2003 economic outlook - bnp paribas

TRANSCRIPT

1

Philippe d�ArvisenetGroup Chief Economist

2003 ECONOMIC OUTLOOK

January 22th 2003

2

BNP PARIBAS RESEARCH DEPARTMENT

Mlle A. ESTIOTUSA, Canada01.43.16.95.52Mme. NEWHOUSE COHENUnited Kingdom, Ireland,Nordic countries01.43.16.95.50Mlle. AV. HERMEZJapan, AustraliaNew Zealand01.42.98.56.03R. VAN DER PUTTENEuroZone, Benelux25399J.M. LUCASFrance01.43.16.95.53Mlle. F. BARJOUItaly, Spain,Portugal, Greece01.42.98.27.62J.L. GUIEZEGermany, Austria, Switzerland01.42.98.43.86

E. VERGNAUDHead of OECD countries

01.42.98.49.80

M. L QUIGNONBanking economy01.42.98.56.54

V. NGUYEN THEHead of Banking economy

01.43.16.95.54

.Delphine CAVALIERAsia01.43.16.95.41R. GALLARDOLatin America01.42.98.56.10Mme. C. PELTIERLatin America01.42.98.26.77Mlle. N. NGOAsia01.43.16.95.44Mlle. E. VULLIEZAfrica01.42.98.56.27Mlle. A. KONATEAfrica01.42.98.02.04P. DEVAUXMiddle East - Scoring andwarning signals for country risk01.43.16.95.51Mlle. T. ESANURussia, Former Soviet Republics01.42.98.48.45F. FAUREEastern Europe, TurkeyCapital flows to emerging markets01.42.98.79.82

G. LONGUEVILLEHead of country risk

01.43.61.95.40

Philippe d'ARVISENETChief Economist01.43.16.95.58

Visit our website : http://www.economic-research.bnpparibas.com

Contact our team :

3

Graph 1

Cumulative GDP growth (q/q, %) since September 11th 2001

Q4 2002: BNPParibas forecasts

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

T4 200

1

T1 200

2

T2 200

2

T3 200

2

T4 200

2

United StatesEuro zoneJapanUK

4

UNITED STATES

5

United States

� Growth seems on the verge of reacceleration� Manufacturing ISM jumped to 54.7 in December after 3 months

below the 50 threshold� Leading indicators pointed to their second consecutive rise in

November� After a 2% growth at the turn of the year, activity should

accelerate, reaching potential by year end

� Consumption :� Household confidence has stabilized� The new Congress is to adopt a fiscal program aimed at

supporting growth : disposable income is to be supported untilthe job recovery takes place in H2

6

United States

� Capex is set to accelerate� The new tax cut plan is investment friendly� Corporate profits are to improve with GDP growth and

productivity gains� A lower dollar is favourable to pricing power

� The Fed will remain on hold, since risks are still a source ofconcern� Profits increase could still be impacted by goodwill write offs

and the defined benefits pensions issue� The war with Iraq could hurt investment and big ticket

purchases as it impacts confidence, incomes and costs (increasein oil prices)

� All in all, growth should accelerate to 2.5% in 2003 and 3.5%in 2004

7

Graph list

� 2 (page 9) : GDP, consumption and investment� 3 (page 9) : GDP growth and ISM indices� 4 (page 10) : Inventories/shipments ratio� 5 (page 10) : Industrial production and capacity utilization� 6 (page 11) : Nonresidential private investment� 7 (page 11) : Productivity and GDP growth� 8 (page 12) : GDP deflator and unit labor costs� 9 (page 13) : Corporate profits� 10 (page 13) : Investment & financing of corporate business� 11 (page 14) : Orders and profits� 12 (page 14) : 10-year interest rate spread� 13 (page 15) : Survey on bank lending practices� 14 (page 15) : Retail sales

United States

8

� 15 (page 16) : Unemployment and jobs creation� 16 (page 16) : Unemployment and initial claims� 17 (page 17) : The insecurity indicator� 18 (page 17) : Unemployment and Conference Board index� 19 (page 18) : Wages, prices and employment� 20 (page 19) : Real personal income� 21 (page 19) : Household investment and debt� 22-23 (page 20) : Household savings, debt and wealth� 24 (page 21) : Public budget and debt as % of GDP� 25 (page 21) : Current-account and foreign investments� 26 (page 22) : Interest rates and inflation� 27 (page 22) : Unemployment and Fed Funds rate

United States

9

Graphs 2 and 3

- 1 2

- 9

- 6

- 3

0

3

6

9

1 2

1 5

1 8

2 1

7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 2

R e a l G D PP r i v a t e c o n s u m p t i o nN o n r e s i d e n t i a l p r i v a t e f i x e d i n v e s t m e n t

G D P , c o n s u m p t i o n a n d i n v e s t m e n t( y / y % c h a n g e )

- 4

- 2

0

2

4

6

8

1 0

7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 22 5

3 0

3 5

4 0

4 5

5 0

5 5

6 0

6 5

7 0

7 5U n i t e d S t a t e s : e c o n o m i c g r o w t h a n d I S M i n d e x

R e a l G D P , y / y % c h a n g e

I S M T o t a l i n d e x

I S M N e w - o r d e r s i n d e x

4 2 . 7

10

Graphs 4 and 5

U n i t e d S t a t e s : i n v e n t o r i e s / s h i p m e n t s r a t i o , m a n u f a c t u r i n g

1 . 3

1 . 4

1 . 5

1 . 6

1 . 7

9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

- 1 5

- 1 0

- 5

0

5

1 0

1 5

7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 26 8

7 2

7 6

8 0

8 4

8 8

9 2U n i t e d S t a t e s : i n d u s t r i a l p r o d u c t i o n a n d c a p a c i t y u t i l i z a t i o n r a t e

C a p a c i t y u t i l i z a t i o n r a t e i n i n d u s t r y , %

I n d u s t r i a l p r o d u c t i o n ,y / y % c h a n g e

( 3 - m o n t h m o v i n g a v e r a g e s )

11

Graphs 6 and 7

8

9

1 0

1 1

1 2

1 3

1 4

6 0 6 2 6 4 6 6 6 8 7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 2

U n i t e d S t a t e s : n o n - r e s i d e n t i a l p r i v a t e i n v e s t m e n t a s % o f G D P

- 8

- 6

- 4

- 2

0

2

4

6

8

1 0

8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

( q / q c h a n g e , a n n u a l i z e d , % )

R e a l G D P

P r o d u c t i v i t y , n o n f a r m b u s i n e s s s e c t o r

U n i t e d S t a t e s : G D P a n d p r o d u c t i v i t y

12

Graph 8

-6

-4

-2

0

2

4

6

8

10

12

14

80 82 84 86 88 90 92 94 96 98 2000 2002

United States : price deflator and unit labor costs

(y/y % change)

GDP price deflator

Unit labor costsin manufacturing

13

Graphs 9 and 10

3

4

5

6

7

8

9

1 0

1 1

8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 2 0 0 0 2 0 0 2

U n i t e d S t a t e s : c o r p o r a t e p r o f i t s * a s % o f G D P

( * w i t h I V A & C C A D J )

B e f o r e t a x

A f t e r t a x

- 2

0

2

4

6

8

1 0

1 2

8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 2 0 0 0 2 0 0 2

U S A : i n v e s t m e n t a n d f i n a n c i n g o f n o n f a r m n o n f i n a n c i a l c o r p o r a t e b u s i n e s s

F i n a n c i n g g a p

G r o s s i n v e s t m e n t

( a s % o f G D P )

14

Graphs 11 and 12

- 6 0

- 4 0

- 2 0

0

2 0

4 0

6 0

8 0

1 0 0

9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

( * q u a r t e r l y c h a n g e , a n n u a l i z e d , % )

U n i t e d S t a t e s : o r d e r s a n d p r o f i t s

C o r p o r a t e p r o f i t s b e f o r e t a x w i t h I V A & C C A D J , y / y % c h a n g e

N e w o r d e r s o f n o n d e f e n s e c a p i t a l g o o d s e x c . A i r c r a f t *

C o r p o r a t e p r o f i t sb e f o r e t a x w i t h I V A & C C A D J *

0

1

2

3

4

5

6

7

8

1 0 - 9 5 0 4 - 9 6 1 0 - 9 6 0 4 - 9 7 1 0 - 9 7 0 4 - 9 8 1 0 - 9 8 0 4 - 9 9 1 0 - 9 9 0 4 - 0 0 1 0 - 0 0 0 4 - 0 1 1 0 - 0 1 0 4 - 0 2 1 0 - 0 23 . 5

4

4 . 5

5

5 . 5

6

6 . 5

7

A A A *

B B B *

B B *

U n i t e d S t a t e s : 1 0 - y e a r i n t e r e s t s p r e a d , %

s o u r c e s : D R I , D a t a s t r e a m

* s p r e a d c o r p o r a t e b o n d s - T . B o n d ( L H s c a l e )

T . B o n d r a t e

15

Graphs 13 and 14

- 2 0

- 1 0

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2- 4

- 2

0

2

4

6

8

1 0

1 2

1 4

l a r g e & m e d i u m c o m p a n i e ss m a l l b u s i n e s s e s

%

s o u r c e : F e d e r a l R e s e r v e ( S e n i o r L o a n O f f i c e r O p i n i o n S u r v e y )

N e t % o f b a n k r e s p o n d e n t s t i g h t e n i n g s t a n d a r d s f o r c o m m e r c i a l & i n d u s t r i a l l o a n s

( F e d - S e n i o r L o a n O f f i c e r O p i n i o n s u r v e y o n b a n k l e n d i n g p r a c t i c e s )

C r e d i t m a r k e t d e b t o f n o n f i n a n c i a l c o r p o r a t e

b u s i n e s s , y / y % c h a n g e

- 4

- 2

0

2

4

6

8

1 0

1 2

1 4

9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

U n i t e d S t a t e s : r e t a i l s a l e s

( q u a r t e r l y c h a n g e , a n n u a l i z e d , % )

T o t a l

T o t a l e x c l m o t o r v e h i c l e & p a r t s

16

Graphs 15 and 16

3 . 5

4

4 . 5

5

5 . 5

6

6 . 5

7

7 . 5

8

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3- 4 0 0

- 3 0 0

- 2 0 0

- 1 0 0

0

1 0 0

2 0 0

3 0 0

4 0 0U n i t e d S t a t e s : u n e m p l o y m e n t a n d j o b s c r e a t i o n t h o u s a n d

U n e m p l o y m e n t r a t e , %

M o n t h l y c h a n g e i n e m p l o y m e n t ,

3 - m o n t h m o v i n g a v e r a g e

2 5 0

3 0 0

3 5 0

4 0 0

4 5 0

5 0 0

5 5 0

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 31

2

3

4

5

6

7

8U n i t e d S t a t e s : u n e m p l o y m e n t a n d i n i t i a l c l a i m st h o u s a n d s %

T o t a l u n e m p l o y m e n t r a t e

I n i t i a l c l a i m s f o r u n e m p l o y m e n t i n s u r a n c e

( m o n t h l y d a t a )

I n s u r e d u n e m p l o y m e n t r a t e

17

Graphs 17 and 18

6

8

1 0

1 2

1 4

1 6

1 8

7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 2

J o b l e a v e r s a s % o f t o t a l u n e m p l o y e d

U n i t e d S t a t e s : t h e i n s e c u r i t y i n d i c a t o r

3

4

5

6

7

8

9

1 0

1 1

7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 20

2 0

4 0

6 0

8 0

1 0 0

1 2 0

1 4 0

1 6 0

1 8 0

2 0 0U n e m p l o y m e n t a n d C o n f e r e n c e B o a r d

C o n f e r e n c e B o a r d i n d e x :p r e s e n t s i t u a t i o n

U n e m p l o y m e n t r a t e

%

C o n f e r e n c e B o a r d i n d e x :e x p e c t a t i o n s

18

Graph 19

0

2

4

6

8

10

82 84 86 88 90 92 94 96 98 00 02-400

-200

0

200

400

600

* y/y, %Inflation *

United States : earnings, inflation and employment

Average hourly earnings,private sector *

Monthly change in employment, 3-month moving average,

thousand

19

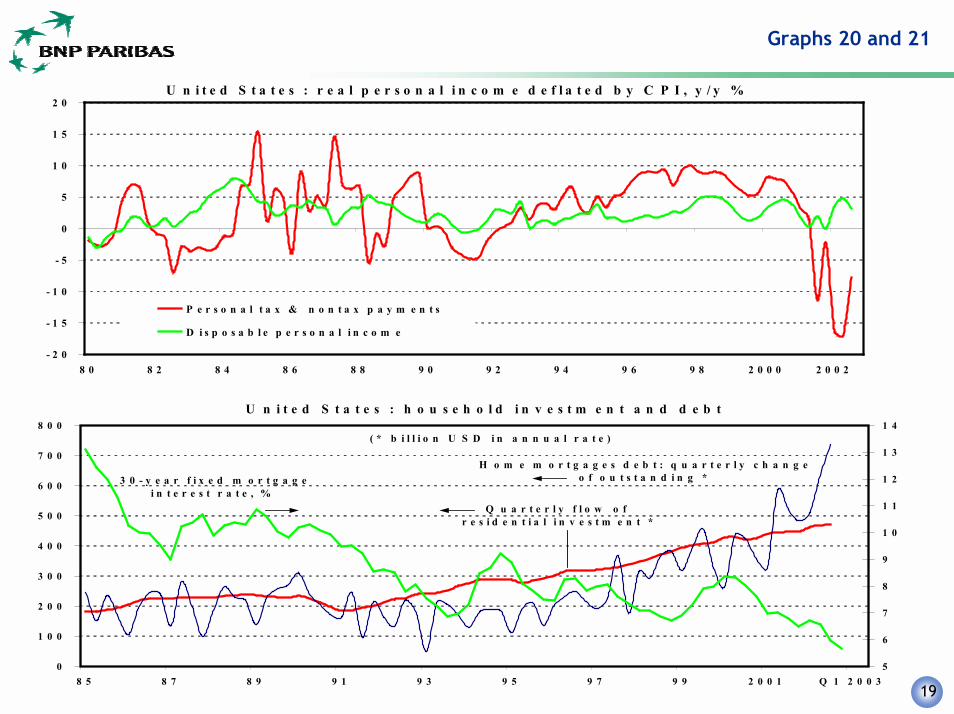

Graphs 20 and 21

- 2 0

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 2 0 0 0 2 0 0 2

P e r s o n a l t a x & n o n t a x p a y m e n t s

D i s p o s a b l e p e r s o n a l i n c o m e

U n i t e d S t a t e s : r e a l p e r s o n a l i n c o m e d e f l a t e d b y C P I , y / y %

0

1 0 0

2 0 0

3 0 0

4 0 0

5 0 0

6 0 0

7 0 0

8 0 0

8 5 8 7 8 9 9 1 9 3 9 5 9 7 9 9 2 0 0 1 Q 1 2 0 0 35

6

7

8

9

1 0

1 1

1 2

1 3

1 4U n i t e d S t a t e s : h o u s e h o l d i n v e s t m e n t a n d d e b t

( * b i l l i o n U S D i n a n n u a l r a t e )

Q u a r t e r l y f l o w o f r e s i d e n t i a l i n v e s t m e n t *

H o m e m o r t g a g e s d e b t : q u a r t e r l y c h a n g eo f o u t s t a n d i n g * 3 0 - y e a r f i x e d m o r t g a g e

i n t e r e s t r a t e , %

20

Graphs 22 and 23

0

2

4

6

8

1 0

1 2

1 4

7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 29 0

1 2 0

1 5 0

1 8 0

2 1 0

2 4 0

2 7 0

3 0 0

3 3 0

3 6 0

3 9 0

4 2 0U n i t e d S t a t e s : h o u s e h o l d s a v i n g s r a t e a n d w e a l t h

S a v i n g s r a t e

N e t f i n a n c i a l a s s e t s

( a s % o f p e r s o n a l d i s p o s a b l e i n c o m e )

R e a l e s t a t e a s s e t s

0

2

4

6

8

1 0

1 2

1 4

1 6

1 8

6 0 6 2 6 4 6 6 6 8 7 0 7 2 7 4 7 6 7 8 8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 2

P e r s o n a l s a v i n g s r a t e , %

U n i t e d S t a t e s : h o u s e h o l d s a v i n g s a n d d e b t

C r e d i t m a r k e t d e b t , y / y % c h a n g e

21

Graphs 24 and 25

- 6

- 5

- 4

- 3

- 2

- 1

0

1

2

3

8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 e 0 3 p4 0

4 5

5 0

5 5

6 0

6 5

7 0

7 5

8 0

B u d g e t b a l a n c eD e b t

U n i t e d S t a t e s : b u d g e t b a l a n c e a n d d e b t a s % o f G D P

s o u r c e s O E C D , B N P P a r i b a s

- 5 0 0

- 4 0 0

- 3 0 0

- 2 0 0

- 1 0 0

0

1 0 0

2 0 0

3 0 0

4 0 0

8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 2

C u r r e n t - a c c o u n t b a l a n c eD i r e c t i n v e s t m e n tE q u i t i e sB o n d sG o v t s e c u r i t i e s

( o n e - y e a r m o v i n g a v e r a g e o f f l o w s , a n n u a l i z e d d a t a s i n b i l l i o n U S D )

U n i t e d S t a t e s : c u r r e n t - a c c o u n t b a l a n c e a n d f o r e i g n i n v e s t m e n t s

22

Graphs 26 and 27

1

2

3

4

5

6

7

8

9

1 0

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

3 - m o n t h1 0 - y e a r3 0 - y e a rI n f l a t i o n y / y

U n i t e d S t a t e s : i n t e r e s t r a t e s a n d i n f l a t i o n%

( m o n t h l y a v e r a g e s )

0

4

8

1 2

1 6

2 0

7 0 7 1 7 2 7 3 7 4 7 5 7 6 7 7 7 8 7 9 8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

R e c e s s i o n p e r i o d sU n e m p l o y m e n t r a t eF e d F u n d s

U n i t e d S t a t e s : u n e m p l o y m e n t a n d F e d F u n d s r a t e

23

EURO ZONE

24

Euro zone

� Economic activity� Euroland avoided recession last year but growth has been

mediocre in 2002: 1.6% annualized in Q1 and Q2, it hasdisappointed even more in Q3 (1.3%)

� Leading indicators point to more weakness in the coming months� All in all, growth is not expected to be higher than 0.8% in 2002

and 1.25% in 2003

� Monetary policy� Unchanged from November 2001 to November 2002� Last summer, ECB considered the inflationary risks as dominant.

Economic activity was disappointing but unit labor costs wereaccelerating and core inflation was creeping up. That was aninvitation to keep a restrictive stance

� Financial turbulence and the deterioration in the economicoutlook have changed the landscape

25

Euro zone

� Sentiment indicators went back to their early 1999 level when ECBcut rates down to 2.5%

� ECB has to takes the growth outlook into consideration (second pillar)

� Monetary policy is set to become more accommodative� 2 years in a row (a 3rd coming) with growth below potential will bring

a moderation in core inflation� specific supply shocks (energy, food, introduction of notes and coins

in euros) will stop impacting headline inflation in 2003 H1� the appreciation of the euro has tightened monetary conditions� the rhetoric has changed : last spring, the inflationary risk was

considered as dominant, during the summer risks were �balanced�,since September, growth outlook has become a source of concern.ECB finally delivered � we see more to come

� Revision of monetary policy during 2003 H1 (M3, inflation targetceiling)

� Coordination with fiscal policy. When EcoFin declared it launched aprocedure vis a vis Portugal and EC announced the possibility of earlywarnings (France close to a 3% deficit) and an excessive deficitprocedure for Germany, the path towards lower rates opened

26

Graph list

� 28 (page 28) : Euro zone / USA, GDP growth� 29 (page 28) : Euro zone / USA, industrial production� 30-31 (page 29): Euro zone / USA, industrial & consumer

confidences� 32-33 (page 30) : PMI� 34 (page 31) : Euro zone / USA, total employment� 35 (page 31) : Euro zone / USA, unemployment rate� 36-37 (page 32) : ECB repo rate, confidence and inflation� 38 (page 33) : Interest rates� 39 (page 33) : Inflation and PMI� 40 (page 34) : Euro zone / USA, capacity utilization rate� 41 (page 34) : Labor costs

Euro zone

27

� 42-43 (page 35) : Budget balance / country� 44 (page 36) : USA / Euro zone, interest and exchange rates� 45 (page 36) : USA, direct investments

Euro zone

28

Graphs 28 and 29

- 8

- 6

- 4

- 2

0

2

4

6

8

1 0

1 2

1 4

8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

E u r o Z o n eU S A

U n i t e d S t a t e s / E u r o z o n e : G D P g r o w t h( q / q c h a n g e a n n u a l i z e d , % )

- 8

- 6

- 4

- 2

0

2

4

6

8

1 0

8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

U S AE u r o Z o n e

U n i t e d S t a t e s / E u r o z o n e : i n d u s t r i a l p r o d u c t i o n

( y / y % c h a n g e )

29

Graphs 30 and 31

3 5

4 0

4 5

5 0

5 5

6 0

6 5

8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3- 3 5

- 3 0

- 2 5

- 2 0

- 1 5

- 1 0

- 5

0

5

1 0U n i t e d S t a t e s / E u r o z o n e : i n d u s t r i a l c o n f i d e n c e

E u r o z o n e ( b a l a n c e o f o p i n i o n s , % , E u r o p e a n C o m m i s s i o n )

U n i t e d S t a t e s ( I S M i n d e x )

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 5 0

8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3- 3 0

- 2 5

- 2 0

- 1 5

- 1 0

- 5

0

5U n i t e d S t a t e s / E u r o z o n e : c o n s u m e r c o n f i d e n c e

E u r o z o n e( b a l a n c e o f o p i n i o n s , % ,E u r o p e a n C o m m i s s i o n )U n i t e d S t a t e s

( C o n f e r e n c e B o a r d i n d e x )

30

Graphs 32 and 33

4 0

4 5

5 0

5 5

6 0

6 5

0 7 - 9 7 0 1 - 9 8 0 7 - 9 8 0 1 - 9 9 0 7 - 9 9 0 1 - 0 0 0 7 - 0 0 0 1 - 0 1 0 7 - 0 1 0 1 - 0 2 0 7 - 0 2 0 1 - 0 3

T o t a l i n d e xN e w o r d e r sO u t p u t

E u r o z o n e : P u r c h a s i n g M a n a g e r s ' i n d i c e s

s o u r c e R e u t e r s

4 0

4 5

5 0

5 5

6 0

6 5

9 8 9 9 0 0 0 1 0 2 0 3

E u r o z o n eF r a n c eG e r m a n yI t a l y

P u r c h a s i n g M a n a g e r s ' i n d i c e s

s o u r c e R e u t e r s

31

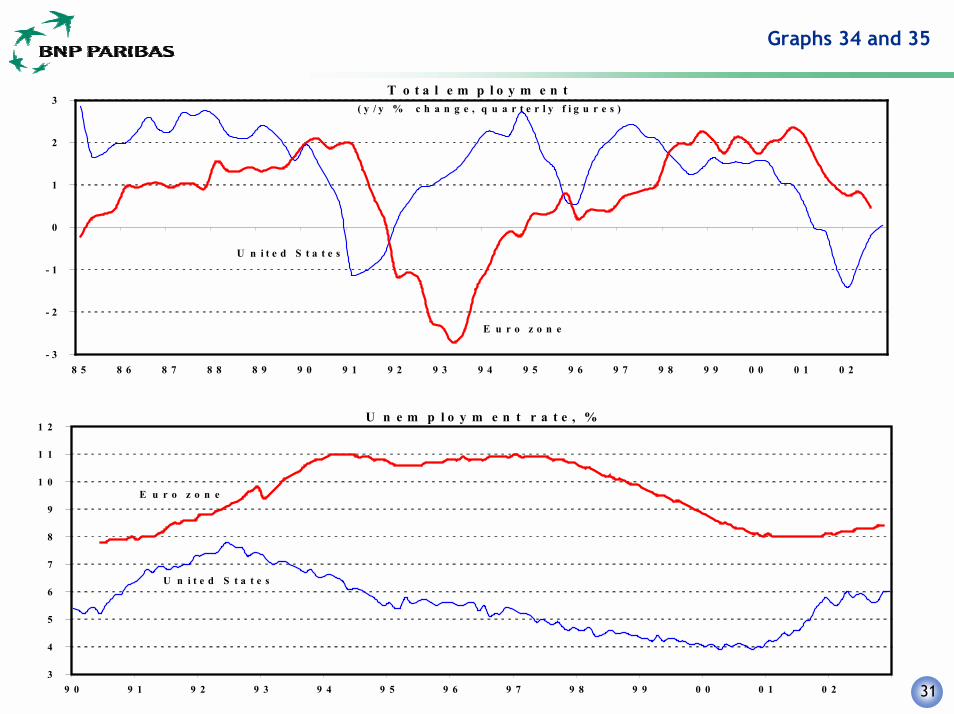

Graphs 34 and 35

- 3

- 2

- 1

0

1

2

3

8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

T o t a l e m p l o y m e n t

E u r o z o n e

U n i t e d S t a t e s

( y / y % c h a n g e , q u a r t e r l y f i g u r e s )

3

4

5

6

7

8

9

1 0

1 1

1 2

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

U n e m p l o y m e n t r a t e , %

E u r o z o n e

U n i t e d S t a t e s

32

Graphs 36 and 37

0 . 5

1 . 0

1 . 5

2 . 0

2 . 5

3 . 0

3 . 5

4 . 0

4 . 5

5 . 0

1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3

T o t a l i n f l a t i o n

C o r e i n f l a t i o n

E u r o z o n e : E C B r e p o r a t e a n d i n f l a t i o n

E C B s h o r t - t e r m r e p o r a t e

2 . 0

2 . 5

3 . 0

3 . 5

4 . 0

4 . 5

5 . 0

1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3- 2 5

- 2 0

- 1 5

- 1 0

- 5

0

5

1 0E u r o z o n e : E C B r e p o r a t e a n d c o n f i d e n c e

C o n s u m e r c o n f i d e n c e *

E C B s h o r t - t e r m r e p o r a t e

* b a l a n c e o f o p i n i o n s ( E u r o p e a n C o m m i s s i o n )

I n d u s t r i a l c o n f i d e n c e *

33

Graphs 38 and 39

0 . 5

1 . 0

1 . 5

2 . 0

2 . 5

3 . 0

3 . 5

4 . 0

4 . 5

5 . 0

1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3

E u r o z o n e : i n t e r e s t r a t e s

R e a l 1 0 - y e a r r a t e

R e a l 3 - m o n t h r a t e

E C B s h o r t - t e r m r e p o r a t e

E u r o z o n e : i n f l a t i o n a n d P M I

0 . 5

1

1 . 5

2

2 . 5

3

3 . 5

4 0 4 5 5 0 5 5 6 0 6 5

Infla

tion,

y/y

%

P M I I n d i c e

j u i l - 9 7

o c t - 0 2o c t - 0 1s e p t - 0 1

m a i - 0 1

d é c - 9 8

f é v r - 9 9

m a r s - 9 8

a v r - 0 0

34

Graphs 40 and 41

7 2

7 4

7 6

7 8

8 0

8 2

8 4

8 6

8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

E u r o z o n e / U n i t e d S t a t e s : c a p a c i t y u t i l i z a t i o n r a t e , %

( m a n u f a c t u r i n g s e c t o r )

U n i t e d S t a t e s E u r o z o n e

- 2

- 1

0

1

2

3

4

9 6 9 7 9 8 9 9 2 0 0 0 2 0 0 1 2 0 0 2

U n i t l a b o u r c o s t

L a b o u r p r o d u c t i v i t y

E u r o z o n e : l a b o u r c o s t s

( y / y % c h a n g e )

E C B s o u r c e

35

Graphs 42 and 43

-8 0

-6 0

-4 0

-2 0

0

2 0

4 0

6 0

8 0

1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 o c t -0 1 o c t -0 2

C u r r e n t - a c c o u n t b a la n c e

- 2 5 0

- 2 0 0

- 1 5 0

- 1 0 0

-5 0

0

5 0

1 0 0

1 5 0

1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 o c t-0 1 o c t-0 2

D ir e c t in v e s t m e n tE q u ity in v e s tm e n tD e b t in s t r u m e n t s in v .

-8

-7

-6

-5

-4

-3

-2

-1

0

1 9 9 5 1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 e 2 0 0 3 p

Z o n e e u r o A lle m a g n e

F r a n c e I ta l ie

E t t é i i B N P P ib

D é f ic it p u b l ic e n % d u P I B

- 1 4

- 1 2

- 1 0

-8

-6

-4

-2

0

1 9 9 0 1 9 9 1 1 9 9 2 1 9 9 3 1 9 9 4 1 9 9 5 1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1

A l le m a g n eF r a n c eI ta l ie

D é f ic i t s t r u c tu r e l e n % d u P I B

s o u r c e O C D E

-8

-7

-6

-5

-4

-3

-2

-1

0

1

1 9 9 5 1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 e 2 0 0 3 p

E u r o z o n e G e r m a n y

F r a n c e I ta ly

s o u r c e E u r o s ta t , B N P P a r ib a s f o r e c a s ts

P u b l ic b u d g e t a s % o f G D P

- 8

- 6

- 4

- 2

0

1 9 9 5 1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 e 2 0 0 3 p

G e r m a n yF r a n c eI t a ly

S tr u c tu r a l b u d g e t a s % o f G D P

O E C D s o u r c e & f o r e c a s ts

36

Graphs 44 and 45

- 2

- 1 . 5

- 1

- 0 . 5

0

0 . 5

1

1 . 5

2

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 30 . 8

0 . 9

1

1 . 1

1 . 2

1 . 3

1 . 4U n i t e d S t a t e s / E u r o z o n e : i n t e r e s t r a t e & e x c h a n g e r a t e

E U R / U S D e x c h a n g e r a t e

( m o n t h l y a v e r a g e s )

U S A - G e r m a n y : 1 0 - y e a r i n t e r e s t s p r e a d , %

- 5

- 4

- 3

- 2

- 1

0

1

2

3

8 0 8 2 8 4 8 6 8 8 9 0 9 2 9 4 9 6 9 8 2 0 0 0 2 0 0 2

C u r r e n t - a c c o u n t b a l a n c eD i r e c t i n v e s t m e n tC o r p o r a t e - e q u i t i e s p u r c h a s e sU S c o r p o r a t e b o n d s

U n i t e d S t a t e s : p o r t f o l i o a n d d i r e c t i n v e s t m e n t s

( n e t a s % o f n o m i n a l G D P , 2 - q u a r t e r m o v i n g a v e r a g e )

37

JAPAN

38

Japan

� A rebound in exports in Q2 has been followed by anacceleration in consumption and government expenditure inQ3

� The favourable momentum is eroding (confidence and leadingindicators are disappointing)

� Deflationary pressures are an impediment to self-sustainedgrowth

� The deterioration in the labor market is weighting on incomesand confidence

� Monetary policy has no impact on the real economy. Theeconomic situation of Japan is adversely impacted by theburden of banks�NPLs and its consequences on credit

39

Japan

� The latest �anti-deflation� and stimulus plans are notambitious enough to push prices upwards nor revive growth

� The health of the financial sector is the key question. Banksrecap by the government seems unavoidable as well asunorthodox monetary measures

40

Japan

Graph list

� 46 (page 41) : GDP and industrial production� 47 (page 41) : Foreign and domestic demands� 48 (page 42) : Profits and business climate� 49 (page 43) : Industrial production and inventories� 50 (page 43) : Orders and leading indicator� 51 (page 44) : Labor market� 52 (page 44) : Wages and prices� 53 (page 45) : Public budget and debt� 54 (page 45) : Interest and exchange rates� 55 (page 46) : Monetary sector� 56 (page 46) : Bank reserves

41

Graphs 46 and 47

- 8

- 6

- 4

- 2

0

2

4

6

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

G D P v o l u m eI n d u s t r i a l p r o d u c t i o n

( q u a r t e r l y c h a n g e , % )

J a p a n : G D P a n d i n d u s t r i a l p r o d u c t i o n

- 6

- 4

- 2

0

2

4

6

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 2 0 0 0 2 0 0 1 2 0 0 2

D o m e s t i c d e m a n d

J a p a n : f o r e i g n a n d d o m e s t i c d e m a n d s

E x p o r t s o f G o o d s & S e r v i c e s

I m p o r t s o f G o o d s & S e r v i c e s

( v o l u m e , q u a r t e r l y c h a n g e % )

42

Graph 48

-50

-40

-30

-20

-10

0

10

20

30

40

50

90 91 92 93 94 95 96 97 98 99 00 01 02

Japan: profits and business climate

Current profits, all industries, y/y % change

Tankan surveys: business condition, actual situation, all industries, %

43

Graphs 49 and 50

6 5

7 0

7 5

8 0

8 5

9 0

9 5

1 0 0

1 0 5

1 1 0

1 1 5

1 2 0

8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

I n d u s t r i a l p r o d u c t i o nI n v e n t o r y r a t i o

J a p a n : i n d u s t r i a l p r o d u c t i o n a n d i n v e n t o r i e s

( i n d i c e s , 1 9 9 5 = 1 0 0 )

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2- 2 8

- 2 1

- 1 4

- 7

0

7

1 4

2 1

2 8J a p a n : o r d e r s a n d l e a d i n g i n d i c a t o r

E P A l e a d i n g i n d i c a t o r

O r d e r s f o r m a c h i n e s ,

y / y % c h a n g es o u r c e : C a b i n e t O f f i c e o f J a p a n

( 3 - m o n t h m o v i n g a v e r a g e s )

44

Graphs 51 and 52

- 2 . 5

- 2

- 1 . 5

- 1

- 0 . 5

0

0 . 5

1

1 . 5

2

2 . 5

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 31 . 5

2

2 . 5

3

3 . 5

4

4 . 5

5

5 . 5

6T h e l a b o u r m a r k e t i n J a p a n

U n e m p l o y m e n t r a t e , %

T o t a l e m p l o y m e n t , y / y % c h a n g e

- 4

- 2

0

2

4

6

8

1 0

8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

J a p a n : w a g e s a n d i n f l a t i o n

C o n s u m e r p r i c e i n d e x

A v e r a g e e a r n i n g s ( 6 - m o n t h m o v i n g a v e r a g e )

( y / y % c h a n g e )

45

Graphs 53 and 54

- 1 0

- 8

- 6

- 4

- 2

0

2

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 e 0 3 p5 0

7 0

9 0

1 1 0

1 3 0

1 5 0

1 7 0J a p a n : f i s c a l b a l a n c e a n d p u b l i c d e b t a s % o f G D P

P u b l i c d e b t

F i s c a l b a l a n c e

2 0 0 2 - 2 0 0 3 : B N P P a r i b a s f o r e c a s t s

0

1

2

3

4

5

6

7

8

9

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 38 0

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 5 0

1 6 0

1 7 0% J a p a n : i n t e r e s t & e x c h a n g e r a t e s

( m o n t h l y a v e r a g e )

U S D / J P Y e x c h a n g e r a t e

3 - m o n t h i n t e r e s t r a t e

1 0 - y e a r i n t e r e s t r a t e

46

Graphs 55 and 56

- 2 0

- 1 0

0

1 0

2 0

3 0

4 0

5 0

9 7 9 8 9 9 0 0 0 1 0 2

J a p a n : m o n e t a r y s e c t o r , y / y % c h a n g e

M 2 + C D

M o n e t a r y b a s e

2

4

6

8

1 0

1 2

1 4

1 6

1 8

2 0

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

J a p a n : b a n k r e s e r v e s , t r i l l i o n J P Y

R e q u i r e d r e s e r v e s

T o t a l r e s e r v e s

B a n k o f J a p a n s o u r c e

47

UNITED KINGDOM

48

United Kingdom

� UK Q3 GDP growth was revised upwards from 0.8% to 0.9%q/q. Nonetheless without the technical impact of the GoldenJubilee extra holidays in June, GDP should have been lower,growing around 0.6% over the period

� UK Q4 GDP is likely to have decelerated further : Householdconsumption has slowed down both in November andDecember ; the manufacturing sector is still in the doldrums ;its output perspectives are low and no early rebound inbusiness investment can be expected in this context ; UKgoods exports are hurt by the weakness in euro-zone activity

� Despite an all-time low unemployment rate (3.1%, accordingto the claimant count definition), the job market is notlooking as bright as before: part time jobs are rising at theexpense of full time jobs; manufacturing jobs have beensteadily destroyed since 1998

49

United Kingdom

� Public expenditure should continue to back growth in 2003.Nonetheless, the government could be compelled to raisetaxes before the end of this year in order to meet its deficittarget. Indeed, its assumption on economic growth, around2.5% for this year, looks very much too optimistic comparedto our of 1.8%

� Inflation is likely to overshoot the Bank of England�s target(2.5% on a 2-year horizon) during most of this year. Rising oilprices as well house prices impact on the house depreciationcomponent are mainly to blame on

� The housing market evolution is no more sustainable. Weassume that the rate of price increase should orderlyslowdown during this year. However a U-turn in the marketcan�t be totally excluded and could well be triggered by afurther weakness in stocks coupled with renewed threat ofterrorist attacks in the UK

50

United Kingdom

� The Bank of England�s leeway is very tight in this context.The main risk to its central scenario is a larger or earlier thanexpected deceleration in households� consumption.Therefore, monetary authorities are to remain very prudentat least during the first half of this year

� By June 2003, the Treasury will issue its conclusions on the 5tests whether the UK should join the euro or not. Given afavourable conclusion, a referendum is unlikely to be calledthis year. Indeed there is still a large public opposition to theSterling entry into the euro. Nonetheless, a �yes� vote at theSwedish Referendum on September 14 could gradually beginchanging British mentalities

� In this context, the Sterling should weaken further versus theeuro, falling around 0.67 by the end of this year

51

United Kingdom

Graph list

� 57 (page 52) : Real GDP growth� 58 (page 52) : Industrial production and retail sales� 59 (page 53) : CBI industrial survey� 60 (page 53) : Retail sales and confidence� 61 (page 54) : House price index� 62 (page 54) : Average earnings� 63-64 (page 55) : Labour costs� 65 (page 56) : Inflation� 66 (page 56) : Public budget as % of GDP� 67 (page 57) : Interest rates� 68 (page 57) : Exchange and interest rates

52

Graphs 57 and 58

- 6

- 4

- 2

0

2

4

6

1 9 9 5 1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2

R e a l G D PS e r v i c e sI n d u s t r y

U K : r e a l G D P g r o w t h

( y / y % c h a n g e )

- 8

- 6

- 4

- 2

0

2

4

6

8

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

U K : i n d u s t r i a l p r o d u c t i o n a n d r e t a i l s a l e s

( y / y % c h a n g e )

I n d u s t r i a l p r o d u c t i o n

R e t a i l s a l e s , v o l u m e

53

Graphs 59 and 60

- 7 0

- 6 0

- 5 0

- 4 0

- 3 0

- 2 0

- 1 0

0

1 0

2 0

3 0

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

T o t a l o r d e r b o o kE x p o r t o r d e r b o o kB u s i n e s s o p t i m i s m

U K : C B I i n d u s t r i a l s u r v e y

( b a l a n c e o f o p i n i o n s , % )

- 2

- 1

0

1

2

3

4

5

6

7

9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3- 3 0

- 2 5

- 2 0

- 1 5

- 1 0

- 5

0

5

1 0U K : r e t a i l s a l e s a n d c o n s u m e r c o n f i d e n c e

C o n s u m e r c o n f i d e n c e : b a l a n c e o f o p i n i o n s

R e t a i l s a l e s , v o l u m e : 3 - m t h m a v , y - o - y % c h a n g e

54

Graphs 61 and 62

- 1 0

- 5

0

5

1 0

1 5

2 0

2 5

3 0

3 5

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

U K : h o u s e p r i c e i n d e x

( a l l h o u s e s , y / y % c h a n g e )

H a l i f a x s o u r c e

0

2

4

6

8

1 0

1 2

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

U n i t e d K i n g d o m : a v e r a g e e a r n i n g s

( y / y % c h a n g e )

s o u r c e O N S

P r i v a t e s e c t o r

P u b l i c s e c t o r

55

Graphs 63 and 64

- 4

- 2

0

2

4

6

8

1 0

1 2

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

U K : l a b o u r c o s t s

( y / y % c h a n g e )

U n i t w a g e c o s t s

A v e r a g e e a r n i n g s

T a r g e t : 4 . 5 %

- 4

- 2

0

2

4

6

8

1 0

1 2

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2

U K : l a b o u r c o s t s

( 3 - m o n t h m o v i n g a v e r a g e o f t h e y / y % c h a n g e )

U n i t w a g e c o s t s

A v e r a g e e a r n i n g s

T a r g e t : 4 . 5 %

56

Graphs 65 and 66

- 2

0

2

4

6

8

1 0

1 2

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

U n i t e d K i n g d o m : i n f l a t i o n

( y / y % c h a n g e )

A l l g o o d s

A l l s e r v i c e s

- 8

- 6

- 4

- 2

0

2

4

6

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 e 0 3 p4 0

4 5

5 0

5 5

6 0

6 5U K : p u b l i c a c c o u n t s a s % o f G D P

P u b l i c d e b t

P u b l i c s e c t o r b a l a n c e O E C D s o u r c e

57

Graphs 67 and 68

0

2

4

6

8

1 0

1 2

1 4

1 6

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3

U K : i n t e r e s t r a t e s

I n t e r b a n k 3 - m o n t h r a t e

1 0 - y e a r b o n d y i e l d

( m o n t h l y a v e r a g e , % )

1 . 4

1 . 4 5

1 . 5

1 . 5 5

1 . 6

1 . 6 5

1 . 7

1 . 7 5

j a n v - 9 9 j u i l - 9 9 j a n v - 0 0 j u i l - 0 0 j a n v - 0 1 j u i l - 0 1 j a n v - 0 2 j u i l - 0 2 j a n v - 0 30

0 . 8

1 . 6

2 . 4

3 . 2U K / E u r o z o n e : e x c h a n g e r a t e a n d i n t e r e s t r a t e s p r e a d

3 - m o n t h i n t e r e s t r a t e s p r e a d , % : U K - E u r o z o n e

G B P / E U R e x c h a n g e r a t e

( w e e k l y d a t a )

58

This publication was produced by a BNP Paribas Company. It will have been approved for publication and distribution in the UnitedKingdom by BNP Paribas London Branch, a branch of BNP Paribas SA whose Head Office is in Paris, France. BNP Paribas LondonBranch is regulated by the Financial Services Authority (�FSA�), for the conduct of its designated investment business in the UnitedKingdom and is a member of the London Stock Exchange. BNP Paribas Securities Corp. in the United States accepts responsibility forthe contents of this publication in circumstances where the report has been distributed by BNP Paribas Securities Corp. direct to U.Srecipients.

This publication reflects the view of the Economic Research Department of BNP Paribas. It is published for information purposesonly. Neither the information nor the opinion expressed constitutes an offer or solicitation to buy or sell any investments. Informationcontained herein has been obtained from sources believed to be reliable but BNP Paribas does not guarantee its accuracy orcompleteness. All opinions and forecasts are subject to change. Discretion with respect to suitability should prudently exercised.

A BNP Paribas Group Company and/or persons connected with it may effect or have effected a transaction for their own account inthe investments referred to in the material contained in this report or any related investment before the material is published to anyBNP Paribas Group Company�s customers. On the date of this report a BNP Paribas Group Company, persons connected with it andtheir respective directors and/or representatives and/or employees may have a long or short position in any of the investmentsmentioned in this report and may purchase and/or sell the investments at any time in the open market or otherwise, in each caseeither as principal or as agent. Additionally, a BNP Paribas Group Company within the previous twelve months may have acted as aninvestment banker or may have provided significant advice or investment services to the companies or in relation to theinvestment(s) mentioned in this report.

This publication is not intended for private customers in the UK (as defined by the rules of the FSA) and should notbe passed to such persons.By accepting this publication you agree to be bound by the foregoing limitations.