1 the games economists play: interactive public policy capital campus texas july 9, 2008 copies of...

TRANSCRIPT

1

The Games Economists Play: Interactive Public Policy

Capital Campus TexasJuly 9, 2008

copies of this presentation can be found atwww.antolin-davies.com

Please sit as follows:

1. One person at each consumer station.

2. Two people at each insurer station.

Ideally, we need one person who is comfortable with basic math at each insurer station.

2

The purpose of this simulation is to create a competitive market and to observe the market as it achieves equilibrium.

In this simulation, you will experience real market forces. The same human traits and behaviors that govern real markets exist in the simulation.

What are artificial are your surroundings. The market forces are real.

3

The Players and the Goals

In this experiment, there are CONSUMERS and INSURERS.

INSURERS sell INSURANCE.

CONSUMERS buy FOOD and INSURANCE.

4

Consumers

Each consumer has $20 to spend.

A unit of food costs $1.

5

$20

Food Eaten Happiness0 01 1002 1413 1734 2005 2246 2457 2658 2839 300

10 316

The more food the consumer eats, the happier the consumer becomes.

Consumers: The Catch

Each consumer faces some risk of badness.

6

vs.

If badness befalls the consumer, the consumer loses all of the purchased food.

Consumers: The Insurance

But, consumers can purchase insurance contracts from the insurance companies.

7

Each contract pays the consumer one unit of food if badness befalls that consumer.

Consumers: Example

Suppose a consumer can purchase insurance contracts at a price of $0.50 each (the price of food is always $1 each).

8

$20

Suppose that the consumer spends $5 on insurance contracts. The remaining $15 is automatically spent on food.

10 insurance contracts

15 food

Consumers: Example

If badness does not befall the consumer, the consumer eats 15 units of food and receives 387 happiness.

9

Food Eaten Happiness10 31611 33212 34613 36114 37415 38716 40017 41218 42419 43620 447

Food Eaten Happiness10 31611 33212 34613 36114 37415 38716 40017 41218 42419 43620 447

Consumers: Example

If badness does befall the consumer, the 15 units of food disappear, each insurance contract pays $1.00 (which buys 1 unit of food), and the consumer receives 316 happiness.

10

Consumers

Each consumer’s goal: Maximize expected happiness

More insurance means

More food when badness befalls.

Less food when badness does not befall.

Too little insurance is bad. Too much insurance is also bad.

11

Insurers

Each insurer can write as many insurance contracts as liked and charge any price.

12

Insurers

If badness does not befall the consumer, the insurer walks away with the money the consumer paid for the contracts.

13

$ $ $

$ $ $

Insurers

If badness does befall the consumer, the insurer pays the consumer $1.00 for each contract the insurer sold the consumer.

14

Insurers: Example

Suppose an insurer sells Consumer A six contracts for $0.60 each, and sells Consumer B five contracts for $0.30 each.

15

The insurer collects $3.60 from Consumer A and $1.50 from Consumer B.

$3.60

$1.50

$5.10

Revenue =

Insurers: Example

Suppose badness befalls Consumer B but not Consumer A.

16

The insurer owes Consumer B $1.00 for each contract Consumer B purchased.

$5.00

$5.10

Revenue =

$5.00

Cost =

$0.10

Profit =

Insurers: Example

Suppose badness befalls Consumer A but not Consumer B.

17

The insurer owes Consumer A $1.00 for each contract Consumer A purchased.

$6.00

$5.10

Revenue =

$6.00

Cost =

$0.90

Loss =

(Insurers do not need a cash reserve to cover policies.)

Insurers

Each insurer’s goal: Maximize expected profit

Insurers can ask whatever prices they like for contracts

Too low a price is bad. Too high a price is also bad.

18

19

Type 1

10%

Consumer Types

There are five types of consumer. Each faces a different probability of badness.

Type 2

20%

Type 3

30%

Type 4

40%

Type 5

50%

20

Type ?

?

Consumer Types

Each consumer knows which type he/she is, but insurers don’t.

The average probability of badness is 30%.

The Objects

21

= 1 dollar

= 10 cents (each)

= insurance contract(s)

= 5 dollars

Contracts

22

12 6

$4.80

The Mechanics

23

Agent

Insurers Consumers

Head Office

$0.30Yes

The Mechanics

24

Agent

Insurers Consumers

Head Office

The Mechanics

25

Agent

Insurers Consumers

Head Office

Ready to begin…

26

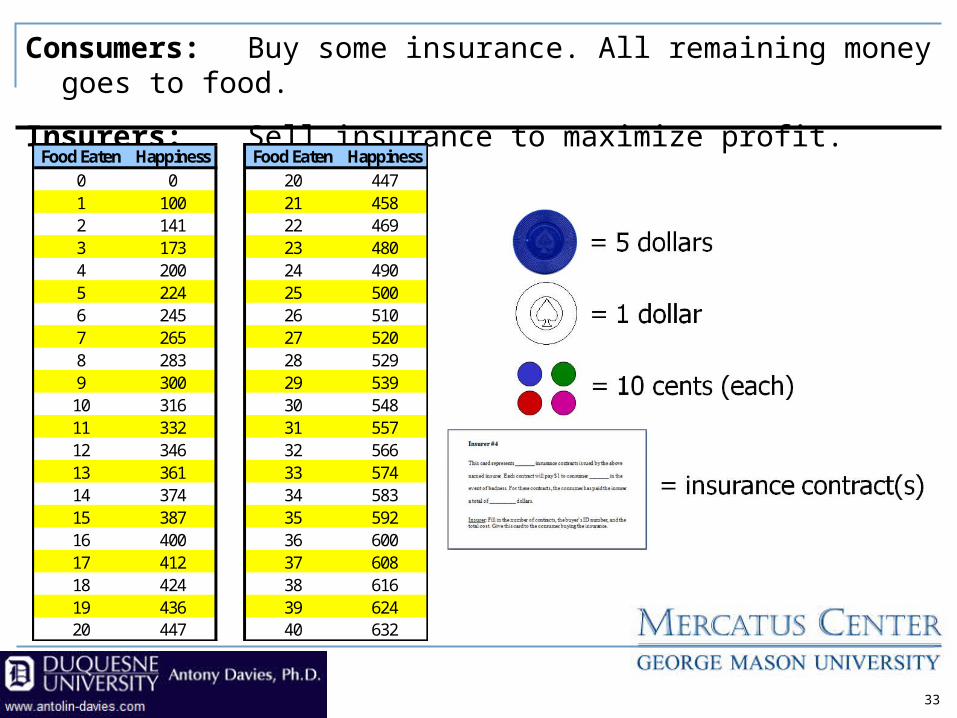

Consumers: Buy some insurance. All remaining money goes to food.

Insurers: Sell insurance to maximize profit.

27

Food Eaten Happiness Food Eaten Happiness0 0 20 4471 100 21 4582 141 22 4693 173 23 4804 200 24 4905 224 25 5006 245 26 5107 265 27 5208 283 28 5299 300 29 539

10 316 30 54811 332 31 55712 346 32 56613 361 33 57414 374 34 58315 387 35 59216 400 36 60017 412 37 60818 424 38 61619 436 39 62420 447 40 632

Accounting Phase

Consumers report:

• Contracts purchased, cost, and from which insurer(s)

28

29

1 no2 YES3 no4 YES5 no6 no7 no8 YES9 no10 YES11 no12 YES13 no14 no15 no16 YES17 no18 no19 no20 no

BadnessConsumer

0

5

10

15

20

25

30

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Consumer #

Food Purchased Contracts Purchased Food Consumed

30

1 no2 YES3 no4 YES5 no6 no7 no8 YES9 no10 YES11 no12 YES13 no14 no15 no16 YES17 no18 no19 no20 no

BadnessConsumer

-$20.00

-$15.00

-$10.00

-$5.00

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

1 2 3 4 5 6 7 8 9 10

Insurer #

Revenue Indemnities Profit

Mandated Insurance

Concerned that some consumers do not have enough insurance coverage, the law stipulates that an insurer may not sell less than 35 contracts to a buyer unless the buyer has already purchased at least 35 contracts (from any insurer) this round.

31

Ready to begin…

32

Consumers: Buy some insurance. All remaining money goes to food.

Insurers: Sell insurance to maximize profit.

33

Food Eaten Happiness Food Eaten Happiness0 0 20 4471 100 21 4582 141 22 4693 173 23 4804 200 24 4905 224 25 5006 245 26 5107 265 27 5208 283 28 5299 300 29 539

10 316 30 54811 332 31 55712 346 32 56613 361 33 57414 374 34 58315 387 35 59216 400 36 60017 412 37 60818 424 38 61619 436 39 62420 447 40 632

34

Accounting Phase

Consumers report:

• Contracts purchased, cost, and from which insurer(s)

35

1 no2 no3 no4 no5 no6 YES7 no8 YES9 YES

10 no11 no12 no13 no14 YES15 no16 no17 no18 YES19 no20 YES

BadnessConsumer

0

20

40

60

80

100

120

140

160

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Consumer #

Food Purchased Contracts Purchased Food Consumed

36

1 no2 no3 no4 no5 no6 YES7 no8 YES9 YES

10 no11 no12 no13 no14 YES15 no16 no17 no18 YES19 no20 YES

BadnessConsumer

-$100.00

-$50.00

$0.00

$50.00

$100.00

$150.00

1 2 3 4 5 6 7 8 9 10

Insurer #

Revenue Indemnities Profit

Mandatory Insurance

Concerned that some consumers do not have any insurance, the law requires that all consumers buy a total of no less than 35 contracts this round.

37

Ready to begin…

38

Consumers: Buy some insurance. All remaining money goes to food.

Insurers: Sell insurance to maximize profit.

39

Food Eaten Happiness Food Eaten Happiness0 0 20 4471 100 21 4582 141 22 4693 173 23 4804 200 24 4905 224 25 5006 245 26 5107 265 27 5208 283 28 5299 300 29 539

10 316 30 54811 332 31 55712 346 32 56613 361 33 57414 374 34 58315 387 35 59216 400 36 60017 412 37 60818 424 38 61619 436 39 62420 447 40 632

40

Accounting Phase

Consumers report:

• Contracts purchased, cost, and from which insurer(s)

41

1 no2 YES3 no4 no5 YES6 no7 no8 no9 no

10 no11 YES12 no13 no14 YES15 YES16 no17 no18 no19 no20 YES

BadnessConsumer

0

10

20

30

40

50

60

70

80

90

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Consumer #

Food Purchased Contracts Purchased Food Consumed

42

1 no2 YES3 no4 no5 YES6 no7 no8 no9 no

10 no11 YES12 no13 no14 YES15 YES16 no17 no18 no19 no20 YES

BadnessConsumer

-$40.00

-$20.00

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

1 2 3 4 5 6 7 8 9 10

Insurer #

Revenue Indemnities Profit

Results…

43

44

Insurance Contracts Purchased

0

100200

300400

500

600700

800

Type 1 Type 2 Type 3 Type 4 Type 5

Free Market Required Minimum Required PurchaseMandatoryMandated

45

Food Purchased

0

50100

150

200250

300

350400

450

Type 1 Type 2 Type 3 Type 4 Type 5

Free Market Mandated Mandatory

46

Happiness

0

2000

4000

6000

8000

10000

Type 1 Type 2 Type 3 Type 4 Type 5

Free Market Mandated Mandatory

47

Insurance Price per Contract

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

Free Market Mandated Mandatory

48

Insurance Profits

($200.00)

($150.00)

($100.00)

($50.00)

$0.00

$50.00

$100.00

$150.00

$200.00

Type 1 Type 2 Type 3 Type 4 Type 5

Free Market Required Minimum Required PurchaseMandatoryMandated

49

Happiness

0

2000

4000

6000

8000

10000

Type 1 Type 2 Type 3 Type 4 Type 5

Free Market (full info) Free Market Mandated Mandatory

50

Insurance Contracts Purchased

0

100

200

300

400

500

600

700

800

Type 1 Type 2 Type 3 Type 4 Type 5

Free Market (full info) Free Market Mandated Mandatory

51

Food Purchased

0

50100

150

200250

300

350400

450

Type 1 Type 2 Type 3 Type 4 Type 5

Free Market (full info) Free Market Mandated Mandatory

52

Insurance Price per Contract

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

Free Market (full info) Free Market Mandated Mandatory

• Forces lower risk people to consume quantities of goods that they may not want to consume.

• End result is a transfer of wealth from low risk to high risk people.

• A better solution is simply to tax the low risk people, give the money to the high risk people and let them buy what they want.

53

What is the effect of insurance mandates?

But, we have to do something!

Look at what has been happening to the cost of health care over time!

54

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

1980

1981

1982

1983

1984

1985

1986

1987

1988

19

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

06

Price of Medical Care Consumer Prices Excluding Medical Care

55

Source: Bureau of Labor Statistics (www.economy.com)

Price of medical care has increased 349% since 1980 versus 135% for other consumer prices.

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

1980

1981

1982

1983

1984

1985

1986

1987

1988

19

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

06

Price of Physicians Services

Price of Hospital Services

Price of Prescription Drugs and Medical Supplies

56

Source: Bureau of Labor Statistics (www.economy.com)

Hospital services + 576%

Drugs and supplies + 402%

Physician services + 282%

Other consumer prices+ 135%

57

Source: Bureau of Labor Statistics (www.economy.com)

-800%

-600%

-400%

-200%

0%

200%

400%

600%

Co

lle

ge

Tu

itio

n

Me

dic

al C

are

Sta

te/L

oca

l Go

v't

(pe

r-c

ap

ita

)

Fed

era

l Go

v't

(pe

r-c

ap

ita

)

Ho

usi

ng

Foo

d

Ga

soli

ne

Ne

w C

ars

1 G

Hz

of

Co

mp

uti

ng

Po

we

r

Gro

wth

in P

rice

s 1

98

0

-20

06

But, the cost of health care is only half of the picture.

What has been happening to the quality of health care?

58

How do we measure the quality of health care?

1. What is “quality?”

2. How do we account for health care that has become routine but didn’t exist in the past (e.g., pre-natal care)?

3. How do we weigh qualities across different types of care (e.g., dental vs. catastrophic)?

59

How does one measure the quality of health care?

An easy measure of the effectiveness of health care is the mortality rate.

Some health care may have little or no impact on the mortality rate (e.g., orthodonture).

But, it is not unreasonable to assume that the qualities of other types of health care grow at similar rates. 60

61

7.5

8.0

8.5

9.0

9.5

10.0

1960

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Deaths per 1,000 People

Source: Statistical Abstract of the United States, 2008, Table 77.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1960

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Infant Mortality per 1,000 Live Births

62

Source: Statistical Abstract of the United States, 2008, Table 77.

63

Source: Statistical Abstract of the United States, 2008, Table 110.

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Deaths by Influence and Pneumonia (per 100,000 population)Deaths by Influenza and Pneumonia (per 100,000 population)

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

1960

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Mill

ions

Actual Deaths in the Current Year Deaths at the 1960 Mortality Rate

64

Source: Derived from Statistical Abstract of the United States, and the Bureau of Economic Analysis.

What does increased cost of health care buy us?

400,000 lives saved annually

But, what about the uninsured?

They aren’t sharing in this increased quality of health care.

65

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

66

Source: Income, Poverty, and Health Insurance Coverage in the U.S.: 2006, US Census Bureau.

The percentage of the population that is uninsured has remained stable over time.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

1999 2000 2001 2002 2003 2004 2005 2006

Under 18 18 to 24 25 to 34 35 to 44 45 to 54 55 to 64

67

Source: Income, Poverty, and Health Insurance Coverage in the U.S.: 2006, US Census Bureau.

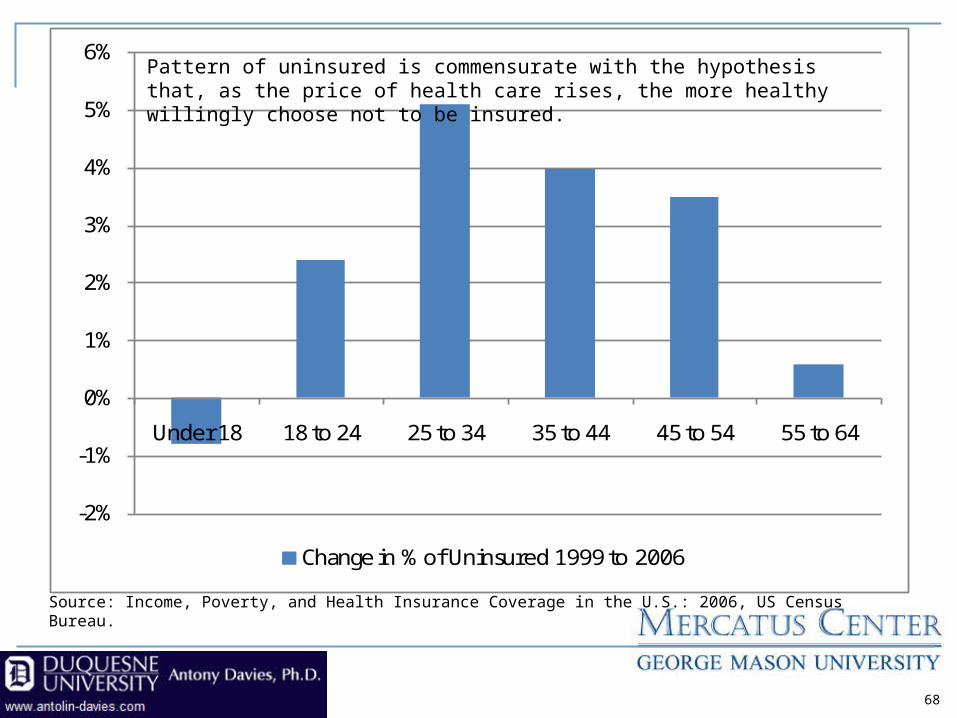

Percentage of uninsured has remained relatively constant for the young and the old – the two groups for whom there is the least incentive to tradeoff health care for spending on other things.

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Under 18 18 to 24 25 to 34 35 to 44 45 to 54 55 to 64

Change in % of Uninsured 1999 to 2006

68

Source: Income, Poverty, and Health Insurance Coverage in the U.S.: 2006, US Census Bureau.

Pattern of uninsured is commensurate with the hypothesis that, as the price of health care rises, the more healthy willingly choose not to be insured.

A free choice to purchase is a vote, but with three important differences.

Political vote: One size fits all.

Free market vote: Multiple sizes for multiple recipients.

Political vote: Speed of change is driven by the election cycle.

Free market vote: Speed of change is driven by the accounting cycle.

Political vote: Signal is distorted because the vote is for a “bundle” of issues embodied by one candidate.

Free market vote: Signal is clear because the vote is for a specific issue. 69

Voting for the “right” amount of insurance

70

The Games Economists Play: Interactive Public Policy

Capital Campus TexasJuly 9, 2008

copies of this presentation can be found atwww.antolin-davies.com