2-1700 capital asset accounting

DESCRIPTION

TRANSCRIPT

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1700 CAPITAL ASSET ACCOUNTING.................................................................5

2-1701.00 Introduction...........................................................................................................52-1701.10 Assets not recorded in SABHRS.........................................................................52-1701.20 Objectives and benefits of property accounting..................................................6

2-1701.21 Capitalization thresholds (modified April 2010).................................................72-1701.22 Depreciable versus non-depreciable assets.........................................................72-1701.23 Infrastructure to use depreciation method...........................................................82-1701.24 Assets by fund type.............................................................................................82-1701.25 Asset balance sheet accounts...............................................................................82-1701.26 Additions, betterments, preservation versus maintenance and repair costs........9

2-1705.00 Definitions relating to assets (modified April 2010)...........................................9

2-1710.00 Responsibilities.....................................................................................................112-1710.10 Department of Administration (DOA)..............................................................11

2-1710.11 Responsibilities of the Accounting Bureau.......................................................112-1710.12 Responsibilities of the SABHRS Finance and Budget Bureau.........................112-1710.13 Responsibilities of the Property and Supply Bureau.........................................11

2-1710.20 Agency property coordinator.............................................................................122-1710.21 Duties of the agency property coordinator........................................................12

2-1710.30 Property officers................................................................................................122-1710.31 Duties of property officers................................................................................12

2-1715.00 Capital asset reported cost..................................................................................122-1715.10 Calculation of historical cost.............................................................................122-1715.20 Historical cost estimation procedures................................................................13

2-1715.21 Standard costing method...................................................................................132-1715.22 Price level index method...................................................................................132-1715.23 Price level indicators.........................................................................................132-1715.24 Estimation procedures.......................................................................................132-1715.25 Example - historical cost estimation.................................................................14

2-1720.00 General property management..........................................................................142-1720.10 Identification of property...................................................................................14

2-1720.11 Property tags......................................................................................................142-1720.12 Ordering tags.....................................................................................................152-1720.13 Affixing tags......................................................................................................152-1720.14 Control of unmissed tags...................................................................................152-1720.15 Sensitive equipment..........................................................................................152-1720.16 Expendable supplies..........................................................................................152-1720.17 Rental or leased equipment...............................................................................15

2-1720.20 Physical inventories...........................................................................................162-1720.21 Agency inventory plan......................................................................................162-1720.22 Missing tags or untagged items.........................................................................162-1720.23 Inspection of equipment....................................................................................17

1700-1

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1720.24 Reconciliation and adjustments.........................................................................172-1720.30 Asset characteristics..........................................................................................17

2-1720.31 Useful life and/or salvage value........................................................................172-1720.32 Asset class.........................................................................................................172-1720.33 Asset profile / salvage value / useful life / category / class table (modified April

2010)..................................................................................................................18

2-1730.00 Inventory (supplies, merchandise, etc.).............................................................282-1730.10 General information...........................................................................................292-1730.20 Accounting entries for recording inventories....................................................29

2-1730.21 Governmental fund entries................................................................................292-1730.22 Proprietary fund entries.....................................................................................292-1730.23 Surplus Property Fund inventory entries...........................................................302-1730.24 Livestock inventory entries...............................................................................30

2-1740.00 Asset accounting general discussion..................................................................312-1740.10 Accounting for capital assets.............................................................................31

2-1740.11 Assets to be recorded in the entitywide ledger..................................................312-1740.12 Assets to be recorded in the actuals ledger........................................................312-1740.13 Accounting for expensed assets........................................................................31

2-1740.20 Purchase of split funded assets..........................................................................312-1740.21 Examples of split funded asset..........................................................................31

2-1750.00 Recording capital asset related expenses...........................................................322-1750.10 Capital asset cost budgeted in a range other than the capital outlay expense

level...................................................................................................................322-1750.11 Example of internally developed software costs...............................................322-1750.12 Result for GAAP financial statements..............................................................332-1750.13 Correction needed by agency............................................................................33

2-1750.20 Budgeted capital outlay expense that won’t be capitalized...............................332-1750.21 Example of building construction costs............................................................332-1750.22 Result for GAAP financial statements..............................................................342-1750.23 Correction needed by agency............................................................................34

2-1750.30 List of accounts used to offset budgeted expenses for GAAP reporting...........34

2-1760.00 General asset accounting structure and procedures........................................352-1760.10 Things to remember about AM.........................................................................35

2-1760.11 Reminders when adding assets to AM..............................................................352-1760.12 AM generated journals......................................................................................362-1760.13 Changing the useful life or salvage value of an asset (modified April 2010)...362-1760.14 Changing the historical cost of an existing asset...............................................372-1760.15 General ledger cleanup required when you retire/add the same asset on AM. .37

2-1760.20 Recording land, buildings and construction work-in-progress..........................382-1760.30 Purchase of capital assets..................................................................................39

2-1760.31 Recording purchase of capital assets.................................................................392-1760.32 Adding capital assets to AM.............................................................................392-1760.33 Capital asset entries...........................................................................................39

1700-2

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

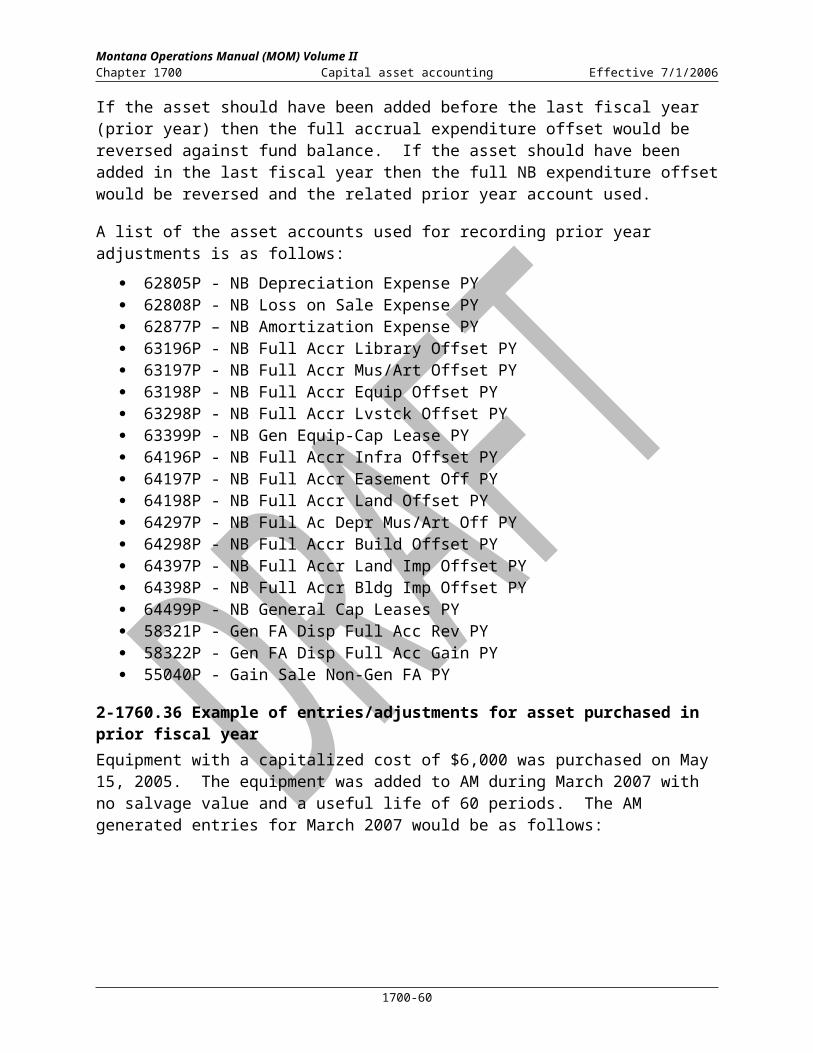

2-1760.34 Capital asset entries (asset purchased in prior period month)...........................402-1760.35 Adjustments in regard to an asset purchased in a prior fiscal year...................402-1760.36 Example of entries/adjustments for asset purchased in prior fiscal year..........41

2-1760.40 Gifts/donated assets...........................................................................................422-1760.41 Gift/donated asset accounting entries................................................................42

2-1760.50 Recording intangible assets (modified April 2010)...........................................422-1760.51 Recording intangible assets not completed at year-end....................................432-1760.52 Capitalizable software (modified April 2010)...................................................432-1760.53 Adding intangibles to AM (modified April 2010)............................................452-1760.54 Recording purchase of intangible asset.............................................................452-1760.55 Intangible asset entries subject to amortization.................................................452-1760.56 Intangible asset entries when asset completed/purchased in prior period month

...........................................................................................................................452-1760.57 Adjustments in regard to an asset completed/purchased in a prior fiscal year..462-1760.58 Example of entries/adjustments for asset purchased in prior fiscal year

(modified April 2010).......................................................................................462-1760.59 Easements and other Land Use Rights (modified April 2010).........................47

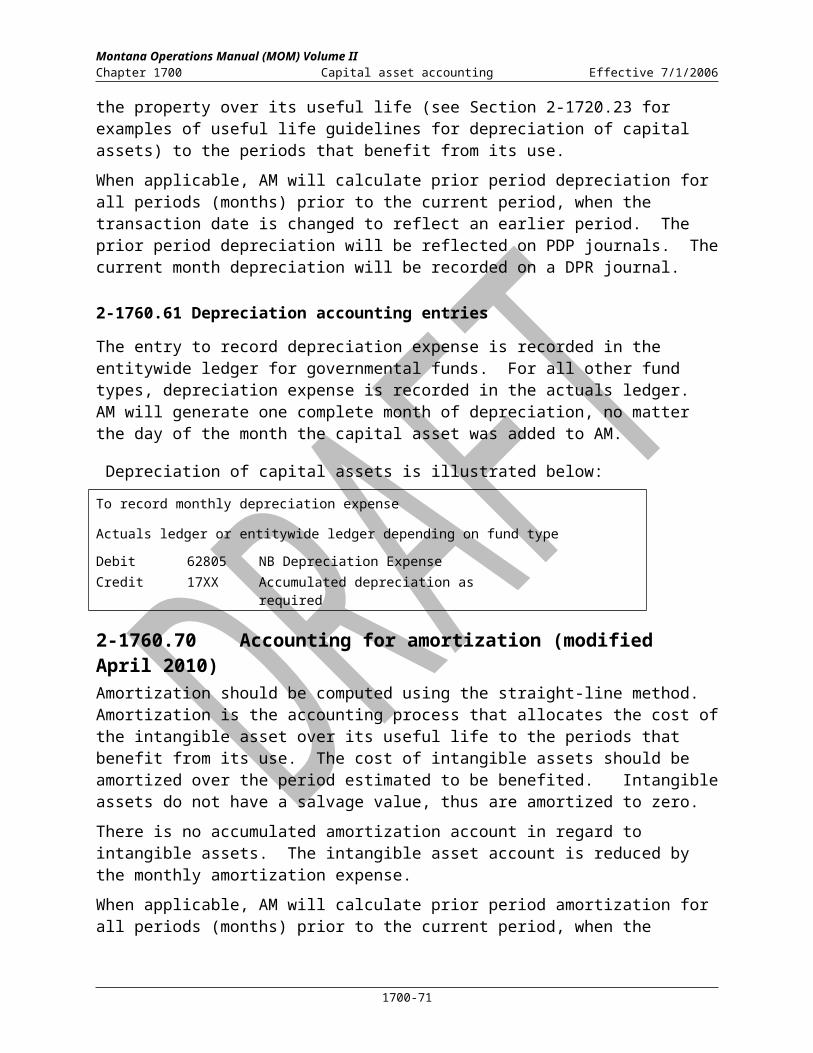

2-1760.60 Accounting for depreciation..............................................................................472-1760.61 Depreciation accounting entries........................................................................48

2-1760.70 Accounting for amortization (modified April 2010).........................................482-1760.71 Amortization accounting entries.......................................................................48

2-1760.80 Transfer of capital assets...................................................................................482-1760.81 Asset transferred is fully depreciated without a salvage value.........................492-1760.82 Asset is fully depreciated with a salvage value or not fully depreciated..........492-1760.83 Asset transferred with monetary compensation to the transferor fund.............51

2-1760.90 Construction work-in-progress (CWIP)............................................................512-1760.91 Manufactured locally.........................................................................................522-1760.92 A&E appropriated.............................................................................................522-1760.93 Agency appropriated.........................................................................................532-1760.94 Accounting entries to add CWIP.......................................................................532-1760.95 Accounting entries to add completed capital asset............................................54

2-1770.00 Disposition of property........................................................................................542-1770.10 Sale of property.................................................................................................55

2-1770.11 Sale of property – surplus property entries.......................................................552-1770.20 Trade-in of property...........................................................................................55

2-1770.21 Trade-in with a loss...........................................................................................562-1770.22 Trade-in of asset when fair market value is greater than the book value of the

exchanged asset (boot paid or no boot involved)..............................................572-1770.23 Trade-in of asset when fair market value is greater than the book value of the

exchanged asset (boot received)........................................................................582-1770.30 Junked property.................................................................................................592-1770.40 Lost, stolen, or destroyed property....................................................................60

2-1780.00 Lease/installment purchases...............................................................................60

2-1790.00 Asset impairment.................................................................................................60

1700-3

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1790.10 Identifying potential impairments.....................................................................612-1790.20 Testing for the impairment................................................................................612-1790.30 Measuring the impairment of capital assets......................................................63

2-1790.31 Asset no longer used, construction and/or development stoppage....................632-1790.32 Asset will continue to be used...........................................................................632-1790.33 Restoration cost approach.................................................................................642-1790.34 Example of the restoration cost approach.........................................................652-1790.35 Service units approach.......................................................................................652-1790.36 Example of service units approach....................................................................652-1790.37 Deflated depreciated replacement cost approach..............................................652-1790.38 Example of deflated depreciated replacement cost approach...........................65

2-1790.40 Insurance recoveries..........................................................................................662-1790.41 Insurance recoveries in modified accrual funds................................................662-1790.42 Insurance recoveries in full accrual funds.........................................................66

2-1790.50 Recording impairment write-down in a modified accrual fund........................662-1790.51 Insurance proceeds realized or realizable in the same year the impairment

write-down is recorded......................................................................................672-1790.52 Insurance proceeds realized or realizable in a year subsequent to the

impairment write-down.....................................................................................682-1790.60 Recording impairment write-down in a full accrual fund.................................69

2-1790.61 Insurance proceeds realized or realizable in the same year the impairment write-down is recorded......................................................................................69

2-1790.62 Insurance proceeds realized or realizable in a year subsequent to the impairment write-down.....................................................................................70

2-1790.70 Replacement or repair costs of the impaired asset............................................712-1790.80 Other asset impairment topics...........................................................................71

2-1790.81 Temporary impairments....................................................................................712-1790.82 Assets impaired prior to implementation of GASB Statement No. 42.............712-1790.83 Disclosure of asset impairment.........................................................................72

1700-4

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1700 Capital asset accounting

2-1701.00 IntroductionThe asset management system (AM) is an integrated module of the Statewide Budgeting Accounting and Human Resource System (SABHRS) used to manage and account for the State of Montana's investment in all capital assets: property, plant, and equipment. This includes intangible assets that meet the capitalization threshold. All agencies are required to use AM, except the Higher Ed Units, which maintain their capital assets on a BANNER asset subsystem similar to asset management. The capital asset balances for the Higher Ed Units are posted to the general ledger module of SABHRS through an interface process.

As a subsystem of SABHRS, AM provides general ledger accounting in SABHRS and property subsidiary detail in AM. To facilitate full disclosure in SABHRS financial reports, this chapter is in agreement with guidelines set forth by the GASB (Governmental Accounting Standards Board).

In addition to providing asset detail, AM provides information to conduct regular asset inventories as well as depreciation/amortization schedules for all funds. AM incorporates the ability to perform inventories using barcode scanners and to print barcode labels to use as asset tags.

Each capital asset item is assigned a property number and a corresponding property tag is affixed thereto, as appropriate. Section 2-1720.20 includes procedures for the taking of an inventory upon implementation of AM and periodic physical inventories thereafter.

The assets are generally recorded in the fund(s) that purchased the assets. When reconciling assets, the related reports or queries must be ran using the correct fund and ledger combination. It is also important to reconcile both the governmental and proprietary fund assets to the general ledger. All assets are now included in the State of Montana’s general purpose financial statements and should be in the scope of the independent auditor’s audit process. This will be discussed further in the accounting methods section.

2-1701.10 Assets not recorded in SABHRSThose agencies maintaining a more detailed capital asset system must submit summary totals at fiscal year-end to affect AM. These summary entries must include total increases and total decreases for the year (i.e., not a net increase or net decrease) by fund.

Agencies must receive Department of Administration approval prior to using systems other than AM to maintain their capital asset detail. An example of a system maintaining more detailed information relating to capital assets is the Department of Transportation’s Land and Right of Way system.

In addition to recording assets on BANNER, the State of Montana universities have chosen to maintain the fund structure and accounting methods used prior to GASB 34. The funds and accounts used for these transactions on the university BANNER systems are posted in total to SABHRS; the related accounting entries are not presented in this chapter. However, the university systems are required to follow the general accounting guidance contained in this chapter.

1700-5

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1701.20 Objectives and benefits of property accountingIn the following sections, instructions for real and personal property asset accounting on a uniform statewide basis are detailed. The importance of complete and accurate accounting cannot be overemphasized. Adequate accounting procedures and records are essential for the protection of State of Montana property. The responsibilities of stewardship involved in safeguarding such a large public investment are of the utmost importance to sound financial administration. This responsibility can be more effectively discharged through adequate property accounting.

In addition to protective custody of the State of Montana's property, a system of property accounting permits the assignment of responsibility for custody and proper use of specific property with individual public officials. Such a system also makes possible the provision of data essential to the proper management of property. This includes such information as type of assets, location, cost, funding source and useful life.

Finally, an accounting of property is a prerequisite to the preparation of satisfactory and complete financial reports. An annual financial report of a governmental unit without complete and accurate property information does not meet the objective of full disclosure and, to that extent, is deficient.

Adherence to the guidelines contained in this chapter will provide:

Property records, if properly maintained, that furnish information about the investment taxpayers and others have made for the future benefit to users of government property. This should be contrasted with expenditures for current purposes.

A basis for adequate insurance coverage on insurable assets. Although cost is not the only determinant of insurable value, it is a necessary consideration.

The ability to identify worn-out or obsolete equipment on a concurrent basis. Provision for replacement can be included in a budget before emergency replacement or unwarranted repairs are necessary.

Information necessary to perform regular inventories to determine physical condition, theft, or unauthorized transfers.

Reliable information about assets now owned. Because capital budgets are best developed on a long-term basis, such information is invaluable in projecting future requirements.

Assistance in maintaining accountability for the custody of individual items and in determining who is responsible for their care and maintenance.

The ability to centralize property management, either statewide or within an agency, so that location is readily determinable for physical control. This should also alleviate the problem of excess equipment in one department while a shortage of like equipment exists in another department. It will also help to avoid unwarranted purchases of duplicate equipment.

Comprehensive asset records for all funds to use as a basis for computing depreciation or amortization.

2-1701.21 Capitalization thresholds (modified April 2010)In general, all State of Montana agencies are required to capitalize tangible and intangible assets if an item's unit cost meets or exceeds the capitalization threshold. Capital assets consist of

1700-6

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

assets of a relatively permanent nature with a useful life of more than one year. Items costing less than the capitalization threshold must be expensed in the year of purchase.

Individual collections or land items may consist of individual items less than the capitalization limit if the total collection value exceeds the capitalization limit. Software license purchases should be capitalized if the aggregate purchase price, not the individual price per license, is greater than the capitalization threshold.

The State of Montana’s capitalization thresholds are as follows:

Asset Type Threshold

Equipment 5,000

Land 5,000

Library Materials 5,000

Museum & Art 5,000

Museum & Library Collections 5,000

Other Assets 5,000

Land Improvements 25,000

Buildings 25,000

Building Improvements 25,000

Land Use Rights 100,000

Land Use Rights – Permanent 100,000

Other Intangibles 100,000

Software - Purchased 100,000

Infrastructure 500,000

Software – Internally Generated 500,000

The capitalization thresholds listed above will be used because the cost of keeping dollar value records of most items costing less than these amounts usually exceeds the value of the benefits received. All other property is expensed in the year that it is purchased.

If an intangible asset type’s capitalization threshold has increased, and an intangible asset has already been capitalized under the previous capitalization threshold, the intangible asset should remain a capital asset and continue to be amortized for the remainder of its useful life. The capitalization thresholds increased from $5,000 to $100,000 and $500,000 for land use rights and purchased or internally generated software respectively in fiscal year 2010.

For accountability purposes, applicable agencies are encouraged to utilize AM to keep records detailing expensed property, especially items that are sensitive to theft, i.e., laptop computers, cell phones, and guns.

2-1701.22 Depreciable versus non-depreciable assetsLand, construction work in progress, museum and art collections, library collections, and easements are not depreciable. Per GASB 34, capitalized museum and art collections or individual items are not depreciable if all the following conditions are met in regard to the collections or items:

Held for public exhibition, education, or research in furtherance of public service, rather than financial gain

1700-7

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Protected, kept unencumbered, cared for, and preserved Subject to an organizational policy that requires the proceeds from sales of collection

items to be used to acquire other items for collections.

All other capital assets that meet the capitalization threshold are required to be depreciated or amortized using the straight-line depreciation method. This requirement is for both Governmental and Proprietary assets.

2-1701.23 Infrastructure to use depreciation method Infrastructure is required to be capitalized at its historical cost and depreciated over its useful life.

Under GASB 34 the state agencies must, at a minimum, retroactively report major capital assets that were acquired in fiscal years ending after June 30, 1980. Major general infrastructure is defined as either a subsystem or network for which the related cost or estimated cost is expected to be 5% or 10% of the total cost of all general assets reported for fiscal year 1999. For this calculation state agencies should use $54,000,000 as the 10% threshold and $27,000,000 for the 5% threshold. This threshold is only applicable to adding assets not already on Asset Management.

2-1701.24 Assets by fund typeGovernmental assets are assets, which are purchased by any governmental fund, i.e., all funds except for 06XXX, 065XX, 07XXX, 086XX and 095XX funds. Governmental assets are found in the entitywide ledger of the general ledger.

Proprietary assets are assets, which are purchased by any proprietary fund, i.e., all 06XXX, 065XX, 086XX and 095XX funds. Proprietary assets are found in the actuals ledger of the general ledger.

Agency funds (07XXX) should only be used to report resources held by the State of Montana in a purely custodial capacity. Therefore, no assets should ever be reported in agency funds on AM.

2-1701.25 Asset balance sheet accountsThe following is a list of the balance sheet accounts used in regard to capital assets and their related depreciation accounts, if required:

1701 Land 1702 Buildings 1703 Building Improvements 1704 Equipment 1705 Other Capital asset 1706 Construction Work In Progress 1707 Accum Depr – Buildings 1708 Accum Depr - Bldg Improvements 1709 Accum Depr – Equipment 1710 Accum Depr - Other FA 1711 Livestock

1700-8

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

1712 Easements 1713 Library Books 1714 Museum and Art 1715 Land Improvements 1716 Infrastructure 1718 Library Collections 1719 Museum and Art Depreciable 1720 Accum Depr Land Improvements 1721 Accum Depr Infrastructure 1722 Accum Depr Museum and Art 1723 Accum Depr Library Books 1809 Intangible Asset

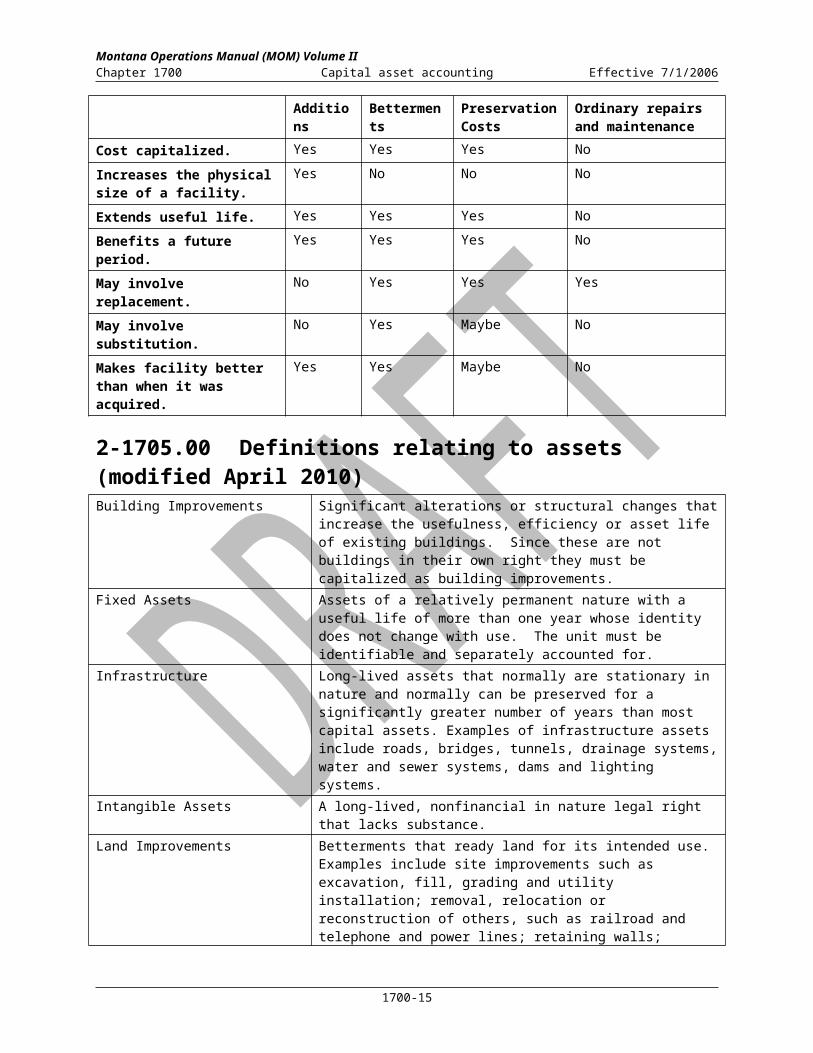

2-1701.26 Additions, betterments, preservation versus maintenance and repair costsPreservation costs are those costs that extend the useful life of an asset beyond its original estimated useful life, but do not increase the capacity or efficiency of the asset.

The table below summarizes the similarities and distinctions for additions, betterments, and repairs and maintenance.

Additions Betterments Preservation Costs

Ordinary repairs and maintenance

Cost capitalized. Yes Yes Yes No

Increases the physical size of a facility.

Yes No No No

Extends useful life. Yes Yes Yes No

Benefits a future period. Yes Yes Yes No

May involve replacement. No Yes Yes Yes

May involve substitution. No Yes Maybe No

Makes facility better than when it was acquired.

Yes Yes Maybe No

2-1705.00 Definitions relating to assets (modified April 2010)Building Improvements Significant alterations or structural changes that increase the

usefulness, efficiency or asset life of existing buildings. Since these are not buildings in their own right they must be capitalized as building improvements.

Fixed Assets Assets of a relatively permanent nature with a useful life of more than one year whose identity does not change with use. The unit must be identifiable and separately accounted for.

Infrastructure Long-lived assets that normally are stationary in nature and normally can be preserved for a significantly greater number of years than most capital assets. Examples of infrastructure assets include roads, bridges, tunnels, drainage systems, water and sewer systems, dams and lighting systems.

Intangible Assets A long-lived, nonfinancial in nature legal right that lacks substance.

Land Improvements Betterments that ready land for its intended use. Examples include site improvements such as excavation, fill, grading and utility

1700-9

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

installation; removal, relocation or reconstruction of others, such as railroad and telephone and power lines; retaining walls; parking lots; fencing; and landscaping.

For example, if a house and land are purchased and the house razed immediately then the cost of the land, house, any land improvements and the demolition costs would be included as the cost of the land. If the house remains standing and is used for state purposes or as rental property until it is razed sometime in the future the house and land components (if material) should be estimated and capitalized separately. The house will then be depreciated until it is demolished sometime in the future. When the house is demolished the demolition costs will become part of the cost of the land.

Land Use Right A legal right to use conservation easements and right-a-ways, as well as minerals, timber, and water.

Major Property Property items having a normal useful life of one year or more (including extended life due to repairs), an identity which does not change with use (i.e. retains its identity throughout its useful life), is identifiable and separately accounted for, and has a unit cost greater than the capitalization threshold.

Minor Property Property items having a normal useful life of one year or more, an identity which does not change with use, is identifiable, can be separately accounted for, and has a unit cost of less than the capitalization threshold.

Network of Assets All assets that provide a particular type of service for a government. A network of infrastructure assets may be only one infrastructure asset that is composed of many components. For example, a network of infrastructure assets may be a dam composed of a concrete dam, a concrete spillway and a series of locks.

Other Capitalized Assets All assets that meet the definition of major property not in another asset type. For example, this category could include livestock.

Other Intangibles All intangible assets that meet the definition of an intangible asset not in another intangible asset type. Examples are copyrights, patents and trademarks.

Software – Purchased Commercially available software that is purchased or licensed with little or no modifications necessary before being put into operation.

Software – Internally Generated Software developed in-house or by a third-party contractor on behalf of the organization. Also includes commercially available software that is modified using more than minimal effort before being put into operation.

Subsystem of a Network of Assets All assets that make up a similar portion or segment of a network of assets. For example, all the roads of a government could be considered a network of infrastructure assets. Interstate highways, state highways and rural roads could each be considered a subsystem of that network.

Supplies and Materials Consumable commodities purchased for inventory or immediate consumption; articles and commodities, which are consumed or materially altered when used; and software and fixed assets with a unit cost of less than the capitalization threshold. This may include operating supplies, office supplies, and small tools (Expenditure accounts 622XX).

Works of Art and Historical Works of art and historical treasures (including related collections)

1700-10

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Collections will be capitalized as required under GASB 34 para 27 through 29 and note 22. These will be capitalized by the state and are not depreciable. Capitalized collections or individual items that are “exhaustible such as exhibits whose useful lives are diminished by display or educational or research activities will be depreciated.” A separate depreciable category and related accounts have been established for this activity.

2-1710.00 Responsibilities

2-1710.10 Department of Administration (DOA)Section 17-1-102 (2) MCA, provides that the Department of Administration “shall prescribe and install a uniform accounting and reporting system for all state agencies and institutions, reporting the receipt, use and disposition of all public money and property in accordance with generally accepted accounting principles”.

Statewide administration of AM is divided within the Department of Administration, between the Accounting Bureau, the SABHRS Finance and Budget Bureau and the Property and Supply Bureau.

2-1710.11 Responsibilities of the Accounting Bureau 1. Issue related accounting policy and development of procedures.2. Work with agencies and SABHRS to insure AM complies with GAAP.3. Provide primary helpdesk support.4. Assist with report and query development.5. Assist with the correction of system deficiencies.

2-1710.12 Responsibilities of the SABHRS Finance and Budget Bureau 6. Maintenance of AM.7. Work with DOA Accounting Bureau and PeopleSoft to correct system deficiencies.8. Run monthly AM processes.9. Develop reports and public queries.10. Correct system deficiencies.

2-1710.13 Responsibilities of the Property and Supply Bureau11. Coordinate disposal of surplus property for agencies.12. Dispose of surplus property.13. Provide agencies with notification that the surplus process has been completed.

2-1710.20 Agency property coordinatorAgencies are to designate an agency property coordinator who will serve as the liaison with the DOA Accounting Bureau in carrying out duties assigned relative to property management and to assure the exchange of administrative information between the DOA Accounting Bureau and the agency. Agencies must notify the DOA Accounting Bureau of the individual designated as the agency's property coordinator.

1700-11

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1710.21 Duties of the agency property coordinator14. Timely and accurate entry of asset information into SABHRS. This entry should be

performed as assets are received. The entries should, at a minimum, be made on a monthly basis, and not be accumulated until fiscal year-end.

15. Analysis of asset balances and information and correction of data accordingly.16. Assign responsibility for property matters to property officers within the agency.17. Assign responsibility for the physical inventory of property to personnel within the

agency.18. Assign responsibility for the coordination of surplus equipment.19. Control and distribute of property tags.

2-1710.30 Property officersThe number of property officers within each agency will be designated by the agency property coordinator, with the approval of the agency director, considering such factors as the size and organizational structure of the agency, geographical locations and number of property items.

In general, the property officer should be the individual having direct supervision over the persons using the property, (e.g., the foreman in a carpenter shop, the accounting supervisor in an accounting office, etc.).

2-1710.31 Duties of property officers20. Ensure the proper use and maintenance of property.21. Promptly report any property loss, misuse of property or any condition requiring repair

or which creates a hazardous working condition.22. Responsible for the assignment of property within their area of responsibility.23. Responsible for the tagging of property within their area of responsibility.

2-1715.00 Capital asset reported costCapital assets should be reported at their historical cost (after any cash discounts). In the absence of historical cost information, the asset’s estimated historical cost may be used. Assets donated by discretely presented component units or by parties outside the financial reporting entity should be reported at their fair value on the date the donation is made. When capital assets are moved from one fund to another, the recipient fund should continue to report those assets at their historical cost as of the date they were acquired by the primary government.

2-1715.10 Calculation of historical costThe historical cost of a capital asset should include all of the following:

24. Ancillary charges necessary to place the asset in its intended location (for example, freight charges).

25. Ancillary charges necessary to place the asset in its intended condition for use (for example, installation and site preparation charges).

26. Capitalized interest on debt incurred during the construction phase of a project. This is only applicable for debt issued in enterprise funds for a project that will be paid for out of enterprise funds.

1700-12

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

The historical cost of a capital asset should include the cost of any subsequent additions or improvements but exclude the cost of repairs. An addition or improvement, unlike a repair, either enhances a capital asset’s functionality (effectiveness or efficiency), or it extends a capital asset’s expected useful life.

If additional costs need to be added to an asset’s historical cost, they should be added as a separate asset on AM and linked to the original asset using the parent/child functionality.

2-1715.20 Historical cost estimation proceduresWhen the historical cost of capital assets is no longer available, the estimated historical cost can be calculated by using either the standard costing method or the price level index method. In either case once calculated, the estimated historical cost of the capital asset would need to be reduced by an appropriate amount of accumulated depreciation/amortization. This is accomplished in AM by changing the transaction date to correspond to the actual in-service date of the asset when it is added.

2-1715.21 Standard costing methodStandard costing involves using historical sources, such as sales catalogs or advertisements, to establish the average cost of obtaining the same or similar assets. In addition, the standard costing method could use a quote from a manufacturer as to the cost at the time of purchase.

2-1715.22 Price level index methodThe price level index method deflates the current cost of the same or similar asset using an appropriate price index.

2-1715.23 Price level indicatorsAnnual price levels are measured in terms of the Gross National Product Implicit Price Deflators (GNP Deflators) for government purchases of goods/services. GNP Deflators can be found at the following website.

http://www.bea.gov/bea/dn/nipaweb/SelectTable.asp?Selected=N

2-1715.24 Estimation proceduresThe following steps are used in converting the current cost of purchasing an asset at today's prices into the estimated historical cost of a capital asset:

27. Calculate the conversion factor by determining the deflator prevailing when the capital asset was acquired and dividing it by the current year GNP Deflator.

28. Calculate the estimated historical cost by multiplying capital asset cost times the conversion factor determined in step 1.

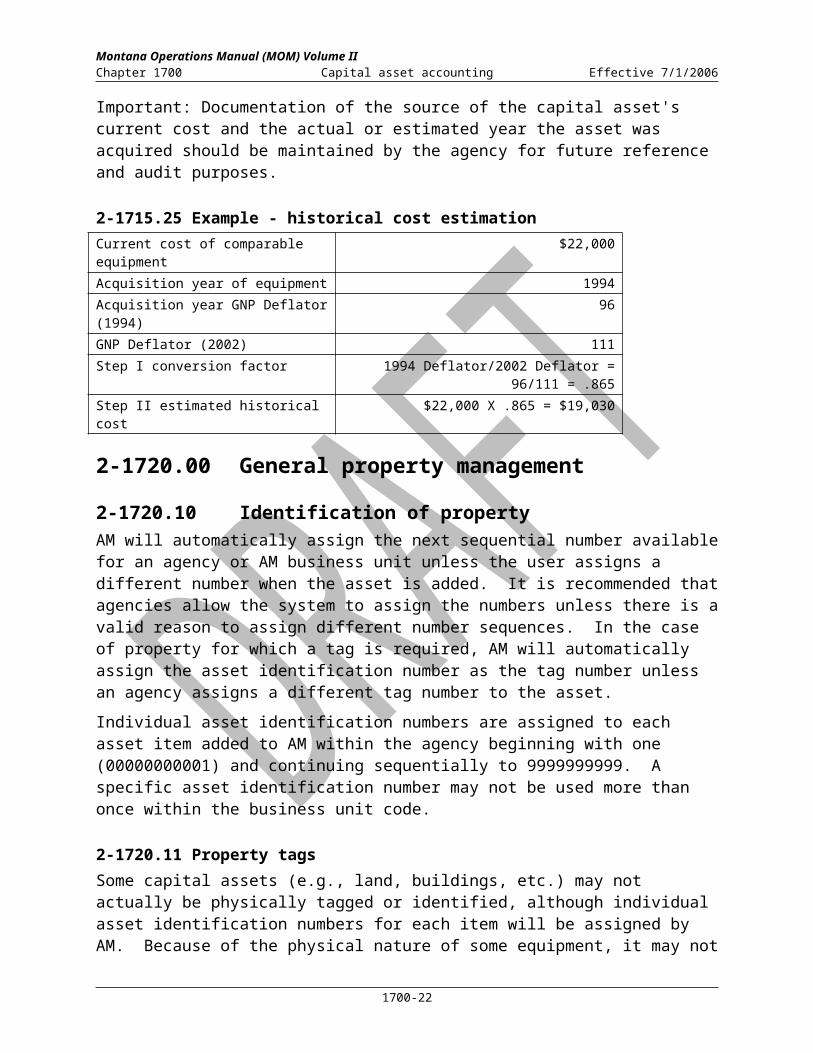

Important: Documentation of the source of the capital asset's current cost and the actual or estimated year the asset was acquired should be maintained by the agency for future reference and audit purposes.

1700-13

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1715.25 Example - historical cost estimationCurrent cost of comparable equipment $22,000

Acquisition year of equipment 1994

Acquisition year GNP Deflator (1994) 96

GNP Deflator (2002) 111

Step I conversion factor 1994 Deflator/2002 Deflator = 96/111 = .865

Step II estimated historical cost $22,000 X .865 = $19,030

2-1720.00 General property management

2-1720.10 Identification of propertyAM will automatically assign the next sequential number available for an agency or AM business unit unless the user assigns a different number when the asset is added. It is recommended that agencies allow the system to assign the numbers unless there is a valid reason to assign different number sequences. In the case of property for which a tag is required, AM will automatically assign the asset identification number as the tag number unless an agency assigns a different tag number to the asset.

Individual asset identification numbers are assigned to each asset item added to AM within the agency beginning with one (00000000001) and continuing sequentially to 9999999999. A specific asset identification number may not be used more than once within the business unit code.

2-1720.11 Property tagsSome capital assets (e.g., land, buildings, etc.) may not actually be physically tagged or identified, although individual asset identification numbers for each item will be assigned by AM. Because of the physical nature of some equipment, it may not be feasible to affix one of the standard tags. However, whenever possible, the tag number will still be identified on the item by some means such as etching, decal, indelible ink, etc.

Where possible, property tags should conform to the following specifications:

29. Tags shall contain the description "State of Montana"30. Tags shall contain the responsible agency name.31. They can be numbered from 00000000001 to 99999999999.

Non-numbered tags can be ordered. These can be used to replace missing numbered tags by typing the tag number directly on the property tag. Barcode labels used in place of metal tags must contain the same information noted above.

Departments that have established identifying and tagging procedures that meet or exceed the above specifications will be allowed to retain their property tags.

2-1720.12 Ordering tagsAgency property coordinators should contact the Department of Administration Property and Supply Bureau for instructions on ordering property tags.

1700-14

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1720.13 Affixing tagsAll major equipment (equipment meeting the capitalization threshold) should be identified in the manner that promotes easy identification. At the agencies discretion, minor equipment should have a property tag attached. Property tags should be placed in plain sight on the equipment, but in such a manner so as not to interfere with the operation of the equipment or be easily removed during the use of the equipment as physical conditions permit.

Any manufacturer's mark and/or serial number should remain exposed and intact in order to expedite repair and facilitate the maintenance of service records.

2-1720.14 Control of unmissed tagsProper control must be exercised over the issuance of property tags. An example of a format to record the information necessary to control the issuing of tags is shown below:

PROPERTY TAG CONTROL SHEET DEPARTMENT OF ABC

FOR TAG NUMBERS: through

Tag Number(s) Date Issued Issued By Issued To

2-1720.15 Sensitive equipmentAgencies must track, and inventory sensitive items with a cost under the capitalization limit. Examples of sensitive items include personal computers, laptops, cameras, spotting scopes, firearms, etc. If possible, these items must be tagged in the same manner as capital equipment. It is recommended these be added to AM as expensed assets for inventory control purposes.

2-1720.16 Expendable suppliesExpendable supplies, to the extent considered necessary, will be identified and marked in an appropriate manner that will identify them as belonging to a specific agency of the State of Montana. Examples: (1) wood handled tools can be marked by branding, stamping with a dye or by distinctive paint marks; (2) cloth items, such as sheets, blankets, and mattresses, can be stenciled.

2-1720.17 Rental or leased equipmentA property tag or decal that can be removed later without defacing the equipment should be affixed to rented or leased equipment to distinguish them from State of Montana property and to assure their proper care and return.

2-1720.20 Physical inventoriesAn agency must take a complete physical inventory of all capital assets, tagged minor equipment, and sensitive equipment using either the inventory listing available from either an asset management system or an automated barcode scanner process. At a minimum, this inventory must be taken every two years.

1700-15

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1720.21 Agency inventory planThe agency property coordinator will designate personnel or work with agency management to obtain personnel who are to take the inventory. The custodian of the property records or the person to whom the capital assets have been assigned should not exclusively control the inventory. Property records should be utilized whenever possible to assist in locating capital asset items. Inventories should be taken progressively from one small area to another (e.g., a building, one floor at a time, room by room). All capital assets, tagged minor equipment, and sensitive equipment should be included in the inventory.

Personnel conducting a manual inventory should record all data possible on the inventory by location report to be utilized in the update of the asset management system for individual capital asset items.

Upon completion of the capital asset inventory, the asset management system should be updated and accounting entries recorded on SABHRS, when appropriate. Inventory records must be retained in the agency files. Additional documents related to individual property items should be filed with the inventory records.

The frequency of a physical inspection and inventory of all capital assets will be determined by each agency's inventory system. If an agency has a perpetual capital asset inventory system where the records are updated every time a capital asset is purchased or disposed of, a physical inventory need only be taken once every two years. If the agency does not have a perpetual inventory system, a physical inventory must be performed every year near June 30. The annual inventory will insure that the capital assets recorded on asset management at fiscal year-end are correctly stated. A physical inventory should be taken to coincide with the June 30 fiscal year-end.

While taking inventories, it may be desirable to prepare separate listings of minor, expendable, rental or leased equipment for which tagging or other identification is considered necessary.

2-1720.22 Missing tags or untagged itemsWhile the physical inventory of capital assets is being conducted, attention should be directed to any capital assets without tags. It is possible that the item's original tag is missing or that it was not initially tagged. Sufficient information should be noted so that a research of property records can determine if the item needs to be tagged or retagged.

If the untagged item is on the inventory list correctly and a new tag number is given to that asset, no adjustment is needed to the asset management system other than noting of the new tag number.

2-1720.23 Inspection of equipmentEquipment should be inspected during inventories to determine its condition and the appropriate condition code entered on the inventory listing.

If the personnel conducting the inventory suspect that replacement or extensive repairs may be necessary, it should be reported to the custodian of the asset and the agency property coordinator.

1700-16

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1720.24 Reconciliation and adjustmentsCapital assets disclosed by the physical inventory should agree with the items as listed on the inventory list. Discrepancies must be thoroughly investigated and reported to the agency property coordinator. Any necessary write-offs because of missing capital assets should be documented and submitted to the Legislative Audit Division and the Attorney General. The Report of Property Survey form may be used for this. It is available at the following address:

http://accounting.mt.gov/accountingformsinfo.mcpx

Upon completion of the physical inventory, all necessary adjustments should be made to the asset management system to accurately reflect capital asset totals. If the item was found not to have been included on the asset management inventory list, then the asset must be added to asset management. In SABHRS, the transaction date must be changed to properly reflect in-service date of the asset.

2-1720.30 Asset characteristics

2-1720.31 Useful life and/or salvage valueThe useful life and salvage value of an asset is defined based on the Profile ID as designated on AM. The useful life and/or the salvage value of an asset can be changed in certain circumstances. Reasons to adjust the useful life and/or salvage value of an asset could include, but is not limited to, experience with similar assets or a need to meet federal depreciation/amortization allowance guidance. Supporting documentation for determining the estimated useful lives of fixed assets would be engineering studies, actual experience documented in the records of similar assets, etc. Agencies may also be required to follow the useful lives identified by third party regulators such as those specified by the American Hospital Association Depreciation Guide. Any change of the useful life and/or salvage value of an asset should be documented and maintained by each agency. The useful life of an asset is expressed in periods (months) on AM.

2-1720.32 Asset classIn AM, a five-digit number has been assigned to the various classes of property as listed below. The first two digits represent the classification of property and the next three digits represent the type of property within the classification. Agencies must include a class type to each asset as it is added to AM. The class type is not defaulted into the asset as part of the profile. This is also not a system-required field because it is not available in some AM panels. However, this field is required by State of Montana policy on AM panels that it appears on.

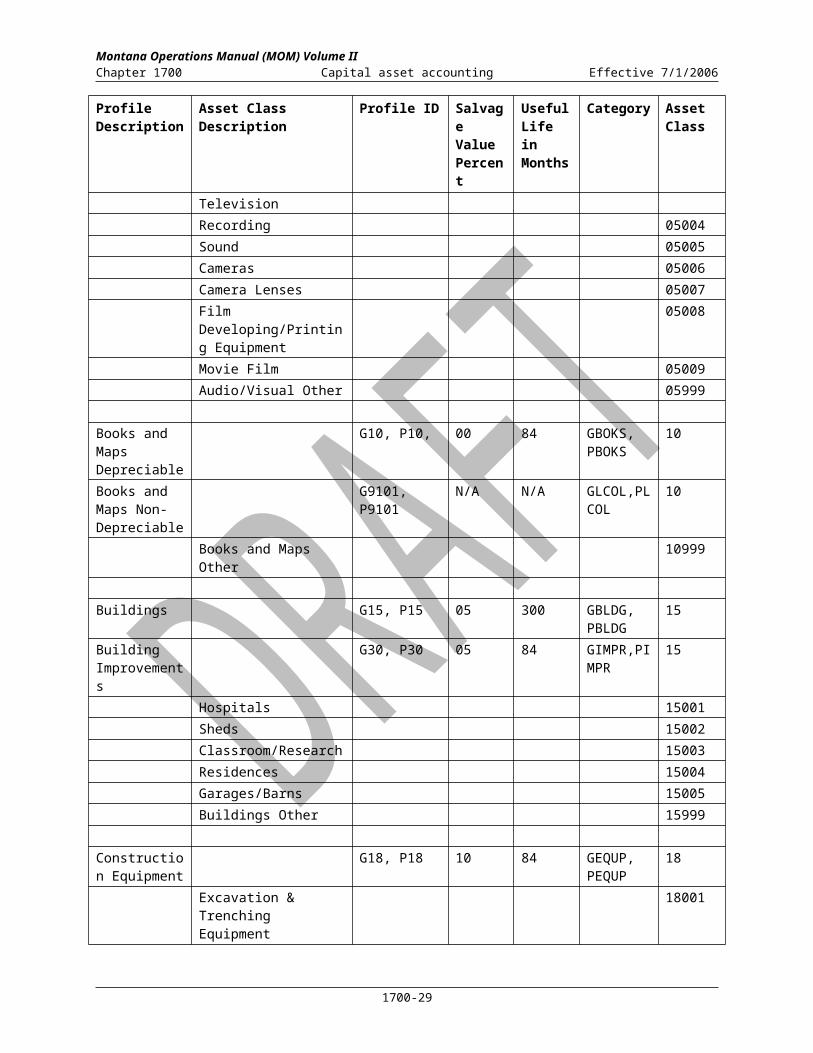

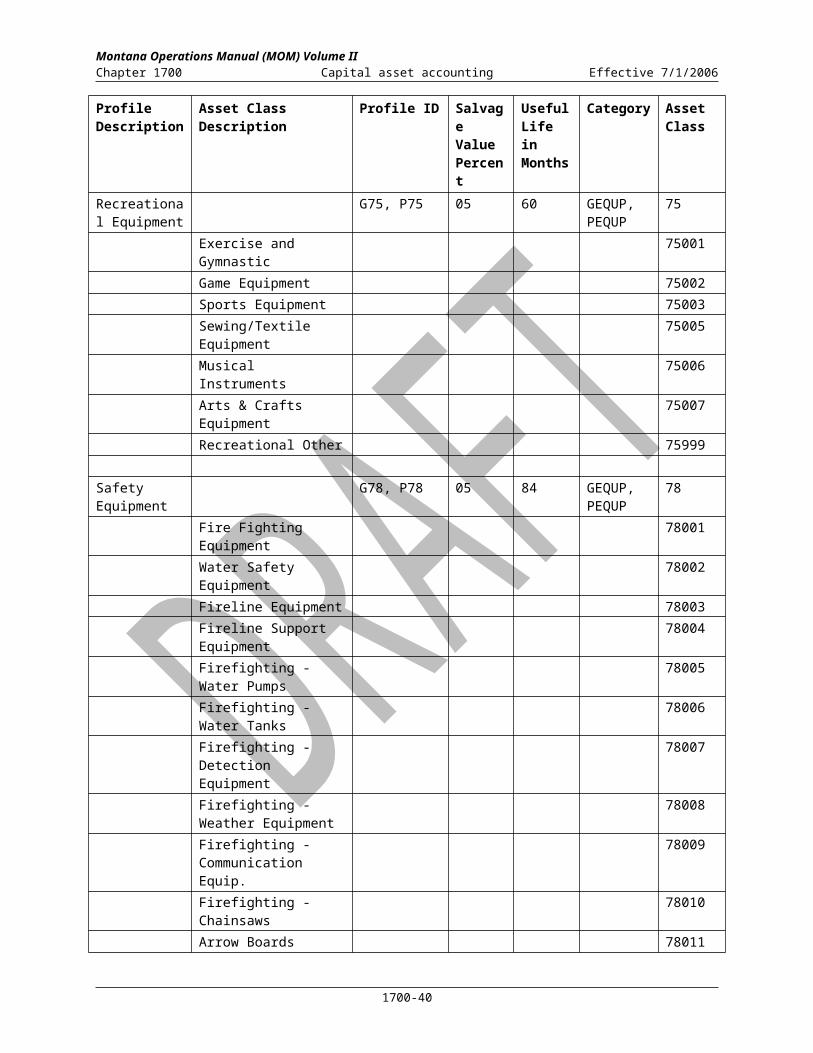

2-1720.33 Asset profile / salvage value / useful life / category / class table (modified April 2010)

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Expensed EXPENSED N/A N/A EXPEN As Req’d

Agricultural G03, P03 10 120 GEQUP, 03

1700-17

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Equipment PEQUP

Field Machinery 03001

Attachments 03002

Tractors 03003

Farm Wagons 03004

Livestock Feeding Equipment

03005

Grain Moving Equipment

03006

Tractors/Mowers 03033

Agriculture Other 03999

Airport & Airways Equipment

G04, P04 05 120 GEQUP, PEQUP

04

Airway Beacons 04001

Non-Directional Radio Beacons

04002

Unicom Radios 04003

ELT Homer 04004

Weather System 04005

Airport/Airway Other 04999

Audio-Visual & Photo Equipment

G05, P05 08 60 GEQUP, PEQUP

05

Microfilm 05001

Projection 05002

Radio and Television 05003

Recording 05004

Sound 05005

Cameras 05006

Camera Lenses 05007

Film Developing/Printing Equipment

05008

Movie Film 05009

Audio/Visual Other 05999

Books and Maps Depreciable

G10, P10, 00 84 GBOKS, PBOKS

10

Books and Maps Non-Depreciable

G9101, P9101

N/A N/A GLCOL,PLCOL

10

Books and Maps Other 10999

1700-18

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Buildings G15, P15 05 300 GBLDG, PBLDG

15

Building Improvements

G30, P30 05 84 GIMPR,PIMPR

15

Hospitals 15001

Sheds 15002

Classroom/Research 15003

Residences 15004

Garages/Barns 15005

Buildings Other 15999

Construction Equipment

G18, P18 10 84 GEQUP, PEQUP

18

Excavation & Trenching Equipment

18001

Earth-Moving Equipment

18002

Loaders 18003

Crawlers 18005

Fork Lift 18006

Motor Patrol/Graders 18030

Rollers 18031

Loaders 18032

Crawler/Tractors 18035

Pulverizers 18037

Const Equip Other 18999

Construction Work in Progress

G19, P19 N/A N/A GCWIP, PCWIP

19999

Data Processing Equipment

G20, P20 10 60 GEQUP, PEQUP

20

Computers 20001

Terminals 20002

Communications Equipment

20003

Peripheral Equipment 20004

Printers 20005

Scanners 20006

Data Processing Other 20999

Firearms G22, P22 10 84 GOTHR, POTHR

22

1700-19

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Handguns 22001

Rifles 22002

Shotguns 22003

Tranquilizing Guns 22004

Firearms Other 22999

Furniture and Fixtures

G25, P25 02 120 GEQUP, PEQUP

25

Beds 25001

Benches 25002

Bookcases 25003

Carpeting 25004

Chairs 25005

Desks 25006

Drapes 25007

Filing Cabinets 25008

Lamps 25009

Shelves, Movable 25010

Sofas 25011

Stools 25012

Tables 25013

Tubs and Showers 25014

Clocks 25015

Dressers 25016

Furnaces 25017

Decorative & Ornamental Items

25018

Storage Cabinets 25021

Display Cases 25023

Files - Fiche, Card, Map & Plan

25025

Furniture/Fixtures Other 25999

Infrastructure 90

Dams G9001, P9001

0 600 GINFR 90001

Paved Roads G9002, P9002

0 240 GINFR 90002

Gravel Roads G9003, P9003

0 120 GINFR 90003

Sewage Lagoons G9004, P9004

0 480 GINFR 90004

Water Systems G9005, P9005

0 480 GINFR 90005

1700-20

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Hatchery Raceways G9006, P9006

0 600 GILND 90006

Urbanized Interstate G9012 0 336 GINFR 90007

Urbanized Other Princ Arterial

G9012 0 336 GINFR 90008

Urbanized Minor Arterial G9012 0 336 GINFR 90009

Urbanized Collectors G9012 0 336 GINFR 90010

Highways Miscellaneous G9012 0 336 GINFR 90011

Bridges G9011, P9011

0 420 GINFR 90012

Interstate Highways G9007 0 336 GINFR 90013

National Highway System

G9008 0 336 GINFR 90014

Primary Highways G9009 0 336 GINFR 90015

Secondary Highways G9010 0 336 GINFR 90016

Dams G9001, P9001

0 600 GINFR 90017

Lakes/Ponds G9001, P9001

0 600 GINFR 90018

Reservoirs G9001, P9001

0 600 GINFR 90019

Septic Systems G9099, P9099

0 300 GINFR 90020

Ditches G9099, P9099

0 300 GINFR 90021

Natural Gas Lines G9099, P9099

0 300 GINFR 90022

Electrical Lines G9099, P9099

0 300 GINFR 90023

Telephone Lines G9099, P9099

0 300 GINFR 90024

Water Lines G9099, P9099

0 300 GINFR 90025

Fiber Optic Lines G9099, P9099

0 300 GINFR 90026

Infrastructure Other G9099, P9099

0 300 GINFR 90099

Kitchen Equipment

G35, P35 02 60 GEQUP, PEQUP

35

Dishwasher 35001

Food Proc. & Handling Equipment

35002

Freezers 35003

Ovens 35004

Ranges 35005

1700-21

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Refrigerators 35006

Kitchen Fixtures 35007

Kitchen Equip Other 35999

Laboratory & Scientific Equipment

Laboratory & Scientific Equipment

G40, P40 02 84 GEQUP, PEQUP

40

Analysis 40001

Electronic 40002

Heating & Cooling Devices

40003

Measuring & Control Devices

40004

Optical 40005

Collecting Devices 40006

Animal Care & Propagation Equipment

40007

Purifying Apparatus 40008

Electricity Variance Equipment

40009

Scales and Balances 40010

Mixing/Separating Equipment

40011

Electrical Test Equipment

40012

Microtome Equipment 40013

Laser/X-ray Equipment 40014

Medical Equipment 40017

Drilling Equipment 40018

Traffic Counters 40019

Laboratory Other 40999

Land G42, P42 N/A N/A GLAND, PLAND

45

Land Other 45999

Land Improvements

G32, P32 05 84 GLIMP, PLIMP

30

Fences & Barriers 30002

Pavement 30004

Sidewalks 30005

Walls, Retaining 30007

Boat Docks, Landings 30008

Camping & Picnic Sites 30009

Corrals, Chutes 30010

1700-22

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Landscaping, shrubbery 30011

Wildlife Habitat Modifications

30012

Picnic Tables 30014

Latrines 30015

Signs 30021

Storage Tanks 30023

Land Improvements Other

30999

Land Use Rights

G41, P41 N/A 360 GESAM, PESAM

41

Easements/Right-a-ways

41001

Mineral Rights 41002

Timber Rights 41003

Water Rights 41004

Land Use Rights - Permanent

G43, P43 N/A N/A GEASE, PEASE

43

Easements/Right-a-ways

43001

Mineral Rights 43002

Timber Rights 43003

Water Rights 43004

Leased Building

G44, P44 05 300 GLBLD, PLBLD

As Req’d

Leased Machinery/ Equipment

G45, P45 05 84 GLME, PLME

As Req’d

Leased Land G46, P46 00 360 GLLND, PLLND

As Req’d

Leased Improvement

G47, P47 05 84 GLIMP, PLIMP

As Req’d

Leased Other G48, P48 00 60 GLOTH, PLOTH

As Req’d

Livestock G50, P50 00 60 GSTCK, PSTCK

50

1700-23

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Livestock Other 509999

Maintenance and Janitorial

G55, P55 05 60 GEQUP, PEQUP

55

Floor Polishers, Waxers, Sanders

55001

Laundry Equipment 55002

Vacuum Cleaners 55003

Grounds-Keeping Equipment

55004

Garbage Containers/Packers

55005

Maint/Janitorial Other 55999

Major Maintenance Equipment

G87, P87 10 180 GEQUP, PEQUP

87

Truck-Dump Under 250HP

87019

Truck 5th Wheel or Stake Under 250HP

87021

Truck-Core Drill/Hole Auger/Water Under 250HP

87022

Paint Stripers 87023

Truck with Wing Plow Under 250HP

87025

Truck - Dump or 4x4 Over 250HP

87027

TMA Trucks 87028

Truck - Tandem Axle 87029

Truck - Mounted Special Equipment

87034

One Way Plows 87050

Reversible Plows 87051

V-Plows 87053

Snow Blowers 87054

Sanders/Spreaders 87057

Asphalt Dist -Rd Oil, Crack Sealers, Tar Pots, etc

87062

Asphalt Equip -Hot Plants, Towed Pavers, etc

87063

Miscellaneous G88, P88 10 240 GEQUP, 88

1700-24

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Major Maintenance Equipment

PEQUP

Miscellaneous Equipment

88036

Drilling Equipment 88039

Air Compressors 88041

Broom and Sweepers 88042

Support Equipment 88044

Trailers (61-21T, Safety, Pup and Belly Dumps)

88061

Mobile Office and Lab Trailers

88064

Museum and Art Purchased

G60, P60 00 360 GMUSE, PMUSE,

60

Museum Depreciable

G9201, P9201,

00 240 GMUSD, PMUSD,

60

Museum and Art Donated

G9301, P9301

GMADN, PMADN

60

Collections 60001

Paintings 60002

Pictures 60003

Plaques 60004

Specimens 60005

Statutes 60006

Mounts and Hides 60007

Historical Maps 60008

Museum Other 60999

Operating Lease

OPERLEASE N/A N/A OPLSE N/A

Office Equipment

G65, P65 05 60 GEQUP, PEQUP

65

Adding Machines 65001

Air Conditioners, Portable

65002

Bookkeeping Machines 65003

Calculators 65004

Cash Registers 65005

Computers 65006

Fans, Electric 65007

Copying Machines 65009

Transcribing Machines 65010

1700-25

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Typewriters 65011

Safes 65012

Addressing & Mailing Equipment

65013

Printing & Assembly Equipment

65014

Microfiche Reader 65015

Telephones & Communications System

65016

Office Equipment Other 65999

Other Intangibles

G66, P66 N/A 240 GOTIN, POTIN

66

Copyrights 66001

Patents 66002

Trademarks 66003

Other Intangibles 66004

Outdoor Equipment

G67, P67 05 60 GEQUP, PEQUP

67

Tents 67001

Stoves & Cooking Equipment

67002

Snowshoes 67005

Saddles, Bridals, Etc. 67006

Diving Equipment 67007

Outdoor Equipment Other

67999

Professional Equipment

G70, P70 05 84 GEQUP, PEQUP

05

Drafting 70001

Engineering 70002

Surveying 70003

Professional Other 70999

Recreational Equipment

G75, P75 05 60 GEQUP, PEQUP

75

Exercise and Gymnastic 75001

Game Equipment 75002

Sports Equipment 75003

Sewing/Textile Equipment

75005

Musical Instruments 75006

1700-26

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Arts & Crafts Equipment 75007

Recreational Other 75999

Safety Equipment

G78, P78 05 84 GEQUP, PEQUP

78

Fire Fighting Equipment 78001

Water Safety Equipment 78002

Fireline Equipment 78003

Fireline Support Equipment

78004

Firefighting - Water Pumps

78005

Firefighting - Water Tanks

78006

Firefighting - Detection Equipment

78007

Firefighting - Weather Equipment

78008

Firefighting - Communication Equip.

78009

Firefighting - Chainsaws 78010

Arrow Boards 78011

Safety Other 78999

Shop Equipment

G80, P80 05 84 GEQUP, PEQUP

80

Machine Tools & Related Equipment

80001

Power Equipment 80002

Work Benches 80003

Work Tables 80004

Tool Cabinets 80005

Two-way Portable Radios

80006

Vehicle Service Equipment

80007

Generators/Alternators 80008

Timing Gauges 80009

Tire Equipment 80010

Cleaning Equipment 80011

Shop Other 80999

Software - Purchased

G89, P89 N/A 48 GINTG, PINTG

89

Software 89001

1700-27

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

Profile Description

Asset Class Description

Profile ID Salvage Value Percent

Useful Life in Months

Category Asset Class

Software Modifications 89002

Licenses 89003

Software – Internally Generated

G84, P84 N/A 48 GIGSF, PIGSF

84

Software 84001

Software Modifications 84002

Vehicles G85, P85 15 60 GEQUP, PEQUP

85

Automobiles & Vans 85001

Airplanes 85002

Boats 85003

Campers & House Trailers

85004

Motorcycles 85005

Snowmobiles 85006

Trailers 85007

Trucks 85008

Buses 85009

Suburbans 85010

Vans 85012

Trucks-Tractor 85019

Trucks-Fire 85022

Vehicles Other 85999

Vehicle Accessories

G86, P86 05 60 GEQUP, PEQUP

86

Canopies 86001

Two-Way Radios 86002

Tool Boxes 86003

Winches 86004

Boat Motors 86005

Other 86999

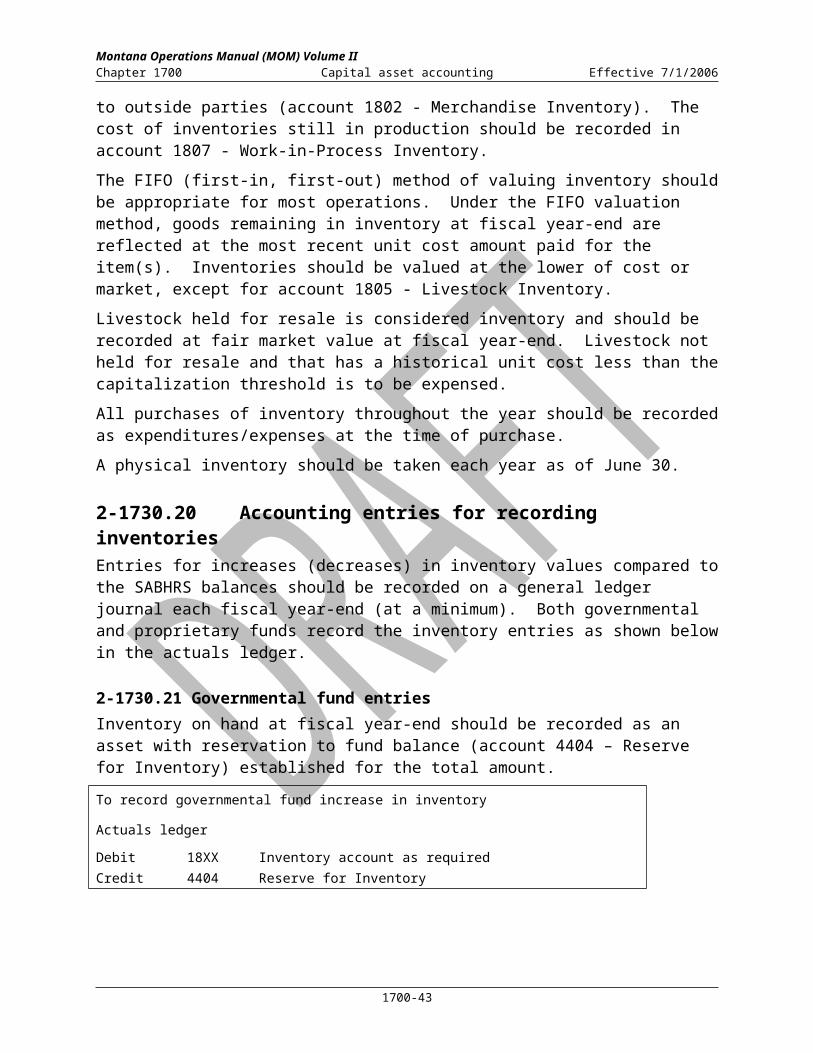

2-1730.00 Inventory (supplies, merchandise, etc.) The inventories discussed in this section are recorded in the SABHRS general ledger not AM.

2-1730.10 General informationInventories are assets (e.g., supplies, merchandise, etc.) that may be held for use in general operations (account 1804 - Supplies Inventory) or for resale to other state agencies and/or to

1700-28

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

outside parties (account 1802 - Merchandise Inventory). The cost of inventories still in production should be recorded in account 1807 - Work-in-Process Inventory.

The FIFO (first-in, first-out) method of valuing inventory should be appropriate for most operations. Under the FIFO valuation method, goods remaining in inventory at fiscal year-end are reflected at the most recent unit cost amount paid for the item(s). Inventories should be valued at the lower of cost or market, except for account 1805 - Livestock Inventory.

Livestock held for resale is considered inventory and should be recorded at fair market value at fiscal year-end. Livestock not held for resale and that has a historical unit cost less than the capitalization threshold is to be expensed.

All purchases of inventory throughout the year should be recorded as expenditures/expenses at the time of purchase.

A physical inventory should be taken each year as of June 30.

2-1730.20 Accounting entries for recording inventoriesEntries for increases (decreases) in inventory values compared to the SABHRS balances should be recorded on a general ledger journal each fiscal year-end (at a minimum). Both governmental and proprietary funds record the inventory entries as shown below in the actuals ledger.

2-1730.21 Governmental fund entriesInventory on hand at fiscal year-end should be recorded as an asset with reservation to fund balance (account 4404 – Reserve for Inventory) established for the total amount.

To record governmental fund increase in inventory

Actuals ledger

Debit 18XX Inventory account as requiredCredit 4404 Reserve for Inventory

To record governmental fund decrease in inventory

Actuals ledger

Debit 4404 Reserve for inventoryCredit 18XX Inventory account as required

2-1730.22 Proprietary fund entriesProprietary funds do not record a reservation to fund balance for inventory. Instead, the increase or decrease in inventory is generally offset against current year expenditures using a non-budgeted expense account. All proprietary funds use the following examples, except for the DOA Surplus Property Bureau and the Department of Correction’s prison ranch program, which are detailed separately.

1700-29

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

To record proprietary fund increase in inventory

Actuals ledger

Debit 18XX Inventory account as requiredCredit 62855 Inventory adjustment non-budgeted

To record proprietary fund decrease in inventory

Actuals ledger

Debit 62855 Inventory adjustment non-budgetedCredit 18XX Inventory account as required

2-1730.23 Surplus Property Fund inventory entries Surplus Property should record one or both of the following entries at the end of each month:

To record increase in inventory for Surplus Property Fund

Actuals ledger

Debit 1802 Merchandise InventoryCredit 549002 Inventory contributions, P&S

To record decrease in inventory for Surplus Property Fund

Actuals ledger

Debit 62855 Inventory adjustment-nonbudgetedCredit 1802 Merchandise Inventory

2-1730.24 Livestock inventory entriesEntries to record livestock inventory are as follows:

To record increase in inventory of livestock

Actuals ledger

Debit 1805 Livestock inventoryCredit 62844 Livestock inventory adjustment

To record decrease in inventory of livestock

Actuals ledger

Debit 62844 Livestock inventory adjustmentCredit 1805 Livestock inventory

1700-30

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

2-1740.00 Asset accounting general discussion

2-1740.10 Accounting for capital assets Acquisitions of capital assets will be recorded in either the entitywide or the actuals ledger, based on the classification of the fund responsible for the asset. Capital assets in both ledgers are reported using the full accrual basis of accounting.

2-1740.11 Assets to be recorded in the entitywide ledgerAll assets acquired by governmental funds will be recorded in the entitywide ledger. Governmental funds are the general, special revenue, debt service, capital project, and permanent trust funds (funds 01100 - 05XXX, 080XX – 08499, 090XX – 094XX).

On AM, these assets are referred to as governmental and are designated with a “G” profile, a “G” category and are found in the Government Book.

2-1740.12 Assets to be recorded in the actuals ledgerAll assets acquired by nongovernmental funds will be recorded in the actuals ledger. Nongovernmental funds are the enterprise, internal service, private purpose trust, pension, and higher education funds (funds 40XXX, 086XX, 095XX, 2XXXX – 8XXXX).

On AM, these assets are referred to as proprietary and are designated with a “P” profile, a “P” category and are found in the State Book.

2-1740.13 Accounting for expensed assetsNo accounting entries will be generated by AM in regard to expensed assets. The purchase of expensed assets is generally recorded in SABHRS via an accounts payable (AP) voucher using an expenditure account in the 62XXX range with the offset to cash in the actuals ledger.

2-1740.20 Purchase of split funded assets Governmental fund assets may be split-funded and proprietary fund assets may be split-funded as long as the asset is recorded in only one fund type, i.e., governmental or proprietary. Please note that when an item is split-funded on AM, the same asset number must be used for the entire asset.

A capital asset funded from both governmental and proprietary fund types will require special accounting treatment in the general ledger to properly record the asset in both the general ledger and AM. In this situation, an operating transfer must be recorded to transfer the amount from one fund type to the fund type that is recording the asset.

2-1740.21 Examples of split funded asset The General Fund (01100) pays $7,000 and an enterprise fund pays $9,000 (06XXX) for

a single capital asset. The item will be recorded as a governmental asset. The enterprise fund transfers $9,000 to the General Fund, which then shows a total capital outlay expenditure of $16,000, which must be appropriated. The entire amount is capitalized in the General Fund with a “G” profile and a “G” category.

1700-31

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

A governmental fund and a proprietary fund type purchase a capital asset with the intent that the asset will be capitalized and depreciated within the proprietary fund. The governmental fund records a “transfer-out” and the proprietary fund records a “transfer-in”. The proprietary fund then records the entire amount of the purchase and capitalizes the asset in that fund.

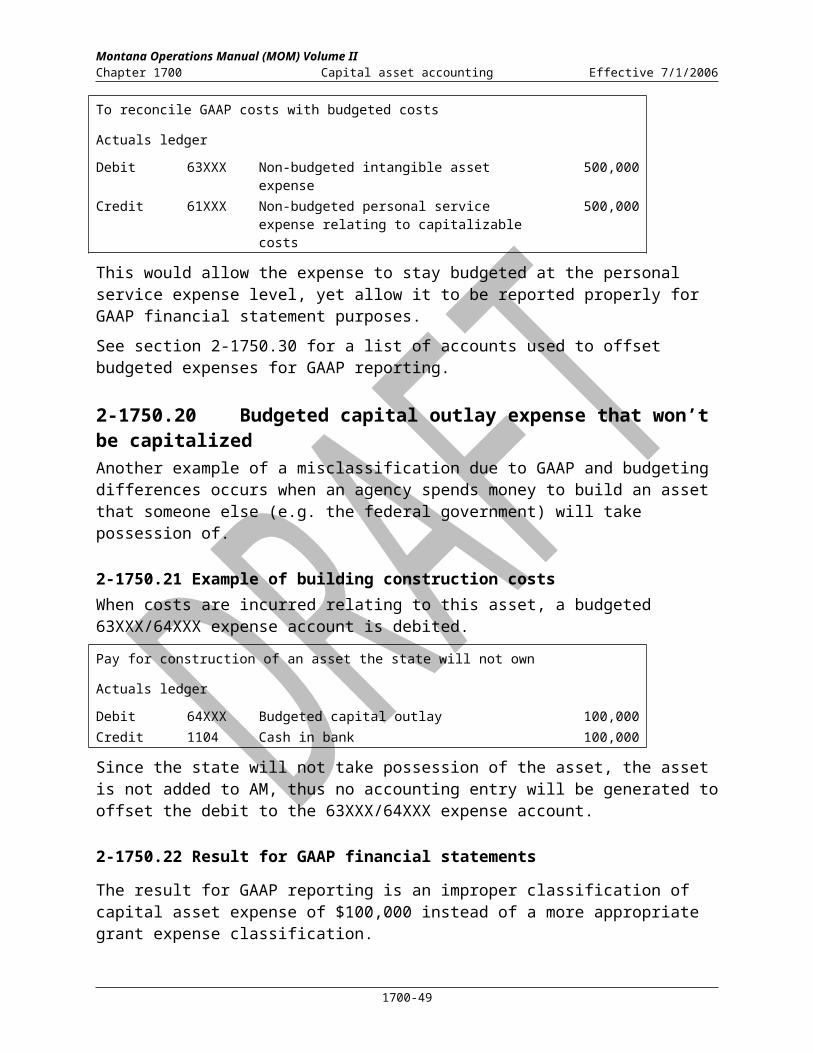

2-1750.00 Recording capital asset related expensesExpenses related to capital assets or capital projects are normally recorded in budgeted 63XXX/64XXX level expense accounts. When the capital asset is added to AM, the budgeted 63XXX/64XXX level expense is offset with a non-budgeted 63XXX/64XXX expense account. This accounting reflects a budgeted expense in the year the money was spent, yet for financial statement reporting, on a full accrual basis, the expense is capitalized and depreciated over its useful life.

All expenditures of less than the capitalization threshold should normally be considered an expenditure that benefits the current period. Repair and maintenance costs are to be expensed in the year incurred using a 62XXX account.

For GAAP basis financial statement reporting, problems arise when an asset is capitalized that was not budgeted at a 63XXX/64XXX level or when an asset is not capitalized that was budgeted at a 63XXX/64XXX level. The following adjusting entries will convert the budgetary basis accounting to a GAAP basis. Thus, GAAP reporting can be achieved and the budget can remain the same.

2-1750.10 Capital asset cost budgeted in a range other than the capital outlay expense levelSometimes costs related to capital assets are recorded using expense accounts that do not fall within the capital outlay level expenses (63XXX/64XXX). This activity causes a financial statement misclassification for reporting due to GAAP and budgeting differences.

2-1750.11 Example of internally developed software costsIn the following example, a State employee worked on an internally generated software project that will be capitalized, a 61XXX level expense account is debited to reflect their salary expense, as follows:

Pay payroll costs

Actuals ledger

Debit 61XXX Budgeted personal service expense 500,000Credit 1104 Cash in bank 500,000

However, when the asset is capitalized on AM, a non-budgeted 63XXX/64XXX expense account is credited, as follows:

1700-32

Montana Operations Manual (MOM) Volume IIChapter 1700 Capital asset accounting Effective 7/1/2006

AM entry to capitalize the asset

Actuals or entitywide ledger

Debit 1809 Intangible asset 500,000Credit 63XXX Non-budgeted intangible asset expense 500,000

2-1750.12 Result for GAAP financial statements