2 wheat and maize outlook€¦ · world stock-to-use ratio (%) 34.9 37.2 36.9 million tonnes world...

TRANSCRIPT

04‐May‐18

1

13th Session of the AMIS Global Food Market Information Group

Food Markets Wheat & Maize Outlook 2018/19

THIRTEENTH SESSION OF THE AMIS GLOBAL FOOD MARKET INFORMATION GROUP

FAO Headquarters, Rome3-4 May 2018

13th Session of the AMIS Global Food Market Information Group

I. Macro conditions & food markets

II. Market Outlook for wheat and maize

Presentation Outline

04‐May‐18

2

13th Session of the AMIS Global Food Market Information Group

• “The global economic upswing that began around mid-2016 has become broader and stronger”

• World economy to grow at 3.9% this year and next

• Advanced economies to grow by 2.5% this year while emerging market and developing economies grow by 4.9%

• But “the prospect of trade restrictions and counter-restrictions threatens to undermine confidence and derail global growth prematurely”

World economy in 2018 to grow even faster than in 2017, but!

Source: World Economic Outlook, IMF April 2018

13th Session of the AMIS Global Food Market Information Group

Commodity and oil pricesDeflated using US consumer price index; index, 2014 = 100

• The IMF’s sub-indices of food and agricultural raw materials rose 4.1 percent and 6.0 percent between Aug. 2017 to Feb. 2018, respectively, mostly reflecting diminishing excess supply

• Commodity prices, notably of oil and natural gas, have risen since last year, “but the medium-term outlook remains subdued” – not so sure!

• Oil prices (not shown) continue to rise, hitting near 4-year highs recently

Source: World Economic Outlook, IMF April 2018

04‐May‐18

3

13th Session of the AMIS Global Food Market Information Group

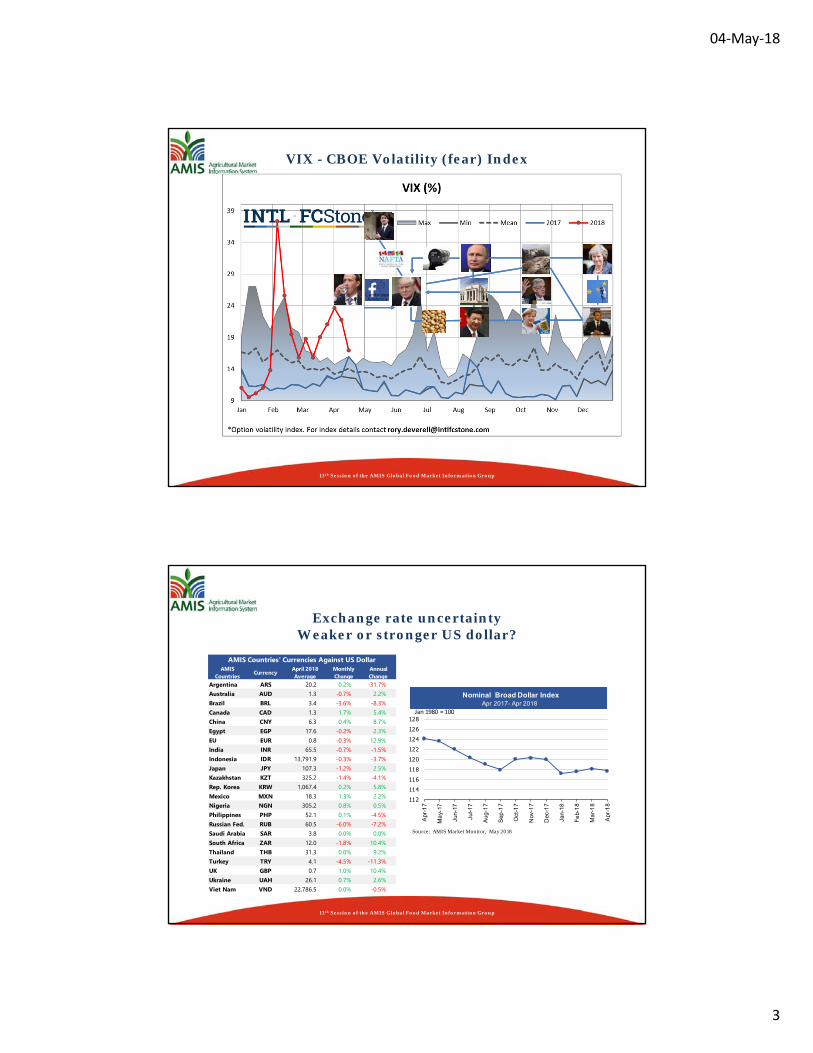

VIX - CBOE Volatility (fear) Index

13th Session of the AMIS Global Food Market Information Group

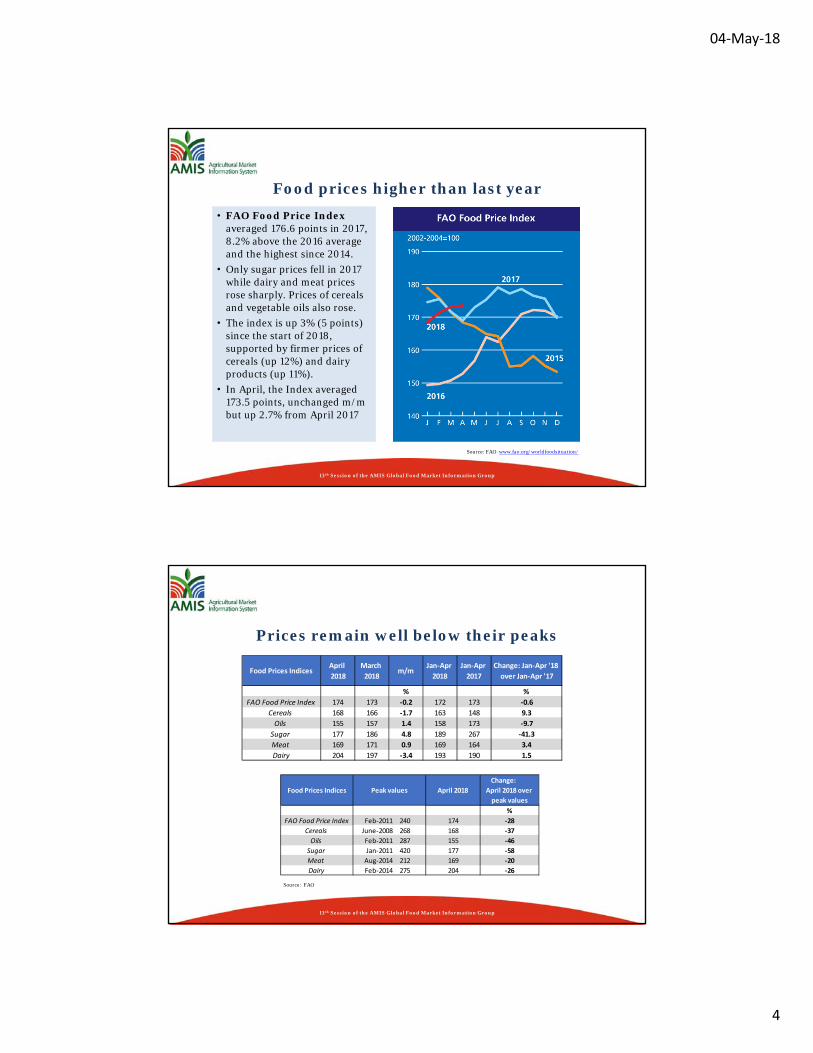

Exchange rate uncertaintyWeaker or stronger US dollar?

Source: AMIS Market Monitor, May 2018

112114116118120122124126128

Apr

-17

Ma

y-17

Jun-

17

Jul-1

7

Aug

-17

Sep

-17

Oct

-17

Nov

-17

Dec

-17

Jan-

18

Fe

b-1

8

Ma

r-1

8

Apr

-18

Nominal Broad Dollar Index Apr 2017- Apr 2018

Jan 1980 = 100

AMIS Countries Currency April 2018

AverageMonthly Change

Annual Change

Argentina ARS 20.2 0.2% -31.7%Australia AUD 1.3 -0.7% 2.2%Brazil BRL 3.4 -3.6% -8.3%Canada CAD 1.3 1.7% 5.4%China CNY 6.3 0.4% 8.7%Egypt EGP 17.6 -0.2% 2.3%EU EUR 0.8 -0.3% 12.9%India INR 65.5 -0.7% -1.5%Indonesia IDR 13,791.9 -0.3% -3.7%Japan JPY 107.3 -1.2% 2.5%Kazakhstan KZT 325.2 -1.4% -4.1%Rep. Korea KRW 1,067.4 0.2% 5.8%Mexico MXN 18.3 1.3% 2.2%Nigeria NGN 305.2 0.8% 0.5%Philippines PHP 52.1 0.1% -4.5%Russian Fed. RUB 60.5 -6.0% -7.2%Saudi Arabia SAR 3.8 0.0% 0.0%South Africa ZAR 12.0 -1.8% 10.4%Thailand THB 31.3 0.0% 9.2%Turkey TRY 4.1 -4.5% -11.3%UK GBP 0.7 1.0% 10.4%Ukraine UAH 26.1 0.7% 2.6%Viet Nam VND 22,786.5 0.0% -0.5%

AMIS Countries' Currencies Against US Dollar

04‐May‐18

4

13th Session of the AMIS Global Food Market Information Group

• FAO Food Price Index averaged 176.6 points in 2017, 8.2% above the 2016 average and the highest since 2014.

• Only sugar prices fell in 2017 while dairy and meat prices rose sharply. Prices of cereals and vegetable oils also rose.

• The index is up 3% (5 points) since the start of 2018, supported by firmer prices of cereals (up 12%) and dairy products (up 11%).

• In April, the Index averaged 173.5 points, unchanged m/m but up 2.7% from April 2017

Food prices higher than last year

Source: FAO www.fao.org/worldfoodsituation/

13th Session of the AMIS Global Food Market Information Group

Prices remain well below their peaks

Source: FAO

Food Prices IndicesApril

2018

March

2018m/m

Jan‐Apr

2018

Jan‐Apr

2017

Change: Jan‐Apr '18

over Jan‐Apr '17

% %

FAO Food Price Index 174 173 ‐0.2 172 173 ‐0.6

Cereals 168 166 ‐1.7 163 148 9.3

Oils 155 157 1.4 158 173 ‐9.7

Sugar 177 186 4.8 189 267 ‐41.3

Meat 169 171 0.9 169 164 3.4

Dairy 204 197 ‐3.4 193 190 1.5

Food Prices Indices April 2018

Change:

April 2018 over

peak values

%

FAO Food Price Index Feb‐2011 240 174 ‐28

Cereals June‐2008 268 168 ‐37

Oils Feb‐2011 287 155 ‐46

Sugar Jan‐2011 420 177 ‐58

Meat Aug‐2014 212 169 ‐20

Dairy Feb‐2014 275 204 ‐26

Peak values

04‐May‐18

5

13th Session of the AMIS Global Food Market Information Group

Market outlook 2018/19

13th Session of the AMIS Global Food Market Information Group

• Generally good conditions in the northern hemisphere

• In the US, conditions continue to deteriorate in the southern Great Plains due to prolonged drought

• Exceptional conditions in the eastern parts of EU and southern Russia, owing to favourable temperatures and soil moisture

Crop Monitor - Wheat (as of late April 2018)

04‐May‐18

6

13th Session of the AMIS Global Food Market Information Group

Wheat supply and demand outlook: still large supplies

100

145

190

235

280

400

500

600

700

800

18/1916/1714/1512/1310/1108/09

million tonnes million tonnes

Stocks (right axis)Production (left axis)

Utilization (left axis)

Production declines for the second consecutive season but still above-average

Russia down 8.9mt, at 77mt Australia up 2.5mt, at 23.7mt

EU down 2mt, at 150mt US up 1.1mt, at 48.5mt

India down 2.5mt, at 96mt

Argentina down 1.4mt, 17.1mt

Utilization growth to increase more slowly, on weaker feed use

2016/172017/18 estim.

2018/19 f'cast

Change: 2018/19 over 2017/18

%

World Balance Production 759.6 757.9 746.6 -1.5Supply 995.9 1 015.5 1 023.3 0.8Trade 176.5 173.6 174.1 0.3Total utilization 734.5 737.7 743.3 0.8Food 497.5 503.2 508.2 1.0Ending stocks 257.6 276.7 279.0 0.8World stock-to-use ratio (%) 34.9 37.2 36.9

million tonnes

World wheat market at a glance

13th Session of the AMIS Global Food Market Information Group

Record wheat stocks, but!

• Wheat stocks in China climbing to 115mt in 2018/19– up almost 12% y/y and representing over 40% of the global total.

• Excluding China, world wheat stocks falling for the seventh consecutive season. Inventories to decline in the EU, Russia and US.

• Stocks-to-disappearance (major exporters) to fall from 20.9% in 2017/18 to 19.2% in 2018/19.

0

80

160

240

320

2018/192017/182016/172015/162014/150

10

20

30

40million tonnes percent

Rest ofthe world

China

World stocks-to-use ratioStocks-to-disappearance ratio of major exporters

estim. f’cast

Majorexporters

04‐May‐18

7

13th Session of the AMIS Global Food Market Information Group

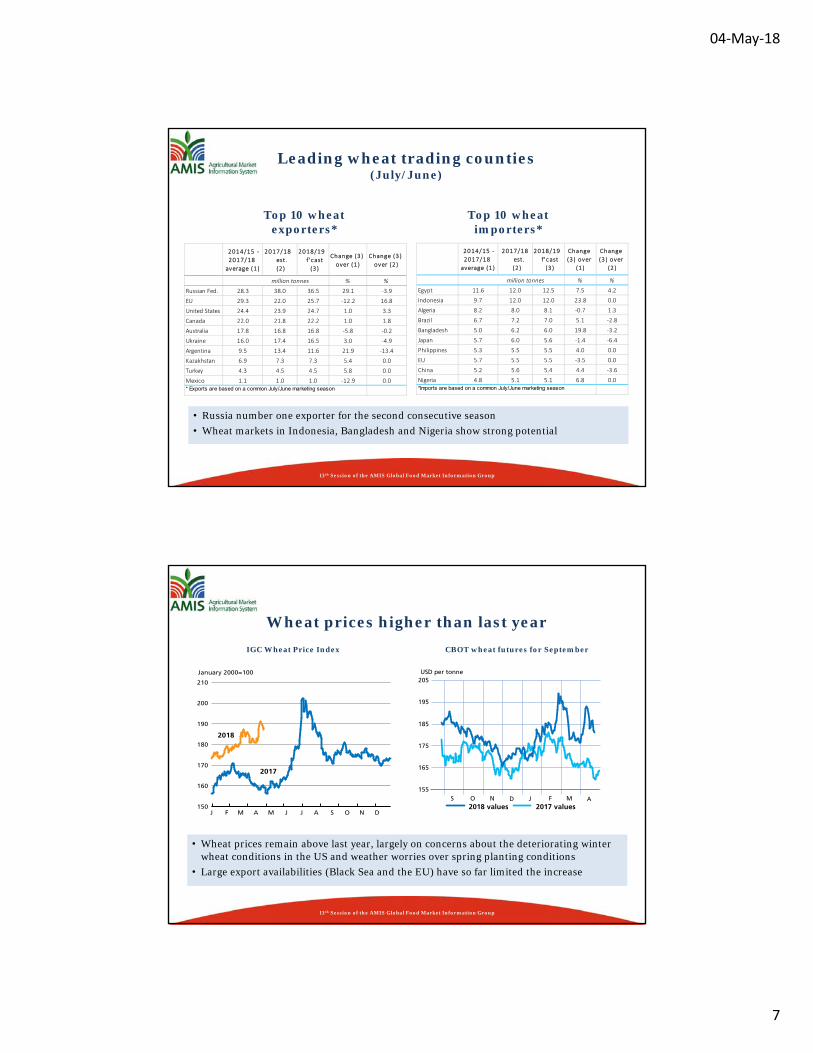

Top 10 wheat importers*

Top 10 wheat exporters*

Leading wheat trading counties(July/June)

2014/15 ‐

2017/18

average (1 )

2017/18

est.

(2 )

2018/19

f 'cast

(3 )

Change (3 )

over (1 )

Change (3 )

over (2 )

% %

Russian Fed. 28.3 38.0 36.5 29.1 ‐3.9

EU 29.3 22.0 25.7 ‐12.2 16.8

United States 24.4 23.9 24.7 1.0 3.3

Canada 22.0 21.8 22.2 1.0 1.8

Australia 17.8 16.8 16.8 ‐5.8 ‐0.2

Ukraine 16.0 17.4 16.5 3.0 ‐4.9

Argentina 9.5 13.4 11.6 21.9 ‐13.4

Kazakhstan 6.9 7.3 7.3 5.4 0.0

Turkey 4.3 4.5 4.5 5.8 0.0

Mexico 1.1 1.0 1.0 ‐12.9 0.0

million tonnes

* Exports are based on a common July/June marketing season

2014/15 ‐

2017/18

average (1 )

2017/18

est.

(2 )

2018/19

f 'cast

(3 )

Change

(3 ) over

(1 )

Change

(3 ) over

(2 )

% %

Egypt 11.6 12.0 12.5 7.5 4.2

Indonesia 9.7 12.0 12.0 23.8 0.0

Algeria 8.2 8.0 8.1 ‐0.7 1.3

Brazil 6.7 7.2 7.0 5.1 ‐2.8

Bangladesh 5.0 6.2 6.0 19.8 ‐3.2

Japan 5.7 6.0 5.6 ‐1.4 ‐6.4

Philippines 5.3 5.5 5.5 4.0 0.0

EU 5.7 5.5 5.5 ‐3.5 0.0

China 5.2 5.6 5.4 4.4 ‐3.6

Nigeria 4.8 5.1 5.1 6.8 0.0

million tonnes

*Imports are based on a common July/June marketing season

• Russia number one exporter for the second consecutive season

• Wheat markets in Indonesia, Bangladesh and Nigeria show strong potential

13th Session of the AMIS Global Food Market Information Group

Wheat prices higher than last year

IGC Wheat Price Index CBOT wheat futures for September

150

160

170

180

190

200

210

DNOSAJJMAMFJ

2017

2018

January 2000=100

155

165

175

185

195

205USD per tonne

2017 values2018 valuesS O N D J F M A

• Wheat prices remain above last year, largely on concerns about the deteriorating winter wheat conditions in the US and weather worries over spring planting conditions

• Large export availabilities (Black Sea and the EU) have so far limited the increase

04‐May‐18

8

13th Session of the AMIS Global Food Market Information Group

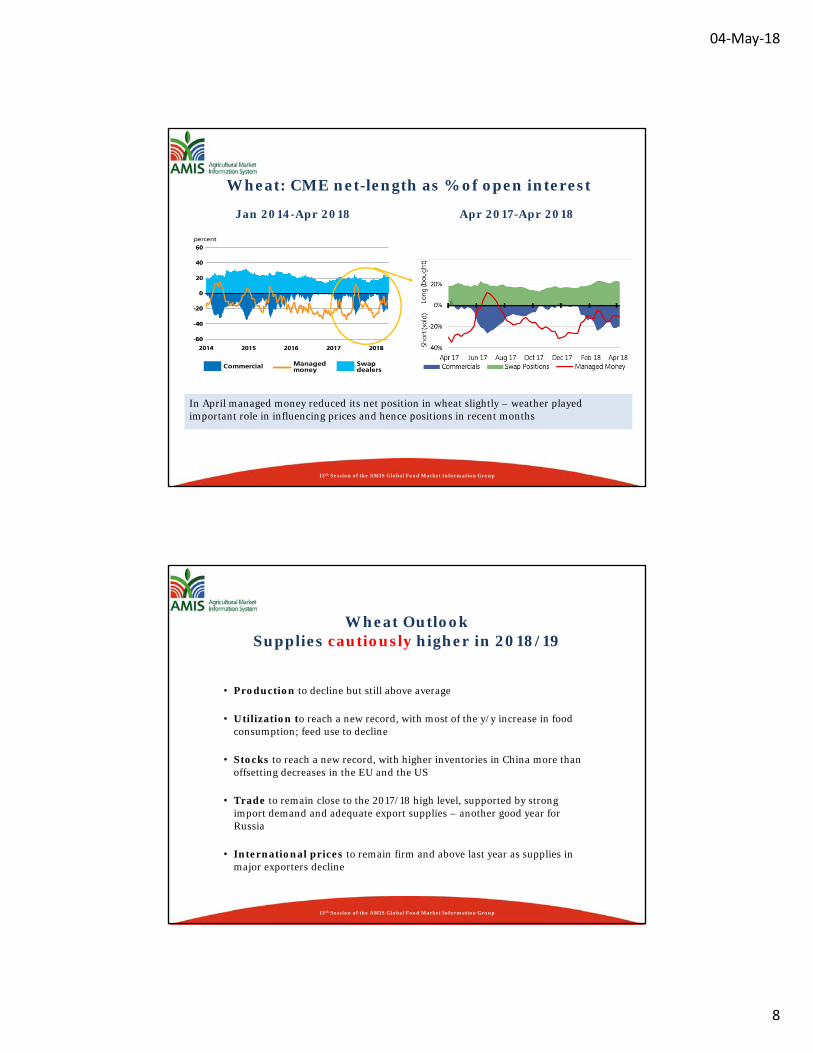

Wheat: CME net-length as % of open interest

In April managed money reduced its net position in wheat slightly – weather played important role in influencing prices and hence positions in recent months

-60

-40

-20

0

20

40

60

20182017201620152014

-60

-40

-20

0

20

40

60

20182017201620152014

percent

Commercial Managedmoney

Swapdealers

Jan 2014-Apr 2018 Apr 2017-Apr 2018

13th Session of the AMIS Global Food Market Information Group

• Production to decline but still above average

• Utilization to reach a new record, with most of the y/y increase in food consumption; feed use to decline

• Stocks to reach a new record, with higher inventories in China more than offsetting decreases in the EU and the US

• Trade to remain close to the 2017/18 high level, supported by strong import demand and adequate export supplies – another good year for Russia

• International prices to remain firm and above last year as supplies in major exporters decline

Wheat Outlook Supplies cautiously higher in 2018/19

04‐May‐18

9

13th Session of the AMIS Global Food Market Information Group

• Harvests begins in southern hemisphere – good conditions in Brazil but not in Argentina

• Sowing is ongoing in northern hemisphere under generally favourable conditions

Crop Monitor - Maize (as of late April 2018)

13th Session of the AMIS Global Food Market Information Group

100

140

180

220

260

18/1916/1714/1512/1310/1108/09700

800

900

1000

1100

18/1916/1714/1512/1310/1108/09

million tonnes million tonnes

Stocks (right axis)Production (left axis)

Utilization (left axis)

Maize supply and demand outlook: markets a bit tighter

Production is projected down from 2017 record

US down 15.6mt, at 355mt Ukraine up 2.9mt, at 27mt

Brazil down 10.7mt, at 88.6mt China up 2.1mt, at 218mt

EU down 4mt, at 61mt

Argentina down 7.5mt, at 42mt

South Africa down 3.4mt, at 13.4mt

Total use up thanks to a projected 2.8% growth in feed use compensating for slower intake for industrial use

2016/172017/18 estim.

2018/19 f'cast

Change: 2018/19 over 2017/18

%

World Balance Production 1 046.6 1 087.8 1 047.3 -3.7Supply 1 283.7 1 330.6 1 301.5 -2.2Trade 139.8 145.5 143.6 -1.3Total utilization 1 039.5 1 067.2 1 072.4 0.5

Food 128.6 130.7 131.5 0.6Ending stocks 242.8 254.2 226.9 -10.7

World stock-to-use ratio (%) 22.7 23.7 20.2

million tonnes

World maize market at a glance

04‐May‐18

10

13th Session of the AMIS Global Food Market Information Group

0

100

200

300

2018/192017/182016/172015/162014/158

14

20

26

million tonnes percent

Rest ofthe world

China

World stocks-to-use ratio

Stocks-to-disappearance ratio of major exporters

estim. f’castMajorexporters

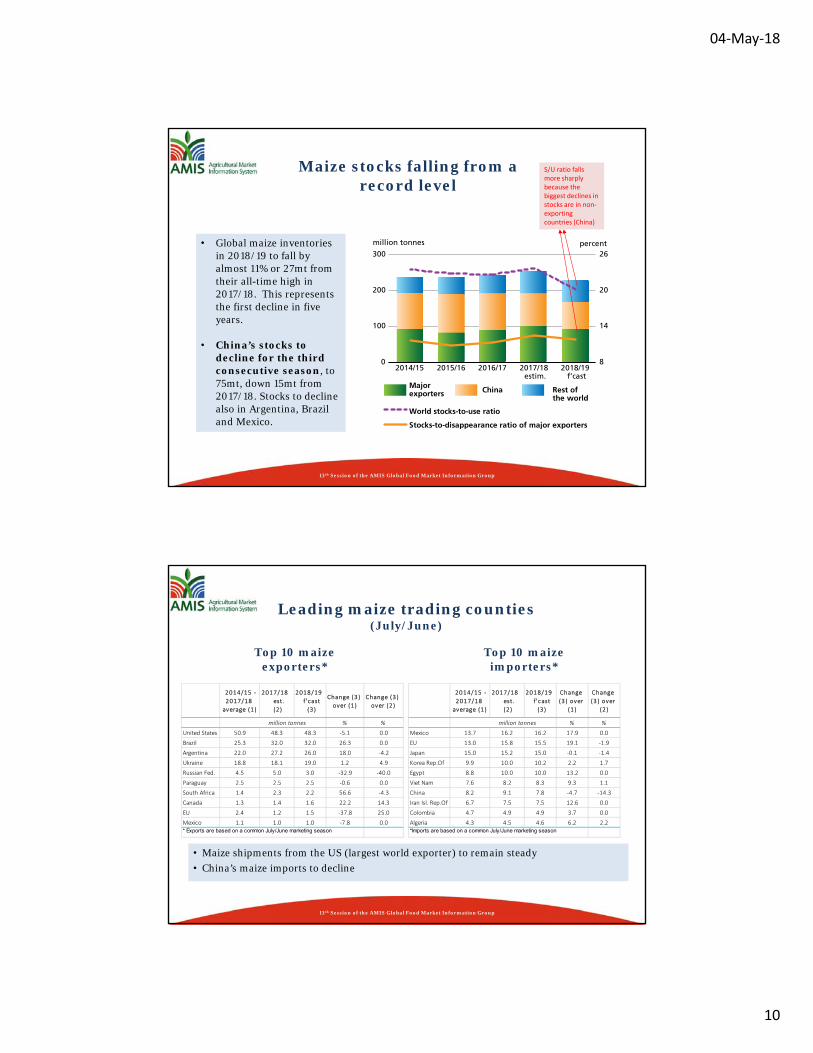

Maize stocks falling from a record level

• Global maize inventories in 2018/19 to fall by almost 11% or 27mt from their all-time high in 2017/18. This represents the first decline in five years.

• China’s stocks to decline for the third consecutive season, to 75mt, down 15mt from 2017/18. Stocks to decline also in Argentina, Brazil and Mexico.

S/U ratio falls more sharply because the biggest declines in stocks are in non‐exporting countries (China)

13th Session of the AMIS Global Food Market Information Group

2014/15 ‐

2017/18

average (1 )

2017/18

est.

(2 )

2018/19

f 'cast

(3 )

Change (3 )

over (1 )

Change (3 )

over (2 )

% %

United States 50.9 48.3 48.3 ‐5.1 0.0

Brazil 25.3 32.0 32.0 26.3 0.0

Argentina 22.0 27.2 26.0 18.0 ‐4.2

Ukraine 18.8 18.1 19.0 1.2 4.9

Russian Fed. 4.5 5.0 3.0 ‐32.9 ‐40.0

Paraguay 2.5 2.5 2.5 ‐0.6 0.0

South Africa 1.4 2.3 2.2 56.6 ‐4.3

Canada 1.3 1.4 1.6 22.2 14.3

EU 2.4 1.2 1.5 ‐37.8 25.0

Mexico 1.1 1.0 1.0 ‐7.8 0.0* Exports are based on a common July/June marketing season

million tonnes

Top 10 maize importers*

Top 10 maize exporters*

Leading maize trading counties (July/June)

• Maize shipments from the US (largest world exporter) to remain steady

• China’s maize imports to decline

2014/15 ‐

2017/18

average (1 )

2017/18

est.

(2 )

2018/19

f 'cast

(3 )

Change

(3 ) over

(1 )

Change

(3 ) over

(2 )

% %

Mexico 13.7 16.2 16.2 17.9 0.0

EU 13.0 15.8 15.5 19.1 ‐1.9

Japan 15.0 15.2 15.0 ‐0.1 ‐1.4

Korea Rep.Of 9.9 10.0 10.2 2.2 1.7

Egypt 8.8 10.0 10.0 13.2 0.0

Viet Nam 7.6 8.2 8.3 9.3 1.1

China 8.2 9.1 7.8 ‐4.7 ‐14.3

Iran Isl. Rep.Of 6.7 7.5 7.5 12.6 0.0

Colombia 4.7 4.9 4.9 3.7 0.0

Algeria 4.3 4.5 4.6 6.2 2.2

million tonnes

*Imports are based on a common July/June marketing season

04‐May‐18

11

13th Session of the AMIS Global Food Market Information Group

Maize prices higher than last year

Maize export price (US No.2 yellow, Gulf) CBOT maize futures for September

Source: FAO, Food Outlook November 2017

130

140

150

160

170

180

190

DNOSAJJMAMFJ

2017

2018

USD per tonne

140

144

148

152

156

160USD per tonne

2017 values2018 valuesS O N D J F M A

• The US maize prices have risen sharply on brisk import demand

• Expectations of lower plantings in the US and reduced supplies in Argentina underpin the futures

13th Session of the AMIS Global Food Market Information Group

Maize: CME net-length as % of open interest

Tightening supply prospects have pushed up managed money from short to long positions.

Jan 2014-Apr 2018 Apr 2017-Apr 2018

-60

-40

-20

0

20

40

percent

Commercial Managedmoney

Swapdealers

04‐May‐18

12

13th Session of the AMIS Global Food Market Information Group

• Production to decline from last year’s record

• Utilization to expand fastest for feed

• Stocks to fall significantly with most of the reduction in China and in South America

• Trade to contract slightly, mostly on prospects for smaller purchases by China and the EU

• International prices to stay above last year, on reduced overall supplies in several major exporting countries

Maize OutlookSupplies getting tighter in 2018/19

13th Session of the AMIS Global Food Market Information Group