140146 stratfor global vantage europe 6 05

TRANSCRIPT

GL

OB

AL

VA

NT

AG

EE u r o p e

S T R AT E G I C F O R E C A S T I N G , I N C .STRATFOR is the world’s leading private intelligence firm providing corporations, governments and individuals with intelligence and analysis to anticipate the political, economic, and security issues vital to their interests. Armed with powerful intelligence-gathering capabilities and working in close collaboration with STRATFOR’s experienced team of professionals, our clients are better able to protect their assets, diminish risk, and increase opportunities to compete in the global market.

J U N E 2 0 0 5

ii© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

A b o u t S t r at f o r . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i i i

E u r o p e . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

E x e c u t i v e S u m m a r y . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 M a y : T h e M o n t h i n R e v i e w . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 K e y I s s u e s . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 T h e M o n t h A h e a d : F o r e c a s t s f o r J u n e . . . . . . . . . . . . . . . . . . . . . 1 0 T r e n d s , S t a t s a n d I n d i c a t o r s . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 5 N o t e w o r t h y E v e n t s . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 9

S t r at f o r S e r v i c e s . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 0

C o n ta c t S t r at f o r . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 2

iii© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

STRATFOR is the world’s leading private intelligence firm providing corporations, governments and indi-viduals with geopolitical intelligence and analysis to manage risk and anticipate the political, economic and security issues vital to their interests. Armed with powerful intelligence-gathering capabilities and work-ing in close collaboration with STRATFOR’s expert team of analysts, clients are better able to protect their assets, diminish risk, compete in the global market and increase opportunities. STRATFOR has an unparal-leled record for accuracy and clarity in its forecasts and has been called “the Shadow CIA” by Barron’s.

Hundreds of Fortune 500 companies and government agencies rely on STRATFOR for unbiased, insightful, actionable analysis of global activities to keep ahead of local, national and international developments to plan strategy and be more confidently informed.

· Hedge Fund Managers use STRATFOR intelligence to identify future market opportunities. · Oil & Gas Executives rely on STRATFOR intelligence to look into the future to determine areas for exploration, investment and market volatility. · Government & Military Personnel utilize STRATFOR intelligence to gain insights on triggers affecting geopolitical events and potential movements around the world. · Manufacturers gain intelligence on emerging markets, resource fluctuations and potential regional threats in the coming years. · Logistics Company Executives use STRATFOR intelligence to be informed on what disruptions could impact their supply chains. · Global Finance, Insurance and Investment Executives use STRATFOR intelligence to be prepared for any market fluctuations that may impact their clients’ businesses.

Unlike news organizations and research firms that are set up to deliver information on what’s already happened — so all you can do is react — STRATFOR was founded in 1996 to deliver insights and fore-casts our clients can use to stay ahead of the curve.

Our services range from online Geopolitical Intelligence & Analysis subscriptions to confidential Custom Intelligence Services. We provide geopolitical and strategic intelligence services focused on international political, economic and security issues; business intelligence on issues ranging from technology to global alliances; and issues analysis and intelligence on public policy issues and the international legislative, legal and regulatory environments that shape those issues.

For more information on how STRATFOR’s services can impact your business, please contact us at:

Strategic Forecasting, Inc.1666 K Street, Suite 600Washington, D.C. 20006

(U.S.) 202.429.1800www.STRATFOR.com

1© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

rench voters gave the EU constitution a resounding “no” vote May 29. With the French government in knots, the German government of Chancellor Gerhard Schroeder hanging by a thread and the idea of unity unraveling, Europe is trying to figure out: “What now?” In June, they will not have an answer.

T h i s M o n t h ’ s H i g h l i g h t s : I n E v e r y I s s u e : • EU Constitutional Failure • Trends, Stats and Indicators • The Dollar and the Euro • Noteworthy Events • A New Cold War? • The Month Ahead: France, Germany and the Voters

F

2© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

urope is shaping up for its most dramatic political transformation since German reunification in 1993. The EU constitution, defeated in the May 29 French referendum, is on the rocks; the German government is in crisis and dissolving; and the United Kingdom — among the most euroskeptic of states — is about to take over the reins of EU leadership.

The result is a continent in transition as the dream of a fully united Europe finally gives way to the stark — and dramatically different — realities on the ground. The attitude throughout Europe has become a mix of confusion, resentment and apathy as few citizens understand where the European Union is going, what it means for them, or what the constitution is about in the first place. In the long run the constitution’s failure will not be mourned over too much, but for now its loss will create utter confusion throughout Europe as to both its significance and the path the European Union should take — if any — in the future. Such pensive wandering will persist throughout the rest of 2005.

Against this backdrop, many portions of Europe are independently churning, contributing to the sense of confusion and dawning change. In addition to the German government sliding into dissolution, the French government is losing its mandate to govern and the Basque rebellion in Spain is once again heating up.

Overarching it all, the United States is pushing deep in the Russian sphere of influence, complicating already strained relations between Moscow and a changing Europe.

EE x e c u t i v e S u m m a r y

3© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

M a y : T h e M o n t h I n R e v i e w

U n r a v e l i n g t h e T i e T h a t B i n d sA new Europe is in the making. Dawning political crises in France and Germany combined with a stark rejection of the EU constitution in two referendums will tear apart the foundations of the previous 57 years of European integration. June 2005 will be marked as the point at which Europe as we know it began to change.

On May 29 French voters rejected the EU constitution — an act repeated June 1 by their Dutch counterparts. In doing so the two countries have not only set back the process of inexorable — if exhausting — European integration that began in 1948, but they have set the stage for an unraveling of both common European institutions and the French government itself.

The German government also landed itself in trouble. Facing a party brimming with discontent, German Chancellor Gerhard Schroeder called on his Social Democratic Party (SPD) to bring down his government in a vote that is technically unconstitutional.

4© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

Only in Italy could stability be found. In late April the Italian coalition government descended into internal squabbling and teetered on the brink of collapse. Yet President Silvio Berlusconi managed to pull his disparate partners together and re-forge his government with minimal changes. Berlusconi already is the longest serving Italian prime minister in Italian post-World War II reconstruction history and now perhaps stands to be the only Italian leader of his era to serve out his entire term.

A N e w C o l d W a r ?Europe’s near abroad is undergoing massive changes as well. The United States in May intensified a standing policy that seeks to tease apart the Russian Federation’s final outposts as well as begin to break apart the Russian Federation itself. During U.S. President George W. Bush’s trip to Moscow for V-E Day commemorations, his jet landed long enough only for the president to take in a quick — and nearly hermetically sealed — parade between extended stops in Latvia and Georgia. U.S. policy already is deeply rooted, and Washington is sweeping Europe up in its plots, ready or not.

T h e B a s q u e R e s u r g e n c eOn the opposite end of the Continent the government of Spanish Prime Minister Jose Luis Rodriguez Zapatero attempted to capitalize on the weakening of nationalist Basque forces in regional elections in April by reaching out to the political moderates in the Basque Nationalist Party. That strategy is failing.

A last-minute decision by the outlawed Batasuna party, the political representative of the ETA separatist movement, to throw its support behind a dark horse party resulted in a shuffling of power away from moderate, nonviolent Basque separatists. The extreme nationalists feel completely ostracized by the system and are acting as if they have less to lose. Bombings are again becoming common in Spain’s Basque regions; a May 25 daytime car bomb injured 52 people.

K e y I s s u e s

E u r o p e a n U n i t y a n d t h e F r a n c o - G e r m a n C o r eEuropean unity has always found itself threatened by the Continent’s history of nationalistic clashes and wars, and now is no exception. But the failure to approve the EU constitution not only confirms Stratfor’s 2004 annual forecast

5© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

that the year was actually the high-water mark for European political integration, but also that the underlying idea driving European unity — the goal of a federated super state — is fundamentally unworkable. A “united” Europe has now been rejected by none other than France, the architect of the original concept of a superpower Europe, and there is nowhere to go but down.

Until now the chief driver toward the ideal of a united Europe has been the Franco-German core. Europe pulls together almost by default as the two European heavyweights push ahead with major joint initiatives. That core is breaking up.

On May 22, Schroeder stunned his own party’s Bundestag representatives by announcing his intention to dissolve the Bundestag and call fresh elections. Technically, such an action is illegal under the German Constitution, but the SPD leadership already has backed the chancellor. Barring a mass effort by the socialist rank-and-file to restructure the party leadership, therefore, the standing government is about to pass on. Initial polls indicate that elections will decimate the Socialists and perhaps even grant the Christian Democratic Union (CDU) a majority for the first time in decades.

Schroeder is shaking up politics for two simple reasons. First, the German economy is in the doldrums, and Schroeder — rightly — believes the only way to salvage it is to engage in broad, deep reforms. However, his own party is ideologically hostile to the chancellor’s free-ish market efforts, forcing Schroeder to rely on opposition support in the Bundestag for economic policy. Schroeder wants his party to either issue him a blank check or step out of the way.

Second, Schroeder’s half-hearted attempts to implement reforms over his party’s opposition have landed him in the voters’ dog house. The German populace might realize the country needs reforms, but no one wants to pay for them. In trying to walk such a political tightrope, Schroeder has found himself with the worst of both worlds: enacting sufficient reforms to anger the populace, but not enough to restart growth. With growth perennially sluggish and unemploy-ment at 80-year highs, facing the electorate now would de facto mean a new government. The SPD plans to hold a vote of no confidence — in which

“United” Europe has nowhere to go but down.

Walking a political tightrope, Schroeder finds himself in the worst of both worlds.

6© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

it is recommending its own members vote against the SPD-led government — by July 1.That would have massive implications for the European Union since the Schroeder government has been France’s most reliable and loyal partner in the entire post-World War II era. A German government under the CDU would hardly treat Paris coldly, but its views on everything from the United States to Russia to Turkey are worlds apart from the current broad alignment of interests.

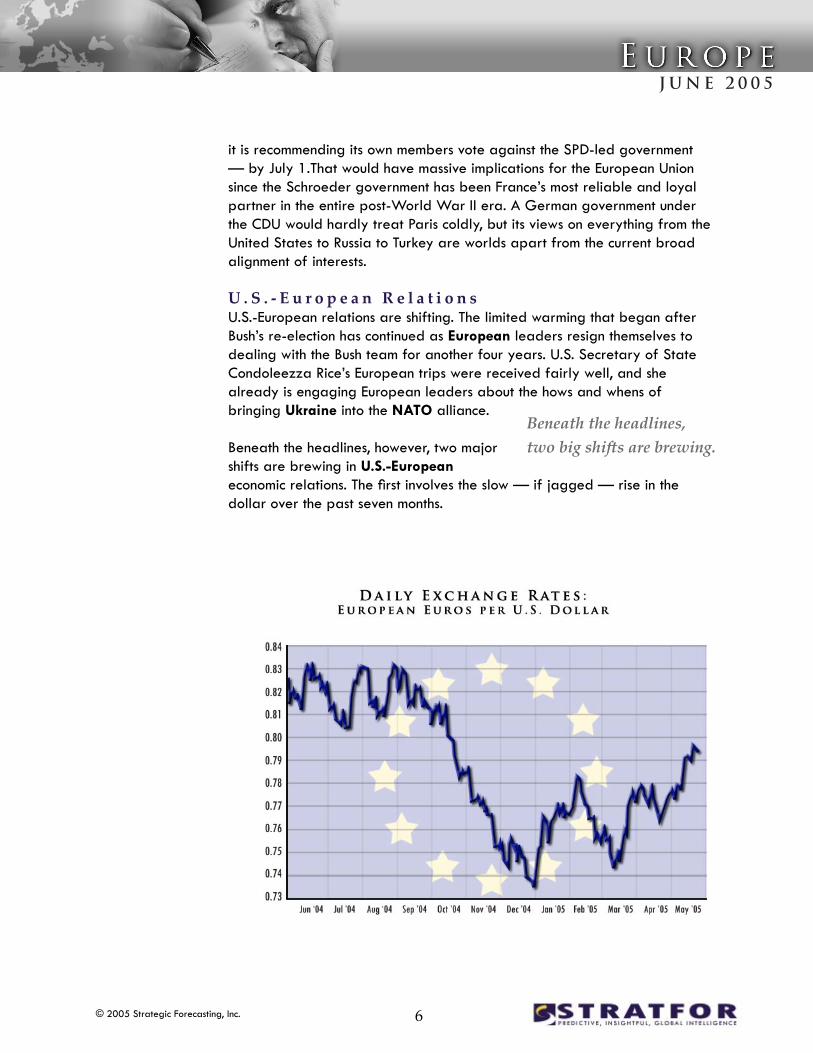

U . S . - E u r o p e a n R e l a t i o n sU.S.-European relations are shifting. The limited warming that began after Bush’s re-election has continued as European leaders resign themselves to dealing with the Bush team for another four years. U.S. Secretary of State Condoleezza Rice’s European trips were received fairly well, and she already is engaging European leaders about the hows and whens of bringing Ukraine into the NATO alliance.

Beneath the headlines, however, two major shifts are brewing in U.S.-European economic relations. The first involves the slow — if jagged — rise in the dollar over the past seven months.

Beneath the headlines, two big shi�s are brewing.

7© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

Europe’s core economic problem is that it does not react well to change — whether in the form of looser labor laws or more shareholder oversight. So the ideal situation for Europe would be a near-fixed exchange rate to eliminate meaningful currency risk. That, however, is not a world in which Europe lives. As a result, the European economy suffers whenever change is in the air and growth slows to a crawl as it has in the post-Sept. 11 period. In that period the falling U.S. dollar has made it difficult to increase exports to the United States, even as the Chinese currency peg (to the U.S. dollar) allows Chinese products to undermine European goods in their home market.

With the tide turning in the currency markets, Europe has a new problem to wrestle with. The one saving grace of the past three years for Europe has been that all crude oil and natural gas contracts are carried out in U.S. dollars, meaning that as the dollar has fallen the relative price of crude oil has not risen overmuch. With the dollar rising, however, the impact of crude oil prices will hit both Europe’s bottom line and its headline inflation — both of which will mitigate the export boom that Europe would otherwise have enjoyed.

The second economic shift affects both U.S. and European trade relations with China. As expected, Chinese textile exports surged in January 2005 as decades-old quota systems were abandoned as part of World Trade Organization (WTO)-mandated policy changes. Also as expected, politicians in both Europe and the United States were caught by surprise and acted with stunned disbelief when Chinese imports, which they had been warned about five years previously, began washing away domes-tic producers.

The question on both sides of the Atlantic is how to deal with the rising deluge of Chinese textiles — a question that dovetails nicely with mounting concern over the flood of Chinese goods in general. EU Trade Commissioner Peter Mandelson, under heavy pressure from the member states, has announced some limited sanctions of Chinese goods while, as of May 23, giving the Chinese only until May 31 to “rectify” the situation. As of June 1, the Chinese have chosen to pursue the nationalist route and instead surge exports — a move that will not impress the Europeans, whose desire for stability has made them long accustomed to robust trade barriers.

Both the United States and European Union are major importers of Chinese goods, but exports to China are but a minor portion of the Western total. In

China’s action is a no-surprise surprise.

8© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

the case of the Europe, the EU-25 import more than 2.5 times as much in Chinese goods by value as they export to China. In short, if China does not play ball by American and European rules, Washington and Brussels would have little trouble launching — and winning — a trade war.

The question, therefore, is how much will the Europeans move? On that issue, they are likely to take their cue from the Bush administration. Europe knows full well it is in a position of strength. It also knows the White House is facing similar pressure from Congress, which is pushing for the executive branch to levy a 27.5 percent tariff on all Chinese imports. The Bush administration is trying to get the Chinese to fix the trade imbalance without trade sanctions by leaking that it wants to see Beijing unilaterally revalue the yuan upward from its current peg by at least 10 percent.

Such an amount would not satisfy Congress, or Europe, but would be a step in the right direction that would buy all parties a bit more time. For now, the issue is in Beijing’s hands and Brussels is content to take a backseat, playing less-bad cop to Washington’s bad cop, and U.S. Congress’ extremely bad cop. Ideally, Brussels would like to see the Chinese unilaterally alter their policies, but it will not shy away from strong action once the United States is on board as well.

R u s s i a n - W e s t e r n R e l a t i o n sRelations between the West and Russia are staggering under a broad Western geopolitical offensive into the former Soviet Union (FSU). The United States, with enthusiastic support from Central European EU members, is pushing deep into the former Soviet Union. Some, such as Poland, have helped draw countries such as Ukraine and Georgia away from the Russian orbit. Others, such as Latvia, are taking a more direct bead and are pursuing territorial claims against Russia itself.

As such the FSU-European border regions are turning into geopolitical pressure cookers. • Neither the Estonian nor Lithuanian leadership deigned to attend V-E Day celebrations in Moscow, and the Latvian president only attended to raise a fuss about how V-E Day for the Baltics marked the beginning — not the end — of a life under tyranny.

Europe is in a position of strength vis-à-vis China.

Central European EU members back the U.S. push.

9© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

• The Baku-Tbilisi-Ceyhan pipeline, which will transport Caspian crude directly to the Eastern Mediterranean where it will be loaded onto tankers bound for the Eastern United States and Southern Europe, was inaugurated May 25. It was designed explicitly to avoid Russian territory. • The Bush administration and several European allies have formally put the government of Belarus in their sights and actively are calling for a Ukrainian-style revolution. • Bulgaria and Romania were both officially invited to join the European Union in late April. Their admission — in 2007 or 2008 — will geographically block all Russian influence into the Balkans. Both states are already NATO members. Bulgaria confirmed May 14 that it would be offering the United States the use of three of its military bases as part of Washington’s new “lily pad” strategy.

In general, the European states are broadly on board with the U.S. effort, mostly because they have no desire to live under threat of a nuclear war again; Central European states, having lived directly under Moscow’s yoke, are among the most supportive.

That has not gone unnoticed in Moscow, particularly among those in the security services, who (correctly) view the effort as nothing less than an attempt to destroy Russia as a geopolitical power. So far the Kremlin has withheld all but purely rhetorical responses, but barring a decision in Moscow to simply lie down and die this cannot last forever. If Russia is going to attempt to survive — much less restore its power — sooner or later it must act, and that will affect Europe’s entire eastern edge. The first meaningful action probably will involve Russia changing the amount it charges for its natural gas exports, for which most European states have no sufficient alternative suppliers.

For Russia to survive it must act – sooner or later.

10© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

The euro is at a seven-month low.

T h e M o n t h A h e a d : F o r e c a s t s f o r J u n e

H i g h l i g h t s : • Dealing With Constitutional Failure • French Presidential Campaign Begins • Auf Wiedersehen to Schroeder

June is going to be an extremely awkward month in Europe. With the failed EU referendums hanging like a pall over the Continent, the obvious question is: “What now?” Ever since French opinion polls began to report a less than enthusiastic mood, sources throughout the Continent have reported intense discussions at multiple levels as to how to answer that question. Though the sources made it all sound sophisticated, measured and cultured, the core response can most aptly be distilled down to an embarrassed, “We have no [expletive deleted] idea.”

L i f e B e y o n d t h e C o n s t i t u t i o nThe lack of an “idea” will dominate European news for the next month as politicians, citizens and market players all slowly digest precisely what it means when France rejects Europe. Those on both sides of every ideological divide will carry on endlessly about how their causes have been irrevocably supported or damaged by the lack of a constitution.

The markets and the euro will suffer — in no small part from European leaders saying that they would like to convince the French to vote “yes” — from the perceived lack of a European future, particularly when pundits begin to hypothesize about whether this is the beginning of the end of the Union. Already the euro is at a seven-month low. Stratfor fully expects the markets to finally take all of the atrocious data — from lackluster gross domestic product growth to sobering unemployment statistics — that Europe has produced over the past six months more seriously.

Beyond Europe the reaction to the constitution’s failure will be weak and extremely disjointed. The world has had more than a half century to get used to the idea of a slowly uniting Europe, and more than a decade to

11© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

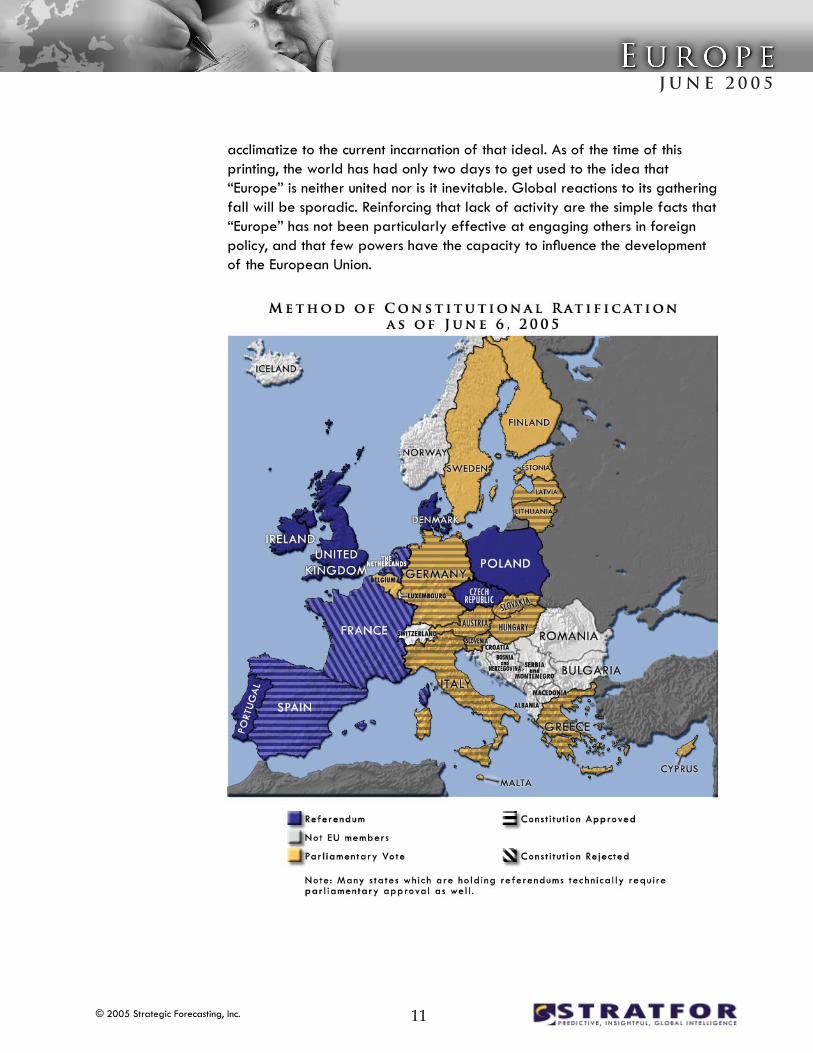

acclimatize to the current incarnation of that ideal. As of the time of this printing, the world has had only two days to get used to the idea that “Europe” is neither united nor is it inevitable. Global reactions to its gathering fall will be sporadic. Reinforcing that lack of activity are the simple facts that “Europe” has not been particularly effective at engaging others in foreign policy, and that few powers have the capacity to influence the development of the European Union.

12© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

The holder of the EU presidency, Luxembourg will bring no clarity to this agony as Prime Minister Jean-Claude Juncker inadvertently has been a force for exposing and widening splits within the EU during the first five months of his six-month term. After rubbing most European leaders the wrong way on issues such as Croatia’s potential accession, reforming the Stability and Growth Pact and relations with the United States and Russia, Juncker is perhaps the worst EU head of government to be responsible for picking up the pieces after the French and Dutch rejections.

Perhaps the second worst is British Prime Minister Tony Blair — who takes over Juncker’s position July 1. Blair will be the first British leader since Winston Churchill to have a realistic chance of changing Europe’s direction, and the United States will seize on its partner’s coming term to make its own impact felt. But that is a forecast for another month.

This month will see quite a load of fallout from the vote. The United Kingdom already has made it (unofficially) clear that its own referendum will be delayed indefinitely, and the Poles are musing about whether to follow suit. But what is most notable is not what will happen in the as-yet misty months of 2006 when the constitution was supposed to be fully ratified, but what the Europeans will do about the constitutional crisis in June.

We expect nothing. Absolutely nothing.

There is little reason to feel so optimistic to think that damage will be limited to the constitution. A fate of the entire raft of other potential EU policies must be viewed in the context of the constitutional debate. Everything from the services directive (which would allow services firms the ability to freely compete across borders within the European Union) to the Lisbon Agenda (which aimed to im-prove European competitiveness) to pres-suring Croatia on participating with the International Criminal Tribunal for the former Yugoslavia (a precondition to membership talks) is shriveling on the vine due to a lack of attention. Now that the EU constitution has flopped, there will be even less attention to go around. Those who were hoping for something other than a bureaucracy stuck on autopilot will be grossly disappointed.

Tony Blair will take over the EU presidency.

The damage will not be limited to the EU constitution

13© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

The constitution, despite all its flaws, might have made the Union more transparent, more functional and more accountable. No such luck. Instead, Stratfor fully expects June of 2005 to be the month that history ultimately pegs as the beginning of the end of Europe’s political union.

F r a n c e S t a l l sIn the meantime, the political chaos will be most acute in France, the country largely responsible for “Europe” in the first place as well as the vote that killed its constitution. Already the defeat has claimed the head of Prime Minister Jean-Pierre Raffarin. His replacement, Dominique de Villepin, is an ally of French President Jacques Chirac ideologically and personally and will implement nothing that varies from his predecessor.

After a few days of hand wringing the focus will shift from Europe and back to things closer to home such as the upcoming 2007 presidential elections. After the splitting of both the left and the right over the failed constitution, Chirac is a lame duck. In June, the French presidential campaign will unofficially kick into high gear.

The result is that Europe — at the EU level at least — is stalled. The European Commission is not at this point even trying to get back to business as usual, since doing so would require some of Europe’s major powers to at least pay attention. Instead, they all are occupied with their own concerns.

The best bet the Europeans have of resurrecting the constitution process involves letting political events in France run their course. The EU already has trotted out all of its top representatives — many of them French — in an ultimately failed effort to tease a “oui” out of the country that was until recently Europe’s greatest champion. What failed was not the EU as an institution or even the constitution as a document, but the French belief that the European Union is actually in its best interests.

France long championed the idea of a united Europe because Paris always assumed it would be able to lash the rest of the European states together into a platform from which it could punch above its weight in the international arena. But between the mass desertion from the common European (read:

European powers are occupied with their own concerns.

14© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

Franco-German) position during the Iraq war and then the admittance of a gaggle of former Soviet states and satellites — that are both anti-Russian and pro-American — into the European Union in 2004, France found it driven home that the EU may be a supranational entity, but it is not one in which it can dictate its desires. In fact, under the constitution, a large enough majority of EU states could have forced policies on the Franco-German bloc.

That is the realization the French had to deal with May 29. If the EU constitution is going to have a future, one of two things must happen: either France must abandon all pretensions of international influence, or it must come to believe that at some point in the future it will be able to steer a Europe of 27 members as easily as it once steered a Europe of six. Either way, the decision must be made by the French in France, and either conclu-sion involves such heavy cultural implications that it could not possibly be resolved in 30 days.

In fact, the situation is even worse (for the constitution) than it appears. Much of the European populace — and governments — take extended vacations in July and August, making arranging a meeting, much less brokering agreement on any plan of action, extremely difficult. Also consider that on July 1 the United Kingdom, perhaps the country least inclined to ratify the constitution, takes on the EU presidency and chances are the entire constitutional issue is about to be put on ice.

S u n s e t a n d D a w n i n G e r m a n yBeyond the fallout from the constitutional debate, Germany will be the place to watch. Constitutional or not, the German government will vote itself out of power in a no confidence motion in June, paving the way for the Bundestag to be formally dissolved.

The one development that might forestall such German instability would be a capitulation in favor of economic reforms by the SPD’s left wing. If Schroeder succeeds in getting a blank check of support from his wayward party members, he will be able to suffer through the rest of his term. If not, the only questions left will be how deep will the German left split? And for how long? We will know the answer to the first question by the end of July. The second could well remain unanswered for years.

Now a decision with cultural implications must be made in France.

15© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

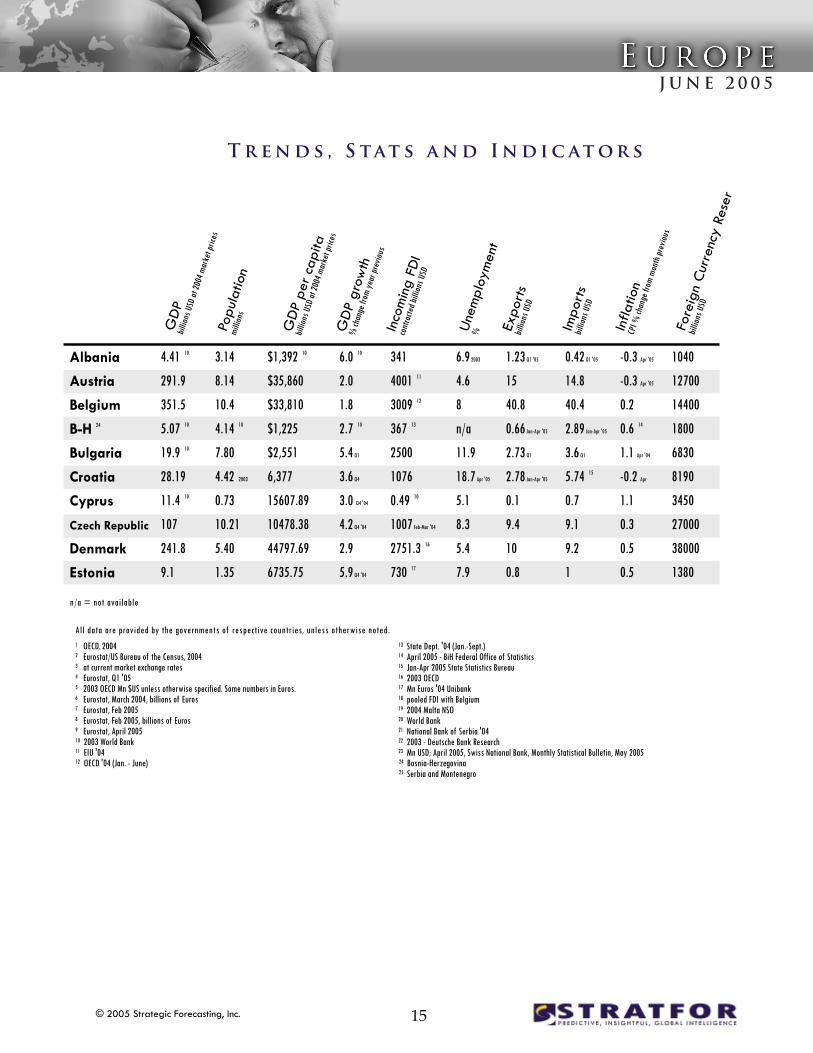

T r e n d s , S tat s a n d I n d i c at o r s

Albania

Austria

Belgium

B-H 24

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Macedonia

Malta

Netherlands

Norway

Poland

Portugal

Romania

S & M 25

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom

n/a = not available

4.41 10

291.9

351.5

5.07 10

19.9 10

28.19

11.4 10

107

241.8

9.1

185.9

2010.4

2703.1

205.2

99.7

12.16

181.7

1677.9

3.93 Q4 ‘04

6.32 Q1 ’05

31.7

4.7

5.37

579.0

250.1

241.6

167.7

36.0

14.9

41.2

25.4

991.7

346.0

358.8

2124.5

3.14

8.14

10.4

4.14 10

7.80

4.42 2003

0.73

10.21

5.40

1.35

5.22

59.90

82.53

11.04

10.12

0.29

4.03

57.89

2.32

3.44

0.45

2 10

0.4

16.26

4.55

38.19

10.41

21.71

8.16

5.4 10

2 10

42.34

8.97

7.36

59.67

$1,392 10

$35,860

$33,810

$1,225

$2,551

6,377

15607.89

10478.38

44797.69

6735.75

35615.07

33562.21

32752.26

18585.27

9854.99

41,865

45112.59

28985.18

1695.41

1833.48

70194.86

2350

13431.99 19

35613.24

54939.26

6326.16 20

16113.38

1658.12

1826.43

7629.63

12700

23419.36

38548.52

48722.86

35602.31

6.0 10

2.0

1.8

2.7 10

5.4 Q1

3.6 Q4

3.0 Q4 '04

4.2 Q4 '04

2.9

5.9 Q4 '04

2.0

2.3 Q4 '04

1.1

4.2 Q4 '04

3.9 Q4 '04

5.2

2.7 Q4 '04

-0.2

8.6 Q4 '04

5.6

3.8 Q4 '04

3.4 2003

2.3 Q4 '04

-0.3

2.9 Q4 '04

3.9 Q4 '04

0.6

4.3

8.0

5.8 Q4 '04

3.4 Q4 '04

2.7 Q4 '04

2.6 Q4 '04

1.2 Q4 '04

2.8

341

4001 11

3009 12

367 13

2500

1076

0.49 10

1007 Feb-Mar '04

2751.3 16

730 17

3299.3

47025.5

12878.4

661.6

2287

379.4

26912.6

16435.8

540 17

481.9

3009 18

150.1

0.29 10

19349.3

2632.4

7860

962.7

4100

996 21

678

-0.13 10

7187

2528.8

16565.7

14573.8

6.9 2003

4.6

8

n/a

11.9

18.7 Apr '05

5.1

8.3

5.4

7.9

8.3

9.8

9.8

10.5

6.3

3 Q1

4.3

8

9.4

8.6

4.5

n/a

6.8 7

4.6

4.4

18.1

6.9

7.1

n/a

15.9

5.8

10.2

6.3

4.3

4.7 Jan '05

1.23 Q1 '05

15

40.8

0.66 Jan-Apr '05

2.73 Q1

2.78 Jan-Apr '05

0.1

9.4

10

0.8

8

55.3

119.1

1.9

7.1

0.67

13

40.7

0.6

1.2

2.1

1.67

0.3

48

30.7 Q4

10.6

4.4

18.8

3.8

3.6

2.1

22.9

15.7

150 10

41.8

0.42 Q1 '05

14.8

40.4

2.89 Jan-Apr '05

3.6 Q1

5.74 15

0.7

9.1

9.2

1

6.5

59.5

92.7

6.4

7.6

0.83

8.3

44.3

0.9

1.5

2.6

2.9

0.4

42.8

20.7 Q4

11.3

6.5

24.7

11.75

3.8

2.2

33

12.9

n/a

57.4

-0.3 Apr '05

-0.3 Apr '05

0.2

0.6 14

1.1 Apr '04

-0.2 Apr

1.1

0.3

0.5

0.5

0.3

0.2

0

0.8

0.7

-0.5 May '05

0.6

0.8

1.1

0.3

0.7

1.2 2003

3.6 9

0.2

0.5

0.4

0.7

n/a

10.8

12.5

-0.1 22

1.4

0.2

0

1.9 Apr '05

1040

12700

14400

1800

6830

8190

3450

27000

38000

1380

11200

70800

96800

5800

12800

819

4150

63300

1540

3450

311

935

n/a

21400

37700

34000

12800

9450

4468.5 Apr '05

12100

8600

26800

22200

72.18 23

46100

All data are provided by the governments of respective countries, unless otherwise noted.1 OECD, 20042 Eurostat/US Bureau of the Census, 20043 at current market exchange rates4 Eurostat, Q1 '055 2003 OECD Mn $US unless otherwise specified. Some numbers in Euros.6 Eurostat, March 2004, billions of Euros7 Eurostat, Feb 20058 Eurostat, Feb 2005, billions of Euros9 Eurostat, April 200510 2003 World Bank11 EIU '0412 OECD '04 (Jan. - June) 24 Bosnia-Herzegovina 25 Serbia and Montenegro

13 State Dept. '04 (Jan.-Sept.)14 April 2005 - BiH Federal Office of Statistics15 Jan-Apr 2005 State Statistics Bureau16 2003 OECD17 Mn Euros '04 Unibank18 pooled FDI with Belgium19 2004 Malta NSO20 World Bank21 National Bank of Serbia '0422 2003 - Deutsche Bank Research23 Mn USD; April 2005, Swiss National Bank, Monthly Statistical Bulletin, May 2005

GDP

bil

lions

USD

at 20

04 m

arke

t pric

esPo

pula

tion

millio

ns

GDP

per

cap

ita

billio

ns U

SD at

2004

mar

ket p

rices

G

DP g

row

th

% ch

ange

from

year

prev

ious

Inco

min

g FD

I co

ntra

cted b

illion

s USD

Unem

ploy

men

t % Ex

port

sbil

lions

USD

Fore

ign

Curr

ency

Res

erve

s

billio

ns U

SD

Impo

rts

billio

ns U

SD

Infla

tion

CPI %

chan

ge fr

om m

onth

prev

ious

Albania

Austria

Belgium

B-H 24

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Macedonia

Malta

Netherlands

Norway

Poland

Portugal

Romania

S & M 25

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom

n/a = not available

4.41 10

291.9

351.5

5.07 10

19.9 10

28.19

11.4 10

107

241.8

9.1

185.9

2010.4

2703.1

205.2

99.7

12.16

181.7

1677.9

3.93 Q4 ‘04

6.32 Q1 ’05

31.7

4.7

5.37

579.0

250.1

241.6

167.7

36.0

14.9

41.2

25.4

991.7

346.0

358.8

2124.5

3.14

8.14

10.4

4.14 10

7.80

4.42 2003

0.73

10.21

5.40

1.35

5.22

59.90

82.53

11.04

10.12

0.29

4.03

57.89

2.32

3.44

0.45

2 10

0.4

16.26

4.55

38.19

10.41

21.71

8.16

5.4 10

2 10

42.34

8.97

7.36

59.67

$1,392 10

$35,860

$33,810

$1,225

$2,551

6,377

15607.89

10478.38

44797.69

6735.75

35615.07

33562.21

32752.26

18585.27

9854.99

41,865

45112.59

28985.18

1695.41

1833.48

70194.86

2350

13431.99 19

35613.24

54939.26

6326.16 20

16113.38

1658.12

1826.43

7629.63

12700

23419.36

38548.52

48722.86

35602.31

6.0 10

2.0

1.8

2.7 10

5.4 Q1

3.6 Q4

3.0 Q4 '04

4.2 Q4 '04

2.9

5.9 Q4 '04

2.0

2.3 Q4 '04

1.1

4.2 Q4 '04

3.9 Q4 '04

5.2

2.7 Q4 '04

-0.2

8.6 Q4 '04

5.6

3.8 Q4 '04

3.4 2003

2.3 Q4 '04

-0.3

2.9 Q4 '04

3.9 Q4 '04

0.6

4.3

8.0

5.8 Q4 '04

3.4 Q4 '04

2.7 Q4 '04

2.6 Q4 '04

1.2 Q4 '04

2.8

341

4001 11

3009 12

367 13

2500

1076

0.49 10

1007 Feb-Mar '04

2751.3 16

730 17

3299.3

47025.5

12878.4

661.6

2287

379.4

26912.6

16435.8

540 17

481.9

3009 18

150.1

0.29 10

19349.3

2632.4

7860

962.7

4100

996 21

678

-0.13 10

7187

2528.8

16565.7

14573.8

6.9 2003

4.6

8

n/a

11.9

18.7 Apr '05

5.1

8.3

5.4

7.9

8.3

9.8

9.8

10.5

6.3

3 Q1

4.3

8

9.4

8.6

4.5

n/a

6.8 7

4.6

4.4

18.1

6.9

7.1

n/a

15.9

5.8

10.2

6.3

4.3

4.7 Jan '05

1.23 Q1 '05

15

40.8

0.66 Jan-Apr '05

2.73 Q1

2.78 Jan-Apr '05

0.1

9.4

10

0.8

8

55.3

119.1

1.9

7.1

0.67

13

40.7

0.6

1.2

2.1

1.67

0.3

48

30.7 Q4

10.6

4.4

18.8

3.8

3.6

2.1

22.9

15.7

150 10

41.8

0.42 Q1 '05

14.8

40.4

2.89 Jan-Apr '05

3.6 Q1

5.74 15

0.7

9.1

9.2

1

6.5

59.5

92.7

6.4

7.6

0.83

8.3

44.3

0.9

1.5

2.6

2.9

0.4

42.8

20.7 Q4

11.3

6.5

24.7

11.75

3.8

2.2

33

12.9

n/a

57.4

-0.3 Apr '05

-0.3 Apr '05

0.2

0.6 14

1.1 Apr '04

-0.2 Apr

1.1

0.3

0.5

0.5

0.3

0.2

0

0.8

0.7

-0.5 May '05

0.6

0.8

1.1

0.3

0.7

1.2 2003

3.6 9

0.2

0.5

0.4

0.7

n/a

10.8

12.5

-0.1 22

1.4

0.2

0

1.9 Apr '05

1040

12700

14400

1800

6830

8190

3450

27000

38000

1380

11200

70800

96800

5800

12800

819

4150

63300

1540

3450

311

935

n/a

21400

37700

34000

12800

9450

4468.5 Apr '05

12100

8600

26800

22200

72.18 23

46100

All data are provided by the governments of respective countries, unless otherwise noted.1 OECD, 20042 Eurostat/US Bureau of the Census, 20043 at current market exchange rates4 Eurostat, Q1 '055 2003 OECD Mn $US unless otherwise specified. Some numbers in Euros.6 Eurostat, March 2004, billions of Euros7 Eurostat, Feb 20058 Eurostat, Feb 2005, billions of Euros9 Eurostat, April 200510 2003 World Bank11 EIU '0412 OECD '04 (Jan. - June) 24 Bosnia-Herzegovina 25 Serbia and Montenegro

13 State Dept. '04 (Jan.-Sept.)14 April 2005 - BiH Federal Office of Statistics15 Jan-Apr 2005 State Statistics Bureau16 2003 OECD17 Mn Euros '04 Unibank18 pooled FDI with Belgium19 2004 Malta NSO20 World Bank21 National Bank of Serbia '0422 2003 - Deutsche Bank Research23 Mn USD; April 2005, Swiss National Bank, Monthly Statistical Bulletin, May 2005

GDP

bil

lions

USD

at 20

04 m

arke

t pric

esPo

pula

tion

millio

ns

GDP

per

cap

ita

billio

ns U

SD at

2004

mar

ket p

rices

G

DP g

row

th

% ch

ange

from

year

prev

ious

Inco

min

g FD

I co

ntra

cted b

illion

s USD

Unem

ploy

men

t % Ex

port

sbil

lions

USD

Fore

ign

Curr

ency

Res

erve

s

billio

ns U

SD

Impo

rts

billio

ns U

SD

Infla

tion

CPI %

chan

ge fr

om m

onth

prev

ious

16© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

Albania

Austria

Belgium

B-H 24

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Macedonia

Malta

Netherlands

Norway

Poland

Portugal

Romania

S & M 25

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom

n/a = not available

4.41 10

291.9

351.5

5.07 10

19.9 10

28.19

11.4 10

107

241.8

9.1

185.9

2010.4

2703.1

205.2

99.7

12.16

181.7

1677.9

3.93 Q4 ‘04

6.32 Q1 ’05

31.7

4.7

5.37

579.0

250.1

241.6

167.7

36.0

14.9

41.2

25.4

991.7

346.0

358.8

2124.5

3.14

8.14

10.4

4.14 10

7.80

4.42 2003

0.73

10.21

5.40

1.35

5.22

59.90

82.53

11.04

10.12

0.29

4.03

57.89

2.32

3.44

0.45

2 10

0.4

16.26

4.55

38.19

10.41

21.71

8.16

5.4 10

2 10

42.34

8.97

7.36

59.67

$1,392 10

$35,860

$33,810

$1,225

$2,551

6,377

15607.89

10478.38

44797.69

6735.75

35615.07

33562.21

32752.26

18585.27

9854.99

41,865

45112.59

28985.18

1695.41

1833.48

70194.86

2350

13431.99 19

35613.24

54939.26

6326.16 20

16113.38

1658.12

1826.43

7629.63

12700

23419.36

38548.52

48722.86

35602.31

6.0 10

2.0

1.8

2.7 10

5.4 Q1

3.6 Q4

3.0 Q4 '04

4.2 Q4 '04

2.9

5.9 Q4 '04

2.0

2.3 Q4 '04

1.1

4.2 Q4 '04

3.9 Q4 '04

5.2

2.7 Q4 '04

-0.2

8.6 Q4 '04

5.6

3.8 Q4 '04

3.4 2003

2.3 Q4 '04

-0.3

2.9 Q4 '04

3.9 Q4 '04

0.6

4.3

8.0

5.8 Q4 '04

3.4 Q4 '04

2.7 Q4 '04

2.6 Q4 '04

1.2 Q4 '04

2.8

341

4001 11

3009 12

367 13

2500

1076

0.49 10

1007 Feb-Mar '04

2751.3 16

730 17

3299.3

47025.5

12878.4

661.6

2287

379.4

26912.6

16435.8

540 17

481.9

3009 18

150.1

0.29 10

19349.3

2632.4

7860

962.7

4100

996 21

678

-0.13 10

7187

2528.8

16565.7

14573.8

6.9 2003

4.6

8

n/a

11.9

18.7 Apr '05

5.1

8.3

5.4

7.9

8.3

9.8

9.8

10.5

6.3

3 Q1

4.3

8

9.4

8.6

4.5

n/a

6.8 7

4.6

4.4

18.1

6.9

7.1

n/a

15.9

5.8

10.2

6.3

4.3

4.7 Jan '05

1.23 Q1 '05

15

40.8

0.66 Jan-Apr '05

2.73 Q1

2.78 Jan-Apr '05

0.1

9.4

10

0.8

8

55.3

119.1

1.9

7.1

0.67

13

40.7

0.6

1.2

2.1

1.67

0.3

48

30.7 Q4

10.6

4.4

18.8

3.8

3.6

2.1

22.9

15.7

150 10

41.8

0.42 Q1 '05

14.8

40.4

2.89 Jan-Apr '05

3.6 Q1

5.74 15

0.7

9.1

9.2

1

6.5

59.5

92.7

6.4

7.6

0.83

8.3

44.3

0.9

1.5

2.6

2.9

0.4

42.8

20.7 Q4

11.3

6.5

24.7

11.75

3.8

2.2

33

12.9

n/a

57.4

-0.3 Apr '05

-0.3 Apr '05

0.2

0.6 14

1.1 Apr '04

-0.2 Apr

1.1

0.3

0.5

0.5

0.3

0.2

0

0.8

0.7

-0.5 May '05

0.6

0.8

1.1

0.3

0.7

1.2 2003

3.6 9

0.2

0.5

0.4

0.7

n/a

10.8

12.5

-0.1 22

1.4

0.2

0

1.9 Apr '05

1040

12700

14400

1800

6830

8190

3450

27000

38000

1380

11200

70800

96800

5800

12800

819

4150

63300

1540

3450

311

935

n/a

21400

37700

34000

12800

9450

4468.5 Apr '05

12100

8600

26800

22200

72.18 23

46100

All data are provided by the governments of respective countries, unless otherwise noted.1 OECD, 20042 Eurostat/US Bureau of the Census, 20043 at current market exchange rates4 Eurostat, Q1 '055 2003 OECD Mn $US unless otherwise specified. Some numbers in Euros.6 Eurostat, March 2004, billions of Euros7 Eurostat, Feb 20058 Eurostat, Feb 2005, billions of Euros9 Eurostat, April 200510 2003 World Bank11 EIU '0412 OECD '04 (Jan. - June) 24 Bosnia-Herzegovina 25 Serbia and Montenegro

13 State Dept. '04 (Jan.-Sept.)14 April 2005 - BiH Federal Office of Statistics15 Jan-Apr 2005 State Statistics Bureau16 2003 OECD17 Mn Euros '04 Unibank18 pooled FDI with Belgium19 2004 Malta NSO20 World Bank21 National Bank of Serbia '0422 2003 - Deutsche Bank Research23 Mn USD; April 2005, Swiss National Bank, Monthly Statistical Bulletin, May 2005

GDP

bil

lions

USD

at 20

04 m

arke

t pric

esPo

pula

tion

millio

ns

GDP

per

cap

ita

billio

ns U

SD at

2004

mar

ket p

rices

G

DP g

row

th

% ch

ange

from

year

prev

ious

Inco

min

g FD

I co

ntra

cted b

illion

s USD

Unem

ploy

men

t % Ex

port

sbil

lions

USD

Fore

ign

Curr

ency

Res

erve

s

billio

ns U

SD

Impo

rts

billio

ns U

SD

Infla

tion

CPI %

chan

ge fr

om m

onth

prev

ious

Albania

Austria

Belgium

B-H 24

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Macedonia

Malta

Netherlands

Norway

Poland

Portugal

Romania

S & M 25

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom

n/a = not available

4.41 10

291.9

351.5

5.07 10

19.9 10

28.19

11.4 10

107

241.8

9.1

185.9

2010.4

2703.1

205.2

99.7

12.16

181.7

1677.9

3.93 Q4 ‘04

6.32 Q1 ’05

31.7

4.7

5.37

579.0

250.1

241.6

167.7

36.0

14.9

41.2

25.4

991.7

346.0

358.8

2124.5

3.14

8.14

10.4

4.14 10

7.80

4.42 2003

0.73

10.21

5.40

1.35

5.22

59.90

82.53

11.04

10.12

0.29

4.03

57.89

2.32

3.44

0.45

2 10

0.4

16.26

4.55

38.19

10.41

21.71

8.16

5.4 10

2 10

42.34

8.97

7.36

59.67

$1,392 10

$35,860

$33,810

$1,225

$2,551

6,377

15607.89

10478.38

44797.69

6735.75

35615.07

33562.21

32752.26

18585.27

9854.99

41,865

45112.59

28985.18

1695.41

1833.48

70194.86

2350

13431.99 19

35613.24

54939.26

6326.16 20

16113.38

1658.12

1826.43

7629.63

12700

23419.36

38548.52

48722.86

35602.31

6.0 10

2.0

1.8

2.7 10

5.4 Q1

3.6 Q4

3.0 Q4 '04

4.2 Q4 '04

2.9

5.9 Q4 '04

2.0

2.3 Q4 '04

1.1

4.2 Q4 '04

3.9 Q4 '04

5.2

2.7 Q4 '04

-0.2

8.6 Q4 '04

5.6

3.8 Q4 '04

3.4 2003

2.3 Q4 '04

-0.3

2.9 Q4 '04

3.9 Q4 '04

0.6

4.3

8.0

5.8 Q4 '04

3.4 Q4 '04

2.7 Q4 '04

2.6 Q4 '04

1.2 Q4 '04

2.8

341

4001 11

3009 12

367 13

2500

1076

0.49 10

1007 Feb-Mar '04

2751.3 16

730 17

3299.3

47025.5

12878.4

661.6

2287

379.4

26912.6

16435.8

540 17

481.9

3009 18

150.1

0.29 10

19349.3

2632.4

7860

962.7

4100

996 21

678

-0.13 10

7187

2528.8

16565.7

14573.8

6.9 2003

4.6

8

n/a

11.9

18.7 Apr '05

5.1

8.3

5.4

7.9

8.3

9.8

9.8

10.5

6.3

3 Q1

4.3

8

9.4

8.6

4.5

n/a

6.8 7

4.6

4.4

18.1

6.9

7.1

n/a

15.9

5.8

10.2

6.3

4.3

4.7 Jan '05

1.23 Q1 '05

15

40.8

0.66 Jan-Apr '05

2.73 Q1

2.78 Jan-Apr '05

0.1

9.4

10

0.8

8

55.3

119.1

1.9

7.1

0.67

13

40.7

0.6

1.2

2.1

1.67

0.3

48

30.7 Q4

10.6

4.4

18.8

3.8

3.6

2.1

22.9

15.7

150 10

41.8

0.42 Q1 '05

14.8

40.4

2.89 Jan-Apr '05

3.6 Q1

5.74 15

0.7

9.1

9.2

1

6.5

59.5

92.7

6.4

7.6

0.83

8.3

44.3

0.9

1.5

2.6

2.9

0.4

42.8

20.7 Q4

11.3

6.5

24.7

11.75

3.8

2.2

33

12.9

n/a

57.4

-0.3 Apr '05

-0.3 Apr '05

0.2

0.6 14

1.1 Apr '04

-0.2 Apr

1.1

0.3

0.5

0.5

0.3

0.2

0

0.8

0.7

-0.5 May '05

0.6

0.8

1.1

0.3

0.7

1.2 2003

3.6 9

0.2

0.5

0.4

0.7

n/a

10.8

12.5

-0.1 22

1.4

0.2

0

1.9 Apr '05

1040

12700

14400

1800

6830

8190

3450

27000

38000

1380

11200

70800

96800

5800

12800

819

4150

63300

1540

3450

311

935

n/a

21400

37700

34000

12800

9450

4468.5 Apr '05

12100

8600

26800

22200

72.18 23

46100

All data are provided by the governments of respective countries, unless otherwise noted.1 OECD, 20042 Eurostat/US Bureau of the Census, 20043 at current market exchange rates4 Eurostat, Q1 '055 2003 OECD Mn $US unless otherwise specified. Some numbers in Euros.6 Eurostat, March 2004, billions of Euros7 Eurostat, Feb 20058 Eurostat, Feb 2005, billions of Euros9 Eurostat, April 200510 2003 World Bank11 EIU '0412 OECD '04 (Jan. - June) 24 Bosnia-Herzegovina 25 Serbia and Montenegro

13 State Dept. '04 (Jan.-Sept.)14 April 2005 - BiH Federal Office of Statistics15 Jan-Apr 2005 State Statistics Bureau16 2003 OECD17 Mn Euros '04 Unibank18 pooled FDI with Belgium19 2004 Malta NSO20 World Bank21 National Bank of Serbia '0422 2003 - Deutsche Bank Research23 Mn USD; April 2005, Swiss National Bank, Monthly Statistical Bulletin, May 2005

GDP

bil

lions

USD

at 20

04 m

arke

t pric

esPo

pula

tion

millio

ns

GDP

per

cap

ita

billio

ns U

SD at

2004

mar

ket p

rices

G

DP g

row

th

% ch

ange

from

year

prev

ious

Inco

min

g FD

I co

ntra

cted b

illion

s USD

Unem

ploy

men

t % Ex

port

sbil

lions

USD

Fore

ign

Curr

ency

Res

erve

s

billio

ns U

SD

Impo

rts

billio

ns U

SD

Infla

tion

CPI %

chan

ge fr

om m

onth

prev

ious

Albania

Austria

Belgium

B-H 24

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Macedonia

Malta

Netherlands

Norway

Poland

Portugal

Romania

S & M 25

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom

n/a = not available

4.41 10

291.9

351.5

5.07 10

19.9 10

28.19

11.4 10

107

241.8

9.1

185.9

2010.4

2703.1

205.2

99.7

12.16

181.7

1677.9

3.93 Q4 ‘04

6.32 Q1 ’05

31.7

4.7

5.37

579.0

250.1

241.6

167.7

36.0

14.9

41.2

25.4

991.7

346.0

358.8

2124.5

3.14

8.14

10.4

4.14 10

7.80

4.42 2003

0.73

10.21

5.40

1.35

5.22

59.90

82.53

11.04

10.12

0.29

4.03

57.89

2.32

3.44

0.45

2 10

0.4

16.26

4.55

38.19

10.41

21.71

8.16

5.4 10

2 10

42.34

8.97

7.36

59.67

$1,392 10

$35,860

$33,810

$1,225

$2,551

6,377

15607.89

10478.38

44797.69

6735.75

35615.07

33562.21

32752.26

18585.27

9854.99

41,865

45112.59

28985.18

1695.41

1833.48

70194.86

2350

13431.99 19

35613.24

54939.26

6326.16 20

16113.38

1658.12

1826.43

7629.63

12700

23419.36

38548.52

48722.86

35602.31

6.0 10

2.0

1.8

2.7 10

5.4 Q1

3.6 Q4

3.0 Q4 '04

4.2 Q4 '04

2.9

5.9 Q4 '04

2.0

2.3 Q4 '04

1.1

4.2 Q4 '04

3.9 Q4 '04

5.2

2.7 Q4 '04

-0.2

8.6 Q4 '04

5.6

3.8 Q4 '04

3.4 2003

2.3 Q4 '04

-0.3

2.9 Q4 '04

3.9 Q4 '04

0.6

4.3

8.0

5.8 Q4 '04

3.4 Q4 '04

2.7 Q4 '04

2.6 Q4 '04

1.2 Q4 '04

2.8

341

4001 11

3009 12

367 13

2500

1076

0.49 10

1007 Feb-Mar '04

2751.3 16

730 17

3299.3

47025.5

12878.4

661.6

2287

379.4

26912.6

16435.8

540 17

481.9

3009 18

150.1

0.29 10

19349.3

2632.4

7860

962.7

4100

996 21

678

-0.13 10

7187

2528.8

16565.7

14573.8

6.9 2003

4.6

8

n/a

11.9

18.7 Apr '05

5.1

8.3

5.4

7.9

8.3

9.8

9.8

10.5

6.3

3 Q1

4.3

8

9.4

8.6

4.5

n/a

6.8 7

4.6

4.4

18.1

6.9

7.1

n/a

15.9

5.8

10.2

6.3

4.3

4.7 Jan '05

1.23 Q1 '05

15

40.8

0.66 Jan-Apr '05

2.73 Q1

2.78 Jan-Apr '05

0.1

9.4

10

0.8

8

55.3

119.1

1.9

7.1

0.67

13

40.7

0.6

1.2

2.1

1.67

0.3

48

30.7 Q4

10.6

4.4

18.8

3.8

3.6

2.1

22.9

15.7

150 10

41.8

0.42 Q1 '05

14.8

40.4

2.89 Jan-Apr '05

3.6 Q1

5.74 15

0.7

9.1

9.2

1

6.5

59.5

92.7

6.4

7.6

0.83

8.3

44.3

0.9

1.5

2.6

2.9

0.4

42.8

20.7 Q4

11.3

6.5

24.7

11.75

3.8

2.2

33

12.9

n/a

57.4

-0.3 Apr '05

-0.3 Apr '05

0.2

0.6 14

1.1 Apr '04

-0.2 Apr

1.1

0.3

0.5

0.5

0.3

0.2

0

0.8

0.7

-0.5 May '05

0.6

0.8

1.1

0.3

0.7

1.2 2003

3.6 9

0.2

0.5

0.4

0.7

n/a

10.8

12.5

-0.1 22

1.4

0.2

0

1.9 Apr '05

1040

12700

14400

1800

6830

8190

3450

27000

38000

1380

11200

70800

96800

5800

12800

819

4150

63300

1540

3450

311

935

n/a

21400

37700

34000

12800

9450

4468.5 Apr '05

12100

8600

26800

22200

72.18 23

46100

All data are provided by the governments of respective countries, unless otherwise noted.1 OECD, 20042 Eurostat/US Bureau of the Census, 20043 at current market exchange rates4 Eurostat, Q1 '055 2003 OECD Mn $US unless otherwise specified. Some numbers in Euros.6 Eurostat, March 2004, billions of Euros7 Eurostat, Feb 20058 Eurostat, Feb 2005, billions of Euros9 Eurostat, April 200510 2003 World Bank11 EIU '0412 OECD '04 (Jan. - June) 24 Bosnia-Herzegovina 25 Serbia and Montenegro

13 State Dept. '04 (Jan.-Sept.)14 April 2005 - BiH Federal Office of Statistics15 Jan-Apr 2005 State Statistics Bureau16 2003 OECD17 Mn Euros '04 Unibank18 pooled FDI with Belgium19 2004 Malta NSO20 World Bank21 National Bank of Serbia '0422 2003 - Deutsche Bank Research23 Mn USD; April 2005, Swiss National Bank, Monthly Statistical Bulletin, May 2005

GDP

bil

lions

USD

at 20

04 m

arke

t pric

esPo

pula

tion

millio

ns

GDP

per

cap

ita

billio

ns U

SD at

2004

mar

ket p

rices

G

DP g

row

th

% ch

ange

from

year

prev

ious

Inco

min

g FD

I co

ntra

cted b

illion

s USD

Unem

ploy

men

t % Ex

port

sbil

lions

USD

Fore

ign

Curr

ency

Res

erve

s

billio

ns U

SD

Impo

rts

billio

ns U

SD

Infla

tion

CPI %

chan

ge fr

om m

onth

prev

ious

T r e n d s , S tat s a n d I n d i c at o r s

17© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

Albania

Austria

Belgium

B-H 24

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Macedonia

Malta

Netherlands

Norway

Poland

Portugal

Romania

S & M 25

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom

n/a = not available

4.41 10

291.9

351.5

5.07 10

19.9 10

28.19

11.4 10

107

241.8

9.1

185.9

2010.4

2703.1

205.2

99.7

12.16

181.7

1677.9

3.93 Q4 ‘04

6.32 Q1 ’05

31.7

4.7

5.37

579.0

250.1

241.6

167.7

36.0

14.9

41.2

25.4

991.7

346.0

358.8

2124.5

3.14

8.14

10.4

4.14 10

7.80

4.42 2003

0.73

10.21

5.40

1.35

5.22

59.90

82.53

11.04

10.12

0.29

4.03

57.89

2.32

3.44

0.45

2 10

0.4

16.26

4.55

38.19

10.41

21.71

8.16

5.4 10

2 10

42.34

8.97

7.36

59.67

$1,392 10

$35,860

$33,810

$1,225

$2,551

6,377

15607.89

10478.38

44797.69

6735.75

35615.07

33562.21

32752.26

18585.27

9854.99

41,865

45112.59

28985.18

1695.41

1833.48

70194.86

2350

13431.99 19

35613.24

54939.26

6326.16 20

16113.38

1658.12

1826.43

7629.63

12700

23419.36

38548.52

48722.86

35602.31

6.0 10

2.0

1.8

2.7 10

5.4 Q1

3.6 Q4

3.0 Q4 '04

4.2 Q4 '04

2.9

5.9 Q4 '04

2.0

2.3 Q4 '04

1.1

4.2 Q4 '04

3.9 Q4 '04

5.2

2.7 Q4 '04

-0.2

8.6 Q4 '04

5.6

3.8 Q4 '04

3.4 2003

2.3 Q4 '04

-0.3

2.9 Q4 '04

3.9 Q4 '04

0.6

4.3

8.0

5.8 Q4 '04

3.4 Q4 '04

2.7 Q4 '04

2.6 Q4 '04

1.2 Q4 '04

2.8

341

4001 11

3009 12

367 13

2500

1076

0.49 10

1007 Feb-Mar '04

2751.3 16

730 17

3299.3

47025.5

12878.4

661.6

2287

379.4

26912.6

16435.8

540 17

481.9

3009 18

150.1

0.29 10

19349.3

2632.4

7860

962.7

4100

996 21

678

-0.13 10

7187

2528.8

16565.7

14573.8

6.9 2003

4.6

8

n/a

11.9

18.7 Apr '05

5.1

8.3

5.4

7.9

8.3

9.8

9.8

10.5

6.3

3 Q1

4.3

8

9.4

8.6

4.5

n/a

6.8 7

4.6

4.4

18.1

6.9

7.1

n/a

15.9

5.8

10.2

6.3

4.3

4.7 Jan '05

1.23 Q1 '05

15

40.8

0.66 Jan-Apr '05

2.73 Q1

2.78 Jan-Apr '05

0.1

9.4

10

0.8

8

55.3

119.1

1.9

7.1

0.67

13

40.7

0.6

1.2

2.1

1.67

0.3

48

30.7 Q4

10.6

4.4

18.8

3.8

3.6

2.1

22.9

15.7

150 10

41.8

0.42 Q1 '05

14.8

40.4

2.89 Jan-Apr '05

3.6 Q1

5.74 15

0.7

9.1

9.2

1

6.5

59.5

92.7

6.4

7.6

0.83

8.3

44.3

0.9

1.5

2.6

2.9

0.4

42.8

20.7 Q4

11.3

6.5

24.7

11.75

3.8

2.2

33

12.9

n/a

57.4

-0.3 Apr '05

-0.3 Apr '05

0.2

0.6 14

1.1 Apr '04

-0.2 Apr

1.1

0.3

0.5

0.5

0.3

0.2

0

0.8

0.7

-0.5 May '05

0.6

0.8

1.1

0.3

0.7

1.2 2003

3.6 9

0.2

0.5

0.4

0.7

n/a

10.8

12.5

-0.1 22

1.4

0.2

0

1.9 Apr '05

1040

12700

14400

1800

6830

8190

3450

27000

38000

1380

11200

70800

96800

5800

12800

819

4150

63300

1540

3450

311

935

n/a

21400

37700

34000

12800

9450

4468.5 Apr '05

12100

8600

26800

22200

72.18 23

46100

All data are provided by the governments of respective countries, unless otherwise noted.1 OECD, 20042 Eurostat/US Bureau of the Census, 20043 at current market exchange rates4 Eurostat, Q1 '055 2003 OECD Mn $US unless otherwise specified. Some numbers in Euros.6 Eurostat, March 2004, billions of Euros7 Eurostat, Feb 20058 Eurostat, Feb 2005, billions of Euros9 Eurostat, April 200510 2003 World Bank11 EIU '0412 OECD '04 (Jan. - June) 24 Bosnia-Herzegovina 25 Serbia and Montenegro

13 State Dept. '04 (Jan.-Sept.)14 April 2005 - BiH Federal Office of Statistics15 Jan-Apr 2005 State Statistics Bureau16 2003 OECD17 Mn Euros '04 Unibank18 pooled FDI with Belgium19 2004 Malta NSO20 World Bank21 National Bank of Serbia '0422 2003 - Deutsche Bank Research23 Mn USD; April 2005, Swiss National Bank, Monthly Statistical Bulletin, May 2005

GDP

bil

lions

USD

at 20

04 m

arke

t pric

esPo

pula

tion

millio

ns

GDP

per

cap

ita

billio

ns U

SD at

2004

mar

ket p

rices

G

DP g

row

th

% ch

ange

from

year

prev

ious

Inco

min

g FD

I co

ntra

cted b

illion

s USD

Unem

ploy

men

t % Ex

port

sbil

lions

USD

Fore

ign

Curr

ency

Res

erve

s

billio

ns U

SD

Impo

rts

billio

ns U

SD

Infla

tion

CPI %

chan

ge fr

om m

onth

prev

ious

Albania

Austria

Belgium

B-H 24

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Macedonia

Malta

Netherlands

Norway

Poland

Portugal

Romania

S & M 25

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom

n/a = not available

4.41 10

291.9

351.5

5.07 10

19.9 10

28.19

11.4 10

107

241.8

9.1

185.9

2010.4

2703.1

205.2

99.7

12.16

181.7

1677.9

3.93 Q4 ‘04

6.32 Q1 ’05

31.7

4.7

5.37

579.0

250.1

241.6

167.7

36.0

14.9

41.2

25.4

991.7

346.0

358.8

2124.5

3.14

8.14

10.4

4.14 10

7.80

4.42 2003

0.73

10.21

5.40

1.35

5.22

59.90

82.53

11.04

10.12

0.29

4.03

57.89

2.32

3.44

0.45

2 10

0.4

16.26

4.55

38.19

10.41

21.71

8.16

5.4 10

2 10

42.34

8.97

7.36

59.67

$1,392 10

$35,860

$33,810

$1,225

$2,551

6,377

15607.89

10478.38

44797.69

6735.75

35615.07

33562.21

32752.26

18585.27

9854.99

41,865

45112.59

28985.18

1695.41

1833.48

70194.86

2350

13431.99 19

35613.24

54939.26

6326.16 20

16113.38

1658.12

1826.43

7629.63

12700

23419.36

38548.52

48722.86

35602.31

6.0 10

2.0

1.8

2.7 10

5.4 Q1

3.6 Q4

3.0 Q4 '04

4.2 Q4 '04

2.9

5.9 Q4 '04

2.0

2.3 Q4 '04

1.1

4.2 Q4 '04

3.9 Q4 '04

5.2

2.7 Q4 '04

-0.2

8.6 Q4 '04

5.6

3.8 Q4 '04

3.4 2003

2.3 Q4 '04

-0.3

2.9 Q4 '04

3.9 Q4 '04

0.6

4.3

8.0

5.8 Q4 '04

3.4 Q4 '04

2.7 Q4 '04

2.6 Q4 '04

1.2 Q4 '04

2.8

341

4001 11

3009 12

367 13

2500

1076

0.49 10

1007 Feb-Mar '04

2751.3 16

730 17

3299.3

47025.5

12878.4

661.6

2287

379.4

26912.6

16435.8

540 17

481.9

3009 18

150.1

0.29 10

19349.3

2632.4

7860

962.7

4100

996 21

678

-0.13 10

7187

2528.8

16565.7

14573.8

6.9 2003

4.6

8

n/a

11.9

18.7 Apr '05

5.1

8.3

5.4

7.9

8.3

9.8

9.8

10.5

6.3

3 Q1

4.3

8

9.4

8.6

4.5

n/a

6.8 7

4.6

4.4

18.1

6.9

7.1

n/a

15.9

5.8

10.2

6.3

4.3

4.7 Jan '05

1.23 Q1 '05

15

40.8

0.66 Jan-Apr '05

2.73 Q1

2.78 Jan-Apr '05

0.1

9.4

10

0.8

8

55.3

119.1

1.9

7.1

0.67

13

40.7

0.6

1.2

2.1

1.67

0.3

48

30.7 Q4

10.6

4.4

18.8

3.8

3.6

2.1

22.9

15.7

150 10

41.8

0.42 Q1 '05

14.8

40.4

2.89 Jan-Apr '05

3.6 Q1

5.74 15

0.7

9.1

9.2

1

6.5

59.5

92.7

6.4

7.6

0.83

8.3

44.3

0.9

1.5

2.6

2.9

0.4

42.8

20.7 Q4

11.3

6.5

24.7

11.75

3.8

2.2

33

12.9

n/a

57.4

-0.3 Apr '05

-0.3 Apr '05

0.2

0.6 14

1.1 Apr '04

-0.2 Apr

1.1

0.3

0.5

0.5

0.3

0.2

0

0.8

0.7

-0.5 May '05

0.6

0.8

1.1

0.3

0.7

1.2 2003

3.6 9

0.2

0.5

0.4

0.7

n/a

10.8

12.5

-0.1 22

1.4

0.2

0

1.9 Apr '05

1040

12700

14400

1800

6830

8190

3450

27000

38000

1380

11200

70800

96800

5800

12800

819

4150

63300

1540

3450

311

935

n/a

21400

37700

34000

12800

9450

4468.5 Apr '05

12100

8600

26800

22200

72.18 23

46100

All data are provided by the governments of respective countries, unless otherwise noted.1 OECD, 20042 Eurostat/US Bureau of the Census, 20043 at current market exchange rates4 Eurostat, Q1 '055 2003 OECD Mn $US unless otherwise specified. Some numbers in Euros.6 Eurostat, March 2004, billions of Euros7 Eurostat, Feb 20058 Eurostat, Feb 2005, billions of Euros9 Eurostat, April 200510 2003 World Bank11 EIU '0412 OECD '04 (Jan. - June) 24 Bosnia-Herzegovina 25 Serbia and Montenegro

13 State Dept. '04 (Jan.-Sept.)14 April 2005 - BiH Federal Office of Statistics15 Jan-Apr 2005 State Statistics Bureau16 2003 OECD17 Mn Euros '04 Unibank18 pooled FDI with Belgium19 2004 Malta NSO20 World Bank21 National Bank of Serbia '0422 2003 - Deutsche Bank Research23 Mn USD; April 2005, Swiss National Bank, Monthly Statistical Bulletin, May 2005

GDP

bil

lions

USD

at 20

04 m

arke

t pric

esPo

pula

tion

millio

ns

GDP

per

cap

ita

billio

ns U

SD at

2004

mar

ket p

rices

G

DP g

row

th

% ch

ange

from

year

prev

ious

Inco

min

g FD

I co

ntra

cted b

illion

s USD

Unem

ploy

men

t % Ex

port

sbil

lions

USD

Fore

ign

Curr

ency

Res

erve

s

billio

ns U

SD

Impo

rts

billio

ns U

SD

Infla

tion

CPI %

chan

ge fr

om m

onth

prev

ious

T r e n d s , S tat s a n d I n d i c at o r s

18© 2005 Strategic Forecasting, Inc.

J U N E 2 0 0 5

Albania

Austria

Belgium

B-H 1

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Ireland

Italy

*Closing Rates1 Bosnia-Herzegovina2 Serbia and Montenegro

Beginning

96.700

0.7776

0.7776

1.5210

1.5167

5.7255

0.4524

23.609

5.7911

12.1572

0.7776

0.7776

0.7776

0.7776

196.02

63.249

0.7776

0.7776

Low

96.180

0.7730

0.7730

1.5119

1.5097

5.6524

0.4479

23.178

5.7552

12.0458

0.7730

0.7730

0.7730

0.7730

193.16