2 - 1 debits and credits – analyzing and recording business transactions chapter 2

TRANSCRIPT

2 - 1

Debits and Credits –Analyzing and

RecordingBusiness Transactions

Chapter 2

2 - 2

Setting up and organizing

a chart of accounts.

Learning Objective 1

2 - 3

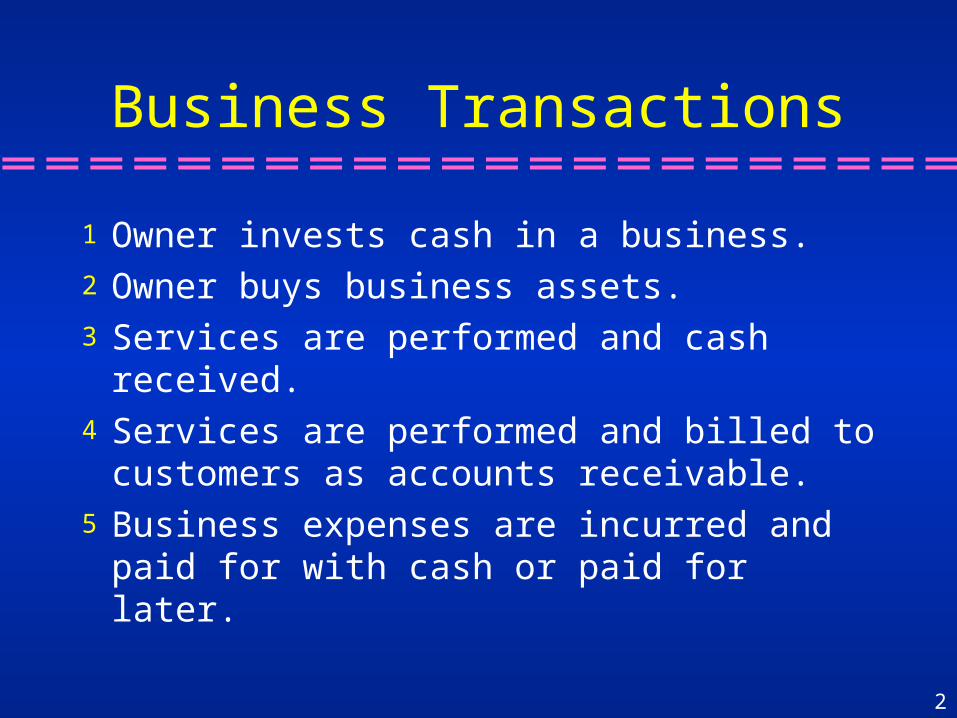

Business Transactions

1 Owner invests cash in a business.2 Owner buys business assets.3 Services are performed and cash received.4 Services are performed and billed to

customers as accounts receivable.5 Business expenses are incurred and paid for

with cash or paid for later.

2 - 4

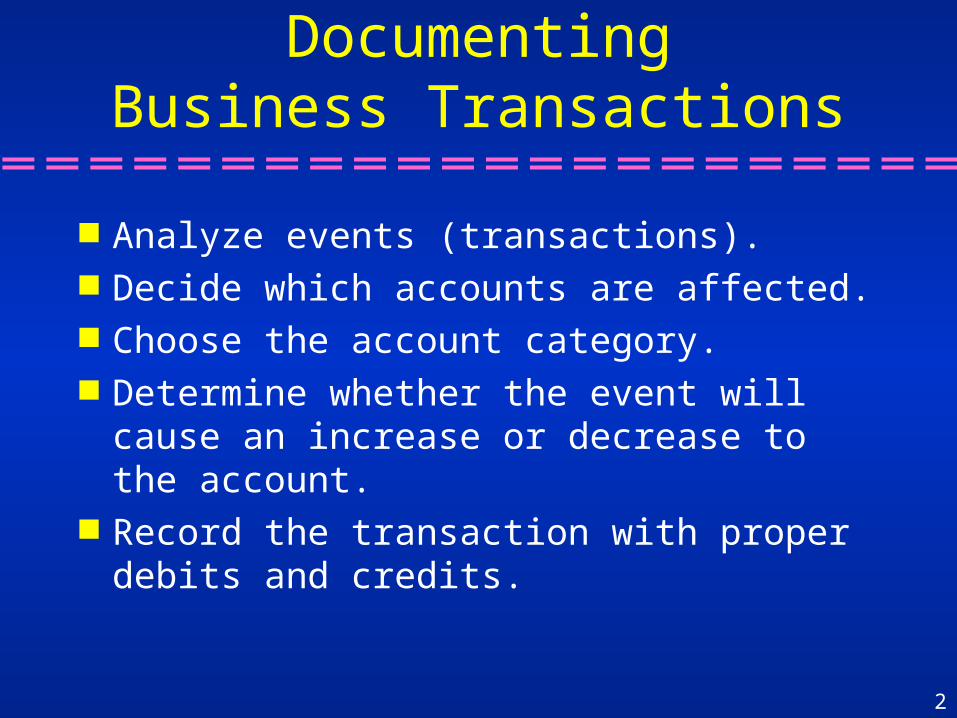

DocumentingBusiness Transactions

Analyze events (transactions). Decide which accounts are affected. Choose the account category. Determine whether the event will cause an

increase or decrease to the account. Record the transaction with proper debits

and credits.

2 - 5

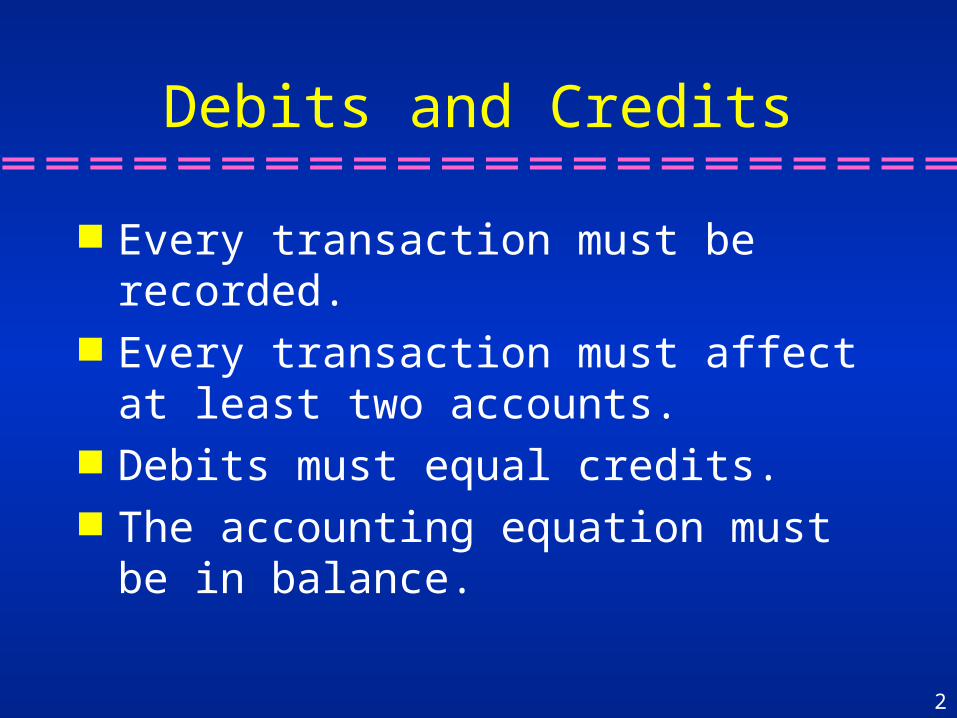

Debits and Credits

Every transaction must be recorded. Every transaction must affect at least two

accounts. Debits must equal credits. The accounting equation must be in

balance.

2 - 6

Left Right

Debit Credit

Learning Unit 2-1

A T account is a format used to show the effect of transactions.

Dollar signs ($) are not used in accounts.

T account

2 - 7

Learning Unit 2-1

The Ledger Account

Balance

Account: Cash Account: 1000

Date ref. debit credit debit credit

June 1 5,000 5,000

2 - 8

Debits and Credits

What is the definition of debit? The left side of any T account. A number entered on the left side of any account

is said to be debited to an account.

What is the definition of credit? The right side of any T account. A number entered on the right side of any account

is said to be credited to an account.

2 - 9

Account Name (Title)

Left side/Dr. (debit)

Right side/Cr. (credit)

Account Name (Title)

Debits and Credits

2 - 10

Balancing an Account

T accounts:1 Add each side (debit & credit side).2 Foot the account by writing the numbers in

small type at the bottom of each side.3 Calculate the ending balance by subtracting the

smaller side from the larger side. Ledger accounts: Some types contain a running balance.

2 - 11

Recording transactions inT accounts according to

the rules of debit and credit.

Learning Objective 2

2 - 12

Learning Unit 2-2

Recording Business Transactions: Debits and Credits

T accounts will be used. Remember the accounting equation:

Assets = Liabilities + Owner’s Equity

2 - 13

*Dr. (Debit)

assetsexpenses

withdrawals

AccountCategories

Rules of Debit & Credit

A normal balance of an account is theincrease side.*

Normal Balance

2 - 14

Rules of Debit & Credit

A normal balance of an account is theincrease side.*

Normal Balance

liabilitiescapital

revenue

*Cr. (Credit)

AccountCategories

2 - 15

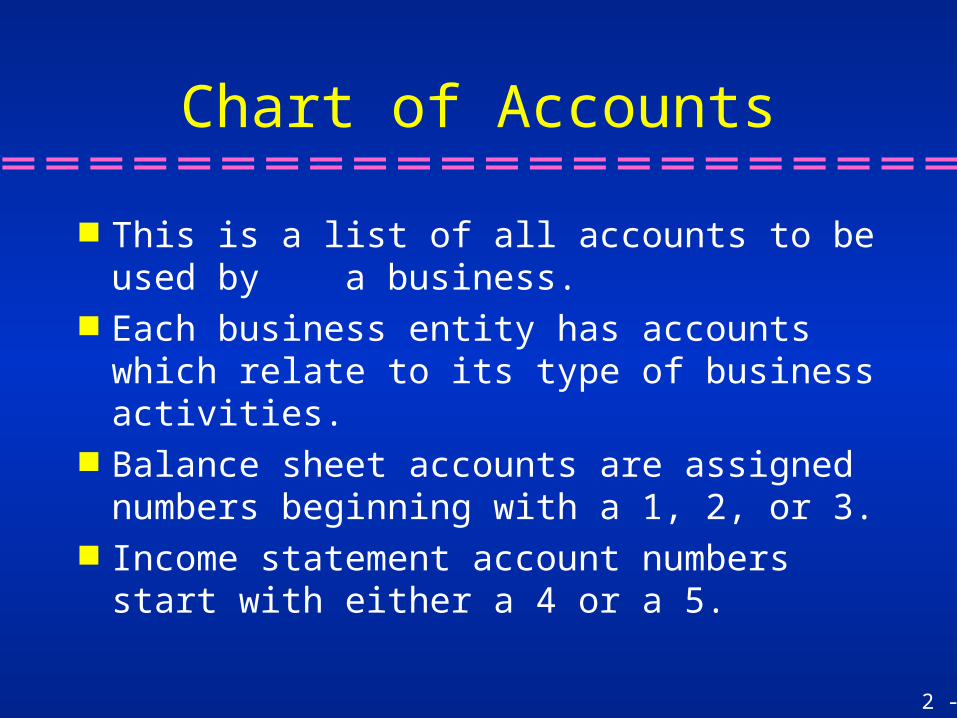

Chart of Accounts

This is a list of all accounts to be used by a business.

Each business entity has accounts which relate to its type of business activities.

Balance sheet accounts are assigned numbers beginning with a 1, 2, or 3.

Income statement account numbers start with either a 4 or a 5.

2 - 16

Balance Sheet

Assets

1000 Cash

1020 Accounts Receivable

1030 Office Supplies

1040 Computer Equipment

1050 Office Equipment

Chart of Accounts

2 - 17

Balance Sheet

Liabilities

2000 Accounts Payable

Owner’s Equity

3010 Capital

3020 Withdrawals

Chart of Accounts

2 - 18

Revenue4000 Service RevenueExpenses5010 Advertising Expense5020 Rent Expense5030 Utilities Expense5040 Phone Expense5050 Supplies Expense5060 Insurance Expense5070 Postage Expense

Income Statement

Chart of Accounts

2 - 19

Clara J. Accounting Practice Example

Assets1000 Cash $4,5001020 Accounts Receivable1030 Office Supplies 3001040 Computer Equipment 1,2001050 Office Equipment

Total $6,000

2 - 20

Clara J. Accounting Practice Example

Expenses5010 Advertising Expense $ 3005020 Rent Expense 4005030 Utilities Expense 2005040 Phone Expense5050 Supplies Expense5060 Insurance Expense5070 Postage Expense

Total $ 900Assets + Expenses $6,900

2 - 21

Clara J. Accounting Practice Example

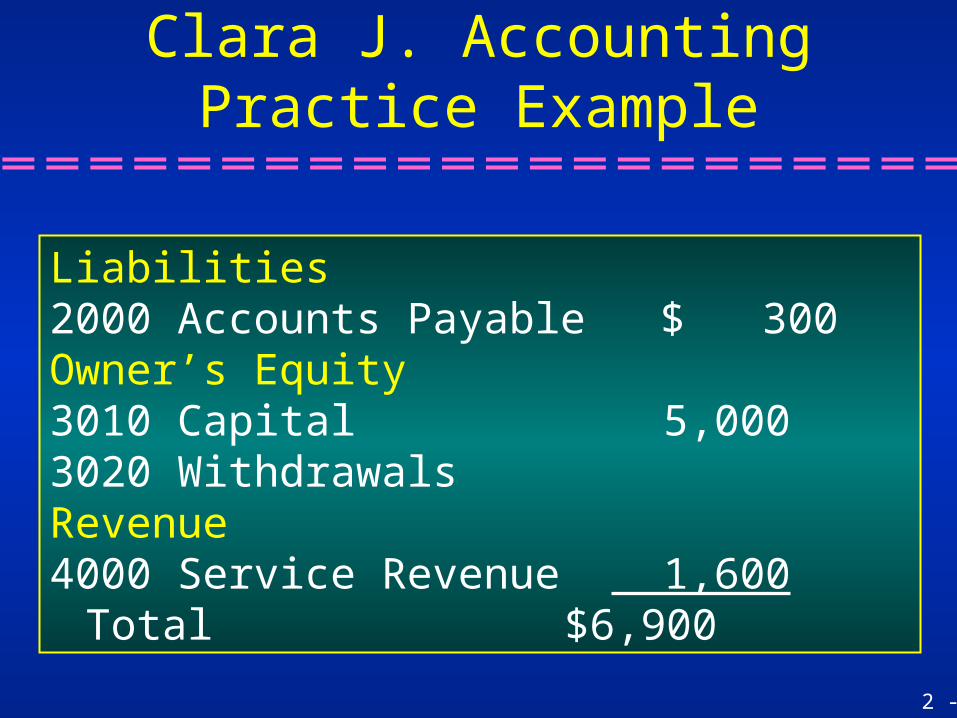

Liabilities2000 Accounts Payable $ 300Owner’s Equity3010 Capital 5,0003020 WithdrawalsRevenue4000 Service Revenue 1,600

Total $6,900

2 - 22

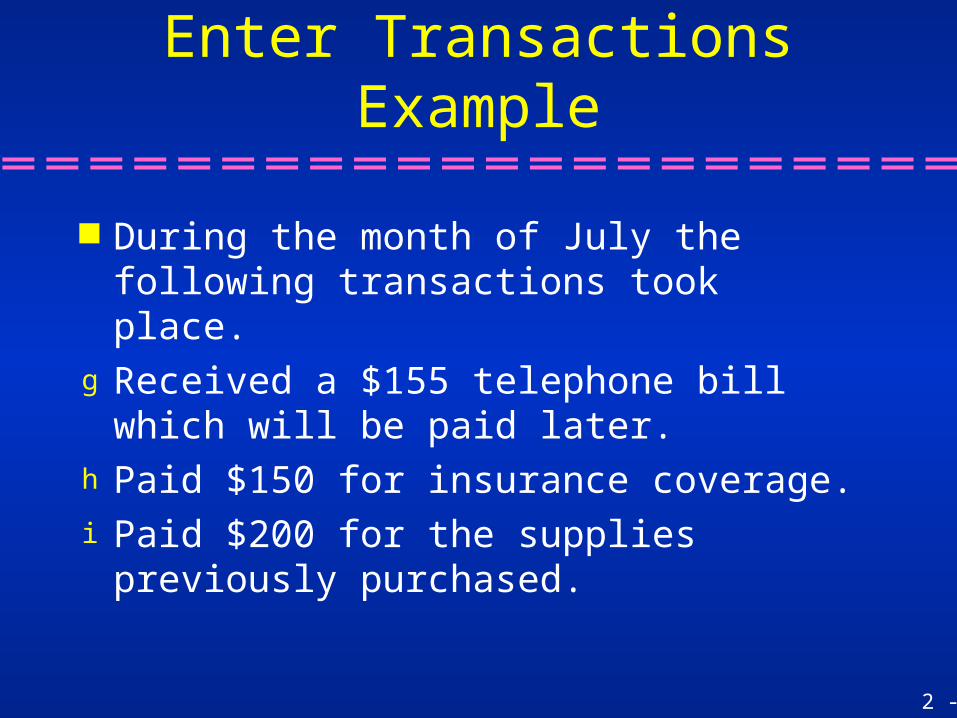

Enter Transactions Example

During the month of July the following transactions took place.

g Received a $155 telephone bill which will be paid later.

h Paid $150 for insurance coverage.i Paid $200 for the supplies previously

purchased.

2 - 23

Enter Transactions Example

j Performed $850 of services on account.k Paid another $85 for the supplies previously

purchased.

2 - 24

Phone Expense g) 155

Accounts Payable 300

g) 155

Enter Transactions Example

g Debit Phone Expense and credit Accounts Payable which increases both accounts’ normal balances.

2 - 25

Enter Transactions Example

h Debit Insurance Expense and credit Cash which increases an expense and decreases an asset.

Insurance Expenseh) 150

Cash 4,500

h) 150

2 - 26

Enter Transactions Example

i Debit Accounts Payable and credit Cash which decreases both accounts’ balances.

Cash 4,500 h) 150

i) 200

Accounts Payable 300 i) 200 g) 155

2 - 27

Enter Transactions Example

j Debit Accounts Receivable and credit Revenue which increases the normal balance of both accounts.

Accounts Receivable j) 850

Service Revenue 1,600 j) 850

2 - 28

Enter Transactions Example

k Debit Accounts Payable and credit Cash which increases the normal balance of both accounts.

Accounts Payable300

i) 200 g) 155 k) 85

Cash 4,500 h) 150

i) 200k) 85

2 - 29

Preparing a trial balance.

Learning Objective 3

2 - 30

Assets1000 Cash $4,0651020 Accounts Receivable 8501030 Office Supplies 3001040 Computer Equipment 1,2001050 Office Equipment

Total $6,415

Learning Unit 2-3

Clara J. Accounting PracticeTrial Balance

2 - 31

Clara J. Accounting Practice Trial Balance

Expenses5010 Advertising Expense $ 3005020 Rent Expense 4005030 Utilities Expense 2005040 Phone Expense 1555050 Supplies Expense5060 Insurance Expense 1505070 Postage Expense

Total $1,205Assets + Expenses $7,620

2 - 32

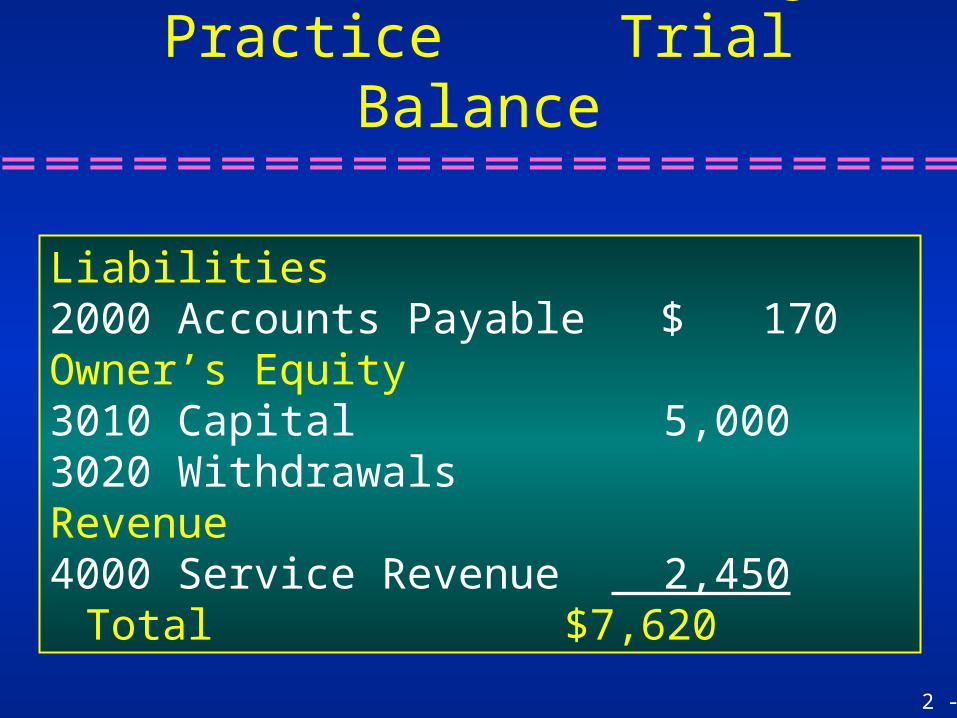

Clara J. Accounting Practice Trial Balance

Liabilities2000 Accounts Payable $ 170Owner’s Equity3010 Capital 5,0003020 WithdrawalsRevenue4000 Service Revenue 2,450

Total $7,620

2 - 33

Learning Objective 4

Preparing financial reports

from a trial balance.

2 - 34

Clara J. Accounting Practice Income Statement

Clara J. Accounting PracticeIncome Statement

Year Ended July 31, 20xx

Revenues (fees earned) $2,450Expenses:

Advertising Expense 300Utilities and Telephone Expenses 355Rent Expense 400Insurance Expense 150 1,205

Net Income $1,245

2 - 35

Clara J. Accounting Practice Statement of Owner’s Equity

Clara J., Capital, June 1, 200x $ 0Contribution Of Capital 5,000Net Income 1,245Clara J., Capital, July 31, 200x $ 6,245

2 - 36

Clara J. Accounting Practice Balance Sheet

Clara J. Accounting PracticeBalance SheetJuly 31, 200x

AssetsCash $4,065Acct. Rec. 850Supplies 300Equipment 1,200Total Assets $6,415

Liabilities and Owner’s EquityAccounts Payable $ 170Owner’s EquityClara J., Capital 6,245

Total $6,415

2 - 37

End of Chapter 2