10.16 residential final - · pdf fileinteragency appraisal and evaluation guidelines •...

TRANSCRIPT

10/16/2015

1

REDEFINING APPRAISALAND ITS ROLES IN AN EVOLVING

BANKING ENVIRONMENT

PRESENTED BY:

Adam A. Alessi, MAI, MRICS

Chief Appraisal & Environmental Risk Officer

Senior Vice President, First Niagara Bank, N.A.

Copyright © 2015 Adam A. Alessi, MAI, MRICS All rights reserved with the author. Commercial use of this presentation,or its any part, is strictly prohibited .

Washington D.C. Metro Area Chapter

Friday, October 16, 2015

Sheraton College Park North Hotel

4095 Powder Mill Rd., Beltsville MD

10 Ground Rules

1. Have patience, wait to be called on2. Stay engaged, participation is key3. Develop concepts instead of tangents4. Minimize sidebars5. Beware of soapboxes6. You have a valid point, and so does your neighbor7. Agree to disagree8. We can’t boil the ocean9. Don’t take yourself too seriously10. Have Fun!

The “Guidance”

Appraisal Regulations

• National banks (OCC): 12 CFR part 34, subpart C

• State member banks (FRB): 12 CFR part 208, subpart E

• Holding companies (FRB): 12 CFR part 225, subpart G

• Nonmember state banks (FDIC): 12 CFR part 323

10/16/2015

2

Interagency Appraisal and Evaluation Guidelines

• Federal Register Notice: 75 FR 77450 (12/10/2010)

• FRB: SR letter 10-16

• FDIC: FIL-82-2010

• OCC: Bulletin 2010-42

The “Guidance”

Monumental Actions

• FIRREA

• FDICIA

• GLB

• Dodd-Frank

The “Guidance”

The “Agencies” and Regulators

• OCC – National banks and national associations

• Federal Reserve – bank holding companies and

members of the FED

• FDIC – state chartered banks not members of the FED

• NCUA – federal credit unions

Also, the CFPB regulates consumer laws for all creditors

10/16/2015

3

Get with the Program

• Provide for independence of the persons ordering,performing or reviewing appraisals or evaluations from thecredit decision

• Ensure appraisals and evaluations contain sufficientinformation and analysis to support the credit decision

• Provide enough time to receive and review appraisal andevaluation reports prior to credit decision

• Implement controls to promote compliance with theappraisal regulation and guidelines

• Establish criteria for monitoring collateral values

Discussion Question…

• What are the most significant changesto your practice since 2008? Have yoursources of business or type’s assignmentschanged dramatically since the downturn?

National Profile

• 2010-2014, roundly consistent makeup of Residential (55%),General (30%), Licensed (15%)

• Less than 10% have 4 or fewer years experience (relatively fewnewcomers)

• Over 60% are over the age of 51 (population at or approachingretirement)

• 22% hold Associates Degree, some college, or high school diploma(new Bachelors Degree requirement threatens existing pool)

• 61% earn $99,000 or less (level of effort and risk commensuratewith income potential?)

• 20% decline (19,650) in active real estate appraisers 2007-2014

July 26, 2015 Joint Regional Meeting Dallas Texas

10/16/2015

4

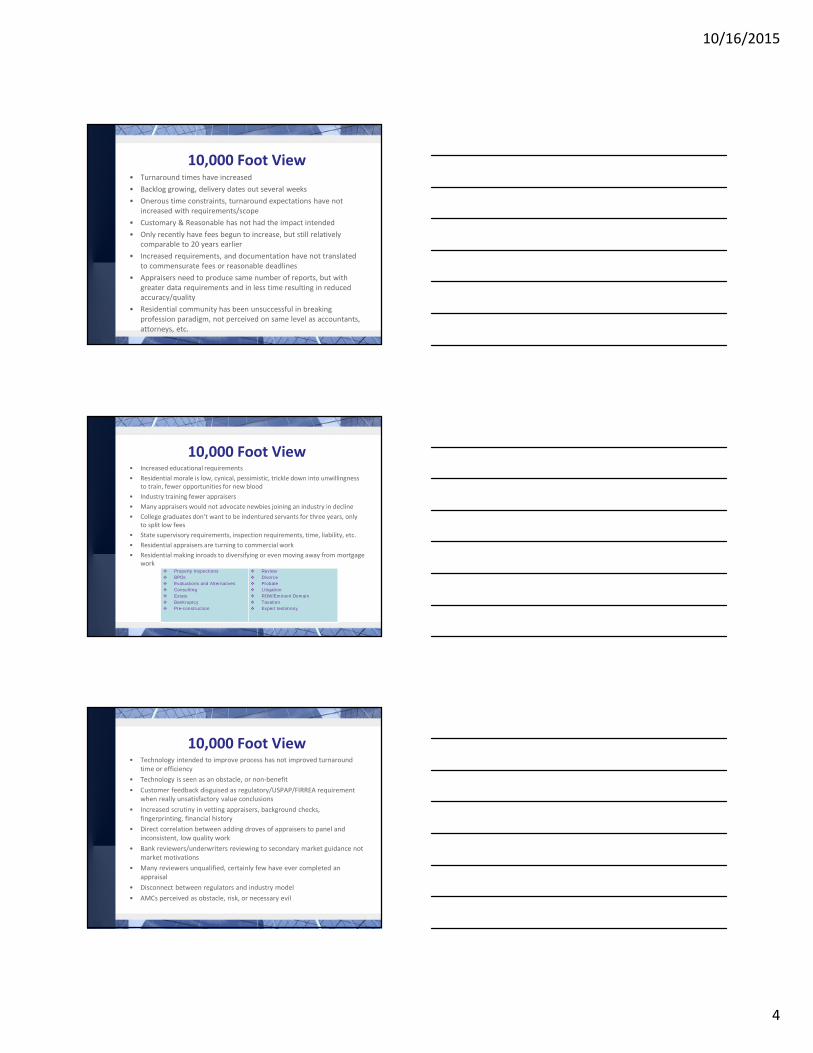

10,000 Foot View• Turnaround times have increased

• Backlog growing, delivery dates out several weeks

• Onerous time constraints, turnaround expectations have notincreased with requirements/scope

• Customary & Reasonable has not had the impact intended

• Only recently have fees begun to increase, but still relativelycomparable to 20 years earlier

• Increased requirements, and documentation have not translatedto commensurate fees or reasonable deadlines

• Appraisers need to produce same number of reports, but withgreater data requirements and in less time resulting in reducedaccuracy/quality

• Residential community has been unsuccessful in breakingprofession paradigm, not perceived on same level as accountants,attorneys, etc.

10,000 Foot View• Increased educational requirements

• Residential morale is low, cynical, pessimistic, trickle down into unwillingnessto train, fewer opportunities for new blood

• Industry training fewer appraisers

• Many appraisers would not advocate newbies joining an industry in decline

• College graduates don’t want to be indentured servants for three years, onlyto split low fees

• State supervisory requirements, inspection requirements, time, liability, etc.

• Residential appraisers are turning to commercial work

• Residential making inroads to diversifying or even moving away from mortgagework

Property Inspections

BPOs

Evaluations and Alternatives

Consulting

Estate

Bankruptcy

Pre-construction

Review

Divorce

Probate

Litigation

ROW/Eminent Domain

Taxation

Expert testimony

10,000 Foot View• Technology intended to improve process has not improved turnaround

time or efficiency

• Technology is seen as an obstacle, or non-benefit

• Customer feedback disguised as regulatory/USPAP/FIRREA requirementwhen really unsatisfactory value conclusions

• Increased scrutiny in vetting appraisers, background checks,fingerprinting, financial history

• Direct correlation between adding droves of appraisers to panel andinconsistent, low quality work

• Bank reviewers/underwriters reviewing to secondary market guidance notmarket motivations

• Many reviewers unqualified, certainly few have ever completed anappraisal

• Disconnect between regulators and industry model

• AMCs perceived as obstacle, risk, or necessary evil

10/16/2015

5

THE POLLS ARE IN!!!

What are the top three areas where you most frequentlydisagree with a review appraiser?

• Lease-up cost and timing• Highest & Best Use – potential uses• USPAP, methodology, and applicable approaches• Subdivision comps – too many from a new development and not

enough from an existing one• Frivolous comments – job justification• Personal feelings and statements in revision requests• Reviews clearly performed by non-appraisers• Scope disagreements and changes to the engagement• Requests for submissions of irrelevant sales - How many comps are

enough?• Amount of adjustment and how it was developed• Classification quality/condition for subject and comps• Wanting adjustments when none are supported

What are the top three areas where you most frequentlydisagree with a review appraiser?

• Insist secondary market requirements where there are none• Allocation of land to total value• Estimate of rental market• Piecemeal revision requests• Reviewer teasing out specific comments when already explained and

supported in report• Reviewer has tunnel vision on one particular element of comparison• Busy work requests that have not value impact• Assumptions• Reviewer style imposed on appraiser• Requests for paired sales on commercial assignments where there

are none• Struggles with hypothetical conditions vs. extraordinary assumptions• Simple cap rate arguments – reviewers reliance on published rates

and not local market data (institutional vs. private)

10/16/2015

6

If you could change one thing about the appraisal reviewprocess, what would it be?

• Less feedback from borrowers being channeled through the bank

• Implications or subtext that report will be rejected and fee not paid

• Require US based reviewers, and even then geographically competent

• Eliminate checklists

• No “review by committee”

• Have more trust in the professionals that are engaged

• Do not make USPAP accusations lightly, legitimate ones are cause forstate submission

• All reviewers should be licensed

• Reviewers should have access to spreadsheets or Argus files

• Do not use competitors to complete field reviews

• No means no, if the reviewer and appraiser cannot see eye-to-eye athird-party review is warranted

• Be an advocate for the appraiser and ensure that information is notwithheld by the lender or borrower

What question would you most like to hear reviewappraisers respond to during the workshop?

• How much say do you have in choosing the appraisers, merit vs. fee?• Why do you cite peer work, anecdotal evidence or data not available to

the appraiser when challenging an appraiser (blanket statements w/outsupport)?

• How much time are you spending on the review and what qualifies youto do so?

• Have you ever done an appraisal?• What percentage of appraisals pass/fail?• How many defaults were the direct results of the appraisal?• How do you manage scope definition and ensure apples-to-apples bids?• How have reviews helped improve your own appraisals?• What are the regulators telling you?• What are the most frequent issues that you see?• Does a change like the addition of an addenda or checklist constitute a

change in report date?• How often do you have much of the information that the appraiser is

going to ask the site contact for anyway?

Ripped from the Headlines

WSJ October 6, 2014 Reports:“Fifth Third Bancorp reached a $85 million settlement of civil fraud charges related

to roughly 1,400 mortgages the Cincinnati-based bank failed to report weredefective, the Justice Department said.”

10/16/2015

7

Consumer Finance

Uniform Collateral Data Portal (UCDP) & UniformAppraisal Dataset (UAD)

• Risk management and fraud avoidancein the sale of loans to Fannie and Freddie

• Need for consistency not only within anappraisal report, but also from report toreport

• Fannie Mae can now see across a broad spectrum of anappraisers’ work

• Sheer volume of transactions and enormity of appraisaldata cache

Consumer Finance

• Inconsistencies uncovered:

- Sale Data – Multiple appraisal reports completed by the sameappraiser, using the same comparable property having thesame sales date but with different sale prices and financing,concessions and property characteristics data.

- Condition/Quality and Other Ratings – Different ratings for thesame subject and comparable in different appraisal reports.Same comps, different conditions over same period.

- How many appraisal inspections can you do in one day - Couldyou have 20 reports with the same effective date, spread 100miles apart?

Consumer Finance

Collateral Underwriter (CU)

• Fannie Mae’s proprietary appraisal

review application

• Performs automated analysis of appraisal

submitted to the Portal

• Identifies appraisals with heightened risk for eligibility,

compliance, overvaluation, and quality control – results

in a risk score

• Provides lenders with same line of sight as the GSE

10/16/2015

8

Consumer Finance

• Is model driven leveraging enormous amounts ofstatistical market data

• Focuses in on:

- Reconciliation – relevant comps given appropriate weight?

- Adjustments – based on market reaction?

- Comp Selection – representative of the subject?

- Data Integrity – are physical and transaction attributesaccurately reported?

Consumer Finance

Collateral Underwriter (CU)

• Data Integrity – are physical and transaction attributes

accurately reported?

- Comps observed multiple times

- Inconsistencies identified within a single appraiser'sbody of work and also relative to their “peers”

Consumer Finance

Collateral Underwriter (CU)

• Quality Assurance Request

- Consider additional appropriate propertyinfo, including comparable propertiesto support conclusions

- Provide further detail, substantiation,or explanation

- Correct factual errors

AMCs need to use extreme caution when making these requests!

10/16/2015

9

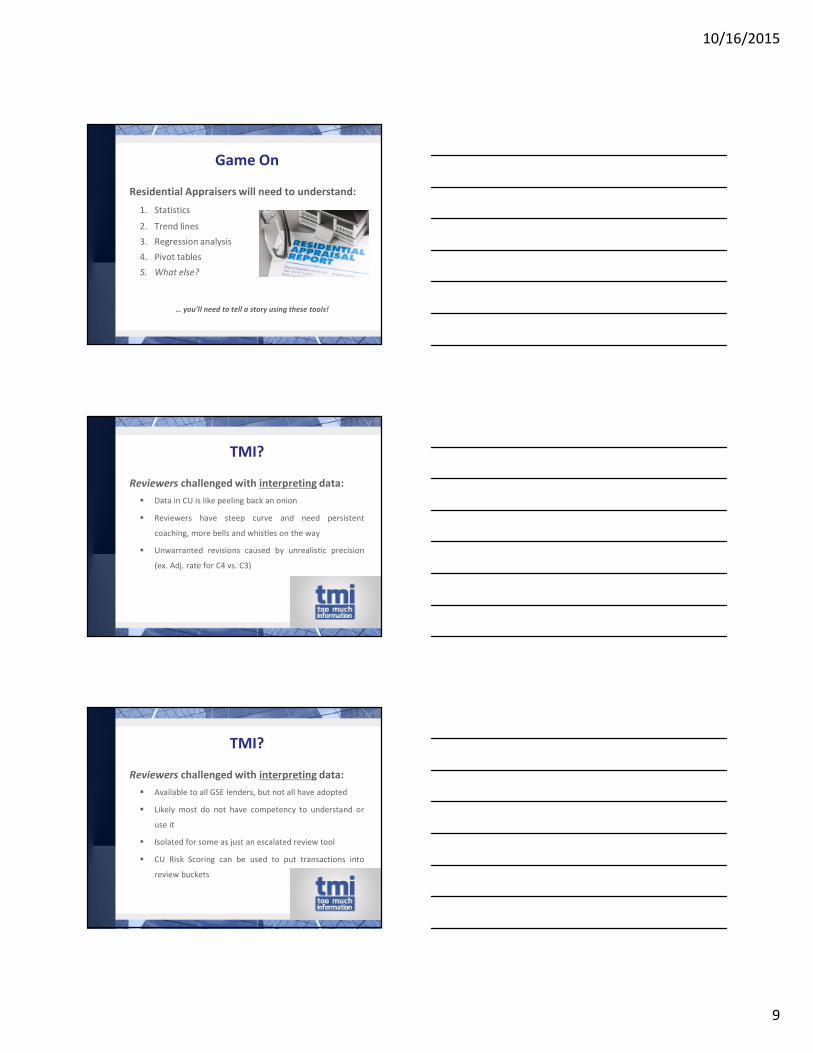

Game On

Residential Appraisers will need to understand:

1. Statistics

2. Trend lines

3. Regression analysis

4. Pivot tables

5. What else?

… you’ll need to tell a story using these tools!

TMI?

Reviewers challenged with interpreting data:

Data in CU is like peeling back an onion

Reviewers have steep curve and need persistent

coaching, more bells and whistles on the way

Unwarranted revisions caused by unrealistic precision

(ex. Adj. rate for C4 vs. C3)

TMI?

Reviewers challenged with interpreting data:

Available to all GSE lenders, but not all have adopted

Likely most do not have competency to understand or

use it

Isolated for some as just an escalated review tool

CU Risk Scoring can be used to put transactions into

review buckets

10/16/2015

10

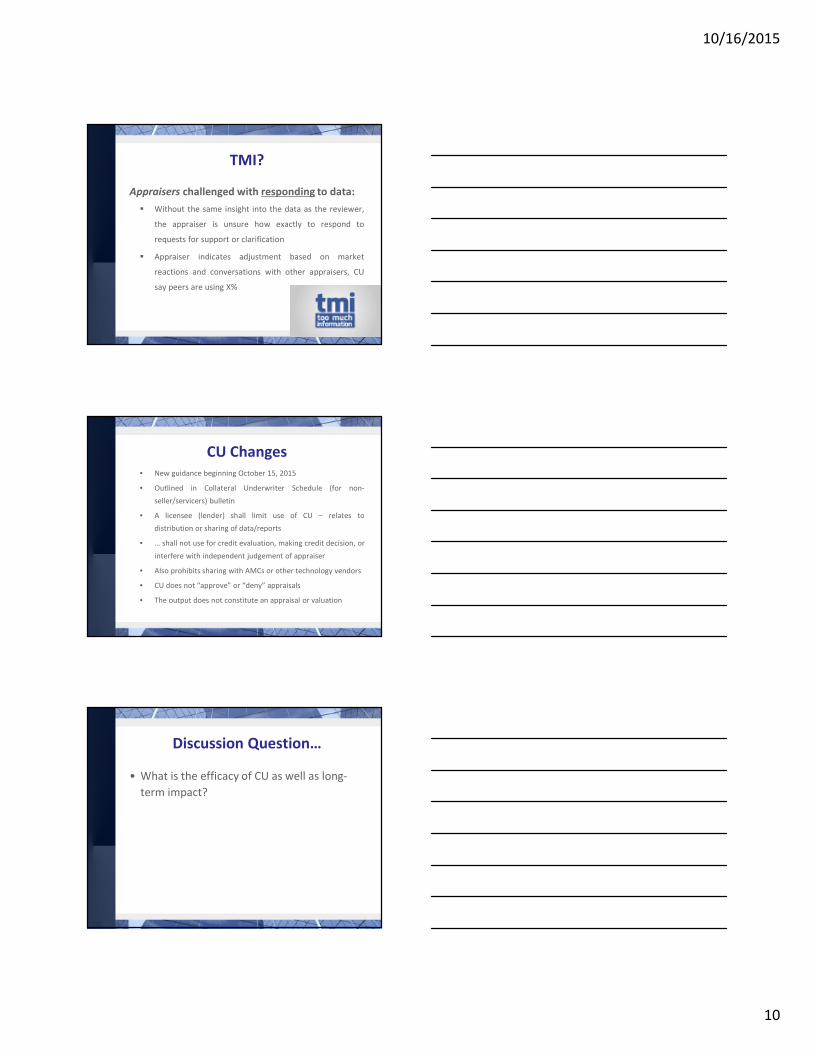

TMI?

Appraisers challenged with responding to data:

Without the same insight into the data as the reviewer,

the appraiser is unsure how exactly to respond to

requests for support or clarification

Appraiser indicates adjustment based on market

reactions and conversations with other appraisers, CU

say peers are using X%

CU Changes• New guidance beginning October 15, 2015

• Outlined in Collateral Underwriter Schedule (for non-

seller/servicers) bulletin

• A licensee (lender) shall limit use of CU – relates to

distribution or sharing of data/reports

• … shall not use for credit evaluation, making credit decision, or

interfere with independent judgement of appraiser

• Also prohibits sharing with AMCs or other technology vendors

• CU does not “approve” or “deny” appraisals

• The output does not constitute an appraisal or valuation

Discussion Question…

• What is the efficacy of CU as well as long-

term impact?

10/16/2015

11

Hot Off the Presses!

New HUD Single Family Handbook 4000.1

• September 14, 2015, HUD rolled out

the new consolidated SF Handbook

• Biggest overhaul of FHA valuationpolicies since ’99 (4150.2) – Bill Clintonimpeached, Wayne Gretzki retired, andMySpace launched!

• Since ‘99, a patchwork of Mortgagee Letters (ML) andAddendums published, 47 MLs in 2000 alone and asimilar number annually thereafter

Hot Off the Presses!

• Attempts made to clarify conflicts and inconsistenciessuch as HUD HOC Reference Guide and FAQs

• Supersedes and consolidates all handbooks,Addendums, and MLs

• In addition to consolidation, 4000.1 contains severalvaluation policy changes

• Many scope requirements exceed Fannie Mae andFreddie Mac

Hot Off the Presses!

Examples of highlighted changes:

Comp history, 3+ years instead of 1

Increased photo requirements

Attic and crawl space inspections requirements

Contributory value of energy-efficient buildingcomponents

Electronic Appraisal Delivery (EAD) portal

For more info:

http://portal.hud.gov/hudportal/documents/huddoc?id=SFH_HB_4000-1_FAQS.PDF

10/16/2015

12

Discussion Question…

• Do revised FHA conditions put most appraisersin conflict with USPAP competency rule?

• Are you competent to opine as to thefunctionality of mechanicals, structuralconditions, etc.?*

• Can you consistently/reliably determineproperty eligibility?

*Ex. “The utilities were on and functioning at the time of inspection andthe home meets 4150.2 & 4905.1 HUD Requirements”

Hot Off the Presses!

TRID – TILA RESPA Integrated Disclosure

• Truth In Lending and Real Estate

Settlement Procedures Initial Disclosures

• Effective October 3, 2015

• Will apply to most closed-end consumer credit

transactions secured by real estate

• Exempt: HELOC, Reverse Mortgage, or mortgages

secured by mobile home or non-attached dwelling

• GFE and Initial Truth in Lending disclosures will be

combined and replaced with a Loan Estimate (LE)

Hot Off the Presses!

• HUD-1 Settlement Statement and Finial Truth inLending disclosure will be combined and replaced witha Closing Disclosure (CD)

• After borrower application, creditor has 3 days todeliver LE

• Borrower has 10 days to declare their “intent toproceed”, and until then cannot charge or collect feesother than those reasonable to pull credit report

• The CD must contain actual terms and costs deliveredto borrower no later than 3 days before close

10/16/2015

13

Hot Off the Presses!• Appraisal Fee needs to be inputted into LE, falls under Zero

Tolerance

• Zero Tolerance – Fees paid to an unaffiliated third-party, ifthe creditor did not permit the consumer to shop for theservice provider, cannot increase at all

• Fee can only be change from quote for “change incircumstance,” an extraordinary event beyond the controlof any interested party or unexpected event specific to theconsumer or transaction; i.e. inaccurate information reliedupon or changed after LE, new information not relied uponfor LE

• Ex) change in loan type, change n assignment type (SF tocondo), misinformation from borrower (wrong income)

Hot Off the Presses!

• Legislators determined that complex property will notconstitute “change in circumstance” since creditor hasproperty address in advance of the LE

• Final inspections or trip fees are grey area, could arguenew info not relied upon for LE

• If not qualified for “change in circumstance”, creditorsoptions are:

- Pay increase or recover somehow at closing window

- AMCs may coverall fees to provide coverage

- East difference as cost of doing business

Hot Off the Presses!

AQB and Licensing Requirements

• The Appraiser Qualifications Board on March 20, 2015

adopted significant changes to the background check

requirements of the Real Property Appraiser

Qualification Criteria. The new requirements will take

effect Jan. 1, 2017.

10/16/2015

14

Hot Off the Presses!

• The Appraiser Qualifications Board will hold a PublicHearing in Washington, DC on Friday, October 16, 2015.To facilitate the consideration of Alternative ExperienceRequirements in the Real Property AppraiserQualification Criteria (Criteria)

Overview of the Mortgage Market

10/16/2015

15

Overview of the Mortgage Market

Example of Overlay

Map of US

10/16/2015

16

How Lenders See the US

.

Protecting Yourself

Lender and Appraisers Dilemma

Tips: Understand the true end user Understand your clients requirements Understanding your clients overlays Read the scope of work The appraisal and inspection should

be written with all of this in mind.

Borrower Expectations

• Quicken Loans reports homeowners are consistently

overvaluing their homes in 2015 (HPPI – Home Price

Perception Index)

• Appraiser opinions 2.65% lower than homeowner estimates in

August, and 2.33% lower for July

• HPPI regionally - -2.32% West, -2.35% Midwest, -2.70 South,

and -2.78% Northeast

• Home Value Index (Quicken) measures home value changes

based on appraisals, reports August was nearly flat from prior

month

10/16/2015

17

Discussion Question…

• How often is the reviewer clearly on a

fishing expedition for their borrower?

• How different would things be if the client

was better able to manage customer

expectations on the front-end?

Revision Log

Common Revisions include:

• Adjustments – either unsupported or inconsistent

• Contract related errors (mortgage only)

• Commentary – inconsistent

• Comparable selection not adequately explained

• Inconsistent description of characteristics

• Reconciliation inadequacies

• Prior sales history analysis

Discussion Question…

• Fannie Mae Sales Guide – are appraiserssimulating the motivations of marketparticipants or the risk management criteriafor the GSEs?

10/16/2015

18

Grinding Gears

A Few Reviewer Pet Peeves :

• Lack of good neighborhood analysis, clear boundary

definition, too much boilerplate

• In SCA, concluded unit value falls outside unadjusted

range

• When CA is attempted, at least consider if it makes

sense

• Simple factual errors and inconsistencies, address, zip,

county, client name!, etc.

• Add your bugaboo here _______________☺

Questions?Please feel free to contact us!

Residential PanelistsBrian C. Coester [email protected] A. Ginter [email protected] R. Keegan [email protected]

Commercial PanelistsJohn S. Atwell, Jr. [email protected] A. Miner [email protected] Sieger [email protected]

ModeratorAdam A. Alessi [email protected]

Thank You!

10/16/2015

19

Panelist BiosBrian C. Coester, CEO Coester Valuation Management ServiceFounder and Chief Executive Officer of CoesterVMS a national valuation service provider for the mortgagebanking industry. CoesterVMS technology suites and service products allow lenders, banks and financialintuitions to remain compliant with the current federal and state regulations as well as provide excellent servicein collateral valuation or residential properties nationally.

Brian A. Ginter, CCIM, Director, Executive-Staff, The Pyramid NetworkOver 30 years in the real estate industry as an appraiser, Realtor, investor, developer, commercial loanofficer/transactional lender, and a general real estate consultant; four of which (2009 – 2013) as the developerand Managing VP of a combined appraisal and environmental department for a major community bank. Mr.Ginter processes extensive experience and the ability to address unique property specific challenges; andadvanced knowledge in the fields of regulatory compliance, construction/rehabilitation, development,litigation, financing, environmental, and property stabilization.

John R. Keegan, President, Dehart and DemingOwner of Dehart and Deming Inc., a ten person, multi-state real estate appraisal and consulting firm. Mr.Keegan has over thirty years of appraisal experience; he is a Certified General Appraiser who specializes incomplex residential appraisal assignments as well as commercial valuations. Mr. Keegan practices in Virginia,Maryland and The District of Columbia. Mr. Keegan currently sits on The Board of Equalization for The City ofAlexandria as a Circuit Court appointee, he formerly served on the Board of Zoning Appeals, and was theappraiser member of The Prince William County Board of Realtors, and additionally Mr. Keegan has served onthe advisory boards of a number of local community banks.

Panelist BiosJohn S. Atwell, Jr., MAI, AI-GRS, Senior Corporate Trainer, CoStar Group D.C.John is currently employed by CoStar Group as a manager in Learning and Development since 2014. Hisprimary function revolves around training newly hired real estate researchers and associates. Prior to this Johnwas a review appraiser with CapitalSource Bank in Chevy Chase, MD. He was born, raised, and worked in So Cal(primarily San Diego) for 58 years; getting his start in CRE with Union Bank in 1972. His commercial appraisaland review experience spans almost 28 years and for some of the nation’s largest institutional lenders such asBank of America, Citicorp, and GMAC Commercial Mortgage. John is an MAI who recently received his AI-GRS,and is an approved instructor for the AI’s General Appraisal Income Approach, Part I.

Christopher A. Miner, MAI, Regional Appraisal Review Mngr., Susquehanna/BB&TChris Miner started the review appraisal department at Susquehanna Bank and currently manages AppraisalReview Officers in BB&T’s Northern Region. Over his 40-year career, he was a review appraiser for the FederalGovernment, Director, Managing Director, COO, and partner at a number of fee appraisal firms. Hedeveloped over a dozen seminars and courses, including the Appraisal Institute’s GIS curriculum; taught dozensof seminars and courses for the Appraisal Institute and the University of Connecticut; an invited speaker forseveral AI chapters and other professional organizations; and was the author and co-author of several articlesand a chapter in Visual Valuation (Appraisal Institute, 2010).

Melanie Sieger, MAI, Real Estate Services Unit, Pacific West BankMelanie Sieger holds the MAI and AI-GRS Designations. She has performed Appraisal Reviews with the RealEstate Services Department of Pacific Western Bank and predecessor CapitalSource Bank since 2009. Her roleincludes reviewing appraisals, overseeing reviews performed by external reviewers and ordering appraisals.Prior to this role, she has worked as an appraiser in Washington, DC and in a large accounting firm. Her 15 yearsof experience in real estate appraisal and review encompasses many commercial property types. Melanieholds a Masters of Science Degree in the Real Estate Program at Johns Hopkins University. She is verycommitted to a high quality of appraisals and serves on three panels at the Appraisal Institute, including theDemonstration of Knowledge and Experience Review Panel.

Panelist BiosAdam A. Alessi, MAI, SVP Chief Appraisal & Environmental Risk Officer, FNFGIn his most current role, Adam is a SVP with First Niagara Bank, N.A.; a top 40 financial institution with almost$40 Billion in assets. As the Chief Appraisal and Environmental Risk Officer, Adam developed the bank’s firstcentralized Collateral Services Group (CSG), creating three distinctly separate and profitable businessoperations: Commercial Appraisal, Residential Appraisal, Environmental Risk & Construction Services. Adamwas the 2011–2012 President of the Appraisal Institute’s Western New York–Ontario and he holds the MAI andMRICS designations. Adam is a respected subject matter expert contributing and participating in various

seminars, lectures, and roundtables to include the AI, RMA, ABA, and the Erie County Bar Association.