12-15-08 final state of the madison region report

TRANSCRIPT

State of the Madison Region

2008‐2009 Report

Issued in December 2008

2008‐2009 STATE OF THE MADISON REGION REPORT 2

Consulting Economist Terry Ludeman

Special Thanks to:

Eric Grosso, Economist Wisconsin Department of Workforce Development Matthew Kures, GIS Specialist University of Wisconsin‐Extension, Center for Community and Economic Development Andrew B. Lewis, Professor University of Wisconsin‐Extension, Center for Community and Economic Development

Report Prepared by: Sue Gleason, Thrive

Director of Regional Assets and Metrics

608‐443‐[email protected]

with assistance from Julia Popolizio, Thrive Project Specialist

andShane Wibeto, Thrive Project Assistant

MEDIA INQUIRIES TO JENNIFER

SMITH at 608‐443‐1961 OR

2008‐2009 STATE OF THE MADISON REGION REPORT 3

GROWING THE MADISON REGION’S ECONOMY IN WAYS THAT

PRESERVE AND ENHANCE QUALITY OF LIFE.

In order to begin a dialogue concerning our shared regional future in five, ten, twenty years and beyond, we need to understand the state of our eight‐county Madison Region today. Thrive’s first annual STATE OF THE MADISON REGION report is that tool, a report to foster a more complete and accurate view of our interdependencies as a region, so we can all move forward… together.

Planning for this report began in 2007 when the Thrive Quality of Life Committee launched a regional survey effort to find out what people cared about and how they thought the region was doing in key areas. Those findings served as the foundation for the development of this STATE OF THE MADISON

REGION report. This new report brings traditional economic indicators together with quality of life indicators for a unique set of quantitative measures that will help guide our decisions as a region and over time, will help monitor the long‐term impact of our region’s collective efforts.

Thrive intends to issue a STATE OF THE MADISON REGION report on an annual basis, and will include updates and changes to the measures as we learn what is most useful for the region. The report here is just the start of a long‐term process of monitoring and measuring performance and motivating action. As part of an ongoing process using the report, Thrive will focus on one key theme each month by engaging experts, delving into the nuances of the data, and providing insights into how we can use this data to celebrate our strengths and work together to better understand and tackle areas where there is room for improvement. Be sure to sign up for the Thrive Newsletter on any page of the www.thrivehere.org website to get the Monthly Insights. In addition, look for our Sector Snapshots in early 2009 and a Regional Innovation report mid‐year. We recognize that we are issuing this report at an unprecedented time in the world and in our nation’s history and expect that the next few years will bring changes and impacts to the region that no one can foresee. Nevertheless, we are excited to offer this report to the Madison Region and on behalf of the Thrive Board and staff we look forward to joining with all of our regional leaders and stakeholders as we embark on a new chapter in defining the Madison Region, celebrating its strengths and working together to make it even better.

Jennifer Alexander, Thrive President John Biondi, Thrive Board Chair

2008‐2009 STATE OF THE MADISON REGION REPORT 4

The Madison Region consists of the eight counties in south central Wisconsin that

cluster around the State Capital and contain some of the most

beautiful geography in the nation.

The region’s rich agricultural heritage combined with a world renowned university in the center

of the region, surrounded by a strong

manufacturing network of small, medium, and large firms creates a region that feeds, educates and builds the world.

2008‐2009 STATE OF THE MADISON REGION REPORT 5

TTaabbllee ooff CCoonntteennttss

Executive Summary 6‐7 Choosing our Peer Regions 8‐9 Choosing our Measures 9 State of the Region Themes

Life at Work 10 1. Employment Growth 2. Establishment Growth 3. Productivity 4. Employer Supplement to Wages 5. Per Capita Personal Income 6. Average Wage per Job

Life at Home 14 7. Home Ownership 8. Cost of Home Ownership per Income 9. Poverty Rate 10. Median Household Income

Life at School 16 11. 3rd Grade Reading and 5th Grade Math Levels 12. Eligibility for Subsidized Lunch 13. K‐12 Enrollment 14. High School Degree in Adult Population 15. Associates Degree in Adult Population 16. Bachelor’s Degrees and Higher in Adult Population

Life in our Communities 18 17. Population Change 18. Age Dependency 19. Crime Rate 20. Local Governments

Life on the Move 20 21. Biking or Walking to Work 22. Traveling Over 30 Minutes to Work 23. Vehicle Miles Traveled 24. Traffic Fatalities 25. Alcohol Impaired Drivers in Fatal Crashes

A Healthy Active Life 22 26. Low Birth Weight Births 27. Health Insurance Coverage 28. Fitness and Sports Centers 29. Air Quality Index‐ Ozone Days 30. Special Outdoor Places

Regional Maps 24 Additional Reports Planned in 2009 26

2008‐2009 STATE OF THE MADISON REGION REPORT 6

PPEEEERR RREEGGIIOONNSS LLiinnccoollnn,, NNeebbrraasskkaa CCoolluummbbuuss,, OOhhiioo SSaalleemm,, OOrreeggoonn

CCoolluummbbiiaa,, SSoouutthh CCaarroolliinnaa

RRiicchhmmoonndd,, VViirrggiinniiaa

EExxeeccuuttiivvee SSuummmmaarryy The first annual State of the Madison Region Report provides a unique set of regional economic and quality of life metrics. This annual report will inform us about where we are doing well, where we can improve, and will help regional decision‐makers make focused decisions in a collaborative manner for the good of the overall region. To ensure a comprehensive look at the region, we selected measures that tell the full story about our region. To that end, there are thirty individual metrics grouped into six topic areas to cover all aspects of life.

In addition to reporting on the overall “health” of the Madison Region, metrics are included for five peer regions, and when appropriate, for the state and the nation. There might be some surprise at the five regions that were chosen as our representative peers as they are not the usual areas that are often compared Madison. But they are unique similar in many ways to our region as a whole and will serve us well as overall benchmark regions. They were chosen based on key similarities such as being a State Capital and having a major university important to the region. They are all key regions in their states but not the primary metro region. These are important features to benchmark against, but we recognize that a different set of regions might be chosen to look at related to specific aspects of the region. In fact we may compare ourselves to others for reports with a different focus such as the Sector Snapshots or Regional Innovation report. See page 8‐9 on more about choosing these peer regions.

Thrive’s objective with this report is to inform and to spur action for individuals and organizations in the region as we move toward a shared regional vision. The metrics used are objective, quantitative measures of specific aspects of our region, chosen for this inaugural report with guidance from the Summary of the Madison Region Quality of Life Indicators. We anticipate changes over the coming years as we fine‐tune our metrics to best tell our story and help us grow together as a region. Still to come in 2009 are Monthly Insights to further explore these measures, Sector Snapshots on our targeted three sectors of agriculture, biotechnology and healthcare, and planning is underway for a mid‐year Regional Innovation report.

Life at Work ‐ Work is one of the activities in life that give us meaning, an opportunity to contribute, to create, and to provide for our families. The kinds of work we do help define our communities and our region. o Per capita income, including all forms of income, was quite high in the Madison Region, estimated at

$36,071, 3rd among the peer regions with the weighted peer average at $35,006.

o For wages per job, the Madison Region averaged $36,348; lower than the peer average of $38,001 but placing 3rd, behind the Columbus, OH and Richmond, VA regions.

o Employer contributions to pension and insurance funds, ranged from a low of 15.7% of wages/salaries to a high of 18.6% with the Madison Region at 16.7%.

o Productivity is an important measure of output per measured input. Every dollar paid for wages and salaries produced $1.71 in the Madison Region and the highest was Columbus, OH at $1.78, a seemingly small gap that translates to a difference of $1.75 billion per year.

o In growth of business establishments, the Madison Region, at 8.5%, was slightly above the 8.1% average for the peer regions.

o Actual employment growth in most of the peer regions has been quite robust at 7.1% over the period from 2001 to 2006. The Madison Region was second at 8.4% with Salem, OR leading at 10%.

2008‐2009 STATE OF THE MADISON REGION REPORT 7

EExxeeccuuttiivvee SSuummmmaarryy Life at Home – The shelter of a home has always been one of the most important components of quality of life along with having the means to care for one’s family. Success at school and at work often starts at home. o The Madison Region has the 3rd highest rate of ownership compared to the peer regions, but ranks 2nd in

terms of the percent of household income that goes to mortgage costs.

o Our region boasts the lowest poverty rates among the peer regions but has seen the 3rd highest increase in the percent of the population in poverty from 2000 to 2005.

Life at School – Education has become widely recognized as a foundation of both quality of life and economic vitality. We must have an adequate and well‐educated pipeline for the future.

o Looking at just the Madison Region since 2005, 5th graders have increased 2.2% in math skills, while 3rd graders dropped 1.7% in reading skills.

o From 2000 to 2005, the Madison Region declined in overall K‐12 enrollment, rebounding slightly in 2007 but still lagging our peers.

o Again just for the Madison Region, the percentage of children that met poverty thresholds to be eligible for subsidized lunches increased from 17.8% in 2000 to 25.7% in 2007, now over a quarter of the children in our region’s schools.

o Among our peer regions adult populations, we have a high percent of high school graduates, the 2nd highest in associate’s degrees, and are 4th in bachelor’s degrees or better.

Life in our Communities – Vital and safe communities contribute immensely to the quality of life in the Madison Region and are at the heart of what makes this region such a great place to live. o The Madison Region has the lowest rate of violent and property crime combined of the peer regions.

o Our population growth lagged behind all but one of the other peer regions from 2000 to 2007.

o We have the 2nd highest number of local governmental units per 10,000 in population among the peers.

Life on the Move – How we get from one place to the other is more important than ever and will help define our region in the future. o The Madison Region is the highest among the peer regions in walking

or biking to work and 2nd lowest in traveling over 30 minutes to work.

o Our traffic fatalities per capita have decreased since 2000 compared to the peer regions.

o Compared to our peer regions, we were #1 in 2000 and #2 in 2007 for alcohol impaired drivers involved in those fatal crashes.

Living a Healthy, Active Life – Health and activity go hand‐in‐hand and are important components of our regions’ quality of life. o Among the peers, the Madison Region was 1st for health insurance coverage in 2000 and 3rd in 2007.

o The Madison Region has the 2nd lowest percentage of low birth weight births of the peer regions.

o Somewhat surprisingly, the region has the lowest number of fitness centers per 1,000 of population.

o Related to air quality, the region had the 2nd highest increase in ozone days from 2000 to 2007.

o Our region is 2nd in the number of special places like national and state parks, and rails to trails.

2008‐2009 STATE OF THE MADISON REGION REPORT 8

CChhoooossiinngg oouurr PPeeeerr RReeggiioonnss

LLIINNCCOOLLNN,, NNEEBBRRAASSKKAA AANNDD AA SSIIXX‐‐CCOOUUNNTTYY SSUURRRROOUUNNDDIINNGG AARREEAA See pages 24‐25 for detailed maps

Population 342,300, and 19 percent of Nebraska’s total population Growth 16 percent growth from 1990 to 2000, and 8 percent from 2000 to 2007 Features State Capital; University of Nebraska; Lincoln is 40 miles from Omaha, the largest city

CCOOLLUUMMBBUUSS,, OOHHIIOO AANNDD AANN EEIIGGHHTT‐‐CCOOUUNNTTYY SSUURRRROOUUNNDDIINNGG AARREEAA Population 1,754,300, and 15 percent of Ohio’s total population Growth 14.8 percent growth from 1990 to 2000 and 8.8 percent from 2000 to 2007 Features State Capital; Ohio State University; Columbus is Ohio’s largest city but slightly smaller

than the metro areas of Cincinnati and Cleveland

CCOOLLUUMMBBIIAA,, SSOOUUTTHH CCAARROOLLIINNAA AANNDD AA SSIIXX‐‐CCOOUUNNTTYY SSUURRRROOUUNNDDIINNGG AARREEAA Population 716,000, and 15 percent of South Carolina’s total population Growth 18 percent growth from 1990 to 2000 and 10.6 percent growth from 2000 to 2007 Features State Capital; University of South Carolina; South Carolina’s largest metro area, although

the City of Charleston is a somewhat larger city than Columbia

SSAALLEEMM,, OORREEGGOONN AANNDD AA FFIIVVEE ‐‐CCOOUUNNTTYY SSUURRRROOUUNNDDIINNGG AARREEAA Population 925,000, and 25 percent of Oregon’s total population Growth 15.7 percent growth from 1990 to 2000, and 8.8 percent growth from 2000 to 2007 Features State Capital; University of Oregon at Eugene and Oregon State University at Corvallis,

region contains three mid‐size cities; Salem, Corvallis and Eugene, and is 35 miles south of Portland, Oregon’s largest city

RRIICCHHMMOONNDD,, VVIIRRGGIINNIIAA AANNDD AA SSIIXXTTEEEENN‐‐CCOOUUNNTTYY AARREEAA,, PPLLUUSS FFOOUURR CCIITTIIEESS Population 1,220,000, and 15 percent of Virginia’s total population Growth 15.6 percent growth from 1990 to 2000, and 11.2 percent from 2000 to 2007 Features State Capital; University of Richmond; and near two super metros, the Virginia

Beach/Newport News, Norfolk metro and of course the Washington, D.C metro. Also nearby are several other well known colleges and universities

MMAADDIISSOONN,, WWII AANNDD AANN EEIIGGHHTT‐‐CCOOUUNNTTYY SSUURRRROOUUNNDDIINNGG AARREEAA Population 977,500, and 17 percent of Wisconsin’s total population Growth 11 percent growth from 1990 to 2000, and 8.3 percent growth from 2000 to 2007 Features State Capital; University of Wisconsin‐Madison; 2nd largest metro area in WI, between

Milwaukee, Chicago, and Twin Cities

Salem OR Region

Lincoln NERegion

Madison WIRegion

Columbus OHRegion

Columbia SC Region

Richmond VA Region

2008‐2009 STATE OF THE MADISON REGION REPORT 9

CChhoooossiinngg oouurr PPeeeerr RReeggiioonnss These five regions were chosen because they possess many of the same advantages present in the Madison Region, including their respective State Capitals and therefore the seat of their state governments, and the presence or close proximity to a major University. They are not the largest area in their states, but they have enough of their respective state’s population to be vital in their own right. They have research and innovation occurring at their universities, stable economies anchored by state government employment, and other employment opportunities in vibrant private sectors.

The metropolitan areas included have gross domestic product ranging from $10 billion to $75.4 billion. The Madison Region metro areas combined, Janesville/Beloit and Madison, are near the middle, with about $35.1 billion. The 2005 gross domestic product ranges from $23,362 per capita to $41,776 per capita for all the peer regions. The combined Madison and Janesville metro area is about $39,360 per capita, slightly over $38,095 which the mean for all of the regions.

Each of these region’s populations grew at a fast pace. In the period from 1990 to 2000, the average growth was 16.2 percent, led by Columbia, South Carolina at 18 percent. The Madison Region metros were actually the slowest growing metro areas with a 14.4 percent growth. Between 2000 and 2007, these areas have grown on average about 9.6 percent. Richmond, Virginia was the fastest growing at 11.2 percent, while Lincoln, Nebraska grew the slowest at 8.0 percent. The Madison Region grew from a population of 902,871 in 2000 to 977,470 in 2007, a growth of 8.3 percent, slightly below the average for these regions.

CChhoooossiinngg oouurr MMeeaassuurreess A metric is an objective, quantitative measure that describes some aspect of our region—economic, social, cultural, and environmental—over time. Our goal was to select measures that address both quality of life and economic measures. Based on guidance from the recent Madison Region Quality of Life Indicators Summary, as well as research on other regional indicators/metrics reports, the measures are organized into eight themes: Life at Work, Life at Home, Life at School, Life in our Communities, Life on the Move, and Living a Healthy, Active Life. To ensure that the effort is doable, sustainable, and credible, we have established guidelines for choosing the metrics that will be used:

1. The data must be publicly available without charge. 2. The data should be available at the county level across the nation for comparisons to peer regions.

However, locally collected data is used occasionally to augment or highlight more recent regional data. 3. The data must be the most current available. 4. The data selected must be available at least to 2000 to show trends. 5. The metrics should be actionable, suggesting an important issue for regional leaders to address.

BBUUTT WWHHYY NNOOTT ____________________??

Several capital regions were not chosen due to an overwhelming size compared to their respective states.

o Minneapolis/St. Paul, Indianapolis, Phoenix, Oklahoma City, and Atlanta were not chosen for this reason.

Other regions that were initially considered were ultimately not selected because they were not as dominant in their states as the Madison Region.

o Austin, Texas is often compared to Madison, but the Austin region is only 6 percent of the population of Texas and doesn’t have the same statewide political and economic clout in Texas that Madison does in Wisconsin.

o Lansing, Michigan and Montgomery, Alabama are also too small in their respective states to make the “short list”.

LLiiffee aat

Industry ERegion is stransportarepresentethe profeswhile the tpaying indregions is a

Edu

Nat

Professi

Trade,

Work is onprovide focommunit

Income cavariety of and a meaprovided a

tt WWoorrkk

mployment cstrongest in joation and utilied in jobs in tsional and butrade, transpoustrial sectoralso in the low

Co

ucation & Healt

Financia

In

Leisure &

Man

tural Resource

Oth

ional & Busine

Public Adm

Transportatio

ne of the thinor our familieties and our r

an mean seveincome meaasure of grossand discussed

comparisons obs in the maties sector, athe professionusiness servicortation and rs, the wage sw‐ to middle

SSoouurrcc

0.0%

onstruction

th Services

al Activities

nformation

Hospitality

nufacturing

s & Mining

er Services

ss Services

ministration

n, Utilities

Ind

ngs in life thats. The kinds oregion. Our in

eral things to sures. We ws product. Asd per capita,

10

between the nufacturing snd the leisurenal and busines sector andutilities sectostructure for trange.

ccee:: UUSS CCoommmmeerrcce

% 2.0% 4.0

dustry Sect

Madison

t gives us meof work and tndustry struc

both economill use wages s the regions or, when app

2008‐20090

Madison Regsector, with ge and hospitaess services sd the financiaor and the leisthe Madison

ee,, BBuurreeaauu ooff EEccoo

0% 6.0% 8.0

tor Employ

Region Pe

aning, an opphe income thcture helps us

mists as well aper job, per care varied in propriate, per

9 STATE OF THE

gion and the greater than aality sector. Tsector, and inl services secsure and hospRegion in com

oonnoommiicc AAnnaallyyssiiss,,

0% 10.0% 12

yment ‐ 20

eer Averages

portunity to chat we gain frs understand

as people in gcapita personpopulation, er job.

E MADISON RE

peer regions average repreThe Madison n the financiator tend to bpitality sectormparison to s

,, 22000066

2.0% 14.0% 1

006

contribute, toom that workthe region fu

eneral. This nal income, vaeach of these

EGION REPORT

finds the Maesentation in Region is lessl services secte high‐payingr tend to be losome of the p

6.0% 18.0% 2

o create, and tk help define rther.

report presenalue of benefe measures w

T

dison the trade, s tor. As g jobs ower‐peer

20.0%

to our

nts a fits ill be

Employme7.1 percenRegion at percent. I

As employpeer regioregions experhaps thmanufactu

Another inemploymeproprietorincreased proprietorself‐emplo Establishmlooks at thnumber ofestablishmemploymeperiod of 2The six peeaggregate The Madisabove the regions wiincrease. region hadduring thepercent in

MLinc

ColumSa

ColumRichmAverag

1.

ent Growth Fnt. The Salem8.4 percent. n all peer reg

yment in totaln lost employperienced anhe greatest exuring base, ex

nteresting pheent. Althoughr’s employmeby 4.9 percenr’s employmeoyment as we

ment or firm ghe increase in f business ments with soent activity du2001 througher regions saw8.1 percent ison Region waverage for tith an 8.5 perThe Lincoln Nd the fastest g period with crease.

Madison Regioncoln NE Regionbus OH Regionlem OR Regionmbia SC Regionond VA Regionge Peer Region

Wisconsin

Employment

rom 2001 to m, Oregon regDuring that s

gions except C

Source: U

l was growingyment, led by 11.8 percentxposure in emxperienced on

enomenon is h wage and sant increased nt, while propnt has becomell as locally o

growth the

me uring the 2006. w an ncrease.

was slightly the peer rcent Nebraska growth a 12.3

4.3

4

nnnnnnnn

t Growth 200

11

SSoo

Ma

Linco

Columb

Sale

Colum

Richmo

2.

2006, all peeion reported same period, Columbus, Oh

S Commerce, Bu

g, there werey a loss of 18.t decrease in mployment innly a 7.3 perc

the increase alary employm25.6 percentprietor’s empme 18.9 percewned busine

8.47.3

310

87.77.1

.7

00 to 2006

2008‐20091

oouurrccee:: UUSS CCoommmm

adison Region

oln NE Region

us OH Region

em OR Region

bia SC Region

nd VA Region

WI

US

Peer Average

. Growth in E

r regions expthe fastest gpopulation ghio, employm

ureau of Econom

structural em9 percent in tmanufacturin manufacturient decline.

in proprietorment on aver. In the Madloyment increent, very nearsses paying w

‐17

‐18.9

9 STATE OF THE

eerrccee,, BBuurreeaauu ooff

Establishme

perienced emrowth, at 10.grew for the sment growth o

mic Analysis, 200

mployment chthe Richmondng employmeng based on

r’s employmerage for the pison Region, weased by 26.1rly one‐fifth owages to the o

‐17.3

‐9

‐11

Manufactu

E MADISON RE

EEccoonnoommiicc AAnnaallyy

8.5

4.6%

9

9

8.1%

ents ‐ 2000 t

ployment gro0 percent, fosix peer regionoutpaced pop

00 to 2006

hanges. Mand, VA region. ent. The Madits relatively s

ent as opposepeer regions inwage and sal1 percent. In of total emploowner.

‐7.311.2

‐1.9‐10.8

1.8‐8.5

LiColu

SColRichAver

uring Change

EGION REPORT

yyssiiss,, 22000066

5%

12.3%

11.7%

9.3%

9.0%

9.1%

10.0%

%

o 2006

LLiiffee aatt

owth. The avellowed by thens, averagingpulation grow

nufacturing in On average,dison Region, stronger

ed to wage anncreased 3.8ary employmthe Madison

oyment. This

Madison Regiincoln NE Regimbus OH RegiSalem OR Regiumbia SC Regimond VA Regirage Peer Regi

Wiscon

2000 to 2006

T

%

WWoorrkk

erage was e Madison g 6.2 th.

each , the peer with

nd salary percent,

ment n Region, includes

ionionionionionionionsin

6

LLiiffee aat

Productiviper input, input of toRegion it wfigure is $1

Although tlike a smalvariance injob of $47, “Fringe Beby looking salaries. Coranged fropercent in percent in pensions asocial insuthe peer reaverage emgovernmeand salarieas well. Alcontributiosame throthe Salem,high, and tVA region

MadisLinc

ColumbSal

ColumRichmo

tt WWoorrkk

Source: US

ty is an extreusually a labootal employerwas $1.71. Th1.77, and for

the differencel differential,nto perspectiv,155 equals a

enefits” can bat employer ontributions fom 15.7 perce2006. The pemployer co

and insurancerance. The Megion averagmployer contnt social insues, and the Mlthough it woons for goverughout the re, OR region hathe Columbushad a low of

son WI Regioncoln NE Regionbus OH Regionem OR Region

mbia SC Regionond VA Region

WIUS

Peer Average

3. Amount

S Commerce, Bu

emely importaor cost figurer wage and sae highest outWisconsin th

e between $1, using the nuve. The avera productivity

be roughly estsupplementsfor insuranceent of wages aeer regions antributions foe funds not coMadison Regige, at 16.7 peribution for erance was 7.4

Madison Regioould be expecnment insuraegions, this wad an 8.8 pes, OH region a7.2 percent.

1.55 1.6

Productivity Produced pWages/Sa

12

ureau of Econom

ant metric as . The figure ualary input. Thtput was repoe figure was

1.71 and $1.7umber of wagage peer regi difference be

timated s to wages ane and pensionand salaries tveraged 16.6or employee ounting goveron was just arcent. The peemployee 4 percent of won was at thatted that empance would bwas not the carcent figure fand the Richm

1.631.67

1.6

1.65 1.7

y Measureper Dollar Paalaries

2008‐20092

mic Analysis, 200

it looks at thused here is thhe peer averaorted for the reported at $

8 as reportede and salary jon had 530,4etween $1.71

nd ns to 18.6 6

rnment above eer

wages t figure ployer e the ase as for a mond,

1.711.76

1

1.768

1.71.72

7 1.75

aid in

9 STATE OF THE

Source: US C

1

4.Wa

06

e value of thehe dollar valuage for this figColumbus, O$1.68.

d for Madisonjobs and the 421 salary job1 and $1.78 o

61.78

77

1.8

E MADISON RE

ommerce, Burea

16.7%16.6%15.

Employer Sage/Salary ‐

Ben

e products prue of Gross Stgure was $1.7H region at $

n and Columbaverage disbus at an averaof output of $

In ProRegionand rig

In EstaMadisothe pee

EGION REPORT

au of Economic

7%

18.0%18.6%

Supplements2006 or "Frefits"

roduced basetate Product p72. For the M1.78. The nat

bus, respectivursement putge disbursem1,750,826,19

ductivity, the is 3rd among ht at the Pee

ablishment Gon Region waer average.

T

Analysis, 2006

%

16.4%16.6%

s to ringe

ed output per dollar adison tional

ely, seems ts the ment per 90.

e Madison the peers

er Average.

rowth, the s above

Per CapitainvestmenRegion in aaverage wapproximaincome, atthe strong

Wages perworkers anindustries on the areconcentratlawyers, ensmall comRegion has

MadiLinc

ColumbSal

ColumRichmo

In averMadiso

Source: US Co

a Personal Incts. The PCPI fa strong thirdas $35,006, aately six percet about 86 peest growth of

r Job Wagesnd is normallyhaving wagesa where the etion of emplongineers), finmunities ands an average o

son WI Regioncoln NE Regionbus OH Regionlem OR Regionmbia SC Regionond VA Region

WIUS

Peer Average

5. Per C

rage wage peon Region ran

ommerce, Burea

come Personafor the Madisd place amongand the nationent higher tharcent of the nf any of the o

s per job is bay compiled pes double the wemployment oyment in higancial service small urban of $36,348; th

nnnnnnI

e

Capita Perso

r job, the nked 3rd..

13

au of Economic A

al income is dson Region wag the peer regnal figure wasan the Madisonorm for the other peer reg

S

sed on place er industry. Twages in otheis measured.h paying serves, or informaareas. It therhe peer avera

onal Income

$38,

PeAver

2008‐20093

Analysis, 2006

defined as all as quite high,gions, close tos $36,744. Ricon Region. Thpeer regions.gions.

Source: US Com

of work dataThere is a greaer industries.. Areas with dvice sectors suation servicesefore has lowage was $38,0

$36,$33,17

$36,$30,065$32,614

$3$34,4$36

$35,0

e ‐ 2006

,001$42,223

eer rage

RichmondVA

Region

9 STATE OF THE

income from, at $36,071 fo the Columbchmond, VA, he Salem, OR. Since 2001,

merce, Bureau o

a. It measureat variation in The structurdense populatuch as profess. The Madisower wages tha001.

,0719,110

438,233606,744006

3 $35,654 $3

d Columbia SC Region

SalR

6. Average W

E MADISON RE

wages, businfor 2006. Thisbus, OH regiohad the highregion had ththe Richmon

of Economic Ana

s the wages an wages per inre of industry tion often hassional and teon Region conan the peer a

33,565 $40,3

lem OR egion

ColumbOH

Regio

Wage per Jo

Per capimeasureindividuaMadisonamong pstate and

EGION REPORT

LLiiffee aatt

ness enterpriss put the Madn. The weightest per capitahe lowest perd, VA area ha

alysis, 2006

and salary paindustry, withemploymentve heavier echnical servicnsists of a numverage. The M

50 $32,710

bus

on

Lincoln NE

Region

ob ‐ 2006

ta income is ae of all incomals and the n Region rankpeers, ahead d the nation.

T

WWoorrkk

se and dison ted peer a income, r capita as seen

id to some t depends

ces (i.e., mber of Madison

$36,348

Madison Region

a e for

ked 3rd of the

LLiiffee aat

The sheltealways beimportantquality of having theone’s fam

Success atoften star

Theranpeeow

Theat tfor incotha

Thto owissmadrpanewithhacope

tt HHoommee

er of a homeeen one of tht componenlife along we means to c

mily.

t school andrts at home.

Madison Renks 3rd amoner regions fonership.

e Madison Rthe national mortgage coome, slightlyn the peer a

his is a difficuaddress hom

wnership andsues as the harket has chamatically inast two yearsext Census inll help us see Madison Ras fared in thompared to oeers.

ee

e has he most ts of

with care for

d at work

egion g the or home

egion is average ost per y more average/

ult time me d cost housing anged n the s. The n 2010 e how Region his area our

14

Ma

L

Colu

Colu

Rich

Mad

Lin

Colum

S

Colu

Richm

2008‐20094

adison WI Regi

Lincoln NE Regi

umbus OH Regi

Salem OR Regi

umbia SC Regi

hmond VA Regi

7. H

dison WI Regio

ncoln NE Regio

mbus OH Regio

Salem OR Regio

mbia SC Regio

mond VA Regio

W

U

Peer Averag

8. Homeo

9 STATE OF THE

Source: US C

Source: US C

ion

ion

ion

ion

ion

ion

WI

US

ome Owner

on

on

on

on

on

on

WI

US

ge

owner Cost a

E MADISON RE

Census, 2000

Census, 2000

62.9%

63.0%

63.1%

rship Rate ‐ 2

20.2%

20.2%

2

2

as % of Inco

EGION REPORT

65.3%

68.7

68.4

66.2%

2000

21.8%

21.1%

21.0%

0.9%

21.7%

21.2%

me ‐ 2000

T

70.2%

7%

%

23.1%

Source: US

Source: US

Madi

Linc

Columb

Sal

Colum

Richmo

9

Madis

Linc

Columb

Sale

Colum

Richmo

S Census, Small A

S Census, Small A

son WI Region

coln NE Region

bus OH Region

lem OR Region

mbia SC Region

ond VA Region

WI

US

9. Poverty Ra

2005

son WI Region

coln NE Region

bus OH Region

em OR Region

mbia SC Region

ond VA Region

WI

US

10. Median

Area Income an

Area Income an

n

n

n

n

n

n

I

S

ate ‐ % Popu

5 All ages %

Household from 2000

15

d Poverty Estim

d Poverty Estim

6.9%

8.2%

9.2%

8.1%

9.6%

10

10

ulation ‐ 200

2000 All age

3.7%

5.8

5.9

Income ‐ % to 2005

2008‐20095

ates, 2000 and 2

ates, 2000 and 2

%

11.7%

11.4%

11.9%

11.3%

%

0.5%

13.3%

15.7

13.9%

13.0%

0.2%

13.3%

00 to 2005

es %

6.9%

1

9.8

%

11

9%

10

increase

9 STATE OF THE

2005

2005

%

10.8%

8%

1.3%

0.1%

Atds

Hint

Dtinhkinloo

E MADISON RE

L

Adequate inche most impdeterminantuccess and q

Lowestin 2005peers, tnation,highest2000 topeers aincreasthan W

Fourth incomecomparlaggingahead o

Household inncome fromhe househo

During the saime, our povncreased anhousehold inkeep pace wndication of ower wage jour region’s

EGION REPORT

LLiiffee aatt HH

come is one portant s of economquality of lif

% poverty r5 compared tthe state an though 3rdt % increase o 2005 amonand a higher e in poverty

WI and the U.

in househole increase red to peers the US, andof WI.

ncome calcum all workers ld.

ame period overty rate d our mediancome did noith our peeran increaseobs for morworkers.

T

HHoommee

of

mic e.

rate to d the

from ng

y rate S.

ld

s, d

lates in

of

an ot s, an e in re of

LLiiffee aat

Education hrecognized both qualityvitality. Weadequate apipeline for

Preparationlevel is crucacademic sgrade readito read” shlearn,” and where basicachieved tomath skills.

In ththe Mseen 3rd grabove

In ththe Mseen of 5th

proficmath

SinceRegioperceincomfor su

Enroin thfromwas 2007Regi

tt SScchhoooo

has become was a foundaty of life and ee must have and well‐educr the future.

n at the elemcial for futureuccess. We loing, where “leifts to “readin5th grade mac skills need to build higher

he past three Madison Regioa decline in trades readinge grade level.

he past three Madison Regioan increase i

h graders withcient or adva skills.

e 2000, the Mon has seen aent increase ime children eubsidized mea

ollment has dehe Madison Rm 2000 to 200slight increas7 for the Madion.

ooll

widely ion of economic an cated

entary e ook at 3rd earning ng to ath, to be r level

years, on has the % of g at or .

years, on has n the % h nced

Madison n 8 n low ligible als.

eclined egion 05. There se in dison

16

So

Source: Enroon Kids based

8

M

Lin

Colum

S

Colu

Richm

2008‐20096

Source: Madiso

ource: Madison Re

ollment Data frod on data contri

83.7%

78.1%

2005

P3rd Grad

3rd Grade R

17.8%

2000

Increfor S

Madison Regio

ncoln NE Regio

mbus OH Regio

alem OR Regio

umbia SC Regio

mond VA Regio

W

U

13. K‐12 E

9 STATE OF THE

on Region only – W

gion data only – W

om Annie E. Casebuted form each

83.4%

7

200

11. MadisoProficient orde Reading a

Reading Level

24.4

200

12. Madisease in K‐12Subsided Lun

Inc

‐0.12

2

‐1.15

‐0.49

on

on

on

on

on

on

WI

US

Enrollment C

E MADISON RE

Wisconsin Departm

Wisconsin Departm

ey Kids Count Coh state educatio

79.2%

06

on Regionr Advancedand 5th Grad

5th Grad

40% 2

05 2

son Region Students Elnch due to Fome

.00

3.42

6

3.78

Change 2000

EGION REPORT

ment of Public Inst

ment of Public Inst

ommunity‐Level on department, 2

82.0%80.3%

2007

de Math

e Math Level

25.7%

2007

ligible Family

6.08

0 to 2005

T

truction WINSS

ruction WINSS

Information 2000 to 2005

%

11.24

MadiLinc

ColumbSal

ColumRichmo

MadiLinc

ColumbSal

ColumRichmo

Mad

Lin

Colum

Sa

Colu

Richm

Source: US

Source: US

Source: US

son WI Regioncoln NE Regionbus OH Regionlem OR Regionmbia SC Regionond VA Region

WIUS

14. High SAdult P

son WI Regioncoln NE Regionbus OH Regionlem OR Regionmbia SC Regionond VA Region

WIUS

15. AA

dison WI Regio

ncoln NE Regio

mbus OH Regio

alem OR Regio

mbia SC Regio

mond VA Regio

16. BachA

Census, Educati

Census, Educati

Census, Educati

nnnnnnIS

School DegrPopulation o

nnnnnnIS

Associates DAdult Popula

on

on

on

on

on

on

elor's DegreAdult Popula

17

ion Attainment,

ion Attainment,

ion Attainment,

8281.5

80.4%

ree or Higheover 25 yrs ‐

5

Degrees in tation ‐ 2000

ee or Higheration ‐ 2000

2008‐20097

2000

2000

2000

87.9%88.9%

85.7%

.1%5%

85.1%%

er in the‐ 2000

8.0

5.7%7.0%7.4%

.1%7.5%

6.3%

he

27.6%

29.0%

28.3%

24.0%

26.6%

27.8%

r in the

9 STATE OF THE

%

91.4%

0%8.6%

Itcsinesc

Rasmhpra

HncMn

RofrInHrRra

E MADISON RE

LL

t is more impcontinue educchool, both tn demand secembrace life‐lkill upgradingcentury globa

Regardless of against our petrive to impromeasures as whave residentsprosper and cegion due to and skills.

2nd schhigpo

2nd deg

4th bachig

High school grnot included acalculated uniMadison Regionation.

Recently releaon high schoorom the UW nstitute in theHealth Rankinange across tRegion from 5anking betweamong WI cou

EGION REPORT

LLiiffee aatt SS

ortant than ecation beyondo achieve degctors and alsoong learning g for the 21st l economy.

where we raeers, we mustove on all of twe cannot affs unable to ontribute to ta lack of edu

highest high hool diploma gher in adult pulation

highest assogree

highest with chelors’ degrgher

raduation ratas these are niformly in theon or across t

ased informatol non‐complePopulation He 2008 WI Congs indicates athe Madison 5.7 to 13.9 peeen 23 and 65unties.

T

SScchhooooll

ever to d high grees o to and

nk t these ford to

the cation

or

ciate’s

ee or

es are not e the

tion etion ealth ounty a

rcent, 5

LLiiffee iinn

Vital acontribqualityRegionwhat mgreat p

Htna

TdMe4a

An intemeasuwhich 65+ agworkinchild da low navailabfuture. For theRegionratio—of the indicatfor theshortafor the The avdepenpopulaMadiso

nn oouurr CCoo

nd safe commbute immensey of life in then and are at thmakes this regplace to live.

Higher populathan the statenation, but 2n

among peer r

The populatiodependency rMadison Regiestimated at 43.6, the loweamong the pe

eresting popuure is the depelooks at the 0ge cohorts agang age populaependency ranumber of yoble for work in.

e 0‐14 cohortn registered a—good for nowpeer regions tive of a saggie area and a pge of entry lee future.

verage peer redency ratio foation was 16.3on Region at

oommmmuunn

munities ely to the e Madison he heart of gion such a

ation growth e or the nd to last regions

on ratio for ion was a total of est figure eer regions.

ulation endency ratio0‐14 and the ainst the ation. A low atio indicatesoung people n the near

t the Madison 27.1 percentw, but lowestand an ing birth totapotential evel workers

egion or the 65+ 3 percent the16.5 percent

18

niittiieess

C

R

C

C

R

o

s

n t t

l

e .

2008‐20098

Source: U

Sourc

Madison WI R

Lincoln NE R

Columbus OH R

Salem OR R

Columbia SC R

Richmond VA R

17. %

Madison R

Lincoln NE R

olumbus OH R

Salem OR R

Columbia SC R

Richmond VA R

Peer Av

18. Age

0‐14

9 STATE OF THE

US Census, Popu

ce: US Census, P

Region

Region

Region

Region

Region

Region

WI

US

Population

Region

Region

Region

Region

Region

Region

erage

Dependenc

4 Child Depend

E MADISON RE

lation Estimates

Population Estim

4

Change ‐ 20

27.1

28.6

31.0

27.7

28.9

28.6

29.0

cy Ratio ‐ Ag

dency 65+

EGION REPORT

s, 2000 to 2007

mates, 2006

7.

7.0

4.06

5.47

000 to 2007

16.5

17.0

14.

19.5

13.8

16.5

16.1

ges 0‐14 & 6

+ Dependency

T

.15

03

7.68

7.79

9.34

9.16

0

6

5

1

5+

y

Madi

Linc

Columb

Sal

Colum

Richmo

1

0.001.002.003.004.005.006.007.008.009.0010.00

Source: U

son WI Region

oln NE Region

bus OH Region

lem OR Region

mbia SC Region

ond VA Region

WI

US

19. Total Vio

3.48

8.6

00000000000

20. Local G

Total

Schoo

Specia

Source

US Census, Local

n

n

n

n

n

I

S

olent and ProResidents

2

1.892

Government

Local Govts. Pe

ol Districts per 0

al Districts per

19

e:

Governments, 2

29.

28.

operty Crims ‐ 2005

2.64

0.94

ts per 10,00

er 10,000

0‐19 Ages oer

10,000

2008‐20099

2002

.0

49

47.4

38.7

4

37.0

e per 1000

0.55

3.86

00 ‐ 2002

10,000

9 STATE OF THE

LLiiffee

9.2

51.8

52.6

4

6

E MADISON RE

iinn oouurr CC

Our communsafe places foproperty andand cost‐effegovernments

Lowestcapita

2nd Higtotal lounits

Local governan interestinand includes villages, schospecial districsewer, and w The Madisonreflects the logovernment doubt contribof life. The questionwhether the comes at a pwhether we efforts to shasome case comakes sense governments

EGION REPORT

CCoommmmuu

nities need toor both peopd we need accective local s and schools

t crime rate p

hest numberocal governm

ments per cag measure ofall cities, tow

ool districts, acts such as firwater.

n Region’s ranong history oin Wisconsin butes to our q

n can be askedincreased accrice and as a have seen recare services aonsolidate wh for local s.

T

uunniittiieess

o be le and cessible

.

er

of ent

pita is f access wns, and re,

nk at 2nd f local and no quality

d cess result, cent and in here it

LLiiffee oonn

How we gethe other ithan ever aour region

While the be more omore denswe can celdrive less afor ways tomiles trave

Highbikin

2nd lotravemor

Dailyhas dfrom

Most transfound in thwhich is noso is minimlook forwafor new m

Vehicle Miwas not repeer regiohere for th

A positive regional Vthe same pgrowth.

nn tthhee MM

et from one pis more impoand will help in the future

Midwest mayf a car culturesely populateebrate our efand continue o reduce our eled (VMT).

est percent wng to work

owest perceneling 30 minue to work

y vehicle miledecreased sligm 2000 to 200

sportation dahe decennial ow eight yearmally useful toard to the 201eaningful dat

iles Traveled eadily availablns but is preshe Madison R

trend is that MT is not incpace as our p

MMoovvee

place to rtant define e.

y always e than d regions, fforts to to look vehicle

walking or

nt utes or

s traveled ghtly 07

ata is census rs old and o us. We 10 Census ta.

(VMT) le for sented egion.

the reasing at opulation

20

Madi

Linc

Columb

Sal

Colum

Richmo

Madi

Linc

Columb

Sal

Colum

Richmo

2008‐20090

Source: U

So

Source: Wi

son WI Region

coln NE Region

bus OH Region

lem OR Region

mbia SC Region

ond VA Region

WI

US

21. Popu

son WI Region

coln NE Region

bus OH Region

lem OR Region

mbia SC Region

ond VA Region

WI

US

22. Trave

2007

2000

Dap

9 STATE OF THE

US Census, Mean

urce: US Census

isconsin DepartmUS Census Popu

0.0% 2.0%

n

n

n

n

n

n

I

S

ulation Bike/

n

n

n

n

n

n

I

S

ling Over 30

23. Madisaily Vehicle per Capita ‐2

E MADISON RE

ns of Transporta

s, Travel Time, 20

ment of Transpoulation Estimate

4.0% 6.0

/Walk to Wo

14.9%

0 mins to Wo

30.8

son RegionMiles Travel2000 and 200

EGION REPORT

tion, 2000

000

ortation and s

0% 8.0%

ork ‐ 2000

22.1%

28.7

25.3%

3

22.4%

ork ‐ 2000

31.6

led 07

T

Bike

Walk

7%

31.4%

32.7%

33.4%

Source: US

Source: US

Mad

Lin

Colum

Sale

Colum

Richmo

Mad

Lin

Colum

Sale

Colum

Richmo

2

S Department of

S Department of

ison WI Region

coln NE Region

mbus OH Region

em OR Region

mbia SC Region

ond VA Region

WI

US

24. Traffic Fa

ison WI Region

coln NE Region

mbus OH Region

em OR Region

mbia SC Region

ond VA Region

WI

US

25. Alcohol

f Transportation2000 and

f Transportation2000 and

n

n

n

n

n

n

S

atalities per

n

n

n

n

n

n

S

Impaired Dr2000 an

21

n, Fatality Analys2007

n, Fatality Analys2007

5.7

8

7.

5.1

5.9

7.4

7.3

6.3

6.6

6.6

4.0

6.0

6.7

6.8

r 1000 ‐ 2000

30.

24.6%

26.5%

24.5%

29.7

3

25.6%

32

29.4

22.4%

26.1%

28.1%

26.4%

27.6%

25.9%

rivers in Fatand 2007

2008‐20091

sis Reporting Sys

sis Reporting Sys

.0

10.8

.8

4

3

9.8

0 and 2007

.8%

%

46.0%

7%

34.6%

2.2%

4%

%

%

%

%

%

al Crashes ‐

9 STATE OF THE

stem,

stem,

2000

2007

2000

2007

Wro

Ato

TMWmort

Snpc

Faiwr

E MADISON RE

LLiiffee

While we areregion, safetyof quality of l

A recent induthat 77 perceoccur within

2nd loweper 100our pop7.7% fr

2nd highalcoholfatal craslightly with sli2007

The majority Madison RegiWhile there ismade on moroptions, it is lremain the mtransportatio

Safety on ournot only for dpassengers incyclists and p

Further reseaas well as tracincrease in otwill be includreports.

EGION REPORT

oonn tthhee

on the movey is a key indicife.

ustry survey sent of acciden15 miles of ho

est traffic fata00 in 2007 thopulation grewom 2000 to 2

hest percent o impaired driashes amongbehind WI, aght reduction

of people in tion travel by s progress bere mass transikely this will

major mode ofon.

r roads is impdrivers and n cars but for pedestrians as

arch of these cking the potther transit oped in future

T

MMoovvee

e in our cator

howed nts ome.

alities ough w by 2007

of vers in g peers, and n in

the car. eing it f

ortant,

s well.

issues ential ptions

AA HHeeaa

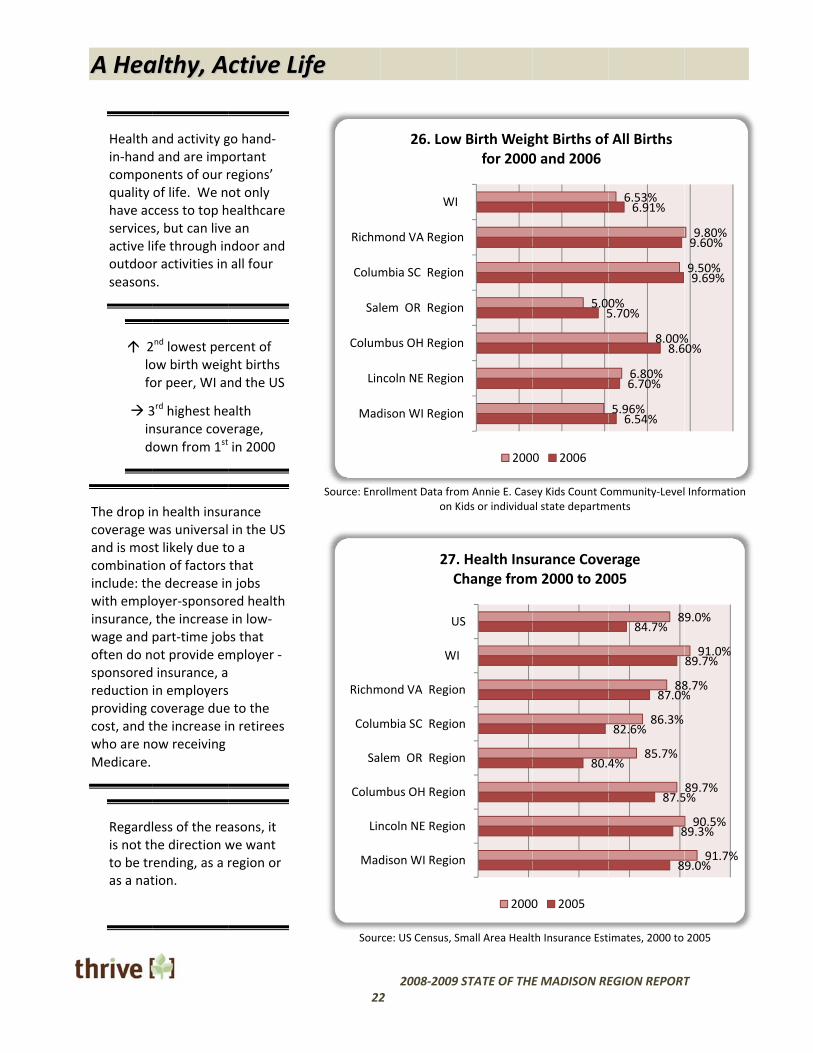

Health in‐handcomponquality have acservicesactive lioutdooseasons

2lofo

3ind

The drop icoverage wand is moscombinatioinclude: thwith emploinsurance,wage and often do nsponsoredreduction providing ccost, and twho are noMedicare.

Regardlis not thto be tras a nat

aalltthhyy,, AA

and activity gd and are impnents of our rof life. We nccess to top hs, but can liveife through inr activities in s.

2nd lowest perow birth weigor peer, WI an

3rd highest hensurance coveown from 1st

n health insuwas universalst likely due toon of factors he decrease inoyer‐sponsor the increasepart‐time jobot provide emd insurance, ain employerscoverage duethe increase iow receiving

less of the reahe direction wrending, as a rtion.

ccttiivvee LLiiff

go hand‐ortant regions’ ot only healthcare e an ndoor and all four

rcent of ght births nd the US

alth erage, in 2000

rance in the US o a that n jobs red health in low‐bs that mployer ‐ e to the n retirees

asons, it we want region or

22

iiffee

Source: Enro

Sour

Mad

Lin

Colum

Sal

Colum

Richm

Mad

Lin

Colum

Sa

Colu

Richm

2008‐20092

ollment Data froon K

rce: US Census, S

dison WI Regio

ncoln NE Regio

mbus OH Regio

lem OR Regio

mbia SC Regio

mond VA Regio

WI

26. Low

dison WI Regio

ncoln NE Regio

mbus OH Regio

lem OR Regio

mbia SC Regio

mond VA Regio

W

U

27C

9 STATE OF THE

om Annie E. CaseKids or individua

Small Area Healt

on

on

on

on

on

on

I

w Birth Weigfor 2000

200

on

on

on

on

on

on

I

US

. Health InsuChange from

2000

E MADISON RE

ey Kids Count Coal state departm

th Insurance Est

55.0

ght Births of0 and 2006

0 2006

80.4

urance Covem 2000 to 20

0 2005

EGION REPORT

ommunity‐Levelments

imates, 2000 to

6.54%

6.70%

8.6

5.70%

6.91%

5.96%

6.80%

8.00%

0%

6.53%

f All Births

8

8

87.5

4%

82.6%

87.0%

84.7%

85.7%

86.3%

88

8

erage 005

T

Information

2005

60%

9.69%

9.60%

%

9.50%

9.80%

9.0%

89.3%

5%

%

89.7%

91.7%

90.5%

89.7%

8.7%

91.0%

9.0%

S

So

Madi

Linc

Colum

Sale

Colum

Richmo

Mad

Lin

Colum

Sale

Colum

Richmo

Mad

Linc

Colum

Sale

Colum

Richm

Source US Comm

Source: EP

ource: National

ison WI Region

coln NE Region

bus OH Region

em OR Region

mbia SC Region

ond VA Region

W

US

28. Fitness/

ison WI Region

coln NE Region

mbus OH Region

em OR Region

mbia SC Region

ond VA Region

29. Air QSensitive &

ison WI Region

coln NE Region

bus OH Region

em OR Region

mbia SC Region

ond VA Region

30.

Rails to Trai

merce, Bureau o

PA Air Quality In

and State Park,

n

n

n

n

n

n

I

S

/Sports Cent

0

13

0

n

n

n

n

n

n

uality ‐ # Un& All Group

0 10

n

n

n

n

n

n

Special Outd

ils Nationa

23

of Economic Ana

ndex, 2000 and 2

and Rails to Tra

ters per 100

34

21

25

34

23

37

32

nhealthy Dayps ‐ 2000 and

20

door Places

al Parks St

2008‐20093

lysis, 2006

2007

ils websites

7.2

8.3

8.9

9.7

9.8

8.0

10.0

9.7

0 ‐ 2006

53

48

ys for d 2007

200

200

30 4

tate Parks

9 STATE OF THE

AA

0

00

07

40

Inseq

Trra

Tgotm

ScwMaaaec

E MADISON RE

AA HHeeaalltthh

n addition to ervices, an acenhances our quality of life.

The region abesources andound indoor activities.

Lowest centers this perentrepreopportu

3rd higheincreasequality d

3rd high“specialnationawithin e

There are magauge our acoptions and wo look for mmeasures in

Special outdochosen as a wwhat is uniquMadison Regalso work to additional spand county pestablish a pacapita pictur

EGION REPORT

hhyy AAccttiivv

healthcare ctive lifestyle overall healt

ounds in natud access to yeand outdoor

number of fiper capita, thhaps presenteneurial unity

est number ae of unhealthdays

hest number o places” – tral and state paeasy drive dist

any ways to ctivity levels we will cont

meaningful this categor

oor places wway to look aue to the gion but we wcatalogue

paces such asparks in ordeark acres pee of the regi

T

vvee LLiiffee

h and

ural ar‐

tness hough s an

nd y air

of ails, arks tance.

and tinue

ry.

was at

will

s city er to er ion.

2008‐2009 STATE OF THE MADISON REGION REPORT 24

RReeggiioonnaall MMaappss

2008‐2009 STATE OF THE MADISON REGION REPORT 25

RReeggiioonnaall MMaappss

2008‐2009 STATE OF THE MADISON REGION REPORT 26

AAddddiittiioonnaall RReeppoorrttss PPllaannnneedd ffoorr 22000099

State of the Madison Region – Monthly Insights focused on further exploring the individual metrics and what regional experts think they mean for the Madison Region

o One of the early 2009 features will explore race and ethnicity in the region Sector Snapshots that will help us further understand the targeted sectors of Agriculture, Biotechnology and Healthcare and how they each compare against a unique set of peer regions

Preliminary planning is underway for a mid‐year Regional Innovations report that will explore how the Madison Region is doing on measures related to entrepreneurism, patents, research funding, etc.

Receive the monthly Thrive Newsletter to get the latest information about the above reports and other regional news. Sign up from any page on our website: www.thrivehere.org

2008‐2009 STATE OF THE MADISON REGION REPORT 27

2008‐2009 STATE OF THE MADISON REGION REPORT 28

Thrive ©Madison Region Economic Development Enterprise

615 East Washington Avenue Madison, WI 53701 (608) 443‐1960

[email protected] www.thrivehere.org