1 tax treaty and legislative developments andrew d. barkin, btmu (moderator) joseph k. dowley,...

TRANSCRIPT

1

TAX TREATY AND LEGISLATIVE DEVELOPMENTS

Andrew D. Barkin, BTMU (Moderator)Joseph K. Dowley, McKenna Long & Aldridge

Yaron Z. Reich, Cleary Gottlieb Steen & Hamilton Thomas A. Stout, Jr., KPMG LLP

Institute of International BankersAnnual Seminar on U.S. Taxation of

International Banks25 June 2008

Thomas A. Stout, Jr.

Washington National TaxWashington, DC

June 25, 2008

New York

Thomas A. Stout, Jr.

Washington National TaxWashington, DC

June 25, 2008

New York

TAX

Tax Treaty Update

3

The information contained herein is general in nature and based on The information contained herein is general in nature and based on authorities that are subject to change. Applicability to specific situations is to authorities that are subject to change. Applicability to specific situations is to

be determined through consultation with your tax adviser.be determined through consultation with your tax adviser.

Circular 230 became effective for tax advice rendered after June 20, 2005. Circular 230 became effective for tax advice rendered after June 20, 2005. Therefore, the following Circular 230 Reliance Opinion Opt-out Disclaimer Therefore, the following Circular 230 Reliance Opinion Opt-out Disclaimer Language should also be prominently disclosed in the attached document, Language should also be prominently disclosed in the attached document, without any revision or modification and must be in all capital letters. The without any revision or modification and must be in all capital letters. The Circular 230 Reliance Opinion Opt-out Disclaimer Language is as follows:Circular 230 Reliance Opinion Opt-out Disclaimer Language is as follows:

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE PRESENTERS TO BE USED, AND CANNOT BE WRITTEN BY THE PRESENTERS TO BE USED, AND CANNOT BE

USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON

ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED

HEREIN.HEREIN.

The information contained herein is general in nature and based on The information contained herein is general in nature and based on authorities that are subject to change. Applicability to specific situations is to authorities that are subject to change. Applicability to specific situations is to

be determined through consultation with your tax adviser.be determined through consultation with your tax adviser.

Circular 230 became effective for tax advice rendered after June 20, 2005. Circular 230 became effective for tax advice rendered after June 20, 2005. Therefore, the following Circular 230 Reliance Opinion Opt-out Disclaimer Therefore, the following Circular 230 Reliance Opinion Opt-out Disclaimer Language should also be prominently disclosed in the attached document, Language should also be prominently disclosed in the attached document, without any revision or modification and must be in all capital letters. The without any revision or modification and must be in all capital letters. The Circular 230 Reliance Opinion Opt-out Disclaimer Language is as follows:Circular 230 Reliance Opinion Opt-out Disclaimer Language is as follows:

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE PRESENTERS TO BE USED, AND CANNOT BE WRITTEN BY THE PRESENTERS TO BE USED, AND CANNOT BE

USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON

ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED

HEREIN.HEREIN.

4© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Recently Ratified Tax TreatiesRecently Ratified Tax Treaties

Tax treaties ratified in 2007Tax treaties ratified in 2007GermanyGermanyBelgiumBelgiumDenmarkDenmarkFinlandFinland

Issue: Mandatory arbitrationIssue: Mandatory arbitration

5© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Tax Treaties Pending RatificationTax Treaties Pending Ratification

Tax treaties signed and transmitted to Senate for approvalTax treaties signed and transmitted to Senate for approval

CanadaCanada

IcelandIceland

BulgariaBulgaria

StatusStatus

Treasury technical explanations completed (joint TE with Canada)Treasury technical explanations completed (joint TE with Canada)

Foreign Relations Subcommittee hearing pending Foreign Relations Subcommittee hearing pending

IssuesIssues

Mandatory arbitration (Canada)Mandatory arbitration (Canada)

Permanent establishment (Canada)Permanent establishment (Canada)

Treatment of hybrids (Canada)Treatment of hybrids (Canada)

Limitation on benefits (Iceland)Limitation on benefits (Iceland)

6© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Anti-treaty Shopping LegislationAnti-treaty Shopping Legislation

Doggett BillDoggett Bill

H.R. 3160H.R. 3160

Limits treaty withholding benefits on deductible Limits treaty withholding benefits on deductible payments to treaty rate of foreign group parentpayments to treaty rate of foreign group parent

““Doggett Lite”Doggett Lite”

H.R. 6275, Alternative Minimum Tax Relief Act of 2008H.R. 6275, Alternative Minimum Tax Relief Act of 2008

Limits treaty withholding benefits on deductible Limits treaty withholding benefits on deductible payments if the country of the foreign parent lacks a payments if the country of the foreign parent lacks a treatytreaty

7© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Tax Treaties in Active NegotiationTax Treaties in Active Negotiation

Negotiations completedNegotiations completed

NorwayNorway

MaltaMalta

Italy (Ratified by US with reservation)Italy (Ratified by US with reservation)

Focus of ongoing negotiations; old treaties with no Focus of ongoing negotiations; old treaties with no limitation on benefitslimitation on benefits

HungaryHungary

PolandPoland

RECENT TREATY DEVELOPMENTS AFFECTING PERMANENT ESTABLISHMENTS (“PEs”)

9

Overview

“Authorized OECD approach” for attributing profits to PEs under Article 7 of OECD Model Treaty

Implementation

– OECD: Revised draft Commentary to Model Treaty (April 2008)

– US position: effective only if treaty countries agree

– Belgium, Germany, Japan, UK (effective); Bulgaria, Canada, Iceland (pending)

– Still awaiting re-proposed global dealing regulations

Technical Explanations (“TEs”) to new Belgian treaty and German protocol articulate a controversial new standard for the “consistency rule” between treaties and domestic law

10

OECD Approach to Attributing Profits to PEs

Authorized OECD approach to attributing profits to PEs

– Article 7(3): “[W]here an enterprise of a Contracting State carries on business in the other Contracting State through a permanent establishment situated therein, there shall in each Contracting State be attributed to that permanent establishment the profits that it might be expected to make if it were a distinct and independent enterprise engaged in the same or similar activities under the same or similar conditions.”

– Authorized OECD approach: applies a transfer pricing functional analysis to determine the profits attributable to a PE

11

OECD Approach to Attributing Profits to PEs

Status of OECD approach

– Report Parts I (General Considerations), II (Banks) and III (Global Trading) finalized (December 2006); Part IV (insurance) in draft form (August 2007)

– Draft commentary to existing Article 7 released and updated (April 2007, April 2008)

– Work on revising Article 7 and commentary for new treaties

– Implementation on a country-by-country basis

12

OECD Approach to Attributing Profits to PEs

Summary of Authorized OECD Approach

– Functionally separate entity approach (not single entity)

– Two step approach to attribute profit

– Use functional and factual analysis to hypothesize the PE as a distinct and separate enterprise

– Application of the arm’s length principle to the hypothetical enterprise in accordance with the 1995 Guidelines (by analogy)

13

OECD Approach to Attributing Profits to PEs

Summary of Authorized OECD Approach (cont’d)

– Hypothesizing the PE as a distinct and separate entity

– PE has the same credit rating as the whole enterprise

– Create separate balance sheet for hypothesized PE, based on an “ownership model”

– In the case of financial institutions, location of the “key entrepreneurial risk-taking” (“KERT”) functions determines where assets are used, where risk is borne and where capital may need to be imputed

– Recognize interbranch dealings when they represent a “real and identifiable event” and are supported by a functional analysis; applyArticle 9 arm’s length principles (by analogy)

– Same rules apply to “dependent agent” PEs, resulting in 2 taxpayers in a country – (1) the dependent agent affiliate and (2) the PE

14

OECD Approach to Attributing Profits to PEs

Capital Attribution

– Determine risks attributable to PE, generally using standard bank regulatory (Basel Accord) risk-weighting methods to determine assets and off-balance sheet items attributable to each PE

– Approved capital attribution approaches

– In proportion to risk-weighted assets and risks

– Thin capitalization (independent bank model)

– Safe harbor: quasi -thin capitalization (minimum bank regulatory capital for independent bank)

– Risk of double taxation from having more than one authorized approach

– New draft commentary: Home country should accept capital attribution by PE “host” country so long as (1) difference results from conflicting domestic law methods and (2) host country used an acceptable OECD method and results are arm’s length

15

OECD Approach to Attributing Profits to PEs

Key Entrepreneurial Risk-Taking (KERT) Functions

– Location(s) where active decision-making regarding the taking on and day-to-day management of risks takes place

– Treat KERT-function location as tax owner of asset

– Impute equity and debt capital for purposes of determining deductible interest expense

– Residual profit allocation to KERT-function location

16

OECD Approach to Attributing Profits to PEs

Flaws in the authorized OECD approach

– Lack of consistent and uniform method for capital allocation exposes taxpayers to multiple taxation

– Draft commentary’s solution is imperfect

– KERT “ownership model” requires fragmentation and constant adjustments in ownership of assets and liabilities by PEs; collateral implications for withholding and reporting of payments in and out of PE

– Failure to practically address the cross-border securities dealing activities of financial institutions that give rise to “dependent agent” PEs

17

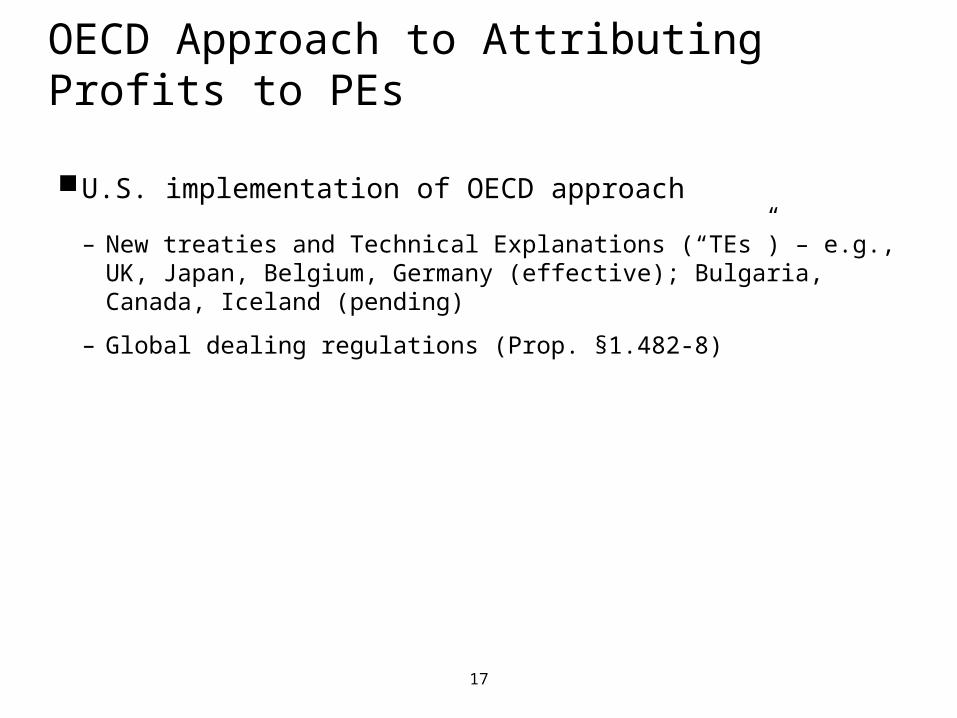

OECD Approach to Attributing Profits to PEs

U.S. implementation of OECD approach

– New treaties and Technical Explanations (“TEs”) – e.g., UK, Japan, Belgium, Germany (effective); Bulgaria, Canada, Iceland (pending)

– Global dealing regulations (Prop. §1.482-8)

18

OECD Approach to Attributing Profits to PEs

New Belgian treaty

– i. Protocol:

“It is understood that the business profits to be attributed to a permanent establishment shall include only the profits derived from the assets used, risks assumed and activities performed by the permanent establishment. The principles of the OECD Transfer Pricing Guidelines will apply for purposes of determining the profits attributable to a permanent establishment, taking into account the different economic and legal circumstances of a single entity. Accordingly, any of the methods described therein as acceptable methods for determining an arm’s length result may be used to determine the income of a permanent establishment so long as those methods are applied in accordance with the Guidelines. In particular, in determining the amount of attributable profits, the permanent establishment shall be treated as having the same amount of capital that it would need to support its activities if it were a distinct and separate enterprise engaged in the same or similar activities. With respect to financial institutions other than insurance companies, a Contracting State may determine the amount of capital to be attributed to a permanent establishment by allocating the institution’s total equity between its various offices on the basis of the proportion of the financial institution’s risk-weighted assets attributable to each of them. In the case of an insurance company, there shall be attributed to a permanent establishment not only premiums earned through the permanent establishment, but that portion of the insurance company's overall investment income from reserves and surplus that supports the risks assumed by the permanent establishment.”

19

OECD Approach to Attributing Profits to PEs

Technical Explanation

– “However, risk-weighting is more complicated than the method prescribed by Section 1.882-5. Accordingly, to ease this administrative burden, taxpayers may choose to apply the principles of Treas. Reg. Section 1.882-5(c) to determine the amount of capital allocable to its U.S. permanent establishment, in lieu of determining its allocable capital under the risk-weighed capital allocation method provided by the Protocol, even if it has otherwise chosen to apply the principles of Article 7 rather than the effectively connected income rules of U.S. domestic law.”

20

Treaty - Code Consistency Rule

Consistency Rule – New articulation under the TEs(see IIB October 1, 2007 letter)

– General rule is that a Treaty shall not restrict any exclusion, exemption, deduction, credit or other allowance allowed under the Code (see Belgian treaty, Article 1(2)) Thus, taxable income is usually filtered through the Code, and then through the Treaty.

– However, a taxpayer cannot choose among the provisions of the Code and a Treaty in order to minimize tax. This is the Consistency Rule.

21

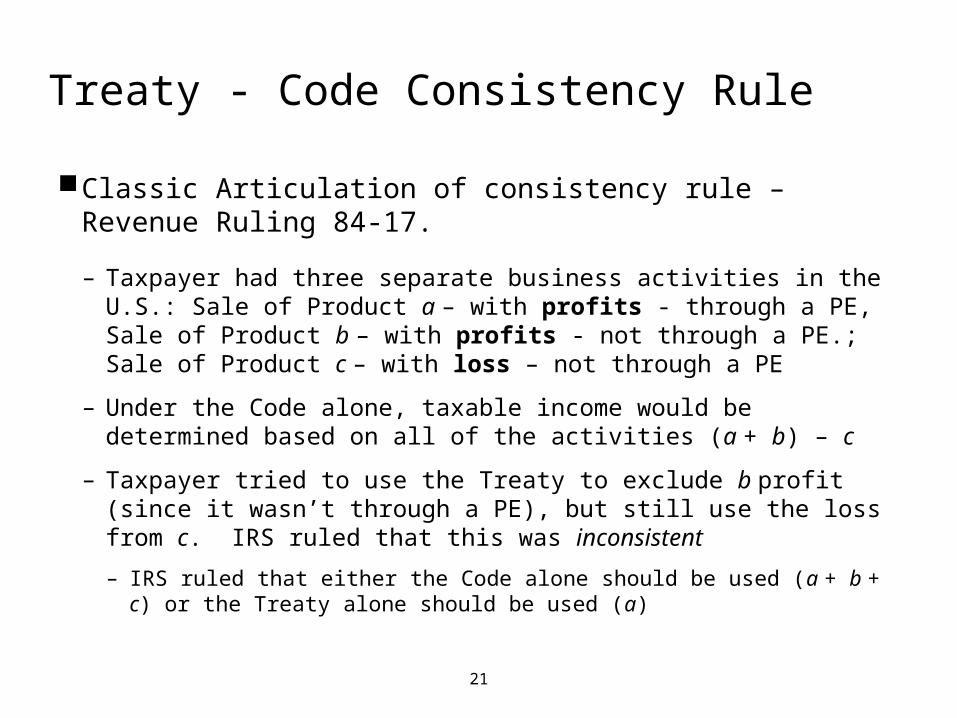

Treaty - Code Consistency Rule

Classic Articulation of consistency rule – Revenue Ruling 84-17.

– Taxpayer had three separate business activities in the U.S.: Sale of Product a – with profits - through a PE, Sale of Product b – with profits - not through a PE.; Sale of Product c – with loss – not through a PE

– Under the Code alone, taxable income would be determined based on all of the activities (a + b) – c

– Taxpayer tried to use the Treaty to exclude b profit (since it wasn’t through a PE), but still use the loss from c. IRS ruled that this was inconsistent

– IRS ruled that either the Code alone should be used (a + b + c) or the Treaty alone should be used (a)

22

Treaty - Code Consistency Rule

Technical Explanations under new Belgian Treaty and German Protocol

– Taxpayer must choose between applying Article 7 or Code provisions in their entirety

– Example: Bank recognizing interbranch swaps under Article 7 must also use OECD approach to determine U.S. income from its loan book (i.e. can’t rely on domestic rules)

– Despite proposed Treasury global dealing regulations

23

Treaty - Code Consistency Rule

Unanswered Questions — When is OECD approach “inconsistent” with Code/regulations?

– Only ECI-related provisions?

– Section 864 safe harbor for trading in stocks and securities?

– Reg. section 1.882-5 vs. treaty risk-weighting method for interest allocation? TEs say taxpayer can elect Article 7 and Reg. section 1.882-5

– Using domestic rules to fill in details under a treaty approach, and vice versa?

24

Treaty - Code Consistency Rule

Recent developments

– Comments from Steven Musher, IRS associate chief counsel (International) at March 2008 IIB Washington Conference:

– New consistency rule should be applied separately to each line of business

– Contrary to Belgian and German TEs, a foreign bank can apply Article 7/proposed global dealing regulations’ interbranch transaction rules to derivatives business and Code rules to bank lending business

– Test is to compare totality of results for line of business under Code vs. under treaty

– Treasury still considering procedural and substantive issues of how to modify the position expressed in the Belgian/German TEs

– Further clarification is expected in the yet-to-be released TEs to the Canadian, Bulgarian and Iceland treaties

25© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Thomas A. Stout, Jr.

Washington National TaxWashington, DC

June 25, 2008

New York

Thomas A. Stout, Jr.

Washington National TaxWashington, DC

June 25, 2008

New York

TAX

Tax Legislation Update

26© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

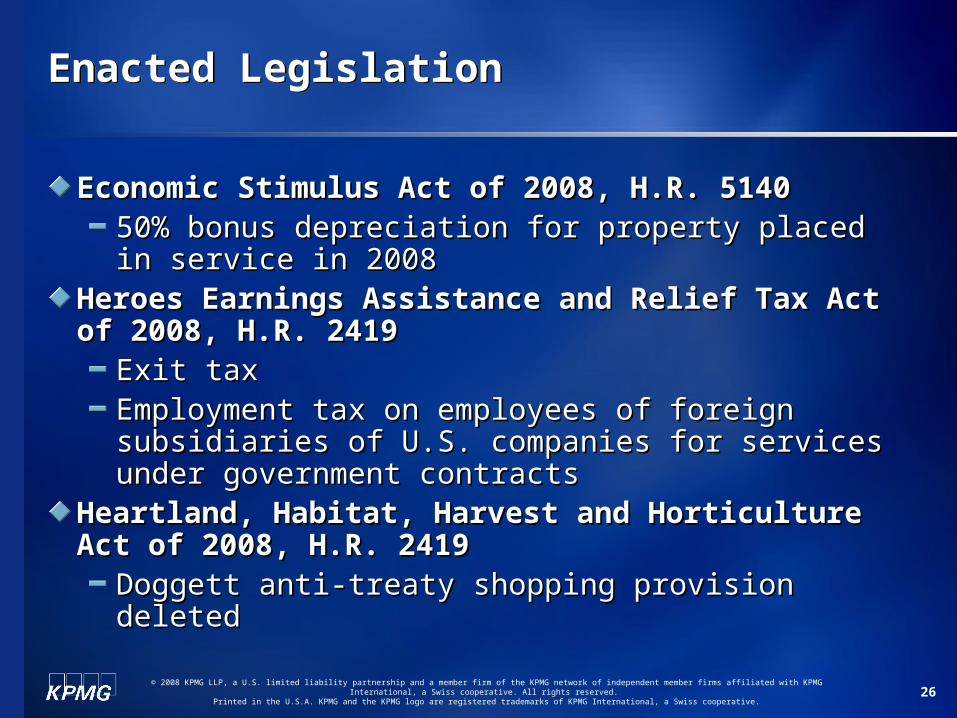

Enacted LegislationEnacted Legislation

Economic Stimulus Act of 2008, H.R. 5140Economic Stimulus Act of 2008, H.R. 514050% bonus depreciation for property placed in service in 50% bonus depreciation for property placed in service in 20082008

Heroes Earnings Assistance and Relief Tax Act of Heroes Earnings Assistance and Relief Tax Act of 2008, H.R. 24192008, H.R. 2419

Exit tax Exit tax Employment tax on employees of foreign subsidiaries of Employment tax on employees of foreign subsidiaries of U.S. companies for services under government U.S. companies for services under government contractscontracts

Heartland, Habitat, Harvest and Horticulture Act of Heartland, Habitat, Harvest and Horticulture Act of 2008, H.R. 24192008, H.R. 2419

Doggett anti-treaty shopping provision deletedDoggett anti-treaty shopping provision deleted

27© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Pending Tax LegislationPending Tax Legislation

Housing Assistance Tax Act of 2008, H.R. 5270Housing Assistance Tax Act of 2008, H.R. 5270

Broker reporting of basis in securities transactionsBroker reporting of basis in securities transactions

One-year delay in worldwide interest allocationOne-year delay in worldwide interest allocation

Taxpayer Assistance and Simplification Act of 2008, Taxpayer Assistance and Simplification Act of 2008, H.R. 5719H.R. 5719

Amends return preparer penalty standardAmends return preparer penalty standard

Renewable Energy and Conservation Tax Act, H.R. Renewable Energy and Conservation Tax Act, H.R. 27762776

Revenue offsets targeting oil and gas industryRevenue offsets targeting oil and gas industry

28© 2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Pending Tax LegislationPending Tax Legislation

Renewable Energy and Job Creation Act of 2008, H.R. 6049Renewable Energy and Job Creation Act of 2008, H.R. 6049

Extends expiring provisions such as active financing exception to Extends expiring provisions such as active financing exception to Subpart F for one yearSubpart F for one year

Revenue offsetsRevenue offsetsModify tax treatment of offshore nonqualified deferred compensationModify tax treatment of offshore nonqualified deferred compensation

Delay implementation of worldwide interest allocation for 10 yearsDelay implementation of worldwide interest allocation for 10 years

Alternative Minimum Tax Relief Act of 2008, H.R. 6275Alternative Minimum Tax Relief Act of 2008, H.R. 6275

Extends individual AMT reliefExtends individual AMT relief

Revenue offsetsRevenue offsetsRequire information reporting on credit card transactionsRequire information reporting on credit card transactions

Doggett LiteDoggett Lite

Taxation of income of carried interests in partnerships as ordinaryTaxation of income of carried interests in partnerships as ordinary

29

The Calm Before the Storm

30

31

32

Moving to a New Era

• Regardless of who is President, several issues will command attention in the next Administration:

• Entitlements (Medicare, Medicaid, Social Security) Growth, Trust Fund Depletion

• Recent vintage income tax cuts expire• Alternative Minimum Tax Impact• The Exploding Debt and Debt Service• Need to Address Climate Change

33

34

35

36

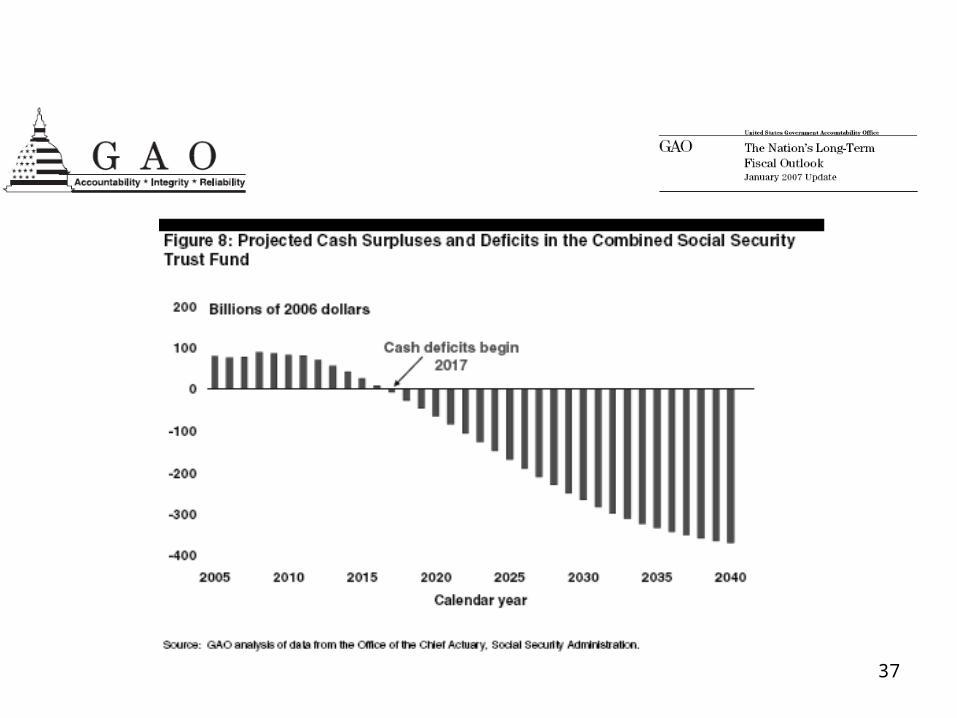

Social Security and Medicare Part A Cumulative Cash

Surpluses and DeficitsIn Constant 2006 Dollars—2006 through 2080

-$2,500

-$2,000

-$1,500

-$1,000

-$500

$0

$500

In B

illion

s o

f C

on

sta

nt

20

06

D

ollars

2006 2010 2020 2030 2040 2050 2060 2070 2080

Calendar Year

Source: Social Security Trustees’ Report—March 2006 (Intermediate Projections)

$692 Billion: Cumulative Social Security Cash Surplus

-$27.4 Trillion: Cumulative Social Security Cash Deficits

-$44.4 Trillion: Cumulative Medicare Part A Cash Deficits

-71.8 Trillion: Cumulative Social Security and Medicare Part A Cash Deficits

37

38

39

Revenue Cost of Making Permanent the 2001/2003 Cuts

Source: Joint Committee on Taxation (in billions)

2008: $2.1

2009: $1.4

2010: $3.1

2011: $152

2007-17: $1,871,539

40

41

Rapidly Rising Interest Costs

Source: Author’s calculations from data from Congressional Budget Office, Budget and Economic Outlook: Fiscal Years 2008 to 2018, March 2008

Projected Debt Service Payments

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Bill

ions

of C

urre

nt D

olla

rs

42

Dependence on Foreign Lenders

Source: U.S. Treasury Department (through September 2007) and Source: U.S. Treasury Department (through September 2007) and U.S. Bureau of Public Debt (through September 2007)U.S. Bureau of Public Debt (through September 2007)

Foreign Holdings as a Share of Net Federal Debt(debt held by the public)

44.5%41.8%41.9%41.7%

36.8%33.5%29.7%

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

$5.5

2001 2002 2003 2004 2005 2006 2007

Trilli

ons of

Cur

rent

Dol

lars

Foreign Holdings of Treasury Securities Domestic Holdings of Treasury Securities

43

Federal Revenue and Outlays

Source: BEA, NIPA Table 1.1.5; FY 2008 Budget of the United States Government, Historical Table 1.1; Author’s calculations from Brookings-Urban Tax Policy Center, Budget Outlook Tables, March 2008, Appendix 3a.

Revenues

Outlays

AverageRevenues,(1965-2007)

Average Outlays,

(1965-2007)

15

16

17

18

19

20

21

22

23

24

25

196519671969197119731975197719791981198319851987198919911993199519971999200120032005200720092011201320152017

Per

cent

age

of G

DP

PredictedActual

44Source: Government Accountability Office, September 2006

Policy Changes MatterProjected Debt Held by the Public as a

Percent of GDP Under Alternative Scenarios (2006-2040)

0%

50%

100%

150%

200%

250%

300%

2006 2010 2015 2020 2025 2030 2035 2040

Assumes discretionary spending grows with the economy and all expiring tax cuts are extended

Assumes discretionary spending increases only with inflation and tax cuts expire

45

Carbon Taxes

Tax Rate %Emission Red.Ann.Revenue

$10/ton 7.4% $55.7B

$15/ton 11.0% $80.2B

$20/ton 14.7% $102.5B

$25/ton 18.4% $122.6B

46

47

Revenue Sources

• Climate Change

• CBO Revenue Options

• JCT Estimates of Federal Tax Expenditures

• Candidates’ Statements

48