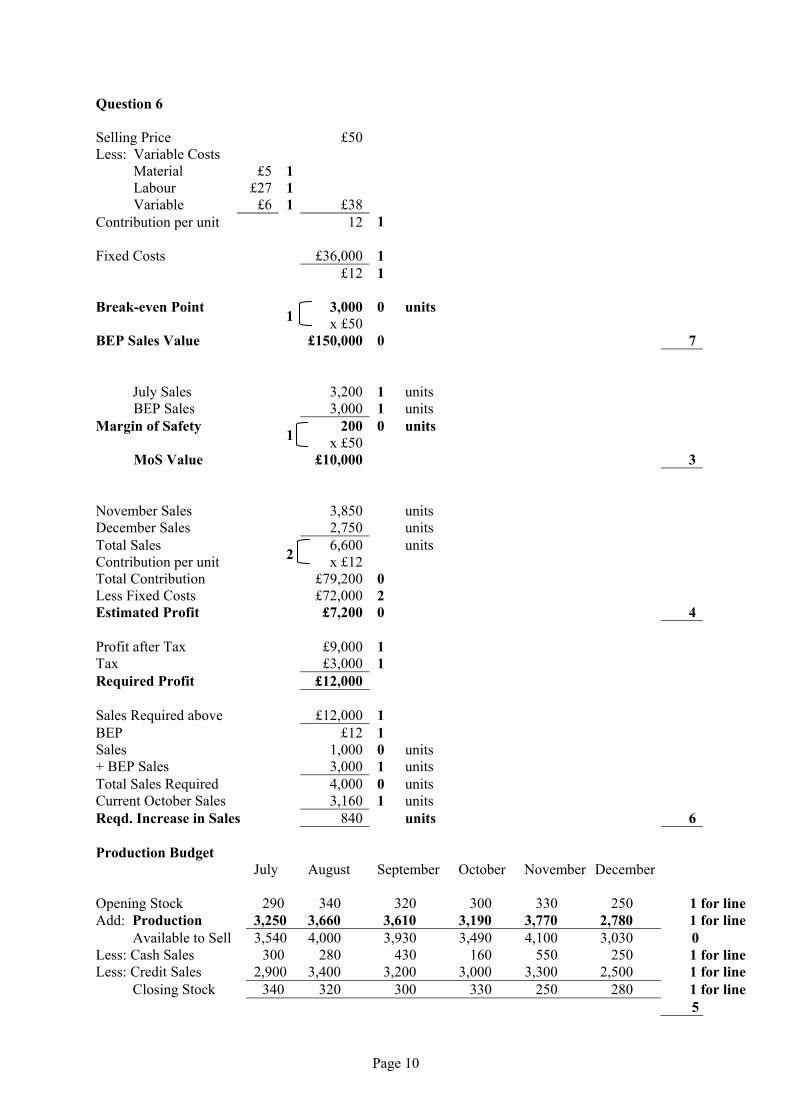

Selling Price £50 Less: Variable Costs Material £5 1 Labour £27 1 Variable £6 1 £38 Contribution per unit 12

1

Fixed Costs £36,000 1 £12 1 Break-even Point 3,000 0 units

1 x £50 BEP Sales Value £150,000 0 7 July Sales 3,200 1 units BEP Sales 3,000 1 units Margin of Safety 200 0 units

1 x £50 MoS Value £10,000 3 November Sales 3,850 units December Sales 2,750 units Total Sales 6,600 units Contribution per unit

2 x £12 Total Contribution £79,200 0 Less Fixed Costs £72,000 2 Estimated Profit £7,200 0 4 Profit after Tax £9,000 1 Tax £3,000 1 Required Profit £12,000 Sales Required above £12,000 1 BEP £12 1 Sales 1,000 0 units + BEP Sales 3,000 1 units Total Sales Required 4,000 0 units Current October Sales 3,160 1 units Reqd. Increase in Sales 840 units 6 Production Budget July August September October November December Opening Stock 290 340 320 300 330 250 1 for line Add: Production 3,250 3,660 3,610 3,190 3,770 2,780 1 for line Available to Sell 3,540 4,000 3,930 3,490 4,100 3,030 0 Less: Cash Sales 300 280 430 160 550 250 1 for line Less: Credit Sales 2,900 3,400 3,200 3,000 3,300 2,500 1 for line Closing Stock 340 320 300 330 250 280 1 for line 5

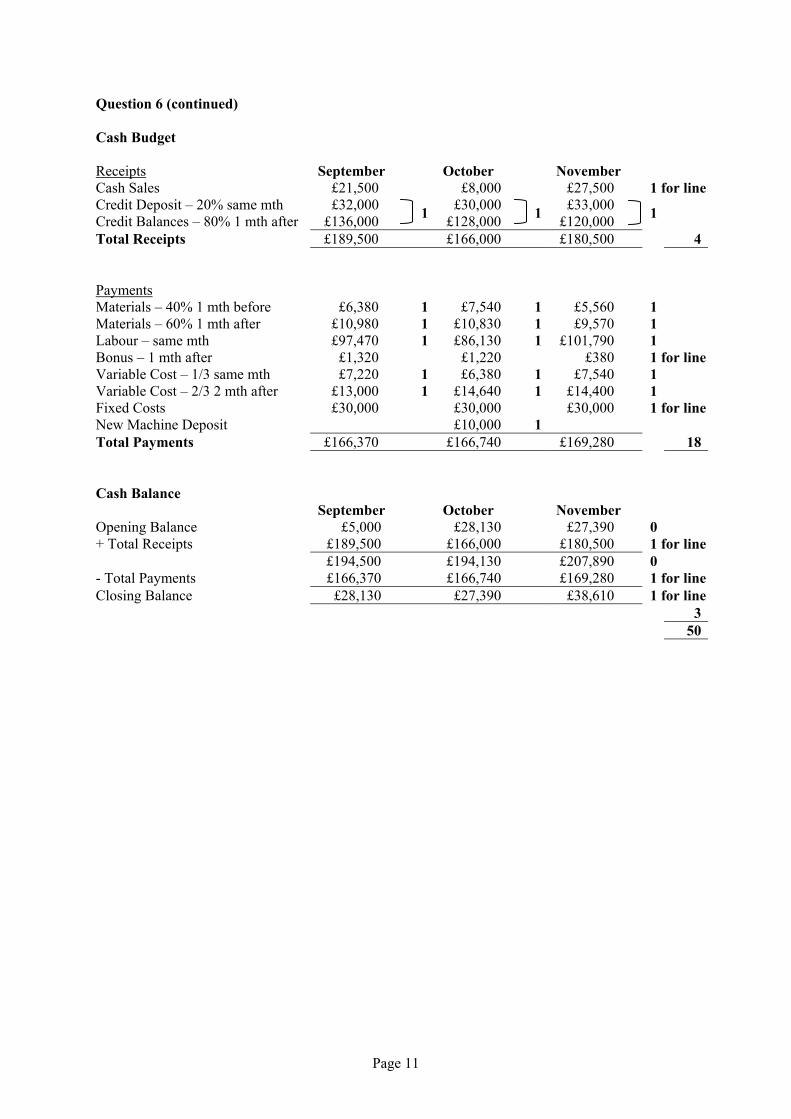

Question 6 (continued) Cash Budget Receipts September October November Cash Sales £21,500 £8,000 £27,500 1 for line Credit Deposit – 20% same mth £32,000 £30,000 £33,000 Credit Balances – 80% 1 mth after £136,000 1 £128,000 1 £120,000 1 Total Receipts £189,500 £166,000 £180,500 4 Payments Materials – 40% 1 mth before £6,380 1 £7,540 1 £5,560 1 Materials – 60% 1 mth after £10,980 1 £10,830 1 £9,570 1 Labour – same mth £97,470 1 £86,130 1 £101,790 1 Bonus – 1 mth after £1,320 £1,220 £380 1 for line Variable Cost – 1/3 same mth £7,220 1 £6,380 1 £7,540 1 Variable Cost – 2/3 2 mth after £13,000 1 £14,640 1 £14,400 1 Fixed Costs £30,000 £30,000 £30,000 1 for line New Machine Deposit £10,000 1 Total Payments £166,370 £166,740 £169,280 18 Cash Balance September October November Opening Balance £5,000 £28,130 £27,390 0 + Total Receipts £189,500 £166,000 £180,500 1 for line £194,500 £194,130 £207,890 0 - Total Payments £166,370 £166,740 £169,280 1 for line Closing Balance £28,130 £27,390 £38,610 1 for line 3 50

Page 11

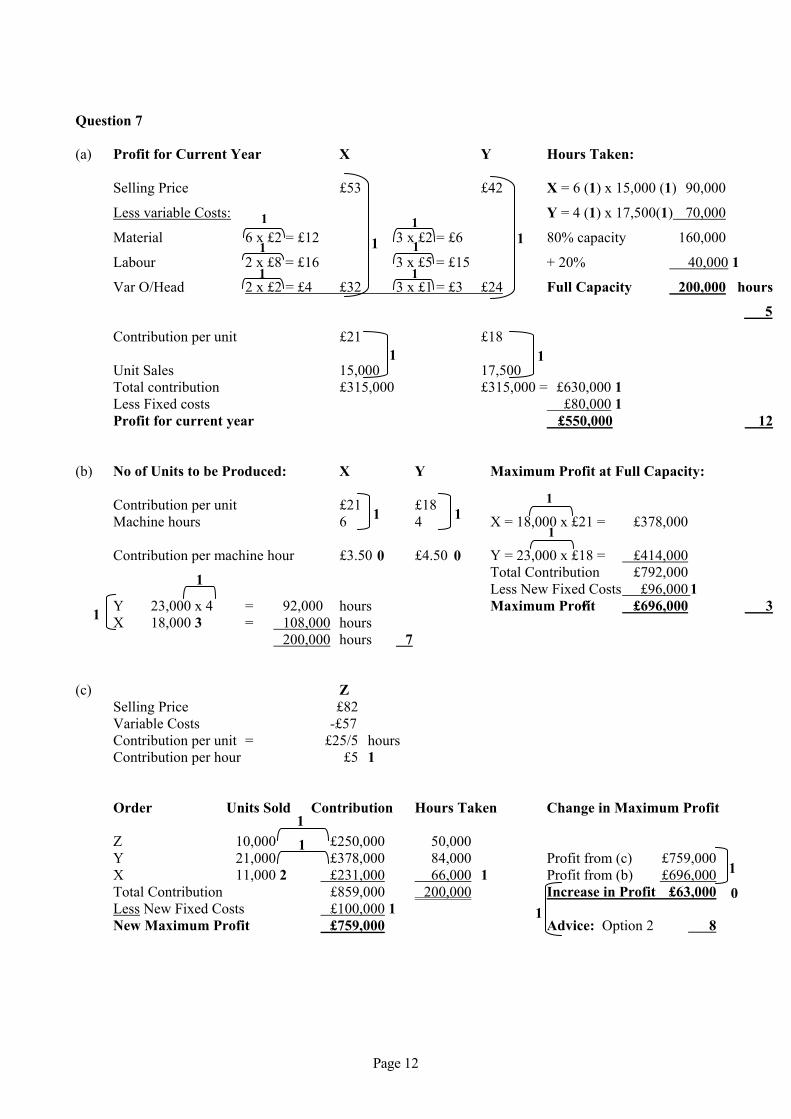

Question 7 (a) Profit for Current Year X Y Hours Taken: Selling Price £53 £42 X = 6 (1) x 15,000 (1) 90,000

Less variable Costs: Y = 4 (1) x 17,500(1) 70,000

Material 6 £2 = £12 3 £2 = £6 80% capacity 160,000

Labour 2 £8 = £16

Var O/Head 2 £2 = £4 £32

1

Contribution per unit £21 Unit Sales 15,0 Total contribution £315 Less Fixed costs Profit for current year (b) No of Units to be Produced: X Contribution per unit £21 Machine hours 6 Contribution per machine hour £3.5 Y 23,000 x 4 = 92,000 hour

1

X 18,000 3 = 108,000 hour 200,000 hour

(c) Z Selling Price £82 Variable Costs -£57 Contribution per unit = £25/5 Contribution per hour £5 Order Units Sold Contribu Z 10,000 £250, Y 21,000 £378,

1

X 11,000 2 £231, Total Contribution £859, Less New Fixed Costs £100, New Maximum Profit £759,

3 £5 = £15

3 £1 = £3 £24

£18

00 17,50,000 £315

Y Ma

£18 4 X =1

0 £4.50 Y =Tot

0

Less Mas s 7

hours 1

tion Hours Taken

000 50,000 000 84,000 000 66,000 1 000 200,000 000 1 000

Page 12

1

+ 20% 40,000 1Full Capacity 200,000 hours

5

1

0,00

xim

18

23al Cs Nxim

1

x

x1

x1

1

1 x1x

x1

0 = £630,000 1 £80,000 1 £550,000 12

um Profit at Full Capacity:

,0 0 x £21 = £378,000 1

,000 x £18 = £414,000 1

ontribution £792,000 ew Fixed Costs £96,000 1 um Profit £696,000 3

11

0Change in Maximum Profit

Profit from (c) £759,000 Profit from (b) £696,000 Increase in Profit £63,000

Advice: Option 2 8

1

1

1

0

0

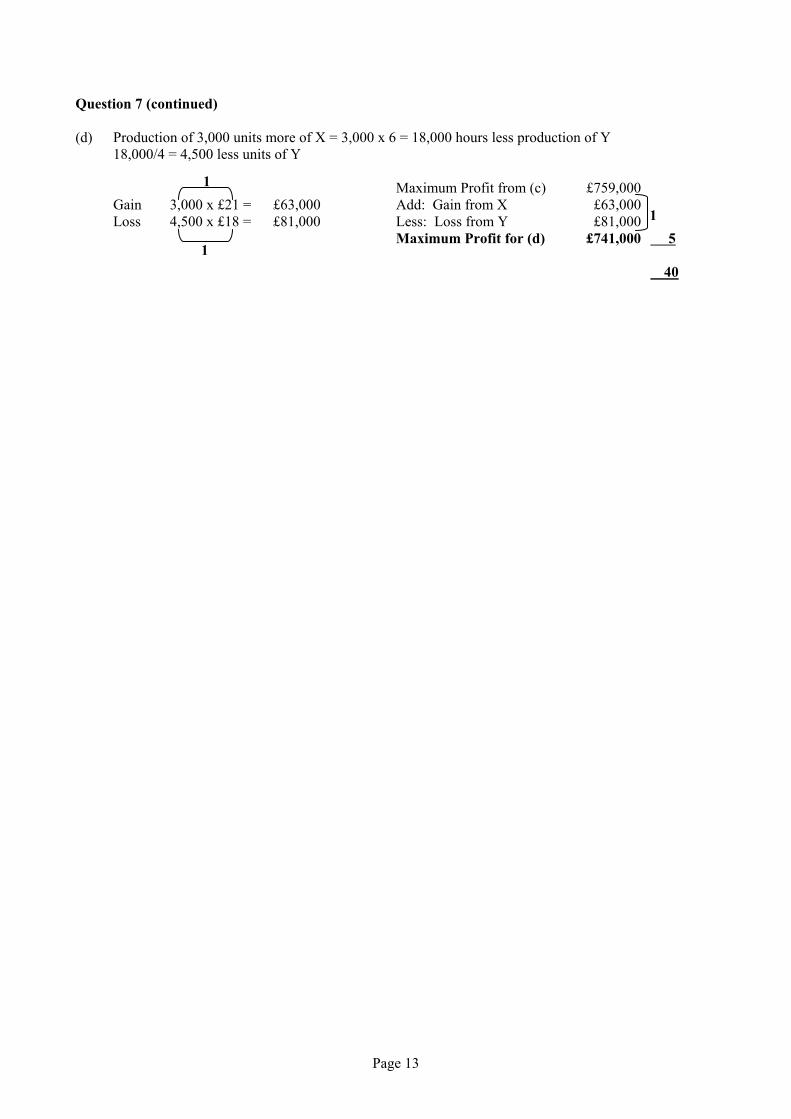

Question 7 (continued) (d) Production of 3,000 units more of X = 3,000 x 6 = 18,000 hours less production of Y 18,000/4 = 4,500 less units of Y Maximum Profit from (c) £759,000 Gain 3,000 x £21 = £63,000 Add: Gain from X £63,000 Loss 4,500 x £18 = £81,000 Less: Loss from Y £81,000 Maximum Profit for (d) £741,000 5

1

1

1

40

Page 13

Question 8 (a) Overhead Recovery Rate Assembly Finishing £30,000/£90,000 £40,000/4,000 hours 33.3% (2)

of material cost £10 (2)

per labour hour

4 (b) Overhead Over/Under Absorbed Assembly

O/Head Recovered = 1/3 x £87,000 = £29,000 3 Actual Overheads = £29,300 1 O/Head Under-absorbed 1 = £300 1 4 Finishing

O/Head Recovered = £10 x 4,200 hrs = £42,000 3 Actual Overheads = £41,500 1 O/head Over-absorbed 1 = £500 1 4

(c) Overhead Analysis Sheet Overheads Cost Assembly Finishing Maintenance Indirect material £6,000 0 £2,900 0 £1,460 0 £1,640 0 Supervision £30,000 0 £6,000 1 £21,000 1 £3,000 1 Insurance – B £2,000 0 £1,280 1 £560 1 £160 1 Insurance – M £3,000 0 £2,820 1 £180 1 Rent £15,000 0 £9,600 1 £4,200 1 £1,200 1 Depreciation – M £10,000 0 £9,400 1 £600 1 Power £4,000 0 £3,200 1 £800 1 Dept Totals £70,000 0 £35,200 £28,800 £6,000 1 for line Share of maintenance £4,800 1 £1,200 1 Dept Totals £40,000 0 £30,000 0 18

Page 14

Question 8 (continued) Working Supervision (workers) £30,000/100 £300.00 Insurance B (area) £2,000/25,000 £0.08 Insurance M (value) £3,000/£100,000 £0.03 Rent (area) £15,000/25,000 £0.60 Depreciation £10,000/£100,000 10% Power (hours) £4,000/20,000 £0.20

Maintenance (Machine hours) £6,000/25,000 £0.24

Recovery Rates Assembly = £40,000/£100,000 = 40% (0) 2 Finishing = £30,000/6000 hours = £5 (0) 2 4 (d) Job No. 4556

1 Materials = 1200 + 200 = £1,400 (0)

1

Labour = 60 + 150 = £210 (0)

1 Overhead – Assembly = 40% x 1200 = £480 (0)

1

Overhead – Finishing £5 x 10 hrs = £50 (0) Total Cost of job = £2,140 (0) Profit Margin = £535 (2) Selling Price of Job = £2,675 (0) 6 40

Page 15

Question 9 (a) Continuous stocktaking involves the counting of only some items on a cyclical basis 1

throughout the year, eg if a firm has 1200 items of stock it will count 100 different items each month and the year end all items would be counted. 1

The advantages of this method is that production is not disrupted and stock

losses/shortages are revealed sooner. Periodic stocktaking is when all stock items are counted and evaluated on specific

dates eg monthly or quarterly. 1 The method is simple but the disadvantage is that it results in production being

disrupted or even halted as workers may be used for the actual count. 1 4 (b) Abnormal Loss is a loss in production that is not expected or a loss that is higher than

expected. 1 Abnormal Loss is used in the calculation of the unit cost of production (1) and

therefore is given the same value as the finished goods in the process account. 1 The value of the abnormal loss is transferred to an abnormal loss account where it is

reduced by any sale/scrap value. 1 Thereafter the balance of this account is written off against profits at year end. 1 Max marks 3 Time rates are used to calculate wages on the basis of the amount of time worked, per

hour, per week, etc. 1 The formula for the amount of wages paid is: hours worked x rate per hour. 1 Time rates are suitable for skilled work where quality is more important than quantity

(1), or for workers who can work without the need for supervision. 1 Time rates are useful where the amount of work being done cannot be easily

measured. 1 Time rates are fairer where the amount of work is controlled by the speed of

machinery. 1 The main disadvantage of time rates is that wages are paid regardless of the amount of

work being done (1). There is no incentive for workers to do any more than necessary. 1

Max marks 3

Page 16

Question 9 (continued) Service Costing or Operational Costing means establishing the cost providing a

service rather than a product (1), eg transport/hospital. 1 mark max All costs – material, labour, overheads – are forecasted and totalled to find running

costs of the organisation for the year. 1 The total cost is then divided by a unit of cost to find the cost per unit of providing the

service. 1 The unit of cost will depend on the type of service being provided (1), eg transport =

cost per passenger mile, hospital = cost per patient day. 1 mark max 3 marks max P/V Ratio shows the relationship between contribution and sales. 1 The formula is: contribution/sales%. 1 The higher the ratio, the greater the profit. 1 The ratio can be improved by higher sales (or selling prices) or lower variable costs

(or cost prices) (1) or by using a product mix which gives the maximum contribution. 1 The ratio can be used for any level of sales and net profit can be found by deducting

fixed costs from contribution. 1 If a firm sells several products the ratio is useful to compare the profitability of each

product. 1 Max marks 3 6

Page 17

Page 18

Question 10 A management accountant will set up and manage a costing system which will: • provide more reliable product cost information 1 • help reduce/control material, labour, and overhead costs 1 • assess the profitability of different products 1 • identify reasons for cost differences, eg inferior materials, poor workmanship, etc 1 • establish objectives and sets targets for individuals, eg heads of departments to achieve 1 • identify responsibility for failure to reach targets for remedial action to be taken as

appropriate 1 • provide management with information that will help decision-making eg whether to

make or buy a component, accept a special order at a reduced price, purchase or lease equipment 1

• provide data that results in the most efficient use of limiting factors, eg if labour or material shortages exist 1

• compare the profitability of different products to establish order of priority of production 1

• provide information to enable budget/break-even statements/future investment plans to be prepared. 1

10

[END OF MARKING INSTRUCTIONS]