111 iii ii1 1lllll 1lll1t1 ll1 !li · ad-a244 111 iii ii1 1lllll 1lll1t1 ll1 670 ... the purpose of...

TRANSCRIPT

AD-A244 670 "2 )111 III II1 1lllll 1lll1t1 ll1 !liINAVAL rOSTGRADUATE SCHOOL

Monterey, California

ALECTI:

-AN24319

92-01590

THESISAVIATION DEPOT LEVEL REPAIRABLE CARCASS TRACKINGAND BILLING: THE EFFECT OF THE TWO PRICE SYSTEM ON

BUDGETING AND FLYING HOUR COST REPORTING

by

Carl Stephen Staggs

December, 1991

Thesis Advisor: Richard B. Doyle

Approved for public release; distribution is unlimited

U'1.

UnclassifiedSECURITY CLASSIFICATION OF THIS PAGE

REPORT DOCUMENTATION PAGE1 a. REPORT SECURITY CLASSIFICATION l b. RESTRICTIVE MARKINGSUnclassified

2a SECURITY CLASSIFICATION AUTHORITY 3 DISTRIBUTION/AVAILABILITY OF REPORTApproved fbr public release; distribution is wilimited.

2b. DECLASSIFICATION/DOWNGRADING SCHEDULE

4. PERFORMING ORGANIZATION REPORT NUMBER(S) S. MONITORING ORGANIZATION REPORT NUMBER(S)

6a. NAME OF PERFORMING ORGANIZATION 6b. OFFICE SYMBOL 7a. NAME OF MONITORING ORGANIZATIONNaval Postgraduate School (If applicable) Naval Postgraduate School

55

6c ADDRESS (City, State, and ZIP Code) 7b ADDRESS (City, State, and ZIP Code)Monterey, CA 93943-5000 Monterey, CA 93943-5000

8a NAME OF FUNDING/SPONSORING 8b. OFFICE SYMBOL 9. PROCUREMENT INSTRUMENT IDENTIFICATION NUMBERORGANIZATION (If applicable)

8c ADDRESS (City, State, and ZIP Code) 10 SOURCE OF FUNDING NUMBERSProgram klement No Project No Task No Work Unit Acce~sson

Number

11 TITLE (Include Security Classification)Aviation Depot Level Repairable Carcass Tracking and Billipg: The Effect of the Two Price System on Budgeting and Flying Hour CostReporting

12 PERSONAL AUTHOR(S)

13a. TYPE OF REPORT 13b- TIME COVERED 14. DATE OF REPORT (year, month, day) 15. PAGE COUNTMaster's Thesis From To December, 1991 95

16. SUPPLEMENTARY NOTATIONThe views expressed in this thesis are those of the author and do not reflect the official policy or position of the Department of Defense or the U.S.Government.17 COSATI CODES 18. SUBJECT TERMS (continue on reverse if necessary and identify by block number)

FIELD GROUP SUBGROUP AVDLR, Aviation Depot Level Repairable, Carcass Tracking, Navy Stock Fund,Flying Hour Cost Reporting

19. ABSTRACT (continue on reverse if necessary and identify by block number)

The purpose of this thesis is to examine problems with the Navy's two price aviation depot level repairable (AVDLRI billing and trackingsystem. These problems include fluctuations in post fiscal year obligation levels and the distortion of flying hour cost reporting due toAVDLR carcass charges and credits received during the expenditure availability periods of the Operations and Maintenance, Navyappropriations used to fund AVDLR purchases. Fluctuations in post fiscal year obligation levels can potentially result in the unintentionaloverobligation of funds. Distortions in flying hour costs result in inaccurate flying hour program budget requests. This thesis also exploresthe feasibility of a two price/one bill system of charging for AVDLRs which has often been proposed as a solution to the problems mentionedabove. The conclusion reached is that the problems have diminished significantly over time. The two price billing system remains the bestmeans of maintaining system visibility of AVDLR carcasses and holding down overall AVDLR costs.

20 DISTRIBUTION/AVAILABILITY OF ABSTRACT 21 ABSTRACT SECURITY CLASSIFICATIONUNCLASSIFIMDRINt IMIOLD '3AME AS REPORT DTIC USERS Unclassified

22a NAME OF RESPONSIBLE INDIVIDUAL 22b TELEPHONE (Include Area code) 22c OFFICE SYMBOLRichard B. Doyle (4081649-3302 AS/DYDO FORM 1473. 84 MAR 83 APR edition may be used until exhausted SECURITY CLASSIFICATION OF THIS PAGE

All other editiwr art 1u,;cte unclassified

Unclassified

Approved for public release; distribution is unlimited

Aviation Depot Level Repairable Carcass Tracking andBilling: The Effect of the Two Price System on

Budgeting and Flying Hour Cost Reporting

by

Carl Stephen StaggsLieutenant Commander, United States NavyB.S., University of South Carolina, 1979

Submitted in partial fulfillment of therequirements for the degree of

MASTER OF SCIENCE IN MANAGEMENT

from the

NAVAL POSTGRADUATE SCHOOLDecember 1991

Author: - ___________

Carl, Stephen/'taggs

Rihard B. Doyle, Thss-Advisor

Paul M. Carrick, Second Reader

David R. ip le, rman,Department of Administrat e Sciences

ii

ABSTRACT

The purpose of this thesis is to examine problems with

the Navy's two price aviation depot level repairable (AVDLR)

billing and tracking system. These problems include

fluctuations in post fiscal year obligation levels and the

distortion of flying hour cost reporting due to AVDLR carcass

charges and credits received during the expenditure

availability periods of the Operations and Maintenance, Navy

appropriations used to fund AVDLR purchases. Fluctuations in

post fiscal year obligation levels can potentially result in

the unintentional over obligation of funds. Distortions in

flying hour costs result in inaccurate flying hour program

budget requests. This thesis also explores the feasibility of

a two price/one bill system of charging for AVDLRs which has

often been proposed as a solution to the problems mentioned

above. The conclusion reached is that the problems with the

two price system have diminished significantly over time. The

two price billing system remains the best means of maintaining

system visibility of AVDLR carcasses and holding down overall

AVDLR costs.

Aeoesslon For

NTIS GRA&IDTIC TAB 0UnwnnouncedJultific~tlo"

Distributitonj/.AvN1 ,l ,t: Code%

iii Dist Spoo ial

TABLE OF CONTENTS

I. INTRODUCTION ................... 1

A. DESCRIPTION OF THE PROBLEMS ASSOCIATED WITH THE

TWO PRICE BILLING SYSTEM ...... ........... 1

B. ORIGIN OF NAVY STOCK FUNDING OF AVDLRS . . .. 2

C. EXPLANATION OF THE TWO PRICE AVDLR BILLING

SYSTEM ........... .................... 7

D. SUMMARY .......... .................... 10

II. AVDLR OPERATIONAL FUNDING .... ............. 13

A. INTRODUCTION ...... ................. 13

B. THE FLOW OF FUNDS ...... ............... 13

C. LIMITATIONS ON OPERATING FUNDS .. ........ 15

D. THE TRANSITION FROM NAVY STOCK FUND TO END USE

MANAGEMENT OF AVDLRS .... ............. 21

E. AVIATION SUPPORT ACTIVITY STRUCTURE ...... .. 22

F. THE POINT OF SALE ...... ............... 24

G. SECONDARY EFFECTS OF END USE OWNERSHIP . . .. 26

III. THE RELATIONSHIP BETWEEN ASO'S AVDLR CARCASS

TRACKING AND BILLING SYSTEM AND THE NAVY'S FLYING

HOUR PROGRAM ........ ................... 30

iv

A. THE AVIATION SUPPLY OFFICE'S CARCASS TRACKING

PROGRAM ........ .................... 30

B. THE FLYING HOUR PROGRAM ... ............ 38

IV. PROBLEMS WITH POST FISCAL YEAR BUDGET MANAGEMENT AND

FLYING HOUR COST REPORTING DUE THE TWO PRICE SYSTEM OF

BILLING FOR AVDIRS ...... ................ 43

A. SIZE OF THE AVDLR BUDGET ... ........... 43

B. POST FISCAL YEAR EFFECTS ON TYPE COMMANDER

BUDGETS ........ .................... 44

C. DISTORTION OF FLYING HOUR PROGRAM COSTS . . .. 52

D. LOST USE OF FUNDS DUE TO CARCASS CHARGES FOR

"PAPER LOSSES" ....... ................ 55

E. SUMMARY ........ .................... 58

V. EXAMINATION OF A TWO PRICE/ONE BILL SYSTEM OF CHARGING

FOR AVDLRS ........ .................... 59

A. THE TWO PRICE/ONE BILL PROPOSAL ......... 59

B. MECHANICS OF THE TWO PRICE/ONE BILL SYSTEM . 60

C. ELIMINATION OF POST FISCAL YEAR SLDGET MANAGEMENT

UNCERTAINTY ....... .................. 61

D. REMOVAL OF DISTORTION IN FLYING HOUR COST

REPORTING AND BUDGET PREPARATION ESTIMATES . 63

E. REDUCTION OF PERSONNEL RESOURCES REQUIRED TO

CORRECT ERRONEOUS CARCASS CHARGES ........ . 65

v

F. ELIMINATION OF THE FINANCIAL INCENTIVE TO MAKE

AVDLR CARCASS TURN INS..............69

G. LOSS OF FLYING HOUR PROGRAM DUE TO ADMINISTRATIVE

OBLIGATION OF FUNDS................73

VI. CONCLUSIONS AND RECOMMENDATIONS............74

A. CONCLUSIONS....................74

B. RECOMMENDATIONS...................77

C. RECOMMENDATIONS FOR FURTHER STUDY..........79

APPENDIX.........................81

LIST OF REFERENCES....................83

BIBLIOGRAPHY.......................85

INITIAL DISTRIBUTION LIST.................86

vi

LIST OF FIGURES

Figure I-1 NSF Revolving Fund Operations ... ....... 6

Figure II-I O&M,N Flow of Funds .... ............ . 16

Figure 11-2 Life of an O&M,M Approximation Account . . 19

Figure 11-3 Local Issue, Repair and Replenishment . . . 25

Figure III-1 Carcass Tracking Follow Up and Billing

Parameters ....... .................... 39

Figure IV-1 COMNAVAIRPAC Outstanding Carcass Charge

Levels ........ ...................... . 47

vii

LIST OF TABLES

Table III-1 Carcass Tracking Synopsis ............ 36

Table IV-l COMNAVAIRPAC AVDLR Expenditures.........44

Table IV-2 COMNAVAIRPAC Outstanding Carcass Changes . 54

Table V-1 COMNAVAIRPAC AVDLR Carcass Tracking

Performance.....................71

viii

I. INTRODUCTION

A. DESCRIPTION OF THE PROBLEMS ASSOCIATED WITH THE TWO PRICE

BILLING SYSTEM

Aviation Depot Level Repairables (AVDLR) are aircraft

components or aviation related components which can be

repaired to make unserviceable aircraft or aviation related

equipment function properly. AVDLRs are typically high cost

and/or long procurement lead time items. Because of these

characteristics, significant economies can be achieved by

repairing these items rather than discarding them when they

become unserviceable. [Ref. l:p. 1-1]

AVDLRs are managed centrally by the Aviation Supply Office

(ASO) in Philadelphia, Pennsylvania as part of the Navy Stock

Fund (NSF) or as "end use" inventories held by aviation

support activities. ASO uses a two price billing system to

charge user activities for AVDLRs issued from the NSF. The

price an activity is charged for each AVDLR it uses is

dependent on whether or not the activity returns an

unserviceable component (carcass) in exchange for each NSF

AVDLR issue. Net price is charged for an AVDLR when a carcass

turn in is made. Standard price, usually significantly higher

1

than net price, is the cost to an activity if no carcass turn

in is made.

ASO's use of the two price AVDLR billing system has

created several problems, or potential problems, at both the

aviation support activity and aviation type commander levels.

These problems include the distortion of costs associated with

flying hour programs, possible post fiscal year budget

management problems, and at the very least an increased

workload due to the carcass tracking and budget management

requirements imposed by the system.

B. ORIGIN OF NAVY STOCK FUNDING OF AVDLRS

Prior to 1 April 1981, all Depot Level Repairable (DLR)

items, both aviation and non-aviation, were procured for the

Navy Supply System with procurement appropriation funding and

held in the Appropriation Purchases Account (APA) inventory.

The appropriations used to procure AVDLRs included the

Aircraft Procurement, Navy (APN), Weapons Procurement, Navy

(WPN), and Other Procurement, Navy (OPN) appropriations.

These are fully funded investment type appropriations with a

three year obligational availability period. "Fully funded",

within this context, means that dollars are specifically

appropriated to construct a specific number of units. [Ref.

2:p. A-17]

2

Repair of DLRs was financed with funds from the Operations

and Maintenance, Navy (O&M,N) appropriation, an annual,

expense type appropriation. Issues of DLRs were made at no

cost to the customer. Procurement and repair management were

done centrally by ASO and the Ships Parts Control Center

(SPCC) in Mechanicsburg, Pennsylvania, the Inventory Control

Points (ICP) for AVDLRs and non-aviation DLRs respectively.

Management and procurement of DLRs was difficult for the

ICPs in terms of material availability and responsiveness to

fleet requirements. This was due to the use of various

appropriations for financing procurement and repair of DLRs as

well as the long budget lead times required for the

procurement appropriations. The difficulties associated with

these separate and inflexible funding mechanisms caused the

Chief of Naval Operations (CNO) to direct a study to consider

and evaluate alternative methods of financing DLRs. The study

concluded that the Navy Stock Fund (NSF) was a practical and

improved method of financing the procurement and repair of

DLRs. (Ref. 3:p. 1]

The Navy began to test stock funding of non-aviation DLRs,

i.e., selected SPCC managed DLRs, on 1 April 1981. The test

period was to have concluded on 30 September 1983. Because of

significant improvements in supply availability of non-

aviation DLRs, the CNO authorized the Chief of Naval Material

3

to develop a plan of action and milestones for a 1 April 1985

extension of NSF financing to AVDLRs managed by ASO. The main

objectives to be accomplished by NSF financing were [Ref. 4:p.

I-2-1]:

1. Improved supply system discipline resulting from thebuyer-seller relationship inherent in a stock fundedenvironment vice the XPA free issue system.

2. Increased financial flexibility due to the ability totrade off NSF procurement and repair during budgetexecution.

3. More accurate budget forecasting due to shorter stockfund lead times.

4. Improved material support responsiveness due to the stockfund's ability to respond to emergent requirements withoutreprogramming requirements/funds.

The NSF is a revolving fund with two primary assets - cash

and material. The cash is used to build up or maintain

material inventory through payment for repair of material at

repair depots and purchases of new items from vendors. When

material is issued to a customer, the NSF is reimbursed from

the customer's operating funds. The cash is then used to

replenish the NSF material inventory and the cycle is

repeated. In addition to cash generated by sales, the NSF has

two other basic sources of cash: transfers from other

Department of Defense (DOD) stock funds, and appropriated

transfers into the fund for specific purposes. Figure I-i

4

[Ref. 5:p. 101-6] is an illustration of the flow of funds and

material into and out of the NSF.

The Naval Supply Systems Command (NAVSUP) is responsible

for overall management of the NSF. The fund is split into

various categories of material, or budget projects, which are

assigned to Navy ICPs and retail offices for management. ASO

is the budget project manager for aviation consumables and

AVDLRs.

NSF material inventories are not stocked at the

controlling ICP. They are instead positioned at various stock

points as wholesale stocks owned by the ICP. Customer demands

are satisfied from these stocks and replenishments are usually

"pushed", or determined, by the ICP. Stock points carrying

wholesale AVDLRs include Naval Supply Centers and Naval Air

Stations. Ships not yet converted to end use management of

AVDLRs carry NSF owned retail AVDLR stocks. The main

difference between retail and wholesale is that retail

inventories are designated specifically to support the

activity carrying them while wholesale inventories are issued

to various activities as directed by ASO.

The conversion to NSF financing of AVDLRs helped to solve

several of the problems with AVDLR funding. Under the old APA

system, the use of investment type appropriations with three

year lead times for procurement caused problems with

5

( CASH

VENDORS MATRIA

DEPOT ___________

RFI MATERIAL

SUPRTSERVICES

ArrmITOt

PHYSICAL LOSSES

6 OBSELESCENCE

SURCARGETRANSPORTATION

Figure 1-1 NSF Revolving Fund Operations

6

forecasting supply system requirements. In addition, O&M,N

funds, an expense type appropriation, were used for

transportation and repair of AVDLRs. With the conversion to

NSF financing, purchases and repairs of AVDLRs are all made

with NSF funds as required. Financial inflexibility and the

need for rigid long run forecasting have been eliminated.

C. EXPLANATION OF THE TWO PRICE AVDLR BILLING SYSTEM

Under the APA "free issue" system of AVDLR management,

problems developed with aircraft squadrons stockpiling AVDLRs.

There were no financial incentives to ensure every AVDLR issue

to a squadron was matched with a turn-in of an inoperable

AVDLR (carcass). In addition, there was no effective carcass

tracking system to keep track of not ready for issue (NRFI)

carcasses returned or not returned to the supply system.

Although individual squadrons were attempting to maximize

their own readiness by hoarding spare AVDLRs, both ready for

issue (RFI) and NRFI, this behavior was extremely

dysfunctional in that it led to decreased readiness Navy wide.

By holding scarce RFI AVDLRs as spares outside of the supply

system, squadrons were keeping material from units that needed

it. The NRFI equipment not being returned to the supply

system was not getting repaired, therefore depleting the

system inventory. This not only resulted in decreased

7

readiness, but greater expense for inventory replenishment as

well.

Upon conversion to NSF financing of AVDLRs on 1 April

1985, two primary mechanisms were implemented to enhance the

system wide availability of all assets and to ensure the

timely return of NRFI carcasses. The first, an upgraded

carcass tracking system, will be discussed in Chapter III.

The second was the use of a two price billing system for

AVDLRs.

Under NSF financing, users reimburse the stock fund for

AVDLRs with their operating funds, usually the user's share of

the annual O&M,N appropriation. At the point of sale from the

NSF, buyers normally provide the NSF with cash through

obligation of their O&M,N funds and a NRFI carcass to be

repaired at a designated depot repair facility (military or

civilian contractor). When a sale is accompanied by a NRFI

turn-in, the buyer is billed by ASO for the sale at net price.

Net price is basically the cost of repair of the NRFI AVDLR.

When a buyer does not provide a turn-in, in exchange for

an RFI AVDLR, it will be charged standard price for the sale.

Standard price is basically the price of purchasing a new item

for the NSF. There are factors other than just the cost of

repair or the vendor's price for a new item which figure into

8

the determination of net and standard prices for individual

AVDLRs.

The base AVDLR procurement and repair prices for standard

and net pricing, respectively, are determined annually by ASO

for each AVDLR. Surcharges to the AVDLR costs are calculated

annually by NAVSUP based on information provided by ASO.

These surcharges, one each for standard and net price, are

provided to ASO by NAVSUP as percentages to be applied across

the board to the procurement and repair costs of each AVDLR.

Surcharges include factors for inflation, inventory

obsolescence, transportation, physical inventory losses, price

stabilization, and the cost of supply operations at Naval

Supply Centers and Inventory Control Points. The price

stabilization factor is figured in to maintain the NSF at its

approved level. It compensates for the difference between

pricing assumptions made in the previous year's budget and the

actual costs incurred during the year [Ref. 2:p. G-6]. Net

price also includes factors for depot washout (irrepairable

carcasses) and carcass losses. The determination oL carcass

losses will be discussed in Chapter III.

The use of a two price system has two major effects.

First, it allows for NSF financial stability and AVDLR

inventory maintenance at prescribed levels by compensating the

NSF for any system losses of material caused by using

9

activities. Secondly, the use of the two price system

provides powerful financial incentives for buyers to make

timely one-for-one exchanges of NRFI AVDLRs for RFI material.

Net price is typically around 40 percent of standard price

for an AVDLR [Ref. 6:p. 35]. The difference between the two

prices is known as a carcass charge and can be in the hundreds

of thousands of dollars for some individual items. With

continually shrinking budgets, user activities can ill afford

to incur carcass charges by not making timely NRFI turn ins

when buying AVDLRs.

D. SW.R

The implementation of NSF, and subsequently end use,

financing of AVDLRs has been a success in terms of achieving

the CNO's objectives - improved supply system discipline,

increased financial flexibility, more accurate budget

forecasting, and improved material support responsiveness.

The two price billing system for AVDLRs used since the

implementation of NSF financing has however, led to problems,

or potential problems, of its own. As mentioned previously,

these problems include the distortion of flying hour cost

reporting, post fiscal year budget management difficulties,

and an increased workload imposed on aviation activities by

the two price system.

10

The primary cause of potential problems associated with

the two price billing system is the difference in timing

between ASO's carcass tracking and billing cycle for AVDLRs

and both the length of the appropriation from which AVDLR

operating funds are provided and the dates on which annual

flying hour cost reports are prepared. Chapters II and III

will provide background information which explains how these

timing differences arise. Chapter IV will discuss how such

timing differences can lead to problems at the aviation

support activity and type commander levels.

A possible solution to the difficulties associated with

the two price system of billing for AVDLRs is the use of a

single bill system. This solution has been proposed at

several levels in the aviation supply community during the

past few years. Chapter V will examine the theoretical

benefits and drawbacks of a type of single bill system, a two

price/one bill system, based on carcass tracking and billing

data gathered for the time period 1986 - 1990. Chapter VI

will develop a conclusion based on data and information

presented in Chapters IV and V.

The focus of this thesis will be on the effects of the two

price system of billing for AVDLRs at one major aviation type

commander, Commander U.S. Naval Air Forces, Pacific Fleet

(COMNAVAIRPAC). This is due primarily to the readily

11

available data at COMNAVAIRPAC and the need to restrict the

scope of the thesis. Explanations and examples will be

restricted mainly to routine stock replenishment requisitions

for the sake of simplicity.

12

II. AVDLR OPERATIONAL FUNDING

A. INTRODUCTION

Since the implementation of NSF financing of AVDLRs on 1

April 1985, customers have had to pay for the consumption of

AVDLRs with their operating funds. Consumption includes

carcass charges, whether anticipated or not, levied against

customers for failing to turn in NRFI AVDLR carcasses as

required. Sections B and C of this chapter will detail the

type and source of operating funds used by aviation support

activities to pay for AVDLRs as well as limitations on these

funds. Sections D through G of the chapter will examine the

differences between NSF and end use ownership of AVDLR

inventories at the aviation support activity level and how

they affect operational funding.

B. TEE FLOW OF FUNDS

AVDLR funds are part of the larger pot of funds provided

to the Navy through the annual Operations and Maintenance,

Navy (O&MN) appropriation. Congress sets the level of O&M,N

funds via annual defense authorization and appropriation

bills. After the final defense appropriation act is signed by

the president, it is implemented through the issuance of an

13

Appropriation Warrant by the Treasury Department which is

countersigned by the head of the General Accounting Office.

The Appropriation Warrant is basically an interpretation of

appropriations legislation. The purpose of this process is to

ensure agreement between the executive and legislative

branches as to how the appropriation is to be executed. [Ref.

2:p. D-4]

After the Appropriation Warrant has been issued and

countersigned, the Office of Management and Budget (0MB)

apportions funds to the Department of Defense (DoD) which in

turn apportions funds to the services. Apportionment is the

time phased release of funds to subordinate activities for

budget execution. Annual appropriations such as the O&M,N

appropriation are apportioned on a quarterly basis.

Funds apportioned to the Department of the Navy are

allocated by the Secretary of the Navy to the Chief of Naval

Operations (CNO) and suballocated by the CNO to the major

claimants. The major claimant for COMNAVAIRPAC is the

Commander in Chief, U. S. Pacific Fleet (CINCPACFLT).

Allocation is the internal distribution of funds apportioned

to the Navy.

Major claimants provide O&M,N funds to type commanders in

the form of expense limitations. Type commanders then pass

funds to aviation support activities in the form of operating

14

budgets or operating targets. Operating budgets are legal

limitations on the amount of money that can be spent while

operating targets are administrative limitations. Typically,

Naval Air Stations receive operating budgets and operating

forces such as ships receive operating targets. Figure II-1

is an illustration of the flow of O&M,N funds from Congress to

the end users of the funds operating under COMNAVAIRPAC. [Ref.

2:p. D-7]

C. LIMITATIONS ON OPERATING FUNDS

The O&M,N appropriation has a one year obligational

availability period. As part of the O&M,N appropriation,

AVDLR funds may only be obligated for new purchases during the

fiscal year for which they are appropriated. Once the

obligational availability period for the appropriation ends,

or expires, the expenditure availability period of two years

begins.

During the expenditure availability period, additional

funds beyond the obligation level achieved during the

obligational authority period may be disbursed only for price

increases and unpreceded disbursements. Price increases apply

only to requisitions originally obligated during the

obligational authority period. Unpreceded disbursements are

commitments made during the obligational authority period for

• 15

II APP- tloF

T.- ,e

NA A

A~ ISrATIaONo

Figure Il-I OM Flw f Fnd

(MADQCL, 1647

which an obligation was never recorded. During the

expenditure availability period, detailed accounting records

must be maintained. As a result, activities must maintain

three years of accounting records at any one time - the

current year and two prior fiscal years.

At the end of the expenditure availability period, the

unexpended balance of the appropriation lapses to either the

successor "M" account or successor merged surplus account.

The "M" account contains money obligated by activities, but

never expended because a bill from a supplier was never

processed against the obligation. The merged surplus account

contains excess funds never obligated or expended. Both

accounts are managed by the Treasury Department.

Recent legislation has begun the phasing out of the

successor accounts and requires that DoD maintain detailed

accounting records of expired appropriations for five years.

This legislation doubles the amount of O&M,N accounting

records to be maintained by type commanders and their

subordinate activities from chree to six years. The increase

in accounting records may cause problems of its own by

straining the capacity of existing automated accounting

systems.

In any event, the elimination of the successor accounts

will not cure the specific problems caused by the two price

17

AVDLR billing system which are addressed in this thesis -

distortion of flying hour cost reporting and post fiscal year

budget management difficulties. If anything, post fiscal year

budget management will become more difficult as the

maintenance of accounting records for expired appropriations

is extended from two to five years. Because the research for

this thesis is concentrated primarily on the time period 1986

- 1990, the remainder of this thesis will be based on the

assumption of a two year expenditure availability period and

the existence of the successor accounts. The life cycle of an

O&M,N appropriation is outlined in Figure 11-2 [Ref. 2:p. A-

20].

In addition to the time limits of an annual appropriation,

O&M,N funds have two other primary limitations - purpose and

dollar amount. Title 31, U.S. Code, Section 1301 (a) prohibits

the use of funds for purposes other than those for which they

were intended. This is not usually a problem with AVDLR

funds.

Title 31, U.S. Code, Section 1517 prohibits the obligation

of funds in excess of the amount available in an appropriation

or any subdivision thereof. The limitation applies to the

obligational and expenditure availability periods of an

appropriation. Over obligation of AVDLR funds is a

potentially more serious problem at the type commander and

18

1 OCT1I9XO 30 SEP 19M1 30SEP 19X3

OBUIGATIONAL EXPENDITURE SUCCESSORAVAlLABI~LrY AVAILABI~LY sPERIOD PERIOD ACCOUNT

(1 YEAR) (2 YEARS) (UNLIMITED)

APPROPRIATION APPRO PRIATIONEXPIRES I LAPSES

OPEN APPROPRIATION ACCOUNT CLOSED APPROPRIATION ACCOUNT

Figure 11-2 Life of an O&M,N Appropriation Account

19

aviation support activity levels than is the misuse of AVDLR

funds.

Naval Air Stations with operating budgets have legal

responsibility for over obligation of funds under Section

1517. Type commanders such as COMNAVAIRPAC also have Section

1517 responsibility for their total expense limitation.

Activities which receive funds in the form of operating

targets do not have legal responsibility for the over

obligation of funds (responsibility is retained at the type

commander level); however the administrative limits of their

operating targets are considered binding.

As mentioned in Chapter I, the issue of timing is the

basis for the problems to be examined in this thesis. The

obligation and expenditure of AVDLR funds are limited by the

life of the O&M,N appropriation to which they belong. ASO's

carcass tracking and billing system has no time limitation, as

will be seen in Chapter III.

Carcass charges, also called carcass value bills, are

charged to the appropriation of the original transaction

requiring a carcass turn in regardless of whether the

appropriation's obligational availability period has expired

or not. Carcass charges may also be reversed after the

expiration of an appropriation's obligational availability

20

period. The difficulties caused by these post-fiscal year

actions will be detailed in Chapter IV.

D. THE TRANSITION FROM NAVY STOCK FUND TO END USE MANAGEMENT

OF AVDLRS

On 1 April 1986, Naval Air Station retail AVDLR

inventories were converted from NSF ownership to end use

ownership. Ships were scheduled for transition to end use

ownership on an activity phased basis commencing 1 August

1986. This transaction is largely complete, although there

are still a few ships such as the aircraft carrier USS Carl

Vinson (CVN 70) still operating under NSF ownership of AVDLRs.

The primary effect of the transition to end use AVDLR

ownership is to change the point of sale of AVDLRs leaving the

NSF. The specific differences in the points of sale under end

use and NSF AVDLR ownership are discussed later in this

chapter. There are also secondary effects/problems caused by

end use AVDLR ownership which have sparked a debate as to

whether to remain with end use or move back to NSF financed

retail AVDLR inventories. Although a thorough examination of

these problems is beyond the scope of this thesis, several

will be mentioned later in this chapter as they can affect

carcass tracking and budget management.

21

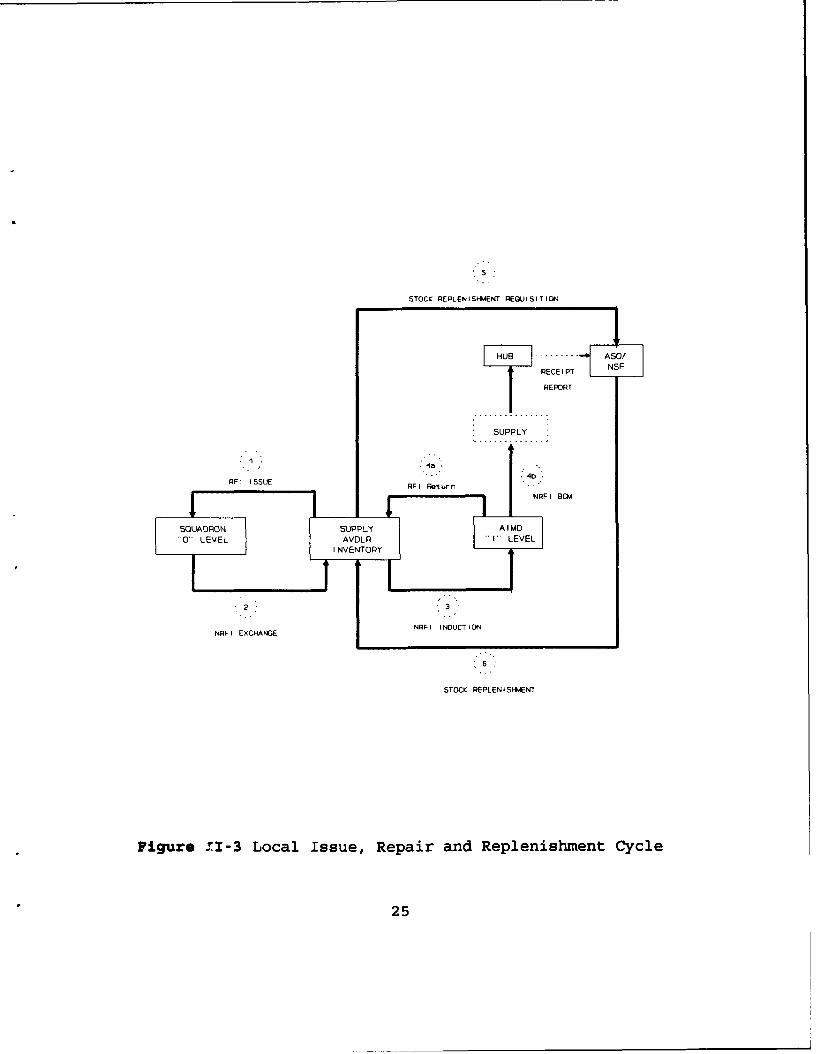

E. AVIATION SUPPORT ACTIVITY STRUCTURE

In order to explain how both NSF and end use ownership of

AVDLRs affect AVDLR billing and carcass tracking, the basic

structure of an aviation support activity must be understood.

A typical aviation support activity, whether afloat or ashore,

has among its departments, two which are dedicated primarily

to the support of aircraft squadrons - the Supply Department

and the Aircraft Intermediate Maintenance Department (AIMD).

These departments can support a wide or narrow range of

aircraft depending on the mission of a ship or station. Most

supporting activities support multiple squadrons which can be

either permanently or temporarily based at the activity.

The Supply Department maintains the local inventory of

AVDLRs based on a predetermined allowance list provided by

ASO. Although allowances are determined by ASO, local

activities usually negotiate individual AVDLR allowances with

ASO prior to the list being finalized. Each AVDLR issue to a

squadron is made in exchange for a not ready for issue (NRFI)

AVDLR which is inducted from Supply into AIMD for local

repair.

Supply (in conjunction with the comptroller at a shore

activity) is also responsible for the management of AVDLR

funds received from the activity's type commander. Squadrons

do not receive AVDLR funds, hence AVDLR issues are free to the

22

squadrons with the exception of providing a carcass turn in to

supply. At the point of sale of an AVDLR from the NSF, Supply

obligates a portion of its AVDLR funds to ASO to pay for the

item.

AIMD is an intermediate maintenance activity (IMA) which

performs local, or "I" level repair of AVDLRs. When a NRFI

AVDLR carcass is inducted for repair, AIMD either repairs the

item or determines that it is beyond the capability of

maintenance (BCI). If the item is repaired, it is returned to

Supply as ready for issue (RFI) and placed back into inventory

until requisitioned by a squadron. If the item is BCM'd,

Supply will ship the NRFI carcass to a central hub activity

which routes carcasses to the appropriate depot level repair

facilities. Supply will also requisition an inventory

replacement.

Squadron maintenance departments perform organizational,

or "0" level maintenance. Squadrons do not repair AVDLRs.

They are responsible for determining if an AVDLR is

inoperable, removing it from the aircraft, and replacing it

with an RFI part obtained from Supply. NRFI AVDLRs are turned

in to Supply when the RFI parts are requisitioned. In the

event a squadron does not have a NRFI AVDLR to turn in, a

survey or other documentation, such as for initial outfitting,

must accompany the requisition to supply. Th entire local

23

issue, repair, and replenishment cycle is illustrated in

Figure 11-3.

F. THE POINT OF SALE

Activities operating under NSF financing of local AVDLR

inventories do not actually own the retail AVDLRs held as part

of their allowance to support aircraft squadrons. This

material is owned by the NSF. The point of sale of an AVDLR

from the NSF occurs when a NRFI item is BCM'd by AIMD and not

returned to the local retail inventory (Figure II-3:point 4b).

The point of sale is also the point at which ASO initiates

carcass tracking. Because local inventories are owned by the

NSF, stock replenishment is free to the activity. Stock

replenishment is simply a transfer of goods within the NSF.

The conversion to end use ownership of local AVDLR

inventories brought about several changes in both AVDLR

billing and carcass tracking. The biggest change is the

change in the point of sale of an AVDLR from the NSF. Because

end use aviation support activities now own their retail AVDLR

inventories, they now obligate AVDLR funds when they

requisition AVDLRs from ASO for stock replenishment (Figure

II-3:point 5). End users are billed for AVDLRs when ASO

directs shipment of an item for stock replenishment. Carcass

24

STOCK REPLENIS-&ENT REQUISITION

HUB - -... ASO/

RECEIPT NSF

REPORT

RFI IXCHAUEERIRtr

STOCK

Q F

RELEIS9#.

2 25

tracking is also initiated at the point of the stock

replenishment requisition.

G. SECONDARY EFFECTS OF END USE OWNERSHIP

End use ownership of AVDLRs has disassociated the NSF from

the AIMD repair process. No AVDLR billing or carcass tracking

transactions take place until stock replenishment is

initiated. The customer must take into account its inventory

position and availability of operating funds before placing a

stock replenishment requisition.

On the surface, the difference between NSF and end use

financing of AVDLRs appears to be simply a matter of timing as

to the point of sale of an AVDLR from the NSF. However, there

are other effects. These have prompted CINCPACFLT and

CINCLANTFLT, the major claimants for COMNAVAIRPAC and

COMNAVAIRLANT, respectively, to recommend a return to NSF

financing of AVDLR inventories afloat [Ref s. 7 and 8]. An

AVDLR working group consisting of representatives from the

CNO's office, NAVSUP, both major claimants and type

commanders, and others was convened on 19 December 1990. The

purpose of the working group was to evaluate the major

claimants' recommendation, consider alternatives, and make a

recommendation to an AVDLR flag steering group based on a

cost/benefit analysis [Ref. 6].

26

Some of the major concerns behind the call for a return to

NSF financing of AVDLR inventories afloat include readiness,

flexibility in transferring AVDLR assets between units,

difficulties associated with end use accounting, and reduced

operating funds due to fleet financing of inventory and

shipment losses. In terms of readiness, advocates of NSF

financing point out that NSF funding allows spares to be

positioned where and when needed without regard to

fluctuations in operating budgets. On the other hand, annual

operating budget shortfalls can result in unfilled shortages

in end use AVDLR inventories, adversely affecting the level of

future material support an activity is able to provide. NSF

financing promotes readiness by allowing more efficient use of

scarce resources in that operating (O&M,N) dollars are used

only to finance consumption of AVDLRs while NSF dollars

finance lead times and inventories. [Ref. 7]

Difficulties with end use accounting and inflexibility in

transferring assets between units are related problems under

end use funding of AVDLR inventories. AVDLR assets are

routinely transferred between aviation activities as needed.

Transfers between NSF funded inventories are simply transfers

within the NSF itself and are easily handled by fleet

inventory and financial management systems. These systems are

unable to accommodate simple AVDLR movements between end use

27

units without extremely complex financial transactions. On

the whole, NSF funding of AVDLRs lends itself to simpler

financial management requirements.

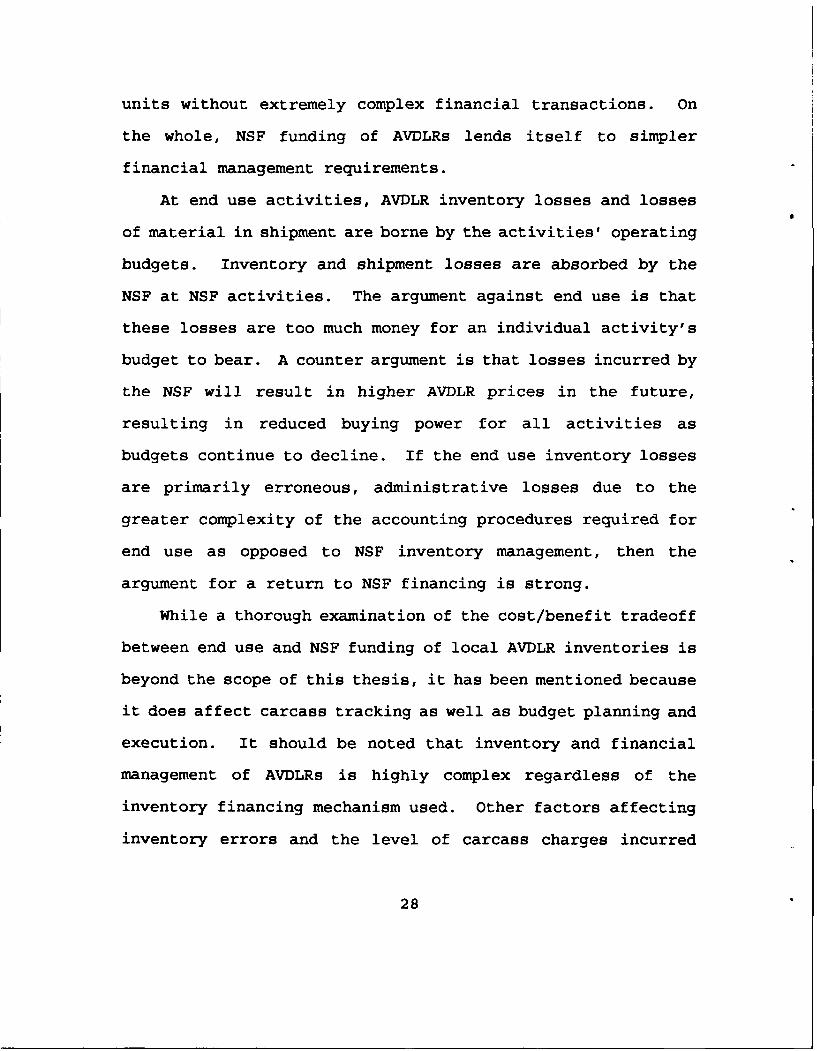

At end use activities, AVDLR inventory losses and losses

of material in shipment are borne by the activities' operating

budgets. Inventory and shipment losses are absorbed by the

NSF at NSF activities. The argument against end use is that

these losses are too much money for an individual activity's

budget to bear. A counter argument is that losses incurred by

the NSF will result in higher AVDLR prices in the future,

resulting in reduced buying power for all activities as

budgets continue to decline. If the end use inventory losses

are primarily erroneous, administrative losses due to the

greater complexity of the accounting procedures required for

end use as opposed to NSF inventory management, then the

argument for a return to NSF financing is strong.

While a thorough examination of the cost/benefit tradeoff

between end use and NSF funding of local AVDLR inventories is

beyond the scope of this thesis, it has been mentioned because

it does affect carcass tracking as well as budget planning and

execution. It should be noted that inventory and financial

management of AVDLRs is highly complex regardless of the

inventory financing mechanism used. Other factors affecting

inventory errors and the level of carcass charges incurred

28

include an activity's operating tempo and constant personnel

turnover which add to the difficulty of AVDLR management.

29

III. THE RELATIONSHIP BETWEEN ASO'S AVDLR CARCASS TRACKINGAND BILLING SYSTEM AND THE NAVY'S FLYING HOUR PROGRAM

A. THE AVIATION SUPPLY OFFICE'S CARCASS TRACKING PROGRAM

Because AVDLRs are expensive and normally require a long

procurement lead time, the repair of defective units is the

primary source of system replenishment. Strict carcass turn

in discipline is vital in order to reduce the investment

required for AVDLR inventories. Since the implementation of

NSF, and subsequently end use financing of AVDLRs, accurate

and complete carcass tracking has become even more significant

due to the impact of carcass charges on customers' operating

funds. [Ref. 4:p. 1-3-1]

ASO's carcass tracking system is automated via the B35

program, a module of the Uniform Inventory Control Point

(UICP) data processing system used by ASO for inventory and

financial management. Customers, the various aviation support

activities, use one of several different data processing

systems. Despite the variety of systems involved, customers

can be grouped into two general categories - transaction item

reporting (TIR) activities and non-transaction item reporting

(non-TIR) activities.

30

TIR activities are linked directly to ASO via computer.

Transactions affecting ASO managed material are transmitted to

ASO on a daily basis. Naval supply centers, including those

which function as hubs for NRFI AVDLRs, and most naval air

stations are TIR activities. Non-TIR activities, primarily

ships, transmit reports of transactions via message and

monthly computer tapes. All transactions are assigned a

document identifier, a three digit code identifying the type

of transaction taking place, e.g., receipt, issue, etc.

The B35 program builds a data base called the carcass

tracking file (CTF) by keying on certain document identifiers

of transactions transmitted to ASO. AVDLR issues,

requisitions, transfers, and receipts, depending on the type

of activity involved, will all establish carcass tracking

records within the CTF by individual customer document number.

Before the implementation of NSF financing of AVDLRs, when

AVDLRs were free to customers, the B35 program would generate

follow up inquiries to customers if a carcass had not been

turned in within a specified period of time after an AVDLR

issue or requisition had taken place. In addition, the system

tracked carcasses only through the first reported receipt by

a transshipper while they were en route to a depot level

repair facility.

31

The total system carcass tracking concept was introduced

simultaneously with NSF AVDLR financing. Total system carcass

tracking involved numerous enhancements to the B35 program

which greatly expanded the capabilities of the program. The

program in its current form now tracks carcass returns all the

way from the end use customer to the appropriate depot level

repair facility.

Among the expanded capabilities of the B35 program is the

ability to assess carcass value bills to customers for failure

to make required carcass turn ins. When a customer reports an

AVDLR transaction for which a carcass turn in is required, a

carcass tracking record is established in the CTF, "turning

on" carcass tracking for the individual item. If either a

notification of carcass shipment by the customer or a

notification of carcass receipt by a transshipper or depot

repair facility is not recorded in the individual carcass

tracking record, the customer will be assessed a carcass value

bill. In this respect, the B35 program serves as a

"policeman" for the NSF. [Ref. 9:p. 6]

The B35 program can also provide carcass value credits, or

bill reversals, to customers. These credits are issued when

a customer notification of carcass shipment or a system

receipt (transshipper or depot repair facility) is recorded

against a CTF carcass tracking record for which a carcass

32

value bill had previously been assessed. It is important to

note that, as mentioned previously in Chapter II, carcass

value bills and credits are assessed to the fiscal year

appropriation cited on the customer's original transaction

document, despite the actual date of the bill or credit. The

potential problems caused by carcass value bills and credits

received by customers after the end of the obligational

availability period of an appropriation are the focus of the

research for this thesis.

The B35 program also records system and transshipment

losses of AVDLR carcasses. A system loss occurs when a

carcass reported as shipped by a customer is never recorded as

received by the initial receiving activity, normally one of

the centralized hub activities. A transshipment loss is

similar, except that the hub has reported receipt and shipment

of a carcass which is never received by the depot repair

facility. The recording of these losses is important in that

they figure prominently in the annual pricing of AVDLRs. (Ref.

9:p. 6]

Serving as a data base, the B35 program consolidates data

on retrograde carcass tracking, carcass value bills, and

losses. These data are provided to type commanders and

activities under their cognizance in the form of periodic

management reports. The management reports include listings

33

of individual carcass bills by activity to facilitate the

focus of research by activities trying to reverse carcass

charges. The program also provides data in the form of

statistical reports to NAVSUP. [Ref. 9:p. 6]

The entire carcass tracking and billing cycle is easily

illustrated with a simple example, an AVDLR stock

replenishment requisition from an end use naval air station.

When the customer submits its requisition, a carcass tracking

record is established in the B35 CTF under the station's

replenishment document number and carcass tracking is "turned

on". The B35 program will track the customer through a series

of inquiries until the customer provides notification of

carcass shipment. Once carcass shipment notification is

provide by the customer, the program will track the designated

receiving activity.

Ideally, the station should transmit carcass turn in data

to ASO at the same time it submits its replenishment

requisition. The turn in should be made under the same

document number as the requisition and the item turned in

should match the part which was ordered. Once the station

provides notification of correct carcass shipment to ASO,

carcass tracking to the station is "turned off". The station

will not be billed for any more than the net price it

originally obligated for the requisition.

34

If the air station does not transmit carcass shipment data

to ASO when it submits the replenishment requisition, it will

continue to be tracked for the carcass until it does so or

until a receiving activity, normally the hub, reports receipt

of the carcass to ASO. Once the air station transmits carcass

turn in data to ASO, the B35 program will track the hub and

other transshippers until receipt of the carcass is recorded

at the depot level repair facility. Unlike the air station

which can be assessed a carcass value bill for failure to turn

in the carcass or failure to transmit carcass turn in data to

ASO, receiving activities are not billed for carcass losses.

These losses are instead recorded as system or transshipment

losses as described earlier. Table III-1 provides a synopsis

of the carcass tracking system [Ref. 9:p. 7].

ASO inquiries and bill notifications, as well as all

customer/receiver responses, are formatteC in the same manner

as standard supply transactions, i.e., requisitions, receipts,

issues, etc. Each type of inquiry, notification, or response

is assigned a unique document identifier. Once the carcass

tracking record is established in the CTF, the starting date

for the inquiry, response, and bill notification cycle is the

date on the document number of the transaction triggering

carcass tracking, not the date the transaction is received by

ASO.

9 35

CARCASS TRACKING SYNOPSIS

Customer NSF

Carcass is recorded to ultimate Matchdestination

Carcass is recorded to hub, but Match Transshipmentnot ultimate destination Loss

Activity provides notification of Match System Lossshipment and/or valid BK2response, no receipt in system

Carcass is not recorded in system Carcassand no response or notification Valueof shipment provided by activity Bill

Table III-I

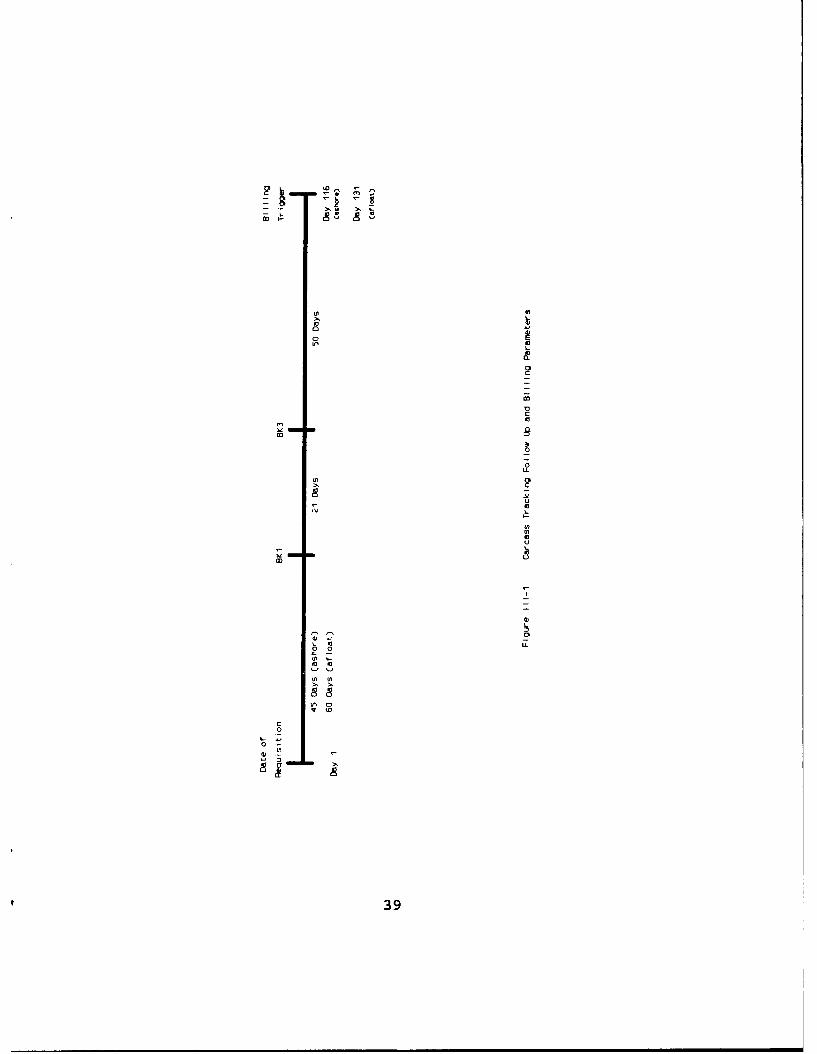

Reuurning to the air station example, if the station does

not provide carcass shipment data to ASO within 45 days of the

date of its requisition, the B35 program will generate a

follow up inquiry to the station with document identifier BK1

(assuming no carcass receipt has been recorded by a receiving

activity). For afloat activities, BKI's are generated 60 days

after the date of transactions requiring carcass turn ins.

BK1's can also be sent to the station if its response to a

previous BKl is rejected.

Upon receipt of a BK1, the air station has 21 days to

answer the inquiry with a document identifier BK2 response.

This BK2 response can be coded to provide a variety of

explanations as to the disposition of the carcass. The

36

simplest response is that the carcass was indeed turned in

under the correct document number. The fact that the turn in

was made under a different document number or that the turn in

will be delayed are among other responses which can be cited

on a BK2. A satisfactory BK2 will "turn off" carcass

tracking to the air station and avert a carcass bill if turn

in of the carcass is indicated in the response.

If the air station fails to provide a satisfactory

response within 21 days of a BKl follow up inquiry, a

notification of billing, document identifier BK3, will be

generated by the B35 program (again, assuming no system

receipt has been recorded). The BK3 is not a notice that a

carcass value bill has been assessed to the air station, but

a notice that a bill will be forthcoming in 50 days. The air

station can still avoid a carcass charge if it sends a BK2

response before the bill is triggered. If the charge is

avoided, ASO will send a document identifier BK4 notifying the

station that it will not be billed for the carcass.

If the air station has received a carcass value bill, it

may still provide a BK2 response which, if satisfactory, will

reverse the bill. A carcass receipt reported by a receiving

activity can also reverse a carcass value bill. The air

station will be notified of the reversal by ASO with a BK4.

S37

The entire carcass tracking cycle, from initial carcass

exchange transaction to carcass value billing is 116 days for

shore activities, 131 days afloat. The follow up and billing

parameters of the carcass tracking system are illustrated in

Figure III-i [Ref. 9:p. 11]. This cycle, which can be

extended through bill reversals, operates without regard to

the fiscal year of the appropriation cited on the original

carcass exchange transaction.

ASO's B35 carcass tracking and billing program as outlined

above directly affects the Navy's flying resources which are

funded through the flying hour program. AVDLR carcass value

bills generated by the B35 program are properly chargeable to

flying hour program funds. Historical flying hour costs are

used as the basis for determining future flying hour program

resource needs. The flying hour program is described below as

are the effects of the B35 program on flying hour cost

reporting accuracy under the two price AVDLR billing system.

B. THE FLYING HOUR PROGPAM

Navy and Marine Corps aviators must be well trained and

highly skilled in order to accomplish their aviation missions.

An aviator's primary means of gaining this skill and

maintaining proficiency is through the hands-on training

funded by the Navy's flying hour program. The flying hour

38

Lb9

0-

Enn

10

V ID

€39

0

0

JUo Lb

J Lb

j I Lb

3Lb

program encompasses all flying activity from initial training

of new personnel to the day to day operations of fleet

aviation squadrons. [Ref. 10:p. 1]

The Navy's flying hour program, which includes the Marine

Corps, is funded by the O&M,N appropriation. The program

accounts for part of the operating costs for most Navy and

Marine Corps aircraft. These costs include the costs for

fuel, other petroleum products, and repairs to aircraft

components as well as costs associated with administrative

supplies and services. Costs not covered by the flying hour

program include procurement, overhaul, and repair of aircraft

(vice components) and engines. The payroll for aircrew and

maintenance personnel, maintenance training, and the costs of

aviation facilities are also paid for by other programs. [Ref.

11:p. 8]

Aviation elements of the flying hour program include [Ref.

10:p. 171:

* Tactical air/antisubmarine warfare, consisting of frontline fleet squadrons operating Navy and Marine Corpscombat and patrol aircraft.

* Fleet air training, consisting of the fleet trainingsquadrons which train replacement aviators to fly specifictypes of aircraft before assignment to fleet squadrons.

* Fleet air support, consisting of ship and shore-based airlogistics support squadrons as well as special operationaltest and evaluation support squadrons.

40

* Undergraduate pilot and flight officer training,consisting of squadrons which provide basic flighttraining to new naval aviators.

The Special Assistant to the Deputy Chief of Naval

Operations for Air Warfare is designated as the flying hour

program manager. The program manager is responsible for

program budgeting, coordination, and monitoring. During

program execution, the Navy Comptroller allocates funds on a

quarterly basis to the fleet commanders in chief and monitors

program spending. The fleet commanders are responsible for

providing combat ready aircrews and for ensuring that hours

flown and funds spent do not exceed those allocated.

Budget requests are prepared at the type commander and

program manager levels based on cost information provided by

the flying hour cost reporting system (FHCRS). Budget

requests are prepared by type, model, series (TMS) of aircraft

using a historical cost per flying hour adjusted for inflation

(or deflation) multiplied by anticipated flying hours for each

TMS. The historical cost used is a three year moving average

based on flying hour cost reports prepared by the type

commanders. Anticipated flying hours are projected from

various formulas for each of the elements of the flying hour

program, i.e., tactical air/ antisubmarine warfare, fleet air

training, etc.

41

Under the FHCRS, type commanders submit monthly flying

hour cost reports to the program manager. These reports list

financial obligations directly associated with operating and

maintaining aircraft as well as the number of hours flown and

the number of operational aircraft. AVDLRs account for

approximately one third of the flying hour costs incurred by

COMNAVAIRPAC.

Flying hour cost reports include only current fiscal year

financial obligations. Post fiscal year transactions such as

carcass charges and credits generated by the B35 program, are

not included in the FHCRS under the current two price AVDLR

billing system. Because these post fiscal year carcass

charges and credits, which are legitimate flying hour costs,

are not recorded, the costs to be used in the determination of

future flying hour program resource needs are inaccurate.

42

IV. PROBLEMS WITH POST FISCAL YEAR BUDGET MANAGEMENT ANDFLYING HOUR COST REPORTING DUE THE TWO PRICE SYSTEM OF BILLINGFOR AVDLRS

A. SIZE OF THE AVDLR BUDGET

AVDLRB comprise a large portion of an aviation type

commander's total O&M,N budget. COMNAVAIRPAC's annual O&M,N

expense limitation has been approximately two billion dollars

for the past five fiscal years (1986-1987). Of this total

annual expense limitation, one quarter, or approximately $500

million, has historically been designated for AVDLR purchases.

In addition, AVDLRs typically account for one third of all

flying hour costs incurred by COMNAVAIRPAC. [Ref. 12]

The actual amount of money spent on AVDLRs by COMNAVAIRPAC

since 1986 is shown in Table IV-l. Table IV-l also shows that

when adjusted to constant 1986 NSF prices and constant 1986

flight hours, AVDLR expenditures for COMNAVAIRPAC have

remained fairly constant relative to flight hours over time.

The actual AVDLR expenditures listed in Table IV-I are as of

the end of each fiscal year and do not reflect any carcass

charges or credits received after fiscal year end. These

figures are provided here to illustrate the magnitude of AVDLR

expenditures at COMNAVAIRPAC. [Ref. 13]

43

COMNAVAIRPAC AVDLR EXPENDITURES

FY AVDLR NSF PRICE AVDLR OPTEMPO AVDLR

ACTUAL CHANGE CONSTANT PERCENT ADJUSTED$$$ FY 86 $$$ CHANGE" $$$

86 553,216 0.0% 553,216 0.0% 553,216

87 581,367 (0.5%) 584,288 3.7% 563,853

88 536,659 (6.5%) 576,851 (3.0%) 593,214

89 447,063 (13.3%) 554,262 1.4% 546,494

90 427,720 (2.0%) 541,103 (4.0%) 563,196

91 483,543 14.9% 532,397 (2.5%) 546,405

*All AVDLR data is actual cost in thousands as of fiscal yearend except for FY 91. Budgeted figures were used for FY 91.

"'OPTEMPO percent change computed as fiscal year to date flighthours divided by FY 86 flight hours.

Source: COMNAVAIRPAC, Code 01911

Table IV-l

B. POST FISCAL YEAR EFFECTS ON TYPE CO MANDER BUDGETS

The two price AVDLR billing system can and does affect

post fiscal year budget management at both the aviation

support activity and type commander levels. The budget

management effects at the type commander are parallelled at

the aviation support activity, though on a smaller scale. For

the purposes of this thesis, the impact of the two price AVDLR

billing system on post fiscal year budget management will be

examined primarily at the type commander level.

44

As explained in previous chapters, the primary source of

post fiscal year budget management difficulties created by the

two price AVDLR billing system is the timing difference

between the length of the O&M,N appropriation used to pay for

AVDLR consumption and the length of ASO's carcass tracking and

billing cycle. AVDLR carcass charges and credits generated by

ASO's B35 program are not limited by fiscal year as is the one

year obligational authority period of an O&M,N appropriation.

AVDLR transactions occurring late in a fiscal year can result

in carcass value bills being charged to that fiscal year's

O&M,N appropriation after the end of the fiscal year.

Similarly, credits may also be obtained through carcass bill

reversals after the end of a fiscal year. During the two year

expenditure availability period of an O&M,N appropriation, the

type commander and its subordinate activities are still

responsible for any over obligation of funds.

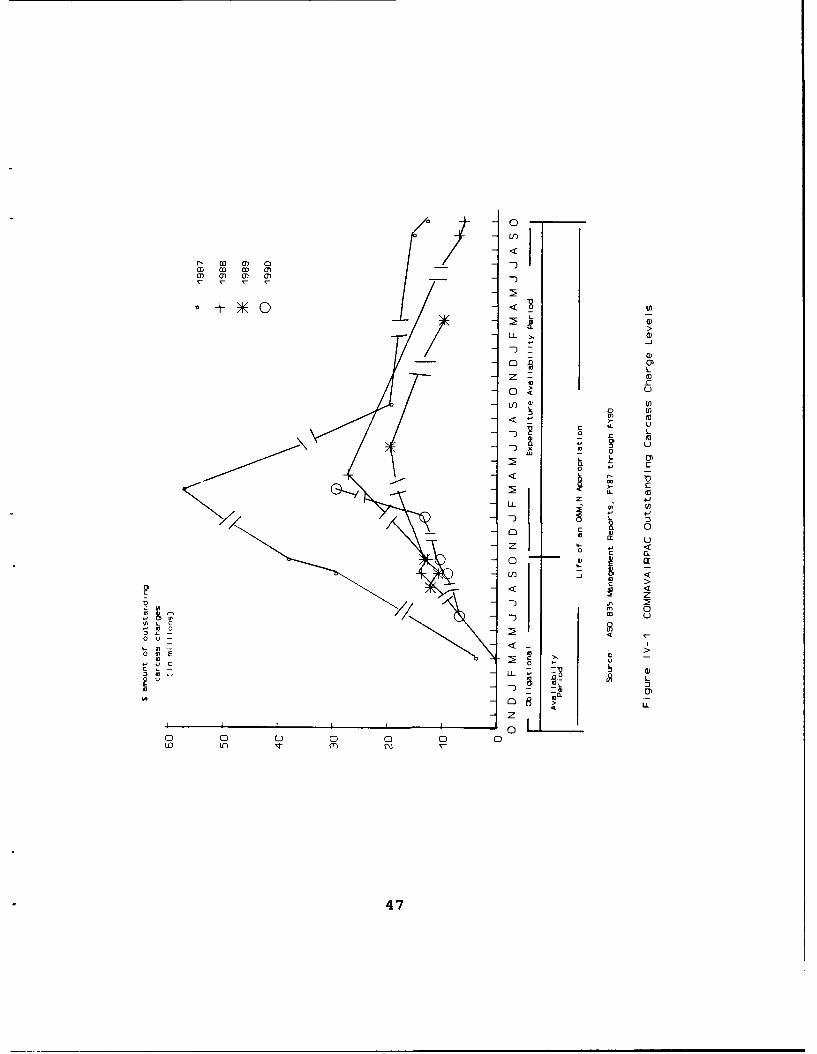

Figure IV-l is a graphic illustration of outstanding post

fiscal year carcass charges for COMNAVAIRPAC throughout the

O&M,N expenditure availability periods of fiscal years 1987

through 1990 as of 6 March 1991. Fiscal years 1989 and 1990

are only partially complete because the expenditure

availability period for each had not ended at the time the

data for the graph was compiled. Also included in the graph

45

are the outstanding carcass charges during the second quarter

of the obligational availability period of each year.

The data for the graph was compiled from management

zeport3 !uerated by ASO's B35 program. Fiscal year 1986 was

not included because fiscal year 1987 was the first full year

of end use management of AVDLRs. The use of fiscal years 1987

through 1990 provides a basis for analysis of trends under a

constant method of AVDLR management and financing. It should

be noted that the B35 management reports do not list all

carcass charges incurred by a type commander's subordinate

activities.

AVDLR transactions transmitted to ASO citing no carcass

turn in (such as initial outfitting requisitions and survey

replacements) are billed to the customer at standard price.

The carcass tracking files for these transactions are purged

from the B35 program's live files in one day and are not

reflected in the management reports generated by the program.

However, these types of transactions should not affect post

fiscal year budget management, as no furthercarcass bills are

assessed to the customer on these transactions.

As can be seen in Figure IV-1, carcass charges generated

by the B35 program are delayed until well into the

obligational availability period of each fiscal year. Even as

46

0

r, (0 0Y 0i0) 0) 0) (71

0)L

-C0<

0) L).- U)

< (a0 L0

41 U

x 0)

0 c

z 4LL U; E

0 ~ L0

zI <

4 >

r'1 0

I r -n <

*-)- -0 03

z0

0 0 0 0 0 0 0LO in)

47

late as the second quarter of each fiscal year, only minimal

carcass charges, if any, had been incurred. The level of

outstanding carcass value bills continued to rise after the

end of each fiscal year as bills from the final two quarters

of the year were assessed. After peaking during the first

year of the expenditure availability period, the amount of

outstanding bills dropped as the individual customers

researched and responded to the bills (or as system receipts

of carcasses were recorded).

COMNAVAIRPAC does not manage AVDLR money as a distinct set

of funds during the expenditure availability period of an

O&M,N appropriation. They are instead managed within

CONIAVAIRPAC's total O&M,N expense limitation for that fiscal

year on a cash basis. Management on a cash basis simply means

that funds designated for specific purposes within an

appropriation, such as AVDLRs, are not tracked individually

for obligation levels. The goal during expenditure

availability periods is to keep the O&M,N expense limitation

as a whole in the black. [Ref. 12]

AVDLR carcass charges and credits are not the only sources

of post fiscal year budget management difficulties.

Additional factors which can affect the O&M,N expense

limitation during its expenditure availability period include

requisition cancellations, unpreceded disbursements, and price

48

changes. These types of transactions are not limited to

AVDLRs and can include services as well as consumable (non-

DLR) materials purchased with O&M,N funds.

When an activity cancels a requisition, it de-obligates

the funds which were to have paid for the item ordered. As

with carcass bill reversals, cancellations have the effect of

returning funds for re-obligation. If a cancellation occurs

after the end of a fiscal year in which the funds were

originally obligated, the money is no longer available for re-

obligat on.

Unpreceded disbursements occur when activities are billed

for material or services for which they failed to record an

obligation. Such unexpected losses of funds can result in the

over obligation of funds at both the activity and type

commander level. Unpreceded disbursements are similar to

carcass charges in that they can occur after the end of the

fiscal year to which they are billed.

Price changes for material and services can happen between

the time money is obligated for a requisition and the time an

activity is billed for the requisition. Price changes can be

either upward or downward. Regardless of the direction, price

changes directly affect obligation levels.

It is clear that difficulties in the post fiscal year

budget management process would exist with or without AVDLR

49

carcass charges and credits. According to LCDR Krista Selig,

the Fleet Budget and Accounting Officer of the COMNAVAIRPAC

Force Comptroller's Office, AVDLR carcass charges and credits

add to the uncertainty of post fiscal year budget management.

These charges and credits are not however, insurmountable

problems in and of themselves. [Ref. 12]

The uncertainty in the variability of obligation levels is

worse in the first year of an O&M,N appropriation's

expenditure availability period than in the second year. In

the case of AVDLRs, this is illustrated in Figure IV-l. As

mentioned earlier, the amount of outstanding carcass charges

continues to grow during the first year of an expenditure

availability period until peaking during the second or third

quarter of that year. Afterwards, the level of outstanding

carcass charges declines continually until the end of the

expenditure availability period. It should be noted that the

volatility of post fiscal year carcass charges decreased for

each fiscal year from 1987 to 1989 as evidenced by lower peaks

in the level of outstanding carcass charges for each year.

Fiscal year 1990 is a special case due to the Persian Gulf

War. In addition to aircraft carriers and air stations,

COMNAVAIRPAC also provides funding to west coast Marine Air

Groups (MAG) through its O&M,N expense limitation.

COMNAVAIRPAC, while not having operational control of the

5o

MAGs, issues budgets in the form of operating targets to the

MAGs. The accounting and budget management system for the

MAGs is very similar to that used by aircraft carriers.

COMNAVAIRPAC received approximately $20 million of fiscal

year 1990 carcass charges during March and April 1991 as a

result of MAG 70 operations in the Persian Gulf during August

and September of 1990. Because the MAG was pressed into

service before its supply operations were completely set up,

it lost control of the carcass tracking process for the AVDLRs

used early in the deployment. As of September 1991, MAG 70

had received $19.8 million in 1990 carcass credits after

researching the documents involved and providing turn in

information to ASO. [Ref. 12]

Aside from the aberration in fiscal year 1990, the post

fiscal year pattern of AVDLR carcass charges for COMNAVAIRPAC

has become predictable. While amounts are still not

completely certain, AVDLR carcass charges are more

controllable within the scope of COMNAVAIRPAC's overall

expense limitation. The declines in the peak levels of post

fiscal year outstanding carcass charges from 1987 to 1989 were

significant as the aviation support activities gained

experience in AVDLR management and carcass tracking. Although

the learning curve for the support activities is no longer

51

very steep, modest declines in the level of carcass charges

can probably be expected in the future.

C. DISTORTION OF FLYING HOUR PROGRAM COSTS

The Navy's flying hour program, discussed in Chapter III,

funds part of the costs of daily operations for most Navy and

Marine Corps aircraft. Costs covered by the program include

the costs for fuel, other petroleum products, and repair to

aircraft components as well as costs associated with

administrative supplies and services. Flying hour program

money is appropriated annually as part of the O&M,N

appropriation.

Flying hour funds are provided to type commanders as part

of their annual O&M,N expense limitation. As of 23 September

1991, COMNAVAIRPAC's total 1991 O&M,N expense limitation was

$2,126,000,000.00. Of this amount, $1,441,377,000.00 was

budgeted for the flying hour program. In addition, 39 percent

of the flying hour program budget, or $561,811,000.00, was

slated to cover the cost of AVDLRs used by COMNAVAIRPAC

activities in the course of daily flying operations. [Ref. 12]

Cost information for the flying hour program is recorded

in the flying hour cost reporting system (FHCRS). Flying hour

cost reports are prepared by the type commanders and sent to

the Navy's flying hour program manager on a monthly basis.

52

These reports provide the per hour operating cost by type,

model, series (TMS) of aircraft and form the basis of future

flying hour program budget requests.

The FHCRS captures only current year costs (including

current year carcass charges). Any costs chargeable to a

fiscal year which are incurred after the fiscal year has ended

are not included in flying hour costs reports. These post

fiscal year costs can include AVDLR carcass charges,

unpreceded disbursements, and upward price changes. If these

costs drive the eventual level of obligations above the amount

reported at the end of a fiscal year, then the costs of the

flying hour program for that year would be understated.

Similarly, reductions in the amount of obligations reported as

of the end of a fiscal year would result in the overstatement

of costs for that year.

Because COMNAVAIRPAC manages its post fiscal year expense

limitations on a cash basis, the differences in AVDLR

obligations as of the end of a fiscal year and at the end of

the expenditure availability period for that year cannot be

readily compared. In any case, such a comparison would reveal

only the total understatement or overstatement of flying costs

associated with AVDLRs without identifying that portion caused

by the two price system of billing for AVDLRs. One method of

identifying these cost distortions is to compare the amount of

53

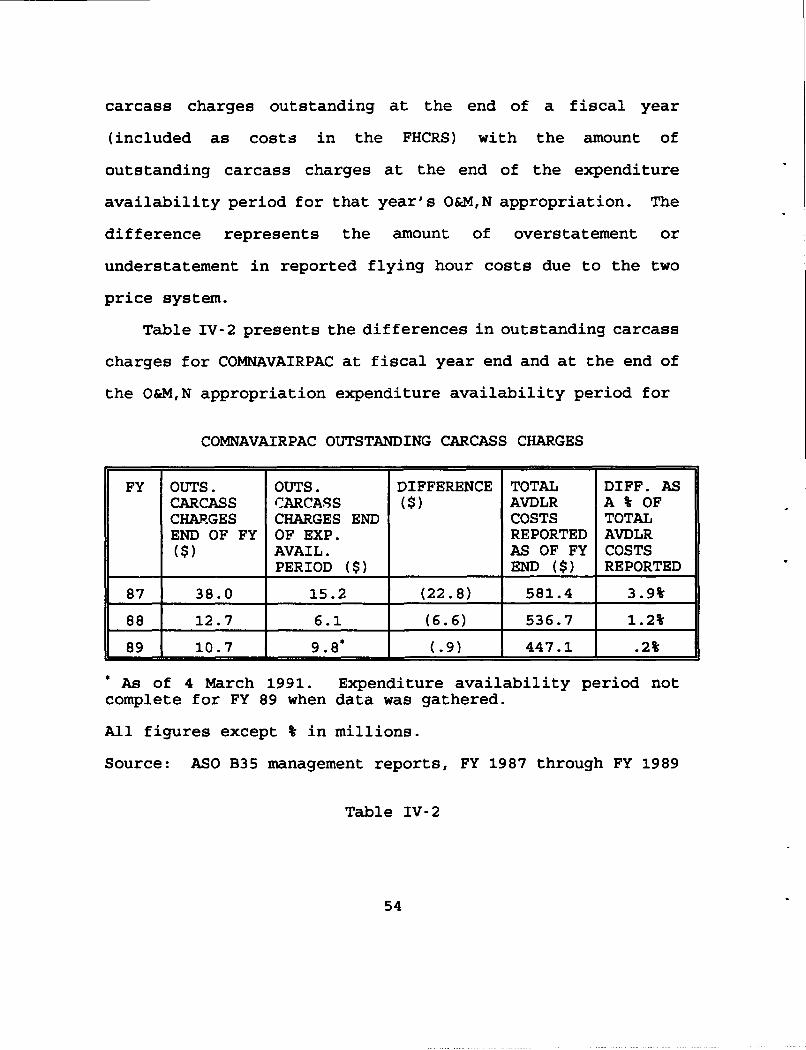

carcass charges outstanding at the end of a fiscal year

(included as costs in the FHCRS) with the amount of

outstanding carcass charges at the end of the expenditure

availability period for that year's O&M,N appropriation. The

difference represents the amount of overstatement or

understatement in reported flying hour costs due to the two

price system.

Table IV-2 presents the differences in outstanding carcass

charges for COMNAVAIRPAC at fiscal year end and at the end of

the O&M,N appropriation expenditure availability period for

COMNAVAIRPAC OUTSTANDING CARCASS CHARGES

FY OUTS. OUTS. DIFFERENCE TOTAL DIFF. ASCARCASS CARCASS ($) AVDLR A % OFCHAR.GES CHARGES END COSTS TOTALEND OF FY OF EXP. REPORTED AVDLR($) AVAIL. AS OF FY COSTS

PERIOD ($) END ($) REPORTED

87 38.0 15.2 (22.8) 581.4 3.91

88 12.7 6.1 (6.6) 536.7 1.2%

89 10.7 9.80 (.9) 447.1 .2%

As of 4 March 1991. Expenditure availability period notcomplete for FY 89 when data was gathered.

All figures except W in millions.

Source: ASO B35 management reports, FY 1987 through FY 1989

Table IV-2

54

fiscal years 1987 through 1989. Fiscal year 1990 is not

included because it was still in the first year of its

expenditure availability period at the time data was collected

for the comparison. Fiscal year 1989, though not complete,

was in the second year of its expenditure availability period.

The data used for the comparison was compiled from ASO B35

management reports. Although the management reports were not

generated exactly as of the end of each fiscal year or

expenditure availability period, all were dated within one

month of the point in time cited.

While not exact, Table IV-2 does show that carcass bill

reversals after the end of a fiscal year eventually outweigh

post fiscal year carcass charges. As a result, COMNAVAIRPAC

flying hour program costs were overstated in each of the years

listed. Although the overstatement was large for fiscal year

1987 ($22.8 million), the overstatement as a percentage of

AVDLR costs reported has declined each year to only .2 percent

for fiscal year 1989.

D. LOST USE OF FUNDS DUE TO CARCASS CHARGES FOR "PAPER

Many of the AVDLR carcass charges incurred by the fleet

are as a result of "paper losses" vice actual losses of

material. Such losses can occur in a number of ways,

55

including the failure of customers to transmit carcass turn in

data to ASO and the miscoding of turn in documents. Most of

these losses are eventually found, though the research

involved in investigating BK1 inquiries and carcass charges

can be quite complicated and time consuming. The delay

involved in researching carcass charges and in the bill

reversal process at ASO results in the reversal of many

carcass charges after the end of the fiscal year to which they

were originally billed.

As noted earlier, carcass bill reversals have resulted in

lower actual AVDLR carcass costs than were recorded as fiscal

year end obligations for fiscal years 1987 through 1989.

These funds returned during the expenditure availability

period of an appropriation are no longer available to incur

new obligations. Excess funds returned to COMNAVAIRPAC during

this period are eventually recouped by CINCPACFLT.

Funds recouped by CINCPACFLT can possibly end up lapsing

to the successor accounts discussed in Chapter II. In

essence, the funds would be wasted. However, the O&M,N funds

recouped by CINCPACFLT can be used to fund within scope growth

of work in the Ship's Maintenance Account. The Ship's

Maintenance Account is used to fund overhauls of CINCPACFLT

ships. Within scope growth refers to increased costs over

initial estimates for repair work. If money for a particular

56

job was initially obligated in a previous fiscal year, O&M,N