1 stat & gaap update brian kilbane. 2 agenda statutory-accounting update naic update us gaap...

TRANSCRIPT

1

STAT & GAAP UpdateBrian Kilbane

2

Agenda

• Statutory-Accounting Update• NAIC Update• US GAAP Update

3

Statutory Accounting Update

4

Adopted SSAP Amendments – 2015

• No substantive revisions to the 2015 AP&P Manual yet• SSAP No. 1 - Disclosure of Accounting Policies, Risks &

Uncertainties, and Other Disclosures and SSAP No. 4—Assets and Nonadmitted Assets and various other statements – Revisions adopt ASU 2014-15, Presentation of Financial

Statements – Going Concern and incorporate audited disclosure requirements for a reporting entity to evaluate and disclose whether there is substantial doubt on the entity’s ability to continue as a going concern.

– In addition, revisions to SSAP Nos. 48, 68 and 97 nonadmit investments in related affiliate holdings whose audited financial statements include going concern notes.

5

Adopted SSAP Amendments – 2015

• SSAP No. 69 - Statement of Cash Flow– Revisions clarify that the cash flow statement

should be limited to transactions involving “cash,” which is defined to include cash, cash equivalents and short-term investments, and to expand the disclosures to include non-cash operating items.

– Effective December 31, 2015

6

Adopted SSAP Amendments – 2015

• SSAP No. 36 – Troubled Debt RestructuringSSAP No. 37 – Mortgage LoansSSAP No. 40R – Real Estate Investments

– Adopt with modification ASU 2014-04, Receivables – Troubled Debt Restructuring by Creditors – Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans Upon Foreclosure and adopt ASU 2014-14, Receivables – Troubled Debt Restructuring by Creditors – Classification of Certain Government-Guaranteed Mortgage Loans Upon Foreclosure. Revisions prescribe accounting and reporting for foreclosed mortgage loans collateralized by real estate and foreclosed mortgage loans guaranteed by a government-sponsored program.

7

Adopted SSAP Amendments – 2015

• SSAP No. 74 - Accounting for the Issuance of Insurance-Linked Securities Issued by a Property and Casualty Insurer Through a Protected Cell – Revisions reference existing reporting lines for

protected cells. • SSAP No. 92 - Accounting for Postretirement

Benefits Other Than Pensions SSAP No. 102 – Accounting for Pensions

– Revisions incorporate the guidance from INT 13-03—Clarification of Surplus Deferral

8

Adopted SSAP Amendments – 2015

• Issue Paper No. 99 – Non-applicable GAAP Pronouncements– Revisions reject ASU 2014-13, Measuring the Financial

Assets and Financial Liabilities of a Consolidated Collateralized Financing Entity as not applicable to statutory accounting.

• SSAP No. 11 - Postemployment Benefits and Compensated Absences – Revisions delete disclosures that pertain to defined

benefit and defined contribution plans, with a reference to complete the disclosures in SSAP No. 92 if the entity is providing special or contractual termination benefits.

9

Adopted SSAP Amendments – 2015

• SSAP No. 93 – Accounting for Low Income Housing Tax Credit Property Investments– Revisions adopt with modification ASU 2014-01.

These revisions reflect GAAP terminology but maintain the prior statutory accounting methodology, including gross income statement presentation.

• SSAP No. 61R- Life, Deposit-Type and Accident and Health Reinsurance– Revisions incorporate a disclosure related to

compliance with XXX/AXXX Reinsurance Model Regulation, Actuarial Guideline 48 or state’s variation.

10

Adopted SSAP Amendments – 2015

• SSAP No. 54 – Individual and Group Accident and Health Contracts– Revisions specify the asset and liability lines for contracts subject

to redetermination. Also noted during the call, current guidance generally prohibits prior year restatement except in instances of a merger or quasi re-organization and audited financial statements may require identification of different approaches applied in comparable years and may require restatement to improve comparability, subject to auditor judgment under Generally Accepted Auditing Standards (GAAS).

– Revisions adopt the ASU 2010-23 Health Care Entities, Measuring Charity Care definition of charity care, and adopt with modification the charity care disclosure within ASU 2010-23.

11

Adopted SSAP Amendments – 2015

• SSAP No. 25 – Accounting for and Disclosures about Transactions with Affiliates and Other Related Parties– Revisions reject ASU 2013-06 Not-For-Profit Entities

– Services Received from Personnel of Affiliate in SSAP No. 25

• SSAP No. 86 – Accounting for Derivative Instruments and Hedging, Income Generation, and Replication (Synthetic Asset) Transactions– Revisions reject ASU 2014-16 Derivatives and

Hedging (Host Contract) for statutory accounting

12

Adopted SSAP Amendments – 2015

• SSAP No. 40R – Real Estate Investments– Revisions clarify when an encumbrance on wholly owned real

estate held in an LLC is allowed for SSAP No. 40R (Schedule A) reporting.

– A standard mortgage or encumbrance by an unrelated party is allowed within this guidance.

– However, a participating mortgage loan (paragraph 22) with related or unrelated parties, or loans or other encumbrances from related parties would not be allowed – not solely and distinctly possessing all risks and rewards of ownership.

• SSAP No. 68 – Business Combination and Goodwill– Revisions provide a consistency clarification that the goodwill

limitation test is completed at the individual reporting company level.

13

Adopted SSAP Amendments – 2015

• SSAP No. 24 – Discontinued Operations and Extraordinary Items– Revisions adopt with modification ASU 2015-01 Income

Statement – Extraordinary and Unusual Items, to be consistent with existing guidance that prohibits separate reporting for extraordinary items.

– Revisions adopt with modification ASU 2014-08 Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity, which intend to be consistent with existing guidance that prohibits separate reporting and prohibit gain recognition until the disposal transaction is complete. Also adopted were reduced disclosure requirements.

14

Exposed Substantive SSAP Amendments – 2015

Ref # Title Description of Change2014-25

SSAP No. 41—Surplus Notes

Exposed issue paper detailing revisions to the measurement method for holders of non-rated surplus notes and surplus notes with a designation below an NAIC 1. This issue paper requests comments on specific discussion points, including whether the use of amortized cost should be expanded.

2015-31

Various SSAPs

Received a referral from the Valuation of Securities (E) Task Force regarding non-recourse charity loans and notes and exposed an agenda item requesting comments on the structure of transactions that could be considered in-scope and proposals to clarify the accounting and reporting.

15

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change

2013-36

SSAP No. 26-Bonds, Excluding Loan-Backed and Structured Securities

With regards to the Investment Classification Project, exposed the Blackrock comment letter, specifically requesting comment on Blackrock’s proposed calculation of “amortized cost” for Exchange Traded Funds.

2014-28

SSAP No. 62R-Property Casualty Reinsurance

Exposed revisions and an illustration to decrease the provision for reinsurance liability related to certain asbestos and environmental reinsurance with retroactive counterparties and to provide consistency with the proposed annual statement reporting.

16

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change

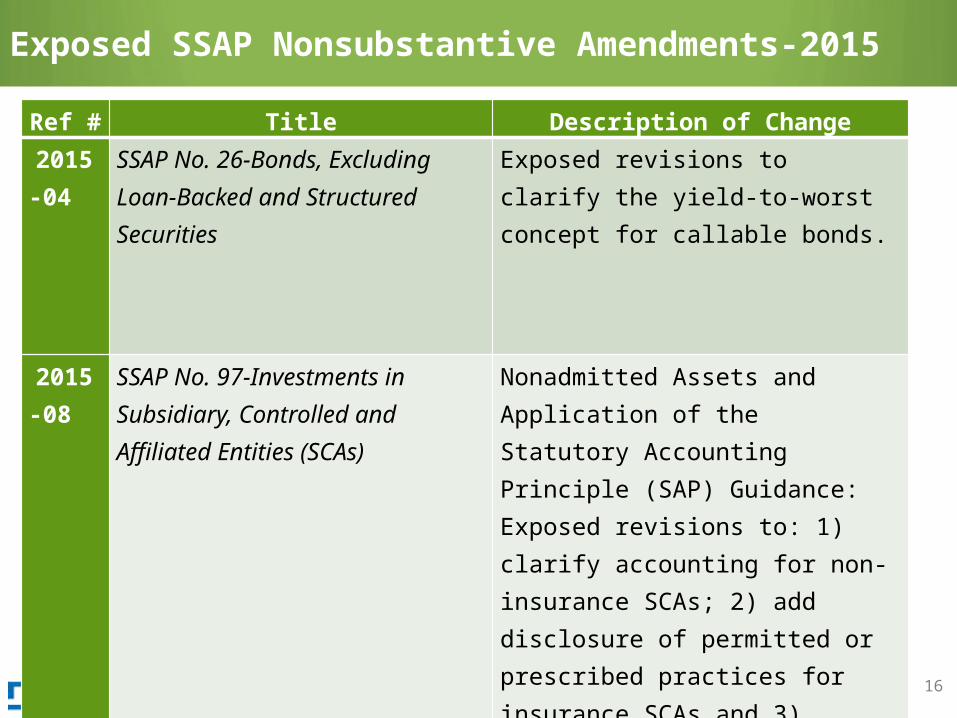

2015-04

SSAP No. 26-Bonds, Excluding Loan-Backed and Structured Securities

Exposed revisions to clarify the yield-to-worst concept for callable bonds.

2015-08

SSAP No. 97-Investments in Subsidiary, Controlled and Affiliated Entities (SCAs)

Nonadmitted Assets and Application of the Statutory Accounting Principle (SAP) Guidance: Exposed revisions to: 1) clarify accounting for non-insurance SCAs; 2) add disclosure of permitted or prescribed practices for insurance SCAs and 3) clarify adjustments for non-insurance SCAs meeting the revenue and activity test.

17

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change

2015-10

SSAP No. 15-Debt and Holding Company Obligations

Exposed revisions to reject ASU 2015-03: Simplifying the Presentation of Debt Issuance Cost and maintain the current charge to operations for these costs.

2015-13

SSAP No. 92-Postretirement Benefits Other than Pensions

SSAP No. 102-Pensions

Exposed revisions to include guidance regarding interim re-measurement of plan assets and benefit obligations due to a significant event and adopt with modification ASU 2015-04: Practical Expedient for the Measurement Date of An Employer’s Defined Benefit Obligation and Plan Assets. Also incorporated a title change to SSAP No. 102 so that the title mirrors other recent revisions, removing reference to “Accounting for”.

18

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change

2015-17

SSAP No. 26-Bonds, Excluding Loan-Backed and Structured Securities

SSAP No. 43R-Loan-Backed and Structured Securities

Exposed revisions to require Asset Valuation Reserve (AVR) filer investments designated NAIC 5 to be reported at the lower of amortized cost or fair value.

2015-21

SSAP No. 55-Unpaid Claims, Losses and Loss Adjustment Expenses

Exposed revisions to clarify that fees incurred for salvage and subrogation recoveries shall be reported gross, regardless of whether the fees are paid to third parties or processed internally.

19

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change

2015-23

SSAP No. 26-Bonds, Excluding Loan-Backed and Structured Securities

Exposed three options for the accounting and reporting treatment of prepayment penalties.

2015-24

SSAP No. 23-Foreign Currency Transactions and Translations

Exposed revisions to clarify the optional accounting treatment for translation of Canadian Insurance Operations.

20

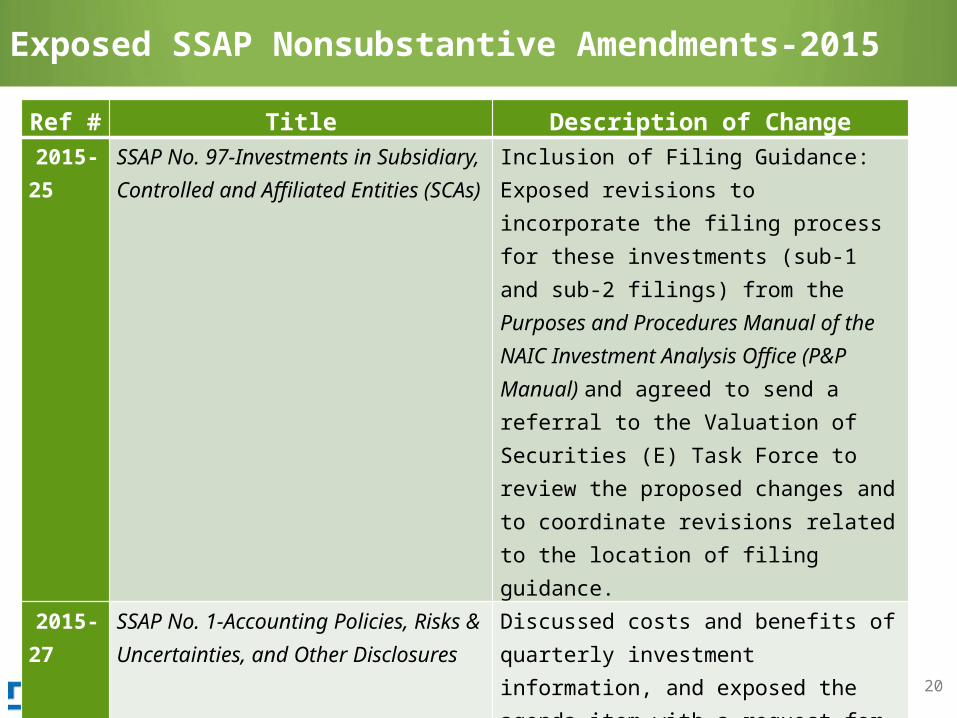

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change2015-

25SSAP No. 97-Investments in Subsidiary, Controlled and Affiliated Entities (SCAs)

Inclusion of Filing Guidance: Exposed revisions to incorporate the filing process for these investments (sub-1 and sub-2 filings) from the Purposes and Procedures Manual of the NAIC Investment Analysis Office (P&P Manual) and agreed to send a referral to the Valuation of Securities (E) Task Force to review the proposed changes and to coordinate revisions related to the location of filing guidance.

2015-27

SSAP No. 1-Accounting Policies, Risks & Uncertainties, and Other Disclosures

Discussed costs and benefits of quarterly investment information, and exposed the agenda item with a request for proposals on what should be captured, and the form of such submissions.

21

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change2015-

28Preamble Exposed revisions to: 1) restructure

to clarify historical guidance, 2) include the preamble within level 4 of the SAP Hierarchy and 3) add a narrative reference to INT 00-20: Application of SEC SAB No. 99, Materiality to the Preamble of the Accounting Practices and Procedures Manual.

2015-30

SSAP No. 107-Risk-Sharing Provisions of the Affordable Care Act

Exposed revisions regarding contracts subject to redetermination which are consistent with recent revisions adopted in SSAP No. 54-Individual and Group Accident and Health Contracts.

22

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change2015-

32SSAP No. 97-Investments in Subsidiary, Controlled and Affiliated Entities (SCAs)

Application of Equity Method: Exposed revisions clarify the guidance in paragraphs 10-12.

2015-33

SSAP No. 78-Multiple Peril Crop Insurance

Exposed agenda item to collect information from regulators, industry, and the U.S. Department of Agriculture (USDA) Risk Management Agency (RMA) regarding any needed updates to SSAP No. 78 and the intent to develop clarifying language regarding: 1) the use of the billing date for application of the 90-day rule; 2) defining the processing date or updating the term; 3) providing more specificity regarding the period of risk for purposes of earning revenue; and 4) developing a glossary of terms including dates that are specific to the federal crop programs.

23

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change2015-

34SSAP No. 1-Accounting Policies, Risks & Uncertainties, and Other Disclosures

Exposed agenda item to collect information regarding the use of insurance-linked securities by both insurers and reinsurers, with an example template of what may be requested for disclosure.

2015-35

SSAP No. 65-Property and Casualty Contracts

Received referral from the Financial Analysis (E) Working Group and exposed an agenda item proposing disclosures to capture information regarding recoverables from policyholders under high deductible policies.

24

Exposed SSAP Nonsubstantive Amendments-2015

Ref # Title Description of Change2015-

36SSAP No. 61R-Life, Deposit-Type and Accident and Health Reinsurance

Exposed new disclosures proposed by the American Council of Life Insurers (ACLI) to get information on the reinsurance of variable annuity contracts with an affiliated captive reinsurer and reinsurance agreements with an affiliated captive reinsurer.

2015-37

ASU 2015-09-Financial Services - Insurance, Disclosures about Short-Duration Contracts

Exposed the agenda item requesting for comments from regulators and industry representatives on the GAAP disclosures for short-duration insurance contracts.

25

Exposed SSAP Amendments – Spring 2015

Ref # Title Description of Change2015-03

SSAP No. 22—Leases

Exposed agenda item requests comments on issues with sale-leasebacks

2015-08

SSAP No. 97—Investments in Subsidiary, Controlled and Affiliated Entities, A Replacement of SSAP No. 88

Exposed agenda item requests comments on issues with the reporting of investments in subsidiary, controlled and affiliated entities

26

NAIC Update

27

Risk-Based Capital Updates– 2015

• Investment RBC– American Academy of Actuaries presented its

proposed methodology for C-1 charges• 6 categories to 14 categories of fixed income assets• Expected impacts are an increase in capital

requirements, possibly double.• 45 day comment period

• Operational Risk– Information-only supplement in 2015– Possible implementation for 2016 or 2017

28

Risk-Based Capital Updates– 2015

• Life Entities– Information-Only Alternative C-3 RBC Cash Flow

Testing • Not required for 2015

– Management Discussion and Analysis • The instructions were revised to indicate that the RBC

requirement, total adjusted capital and RBC factors cannot be modified for the calculation of authorized control level.

29

Risk-Based Capital Updates– 2015

• P&C Entities– Adopted:

• A new Underwriting Risk-Experience Fluctuation Risk PR020A and Risk Adjustment and Risk Corridor Sensitivity Test

• R6 and R7 Contingent Credit Risk Factors; (3) PR012A for Credit Risk for Informational purposes only

• PR012A for Credit Risk for Informational purposes only• Exemption Criteria to PR026 Interrogatory; 2015-04CR for Curve

Sorting

– Discussion to simplify the RBC charge for the ownership of Investment Affiliates (affiliate Type 7) to be a fixed factor times the carrying value of the common stock, preferred stock and bonds, as the current P&C RBC charge cannot be validated/verified

30

Captive Insurance Updates – 2015

• XXX/AXXX Supplemental Reinsurance Exhibit Adopted• RBC Cushion is still being determined

– Primary Securities Shortfall – This proposal adds a new schedule showing the primary security shortfall by individual cession. The cumulative amount of primary security shortfall, with no offset for any surplus, is then taken as a dollar-for-dollar addition to the reporting company’s authorized control level

– RBC Shortfall – This proposal adds a new schedule which shows the RBC calculation by individual captive. The cumulative amount of RBC shortfalls, with no offset for any surpluses, is then taken as a dollar-for-dollar reduction to the reporting company’s total adjusted capital

31

Captive Insurance Updates – 2015

• Captive Accreditation– The following captive insurers are required to

comply with the Preamble of the Accreditation Program and are considered multi-state insurers:• Captives and SPVs that assume:

– XXX/AXXX business (effective 1/1/2016)–Variable annuities valued under VA-

CARVM (effective date TBD)–Long-term care (effective date TBD)

32

Captive Insurance Updates – 2015

• Credit for Reinsurance for XXX/AXXX Captives– Proposed that credit for reinsurance is only allowed

if the entity maintains primary security holdings equal to the PBR (required level of primary security).

– If the entity maintains the required level of primary security, the credit for reinsurance allowed is equal to the ceded AG 48 reserves (full credit for reinsurance).

– If the entity does not maintain the required level of primary security, no credit for reinsurance is allowed

33

Principles-Based Reporting Updates – 2015

• 42 states representing 75% of premiums must adopt to become effective– 36 states have adopted representing 60% of

premiums• Earliest possible effective date is January 1,

2017• Proposed a PBR implementation pilot program

34

Terrorism Risk Updates– 2015

• Congress passed Terrorism Risk Insurance Reauthorization Act of 2015– Extends TRIA through December 31, 2020

• Requested data to assess further continuation of TRIA– lines of insurance with exposure to such losses;– premiums earned on such coverage;– geographical location of exposures;– pricing of such coverage;– the take-up rate for such coverage;– the amount of private reinsurance for acts of terrorism

purchased; and– such other matters as the Secretary of Treasury considers

appropriate

35

Terrorism Risk Updates– 2015

• Blanks (E) Working Group submitted a proposal to data collect through an Annual Statement Supplement

• Voted down due to:– Industry concerns about ability to collect data– Concerns that proposal was rushed and didn’t take

into consideration industry’s concerns• Federal Insurance Office (FIO) also noted that

they would take up the data collection effort.– Certain NAIC members concerned this could take

away NAIC authority

36

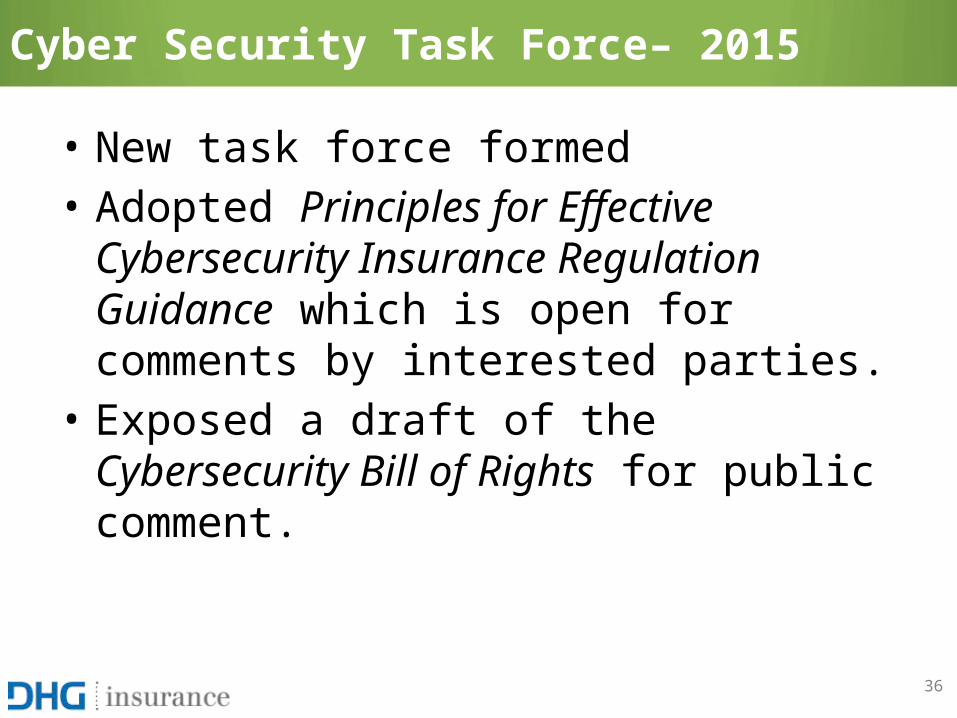

Cyber Security Task Force– 2015

• New task force formed• Adopted Principles for Effective Cybersecurity

Insurance Regulation Guidance which is open for comments by interested parties.

• Exposed a draft of the Cybersecurity Bill of Rights for public comment.

37

Other NAIC Updates – 2015

• Creditor-Placed Insurance Model Act Review (C) Working Group– Met for the first time in August. – Charged with reviewing information from the public hearing on

lender-placed insurance and determine if changes to the Creditor-Placed Insurance Model Act (#375) are warranted.

• Workers’ Compensation (C) Task Force – Received a report from the NAIC/IAIABC Joint (C) Working Group

in regards to a request to study large/mega deductibles as several recent workers’ compensation carrier insolvencies appeared to have been triggered by companies writing large deductible workers’ compensation policies without securing appropriate collateral.

38

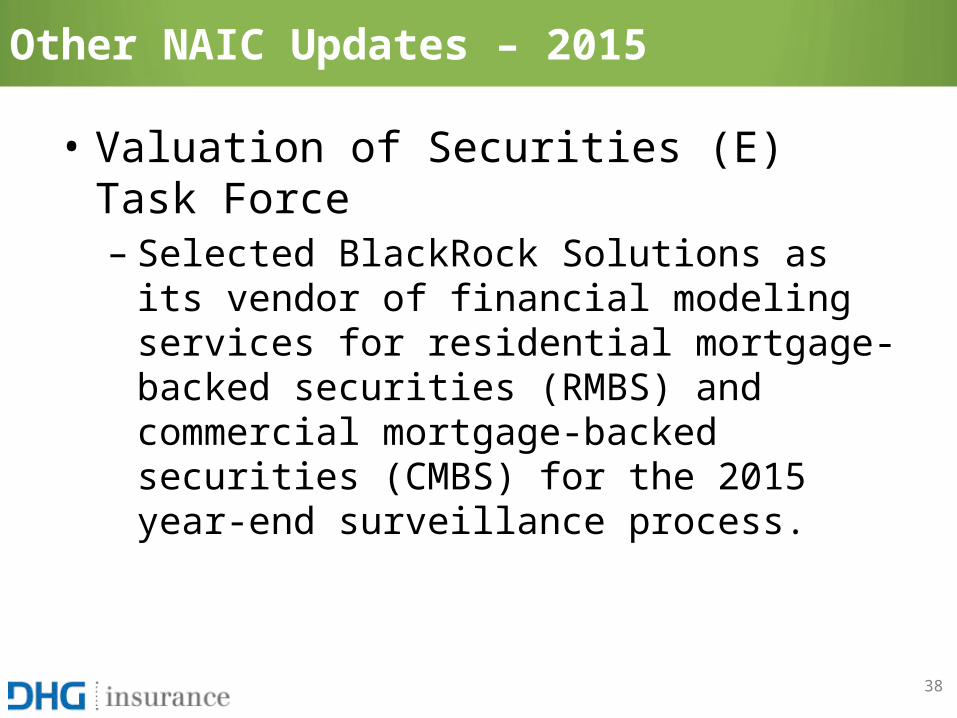

Other NAIC Updates – 2015

• Valuation of Securities (E) Task Force– Selected BlackRock Solutions as its vendor of

financial modeling services for residential mortgage-backed securities (RMBS) and commercial mortgage-backed securities (CMBS) for the 2015 year-end surveillance process.

39

US GAAP Update

40

New Accounting Standards Updates

• ASU 2015-01 – Income Statement – Extraordinary and Unusual Items

• ASU 2015-02 – Consolidation• ASU 2015-03 – Interest – Imputation of Interest• ASU 2015-04 – Compensation –Retirement

Benefits• ASU 2015-05 – Intangibles – Goodwill and

Other – Internal-Use Software (Cloud Computing)

41

New Accounting Standards Updates

• ASU 2015-07 – Fair Value Measurement• ASU 2015-09 – Financial Services - Insurance• ASU 2015-14 – Revenue from Contracts with

Customers• ASU 2015-15 – Imputation of Interest

42

ASU 2015-09 – Disclosures about Short Duration Contracts

• Main Provisions– Incurred and paid claims development information by

accident year, on a net basis, for the number of years claims typically remain outstanding (not to exceed 10 years)

• Periods presented prior to the current reporting period is considered supplementary information

– A reconciliation of incurred and paid claims development information to the aggregate carrying amount of the liability for unpaid claims and claim adjustment expenses, with separate disclosure of reinsurance recoverable on unpaid claims for each period presented in the statement of financial position

43

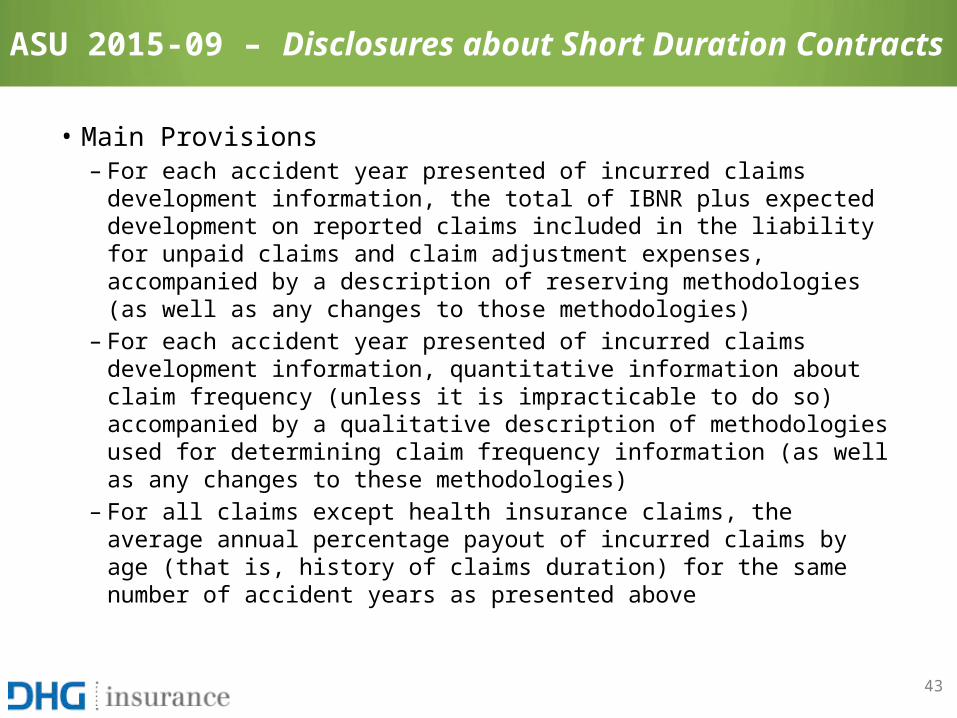

ASU 2015-09 – Disclosures about Short Duration Contracts

• Main Provisions– For each accident year presented of incurred claims development

information, the total of IBNR plus expected development on reported claims included in the liability for unpaid claims and claim adjustment expenses, accompanied by a description of reserving methodologies (as well as any changes to those methodologies)

– For each accident year presented of incurred claims development information, quantitative information about claim frequency (unless it is impracticable to do so) accompanied by a qualitative description of methodologies used for determining claim frequency information (as well as any changes to these methodologies)

– For all claims except health insurance claims, the average annual percentage payout of incurred claims by age (that is, history of claims duration) for the same number of accident years as presented above

44

ASU 2015-09 – Disclosures about Short Duration Contracts

• Main Provisions– Disclose for annual and interim reporting periods a rollforward of the

liability for unpaid claims and claim adjustment expenses.• For health insurance claims, the amendments require the disclosure of the

total of incurred-but-not-reported liabilities plus expected development on reported claims included in the liability for unpaid claims and claim adjustment expenses.

– Additional disclosures about liabilities for unpaid claims and claim adjustment expenses reported at present value include the following:

• For each period presented in the statement of financial position, the aggregate amount of discount for the time value of money deducted to derive the liability for unpaid claims and claim adjustment expenses

• For each period presented in the statement of income, the amount of interest accretion recognized

• The line item(s) in the statement of income in which the interest accretion is classified.

45

ASU 2015-09 – Disclosures about Short Duration Contracts

• Effective Date– Public Entities

• Annual periods beginning after December 15, 2015• Interim periods within annual periods beginning after

December 15, 2016

– Nonpublic Entities• Annual periods beginning after December 15, 2016• Interim periods within annual periods beginning after

December 15, 2017

46

ASU 2015-09 – Disclosures about Short Duration Contracts

• Transition Requirements– Initial year of application

• Need not disclose information about claims development for a particular category that occurred earlier than 5 years before the end of the first reporting year in which amendments are applied if it is impracticable.

• For each subsequent year, the minimum required number of years increases by one year, not to exceed 10 years.

– Early adoption permitted– Retrospectively applied, except for those that only

apply to current period.

47

ASU 2015-01 – Income Statement – Extraordinary and Unusual Items

• Eliminates the concept of extraordinary items being separately stated on income statement

• Presentation and disclosure guidance still retained

• Effective for fiscal years and interim periods beginning after December 15, 2015.– Applied prospectively or retrospectively

48

ASU 2015-02 – Consolidation

• Key areas affected by the ASU include: – The deferral of ASU 2009-17 for investments in certain

investment funds has been eliminated – The ASU reduces the likelihood that fees paid to a decision

maker or service provider will result in consolidation – Limited partnerships will be variable interest entities (VIEs),

unless the limited partners (LPs) have either substantive kick-out or participating rights

– For entities other than limited partnerships, the ASU clarifies how to determine whether the equity holders (as a group) have power over the entity

– The ASU reduces the likelihood that interests held by a reporting entity’s related parties or de facto agents will result in consolidation

49

ASU 2015-02 – Consolidation

• Effective for public business entities for annual periods beginning after December 15, 2015. One year deferral for nonpublic entities

• Early adoption is permitted but guidance must be applied as of the beginning of the annual period containing the adoption date

• Transition–either full retrospective or modified retrospective adoption

50

ASU 2015-03 – Interest – Imputation of Interest

• Debit issuance costs related to a recognized debt liability should be presented as a direct deduction from the carrying amount of the debt liability

• Public - Effective for public business entities for annual periods beginning after December 15, 2015 and interim periods within those fiscal years

• Non-public - Effective for public business entities for annual periods beginning after December 15, 2015 and interim periods within fiscal years beginning after December 15, 2016

• Early adoption permitted. Apply retrospectively.

51

ASU 2015-03 – Interest – Imputation of Interest

• ASU 2015-15 was issued to address line-of-credit arrangements as commented by the SEC.

• The SEC staff would not object to an entity deferring and presenting debt issuance costs as an asset and subsequently amortizing the deferred debt issuance costs ratably over the term of the line-of-credit arrangement, regardless of whether there are any outstanding borrowings on the line-of-credit arrangement.

52

ASU 2015-04 – Compensation –Retirement Benefits

• Gives an employer whose fiscal year-end does not coincide with a calendar month-end (e.g., an entity that has a 52- or 53-week fiscal year) the ability, as a practical expedient, to measure defined benefit retirement obligations and related plan assets as of the month-end that is closest to its fiscal year-end.

• Accounting for contributions– Funded status should be adjusted to reflect:

• Additions to plan assets for contributions made after the measurement date but before fiscal year end or

• Deductions from plan assets for a contribution made after fiscal year-end but before measurement date

53

ASU 2015-04 – Compensation –Retirement Benefits

• Accounting for significant events that require remeasurement that occur during the period between a month-end measurement date and the employer’s fiscal year end.– Event should be recorded in fiscal year in which

the event occurs.– However, entity may elect to measure the effects

of a significant event as of the calendar month nearest to the date of the significant event.

– Case-by-case basis

54

ASU 2015-04 – Compensation –Retirement Benefits

• Public - Effective for public business entities for annual periods beginning after December 15, 2015 and interim periods within those fiscal years

• Non-public - Effective for public business entities for annual periods beginning after December 15, 2016 and interim periods within fiscal years beginning after December 15, 2017

• Early application permitted. Apply prospectively.

55

ASU 2015-05 – Intangibles – Goodwill and Other – Internal-Use Software (Cloud Computing)

• Determine whether cloud computing arrangement contains a software license that should be accounted for as internal-use software.– software as a service, platform as a service, infrastructure as

a service, and other similar hosting arrangements• If contains a software license:

– Account for fees related to software license element consistent with acquisition of software license under ASC 350-40.

– Similar to accounting for other licenses and intangible assets• If does not contain a software license:

– Account for arrangement as a service contract

56

ASU 2015-05 – Intangibles – Goodwill and Other – Internal-Use Software (Cloud Computing)

• Arrangement contains a software license if both the following are met:– The customer has the contractual right to take possession

of the software at any time during the hosting period without significant penalty.

– It is feasible for the customer to either run the software on its own hardware or contract with another party unrelated to the vendor to host the software.

• “Without significant penalty” defined as:– the “ability to take delivery of the software without

incurring significant cost” – the “ability to use the software separately without a

significant diminution in utility or value.”

57

ASU 2015-05 – Intangibles – Goodwill and Other – Internal-Use Software (Cloud Computing)

• Public - effective for annual periods (and interim periods therein) beginning after December 15, 2015;

• Non-public - effective for annual periods beginning after December 15, 2015, and interim periods in annual periods beginning after December 15, 2016.

• Early adoption permitted.• Apply retrospectively or prospectively.

58

ASU 2015-07 - Fair Value Measurement

• Permits a reporting entity, as a practical expedient, to measure the fair value of certain investments using the net asset value (NAV) per share of the investment.– No longer required to classify in fair value hierarchy,

however should include in the total fair value of investments in order to reconcile to balance sheet.

• Currently, investments valued using NAV are categorized within the fair value hierarchy on the basis of whether the investment is redeemable with the investee at NAV on the measurement date, never redeemable with the investee at NAV, or redeemable with the investee at NAV at a future date

59

ASU 2015-07- Fair Value Measurement

• Effective Date– Public Entities

• Fiscal years beginning after December 15, 2015, and interim periods within that fiscal year

– Nonpublic Entities• Fiscal years beginning after December 15, 2016, and

interim periods within that fiscal year

• Transition– Apply retrospectively– Early adoption permitted

60

ASU 2015-14 – Revenue from Contracts with Customers

• Defers the effective date of the new revenue recognition guidance.• Public business entities, certain not-for-profit entities, and certain

employee benefit plans – Apply the guidance to annual reporting periods beginning after December 15,

2017, including interim reporting periods within that reporting period. – Earlier application is permitted only as of annual reporting periods beginning

after December 15, 2016, including interim reporting periods within that reporting period.

• All other entities – Apply the guidance to annual reporting periods beginning after December 15,

2018, and interim reporting periods within annual reporting periods beginning after December 15, 2019.

– Earlier application is permitted only as of an annual reporting period beginning after December 15, 2016, including interim reporting periods within that reporting period, or an annual reporting period beginning after December 15, 2016, and interim reporting periods within annual reporting periods beginning one year after the annual reporting period in which an entity first applies the guidance.

61

Insurance Matters Update – Long Duration Contracts Targeted Improvements

• FASB currently in redeliberations• Considering what method should be used to calculate and

record the effect of updating assumptions for liability for future policy benefits for traditional long-duration contracts and limited-pay contracts.– Occurs during Q4 of the fiscal year

• Provision for adverse deviation is not included in the calculation of liability.

• FASB decided that updating of cash flow assumptions using a retrospective approach.

• FASB decided that updating of discount rate assumptions using an immediate approach.

62

Insurance Matters Update – Long Duration Contracts Targeted Improvements

• Under this assumption update method, a revised net premium ratio is calculated as of contract inception using actual historical experience and updated future cash flow assumptions.

• The revised net premium ratio is then applied to derive a cumulative catch-up adjustment to be recorded in current-period earnings.

• In subsequent periods, the revised net premium ratio is used to accrue the liability for future policy benefits.

• As a result of the Board’s prior decision to eliminate premium deficiency testing, the net premium ratio is capped at 100 percent so that losses are not deferred into future periods.

• The net premium ratio is not updated for discount rate assumption changes. Rather, the effect of discount rate changes is recorded immediately in other comprehensive income.

• The amount included in accumulated other comprehensive income represents the difference between the carrying amount of the liability for future policy benefits measured using updated discount rates and locked-in rates at contract inception.

63

Insurance Matters Update – Long Duration Contracts Targeted Improvements

• Discount rate– If using an expected investment yield under existing GAAP,

discount rate would be a rate based on a portfolio of high-quality, fixed-income securities

• Amortization of DAC– Certain investment contracts

• Use effective interest method– Other types of long-duration contracts

• Amortize of the expected life of a book of contracts in proportion to the amount insurance inforce.

64

Insurance Matters Update – Long Duration Contracts Targeted Improvements

• Disclosures– Disaggregated balance of the liability for future policy benefits and the

weighted average discount rates used to measure the liability for future policy benefits in time bands and any additional information about amounts and rates within the time bands provided that significantly affect the discount rates

– Disaggregated quantitative and qualitative information about the methods and inputs used to develop the measurement of the liability for future policy benefits, including disclosure of assumptions used (such as discount rate, mortality, morbidity, termination [lapse], and expense assumptions)

– Disaggregated reconciliations from the opening to the closing balance of the liability for future policy benefits, with separate disclosure of changes in the liability for future policy benefits due to new contracts, benefit payments, changes in assumptions, and derecognition of contracts.

65

Lease Accounting Update

• Requires most leases to be recorded on the balance sheet.• Modified retrospective adoption will be required for

adoption.• Elimination of current guidance for build-to-suit transactions.• Transition guidance for build-to-suit transactions and

leaseback transactions. • Affirmation that a lessee should not reassess variable

payments based on an index or rate unless the lease liability has to be remeasured for other reasons (e.g. change in lease term)

• Expect new standard second half Q4 2015.• Effective date has not been decided.

66

Other Pending GAAP Updates

Topic Status Update

Accounting for Financial Instruments: Classification and Measurement

Final Standard Q4 2015

Accounting for Financial Instruments: Hedging

Exposure Draft Q4 2015

Accounting for Financial Instruments: Impairment

Final Standard Q4 2015

Accounting for Measurement Period Adjustments in a Business Combination

Final Standard Q3 2015

Clarifying the Definition of a Business Exposure Draft Q4 2015