20 13 financial r eports of firstontario credit … · financ we b for ou opini in ou conso conso...

TRANSCRIPT

20

FIR

13 FIN

RSTO

NANC

NTAR

IAL R

RIO CR

EPOR

REDIT

RTS O

UNIO

F

ON LIMMITED

CONTENTS

Report on Management Responsibility 1

Loan Statistics 2

Report of the Audit Committee 3

Consolidated Financial Statements

Independent Auditors’ Report 4

Consolidated Statement of Financial Position 5

Consolidated Statement of Income 6

Consolidated Statement of Income and Other Comprehensive Income 7

Consolidated Statement of Changes in Members’ Equity 7

Consolidated Statement of Cash Flows 8

Notes to Consolidated Financial Statements 9

REP

The a

Repo

respo

opinio

accor

Popul

effect

To m

Mana

believ

are re

prope

The B

Statem

The B

review

audito

with t

relatin

The

condit

with th

KPMG

Statem

shown

Kelly

Presid

Octob

PORT ON

accompanying

rt are the re

onsible for the

on of Manag

rdance with I

laires Act, 19

ts of current e

meet its resp

agement has

ves that this s

eliable and f

erly accounted

Board of Dir

ments and fo

Board of Dire

w of financial

ors have full a

he Board of

ng to financia

Deposit Insu

tions and affa

he provisions

G LLP, Mem

ments in acc

n as part of th

McGiffin

dent and Chie

ber 30, 2013

N MANAG

g Consolidate

esponsibility o

e integrity and

gement, have

nternational

994 (Ontario)

events and tra

ponsibility for

developed a

system of inte

form a prope

d for and are

rectors is re

or overseeing

ectors carried

results and

and free acce

Directors, wit

l statement p

urance Corpo

airs of FirstO

s of the Act.

mber–appoint

cordance with

he Consolidat

ef Executive O

GEMENT R

ed Financial

of the Mana

d fairness of th

e been prepa

Financial Re

and are base

ansactions.

r the integrity

nd maintains

ernal controls

er basis for p

safeguarded.

sponsible for

Managemen

d out its resp

operations an

ess to, and m

th or without

resentation, i

oration of O

Ontario. The e

ted external

h Canadian g

ted Financial

Officer

RESPONS

Statements a

agement of F

he information

ared using a

eporting Stan

ed on informe

y and objec

s a system of

provides rea

preparation o

.

r reviewing a

nt’s performan

onsibility for

nd through its

meet periodica

Management

nternal contro

Ontario condu

examination i

auditors, h

generally acce

Statements.

Barry Do

Executiv

Officer

SIBILITY

and all inform

FirstOntario C

n presented.

appropriate a

ndards and th

ed judgments

ctivity of data

f internal acc

sonable assu

of financial st

and approvin

nce of its fina

the financial

s Audit Comm

ally with, the A

t present, to

ols and audit

ucts periodic

ncludes revie

as examined

epted auditin

oan, CPA, CA

ve Vice–Pre

mation contai

Credit Union

The financial

accounting po

he Credit Un

s and estimate

a in the fina

counting cont

urance that th

tatements an

ng the Cons

ancial reporti

statements t

mittee. The M

Audit Commit

discuss their

procedures.

c examination

ew of FirstOn

d the Cons

g standards

A, MAcc

esident and

ned in this A

Limited, wh

l statements,

olicies that a

nions and Ca

es of the exp

ancial statem

trols. Manage

he financial re

nd that asset

solidated Fin

ng responsib

through its re

Member–appo

ttee and may

r audit and m

n of the fin

ntario’s comp

olidated Fin

and their rep

Chief Fin

1

Annual

ich is

in the

are in

aisses

pected

ments,

ement

ecords

ts are

ancial

bilities.

egular

ointed

y meet

matters

ancial

liance

ancial

port is

ancial

2

Loan Statistics

For the year ended August 31, 2013

Total retail loan applications received 14,372

Total retail loans declined 5,130

Retail loans granted include:

Personal loans 3,732 for $ 49,030,933

Mortgages 1,379 for $ 250,550,684

Lines of Credit 648 for $ 7,549,937

Authorized Overdrafts 238 for $ 229,100

MeritLines 413 for $ 46,252,141

Commercial loans granted include:

Demand term loans 36 for $ 79,974,347

Demand operating loans 10 for $ 13,460,800

Commercial mortgages 17 for $ 39,266,610

Delinquent loans:

Total loans delinquent, 90 days and over 104 loans

Value of loans delinquent, 90 days and over $ 9,322,867

REP

FirstO

to Se

Ontar

all of

Act.

The A

mand

activit

S

D

th

fin

O

im

an

S

w

R

pa

There

imple

Audit

there

theret

Based

of Dir

follow

Comm

role in

struct

Diann

Chair

Octob

PORT OF

Ontario Credit

ction 125 of

rio Regulation

the duties, w

Audit Committ

ate. During t

ties:

erved as the

Directors and,

he conversion

nancial statem

Obtained a re

mportant to s

nd ensuring c

erved as the

work plan and

Reviewed the

articular focus

e are no sign

mented or ar

Committee b

any further m

to.

d on its findin

rectors or sen

ws up to ensur

mittee receive

n maintaining

ture of the Cre

ne MacLean

, Audit Comm

ber 30, 2013

THE AUD

t Union Limite

the Credit U

n 237/09. The

which are spe

tee is pleased

he year the C

e principal co

in particular,

n to Internatio

ments prior to

easonable un

afeguarding t

compliance w

Board’s liais

reports.

policies, pro

s on requirem

ificant recom

re in the proce

believes shoul

matters that

ngs, the Audit

nior managem

re that the rec

ed full co–ope

the quality o

edit Union.

mittee

DIT COM

ed’s Audit Com

nions and Ca

e Committee,

ecified to be p

d to report to

Committee he

ommunication

, reviewed the

onal Financial

o Board appro

nderstanding

the assets of

with policies an

son with the i

ocedures and

ments for liqui

mendations m

ess of being

ld be reported

are required

t Committee i

ment, as app

commendatio

eration and su

of financial rep

MITTEE

mmittee is a c

aisses Popula

which consis

performed by

the Members

eld four meet

n link betwee

e terms of en

Reporting St

oval for issuan

of the impor

f FirstOntario

nd procedure

nternal audito

controls, wh

dity, capital a

made by the

implemented

d to the Mem

to be disclos

ssues reports

propriate, with

ons are consid

upport from m

porting to the

committee of

aires Act, 19

sts of four dir

y audit comm

s of FirstOnta

tings and com

en the extern

ngagement a

tandards and

nce to the Me

rtant element

o, ensuring th

s.

or and review

hich relate to

adequacy and

Audit Comm

. In addition,

bers, other th

sed pursuant

s and makes

h respect to t

dered and im

management

Members an

the Board of

94 (Ontario)

rectors, has a

mittees in the

ario that it has

mpleted the fo

nal auditors

nd scope of

d reviewed Fir

embers.

ts of internal

he accuracy o

wed the intern

o legislative c

d interest rate

mittee that hav

there are no

han as describ

t to the Act o

recommenda

the matters o

plemented. D

to enable it t

nd enhancing

Directors pur

and Section

a mandate to

Regulations

s fulfilled its a

ollowing sign

and the Boa

the audit, ove

rstOntario’s a

l controls tha

of financial re

nal audit man

compliance, w

managemen

ve not been

matters whic

bed above, no

or the Regula

ations to the B

outlined above

During the yea

to play an eff

the overall c

3

rsuant

27 of

cover

of the

annual

ificant

ard of

ersaw

annual

at are

eports

ndate,

with a

nt.

either

ch the

or are

ations

Board

e and

ar, the

fective

control

To the

We hLimiteconsoand cpolicie

Mana

Manastatemcontrostatem

Audit

Our reaudit.Thoseobtainmater

An auin thethe awhethto thedesigexpreevaluestimfinanc

We bfor ou

Opini

In ouconsoconsoaccor

Chart

HamilOctob

KPMCharBox 21 KHam

e Members of

ave audited ed, which comolidated statecash flows fores and other

agement’s Re

agement is rements in accol as managements that are

tor’s Respon

esponsibility We conducte standards rn reasonablerial misstatem

udit involves p consolidated

assessment oher due to frae entity’s prepn audit proc

essing an opiating the appates made bycial statement

elieve that thur audit opinio

ion

r opinion, tholidated finanolidated finanrdance with In

tered Account

lton, Canada ber 30, 2013

MG LLP rtered Accountants 976

King Street West Sumilton ON L8N 3R1

KPMG LLP is network of ind(“KPMG InternKPMG Canad KPMG Conf

INDEP

f FirstOntario

the accompamprise the coments of incr the year theexplanatory in

esponsibility

esponsible forcordance withement determe free from m

nsibility

is to expressted our audit require that we assurance ment.

performing prd financial staof the risks ud or error. Inparation and

cedures that inion on the propriatenessy managemets.

e audit evideon.

he consolidatcial position

ncial performnternational F

tants, License

uite 700

a Canadian limited liabilityependent member firms a

national”), a Swiss entity. a provides services to KPM

idential

PENDENT

Credit Union

anying consoonsolidated stome and oth

en ended, annformation.

y for the Con

r the preparah Internationamines is nece

aterial missta

s an opinion oin accordanc

we comply witabout wheth

rocedures to oatements. Theof material m

n making thosfair presentaare appropreffectiveness

s of accountinent, as well a

ence we have

ed financial of FirstOntarance and itsinancial Repo

ed Public Acc

y partnership and a membeffiliated with KPMG Interna

MG LLP.

T AUDITO

n Limited

lidated financtatement of fi

her comprehed notes, com

solidated Fin

tion and fair al Financial Rssary to enab

atement, whet

on these conce with Canath ethical requer the conso

obtain audit ee procedures misstatementse risk assessation of the ciate in the cs of the entitng policies us evaluating

e obtained is s

statements prio Credit Uns consolidateorting Standa

countants

er firm of the KPMG ational Cooperative

ORS’ REP

cial statemeninancial posit

ensive incomemprising a sum

nancial State

presentation Reporting Stable the prepather due to fra

solidated finadian generalluirements anolidated finan

evidence aboselected dep

t of the consments, we c

consolidated fcircumstancesty’s internal csed and the the overall p

sufficient and

present fairlynion Limited aed cash flowards.

TelephTelefawww.k

PORT

nts of FirstOntion as at Aue, changes inmmary of sig

ements

of these conandards, andaration of conaud or error.

ancial statemly accepted ad plan and p

ncial stateme

ut the amounpend on our jusolidated fina

consider internfinancial states, but not focontrol. An areasonablen

presentation o

d appropriate

y, in all mateas at August

ws for the ye

hone (905) 523-820ax (905) 523-2222kpmg.ca

ntario Credit gust 31, 201n members’ enificant accou

nsolidated find for such innsolidated fin

ents based oauditing standerform the au

ents are free

nts and discloudgment, inclancial statemnal control relements in ordor the purpoaudit also incness of accouof the consoli

to provide a

erial respects31, 2013, a

ear then end

00

4

Union 3, the equity unting

ancial nternal ancial

on our dards. udit to

e from

osures luding

ments, levant der to

ose of cludes unting idated

basis

s, the nd its

ded in

FIRSCons As at

(In tho

AsseLoaResPerComAcc

OthCasInveFixeDerOth

LiabiMemDepMemInveAcc

OthLoaAccDer

Mem Inve Con Ret Acc

Comm

See a

On be

Direct

STONTARsolidated S

August 31, 2

ousands of do

ets ans Receivabsidential mortrsonal loans (mmercial loancrued interest

her sh and cash eestments (noted assets (norivative financher assets

ilities mbers’ Depoposits (note 1mbership shaestment sharecrued interest

her ans payable (ncounts payablrivative financ

bers’ Equitestment sharentributed surptained earningcumulated oth

mitments (not

accompanying

ehalf of the Bo

tor

RIO CREStatement

013, with com

ollars)

ble from Memgage loans (nnote 5)

ns (note 5) receivable

equivalents (nte 9)

ote 10) cial instrumen

osits and Sha1)

ares (note 12)es (note 12) on deposits a

note 14) le and accruecial instrumen

ty es (note 12)

plus gs her comprehe

te 20)

g notes to Co

oard:

DIT UNIOof Financi

mparative info

mbers note 5)

note 7)

nts (note 15)

ares

)

and shares

ed liabilitiesnts (note 15)

ensive loss

nsolidated Fi

ON LIMITEial Position

ormation for 2

nancial State

Director

ED n

2012

ements.

2013

$ 1,176,256 141,178

554,391 10,459

1,882,284

23,276 150,871 17,480

1,342 3,174

$ 2,078,427

$ 1,483,596 6,459

12,293 10,014

1,512,362

441,815 18,291

1,770 1,974,238

36,440 645

67,658 (554)

104,189

$ 2,078,427

$ 971449

1,62

2131

$ 1,80

$ 1,28

1

1,31

371

1,70

3

6 (

9

$ 1,80

5

2012

73,634 40,913 99,125 7,289

20,961

27,105 35,845 6,379 1,140 4,203

05,633

89,132 6,238 2,074 9,030

6,474

75,824 4,852 2,711

09,861

34,657 645

61,738 (1,268)

95,772

05,633

6

FIRSTONTARIO CREDIT UNION LIMITED Consolidated Statement of Income For the year ended August 31, 2013, with comparative information for 2012

(In thousands of dollars) 2013 2012

Interest and Investment Income Residential mortgage loans (note 5) $ 38,259 $ 32,885 Personal loans (note 5) 9,401 9,756 Commercial loans (note 5) 27,795 26,883 Other 3,288 3,704 78,743 73,228

Interest Expense Members’ deposits (note 11) 23,516 22,166 Dividends on membership and investment shares (note 12) 869 868 Derivative instruments 810 1,572 Loans (note 14) 10,108 7,714 35,303 32,320

Operating Margin before the Following 43,440 40,908 Provision for impaired loans (note 6) 585 (4,268) Other income 8,603 7,770 Gain on sale of joint venture (note 9) – 10,334 Operating Margin 52,628 54,744

Operating Expenses Salaries and employee benefits 23,485 22,595 Administrative 14,886 13,368 Occupancy 4,336 4,135 Members' deposit insurance protection 1,214 996 43,921 41,094

Operating Income 8,707 13,650

Unrealized Gains (Losses) Investments 752 440 Net gains (losses) on derivative financial instruments (863) 696

(111) 1,136

Income before Income Taxes 8,596 14,786

Income taxes (note 19) 1,077 1,688 Net income for the year $ 7,519 $ 13,098

See accompanying notes to Consolidated Financial Statements.

7

FIRSTONTARIO CREDIT UNION LIMITED Consolidated Statement of Income and Other Comprehensive Income For the year ended August 31, 2013, with comparative information for 2012

(In thousands of dollars) 2013 2012

Net income for the year $ 7,519 $ 13,098 Other Comprehensive Income (Loss) Items that are or may be reclassified subsequently to net income: Net gain (loss) on cash flow hedges (93) 594 Net gain (loss) on cash flow hedges transferred to earnings 863 (529) Net change in fair value of available–for–sale investments 37 (398) Net fair value amount of available–for–sale investments transferred to net income – 594 Related income taxes (note 19) (93) (40)

Total Income and Other Comprehensive Income for the year $ 8,233 $ 13,319

Consolidated Statement of Changes in Members’ Equity For the year ended August 31, 2013, with comparative information for 2012

(In thousands of dollars) 2013 2012

Investment Shares (Note 12) Balance at beginning of year $ 34,657 $ 32,824 Shares issued during year 1,920 1,833 Shares redeemed during year (137) –

Balance at end of year 36,440 34,657 Contributed Surplus Balance at beginning of year 645 645

Balance at end of year 645 645 Retained Earnings Balance at beginning of year 61,738 50,175 Net income for the year 7,519 13,098 Dividends paid (net of income tax recovery of $321 (2012– $281)) (1,599) (1,535)

Balance at end of year 67,658 61,738 Accumulated Other Comprehensive Income (Loss), net of tax Cash flow hedging reserve: Balance at beginning of year (1,303) (1,358) Other comprehensive income for the year 683 55

Balance at end of year (620) (1,303) Fair value reserve on available for sale investments: Balance at beginning of year 35 (131) Other comprehensive income for the year 31 166

Balance at end of year 66 35 Balance at end of year (554) (1,268)

Total Members’ Equity $ 104,189 $ 95,772

See accompanying notes to Consolidated Financial Statements.

8

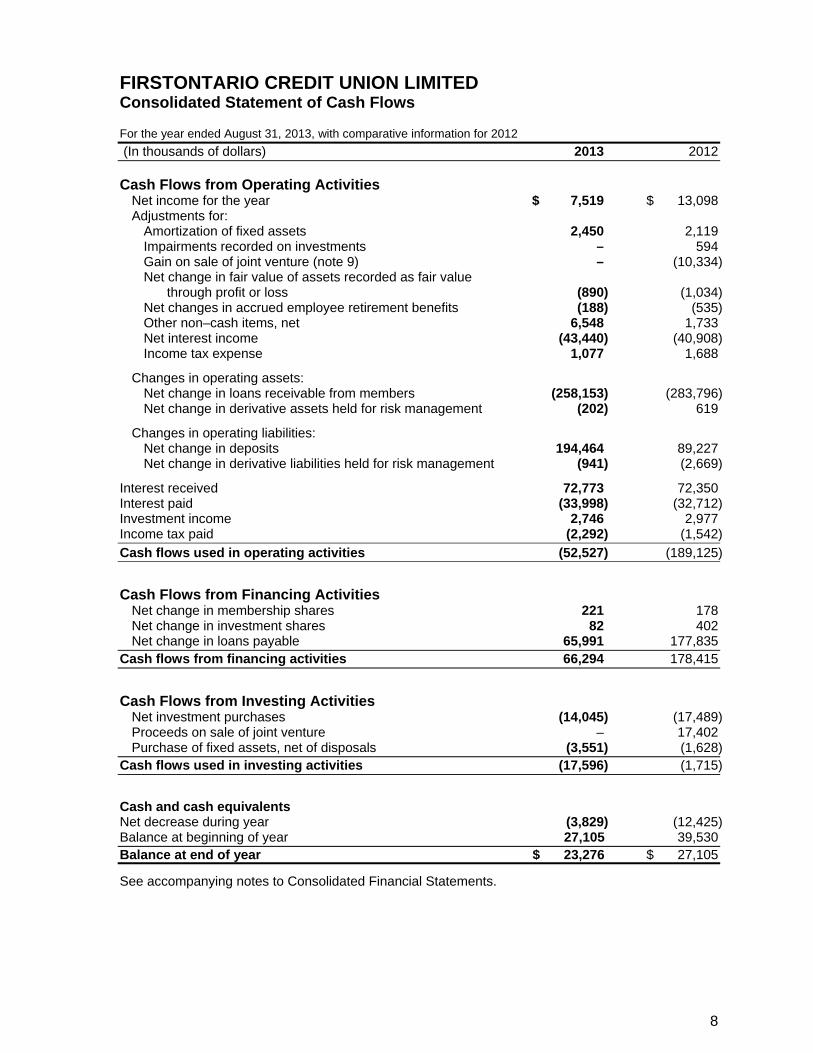

FIRSTONTARIO CREDIT UNION LIMITED Consolidated Statement of Cash Flows For the year ended August 31, 2013, with comparative information for 2012

(In thousands of dollars) 2013 2012

Cash Flows from Operating Activities Net income for the year $ 7,519 $ 13,098 Adjustments for: Amortization of fixed assets 2,450 2,119 Impairments recorded on investments – 594 Gain on sale of joint venture (note 9) – (10,334) Net change in fair value of assets recorded as fair value through profit or loss (890) (1,034) Net changes in accrued employee retirement benefits (188) (535) Other non–cash items, net 6,548 1,733 Net interest income (43,440) (40,908) Income tax expense 1,077 1,688

Changes in operating assets: Net change in loans receivable from members (258,153) (283,796) Net change in derivative assets held for risk management (202) 619

Changes in operating liabilities: Net change in deposits 194,464 89,227 Net change in derivative liabilities held for risk management (941) (2,669)

Interest received 72,773 72,350 Interest paid (33,998) (32,712) Investment income 2,746 2,977 Income tax paid (2,292) (1,542)

Cash flows used in operating activities (52,527) (189,125)

Cash Flows from Financing Activities Net change in membership shares 221 178 Net change in investment shares 82 402 Net change in loans payable 65,991 177,835 Cash flows from financing activities 66,294 178,415

Cash Flows from Investing Activities Net investment purchases (14,045) (17,489) Proceeds on sale of joint venture – 17,402 Purchase of fixed assets, net of disposals (3,551) (1,628) Cash flows used in investing activities (17,596) (1,715)

Cash and cash equivalents Net decrease during year (3,829) (12,425) Balance at beginning of year 27,105 39,530 Balance at end of year $ 23,276 $ 27,105

See accompanying notes to Consolidated Financial Statements.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

9

1. Corporate Information

FirstOntario Credit Union Limited (“FirstOntario”) is a financial institution incorporated in Ontario

which operates in compliance with the Credit Unions and Caisses Populaires Act of Ontario (the

“Act”) and is a member of Central 1 Credit Union (“Central 1”). The location of the head office and

principal place of business of FirstOntario is 688 Queensdale Avenue East, Hamilton, Ontario,

L8V 1M1.

FirstOntario exists to help Members meet their financial needs in their local communities.

FirstOntario’s principal activities are the provision of deposit–taking, lending and other financial

services.

FirstOntario’s Member deposits are insured by the Deposit Insurance Corporation of Ontario

(“DICO”) under a mandatory program, the expense for which amounted to $1,214,000 in 2013

and $996,000 in 2012. At August 31, 2013 there were 90,167 Members (2012 – 87,822).

2. Basis of Preparation:

Statement of compliance

The Consolidated Financial Statements of FirstOntario have been prepared in accordance with

International Financial Reporting Standards (“IFRS”). IFRS comprise of accounting standards

issued by the International Accounting Standards Board (“IASB”) as well as interpretations issued

by the IFRS Interpretations Committee.

These financial statements were approved by FirstOntario’s Board of Directors on October 30,

2013. The significant accounting policies used in the preparation of these Consolidated Financial

Statements are summarized below and have been applied consistently to all years presented in

the financial statements.

Use of estimates and judgments

The preparation of Consolidated Financial Statements in conformity with IFRS requires

management to make estimates and assumptions that affect the reported amounts of assets and

liabilities and the reported amounts in revenue and expenses during the reporting year. Actual

future results could differ from those estimates.

Items which result in the most significant areas of application of judgment and estimates include

the following:

(a) Fair value of financial instruments:

Where fair value of financial assets and liabilities cannot be derived from active markets,

FirstOntario uses valuation techniques that include inputs derived from either observable market

data or utilizing management judgment. Refer to Note 17 for information relating to these

estimates.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

10

2. Basis of Preparation (continued):

Use of estimates and judgments (continued)

(b) Allowance for impairment on loans:

FirstOntario reviews its loan portfolio frequently to assess impairment, and uses considerable

judgment in determining whether or not a loan is impaired as a result of observable evidence.

If a loan is considered to be impaired, the amount of the loss is estimated based on

management’s best estimates. Refer to Note 6 for information relating to these estimates.

(c) Employee retirement benefits:

FirstOntario estimates the present value of employee retirement benefits, which depends on

a number of assumptions including discount rates, expected salary and other cost increases,

and mortality rates. This estimate is used in the computation of pension expense for the year,

in accordance with the ‘corridor’ method (refer to Note 3(n)) after taking into account

management’s estimate of the expected return on plan assets. Refer to Note 18 for

information relating to these estimates.

3. Significant Accounting Policies:

These consolidated financial statements have been prepared on a going concern basis. The

significant accounting policies applied in the preparation of these consolidated financial

statements are set out below. The policies have been consistently applied to all of the years

presented.

(a) Basis of consolidation:

The Consolidated Financial Statements include the assets, liabilities and results of the

operations of FirstOntario and its wholly owned subsidiary 1320818 Ontario Limited which

supplies information technology services and operates the banking system for FirstOntario.

All intercompany transactions and balances have been eliminated.

Investments in which FirstOntario exercises joint control are accounted for as jointly

controlled assets, whereby FirstOntario’s share of revenue and expenses of the joint venture

are included in the Consolidated Statement of Income. FirstOntario’s net share of assets and

liabilities of the investments are included in the Consolidated Statement of Financial Position.

Investments are considered to be jointly controlled if there is a contractual agreement to

share authority over determining the investments’ operating, investment and financing

policies. The joint venture in which FirstOntario participates consist of investments in retail

complexes which generate income from the leasing of space for commercial use.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

11

3. Significant Accounting Policies (continued):

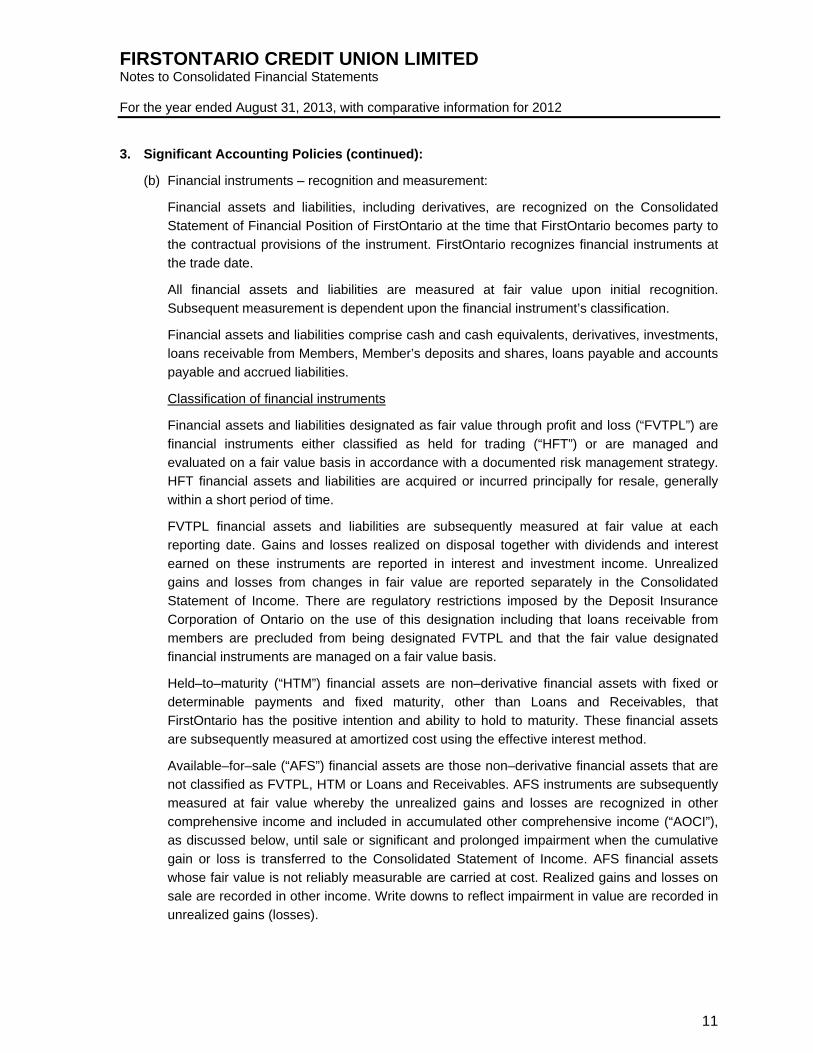

(b) Financial instruments – recognition and measurement:

Financial assets and liabilities, including derivatives, are recognized on the Consolidated

Statement of Financial Position of FirstOntario at the time that FirstOntario becomes party to

the contractual provisions of the instrument. FirstOntario recognizes financial instruments at

the trade date.

All financial assets and liabilities are measured at fair value upon initial recognition.

Subsequent measurement is dependent upon the financial instrument’s classification.

Financial assets and liabilities comprise cash and cash equivalents, derivatives, investments,

loans receivable from Members, Member’s deposits and shares, loans payable and accounts

payable and accrued liabilities.

Classification of financial instruments

Financial assets and liabilities designated as fair value through profit and loss (“FVTPL”) are

financial instruments either classified as held for trading (“HFT”) or are managed and

evaluated on a fair value basis in accordance with a documented risk management strategy.

HFT financial assets and liabilities are acquired or incurred principally for resale, generally

within a short period of time.

FVTPL financial assets and liabilities are subsequently measured at fair value at each

reporting date. Gains and losses realized on disposal together with dividends and interest

earned on these instruments are reported in interest and investment income. Unrealized

gains and losses from changes in fair value are reported separately in the Consolidated

Statement of Income. There are regulatory restrictions imposed by the Deposit Insurance

Corporation of Ontario on the use of this designation including that loans receivable from

members are precluded from being designated FVTPL and that the fair value designated

financial instruments are managed on a fair value basis.

Held–to–maturity (“HTM”) financial assets are non–derivative financial assets with fixed or

determinable payments and fixed maturity, other than Loans and Receivables, that

FirstOntario has the positive intention and ability to hold to maturity. These financial assets

are subsequently measured at amortized cost using the effective interest method.

Available–for–sale (“AFS”) financial assets are those non–derivative financial assets that are

not classified as FVTPL, HTM or Loans and Receivables. AFS instruments are subsequently

measured at fair value whereby the unrealized gains and losses are recognized in other

comprehensive income and included in accumulated other comprehensive income (“AOCI”),

as discussed below, until sale or significant and prolonged impairment when the cumulative

gain or loss is transferred to the Consolidated Statement of Income. AFS financial assets

whose fair value is not reliably measurable are carried at cost. Realized gains and losses on

sale are recorded in other income. Write downs to reflect impairment in value are recorded in

unrealized gains (losses).

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

12

3. Significant Accounting Policies (continued):

(b) Financial instruments – recognition and measurement (continued):

Loans and Receivables are non–derivative financial assets with fixed or determinable

payments that are not quoted in an active market. Financial assets classified as Loans and

Receivables are initially accounted for net of transaction costs and are subsequently

measured at amortized cost by applying the effective interest method.

Financial liabilities classified as Other Liabilities are subsequently measured at amortized

cost. Financial liabilities are initially recognized on the trade date FirstOntario becomes party

to the contractual provision of the instrument. FirstOntario derecognizes a financial liability

when its contractual obligations are discharged, cancelled or expire.

Classification of investment instruments is outlined in Note 9. Classification of all financial

instruments is outlined in Note 17.

Effective interest method

Interest income and expense are recognized in the Consolidated Statement of Income using

the effective interest method. The effective interest rate is the rate that discounts the

estimated future cash payments and receipts through the expected life of the financial asset

or liability to its net carrying amount upon initial recognition. The effective interest rate is

established on initial recognition of the financial asset or liability and is not revised

subsequently. The calculation of the effective interest rate includes transaction costs, fees

and discounts or premiums that are an integral part of the effective yield on the financial

asset or liability.

Transaction costs

Transaction costs are incremental costs that are directly attributable to the acquisition,

issuance or disposal of a financial asset or liability. Transaction costs related to FVTPL

financial assets and liabilities are expensed as incurred. Transaction costs relating to AFS

and HTM financial assets and loans and receivables are capitalized and amortized over the

expected life of the instrument using the effective interest method.

Offsetting

Financial assets and liabilities are offset and the net amount presented in the statement of

financial position when, and only when, FirstOntario has a legal right to set off the recognized

amounts and it intends either to settle on a net basis or to realize the asset and settle the

liability simultaneously.

Income and expenses are presented on a net basis only when permitted under IFRSs, or for

gains and losses arising from a group of similar transactions.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

13

3. Significant Accounting Policies (continued):

(b) Financial instruments – recognition and measurement (continued):

Identification and measurement of impairment losses

At each reporting date FirstOntario assesses whether there is objective evidence that

financial assets not carried at fair value through profit or loss are impaired. A financial asset

or group of financial assets is (are) impaired when objective evidence demonstrates that a

loss event has occurred after the initial recognition of the asset(s), and that the loss event has

an impact on the future cash flows of the asset(s) that can be estimated reliably.

For available–for–sale investments in equity securities, objective evidence includes a

significant or prolonged decline in its fair value below its cost.

For loans and receivables and held to maturity assets, impairment is assessed at the

individual and collective levels. Objective evidence can include, but is not limited to,

reasonable doubt as to the collectability of principal and interest, or when loan payments are

90 days past due. Collective allowances are established on a portfolio basis to absorb

probable loan losses for which a loss event has occurred but has not yet been identified by

management. The collectively assessed allowance is based on portfolio quality, past

experience, current economic conditions and management’s judgment.

Derivative financial instruments

Derivative financial instruments are financial contracts whose value is derived from interest

rates or other financial indices in the equity markets. In the ordinary course of business,

FirstOntario enters into various derivative contracts, including interest rate swaps, equity–

linked options, foreign exchange forwards and bond forwards. FirstOntario enters into such

contracts to manage interest rate fluctuations and foreign exchange risk as part of

FirstOntario’s asset/liability management program.

Interest rate swaps involve the periodic exchange of payments without the exchange of the

notional principal amount upon which the payments are based. Equity–linked options are

purchased to hedge deposit products whose interest is linked to various equity indices or a

specific bundle of equities. These contracts pay returns based on the change in value of

equity indices or a specific bundle of equities.

Foreign exchange contracts are used to hedge FirstOntario’s net US dollar liability position.

Derivatives are measured at fair value and are reported as assets where they have a positive

fair value and as liabilities where they have a negative fair value. In both cases they are

reported as derivative financial instruments in the financial statements.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

14

3. Significant Accounting Policies (continued):

(b) Financial instruments – recognition and measurement (continued):

Derivatives embedded in other financial instruments are separated from the host contract and

accounted for separately if their economic characteristics and risks are not closely related to

those of the host contract; the terms of the embedded derivatives would meet the definition of

a derivative if it was a free standing instrument, and the combined contract is not designated

as FVTPL and recorded at fair value. These embedded derivatives are classified as part of

the host instrument and measured at fair value with changes therein recognized on the

Consolidated Statement of Income.

Accrued interest receivable is recorded in other assets and accrued interest payable is

recorded in accounts payable and accrued liabilities. Interest income or expense is recorded

in interest income or interest expense, as applicable.

Hedge accounting

FirstOntario formally documents all relationships between hedging instruments and hedged

items; as well as risk management objectives and strategies for undertaking various hedge

transactions. This process includes linking all derivatives to specific assets and liabilities

recognized on the Consolidated Statement of Financial Position or specific firm commitments

or forecasted transactions that are highly probable to occur and prevent exposure to

variations in cash flows that could ultimately affect reported net income. FirstOntario also

formally assesses, both at the hedge’s inception and on an ongoing basis, whether the

derivatives that are used in hedging transactions are highly effective in offsetting changes in

fair values or cash flows of hedged items attributable to the hedged risk. FirstOntario

designates its interest rate hedge agreements as hedges of the underlying financial

instrument.

IFRS specifies the criteria that must be satisfied in order for hedge accounting to be applied

and prescribes the accounting treatment for those permitted hedging strategies applicable to

FirstOntario – fair value hedges and cash flow hedges.

In a fair value hedge, the change in fair value of the hedging derivative is offset on the

Consolidated Statement of Income by the change in fair value of the hedged item relating to

the hedged risk. FirstOntario utilizes fair value hedges primarily to convert fixed rate financial

assets and liabilities to floating rate. The main financial instruments designated in fair value

hedging relationships are loans. If the derivative expires or is sold, terminated or exercised,

no longer meets the criteria for fair value hedge accounting, or the designation is revoked,

hedge accounting is discontinued prospectively. The fair value of the hedged item related to

the hedged risk is reported as other assets. The fair value of the hedging instrument is

recorded as a derivative asset or liability.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

15

3. Significant Accounting Policies (continued):

(b) Financial instruments – recognition and measurement (continued):

In a cash flow hedge, the effective portion of changes in fair value of the derivative is

recognized in other comprehensive income (“OCI”) and presented in the cash flow hedging

reserve in equity. The amount recognized in OCI is reclassified and included on the

Consolidated Statement of Income in the same year that the hedged cash flows affect

income. This will be offset by increased net interest income on assets and liabilities that are

hedged. FirstOntario utilizes cash flow hedges primarily to convert floating rate assets and

liabilities to fixed rate. Any hedge ineffectiveness is measured and is immediately recognized

in the Consolidated Statement of Income.

When either a fair value or cash flow hedge is discontinued, any cumulative adjustment to

either the hedged item or other comprehensive income (loss) is recognized in income over

the remaining term of the original hedge (fair value hedge) and as the hedged item impacts

earnings (cash flow hedge) or immediately if the forecast transaction is no longer expected to

occur.

(c) Loan securitizations:

FirstOntario periodically securitizes residential mortgages and commercial loans by legally

selling them to funding partners. Securitized assets are assessed for derecognition under IAS

39 Financial Instruments: Recognition and Measurement. When the derecognition criteria are

met, the assets are de–recognized from the Consolidated Statement of Financial Position.

Under the transition to IFRS, the derecognition criteria is applied prospectively from the date

of transition and transactions entered into prior to the transition date (September 1, 2010) are

assessed under previous Canadian GAAP.

Securitized residential mortgages that are assessed under IAS 39 do not meet derecognition

requirements as substantially all of the risks and rewards of the loans are held with

FirstOntario. As a result, these loans are reported on the Statement of Financial Position.

Securitized residential mortgages that are not reported on the Statement of Financial Position

met the derecognition requirements of previous Canadian GAAP.

Commercial loans sold met the derecognition requirements and are not reported on the

Statement of Financial Position as substantially all of the risks and rewards of the loan is

transferred to the funding partner and FirstOntario has received consideration in exchange.

For those commercial loans sold, no gain is recorded as the consideration received is

equivalent to the carrying value of the asset.

Revenue from servicing loans and mortgages is recorded as the services are provided.

(d) Cash and cash equivalents:

Cash and cash equivalents includes cash on hand, current accounts, short term deposits with

other financial institutions, cheques and other items in transit. Given their short term nature,

the carrying value of cash and cash equivalents equals fair value.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

16

3. Significant Accounting Policies (continued):

(e) Investments:

Investments are recorded at fair value unless the investment is designated as Loans and

Receivables or represents an interest in a investment property held under a joint venture

agreement. Any gains and losses on disposal of investments are recorded in the year they

occur and are included in other investment income in the Consolidated Statement of Income.

(f) Intangible assets:

Computer software that is not an integral part of other property is accounted for as intangible

assets. Computer software is stated at cost less accumulated amortization and accumulated

impairment losses and is presented as part of fixed assets in the Consolidated Statement of

Financial Position. Amortization of computer software is calculated by applying the straight–

line method at rates based on estimated useful lives between 3 and 7 years. Amortization

methods and useful lives are reviewed at each reporting date and adjusted if appropriate.

(g) Fixed assets:

Fixed assets are stated at cost less accumulated amortization and accumulated impairment

losses. When parts of an item of fixed assets have different useful lives, they are accounted

for as separate items (major components) of fixed assets. Amortization is based on the cost

of an asset less its residual value. Major components are amortized separately. Land is not

amortized. Amortization on buildings and equipment is recognized in net income using the

straight–line method at rates based on the estimated useful lives of the related assets and

components as follows:

Asset

Buildings 20 – 40 years Parking lots and site improvements 10 – 25 years Equipment 3 – 10 years Leasehold improvements Shorter of useful life and term of lease + one renewal period

Depreciation methods, useful lives and residual values are reviewed at each financial year

end and adjusted if appropriate.

(h) Investment property:

Investment property is property held to earn rentals and/or for capital appreciation.

FirstOntario applies the cost model in accounting for investment property. Investment

property primarily consists of land and buildings held under a joint venture agreement.

Amortization of buildings is based on the straight–line method at rates based on estimated

useful lives of 40 years. Land is not amortized.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

17

3. Significant Accounting Policies (continued):

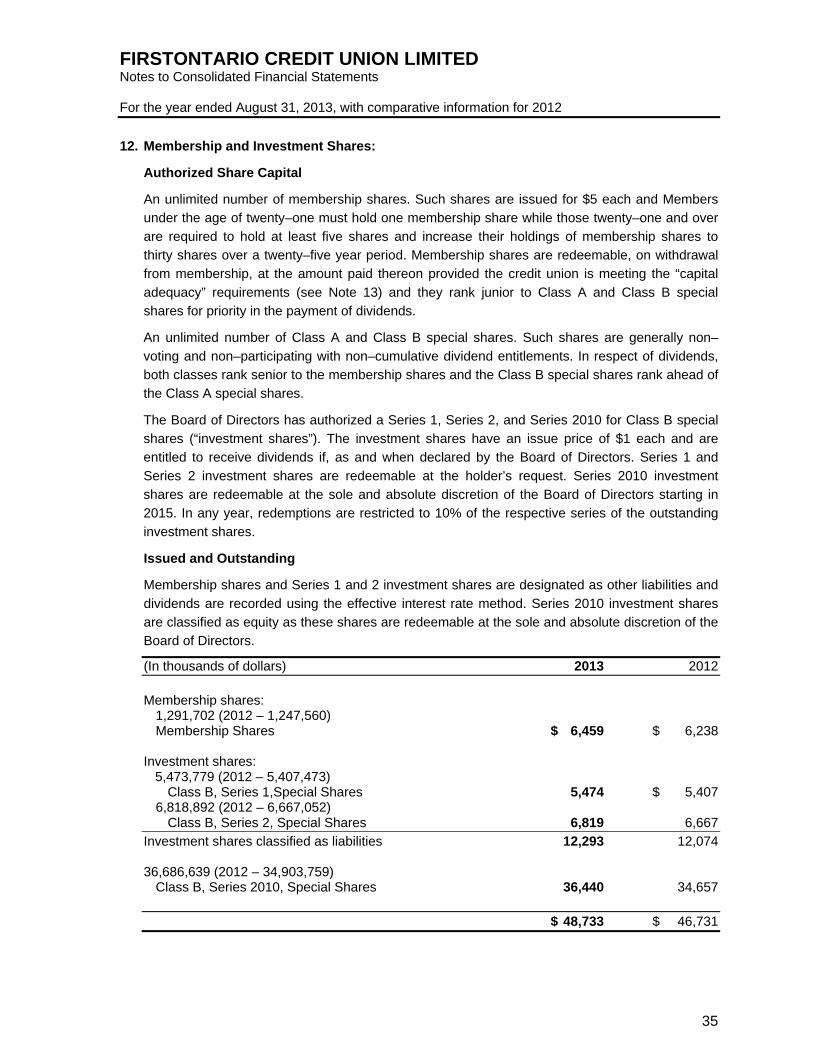

(i) Shares:

Membership and investment shares are classified either as liabilities or member’s equity.

Where shares are redeemable at the option of the Member, either on demand or on

withdrawal from membership, the shares are classified as other liabilities and carried at

amortized cost. Shares that are redeemable at the discretion of FirstOntario’s Board of

Directors are classified as equity.

(j) Dividends on shares classified as other liabilities are reported as interest expense. Dividends

on shares classified as equity are charged to retained earnings on the date at which

distributions are declared payable by the Board of Directors. All dividends on shares are

deductible for income tax purposes.Impairment of non–financial assets:

Non–financial assets other than deferred tax assets are reviewed for impairment whenever

events or changes in circumstances indicate that the carrying value may not be recoverable

and at each reporting date. An impairment loss is recognized for the amount by which the

asset’s carrying value exceeds its recoverable amount. The recoverable amount is the higher

of an asset’s fair value less costs to sell and value in use. Impairment losses are recognized

in net income.

Non–financial assets that have incurred impairment losses in prior years are reviewed for

possible reversal of the impairment loss at each reporting date. A reversal of impairment is

limited to the original impaired amount.

(k) Revenue recognition:

Loan interest and revenue is recognized on the effective yield basis.

(l) Foreign exchange:

The Consolidated Financial Statements are presented in Canadian dollars, which is

FirstOntario’s functional currency. Monetary assets and liabilities denominated in foreign

currencies, primarily US dollars, are translated into Canadian dollars at exchange rates

prevailing at the year–end. Fixed assets, intangible assets and investment property are

carried at the historical Canadian dollar cost. Income and expenses are translated at the

exchange rates in effect on the date of the transactions. Exchange gains and losses arising

on the translation of monetary assets and liabilities are included in other income. Foreign

currency differences arising on translation of available–for–sale equity investments and cash

flow hedges are recognized in other comprehensive income.

(m) Provisions:

A provision is recognised if, as a result of a past event, FirstOntario has a present legal or

constructive obligation that can be estimated reliably, and it is probable that an outflow of

economic benefits will be required to settle the obligation. Provisions are determined by

discounting the expected future cash flows at a pre–tax rate that reflects current market

assessments of the time value of money and the risks specific to the liability.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

18

3. Significant Accounting Policies (continued):

(n) Employee retirement benefits:

FirstOntario provides retirement benefits to certain employees. These benefits include

registered pension plans, medical benefits, dental care and life insurance.

A defined contribution plan is a pension plan under which FirstOntario pays contributions to a

separate entity. FirstOntario has no legal or constructive obligation to pay further

contributions after its payment of a contribution in accordance with the pension plan. Defined

contribution pension plan contributions are expensed in the year during which services are

rendered by employees.

A defined benefit plan is a pension plan that defines the amount of the pension benefit that an

employee will receive upon retirement, usually dependent on one or more factors, such as

age, years of service and compensation. Employment retirement benefits include both

pension and other post–retirement benefits.

The costs of defined benefit post–employment benefits (including medical benefits, dental

care, life insurance, and defined benefit pension plans) related to the employees' current

service is charged to income annually. The cost is computed on an actuarial basis using the

projected unit credit method estimating the usage frequency and cost of services covered

and management's best estimates of investment yields, salary escalation, and other factors.

Benefits are discounted to determine their present value based on the market yield, at the

reporting date, of high quality corporate bonds that have maturity dates approximating the

terms of the obligations. The fair value of plan assets is deducted in determining the net

obligation. FirstOntario recognizes all actuarial gains or losses by using the corridor method

to amortize actuarial gains or losses (such as changes in actuarial assumptions and

experience gains or losses) over the average remaining service life of active employees.

Under the corridor method, amortization is recorded only if the accumulated net actuarial

gains or losses exceed 10% of the greater of the accrued benefit obligation and the value of

the plan assets. The average remaining working lives of the active employees participating in

the defined benefit pension plans is 17 years. The average remaining service period of the

active employees covered by the other post–employment benefit plan is 7 years. Past service

costs are deferred and amortized on a straight line basis over the average period until the

benefits come vested. To the extent that the benefits vest immediately, the expense is

recognized immediately in net income.

When the restructuring of a benefit plan gives rise to a curtailment, the curtailment is

accounted for at the time of restructuring.

(o) Income taxes:

FirstOntario follows the asset and liability method of accounting for income taxes, whereby

FirstOntario recognizes both the current and future income tax consequences of all

transactions that have been recorded in the financial statements.

Current income taxes are the expected taxes refundable or payable on the taxable income for

the year, using tax rates enacted or substantively enacted at the balance sheet date, and any

adjustment to taxes payable in respect of previous years.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

19

3. Significant Accounting Policies (continued):

(o) Income taxes (continued):

Deferred income taxes provide for temporary differences between the carrying values of

assets and liabilities and the amounts used for taxation purposes. The amount of deferred

income tax provided is based on the expected timing of realization or settlement of the

carrying value of assets and liabilities, using tax rates enacted or substantively enacted at the

balance sheet date. A deferred income tax asset is recognized only to the extent that it is

probable that future taxable income will be available to utilize taxable benefits associated with

the temporary difference in carrying value.

Deferred tax assets and liabilities are included either in other assets or accounts payable and

accrued liabilities, as applicable, in the Consolidated Statement of Financial Position.

4. New Standards and Interpretations not yet effective:

Future changes in accounting policy

(a) Amendments to IAS 32 and IFRS 7, Offsetting Financial Assets and Liabilities

The amendments to IAS 32 clarify the allowable circumstances for an entity to present a

financial asset and liability as a net balance (‘offsetting’). The amendments also describe

when a settlement mechanism provides for net settlement or gross settlement that is

equivalent to net settlement.

The amendments to IFRS 7 contain new disclosure requirements for financial assets and

liabilities that are offset in the statement of financial position or subject to master netting

arrangements or similar arrangements.

FirstOntario intends to adopt the amendments to IFRS 7 in its financial statements for the

fiscal year beginning on September 1, 2013, and the amendments to IAS 32 in its financial

statements for the fiscal year beginning September 1, 2014 with the amendments applied

retrospectively. FirstOntario does not expect the amendments to have a material impact on

the financial statements.

(b) IFRS 10 Consolidated Financial Statements replaces the guidance in IAS 27 Consolidated

and Separate Financial Statements and SIC–12 Consolidation – Special Purpose Entities.

IAS 27 (2008) survives as IAS 27 (2011) Separate Financial Statements, only to carry

forward the existing accounting requirements for separate financial statements.

IFRS 10 provides a single model to be applied in the control analysis for all investees,

including entities that currently are special purpose entities (“SPE’s”) in the scope of SIC–12.

In addition, the consolidation procedures are carried forward substantially unmodified from

IAS 27 (2008). The changes are effective for fiscal years beginning on or after

January 1, 2013 and FirstOntario intends to adopt IFRS 10 in its financial statements for the

fiscal year beginning September 1, 2013. FirstOntario does not expect IFRS 10 to have a

material impact on the financial statements.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

20

4. New Standards and Interpretations not yet effective (continued):

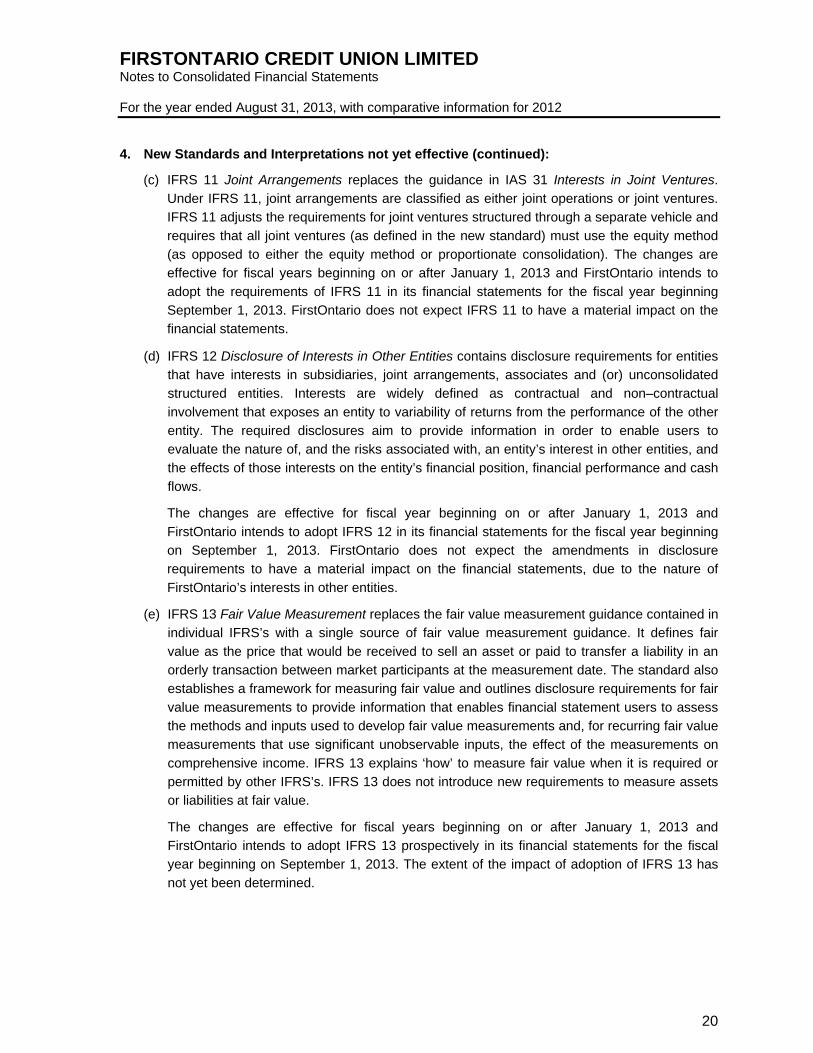

(c) IFRS 11 Joint Arrangements replaces the guidance in IAS 31 Interests in Joint Ventures.

Under IFRS 11, joint arrangements are classified as either joint operations or joint ventures.

IFRS 11 adjusts the requirements for joint ventures structured through a separate vehicle and

requires that all joint ventures (as defined in the new standard) must use the equity method

(as opposed to either the equity method or proportionate consolidation). The changes are

effective for fiscal years beginning on or after January 1, 2013 and FirstOntario intends to

adopt the requirements of IFRS 11 in its financial statements for the fiscal year beginning

September 1, 2013. FirstOntario does not expect IFRS 11 to have a material impact on the

financial statements.

(d) IFRS 12 Disclosure of Interests in Other Entities contains disclosure requirements for entities

that have interests in subsidiaries, joint arrangements, associates and (or) unconsolidated

structured entities. Interests are widely defined as contractual and non–contractual

involvement that exposes an entity to variability of returns from the performance of the other

entity. The required disclosures aim to provide information in order to enable users to

evaluate the nature of, and the risks associated with, an entity’s interest in other entities, and

the effects of those interests on the entity’s financial position, financial performance and cash

flows.

The changes are effective for fiscal year beginning on or after January 1, 2013 and

FirstOntario intends to adopt IFRS 12 in its financial statements for the fiscal year beginning

on September 1, 2013. FirstOntario does not expect the amendments in disclosure

requirements to have a material impact on the financial statements, due to the nature of

FirstOntario’s interests in other entities.

(e) IFRS 13 Fair Value Measurement replaces the fair value measurement guidance contained in

individual IFRS’s with a single source of fair value measurement guidance. It defines fair

value as the price that would be received to sell an asset or paid to transfer a liability in an

orderly transaction between market participants at the measurement date. The standard also

establishes a framework for measuring fair value and outlines disclosure requirements for fair

value measurements to provide information that enables financial statement users to assess

the methods and inputs used to develop fair value measurements and, for recurring fair value

measurements that use significant unobservable inputs, the effect of the measurements on

comprehensive income. IFRS 13 explains ‘how’ to measure fair value when it is required or

permitted by other IFRS’s. IFRS 13 does not introduce new requirements to measure assets

or liabilities at fair value.

The changes are effective for fiscal years beginning on or after January 1, 2013 and

FirstOntario intends to adopt IFRS 13 prospectively in its financial statements for the fiscal

year beginning on September 1, 2013. The extent of the impact of adoption of IFRS 13 has

not yet been determined.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

21

4. New Standards and Interpretations not yet effective (continued):

(f) Amendments to IAS 28 Investments in Associates and Joint Ventures include the following:

New requirements relating to the method of recording associates and joint ventures that

are held for sale; and,

Disclosures relating to changes in interests held in associates and joint ventures.

The changes are effective for fiscal years beginning on or after January 1, 2013 and

FirstOntario intends to adopt IAS 28 prospectively in its financial statements for the fiscal year

beginning on September 1, 2013. The extent of the impact of adoption of IAS 28 has not yet

been determined.

(g) Amendments to IAS 19 Employee Benefits require the following:

Recognition of actuarial gains and losses immediately in other comprehensive income.

The corridor method will be eliminated and actuarial gains and losses are not transferred

to net income

Full recognition of past service costs immediately in net income

Recognition of expected return on plan assets in profit or loss to be calculated based on

the rate used to discount the defined benefit obligation

Additional disclosures that explain the characteristics of the entity’s defined benefit plans

and risks associated with the plans, as well as disclosures that describe how defined

benefit plans may affect the amount, timing and uncertainty of future cash flows, and

details of any asset–liability matching strategies used to manage risks.

The amendments also impact termination benefits, which would now be recognized at the

earlier of when the entity recognizes costs for a restructuring within the scope of IAS 37

Provisions, and when the entity can no longer withdraw the offer of the termination benefits.

The changes are effective for fiscal year beginning on or after January 1, 2013 and

FirstOntario intends to adopt the amendments in its financial statements for the fiscal year

beginning on September 1, 2013. The extent of the impact of adoption of these amendments

to the accrued benefit liability is estimated to increase the defined benefit pensions liability by

$1,351,000 and decrease other defined benefit pensions liability by $132,000. The net

actuarial gains and losses will be recorded through OCI as incurred. Management is

reviewing disclosure requirements related to these amendments.

(h) Novation of Derivatives and Continuation of Hedge Accounting (Amendments to IAS 39):

The amendments add a limited exception to IAS 39, to provide relief from discontinuing an

existing hedging relationship when a substitution of a derivative contract that was not

contemplated in the original hedging documentation meets specific criteria.

FirstOntario intends to adopt the amendments in its financial statements for the annual period

beginning September 1, 2014. The extent of the impact of adoption of the amendments has

not yet been determined.

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

22

4. New Standards and Interpretations not yet effective (continued):

(i) IFRS 9 Financial Instruments (“IFRS 9”) replaces the guidance in IAS 39 Financial

Instruments: Recognition and Measurement, on the classification and measurement of

financial assets. The Standard eliminates the existing IAS 39 categories of held to maturity,

available–for–sale and loans and receivable.

Financial assets will be classified into one of two categories on initial recognition:

financial assets measured at amortized cost; or

financial assets measured at fair value.

Gains and losses on remeasurement of financial assets measured at fair value will be

recognized in net income, except that for an investment in an equity instrument which is not

held–for–trading, IFRS 9 provides, on initial recognition, an irrevocable election to present all

fair value changes from the investment in OCI. The election is available on an individual

share–by–share basis. Amounts presented in OCI will not be reclassified to net income at a

later date.

Under IFRS 9, for financial liabilities measured at fair value under the fair value option,

changes in fair value attributable to changes in credit risk will be recognized in OCI, with the

remainder of the change recognized in profit or loss. However, if this requirement creates or

enlarges an accounting mismatch in net income, the entire change in fair value will be

recognized in net income. Amounts presented in OCI will not be reclassified to net income at

a later date.

IFRS 9 also requires derivative liabilities that are linked to and must be settled by delivery of

an unquoted equity instrument to be measured at fair value, whereas such derivative

liabilities are measured at cost under IAS 39.

IFRS 9 also includes the requirements of IAS 39 for the derecognition of financial assets and

liabilities without change.The IASB has deferred the mandatory effective date of the existing

chapters of IFRS 9 to fiscal years beginning on or after January 1, 2015. The early adoption

of the standard is permitted.

FirstOntario intends to adopt IFRS 9 in its financial statements for its fiscal year beginning on

September 1, 2015. It is expected that IFRS 9, when initially applied, will have a significant

impact on FirstOntario’s financial statements. As well, the implementation and ability to elect

options provided by the new standards may be influenced by the regulators (DICO).

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

23

5. Loans Receivable from Members:

Loans receivable from Members, which have been designated as loans and receivables, are as

follows:

(In thousands of dollars) 2013 2012

Residential Mortgage Loans $ 1,176,519 $ 973,833 Allowance for impaired loans (263) (199)

1,176,256 973,634

Personal Loans 143,658 143,252 Allowance for impaired loans (2,480) (2,339)

141,178 140,913

Commercial Loans 557,905 504,412 Allowance for impaired loans (3,514) (5,287)

554,391 499,125

$ 1,871,825 $ 1,613,672

Certain Residential Mortgage Loans are securitized and have been legally transferred to other

entities for funding purposes. These loans are administered by FirstOntario and recognized on

the Consolidated Statement of Financial Position to the extent of FirstOntario’s continuing

involvement. A summary of the carrying values of Residential Mortgage Loans is as follows:

(In thousands of dollars) 2013 2012

Loans held by FirstOntario $ 812,761 $ 651,669 Loans held by Securitization Trusts 363,758 322,164

$ 1,176,519 $ 973,833

Certain loans transferred to a funding partner transacted prior to the transition to IFRS are not

recorded on the Statement of Financial Position and are not included in the above figures. Further

details are provided in Note 8.

Interest income for the year is as follows:

(In thousands of dollars) 2013 2012

Residential Mortgage Loans $ 38,259 $ 32,885 Personal Loans 9,401 9,756 Commercial Loans 27,795 26,883

$ 75,455 $ 69,524

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

24

5. Loans Receivable from Members (continued):

Total fees paid to third parties associated with lending activities capitalized in other assets were

$5,921,000 as at August 31, 2013 (2012 – $4,607,000). Charges amortized into interest expense

in respect of these fees was $1,910,000 during 2013 (2012 – $1,602,000).

The following summarizes FirstOntario’s loan portfolio by the contractual repricing or maturity

date, whichever is earlier: 2013 2012 Principal Average Principal Average (In thousands of dollars) Balance Yield Balance Yield

Floating $ 487,199 4.32% $ 433,241 4.29% Within 1 year 154,079 5.11% 190,989 5.56% Over 1 year 1,236,804 4.30% 997,267 4.66% 1,878,082 4.37% 1,621,497 4.67% Provision for loan losses (6,257) (7,825)

$ 1,871,825 $ 1,613,672

6. Allowance for Impaired Loans:

A summary of the allowance for impaired loans is as follows:

2013 2012

Residential

Mortgage Personal Commercial Collective

(In thousands of dollars) Loans Loans Loans Allowance Total Total

Balance at beginning of year $ 25 $ 845 $ 2,978 $ 3,977 $ 7,825 $ 5,603

Loans written off (20) (1,097) – – (1,117) (2,151)

Recoveries – 134 – – 134 105

Net provision for impaired loans 56 1,076 (2,060) 343 (585) 4,268

Balance at end of year $ 61 $ 958 $ 918 $ 4,320 $ 6,257 $ 7,825

A summary of impaired loans are as follows:

2013 2012

Residential

Mortgage Personal Commercial

(In thousands of dollars) Loans Loans Loans Total Total

Gross amount of loans identified as impaired $ 17,007 $ 2,075 $ 5,578 $ 24,660 $ 21,351

Related security less expected costs 16,946 1,117 4,660 22,723 17,503

Balance at end of year $ 61 $ 958 $ 918 $ 1,937 $ 3,848

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

25

6. Allowance for Impaired Loans (continued):

A summary of loans past due but not impaired are as follows:

2013 2012

< 30 30–59 60–89

(In thousands of dollars) days days days Total Total

Residential mortgage loans $ 19,350 $ 5,536 $ 1,679 $ 26,565 $ 18,139

Personal loans 4,294 1,537 299 6,130 8,021

Commercial loans 21,114 5 59 21,178 1,607

Balance at end of year $ 44,758 $ 7,078 $ 2,037 $ 53,873 $ 27,767

The carrying amount of loans that were renegotiated during the year that otherwise would have

been listed as past due greater than 90 days were nil (2012 – $467,000).

FirstOntario’s commercial loan portfolio contains Member concentration risk, whereby a large

amount of the loans are connected to certain individuals. Collectively, the largest five commercial

Members by loan dollar value are associated with approximately 21% (2012 – 21%) of the

commercial loan portfolio.

FirstOntario’s commercial loan portfolio consists of the following industry sectors:

2013 2012

Hospitality 25% 23%

Retail & Commercial Buildings 50% 55%

Other 25% 22%

Collateral

There are documented policies and procedures in place for the valuation of financial and non–

financial collateral. The fair value of non–financial collateral is updated if there has been a

significant change in the terms and conditions of the loan and (or) the loan is considered

impaired. For impaired loans, an assessment of the collateral is taken into consideration when

estimating the expected future cash flows and net realizable amount of the loan.

The amount and type of collateral and other credit enhancements required depend upon

FirstOntario’s assessment of counterparty credit quality and repayment capacity. FirstOntario

complies with industry standards for collateral valuation, frequency of recalculation of the

collateral requirements, documentation, registration and perfection procedures, and monitoring.

Non–financial assets accepted by FirstOntario as collateral include vehicles, residential real

estate, real estate under development, commercial real estate and certain business assets

(accounts receivable, inventory, and fixed assets). Financial collateral includes cash and

negotiable securities issued by governments and investment grade issuers. Guarantees are also

accepted to reduce credit risk.

The fair value of collateral held with respect to assets that are either past due greater than 30

days or impaired is $46,160,000 as at August 31, 2013 (2012 – $33,765,000).

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

26

6. Allowance for Impaired Loans (continued):

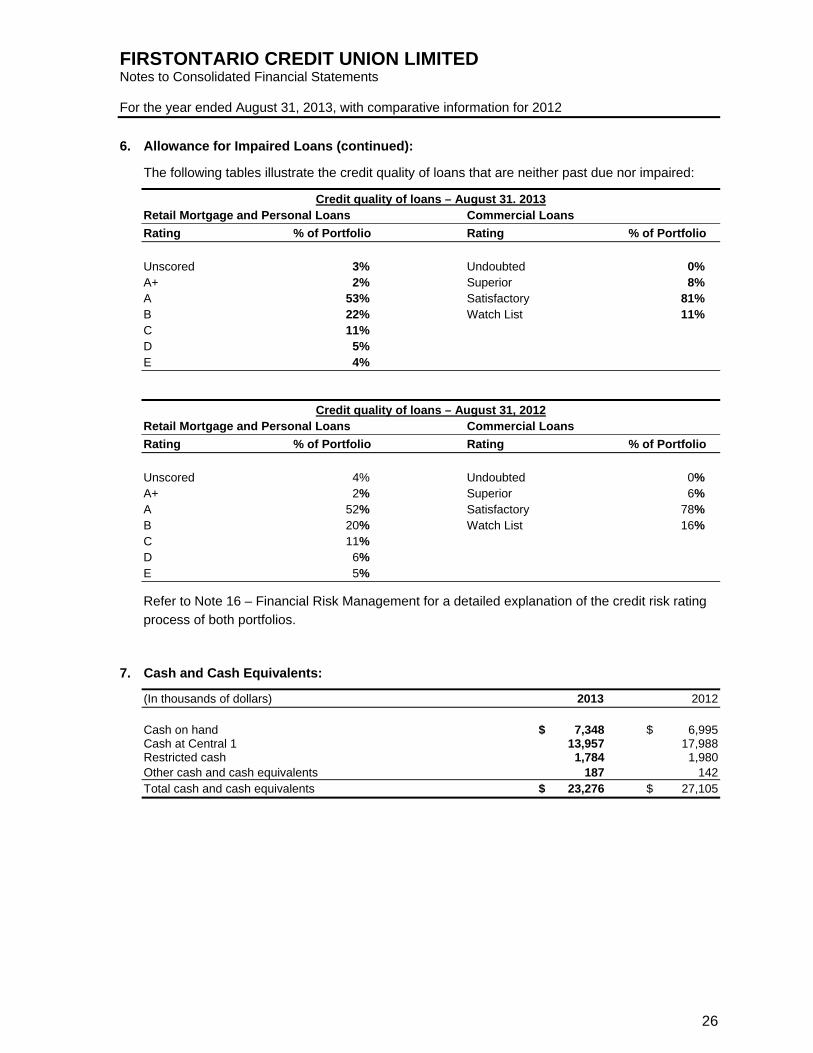

The following tables illustrate the credit quality of loans that are neither past due nor impaired:

Credit quality of loans – August 31. 2013 Retail Mortgage and Personal Loans Commercial Loans

Rating % of Portfolio Rating % of Portfolio

Unscored 3% Undoubted 0% A+ 2% Superior 8% A 53% Satisfactory 81% B 22% Watch List 11% C 11% D 5% E 4%

Credit quality of loans – August 31, 2012 Retail Mortgage and Personal Loans Commercial Loans

Rating % of Portfolio Rating % of Portfolio

Unscored 4% Undoubted 0% A+ 2% Superior 6% A 52% Satisfactory 78% B 20% Watch List 16% C 11% D 6% E 5%

Refer to Note 16 – Financial Risk Management for a detailed explanation of the credit risk rating

process of both portfolios.

7. Cash and Cash Equivalents:

(In thousands of dollars) 2013 2012

Cash on hand $ 7,348 $ 6,995 Cash at Central 1 13,957 17,988 Restricted cash 1,784 1,980 Other cash and cash equivalents 187 142 Total cash and cash equivalents $ 23,276 $ 27,105

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

27

8. Loan Securitizations:

FirstOntario enters into transactions in the normal course of business by which it transfers

recognized financial assets directly to third parties or SPE’s. FirstOntario securitizes mortgage

backed securities through programs sponsored by the Canada Mortgage and Housing

Corporation and other third party programs.

Full derecognition occurs when FirstOntario transfers its contractual right to receive cash flows

from the financial assets, or retains the right but assumes an obligation to pass on the cash flows

from the asset, and transfers substantially all the risks and rewards of ownership. The risks

include credit, interest rate, prepayment and other price risks.

The financial assets that do not qualify for derecognition are mortgages converted into mortgage

backed securities and then subsequently sold. Residential and commercial mortgages that have

been derecognized are those that meet the qualifications required to be derecognized under

IFRS.

The following table summarizes FirstOntario’s securitization activity during the years ended

August 31, 2013 and 2012:

2013 2012

Residential Commercial Residential Commercial

(in thousands of dollars) mortgages mortgages mortgages mortgages

Amount securitized/sold $ 78,411 $ 6,000 $ 154,869 $ 11,984

Net cash proceeds received 77,761 6,000 154,180 11,984 Outstanding balances of securitized loans 408,696 106,001 397,048 113,871

The following table summarizes the balances for securitized loans that are not recorded on the Statement of Financial Position:

2013 2012

Residential Commercial Residential Commercial

(in thousands of dollars) mortgages mortgages mortgages mortgages

Retained rights to future excess spread $ 459 $ – $ 1,430 $ – Outstanding balances of off–balance sheet securitized loans 44,928 106,001 74,884 113,871

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

28

8. Loan Securitizations (continued):

Retained rights are reported as investments on the Consolidated Statement of Financial Position

(Note 9). The following table summarizes the weighted average key assumptions at the date of

off–balance sheet securitization for retained rights related to mortgage pools sold prior to

September 1, 2010:

2013 2012

Residential Commercial Residential Commercial

mortgages mortgages mortgages mortgages

Average life 0.7 years na 1.6 years na

Prepayment rate 39.96% na 39.96% na

Excess spread 2.90% na 2.66% na

Discount rate 1.83% na 2.29% na

Expected credit losses 0.00% na 0.00% na

9. Investments:

Investments are as follows:

(In thousands of dollars) 2013 2012

Investments held to maturity Liquidity reserve deposits – Central 1 (c) $ 121,088 $ 106,255

Accrued interest 1,030 926 Investments available for sale, fair value

Preferred shares (a) 9 9 Common shares (a) 317 359 Income trusts and limited partnerships (a) 239 245

Total liquid investments 122,683 107,794

Investment held as fair value through profit and loss CUCO Cooperative Association (b) 5,972 6,003

Investments available for sale

Cost Shares – Central 1 (c) 11,177 9,865

Fair value Retained rights – loan securitizations 459 1,430

Real Estate Joint Ventures (d) 10,296 10,504 Other investments 284 249

$ 150,871 $ 135,845

FIRSTONTARIO CREDIT UNION LIMITED Notes to Consolidated Financial Statements For the year ended August 31, 2013, with comparative information for 2012

29

9. Investments (continued):

The following summarizes FirstOntario’s investments by the contractual repricing or maturity date,

whichever is earlier:

2013 2012 Carrying Average Carrying Average (In thousands of dollars) Amount Yield Amount Yield Within 1 year $ 21,453 2.29% $ 24,721 2.17% Over 1 year 99,635 1.91% 81,534 2.05% 121,088 1.98% 106,255 2.08% Non–rate sensitive 28,753 28,664 Accrued interest 1,030 926

$150,871 $135,845

(a) Financial instruments classified as AFS

The table below presents the income and losses of the financial assets classified as AFS.

(In thousands of dollars) 2013 2012

Interest and investment income $ 126 $ 19

Impairment loss recorded on common shares – (594)

Unrealized pre–tax income recognized in OCI 37 196

(b) CUCO Cooperative Association:

As a result of the merger between Credit Union Central of Ontario Limited (“CUCO”) and

Credit Union Central of British Columbia (“CUCBC”) to form Central 1 in 2008, member credit

unions were required to invest in a limited partnership (“ABCP LP”) in order to acquire third–

party asset–backed commercial paper (“ABCP”). Members of CUCO were required to

purchase units in the ABCP LP based on their proportionate asset size. FirstOntario was

required to purchase 6,667,059 units in the ABCP LP.

On August 31, 2011, the ABCP LP sold its assets to CUCO Cooperative Association (“CUCO

Co–op”) in consideration for CUCO Co–op Class B Investment shares. On the date of the

transfer, FirstOntario was issued 5.4% of the outstanding CUCO Co–op Class B investment

shares, equivalent to FirstOntario’s share of the fair value of the assets transferred by ABCP

LP. As a result, FirstOntario holds the same relative holdings under the current capital

structure of the CUCO Co–op as it did under the ABCP LP.

The CUCO Co–op is governed by a Board of Directors that was elected by Ontario member

credit unions and each member records its proportionate share of net income or loss in the

CUCO Co–op as determined in accordance with IFRS.