1 vitality.co.uk/life life cover term assurance, whole of life cover and lifestylecare cover

TRANSCRIPT

1VITALITY.CO.UK/LIFE

LIFE COVER

Term Assurance, Whole of Life Cover and LifestyleCare Cover

VITALITY.CO.UK/LIFE2

• Premiums available on a guaranteed or reviewable basis

• Minimum term – 5 years

• Maximum term:– Reviewable premiums - 60 years– Guaranteed premiums - 50 years

• Minimum sum assured - £10,000

• Maximum sum assured - £20,000,000

• Minimum entry age – 17 years of age next birthday

• Maximum entry age – 75 years of age next birthday

• Maximum expiry age – 80 years of age

• Life Cover for people with HIV – we’ll provide core Life Cover of up to a maximum of £500,000 for a maximum of 20 years (subject to different criteria – min age of entry is 25, max age of entry is 60. Other terms and conditions apply).

TERM ASSURANCE FROM VITALITYLIFEKey points

VITALITY.CO.UK/LIFE

WHOLE OF LIFE COVER

VITALITY.CO.UK/LIFE4

• Guaranteed Insurability Option – increase cover levels as circumstances change without additional underwriting

• Guaranteed premiums – for the whole of your client’s life

• Flexible benefit options– Add Serious Illness Cover at any time (subject to underwriting)– Pays out on first or second death (on joint-life policies)– Option to protect policy against inflation (indexation)

• LifestyleCare Cover – can be added to a Whole of Life policy so your client can have early access to their cover earlier if they need to pay for care costs caused by degenerative conditions

WHOLE OF LIFE COVER FROM VITALITYLIFEKey points

VITALITY.CO.UK/LIFE5

• Guarantee loved ones a lump sum on death – there’s no maximum term on a Whole of Life Cover policy, so provided your client continues to pay their premiums and their claim is valid, they’ll receive a guaranteed payout

• Cover inheritance tax liability they may leave behind – clients can use Whole of Life Cover to insure against any inheritance tax billl there may be on their estate. As long as the correct level of cover is in place, any tax bill could be taken care of

• Help loved ones pay the bills – the lump sum could help your clients’ families pay other bills, for example funeral costs and every day living expenses

• Leaving a gift behind for loved ones – the lump sum could be used as a gift for loved ones.

BENEFITSHow could Whole of Life Cover help your clients?

VITALITY.CO.UK/LIFE6

• Our Whole of Life Cover comes with the option to add LifestyleCare Cover to the plan, a new category of protection which will help your clients pay for their later life care needs if they suffer a degenerative disease

PROTECTION FOR LONG-TERM NEEDSHow does Whole of Life Cover help your clients?

VITALITY.CO.UK/LIFE

LIFESTYLECARE COVER

VITALITY.CO.UK/LIFE8

WE ARE LIVING LONGER

Source: Coolgeography.co.uk 2010 and ONS based population projections 2010

UNITED KINGDOM2015 - 63.9 million people

UNITED KINGDOM2035 – 73.2 million people

Population over 75Population over 75 Population over 75Population over 75

10 % 15%

Dependency ratioDependency ratio Dependency ratioDependency ratio

75+

75+

Working population

Working population

UNITED KINGDOM1971 – 55.9 million people

VITALITY.CO.UK/LIFE9

Just like we sell term life

cover with serious illness

cover, we need to give

people flexibility with

whole of life

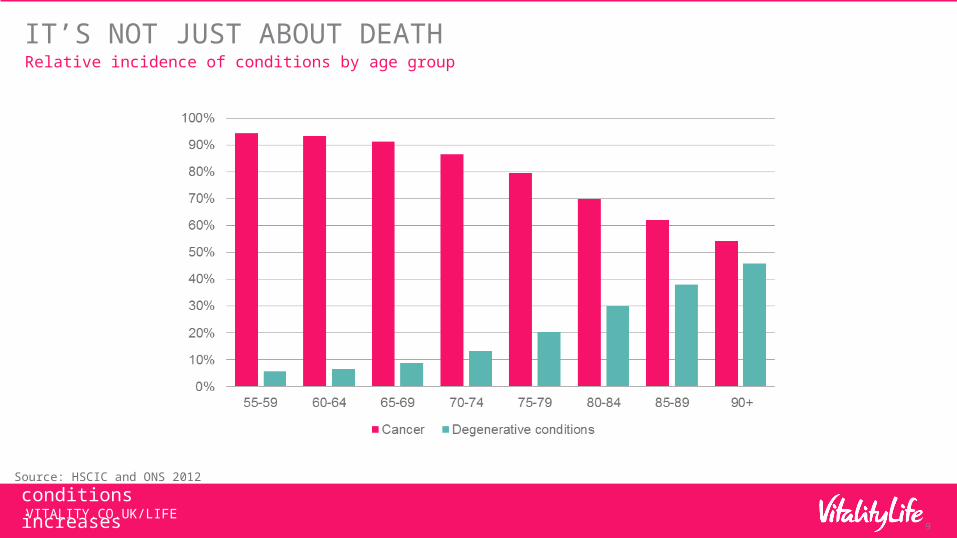

As we increasingly

survive physical illnesses

the risk

of degenerative

conditions increases

IT’S NOT JUST ABOUT DEATHRelative incidence of conditions by age group

Source: HSCIC and ONS 2012

VITALITY.CO.UK/LIFE10

Social care cap of £72,000 only caps nursing costs, not living costs

92% of men will never reach the cap so won’t receive any financial assistance from the tate

Personal care is free in Scotland, but means testing for care home costs

YEARS IN CARE

WE CAN’T RELY ON THE STATECumulative costs incurred after going into a London based care home

Care home costs

Nursing costs

CO

ST

(£

s)

Source: Based on VitalityLife analysis 2014, IFoA report 2014

VITALITY.CO.UK/LIFE11

• Only available as an option on Whole of Life Cover. It can’t be taken out on it’s own

• Minimum sum assured - £10,000

• Maximum sum assured – 100% of Whole of Life Cover amount, or £250,000

• Minimum entry age – 17 years of age next birthday

• Maximum entry age – 75 years of age next birthday

Why add LifestyleCare Cover to your client’s Whole of Life Cover?

• Provides lifetime protection – Life insurance that covers your clients for the whole of their lives

• Cover when it’s really needed – your clients can access their Whole of Life Cover early if they can no longer look after themselves due to degenerative illnesses

• Helping you improve your health – access to our healthy discounts and rewards with Vitality Optimiser (an additional monthly fee applies)

LIFESTYLECARE COVERKey points

VITALITY.CO.UK/LIFE12

Alzheimers Disease - resulting in permanent symptomsA definite diagnosis of Alzheimer’s disease by a Consultant Neurologist, Psychiatrist or Geriatrician. There must be permanent

clinical loss of ability to do all of the following:• Remember• Reason• Perceive, understand, express and give effect to ideasFor the above definition, the following are not covered: Other types of dementia Dementia - resulting in permanent symptomsA definite diagnosis of dementia by a Consultant Neurologist, Psychiatrist or Geriatrician. There must be permanent Clinical loss

of ability to do all of the following:• Remember• Reason• Perceive, understand, express and give effect to ideas Parkinson’s Disease – resulting in permanent symptomsA definite diagnosis of Parkinson’s disease by a Consultant Neurologist. There must be permanent clinical impairment of motor

function with associated tremor, muscle rigidity and postural instability. Parkinson’s disease secondary to drug abuse is not covered

CLAIMS TRIGGERS – LEVEL 1Severity Level 1 – 20% of LifestyleCare Cover amount

VITALITY.CO.UK/LIFE13

Permanent Inability to perform 3 ADLsPermanent failure of 3 or more of the following activities designed to assess whether you can look after yourself ever again:• Washing• Getting dressed and undressed• Maintaining personal hygiene• Feeding yourself• Getting between rooms• Getting in and out of bed

Persistent Confusional StatePersistent confusional state leading to inability to follow simple instructions, perform simple daily tasks and have insight into their

disability. A court order should also be granted. Stroke – resulting in permanent symptomsSevere stroke leading to inability to look after yourself ever again.

CLAIMS TRIGGERS – LEVEL 2Severity Level 2 – 100% of LifestyleCare Cover amount

VITALITY.CO.UK/LIFE14

45 year old £50k Cover

Whole Life Premium £38.11

With LifestyleCare Cover £50.30

• Adding £50k of LifestyleCare Cover to a £50k Whole of Life policy for a 45 year old will increase the monthly premium by around £12

HOW MUCH DOES IT COST – A CASE STUDY45 year old with £50k Whole of Life and £50k LifestyleCare Cover

VITALITY.CO.UK/LIFE15

• Level 1 - Provides a tax-effective solution for plans placed in trust (when 100% LAC is selected), because any benefit paid on death will be 100% of sum assured, and therefore does not fall foul of Gift With Reservation rules for IHT.

• Level 1 and 2 - When you want to use the cover for IHT planning as well as paying for care needs

LIFESTYLECARE COVER PROTECTORGives clients a choice of reinstatement options to protect their benefits following a claim

Severity Level 1 - Diagnosis with lifestyle

impact

Severity Level 2 - Loss of

independence

DeathStart of plan

LifestyleCare Cover no Protector £10k £40k nil TOTAL PAYOUT = £50k

LifestyleCare Cover Protector (Level 1) £10k £50k nil TOTAL PAYOUT = £60k

LifestyleCare Cover Protector (Level 1 & 2) £10k £50k £50k TOTAL PAYOUT = £110k

VITALITY.CO.UK/LIFE16

Whole Life Premium £38.11

With LifestyleCare Cover £50.30

With Protector level 1 and 2 £75.08

• Adding Protectors at level 1 and 2 increases the premium by another £15 a month on top of the standard LCC premium.

• The cost of this comprehensive cover may be too high for many people, but by adding VO to the plan, cover can be made more affordable

HOW MUCH DOES IT COST – A CASE STUDY45 year old with £50k Whole of Life and £50k LifestyleCare Cover

Whole Life Premium £38.11

With LifestyleCare Cover £50.30

With Protector level 1 and 2 £75.08

With Vitality Optimiser* £48.35

26% increase in premium for access to more than twice the

cover!

26% increase in premium for access to more than twice the

cover!

VITALITY.CO.UK/LIFE17

Having Vitality Optimiser on your plan not only makes your initial premium lower, it gives you access to our healthy discounts and rewards. And taking steps to improve your health also makes you less likely to suffer from illnesses typically acquired in later life:

•35% lower risk of heart disease and stroke

•50% lower risk of type 2 diabetes

•68% lower risk of hip fracture

•30% lower risk of falls (among older adults)

BEING HEALTHIER IS AN ANTIDOTE TO AGEINGA healthy lifestyle reduces the risk of later life illnesses

Source: NHS, 2014

VITALITY.CO.UK/LIFE18

• 75% of advisers agree that later life protection products present an opportunity to grow the market

• LifestyleCare Cover is NOT Long-Term Care

• You don’t need to be a specialist in care

• State benefits can be a minefield - Focus on customer needs and how these products can help

• It’s not just for clients at retirement

• If you can sell Serious Illness Cover with Term Life Cover you can sell LifestyleCareCover with Whole of Life!

THE OPPORTUNITY FOR LATER LIFE PROTECTION PRODUCTSKey points

VITALITY.CO.UK/LIFE