1.barter 2.what is money? 3.the functions of money 4.commodity, representative, and fiat money...

Post on 19-Dec-2015

219 views

TRANSCRIPT

Money and the Financial System

1. Barter2. What is money?3. The functions of money4. Commodity, representative, and fiat

money5. Financial intermediaries6. The Federal Reserve System7. Structure of the U.S. banking system

Barter exchangeGoods exchange for other goods

Barter exchange is not possible without

a “double coincidence of

wants.”

Money is anything that is generally acceptable in

exchange for goods, services, economic

resources, or for the settlement of debts

Advantages of monetary exchange

•Eliminates the coincidence of wants problem.•Facilitates economic specialization

Functi ons of money1. Medium of exchange2. Unit of account3. Store of value (or wealth)

Liquidity refers to two properties of assets or stores of value, namely:

•The ready convertibility of the asset to generalized purchasing power (or money)

•The comparative safety of the asset. Money is the most

liquid asset available under normal circumstances

7

Purchasing power of $1 measured in 1982-1984 constant dollars

An increase in the price level over time reduces what $1.00 buys. The price level has risen every year since 1960, so the purchasing power of $1.00 (measured in 1982-1984 constant dollars) has fallen from $3.38 in 1960 to $0.48 in 2007

Commodity money

Anything that serves both as money and as a commodity; money that has intrinsic worth.

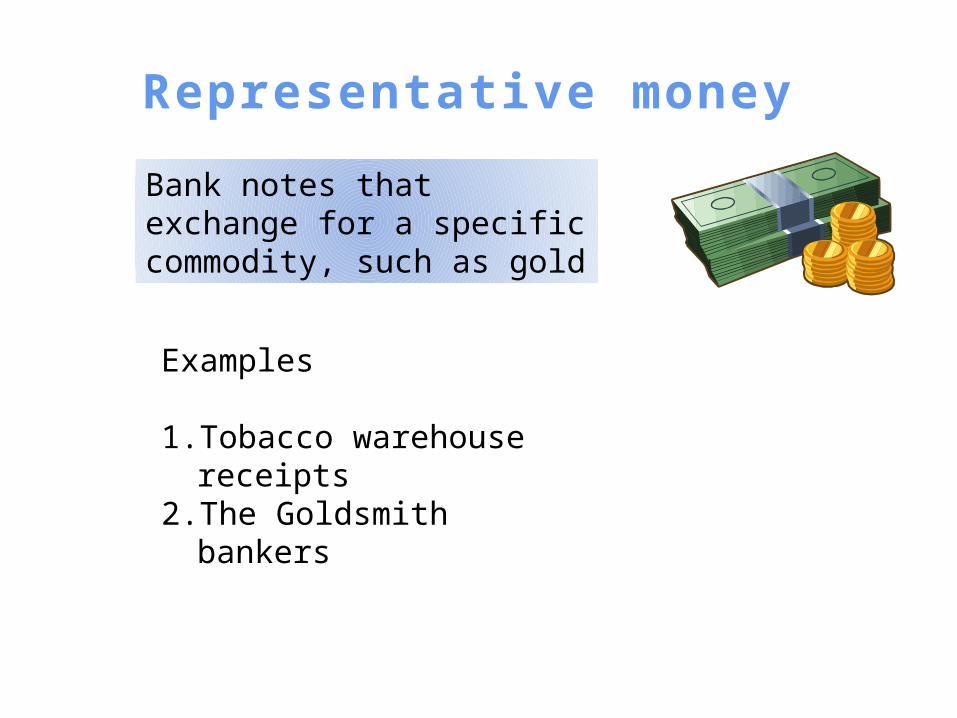

Representati ve money

Bank notes that exchange for a specific commodity, such as gold

Examples

1. Tobacco warehouse receipts2. The Goldsmith bankers

This Note Is Legal Tender For All Debts, Public and Private

Fiat Money: Anything which serves as a means of payment by government declaration

You are willing to accept money not because it is

“backed” by precious metals; but rather because you know it is generally acceptable in

exchange

11

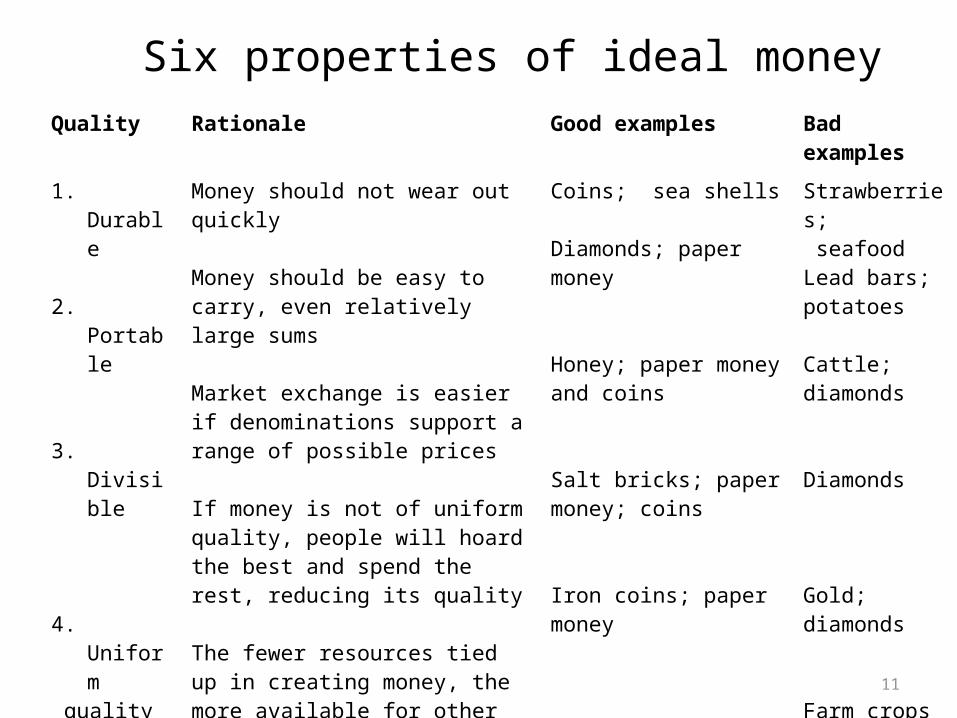

Six properties of ideal moneyQuality Rationale Good examples Bad examples

1. Durable

2. Portable

3. Divisible

4. Uniform quality

5. Low opportunity cost

6. Stable value

Money should not wear out quickly

Money should be easy to carry, even relatively large sums

Market exchange is easier if denominations support a range of possible prices

If money is not of uniform quality, people will hoard the best and spend the rest, reducing its quality

The fewer resources tied up in creating money, the more available for other uses

People are more willing to accept and hold money if they believe it will keep its value over time

Coins; sea shells

Diamonds; paper money

Honey; paper money and coins

Salt bricks; paper money; coins

Iron coins; paper money

Anything whose supply can be controlled by issuing authorities, such as paper money

Strawberries; seafoodLead bars; potatoes

Cattle; diamonds

Diamonds

Gold; diamonds

Farm crops

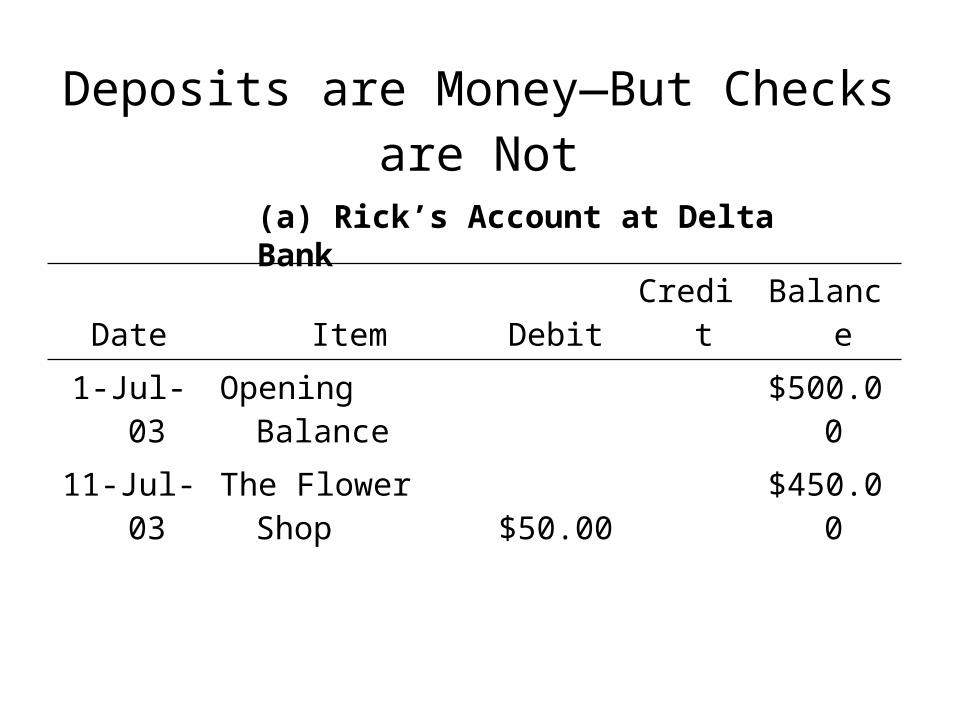

Deposits are Money—But Checks are Not

Date Item Debit Credit Balance

1-Jul-03 Opening Balance $500.00

11-Jul-03 The Flower Shop $50.00 $450.00

(a) Rick’s Account at Delta Bank

Date Item Debit Credit Balance

1-Jul-03 Opening Balance $3,000.00

11-Jul-03 Rick’s check $50.00 $3,050.00

(b) The Flower Shop’s Account at Delta Bank

The Monetary System

The monetary system consists of the Federal Reserve and the

banks and other institutions that accept deposits and provide the services that

enable people and businesses to make and receive payments.

Financial Intermediaries

These units are interposed between depositors and borrowers

1. Commercial banks

2. Thrift institutions

3. Money market funds: A financial institution that obtains funds by selling shares and uses these funds to purchase assets such as U.S. Treasury bills.

The Fractional Reserve System

•Reserves: The currency in a bank’s vaults plus the balance on its reserve account at the Federal Reserve Bank.

•Required reserve ratio: The minimum percentage of deposits that banks and other financial institutions must hold in reserves.

•Excess reserves: Banks reserves that exceed those needed to meet the required reserve ratio.

Federal Funds

•Banks that have excess reserves may loan them to banks with reserve deficiencies

•These loans are made in the interbank loan, or federal funds, market.

•The interest rate on loans in the interbank market is the federal funds rate.

Assets Liabilities Cash in vault Demand(checkable)

deposits Reserves on account

Savings deposits

Federal funds sold

Time deposits

Government securities

Federal funds bought

Loans

A Typical Bank Balance Sheet

The Economic Functions of Monetary Institutions

• Create liquidity (money)• Lower costs• Pool risks• Make payments

The Federal Deposit Insurance Corporation (FDIC)

•Created in 1933

•A government agency that insures deposits in commercial banks (up to $100,000 per account).

•Banks pay premiums to the FDIC

Bank failureswere often a

“self-fulfilling

prophesy.”

Federal Reserve Act of 1913

•The history of banking in the U.S. prior to 1913 is messy—featuring widespread panic and runs on banks—for example, in 1893 and 1907.•The Federal Reserve System was created in 1913.

The Structure of the Federal Reserve System

Senate confirms

Chair of Board of Governors

12 Federal ReserveDistrict Banks

• Lend reserves • Clear checks

• Provide currency

3,500 Member Banks

Elect 6 directorsof each

Federal ReserveBank

Appoints 3 directors of each Federal Reserve BankPresident

appoints

Federal Open MarketCommittee

(7 Governors + 5 Reserve Bank Presidents)

• Conducts open market operations to control the money supply

Board of Governors(7 members, including chair)

• Supervises and regulates member banks

• Supervises 12 Federal Reserve District Banks

• Sets reserve requirements and approves discount rate

23

The twelve Federal Reserve Districts

The map shows by color the area covered by each of the 12 Federal Reserve districts. Black dots note the locations of the Federal Reserve Bank in each district. Identified with a star is the Board of Governors headquarters in Washington, D.C.

The instruments of monetary policy

• Reserve requirements• The discount rate• Open market

operations

Legislation:

•Federal Reserve Act of 1913

•DIDMCA of 1982

Depository institutionsare required by law to

hold a minimum fractionof their liabilities on account at the FED

The discount rate The rate of interest charged on loans made at the FED discount window.

The FED is known as the “lender of last resort” to the

banking system

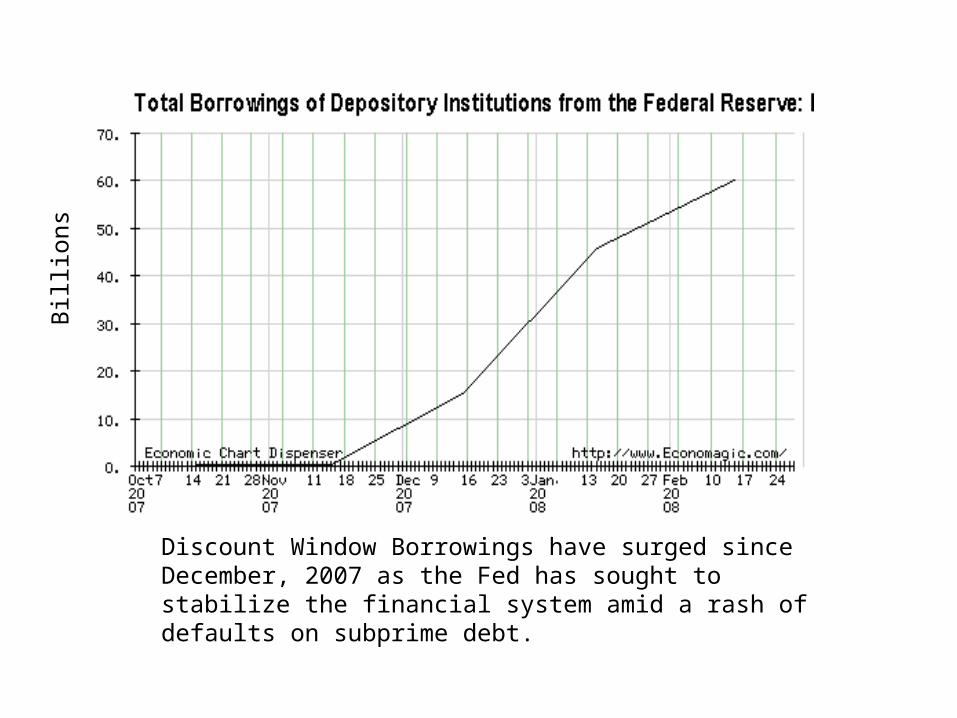

Discount Window Borrowings have surged since December, 2007 as the Fed has sought to stabilize the financial system amid a rash of defaults on subprime debt.

Billi

ons

Open market operationsare the purchase or sale ofU.S. government securitieson the open market by the

Federal Reserve system

The FED Open Market Committee is the unit in

charge ofopen market operations

30

Failures of US savings banks peaked in 1989

31

Failures of US commercial banks peaked in 1988

Exhibit 7

• Number of commercial banks declined over the last two decades, but the number of branches continue to grow

32

33

• (a) Largest US banks based on total domestic deposits

34

• (b) World’s largest banks based on total assets