2 november 2010 monthly market outlook · gold continues to shine but… gold hit a record high of...

TRANSCRIPT

…/ continued

� We maintain equities Overweight on 12m basis; favoring Asia and

Emerging Markets over Developed Markets.

� Equity-Bond yields widening, making stocks more compelling over

corporate bonds.

� Weak USD coupled with our base case scenario of 1% US GDP

growth and 8.5% for China in 2011 provides support for commodity

prices.

� While gold continues to shine over medium term, some

consolidation would not be surprising. We expect a modest

increase in crude oil prices in 2011.

Maintain Overweight positions in equities.

Since the start of the correction in equities in Q2-10, SCB analysts believe

that the correction is a mid-cycle pause, rather than the end of the rally.

Stocks markets have recently broken higher, boosted by evidence that the

Chinese economic growth is bottoming, reducing fears of a “double-dip”

recession in the US and resilience of the rest of the world (RoW).

Recent data from China have confirmed that the economic downturn is

stabilizing and the economy could accelerate in coming months (see

Exhibit 1). The correction in property prices in China has not been as deep as

some had initially feared. In fact, transaction volumes, particularly in Tier 2

cities have started to pick up again. Furthermore, tightening by the People’s

Bank of China and the Monetary Authority of Singapore this month is a

reflection of the central banks’ confidence in the domestic economy and their

outlook on the global economy.

Pessimism with regards to the US economy has reduced after recent better-

than-expected economy data. The RoW, led by Asia, continues to be resilient

on strong domestic consumption. We continue to remain Overweight on

12-month basis for equities.

Favor Asia and Emerging Markets over Developed Markets.

We continue to favor Asia ex-Japan (AxJ) and Emerging Markets (EM) over

DM due to strong structural and cyclical factors. EM benefits from broad USD

weakness. Asian governments have relatively lower fiscal deficits than some

of the DMs like the US, UK and Japan. Also, the losses suffered by the Asian

banking sector in the aftermath of the US subprime-mortgage crisis were a lot

smaller than the US and EU. Cyclically, the Asian consumer continues to be

Summary

Monthly Market Outlook

2 November 2010

Exhibit 1: China Growth May Have Bottomed

Source: SCB Global Research

Content Market Outlook Pg 1- 3 Country Views Pg 4- 6 SCB Forecasts Pg 7-10 Disclaimer Pg 11-13

2 November 2010

…/ continued

the driving force for the region. Despite slight moderation recently, retail sales

growth continues to be robust, especially when compared with growth rates

of the current decade. The spectacular growth in Asian exports seen earlier

this year has also moderated, but it is still around the pre-crisis growth rates.

Part of the reason for the resilience in Asian exports, despite the slowdown in

the US, is because intraregional trade has gained momentum in recent years.

Excluding China and Philippines, exports to US and EU account for less than

20% of total Asian exports. We continue to remain Overweight on 3-

month and 12-month basis on AxJ.

Equities favored over corporate bonds.

The gap between the US equities earnings yield and the investment grade

bond yield continues to widen, making the argument for stocks even more

compelling (see Exhibit 2). This is associated with record low interest rates in

the developed world. As a result, share buybacks in the US have surged this

year. US companies have announced $258 billion buybacks so far this year,

compared with $125 billion in 2009.

Outlook on the US dollar continues to be weak, supportive for

commodities

The US dollar continues to be weighed by the burden of twin deficits -- a

budget deficit and a current account deficit -- and prospects of additional

quantitative easing (the so-called QE2) by the US Federal Reserve, and

ongoing central banks’ diversification away from US assets. QE by US

Federal Reserve will result in USD weakness which in turn is bullish for

commodities that are priced in USD. Our base case scenario in 2011 that

forecast US GDP growth of 1% and China’s growth of 8.5% will further

translate into rising demand for commodities.

Furthermore, the US economy continues to underperform RoW (see Exhibit

3), while Asian central banks are in tightening mode, leading to wider yield

differentials Vs the US dollar, further increasing Asian currencies’ attraction

amongst investors. We remain particularly bullish on AxJ currencies over

the medium-term.

Over the near term, a USD technical rebound scenario is possible. This may

partially reverse the liquidity flood that buoyed Asian markets since

September. Hence outlook is more encouraging for US equities in the near

term as liquidity flows back to the US markets.

Gold continues to shine but…

Gold hit a record high of $1,387 an ounce earlier this month on a combination

of factors, including broad US dollar weakness, elevated sovereign risk,

ample liquidity, low real interest rates and inflation fears (see Exhibit 4). We

continue to remain bullish on gold from a medium-term perspective, but

wouldn’t chase the rally in the yellow metal. We would prefer to buy on

EXHIBIT 2: Equity-Bond Yield Gap Compelling, Making Equities More Attractive

Source: Thomson Datastream

EXHIBIT 3: Outperformance of G10 Economies vs. US Economy

Source: Bloomberg

…/ continued

dips. The rally in gold since August has been too sharp and some

consolidation wouldn’t be surprising. Overall, there is scope for gold to rise

further next year, possibly towards $1,475/oz by Q3-11.

Crude oil has potential to rise.

Crude oil has underperformed the commodities space in the most recent

rally. The demand picture continues to be mixed. Despite the moderation in

the Chinese economy, crude oil imports are still higher than in recent years

(see Exhibit 5). In contrast, US oil demand is well below historical averages.

Crude oil inventories in the US are still running above historical averages,

which have capped oil prices. But broad US dollar weakness and gradually

improving risk appetite should support oil. We expect a modest increase in

market tightness as Q4 progresses, due to seasonal demand strength. We

expect crude oil to rise towards $93/barrel by the end of Q1-11.

Table 1: Tactical Asset Allocation for November

Nov 10: 3M Oct 10: 3M Nov 10: 12M Oct 10: 12M

Cash Neutral Neutral Underweight Underweight Equities Neutral Neutral Overweight Overweight North America Neutral Underweight Neutral Neutral Europe Neutral Neutral Neutral Neutral

Japan Underweight Underweight Underweight Underweight Emerging Markets Neutral Overweight Overweight Overweight Asia Ex-Japan Overweight Overweight Overweight Overweight Bonds Neutral Neutral Neutral Neutral Global Neutral Neutral Underweight Underweight Emerging Neutral Neutral Neutral Neutral Asia Neutral Neutral Overweight Overweight Alternatives Neutral Neutral Neutral Neutral Hedge Funds Neutral Neutral Neutral Neutral Commodities Neutral Neutral Overweight Overweight Property Neutral Neutral Underweight Underweight

EXHIBIT 4: Liquidity Supporting Gold

Source: Bloomberg

EXHIBIT 5: China Oil Imports At Historic Highs

Source: Bloomberg

…/ continued

HONG KONG 3M: Remain Overweight 12M: Remain Overweight

� Economy: The authority’s temporary removal of real estates from the investment class for eligible mainland investors may impact

short term appetite. But recent economic data on resilient domestic consumption and decent capital market inflows indicates

recovery is on a firmer footing.

� Equity: HSI 2011 consensus forward P/E is trading close to historical average of 12.9x. Equity valuation remains below the one

standard deviation deviation band (implying 17.6x), the level at which the HSI has traded in previous market upcycles. SCB analysts

remain over-weight Hong Kong on 3m and 12m view and continue to recommend well-capitalized conglomerates, banks and utilities

but are cautious on property developers following the recent cooling off measures.

� Currency: Speculation surfaced on a possible change of the Hong Kong dollar (HKD) peg. SCB analysts expect the HKD peg

against the USD to be maintained for the foreseeable future. Mainland China’s capital account is still largely closed and it remains

inappropriate for fully convertible currency like HKD to be pegged to the CNY at this point.

TAIWAN 3M: Remain Overweight 12M: Remain Overweight

� Economy: Taiwan’s Leading Indicator Index slipped for the fourth consecutive month. It is marked by weakness in export orders and

the semiconductor book-to-bill ratio. But with unemployment slipping to two years lows and rising tourist arrivals, the domestic

consumption growth would be well supported to cushion external uncertainty. Spillover effects from excessive global liquidity

coupled with a gradual rise in interest rate may continue to keep local asset price buoyant. This would fuel the positive wealth effects

and support domestic recovery.

� Equity: On a forward PE basis of 11x, MSCI Taiwan has a very attractive PE valuation, which stands near historic low. Taiwan’s

average dividend yield of 4% pa is also among the highest in AXJ. The impending elections for five metropolitan cities in November

would remove potential overhang of challenge to the ruling KMT. This may pave way for further ‘cross straits’ improvement with

China; a potential catalyst for upward equity re-rating. GIC remains over-weight Taiwan on 3m and 12m views.

� Currency: Central bank is expected the hike rates by 12.5bps per quarter over the next five quarters. SCB analysts expect the

Taiwan dollar (TWD) to catch up to regional peers after lagging during the first nine months.

SINGAPORE 3M: Remain Neutral 12M: Remain Overweight

� Economy: While the rest of Asia is managing the risk of excessive capital inflows by introducing regulations, Singapore is expected

to focus efforts using a stronger SGD and administrative measures. Aside from managing inflows and curbing asset bubble risks,

non regulatory measures also avoid doing harm to their offshore financial center status.

� Equity: The MAS tightened monetary policy on 14 October on concerns of rising inflation and probably also reflects Central Bank’s

assessment that the exchange rate remains effective in tackling wage inflation pressures. The band widening (from +/-2 to +/-3%)

allowed for an additional 100bps upside to SGD NEER. SCB analysts expect full year 2011 inflation to moderate to 2.5% (from 2.9%

in this year).

� Currency: The surprise MAS tightening in mid October caused the SGD to strengthen against the USD, EUR, JPY, AUD and GBP.

SCB analysts expect a gradual downwards movement of USD-SGD towards 1.32 by end first half next year. Albeit near-term

Country View

…/ continued

pressure on the SGD should be upward, the strength of the SGD leaves it vulnerable to downside growth surprises. We expect GDP

to moderate to 4% in 2011; from 12.3% forecast for 2010.

INDIA 3M: Remain Neutral 12M: Remain Overweight

� Economics: Recent August Industrial Output turned in weaker than expected as manufacturing sector growth slowed to +5.9%

(from 16.7% in July). Notwithstanding that 2010 inflation forecast remained above trend rate of 5.5%, any further moderation in

manufacturing growth suggests that the RBI may have room to halt further rate hikes. SCB analysts kept FY10 and FY11 GDP

estimates at 8.1% and 8.5%, respectively. September trade deficit provided an encouraging surprise, narrowing USD 3.9bn to USD

9.12bn versus August driven by higher exports and slower imports.

� Equity: India is likely to face heavy new IPOs in the months ahead. While the public listing of state owned coal company may bring

fresh hope of privatizations and excitement to capital markets, big new issuance is a risk to stock prices if capital flows into Asia

slow. With industrial output providing uneven monthly signals recently and potential of stock issuance overhang, we are Neutral on

Indian Equities in the short term. But with impressive equities earnings growth outlook of 23% (almost double MSCI EM Asia

average) and mid teens PE multiple, India remains overweight over 12 months.

� Currency: SCB analysts maintain INR appreciation view, given that capital inflows are more than sufficient to finance the current

account deficit and growth and interest rate differentials. A significant improvement in the trade deficit, as witnessed in September, is

not priced into SCB forecasts. If the deficit improvement trend persists, it may provide a positive surprise to current year-end forecast

of 45.50. In the immediate future, USD-INR is likely to trade on global cues.

KOREA 3M: Remain Neutral 12M: Remain Overweight

� Economics: Economic growth has moderated mainly led by deteriorating export growth. While manufacturing remained key engine

of growth, the pace of growth has decelerated rather than a scenario of shrinking exports. Domestic consumption and investments

would likely continue to take the slack to provide an offset to growth. SCB analysts believe GDP slowdown is one of the key reasons

for BoK to pause its rate hiking cycle until 1Q 2011.

� Equity: MSCI Korea equity valuations are the most attractive among EM Asian markets. Forward Price Earnings multiple is still

under the 12 year average and below 10x on absolute basis. Price-to-Book multiple of 1.4x is also attractive relative to EM Asia peer

(2x) and historical average (1.3x). GIC remains neutral Korea on a 3-month view, and overweight on a 12-month view, given the

attractive valuations.

� Currency: Korea has permitted its interest rates to stay low (in real terms) by historical standards, and its exchange rate is weak

relative to regional peers. This drew criticism from Japanese officials ahead of the recent G20 summit. SCB analysts expect the

Korean Won (KRW) to gradually catch up to regional peers after lagging during the first nine months. With possible rate hike in early

2011, SCB analysts revised USD/KRW forecast for 1Q 2011 to 1,050 (from 1,100). Abundant liquidity in Asia, relatively favorable

yields of Korean sovereign compared to sovereign risk and China’s diversification of foreign reserves may further fuel KRW to

strengthen against USD over the medium term.

CHINA 3M: Remain Overweight 12M: Remain Overweight

� Economy: The 3Q data has confirmed the trend of slower growth alongside rising inflationary pressure. 3Q GDP growth decelerated

to 9.6% yoy, from 10.3% in 2Q. Inflation picked up to 3.5% in 3Q; from 2.9% in 2Q. Food price inflation remains a risk next year

alongside the effects of excess liquidity and wage inflation next year. CPI inflation in 2011 could exceed 4%. In the near term, the

government is expected to gradually hike policy rates without greatly hurting growth momentum.

…/ continued

� Equity: China's 12th Five-Year Plan (FYP) will focus on shifting from the export-led sectors to increasing domestic consumer

demand by raising Chinese labors' incomes to allow all Chinese residents (particularly rural) to prosper in the new era. Income

increase obviously will lead to labor cost increase, which is possible to impact export-led sectors as well as encourage high inflation.

Hence an important task for China is to balance the inflation threats with increasing domestic demand while maintaining export-led

sectors. MSCI China’s Forward PE multiple of 12x is trading at parity with EM Asia peer average but with more superior forward

earnings growth rates (14.9% vs. 12.5%). Follow up policies from FYP may provide catalyst for market re-rating as current earnings

forecast does not reflect growth potential from the 12th FYP. With further upward consensus EPS revision expected, GIC remains

over-weight China on 3-month and 12-month basis.

� Currency: Our view is for continued USD-CNY appreciation, as continued concerns about quantitative easing should be bearish for

the USD. SCB analysts believe the PBoC will allow very gradual CNY appreciation, with USDCNY to reach 6.64 by the end of 2010

and 6.57 by end 1Q 2011. The widening interest rate gap between China and the US could attract further inflows and add fresh

pressure on RMB appreciation.

MALAYSIA 3M: Remain Neutral 12M: Remain Neutral

� Economy: Fiscal consolidation that started in Budget 2010 appears to have halted with Budget 2011 announcements. The Budget

2011 was a flashback to the pump-priming days of the mid 90s era via a flurry of megaprojects. The 2011 expansionary stance

reinforces Malaysia’s true commitment towards fiscal consolidation. Fiscal deficit is -5.6% of 2010 GDP. The Budget appears to lack

specific measures to tackle fundamental issues notably household debt which is 75% of GDP (among the highest in Asia). Close to

a quarter of total household borrowings (at end Aug 2010) were for non-productive consumption loans like car and credit cards.

� Equity: As analysts factor in the impact of Budget 2011, forward corporate earnings growth may continue to head north from existing

levels. However MSCI Malaysia Forward Price-Earnings multiple is already trading at 20% premium to regional EM Asia average.

After the YTD market run-up we are neutral over 12 months, given Malaysia’s higher average dividend yield and defensive low beta

market features.

� Currency: SCB analyst believe BNM has made subtle change in its FX policy since mid-September, which may suggest that the

central bank has become more concerned that sharp MYR appreciation is out of line with economic fundamentals. We expect USD-

MYR to grind lower into year-end on broad USD weakness and seasonality, but USD-MYR should bounce in H1-2011 on Malaysia’s

economic slowdown.

…/ continued

Forecasts – Economics and FX Rates

As of 29 October 2010

…/ continued

Forecasts – Policy Rates, Market Rates, Yields

As of 29 October 2010

…/ continued

Forecasts – Policy Rates, Market Rates, Yields

As of 29 October 2010

…/ continued

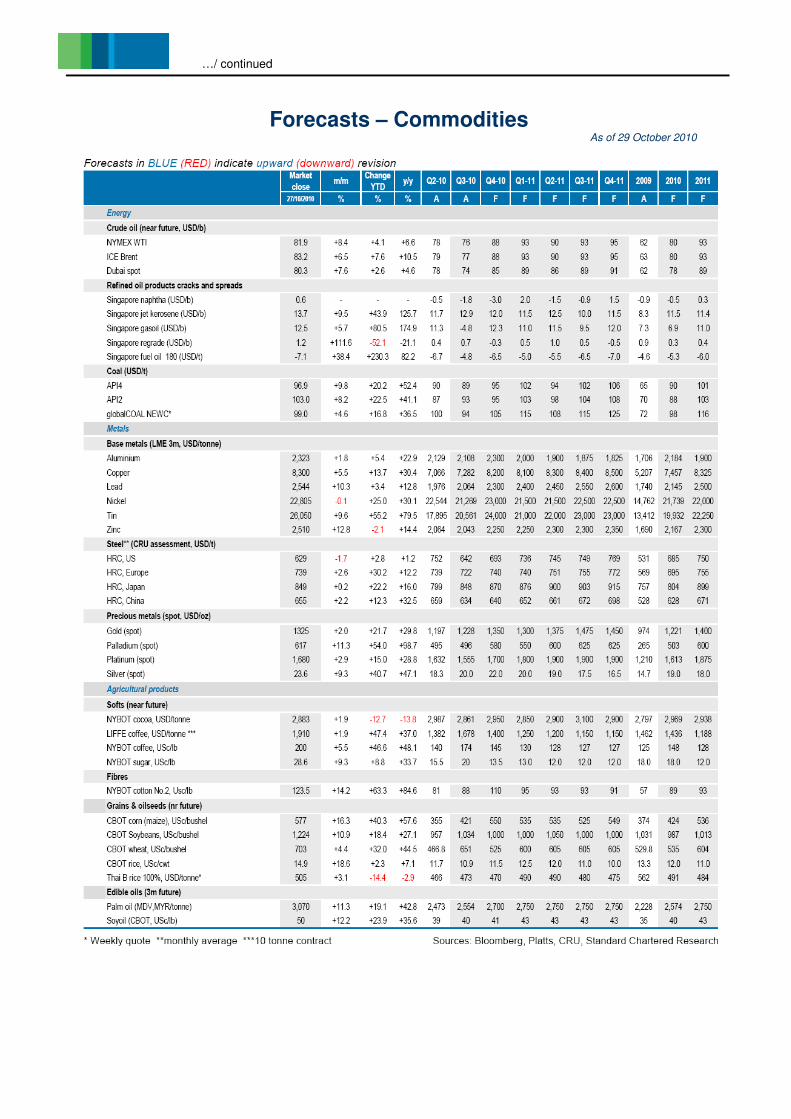

Forecasts – Commodities

As of 29 October 2010

…/ continued

Disclosure Appendix

Global disclaimer:

This document was originally issued as of the date and time as stated at the end of this document by Standard Chartered Global Research, and is now distributed by Standard Chartered Bank on 2 November. This document must not be redistributed or forwarded to any other person without the express written consent of the Standard Chartered Bank (“SCB”).

Standard Chartered Bank is incorporated in England and Wales with limited liability by Royal Charter 1853, Reference number ZC 18. The Principal Office of the Company is situated in England at 1 Aldermanbury Square London EC2V 7SB. Standard Chartered Bank is authorised and regulated by the Financial Services Authority under FSA register number 114276.

To The Standard Chartered Private Bank clients: The Standard Chartered Private Bank is the private banking division of Standard Chartered Bank.

Private banking activities may be carried out internationally by different SCB legal entities and affiliates according to local regulatory requirements. Not all products and services are provided by all SCB branches, subsidiaries and affiliates. Some of the SCB entities and affiliates only act as representatives of the Standard Chartered Private Bank, and may not be able to offer products and services, or offer advice to clients. They serve as points of contact only.

SCB makes no representation or warranty of any kind, express, implied or statutory regarding this document or any information contained or referred to on the document.

If you are receiving this document in any of the countries listed below, please note the following:

China1: This document is being distributed in China by, and is attributable to, Standard Chartered Bank (China) Limited which is mainly

regulated by China Banking Regulatory Commission (CBRC), State Administration of Foreign Exchange (SAFE), and People’s Bank of China (PBOC). In China, the Standard Chartered Private Bank is the private banking division of Standard Chartered Bank (China) Limited.

Dubai International Financial Centre (DIFC): This document is distributed by SCB DIFC on behalf of the product and/or service provider. SCB DIFC is regulated by the Dubai Financial Services Authority (DFSA) and is authorised to provide financial products and services to persons who meet the qualifying criteria of a Professional Client under the DFSA rules. The protection and compensation rights that may generally be available to retail customers in the DIFC or other jurisdictions will not be afforded to Professional Clients in the DIFC.

Hong Kong: This document is being distributed in Hong Kong by, and is attributable to, Standard Chartered Bank (Hong Kong) Limited which is regulated by Hong Kong Monetary Authority and Securities and Futures Commission. In Hong Kong, The Standard Chartered Private Bank is the private banking division of Standard Chartered Bank (Hong Kong) Limited.

Japan: This document is being distributed to the Specified Investors, as defined by the Financial Instruments and Exchange Law of Japan (FIEL), for information only and not for the purpose of soliciting any Financial Instruments Transactions as defined by the FIEL or any Specified Deposits, etc. as defined by the Banking Law of Japan.

Jersey, Channel Islands: The Standard Chartered Private Bank is the Registered Business Name of Standard Chartered (Jersey) Limited (“SCJ”) in Jersey. SCJ is regulated by the Jersey Financial Services Commission. It is also an authorised financial services provider under license number 9790 issued by the Financial Services Board of the Republic of South Africa. Copies of the latest audited accounts are available from the registered office and principal place of business: PO Box 80, 15 Castle Street, St Helier, Jersey, JE4 8PT.

Korea: This document is distributed in Korea by Standard Chartered First Bank Korea Limited.

Malaysia: This document is distributed in Malaysia by Standard Chartered Bank Malaysia Berhad.

Singapore: This document is being distributed in Singapore by SCB Singapore branch only to accredited investors, expert investors or institutional investors, as defined in the Securities and Futures Act, Chapter 289 of Singapore. Recipients in Singapore should contact SCB Singapore branch in relation to any matters arising from, or in connection with, this document. In Singapore, the Standard Chartered Private Bank is the Private Banking division of SCB, Singapore branch.

South Africa: SCB is licensed as a Financial Services Provider in terms of Section 8 of the Financial Advisory and Intermediary Services Act 37 of 2002. SCB is a Registered Credit provider in terms of the National Credit Act 34 of 2005 under registration number NCRCP4.

Switzerland: This document is distributed in Switzerland by Standard Chartered Bank (Switzerland) SA.

Taiwan: This document is being distributed in Taiwan by, and is attributable to, Standard Chartered Bank (Taiwan) Limited which is regulated by the Taiwan Financial Supervisory Commission. In Taiwan, The Standard Chartered Private Bank is the private banking division of Standard Chartered Bank (Taiwan) Limited.

United Arab Emirates (UAE): This document is distributed by SCB, UAE on behalf of the product and/or service provider. SCB UAE is regulated by the Central Bank of the United Arab Emirates and subject to its laws and regulations.

United Kingdom: In the United Kingdom, the Standard Chartered Private Bank is the Private Banking division of Standard Chartered Bank.

United States: Except for any document relating to foreign exchange, FX or global FX, Rates or Commodities, distribution of this document in the United States or to US persons is intended to be solely to major institutional and accredited investors as defined in Rule 15a-6(a)(2) and Regulation D Rule 501 under the US Securities Act of 1933. All US persons that receive this document by their acceptance thereof represent and agree that they are major institutional or accredited, private bank investors and understand the risks involved in executing transactions in securities. Any US recipient of this document wanting additional information or to effect any transaction in any security or

1 For the purposes of this document, China does not include the Hong Kong Special Administrative Region, the Macau Special Administrative Region and Taiwan.

…/ continued

financial instrument mentioned herein must do so by contacting a registered representative of Standard Chartered Securities (North America) Inc. (“SCSI”) 1 Madison Avenue, New York, NY 10010, US, tel +1 212 667 1000. Private banking products and services are offered through Standard Chartered Bank International (Americas) Limited (“SCBI”), 1111 Brickell Avenue, 16th Floor, Miami, FL 33131 tel. + 1 305 530 2169. SCSI and SCBI are wholly owned subsidiaries of the Standard Chartered Bank.

The Standard Chartered Private Bank is the private banking division of Standard Chartered Bank. Not all products and services are available to clients of SCBI.

The securities or financial instruments mentioned herein may not have not been registered under the United States Securities Act of 1933, as amended (the “Securities Act”), the securities laws of any state, or the securities laws of any other jurisdiction, nor such registration may be contemplated. SCBI will offer and sell securities or financial instruments exclusively to non-US persons in offshore transactions pursuant to Regulation S under the Securities Act. For this purpose “US Persons” means a US person as defined in Rule 902(k) of Regulation S of the Securities Act. All non-US persons that receive this document by their acceptance thereof represent and warrant that (i) they are not a U.S. Person as defined in Rule 902(k) of Regulation S under the Securities Act and (ii) all offers to sell and offers to buy any security or financial instrument mentioned herein was made to or by the non-US person while the non-US persons was outside the jurisdictional boundaries of the United States and, at the time the non-US persons’ order to buy any security or financial instrument mentioned herein was originated, the non-US person was outside the jurisdictional boundaries of United States.

WE DO NOT OFFER OR SELL SECURITIES TO US PERSONS UNLESS EITHER A) THOSE SECURITIES ARE REGISTERED FOR SALE WITH THE US SECURITIES AND EXCHANGE COMMISSION AND ALL APPROPRIATE US STATE AUTHORITIES; OR B) THE SECURITIES OR SPECIFIC TRANSACTION QUALIFY FOR AN EXEMPTION UNDER THE US FEDERAL AND STATE SECURITIES LAW NOR DO WE OFFER OR SELL SECURITIES TO US PERSONS UNLESS (I) WE, OUR AFFILIATED COMPANY AND THE APPROPRIATE PERSONNEL ARE PROPERLY LICENSED TO CONDUCT BUSINESS OR (II) WE, OUR AFFILIATED COMPANY AND THE APPROPRIATE PERSONNEL QUALIFY FOR EXEMPTIONS UNDER US FEDERAL AND STATE LAW.

Investment products are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any government agency. Investment products are not a deposit or other obligation of, or guaranteed by, SCB, SCBI, SCSI or any of their respective affiliates, and may be subject to investment risks, which may include market and currency exchange risk, fluctuations in value, and possible loss of the principal invested. Investment products are also subject to economic, political, and social risks occurring in the United States and abroad. The past performance of investment products is not predictive of future results.

INVESTMENT PRODUCTS: ARE NOT FDIC INSURED – HAVE NO BANK GUARANTEE – MAY LOSE VALUE

This document has been produced for the purposes of marketing and is not independent research.

The information in this document is provided for information purposes only. It does not constitute any offer, recommendation or solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. Users of this document should seek advice regarding the appropriateness of investing in any securities, financial instruments or investment strategies referred to on this document and should understand that statements regarding future prospects may not be realised. Opinions, projections and estimates are subject to change without notice. The value and income of any of the securities or financial instruments mentioned in this document can fall as well as rise and an investor may get back less than invested. Foreign-currency denominated securities and financial instruments are subject to fluctuation in exchange rates that could have a positive or adverse effect on the value, price or income of such securities and financial instruments.

Past performance is not indicative of comparable future results and no representation or warranty is made regarding future performance.

SCB is not a legal or tax adviser, and is not purporting to provide you with legal or tax advice. If you have any queries as to the legal or tax implications of any investment you should seek independent legal and/or tax advice.

SCB, and/or a connected company, may have a position in any of the instruments or currencies mentioned in this document. SCB has in place policies and procedures and physical information walls between its Research Department and differing public and private business functions to help ensure confidential information, including ‘inside’ information is not publicly disclosed unless in line with its policies and procedures and the rules of its regulators. You are advised to make your own independent judgment with respect to any matter contained herein.

SCB and/or any member of the SCB group of companies may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to on the website or have a material interest in any such securities or related investment, or may be the only market maker in relation to such investments, or provide, or have provided advice, investment banking or other services, to issuers of such investments. Accordingly, SCB, its affiliates and/or subsidiaries may have a conflict of interest that could affect the objectivity of this document.

SCB accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from your use of this document, howsoever arising, and including any loss, damage or expense arising from, but not limited to, any defect, error, imperfection, fault, mistake or inaccuracy with this document, its contents or associated services, or due to any unavailability of the document or any part thereof or any contents or associated services.

Copyright: Standard Chartered Bank 2010. Copyright in all materials, text, articles and information contained herein is the property of, and may only be reproduced with permission of an authorised signatory of, Standard Chartered Bank. Copyright in materials created by third parties and the rights under copyright of such parties are hereby acknowledged. Copyright in all other materials not belonging to third parties

Do not invest in investment products unless you fully understand and are willing to assume the risks associated with them.

…/ continued

and copyright in these materials as a compilation vests and shall remain at all times copyright of Standard Chartered Bank and should not be reproduced or used except for business purposes on behalf of Standard Chartered Bank or save with the express prior written consent of an authorised signatory of Standard Chartered Bank. All rights reserved. © Standard Chartered Bank 2010.

Regulation AC Disclosure:

The research analyst or analysts responsible for the content of this research report certify that: (1) the views expressed and attributed to the research analyst or Analysts in the research report accurately reflect their personal opinion(s) about the subject securities and issuers and/or other subject matter as appropriate; and, (2) No part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this research report. On a general basis, the efficacy of recommendations is a factor in the performance appraisals of analysts.

Data available as of 09:00 GMT 2 November 2010. This document is released at 09:00 GMT 2 November 2010.

Document approved by: Michael Rainer Preiss, Head of Consumer Bank Client Research & Danny Chang, Head of Retail Distribution and Due Diligence

THIS IS NOT A RESEARCH REPORT AND HAS NOT BEEN PRODUCED BY A RESEARCH UNIT