15-1 copyright 2007 mcgraw-hill australia pty ltd ppts t/a australian financial accounting 5e by...

TRANSCRIPT

15-1 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Chapter 15

Accounting for financial instruments

15-2 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Learning objectives

• Understand what a financial instrument is• Be able to describe various types of financial

instruments• Understand the difference between a primary

financial instrument and a derivative financial instrument

• Understand that some derivative financial instruments can significantly increase the risk exposure of an organisation, and so appreciate the necessity for full disclosure in relation to such instruments

15-3 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Learning objectives (cont.)

• Understand what a compound financial instrument is and how the debt and equity components of a compound equity instrument are to be determined

• Understand the requirements of AASB 7 - ‘Financial Instruments: Disclosure’; AASB 132 - ‘Financial Instruments: Presentation’ and AASB 139

- ‘Financial Instruments: Recognition and Measurement’

• Be able to provide accounting entries for various types of futures contracts, options, swap agreements and compound financial instruments

15-4 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Relevant accounting standardsThere are three standards:

1. AASB 7 ‘Financial Instruments: Disclosure’

2. AASB 132 ‘Financial Instruments: Presentation’; and

3. AASB 139 ‘Financial Instruments: Recognition and Measurement’

15-5 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Financial instruments defined

• A financial instrument (AASB 132) is– any contract that gives rise to both a financial asset of

one entity and a financial liability or equity instrument of another entity

• A financial asset (AASB 132) is– cash; or

– a contractual right to receive cash or another financial asset from another entity; or

– a contractual right to exchange financial instruments with another entity under conditions that are potentially favourable; or

– an equity instrument of another entity

15-6 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Financial instruments defined (cont.)

• A financial liability (AASB 132) is– any liability that is a contractual obligation

to deliver cash or another financial asset to another entity; or

to exchange financial assets or liabilities with another entity under conditions that are potentially unfavourable; or

– a contract that is a derivative; or

– a non-derivative

• An equity instrument (AASB 132) is– any contract that evidences a residual interest in the

assets of another entity after deduction of all its liabilities

15-7 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Financial instruments defined (cont.)• Central to the definition is whether or not a

‘contractual obligation’ exists– if there is no contractual obligation to deliver cash or

another financial asset, or to exchange another financial instrument under conditions that are potentially unfavourable, it is considered to be an equity instrument

– what does ‘unfavourable’ mean in this context? – see Worked Example 15.1 (p. 507) which shows how the issue of share options creates a financial asset in the accounts of the holder of the options, and a financial liability in the accounts of the issuer

– in the context of the issue of options, the likelihood of the option being exercised does not impact on its classification as a financial liability

15-8 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Financial instruments defined (cont.)

• Examples of financial instruments– cash at bank

– bank overdrafts

– term deposits

– trade receivables and payables

– investments

– options

– forward foreign exchange agreements

– foreign currency swaps

15-9 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Financial instruments defined (cont.)

• Primary financial instruments– include receivables, payables and equity securities such

as ordinary shares – accounting treatment fairly straightforward

• Derivative financial instruments– create rights and obligations with the effect of

transferring one or more of the financial risks inherent in an underlying primary financial instrument

– include financial options, futures, forward contracts and interest rate and currency swaps

• Refer to Worked Example 15.2 (p. 510)

15-10 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Debt versus equity components of financial instruments

• The issuer of a financial instrument must determine whether to disclose it as a liability or equity (AASB 132)– they are required to consider economic substance rather

than just the legal form

• Critical feature in differentiating financial liability from equity is the existence of a contractual obligation on the part of one entity either to deliver cash or another financial asset to, or to exchange another financial instrument

15-11 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Debt versus equity components of financial instruments (cont.)

• Preference shares– if there is an option to redeem the shares for cash,

should be debt rather than equity

– when distributions to shareholders are at the issuer’s discretion, shares are equity

• If classified as debt, then periodic payments are classified as interest expenses, which will affect profits

15-12 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Debt versus equity components of financial instruments (cont.)

• Convertible notes– debt giving the holder the right to convert securities into

the issuer’s ordinary shares

– often classified as compound financial instruments, containing both a financial liability and equity component

– debt and equity components to be accounted for and disclosed separately

• Interest can be treated as part of the cost of an asset under construction

15-13 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Debt versus equity components of financial instruments (cont.)

• Instruments cannot be reclassified after initial recognition unless– their substance is altered by a transaction or other

specific action by the issuer (AASB 132)

• The AASB Framework allows reclassifications based on revised probabilities (however, accounting standards take precedence)

• Determine fair value of liability component and equity component as the residual

15-14 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Measurement of financial instruments

• According to AASB 139– financial instruments are generally to be measured at

fair value, with some exceptions

• Categories of financial instruments (AASB 139)– financial asset or financial liability at fair value through

profit and loss;

– held-to-maturity investments;

– loans and receivables;

– available-for-sale financial assets

15-15 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Financial asset or financial liability at fair value through profit or loss

• Financial asset or financial liability at fair value through profit or loss if (AASB 139)– classified as held for trading; or

– upon initial recognition it is designated by entity as at fair value through profit or loss

– periodic adjustments go to profit or loss

15-16 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Available-for-sale financial assets

• Includes all financial assets that don’t fall into other categories

• Equity investments to be measured at fair value

• Changes in fair value recognised in equity until financial asset is derecognised

15-17 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Loans and receivables and held-to-maturity investments

• To be measured at amortised cost using the effective-interest method

• If an impairment loss has been incurred, amount of loss is calculated as (AASB 139)– the difference between asset’s carrying amount and

present value of estimated future cash flows with; carrying amount to be reduced directly or through an

allowance account loss to be recognised in profit or loss

15-18 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Other financial liabilities

• To be recognised at amortised cost using effective-interest method subsequent to initial measurement (AASB 139)

• Refer to Worked Example 15.3 (p. 521)

15-19 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Derivative financial instruments

• Can include– futures contracts

– options contracts

– interest rate swaps

– foreign currency swaps

– forward-rate contracts

• To be recognised initially at fair value (AASB 139)

15-20 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Derivatives used within a hedging arrangement

• Derivatives often used to hedge gains or losses in future in relation to other assets or liabilities

• Hedge contract– arrangement with another party in which that party accepts

the risks associated with changing commodity prices or exchange rates

• Three principal types of hedges (AASB 139)1. fair value hedges2. cash-flow hedges 3. hedges of net investments in foreign operations

• Need to differentiate between hedged item and hedging instrument

• Refer to Worked Example 15.4 (p. 522)

15-21 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Derivatives used within a hedging arrangement (cont.)

• Fair value hedge– used to hedge the value of particular assets or liabilities

• Cash-flow hedge– used to hedge a future expected cash flow

• Unless certain strict requirements are satisfied (AASB 139)– any gain or loss on hedging instrument to be taken to

profit or loss

15-22 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Derivatives used within a hedging arrangement (cont.)

• Tests for hedge effectiveness– at inception of hedge and throughout its life, hedge must

be ‘highly effective’

– as measured each financial period, hedge is deemed to be highly effective so that actual results are between 80 and 125%

• Fair value hedge– both hedged item and hedging instrument to be

measured at fair value

– any gains or losses to be included as part of profit or loss

15-23 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Derivatives used within a hedging arrangement (cont.)

• Cash-flow hedge– gain or loss on measuring hedged item at fair value is to

be part of period’s profit or loss

– gain or loss on hedging instrument initially transferred to equity, then transferred to income statement to offset gains or losses on hedged item

15-24 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Futures contracts

• A contract to buy or sell an agreed quantity of a particular item, at an agreed price, on a specific date

• Buy or sell price determined on date contract entered into

• First futures contracts introduced in 1960 in Australia for greasy wool

• Majority of trading volume now relates to financial futures– result in the ultimate transfer of cash or another financial

instrument

15-25 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Futures contracts (cont.)

• Financial futures currently traded– 90-day bank bill futures

– 3-year bond futures

– 10-year bond futures

– share price index futures (SPI futures)

– futures for shares in specific companies

• Huge losses (or gains) can be made on the futures market

• Refer to Worked Examples 15.5 and 15.6

15-26 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Futures contracts (cont.)

• Share price index (SPI) futures– based on e.g. market prices of top 200 companies and

on performance of top 50 companies

– directly related to the All Ordinaries SPI

– may be used for hedging purposes or speculation

• Refer to Worked Example 15.7 (p. 529)

15-27 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for SPI futures

• To make a percentage deposit with the futures broker

Debit Deposit on SPI futuresCredit Cash at bank

• To ‘mark to market’ the value of the organisation’s share portfolio

Debit Loss on share portfolio

Credit Share portfolio

• To credit gains to the initial deposit held by the futures broker

Debit Deposit held by brokerCredit Gain on futures contract

15-28 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for SPI futures (cont.)

• If shares are sold and futures contract is closed out

Debit Cash

Debit Loss on share portfolio

Credit Share portfolio

Debit Deposit held by broker

Credit Gain on futures contract

Debit Cash at bank

Credit Deposit held by broker

15-29 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for currency futures• Refer to Worked Example 15.8

• To record sale at spot rateDebit Accounts receivableDebit Cost of goods sold

Credit Sales revenueCredit Inventory

• To record deposit made with futures brokerDebit Deposit on futures contract

Credit Cash at bank

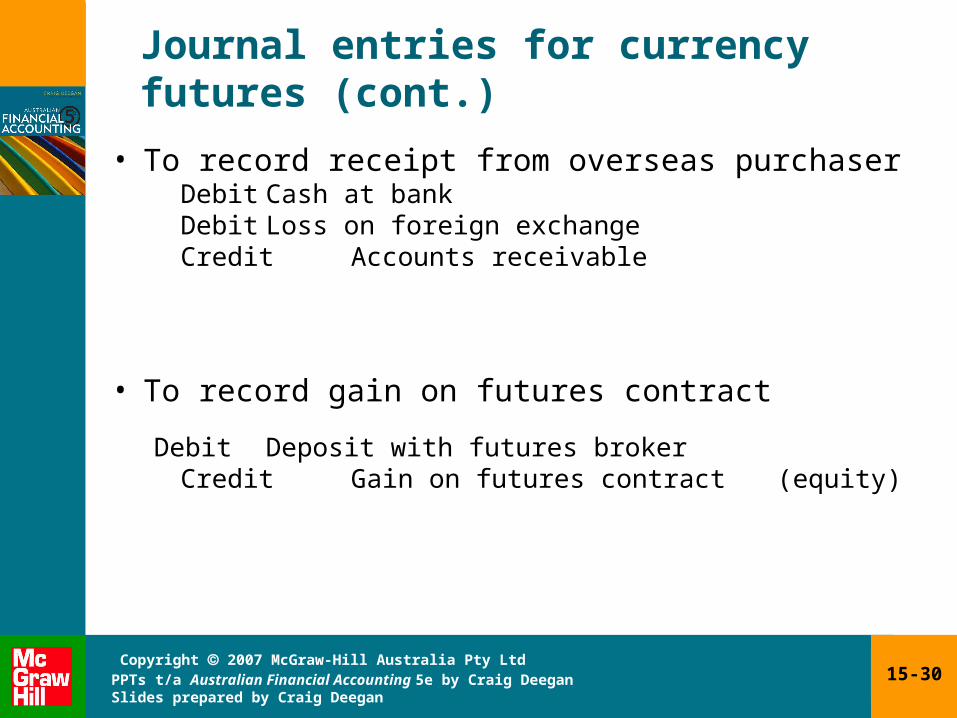

15-30 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for currency futures (cont.)

• To record receipt from overseas purchaserDebit Cash at bankDebit Loss on foreign exchange

Credit Accounts receivable

• To record gain on futures contract

Debit Deposit with futures brokerCredit Gain on futures contract

(equity)

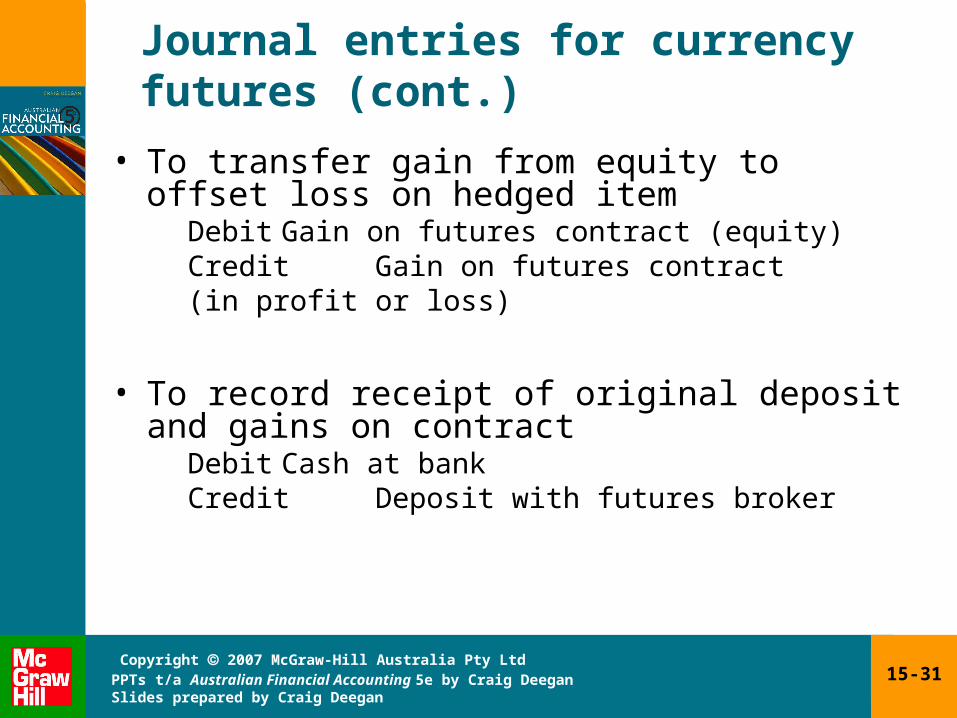

15-31 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for currency futures (cont.)

• To transfer gain from equity to offset loss on hedged item

Debit Gain on futures contract (equity)Credit Gain on futures contract

(in profit or loss)

• To record receipt of original deposit and gains on contract

Debit Cash at bankCredit Deposit with futures broker

15-32 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Options

• Put options– give their holder the right to sell an asset, at a specified

exercise price, on or before a specified date

– value of option depends on market price of underlying security

• Call options– give their holder the right to buy an asset, at a specified

exercise price, on or before a specified date

15-33 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Options (cont.)

• Exercise price– the price the option holder will pay to buy a company’s

shares

• Once exercise price is determined, it remains fixed, regardless of variations in market price of shares

• When an option is acquired on the ASX, an amount is paid for it

• The holder of the option has the right to exercise the option, but typically does not have to do so

• Options are to measured at fair value, with changes included as part of profit or loss

15-34 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for options

• Refer to Worked Example 15.9 (p. 535)

• To record investment in share optionsDebit Investment in share options

Credit Cash at bank

• To value share options at fair valueDebit Investment in share options

Credit Profit on share options

15-35 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

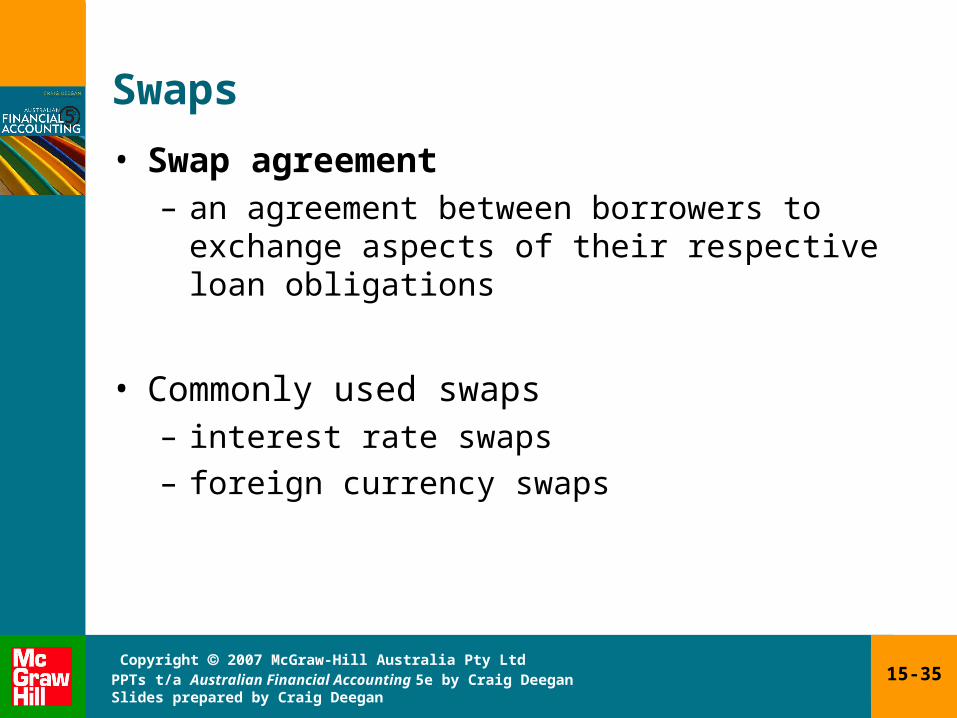

Swaps

• Swap agreement– an agreement between borrowers to exchange

aspects of their respective loan obligations

• Commonly used swaps– interest rate swaps– foreign currency swaps

15-36 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Swaps (cont.)

• Foreign currency swaps– obligation relating to a loan in one currency is swapped

for that of a loan in another currency

– used when entity has receivables and payables both denominated in a different foreign currency

– used to hedge against effects of changes in exchange rates

– entity seeks another entity that is prepared to swap its foreign currency loans for the entity’s domestic loans

– primary borrower still has commitment to primary lender should the other party to the swap default on the arrangement

15-37 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for foreign currency swaps

• Refer to Worked Examples 15.10 and 15.11• To recognise initial loan received

Debit CashCredit Foreign loan

• To recognise the swapDebit Foreign currency receivable

Credit Australian loan

• To recognise loss on the foreign loanDebit Foreign exchange loss

Credit Foreign loan

• To recognise gain on the receivableDebit Foreign currency receivable

Credit Foreign exchange gain

15-38 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for foreign currency swaps (cont.)• To recognise payment made to foreign company

Debit Interest expenseCredit Cash

• To recognise payment made to other companyDebit Interest expense

Credit Cash

• To recognise domestic loan taken outDebit Cash

Credit Loan• To recognise the swap

Debit Loan receivableCredit Foreign currency payable

15-39 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for foreign currency swaps (cont.)

• To recognise the loss on the foreign loanDebit Foreign exchange loss

Credit Foreign currency payable

• To recognise interest payment on domestic loanDebit Interest expense

Credit Cash

• To recognise adjustment to interest expenseDebit Cash

Credit Interest expense

15-40 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Swaps (cont.)

• Interest rate swaps– one party exchanges interest payments of a specified

amount with another party

– generally involves swapping variable or floating interest rate payments for a fixed interest rate obligation

– for a swap to proceed both parties need to receive benefits in the form of a reduction in total interest payments

• Refer to Worked Example 15.12

15-41 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Compound instruments

• Contain both a financial liability and an equity component

• Include convertible notes– similar to convertible bonds, except less formal in the

absence of a detailed deed

• AASB 132 requires– equity component to be fair value of the whole

instrument less fair value of the liability component. That is, the equity component is the residual measure

• The AASB Framework considers perceived probabilities of conversion– differently from AASB 132

15-42 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for compound instruments

• Refer to Worked Example 15.13 (p. 542)• To record the issue of the convertible bonds

Debit Cash at bankCredit Convertible bonds (liability)Credit Convertible bonds (equity)

The liability component is determined by calculating the present value of the future cash flows at the market’s required rate of return based on “instruments of comparable credit status and providing substantially the same cash flows, on the same terms, but without the conversion option” (AASB 132)

• To recognise interest expenseDebit Interest expense

Credit CashCredit Convertible bonds (liability)

Interest expense equals the present value of the opening liability multiplied by the market rate if interest

15-43 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Journal entries for compound instruments (cont.)

If option holders elect to convert options to ordinary shares

• To recognise interest expenseDebit Interest expense

Credit Cash

Credit Convertible bonds (liability)

• To recognise conversion of bonds into sharesDebit Convertible bonds (liability)

Debit Convertible bonds (equity)

Credit Share capital

15-44 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Disclosure requirements

• Large number of detailed disclosure requirements in AASB 7– a direct consequence of large losses incurred by many

organisations

• Purpose of AASB 7’s disclosure requirements– to enhance understanding of significance of financial

instruments; and

– to assist in assessing amounts, timing and certainty of cash flows

15-45 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Disclosure requirements (cont.)• Numerous disclosure requirements in AASB 7 – best

way to appreciate the extensive nature of the disclosures is to review the standard

• Interesting to see that there are various disclosures related the ‘risks’ associated with financial instruments (par. 32 – 42)

• Risk to be disclosed relate to:– credit risk (the risk that one party to a financial instrument will

cause a financial loss for the other party by failing to discharge an obligation)

– liquidity risk (the risk that an entity will encounter difficulty in meeting obligations associated with financial liabilities)

– market risk (the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices)

15-46 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Summary

• The chapter addresses issues associated with financial instruments

• ‘Financial instruments’ includes a wide range of items– can be classified as primary or derivative

• AASB 7 provides many disclosure requirements for financial instruments

• AASB 132 provides guidance for determining whether a financial instrument is a financial liability or an equity instrument

• AASB 139 provides requirements for recognition and measurement of financial instruments