1818 society tax presentation - world...

TRANSCRIPT

The Wolf Group, PC • 4401 Fair Lakes Court, Suite 310, Fairfax, VA 22033 • Tel: (703) 502-9500

1818 Society Tax Presentation

Dale Mason, CPA Robert Len, CPA, PFS

The Wolf Group

Agenda

The Exit Tax

FBAR and Other Reporting

Tax Aspects of “Consulting”

Roth IRA Conversions

© 2011 The Wolf Group

Worldwide Income Tax Reporting

U.S citizens and residents must report all income from whatever source derived to the U.S. government

U.S. Income Tax Residency:

• “Substantial Presence Test”

• “Green Card Test”

Worldwide Income Tax Reporting

Elimination of double taxation

• Foreign tax credits

• Tax treaties

• The “Saving Clause”

• State taxation – No foreign tax credits

Tax Aspects of “Consulting”

U.S. citizen

Green card holder

G-4 visa holder

© 2011 The Wolf Group

Employee vs. Independent Contractor

Based on common law rules Evidence of degree of control and independence

• Behavioral • Financial • Type of Relationship

20 factors • Instructions • Training • Services offered to general public • Full-time work • Etc.

© 2011 The Wolf Group

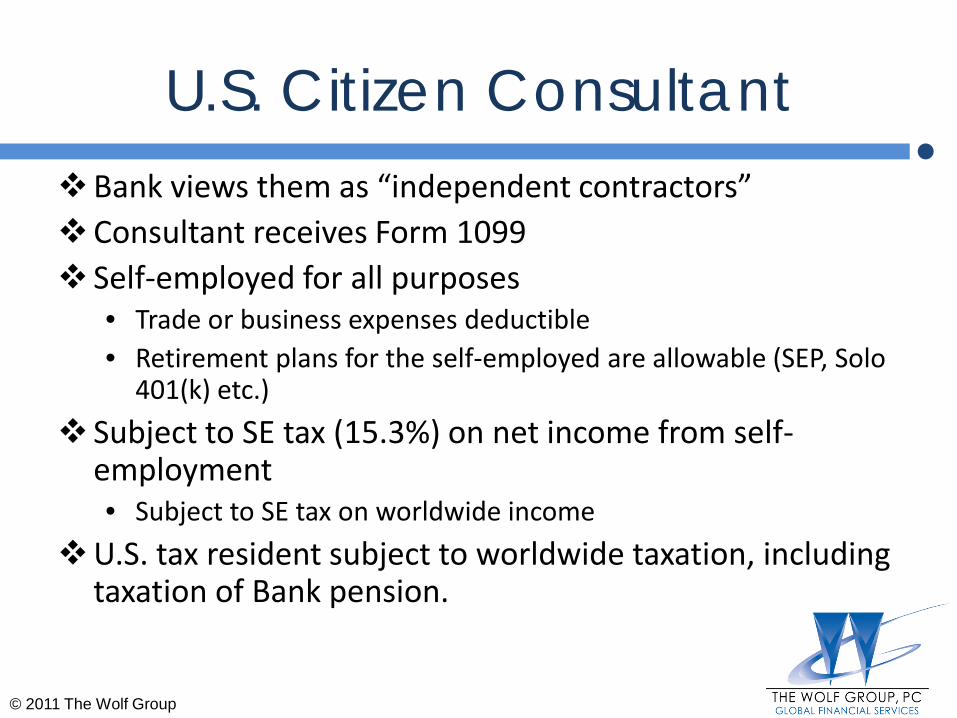

U.S. Citizen Consultant Bank views them as “independent contractors” Consultant receives Form 1099 Self-employed for all purposes

• Trade or business expenses deductible • Retirement plans for the self-employed are allowable (SEP, Solo

401(k) etc.)

Subject to SE tax (15.3%) on net income from self-employment • Subject to SE tax on worldwide income

U.S. tax resident subject to worldwide taxation, including taxation of Bank pension.

© 2011 The Wolf Group

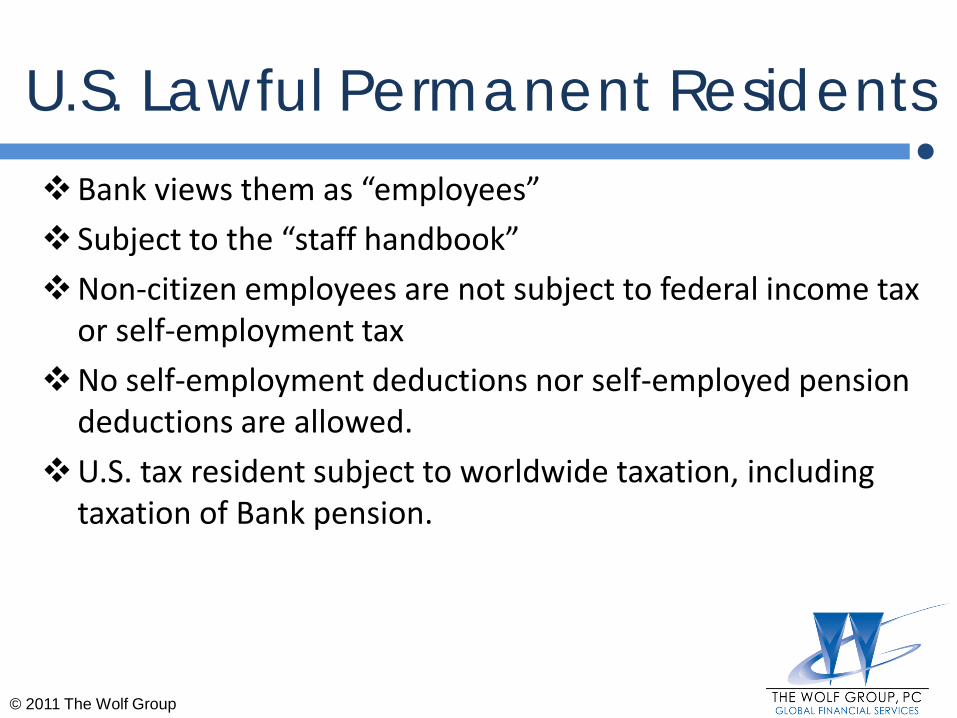

U.S. Lawful Permanent Residents Bank views them as “employees”

Subject to the “staff handbook”

Non-citizen employees are not subject to federal income tax or self-employment tax

No self-employment deductions nor self-employed pension deductions are allowed.

U.S. tax resident subject to worldwide taxation, including taxation of Bank pension.

© 2011 The Wolf Group

G-4 Visa Holders Viewed by the Bank as “employees” for purposes of U.S.

income tax. Treated as exempt under IRC Sec. 893.

Non-citizen employees are not subject to federal income tax or self-employment tax

No self-employment deductions nor self-employed pension deductions are allowed.

© 2011 The Wolf Group

G-4 Visa Holder Tax Residency Substantial Presence Test

• 183 day test

• Actual number of days in current year, plus

• 1/3 of the number of days in the prior year, plus

• 1/6 of the number of days in the second preceding yr.

Generally, if the total equal or exceeds 183 days then the person is a resident for the current year.

However…

© 2011 The Wolf Group

G-4 Visa Holder Tax Residency Exception for “Exempt Individual”

Any day an individual is an “exempt individual”, that day is not counted toward the substantial presence test of residency.

An exempt individual includes anyone who is present in the U.S. by reason of: • “His or her full-time employment with an international organization.

• (The law does not make reference to the term “G-4” visa.)

© 2011 The Wolf Group

The Wolf Group, PC • 4401 Fair Lakes Court, Suite 310, Fairfax, VA 22033 • Tel: (703) 502-9500

Q & A

Foreign Bank Account Reports (“FBARs”) – Reporting Rules

Reported on Form TD F 90-22.1 by June 30th of following year

Who must file an FBAR?

• U.S. citizens and residents

• Financial interest or signature authority

• Foreign financial account(s)

• Aggregate exceeding $10,000 at any time during the year

© 2011 The Wolf Group

FBAR – What is Ownership and Signature Authority?

Ownership • Owner of Record • Legal Title • Agents and Nominees • Greater than 50% interest in a corporation,

partnership, or trust

Signature Authority • Power of Disposition

© 2011 The Wolf Group

FBAR – What is a Foreign Financial Account?

Bank accounts

• Checking, savings, time deposits

Securities accounts

• Mutual funds, brokerage accounts, derivatives accounts

Insurance policies with cash surrender value

NOT individual securities owned directly

The account is located outside the U.S.

• Nationality of the institution does not matter

© 2011 The Wolf Group

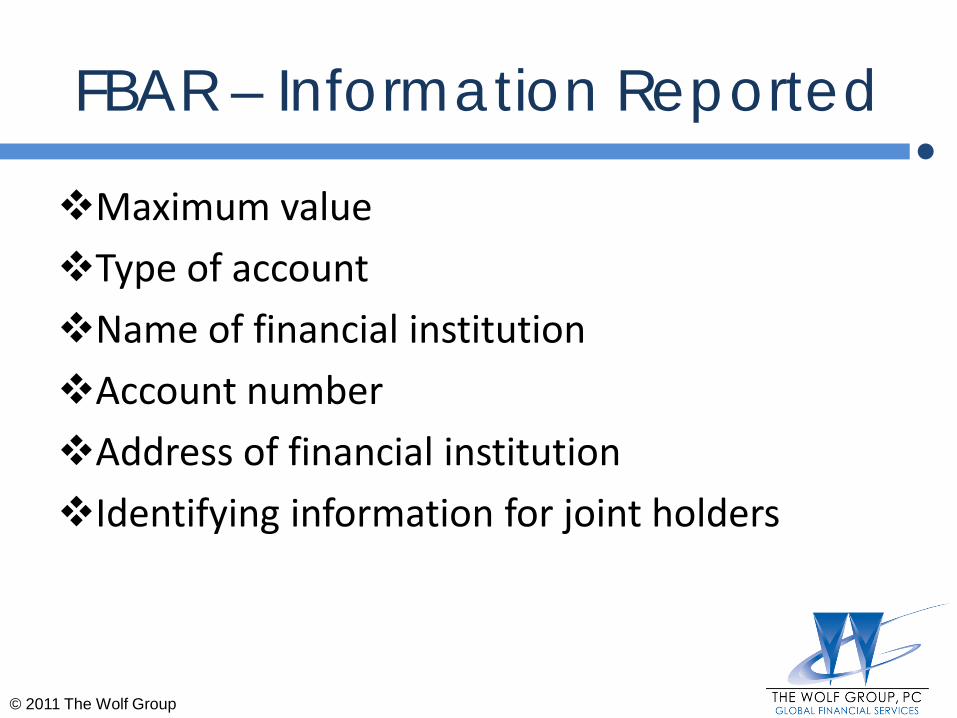

FBAR – Information Reported

Maximum value

Type of account

Name of financial institution

Account number

Address of financial institution

Identifying information for joint holders

© 2011 The Wolf Group

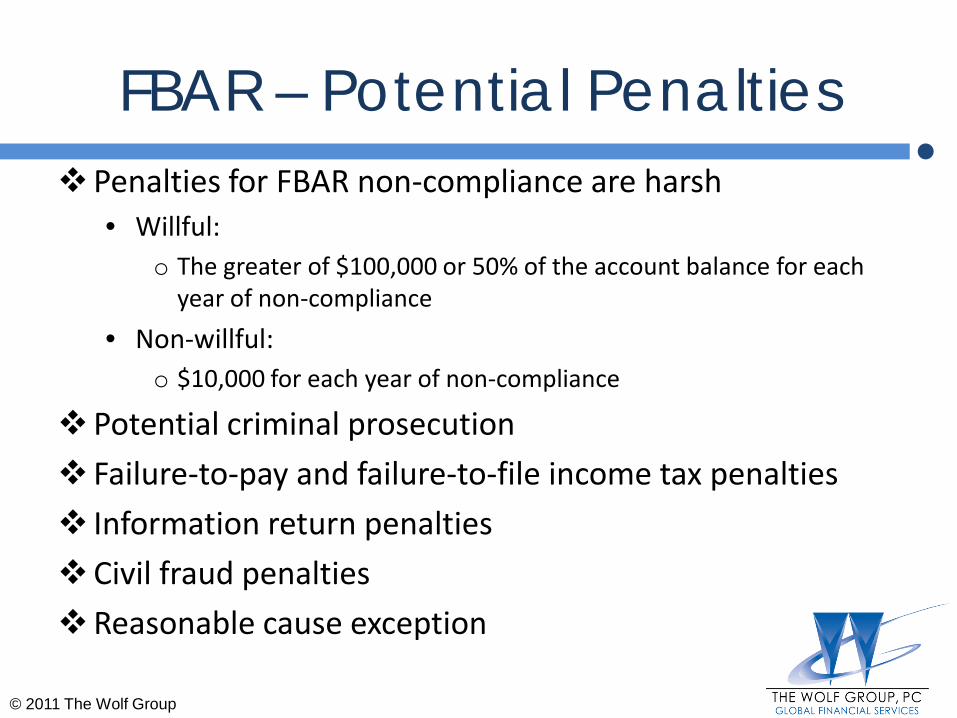

FBAR – Potential Penalties Penalties for FBAR non-compliance are harsh

• Willful: o The greater of $100,000 or 50% of the account balance for each

year of non-compliance

• Non-willful: o $10,000 for each year of non-compliance

Potential criminal prosecution

Failure-to-pay and failure-to-file income tax penalties

Information return penalties

Civil fraud penalties

Reasonable cause exception

© 2011 The Wolf Group

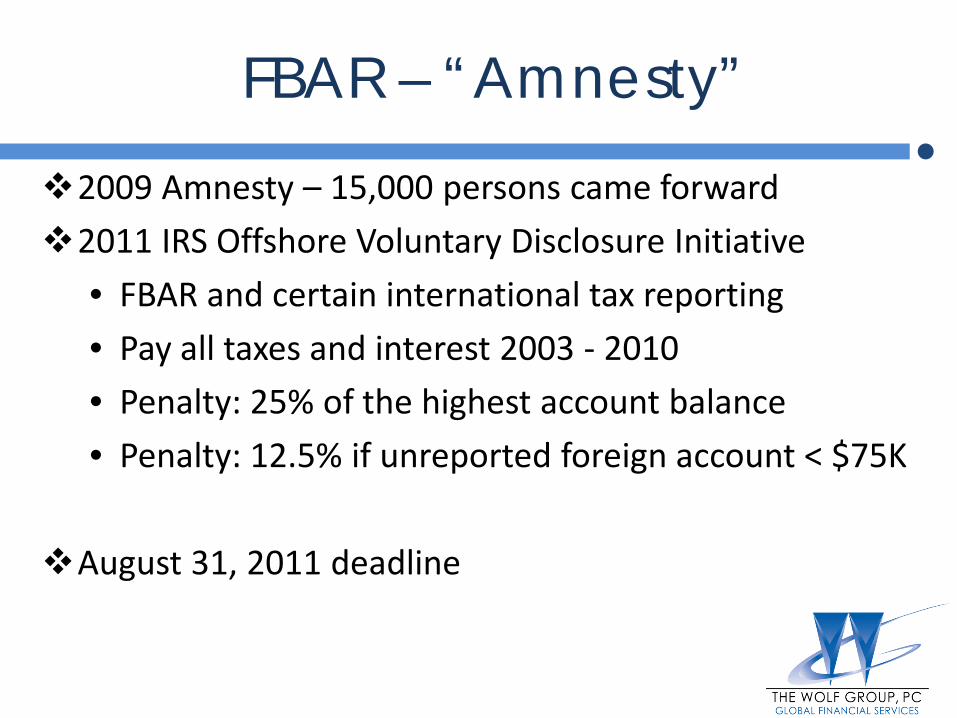

FBAR – “Amnesty”

2009 Amnesty – 15,000 persons came forward

2011 IRS Offshore Voluntary Disclosure Initiative

• FBAR and certain international tax reporting

• Pay all taxes and interest 2003 - 2010

• Penalty: 25% of the highest account balance

• Penalty: 12.5% if unreported foreign account < $75K

August 31, 2011 deadline

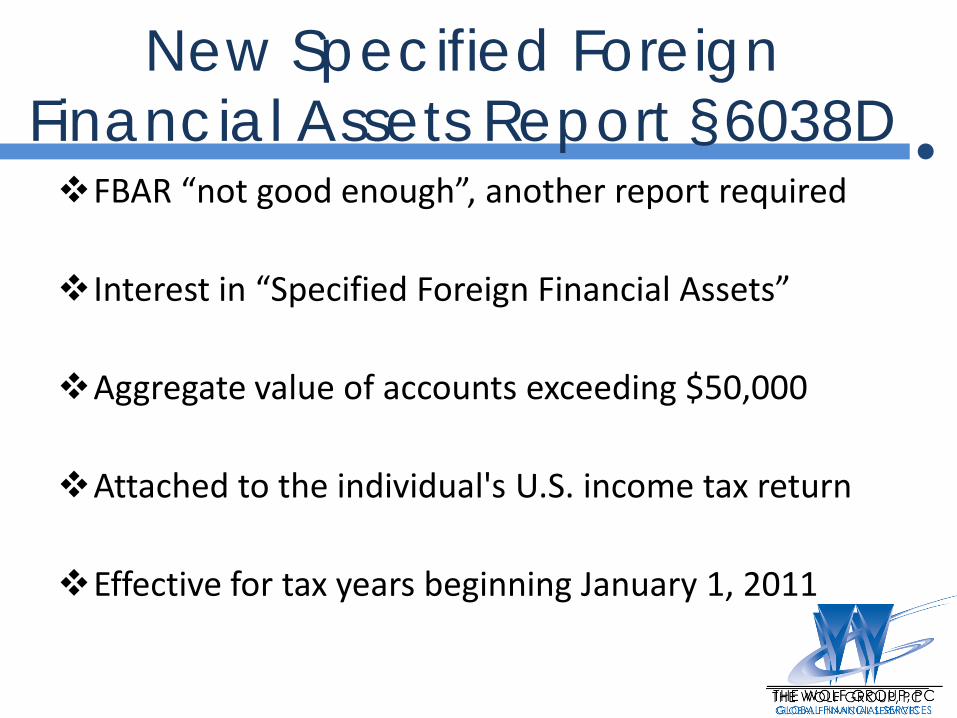

New Specified Foreign Financial Assets Report §6038D FBAR “not good enough”, another report required Interest in “Specified Foreign Financial Assets”

Aggregate value of accounts exceeding $50,000 Attached to the individual's U.S. income tax return Effective for tax years beginning January 1, 2011

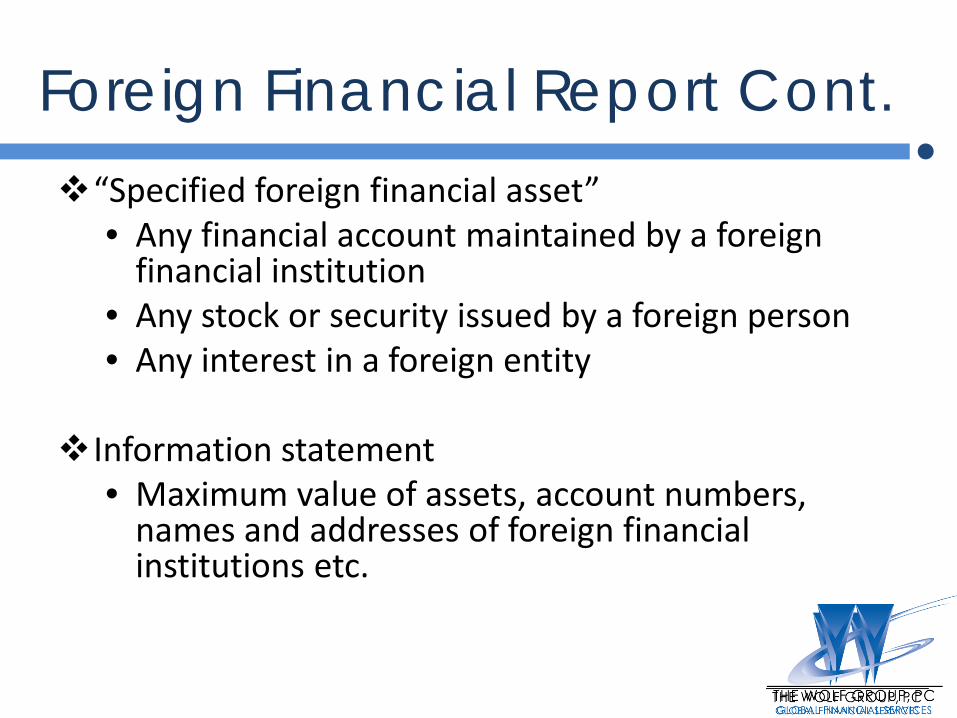

Foreign Financial Report Cont.

“Specified foreign financial asset” • Any financial account maintained by a foreign

financial institution • Any stock or security issued by a foreign person • Any interest in a foreign entity

Information statement • Maximum value of assets, account numbers,

names and addresses of foreign financial institutions etc.

Foreign Financial Report Cont. Penalties – Failure to File

• Minimum penalty $10,000

• Maximum penalty $50,000

• Presumption is that the value of the account is in excess of $50,000

• Statute of limitations does not run

• Reasonable cause exception

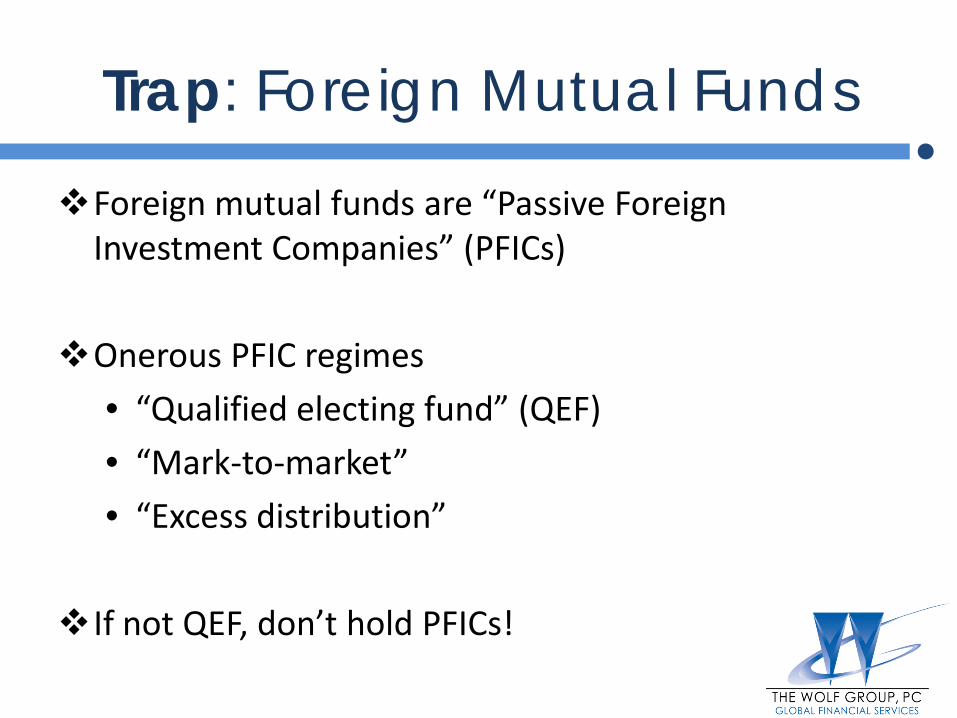

Trap: Foreign Mutual Funds

Foreign mutual funds are “Passive Foreign Investment Companies” (PFICs)

Onerous PFIC regimes

• “Qualified electing fund” (QEF)

• “Mark-to-market”

• “Excess distribution”

If not QEF, don’t hold PFICs!

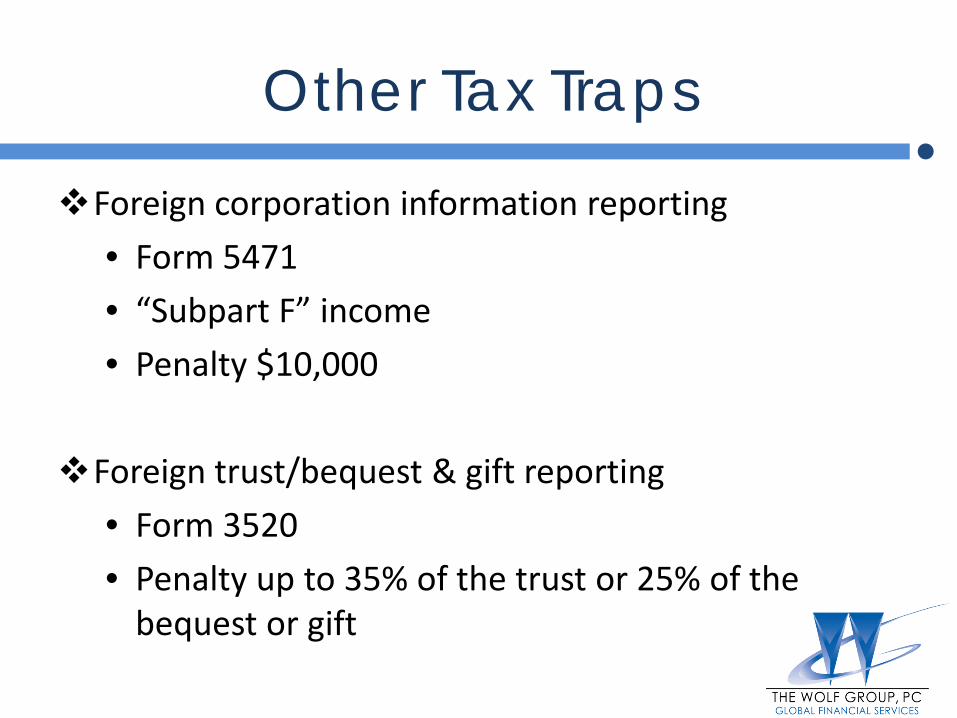

Other Tax Traps

Foreign corporation information reporting

• Form 5471

• “Subpart F” income

• Penalty $10,000

Foreign trust/bequest & gift reporting

• Form 3520

• Penalty up to 35% of the trust or 25% of the bequest or gift

The Wolf Group, PC • 4401 Fair Lakes Court, Suite 310, Fairfax, VA 22033 • Tel: (703) 502-9500

Q & A

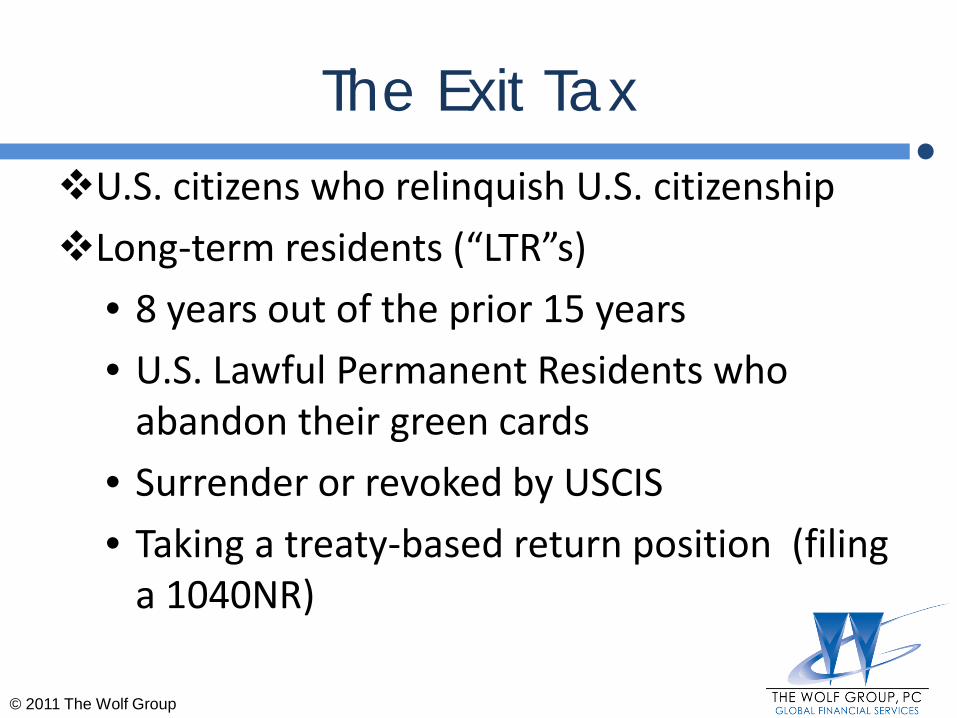

The Exit Tax U.S. citizens who relinquish U.S. citizenship

Long-term residents (“LTR”s)

• 8 years out of the prior 15 years

• U.S. Lawful Permanent Residents who abandon their green cards

• Surrender or revoked by USCIS

• Taking a treaty-based return position (filing a 1040NR)

© 2011 The Wolf Group

Who is subject to the Exit Tax?

Net Worth of $2 Million or

Average 5 year tax liability of $145,000 (2010 amount) or

Failure to certify (on Form 8854) compliance with all U.S. tax laws for the previous 5 years.

© 2011 The Wolf Group

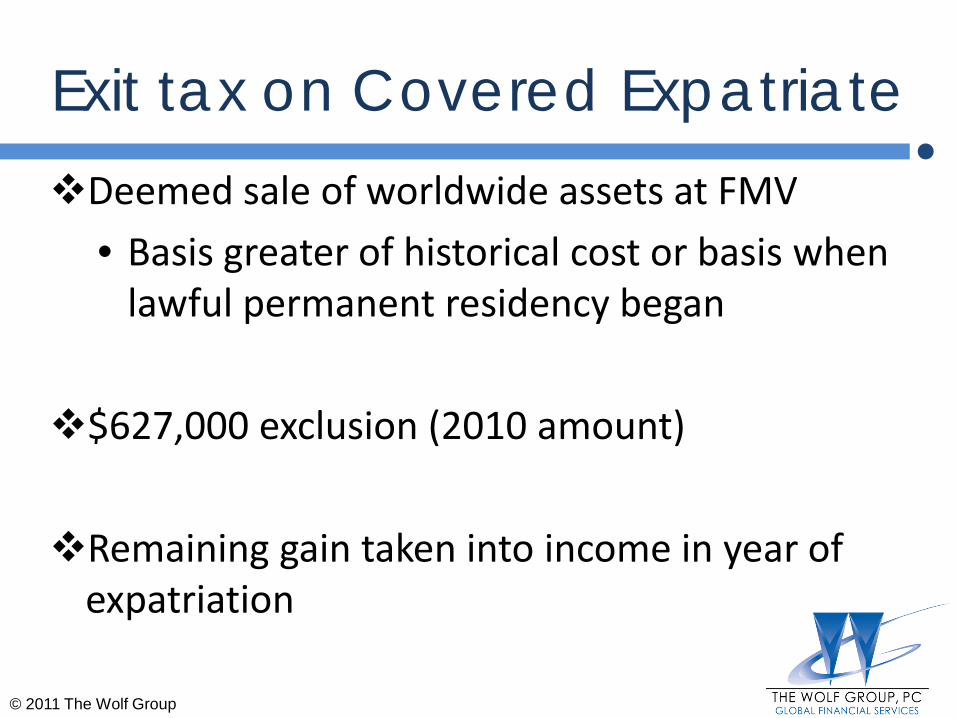

Exit tax on Covered Expatriate Deemed sale of worldwide assets at FMV

• Basis greater of historical cost or basis when lawful permanent residency began

$627,000 exclusion (2010 amount)

Remaining gain taken into income in year of expatriation

© 2011 The Wolf Group

Exit tax on Covered Expatriate “Eligible Deferred Compensation”

• Not subject to the exit tax • Paid by a U.S. payer on which 30 percent tax is

withheld

“Ineligible Deferred compensation” • Pensions paid by non-U.S. payer (World Bank) • Taxed based on present value of ineligible deferred

compensation • Election to treat non-U.S. payer as U.S. person

© 2011 The Wolf Group

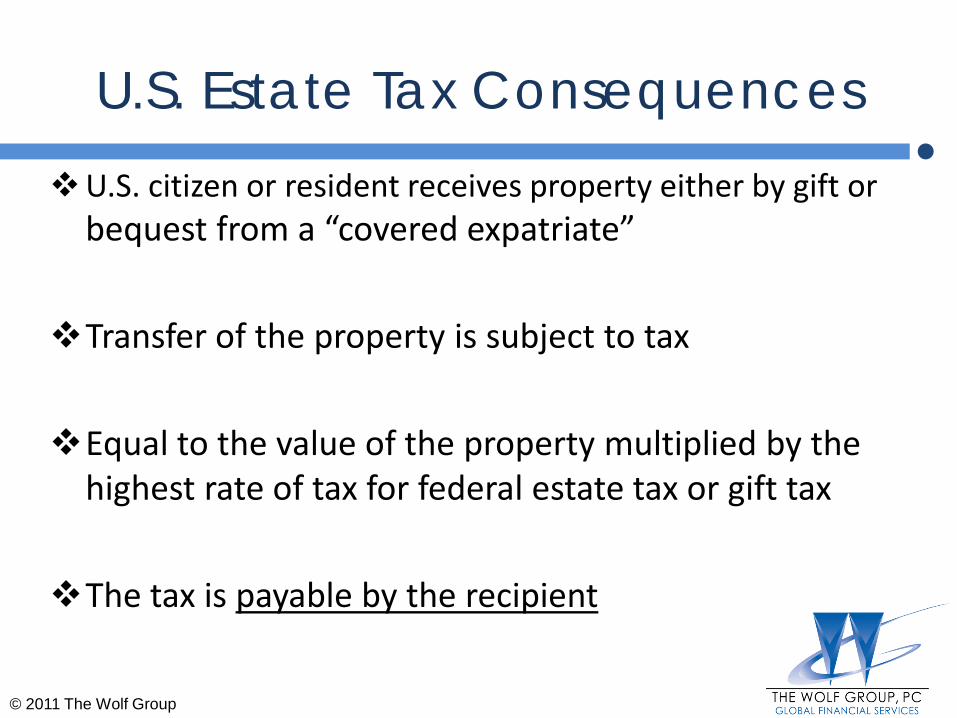

U.S. Estate Tax Consequences U.S. citizen or resident receives property either by gift or

bequest from a “covered expatriate”

Transfer of the property is subject to tax

Equal to the value of the property multiplied by the highest rate of tax for federal estate tax or gift tax

The tax is payable by the recipient

© 2011 The Wolf Group

The Wolf Group, PC • 4401 Fair Lakes Court, Suite 310, Fairfax, VA 22033 • Tel: (703) 502-9500

Q & A

Contact Us

4401 Fair Lakes Court

Suite 310

Fairfax, VA 22033

Tel: (703) 502-9500

www.thewolfgroup.com

1875 I Street

Suite 500

Washington, DC 20006

© 2011 The Wolf Group

Pursuant to Circular 230, promulgated by the Internal Revenue Service, any U.S. tax advice contained in the body of this presentation was not intended or written to be used, and cannot be used, by the recipient for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

© 2011 The Wolf Group