1 short-term outlook presented by: garret sloan, cfa, short-term fixed income strategist october...

TRANSCRIPT

1

Short-term Outlook Presented by:Garret Sloan, CFA, Short-term Fixed Income Strategist

October 2011

2

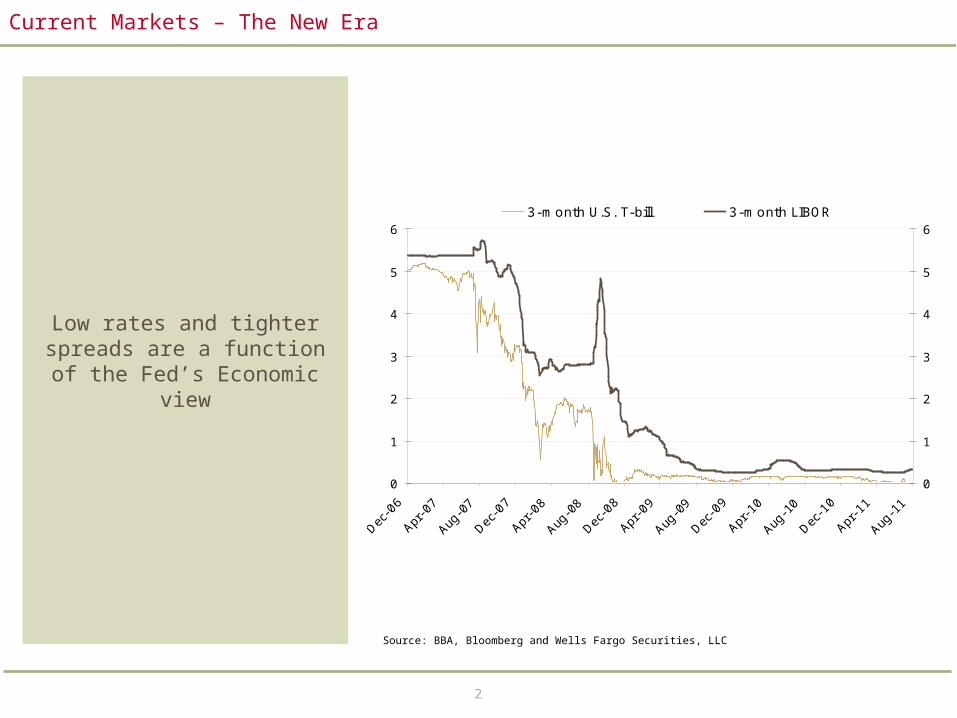

Current Markets – The New Era

Low rates and tighter spreads are a function of the Fed’s Economic view

Source: BBA, Bloomberg and Wells Fargo Securities, LLC

0

1

2

3

4

5

6

Dec-0

6

Apr-0

7

Aug-0

7

Dec-0

7

Apr-0

8

Aug-0

8

Dec-0

8

Apr-0

9

Aug-0

9

Dec-0

9

Apr-1

0

Aug-1

0

Dec-1

0

Apr-1

1

Aug-1

1

0

1

2

3

4

5

63-month U.S. T-bill 3-month LIBOR

Source: BBA, Bloomberg

Short Term Rates Remain Low

3

The Great Recession in Perspective

The hole this recession dug was large and will take years to climb out

Source: U.S. Department of Commerce, Congressional Budget Office, U.S. Department of Labor and Wells Fargo Securities, LLC

Labor MarketOutput Gap

Employment CyclesPercent Change from Cycle Peak

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

0 4 8 12 16 20 24 28 32 36 40 44 48

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%1948-1949 Cycle1981-1982 Cycle1989-1991 Cycle2001 Cycle2007-To-DateForecast

Output Gap in the U.S. Trillions of Dollars, Potential vs. Actual GDP, Inflation Adjusted

$10.7

$11.2

$11.7

$12.2

$12.7

$13.2

$13.7

$14.2

2000 2002 2004 2006 2008 2010

$10.7

$11.2

$11.7

$12.2

$12.7

$13.2

$13.7

$14.2

Potential GDP: Q3 @ $14.1 Trillion

Actual GDP: Q3 @ $13.3 Trillion

Output Gap = $860 Billion

GDP

Real GDP Change in RecessionsPercentage Change Peak- to-Trough

-5%

-4%

-3%

-2%

-1%

0%

1%

1948-1949Cycle

1953-1954Cycle

1957-1958Cycle

1960-1961Cycle

1969-1970Cycle

1973-1975Cycle

1980Cycle

1981-1982Cycle

1989-1991Cycle

2001Cycle

2007-2009Cycle

-5%

-4%

-3%

-2%

-1%

0%

1%

4

Slow progress in unemployment continues to weigh heavily on Fed policy.

Deleveraging of consumer balance sheets has leveled off, but credit-related spending is expected to remain subdued.

Both new and existing home sales plummeted following the expiration of the homebuyer tax credit program. The gap between existing and new home sales is widening.

The U.S. housing market is still being weighed down by the enormous supply of vacant homes for rent and for sale.

Rising interest rates will make it even more difficult for housing to recover, making the Fed more convinced that it needs to keep rates lower for longer.

Regulatory uncertainty is causing banks, companies and individuals to become more risk-averse

Highlights

What is the Fed Looking at?

Source: BLS, Federal Reserve, U.S. Department of Commerce, Federal Housing Finance Agency, National Association of Realtors, S&P Corp. and Wells Fargo Securities, LLC

Metrics continue to indicate that the Fed Policy will remain highly accommodative

0

500

1000

1500

2000

2500

3000

0

500

1000

1500

2000

2500

3000

Source: Federal Reserve

Total Consumer Credit Outstanding($ billions)

Total Decline: -6.57%

Non-Revolving: +2.4%Revolving: -18.0%

3

3.5

4

4.5

5

5.5

6

6.5

7

7.5

8

0

200

400

600

800

1000

1200

1400

1600

New Home Sales: Aug @ 295 thousand

Existing Home Sales: Aug @ 5.03 million

Existing New and Single Family Home SalesSeasonally Adjusted Annual Rate

0

1

2

3

4

5

6New Homes Inventory: August @ 164 thousand

Existing Homes Inventory: August @ 3.58 million

Single-Family Home InventoryMillions of Units

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

16

18

20U6 U3

Source: BLS

Total Unemployment

5

The Unemployment Rate Remains Flat

The Unemployment Rate remains above 9 percent.

Meanwhile, participation rates have risen slightly.

The flat unemployment rate, coupled with a rising

participation rate likely means that workers are

accepting part-time employment.

Source: BLS and Wells Fargo Securities, LLC

0

2

4

6

8

10

12

62

63

64

65

66

67

68

69

70Unemployment (LHS) Labor Participation (RHS)

Source: BLS

Unemployment vs. Participation

Mar '84 = 64.1 Sep '11 = 64.2

6

The Fed Continues to Exert Control

The amount of cash sitting on bank balance sheets is

indicative of a lack of credit demand, a relative

unwillingness by banks to lend based on regulatory and economic uncertainty and highly accommodative

Fed monetary policy.

Source: Federal Reserve and Wells Fargo Securities, LLC

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jul-9

3

J ul-9

4

J ul-9

5

J ul-9

6

J ul-9

7

J ul-9

8

J ul-9

9

J ul-0

0

J ul-0

1

J ul-0

2

J ul-0

3

J ul-0

4

J ul-0

5

J ul-0

6

J ul-0

7

J ul-0

8

J ul-0

9

J ul-1

0

J ul-1

1

.

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Source: Federal Reserve

Excess ReservesAt Commercial Banks ($ billions)

$1,577B

9/11, 2001 - $38 billion

QE2

7

The Fed Continues to Exert Control - QE2, Forward Rate Transparency and Operation Twist

The impact of the August change in the Fed policy

statement had an immediate impact on the shape of the

yield curve.

After the August announcement, the 3-year fell close to 2-year levels

and the 2-year closed in on the 1-year yield.

Source: Federal Reserve and Wells Fargo Securities, LLC

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1M 3M 6M 1Y 2Y 3Y 5Y

Current 15-Jul QE2

Treasury Yield Curve

15 bps

23 bps

37 bps38 bps

8

Operation Twist began last week with three purchases

and one sales operation. The impact has been

minimal as markets have been more focused on other

influences.

The sales operation for short-dated Treasury

collateral was oversubscribed more than

30 times.

Source: Bloomberg and Wells Fargo Securities, LLC

The Fed Continues to Exert Control –Operation Twist

914

41

25

4239

28

1 2.5

1611

54

111

130

0

20

40

60

80

100

120

140

1-3 mo 3-6 mo 6M-2 Yr 2-3 Yr 3-5 Yr 5 -10 Yr 10 - 30 Yr

0

20

40

60

80

100

120

140Average Roll Current Roll

Source: Bloomberg

Shape of Treasury Curve

"Operation Twist" would likely focus on flattening this area of

the curve

And possibly result in flattening this area of the curve even further...

9

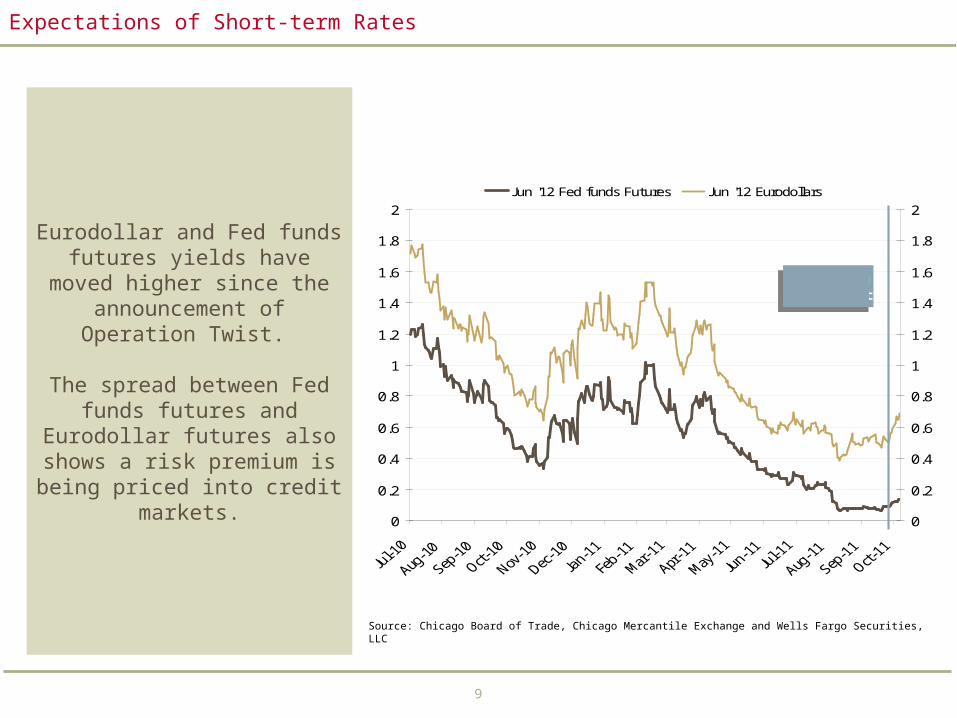

Expectations of Short-term Rates

Eurodollar and Fed funds futures yields have moved

higher since the announcement of Operation

Twist.

The spread between Fed funds futures and

Eurodollar futures also shows a risk premium is being priced into credit

markets.

Source: Chicago Board of Trade, Chicago Mercantile Exchange and Wells Fargo Securities, LLC

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2Jun '12 Fed funds Futures Jun '12 Eurodollars

Source: CBOT, CME

Futures-Implied Yields

Operation Twist

10

Corporate Balance Sheets Remain Flush

Cash accumulation on corporate balance sheets had begun to decrease in

Q4 2010, but cash accumulation has

accelerated in 2011, putting more downward pressure

on rates.

Source: Bloomberg and Wells Fargo Securities, LLC

-

500

1,000

1,500

2,000

2,500

3,000

Q1 1999

Q4 1999

Q3 2000

Q2 2001

Q1 2002

Q4 2002

Q4 2003

Q2 2004

Q1 2005

Q4 2005

Q3 2006

Q2 2007

Q1 2008

Q4 2008

Q3 2009

Q2 2010

Q4 2010

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

Source: Bloomberg, Wells Fargo Securities

Cash and Short-Term Investments($ billions) through Q2

$2.725 trillion

11

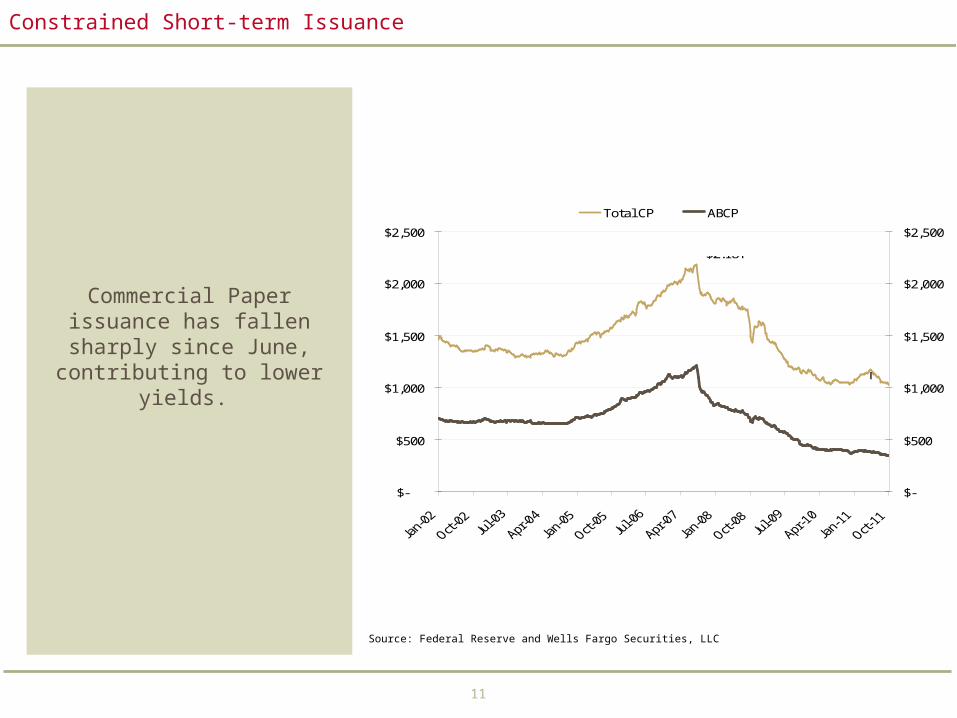

Constrained Short-term Issuance

Commercial Paper issuance has fallen sharply since

June, contributing to lower yields.

Source: Federal Reserve and Wells Fargo Securities, LLC

$-

$500

$1,000

$1,500

$2,000

$2,500

$-

$500

$1,000

$1,500

$2,000

$2,500

Total CP ABCP

Source: Federal Reserve

$2.18T

$1.21T

$350B

$1.025T

Commercial Paper Outstanding

12

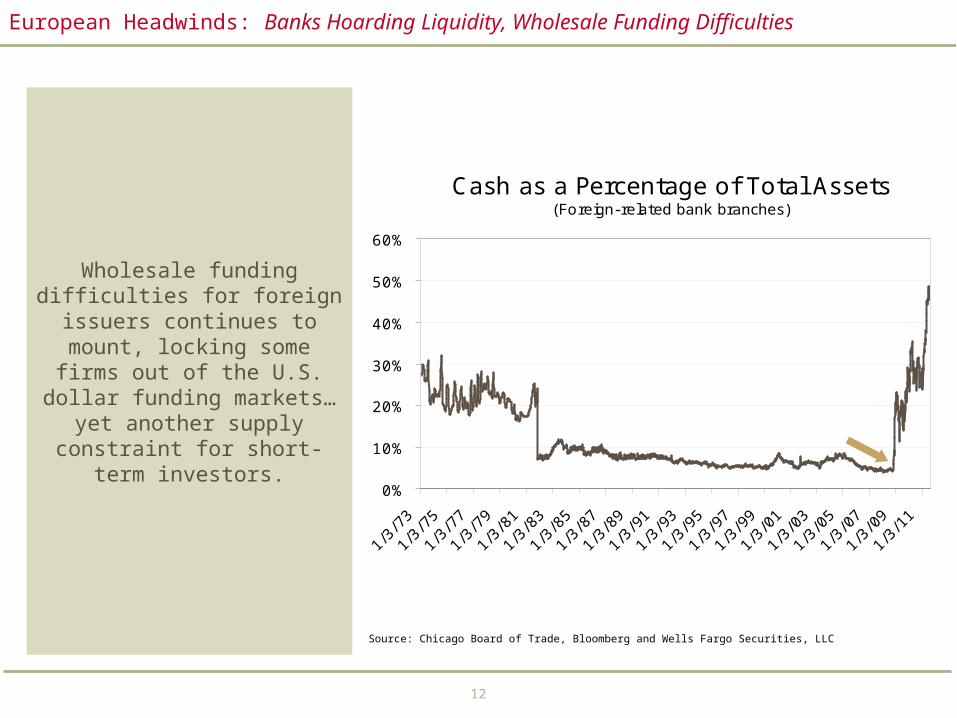

European Headwinds: Banks Hoarding Liquidity, Wholesale Funding Difficulties

Wholesale funding difficulties for foreign

issuers continues to mount, locking some firms out of the U.S. dollar funding markets…yet another

supply constraint for short-term investors.

Source: Chicago Board of Trade, Bloomberg and Wells Fargo Securities, LLC

Cash as a Percentage of Total Assets(Foreign-related bank branches)

0%

10%

20%

30%

40%

50%

60%

1/3/

73

1/3/

75

1/3/

77

1/3/

79

1/3/

81

1/3/

83

1/3/

85

1/3/

87

1/3/

89

1/3/

91

1/3/

93

1/3/

95

1/3/

97

1/3/

99

1/3/

01

1/3/

03

1/3/

05

1/3/

07

1/3/

09

1/3/

11

Source: Federal Reserve

48.60%

4.58%

13

Large Time Deposit Funding has declined

significantly, while balances owed to parent-related

entities has sharply increased.

Source: Federal Reserve and Wells Fargo Securities, LLC

Wholesale Funding(as a % of total assets/ liabilities)

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%Large Time Deposits Net Due to Foreign Parent

Source: Federal Reserve

85%

44%

- 47%

11%

European Headwinds: Banks Hoarding Liquidity, Wholesale Funding Difficulties

14

Balance Sheet Headwinds: Deleveraging and Housing Difficulties Continue

Distress in the U.S. housing market is likely causing a

drag on the economy regardless of whatever

monetary and fiscal stimulus is provided.

Source: Federal Reserve and Wells Fargo Securities, LLC

$-

$5

$10

$15

$20

$25

$30

$ trillio

ns

Total Assets OE Mortgages

Source: Federal Reserve

U.S. Real Estate Assets, Liabilities and Equity

15

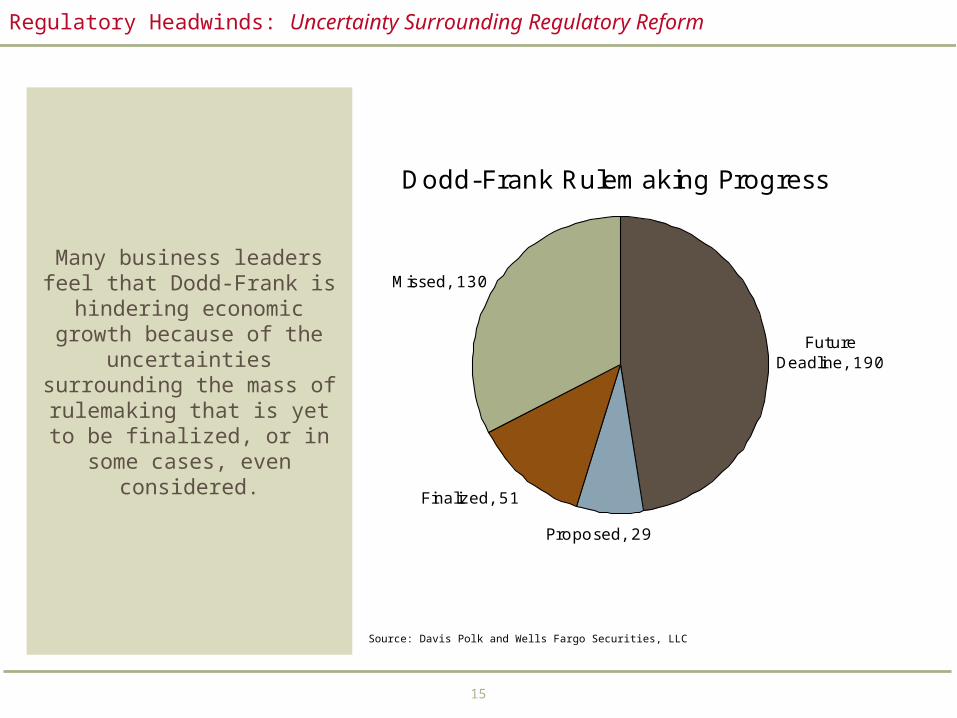

Regulatory Headwinds: Uncertainty Surrounding Regulatory Reform

Many business leaders feel that Dodd-Frank is

hindering economic growth because of the uncertainties

surrounding the mass of rulemaking that is yet to be finalized, or in some cases,

even considered.

Source: Davis Polk and Wells Fargo Securities, LLC

Dodd-Frank Rulemaking Progress

Future Deadline, 190

Proposed, 29

Finalized, 51

Missed, 130

16

The Fed’s Next Move

“U.S. fiscal policy must be placed on a sustainable path that ensures that debt relative to national income is at least stable or, preferably, declining over time. .”

- Ben Bernanke in Jackson Hole August 2011

Source: Federal Reserve and Wells Fargo Securities, LLC

ActionsStatements

Unfortunately, the recession, besides being extraordinarily severe as well as global in scope, was also unusual in being associated with both a very deep slump in the housing market and a historic financial crisis.

These two features of the downturn, individually and in combination, have acted to slow the natural recovery process.

Although we expect a moderate recovery to continue and indeed to strengthen over time, the Committee has marked down its outlook for the likely pace of growth over coming quarters.

The target for the federal funds rate would be held at its current low levels for at least two more years.

Without significant policy changes, the finances of the federal government will inevitably spiral out of control, risking severe economic and financial damage.

The Committee currently anticipates that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013.

The Committee also will maintain its existing policy of reinvesting principal payments from its securities holdings. The Committee will regularly review the size and composition of its securities holdings and is prepared to adjust those holdings as appropriate.

Operation Twist - the Committee decided today to extend the average maturity of its holdings of securities. The Committee intends to purchase, by the end of June 2012, $400 billion of Treasury securities with remaining maturities of 6 years to 30 years and to sell an equal amount of Treasury securities with remaining maturities of 3 years or less. This program should put downward pressure on longer-term interest rates and help make broader financial conditions more accommodative.

17

The Fed’s Exit Strategy

The Fed eventually expects to begin reducing the size of

its balance sheet and adjusting it back to primarily Treasury

securities.

With recent discussions around “Operation Twist” and clarity on the path of

short-term rates, the timeline for reductions in the Fed’s balance sheet have been moved out

further.

Source: Federal Reserve and Wells Fargo Securities, LLC

US Factors Supplying Reserve Funds

-

500

1,000

1,500

2,000

2,500

3,000

1/5/

05

5/5/

05

9/5/

05

1/5/

06

5/5/

06

9/5/

06

1/5/

07

5/5/

07

9/5/

07

1/5/

08

5/5/

08

9/5/

08

1/5/

09

5/5/

09

9/5/

09

1/5/

10

5/5/

10

9/5/

10

1/5/

11

5/5/

11

($ B

illio

ns)

Treasury Agency MBS Other

Source: Federal Reserv e. Wells Fargo Securities

Federal Reserve Securities Holdings

18

Positioning Corporate Cash Portfolios

Framing the structure of a cash portfolio is important to determining the appropriate investment strategy

Source: ICI, Wells Fargo Securities, LLC

Segmentation of the Corporate Cash Portfolio – For Illustrative Purposes Only

Operating Cash (Horizon - daily)

Reserve Cash (Horizon - Quarterly)

Restricted Cash (Horizon - longer-term)

Strategic Cash (Horizon - longer-term)

Liquidity, Stability

of Principal

Less liquidity, higher yields,

more price volatility

Q1 Q2 Q3 Q4

19

Positioning Corporate Portfolios

There is little to no pickup in yield for taking on duration risk outside of the credit markets.

Source: Wells Fargo Securities, LLC

Relative Value in the Money Markets – For Illustrative Purposes Only

0

5

10

15

20

25

30

35

40

45

1-Day 7-Day 30- 60- 90-

A2/P2

VRDN

UK

Nordics

Aussies

J apanese

Canadians

Non-Financials

Financials

DiscosBills

ECR

202020

Market Strategist Commentary is a product of Wells Fargo Securities, LLC’s fixed income trading desk and is not a product of Wells Fargo Securities, LLC’s Global Research Department. The views of the Market Strategist may differ from that of the Global Research Department. Publications of Wells Fargo Securities, LLC’s Global Research Department may be viewed at www.wellsfargo.com/research. Additional information is available on request.

About Wells Fargo Securities Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its affiliates, including Wells Fargo Securities, LLC, member FINRA and SIPC.

Important Information for Non-U.S.. Recipients

The securities and related financial instruments described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. For certain non-U.S.. institutional readers (including readers in the EEA), this report is distributed by Wells Fargo Securities International Limited. For the purposes of Section 21 of the U.K. Financial Services and Markets Act 2000, this report has been approved by Wells Fargo Securities International Limited. This report is not intended for, and should not be relied on by, private customers. Please consult your Financial Advisor or the Wells Fargo Securities office in your area for additional information. U.S. residents are directed to wachovia.com for investment and related services. For Wells Fargo SecuritiesInternational Limited's policy for managing conflicts of interest in connection with research, please go to: www.wachoviaresearch.com/conflicts

Important Information for Australian Recipients

Wells Fargo Securities, LLC is exempt from the requirements to hold an Australian financial services license in respect of the financial services it provides to wholesale clients in Australia. Wells Fargo Securities, LLC is a U.S. broker-dealer registered with the U.S. Securities and Exchange Commission and a member of FINRA and SIPC. Wells Fargo Securities, LLC is regulated under U.S. laws which differ from Australian laws. Any offer or documentation provided to you by Wells Fargo Securities, LLC in the course of providing the financial services will be prepared in accordance with the laws of the United States and not Australian laws.

Important Disclosures Relating to Conflicts of Interest and Potential Conflicts of Interest

Wells Fargo Securities, LLC may sell or buy the subject securities to/from customers on a principal basis. Wells Fargo Securities, LLC has or may have proprietary positions in the securities mentioned herein. The trading desk has or may have proprietary positions in the securities mentioned herein. The author’s compensation is based on, among other things, Wells Fargo Securities, LLC’s overall performance, the profitability of Wells Fargo Securities, LLC’s Fixed income Department and the profitability of the trading desk.

This report, IDs and passwords are available at www.wellsfargo.com/researchThis report is for your information only and is not an offer to sell, or a solicitation of an offer to buy, the securities or instruments named or described in this report. Interested parties are advised to contact the entity with which they deal, or the entity that provided this report to them, if they desire further information. The information in this report has been obtained or derived from sources believed by Wells Fargo Securities, LLC to be reliable, but Wells Fargo Securities, LLC does not represent that this information is accurate or complete. Any opinions or estimates contained in this report represent the judgment of Wells Fargo Securities, LLC at this time and are subject to change without notice. Wells Fargo Securities, LLC and its affiliates may from time to time provide advice with respect to, acquire, hold or sell a position in, the securities or instruments named or described in this report. Wells Fargo Securities, LLC is a separate legal entity and distinct from affiliated banks.Copyright © 2009 Wells Fargo & Company

SECURITIES: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE

Disclosure Appendix