1 swaps – meeting demand for fixed-rate loans bob newman, cfa march 19-20, 2014

TRANSCRIPT

1

Swaps – Meeting Demand for Fixed-Rate Loans

Bob Newman, CFAMarch 19-20, 2014

2

Derivatives – The Perception

3

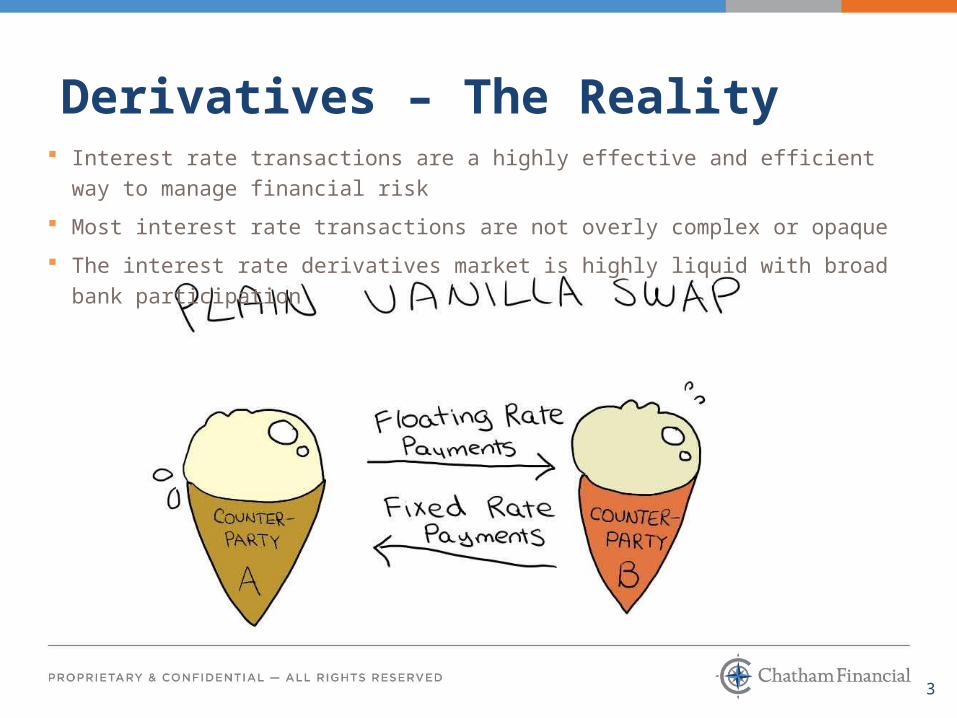

Derivatives – The Reality Interest rate transactions are a highly effective and efficient way to manage financial risk

Most interest rate transactions are not overly complex or opaque

The interest rate derivatives market is highly liquid with broad bank participation

4

LIBOR

Fixed Rate

What is an Interest Rate Swap?• An agreement between two parties in which one party agrees to pay a fixed rate of

interest and the other agrees to pay a floating rate of interest on an agreed upon notional amount• No principal changes hands, simply an exchange (“swap”) of interest payments for a set

period of time

• Swap rate is derived from market expectations

• LIBOR is the foundation of the swap market

• A swap agreement is a separate contract from the loan

Borrower Bank

5

Issue: Long-Term Fixed-Rate Loan PricingBorrower Perspective

Market interest rates hovering near all-time lows

Rumblings of rate increases in the air

+

= Borrowers demanding long-term fixed-rate pricing

6

Issue: Long-Term Fixed-Rate Loan PricingBank Perspective

Market interest rates hovering near all-time lows

Margin compression due to loans re-pricing

+

= Banks willing to accommodate borrowers out 10 yrs

or longer

7

Can Swaps Solve This Problem?

Swaps can help, but…… Swaps are a powerful tool to manage interest rate risk… Convert 10-15y fixed to L +

spread

…but not a “magic bullet”: Swaps cannot convert an

unprofitable fixed-rate into a PROFITABLE floating rate

“What are our peers doing that we’re not doing?”

8

Borrower

Fixed Rate Loan4.75%

FHLB

Fixed Rate Advance3.25%

Match-Funded Fixed-Rate Loan – FHLBA Fixed-Rate Loan Funded with a Matching FHLB Advance

• Matching FHLB advance rate for 15y/15y structure = 3.25%• Market prepayment penalty for early extinguishment

• Fixed-Rate Loan for 15y/15y structure = 4.75%• Bank nets a spread of 1.50%• Potential risk of loss on prepayment unless penalty

matches FHLB advance• Would an interest rate swap provide a different answer?

$5mm Loan

BankNet Spread =

1.50%

Loan Terms $5 million loan 15 year term 15 year amortization Minimum Spread = 1.50%

9

Short-term Funding Swapped to Fixed“Synthetic” Match Funding

DealerBankBankFHLB

1m LIBOR

2.75%Advance Terms• $5 million FHLB funding• 15 year maturity• 15 year amortization• Monthly pay

FHLB Funding Swap

1-month advance

Key Considerations – Cash Flow Hedge

Funding, or suitable replacement debt, must remain outstanding through the life of the swap

Matching swap and debt terms exactly minimizes/ eliminates ineffectiveness

1. Bank borrows $5 million in wholesale funding from FHLB monthly and rolls the advance

2. Bank executes a pay-fixed swap at 2.75% and receives 1-month LIBOR for fifteen years

3. FHLB 1-month advance rate is converted to 2.75% 15-year funding via the swap (+/- basis difference)

4. The 2.75% 15-year swap rate compares favorably to the FHLB 15-year advance rate of 3.25%

5. Save 50 bps by funding short and using swap to lock rate6. Swap provides Bank with 2-way prepay make-whole

instead of 1-way penalty in term fixed-rate advance

10

Borrower

Fixed Rate Loan4.75%

Fixed Rate Swap4.75%

1mL + 200 bps

Fixed-Rate Loan Swapped to Floating Behind the Scenes

• Fixed-rate loan is effectively converted to a floating rate• 15y/15y LIBOR swap rate = 2.75% today

• 4.75% fixed = 1mL + 2.00% floating (2.16% yield today)• No fee income recognized – all economics built-into spread over LIBOR

• Loan hedged with swap needs market-based prepay provision• Essentially embedding the worst feature of direct swap into the loan

$5mm Loan

Premium

Bank Dealer Bank

11

Loan Terms $5 million loan 15 year term, L + 175bps 15 year amortization PV01 = $3,840

Back-to-Back Swap ProgramSell the Swap to the Borrower

1. Borrower enters into loan with Bank, paying L + 1.75%2. Borrower executes “retail” swap with Bank, paying fixed at

4.75% and receiving L + 1.75% (offsetting the loan payment)3. Bank enters into “wholesale” swap with Dealer Bank, passing

on fixed rate exposure, leaving Bank with variable rate loan4. 4.75% is 25 bps higher than what Dealer Bank expects to

receive; therefore, Dealer Bank pays Bank the present value of 25 basis points or $96,000

5. All-in economics = 200 bps spread (175 in margin; 25 PV in non-interest income)

Dealer BankBankBorrower

(Loan)

LIBOR + 1.75%

LIBOR + 1.75%

4.75%

(Retail Swap)

LIBOR + 1.75%

4.75%

(Wholesale Swap)

$96,000 (25 bps x $3,840)

Pricing as of 3/18/14

12

Summary• Direct Match-Funding with FHLB

• 50 basis points more expensive due to liquidity premium in term fixed advance

• Swaps (borrower gets lower rate / bank gets better spread):• Directly with Borrowers

• Fee income opportunity• More explaining/documentation for borrower• Eligibility requirements and suitability/sophistication

• Fixed-Rate Loan (behind the scenes)• No fee income / hedge accounting designation and testing• Need market-based prepayment language

• Balance Sheet Hedge• Works best with short-term borrowings / market-linked funding• Hedge accounting designation and testing

13

How Do I “Break Ground” on Hedging?• Lay the Foundation

• Board and Management Education• Hedging Policy and Approval• Set up Swap Counterparty – Documentation• Regulatory/Accounting groundwork• Assess IRR / Borrower Demand-Suitability

• Build the House• Balance Sheet Hedging Program

• Structure-Execute-Designate-Document• Borrower-Facing Swap Program

• Implementation-Training• Product “on shelf”

14

Questions?

15

Chatham Financial Corp.235 Whitehorse LaneKennett Square, PA 19348

Bob Newman, [email protected]

Contact Informationwww.chathamfinancial.com