20-f 2001 ing

TRANSCRIPT

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F [ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR [X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2001

Commission file number 1-14878

GERDAU S.A. (Exact Name of Registrant as Specified in its Charter)

Federative Republic of Brazil

(Jurisdiction of Incorporation or Organization)

N/A (Translation of Registrant's name into English)

Av. Farrapos 1811

Porto Alegre, Rio Grande Do Sul - Brazil CEP 90220-005 (Address of principal executive offices) (Zip code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class Preferred Shares, no par value per share, each represented by American Depositary Shares

Name of Each Exchange in Which Registered New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation

pursuant to Section 15(d) of the Act:

None

The total number of issued shares of each class of stock of GERDAU S.A. as of December 31, 2001 was: 39,382,020,386 Common Shares, no par value per share 74,109,685,986 Preferred Shares, no par value per share Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No Indicate by check mark which financial statement item the Registrant has elected to follow Item 17 Item 18 X .

i

TABLE OF CONTENTS

Page

INTRODUCTION ................................................................................................................................................................ 1

PART I.................................................................................................................................................................................. 2 ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS................................ 2 ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE .................................................................. 2 ITEM 3. KEY INFORMATION.......................................................................................................................... 2 ITEM 4. INFORMATION ON THE COMPANY............................................................................................. 10 ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS .................................................... 32 ITEM 6. DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES ...................................................... 40 ITEM 7. MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS .................................. 46 ITEM 8. FINANCIAL INFORMATION........................................................................................................... 47 ITEM 9. THE OFFER AND LISTING................................................................................................................ 48 ITEM 10. ADDITIONAL INFORMATION..................................................................................................... 52 ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK .............. 60 ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES.................................. 62

PART II................................................................................................................................................................................. 62 ITEM 13. DEFAULTS, DIVIDEND ARREARAGES AND DELIQUENCIES .............................................. 62 ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND

USE OF PROCEEDS...................................................................................................................................... 63 ITEM 15. .............................................................................................................................................................. 63 ITEM 16. .............................................................................................................................................................. 63

PART III................................................................................................................................................................................ 64 ITEM 17. FINANCIAL STATEMENTS........................................................................................................... 64 ITEM 18. FINANCIAL STATEMENTS........................................................................................................... 64 ITEM 19. FINANCIAL STATEMENTS AND EXHIBITS ............................................................................. 64

F-1

INTRODUCTION Unless otherwise indicated, all references herein (i) to the "Company" or to "Gerdau" are references to Gerdau S.A., a corporation organized under the laws of the Federative Republic of Brazil ("Brazil") and its consolidated subsidiaries, and (ii) to "Prefe rred Shares" and "Common Shares" refer to the Company's authorized and outstanding preferred stock and common stock, designated as ações preferenciais and ações ordinárias, respectively, each without par value. All references herein to the "real," "reais" or "R$" are to the Brazilian real, the official currency of Brazil. All references to (i) "U.S. dollars," "dollars" or "U.S.$" are to United States dollars, (ii) "billions" are to thousands of millions, (iii) "km" are to kilometers, and (iv) "tons" denote metric tons. The Company has prepared the consolidated financial statements included herein in conformity with accounting principles generally accepted in the United States ("U.S. GAAP").

CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS

Statements made in this annual report with respect to the Company’s current plans, estimates, strategies and beliefs and other statements that are not historical facts are forward-looking statements about the Company’s future performance. Forward-looking statements include but are not limited to those using words such as “believe”, “expect”, “plans”, “strategy”, “prospects”, “forecast”, “estimate”, “project”, “anticipate”, “may” or “might” and words of similar meaning in connection with a discussion of future operations or financial performance. From time to time, oral or written forward -looking statements may also be included in other materials released to the public. These statements are based on management’s assumption’s and beliefs in light of the information currently available to it. The Company cautions you that a number of important risks and uncertainties could cause actual results to differ materially from those discussed in the forward-looking statements, and therefore you should not place undue reliance on them. You also should not rely on any obligation of the Company to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The Company disclaims any such obligation. Risks and uncertainties that might affect the Company include, but are not limited to, (i) general economic conditions in the Company’s markets, particularly levels of spending; (ii) exchange rates, particularly between the real and the U.S. dollar, and other currencies in which the Company makes significant sales or in which its assets and liabilities are denominated; and (iii) the outcome of contingencies.

2 - 2 --1

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable, as the Company is filing this Form 20-F as an annual report.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable, as the Company is filing this Form 20-F as an annual report.

ITEM 3. KEY INFORMATION

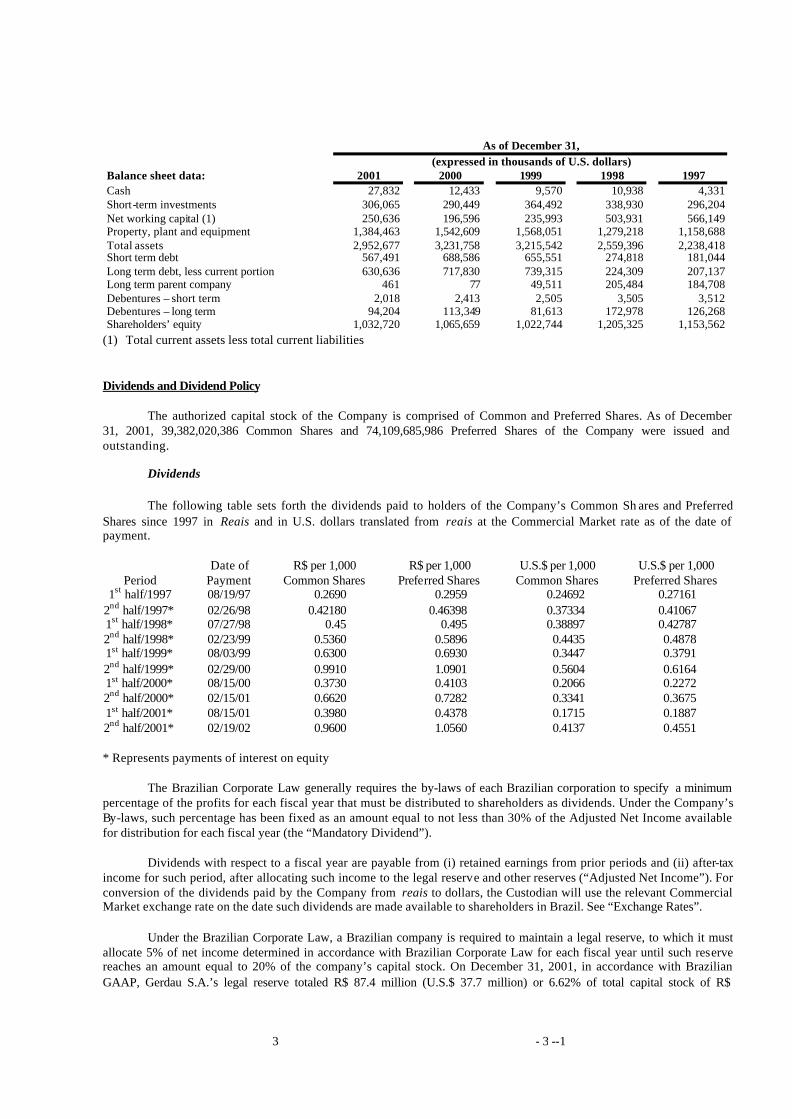

A. SELECTED FINANCIAL DATA

U.S. GAAP Presentation

The selected financial information for the Company included in the following table should be read in conjunction with, and is qualified in its entirety by, the U.S. GAAP financial statements of the Company and “Operating and Financial Review and Prospects appearing elsewhere herein. The consolidated financial data for the Company as of December 31, 2001, 2000 and 1999, are derived from the U.S. GAAP financial statements included elsewhere herein. The financial statements as of December 31, 2001, 2000 and 1999 have been audited by Arthur Andersen S/C.

For the years ended December 31, (expressed in thousands of U.S. dollars)

Statement of income data: 2001 2000 1999 1998 1997 Net sales 2,320,530 2,676,714 1,720,988 1,885,061 1,824,108 Cost of sales (1,641,620) (1,964,353) (1,101,371) (1,315,179) (1,296,453) Gross profit 678,910 712,361 619,617 569,882 527,655 Sales and marketing expenses (105,801) (112,195) (86,007) (101,386) (107,199) General and administrative expenses (181,108) (213,143) (157,755) (175,457) (198,083) Operating income 392,001 387,023 375,855 293,039 222,373 Interest expense and exchange loss (238,269) (243,477) (222,414) (151,739) (54,359) Interest income 55,002 57,324 64,166 86,897 31,626 Other non-operating income (expense) (7,853) 2,165 5,196 18,798 17,330 Equity pickup on non-consolidated company 18,324 33,962 (4,903) - - Income before income taxes and minority interest 219,205 236,997 217,900 246,995 216,970 Provision for income taxes:

Current (40,981) (36,725) (17,456) (38,460) (17,335) Deferred (13,666) (8,899) (3,080) (13,843) (21,710)

Income before minority interest 164,558 191,373 197,364 194,692 177,925 Minority interest 2,795 (2,815) 328 (844) (21,182) Net income available to common and preferred

shareholders

167,353

188,558

197,692

193,848

156,743 Basic earnings per 1,000 shares

Common 1.38 1.56 1.65 3.22 2.76 Preferred 1.52 1.72 1.79 3.54 3.10

Diluted earnings per 1,000 shares Common 1.38 1.55 1.65 3.06 2.69 Preferred 1.52 1.70 1.78 3.35 3.00

Cash dividends declared per 1,000 shares Common 0.58 0.55 1.20 0.76 0.68 Preferred 0.65 0.60 1.27 0.81 0.74

Number of common shares outstanding 39,382,020,386 33,070,107,530 19,691,010,193 19,691,010,193 19,314,516,379

3 - 3 --1

As of December 31, (expressed in thousands of U.S. dollars)

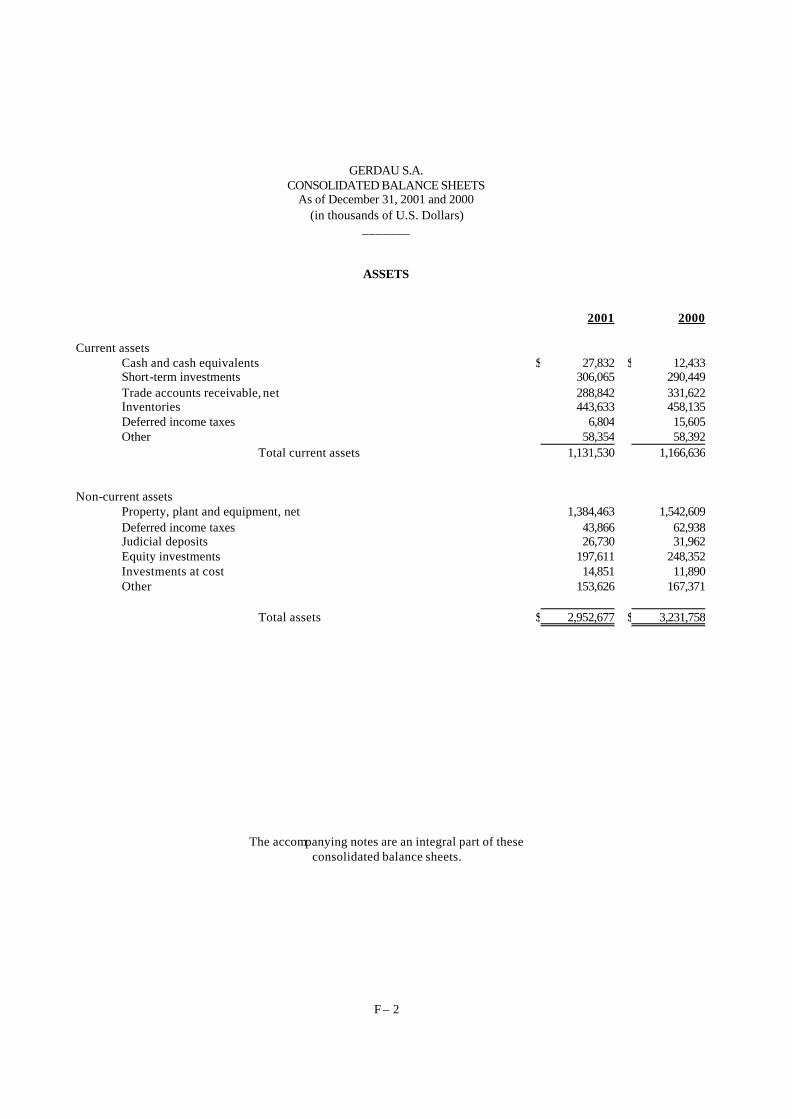

Balance sheet data: 2001 2000 1999 1998 1997 Cash 27,832 12,433 9,570 10,938 4,331 Short-term investments 306,065 290,449 364,492 338,930 296,204 Net working capital (1) 250,636 196,596 235,993 503,931 566,149 Property, plant and equipment 1,384,463 1,542,609 1,568,051 1,279,218 1,158,688 Total assets 2,952,677 3,231,758 3,215,542 2,559,396 2,238,418 Short term debt 567,491 688,586 655,551 274,818 181,044 Long term debt, less current portion 630,636 717,830 739,315 224,309 207,137 Long term parent company 461 77 49,511 205,484 184,708 Debentures – short term 2,018 2,413 2,505 3,505 3,512 Debentures – long term 94,204 113,349 81,613 172,978 126,268 Shareholders’ equity 1,032,720 1,065,659 1,022,744 1,205,325 1,153,562

(1) Total current assets less total current liabilities

Dividends and Dividend Policy

The authorized capital stock of the Company is comprised of Common and Preferred Shares. As of December 31, 2001, 39,382,020,386 Common Shares and 74,109,685,986 Preferred Shares of the Company were issued and outstanding.

Dividends

The following table sets forth the dividends paid to holders of the Company’s Common Sh ares and Preferred Shares since 1997 in Reais and in U.S. dollars translated from reais at the Commercial Market rate as of the date of payment.

Date of R$ per 1,000 R$ per 1,000 U.S.$ per 1,000 U.S.$ per 1,000 Period Payment Common Shares Preferred Shares Common Shares Preferred Shares

1st half/1997 08/19/97 0.2690 0.2959 0.24692 0.27161 2nd half/1997* 02/26/98 0.42180 0.46398 0.37334 0.41067 1st half/1998* 07/27/98 0.45 0.495 0.38897 0.42787 2nd half/1998* 02/23/99 0.5360 0.5896 0.4435 0.4878 1st half/1999* 08/03/99 0.6300 0.6930 0.3447 0.3791 2nd half/1999* 02/29/00 0.9910 1.0901 0.5604 0.6164 1st half/2000* 08/15/00 0.3730 0.4103 0.2066 0.2272 2nd half/2000* 02/15/01 0.6620 0.7282 0.3341 0.3675 1st half/2001* 08/15/01 0.3980 0.4378 0.1715 0.1887 2nd half/2001* 02/19/02 0.9600 1.0560 0.4137 0.4551 * Represents payments of interest on equity

The Brazilian Corporate Law generally requires the by-laws of each Brazilian corporation to specify a minimum percentage of the profits for each fiscal year that must be distributed to shareholders as dividends. Under the Company’s By-laws, such percentage has been fixed as an amount equal to not less than 30% of the Adjusted Net Income available for distribution for each fiscal year (the “Mandatory Dividend”).

Dividends with respect to a fiscal year are payable from (i) retained earnings from prior periods and (ii) after-tax income for such period, after allocating such income to the legal reserve and other reserves (“Adjusted Net Income”). For conversion of the dividends paid by the Company from reais to dollars, the Custodian will use the relevant Commercial Market exchange rate on the date such dividends are made available to shareholders in Brazil. See “Exchange Rates”.

Under the Brazilian Corporate Law, a Brazilian company is required to maintain a legal reserve, to which it must allocate 5% of net income determined in accordance with Brazilian Corporate Law for each fiscal year until such reserve reaches an amount equal to 20% of the company’s capital stock. On December 31, 2001, in accordance with Brazilian GAAP, Gerdau S.A.’s legal reserve totaled R$ 87.4 million (U.S.$ 37.7 million) or 6.62% of total capital stock of R$

4 - 4 --1

1,320.1 million (U.S.$ 568.9 million).

According to Law 9,457, holders of preferred shares in a Brazilian corporation (including the Preferred Shares) are entitled to receive dividends at least 10% greater than dividends paid on Common Shares unless there is a provision for a fixed minimum dividend on preferred shares based on capital. The Company has no such provision and, accordingly, pays dividends on Preferred Shares 10% higher than those paid on Common Shares. The Gerdau S.A. executive management presented a proposal at the shareholders' year-end meeting which has been approved to grant both Common Shares and Preferred Shares a 100% tag along right with the control block of Common Shares. This measure was approved by shareholders on April 30, 2002, and it will extend to all shareholders a right that the new Brazilian Corporate Law required only for minority holders of Common Shares (and at only 80% of the consideration paid to the controlling shareholders).

Under the recent amendments to the Brazilian Corporate Law, by extending the tag along right to minority shareholders, the Company will no longer need to comply with the requirement to pay an additional 10% premium on dividends paid to preferred shareholders. Upon approval and effectiveness of the amendments to the Company’s by-laws to provide for the tag-along as described above, the Company will pay the stated 30% (By -Law) of Adjusted Net Profit to all shareholders, without any premium to preferred shareholders.

As a general requirement, shareholders who are not residents of Brazil must have their investment in a Brazilian company registered with the Central Bank to have dividends, sales proceeds or other amounts related to their shares eligible for conversion into foreign currency for remittance outside Brazil. Preferred Shares underlying the ADSs will be held in Brazil by the Custodian as agent for the Depositary. The holder of Preferred Shares will be the registered owner on the records of the Depositary for the Preferred Shares.

Payments of cash dividends and distributions, if any, will be made in Brazilian currency to the Custodian, on behalf of the Depositary, which will then convert such proceeds into U.S. dollars and will cause such U.S. dollars to be delivered to the Depositary for distribution to holders of ADRs. If the Custodian is unable to immediately convert the Brazilian currency received as dividends into U.S. dollars, the amount of U.S. dollars payable to holders of ADRs may be adversely affected by any devaluation or depreciation of the Brazilian currency in relation to the U.S. dollar that occurs before such dividends are converted and remitted. Dividends in respect of the Preferred Shares paid to holders who are not Brazilian residents, including holders of ADSs, are not subject to Brazilian withholding tax.

Interest on Equity

Law 9,249 of December 1995 provides that a company, at its discretion, may pay interest on equity to shareholders as an addition or an alternative to dividends. A Brazilian corporation is entitled to pay (and set off against the Mandatory Dividend for each fiscal year) to its shareholders as interest on equity up to the limit of the TJLP (Long-Term Interest Rate). The payment of interest as described herein is subject to a 15% withholding income tax. See “Item 10 E - Taxation”.

Dividend Policy

The Company currently intends to pay dividends on its outstanding Preferred Shares in the amount of its required distributions for any particular fiscal year, subject to any determination by the Board of Directors that such distributions would be inadvisable in view of the Company’s financial condition. As a policy, although not required to do so by law, the Company pays dividends or interest on capital twice a year.

Exchange Rates

There are two legal foreign exchange markets in Brazil, the Commercial Market and the Floating Market. The Commercial Market is reserved primarily for foreign trade transactions and transactions that generally require prior approval from Brazilian monetary authorities, such as the purchase and sale of registered investments by foreign persons and related remittances of funds abroad. Purchases of foreign exchange in the Commercial Market may be carried out only through a financial institution in Brazil authorized to buy and sell currency in that market. The Commercial Market rate is the commercial selling rate for Brazilian currency into U.S. dollars, as reported by the Central Bank. The "Floating Market rate" is the prevailing selling rate for Brazilian currency into U.S. dollars which applies to transactions to which

5 - 5 --1

the Commercial Market rate does not apply, as reported by the Central Bank. Prior to the implementation of the Real Plan, the Commercial Market rate and the Floating Market rate differed significantly at times. Since the introduction of the real, the two rates have not differed significantly, although there can be no assurance that there will not be significant differences between the two rates in the future. Both the Commercial Market rate and the Floating Market rate are reported by the Central Bank on a daily basis .

Both the Commercial Market rate and the Floating Market rate are freely negotiated but have been subject to limited intervention by the Central Bank. After implementation of the Real Plan, the Central Bank initially allowed the real to float with minimal intervention.

On January 18, 1999, the Central Bank officially announced its new policy to allow the real’s value to be determined by the foreign exchange markets, intervening only to limit wide swings in the value of the currency. The pressure on the real during the beginning of March that same year caused the government to drop the managed band exchange rate system and to adopt a free floating exchange rate system. Following the adoption of this system and with the designation of a new Central Bank president, Armínio Fraga, as well as other macro-economic factors, the real strengthened so that on December 31, 1999, the exchange rate was R$ 1.79 per US$ 1.00. Since that date, however, it has declined against the Dollar. On December 31, 2000 the Commercial Market rate was R$ 1.9554 per U.S.$ 1.00 and on December 31, 2001, the exchange rate was R$ 2.32 per US$ 1.00. The year of 2001 was strongly influenced by the economic and political crises in Argentina. The real fluctuated heavily against the U.S. dollar. By the end of the year, however, the financial situation of Brazil as perceived by economic agents caused the Brazilian currency to recover and regain value. Since then it has fluctuated well within the ratios considered stable by the financial markets. The net devaluation in the period was 18.67%. On April 30, 2002 the rate was R$ 2.36 per U.S.$ 1.00.

The following table sets forth information on prevailing Commercial Market rates for the periods indicated.

Exchange Rates Reais per U.S.$ 1.00 Year Average Price 1997 Average 1.0784 1998 Average 1.1609 1999 Average 1.8133 2000 Average 1.8293 2001 Average 2.3504

Exchange Rates Exchange Rates Reais per US$ 1.00 Reais per U.S.$ 1.00 Year Month Lowest Rate Highest Rate 2001 July 2.3249 2.5979 2001 August 2.4463 2.5585 2001 September 2.5590 2.8007 2001 October 2.6866 2.7828 2001 November 2.4604 2.6820 2001 December 2.2930 2.4672

Source: Economática

The Company will make any cash distributions related to the Preferred Shares in Brazilian currency. Accordingly, exchange rate fluctuations may affect the U.S. dollar amounts received by the holders of Preferred ADSs on conversion by the Depositary of such distributions into U.S. dollars for payment to holders of Preferred ADSs. Fluctuations in the exchange rate between reais and the U.S. dollar may also affect the U.S. dollar equivalent of the reais price of the Preferred Shares on the Brazilian stock exchanges.

Brazilian law provides that, whenever there is a serious imbalance in Brazil’s balance of payments or serious factors that enable it to foresee such imbalance, temporary restrictions may be imposed on remittances of foreign capital abroad. For approximately nine months in 1989 and early 1990, for example, to maintain Brazil’s foreign currency reserves, the amounts were subsequently released in accordance with Brazilian Government directives. There can be no

6 - 6 --1

assurance that similar measures will not be taken by the Brazilian Government in the future.

B. CAPITALIZATION AND INDEBTEDNESS

Not required.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not required.

D. RISK FACTORS

Factors Relating to Brazil and to the Company Political and Economic Condition

The Brazilian economy has been affected by frequent and occasionally drastic intervention by the Brazilian Government, which has often changed monetary, credit, tariff and other policies to influence the course of Brazil's economy. Changes in policy involving tariffs, exchange controls, regulatory policy and taxation could adversely affect the Company’s business and financial results, as could inflation, devaluation, social instability and other political, economic or diplomatic developments and the Brazilian Government’s response to such developments.

Brazil’s latest economic stabilization plan (the “Real Plan”) which effectively reduced inflation since the introduction of the new currency, the real, in July 1994, does not contain any wage or price controls, and has been supported by the government of President Fernando Henrique Cardoso, who was Finance Minister at the time of the adoption of the Real Plan. Although President Cardoso has stated his intention to continue to support the market and privatization measures of recent years, there is no guarantee that the actions taken by the Brazilian Government will be continued or will be successful.

Brazil experienced a financial and economic crisis in the first quarter of 1999 following the financial and economic crisis in Asia. In response, the Government adopted economic measures to protect the Real Plan and the stability of the Brazilian currency. The effects of these measures are exp ected to continue in force during 2002.

The highlights of these measures include the approval of an increase in the CPMF (temporary financial transaction contribution) from 0.30% to 0.38%, (ii) a R$ 8.7 billion cut in the Federal Budget, (iii) an increase in the COFINS (contribution for the financing of Social Security) from 2% to 3%, (iv) an increase from 20% to 40% in the percentage of funds the Federal Administration transfers to the States, (v) a reduction in spending for state-run companies of R$ 2.7 billion and (vi) an increase in the FEF (fiscal stabilization fund). Furthermore, the Federal Administration is currently attempting to have Congress approve a Tax Reform bill. A Social Security reform bill proposed by the Federal Administration was voted and approved by Congress, in 1999.

These reforms have re-established the international financial community's confidence in Brazil which, combined with the decrease in tax rates, have allowed for the resumption of economic growth.

The Brazilian economy, however well it has performed, is still part of the greater world economy and is not immune to the adverse effects that may spill over from its neighbors or other related economies in the world.

Inflation; Effects of Economic Stabilization Program and Change of Currency.

Brazil experienced extremely high and generally unpredictable rates of inflation for several years. For this reason, the Federal Government developed a series of mechanisms to protect the value of assets. The main instruments have been inflation indices with particular attention to the INPC (National Index for Consumer Prices). With the end of high inflation and the newly acquired status of stable economy, Brazil changed its reference for inflation tracking by instituting the IPCA (National Extended Consumer Price Index). This index has been used for setting inflation targets with the IMF and for domestic purposes. Inflation in Brazil, as stated by the INPC, was 2,489.11% in 1993 and, 929.32% in 1994. After 1994, inflation reached lower levels. From 1999 on, the IPCA became the reference. Inflation in Brazil was 22.41% in 1995, 9.56% in 1996, 5.22% in 1997, 1.66% in 1998, 8.94% in 1999 and 5.97% in 2000. In 2001, the inflation as

7 - 7 --1

calculated by this index reached 7.67%, slightly above the upper limit margin of 7% as defined by the Brazilian monetary authorities.

Inflation, as well as governmental efforts to combat inflation, have historically had significant negative effects on the Brazilian economy generally and on the profitability and results of operations of the Company in particular. In an attempt to control inflation, the Government has at times imposed wage and price controls, and reduced Government spending among other measures. Inflation, as well as governmental measures to combat inflation, combined with public speculation about possible future actions, has also contributed to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets. Furthermore, the Government’s desire to control inflation and to reduce budget deficits may cause it to make actions that may slow or halt Brazilian economic growth. A significant increase in inflation in Brazil could have serious adverse consequences on the Company.

Effects of Currency Devaluations and Exchange Rate Fluctuations.

The value of various South American currencies, including currencies in the countries in which the Company operates, when compared to each other and to the United States and the Canadian dollar, has fluctuated significantly and can be expected to continue to do so. In Brazil, the recent successive crises in the international financial markets have created a significant threat to the stability of the Brazilian currency and, on January 18, 1999 led to the Central Bank’s announcement that the real would trade freely on foreign-exchange markets, with the Central Bank intervening only to limit wide swings in the real’s value. See “Risk Factors – Factors Relating to Brazil and to the Company – Political and Economic Condition.” These fluctuations may have significant effects on the Company’s results of operations and financial condition and on its consolidated financial statements, which are denominated in U.S. dollars.

The Company maintains assets denominated in reais and, to a lesser extent, in U.S. and Canadian dollars, Chilean, Uruguayan and Argentinean pesos, and it regularly experiences gains and losses due to exchange movements between such currencies and the U.S. dollar. At the same time, the Company has loans contracted in Brazil and indexed to the U.S. dollar and to other currencies, which also suffer the impact of the exchange rates between these currencies and the real. As a result, the Company may be exposed to significant exchange losses from further devaluation of the Brazilian real and/or other currencies against the U.S. dollar. The Company’s net sales, gross profit and operating margins may also be influenced by changes in exchange rates. The Company’s sales denominated in the currencies of Brazil, Canada, Uruguay, Chile, Argentina and the United States represented 63.6%, 8.9%, 0.7%, 2.7%, 0.6% and 23.5%, respectively, of the Company’s consolidated gross sales for the year ended December 31, 2001. Because the Company’s U.S. GAAP financial statements are denominated in U.S. dollars, net sales and other financial statement accounts (including net income) could be adversely affected by a devaluation of a local currency relative to the U.S. dollar.

Controls and Restrictions on U.S. Dollar Remittances.

Brazilian law provides that, whenever there exists, or is a serious risk of a material imbalance in Brazil balance of payments, the Government may, for a limited period of time, impose restrictions on the remittance to foreign investors of the proceeds of their investments in Brazil. This situation did occur for approximately six months in 1989 and early 1990, as did the imposition of a restriction on the conversion of the Brazilian currency into foreign currencies. Such restrictions could hinder or prevent the Custodian or holders who have surrendered ADSs for the underlying Preferred Shares from converting dividends, distributions or the proceeds from the sale of such Preferred Shares into U.S. dollars and remitting such U.S. dollars abroad. Holders of ADSs could be adversely affected by delays in, or refusals to grant, any required governmental approvals for conversion of Brazilian currency payments and remittances abroad in respect of the Preferred Shares underlying the ADSs.

Developments in Other Emerging Market Countries

The Brazilian securities markets are, to varying degrees, influenced by economic and market conditions in other emerging market countries. Although economic conditions are different in each country, investors' reaction to developments in one country can have effects on the securities of issuers in other countries. For example, in December 1994, the government of Mexico sharply devalued the peso and allowed its value to float, triggering an economic crisis in Mexico which negatively affected the securities markets in many Latin American countries, including Brazil. Last year, the worsening of the economic crisis in Argentina had a materially adverse effect on the Brazilian economy and on its securities markets and led to the adoption of Government policies that may have further adverse effects on both economic growth and on the Brazilian securities markets. There can be no assurance that the Brazilian securities markets or

8 - 8 --1

economy will not continue to be affected negatively by events (including economic crises or currency fluctuations) elsewhere, especially in emerging markets, or that such effects will not adversely affect the Company's business, financial condition, results of operation or prospects or the value of the Shares or ADSs.

Since the end of 1997, and in part icular during 2001, investors have been demonstrating a high level of concern regarding the risk in investing in emerging economies due to the economic problems faced by many these countries, including Argentina. Consequently, on certain occasions, Brazil has faced significant U.S. dollar outflows as Brazilian companies faced higher financing costs, both in domestic and international markets. Moreover, the companies are, in a way, inhibited to access the international capital markets.

In addition, the Brazilian Government has exercised and continues to exercise substantial influence over many aspects of the private sector. The Brazilian Government owns or controls many companies, including some of the largest in the country. Government action in the future could have a significant effect on economic and market conditions in Brazil, affecting prices and returns on Brazilian securities. There can be no assurance that future economic or market developments in Brazil will not impact the Company's results of operations.

Political and Economic impacts on the Company's operations

The most notable effect of the current instability of the financial markets in Brazil on the Company would be that of the impact of additional devaluation of the Brazilian currency. Although the Brazilian operating units have costs based on the real, they nonetheless do have processes that are influenced or determined by international pricing, i.e., in U.S. dollars such as pig iron, an important metallic input, and iron ore. Furthermore, the devaluation of the real could impact significantly other sectors of the economy and affect the sales of the Gerdau mills. A resulting negative side effect would be the increase in the inflation figures: the impact of dollar-related price references has the effect of contaminating local prices and causing a reduction in consumption and a decrease in GDP growth (see item 11, "Quantitative and Qualitative Disclosures about Market Risks").

It is not possible, however, to predict how these measures will affect the business, financial condition, results of operations, cash flows and overall prospects of the Company. This or future economic slowdowns could have a material adverse effect on the Company’s business, financial condition, results of operations, cash flows and overall prospects .

Risk factors relative to the Company

Costs Resulting from the Enforcement of Environmental Legislation

The Company's plants are required to comply with a range of laws and regulations at the federal, state and municipal levels in addition to environmental and operational regulations. Should the legislation become more demanding, expenditures on fixed assets and the cost to comply with this legislation may increase in the future and have a negative impact on the Company's financial conditions.

Supply of Electrical Power

Historically, the generation of electrical power in Brazil has been the target of annual investments of about US$ 13 billion. The reduction in these investments made by the Federal Government of Brazil in the nineties (a decade in which investments were reduced to about US$ 7 billion), the increase in the annual consumption throughout that same period of about 5%, and the lack of high capacity transmission lines between the regions in which energy is abundant and those that are lacking energy led to the crisis that hit the southeast, center-west and northeast regions of Brazil. As a consequence, on June 1, 2001, the Federal Government published Provisional Measure 2152-2 ("MP"), that deals with the rationing of electric usage. The MP and the Resolution nr. 8, dated May 25, 2001 (the "Resolution"), were prepared and issued by the Power Crisis Management Chamber and subjected the Company to a consumption goal as of June 2001, equivalent to 75% and 80% of the average monthly consumption of May, June and July of 2000, for semi-integrated mills located in the southeast and northeast regions, and integrated plants in the abovementioned regions, respectively. The Power Crisis Management Commission decreed the end of the rationing in March 2002. The Company did not exceed its consumption goals and, as a consequence, did not suffer penalties and/or power outages. Management believes that the reduction in the consumption of energy did not have a material adverse effect on the business, its financial condition or its

9 - 9 --1

results of operations. In addition, the threat of an increase in electricity tariffs did not materialize although this could happen in the medium term. Power and electricity represents approximately 9% of the Company’s total production cost. Currently, the Company believes that a significant concern is Brazil’s ability to invest in power generation capacity in order to avoid future risks including a new period of rationing, power outages and tariff increments, among others.

Market Concentration

Under Brazilian law, all activities that lead to market concentration involving at least one company with annual gross revenues of at least R$ 400 million or in control of at least a 20% market share must be reported to the authorities responsible for economic protection which, regardless of the approval of the transaction, may impose fines as a result of not presenting the appropriate documents on a timely basis. Any company that has more than 20% in the several different markets in which it operates may have its acquisitions questioned by the CADE - – Conselho Administrativo de Defesa Econômica, (Economic Defense Administrative Council) responsible for the analysis and decision on acts that indicate anticompetitive practices in any market.

Level of Indebtedness and Restrictive clauses to Funding

On December 31st, 2001, the level of indebtedness of the Group including contracts for funding in local and foreign currencies and debentures less cash and cash equivalents was less than its net worth (net debt to equity ratio of 91%).

The Company has entered into several loan contracts in addition to other forms of funding, such as the issuance of debentures, in an approximate total amount of US$ 1.3 billion (as of December 2001). Some of these contracts have restrictive clauses such as (i) issuance of debentures and golden shares and adding debt without the prior consent of the National Bank for Social and Economic Development - (exception made for loans for the regula r operation of the borrower with the sole purpose of replacing of material); (ii) constitution of guarantees as collateral of any kind of operation with other creditors without providing to the BNDES the same guarantees; (iii) the creation of liens on assets with exception made for those already pledged at the date of the signing of the respective contract unless the same conditions are extended to the holders of debentures , exception made for (a) any lien on capital goods placed at the time of their purchase as collateral, (b) liens on commercial goods to guarantee short term debt to be paid through the revenues generated by the sale of these goods, (c) liens on promissory notes and (d) liens given as legal guarantees; (iv) the payment of dividends in cash in excess of 30% of the Net Profit of each period adjusted in accordance with art. 202 of law 6.404/76 if after the payment of such excess: (a) the long term liability exceeds more than 1.5 times the net worth; or (b) current assets are less than current liabilities; (v) payment of dividends or any other form of statutory participation in the profits of the corporation if it is delinquent in the payment of the interest and the principal of the debentures; (vi) voluntary pre -payment of long-term debt without making the proportional buyout of debentures still outstanding in the market, except if these payments are for the replacement of long term debt with long term debt at a lower cost (lower interest rates, same interest rates or better conditions for the Company); (vii) encumbrance, transference, assignment or any form of disposal of quotas and/or the subscription owned or to be owned that may jeopardize directly or indirectly the controlling shareholders' ownership position; (viii) maintain INDAC – Indústria, Comércio e Administração S/A as the direct or indirect controlling entity of voting shares of the Company . Furthermore, many debt contracts require that the Company have, throughout the validity of these contracts, levels of capitalization and of current liquidity as determined by the parties.

Should any events of default as defined by these contracts occur, the Company could face the acceleration of the maturity of this debt as well as other contracts. The acceleration of the maturity of debt and other contracts might result in the Company’s inability to honor its commitments

Consolidation of the Steel market abroad

Market Consolidation

The Group has a substantial part of its business abroad. It is therefore subject to competition in these markets. In recent times, the steel sector has been undergoing a process of consolidation with the resulting creation of companies with greater production capacity. This can represent an important increase in competition. The Group may be forced to decide to acquire other companies or their assets, which may represent the outlay of substantial financial resources. There are no

10 - 10 --1

guarantees that the Group will have the financial resources to make these acquisitions should they become necessary or desirable.

Protectionist Measures

The measures imposed by the U.S. Administration and by the European Union to protect their domestic markets against the import of certain cheap steel products, do not impact directly the operations of Gerdau in Brazil due to the fact that exports to these countries are negligible. The Gerdau units in the U.S. operate independently and do not require any type of steel inputs from Brazil.

Argentine Crisis

Due to the economic crisis in Argentina, long steel demand in that country was reduced by roughly 50% as of the second half of 2001. The impact of this crisis on the Group’s activity level is limited because the Argentine operations represent less than 2% of Gerdau’s total sales. In order to adapt to the new economic reality, Gerdau has: i) adjusted its production to the local demand, ii) restricted credit, and iii) promoted a financial and corporate restructuring of its Argentine business.

The restructuring occurred in March 2002, as follows: Gerdau transferred its 71.77% stake in Sociedad Industrial Puntana S.A. – SIPSA to its partner Sipar Aceros S.A.. Gerdau maintains its stake of 38.18% in Sipar, whereas Sipsa becomes an integral subsidiary of Sipar. This new structure further reduced Gerdau’s exposure to the eventual impact o f any additional currency devaluation in Argentina and allows for better synergies between the two companies.

The significant devaluation of the Argentine peso vis -à-vis the US dollar generated a loss of US$ 21.4 million in Gerdau's business in the last quarter of 2001; in the first quarter of 2002, there was an additional loss of US$ 7.0 million. Moreover, the restructuring promoted in March generated a US$ 1.8 million loss.

ITEM 4. INFORMATION ON THE COMPANY

A. HISTORY AND DEVELOPMENT OF THE COMPANY

Gerdau is part of an industrial conglomerate, which began in 1901 with the acquisition by the Gerdau family of a nail factory located in Porto Alegre, in the Southern region of Brazil. In 1969, the business changed its name to Metalúrgica Gerdau S.A., which today controls Gerdau S.A.

With the objective of assuring the supply of raw material, immediately after the end of World War II, Siderúrgica Riograndense S.A., a steel producer also located in Porto Alegre, was acquired. The Company's output was increased through, among other things, the construction of a new mill. In the second half of the 1960s, the Company began to expand and diversify its activities.

The expansion involved the acquisition of existing companies (which increased the Company's market share) and the construction of new plants, in Brazil and abroad. The first company acquired was Indústria de Arames São Judas Tadeu S.A., in São Paulo, which is today known as "Comercial Gerdau". Comercial Gerdau, through a network of 70 branches, covers all of Brazil for retail sales of product. Subsequently, the Group expanded with various steel mills, drawing mills and factories for the production of strands, steel cables, soldered wire mesh and similar products located in principal Brazilian and foreign markets.

In order to assure competitive advantages in each region in which the Company operates, the Company adopted a principal strategy of acting through medium-sized companies situated in the heart of the economic regions capable of supplying raw materials originating in the same areas in which the final products were sold. See "Business Strategy".

In the beginning of 1995, a corporate restructuring program was initiated to simplify the structure resulting from the process of expansion and development through acquisition and establishment of companies, with the purpose of

11 - 11 --1

improving the transparency of operations, achieving greater acceptance in the modern Brazilian capital markets and enhancing the conditions for access to international capital markets.

The restructuring began with a public exchange offer of preferred shares of the former Companhia Siderúrgica da Guanabara-Cosigua (today Gerdau S.A.) held by the controlling shareholders in exchange for shares held by minority shareholders in the following affiliated companies: Siderúrgica Guaira S.A.(“Guaira”), Siderúrgica Açonorte S.A. (“Açonorte”) and Cia. Siderúrgica Pains (“Pains”). This transaction was conducted through the São Paulo Stock Exchange in February 1995 and the widespread acceptance of this process by the shareholders of these companies permitted the continuation of the restructuring process by merger, during the period of February 1995 through June 1997, of 28 companies then comprising the Gerdau group. In January 1999 Comercial Gerdau was also merged into Gerdau S.A. All of the steel mill operations of Gerdau, installed in Brazil and abroad, are concentrated in Gerdau S.A.

B. BUSINESS OVERVIEW

Gerdau S.A. is a producer of long ordinary and specialty steel through its industrial units located in Brazil and its subsidiaries in Uruguay, Chile, Canada, Argentina and the United States, with installed production capacity of 7.3 million tons of crude steel (not including Açominas and Cartersville), 7.0 million tons of rolled product (not including Açominas, Cartersville and Sipar) and 0.9 million tons of drawn products. The Company produces steel based on the mini-mill concept, whereby steel is produced in electric arc furnaces, starting with scrap and pig iron acquired mainly in the region where each mill operates (the so-called mini-mill concept). Gerdau also operates plants capable of producing steel starting with iron ore in blast furnaces and through the direct reduction process. Gerdau's products are manufactured with a wide range of specifications, intended to satisfy a large spectrum of consuming groups.

The three principal markets in which the Company operates are the civil construction, manufacturing and agricultural and breeding sectors. Last year, the first two represented approximately 98% of the total sales volume of the Company measured in tons. In 2001, Gerdau produced 6.1 million tons of crude steel, of which 3.5 million (not including Açominas’ production) were produced in Brazil (13.0% of national production) and 2.6 million tons through its subsidiaries abroad. In the segment of long rolled steel, Gerdau is the largest Brazilian producer, with approximately 44.5% of total production.

For the fiscal year ended December 31, 2001, the Company achieved consolidated net sales in the amount of U.S.$ 2.3 billion, generating consolidated net income of U.S.$ 167.3 million.

Business Strategy

Gerdau's principal business focus is the decentralized production of long steel products using electric arc furnaces ("EAF") mini-mills employing continuous casting technology. Plants are sized and located in order to fit in the local economy and access markets efficiently. This strategy was a response to the geographical dimensions of Brazil, its limited infrastructure and high freight costs, which motivated growth of a business focused on selling products where raw materials were readily accessible. From the mid 1970s through the early 1990s, Gerdau concentrated on improving its market share in Brazil through a combination of increasing the production capacity of its existing facilities and through strategic acquisitions, typically of distressed mini-mills where the Company's principal contribution would be management skills rather than capital. Gerdau has increased its share of Brazilian long steel production from 14.1% of total tonnage produced in 1975 to 44.5% in 2001. The Company's share of Brazilian crude steel production grew from 6.3% to 13.0% during the same period. See, "Production Process - Domestic Steel Production." Gerdau's strategy has been implemented through the following acquisitions:

• Domestic acquisitions: In the 1960s the Company acquired a mill in Pernambuco in Northeast Brazil. In the 1970s it acquired two mills (Alagoas and Paraná) and constructed its largest mill in Rio de Janeiro. Gerdau's structure further developed as a result of its participation in Brazil's privatization auctions in the late 1980s and early 1990s. In the first phase of privatizations, it acquired Barão de Cocais mill in 1988 and Usina Siderúrgica da Bahia S.A.-Usiba (“Usiba”) in 1989. In the second, broader phase of privatizations, Gerdau acquired Companhia Siderúrgica do Nordeste ("Cosinor") in 1991 and Aços Finos Piratini S.A. (“Piratini”), a specialty steel maker, in part in order to enter the market for high-value-added products. Gerdau has increased productivity of these privatized mills significantly since the acquisition (as measured in metric tons of crude steel per man-year) by reducing the number of employees and investing in technological upgrades of processes and equipment. Through these investments and

12 - 12 --1

business management, Gerdau has been successful in significantly improving the profitably of these businesses and achieving cost efficiencies and productivity improvements within a relatively short time after acquisition. In 1994, the Company acquired Pains, a steel mill located in Divinópolis, Minas Gerais State, through the acquisition of Korf Gmbh, a German corporation. Gerdau has substantially divested itself of other assets acquired through Korf that were unrelated to Gerdau's core business, the production of long ordinary steel. The Pains acquisition was the subject of antitrust proceedings in Brazil that were later successfully settled. In the second half of 1997, Gerdau acquired a participation in the capital of Açominas, a Brazilian producer of semi-finished products. Gerdau purchased additional interests in Açominas since the first acquisition in 1997 and at the end of 2001 held 37.9% of this company. More recently, on December 7th, 2001, Gerdau made an offer of R$ 426.7 million (US$ 177.7 million) for an additional stake in Açominas at an auction sponsored by the Brazilian Central Bank. The transaction was fully concluded on February 19, 2002, and as a result, Gerdau currently holds 54.14% of Açominas. Additionally, on February 8, 2002, Gerdau also formalized an agreement to acquire the 24.8% stake that Natsteel (of Singapore) has in Açominas. According to the terms of the agreement, Gerdau may exercise its right to purchase Natsteel's stake by September 9, 2002.

• Overseas Acquisitions: Gerdau has grown outside Brazil through strategic acquisitions. In 1981, the Company acquired Siderúrgica Laisa S.A. in Uruguay (now known as Gerdau Laisa S.A.), as its first steel manufacturing company outside Brazil. This was followed in 1989 by the acquisition of Courtice Steel Inc. (now known as Gerdau Courtice Steel Inc.) in Canada and, in 1992, by the acquisition of Siderúrgica Aza S.A. (now known as Gerdau Aza S.A.) in Chile. In May 1995, Manitoba Rolling Mills Inc., a profitable steel division affiliated with the Canam Manac Group located in Selkirk, Canada, was acquired by Gerdau. Gerdau assumed managerial control on June 1, 1995, and renamed the facility Gerdau MRM Steel Inc. In December, 1997, the Company acquired control of Sipsa of Argentina, a rolling mill with a production capacity of 75,000 tons of rolled products, in order to increase its presence in an already important export market. In May 1998, the Company concluded an agreement to acquire a one-third interest in an Argentine rolling mill, Sipar, as well as to transfer to the controllers of Sipar a one third interest in Sipsa. On September 27, 1999 Gerdau acquired from Kyoei Steel Ltd. of Osaka, Japan 88% of FLS Holdings Inc. , which in turn holds 85% of the shares of Ameristeel Corp., headquartered in Tampa, Florida, USA. In 2000, Gerdau acquired the remaining 12% of FLS Holding Inc. and increased its participation in Sipsa to 72% and in Sipar to 38%. By the end of 2001, Ameristeel acquired from Birmingham Southeast the operating assets of one of its units for US$ 48.8 million. This steel mill is located in Cartersville, Georgia, and it is now the seventh steel mill owned by Ge rdau in North America. More recently, Gerdau has promoted the financial and corporate restructuring of its operations in Argentina to adapt to the new economic reality of that country. At the end of March, its stake of 71.77% in Sociedad Industrial Puntana S.A. – SIPSA was transferred to its partner Sipar Aceros S.A. This generated losses of US$ 1.8 million, recorded as a non-operating expense. With this operation, Gerdau maintains its stake of 38.18% in Sipar, whereas Sipsa becomes an integral subsidiary of Sipar. This new structure is expected to allow for better synergies between the companies in Argentina. This should maximize business opportunities, enhance results and minimize the impact of the fluctuation of the peso vis-à-vis other currencies.

Along with the acquisitions, the Company's strategy evolved to also include downstream investment through the addition of drawn products and specialty steels, permitting the diversification of its products. Having achieved a major and stable market positioning in the production of long steel products, the extent of downstream diversification is under review, to assure that the Company is invested in value-added products.

The table below shows the Company's various domestic acquisitions and their respective improvements in production volumes and financial results.

COMPANY- Date of Purchase

Fiscal Year Prior to

Fiscal Years following Purchase

Purchase 1 2 3 4 5 AÇONORTE - December/1969 1969 1970 1971 1972 1973 1974 Production of Crude Steel (in 1,000 tons) 35.1 44.8 49.1 59.6 102.8 114.3 Revenue (US$ millions) ND ND ND 13.3 31.6 52.9 Net income (US$ millions) 0.6 1.2 1.4 1.8 5.9 5.4 GUAÍRA - December/1971 1971 1972 1973 1974 1975 1976 Production of Crude Steel (in 1,000 tons) 19.9 34.0 43.2 44.5 42.9 41.5 Revenue (US$ millions) ND 5.8 11.2 18.3 13.3 13.9

13 - 13 --1

Net income (US$ millions) 0.02 0.4 1.4 2.0 1.1 1.0 COMESA - January/1974 1973 1974 1975 1976 1977 1978 Production of Crude Steel (in 1,000 tons) 4.7 11.9 7.0 14.3 16.1 16.8 Revenue (US$ millions) 0.9 4.5 4.6 6.2 6.8 8.3 Net income (US$ millions) (1.7) 0.4 0.1 0.4 0.7 0.7 HIME - February/1985 1984 1985 1986 1987 Production of Crude Steel (in 1,000 tons) 200.2 192.1 188.3 Merged into Cosigua Revenue (US$ millions) 47.7 ND 68.9 (presently Gerdau S.A.) Net income (US$ millions) (5.0) ND (0.4) USIBA - October/1989 1989 1990 1991 1992 1993 1994 Production of Crude Steel (in 1,000 tons) 336.4 315.9 310.0 330.2 377.9 401.4 Revenue (US$ millions) 101.8 78.8 72.9 91.6 96.6 167.4 Net income (US$ millions) (19.2) (12.6) 1.7 (3.1) 2.3 1.2 PIRATINI February/1992 1991 1992 1993 1994 1995 Production of Crude Steel (in 1,000 tons) 171.9 141.4 178.2 192.4 Merged into Riograndense Revenue (US$ millions) 66.8 61.3 94.1 164.6 (presently Gerdau S.A.) Net income (US$ millions) (21.0) (5.1) 1.4 2.3 PAINS - February/1994 10/92 to

09/93 10/93 to

12/94 1995 1996 1997

Production of Crude Steel (in 1,000 tons) 438.2 502.7 343.5 385.5 Merged into Gerdau S.A. Revenue (US$ millions) 138.8 253.0 219.1 193.6 Net income (US$ millions) 2.6 2.6 4.5 6.0

Future

The Company will continue to implement its strategy over the near and medium-term, by undertaking the following steps:

• Financial Management: Given the high cost of financing in Brazil and the current trend toward consolidation in the steel industry worldwide, the Company's medium-term strategy is to consolidate its existing acquisitions and reduce financial expenses. This will be achieved through a financial strategy to extend the tenor of its existing debt in order to increase cash flow available for reinvestment without substantially increasing overall leverage of the Company. The intention is to fund capital expenditures increasingly out of cash flow, with the exception of strategic expansions required to maintain or establish market share in a profitable market segment. The focus is first on increasing the efficiency and profitability of existing operations and limiting allocation of capital for acquisitions to only the most important opportunities.

• Cost Management : The Company will continue to concentrate on securing adequate and reliable steel scrap supplies and adjusting its production levels to minimize variable costs of production. While the Company has the flexibility to switch production from the domestic market to exports, depending on market demand, domestic sales generally have been more profitable than export sales and it is likely in the future to focus heavily on regional sales for each of its companies. Nonetheless, the historical volatility of the Brazilian economy has made it a management priority that Gerdau maintain a high degree of production and market flexibility in order to quickly adapt to changing market conditions.

The acquisition of Cartersville (installed capacity of 726 thousand tons of crude steel per year in the USA) and the increase of the investment in Açominas also constitute important steps for the future development of the Company's business.

14 - 14 --1

Industry Overview - Worldwide and Brazil

Since the 1940s, steel has been of vital importance to the Brazilian economy. As a result of an interruption of steel supplies during World War II, the Brazilian government began developing the domestic steel industry by forming Companhia Siderúrgica Nacional ("CSN"), a flat steel producer, and Companhia Vale do Rio Doce, an iron ore producer. During almost 50 years of state control, the Brazilian flat steel sector was coordinated on a national basis under a steel monopoly, Siderbrá s. The state had far less involvement in the non-flat sector, which has traditionally been made up of smaller private sector companies such as Gerdau. As a result of the debt crisis of the 1980s, the Brazilian government's access to foreign capital became severely restricted and further investment in the state steel sector was reduced. For a general discussion as the Brazilian economic environment, see "Item 3.D - Risk Factors."

In 1990, the Brazilian government selected the steel industry as the first industry to become privatized. Starting in 1991, the larger integrated flat steel producers, which had operated as semi-autonomous companies under the control of Siderbrás, were individually privatized. Today, the Brazilian steel industry is composed of 12 companies, with an installed annual capacity of approximately 33 million tons, producing a full range of flat, non-flat, carbon, stainless and specialty steel. The flat steel industry is currently dominated by the producers that before privatization used to belong to Siderbrás, such as CSN, while Gerdau has become the leading producer of long steel products.

Brazil exports a great part of its steel production. In 2001, the Brazilian steel industry exported 9.3 million tons, while it imported only 1.1 million tons. Steel imports in 2001 represented 6.1% of domestic apparent steel consumption (defined as domestic sales plus imports).

Brazil's production of crude steel rose from 20.6 million tons in 1990 to 26.7 million tons in 2001. In 2001, Brazil accounted for over 51.6% of total steel production in Latin America, with production over two times that of Mexico, the second largest producer in Latin America, and approximately 29.7% of U.S. production.

Crude steel products comprise non-finished ingots, billets, blooms and slabs produced at the melting and casting stage of the production process. Rolled products are higher value-added products manufactured from crude steel at the intermediate stage of production in rolling mills. Long rolled products include wire rod, rebars, profiles, and round, square and flat bars.

All information concerning the steel industry contained herein was obtained from either IBS (the Brazilian Steel Institute) reports or IISI (International Institute for the Steel Industry) and was not prepared specifically for Gerdau. This information is publicly available and is presented in a standardized format. IBS is comprised of Brazilian steel companies, and Gerdau is included among them as an associated member.

The following table shows historical crude steel production (in millions of tons) and related data for the periods indicated: World U.S. South

America Mexico Brazil Brazil - % of

World Production (millions of tons) 1990 770.5 89.7 29.3 8.7 20.6 2.7 1991 733.6 79.7 30.9 8.0 22.6 3.1 1992 719.7 84.3 32.3 8.5 23.9 3.3 1993 727.5 88.8 33.8 9.2 25.2 3.5 1994 725.2 91.2 35.0 10.3 25.7 3.5 1995 752.3 95.2 34.6 12.1 25.1 3.3 1996 750.0 95.5 35.9 13.2 25.2 3.4 1997 798.9 98.5 37.0 14.2 26.2 3.3 1998 777.2 98.7 36.1 14.2 25.8 3.4 1999 788.3 97.4 34.6 15.3 25.0 3.2 2000 829.6 100.7 39.1 15.7 27.9 3.4 2001 831.8 89.7 37.6 13.5 26.7 3.2 Source: IBS / IISI

15 - 15 --1

The following table shows historical rolled steel production (in millions of tons) in Brazil for the periods indicated. Rolled Products - Brazil Flat Long Total (millions of tons) 1990 8.8 6.0 14.8 1991 9.4 5.5 14.9 1992 10.1 5.8 15.9 1993 10.0 6.5 16.5 1994 10.7 6.7 17.4 1995 10.6 5.5 16.1 1996 11.0 5.7 16.7 1997 11.3 6.1 17.4 1998 10.4 6.0 16.4 1999 10.1 6.7 16.8 2000 11.2 7.0 18.2 2001 10.7 7.4 18.1 Source: IBS

Consumption

Real GDP in Brazil grew at a rate of 1.5% in 2001 (based on preliminary data) and 4.5% and 0.8% in 2000 and 1999, respectively. Total domestic steel sales increased by over 33.9% from 11,725 million tons in 1995 to 15,696 million tons in 2001. Brazilian industrial production grew in all of the steel intensive sectors of the economy, especially capital goods and consumer durables.

Historically, the Brazilian steel industry has been affected by substantial fluctuations in domestic demand for steel. Although national per capita demand varies with GDP, fluctuations in steel demand tend to be more pronounced than changes in economic activity. For purposes of comparison, the following table sets forth global steel apparent consumption from 1993 through 2000, the most recent year for which statistics are available. Apparent Steel Consumption of Finished Steel World US

South America Mexico Brazil

(millions tons of finished steel products) 1993 614.1 90.8 18.9 7.5 10.6 1994 619.8 103.1 20.9 8.8 12.1 1995 656.0 100.0 22.1 5.9 12.0 1996 651.8 107.0 23.1 8.1 13.0 1997 701.7 113.4 26.6 9.7 15.3 1998 691.6 119.8 25.7 10.6 14.5 1999 700.3 116.4 22.6 10.9 14.1 2000 761.6 120.0 24.7 11.3 15.8 2001 * * * * 16.7 * 2001 data are not available Source: IISI

Production Costs

Brazil is one of the world's lowest cost producers of steel. Brazil's advantages include a relatively inexpensive and abundant supply of raw ma terials, as well as low labor costs. Brazil also has the benefit of a relatively large internal market. These advantages are offset to some extent by such factors as dependence on imported coal, high internal costs of financing and restricted availability of electric energy.

16 - 16 --1

Production Process

In 2001, the Company was the largest manufacturer of long-rolled steel products and the fourth largest crude steel producer in Brazil. The Company offers over 34,000 products in the commodity steel, rolled steel, dra wn steel and specialty steel segments of the steel market. In 2001, the Company produced 3,470 thousand metric tons of crude steel in Brazil (not including Açominas’ production) and 2,580 thousand metric tons of crude steel abroad.

Domestic Steel Production

The Company's production of steel has increased steadily since 1991 mainly due to the acquisition of several steel companies and increases in the installed capacity of the Company's steel mills. Comparing the production capacities in 1992 and 2001, on the table below, the increase is notable:

Production Capacity

(million of tons) Crude Steel Long rolled products Drawn products 2001 7.3 7.0 0.9 1992 3.9 3.3 0.8

In 2001, 57.4%, or 3.5 million tons of the Company's crude steel was produced in Brazil (excluding Açominas) and 42.6%, or 2.6 million tons, was produced by the Company's subsidiaries located in Canada, Chile, Uruguay and the United States; while 57.1%, or 3.3 million tons, of the Company's long rolled products was produced in Brazil (excluding Açominas), 42.9%, or 2.5 million tons, was produced outside Brazil (excluding Sipar). All of the Company's drawn products are produced in Brazil.

According to IBS data, in 1975 Brazilian steel production equaled 8.3 million tons of crude steel and 3.6 million tons of long rolled products. In the same year Gerdau companies produced 525 thousand tons of crude steel and 506 thousand tons of long rolled products, 6.3% and 14.1%, respectively.

The table below sets forth, for the periods indicated, a comparison of the annual production of crude and long rolled steel for Brazil and for Gerdau S.A. and the percentage of crude and long rolled steel production attributable to the Company:

Output - Gerdau S.A. non-consolidated and Brazil (in millions of tons) Crude Steel Long Rolled Products* Brazil Gerdau S.A.

non-consolidated Gerdau S.A.

(%) Brazil Gerdau S.A.

non-consolidated Gerdau S.A.

(%)

1990 20,567 2,374.0 11.5 5,921 1,900.8 31.1 1991 22,617 2,090.3 9.2 5,533 1,804.7 32.6 1992 23,934 2,427.5 10.1 5,741 2,084.9 36.3 1993 25,207 2,588.2 10.3 6,477 2,268.0 35.0 1994 25,747 3,039.4 11.8 6,618 2,673.8 40.4 1995 25,076 2,752.7 11.0 5,434 2,455.6 45.1 1996 25,237 2,877.9 11.4 5,661 2,528.6 44.7 1997 26,153 3,051.4 11.7 6,158 2,781.4 45.2 1998 25,760 2,974.2 11.6 6,047 2,753.1 46.0 1999 24,996 3,270.5 13.1 6,672 3,054.9 45.8 2000 27,865 3,495.9 12.5 7,000 3,250.3 46.4 2001 26,718 3,470.1 13.0 7.425 3,301.4 44.5

Source: IBS/Gerdau * See also, - “Competition.”

17 - 17 --1

Gerdau S.A.'s production process is based mostly on the mini-mill concept. It has six electric arc furnace ("EAF") mills, two small integrated units and one direct reduction iron ("DRI") plant.

Mini-mills are smaller mills which offer several advantages over the larger integrated steel producers, including: (i) lower capital costs; (ii) lower operational risks due to the avoidance of a concentration of capital and production capacity in a single production unit; (iii) the proximity of production units to raw material sources; (iv) the proximity to the local markets and the ease of adjustments in production levels; (v) less expensive raw material costs, principally due to the use of steel scrap instead of iron ore and coke, which are employed by the larger integrated mills; and (vi) more efficient management structure due to the relative simplicity of the production process and lower manning levels required.

The Company's production process consists of (i) sourcing, (ii) melting, (iii) casting, (iv) rolling and (v) drawing.

Sourcing

The Company's mini-mills (which have annual crude steel production capacities ranging from 70,000 tons to 1.4 million tons) use steel scrap and pig iron produced from within a radius of 120 to 300 miles and manufacture primarily products for consumption within the region in wh ich the mill is located. This production strategy has the advantage of minimizing transportation costs of raw materials and final products and allows capacity adjustments to be made in relatively small increments. The Company acquires its main raw materia l, steel scrap for use in its electric arc furnaces, from an extensive network of more than 4,500 suppliers. The Company believes it is the largest purchaser of steel scrap in Brazil. Iron ore for use in its blast furnaces and DRI plant is bought from several Brazilian mining companies. Pig iron, for use in its electric arc furnaces, is produced by the Company or bought from third parties. In 2001, the Company produced approximately 70% of its pig iron consumption needs.

Liquid Steel Production

Liquid steel is produced in electric arc furnaces, energy optimizer furnaces or in a blast furnace/converter combination. After charging the electric arc furnace with the predetermined mixture of raw materials (i.e., scrap, pig iron or DRI), electric power is applied following a computer-controlled melting profile. The Company's mixture of raw material varies from 60% steel scrap and 40% pig iron to 90% steel scrap and 10% pig iron, depending upon prices and local availability. The Company believes that these ratios optimize the use of available steel scrap without causing demand pressure in the relevant steel scrap markets. In the blast furnace/converter combination, liquid steel is produced by reducing iron ore by burning charcoal, coke or a combination of both with oxygen. DRI is a process that replaces the blast furnace and reduces the amount of iron ore used by injecting hot natural gas, producing what is commonly known as sponge iron, which will then be placed into an electric arc furnace or a converter.

The molten steel is then tapped into the ladle furnace where it is refined according to customer specification. Ferro-alloys are added in the ladle furnace according to the chemical specifications of the grade of steel being produced. In the case of high-alloy steel, or specialty steel, the ladle is taken to a vacuum degasification unit to remove carbon, oxygen and gases.

Continuous Casting

The liquid steel is transferred from the ladle furnace into a continuous casting machine from which it emerges as a continuous square strand of steel that is cut into pre-determined lengths, called billets. In the continuous casting machine, the liquid steel is poured into a mold and cooled from the outside in, so that a solidified shell is formed around the molten metal as it emerges from the mold, allowing it to hold its shape.

Downstream Processing

The billets are transferred to a rolling mill to produce finished, rolled or drawn products. The billets are reheated, reduced in diameter and then rolled into finished reinforcing concrete bars ("rebars"), bars, shapes, and wire rod. These products then are allowed to cool uniformly. Drawn products are created by drawing wire rod, without reheating, producing wires of various shapes and thickness, such as welding wires, barbed and barbless fencing wires, galvanized wires, concrete reinforcing wire, and other wires. Wire is also the input for other products such as wire meshes, chains, nails and clamps.

18 - 18 --1

Set forth below is a brief description of the Company's main product lines and the markets they serve:

Crude Steel - Crude steel has a relatively low value-added process. The Company's main crude steel product is continuously cast billets, most of which is consumed by the Company in the manufacture of finished products and specialty steels. During 2001, billets accounted for 1.6% of the Company's domestic sales and 28.2% of export sales, as measured by weight.

Rolled Steel - Billets are used to manufacture rolled products such as wire rod, rebars, profiles and round, square and flat bars. In 2001, common steel rolled products accounted for 56.4% of the Company's domestic sales, 68.1% of export sales and 100% of the sales of the subsidiaries abroad, as measured by weight. The main market for the Company's domestic sales of rebars is Brazil's civil construction market, which uses finished steel products for a variety of purposes including water dams, port docks and facilities, bridges, highways, tunnels and commercial and residential building construction.

Drawn Steel -These are high value added products and include wires of various shapes and thicknesses, welding wires, barbed and barbless fencing wires, galvanized wires, concrete reinforcing wire mesh, nails and clamps. These products are sold to the manufacturing, the civil construction and the agriculture sector. In 2001, drawn products accounted for 21.0% of the Company's domestic sales and 2.6% of exports, as measured by weight.

Specialty Steel - Specialty or high-alloy steel requires advanced manufacturing processes and normally includes some degree of customization. The Company produces specialty steel, which includes stainless steel, used for the manufacturing of tools and machinery (e.g. cold, hot and high-speed steels), chains, fasteners, railroad spikes and special spring steel, at the Piratini plant. Specialty steel products are mainly consumed by Brazil's manufacturing sector, including the automotive and mechanical industries. In 2001, production at the Piratini plant represented approximately 31.7% of the Brazilian long specialty steel production. Each level of processing adds value to the simple crude steel product and as the product goes through incremental refining processes, it commands a significantly higher price in the market. Specialty steel accounted for 7.6% of domes tic sales and 1.1% of exports in the same year, as measured by weight.

The following is a description of several of the products produced by the Company:

CIVIL CONSTRUCTION PRODUCTS

GG-50, CA-60 and CA-25 concrete reinforcing bars (rebars) Annealed wire

Ribbed welded wire mesh for reinforced concrete

Transfer bars POP columns and meshes Stirrups and supports

Structural profiles Fabricated rebar

Casa Fácil Gerdau (rolled steel structure for low-income housing) INDUSTRIAL PRODUCTS

Hot rolled flat, round and square bars

Cold drawn round, square and hexagonal bars Blooms Angles

Channel, I-beam, T-Shapes and W-beams Ribbed T profile Elevator guide rails

Star profile Slabs

19 - 19 --1

Tribar Wire rod

Rolled and continuous cast billets

Steel railroad ties Special section profiles (manufactured in Canada)

Grader blades

Smelter bars Light rails

Superlight I-beams Elevator guide rails

Metallurgy

Complete line of wires for industrial applications, welding and wire ropes AGRICULTURAL PRODUCTS

Oval-shaped wire and barbed wire

High-Strength steel fence posts Staples for fences

Cercafix post-spacing wire

Wire and posts for electric fences Wire rope for corrals

Wire and wire rope for agricultural products Galvanized wire

Plastic-coated galvanized wire

Chain link fences NAILS

Bulk nails - construction

Bulk nails - carpentry Bulk nails - packaging

SPECIALTY STEELS Engineering steels (carbon and alloyed)

Round and square rolled bars

Wire rod Forged bars

Cold-finished products

Heat treatment Tool steels

Forged bars and blooms

Round, square and flat rolled bars Stainless steels

Round and square rolled bars Wire rod

Forged bars

Cold-finished

20 - 20 --1

Foreign Subsidiaries' Steel Production

The Company's production of steel abroad has grown steadily between 1981 and 1999, through acquisitions and increases in the production capacity of its foreign facilities. In acquiring foreign businesses, the Company has maintained its focus on the mini-mill-based production of long common steel products, but also seeks undervalued or under-performing steel mills. The Company believes that due to the large capital investment required to build a steel mill and the existing global oversupply of steel, acquisitions are the preferred means of expansion outside Brazil.

The following table sets forth, for the periods indicated, the production of crude steel and rolled products of the Company's production facilities abroad (in thousands of tons): LAISA

(Uruguay)

AZA (Chile)

COURTICE (Canada)

MRM (Canada)

SIPSA (Argentina)

AMERISTEEL (USA)

Year Crude Steel

Long Rolled Products

Crude Steel

Long Rolled Products

Crude Steel

Long Rolled Products

Crude Steel

Long Rolled Products

Crude Steel

Long Rolled Products

Crude Steel

Long Rolled Products

1993 29.0 29.0 34.0 25.0 227.0 190.0 - - - - - - 1994 28.9 28.3 41.8 27.9 234.0 199.2 - - - - - - 1995 33.7 29.2 62.7 54.3 245.0 182.2 156.4 142.4 - - - - 1996 43.5 36.1 72.8 68.1 244.5 206.2 273.8 258.0 - - - - 1997 45.9 39.3 79.5 75.9 201.1 176.3 310.3 277.9 - - - - 1998 51.4 45.2 80.4 75.7 259.8 220.5 294.9 265.0 - 39.0 - - 1999 45.4 41.6 140.9 122.2 260.4 250.6 290.6 261.3 - 38.5 453.9* 405.9* 2000 43.7 40.1 216.5 200.6 281.8 269.1 304.8 270.2 - 37.9 1,761.2 1,655.7 2001 41.2 37.3 244.2 225.7 294.4 274.6 321.4 277.8 - 29.4 1,678.8 1,640.3 * October through December

Laisa. In 1981, the Company acquired the Laisa mini-mill, located in Uruguay. Laisa has been profitable for the last 12 years and is the largest producer of long steel products in Uruguay. Laisa has a production capacity of 70,000 tons of crude steel and 72,000 tons of rolled steel per annum. Laisa is the only domestic steel producer in Uruguay. Production statistics are based on Laisa's production and sales added to Uruguayan imports. Import data are provided by the Customs of Uruguay and the Bank of the Republic, its financial agent. These two institutions report to the Ministry of Economy.