11 may 2005 the economy and the housing market fionnuala earley group economist nationwide building...

TRANSCRIPT

11 May 2005

The Economy and The Economy and the Housing the Housing MarketMarket

Fionnuala EarleyFionnuala EarleyGroup EconomistGroup EconomistNationwide Building SocietyNationwide Building Society

Overview

Recent Trends and Outlook

Economic Background

Housing Market

Risk factors

Outlook

Economic growth above trend But questions about level of spare capacity

Economic Growth

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2000q1

2000q2

2000q3

2000q4

2001q1

2001q2

2001q3

2001q4

2002q1

2002q2

2002q3

2002q4

2003q1

2003q2

2003q3

2003q4

2004q1

2004q2

2004q3

2004q4

2005q1

2005q2

2005q3

2005q4

2006q1

2006q2

0

0.2

0.4

0.6

0.8

1

1.2

YoY QoQ

Labour market remarkably stable Record employment but rising unemployment Paradox due to increased size of workforce

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Jan-

00

Apr

-00

Jul-

00

Oct

-00

Jan-

01

Apr

-01

Jul-

01

Oct

-01

Jan-

02

Apr

-02

Jul-

02

Oct

-02

Jan-

03

Apr

-03

Jul-

03

Oct

-03

Jan-

04

Apr

-04

Jul-

04

Oct

-04

Jan-

05

Apr

-05

Jul-

05

Oct

-05

Jan-

06

Apr

-06

27,000

27,500

28,000

28,500

29,000

29,500

Unemployed Employed (rhs)

Economic Background

Inflation Expectations

1.53

1.73

1.93

2.13

2.33

2.53

2.73

2.93

Feb-

05

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb-

06

Apr

-06

Jun-

06

Aug

-06

Energy costs have fuelled inflation Oil prices now falling but utility bills still increasing Inflation expectations are higher

-10

-5

0

5

10

15

20

25

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

CPI CPI Energy CPI Core

Wage growth steady But risk that inflationary expectations will feed into wages For now, wages are kept under control by immigration,

threat of outsourcing and remaining slack in labour market.

Earnings growth, YoY, %

2.5

3

3.5

4

4.5

5

Jan-0

2

Apr-

02

Jul-

02

Oct

-02

Jan-0

3

Apr-

03

Jul-

03

Oct

-03

Jan-0

4

Apr-

04

Jul-

04

Oct

-04

Jan-0

5

Apr-

05

Jul-

05

Oct

-05

Jan-0

6

Apr-

06

Jul-

06

Inc Bonuses Excl Bonuses

Economic recovery

Retail sales picking up and outlook stable Falling petrol prices leaves consumers with more to

spend

Retail Sales Growth

-1

0

1

2

3

4

5

6

7

8

9

Jan-0

0

Apr-

00

Jul-

00

Oct

-00

Jan-0

1

Apr-

01

Jul-

01

Oct

-01

Jan-0

2

Apr-

02

Jul-

02

Oct

-02

Jan-0

3

Apr-

03

Jul-

03

Oct

-03

Jan-0

4

Apr-

04

Jul-

04

Oct

-04

Jan-0

5

Apr-

05

Jul-

05

Oct

-05

Jan-0

6

Apr-

06

Jul-

06

%

retail vol retail val

Economic Summary

Economic growth above trend – despite recent revisions

Inflation well above target Labour market resilient Wage growth steady Retail sales picking up BUT Household income growth (and expectations of its

future growth) slowing No sign of second round impact on wage growth Second interest rate rise on the horizon

Housing Market

Surprisingly strong and enduring revival in housing market

Activity levels picked up in spite of worsening affordability

0%

5%

10%

15%

20%

25%

30%

Jan-0

3

Mar-0

3

May-0

3

Jul-0

3

Sep-0

3

Nov-0

3

Jan-0

4

Mar-0

4

May-0

4

Jul-0

4

Sep-0

4

Nov-0

4

Jan-0

5

Mar-0

5

May-0

5

Jul-0

5

Sep-0

5

Nov-0

5

Jan-0

6

Mar-0

6

May-0

6

Jul-0

6

Sep-0

6

50

60

70

80

90

100

110

120

130

140

House prices YoY% (lhs)

House purchase approvals,000s

Buy-to-Let a factor

Residential property investment a clear boost to the market B2L balances increased from 1% to 8% of total mortgage

balances in 5 years House price growth has allowed existing landlords to gear up Gross buy-to-let lending 11% of total gross lending in H2 2006

Gross B2L lending as % total gross lending

0%

2%

4%

6%

8%

10%

12%

H1 9

9

H2 9

9

H1 0

0

H2 0

0

H1 0

1

H2 0

1

H1 0

2

H2 0

2

H1 0

3

H2 0

3

H1 0

4

H2 0

4

H1 0

5

H1 0

6

H2 0

6

Source: CML

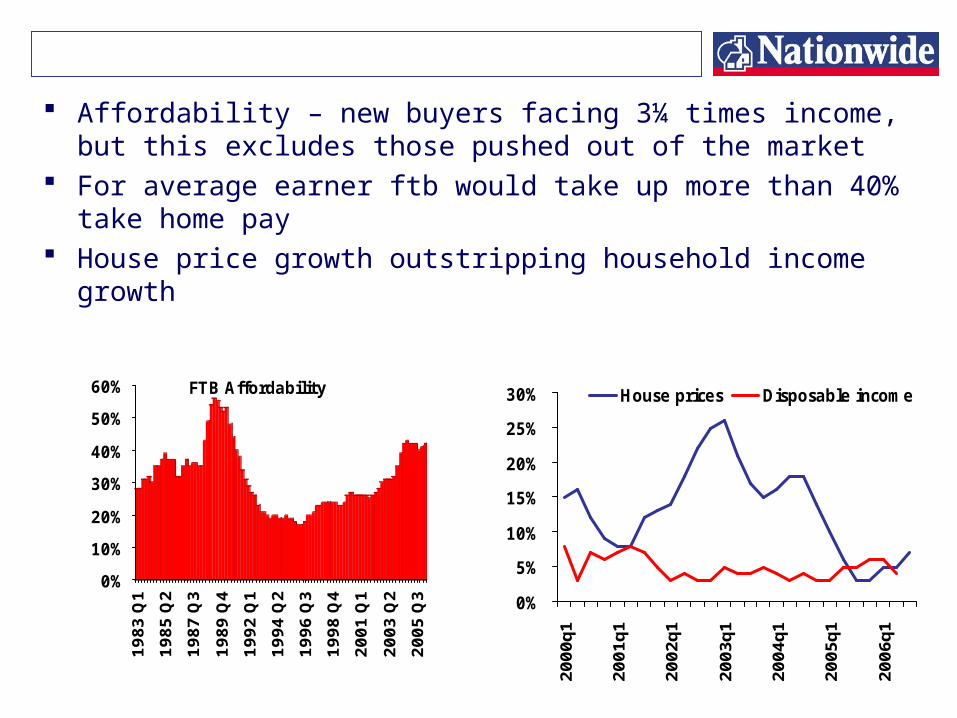

Affordability – new buyers facing 3¼ times income, but this excludes those pushed out of the market

For average earner ftb would take up more than 40% take home pay

House price growth outstripping household income growth

0%

5%

10%

15%

20%

25%

30%

2000

q1

2001

q1

2002

q1

2003

q1

2004

q1

2005

q1

2006

q1

House prices Disposable income

0%

10%

20%

30%

40%

50%

60%

1983

Q1

1985

Q2

1987

Q3

1989

Q4

1992

Q1

1994

Q2

1996

Q3

1998

Q4

2001

Q1

2003

Q2

2005

Q3

FTB Affordability

Default Risks

Small upturn in arrears but remain at low levels Financial distress concentrated in non-owner occupied sector Lending secured on dwellings over £1 trillion But remaining equity in owner occupied housing stock is more

than twice this

£0

£500

£1,000

£1,500

£2,000

£2,500

£3,000

1981 1984 1987 1990 1993 1996 1999 2002 2005

Value of Stock £bn

Loans secured onDwellings (ex HA) £bn

Housing market more resilient than anticipated House price growth now at 8.2% Momentum in the market grown throughout the

summer Strong investor demand – but this is not the whole

story

BUT House prices growing faster than incomes Affordability deteriorating Expectations of house price growth moderating Widespread expectation of further increase in rates