1 seasonal adjustments: causes of revisions Øyvind langsrud statistics norway...

TRANSCRIPT

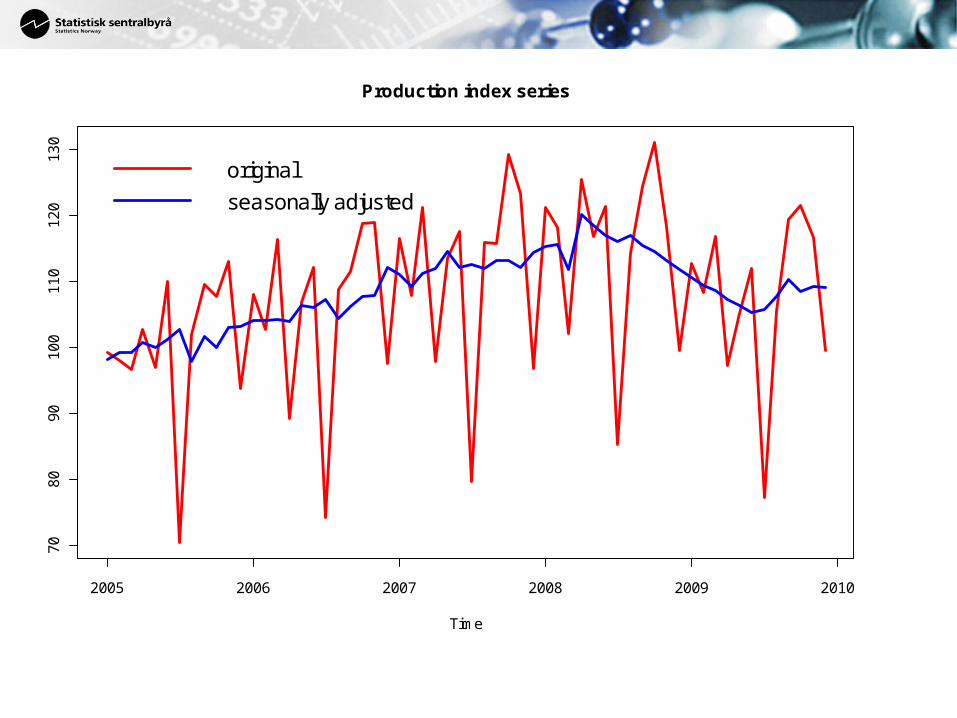

Production index series

Time

2005 2006 2007 2008 2009 2010

70

80

90

10

01

10

12

01

30

original

seasonally adjusted

Seasonally adjustment based on

X12-ARIMA• Two-step procedure: regARIMA + trend and seasonal filters

• regARIMA – Seasonal ARIMA model with regression parameters – Holiday and trading day adjustment– Produce forecasts for use in the next step

• Important choices– Type of ARIMA model– Regression parameters: Holidays and trading days– How to handle outliers

langsrud_pdf_movie.pdf

Revision

• The revision is caused by updated models and parameters

• Revision is a problem– Can be confusing– Not easy to communicate

• Choosing seasonal adjustment methodology can be viewed as a question of balancing

– the requirement of optimal seasonal adjustment at each time point– against the requirement of minimal revisions.

• Can revision be reduced without reducing the quality of the adjustment?

Revision on log-scale

• At = seasonally adjusted series. Yt = original series

• At|t+h is the seasonal adjustment of Yt calculated from the series

where Yt+h is the last observation

• OneMonthRevisiont = (log(At|t+1) – log(At|t) )*100%

one-month revisions

Time

Pe

rce

nt

2005 2006 2007 2008 2009 2010

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Final seasonally adjusted data (d11)

regARIMA modeling:

Comparison by out-of-sample forecasts

• Comparison of methods when model selection is involved is not straightforward

– Standard model fit criteria do not take into account the selection process

– Fair comparison by out-of-sample forecasts

• X-12-ARIMA make use forecasts

Relative forecasting error

• Yt+h|t is the forecast of Yt+h calculated from the series where

Yt is the last observation

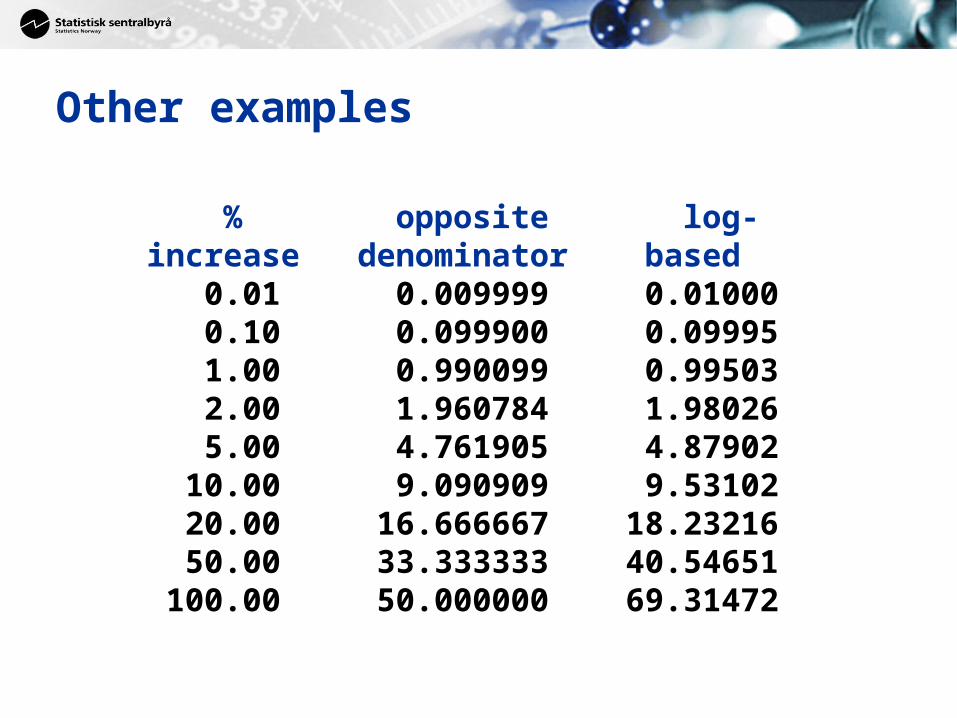

• Example: Yt+h|t =101, Yt+h =100– 100% * (101-100)/101 = 0.99099%– 100% * (log(101)-log(100)) = 0.995033%– 100% * (101-100)/100 = 1.00000%

% opposite log- increase denominator based

0.01 0.009999 0.01000 0.10 0.099900 0.09995 1.00 0.990099 0.99503 2.00 1.960784 1.98026 5.00 4.761905 4.87902 10.00 9.090909 9.53102 20.00 16.666667 18.23216 50.00 33.333333 40.54651 100.00 50.000000 69.31472

Other examples

% opposite log- increase denominator based

0.01 0.009999 0.01000 0.10 0.099900 0.09995 1.00 0.990099 0.99503 2.00 1.960784 1.98026 5.00 4.761905 4.87902 10.00 9.090909 9.53102 20.00 16.666667 18.23216 50.00 33.333333 40.54651 100.00 50.000000 69.31472

Other examples

RMSEroot mean square error

RMSEroot mean square error

• ARIMA model is held fixed from a single analysis of the whole series by using the ARIMA model according to automdl.

• Outliers are held fixed from the same single analysis as above.

• Trading days: six parameters = maximum number of parameters.

• Eastern is handled as usual at Statistics Norway up to three parameters.

Base method:

• ARIMA model is held fixed from a single analysis of the whole series by using the ARIMA model according to automdl.

• Outliers are held fixed from the same single analysis as above.

• Trading days: six parameters = maximum number of parameters.

• Eastern is handled as usual at Statistics Norway up to three parameters.

Comparing methods by deviating from the base method

Automatic ARIMA model selection:

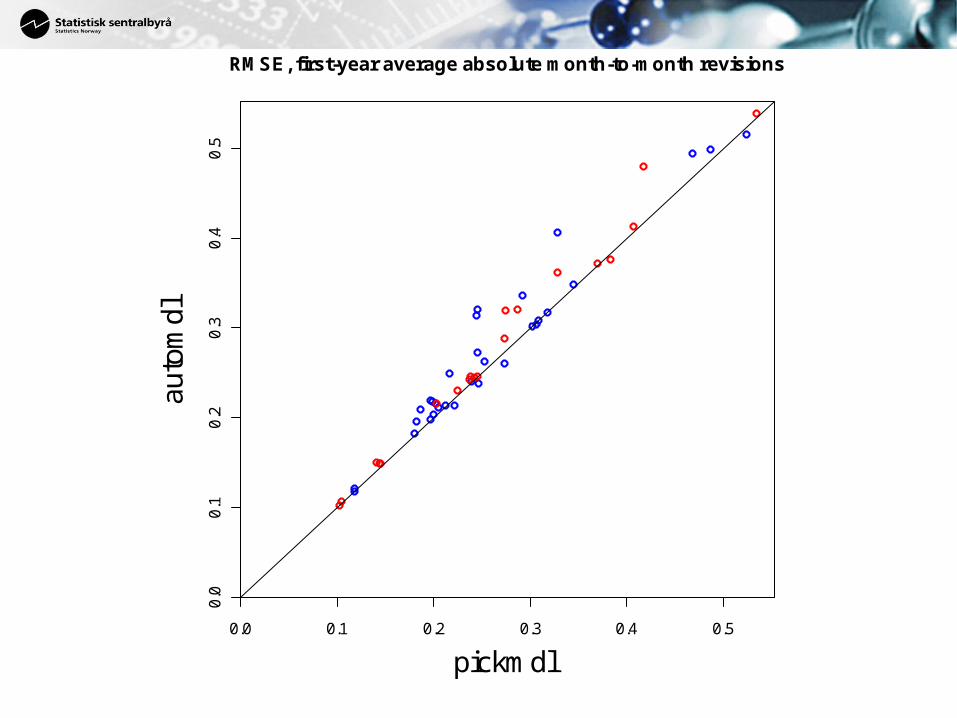

automdl vs pickmdl

• automdl as default in X-12-ARIMA

• pickmdl selects ARIMA model from five candidates

(0 1 1)(0 1 1) *(0 1 2)(0 1 1) X(2 1 0)(0 1 1) X(0 2 2)(0 1 1) X(2 1 2)(0 1 1) X

0 1 2 3 4 5

01

23

45

RMSE, one-month revisions

pickmdl

auto

mdl

Production indexIndex of household consumption of goods

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

RMSE, one-month revisions

pickmdl

auto

mdl

Production indexIndex of household consumption of goods

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

RMSE, one-month revisions

pickmdl

auto

mdl

0.0 0.5 1.0 1.5 2.0 2.5

0.0

0.5

1.0

1.5

2.0

2.5

RMSE, one-year revisions

pickmdl

auto

mdl

0.0 0.1 0.2 0.3 0.4 0.5

0.0

0.1

0.2

0.3

0.4

0.5

RMSE, first-year average absolute month-to-month revisions

pickmdl

auto

mdl

0 2 4 6 8 10 12

02

46

81

01

2

RMSE, one-month out-of-sample forecasts

pickmdl

auto

mdl

Automatic outlier detection:

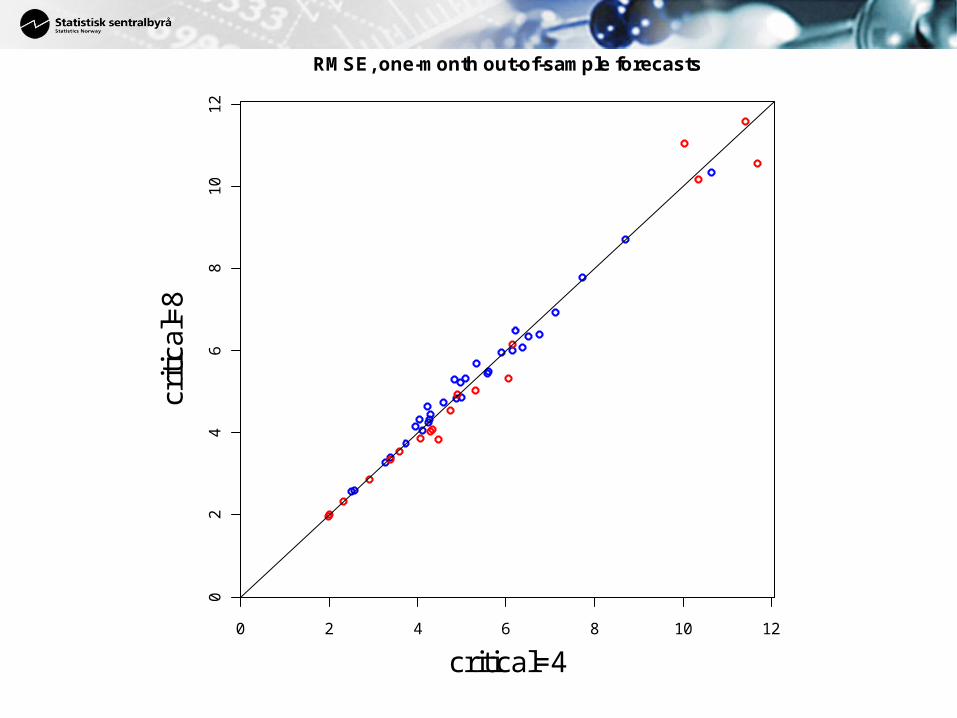

critical=4 vs critical=8

• t-statistic limit

• Both additive outliers and level shifts

• Critical=4 is close to default in X-12-ARIMA

• Critical=8: outliers are extremely rare

0.0 0.5 1.0 1.5 2.0

0.0

0.5

1.0

1.5

2.0

RMSE, one-month revisions

critical=4

criti

cal=

8

0.0 0.2 0.4 0.6 0.8 1.0 1.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

mean(abs( one-month revisions ))

critical=4

criti

cal=

8

0.0 0.5 1.0 1.5 2.0 2.5 3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

RMSE, one-year revisions

critical=4

criti

cal=

8

0.0 0.5 1.0 1.5 2.0

0.0

0.5

1.0

1.5

2.0

mean(abs( one-year revisions ))

critical=4

criti

cal=

8

0.0 0.2 0.4 0.6 0.8

0.0

0.2

0.4

0.6

0.8

RMSE, first-year average absolute month-to-month revisions

critical=4

criti

cal=

8

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

mean(abs( first-year average absolute month-to-month revisions ))

critical=4

criti

cal=

8

0 2 4 6 8 10 12

02

46

81

01

2

RMSE, one-month out-of-sample forecasts

critical=4

criti

cal=

8

0 2 4 6 8

02

46

8

mean(abs( one-month out-of-sample forecasts ))

critical=4

criti

cal=

8

Trading day:6 parameters vs other choices

• 6 parameters = maximum number of parameters

• Other choices – Production index– Standard choice at Statistics Norway based on industrial knowledge – 0, 1, 5 and 6 parameters

• Other choices – Index of household consumption of goods

– 1 parameter, weekdays vs Sundays/Saturdays

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

RMSE, one-month revisions

trading day: 6 parameters

trad

ing

day:

oth

er c

hoic

es

0.0 0.5 1.0 1.5 2.0 2.5

0.0

0.5

1.0

1.5

2.0

2.5

RMSE, one-year revisions

trading day: 6 parameters

trad

ing

day:

oth

er c

hoic

es

0.0 0.1 0.2 0.3 0.4 0.5

0.0

0.1

0.2

0.3

0.4

0.5

RMSE, first-year average absolute month-to-month revisions

trading day: 6 parameters

trad

ing

day:

oth

er c

hoic

es

0 2 4 6 8 10 12

02

46

81

01

2

RMSE, one-month out-of-sample forecasts

trading day: 6 parameters

trad

ing

day:

oth

er c

hoic

es

Moving holiday:

Easter vs no Easter

• Method in Norway– Up to three parameters: Before Easter, Easter, After Easter– Selection based on model fit an t-tests

• History analysis– Exactly as today’s Norwegian procedure

0.0 0.2 0.4 0.6 0.8 1.0 1.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

RMSE, one-month revisions

easter

no e

aste

r

0.0 0.5 1.0 1.5 2.0 2.5 3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

RMSE, one-year revisions

easter

no e

aste

r

0.0 0.1 0.2 0.3 0.4 0.5

0.0

0.1

0.2

0.3

0.4

0.5

RMSE, first-year average absolute month-to-month revisions

easter

no e

aste

r

0 2 4 6 8 10 12

02

46

81

01

2

RMSE, one-month out-of-sample forecasts

easter

no e

aste

r

Conclusion

• Automatic outlier detection and ARIMA model selection leads to revision problems

– Problems can be reduced by using pickmdl and by increasing outlier detection limit

– Better solutions by fixing outliers and models

• Holidays and trading days are less important– Norway’s procedure may be improved– More investigation will be performed

Findley DF (2005),"Some Recent Developments and Directions in Seasonal",JOURNAL OF OFFICIAL STATISTICS, Vol 21, 343–365

Findley DF, Monsell BC, Bell WR, Otto MC, and Chen BC (1998),"New capabilities and methods of the X-12-ARIMA seasonal-adjustment program",JOURNAL OF BUSINESS & ECONOMIC STATISTICS, Vol. 16, 127-152.

Roberts CG, Holan SH, Monsell B (2010),"Comparison of X-12-ARIMA Trading Day and Holiday Regressors with Country Specific

Regressors",JOURNAL OF OFFICIAL STATISTICS, Vol 26, 371-394

US Census Bureau (2011),"X-12-ARIMA Reference Manual",http://www.census.gov/ts/x12a/v03/x12adocV03.pdf

UK - The Office for National Statistics (2007),"Guide to Seasonal Adjustment with X-12-ARIMA **DRAFT**",http://www.ons.gov.uk/ons/guide-method/method-quality/general-methodology/time-series-analysis/guide-to-seasonal-adjustment.pdf

Eurostat - Methodologies and working papers (2009)"Ess Guidelines on Seasonal Adjustment",http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-RA-09-006/EN/KS-RA-09-006-EN.PDF

X12-ARIMA output series

d11 = Y/e18, in our modelleing e18 = e10*d18Y = Original series

d11 = Final seasonally adjusted data (At)

e18 = Final adjustment ratios

d10 = Final seasonal factors

d18 = Combined holiday and trading day factors

• Can calculate revisions in e18, d10, d18 similar to d11d11revision = - e18revision

one-month revisions

Time

Pe

rce

nt

2005 2006 2007 2008 2009 2010

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Final seasonally adjusted data (d11)

one-month revisions

Time

2005 2006 2007 2008 2009 2010

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5 Final adjustment ratios (e18)

Final seasonally adjusted data (d11)

one-month revisions

Time

Pe

rce

nt

2005 2006 2007 2008 2009 2010

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5 Final adjustment ratios (e18)

one-month revisions

Time

2005 2006 2007 2008 2009 2010

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5 Final adjustment ratios (e18)

Final seasonal factors (d10)

Combined holiday and trading day factors (d18)