1q 2018 investment portfolio review - cbisonline.com · era of low equity volatility ending...

TRANSCRIPT

Christian Brothers Investment Services, Inc. n [email protected] PAGE 1

1Q 2018

Investment Portfolio Review

LEADING CATHOLIC INSTITUTIONAL

INVESTMENT MANAGER

} Over $7 billion in assets under management

} Exclusively serve Catholic institutions

} Founded and owned by the De La Salle Christian Brothers

PIONEERED CATHOLIC RESPONSIBLE

INVESTINGSM

} Thoughtful and disciplined Catholic investment screens

} Encourage companies to improve policies and practices through active ownership

DIVERSIFIED INVESTMENT PROGRAMS

} Manager of managers } Institutional pooled funds

and separate accounts

UNIFY FAITH AND FINANCE

} Align investments with mission

DIVERSE RANGE OF NEEDS

} Portfolio services for a range of institutions

} Single- and multi-product relationships with institutions and their consultants

GLOBAL INVESTOR BASE

} Religious Institutes } Dioceses } Education } Healthcare

CBIS helps Catholic organizations achieve their financial goals through the socially responsible management of their investments.

BY PRODUCT TYPE ($MILLION)

BY CUIT TYPE ($MILLION)

Separate Accounts $663Global Funds PLC (UCITS) $641CUIT Funds $6,143

Money MarketOpportunistic BondBalancedCore IndexValue

Short bondInt. Diversified BondSmall capGrowthInternational

CBIS Asset Review

$7.4 BILLION IN TOTAL ASSETS

UNDER MANAGEMENT (3/31/18)

1%

6%

20%

5%6%

5%

6%

14%

30%

6%

8%9%

83%

Key Highlights:Market Overviewpage 2

Investment Program Offeringspage 8

CUIT Fund’s Performancepage 9

CUIT Fund Reportspage 10

Investment Portfolio Review 1Q 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 2Christian Brothers Investment Services, Inc. n [email protected] PAGE 1

MARKET PERSPECTIVE 1Q 2018

The Return of Volatility

Volatility has returned to equity markets, but despite the turbulence, the

overall market saw only modest declines in the first quarter, with the

S&P 500 Index down by less than 1%. A number of economic signals and

policy factors, including normalizing interest rates, drove the change in

volatility—which may signal an opportunity for disciplined investors.

CAPITAL MARKETS REVIEW

Global Overview

U.S. Equity Markets

Fixed Income Markets

Inflation Moving Toward Fed Target

Wages Finally Increasing

Growth Still Dominating Value

Gap Narrows Between Bond & Equity Valuations

MARKET MUSINGS

Era of Low Equity Volatility Ending

Normalizing Interest Rates

Low Unemployment & Labor Participation

Trade Fears: Globalization Is Real

Christian Brothers Investment Services, Inc. n [email protected] PAGE 3

Investment Portfolio Review 1Q 2018

Market Perspective 1Q 2018 APRIL 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 2

Capital Markets Review

Market Performance: 3 Month Market Performance: 12 Month

BB U.S. Short T-Bill (1-3M)

BB U.S. Aggregate

S&P 500

Russell 1000 Value

Russell 1000 Growth

S&P SmallCap 600

MSCI ACWI-Ex US (USD)

MSCI ACWI-Ex US (Local)

MSCI EM (USD)

MSCI EM (Local) 0.8

1.5

-3.0

-1.1

0.6

1.4

-2.8

-.08

-1.5

0.3 BB U.S. Short T-Bill (1-3M)

BB U.S. Aggregate

S&P 500

Russell 1000 Value

Russell 1000 Growth

S&P SmallCap 600

MSCI ACWI-Ex US (USD)

MSCI ACWI-Ex US (Local)

MSCI EM (USD)

MSCI EM (Local) 22.4

25.4

9.4

17.0

12.7

21.3

6.9

14.0

1.2

1.1

S&P 500

Consumer Discretionary

Consumer Staples

Energy

Financials

Healthcare

Industrials

Info Technology

Materials

Real Estate

Telecom

Utilities

S&P 500

Consumer Discretionary

Consumer Staples

Energy

Financials

Healthcare

Industrials

Info Technology

Materials

Real Estate

Telecom

Utilities

1.7

1.9

10.5

27.7

14.0

11.3

18.0

-0.2

-0.9

16.9

14.0

-5.0

-7.5 -4.9

-3.3

-5.5

3.5

-1.6

-1.2

-1.0

-5.9

-7.1

3.1

-0.8

Market Performance: 3 Month Market Performance: 12 Month

GLOBAL OVERVIEW

• Despite increased equity market

volatility and headlines about the

FAANG stocks (Facebook, Apple,

Amazon, Netflix, and Google), U.S.

growth stocks kept advancing while

value stocks lost ground.

• In the last 12 months, growth has

outperformed value by almost 15%.

• Small caps outperformed larger

cap stocks for the quarter, driven

largely by concerns over tariffs and a

resulting trade war.

• Emerging markets stocks

outperformed developed markets in

local and dollar terms.

• U.S. fixed income underperformed

equities as interest rates increased

across the curve during the quarter.

• Despite a weak March, the

Information Technology sector

generated the strongest

performance during 1Q, followed by

Consumer Discretionary.

• The Consumer Staples and Telecom

sectors were relatively weak in the

period.

• Over the last 12 months, only

three of the 11 S&P 500 sectors

outperformed the overall market.

• The Information Technology sector

has provided market leadership

for the last 12 months, followed

distantly by the Financials and

Consumer Discretionary sectors.

U.S. EQUITY MARKETS

Christian Brothers Investment Services, Inc. n [email protected] PAGE 4

Investment Portfolio Review 1Q 2018

Market Perspective 1Q 2018 APRIL 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 3

Treasury Yield Curve

Market Performance: 12 MonthMarket Performance: 3 Month

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

3/31/17Maturity

12/31/173/31/18

30Y10Y7Y5Y3Y2Y1Y6M3M1M

High Yield

Corporate

CMBS

ABS

MBS

Treasury

BB U.S. Aggregate

-1.2

-1.2-0.4

-0.2

High Yield

Corporate

CMBS

ABS

MBS

Treasury

BB U.S. Aggregate -1.5

-0.4

-1.2-0.1

-2.3-0.8

-0.9-0.2

0.4

0.80.3

0.50.6

1.2

1.31.4

2.72.1

3.83.6

Duration-Adjusted Excess ReturnAbsolute Return

FIXED INCOME MARKETS

• While the yield curve has

experienced a significant twist in

the past 12 months, with the 30-

year portion unchanged, it shifted

upward in a parallel fashion in 1Q.

• In contrast, long duration has

outperformed shorter duration

in the past 12 months despite an

overall increases in yields.

• Credit and Asset Backed sectors

underperformed Treasuries in 1Q,

driven partly by increased market

volatility.

• In the past year, sectors offering

“equity-like risk” (e.g., High Yield

bonds) were rewarded.

Duration and performance exhibited a linear relationship in 1Q, with long duration underperforming short duration.

Christian Brothers Investment Services, Inc. n [email protected] PAGE 5

Investment Portfolio Review 1Q 2018

Market Perspective 1Q 2018 APRIL 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 4

Source: U.S. Bureau of Labor Statistics, via Federal Reserve Economic Data, as of 3/31/2018; www.myf.red/g/jelQ

Employment Cost Index

Perce

nt Ch

ange

from

a Ye

ar A

go

2004 2006 2008 2010 2012 2014 20161.0

1.5

2.0

2.5

3.0

3.5

4.0

WAGES FINALLY INCREASING

• Wage increases should be

welcomed, not feared as

inflationary.

• The rate of wage increase is well

below historical norms, at levels

economists generally consider

“healthy.”

• Further increases closer to 3.5%-

4.5% would be a sign of stronger

economic growth.

• The Fed’s preferred measure of

inflation, the Personal Consumption

Expenditures Index, has moved

toward the monetary authority’s

stated target.

• The Fed will welcome consistent

readings between 2% and 2.5%.

INFLATION MOVING TOWARD FED TARGET

1970 1980 1990 2000 2010-2.5

0.0

2.5

5.0

7.5

10.0

12.5

Personal Consumption Expenditures Index

Source: U.S. Bureau of Economic Analysis, via Federal Reserve Economic Data, as of 3/31/2018; www.myf.red/g/iSGP

Perce

nt Ch

ange

from

a Ye

ar A

go

Christian Brothers Investment Services, Inc. n [email protected] PAGE 6

Market Perspective 1Q 2018 APRIL 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 5

• Growth sectors continue to

outperform value despite increased

volatility; when will this trend turn?

• The gap between bond and

equity price-to-earnings ratios has

compressed; this trend is expected

to continue.

GROWTH STILL DOMINATING VALUE

GAP NARROWS BET WEEN BOND & EQUITY VALUATIONS

1980 1990

Relative Cumulative Added Value

Source: Bloomberg, as of 3/31/2018; www.Bloomberg.com

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Feb ‘00

Jul ‘06

2000 2010 2018

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Source: Bloomberg, U.S. Department of the Treasury as of 3/31/2018; www.bloomberg.com, www.treasury.gov

2017201020001990 1995 200519851980

Bond P/E

Stock P/E

Market volatility will increase as the valuation difference narrows between these two asset classes.

Investment Portfolio Review 1Q 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 7

Investment Portfolio Review 1Q 2018Market Perspective 1Q 2018 APRIL 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 6

Thus the equity market volatility we witnessed in the first quarter was not unexpected. Rising interest rates represent change at the margin—in this case, higher borrowing costs for companies. Stock market investors consider that change and adjust their forecasts for the future profitability of companies. As a result, the relative attractiveness of individual stocks changes. Shares are traded. Repricing occurs. Volatility rises. All this happens so we can return the monetary system to the normal footing we require for the economy to function sustainably.

This increased volatility signals opportunity for disciplined investors. It exacerbates valuation differences and increases the potential for market mispricing of securities. This provides the potential for outperformance or alpha by active asset managers. At the portfolio level, volatility provides opportunities for improved outcomes for investors who follow a disciplined rebalancing process. In this case, market volatility encourages investors to “buy low and sell high” through rebalancing. Of course, emotion and institutional decision-making may make this advice difficult to follow. Each of these characteristics serves to transform market volatility from a risk into an asset.

The larger concern for market returns is not the increased volatility, but the potential for policy mistakes from well-intentioned actions and initiatives. This is where the quote from Milton Friedman comes into play.

There is no doubt in my mind the Federal Reserve is on the correct path by normalizing interest rates. In doing so, the Fed removes perverse incentives and potential risks from negative real interest rates. However, in forecasting the relationship between the unemployment rate and inflation in a 21st century

Volatility has returned to equity markets, a development that should cause neither surprise nor apprehension. For most of the past six years, we have been in an environment characterized by low levels of volatility, caused in large part by historically low interest rates. The world’s central banks engineered the low rate environment to stave off economic collapse in the face of the 2008 credit crisis and to prevent recession in the years of fragile recovery that followed.

Think of it as a program of life support—extreme measures applied on a temporary basis. Now the Federal Reserve has been quite eager to move its patient out of treatment and back to routine daily life. To do so, the central bank has been explicit in its desire to normalize interest rates, which means simply raising rates from levels near zero to somewhere in the direction of their longer-term averages. In the case of the federal funds rate, that’s just under 5%. Over the past 16 months, Fed policymakers have approved a series of six 0.25% interest rate increases, lifting the targeted federal funds rate into a range of 1.50% to 1.75%. That’s a significant move from zero, and while still a long way from the long-term historical average, it represents an extremely high percentage of change, coming as it does off a small base.

0%

5%

10%

15%

20%

Normalizing Interest Rates

1954 1962 1970 1978 1986 1994 2002 2010 2018

LT Avg. 4.85%

0.00%

0.50%

1.00%

1.50%

2.00%

2016 2017 2018

Path to Normal

Sep Dec Mar Jun Sep Dec Mar

Effec

tive F

eder

al Fu

nds R

ate

Source: Board of Governors of the Federal Reserve System, via Federal Reserve Economic Data, as of 3/31/2018; www.myf.red/g/iOFF

0%

1988 1998 2008 2018

10%

20%

30%

40%

50%

60%

70%

80%

90%AverageVolatility

Era of Low Equity Volatility Ending

Source: Bloomberg, as of 3/31/2018; www.Bloomberg.com

Equity market volatility has remained below long-run averages for most of the period since

the Global Financial Crisis, but we believe this period of tranquility is over as the Fed moves

toward normalization of short-term rates.

Market Musings

“One of the great mistakes is to judge policies and programs by their intentions rather than their results.” — Milton Friedman

Investment Portfolio Review 1Q 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 8

Market Perspective 1Q 2018 APRIL 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 7

corporations in foreign domiciles. Trade is not a “you win, I lose” proposition but rather a “win-win” or “lose-lose” equation. The dollars we spend on imports find their way back to the U.S. to purchase goods, services, or government debt to support our economic growth. Where else would the dollars

go? Unfortunately, tariffs simply increase the cost of the good or service. As with any product, increased prices result in reduced demand. The market reaction to the trade rhetoric is well-placed, and we anticipate continued volatility as these policies play out.

We have been fortunate to have low market volatility through the period of rehabilitation of global economies in the aftermath of the Financial Crisis. Now as economic growth is becoming more robust, monetary authorities are moving towards normalization of policy. This is a positive development that includes higher market volatility with all its risks and benefits.

economy, members of the Fed’s Open Market Committee risk overshooting—setting interest rates too high and triggering recession. Certainly this fear permeated the market in early February as a result of a strong employment report, a short-term increase in long-term bond yields as a result of increased inflationary expectations, and the first shot of higher volatility.

Shouldn’t we welcome higher wage growth? We have been waiting for this for years. Yes, the unemployment rate is low, and maybe it is close to a level that will spur inflationary wage increases. But, we cannot overlook the fact that the labor participation rate is also low and has not increased. The unemployment rate only factors in those individuals that are actively seeking employment, not those who have given up the job search. The low participation rate points to a supply of potential workers who are not currently seeking employment. With an increase in wages, is it not likely that some of the frustrated job seekers will re-enter the work force? That increase in the supply of labor could mitigate wage inflation. Wage growth remains below historical levels, and while we must always remain vigilant for inflation, at this point it remains a risk—not a reality.

A trade war presents an even greater threat to the market outlook. Trade is an ever-increasing percentage of world economic growth, with significant profits earned by U.S.

Low Unemployment & Labor Participation

1950 1960 1970 1980 1990 2000 20102%

3%

4%

5%

6%

7%

8%

9%

10%

11%

65.00%

63.75%

62.50%

61.25%

60.00%

58.75%

57.50%

66.25%

67.50%

68.75%Civilian Labor Force Participation Rate (right)Civilian Unemployment Rate (left)

Source: U.S. Bureau of Labor Statistics, via Federal Reserve Economic Data, as of 3/31/2018; www.myf.red/g/jeH4

Inflation fears in 1Q were based on the Phillips Curve Theory, which holds that unemployment

and inflation have a stable, inverse relationship. However, the decline in the participation

rate—particularly post-2008—can be viewed as a mitigating factor to offset Phillips Curve

concerns.

Wor

ld Tr

ade a

s Sha

re of

Wor

ld G

DP0%

10%

20%

30%

40%

50%

60%

70%

Trade Fears: Globalization Is Real

1960 1968 1976 1984 1992 2000 2008 2016

Source: World Development Indicators, as of 3/1/2018; databank.worldbank.org

Trade makes up more than 50% of global GDP; an outbreak of trade wars has the potential to

harm both economic growth and corporate earnings in the U.S.

John W. Geissinger, CFACIO, CBIS

Important Information: This is for informational purposes only and does not constitute an offer to sell any investment. The Funds are not available for sale in all jurisdictions. Where available for sale, an offer will only be made through the prospectus for the Funds, and the Funds may only be sold in compliance with all applicable country and local laws and regulations.

Christian Brothers Investment Services, Inc. n [email protected] PAGE 9

INVESTMENT PROGRAM OFFERINGSCBIS Offers Pooled Funds through its CUIT and Global Funds plc (UCITS) Fund families

CUIT FUND BENCHMARK MANAGER(S)

CUIT Money Market Fund Bloomberg Barclays U.S. Short T-Bills (1-3M) Index Wellington

CUIT Short Bond Bloomberg Barclays 1-3 Year Treasury Index Longfellow

CUIT Intermediate Diversified Bond Bloomberg Barclays Aggregate Index Dodge & Cox, Jennison, Reams

CUIT Opportunistic Bond Bloomberg Barclays 1-5 Year US Gov’t Credit Index Longfellow and Reams

CUIT Balanced 60% S&P 500 / 40% BBAgg Dodge & Cox, Jennison, Reams, RhumbLine

CUIT Core Equity Index S&P 500 RhumbLine

CUIT Value Equity Russell 1000 Value Index AJO, Dodge & Cox

CUIT Growth Russell 1000 Growth Index LA Capital, Wellington

CUIT Small-Cap Equity Index S&P SmallCap 600 Index RhumbLine

CUIT International Equity MSCI ACWI Ex-U.S. Index Causeway, Principal Global, WCM

UCITS FUND BENCHMARK MANAGER(S)

European Short-Term Government Bond Bloomberg Barclays Euro Gov’t Bond Index 1-3 Year ARCA

World Bond Bloomberg Barclays Capital Global Aggregate Index Degroof Fund Management Company

European Equity MSCI Europe Index Degroof Fund Management Company

World Equity MSCI AC World IndexScott Investment Partners; Los Angeles Capital Management Equity Research

Note: CUIT Funds are available to tax-exempt Catholic institutions in the United States. CBIS Global (UCITS) Funds can be purchased in select countries around the world.

Investment Management ProcessCBIS hires institutional investment management firms to manage our institutional funds and separately managed portfolios. We typically combine two or more managers in actively managed funds in order to achieve our investment objective.

MANAGERIDENTIFICATIONAND SELECTION

PORTFOLIOCONSTRUCTION

ON-GOINGDUE DILIGENCE

Proven Investment Process

Defined Core Competency

Value add over a full market cycle

Preference for majority-owned firms

Assess CRI Impact

Diversification of manager core competencies

Improved risk-adjusted returns

Managed Active Share

Systematic evaluation process

Quantitative and qualitative assessment

Analyze any disconnect between expectations and reality

Investment Portfolio Review 1Q 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 10

Please review the Important Disclosures on page 32 for further information.

CUIT Funds Performance (March 31, 2018)

INVESTMENT OPTION/BENCHMARK1

MONTH3

MONTHS1

YEAR3

YEARS5

YEARS10

YEARSSINCE

INCEPTIONINCEPTION

DATE

CUIT Money Market Fund 0.12 0.32 1.08 0.52 0.33 0.32 3.24 Jan 1985

Bloomberg Barclays U.S. Short T-Bills (1-3 M) Index ± 0.13 0.33 1.05 0.51 0.32 0.33 3.66

CUIT Short Bond Fund 0.19 (0.06) 1.13 1.26 1.25 2.25 5.15 Jan 1985

Bloomberg Barclays 1-3 Year Treasury Index** 0.20 (0.16) (0.00) 0.38 0.50 1.12 4.95

CUIT Opportunistic Bond Fund Class A 0.07 (0.53) 0.72 1.25 * * 1.13 May 2013

CUIT Opportunistic Bond Fund Class B 0.08 (0.50) 0.87 1.40 * * 1.28 May 2013

Bloomberg Barclays 1-5 Year US Government/Credit Index 0.24 (0.50) 0.19 0.77 * * 0.90

CUIT Intermediate Diversified Bond Fund Class A 0.56 (1.24) 1.30 1.25 1.85 4.31 5.63 Jan 1995

CUIT Intermediate Diversified Bond Fund Class B 0.65 (1.13) 1.52 1.43 2.02 4.47 4.51 Jan 2003

Bloomberg Barclays Aggregate Bond Index 0.64 (1.46) 1.20 1.20 1.82 3.63 5.55 / 3.98

CUIT Balanced Fund (1.76) (0.87) 8.68 7.08 8.62 7.50 8.87 Dec 1983

60% S&P 500 / 40% BB Agg *** (1.24) (0.92) 8.89 7.10 8.81 7.52 9.55

CUIT Value Equity Fund Class A (2.53) (2.01) 10.96 7.87 11.07 8.17 9.66 Jan 1995

CUIT Value Equity Fund Class B (2.51) (1.92) 11.36 8.25 11.46 8.55 9.78 Jan 2003

Russell 1000 Value Index (1.76) (2.83) 6.95 7.88 10.78 7.78 10.02 / 9.19

CUIT Core Equity Index Fund Class A (2.51) (0.70) 14.88 10.50 13.10 9.08 9.67 Jan 1995

CUIT Core Equity Index Fund Class B (2.47) (0.63) 15.13 10.73 13.33 9.30 5.77 Mar 2000

S&P 500 Index (2.54) (0.76) 13.99 10.78 13.31 9.49 9.91 / 5.75

CUIT Growth Fund Class A (2.88) 1.68 18.31 11.18 13.97 9.65 8.70 Jan 1991

CUIT Growth Fund Class B (2.85) 1.74 18.66 11.52 14.33 9.98 9.12 Jan 2003

Russell 1000 Growth Index **** (2.74) 1.42 21.25 12.90 15.53 11.34 9.86 / 10.62

CUIT Small Capitalization Equity Index Fund Class A 1.97 0.56 12.62 8.27 11.18 9.47 7.13 Jan 2007

CUIT Small Capitalization Equity Index Fund Class B 2.00 0.63 12.97 8.58 11.50 9.79 7.43 Jan 2007

S&P SmallCap 600 Index § 2.04 0.57 13.09 8.80 11.72 9.97 7.66

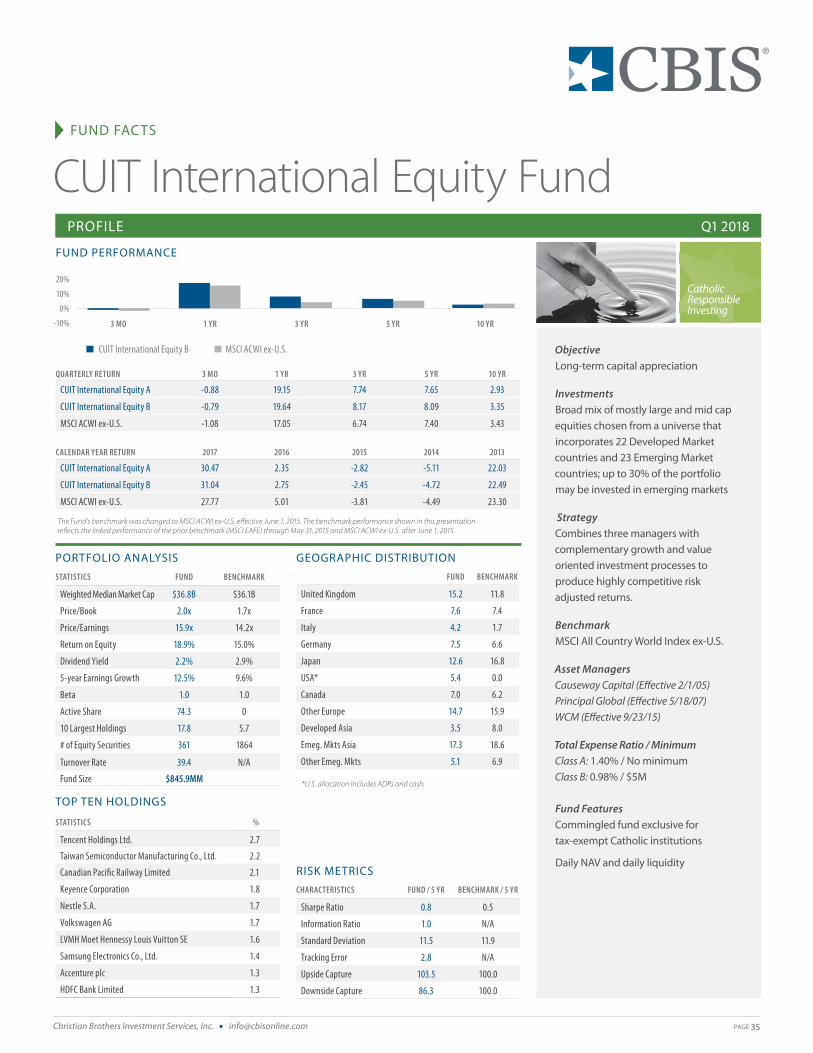

CUIT International Equity Fund Class A (0.88) (0.88) 19.15 7.74 7.65 2.93 6.21 Jan 1995

CUIT International Equity Fund Class B (0.86) (0.79) 19.64 8.17 8.09 3.35 2.68 Mar 2000

MSCI ACWI-ex U.S. ‡ (1.69) (1.08) 17.05 6.74 7.40 3.43 5.76 / 4.07

Investment Portfolio Review 1Q 2018

Christian Brothers Investment Services, Inc. n [email protected] PAGE 11

FUND FACTS

PROFILE Q1 2018

Christian Brothers Investment Services, Inc. (800) 592-8890 n [email protected]

CUIT Money Market Fund

Objective Preserve capital, provide current income; and maintain liquidity

InvestmentsHigh quality, short-term, fixed-income obligations

StrategyLiquidity will be maintained by investing in highly rated securities with short maturities and by constraining the average portfolio maturity to less than 90 days; credit and default risk are further minimized by diversifying among issuers; the Fund attempts to maintain a stable net asset value of $1.00 per unit.

BenchmarkBloomberg Barclays U.S. Short T-Bills (1-3 M) Index

Asset ManagersWellington Management Company (Effective 8/1/01)

Total Expense Ratio / Minimum 0.32% / No Minimum

Fund Features Commingled fund exclusive for tax-exempt Catholic institutions

Daily NAV and daily liquidity

Dividends Distributed Monthly

MATURITY DISTRIBUTION %

FUND

0 to 7 Days 26.4

8 to 29 Days 26.4

30 to 59 Days 18.1

60 to 89 Days 12.8

90 to 179 Days 9.6

180 and Over 6.8

PORTFOLIO ANALYSIS

STATISTICS FUND BENCHMARK

Effective Duration (years) 0.1 Yrs 0.1 Yrs

Average Quality A-1 A-1+

Yield-to-Maturity 1.9% 1.6%

Fund Size $62.1MM

CREDIT QUALITY %

FUND BENCHMARK

A-1+ or higher 71.7 100.0

A-1 25.5 0.0

Less than A-1 1.3 0.0

Cash 1.4 0.0

1.4%

5.0%

4.0%

3.0%

2.0%

1.0%

0.%

CUIT Money Market A BB U.S. Short T-Bills (1-3 M) Index

FUND PERFORMANCE

QUARTERLY RETURN 3 MO 1 YR 3 YR 5 YR 10 YR

CUIT Money Market 0.32 1.08 0.52 0.33 0.32

Bloomberg Barclays U.S. Short T-Bills (1-3 M) Index 0.33 1.05 0.51 0.32 0.33

CALENDAR YEAR RETURN 2017 2016 2015 2014 2013

CUIT Money Market 0.93 0.31 0.02 0.05 0.01

Bloomberg Barclays U.S. Short T-Bills (1-3 M) Index 0.81 0.33 0.05 0.04 0.07

Please see Important Information on Page 2

The Fund’s benchmark was changed to the Bloomberg Barclays U.S. Short Treasury Bills (1-3 Month) Index effective April 1, 2017. For periods prior to

April 1, 2017, the applicable benchmark was the Merrill Lynch 91-Day Treasury Bill Index.

3 MO 1 YR 3 YR 5 YR 10 YR

Christian Brothers Investment Services, Inc. n [email protected] PAGE 12Christian Brothers Investment Services, Inc. n [email protected] PAGE 2 | CB -FFS-000-0000

Important InformationBenchmark Index: The Fund’s benchmark was changed to the Bloomberg Barclays U.S. Short Treasury Bills (1-3 Month) Index effective April 1, 2017. For periods prior to April 1, 2017, the applicable benchmark was the Merrill Lynch 91-Day Treasury Bill Index. Performance for periods of one year and longer are annualized. All Fund performance is reported net of any fees and expenses, but inclusive of dividends and interest. Past performance is not indicative of future performance. The return and principal value of the Fund will fluctuate, and upon redemption, shares in the Fund may be worth less than their original cost. The comparative indices represent unmanaged or average returns on various financial assets which can be compared to the Fund’s total returns for the purpose of measuring relative performance, but are not necessarily intended to parallel the risk or investment approach of your investments. The indices do not incur taxes or expenses but are inclusive of dividends and interest. Comparative index information is provided by BNY Mellon Bank; information regarding composition of the indices may be obtained from our provider or CBIS.

Bloomberg Index Services Limited: BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

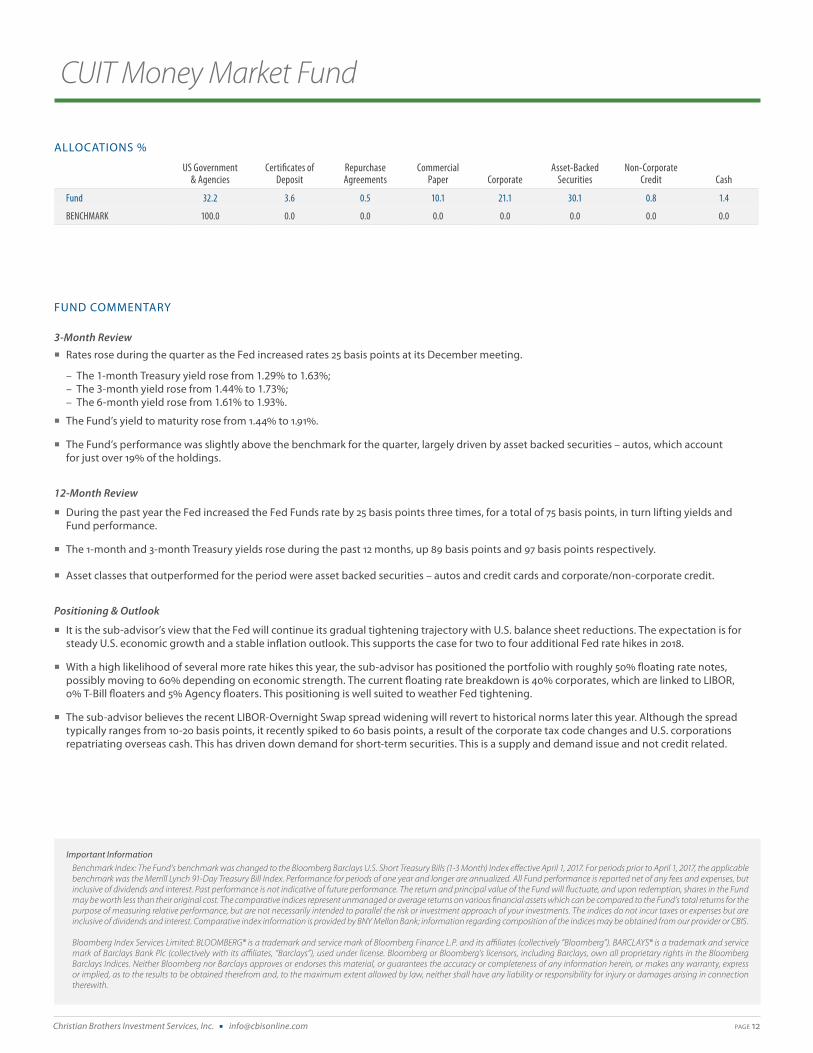

CUIT Money Market Fund

ALLOCATIONS %

US Government & Agencies

Certificates of Deposit

Repurchase Agreements

Commercial Paper Corporate

Asset-BackedSecurities

Non-Corporate Credit Cash

Fund 32.2 3.6 0.5 10.1 21.1 30.1 0.8 1.4

BENCHMARK 100.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

FUND COMMENTARY

3-Month Review

¡ Rates rose during the quarter as the Fed increased rates 25 basis points at its December meeting.

– The 1-month Treasury yield rose from 1.29% to 1.63%;– The 3-month yield rose from 1.44% to 1.73%;– The 6-month yield rose from 1.61% to 1.93%.

¡ The Fund’s yield to maturity rose from 1.44% to 1.91%.

¡ The Fund’s performance was slightly above the benchmark for the quarter, largely driven by asset backed securities – autos, which account for just over 19% of the holdings.

12-Month Review

¡ During the past year the Fed increased the Fed Funds rate by 25 basis points three times, for a total of 75 basis points, in turn lifting yields and Fund performance.

¡ The 1-month and 3-month Treasury yields rose during the past 12 months, up 89 basis points and 97 basis points respectively.

¡ Asset classes that outperformed for the period were asset backed securities – autos and credit cards and corporate/non-corporate credit.

Positioning & Outlook

¡ It is the sub-advisor’s view that the Fed will continue its gradual tightening trajectory with U.S. balance sheet reductions. The expectation is for steady U.S. economic growth and a stable inflation outlook. This supports the case for two to four additional Fed rate hikes in 2018.

¡ With a high likelihood of several more rate hikes this year, the sub-advisor has positioned the portfolio with roughly 50% floating rate notes, possibly moving to 60% depending on economic strength. The current floating rate breakdown is 40% corporates, which are linked to LIBOR, 0% T-Bill floaters and 5% Agency floaters. This positioning is well suited to weather Fed tightening.

¡ The sub-advisor believes the recent LIBOR-Overnight Swap spread widening will revert to historical norms later this year. Although the spread typically ranges from 10-20 basis points, it recently spiked to 60 basis points, a result of the corporate tax code changes and U.S. corporations repatriating overseas cash. This has driven down demand for short-term securities. This is a supply and demand issue and not credit related.

Christian Brothers Investment Services, Inc. n [email protected] PAGE 13

FUND FACTS

PROFILE Q1 2018

Christian Brothers Investment Services, Inc. (800) 592-8890 n [email protected]

CUIT Short Bond Fund

Objective Preserve capital while providing current income in excess of cash market yields with moderate emphasis on capital appreciation

InvestmentsU.S. government, agency, corporate, asset-backed and mortgage-backed securities with an average maturity of less than five years; up to 10% of the portfolio may be invested in securities rated below investment-grade (including U.S. dollar-denominated domestic, supranational or foreign issues)

StrategyFocuses on sector allocation and security selection, coupled with a top-down macroeconomic risk management process; aimed at minimizing downside risk while maximizing income potential

BenchmarkBloomberg Barclays 1–3 Year Treasury Index

Asset ManagersLongfellow Investment Management Co. (Effective 7/1/08)

Total Expense Ratio / Minimum 0.34% / No Minimum

Fund Features Commingled fund exclusive for tax-exempt Catholic institutions

Daily NAV and daily liquidity

Dividends Distributed Monthly

PORTFOLIO ANALYSIS

STATISTICS FUND BENCHMARK

Average Maturity (years) 2.1 Yrs 1.9 Yrs

Effective Duration (years) 1.7 Yrs 1.9 Yrs

Average Quality AA- AAA

Yield-to-Maturity 3.1% 2.3%

Current Yield 3.0% 1.8%

# of Securities 187 95

Fund Size $390.3MM

EFFECTIVE DURATION %

FUND BENCHMARK

< 1 Year 40.4 0.0

1 - 3 Years 46.8 100.0

3 - 5 Years 9.8 0.0

5 - 7 Years 2.6 0.0

7 - 10 Years 0.5 0.0

10 - 20 Years 0.0 0.0

> 20 Years 0.0 0.0

CREDIT QUALITY %

FUND BENCHMARK

AAA 58.9 100.0

AA 8.2 0

A 13.3 0

BBB 15.5 0

Below BBB 3.8 0

Cash 0.3 0

3%

2%

1%

0%

-1%

CUIT Short Bond A BB 1-3 Year Treasury Index

FUND PERFORMANCE

QUARTERLY RETURN 3 MO 1 YR 3 YR 5 YR 10 YR

CUIT Short Bond -0.06 1.13 1.26 1.25 2.25

Bloomberg Barclays 1-3 Year Treasury Index -0.16 0.00 0.38 0.50 1.12

CALENDAR YEAR RETURN 2017 2016 2015 2014 2013

CUIT Short Bond 1.71 1.99 0.81 1.37 0.84

Bloomberg Barclays 1-3 Year Treasury Index 0.42 0.86 0.54 0.62 0.36

Please see Important Information on Page 2 The Fund’s benchmark was changed to the Bloomberg Barclays 1-3 Year Treasury Index effective July 1, 2016. For periods prior to July 1, 2016, the applicable benchmarks were: ML 1-3 Yr Treasury Index effective 7/1/01.

3 MO 1 YR 3 YR 5 YR 10 YR

RISK METRICS

CHARACTERISTICS FUND / 5 YR BENCHMARK / 5 YR

Sharpe Ratio 1.6 0.3

Information Ratio 2.1 N/A

Standard Deviation 0.8 0.7

Tracking Error 0.5 N/A

Upside Capture 153.0 100.0

Downside Capture 36.5 100.0

Christian Brothers Investment Services, Inc. n [email protected] PAGE 14Christian Brothers Investment Services, Inc. n [email protected] PAGE 2 | CB -FFS-000-0000

Important InformationBenchmark Index: The Fund’s benchmark was changed to the Bloomberg Barclays 1-3 Year Treasury Index effective July 1, 2016. For periods prior to July 1, 2016, the applicable benchmarks were: ML 1-3 Yr Treasury Index effective 7/1/01; ML 1-5 Yr G/C Index effective 4/1/98; 50% LB Intermediate Government /50% LB 1-3 Yr Government effective 5/1/96; LB 1-3 Yr Government in prior periods. The performance shown for SBF reflects the linked performance of these benchmarks for each applicable period. Characteristics presented for the Short Bond Fund were also compiled using data from Barclays Capital U.S. 1-3 Year Treasury Bond Index. Performance for periods of one year and longer are annualized. All Fund performance is reported net of any fees and expenses, but inclusive of dividends and interest. Past performance is not indicative of future performance. The return and principal value of the Fund will fluctuate, and upon redemption, shares in the Fund may be worth less than their original cost. The comparative indices represent unmanaged or average returns on various financial assets which can be compared to the Fund’s total returns for the purpose of measuring relative performance, but are not necessarily intended to parallel the risk or investment approach of your investments. The indices do not incur taxes or expenses but are inclusive of dividends and interest. Comparative index information is provided by BNY Mellon Bank; information regarding composition of the indices may be obtained from our provider or CBIS.

Bloomberg Index Services Limited: BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

CBIS offers pooled funds on behalf of a not-for-profit investment trust, the Catholic United Investment Trust (CUIT) Offering Memorandum, which contains further information, is available by calling 800-592-8890. Such information should be carefully considered prior to investing in the Fund. Commingled Fund exclusively for tax-exempt Catholic institutions. All assets are invested in accordance with CBIS’ Catholic Responsible Investing Guidelines. Total expense ratio includes management fee and all other fees (accounting, custody and transfer agent). The Funds provide daily NAV and daily liquidity.

CUIT Short Bond Fund

ALLOCATIONS %

Treasuries Agency Industrials Finance Utilities MBS CMO CMBS ABS Municipals Cash

Fund 23.5 8.7 13.6 17.0 1.7 1.6 1.3 10.8 18.9 2.7 0.3

Benchmark 100.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

FUND COMMENTARY

3-Month Review ¡ The Fed increased benchmark interest rate to 1.50-1.75% in March. As a result, yields rose about 40 basis points across short to intermediate

areas of the curve.

¡ The Fund’s strongest source of return, approximately10 basis points, was its shorter relative duration to the benchmark (1.7 vs. 1.9).

¡ The combination of sector and security selection added modestly to overall outperformance of the Fund.

¡ Curve positioning was neutral for the period.

12-Month Review

¡ The Fund’s combined allocation to corporates and securitized bonds contributed approximately 80 basis points of income advantage over the all-Treasury index. Allocations to financials, industrials, asset backed and commercial mortgage backed securities were additive.

¡ Shorter duration and curve positioning together added approximately 45 basis points to overall performance as yields increased on the front end of the curve.

¡ Security selection added modestly to results.

Positioning & Outlook

¡ The sub-advisor expects modest economic growth in the 2-3% range for 2018 and continues to seek added income from non-Treasury holdings.

¡ The Fund maintains duration slightly below the benchmark in anticipation of the Fed’s desire to raise rates.

¡ Emphasis on industrials, financials, asset backed, and commercial mortgage backed issues provide attractive opportunities to generate stable cash flow in the Fund.

¡ Curve positioning remains “barbelled” versus the benchmark, with an overweight in the 0-1 and 3-5 year duration buckets.

¡ The portfolio maintains close to a 4% exposure to high-yield bonds; the sub-advisor will continue to emphasize upgrade and take-out opportunities within the industrial sector.

Christian Brothers Investment Services, Inc. n [email protected] PAGE 15

FUND FACTS

PROFILE Q1 2018

Christian Brothers Investment Services, Inc. (800) 592-8890 n [email protected]

CUIT Opportunistic Bond Fund

Objective Current income and long-term capital appreciation

InvestmentsU.S. government, agency, corporate, and mortgage-backed securities; primarily investment grade with no more than 20% of the portfolio rated below BBB; up to a 10% allocation to merger/arbitrage sector

StrategyUses top down macroeconomic analysis, along with fundamental industry and company research, to capture inefficiencies in the valuation of sectors and individual securities; this is combined with duration management (+/– 2.5 years of the benchmark) in pursuit of above-benchmark returns over a full market cycle

BenchmarkBloomberg Barclays 1-5 Year Government/Credit Index

Asset ManagersLongfellow Investment Management (Effective 5/1/13); Reams AssetManagement Co. (Effective 5/1/13)

Total Expense Ratio/MinimumClass A: 0.56% / No MinimumClass B: 0.41% / $5M

Fund Features Commingled fund exclusive for tax-exempt Catholic institutions

Daily NAV and daily liquidity

Dividends Distributed Monthly

PORTFOLIO ANALYSIS

STATISTICS FUND BENCHMARK

Average Maturity (years) 3.0 Yrs 2.8 Yrs

Effective Duration (years) 2.5 Yrs 2.7 Yrs

Average Quality A+ AA

Yield-to-Maturity 3.4% 2.6%

Current Yield 3.1% 2.3%

# of Securities 347 2,847

Fund Size $471.8MM

EFFECTIVE DURATION %

FUND BENCHMARK

< 1 Year 15.4 2.9

1 - 3 Years 52.8 59.2

3 - 5 Years 27.8 37.9

5 - 7 Years 3.6 0.0

7 - 10 Years 0.4 0.0

10 - 20 Years 0.1 0.0

> 20 Years 0.0 0.0

CREDIT QUALITY %

FUND BENCHMARK

AAA 38.8 68.7

AA 5.1 6.0

A 19.1 13.0

BBB 25.0 12.2

Below BBB 4.2 0.0

Merger/Arbitrage 6.7 0.0

Cash 1.0 0.0

2%

1%

0%

-1%

CUIT Opport. Bond B Bloomberg Barclays 1-5 Yr Gov't/Credit

FUND PERFORMANCE

QUARTERLY RETURN 3 MO 1 YR 3 YR 5 YR 10 YR

CUIT Opport. Bond A -0.53 0.72 1.25 – –

CUIT Opport. Bond B -0.50 0.87 1.40 – –

Bloomberg Barclays 1-5 Year Government/Credit -0.50 0.19 0.77 – –

CALENDAR YEAR RETURN 2017 2016 2015 2014 2013

CUIT Opport. Bond A 1.63 2.54 0.98 1.23 –

CUIT Opport. Bond B 1.78 2.69 1.23 1.27 –

Bloomberg Barclays 1-5 Year Government/Credit 1.27 1.56 0.97 1.42 –

Please see Important Information on Page 2

3 MO 1 YR 3 YR 5 YR 10 YR

*Allocations exclude M&A.

RISK METRICS

CHARACTERISTICS FUND / 3 YR BENCHMARK / 3 YR

Sharpe Ratio 1.3 0.2

Information Ratio 1.6 N/A

Standard Deviation 1.0 1.2

Tracking Error 0.7 N/A

Upside Capture 113.1 100.0

Downside Capture 34.1 100.0

Christian Brothers Investment Services, Inc. n [email protected] PAGE 16Christian Brothers Investment Services, Inc. n [email protected] PAGE 2 | CB -FFS-000-0000

Important InformationBenchmark Index: Bloomberg Barclays 1–5 Year U.S. Govt/Credit Index. Performance for periods of one year and longer are annualized. All Fund performance is reported net of any fees and expenses, but inclusive of dividends and interest. Past performance is not indicative of future performance. The return and principal value of the Fund will fluctuate, and upon redemption, shares in the Fund may be worth less than their original cost. The comparative index represents unmanaged or average returns on various financial assets which can be compared to the Fund’s total returns for the purpose of measuring relative performance, but is not necessarily intended to parallel the risk or investment approach of your investments. The index does not incur taxes or expenses but is inclusive of dividends and interest. Comparative index information is provided by BNY Mellon Bank; information regarding composition of the index may be obtained from our provider or CBIS.

Bloomberg Index Services Limited: BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

CUIT Opportunistic Bond Fund

ALLOCATIONS %

Treasuries Agency Industrials Finance Utilities Sovereign MBS CMO CMBS ABS MunicipalsMerger/

Arbitrage Cash

Fund 14.9 1.6 22.0 21.4 1.6 0.0 3.6 0.7 11.2 11.6 3.7 6.7 1.0

Benchmark 60.8 6.6 14.8 11.5 1.1 0.6 0.0 0.0 0.0 0.0 0.7 0.0 0.0

All attribution is based on gross portfolio performance.

Active Weights

-45.9%

Treasuries

-5.0%

Agency 3.6%

MBS

0.7%CMO

3.0%

Municipals

6.7%

M&A

1.0%

Cash

7.2%

Industrials

9.9%

Finance0.5%Utilies -0.6%

Sovereign11.2% 11.6%

CMBS ABS

FUND COMMENTARY

3-Month Review ¡ The Fund’s relatively shorter duration (2.5 vs. 2.7) was the main driver of excess returns as yields rose during the quarter.

¡ Curve positioning was neutral for the period.

¡ Security selection added modestly to offset the negative drag caused by key areas such as financials and industrials.

¡ The Fund’s merger and arbitrage sleeve lagged the index due to a difficult regulatory environment and concerns around the uncertain timeline for deal approvals.

12-Month Review ¡ Sector allocation was additive (+79 basis points), due to the Fund’s overweight in the outperforming securitized and corporate sectors.

An underweight to Treasuries also benefitted results.

¡ Over the period, the Fund’s relative shorter duration added 18 basis points to performance.

¡ Curve positioning benefitted due to longer relative to benchmark exposure 5+ years.

¡ Security selection was additive (+27 basis points) largely from strength among corporates; industrial issues contributed 17 basis points.

¡ The merger and arbitrage strategy outperformed the Index and was additive for the trailing 12-month period.

Positioning & Outlook ¡ The Fund continues to maintain shorter duration than the benchmark. Positioning remains defensive given the likelihood of continued Fed

tightening.

¡ The sub-advisor continues to emphasize corporates and securitized sectors with a corresponding underweight to Treasuries. Allocation to industrials, financials, ABS and CMBS remains near 70% of the Fund’s sector exposure.

¡ Curve positioning continues to overweight 0-1 year securities with a significant relative underweight to 3-5 year exposure.

¡ The Fund maintains approximately a 7% allocation to the merger and arbitrage strategy. The sub-advisor seeks to find pockets of opportunity in deals that have the most attractive risk/reward, but where there appears to be a defined path to close.

Christian Brothers Investment Services, Inc. n [email protected] PAGE 17

FUND FACTS

PROFILE Q1 2018

Christian Brothers Investment Services, Inc. (800)-592-8890 n [email protected]

CUIT Int. Diversified Bond Fund

Objective Current income and long-term capital appreciation

InvestmentsU.S. government, agency, corporate, and mortgage-backed securities; holdings are primarily investment grade (BBB to AAA, based on the three primary rating agencies)

StrategyUses top down macroeconomic analysis, along with fundamental research, to capture inefficiencies in the valuation of sectors and individual securities; combined with duration management (+/– 20% of the benchmark) in pursuit of above-benchmark returns over a full market cycle

BenchmarkBloomberg Barclays Aggregate Bond Index

Asset ManagersDodge & Cox, Inc. (Effective 1/1/95); Jennison Associates (Effective 9/2/02); Reams Asset Management Co. (Effective 7/1/08)

Total Expense Ratio/MinimumClass A: 0.53% / No MinimumClass B: 0.38% / $5M

Fund Features Commingled fund exclusive for tax-exempt Catholic institutions

Daily NAV and daily liquidity

Dividends Distributed Monthly

PORTFOLIO ANALYSIS

STATISTICS FUND BENCHMARK

Average Maturity (years) 7.8 Yrs 8.3 Yrs

Effective Duration (years) 5.7 Yrs 6.0 Yrs

Average Quality AA+ AA

Yield-to-Maturity 3.2% 3.1%

Current Yield 3.1% 3.1%

# of Securities 744 9,826

Fund Size $1,239.5MM

EFFECTIVE DURATION %

FUND BENCHMARK

< 1 Year 8.2 1.1

1 - 3 Years 19.6 22.2

3 - 5 Years 29.3 28.9

5 - 7 Years 24.6 26.0

7 - 10 Years 6.4 7.4

10 - 20 Years 11.4 14.2

> 20 Years 0.4 0.2

CREDIT QUALITY %

FUND BENCHMARK

AAA 65.2 71.6

AA 4.2 3.8

A 11.0 11.2

BBB 16.2 13.3

Below BBB 2.4 0.0

Cash 1.2 0.0

6%

4%

2%

0%

-2%

CUIT Int. Divers. Bond B Bloomberg Barclays Aggregate Bond Index

FUND PERFORMANCE

QUARTERLY RETURN 3 MO 1 YR 3 YR 5 YR 10 YR

CUIT Int. Divers. Bond A -1.24 1.30 1.25 1.85 4.31

CUIT Int. Divers. Bond B -1.13 1.52 1.43 2.02 4.47

Bloomberg Barclays Aggregate Bond Index -1.46 1.20 1.20 1.82 3.63

CALENDAR YEAR RETURN 2017 2016 2015 2014 2013

CUIT Int. Divers. Bond A 3.38 3.53 -0.13 5.65 -1.73

CUIT Int. Divers. Bond B 3.54 3.69 -0.05 5.81 -1.51

Bloomberg Barclays Aggregate Bond Index 3.54 2.65 0.55 5.97 -2.02

Please see Important Information on Page 2

3 MO 1 YR 3 YR 5 YR 10 YR

RISK METRICS

CHARACTERISTICS FUND / 5 YR BENCHMARK / 5 YR

Sharpe Ratio 0.7 0.5

Information Ratio 0.9 N/A

Standard Deviation 2.8 2.9

Tracking Error 0.7 N/A

Upside Capture 100.9 100.0

Downside Capture 83.2 100.0

Christian Brothers Investment Services, Inc. n [email protected] PAGE 18Christian Brothers Investment Services, Inc. n [email protected] PAGE 2

CUIT Int. Diversified Bond Fund

ALLOCATIONS %

Treasuries Agency Industrials Finance Utilities Supranational Sovereign MBS CMO CMBS ABS MunicipalsCovered Bonds

Merger Arbitrage Cash

Fund 41.0 0.7 16.2 13.9 1.7 0.0 0.0 18.8 1.0 1.9 2.5 1.2 0.0 0.0 1.2

Benchmark 37.2 3.3 15.4 8.1 1.8 1.6 1.0 28.2 0.0 1.9 0.5 1.0 0.1 0.0 0.0

All attribution is based on gross portfolio performance.

Active Weights

3.8%

Treasuries

-2.6%

0.8%Agency

-1.0%

Sovereign

-9.4%

MBS

2.0%

0.2%1.2%

0.0%ABS Municipals CashMerger

Arbitrage

CoveredBonds

Industrials

5.8%

Finance -0.1% -0.1%

Utilies

-1.6%

Supranational 1.0%CMO

0.0%CMBS

Christian Brothers Investment Services, Inc. n [email protected] PAGE 3 | CB -FFS-000-0000

CUIT Int. Diversified Bond Fund

Important InformationBenchmark Index: Bloomberg Barclays Aggregate Bond Index. Performance for periods of one year and longer are annualized. All Fund performance is reported net of any fees and expenses, but inclusive of dividends and interest. Past performance is not indicative of future performance. The return and principal value of the Fund will fluctuate, and upon redemption, shares in the Fund may be worth less than their original cost. The comparative index represents unmanaged or average returns on various financial assets which can be compared to the Fund’s total returns for the purpose of measuring relative performance, but is not necessarily intended to parallel the risk or investment approach of your investments. The index does not incur taxes or expenses but is inclusive of dividends and interest. Comparative index information is provided by BNY Mellon Bank; information regarding composition of the index may be obtained from our provider or CBIS.

Bloomberg Index Services Limited: BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

CBIS offers pooled funds on behalf of a not-for-profit investment trust, the Catholic United Investment Trust (CUIT) Offering Memorandum, which contains further information, is available by calling 800-592-8890. Such information should be carefully considered prior to investing in the Fund. Commingled Fund exclusively for tax-exempt Catholic institutions. All assets are invested in accordance with CBIS’ Catholic Responsible Investing Guidelines. Total expense ratio includes management fee and all other fees (accounting, custody and transfer agent). The Funds provide daily NAV and daily liquidity.

FUND COMMENTARY

3-Month Review ¡ The Fund’s duration positioning, shorter than the benchmark, was the largest contributor to outperformance for the quarter (+24 basis points).

¡ Curve positioning was a neutral as the curve shifted in parallel for the quarter.

¡ Sector allocation was slightly negative (-3 basis points), primarily due to the 4.1% bank sector overweight.

¡ Security selection was positive (+10 basis points) for the quarter. Corporate names in the industrial and financial sectors were the primary drivers.

12-Month Review

¡ The Fund’s shorter than benchmark duration positioning was positive (+49 basis points). Over the period, the Fund’s duration modestly increased from 5.4 years to 5.7 years.

¡ Curve positioning was a slight negative due to a flattening with no change to the 30-year.

¡ Sector exposure was additive (+8 basis points), largely due the Fund’s 6.2% overweight to corporates.

¡ Security selection was a slight detractor (-5 basis points) due primarily to Treasuries and agencies and offset by corporates and government related.

Positioning & Outlook

¡ The Fund’s sub-advisors are all in a defensive mode due to historically tight spreads and a lack of volatility. They are poised to take advantage of opportunities as they emerge.

¡ The Fund’s effective duration continues to be slightly below benchmark (5.7 vs 6.0 years) as the sub-advisors expectations of continued Fed rate increases and improved economic conditions continue.

¡ The Fund’s curve positioning remains similar to last quarter with an overweight to 0-3 year securities and a slight underweight to 10+ years. During the quarter the sub-advisors increased 5-7 year maturity holdings by about 7% due to relative valuation opportunities.

¡ The Fund’s sector allocation remains similar to the previous quarter end. Overweight sectors are Treasuries (+5%) and corporates (+5%), primarily in Bank names. The largest underweight position is the mortgage backed securities sector (-8%).

Christian Brothers Investment Services, Inc. n [email protected] PAGE 19

Christian Brothers Investment Services, Inc. n [email protected] PAGE 20

FUND FACTS

PROFILE Q1 2018

Christian Brothers Investment Services, Inc. (800) 592-8890 n [email protected]

CUIT Balanced Fund

Objective Long-term capital appreciation and current income

InvestmentsThe equity allocation is comprised primarily of large-cap U.S. companies diversified across industry sectors. Fixed-income instruments include corporate, U.S. government and agency bonds, and asset-backed and mortgage-backed securities.

StrategyThe equity portion blends undervalued companies with a modest exposure to growth through a core equity index allocation. The fixed-income portion leverages economic and fundamental research in an attempt to identify and capture inefficiencies across the yield curve.

Benchmark60% S&P 500 Index / 40% Bloomberg Barclays Aggregate Bond Index

Asset ManagersFixed Income: Dodge & Cox, Inc. (Effective 4/1/91); Jennison Associates(Effective 9/2/02); Reams Asset Management Co. (Effective 7/1/08)

Equities: Dodge & Cox, Inc. – (Effective 4/1/91); RhumbLine Advisers – (Effective 4/1/02)

Total Expense Ratio / Minimum 0.89% / No Minimum

Fund Features Commingled fund exclusive for tax-exempt Catholic institutions

Daily NAV and daily liquidity

Dividends Distributed Monthly

PORTFOLIO ANALYSIS

STATISTICS FUND S&P 500

Weighted Median Market Cap $70.3B $100.5B

Price/Book 2.3x 3.1x

Price/Earnings 17.4x 21.4x

Return on Equity 16.2% 19.8%

Dividend Yield 1.6% 1.9%

5-year Earnings Growth 8.7% 9.5%

Beta 1.0 1.0

10 Largest Holdings 27.6 11.7

# of Equity Securities 474 507

Fund Size $230.3MM

TOP TEN HOLDINGS

STATISTICS %

Microsoft Corporation 3.4

Alphabet Inc. 3.2

Bank of America Corporation 3.1

Charles Schwab Corporation 3.0

Wells Fargo & Company 2.8

Capital One Financial Corporation 2.8

JPMorgan Chase & Co. 2.5

Comcast Corporation 2.3

Twenty-First Century Fox, Inc. 2.3

Goldman Sachs Group, Inc. 2.2

PORTFOLIO ANALYSIS: FIXED INCOME

STATISTICS FUND BBAgg

Average Maturity 7.8 8.3

Effective Duration (years) 5.7 6.0

Average Quality AA AA

Yield-to-Maturity 3.2% 3.1%

Current Yield 3.1% 3.1%

# of Securities 439 9,826

EFFECTIVE DURATION FUND BBAgg

< 1 Year 6.1 1.1

1 - 3 Years 20.8 22.2

3 - 5 Years 31.0 28.9

5 - 7 Years 24.4 26.0

7 - 10 Years 6.2 7.4

10 - 20 Years 11.1 14.2

> 20 Years 0.4 0.2

18%

10%

8%

6%

4%

2%

0%

-2%

CUIT Balanced Fund 60% S&P 500 / 40% BB Agg

FUND PERFORMANCE

% AVERAGE ANNUAL RETURN 3 MO 1 YR 3 YR 5 YR 10 YR

CUIT Balanced -0.87 8.68 7.08 8.62 7.50

60% S&P 500 Index / 40% Bloomberg Barclays Aggregate Bond -0.92 8.89 7.10 8.81 7.52

CALENDAR YEAR RETURN 2017 2016 2015 2014 2013

CUIT Balanced 13.08 12.05 -2.33 8.80 21.29

60% S&P 500 Index / 40% Bloomberg Barclays Aggregate Bond 14.25 8.31 1.28 10.62 17.56

Please see Important Information on Page 2

3 MO 1 YR 3 YR 5 YR 10 YR

Christian Brothers Investment Services, Inc. n [email protected] PAGE 21Christian Brothers Investment Services, Inc. n [email protected] PAGE 2

CUIT Balanced Fund

MARKET SECTOR ANALYSIS % – EQUITY

ConsumerDiscretionary

ConsumerStaples Energy Financials Healthcare Industrials

InformationTechnology Materials Real Estate

Telecomm Service Utilities Cash

Fund 16.7 2.5 7.6 26.0 9.4 7.3 22.4 2.0 1.1 1.8 1.0 2.2

Benchmark 12.7 7.7 5.7 14.8 13.7 10.2 24.8 2.8 2.8 1.9 2.8 0.0

All attribution is based on gross portfolio performance.

Active Weights

4.0%

1.9%

11.2%

ConsumerDiscretionary

Energy Energy

-5.2%

ConsumerStaples

-2.9% -2.4%-1.7% -1.8%

-0.1%-0.8%

IndustrialsInformationTechnology Real Estate Real Estate

TelecommServiceMaterials

2.2%

Cash

-4.3%

Healthcare

MARKET SECTOR ANALYSIS % – FIXED INCOME

Treasuries Agency Industrials Finance Utilities Supranational Sovereign MBS CMO CMBS ABS MunicipalsCovered Bonds

Merger Arbitrage Cash

Fund 41.8 0.6 15.4 12.5 1.6 0.0 0.0 19.5 0.9 1.7 3.0 0.8 0.0 0.0 2.2

Benchmark 37.2 3.3 15.4 8.1 1.8 1.6 1.0 28.2 0.0 1.9 0.5 1.0 0.1 0.0 0.0

Industrials

All attribution is based on gross portfolio performance.

Active Weights

4.6%

Treasuries

-2.7%

0.0%Agency

-1.0%

-8.7%

Sovereign MBS

2.5%2.2%

0.0%ABS

Municipals

CashMergerArbitrage

CoveredBonds

4.4%

Finance -0.2% -0.2%-0.2% -0.1%

Utilies

-1.6%

Supranational 0.9%CMO

CMBS

Christian Brothers Investment Services, Inc. n [email protected] PAGE 3 | CB -FFS-000-0000

Important InformationBenchmark Index: The Fund’s benchmark was changed to 60% S&P 500 Index / 40% Bloomberg Barclays Aggregate effective January 2, 2003. For prior periods, the applicable benchmark was 60% S&P 500 Index / 30% LB Aggregate / 10% T-Bill. Performance for periods of one year and longer are annualized. All Fund performance is reported net of any fees and expenses, but inclusive of dividends and interest. Past performance is not indicative of future performance. The return and principal value of the Fund will fluctuate, and upon redemption, shares in the Fund may be worth less than their original cost. The comparative indices represent unmanaged or average returns on various financial assets which can be compared to the Fund’s total returns for the purpose of measuring relative performance, but are not necessarily intended to parallel the risk or investment approach of your investments. The indices do not incur taxes or expenses but are inclusive of dividends and interest. Comparative index information is provided by BNY Mellon Bank; information regarding composition of the indices may be obtained from our provider or CBIS.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC or its affiliates ("SPDJI"), and has been licensed for use by CBIS. Standard & Poor's® and S&P® are registered trademarks of Standard & Poor's Financial Services LLC ("S&P"); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC ("Dow Jones"); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by CBIS. The CUIT Core Equity Index Fund is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, or their respective affiliates and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index.

Bloomberg Index Services Limited: BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

CBIS offers pooled funds on behalf of a not-for-profit investment trust, the Catholic United Investment Trust (CUIT) Offering Memorandum, which contains further information, is available by calling 800-592-8890. Such information should be carefully considered prior to investing in the Fund. Commingled Fund exclusively for tax-exempt Catholic institutions. All assets are invested in accordance with CBIS’ Catholic Responsible Investing Guidelines. Total expense ratio includes management fee and all other fees (accounting, custody and transfer agent). The Funds provide daily NAV and daily liquidity.

FUND COMMENTARY

3-Month Review ¡ The equity component of the Fund trailed the S&P 500 by a small amount (-32 basis points); the fixed income composite finished ahead of the

Barclays U.S. Aggregate index.

¡ The style tilt of the equity component detracted as value oriented sub-advisor Dodge & Cox did not keep pace with the S&P 500, although it was well ahead of the Russell 1000 Value. This was the case in Q1 and has been for much of the past five years.

¡ Overall stock selection results were weakest in consumer discretionary (media & retail), financials, and healthcare.

¡ The Fund’s fixed income duration positioning, shorter than the benchmark, was the largest contributor to outperformance for the quarter (+24 basis points).

12-Month Review

¡ The Fund underperformed the index over the trailing 12-month period primarily because of the value tilt of the equity allocation and weak stock selection (combined -83 basis points). The fixed income component added value.

¡ The largest negatives for relative performance were media holdings in the consumer discretionary sector of the Dodge & Cox portfolio. The passive index strategy outperformed, driven by the absence of industrial conglomerate GE and several weak performing pharmaceutical stocks.

¡ The fixed income segment’s shorter than benchmark duration positioning was positive (+45 basis points). Over the period, the Fund’s duration modestly increased from 5.5 to 5.7 years.

Positioning & Outlook

¡ The Fund maintains a value tilt within the equity allocation. This has hindered relative performance in the short term, but is generally beneficial over longer time periods.

¡ Within the equity portfolio, the Fund is overweight financials, consumer discretionary (predominately media companies), and energy.

¡ The equity portfolio is underweight consumer staples (predominately tobacco), industrials, healthcare, information technology, utilities, and real estate.

¡ The Fund’s fixed income sub-advisors are all in a defensive mode due to historically tight spreads and a lack of volatility. They are poised to take advantage of opportunities as they emerge.

¡ The Fund’s effective duration continues to be slightly below benchmark (5.7 vs 6.0 years) as the sub-advisors expectations of continued Fed rate increases and improved economic conditions continue.

CUIT Balanced Fund

Christian Brothers Investment Services, Inc. n [email protected] PAGE 22

Christian Brothers Investment Services, Inc. n [email protected] PAGE 23

FUND FACTS

PROFILE Q1 2018

Christian Brothers Investment Services, Inc. (800) 592-8890 n [email protected]

CUIT Core Equity Index Fund

Objective Long-term capital appreciation

InvestmentsCommon stocks of companies that make up the S&P 500, except those excluded as a result of CBIS’ screens (about 6% of the S&P 500's constituent companies – all unscreened companies are held at their index weight or higher)

StrategyTrack the S&P 500 and counter the impact of screens by overweighting select holdings so that the Fund's broadquantitative characteristics match those of the S&P 500 as closely as possible

BenchmarkS&P 500 Index

Asset ManagersRhumbLine Advisers (Effective 1/1/95)

Total Expense Ratio / Minimum Class A: 0.38% / No MinimumClass B: 0.18% / $3M

Fund Features Commingled fund exclusive for tax-exempt Catholic institutions

Daily NAV and daily liquidity

Dividends Distributed Quarterly

PORTFOLIO ANALYSIS

STATISTICS FUND BENCHMARK

Weighted Median Market Cap $86.7B $100.5B

Price/Book 3.1x 3.1x

Price/Earnings 21.3x 21.4x

Return on Equity 20.3% 19.8%

Dividend Yield 1.8% 1.9%

5-year Earnings Growth 10.5% 9.5%

Beta 1.0 1.0

Active Share 14.9 0

10 Largest Holdings 22.9 20.6

# of Equity Securities 465 507

Fund Size $1,847.2MM

TOP TEN HOLDINGS

STATISTICS %

Apple Inc. 3.9

Microsoft Corporation 3.4

Alphabet Inc. 3.0

Amazon.com, Inc. 2.6

Berkshire Hathaway Inc. 2.6

Facebook, Inc. 1.8

JPMorgan Chase & Co. 1.7

Exxon Mobil Corporation 1.5

Bank of America Corporation 1.3

3M Company 1.2

20%

15%

10%

5%

0%

-5%

CUIT Core Equity B S&P 500 Index

RISK METRICSCHARACTERISTICS FUND / 5 YR BENCHMARK / 5 YR

Sharpe Ratio 1.3 1.3

Information Ratio 0.4 N/A

Standard Deviation 10.0 9.9

Tracking Error 0.6 N/A

Upside Capture 101.9 100.0

Downside Capture 101.7 100.0

FUND PERFORMANCE

QUARTERLY RETURN 3 MO 1 YR 3 YR 5 YR 10 YR

CUIT Core Equity A -0.70 14.87 10.49 13.10 9.08

CUIT Core Equity B -0.63 15.12 10.72 13.32 9.30

S&P 500 Index -0.76 13.99 10.78 13.31 9.49

CALENDAR YEAR RETURN 2017 2016 2015 2014 2013

CUIT Core Equity A 22.64 11.27 0.29 13.99 32.03

CUIT Core Equity B 22.87 11.51 0.50 14.19 32.31

S&P 500 Index 21.83 11.96 1.38 13.69 32.39

Please see Important Information on Page 2 The Fund’s benchmark was changed to the Bloomberg Barclays 1-3 Year Treasury Index effective July 1, 2016. For periods prior to July 1, 2016, the applicable benchmarks were: ML 1-3 Yr Treasury Index effective 7/1/01.

3 MO 1 YR 3 YR 5 YR 10 YR

Christian Brothers Investment Services, Inc. n [email protected] PAGE 24Christian Brothers Investment Services, Inc. n [email protected] PAGE 2

CUIT Core Equity Index Fund

MARKET SECTOR ANALYSIS %

Consumer Discretionary

Consumer Staples Energy Financials Healthcare Industrials

Information Technology Materials Real Estate

TelecommService Utilities Cash

Fund 12.9 7.5 5.7 15.6 11.7 9.0 25.4 3.2 3.3 2.0 3.0 0.7

Benchmark 12.7 7.7 5.7 14.8 13.7 10.2 24.8 2.8 2.8 1.9 2.8 0.0

All attribution is based on gross portfolio performance.

Active Weights0.2% 0.4% 0.2%

-0.2%0.0%

0.6% 0.7%0.8%

-1.2%-2.0%

0.5%0.1%

Consumer Discretionary

InformationTechnology

Materials Cash

ConsumerStaples

Energy Financials

Healthcare Industrials

RealEstate

TelecommService

Utilities

Christian Brothers Investment Services, Inc. n [email protected] PAGE 25Christian Brothers Investment Services, Inc. n [email protected] PAGE 3 | CB -FFS-000-0000

Important InformationBenchmark Index: S&P 500 Index. Performance for periods of one year and longer are annualized. All Fund performance is reported net of any fees and expenses, but inclusive of dividends and interest. Past performance is not indicative of future performance. The return and principal value of the Fund will fluctuate, and upon redemption, shares in the Fund may be worth less than their original cost. The comparative index represents unmanaged or average returns on various financial assets which can be compared to the Fund’s total returns for the purpose of measuring relative performance, but is not necessarily intended to parallel the risk or investment approach of your investments. The index does not incur taxes or expenses but is inclusive of dividends and interest. Comparative index information is provided by BNY Mellon Bank; information regarding composition of the index may be obtained from our provider or CBIS.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC or its affiliates ("SPDJI"), and has been licensed for use by CBIS. Standard & Poor's® and S&P® are registered trademarks of Standard & Poor's Financial Services LLC ("S&P"); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC ("Dow Jones"); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by CBIS. The CUIT Core Equity Index Fund is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, or their respective affiliates and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index.

CBIS offers pooled funds on behalf of a not-for-profit investment trust, the Catholic United Investment Trust (CUIT) Offering Memorandum, which contains further information, is available by calling 800-592-8890. Such information should be carefully considered prior to investing in the Fund. Commingled Fund exclusively for tax-exempt Catholic institutions. All assets are invested in accordance with CBIS’ Catholic Responsible Investing Guidelines. Total expense ratio includes management fee and all other fees (accounting, custody and transfer agent). The Funds provide daily NAV and daily liquidity.

CUIT Core Equity Index Fund

FUND COMMENTARY

3-Month Review ¡ The Fund was slightly overweight in the best performing information technology sector, adding 3 basis points to relative return in the quarter.

¡ Pharmaceutical companies had returns averaging -3.0% in Q1. The Fund did not hold most of those companies and redeployed assets into much stronger performing biotech stocks, adding 30 basis points in the quarter.

¡ Tobacco screens by themselves added 9 basis points; however, re-weighting into other industries within consumer staples offset much of that gain.

¡ Aerospace and defense company screens hindered relative performance in the quarter, as those stocks had 8.2% average gains. The restriction on GE added 14 basis points in the quarter. In total the relative performance impact was -16 basis points for the industrials sector.

¡ There were no significant performance differentials in the remaining sectors.

12-Month Review

¡ The largest contributors to the Fund’s outperformance in the 12-month period were noted in healthcare and industrials holdings.

¡ In healthcare, the large underweight in pharmaceuticals, together with the specific performance of the Fund’s pharma holdings added more than 70 basis points in relative return. Some of that gain (approximately 20 basis points) was offset by the subsequent re-weighting into weaker performing biotech stocks.

¡ The industrials sector was additive (+42 basis points) over the past 12 months. Due to screening GE, which returned -53% during the period, the Fund gained nearly 80 basis points.

¡ Also within industrials, aerospace and defense screens subtracted 55 basis points from relative return.

¡ Tobacco screens were additive (+~30 basis points); the total impact within consumer staples was added 12 basis points.

Positioning & Outlook

¡ The Fund is structurally underweight pharmaceuticals (healthcare sector), aerospace and defense and a large conglomerate (industrials sector) and tobacco (consumer staples sector) due to Catholic Responsible InvestingSM screens.

¡ Screened companies represent about 14% of the S&P 500 by market cap.

¡ The Fund is constructed using a portfolio optimization process that aligns the portfolio’s factor exposures as closely as possible with those of its benchmark, using a range of fundamental security and industry factors, while also minimizing specific risk by constraining individual security weights to their Index weights or slightly higher. In so doing it seeks to minimize tracking error, while also constraining trading costs.

Christian Brothers Investment Services, Inc. n [email protected] PAGE 26

FUND FACTS

PROFILE Q1 2018

Christian Brothers Investment Services, Inc. (800) 592-8890 n [email protected]

CUIT Value Equity Fund

Objective Long-term capital appreciation

InvestmentsPrimarily the common stocks of U.S. companies, and the dollar denominated stocks of foreign companies, with market capitalizations greater than $1 billion

StrategyCombines complementary value strategies – one seeks undervalued securities using fundamental research, emphasizing industry-leaders with a medium to long-term investment horizon; the other seeks undervalued securities using a quantitative model to analyze asset values, earnings, and other factors

BenchmarkRussell 1000 Value Index

Asset ManagersDodge & Cox (Effective 2/1/00) AJO (Effective 4/1/02)

Total Expense Ratio / Minimum Class A: 1.04% / No MinimumClass B: 0.69% / $5M

Fund Features Commingled fund exclusive for tax-exempt Catholic institutions

Daily NAV and daily liquidity

Dividends Distributed Quarterly

TOP TEN HOLDINGS

STATISTICS %

Bank of America Corporation 3.8

JPMorgan Chase & Co. 3.7

Microsoft Corporation 2.4

Charles Schwab Corporation 2.4

Capital One Financial Corporation 2.2

Wells Fargo & Company 1.8

Cigna Corporation 1.8

Twenty-First Century Fox, Inc. 1.7

Hewlett Packard Enterprise Company 1.7

Goldman Sachs Group, Inc. 1.7

PORTFOLIO ANALYSIS

STATISTICS FUND BENCHMARK

Weighted Median Market Cap $40.9B $63.4B

Price/Book 2.0x 2.0x

Price/Earnings 15.1x 17.0x

Return on Equity 17.0% 12.3%

Dividend Yield 1.7% 2.4%

5-year Earnings Growth 11.8% 5.9%

Beta 1.1 1.0

Active Share 69.8 N/A

10 Largest Holdings 23.1 9.3

# of Equity Securities 174 711

Turnover Rate 47.0 N/A

Fund Size $338.8MM

RISK METRICSCHARACTERISTICS FUND / 5 YR BENCHMARK / 5 YR

Sharpe Ratio 1.0 1.0

Information Ratio 0.4 N/A

Standard Deviation 11.5 10.0

Tracking Error 3.4 N/A

Upside Capture 109.8 100.0

Downside Capture 102.9 100.0

Please see Important Information on Page 2

20%

10%

0%

-10%

CUIT Value Equity B Russell 1000 Value Index

FUND PERFORMANCE

QUARTERLY RETURN 3 MO 1 YR 3 YR 5 YR 10 YR

CUIT Value Equity A -2.01 10.96 7.87 11.07 8.17

CUIT Value Equity B -1.92 11.36 8.25 11.46 8.55

Russell 1000 Value Index -2.83 6.95 7.88 10.78 7.78

CALENDAR YEAR RETURN 2017 2016 2015 2014 2013

CUIT Value Equity A 16.53 13.98 -3.58 9.57 38.32

CUIT Value Equity B 16.96 14.41 -3.26 9.97 38.80

Russell 1000 Value Index 13.66 17.34 -3.83 13.45 32.53

3 MO 1 YR 3 YR 5 YR 10 YR

Christian Brothers Investment Services, Inc. n [email protected] PAGE 27Christian Brothers Investment Services, Inc. n [email protected] PAGE 2

CUIT Value Equity Fund

All attribution is based on gross portfolio performance.

Active Weights

6.3%

-4.6%

-0.9%

-2.9%

-0.6%

2.0%

6.5%

-0.4% -0.9%

-3.5

1.5%

-2.6%

Consumer Discretionary

InformationTechnology

Materials

Cash

Real EstateConsumer

Staples Energy

Financials

Healthcare IndustrialsTelecomm

Service Utilities

MARKET SECTOR ANALYSIS %

Consumer Discretionary

Consumer Staples Energy Financials Healthcare Industrials

Information Technology Materials Real Estate

TelecommService Utilities Cash

Fund 13.1 3.5 9.8 29.1 10.7 7.6 15.8 2.5 2.0 2.0 2.4 1.5

Benchmark 6.8 8.1 10.7 27.1 13.6 8.2 9.3 2.9 4.6 2.9 5.9 0.0

Christian Brothers Investment Services, Inc. n [email protected] PAGE 28Christian Brothers Investment Services, Inc. n [email protected] PAGE 3 | CB -FFS-000-0000