2 a comparative study of methods of csr … · method-1 (through separate csr project management...

TRANSCRIPT

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

5 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

A COMPARATIVE STUDY OF METHODS OF CSR

IMPLEMENTATION IN INDIAN CONTEXT

Ms. Madhu Bala

Research Scholar, Department of Commerce, Kurukshetra University, Kurukshetra, India

ABSTRACT

How is corporate social responsibility (CSR) implemented / organized in Indian companies?

CSR integration into business operations is one of the great challenge facing Indian organizations

today. The companies facing with CSR problems and challenges are required to manage effective

ways of implementation of CSR projects. CSR integration with business operations involves

planning and implementation of CSR activities. The common requirements of all CSR projects are

resources in the form of finance, manpower and time. Depending on the availability of these

resources, companies opt for different modes of executing CSR. The organizations need to assess the

extent of disturbance in the business operations while adopting a method of implementation of CSR

programmes and initiatives. The overall disturbance should be minimum and controllable. The

results of adopting a particular method, consequences of disturbance in business operations and long

term performance of company must outweigh the cost of adoption of a particular method of

implementation of CSR. This study aims to explore the methods of implementation of CSR in Indian

companies. Further, it is intended to investigate if there are any differences / uniqueness in methods

of CSR implementation and what is the preference of companies in selection of the various methods

of implementation of CSR.A structured questionnaire was used to collect the data from top 500

Indian companies resulting in responses from 162 companies. The data was subjected to computing

percentages analysis and rating method.

Keywords: Corporate Social Responsibility (CSR), NGO, Methods, CSR Implementation.

INTRODUCTION

How should corporate social responsibility (CSR) implemented in Indian companies? CSR

Integration into business operations is one of the great challenges facing Indian organizations today.

Global operation makes it necessary to compare how companies of different regions approach

INTERNATIONAL JOURNAL OF MANAGEMENT (IJM)

ISSN 0976-6502 (Print)

ISSN 0976-6510 (Online)

Volume 6, Issue 1, January (2015), pp. 05-18

© IAEME: http://www.iaeme.com/IJM.asp

Journal Impact Factor (2014): 7.2230 (Calculated by GISI)

www.jifactor.com

IJM

© I A E M E

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

6 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

sustainability (Aaron and Singh, 2005). As the effectiveness of implementation of CSR initiatives in

the form of new practice often depends on linkages with other routines in the organization, an

appropriate response to CSR challenge may require close coordination across relevant functions

(Westely and Vredenburg, 1996). Inadequate cross functional co-ordination and organizational

barriers (Cordano and Frieze, 2000) can lead to internal conflicts and ultimately weak performance

towards achieving societal and corporate goals. After all, companies address social and

environmental issues through different types of communications (Husted, 2003). For instance, firms

can promote human rights through in-house projects, partnership agreements, or by signing up to

industry-wide standards (Abbott, 2012). The companies need to assess to what extent adopting a

method of implementation of CSR programmes and initiatives might disturb current routines,

whereby any inconsistency should be acceptable low and controllable. At minimum, the positive

contribution of CSR programmes to long-run business performance should outweigh the additional

costs resulting from any disturbance to current business practices.

The term “CSR” is brilliant one; it means something, but not always the same thing, to

everybody. To some it conveys the idea of legal responsibilities and liability; to others it means

socially responsible behaviour in an ethical sense, to still others, the meaning transmitted is that of

‘responsible for’, in the causal mode; many simply equate it with charitable contribution (Votaw,

1973). It is also important to note that almost all types of application strategies and CSR

implementation tools depend on type of industry, type of CSR activities/issues undertaken by

companies, cultural and political environments in which companies are operating. Thus there will be

different methods of implementation of CSR activities by different companies. So there is need to

conduct a study to explore the methods of implementation of CSR in Indian companies. Further, it is

intended to investigate if there are any differences / uniqueness in methods of CSR implementation

and what is the preference of companies in selection of the various methods of implementation of

CSR.

METHODS OF IMPLEMENTATION OF CSR AND THEORETICAL FRAMEWORK FOR

RESEARCH

Piercy (2002) has defined implementation as ‘a process of making strategy work and

identifying the things needed to get from the plans to the action’. The Policy implementation has

been defined by Bergen and While (2005) as ‘encompassing those actions by public and private

individuals (or groups) that are directed at the achievement of objectives set forth in prior policy

decisions’. Further Roome and Jonker (2005) has defined implementation of CSR for their purposes

as ‘as an emerging sense making process developed over a period of time, shaped by a series of

(non) intentional choices and actions by various actors and influenced by a changing set of

conditioning and intervening factors’. According to Ahrne & Brunsson’s (2011) the concept of

implementation can be better understood once the organizational elements that are needed to achieve

organized orders are unpacked: i.e., membership, hierarchy, rules, monitoring, and sanctioning. Thus

initially companies have to come up with available resources to organise CSR. These examples show

the variety of ways in which implementation is understood in particular contexts, and show a mix of

views of implementation. However, a context-specific definition of implementation does not exist

(such is the case with CSR implementation).

There is evidence that companies are investing in their own CSR capacity. This is evident in

alignment of CSR with corporate aims and strategy, dedicated CSR personnel and sub-organizational

units, budgets, procedures (Moon 2004; see also Bondy et al. 2012; Strand 2012). However, it is now

also organized by and with external players such as other businesses associates, governmental or

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

7 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

civil society partners, who bring new forms of organization, norms, incentives, and roles (Moon

2004). According to Gond et al. (2011) organising CSR not only involves partnerships (e.g., between

NGOs and firms), CSR standards (e.g., the Global Reporting Initiative), but also regulation through

government policies (e.g., for reporting environmental, social and governance impacts). In Indian

context, the draft Company Bill Act 2013 (Pradeep Udhas and Sai Venkateshwaran, 2013) provides

the guidelines for manner/methods/modes in which the company can undertake/implement CSR

activities and incur CSR spend. These guidelines are given in Table-1.

Table-1 Guidelines of methods of implementation of CSR as per Company Bill Act 2013

Sr. No. Description of Guidelines

I.

The company can set-up a not-for-profit organisation in the form of trust, society or

non-profit company to facilitate implementation of its CSR activities. However, the

contributing company shall specify projects / programs to be undertaken by such an

organisation and the company shall establish a monitoring mechanism to ensure that

the allocation to such organisation is spent for intended purpose only.

II. A company may also implement its CSR programs through not-for-profit

organisations that are not set up by the company itself.

III.

CSR spends may be included as part of company’s prescribed CSR spend only if

such organisations have an established track record of at least 3 years in carrying on

activities unrelated areas.

IV. Companies may also collaborate or pool resources with other companies to undertake

CSR activities.

V. Only CSR activities undertaken in India would be considered as eligible CSR

activities.

VI.

CSR activities may generally be conducted as projects or programmes (either new or

on-going), however, excluding activities undertaken in pursuance of the normal

course of business of a company.

VII. CSR projects/programs may also focus on integrating business models with social

and environmental priorities and processes in order to create shared value.

VIII. CSR activities shall not include activities exclusively for the benefit of employees

and their family members.

IX. CSR spend may contribute towards Central & State Government funds for socio-

economic development and relief.

Source: KPMG, Company Bill Act 2013, New Rules of the Game, Oct’2013

The theoretical framework for this study is derived from the guidelines as given in Table-1.

Based on these guidelines, 5 methods of CSR implementation are found. These 5 methods of CSR

implementation are listed in Table-2.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

8 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

Table - 2 List of Methods of CSR Implementation

Sr. No. Description of Method

Method-1 Through separate CSR Project Management Department

Method-2 Through Partner NGOs

Method-3 Through Establishing Trust/Foundation/Society

Method-4 Through collaborating with other companies

Method-5 Through funding to Government

Source: Data compiled by Author.

The detail explanation of these 5 methods of CSR implementation is given below:-

METHOD-1 (THROUGH SEPARATE CSR PROJECT MANAGEMENT DEPARTMENT)

Setting up CSR Projects Management Department involves appointment of some expert

staff with the responsibility of assessing the social needs and problems and formulate the strategies

to tackle them. These departments are not necessarily called “CSR”, but carry a variety of names,

including sustainable development, sustainability, environmental affairs, social compliance public

affairs or combinations thereof. These CSR departments manage the company's social programs and

make sure that the company's efforts in the field of corporate social responsibility remain in the eyes

of the public. Having a special department to look after CSR issues depends on the size and CSR

issues undertaken by companies. CSR departments have the responsibility of planning,

implementing, and monitoring the CSR practices of the companies. They decide the areas of CSR to

be addressed and come out with a social responsibility project. New Company Bill Act 2013 has

made it mandatory for companies falling under this section to have a CSR committee. The CSR

committee shall consist of 3 or more directors, out of which at least one shall be independent. CSR

committee would be responsible to formulate CSR Policy, recommend the CSR activities as

specified in Schedule VII & monitor the CSR expenditure. Board would be mandatorily required to

disclose its CSR Policy in its report and on the company’s website.

METHOD-2 (THROUGH PARTNER NGOS)

Partnership between business and non-profit organizations is an increasingly prominent

element of CSR. A non-governmental organization (NGO) is any non- profit, voluntary group that is

organized at a local, national or international level. Task-oriented and driven by people with a

common interest, NGOs perform a variety of service and humanitarian functions. They bring

people's concerns to governments, advocate and monitor policies, and encourage political

participation through provision of information. Some are organized for some specific issues, such as

human rights, environment, education, or health. Such cross–sector partnerships have been one of the

most exciting and challenging ways that organizations have been implementing CSR in recent years

(Seitanidi and Ryan, 2007). A general definition of partnerships in a CSR context is ‘‘collaborative

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

9 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

arrangements in which actors from two or more spheres of society (state, market, and civil society)

are involved in a non-hierarchical process, and through which these actors strive for a sustain ability

goal.’’ (van Huijstee et al. 2007). Non-governmental organizations (NGOs) normally don’t have

enough financial or knowledge recourses. However, due to their focus on specific issues, they could

work more effectively and actively on them than the companies that have a commercial goal as their

base. Corporates increasingly join hands with Non-government organizations (NGOs) and use their

expertise in devising programs which address wider social problems.

METHOD-3 (THROUGH ESTABLISHING TRUST/FOUNDATION/SOCIETY)

The trust/foundation/society is established to provide structure and focus to ongoing social

responsibilities of a company. They are given separate budget for the whole year, which may be

evaluated from time to time for enhancement, so that different social responsibilities are executed

successfully. Where a company has been set up with a charitable objective or is a

Trust/Society/Foundation/any other form of entity operating within India to facilitate implementation

of its CSR activities, then it shall be applied that; (a) contributing company would need to specify the

projects/ programs to be undertaken by such an organization, for utilizing funds provided by it; (b)

contributing company shall establish a monitoring mechanism to ensure that the allocation is spent

for the intended purpose only.

METHOD-4 (THROUGH COLLABORATING WITH OTHER COMPANIES)

Companies may collaborate or pool the resources with other companies to undertake CSR

activities. This method is mostly adopted for the bigger projects like construction of orphanage,

schools, hospitals, etc. for the society. Joint ventures are created mainly to achieve synergies that

lead to reduction in the cost.

METHOD-5 (THROUGH FUNDING TO GOVERNMENT)

The contribution to Prime Minister’s National Relief Fund and such other funds as set up by

Government falls under this method. Schedule VII of the Company Bill Act 2013 recommends

“Contribution to PM’s national relief funds and such other funds established by central or state

government for socio-economic development and relief and welfare of scheduled castes and

scheduled tribes and other backwards classes, minorities and women” as one of the activities to be

taken under CSR. The companies may also use this mode of CSR implementation as per Company

Bill Act 2013. .

REVIEW OF LITERATURE

A number of research papers and articles provide a detailed insight on methods of

implementation of CSR activities of companies in different countries in various industries. The

findings from the literature are presented below:-

Andre Nijhof (2008) conceptualised the extent to which partnerships with non-

governmental organisations (NGOs) are necessity for successful efforts of business in the area of

corporate social responsibility (CSR). The study revealed that based on three different strategies

towards CSR, the suggestion is that NGOs tend to become involved in partnerships with companies

that have an interest in postponing concrete results, while partnerships with companies that have the

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

10 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

potential for the biggest contribution to the ambitions of NGOs have the highest risk of diminishing

NGO-legitimacy.

Terje I. Vaaland et. al. (2008) highlighted that CSR should be managed by a combination of

handling unexpected episodes that threaten existing social responsibility (incident recovery) and the

long-term reduction of gaps between stakeholder expectations and the company performance (CSR

enforcement). Furthermore, it was suggested that CSR implies building and maintaining

relationships with society through interplay between actors, resources and activities.

Boston College Center for Corporate Citizenship (2009) also provided insights into the

organization of CSR within large North American companies. The study confirmed that managing a

company’s role in society is becoming a formal part of corporate structure and management, as many

companies are internalising CSR as a function of corporate departments and/or cross-departmental

teams. The survey also reveals that departments dedicated to CSR are beginning to emerge. Studies

thus point towards an increase in the formalization of CSR, made visible by the centralization of

CSR activities in specialised departments.

Hung Woanet. al. (2010) explored the most potent internal resources of a firm that

contribute to the CSR agenda. The results implied that firms that are intent on being CSR-active

should consider implementing the various management systems relevant for their businesses.

Managers responsible for the CSR agenda might wish to highlight the fact that adherence to such

systems actually contributes to the bottom line, thus minimizing resistance from decision-makers,

who might view CSR as a costly initiative.

Jeffrey Avina, (2011) argued that a structured approach of engagement to the private sector

for CSR support is possible if public safety entities understand how to effectively involve private

sector organizations in their work. This includes clear tangible asks with demonstrable returns and an

eye to understanding what effective CSR encompasses from an outcome perspective but also from

the perspective of what drives the private sector to engage in CSR.

David Katambaet. al. (2012) conducted a study to investigate how business enterprises in

Uganda manage their corporate social responsibility (CSR) activities and projects. The findings

showed unbalanced engagement in CSR for business managers in Uganda. Managers are largely

motivated towards CSR by external factors such as attracting and retaining customers, enhancing

reputation and operational efficiencies to achieve competitive advantage, rather than internal factors

such as CSR policies, employee welfare and CSR reporting. Another significant finding was that the

responsibility to initiate, administers, and monitors CSR activities are largely vested in middle-level

managers. These factors pose many challenges to CSR implementation amongst managers in

Uganda.

Baumann-Pauly et al. (2013) studied how firm size affects the organization of CSR. Based

on a comparative study of Swiss MNCs and SMEs, they argued that small firms possess several

organizational characteristics that promote the implementation of CSR-related practices in core

business functions, but, at the same time, constrain external communication and reporting. By

contrast, MNCs possess characteristics that are favourable for promoting external communication

and reporting, but, at the same time, constrain internal implementation.

Arenas et al. (2013) suggested that it is important to examine the role of third parties

in understanding collaboration between firms and civil society organizations. They analysed the

presence of third parties and their different roles to explain how collaboration is facilitated. Further

Burchell and Cook (2013) examined the theoretical implications of the changing relationships

between NGOs and businesses that have emerged as a response to the evolving agenda around CSR

and sustainable development. They do so by focusing on a process of appropriation and co-optation

of protest by the business community.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

11 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

Mohammad Safari Kahreh et al. (2013) investigated the CSFs (Critical success factors) for

CSR implementation in Iranian banking sector. This study first provided a framework for CSR

implementation in the banking sector. Based on the viewpoint of the experts of this research, 23

CSFs for CSR implementation were identified and then the importance of these CSFs was

determined. All the identified CSFs were categorized into the five main sections of the

organizational functional areas. These functional areas include financial, marketing, environmental,

strategic and human resources.

Henry Ogiri Itotenaa et al. (2014) conducted a study for CSR policy making and

implementation in developed countries. The study revealed that: voluntary CSR implementation and

reporting; transparency; and execution of national policy statement on CSR, are the process

indicators of CSR implementation in developed society. The results of this study could have policy

implications for both executive and MPs of national governments in developed society for CSR

regulatory policies.

From above literature review, it is cleared that the companies across the world are involved

in one or another method for implementing their CSR activities and trying to make their effort

successful towards effective implementation of CSR. But it is evident that there is relative paucity of

information in the literature with regards to Indian context. Through this exploratory study, we seek

to partially fill this lacuna by identifying the methods of CSR implementation in Indian companies.

PROBLEM STATEMENT

The companies are involved in various areas of CSR activities. But the question is how

these companies are executing their CSR activities in India. Integration of CSR with business

operations involves planning and implementation of CSR activities. The common requirements of all

CSR projects are resources in the form of finance, manpower and time. Depending upon the

availability of these resources, companies opt for different modes of executing CSR practices. CSR

has varied enormously by context, particularly the context of place, or national business systems

(Matten and Moon 2008). Moreover, the most important characteristic to note in CSR is its

susceptibility to change (Gond and Moon 2011). The Change has been evident through variations in

(i) the relative significance of Garriga and Mele’s (2004) theoretical positions on CSR (ii) the

balance of importance attached to the different levels of responsibility in Carroll’s (1979) CSR

pyramid (iii) the variable prioritization of particular stakeholders(iv) balance of social, economic,

environmental, and governance criteria used in assigning and claiming responsibility. Thus the

method of implementation may vary according to these characteristics. Further, the companies CSR

is currently characterised by many unsystematic practices, i.e. groups of arrangements that are fit for

purpose within specific contexts but which lack transferability and sustainability. There is a lack of

studies in Indian context, which explore the methods of implementation of CSR, their analysis for

most preferred methods and any differences / uniqueness therein. So a need is felt by author to

conduct a study which explores methods of implementation of CSR in Indian companies, and

preferences and any differences / uniqueness among these methods. The comparative study is

conducted among the three groups of companies. The three groups of companies are: Private Indian

Companies (PICs), Multinational Companies (MNCs) and Public Sector Companies (PSCs) and are

explained in Table-3.Existing literature shows that no such study has been undertaken so far to the

best of our knowledge which showcases comparative analysis of methods of implementation of

Private Indian Companies (PICs), Multinational Companies (MNCs) and Public Sector Companies

(PSCs).

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

12 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

Table - 3 Groups of Companies selected for Study

Sr. No. Group of

Companies Label Specification

I Private Indian

Companies PICs

A company owned either by non-government organization

or by a relatively small number of shareholders or company

members and which owns and controls production and

services facilities in India only

II Multinational

Companies MNCs

A company which owns and controls production and

services facilities in more than one country

III

Public Sector

Undertaking

Companies

PSCs

A government-owned corporation in India, in which,

majority (51% or more) of the paid up share capital is held

by central government or by any state government or partly

by the central governments and partly by one or more state

governments.

Source: Data compiled by Author from Wikipedia

OBJECTIVES OF STUDY

The present study aims on identifying and analysing the preferences to methods/modes of

implementation of CSR activities in Indian companies and a comparative study for differences /

uniqueness for that among Private Indian Companies (PICs),Multinational Companies (MNCs) and

Public Sector Companies (PSCs);

Aiming at the following objectives:-

a) To identify methods of implementation of CSR practices in Indian companies.

b) To analyze most preferred method of implementation of CSR activities.

c) To analyze significant differences/uniqueness among CSR implementation methods.

RESEARCH METHODOLOGY

The study is based on both primary and secondary data. The secondary data is used for the

theoretical framework of the study and primary data is used for the comparative analysis. The sample

of top 500 Indian companies is selected. For top 500 Indian companies, help was taken from data

base of Indian companies available on website www.fundoodata.com.The study focuses on

companies that have successfully integrated CSR into corporate strategy and practising successfully

CSR in their companies. Therefore the websites of these companies have been visited to identify that

whether they are following CSR practices or not. For the analysis of the research objectives, a self-

structured questionnaire is devised. In the questionnaire, the respondents were requested to select

methods of implementation of CSR activities / projects being used by their companies. The

questionnaire was sent to each such company (the companies, who practice CSR) on email. The

difficulty was felt to get the concerned CSR person through websites of these companies; so in this

regard help was taken from social network Linked to get contacts of concerned CSR persons of

selected companies. Good efforts are made to contact CSR persons on phone for discussion about the

CSR activities and their methods of implementation. The telephonic discussion with CSR persons

enhances the response rates. The responses from 162 companies (79 Private Indian companies, 54

from Multinational companies and 29 from Public Sector Undertaking companies)were received

from the following sectors :-

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

13 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

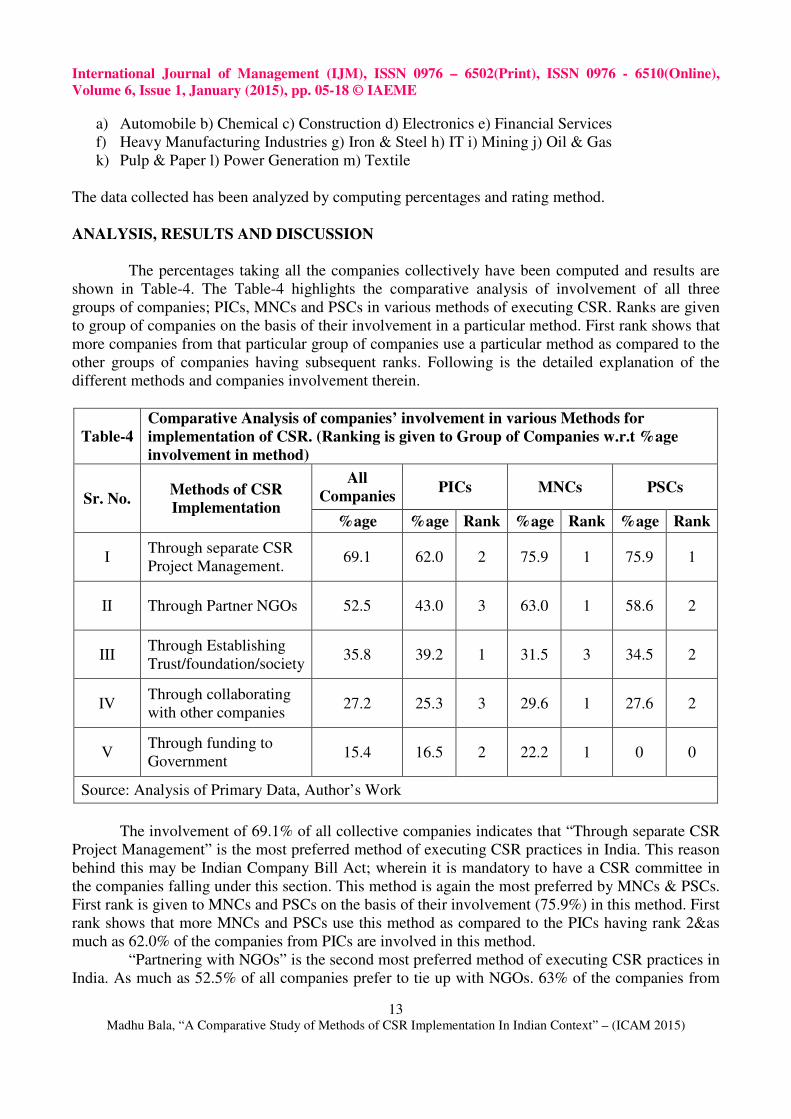

a) Automobile b) Chemical c) Construction d) Electronics e) Financial Services

f) Heavy Manufacturing Industries g) Iron & Steel h) IT i) Mining j) Oil & Gas

k) Pulp & Paper l) Power Generation m) Textile

The data collected has been analyzed by computing percentages and rating method.

ANALYSIS, RESULTS AND DISCUSSION

The percentages taking all the companies collectively have been computed and results are

shown in Table-4. The Table-4 highlights the comparative analysis of involvement of all three

groups of companies; PICs, MNCs and PSCs in various methods of executing CSR. Ranks are given

to group of companies on the basis of their involvement in a particular method. First rank shows that

more companies from that particular group of companies use a particular method as compared to the

other groups of companies having subsequent ranks. Following is the detailed explanation of the

different methods and companies involvement therein.

Table-4

Comparative Analysis of companies’ involvement in various Methods for

implementation of CSR. (Ranking is given to Group of Companies w.r.t %age

involvement in method)

Sr. No. Methods of CSR

Implementation

All

Companies PICs MNCs PSCs

%age %age Rank %age Rank %age Rank

I Through separate CSR

Project Management. 69.1 62.0 2 75.9 1 75.9 1

II Through Partner NGOs 52.5 43.0 3 63.0 1 58.6 2

III Through Establishing

Trust/foundation/society 35.8 39.2 1 31.5 3 34.5 2

IV Through collaborating

with other companies 27.2 25.3 3 29.6 1 27.6 2

V Through funding to

Government 15.4 16.5 2 22.2 1 0 0

Source: Analysis of Primary Data, Author’s Work

The involvement of 69.1% of all collective companies indicates that “Through separate CSR

Project Management” is the most preferred method of executing CSR practices in India. This reason

behind this may be Indian Company Bill Act; wherein it is mandatory to have a CSR committee in

the companies falling under this section. This method is again the most preferred by MNCs & PSCs.

First rank is given to MNCs and PSCs on the basis of their involvement (75.9%) in this method. First

rank shows that more MNCs and PSCs use this method as compared to the PICs having rank 2&as

much as 62.0% of the companies from PICs are involved in this method.

“Partnering with NGOs” is the second most preferred method of executing CSR practices in

India. As much as 52.5% of all companies prefer to tie up with NGOs. 63% of the companies from

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

14 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

MNCs group reported to have tie ups with NGOs in India. However this percentage is 58.6% for

PSCs and 43% for PICs. This shows that alliance with NGOs is the most popular method among

MNCs followed by PSCs and PICs. The reason behind most popular method among MNCs may be

to use expertise of NGOs for particular social cause and want to save time and resources of

company.

Next most preferred way of implementing CSR is “Through establishment of

Trust/foundation/society” for social issues. 35.8% of companies reported to follow this mode. This

method is popular in PICs (39.2%) followed by PSCs (34.5%) and MNCs (31.5%).

The method “Through collaboration with other companies” is at fifth place. As many as

27.2% companies reported to have joined hands with other companies for socially responsible

projects. This method is mostly adopted for the bigger projects like construction of orphanage,

schools, hospitals, etc. for the society. Joint ventures are created mainly to achieve synergies that

lead to reduction in the cost. MNCs (29.6%) reported to have joint ventures with other companies for

social programmers and they are at first place. PSCs are at second place (27.6%), and PICs are at

third place (25.3%).

CSR implementation “Through funding to government” is the least preferred method. Only

as much as 15.4% companies reported to go this way. The reason behind this may be flaw in this

method and subject to misuse. As per the submission of the Prime Minister’s Office (PMO) to the

Central Information Commission, the Prime Minister’s National Relief Fund itself is not a

Government body and is not even answerable to either houses of the parliament. The fund consists

entirely of public contributions and does not get any government budgetary support. MNCs (22.2%)

are at the first place and PICs are at the second place to opt this method of implementation. As per

norms, PSCs cannot contribute to Prime Minister’s National Relief Fund.

Table-5 shows the preference given by companies to different methods of implementing CSR

activities in India. Accordingly, ranks are given to different methods separately for each group of

companies. This ranking shows the preference given to a particular method by various group of

companies.

Table -

5

Comparative Analysis of Methods for Implementation of CSR within the group of

companies. (Ranking is given to Method w.r.t. %age involvement of companies in a

method within the group)

Sr. No. Method of Implementation of

CSR

All

Companies PICs MNCs PSCs

%ag

e

Ran

k

%ag

e

Ran

k

%ag

e

Ran

k

%ag

e

Ran

k

1 Through separate CSR Project

Management. 69.1 1 62.0 1 75.9 1 75.9 1

2 Through Partner NGOs 52.5 2 43.0 2 63.0 2 58.6 2

3 Through Establishing

Trust/foundations/society 35.8 3 39.2 3 31.5 3 34.5 3

4 Through collaborating with

other companies 27.2 4 25.3 4 29.6 4 27.6 4

5 Through funding to

Government 22.2 5 16.5 5 22.2 5 0 0

Source: Analysis of Primary Data, , Author’s Work

International Journal of Management (IJM), ISSN 0976

Volume 6, Issue 1, January (2015), pp. 0

Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context

The percentage analysis shows that

the most preferred and popular method in all group of companies (PICs, MNCs & PSCs)

first rank. The involvement of MNCs (75.9%) and PSCs (79.5%) is more than PICs (62%).

method got the first rank; may be due to effective control and monitoring of

activities under direct supervision of companies own personnel

NGOs” has got second most popularity

involvement is more in this method than PISs (43%)

group is same.

The method “Through Establishing Trust/foundation/society

little difference in percentage involvement in this method (PICs

34.5%). The method “Through collaborating with other companies”

is little difference in percentage involvement in this method (PICs

27.6%). The method “Through funding to Government” is at

MNCs and is the least preferred method for implementation of CSR activities.

involvement in this method.

CONCLUSION

The present study aims on analysing the

of CSR activities in Indian companies and a comparison of that among Private Indian Companies

(PICs), Multinational Companies (MNCs) and Public Sector Companies (PSCs)

analysis (as given in Table-5) clearly indicates

companies in a particular method however the preference to a particular method is same. So

conclusion can be drawn as given in

is concerned.

The method “Through separate CSR Project Management” is first choice of method in all

groups of companies (PICs, MNCs & PSCs). The method “Through Partner NGOs” is second choice

of method in all groups of companies (PICs, MNCs &

Trust/foundation/society” is third choice of method in all groups of companies (PICs, MNCs &

PSCs). The method “Through collaborating with other companies” is fourth choice of method in all

groups of companies (PICs, MNCs & PSCs).

Only in PICs and MNCs group of

companies .

In all group of companies PICs, MNCs & PSCs

In all group of companies PICs, MNCs & PSCs

In all group of companies PICs, MNCs & PSCs

In all group of companies PICs, MNCs & PSCs

Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

15 A Comparative Study of Methods of CSR Implementation In Indian Context

shows that “Through separate CSR Project Management” method is

and popular method in all group of companies (PICs, MNCs & PSCs)

The involvement of MNCs (75.9%) and PSCs (79.5%) is more than PICs (62%).

may be due to effective control and monitoring of implementation of CSR

under direct supervision of companies own personnel. Thereafter method “Through Partner

popularity in all groups of companies, although MNCs (63%)

involvement is more in this method than PISs (43%) and PSCs (58.6%) still preference within the

h Establishing Trust/foundation/society” is at the

little difference in percentage involvement in this method (PICs-39.2%, MNCs

“Through collaborating with other companies” is at fourth place and again there

is little difference in percentage involvement in this method (PICs-25.3%, MNCs

Through funding to Government” is at the fifth place in c

and is the least preferred method for implementation of CSR activities.

on analysing the preferences to methods/mode

of CSR activities in Indian companies and a comparison of that among Private Indian Companies

(PICs), Multinational Companies (MNCs) and Public Sector Companies (PSCs)

clearly indicates that there is percentage variation of

mpanies in a particular method however the preference to a particular method is same. So

as given in Fig-1 as regard to choice of method of implementation of CSR

Fig 1: Choices of Method

The method “Through separate CSR Project Management” is first choice of method in all

groups of companies (PICs, MNCs & PSCs). The method “Through Partner NGOs” is second choice

of method in all groups of companies (PICs, MNCs & PSCs). The method “Through Establishing

Trust/foundation/society” is third choice of method in all groups of companies (PICs, MNCs &

PSCs). The method “Through collaborating with other companies” is fourth choice of method in all

, MNCs & PSCs). The method “Through funding to Government”

Through separate CSR Project Management

(1st Choice of Method)

Through Partner NGOs

(2nd Choice of Method)

Through Establishing trust/foundation/society

(3rd Choice of Method)

Through collaborating with other companies

(4th Choice of Method)

Through funding to Government

(5th Choice of Method)

6502(Print), ISSN 0976 - 6510(Online),

A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

CSR Project Management” method is

and popular method in all group of companies (PICs, MNCs & PSCs) and got the

The involvement of MNCs (75.9%) and PSCs (79.5%) is more than PICs (62%). This

implementation of CSR

reafter method “Through Partner

of companies, although MNCs (63%)

and PSCs (58.6%) still preference within the

the third place; there is

39.2%, MNCs-31.5%, PSCs-

is at fourth place and again there

25.3%, MNCs-29.6%, PSCs-

fifth place in case of PICs and

and is the least preferred method for implementation of CSR activities. PSCs show no

/modes of implementation

of CSR activities in Indian companies and a comparison of that among Private Indian Companies

(PICs), Multinational Companies (MNCs) and Public Sector Companies (PSCs).The percentage

there is percentage variation of involvement of

mpanies in a particular method however the preference to a particular method is same. So the

as regard to choice of method of implementation of CSR

The method “Through separate CSR Project Management” is first choice of method in all

groups of companies (PICs, MNCs & PSCs). The method “Through Partner NGOs” is second choice

PSCs). The method “Through Establishing

Trust/foundation/society” is third choice of method in all groups of companies (PICs, MNCs &

PSCs). The method “Through collaborating with other companies” is fourth choice of method in all

Through funding to Government”

Through collaborating with other

Through funding to Government

International Journal of Management (IJM), ISSN 0976

Volume 6, Issue 1, January (2015), pp. 0

Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context

is fifth choice of method in PICs and MNCs.

particular method (as given in Table

Level represents the 1st group of companies having highest %age involvement in a particular

method; II-Level represents 2nd

%age involvement and lowest %age

group of companies having lowest

The present study highlights the trend of methods of implementation of CSR activities in

Indian companies. There is no difference in c

however the involvement in a particular method varies among groups of companies and within the

group also. The study is useful for other companies who have yet to engage in CSR activities in

developing their methods for execution of CSR activities.

LIMITATIONS AND SCOPE OF FURTHER RESEARCH

The present study gives an idea of ways of CSR implementation among Indian companies

and uniqueness/differences therein among selected group of companies. An industry specific

research can be conducted to know the involvement of companies in various methods.

of implementation of CSR practices of companies across sector wise industries can also be done.

Another possible area for further research is comparison of implementation of CSR practices of

companies across the countries/regions/continents of the world.

There are many other ways

charitable events yearly, direct monetary help to society etc.

identify other possible ways for implementation of CSR practices by companies.

REFERENCES

[1] Aaron, R. & Singh, J. (2005).Getting off

[2] Abbott, K. W., Keohane, R. O

concept of legalization. International Organization

PICs (16.5%) ���� II-Level

Through collaborating with other companiesPICs (25.3%) ���� III-Level

Through Establishing Trust/foundations/society

PICs (39.2%) ���� I-Level

PICs (43%) ���� III-Level

Through separate CSR Project Management

PICs (62%) ���� II-Level

Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

16 A Comparative Study of Methods of CSR Implementation In Indian Context

is fifth choice of method in PICs and MNCs. The analysis of the involvement of companies in a

Table-4), the conclusion can be drawn as explained

group of companies having highest %age involvement in a particular

group of companies having %age involvement

and lowest %age involvement in a particular method, III

lowest %age involvement in a particular method.

The present study highlights the trend of methods of implementation of CSR activities in

Indian companies. There is no difference in choice of selection of method of implementation

however the involvement in a particular method varies among groups of companies and within the

group also. The study is useful for other companies who have yet to engage in CSR activities in

ethods for execution of CSR activities.

Fig 2: Involvement in Methods

LIMITATIONS AND SCOPE OF FURTHER RESEARCH

The present study gives an idea of ways of CSR implementation among Indian companies

therein among selected group of companies. An industry specific

research can be conducted to know the involvement of companies in various methods.

of implementation of CSR practices of companies across sector wise industries can also be done.

Another possible area for further research is comparison of implementation of CSR practices of

companies across the countries/regions/continents of the world.

There are many other ways for implementing the CSR in companies, e.g. conducting

direct monetary help to society etc. So further research can also be

implementation of CSR practices by companies.

Aaron, R. & Singh, J. (2005).Getting off shoring right. Harvard Business

Abbott, K. W., Keohane, R. O., Moravcsik, A., Slaughter, A. M., &Snidal

International Organization, 54(3): 401–419.

Through funding to Government

Level MNCs (22.5%) ���� I-Level PSCs (0.0%) ����

Through collaborating with other companiesLevel MNCs (29.6%) ���� I-Level PSCs (27.6%) ����

Through Establishing Trust/foundations/society

Level MNCs (31.5%) ���� III-

Level PSCs (34.5%) ����

Through Partner NGOs

Level MNCs (63%) ���� I-Level PSCs (58.6%) ����

Through separate CSR Project Management

Level MNCs (75.9%) ���� I-Level PSCs (75.9%) ����

6502(Print), ISSN 0976 - 6510(Online),

A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

he involvement of companies in a

can be drawn as explained in Fig2. Where I-

group of companies having highest %age involvement in a particular

group of companies having %age involvement between highest

a particular method, III-Level represents 3rd

The present study highlights the trend of methods of implementation of CSR activities in

hoice of selection of method of implementation

however the involvement in a particular method varies among groups of companies and within the

group also. The study is useful for other companies who have yet to engage in CSR activities in

The present study gives an idea of ways of CSR implementation among Indian companies

therein among selected group of companies. An industry specific

research can be conducted to know the involvement of companies in various methods. A comparison

of implementation of CSR practices of companies across sector wise industries can also be done.

Another possible area for further research is comparison of implementation of CSR practices of

implementing the CSR in companies, e.g. conducting

research can also be done to

implementation of CSR practices by companies.

Harvard Business Review.

M., &Snidal, D. (2000). The

���� No-Level

���� II-Level

���� II-Level

���� II-Level

���� I-Level

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

17 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

[3] Ahrne, G., & Brunsson, N. (2011). Organization outside organizations: The significance of

partial organization. Organization, 18(1):83–104.

[4] Andre Nijhof, Theo deBruijn, & HakanHonders, (2008). Partnerships for corporate social

responsibility: A review of concepts and strategic options. Management Decision, 46

(1):152-167.

[5] Baumann-Pauly, D.,Wickert, C.,Spence, L. J., &Scherer, A. G. (2013). Organizing

corporate social responsibility in small and large firms: Size matters. Journal of Business

Ethics. 10.1007/s10551-013-1827-7.

[6] Bergen, A. and While, A. (2005). Implementation Deficit’ and ‘Street-level Bureaucracy’:

Policy, practice and Change in the Development of Community Nursing Issues, Health and

Social Care in the Community, 13(1): 1-10.

[7] Bondy, K., Moon, J., & Matten, D. (2012). An institution of corporate social responsibility

(CSR) in multi-national corporations (MNCs): form and implications. Journal of Business

Ethics, 111(2): 281–299.

[8] Boston College Center for Corporate Citizenship (2009). Corporate Citizenship (2009).

Retrieved from available at: www.csrwire.com/News/14396.html.

[9] Burchell, J., & Cook, J. (2013). CSR, co-optation and resistance: The emergence of new

agonistic relations between business and civil society. Journal of Business Ethics.

doi:10.1007/s10551-013-1830-z.

[10] Carroll, A.B. (1979).A three-dimensional conceptual model of corporate performance.

Academy of Management Review, 4(4): 497–505.

[11] Cordano, M. and I.H. Frieze (2000). Pollution Reduction Preferences of U.S. Environmental

Managers: Applying Ajzen’s Theory of Planned Behavior. Academy of Management

Journal, 43(4): 627-641.

[12] David Katamba, Charles TushabomweKazooba, SulaymanBabiihaMpisi, Cedric Marvin

Nkiko, Annet. K. Nabatanzi-Muyimba, Jean Hensley Kekaramu (2012). Corporate social

responsibility management in Uganda: Lessons, challenges, and Policy Implication.

International Journal of Social Economics, 39(6): 375-390.

[13] Garriga, E., &Mele´, D. (2004). Corporate social responsibility theories: Mapping the

territory. Journal of Business Ethics, 53(1): 51–71.

[14] Gond, J.-P., & Moon, J. (2011). Corporate social responsibility in retrospect and prospect.

In J.-P. Gond & J. Moon (Eds.), corporate social responsibility: A reader (pp. 1–28).

London: Routledge.

[15] Henry OgiriItotenaan, Martin Samy, Roberta Bampton(2014). A phenomenological study of

CSR policy making and implementation in developed countries: The case of The

Netherlands and Sweden. Journal of Global Responsibility, 5 (1): 138 - 159.

[16] Hung Woan Ting, BalaRamasamy, Lee Chew Ging (2010). Management systems and the

CSR engagement", Social Responsibility Journal, 6(3): 362-373.

[17] Husted, B. W. (2003). Governance choices for corporate social responsibility: To

contribute, collaborate or internalize? Long Range Planning, 36: 481–498.

[18] Jeffrey Avina, (2011) "Public-private partnerships in the fight against crime: An emerging

frontier in corporate social responsibility", Journal of Financial Crime, 18(3): 282-291.

[19] Matten, D., & Moon, J. (2008). ‘Implicit’ and ‘explicit’ CSR: A conceptual framework for a

comparative understanding of corporate social responsibility. Academy of Management

Review, 33(2): 404–424.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 6, Issue 1, January (2015), pp. 05-18 © IAEME

18 Madhu Bala, “A Comparative Study of Methods of CSR Implementation In Indian Context” – (ICAM 2015)

[20] Mohammad Safari Kahreh, Seyyed Mehdi Mirmehdi, AsgharEram, (2013). Investigating

the critical success factors of corporate social responsibility implementation: evidence from

the Iranian banking sector. Corporate Governance, 13 (2): 184 - 197.

[21] Moon, J. (2004). The institutionalization of business social responsibility: Evidence from

Australia and the UK. The Anahuac Journal (Mexico), 5(1): 40–54.

[22] Piercy, N. (2002). Market-Led Strategic Change: A Guide to Transforming the process of

Going to Market, Oxford: Butterworth-Heineman.

[23] Porter, M.E. & Kramer, M.R. (2006).Strategy & society: the link between competitive

advantage and corporate social responsibility. Harvard Business Review, 84(12): 56-68.

[24] PradeepUdhas & SaiVenkateshwaran (2013). Companies Act 2013: New Rules of the

Game, KPMG, Retrieved from

http://www.kpmg.com/IN/en/Documents/KPMG_Companies_Act_2013.pdf

[25] Roome, N. and Jonker, J. (2005). Whistling in the Dark’, ICCSR Research Paper Series 30,

Retrieved from: www.nottingham.ac.uk/business/iccsr/pdf/ResearchPdfs/30-2005.pdf

[26] Seitannidi, M.M. & A.M. Ryan (2007). A critical Review of Forms of Corporate

Community Involvement: from Philanthropy to Partnerships. International Journal of

Nonprofit and Voluntary Sector marketing, 12: 247-266.

[27] Simmons, C.J. & K.L. Becker-Olsen (2006).Achieving Marketing Objectives through

Social Sponsorships. Journal of Marketing, 70: 154-69.

[28] Strand, R. (2012). In praise of Corporate Social Responsibility bureaucracy. Copenhagen

Business School PhD Series 12: Copenhagen.

[29] Terje I. Vaaland, Morten Heide, (2008). Managing corporate social responsibility: lessons

from the oil industry. Corporate Communications: An International Journal, 13 (2):

212-225.

[30] vanHuijstee, M. M., Francken, M., & Leroy, P. (2007). Partnerships for sustainable

development: A review of current literature. Environmental Sciences, 4(2): 75–89.

[31] Votaw, D. (1973), “Genius becomes rare”, In D. Votaw& S. P. Sethi (Eds.) The corporate

dilemma. Englewood Cliffs, NJ: Prentice Hall.

[32] Waddock, S.A.(1988). Building Successful Partnerships. Sloan Management Review,

Summer, 17-23 Westley, F. and H. Vredenburg(1996). Sustainability and Corporation:

Criteria for Aligning Economic Practice with Environmental Protection. Journal of

Management Inquiry, 5(2): 104-119.

[33] P.Babu Rao and V.Balakrishnan, “CSR in a Public Sector Undertaking in India – A Case

Study”, International Journal of Management (IJM), Volume 1, Issue 2, 2010,

pp. 129 - 140, ISSN Print: 0976-6502, ISSN Online: 0976-6510.