16. supply chains for rice in chennai

TRANSCRIPT

Supply chains for rice in Chennai

Mohan Mani, Gautam Mody and MeghnaSukumar1

November, 2013

Working Paper no 16

http://www.southasia.ox.ac.uk/resources-greenhouse-gases-technology-and-jobs-indias-informal-economy-case-rice

In this paper we look behind the retail labour process (WP11, here) to scope the

supply arrangements through which Chennai is supplied with rice with a view to

evaluating possible changes in employment conditions along the supply chain

that might accompany the entry of large retail conglomerates. So rather than

focussing on commodity contracts, value added, rents and technological

upgrading as is usual in supply or commodity chain analysis, we take a labour

perspective and evaluate the current and likely future impacts of organisational

change – involving new scale of capital and new buyer-driven power – on the

existing supply arrangements.2

For this, as trade union researchers, we have studied managers and employers in

order to scope the several private supply chains ‘backwards’ from retail to rice

milling as well as the public distribution system comprising state agencies and

contracted private firms. Our method is based on case studies, a method

established as appropriate when research questions are new and when existing

1Centre for Workers’ Management

2See Gilbert 2011 for a critique of value chains analysis from a work perspective: P Gilbert 2011 Frontiers of

Commodity Chain Research Anthropology of Work Review vol 32 no 1 pp 43-45

research is thin on the ground, which is the case here.3 Findings are based on

detailed interviews with 10 managers and owners in four large retail chains,

three medium-sized retail outlets, and three small retail outlets; one wholesaler

in Chennai; a large rice miller on the outskirts of the city, supplying rice to large

retailers and wholesalers; plus managers in two mills contracted to the PDS –

fourteen in total. 4 In this working paper, we analyse the logistics of the private

supply chains – and then their labour arrangements backwards to the rice

milling stage; we then follow the same format for the public distribution system.

Large business houses in retail trade

Today a number of large corporate houses have seen it profitable to enter retail

trade. Prominent firms include Reliance Fresh, with over 700 Reliance Fresh

Stores across the country, annual turnover of Rs.7599 crores and a pre-tax loss

of Rs.342 crores for the year 2011-12; Future Retail, with 204 Big Bazaar and

Future Bazaar Stores, annual turnover of Rs.11793 crores and a pre-tax profit

(PBDIT) of Rs.702 crores for the year 2011-12; Birla retail with 560

supermarkets, and a turnover of Rs.1650 crores in 2010-11; and the Tata Group-

owned Trent Hypermarket which owns the Star Bazaar chain of mega

supermarkets - with 15 supermarkets, a turnover of Rs.785.91 crores, and pre-

tax loss of Rs.76 crores for 2012-13.5 While there is substantial interest in the

3M Abraham forthcoming/2014, The new co-operativism : a study of emerging producers organisations in

India, PhD Thesis, Copenhagen Business School4

The data for the large retail supermarkets was obtained through interviews with key managers in Chennai;for the medium stores and small stores from direct contact with the stores owners/in-charges and subsequentinterviews; for the Public Distribution System through interviews with the General Secretary, LPF Union inTNCSC, permission from the MD, TNCSC through the intervention of the General Secretary, LPF Union,interviews with managers in Commercial, Quality Control and General Marketing in TNCSC, factory interviewsat the private rice mill on contract to TNCSC for PDS and a rice mill owned by the TNCSC, and interviews withtransport contractors with the TNCSC. Application under the Right to Information was used to supplementdata collected from direct contact.5

Data for Reliance Retail and Future Retail from articles.economictimes.indiatimes.com; for Birla Retail fromwww.rediff.com; and for Star Bazaar from www.mywestside.com.

sector, with large investment in building a sales infrastructure, the sector is still

to start yielding returns for most of the large companies.

Supply chain logistics, costs and returns – large retail and wholesale

Table 1 gives details of the procurement chain for rice for four large retail

chains, and for a major wholesale dealer supplying rice to many small and

medium retail stores of the kind whose labour force we have researched6. From

the interviews a number of distinctive characteristics of the rice supply chains

became evident.

6Mohan M., G. Mody and M. Sukumar, 2013, ‘Employment and Working Conditions in the Retail Sector –

Chennai’, Working Paper 11, http://www.southasia.ox.ac.uk/working-papers-resources-greenhouse-gases-technology-and-jobs-indias-informal-economy-case-rice#sthash.iyhLdi05.dpuf

Table 1: The private procurement chain: large corporate retail and neighbourhoodwholesale firms

Large retail Wholesale

Chain7 Large-B Large-E Large-A Large-F WS

No. of outlets 1 6 74 56 1

Vendors One - Red Hills Centralisedrice purchaseat Guntur,Chennai,Bangalorethrough sistercompany. Ricefor Chennaioperationspurchasedmostly fromRed Hills

Rice boughtfrom 4-5vendors in RedHills inChennai,Pondicherryand Salem.

Rice bought from tenmillers. Boiledrice:Tindivanam,Arani,Kanchipuram, RedHills and NelloreRaw rice:Nellore andNaidupettai

Rice boughtfrom 25 millersthrough 2-3brokers inAndhra Pradesh– Nellore,Guntur,Naidupettai;Karnataka –Raichur,Tumkur; TN –Arani,Tindivanam,Kallakurichi.

Estimatedmonthlyturnover

20MT permonth all rice

varieties

(1 store)

15MT permonth Ponni

rice

(6 stores)

180 MT permonth Ponni

rice.

(74 stores)

Ponni boiled 90MTper month; Ponni raw

130 MT per month(56 stores)

300MT permonth Ponnirice

(1 outlet)

Warehouse No Yes Yes Yes Yes

Source: Discussions with private sector managers, owner of wholesale rice business,2013

First, contrary to the supposition that large supermarket stores sell more staples

than small ones, the table shows first that procurement operations for rice in

large multi-product retail chains are in most cases substantially smaller, and less

7None of the workers in the sample were from the supermarkets Large-E and Large-F. Also, the managers in

the supermarkets Large-C and Large-D refused to be interviewed or participate in the study.

complex than for the neighbourhood wholesale dealer. Only the retail chains

Large-F, belonging to a large Indian business house, with 56 retail outlets in

Chennai and Large-A belonging to another large business house, with 74

outlets, even approach the size of the wholesaler. Large-F procures an estimated

220 MT per month of Ponni rice (raw and boiled) for its 56 outlets in the city,

and Large-A around 180 MT per month for its 74 outlets, as against 300-450

MT per month Ponni rice procured by the wholesale dealer. The other two

major corporate supermarkets do not approach this operational scale.

We also know (see WP11) that the turnover of rice from a large supermarket is

only around 3-4 times that of a medium retail store, or 15-20 times a small

store. The difference between the large supermarket and the smaller stores for

rice sales is therefore not as significant as would be expected given the

respective differences in overall size.

Second, the local wholesaler8 scopes supply so much more extensively than

does large retail that the rice market appears to be logistically segmented. The

wholesaler’s purchase system covers a much larger set of millers (25 as against

10 for Large-F and 4-5 for Large-A), and from much more widespread regions

in Tamil Nadu, Andhra Pradesh and Karnataka. In the case of Large-E, while

purchase is centralised under a sister company, covering all Large-E stores in

Tamil Nadu, Karnataka and Andhra Pradesh, in practice most of the purchases

for Chennai are sourced from Red Hills. Large-B with a single supermarket

outlet procures all its rice from a single miller in Red Hills. It does not even

have a warehouse, instead paying on a ‘just-in-time’ basis for cleaned, packed

rice which is supplied directly to the store premises.

8The wholesaler in Red Hills explained procurement as the complex part of the rice milling exercise. The profit

of the wholesaler depended on his ability to access the right market at the right time, with a good knowledgeof the seasons. The market determined procurement price could vary by as much as Rs.10 - 20 per 25 kg bag ofrice. He said that this optimum procurement was at the centre of the wholesaler’s business, and was anintegral part of the routine for all wholesalers.

While all three small stores in the sample purchased rice from wholesalers, 2 of

the 3 medium-sized retail stores did not depend on a wholesaler for their rice

purchases, going directly to the millers. One of them, Medium-N in Ambattur,

specified that they made their purchases from millers in Arni (115 kms from

Chennai) as the millers there used old technology for drying rice, resulting in

better quality. This medium store therefore had a more complex structure for

purchase than Large-B, which purchased rice from one miller in Red Hills.

Third, the large retail chains all hire trucks rather than operating their own fleet

of trucks, similar to wholesale dealers. However, while Large-E has a dedicated

transport service for costly white goods, all its bulky low-cost commodity

purchases are transported using hired vehicles.

Fourth, the wholesaler deals solely in rice, and makes a reported net profit

margin of around 5% from that commodity. The wholesaler’s retail costs are

likely to be significantly lower than for corporate retail. The shelf period and

inventory are likely to be low as the wholesaler deals with a smaller number of

customers, its customer being retail stores. Each of these buy fixed quantity of a

limited set of products (different varieties of rice) at reasonably predictable and

fixed schedules. The wholesaler is likely to deal with a more limited number of

transactions each month as compared to the large retailer which caters a larger

number of retail customers with a highly varied product range and varied

buying preferences. This leads to lower transaction costs and overheads for the

wholesaler due to its much simpler business model. For the large retailer

however, rice is a small fraction of the total turnover, with low profit margins.

The large retail chains gave their gross mark-up on rice as between 2-5%9. This

would hardly cover their cost of inventory, shelf space, and the overheads

apportioned to rice. The fixed cost for shelf space would also be significantly

higher for the large retailer. As the Manager at Large-B explained, “the profit

9This margin is much lower than for small retail.

margins are deliberately kept low for certain essential items like rice , pulses,

spices, eggs etc because customers will purchase other items if they feel that

prices are generally lower.” In effect, for these large retail stores, rice along

with other staple commodities is a loss-leader, being cross-subsidised by other

products. Rice attracts customers, while other high value items provide profits.

Logistics, costs and returns:

Paddy-Rice Milling

Further down the supply chain is the paddy milling stage – with a single case

study. The rice miller (CRM)10 in Red Hills gave the following details of the

rice milling operations. The 500 MT rice per month mill has been in operation

for the past 70 years, and was modernised in 2009. All operations were

mechanised except for packaging. Around 80% of the rice processed was

parboiled rice, the remaining 20% being raw rice.

The sourcing of different varieties of paddy was done on a daily basis

depending on the demand from 4-5 private wholesale grain mandis (commodity

markets) in Red Hills. Certain types of paddy were available only seasonally.

Unusually, the mill had no medium term storage warehouses, and so paddy had

to be milled within the week.

Loading and unloading:

Loading and unloading activities in mandis are highly organised, with strict

rules governing entry. From interviews with loading workers in one of the

mandi at Red Hills, the respondents were found to be members of an association

10Assumed name. The names of all mills are assumed, for the sake of maintaining anonimity.

of loading and unloading workers, registered in the year 1982 with a current

membership of 171. Each member registering with the association had to pay a

deposit towards membership; current membership rate was Rs.50000 per

person. Regardless of their age and strength, members all shared equally from

the day’s collection. The oldest member in that association was 80 years old.

There were set timings of work: the day shift was from 5AM to 5PM, and the

night shift from 5PM to 5AM the following day. Work was piece-rated, with the

piece-rate renegotiated every three years. The negotiations were bipartite

between the association and the mandi, and there was no state or party political

involvement. The prevailing rates at the time of interview were based on

negotiations conducted in February 2012, and some of the rates were as follows:

Rs.3.30 for a 75kg rice bag; Rs.1.30 for a 25kg rice bag; Rs.5 for a 75kg bag of

broken rice. Day and night shifts had equal pay rates. The respondent said he

made Rs.800 on a good day, and averaged around Rs.400 per day for six days in

a week. There was a weekly compulsory saving of Rs.100 through the

association, used to give loans to members. Each member received a festival

bonus of Rs.3000 for Deepavali and Pongal from the collective savings of the

association and the interest earned on those savings. In addition, the association

also used the savings to support any member unable to work because of ill

health or injury.

The respondent also reported hazards at work. Bran and husk loading was

dangerous because of the dust particles. Loading paddy could lead to skin

allergies, from the pesticide used with paddy cultivation. Accidents could also

happen from muscle sprain and dislocation of bones because of the heavy loads

handled.

Processing:

The miller supplied processing costs as in Table 2 below. There was no inward

transport cost as paddy was purchased locally, and delivered by the mandi

paddy trader to the miller’s premises.

Table2: Case study of rice milling 2013

Parameter Amount

Capacity (MT rice/month) 500

Normal production

- parboiled rice 80%

- raw rice 20%

Cost and estimated profits

- Sale price (fine Ponni Rs/kg) 48.00

- Purchase price of paddy (Rs/kg) 24.00

- Transport cost (Rs/kg rice) 0.60

(range of Rs.0.50 to Rs.0.70/kg)

- Packaging rice

-1 kg pack 0.30

-20 kg pack 0.70

- Processing and milling (Rs/kg) 1.60

(miller gave cost as Rs.120/75 kg rice)

- of which Labour cost (Rs/kg) 0.40

(labour cost is part of processing cost)

- Estimated total cost of processed rice 39.00

(at very low estimate of 65% outturn)

Profit from rice (Rs/kg)11 9.00

Estimated monthly profit (Rs) 4,500,000

(at 500MT rice production)

Source : data from CRM Chennai

The distribution of costs at this stage in the supply chain is as follows: the

purchase cost of paddy is about 77% of the wholesale sales price for rice.

11This estimated profit is only from rice sales, and does not include valuable by-products like rice bran and

husk.

Milling contributes 5 %. Packing and transporting rice contributes another 2%.

The estimated returns from milling are quite substantial compared with those

from downstream retail activities (see WP11, here).

Implications for Large Retail

Such rates of return are incentives to a new scale of national capital. Set against

these profits, entrants would have to compete with the entrenched interests of

existing millers whose supply networks result from long-standing and in-depth

knowledge of local crop patterns and marketed surplus. If a new large scale of

capital enters the milling stage of the supply chain, large business houses might

also seek to modernise the networks and relations of supply. They have the

financial capacity to sustain such investment on their own.

At present however, the interests of big retail in establishing direct backward or

‘upstream’ linkages in this region of India appears low. The proportion of

business comprised by rice is too small to justify the transactions costs of entry.

This is a specialised business, involving procurement at the paddy stage. For

success, it requires a good understanding of farming practices, the crops

available in a season, the prediction for the season of paddy yields, and hence

price of paddy, and the quality of paddy to be expected. CRM mills referred to

their experience over 70 years of procuring paddy and engaging in rice milling.

Further, any miller would also have to deal with the by-products of rice milling,

including rice bran which has a high value but a low shelf life, and rice husk

which has multiple uses as a cattle feed, fuel, and raw material for the

manufacture of particle boards. As against this, the large retailer is content to

deal with the milled product (rice), and not to bear the costs of engagement with

the procurement chain from the earlier stage of paddy or the additional

complexities of dealing directly with the farm produce and its by-products from

milling. This view of the restricted interest of big retail in establishing

backward linkages in rice appears to be corroborated by CRM mills, which

reported having been approached by Walmart with a view to procuring supplies

of rice from them. Even the mega supermarket, whose entry into retail is feared

by many in the industry, as it is expected to have the power to change the

structure of retail and force out of business existing supply chain players, seems

content to abide by the methods adopted by existing large corporate retail

players in the country, at least with respect to rice.

Supply chain logistics and employment

Currently, the entry of large retail business houses has had little impact on

employment relations in activities related to the supply chain of rice. We have

details of employment in Large-E at their warehouse in Red Hills. This

warehouse dealt with a wide range of commodities, with only about 25% of the

space devoted to storing rice.

The warehouse has two managers, 1 commercial person looking after

administration and stocks, 3 as store vehicle escorts, and 2 to supervise loading

and unloading. All actual transportation, loading, unloading activities are done

by contract workers. In 2012-13, purchasing operations did not create many

regulated jobs. By comparison, the specialist rice wholesaler in our study

employed five workers, all on daily contract.

The milling operations also did not employ regular workers. The mill employed

five daily wage workers, paid on piece rates. The workers came from the Irular

tribe, and the miller did not want to discuss details of employment and payment

terms, as the issue of bonded labour among the tribe had already been

investigated in some of the rice mills in the area.12

The public distribution (PDS) for rice: logistics, costs and returns

The rice procurement for the PDS is of a totally different order of magnitude,

with the scales involved dwarfing the purchasing systems in the private sector.

In Tamil Nadu, the Tamil Nadu Civil Supplies Corporation (TNCSC) projected

its monthly procurement of rice as around 3.2 lakh (320,000) MT.13 This is

more than a thousand times the quantity of rice procured by the large, multi-

branch corporate retail chains in Chennai.

12I Guerin 2009 in (Eds) Breman, Guerin and Prakash’ India's Unfree Workforce: Of Bondage Old and New, New

Delhi, OUP13 http://www.commodityonline.com/news/india-govt-proclaims-msps-for-2013-14-kharif-season-

crops-55184-3-55185.html

Table3: Costing of rice procured by TNCSC

Percent

Item of incidentals Raw rice Par-boiled rice eco-cost

Common Grade A Common Grade A Parboiled

Rs/quintal Rs/quintal Rs/quintal Rs/quintal common

A. Acquisition costs(.68outturn)

Minimum support price (MSP) 1250.00 1280.00 1250.00 1280.00 80.8%

Mandi labour charges 4.06 4.06 4.06 4.06 0.3%

Transport to mill 12.32 12.32 12.32 12.32 0.8%

Driage @ 1% MSP 12.50 12.80 0.00 0.00 0.0%

Commission to societies (2.5%) 31.25 32.00 31.25 32.00 2.0%

Custody & maintenance charges 8.32 8.32 8.32 8.32 0.5%

Interest charges 51.42 52.65 51.42 52.65 3.3%

Milling charges (incl 8km transport) 15.00 15.00 25.00 25.00 1.6%

Administrative charges (1% MSP) 12.50 12.80 12.50 12.80 0.8%

Cost per quintal milled rice 1397.37 1429.95 1394.87 1427.15 90.2%

Out-turn ratio 0.67 0.67 0.68 0.68

Sub-total (cost at mill head) 2085.63 2134.25 2051.28 2098.75 90.2%

Transport miller to warehouse 14.12 14.12 14.12 14.12 0.6%

Cost new gunny bags 70.86 70.86 70.86 70.86 3.1%

Gunny bag depreciation 28.34 28.34 28.34 28.34 1.2%

Acquisition cost for rice 2198.95 2247.57 2164.60 2212.07 95.2%

B. Distribution costs

Storage costs (2 months) 8.58 8.58 8.58 8.58 0.4%

Handling charges 4.47 4.47 4.47 4.47 0.2%

Interest charges (2 months) 43.51 44.46 42.82 43.76 1.9%

Transit and storage loss (0.35%) 7.35 7.52 7.23 7.40 0.3%

Administrative charges (2.5%MSP) 46.64 47.76 45.96 47.06 2.0%

Total distribution cost 110.55 112.79 109.06 111.27 4.8%

Economic cost (A+B) 2309.50 2360.36 2273.66 2323.34 100%

Source: Provisional economic cost of custom milled rice for Kharif 2012, Govt of Tamil

Nadu.

The TNCSC makes a district-wide allocation based on which the Food

Corporation of India (the central government agency for procuring rice) gives a

release order through the 40 depots in various localities in the State.14 In Tamil

Nadu alone a decentralised purchase system is present through which the Tamil

14Sometimes an ad hoc allotment may happen - approximately once every six months.

Nadu Civil Supplies Corporation can procure paddy from farmers on behalf of

FCI. This is done by opening Direct Purchase Centres in each district where

paddy is procured directly from the farmers at the Minimum Support Price

declared by the Central Government.

Table 3 gives Government estimates for costs along the procurement chain. The

percent costs take into account the conversion from paddy to rice, with the

corresponding reduction in weight resulting from the out-turn ratio. The

percentages for parboiled rice are based on 1 quintal (100 kg) paddy being

processed to 68 kg rice.

Broadly the distribution of costs along the procurement chain is as follows: The

procurement cost of paddy is, as in the private sector, about 80% of the final

economic cost of rice at the PDS store. At the stage of milled rice the cost

increases by 10%. The cost of packing rice and transporting it to the FCI or

TNCSC warehouse contributes another 5%. Final distribution costs complete

the last 5%. However there are hidden subsidies in the process, especially at the

milling stage, which will be discussed later.

In the PDS system, the cost of paddy, the “minimum support price”, is 80.8% of

the economic cost of milled rice; as compared to the private sector, where the

miller estimated paddy cost as 77% of the wholesale price for rice. We see that

contrary to general notions of the inefficiency of the government run PDS, in

this case, the government system appears to have a lower mark-up over the

purchase cost of paddy for its economic cost of rice, compared with that for

wholesale price of rice over the purchase cost of paddy in the private system.

These figures indicate that the economics for the PDS are at least as efficient as

in the case of private distribution for rice.

One significant advantage from the large scale of operations of TNCSC is in the

costs of transport. Most of the transport of paddy from the procurement to

milling stage is done by rail. As per TNCSC data for the kharif of 2012, the cost

of transporting paddy by rail from Thanjavur to Chennai (336km) was Rs.540

per MT: Rs.1.61 per km-MT of paddy. The corresponding road haulage cost for

a private wholesaler15 is almost twice as great: Rs.1500 per MT from Raichur

to Chennai (500 kms) i.e. Rs 3 per km-MT of rice. 16

The large scale of operations also allows the TNCSC to engage large

transporters on annual contract for transporting paddy from the rail head in

Chennai to the miller. This has also given the Corporation significant

advantages of scale in driving a good bargain. According to the transport

contractor for 2012-13, he was paid at the rate of Rs.90-140 per MT for

paddy/rice transported from the rail head at Salt Cotaurs in Chennai to Egmore

(around 6 km) and Royapuram (around 10 km). This worked out to around

Rs.15 per km-MT for short distance city transport. In contrast WS Wholesaler

paid Rs.10 per 25 kg bag from the mill head at Red Hills to his premises (10

km): around Rs.40 per km-MT for transport within the city. As per the TNCSC

rules for the contract the contractor had to own at least 15 trucks. This reliance

on larger transporters and ability to negotiate on a greater scale has also ensured

better reliability of transport.

Labour in loading and transport:

According to the transport contractor, the work load varied between around

40000 MT per month during peak season (February, March, April) to 15000

MT per month during the lean season. When a train load arrived, around 120

15WS Wholesaler (name changed – refer to WP(11))16 Corroborated by Large-E : road transport costs through its subsidiary were said to range fromRs.1500-2000 for the procurement of rice from Raichur and Bellary. This works out to Rs.3-4 per km-MT. We should also take into account that the road transport data for the private enterprises wasfor milled rice which has a smaller bulk than paddy, and can hence be packed better. Transport costfor paddy would be higher than for rice.

daily wage migrant workers were employed, in order to clear the railway yard in

the minimum possible time and avoid any demurrage. The workers were paid

Rs.1.50 per 40 kg bag of rice or paddy. A worker loading 10 MT in a day on to

the truck from the railway wagon would earn Rs.375. Drivers were paid Rs.500

per day, plus Rs.100 as mamool17 for a single trip, and Rs.300 if he made two

trips to and fro. During the peak season the driver could even make three trips,

and earn a mamool of Rs.500 in addition to the Rs.500 fee for the day.

Labour in PDS rice milling:

Table 4 gives labour cost estimates for PPP Modern Rice Mill, Red Hills, a

private miller contracted out to the TNCSC for PDS rice and TUV Mill, one of

the 23 mills owned by the TNCSC18. The data for PPP Modern Rice Mill is

based on interviews with the owner, while data for TUV Rice Mill was derived

from the actual monthly working results for July 2013. Both mills are of

comparable size, and milling capacity.

The TNCSC mill and the private mill differ in their use of contracts: for

tenured/ regular and contract/casual labour. The details are as follows:

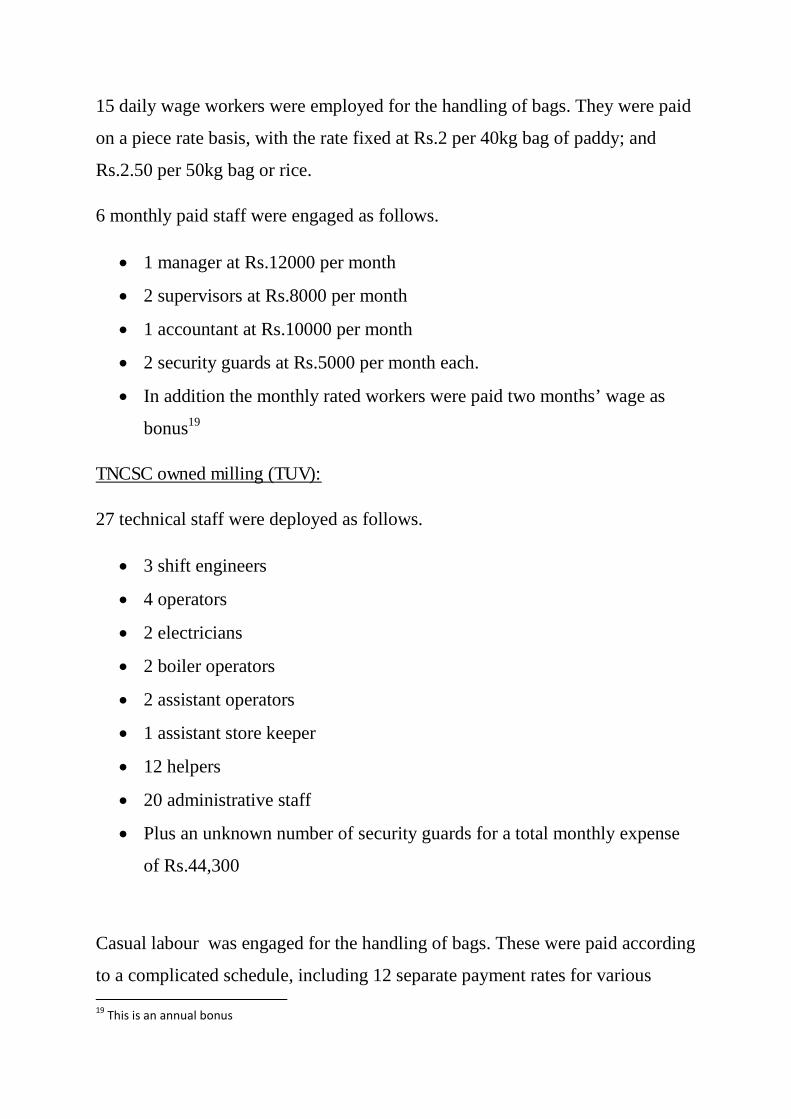

Private milling (PPP):

4 mill operators were employed on 12 hour shifts. The production norm was

48MT rice per shift. The mill employees were:

2 women at Rs. 225 per day

1 man at Rs. 350 per day

1 operator at Rs. 300 per day

In addition the operators were paid Rs.150 per day for food and tea.

17A routine bribe (Tamil)

18Names of rice mills are assumed names.

15 daily wage workers were employed for the handling of bags. They were paid

on a piece rate basis, with the rate fixed at Rs.2 per 40kg bag of paddy; and

Rs.2.50 per 50kg bag or rice.

6 monthly paid staff were engaged as follows.

1 manager at Rs.12000 per month

2 supervisors at Rs.8000 per month

1 accountant at Rs.10000 per month

2 security guards at Rs.5000 per month each.

In addition the monthly rated workers were paid two months’ wage as

bonus19

TNCSC owned milling (TUV):

27 technical staff were deployed as follows.

3 shift engineers

4 operators

2 electricians

2 boiler operators

2 assistant operators

1 assistant store keeper

12 helpers

20 administrative staff

Plus an unknown number of security guards for a total monthly expense

of Rs.44,300

Casual labour was engaged for the handling of bags. These were paid according

to a complicated schedule, including 12 separate payment rates for various

19This is an annual bonus

tasks. Even within the PDS the labour in the state-owned mill works on more

formally regulated terms than its equivalent in the private owned mill contracted

to the PDS. It is significant that both the mills were of comparable production

capacity.

Consequently the ratio of piece-rated wages to the total wage bill in the private

mill was 92%, as compared with just 28% in the TNCSC mill. The cost of

labour per kg rice in the TNCSC mill at full rated mill capacity ( 1751 MT rice,

the equivalent of about 2500 MT paddy), was about 50% higher than for the

private mill that is contracted-in (private mill costs were estimated for the same

assumed production of 1751 MT raw rice). In fact, the private mill costs

confirm the data for the Red Hills private miller, CRM, operating in the private

supply chain to private retailers. The miller gave labour cost as Rs.30 per 75 kg

rice: Rs.0.40 per kg rice milled (see Table2). We may assume that the details of

labour costs here are broadly in line for all large, modern, private rice millers.

Table 4: Comparison of labour costs in milling

Category Private TNSC owned

miller Mill

Capacity (MT /month) 2700 2500

Assumed production of rice (MT) 1751 1751

Monthly rated

Staff salaries (Rs/month)

-4 admin in pvt 38000.00

-27 technical+20 admin in TNSC mill 594514.00

- security staff 10000.00 44830.00

Total monthly rated 48000.00 639344.00

Piece rated

Daily rated (pvt for 1751MT)

- Mill staff (2 women, I man, 40127.08

I operator)

Casual labour

-piece rate in pvt for 1751 MT rice 496975.00

- public for 1751MT rice 253118.00

(Note: in TNSC mill technical staff

includes 12 helpers, who would

also do some casual tasks)

Total piece rated 537102.08 253118.00

Total for 1751MT rice 585102.08 892462.00

Labour cost per kg rice 0.33 0.51

Ratio of piece rate to total wage 92% 28%

Source: Interviews with PPP Modern Rice Mills, Red Hills, private miller contracted out tothe TNCSC for PDS rice and actual milling cost data for TUV Rice Mills, one of the 23 millsowned by the TNCSC.

We see that in the TNCSC mill the labour cost per kg is significantly higher.

However there would be some extra built-in labour costs in the working of a

public sector mill, especially due to the high component of administrative staff.

The mill has 20 administrative staff on its rolls, as compared to 4 in the private

mill. If we factor in the likelihood that administrative staff component in the

public establishment might be excessive, and allow for a leaner establishment, a

private mill contracted to the PDS could, within its present profitability

parameters absorb the increased cost of a regular workforce employed on better

terms and conditions.

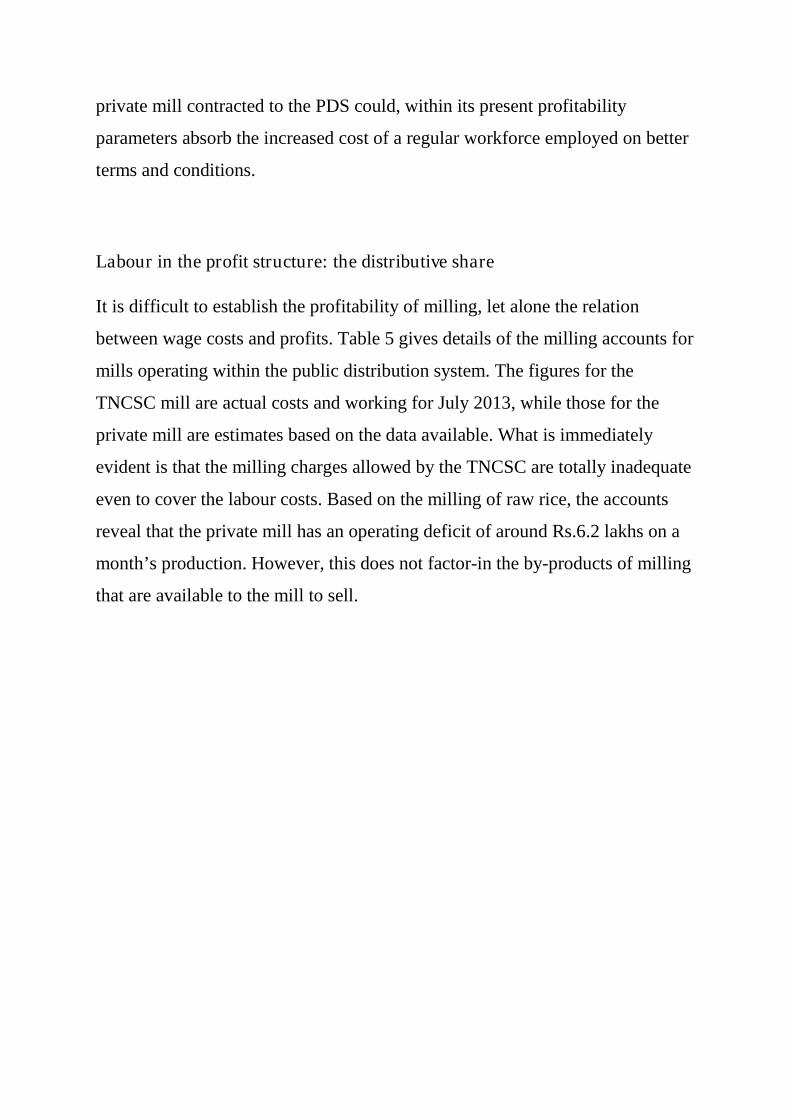

Labour in the profit structure: the distributive share

It is difficult to establish the profitability of milling, let alone the relation

between wage costs and profits. Table 5 gives details of the milling accounts for

mills operating within the public distribution system. The figures for the

TNCSC mill are actual costs and working for July 2013, while those for the

private mill are estimates based on the data available. What is immediately

evident is that the milling charges allowed by the TNCSC are totally inadequate

even to cover the labour costs. Based on the milling of raw rice, the accounts

reveal that the private mill has an operating deficit of around Rs.6.2 lakhs on a

month’s production. However, this does not factor-in the by-products of milling

that are available to the mill to sell.

Table5: Economics of rice milling under PDS

TNSC owned Private

Mill(permonth)

Miller(permonth)

Milling charges for 1751 MT raw rice 257500.00 257500.00

(Rs.10/quintal paddy)

Labour costs (estimates for private) 892462.00 585102.08

Power (private=22 units/MT@ Rs.6.50/unit) 473350.00 250393.00

Other costs (estimates for private) 38910.00 50000.00

Operational margin -1147222.00 -627995.08

Rice bran sale (estimates for private) 1423888.00 1534700.00

(4% bran @ Rs.14900/MT)

Operational profit 276666.00 906704.92

Rice including brokens in excess of20 141.63

milling norm (average yield=73.5%) (MT)

Paddy husk (average yield=21.2%)21 (MT) 540.75

Source: Actual working results of TNSC owned mills for July 2013 and estimates for private

miller

Table 6: Standard yield of rice and by-products from milling

Rice variety Yield (%)

Milled Husk Bran

rice

White Ponni raw 71.3 23.0 3.9

White Ponni parboiled 72.7 21.8 1.8

Average (15 varieties) raw 73.5 21.2 4.5

Average (15 varieties) parboiled 74.4 20.1 2.7

Source: “Milling characteristics of raw and popular rice cultivars”, Armugachary S. et al,

International Rice Research Notes, 20(3), September 1995

20These are standard yields determined in field testing with lab scale milling equipment (results shown in

Table6). The actual milling results in commercial operations might vary substantially from the results.However, the results do suggest that a well run mill can get substantially higher rice yields (whole and brokenrice) than the specified norms of the TNCSC. Some broken rice may emerge with the husk and may not beseparable.21

Rice husk has a ready market, and is used as cattle feed, raw material for particle boards, and fuel inburners. It has a ready market. According to the Technology, Information Forecasting and Assessing Council,Government of India, rice husk price varied between Rs.300-800 per MT in 1993 (www.tifac.org.in).

Table 6 above gives standard yields of rice and by-products during rice milling

undertaken in field testing conditions. The milling of raw rice yields an average

of 4.5% rice bran. Assuming a bran yield of 4% and price of Rs.14,900 per MT,

which was the actual bran price for the TNCSC mill in July 2013, the sale of

bran alone affords the private mill an additional income of Rs.15.3 lakhs. This

would more than sufficient to cover the apparent operational deficit on rice.

We have not taken into account here other costs of finance and depreciation,

and these might still add up to a significant figure. The cost figures given by

CRM Mills, the mill dealing with private retailers, indicated that the total

milling cost was four times the labour cost (see Table 2). This would mean an

additional Rs.15 lakhs cost, over that of labour. However, if we consider the

standard rice-milling yield, the private mill would have generated around

141MT of rice during the month (whole and broken), more than the standard for

production of 67% for raw rice prescribed by the TNCSC. This additional

revenue at even a low price of Rs.15 per kg could give the miller around Rs.21

lakhs. In addition, the paddy husk also has a ready market. In 1993, the

estimated sale value of paddy husk was around Rs.300-800 per MT. As stated,

the returns from rice milling within the PDS system would therefore afford the

mill a substantial return, even though the milling charge given by the TNCSC is

not sufficient to cover labour charges This however is before we have taken into

account the potential returns from paddy husk which also has a commercial

value as a fuel. We can therefore infer that within the system, the mill can, if all

products are taken into account, afford to bear a much higher operational cost.

With regard to the quality of work, it is definitely possible for the private mill to

afford the increased costs of a permanent workforce with labour rights. .

Conclusions – implications of the supply chains for employment

As of 2012-3, the activities in the rice supply chains upstream of big and small

retail do not create substantial regulated employment. The entry of big retail

also appears to generate neither institutional nor employment multipliers. Their

current operations seem to mirror existing purchasing practices, incorporating

reasonably high degrees of operational efficiency, with supply contracts that

allow retailers flexibility with low inventory plus the benefits of multi-sourcing.

In this context, and given the low contribution that rice makes to turnover and

profits, incentives to large corporates to invest substantially in modifying the

supply chain are low.

Three aspects of the rice trade would suggest that a large corporate company

might not find it easy to develop the backward integration of paddy milling,

even if it afforded reasonable profits. First, as explained earlier, paddy milling is

a complex operation. It involves dealing directly with farmers/grain traders. The

existing rice mills would have built their custom over a long period, with

linkages of trust in rice output and quality. Further, the mills would also have to

deal with other by-products of rice milling to obtain returns from the business,

sufficient to cover costs fully.

Second, the scale of operations for a modern rice mill is very high. The two rice

mills studies in the PDS system were of 2500MT per month milling capacity.

This represents around five times the size of monthly rice purchase even for a

large operation like Large-A, with 74 retail stores in Chennai. A rice mill run by

a large corporate would therefore have to get into branding and selling through

other distribution channels not owned by the corporate, in order to fully occupy

its capacity and maximise returns.

Third, rice and staples do not presently seem an important priority for large,

corporate retail. As explained by several managers in the sector, the turnover

from rice was less than 5% of the total turnover. Our own estimates with Large-

B indicated that the annual sales from rice represented only 2% of the total

business of the supermarket. Further, the opinion from managers was also that

staples were not seen as contributing to profits, but were “loss-leaders”,

maintained in order to attract custom of other, more profitable goods. In this

context it seems doubtful that the management in the sector would look consider

investing significantly in backward integration and/or improving returns from

rice in their business model. The only probable exception in our sample was

Large-E, where the group had a sister concern, a wholly owned subsidiary

which handled all sourcing of staples. This model, where an independent

subsidiary was tasked with the procurement business, might see business sense

in exploring profitable backward linkages.

It is possible that corporates could adopt another business model – that of

custom milling by private rice mills. This could give them control over the

quality of rice, better determined at the stage of paddy, together with lower

costs of procurement. They could follow the model adopted by the PDS system

in order to achieve this. However, this would mean having to deal both with

renting-in only part of the capacity of the rice mill, being able to negotiate

returns from by-products into the contract for custom milling.

The analysis of the public distribution system raises important issues in supply

chain management with implications for labour. First, the large scale of PDS

operation allows it both economies of scale and flexibility for cost cutting,

particularly in transport of paddy and rice over long distances. The transport

cost as proportion of total costs (1.4% of the final economic cost of rice as

estimated by the Tamil Nadu Civil Supplies Corporation (TNSCS) is not

significant - at least to the stage at which milled rice reaches the local

warehouse. Second, milling for the PDS is reasonably profitable, depending

upon the economic returns from bran and husk, the by-products of rice milling,

and the profits of informally traded rice that might accrue to the miller from the

difference between the actual milling outturn22 and the lower one stipulated by

the TNCSC.

The rates of return that we have estimated from mill accounts suggest that

workers in private mills within the PDS system could bargain for better pay and

working conditions without threatening the current viability of these mills. The

current system is dominated by low wages and the regular flouting of

employment law, so future bargaining will have real benefit for workers..

Finally, the figures obtained suggested that the paddy procurement and rice

milling and distribution operation under PDS was as cost effective as in the

private sector. This calls to question the position held by proponents of market

efficiency that large-scale state interventions in public service delivery are

necessarily inefficient and essentially ill-advised. We should add the caveat here

that our conclusions for the private sector were based on discussions with one

case-studied rice miller, albeit a miller with a declared 70 years’ experience in

the trade. We should also add that PDS in Tamil Nadu is acclaimed among the

most efficient in the country, and may not represent typical practice. 23

22The proportion of milled rice obtained per unit of un-milled paddy

23See for instance The Hindu, August11, 2010, “Behind the success story of universal PDS in Tamil Nadu”; and

“Brief 101: Trends in Diversion of PDS grains” Centre for Development Studies, Delhi School of Economics,Working Paper No. 198, March, New Delhi Khera, Reetika (2011), www.ifad.org/drd/agriculture/101.htm