10 simple things that can go wrong in ul pricing chris fievoli, fsa, fcia cia annual meeting june...

TRANSCRIPT

10 Simple Things 10 Simple Things That Can Go Wrong That Can Go Wrong

in UL Pricingin UL Pricing

Chris Fievoli, FSA, FCIA

CIA Annual Meeting

June 29, 2005

#1 - Mortality#1 - Mortality

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Why be concerned about mortality?• Longevity continues to improve• Impact of AIDS has been absorbed into

experience• Continual improvement in underwriting

techniques• However, mortality improvements are not

necessarily a good thing

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• “Death supported” business• Can occur on lapse-supported reinsured UL

policies• A product with no reinsurance should exhibit

normal sensitivity• However, assume mortality risk is 100%

reinsured• A death claim then has the same impact as a lapse• Improvement in mortality is equivalent to lower

lapses (and lower profitability)• Where is the crossover point?

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Evidence of death support is negative mortality PfAD

• Can be mitigated by choosing lower level of reinsurance

• What if mortality improves in the future?

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Pricing Implications• Need to look at mortality improvements

• Is reinsurance still necessary then?

• Does reinsurance treaty allow for recapture?• Would recapture terms make treaty less desirable

from ceding company standpoint?

#2 - Lapses #2 - Lapses (As Always)(As Always)

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Lapse rates on Level COI continue to decline

• Well under 2% after duration 7 (2003 CIA study)

• On joint policies – lapse rates approach zero after duration 10

• Reflects sophistication of use in estate planning markets

• Still limited experience in ultimate durations

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Setting of expected lapse rates• Do we expect further reductions in the future?• How sensitive are pricing results?

• Lapse-based capital• 2003 changes base capital on additional PAD• May amplify exposure to lapse issues

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Lapses and alternate COI structures• Several companies now have YRT scales

stopping before age 100• Rates will need to be “loaded” to cover future

costs that are being waived• Does this reverse sensitivity to lapses?

• Can we expect any future lapses when a coverage no longer has charges?

#3 – Minimum Interest Rate #3 – Minimum Interest Rate GuaranteesGuarantees

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• What minimum interest rate guarantees are out there?

• Typically apply to GIAs within a UL policy• Usually apply to 5-, 10-, and 20-year GIAs• Range of guarantees is 1% to 3%

• Higher guarantees on longer terms

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• According to 2005 Munich Re Pricing Survey

• Only two companies include a charge for guaranteed renewal rates

• Only one company stochastically modeled interest rate guarantees

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

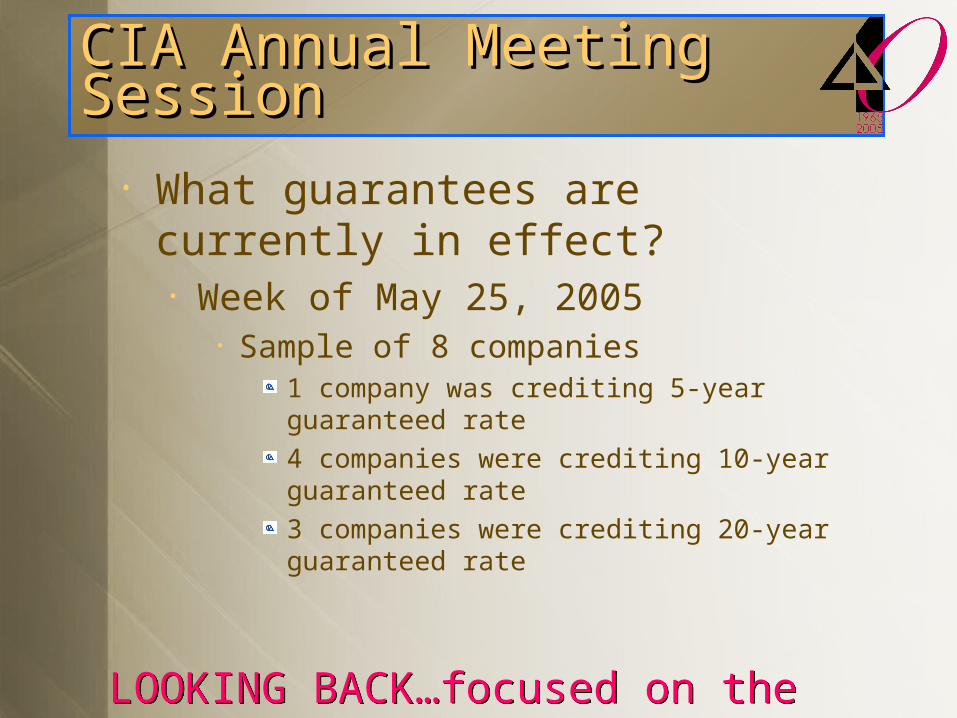

• What guarantees are currently in effect?• Week of May 25, 2005

• Sample of 8 companies1 company was crediting 5-year guaranteed rate

4 companies were crediting 10-year guaranteed rate

3 companies were crediting 20-year guaranteed rate

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Approach to modeling minimum interest rate guarantees

• Adapt model to include GIAs only• Question – how is profitability affected without

spreads from other investments?

• Run paths with and without guarantee in effect

• PV of difference in profitability is cost of guarantee

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Issues to consider in modeling of interest rate guarantees

• What CTE level is relevant?• How to reflect this in pricing?

• Additional spread, or additional capital appropriation?

• Long-term rates of return• Do you assume persistence of current low rates?• Include scenarios where rates drop significantly

lower?

#4 – Premium#4 – Premium Persistency Persistency

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• What level of premiums are you expecting in the long run?

• Will policyholders continue to over-fund, or will they drop or suspend premiums?

• Future economic conditions

• How dependent upon future premiums is your pricing?

• No industry experience to draw upon

#5 – Underlying Investment#5 – Underlying InvestmentReturnsReturns

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• UL can be viewed as a hybrid of two products

• Pure insurance protection• Savings portion that allows tax-deferred

growth• Can be used to pay future charges

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Long-term return assumption especially important for insurance portion

• Especially level COI, where future mortality costs are pre-funded

• Investment returns are required to fund future mortality costs

• Appropriateness of asset strategy• Must balance returns against capital cost

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Long-term growth assumption on account values

• Is it as important?• Yes – will greatly affect future account

balances, which will affect spreads collected• How will policyholders behave in the future?

• Will they shift investments to lower spread options if conditions warrant?

• What is the impact on pricing?

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• May be useful to look at the two pieces separately

• Is the insurance coverage self-supporting?• What levels of cross-subsidy exist?• Does over-funding always mean higher

profitability?

#6 - Management Expense#6 - Management ExpenseRatios and Ratios and

Investment AccountsInvestment Accounts

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Average spread is 290 bp (Munich Re Survey, 2005)

• Marketplace is under pressure to reduce management fees

• Exchange-traded funds

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Do higher MERs deliver the value?• Median MER of Canadian Equity funds

• 2000 – 2.34%• 2005 – 2.64%

• But:• 80% of actively managed mutual funds fail to

beat low cost passive index fundNational Post, June 4, 2005

• Consumers will start to put the pieces together

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Does your product still work under a lower MER?

• May need to• Reduce bonuses• Reduce compensation• Increase prices on other elements of product

• How sensitive to pricing is change in MER?

• Likely quite sensitive

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Is there a practical limit on investment options?

• Additional overhead of multiple fund offerings

• Could policyholders diversify away fund manager expertise?

• Value associated with MER is negated

#7 - Illustration #7 - Illustration and Sales Practicesand Sales Practices

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• What is a realistic rate to use in illustrations?

• 6% net rate implies almost 9% gross rate (assuming average MER of 290 bp)

• Is this too aggressive for a long-term return assumption?

• Will the policy deliver the values the buyer thought it would?

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Bonus structures• Some companies have bonuses that are

triggered by a threshold rate of return• i.e. additional bonus paid if return exceeds 5%• An illustration run at 6% will pay the bonus each

year• However – actual returns could fluctuate above

and below 5%, and still average to 6%• Actual bonus collected will be less than illustrated

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Focus on long-term values• Many advisors still look at 40th year cash

values• Realistic measure of value?• Would be valuable to also show probability

of survival to that age (after mortality and lapses)

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Customer expectations• How significant are the differences in

illustrated vs. actual performance?• Very limited experience at longer durations (i.e.

20+)

• Will customers view shortfalls in performance as the company’s responsibility?

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• YRT as a replacement for Term• Lower initial costs may be attractive• Are policyholders prepared for increases in

costs?• Product structures may alleviate this

• i.e. require higher first-year minimum premium

• Are your products being sold as permanent coverage, or shorter duration term coverage?

#8 - Modeling Shortfalls#8 - Modeling Shortfalls

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Are all product features modeled properly?

• E.g. joint last-to-die with COIs to first death• Requires multiple contingent account value

growth paths• Not handled by conventional pricing software

• Multiple coverages• Do you model policies, or individual coverages?• Are death benefits options (i.e. account value on

first death) adequately modeled?

#9 - Shifts in#9 - Shifts in Mix of Business Mix of Business

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• Level COI vs. YRT COI• Market is moving towards YRT COI

• From 40% in 2001 to 50% in 2004

• Pricing challenges with Level COI• Lower lapse rates• Lower interest rates• More capital intensive (especially lapse capital)

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• If your Level COI sales are more than 50% of your UL portfolio, you are possibly being selected against

• How sensitive are your profit results to shifts in business mix?

• How soon can a trend be recognized?

#10 – The#10 – The Disaster Scenario Disaster Scenario

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

• What if tax deferral of life insurance was rescinded?

• What proportion of your UL business is sold for insurance protection as opposed to tax deferral?

• How dependent is your product line on UL sales?• What level of fixed expense support would be

lost?

CIA Annual MeetingCIA Annual MeetingSession Session

LOOKING BACK…focused on the futureLOOKING BACK…focused on the future

Conclusions:

1. Several things can go wrong.

2. Murphy’s Law:• If anything can go wrong, it will.

3. O’Toole’s Commentary:• Murphy was an optimist

4. UL pricing actuaries must be ever vigilant.