17 - 1 process costing chapter 17. 17 - 2 learning objective 1 identify the situations in which...

Post on 19-Dec-2015

224 views

TRANSCRIPT

17 - 1

Process CostingProcess Costing

Chapter 17

17 - 2

Learning Objective 1

Identify the situations in which

process-costing systems

are appropriate.

17 - 3

Illustrating Process CostingIllustrating Process Costing

Direct Materials, Direct LaborIndirect Manufacturing Costs

DepartmentA

DepartmentB

Finished Goods Cost of Goods Sold

17 - 4

Learning Objective 2

Describe the five steps

in process costing.

17 - 5

Five Steps in Process CostingFive Steps in Process Costing

Step 1: Summarize the flow of physical units of output.

Step 2: Compute output in terms of equivalent units.

Step 3: Compute equivalent unit costs.

Step 4: Summarize total costs to account for.

Step 5: Assign total costs to units completed and to units in ending work in process inventory.

17 - 6

Learning Objective 3

Calculate equivalent units and

understand how to use them.

17 - 7

Physical Units (Step 1)Physical Units (Step 1)

Physical unitsFlow of ProductionWork in process, beginning 0Started during current period 35,000To account for 35,000Completed and transferred out during current period 30,000Work in process, ending (100%/20%) 5,000Accounted for 35,000

17 - 8

Compute Equivalent Units(Step 2)

Compute Equivalent Units(Step 2)

Equivalent unitsDirect Conversion

Flow of Production Materials CostsCompleted and transferred out 30,000 30,000Work in process, ending 5,000 (100%) 1,000 (20%)Current period work 35,000 31,000

17 - 9

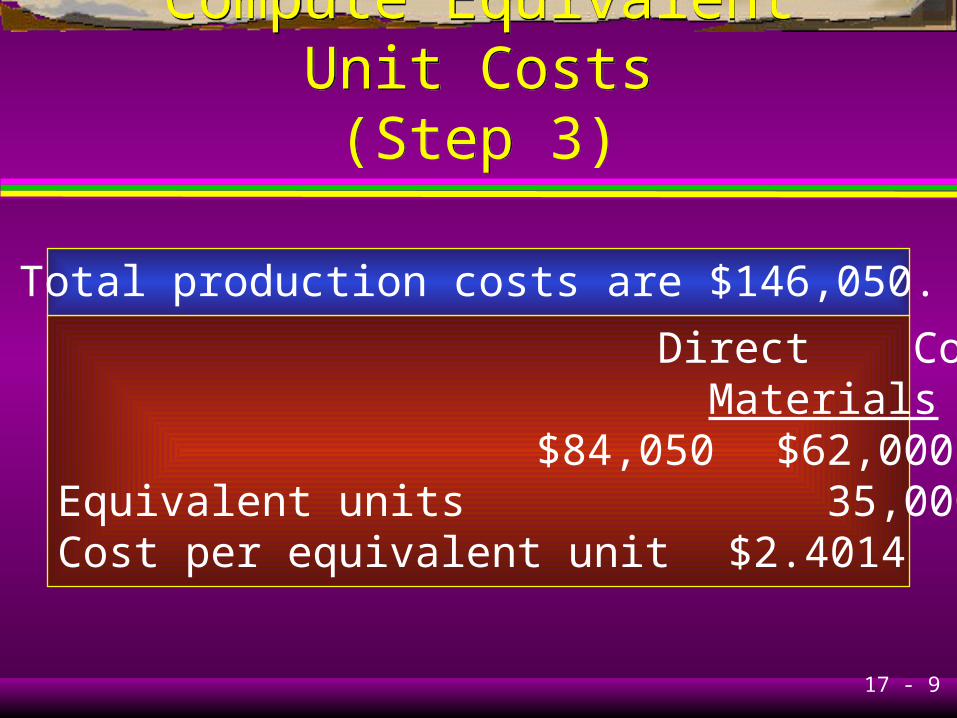

Compute Equivalent Unit Costs(Step 3)

Compute Equivalent Unit Costs(Step 3)

Direct Conversion Materials Costs

$84,050 $62,000Equivalent units 35,000 31,000Cost per equivalent unit $2.4014 $2.00

Total production costs are $146,050.

17 - 10

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Step 4: Total costs to account for: $146,050

Step 5: Assign total costs:

Completed and transferred out30,000 × $4.4014 $132,043

Work in process, ending (5,000 units)Direct materials 5,000 × $2.4014 12,007Conversion costs 1,000 × $2.00 2,000Total $146,050

17 - 11

Learning Objective 4

Prepare journal entries for

process-costing systems.

17 - 12

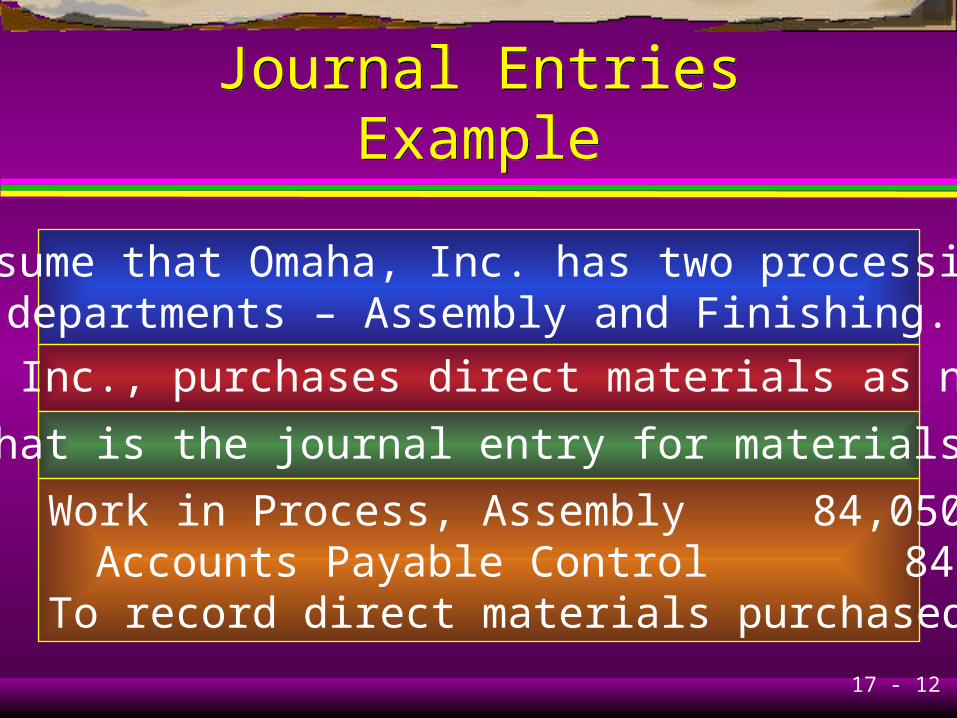

Journal Entries ExampleJournal Entries Example

Assume that Omaha, Inc. has two processingdepartments – Assembly and Finishing.

Omaha, Inc., purchases direct materials as needed.

What is the journal entry for materials?

Work in Process, Assembly 84,050Accounts Payable Control 84,050

To record direct materials purchased and used

17 - 13

Journal Entries ExampleJournal Entries Example

What is the journal entry for conversion costs?

Work in Process, Assembly 62,000Various accounts 62,000

To record Assembly Department conversion costs

What is the journal entry to transfer completedgoods from Assembly to Finishing?

17 - 14

Journal Entries ExampleJournal Entries Example

Work in Process, Finishing 132,043Work in Process, Assembly 132,043

To record cost of goods completed and transferredfrom Assembly to Finishing during the period

17 - 15

Flow of Costs ExampleFlow of Costs Example

Accounts Payable 84,050

Various Accounts 62,000

WIP Assembly84,050 132,04362,00014,007

WIP Finishing 132,043

17 - 16

Learning Objective 5

Use the weighted-average

method of process costing.

17 - 17

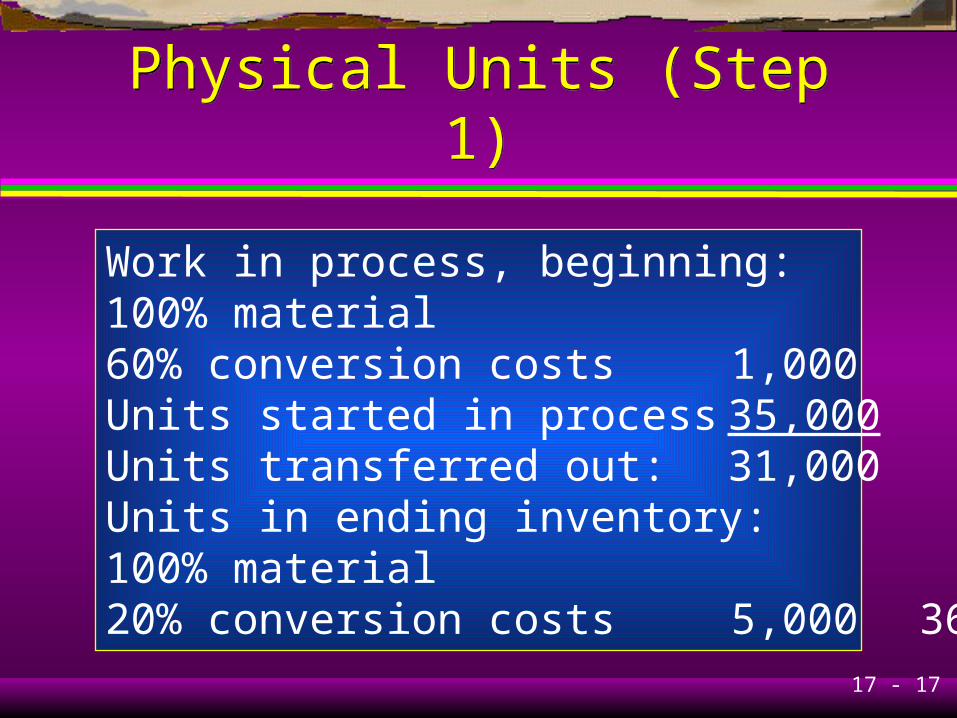

Physical Units (Step 1)Physical Units (Step 1)

Work in process, beginning:100% material60% conversion costs 1,000Units started in process 35,000 36,000Units transferred out: 31,000Units in ending inventory:100% material20% conversion costs 5,000 36,000

17 - 18

Compute Equivalent Units (Step 2)Compute Equivalent Units (Step 2)

Materials ConversionCompleted and transferred 31,000 31,000Ending inventory 5,000 1,000Equivalent units 36,000 32,000

100% 20%

17 - 19

Compute EquivalentUnit Costs (Step 3)

Compute EquivalentUnit Costs (Step 3)

Materials ConversionBeginning inventory $ 2,350 $ 5,200Current costs 84,050 62,000Total $86,400 $67,200Equivalent units 36,000 32,000Cost per unit $2.40 $2.10

17 - 20

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Work in process beginning inventory:Materials $ 2,350Conversion 5,200Total beginning inventory $ 7,550

Current costs in Assembly Department:Materials $ 84,050Conversion 62,000

Costs to account for $153,600

17 - 21

Summarize and Assign Total Costs (Steps 4 and 5)

Summarize and Assign Total Costs (Steps 4 and 5)

This step distributes the department’s costs to unitstransferred out: 31,000 units × $4.50 = $139,500

And to units in ending work in process inventory:$12,000 + $2,100 = $14,100

17 - 22

Summarize and Assign Total Costs (Steps 4 and 5)

Summarize and Assign Total Costs (Steps 4 and 5)

Costs transferred out:31,000 × ($2.40 + $2.10) $139,500

Costs in ending inventory:Materials 5,000 × $2.40 12,000Conversion 1,000 × $2.10 2,100

Total costs accounted for: $153,600

17 - 23

Journalizing: Weighted-AverageJournalizing: Weighted-Average

What are the journal entries in theAssembly Department?

Work in Process, Assembly 84,050Accounts Payable Control 84,050

To record direct materials purchased and used

Work in Process, Assembly 62,000Various accounts 62,000

To record Assembly Department conversion costs

17 - 24

Journalizing: Weighted-AverageJournalizing: Weighted-Average

Work in Process, Finishing 139,500Work in Process, Assembly 139,500

To record cost of goods completed and transferredfrom Assembly to Finishing during the period

17 - 25

Key T-Account:Weighted-Average

Key T-Account:Weighted-Average

Work in Process Inventory, AssemblyBeg. Inv. 7,550 TransferredMaterials 84,050 to FinishingConversion 62,000 139,500Balance 14,100

17 - 26

Learning Objective 6

Use the first-in, first-out (FIFO)

method of process costing.

17 - 27

Compute EquivalentUnits (Steps 1 and 2)Compute EquivalentUnits (Steps 1 and 2)

Materials ConversionCompleted and transferred:From beginning inventory 0 400Started and completed 30,000 30,000Ending inventory 5,000 1,000

35,000 31,400

Quantity schedule (Step 1) is the same asthe weighted-average method.

17 - 28

Compute EquivalentUnits (Step 2)

Compute EquivalentUnits (Step 2)

Materials ConversionCompletedand transferred: 31,000 31,000Ending inventory 5,000 (100%) 1,000 (20%)

36,000 32,000Beginning inventory 1,000 (100%) 600 (60%)Equivalent units 35,000 31,400

17 - 29

Compute EquivalentUnit Costs (Step 3)

Compute EquivalentUnit Costs (Step 3)

Materials ConversionCurrent costs $84,050 $62,000Equivalent units 35,000 31,400Cost per unit $2.40 $1.975

17 - 30

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Work in process beginning inventory: $ 7,550

Current costs:Material 84,050Conversion 62,000Total $153,600

Same as using weighted-average

17 - 31

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Costs transferred out:

From beginning inventory: $7,550Conversion costs added:1,000 × 40% × $1.975 790 $ 8,340

From current production:30,000 × $4.375 131,250

Total $139,590

17 - 32

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Work in process ending inventory:

Materials: 5,000 × $2.40 $12,000

Conversion:5,000 × 20% × $1.975 1,975Total $13,975

17 - 33

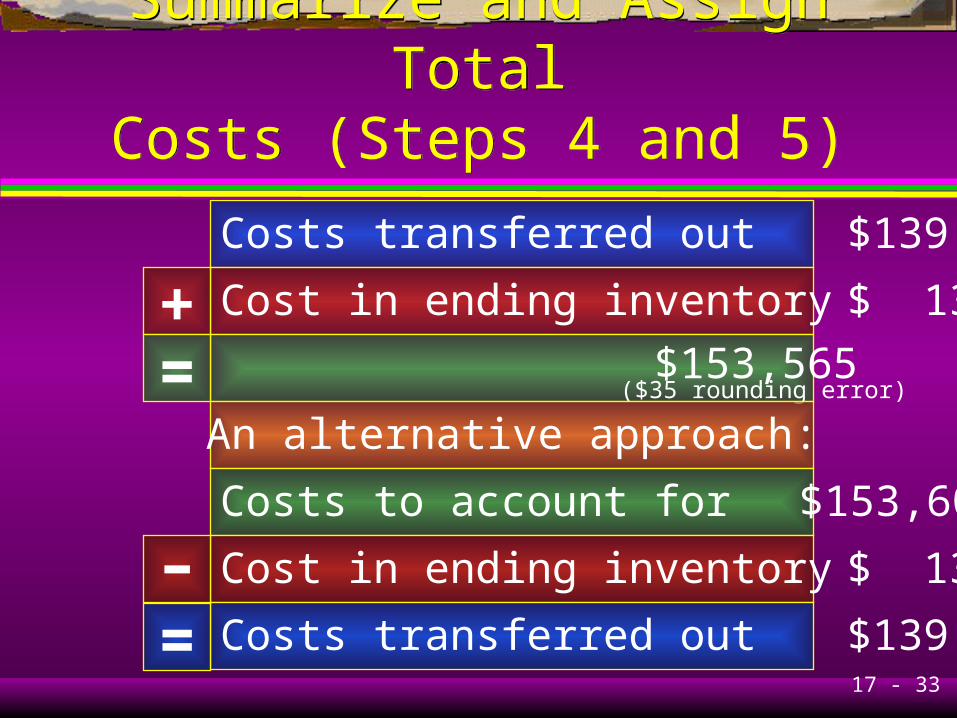

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Costs transferred out $139,590

Cost in ending inventory $ 13,975

$153,565 ($35 rounding error)

An alternative approach:

Costs to account for $153,600

Cost in ending inventory $ 13,975

Costs transferred out $139,625

+=

–=

17 - 34

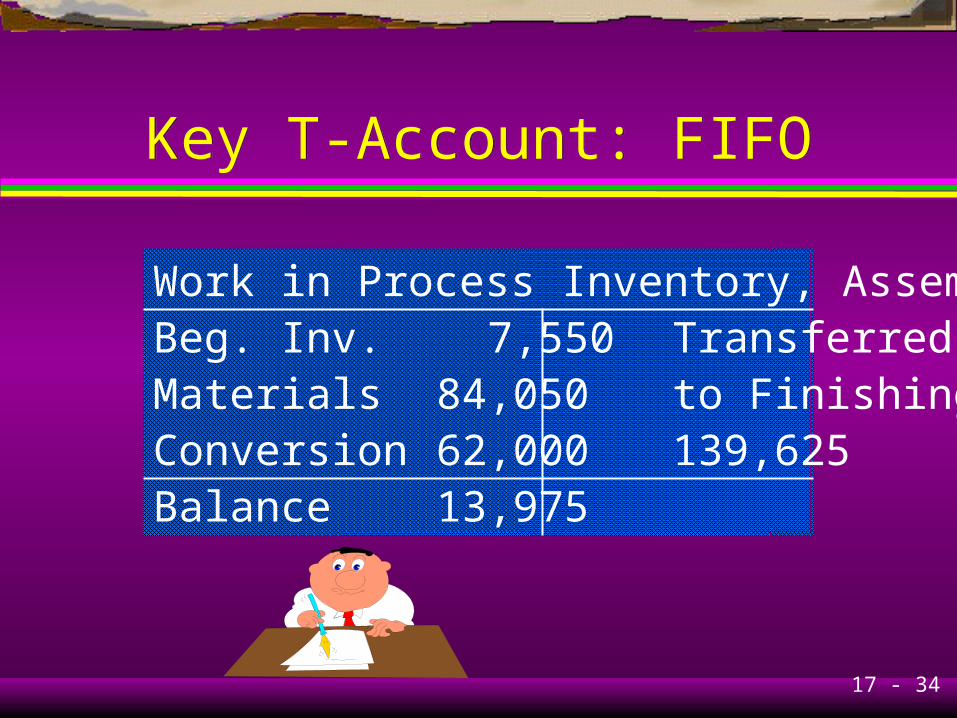

Key T-Account: FIFOKey T-Account: FIFO

Work in Process Inventory, AssemblyBeg. Inv. 7,550 TransferredMaterials 84,050 to FinishingConversion 62,000 139,625Balance 13,975

17 - 35

Comparison of Weighted-Average and FIFO MethodsComparison of Weighted-

Average and FIFO Methods

Weighted Average FIFO Difference

Costs of units completed and transferred out $139,500 $139,625 +$125Work in process, ending 14,100 13,975 –$125Total costs accounted for $153,600 $153,600 0

17 - 36

Learning Objective 7

Incorporate standard costs

into a process-costing system.

17 - 37

Standard-Costing Methodof Process-Costing ExampleStandard-Costing Method

of Process-Costing Example

Process-costing systems using standard costsusually accumulate actual costs incurredseparately from the inventory accounts.

Assume that actual materials cost is $84,050and standard materials cost is $84,250

What are the journal entries in theAssembly Department?

17 - 38

Standard-Costing Methodof Process-Costing ExampleStandard-Costing Method

of Process-Costing Example

Direct Materials Control 84,050Accounts Payable Control 84,050

Work in Process 84,250Direct Material Variances 200Direct Materials Control 84,050

To record direct materials purchased and used inproduction during the period and variances

17 - 39

Learning Objective 8

Apply process-costing methods

to cases with transferred-in costs.

17 - 40

Transferred-In CostsWeighted-Average Example

Transferred-In CostsWeighted-Average Example

Finishing Department beginning WIP inventory:4,000 units (60% materials) (25% conversion)

Ending work in process inventory:2,000 units (100% materials) (40%) conversion)

31,000 units transferred-in from Assembly.

17 - 41

Physical Units (Step 1)Physical Units (Step 1)

Beginning inventory 4,000Units started in process 31,000

35,000

Units completed and transferred to finished goods 33,000Ending inventory 2,000

35,000

17 - 42

Compute EquivalentUnits (Step 2)

Compute EquivalentUnits (Step 2)

Equivalent units for transferred-in costs:

Transferred to finished goods 33,000Ending inventory 2,000

35,000

Inventory is 100% complete for the workperformed in the Assembly Department.

17 - 43

Compute EquivalentUnits (Step 2)

Compute EquivalentUnits (Step 2)

Equivalent units for direct materials costs:Transferred to finished goods 33,000Ending inventory (100%) 2,000

35,000

17 - 44

Compute EquivalentUnits (Step 2)

Compute EquivalentUnits (Step 2)

Equivalent units for conversion costs(ending inventory 2,000):

Transferred to finished goods 33,000Ending inventory (40%) 800

33,800

17 - 45

Compute EquivalentUnit Costs (Step 3)

Compute EquivalentUnit Costs (Step 3)

Assume the following costs in theFinishing Department:

Work in process beginning inventory from:Assembly Department $30,200Direct materials 9,400Conversion costs 8,000Total cost in beginning inventory $47,600

17 - 46

Compute EquivalentUnit Costs (Step 3)

Compute EquivalentUnit Costs (Step 3)

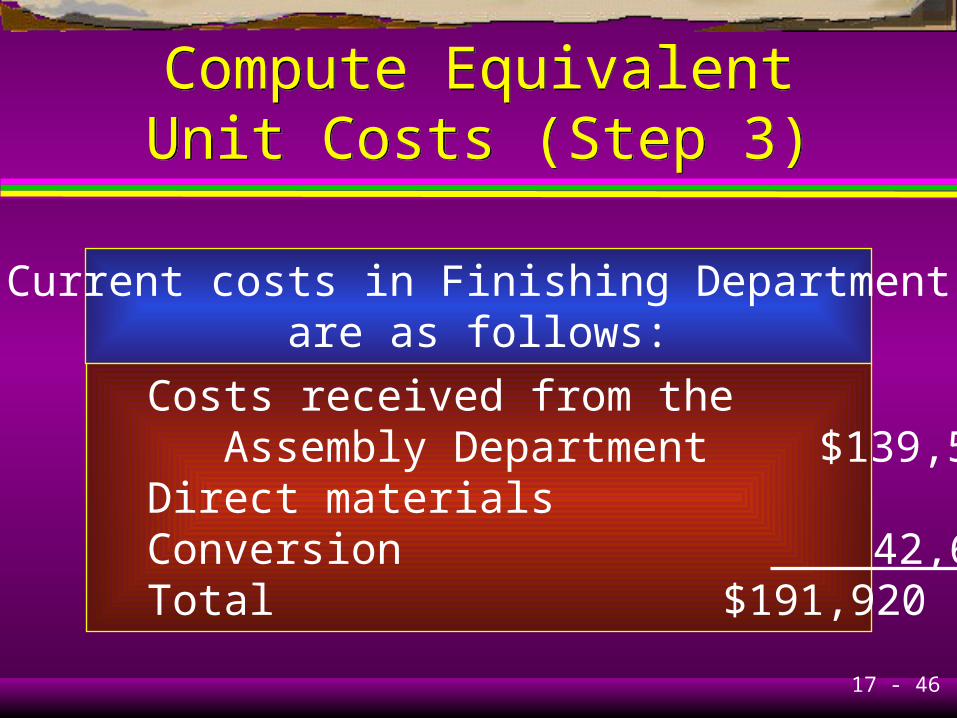

Current costs in Finishing Departmentare as follows:

Costs received from the Assembly Department $139,500 Direct materials 9,780 Conversion 42,640 Total $191,920

17 - 47

Compute EquivalentUnit Costs (Step 3)

Compute EquivalentUnit Costs (Step 3)

(Transferred-in costs $30,200 + Costs transferredin from the Assembly Department $139,500)÷ 35,000 units $4.85

(Direct materials $9,400 + $9,780)÷ 35,000 units $0.55

(Conversion costs $8,000 + $42,640)÷ 33,800 units $1.50

Total unit cost $6.90

17 - 48

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

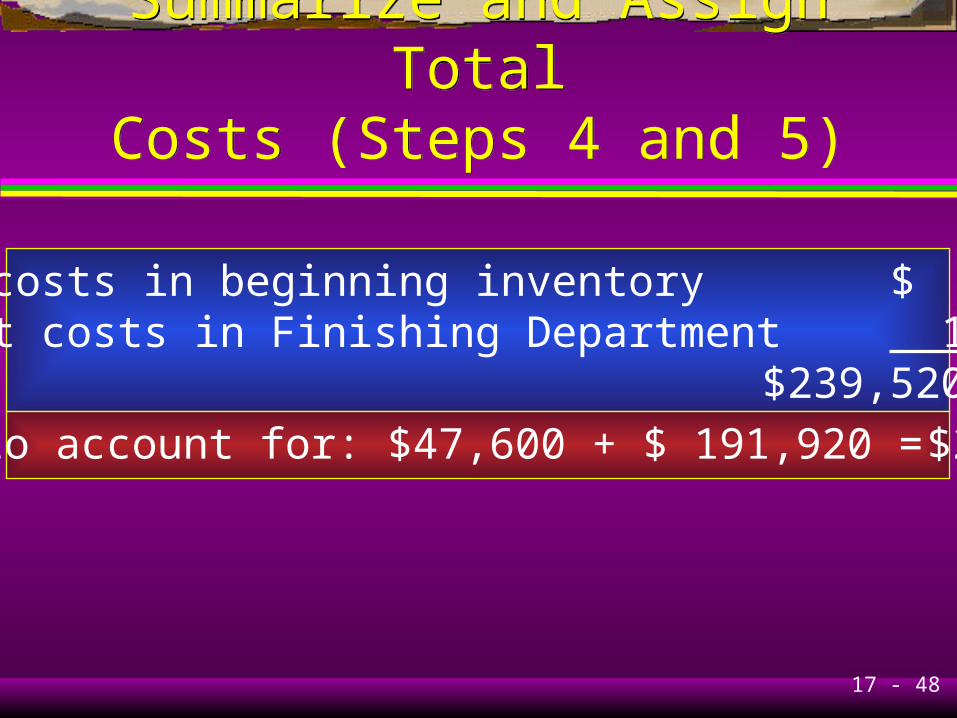

Total costs in beginning inventory $ 47,600Current costs in Finishing Department 191,920

$239,520

Costs to account for: $47,600 + $ 191,920 = $239,520

17 - 49

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Costs in work in process ending inventory:

Transferred-in costs: 2,000 × $4.85 $ 9,700

Direct materials: 2,000 × $0.55 1,100

Conversion: 2,000 × 40% × $1.50 1,200

Total cost in ending inventory $12,000

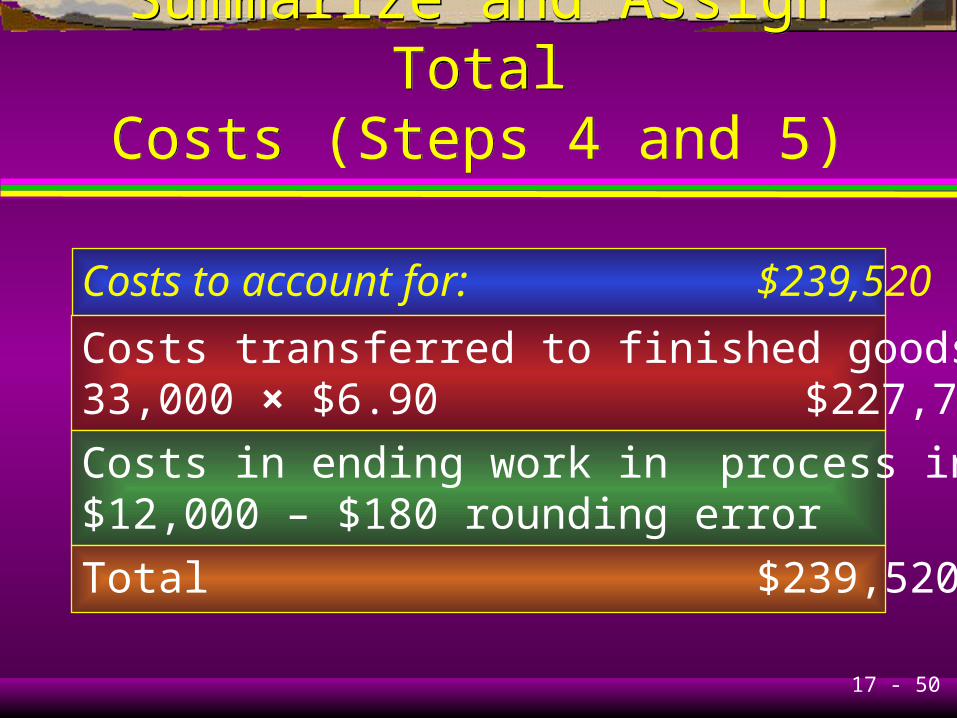

17 - 50

Summarize and Assign TotalCosts (Steps 4 and 5)

Summarize and Assign TotalCosts (Steps 4 and 5)

Costs to account for: $239,520

Costs transferred to finished goods inventory:33,000 × $6.90 $227,700

Costs in ending work in process inventory:$12,000 – $180 rounding error 11,820

Total $239,520

17 - 51

T-Account Finishing DepartmentT-Account Finishing Department

Work in Process Inventory, FinishingBeg. Inv. 47,600 Transferred toTransferred-in 139,500 Finished GoodsMaterials 9,780 227,700Conversion 42,640Balance 11,820

17 - 52

Transferred-In CostsFIFO Method

Transferred-In CostsFIFO Method

The physical units (Step 1) is the sameas in weighted-average.

Beginning inventory 4,000Units started in process 31,000

35,000

Units transferred to finished goods 33,000Ending inventory 2,000

35,000

17 - 53

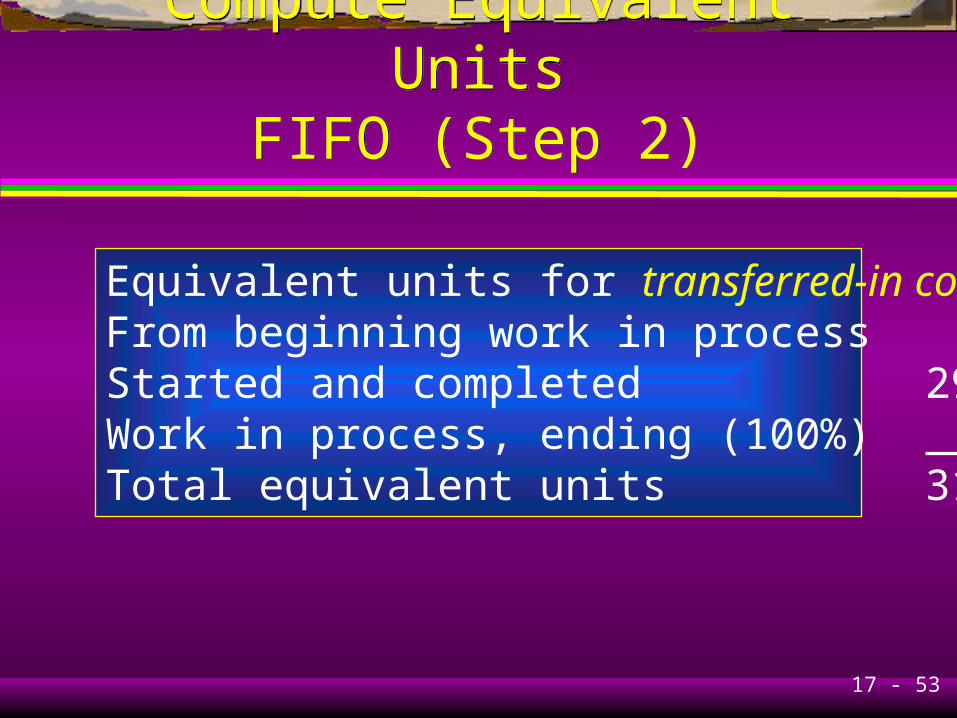

Compute Equivalent UnitsFIFO (Step 2)

Compute Equivalent UnitsFIFO (Step 2)

Equivalent units for transferred-in costs:From beginning work in process 0Started and completed 29,000Work in process, ending (100%) 2,000Total equivalent units 31,000

17 - 54

Compute Equivalent UnitsFIFO (Step 2)

Compute Equivalent UnitsFIFO (Step 2)

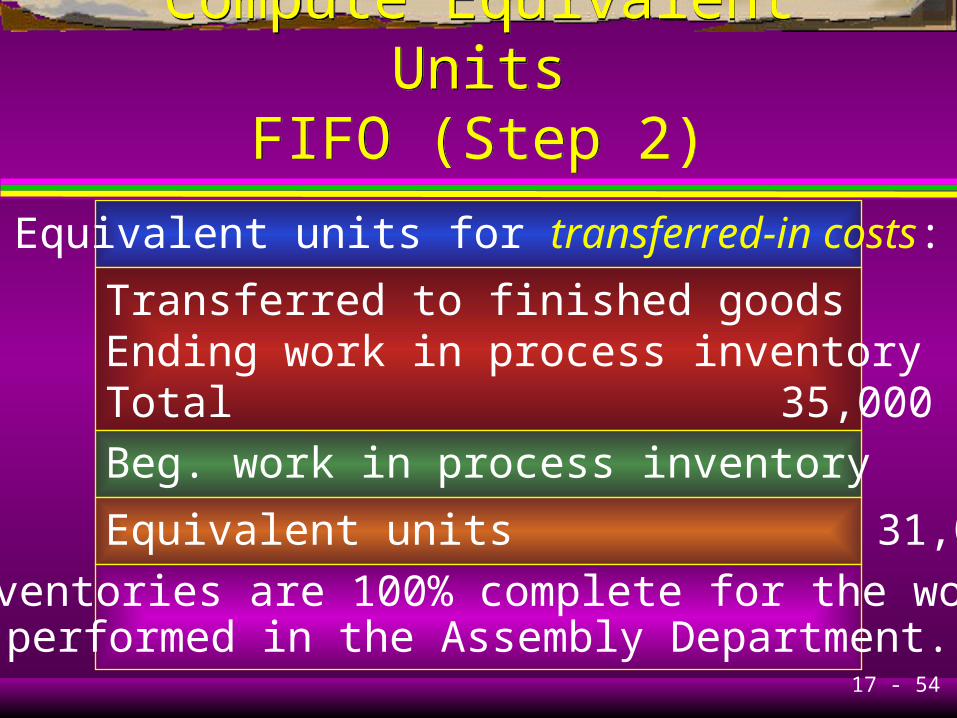

Equivalent units for transferred-in costs:

Transferred to finished goods 33,000Ending work in process inventory 2,000Total 35,000

Beg. work in process inventory – 4,000

Equivalent units 31,000

Inventories are 100% complete for the workperformed in the Assembly Department.

17 - 55

Compute Equivalent UnitsFIFO (Step 2)

Compute Equivalent UnitsFIFO (Step 2)

Equivalent units for materials costs:From beginning work in process 1,600Started and completed 29,000Work in process, ending (100%) 2,000Total equivalent units 32,600

17 - 56

Compute Equivalent UnitsFIFO (Step 2)

Compute Equivalent UnitsFIFO (Step 2)

Equivalent units for material costs(beginning inventory 4,000):

Transferred to finished goods 33,000

Ending inventory (100%) 2,000Total 35,000

Beginning inventory (60%) –2,400

Equivalent units 32,600

17 - 57

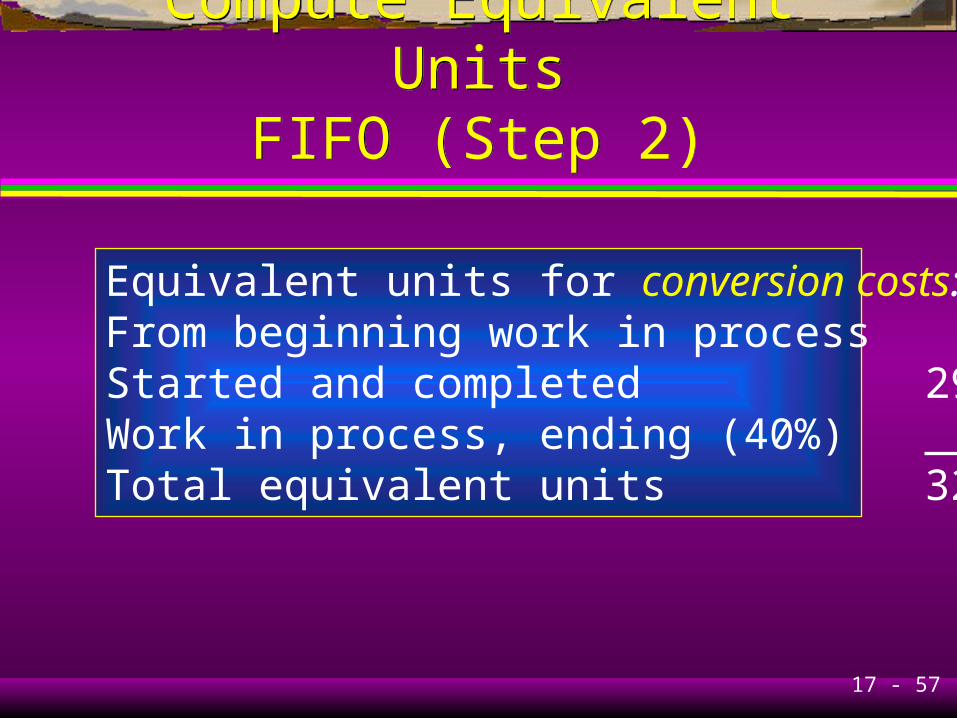

Compute Equivalent UnitsFIFO (Step 2)

Compute Equivalent UnitsFIFO (Step 2)

Equivalent units for conversion costs:From beginning work in process 3,000Started and completed 29,000Work in process, ending (40%) 800Total equivalent units 32,800

17 - 58

Compute Equivalent UnitsFIFO (Step 2)

Compute Equivalent UnitsFIFO (Step 2)

Equivalent units for conversion costs (beginninginventory 4,000, ending inventory 2,000):

Transferred to finished goods 33,000

Ending inventory (40%) 800Total 33,800

Beginning inventory (25%) –1,000

Equivalent units 32,800

17 - 59

Compute Equivalent Unit CostsFIFO (Step 3)

Compute Equivalent Unit CostsFIFO (Step 3)

Cost per equivalent unit:

Transferred-in: $139,590 ÷ 31,000 $4.50

Direct materials: $9,780 ÷ 32,600 0.30

Conversion: $42,640 ÷ 32,800 1.30

Total unit cost $6.10

17 - 60

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Current costs in Finishing Department: $192,010

Work in process beginning inventory: 47,600

Costs to account for:(same as weighted-average) $239,610

17 - 61

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Work in process ending inventory:

Transferred-in: 2,000 × $4.50 $ 9,000

Direct materials: 2,000 × $0.30 600

Conversion: 800 × $1.30 1,040

Total $10,640

17 - 62

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Costs transferred out:

From beginning inventory: $47,600

Direct materials added:4,000 × 40% × $0.30 480

Conversion costs added:4,000 × 75% × $1.30 3,900

Total $51,980

17 - 63

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Total costs transferred out:From beginning inventory $ 51,980From current production: 29,000 × $6.10 176,900Total $228,880

17 - 64

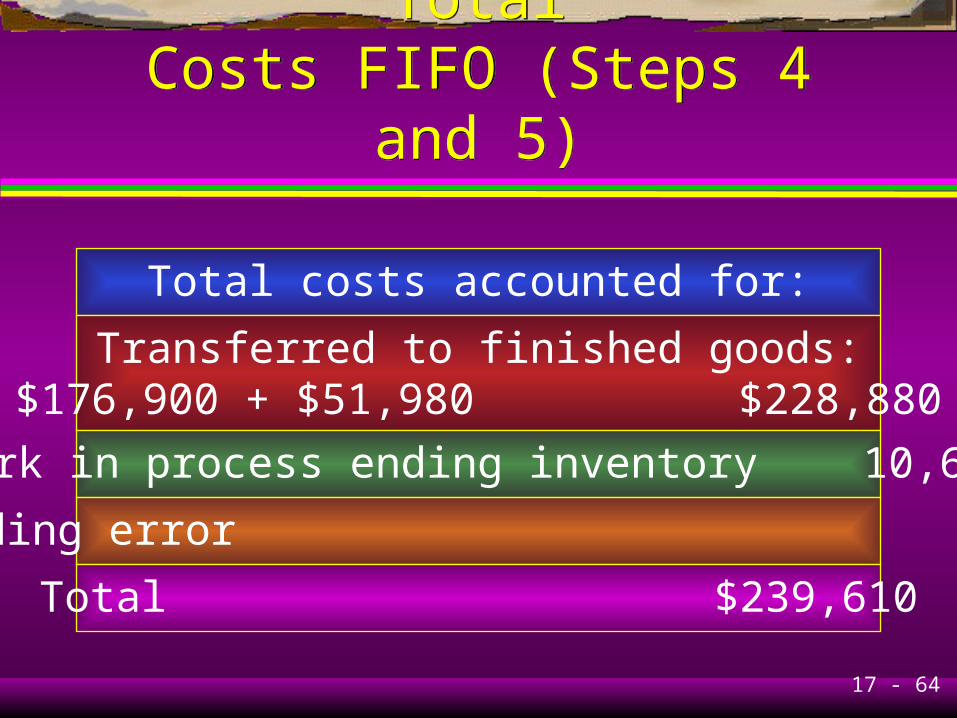

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Total costs accounted for:

Transferred to finished goods:$176,900 + $51,980 $228,880

Work in process ending inventory 10,640

Rounding error 90

Total $239,610

17 - 65

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Summarize and Assign TotalCosts FIFO (Steps 4 and 5)

Costs to account for $239,610

Work in process ending inventory – 10,640

Transferred to finished goods $228,970

17 - 66

End of Chapter 17End of Chapter 17