©2004 infonetrix llc all rights reserved worldwide 1-1 part one executive market briefing michael...

Post on 21-Dec-2015

213 views

TRANSCRIPT

1-1©2004 InfoNetrix LLC All Rights Reserved Worldwide

PART ONEExecutive Market Briefing

Michael A. Marullo Principal & Director

Strategic Market R&D

+ 1 504 466 3460

Market Horizons™ ReportMarket Horizons™ ReportReal-time Automation & Controls (RTAC) in the North

American Water/Wastewater Utilities Marketplace (2003-2007)

1-2©2004 InfoNetrix LLC All Rights Reserved Worldwide

About This Report

InfoNetrix LLC, an independent technical research and consulting firm specialized in

utility automation and information technology (Utility Automation/IT) markets

conducted the research for this report. InfoNetrix reports are available for

subscription by any and all interested parties, foreign and domestic (except as

prohibited by law), in accordance with the pricing and terms set forth in the

prospectus, provided separately.

This report addresses Real-time Automation & Controls (RTAC) in the North

American Water/Wastewater Utilities Marketplace. Other reports in the Market

Horizons™ Series provide similar analyses of Real-time Automation & Controls

(RTAC) in the North American Electric Utilities Marketplace and of Geospatial & Field

Automation Solutions (GFAS) in the North American Utilities Marketplace. Please

visit www.InfoNetrix.com for more information about these and other InfoNetrix

Advisory Services.

InfoNetrix LLC, an independent technical research and consulting firm specialized in

utility automation and information technology (Utility Automation/IT) markets

conducted the research for this report. InfoNetrix reports are available for

subscription by any and all interested parties, foreign and domestic (except as

prohibited by law), in accordance with the pricing and terms set forth in the

prospectus, provided separately.

This report addresses Real-time Automation & Controls (RTAC) in the North

American Water/Wastewater Utilities Marketplace. Other reports in the Market

Horizons™ Series provide similar analyses of Real-time Automation & Controls

(RTAC) in the North American Electric Utilities Marketplace and of Geospatial & Field

Automation Solutions (GFAS) in the North American Utilities Marketplace. Please

visit www.InfoNetrix.com for more information about these and other InfoNetrix

Advisory Services.

1-3©2004 InfoNetrix LLC All Rights Reserved Worldwide

General Information & Notifications

PURPOSE

The information contained in this document is for the sole use of InfoNetrix clients

and is not to be distributed outside client organizations. No part of this publication

may be reproduced, transcribed, or transmitted in any form or by any means,

electronic or mechanical, including photocopying, recording, or by any electronic

storage and retrieval system, without permission in writing from the copyright owner.

DISCLAIMER

This publication has been prepared with care, however, no guarantee of accuracy,

completeness, or warranty of any kind is expressed or implied, nor shall InfoNetrix

be liable to any user of the publication or any portion(s) hereof for any direct or

indirect damages, expenses, costs or losses of any kind resulting from its use.

COUNTRY OF ORIGIN

United States of America

PURPOSE

The information contained in this document is for the sole use of InfoNetrix clients

and is not to be distributed outside client organizations. No part of this publication

may be reproduced, transcribed, or transmitted in any form or by any means,

electronic or mechanical, including photocopying, recording, or by any electronic

storage and retrieval system, without permission in writing from the copyright owner.

DISCLAIMER

This publication has been prepared with care, however, no guarantee of accuracy,

completeness, or warranty of any kind is expressed or implied, nor shall InfoNetrix

be liable to any user of the publication or any portion(s) hereof for any direct or

indirect damages, expenses, costs or losses of any kind resulting from its use.

COUNTRY OF ORIGIN

United States of America

1-4©2004 InfoNetrix LLC All Rights Reserved Worldwide

Research Standards & Methodology

The preparation of this report follows generally accepted standards of market research practice and is based on principles of truthfulness and professionalism. A reasonable and prudent effort has been made to ensure that factors and circumstances having a material impact on any decision-making process derived from, or impacted by, this report are included in the analyses and recommendations. The representations of industry and market data and portrayals of the business environment are based on market research conducted by experienced professionals with broad knowledge and experience in the markets addressed.

The information upon which the findings and analyses contained in this report are based was obtained through a combination of telephone interviews with key suppliers and consultants and other individuals with extensive market knowledge and experience, augmented by survey with a cross section of utility managers and ongoing interactive research with over 1,000 utilities annually. Each telephone interview/survey was guided by a specially designed questionnaire to obtain pertinent data, insights and market perspectives. These interviews were augmented by secondary research across a wide range of reliable public and proprietary information sources pertinent to the study.

The preparation of this report follows generally accepted standards of market research practice and is based on principles of truthfulness and professionalism. A reasonable and prudent effort has been made to ensure that factors and circumstances having a material impact on any decision-making process derived from, or impacted by, this report are included in the analyses and recommendations. The representations of industry and market data and portrayals of the business environment are based on market research conducted by experienced professionals with broad knowledge and experience in the markets addressed.

The information upon which the findings and analyses contained in this report are based was obtained through a combination of telephone interviews with key suppliers and consultants and other individuals with extensive market knowledge and experience, augmented by survey with a cross section of utility managers and ongoing interactive research with over 1,000 utilities annually. Each telephone interview/survey was guided by a specially designed questionnaire to obtain pertinent data, insights and market perspectives. These interviews were augmented by secondary research across a wide range of reliable public and proprietary information sources pertinent to the study.

1-5©2004 InfoNetrix LLC All Rights Reserved Worldwide

Research Reliability & Acceptance

The information presented in this report was gathered, recorded and analyzed with care and precision. However, there will undoubtedly be differences between the findings presented and actual results for various reasons and, because future events and circumstances frequently do not occur as expected, those differences may be material.

For these and other reasons (including, but not necessarily limited to human error, misinterpretations, misunderstandings and information sensitivities among respondents), the resulting data will most likely not be completely accurate in all respects. Moreover, the forecasts presented herein reflect judgments made as of the period during which this report was prepared. As such, some aspects can be expected to change as a result of numerous direct and indirect factors, which are beyond the scope of this report to accurately predict. For example, it assumes that current events will continue to have the same effect on the marketplace in the future and that the conventional wisdom of today will continue to be completely applicable to future market conditions, which is at best, unlikely.

By accepting and using the information contained in this report, the user assumes all responsibility for its use for any and all purposes as user may deem appropriate and agrees to hold InfoNetrix, its principals and its staff harmless from any direct, indirect or consequential damages resulting from, or in any way related to, such use(s). However, InfoNetrix actively solicits and welcomes inquiries or other input regarding any errors, omissions or inconsistencies discovered during the course of using this report. Please direct any such correspondence to InfoNetrix Client Services.

(Detailed company contact information is provided on the web at: www.InfoNetrix.com.)

The information presented in this report was gathered, recorded and analyzed with care and precision. However, there will undoubtedly be differences between the findings presented and actual results for various reasons and, because future events and circumstances frequently do not occur as expected, those differences may be material.

For these and other reasons (including, but not necessarily limited to human error, misinterpretations, misunderstandings and information sensitivities among respondents), the resulting data will most likely not be completely accurate in all respects. Moreover, the forecasts presented herein reflect judgments made as of the period during which this report was prepared. As such, some aspects can be expected to change as a result of numerous direct and indirect factors, which are beyond the scope of this report to accurately predict. For example, it assumes that current events will continue to have the same effect on the marketplace in the future and that the conventional wisdom of today will continue to be completely applicable to future market conditions, which is at best, unlikely.

By accepting and using the information contained in this report, the user assumes all responsibility for its use for any and all purposes as user may deem appropriate and agrees to hold InfoNetrix, its principals and its staff harmless from any direct, indirect or consequential damages resulting from, or in any way related to, such use(s). However, InfoNetrix actively solicits and welcomes inquiries or other input regarding any errors, omissions or inconsistencies discovered during the course of using this report. Please direct any such correspondence to InfoNetrix Client Services.

(Detailed company contact information is provided on the web at: www.InfoNetrix.com.)

1-6©2004 InfoNetrix LLC All Rights Reserved Worldwide

Market Horizons™ Report Contents

1. Executive Market Briefing 2. Marketplace Characteristics

3. Market Drivers, Issues & Trends

4. Market Analysis & Future Outlook

5. Supplier Environment

1-7©2004 InfoNetrix LLC All Rights Reserved Worldwide

Executive Market Briefing

• Market Perspectives• Marketplace Structure & Composition• Prevailing Market Conditions• Market Analysis Synopsis• The 7 Signs7 Signs of Market Evolution (7 Signs)• Future Market Outlook• Suppliers & Competition• Summary/Conclusions

1-8©2004 InfoNetrix LLC All Rights Reserved Worldwide

"Everything that can be said has been said, but we have to say it again because no one was listening.”

- Andre Gide (French novelist)

Market PerspectivesMarket Research

1-9©2004 InfoNetrix LLC All Rights Reserved Worldwide

“You don't take technologies to market, you take products to market. A technology reaches the marketplace if it supports a product that provides utility and value."

- Alberto Leon-Garcia, IEEE Fellow & Professor, University of Toronto

Market PerspectivesTechnology & Innovation

1-10©2004 InfoNetrix LLC All Rights Reserved Worldwide

“Many of the plants have Supervisory Control and Data Acquisition (SCADA) systems for either their process monitoring or control. Plants that do not have around-the-clock operators may use SCADA to monitor or control their systems while the operator is not on site. Nineteen percent of the plants that treat ground water and do not have around-the-clock operators use SCADA for process monitoring; 14 percent use it for process control. The percentages double for surface water plants. For both ground water and surface water plants, large plants and plants in larger systems are more likely to use SCADA than small plants in smaller systems.”

US EPA815-R-02-005A; Community Water System Survey 2000; Volume 1: Overview; Office of Water (4607M); DEC 2002

Market PerspectivesSystem Operations

1-11©2004 InfoNetrix LLC All Rights Reserved Worldwide

“The notion that SCADA systems are highly customized, highly technical, and therefore the guys in the black hats won't be able to figure them out is something Eric Byres of the British Columbia Institute of Technology calls the ‘Myth of Obscurity’.

Forget it. SCADA documents have been recovered from al Qaeda safe houses in Afghanistan. An estimated 60 to 70 percent of all industrial security breaches are carried out by someone on the inside. There is no security through obscurity.”

- Excerpts from keynote address, as prepared by Dr. Arden Bement, Director - National Institute of Standards & Technology, at the NSF Workshop on Critical Infrastructure

Protection for SCADA & IT

October 20, 2003

Market PerspectivesSecurity & Data Integrity

1-12©2004 InfoNetrix LLC All Rights Reserved Worldwide

Marketplace Structure & CompositionWater/Wastewater Environment Cycle

Water Treatment

Plant

BoosterPumps

SewageTreatment

Post TreatmentStorage

Water PipesSewer Pipes

Reservoir

Ground WaterWells

River

Source Treatment Distribution Sewer/Treatment DischargeSource Treatment Distribution Sewer/Treatment DischargeSource Treatment Distribution Sewer/Treatment DischargeSource Treatment Distribution Sewer/Treatment Discharge

SOURCE: Sandia National Laboratories, Albuquerque, NM

1-13©2004 InfoNetrix LLC All Rights Reserved Worldwide

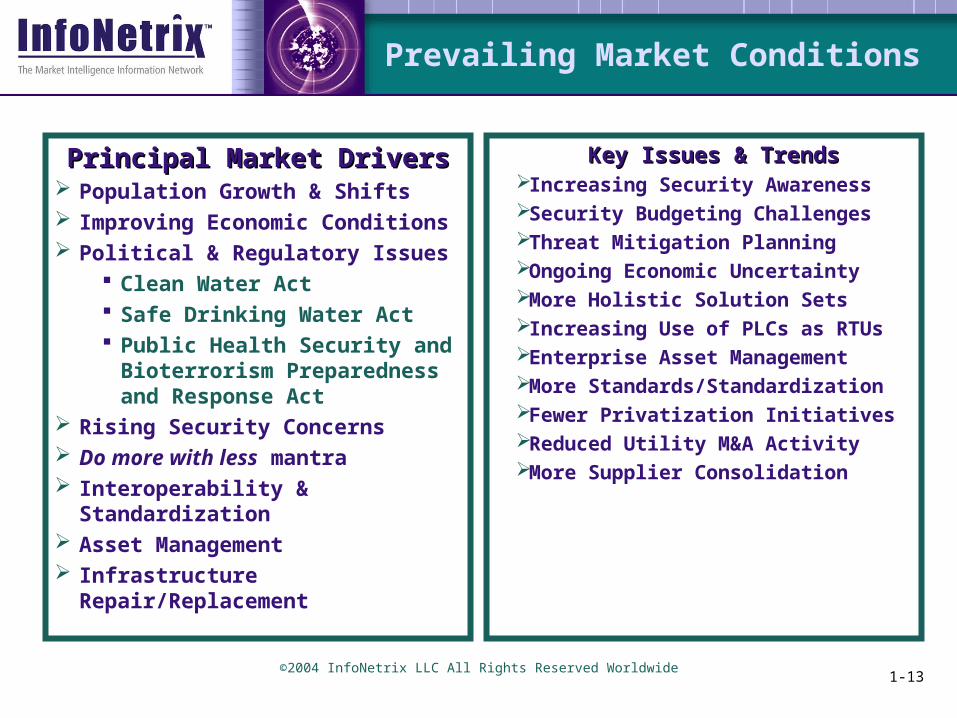

Prevailing Market Conditions

Principal Market DriversPrincipal Market Drivers Population Growth & Shifts Improving Economic Conditions Political & Regulatory Issues

Clean Water Act Safe Drinking Water Act Public Health Security and

Bioterrorism Preparedness and Response Act

Rising Security Concerns Do more with less mantra Interoperability & Standardization Asset Management Infrastructure Repair/Replacement

Key Issues & TrendsKey Issues & TrendsIncreasing Security AwarenessSecurity Budgeting ChallengesThreat Mitigation PlanningOngoing Economic UncertaintyMore Holistic Solution SetsIncreasing Use of PLCs as RTUsEnterprise Asset ManagementMore Standards/StandardizationFewer Privatization InitiativesReduced Utility M&A ActivityMore Supplier Consolidation

1-14©2004 InfoNetrix LLC All Rights Reserved Worldwide

Market Analysis Synopsis

• Expect slow but steady recovery following economic recession Municipal tax coffers drained as economy worsened Economic stability helped get some projects back on track Many utilities afraid to launch new projects until economic

recovery showed sustainability New security mandates further strained utility resources

• Privatization and M&A activity slowed during recession In some cases, privatization did not deliver promised

benefits and ran counter to political interests and expediency Merged utilities needed reorganization & recovery time

• Continued population growth will drive need for more and improved facilities EPA rules are continually being revised and tightened EPA reporting requirements becoming more demanding

1-15©2004 InfoNetrix LLC All Rights Reserved Worldwide

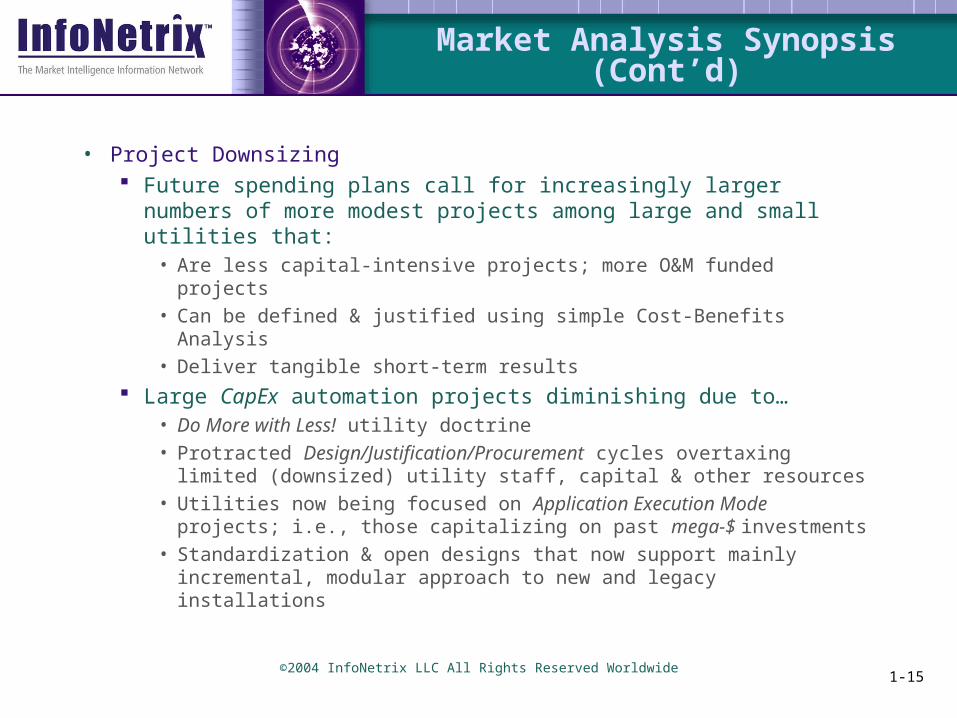

• Project Downsizing Future spending plans call for increasingly larger numbers of

more modest projects among large and small utilities that:• Are less capital-intensive projects; more O&M funded projects

• Can be defined & justified using simple Cost-Benefits Analysis

• Deliver tangible short-term results

Large CapEx automation projects diminishing due to…• Do More with Less! utility doctrine

• Protracted Design/Justification/Procurement cycles overtaxing limited (downsized) utility staff, capital & other resources

• Utilities now being focused on Application Execution Mode projects; i.e., those capitalizing on past mega-$ investments

• Standardization & open designs that now support mainly incremental, modular approach to new and legacy installations

Market Analysis Synopsis (Cont’d)

1-16©2004 InfoNetrix LLC All Rights Reserved Worldwide

• Regulatory & legislative mandates will redefine RTAC markets: Security issues are moving up the priority list and demand an

increasing portion of utility budgets, staff and resources• Some RTAC funds may be redirected or expanded for these purposes• No legislation is likely to specifically fund security improvements

Other mandates are also adding to the demand for better, faster, more accurate information, some of which is resident in RTAC systems and databases

• GASB-34 (Governmental Accounting Standards Board)– Establishes a new financial reporting model for state and local governments

(Key impact on municipal utilities)

– Biggest change in the history of public-sector accounting

• Sarbanes-Oxley Act– Defines new financial reporting rules for corporations in wake of Enron

collapse and corporate accounting scandals

– Primarily an IT issue but will eventually have links in and out of RTAC to validate operational data (Key impact on investor-owned utilities)

Market Analysis Synopsis (Cont’d)

1-17©2004 InfoNetrix LLC All Rights Reserved Worldwide

The 7 Signs of Market Evolution

1.Regulatory Policy & Governance

2.Economics & Investment

3.Technology/Integration/Standardization

4.Data Integrity & System Security

5.Web & Wireless Solutions

6.Enterprise Asset Management (EAM)

7.Customer Care & Satisfaction

SIGNSSIGNSSIGNSSIGNS

of Market Evolution

TheTheTheThe

1-18©2004 InfoNetrix LLC All Rights Reserved Worldwide

1: Regulatory Policy & Governance

• 2002-03: Utilities beginning to

comprehend security threat mitigation issues & costs

EPA funding for vulnerability assessments substantially depleted

Reporting requirements are onerous and getting worse!

• 2004-07: Security mandates will become a

major factor in future RTAC procurements; new & retrofit

Regulatory requirements (e.g., CWA & SDWA) driving more accurate & timely monitoring & reporting

GASB-34 & Sarbanes-Oxley have potentially significant long-term compliance implications

1-19©2004 InfoNetrix LLC All Rights Reserved Worldwide

2: Economics & Investment

• Economics Market recovery closely tied to

economic recovery, population growth & shifts

Municipals still struggling in wake of recession-induced tax funded deficits

More modest projects on the rise• Investment

Privatization still ongoing but slower paced now because:

• Some large privatization projects have been reversed or abandoned

– Atlanta (Canceled in 2002)– New Orleans (Dropped plans)

Some utilities are reluctant to invest despite budgeted projects for fear of being labeled spendthrifts until full economic recovery is apparent

QuickTime™ and aPhoto - JPEG decompressor

are needed to see this picture.

QuickTime™ and aPhoto - JPEG decompressor

are needed to see this picture.

1-20©2004 InfoNetrix LLC All Rights Reserved Worldwide

3: Technology/Integration/Standardization

•Technology Simple; open standards; low or

no maintenance Intuitive operation Easier to support & maintain

•Integration Plant-centric approach Enterprise Application

Integration (EAI) making inroads… slowly

Asset Management still incubating but starting to emerge

•Standardization ModBus (still) rules but also… Ethernet (the way of the future) DF1 (Allen-Bradley) DNP (growing)

1-21©2004 InfoNetrix LLC All Rights Reserved Worldwide

4: Data Integrity & System Security

•System Integrity

Data access & distribution plans

are being negatively impacted by

security concerns, but:

Web-based tools are powerful &

economical for non-critical and/or

monitor-only applications

Lowest Cost vs. Best Solution still

a difficult issue for most

municipal utilities

•Data Security Issues

Access by non-operations staff Corporate I/T network usage

creates new vulnerabilities Encryption & authentication may

be coming (e.g., AGA-12) for critical applications

1-22©2004 InfoNetrix LLC All Rights Reserved Worldwide

5: Web & Wireless Solutions

•Web

Many data access/distribution

vulnerabilities remain unsolved

• RCM/CBM heavily impacted by

bandwidth & access restrictions

• Web-based control on hold (for

now); surveillance-only growing

•Wireless

Coverage improvements driving

increased use But:

• Network saturation looms large

• Negatively impacted by security

issues

•Problems remain in both areas, but resolution is coming; big problems usually command big solutions!

1-23©2004 InfoNetrix LLC All Rights Reserved Worldwide

6: Enterprise Asset Management (EAM)

•EAM is all about the money; not the

technology; ROI/ROA are key

•Aging asset base & useful life extension

issues now evolving (Sweat the Assets!)

•EAM projects are driven by finance; not

engineering or operations

•First targets will be fast, easy pay-backs

•People are assets too (Brain-drain

remains a problem due to downsizing

and retiring workforce talent pools)

Expect increasing reliance on

automation to replace retirees

Increased use of RCM/CBM to extend

asset life; reduce risk

1-24©2004 InfoNetrix LLC All Rights Reserved Worldwide

7: Customer Care & Satisfaction

• Emerging issue for

water/wastewater

utilities

• Increased accountability and

reporting are coming

• Main impact areas for RTAC: Asset Management Work Management

• W/O Scheduling• W/O Assignment• W/O Processing• W/O Tracking

Workforce Management• Crew Allocation• Crew Dispatch/Recall

1-25©2004 InfoNetrix LLC All Rights Reserved Worldwide

Future Market OutlookAutomation & I/T Trends

Potential business benefits achievable

Pro

xim

ity

to c

ore

bu

sin

ess

PC Maintenance

Remote Metering

Internet

Systems Integration

SCADASCADA

External ApplicationDevelopment Call Center

Operation

Asset Management

SOURCE: DATAMONITORSOURCE: DATAMONITOR

Impact & Importance of Automation & IT Initiatives Among Utilities

Mission-critical

1-26©2004 InfoNetrix LLC All Rights Reserved Worldwide

• General Systems OutlookGeneral Systems Outlook RTAC Systems will see modest but steady growth across most

ASP ranges in both the number of opportunities and market values as more small utilities become buyers and larger utilities return to active (yet modest) project development as the economy improves.

• Systems Segment OutlookSystems Segment Outlook SCADA: Good growth for systems priced in lower ASP ranges

(≤750K) with increasing numbers of small utilities moving into digital telemetry and more modest, incremental projects among large utilities

PAS: Good growth for systems priced in middle to upper ASP ranges (≤750K-$5M) as plants prepare for faster, more accurate data acquisition under tighter CWA & SDWA rules

Hybrid: Good growth in systems priced in lower ASP ranges (≤750K) as utilities add SCADA to existing PAS systems

Future Market OutlookWWMS-RTAC Market Trends: Systems

1-27©2004 InfoNetrix LLC All Rights Reserved Worldwide

• General Field Data Devices OutlookGeneral Field Data Devices Outlook FDDs will continue to see good growth across most ASP ranges driven

by various factors including, but not limited to:• Increasingly tighter EPA requirements to satisfy CWA and SDWA rules

driving more data acquisition; better accuracy and reporting• Population growth and shifts placing more demands on aging infrastructure

and creating needs for new facilities• Influx of smaller utilities becoming more sophisticated

PLCs will continue to gradually displace conventional RTUs & DCS nodes due to increasing functionality, simplicity & standardization.

• Field Data Devices Segment OutlookField Data Devices Segment Outlook Distribution & Collection FDDs: Good growth in lower (≤$2K) ranges;

best growth in mainstream (≤$3.5K-$7.5K) ASP range. Most low-end units will be for SCADA expansion & adding SCADA to PAS projects.

Plant FDDs: Good growth across most ASP ranges; best growth in mainstream (≤$3.5K-$7.5K) ASP range; modest growth in lower (≤$2K) ranges. Many low-end units will be for adding SCADA to legacy PAS projects.

Future Market OutlookWWMS-RTAC Market Trends: FDDs

1-28©2004 InfoNetrix LLC All Rights Reserved Worldwide

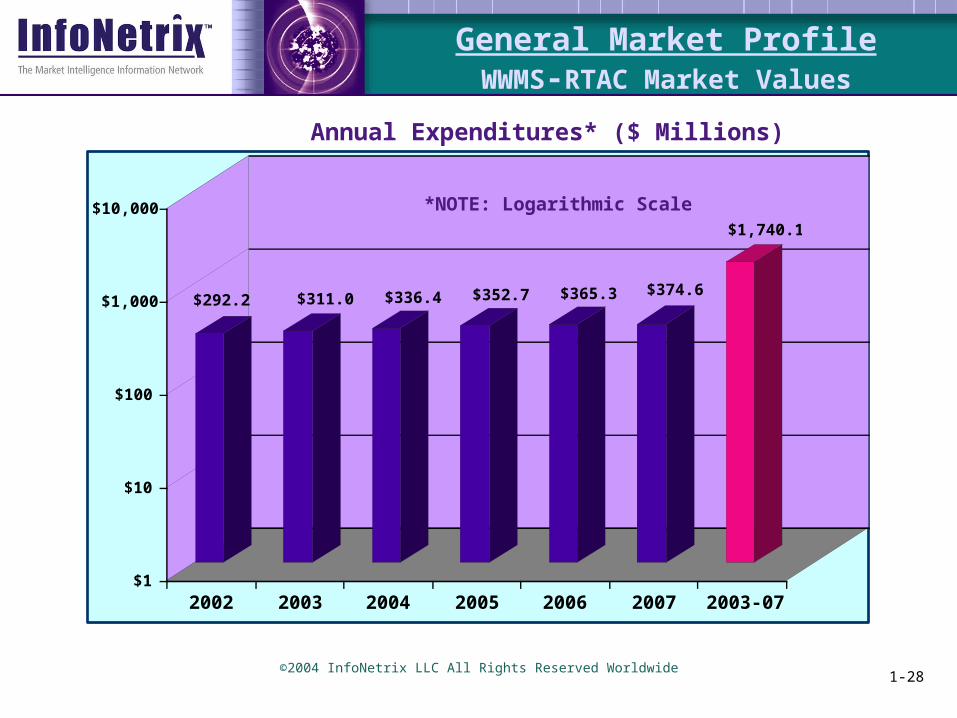

General Market ProfileWWMS-RTAC Market Values

$292.2 $311.0 $336.4 $352.7 $365.3 $374.6

$1,740.1

$1

$10

$100

$1,000

$10,000

2002 2003 2004 2005 2006 2007 2003-07

Annual Expenditures* ($ Millions)

*NOTE: Logarithmic Scale

1-29©2004 InfoNetrix LLC All Rights Reserved Worldwide

$219.9

$72.3

$234.7

$76.3

$255.7

$80.7

$266.9

$85.8

$276.4

$88.9

$285.0

$89.6

$0

$50

$100

$150

$200

$250

$300

$350

$400

2002 2003 2004 2005 2006 2007

All Systems Projects All Field Data Devices

Annual Expenditures ($Millions)

General Market ProfileMarket Composition & Contributions

1-30©2004 InfoNetrix LLC All Rights Reserved Worldwide

• Principal System Solution Providers ABB Bristol Babcock Emerson Process Management Honeywell Invensys-Foxboro Rockwell/Allen-Bradley Telvent Transdyn

Suppliers & CompetitionMarket Leadership: RTAC Systems

1-31©2004 InfoNetrix LLC All Rights Reserved Worldwide

• Principal FDD Suppliers Bristol Babcock Control Microsystems GE-Industrial (GE-Fanuc) Rockwell/Allen-Bradley Schneider Group (Square D; Modicon) Siemens Telvent (formerly Metso Automation)

Suppliers & CompetitionMarket Leadership: RTAC FDDs

1-32©2004 InfoNetrix LLC All Rights Reserved Worldwide

Summary/ConclusionsMarket Challenges & Critical Success Factors

Market Challenges…Market Challenges…• Suppliers

Solve major data security issues• Technological AND• Budgeting/Funding

Define Asset Management Communications transitions (e.g.,

from leased lines to wireless) Downward pressure on System &

FDD average selling prices • Utilities

Security compliance issues & costs

Reduced staff & resources M&A and restructuring activity Economic recovery following

recession

Critical Success Factors…Critical Success Factors…• Low Initial Price (Most MUNIs)• Open standards & open integration at all levels

• Reliability & Reputation for: Quality service & support Proper applications and skillful

execution Holistic solution set

• Ability to augment good products with good services

• Offer viable migration path to next generation products, technologies and applications

• Business Case & Cost/Benefit analysis (for IOUs and private water companies)

1-33©2004 InfoNetrix LLC All Rights Reserved Worldwide

• Short-term (2003-04):Short-term (2003-04): Rise of automation/IT role as part of:

• EPA tightening of monitoring & reporting rules• EPA demands for better, faster, more accurate data• New I/T requirements (GASB-34, Sarbanes-Oxley, etc.)• Enterprise Asset Management

• Long-term (2004-07):Long-term (2004-07): Need for investments in aging infrastructure Growing emphasis on standards and interoperability at

device, data (acquisition) and enterprise levels• Key Utility Key Utility Wants, Needs & ExpectationsWants, Needs & Expectations::

Economical, properly supported business solutions Intuitive; easy-to-own, operate & support technical solutions Solutions that address rising Asset Management objectives Clear, viable migration paths to the next level(s)

Summary/ConclusionsShort-term and Long-term Assessments